DEVELOPMENT FINANCE DEPARTMENT (DFD) REPORT … Activities Report Second... · DEVELOPMENT FINANCE...

25

DEVELOPMENT FINANCE DEPARTMENT (DFD) – REPORT OF THE ACTIVITIES OF THE BUSINESS UNIT FROM APRIL - JUNE, 2015 We provide herewith, the activities of the Development Finance Department for the Governor’s Consultative Committee (GCC) meeting for the Second Quarter of 2015. The Department carried out the following activities during the second quarter of the year in order to achieve its mandate of real sector growth, financial inclusion and entrepreneurship development. The strategic initiatives that drove the operations included: the Nigeria Incentive-Based Risk Sharing System for Agricultural Lending (NIRSAL), Commercial Agriculture Credit Scheme (CACS), Agricultural Credit Guarantee Scheme Fund (ACGSF), Agricultural Credit Support Scheme (ACSS), Interest Drawback Programme (IDP), Microfinance Policy, Financial Inclusion, Entrepreneurship Development activities, Power and Airline Intervention Fund (PAIF), Small and Medium Enterprises Credit Guarantee Scheme (SMECGS), SME Restructuring/Refinancing Fund (RRF), Real Sector Support Facility (RSSF), National Collateral Registry (NCR) and Nigeria Electricity Market Stabilisation Facility (NEMSF). The report which is structured into three parts highlights the achievements (activities), challenges and the way forward. Part 1 reviews the real sector intervention efforts; Part 2 highlights financial inclusion activities and Part 3 dwells on entrepreneurship development initiatives of the Department and commodity promotion activities. PART ONE: REAL SECTOR INTERVENTION INITIATIVES 1.1 Nigeria Incentive-Based Risk Sharing System for Agricultural Lending (NIRSAL) The Nigeria Incentive-Based Risk Sharing System for Agricultural Lending (NIRSAL) is a mechanism designed to provide farmers with affordable financial products, reduce the risk of financial institutions that grant them loans, build capacities of banks to lend to agriculture, as well as develop an incentive mechanism for Nigerian banks based on their commitment to agricultural financing. 1.1.1 Highlight of Activities/Achievements No Credit Risk Guarantees (CRG) was approved during the 2 nd quarter of 2015. However, the total value of N21.327 billion in respect of sixty six (66) Credit Risk Guarantee cover had been issued from inception to date. No GES CRG was approved from April to June, 2015, under the NIRSAL-GES Framework. However, cumulatively, a total of N32.993 billion had been disbursed to 158 projects. IDB claims are paid quarterly in respect of each of the projects. Cumulatively, 32 projects are benefitting under the IDB till date. Seven (7) IDB claims valued N23.646 million was processed and paid in the period, bringing the total IDB claims paid under NIRSAL to N295.221million. A total of N41.802million GES IDP was paid during the 2 nd quarter, 2015 for eleven (11) projects. Cumulatively, the total GES IDP paid to date stood at N439.084 million for 92 projects. Met with Executive Management teams of Dangote group and Bank of Agriculture (BOA) on 16th April, 2015 to discuss mode of facilitating the release of N1.4Bn financing fund for tomato out-growers in Kura, Kano. Met with Propcom Maikarfi (DFID UK) on 16th April, 2015 to discuss mode of partnering in respect of proposed lease financing for power tillers to SWOFON women Co-operatives Nation Wide. Met with Mainsail/ Secure Investment of Dubai on 21st April, 2015 and discussed ways of collaborating to enhance access to finance for Agribusinesses in Nigeria under NIRSAL. Met with Bio Soil on 22nd April, 2015 for a presentation on their soil productivity enhancing product and discussion on how they intend to secure the buy-in of farmers to patronize their product. Carried out nationwide sensitization workshop on NIRSAL and the NIRSAL Mechanization Finance Framework (NMFF) in May, 2015. NIRSAL Plc. has been granted COG approval to collaborate with RUFIN in the issuance of collateral guarantee to their mentored MFIs to enable them bridge their collateral gap by 25% May, 2015.

Transcript of DEVELOPMENT FINANCE DEPARTMENT (DFD) REPORT … Activities Report Second... · DEVELOPMENT FINANCE...

DEVELOPMENT FINANCE DEPARTMENT (DFD) – REPORT OF THE ACTIVITIES OF THE BUSINESS UNIT FROM APRIL - JUNE, 2015

We provide herewith, the activities of the Development Finance Department for the Governor’s Consultative

Committee (GCC) meeting for the Second Quarter of 2015.

The Department carried out the following activities during the second quarter of the year in order to achieve its

mandate of real sector growth, financial inclusion and entrepreneurship development. The strategic initiatives

that drove the operations included: the Nigeria Incentive-Based Risk Sharing System for Agricultural Lending

(NIRSAL), Commercial Agriculture Credit Scheme (CACS), Agricultural Credit Guarantee Scheme Fund

(ACGSF), Agricultural Credit Support Scheme (ACSS), Interest Drawback Programme (IDP), Microfinance

Policy, Financial Inclusion, Entrepreneurship Development activities, Power and Airline Intervention Fund

(PAIF), Small and Medium Enterprises Credit Guarantee Scheme (SMECGS), SME Restructuring/Refinancing

Fund (RRF), Real Sector Support Facility (RSSF), National Collateral Registry (NCR) and Nigeria Electricity

Market Stabilisation Facility (NEMSF). The report which is structured into three parts highlights the

achievements (activities), challenges and the way forward. Part 1 reviews the real sector intervention efforts;

Part 2 highlights financial inclusion activities and Part 3 dwells on entrepreneurship development initiatives of

the Department and commodity promotion activities.

PART ONE: REAL SECTOR INTERVENTION INITIATIVES

1.1 Nigeria Incentive-Based Risk Sharing System for Agricultural Lending (NIRSAL)

The Nigeria Incentive-Based Risk Sharing System for Agricultural Lending (NIRSAL) is a mechanism designed

to provide farmers with affordable financial products, reduce the risk of financial institutions that grant them

loans, build capacities of banks to lend to agriculture, as well as develop an incentive mechanism for Nigerian

banks based on their commitment to agricultural financing.

1.1.1 Highlight of Activities/Achievements

No Credit Risk Guarantees (CRG) was approved during the 2nd quarter of 2015. However, the total value of N21.327 billion in respect of sixty six (66) Credit Risk Guarantee cover had been issued from inception to date.

No GES CRG was approved from April to June, 2015, under the NIRSAL-GES Framework. However, cumulatively, a total of N32.993 billion had been disbursed to 158 projects.

IDB claims are paid quarterly in respect of each of the projects. Cumulatively, 32 projects are benefitting under the IDB till date. Seven (7) IDB claims valued N23.646 million was processed and paid in the period, bringing the total IDB claims paid under NIRSAL to N295.221million.

A total of N41.802million GES IDP was paid during the 2nd quarter, 2015 for eleven (11) projects. Cumulatively, the total GES IDP paid to date stood at N439.084 million for 92 projects.

Met with Executive Management teams of Dangote group and Bank of Agriculture (BOA) on 16th April, 2015 to discuss mode of facilitating the release of N1.4Bn financing fund for tomato out-growers in Kura, Kano.

Met with Propcom Maikarfi (DFID UK) on 16th April, 2015 to discuss mode of partnering in respect of proposed lease financing for power tillers to SWOFON women Co-operatives Nation Wide.

Met with Mainsail/ Secure Investment of Dubai on 21st April, 2015 and discussed ways of collaborating to enhance access to finance for Agribusinesses in Nigeria under NIRSAL.

Met with Bio Soil on 22nd April, 2015 for a presentation on their soil productivity enhancing product and discussion on how they intend to secure the buy-in of farmers to patronize their product.

Carried out nationwide sensitization workshop on NIRSAL and the NIRSAL Mechanization Finance Framework (NMFF) in May, 2015.

NIRSAL Plc. has been granted COG approval to collaborate with RUFIN in the issuance of collateral guarantee to their mentored MFIs to enable them bridge their collateral gap by 25% May, 2015.

2

Met with National Agricultural Insurance Corporation (NAIC) National Insurance Commission (NAICOM), Leadway Insurance Company, IGI Insurance Company, and Finsurance on 28th May, 2015 to discuss mode of kick-starting the NIRSAL Insurance Pillar.

NIRSAL Plc. was assigned the task of implementing the CBN Governor’s special project on Anchor Out-grower Scheme (AOS) within the period under review.

Met with Stallion Nig. Ltd. (Rice Processor) in Lagos State on 4th June, 2015 and West African Cotton Company (WACOT) Ltd. (Rice Processor) in Kebbi State on 9th June, 2015 to discuss mode of partnership under the CBN Governor’s special project on Anchor Out-grower Scheme (AOS).

1.1.2 Challenges

Validity of information provided by counter parties for Credit Risk Guarantee;

Low public awareness and poor perception of NIRSAL

Lack of Information Technology (IT) infrastructure in respect of movement to

NIRSAL head office

The inability of the Federal Ministry of Agriculture & Rural Development living up to its responsibility of paying

the 50% product subsidy as agreed.

1.1.3 Going Forward

Nirsal will sell guarantee on 75%, 50% and 30% to primary producers, processors and logistics provider respectively Guarantee to be issued on Face Value as against First Loss. Continue to collaborate with stakeholders on the way forward

1.2 Commercial Agriculture Credit Scheme (CACS)

The Commercial Agriculture Credit Scheme (CACS) was established in 2009 to finance large ticket projects along

the agricultural value chain. It is administered at a single digit interest rate of 9 per cent to beneficiaries. State

Governments, including the FCT can access a maximum of N1.0 billion each for on lending to farmers’

cooperatives or other areas of their agricultural intervention. The Scheme is managed by the CBN. The exit date

for the Scheme is 2025.

The Bank reviewed the interest rate of CACS and approved that the 9% interest rate should be shared between

the CBN and DMBs in the ratio 2:7 percent respectively. The CACS guideline was also revised on April 29, 2015

to reflect the re-pricing. The following activities were carried out In the period under review;

1.2.1 Highlight of Activities/Achievements

The sum of N13.095billion was released from CACS Repayments to twelve (12) Banks in respect of sixteen (16) projects between April and June, 2015 out of which thirteen (13) projects were disbursed under the new pricing regime which took effect from April 29, 2015.

No funds was released from CACS Receivable Account during the same period. From inception in 2009 to June, 2015, the sum of N287.494 billion was released to the economy under the

Commercial Agriculture Credit Scheme in respect of 369 projects. This comprised the sum of N199.831 billion released from the CACS Receivable Account for 273 projects and the sum of N87.663 billion released from Repayment Account for 127 new projects including 31 enhancements. This also included, thirty (30) State Governments and the FCT which altogether accessed the sum of N49.0 billion from CACS fund from inception to June, 2015.

The sum of N8.662 billion was recorded as repayments by twenty two (22) banks during the quarter under review, bringing the total fund repaid to N126.109 billion in respect of 113 fully repaid projects and 177 steady repayments.

3

In pursuit of the real sector development, with special focus on five commodities (rice wheat, sugar, fish and cotton), a total sum of N3.970 billion has been released to the rice sub-sector within the quarter. Consequently, giving rise to a cumulative operating capacity of 709,476 metric tonnes of rice per annum under the Scheme. The sum of N62.576 billion has been released to the economy with respect to all the focal commodities as at June, 2015.

The balance of CACS Receivable Account fund as at end of June, 2015 was N0.169 billion The balance on CACS Repayment Account as at end June, 2015 was N37.753 billion. From inception in 2009 to December, 2014, 194,556 jobs were created; Eight out of the 332 private projects are owned and managed by women. No bank was sanctioned during the quarter under review. However, the balance of CACS penalty account as

at June, 2015 was N1.413billion. Table 1: Total Disbursement by Deposit Money Banks (DMBs) under CACS

Receivable from DMBs

Accounts Repayment Account

Financing Bank Projects

Amount Released to Banks

(N'Bn)

Projects

New Project Enhancement

Amount released (N'Bn)

Total Amount Released

1

Access Bank Nigeria Plc

11 10.326 5 0 3.30 13.626

2 Citibank 2 3 0 0 0 3

3 Diamond Bank 12 2.744 3 2 1.616 4.360

4 EcoBank Plc 7 3.82 3 2 2.555 6.376

5 Enterprise Bank 6 0.519 0 0 0 0.519

6 Fidelity Bank Plc 8 8.575 1 2 2.295 10.87

7 First Bank of Nigeria 62 22.359 27 3 14.147 36.506

8 First City Monument Bank

8 4.785 8 2 2.491 7.276

9 Guaranty Trust Bank Plc

9 5.8 3 0 5.6 11.4

10 Heritage Bank 0 0 3 1 3.172 3.172

11 Mainstreet Bank 1 2 0 0 0 2

12 Keystone Bank 1 0.2 3 0 2.005 2.205

13 Skye Bank Plc 7 9.217 0 2 0.475 9.692

14 Stanbic IBTC 23 11.742 9 3 5.566 17.308

15 Sterling Bank 14 7.193 8 7 8.445 15.638

16 Union Bank Plc 21 18.167 1 0 1.970 20.137

17 United Bank for Africa Plc

35 41.757 2 0 4.0 45.757

18 Unity Bank Plc 23 19.932 2 3 4.25 24.182

19 Wema Bank 5 0.74 2 2 0.390 1.13

20 Zenith Bank Plc 18 26.955 16 2 25.386 52.34

Total 273 199.831 96 31 87.663 287.494

4

Releases under CACS to Deposit Money Banks (DMBs)

The analysis of number of projects financed under CACS by value chain showed that out of sixteen (16) CACS private sector projects, sponsored from inception, production accounted for 75% while Processing recorded 25%. (Table 2) Table 2: Analysis of CACS Financed Private Projects by Value Chain as at 2nd quarter, 2015

Category

Value {N ’billions and %} Number (%) of Projects

Production 12(75%) 8.39(64.1%)

Processing 4(25.0%) 4.7(35.9%)

Total 16 13.09

Analysis by value of funds released showed that production accounted for 64.1% while Processing recorded 35.9%. (Table 2)

Figure 1: Banks’ Disbursements to Projects by value of funds under CACS as at 2nd Quarter, 2015

based on Value Chain Distribution

1.2.2 Challenges

Poor monitoring of projects by some participating banks.

Slow pace of implementation of projects by State Governments.

Non-adherance to CACS guidelines by banks.

1.2.3 Going Forward

Improved monitoring of CACS projects by CBN. Impact Assessment to ascertain the actual gains of CACS. Increased monitoring and sensitization of DMBs

5

1.3 Agricultural Credit Guarantee Scheme (ACGS)

The ACGS was established by Decree 20 of 1977 to provide 75 per cent guarantee cover in respect of loans

granted to the agricultural sector by Deposit Money Banks. The Scheme pledges to pay 75 per cent of any

outstanding default balance to the bank after the security pledged has been realized.

1.3.1 Loans Guaranteed

In June, 2015, a total of 5,329 loans valued N1.079 billion was guaranteed in respect of one (1) DMBs and 26

Microfinance banks. Between the period April-June, 2015 a total of 14,229 loans valued N2.681bn billion was

guaranteed as against 18,346 loans valued N3.312 billion guaranteed in April-June, 2014. This showed a

decrease of 4,117 or 22.44 per cent in number and N0.631 billion or 19.05 per cent in value.

The number and value of loans guaranteed in 2015 is 28,702 valued N5.928 billion. Cumulatively from inception

in 1978, the figure stood at 960,565 loans valued N89.909 billion.(Table 3).

PARAMETERS

APRIL- JUNE, 2015 POSITION

APRIL- JUNE, 2014 POSITION

1. Guaranteed

ACGS Loans

Guaranteed 5,329 loans valued N1.079 billion

in June, 2015 and 14,229 loans valued N2.681

billion from April–June, 2015, as against 18,346

loans valued N3.312 billion guaranteed from

April to June, 2014. This showed a decrease of

4,117 or 22.44 per cent in number and N631.0

million or 19.05 per cent in value. A total of

960,565 loans valued N89.909 billion was

guaranteed from inception in 1978 to June

2015.

Guaranteed 8,251 loans valued N1.472 billion

in June, 2014 and 18,346 loans valued N3.312

billion from April–June, 2014, as against

12,286 loans valued N1.696 billion

guaranteed from April to June, 2013. This

showed an increase of 6,060 or 49.3 per cent

in number and N1.616bn or 95.2 per cent in

value. A total of 894,954 loans valued

N77.398 billion was guaranteed from

inception in 1978 to June 2014

2. Number of

Loans

Guaranteed

ranked on

State Basis

Highest: Edo State with 2,851 (20.04%) valued

N282.135 million (10.52%).

Second: Ondo State with 1,188 loans (8.35%)

valued N180.340 million (6.73%).

Third: Sokoto State with 827 loans (5.81%)

valued N92.297 million (3.44%).

Highest: Delta State with 4,545 (24.77%)

valued N399.966 million (12.07%).

Second: Kebbi State with 1,715 loans (9.35%)

valued N342.404 million (10.33%).

Third: Sokoto State with 1,588 loans (8.66%)

valued N160.522million (4.85%).

6

3. Number of

Loans

Guaranteed

by Category

of Loan

The breakdown of the performance of Second Quarter, 2015 is as follows: Individuals = 14,065 loans valued N2.647bn

Informal Groups = 106 loans valued N22.690m

Co-operatives =56 loans valued N7,980m

Companies = 2 loans valued N3.000m

The breakdown of the performance as at June, 2014 is as follows: Individuals = 18,146 loans valued N3.156bn

Informal Groups = 166 loans valued

N112.200m

Co-operatives =9 loans valued N22.480m

Companies = 25 loans valued N21.300m

4. Loans

Guaranteed

by Purpose/

Type of

Agricultural

business

April, 2007

January - The breakdown of the second quarter, 2015

performance is as follows:

Livestock = 859 loans valued N268.936 million

Fisheries = 280 loans valued N96.500m

Mixed crops= 890 loans valued N129.040m

Food Crops = 10,635loans valued N1.874 billion

Cash Crops = 828 loans valued N185.540m

Others = 737 loans valued N126.384m

The The breakdown of the second quarter, 2014

performance is as follows:

Livestock = 2,042 loans valued N664.692m

Fisheries = 683 loans valued N103.866m

Mixed crops= 2,585 loans valued N340.080m

Food Crops = 11,112 loans valued N1.878b

Cash Crops = 1,473 loans valued N148.305m

Others = 451 loans valued N177.650m

5. Number and

value of

Loans Repaid

A total of 6,735 loans valued N910.726 million

was fully repaid under the Scheme in June,

2015 and 13,919 loans valued N2.340 billion

were fully repaid between April and June 2015

as against 10,449 loans valued N1.609 billion

that was recovered between April and June

2014. This brings the cumulative fully repaid

loans from inception to June, 2015 to 722,845

valued N60.835 billion.

A total of 3,665 loans valued N490.860 million

was fully repaid under the Scheme in June,

2014 and 10,449 loans valued N1.609 billion

were fully repaid between April and June

2014 as against 11,379 loans valued N1.72

billion that was recovered between April and

June 2013. This brings the cumulative fully

repaid loans from inception to June, 2014 to

670,557 valued N52.486billion.

7

6. Number of

Loans Repaid

ranked on

State Basis

The breakdown of the second quarter, 2015

performance is as follows:

Highest: Bauchi State with 1,716 loans

(12.33%) valued N183.000 million (7.82%).

Second: Delta State with 1,514 loans (10.88%)

valued N455.809 million (19.48%).

Third: Adamawa State with 1,420 loans (10.2%)

valued N172.939 million (7.39%).

The breakdown of the second quarter, 2014

performance is as follows:

Highest: Zamfara State with 1,329 loans

(12.72%) valued N62.783 million (3.90%).

Second: Kwara State with 1,146 loans

(10.97%) valued N115.139 million

(7.15%).

Third: Sokoto State with 909 loans (8.69%)

valued N68.379million (4.24%).

7. Loans Repaid

Analyzed by

Size of Credit

Granted

The breakdown of the loans repaid under the Scheme as at the end of June, 2015 is as follows:

N5,000 and below = 17 loans valued N0.827m

N5,001-N20,000 =1,415loans valued N23.674m

N20,001-N50,000=3,142 loans valued N117.133m

N50,001-N100,000=3,131 loans valued N280.673m

Above N100,000 = 6,214 loans valued N1.918bn

The breakdown of the loans repaid under the Scheme as at the end of June, 2014 is as follows: N5,000 and below = Nil N5,001-N20,000=1,356 loans valued N24.751m

N20,001-N50,000=3,337loans valued N137.616m N50,001-N100,000=2,357loans valued N219.471 m Above N100,000 = 3,399 loans valued N1.227bn

8. ACGSF Claims

received/

Settled

26 ACGS claims valued N3.671mn was settled

from April-June, 2015. The cumulative number

of settled claims since inception is 16,761

valued N615.604mn as at the end of June,

2015.

211 ACGS claims valued N16.440mn was

settled from April-June, 2014. The cumulative

number of settled claims since inception is

14,691 valued N546.932mn as at the end of

June, 2014.

9. IDP Claims

received/

Settled

4,997 IDP Claims valued N33.128mn were settled in June, 2015. In the 2nd quarter of 2015, 12,301 IDP claims valued N138.795mn were settled. The total number and value of IDP claims settled since inception in 2004 is 270,894 claims valued N2.453billion as at the end of June, 2015.

4,659 IDP claims valued N48.820mn were

settled in the period under review. Bringing,

the total number and value of IDP claims

settled since inception in 2004, to 246,426

claims valued N1.936billion as at the end of

June, 2014.

8

10. Banks

Participation

under the

ACGS

[ranked by

number of

loans

granted]

Below is the performance of participating

banks under ACGS as at 2nd Quarter, 2015:

(i) Deposit Money Banks (DMBs)

4 DMBs granted a total of 3,239 loans valued

N1.356 bn under the ACGS between April to

June, 2015. The breakdown of the

disbursements by the banks is as follows:

Diamond Bank of Nigeria (DBN) Plc {1 loan

valued N2,000m}, First Bank of Nigeria

(FBN) Plc {568 loans valued N294.711m}:

Sterling Bank Plc {10 loan valued

N10.000m}, Union Bank of Nigeria (UBN)

Plc {2,660 loans valued N1.070 bn},

(ii) Microfinance Banks (MFBs)

A total of 10,990 loans valued N1.324bn was

granted by microfinance banks between

April to June, 2015 under the ACGSF.

Below is the performance of participating

banks under ACGS as at 2nd Quarter, 2014:

(i) Deposit Money Banks (DMBs)

5 DMBs granted a total of 4,043 loans valued

N1.619 bn under the ACGS between April to

June, 2014. The breakdown of the

disbursements by the banks is as follows:

Diamond Bank of Nigeria (DBN) Plc {15 loans

valued N15.00m}, First Bank of Nigeria (FBN)

Plc {1,034 loans valued N433.84m}: Stanbic

Bank Plc {1 loan valued N0.300m}, Union

Bank of Nigeria (UBN) Plc {2,853 loans valued

N1.140m}, Keystone Bank Plc. {140 loans

valued N29.300m}

(ii) Microfinance Banks (MFBs)

A total of 14,303 loans valued N1.694bn

was granted by microfinance banks

between April to June, 2014 under the

ACGSF.

11. Number of

(MOUs) signed

under the Trust

Fund Model

(TFM)

No new Memorandum of Understanding

(MOU) was signed by the Department under

the TFM during the period under review;

however, 56 Stakeholders made up of State

Governments, Multinational Agencies, LGAs,

NGOs and Individuals signed MOUs under the

programme and placed/ pledged a total sum of

N5, 516.10 billion.

No new Memorandum of Understanding

(MOU) was signed by the Department under

the TFM during the period under review;

however, 56 Stakeholders made up of State

Governments, Multinational Agencies, LGAs,

NGOs and Individuals signed MOUs under the

programme and placed/ pledged a total sum

of N5, 516.10 billion.

12. Resources

of ACGSF

The total resources of the ACGSF as at June of

2015 stood at N5.998billion.

The total resources of the ACGSF as at June of

2014 stood at N6.140billion.

13. Resources of the Interest Drawback Programme (IDP)

The value of the total resources of IDP at the

end of June 2015 was N1.581 billion.

The value of the total resources of IDP at the

end of June 2014 was N1.761 billion.

14. Expenses Recoverable Payable to the Managing Agent (CBN)

The recoverable expenses incurred by the

Development Finance Offices and Head Office

under ACGSF for the month of June, 2015

amount to N67.420 million.

The recoverable expenses incurred by the

Development Finance Offices and Head Office

under ACGSF for the month of June, 2014

amount to N54.82 million.

9

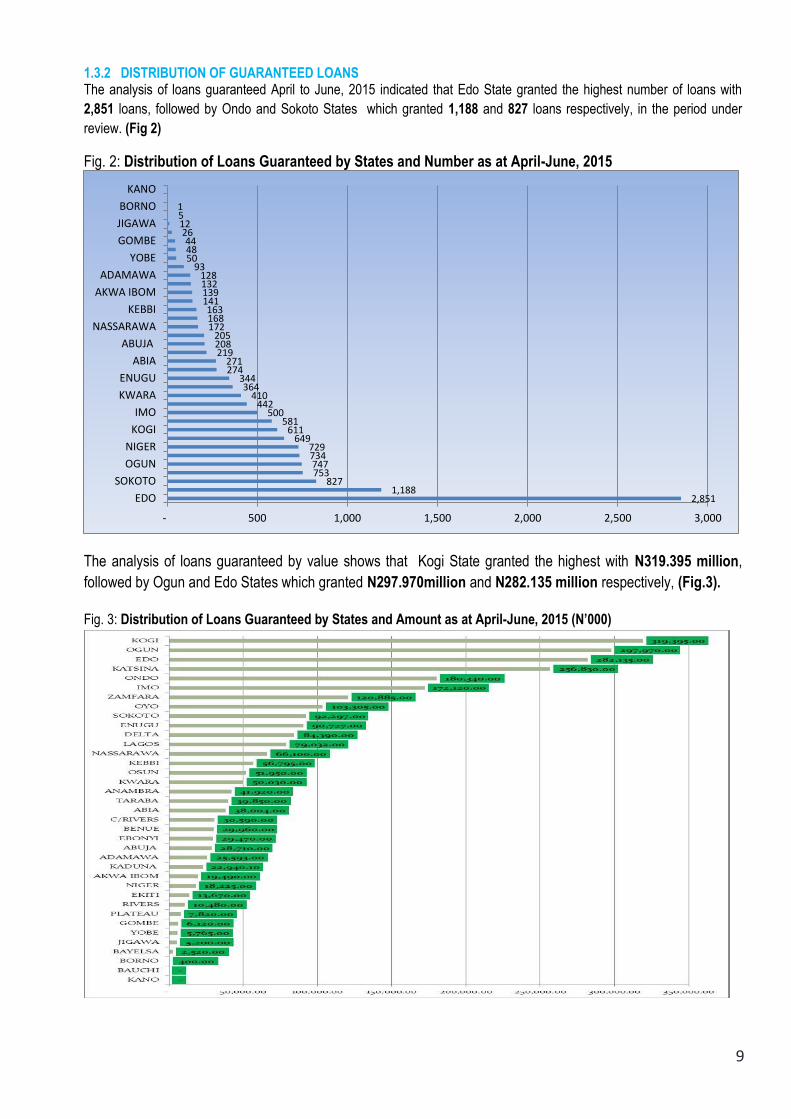

1.3.2 DISTRIBUTION OF GUARANTEED LOANS The analysis of loans guaranteed April to June, 2015 indicated that Edo State granted the highest number of loans with

2,851 loans, followed by Ondo and Sokoto States which granted 1,188 and 827 loans respectively, in the period under

review. (Fig 2)

Fig. 2: Distribution of Loans Guaranteed by States and Number as at April-June, 2015

The analysis of loans guaranteed by value shows that Kogi State granted the highest with N319.395 million,

followed by Ogun and Edo States which granted N297.970million and N282.135 million respectively, (Fig.3).

Fig. 3: Distribution of Loans Guaranteed by States and Amount as at April-June, 2015 (N’000)

2,851 1,188

827 753 747 734 729

649 611

581 500

442 410

364 344

274 271

219 208 205

172 168 163

141 139 132 128

93 50 48 44

26 12 5 1

- 500 1,000 1,500 2,000 2,500 3,000

EDO

SOKOTO

OGUN

NIGER

KOGI

IMO

KWARA

ENUGU

ABIA

ABUJA

NASSARAWA

KEBBI

AKWA IBOM

ADAMAWA

YOBE

GOMBE

JIGAWA

BORNO

KANO

10

1.3.3 DISTRIBUTION OF LOANS BY PURPOSE

The distribution of number of loans guaranteed by purpose indicated that food crops accounted for 10,635 loans (74.7 per cent), followed by mixed farming and livestock which recorded 890 ( 6.3 per cent) and 859 loans ( 6 per cent) respectively while cash crops, others and fisheries recorded 828 loans,737 loans and 280 loans respectively (Fig.4)

Fig. 4: Distribution of Loans Guaranteed by Purpose as at April-June, 2015.

1.3.4 Analysis of Loans by Gender of Borrowers

In June, 2015, a total of 2,774 male beneficiaries obtained loans under the ACGS, amounting to N616.719

million, while 2,539 were female borrowers who received N444.952 million. Cumulatively, from April to June,

2015, 8,439 (59.31%) loans valued N1.672billion was granted to male borrowers, while 5,769(40.54%) loans

valued N986.235 million were accessed by female farmers. (Fig5)

1.3.5 LOANS ANALYSIS BY GEO-POLITICAL ZONES

Analysis of loans guaranteed by States in the geo-political zones in the second quarter 2015 revealed that South-

South zone (Akwa-Ibom, Bayelsa, Cross-River, Delta, Edo, Rivers States) had 3,770 loans valued N429.605

million, followed by South-West (Ekiti, Lagos, Ogun, Ondo, Osun and Oyo States) had a total of 3,478 loans

Food Crops, 10,635

Food Crops Cash Crops Others Livestock Fisheries Mixed Farming

Male, 8,439 Female, 5,769

Male

Female

11

amounting to N726.267 million, while North-West (Kaduna, Kano, Katsina, Kebbi, Jigawa, Sokoto, Zamfara)

granted 2,545 loans valued N554.947 million.(Fig 6)

Distribution of Loans Guaranteed by Number and Geo-Political Zones, April-June, 2015.

1.3.6 Loans Repayment

In June, 2015, a total of 6,735 loans valued N910.726million were fully repaid. The total number of loans

recovered from April to June, 2015 was 13,919 loans valued N2.340 as against 10,449 loans valued N1.609

billion in the same period of 2014. This brings the cumulative number of loans repaid from inception to June, 2015

to 722,845 valued N60.835 billion.

1.3.6.1 Analysis of Loan Repaid by States and Number

An analysis of repayment from April to June, 2015, by States showed that Bauchi State had the highest with 1,716 loans which represents 12.3 per cent in number, followed by Delta and Adamawa States which recorded 1,514 and 1,420 loans, respectively, representing 10.9 per cent and 10.2 per cent in number respectively. (Fig.7)

Fig. 7: Distribution of Loans Repaid by States and Number as at April-June, 2015

1.3.6.2 Analysis of Loan Repaid by States and Amount

Further analysis of repayment from April to June, 2015, by States and amount showed that Delta State recorded

the highest amount of repayment of N455.809 million which represents 19.48 per cent, followed by Taraba and

0 500 1,000 1,500 2,000 2,500 3,000 3,500 4,000

South-South

South-West

North-West

North-Central

South-East

North-East

3,770

3,478

2,545

2,383

1,466

587 South-South

South-West

North-West

North-Central

12

Katsina States with N236.630 million and N217.000 million respectively, representing 10.11 per cent and 9.27

per cent respectively. (fig.8)

Fig. 8: Distribution of Loans Repaid by States and Amount, April-June, 2015 (N’000)

1.3.6.3 Loans Repayment by Gender of Borrowers

In June, 2015, the analysis of repayment by gender of borrowers showed that 5,467 male beneficiaries

representing 81.17 per cent repaid N720.933 million or 79.16 per cent while, female borrowers repaid 1,249

loans or 18.54 per cent valued N164.392 million or 18.05 per cent.

In the period April-June 2015, 11,069 (79.52%) male borrowers repaid loans valued N1.745 bn (77.56%) while

2,821 (20.27) female borrowers repaid loans valued N577.740 million (23.83). (fig9)

Male, 11,069

Female, 2,821

Male

Female

13

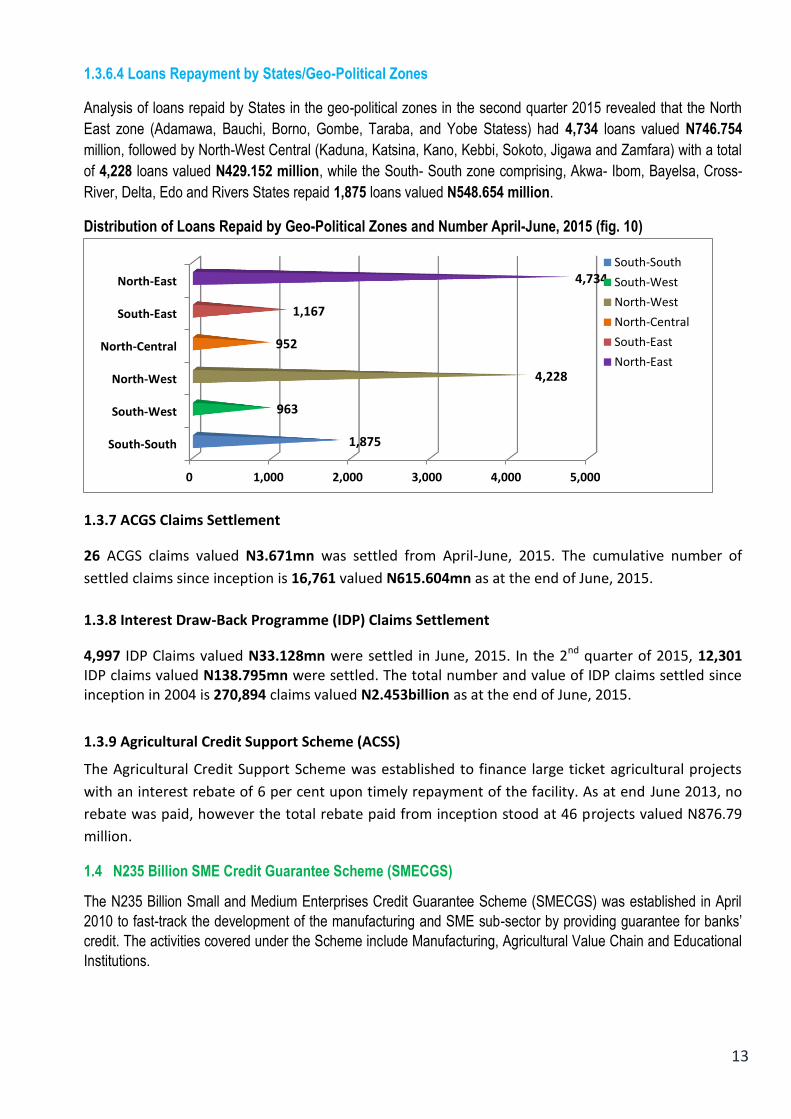

1.3.6.4 Loans Repayment by States/Geo-Political Zones

Analysis of loans repaid by States in the geo-political zones in the second quarter 2015 revealed that the North

East zone (Adamawa, Bauchi, Borno, Gombe, Taraba, and Yobe Statess) had 4,734 loans valued N746.754

million, followed by North-West Central (Kaduna, Katsina, Kano, Kebbi, Sokoto, Jigawa and Zamfara) with a total

of 4,228 loans valued N429.152 million, while the South- South zone comprising, Akwa- Ibom, Bayelsa, Cross-

River, Delta, Edo and Rivers States repaid 1,875 loans valued N548.654 million.

Distribution of Loans Repaid by Geo-Political Zones and Number April-June, 2015 (fig. 10)

1.3.7 ACGS Claims Settlement

26 ACGS claims valued N3.671mn was settled from April-June, 2015. The cumulative number of

settled claims since inception is 16,761 valued N615.604mn as at the end of June, 2015.

1.3.8 Interest Draw-Back Programme (IDP) Claims Settlement

4,997 IDP Claims valued N33.128mn were settled in June, 2015. In the 2nd quarter of 2015, 12,301 IDP claims valued N138.795mn were settled. The total number and value of IDP claims settled since inception in 2004 is 270,894 claims valued N2.453billion as at the end of June, 2015.

1.3.9 Agricultural Credit Support Scheme (ACSS)

The Agricultural Credit Support Scheme was established to finance large ticket agricultural projects

with an interest rebate of 6 per cent upon timely repayment of the facility. As at end June 2013, no

rebate was paid, however the total rebate paid from inception stood at 46 projects valued N876.79

million.

1.4 N235 Billion SME Credit Guarantee Scheme (SMECGS)

The N235 Billion Small and Medium Enterprises Credit Guarantee Scheme (SMECGS) was established in April

2010 to fast-track the development of the manufacturing and SME sub-sector by providing guarantee for banks’

credit. The activities covered under the Scheme include Manufacturing, Agricultural Value Chain and Educational

Institutions.

0 1,000 2,000 3,000 4,000 5,000

South-South

South-West

North-West

North-Central

South-East

North-East

1,875

963

4,228

952

1,167

4,734 South-South

South-West

North-West

North-Central

South-East

North-East

14

1.4.1 Achievements/Activities:

No project was guaranteed under the Small and Medium Enterprises Credit Guarantee Scheme (SMECGS) from April to June, 2015. However, the total number of projects guaranteed since inception stood at 81 (Eighty One), valued N3.77 billion.

One (1) project valued N100.00m was repaid within the quarter bringing the total number of fully repaid projects to 36 valued N2.435 billion from inception to date.

1.4.2 Challenges:

Low Stakeholder Buy-in for SMECGS.

1.4.3 Way Forward:

Introduce Interest Draw-back Programme (IDP).

1.5 N200 Billion SME Restructuring/Refinancing Fund (RRF)

The N200 Billion SME Restructuring /Refinancing Fund (RRF) has been discontinued by the Management of the

bank. However, the repayment from RRF will be utilised in the new Scheme (RSSF).

1.5.1 UPDATE ON SME/RRF

The total amount disbursed from the RRF Repayment Account for the quarter under review stood at N1.0b

to Kam Industries.

Total releases to BOI so far, stood at N360.725 billion (N235 billion from the main Account and

N125.725 billion from the repayment account) and disbursed to 602 projects from inception to date.

Total loan repayments by the DMB’s for the 2nd quarter stood at N8.999billion

Total Loan Repayments by the DMBs as at June, 2015 under SME-RRF stood at N113.724 billion

(N104.725 billion repaid as at end of 2014 and N8.999 billion recovered within the 2nd quarter, 2015)

and disbursed to 602 projects from inception to date.

1.6 Establishment of a Real Sector Support Facility (RSSF)

The COG at its 375th Meeting of the 26th November, 2014 approved the establishment of a N300 billion Real

Sector Support Facility (RSSF) to address the funding needs of large ticket SMEs in Nigeria. It is aimed

towards closing the short-term and high- interest financing gap for SME/Manufacturing and start-ups as well

as create jobs through the Real Sector of the Nigerian economy.

1.6.1 Disbursements

The sum of N3.5bn was disbursed to one (1) project within the second quarter, 2015 under RSSF.

1.6.2 Challenges

Inability to complete the application requirement on RSSF by the stakeholders

15

1.6.3 Way Forward

Introduce Interest Draw-back Programme (IDP). Stakeholders sensitization

1.7 Power and Airline Intervention Fund (PAIF)

The sum of N500 billion was approved by the Monetary Policy Committee in 2010 for investments in

debentures issued by the Bank of Industry (BOI) out of which the sum of N300 billion would finance power

and airline projects and N200 billion for RRF. PAIF was designed as part of the quantitative easing measure

to address the paucity of long-term credit and acute power shortage in the country.

1.7.1 Disbursements

The sum of N13.260 billion was released to two projects under the Power and Airline Intervention Fund

(PAIF) from April to June, 2015 (N9.924 billion was disbursed to one power project while one airline

project was N3.335 billion). Cumulatively, the total sum of N249.614 billion had been released to BOI

from inception to date and disbursed through banks to 55 projects (39 power projects received

N128.852 billion while 16 airline projects had N120.762 billion (Table 4).

Activity Report for the Month of: 2nd Quarter , 2015

PAIF FACILITY 300 Billion (N)

Amount released to BOI (April- June,2015) 13.260 billion

Net Amount Released to BOI as @ April-June, 2015 249.614billion

Amount Disbursed by BOI as @ April-June, 2015 249.614billion

Amount released to BOI but not yet disbursed to PBs as @ April-June, 2015

NIL

1.7.2 PAIF LOAN REPAYMENT

The sum of N5.329 billion was remitted by the BOI to CBN under the PAIF during the period under review. Bringing the total repayments to N53.101billion by fifty one (51) projects in the following order;

Table 5: PAIF LOAN REPAYMENTS RECEIVED BY CBN

Type No of Projects

Amount

Amount Paid to CBN as PAIF Repayments during the 2nd quarter, 2015

5,329,313,744.87

Airline Projects (From Inception) 15 27,009,598,482.30

Power Projects (From Inception) 36 20,762,312,409.15

Cumulative Amount Paid to CBN as PAIF Repayments 51 N53,101,224,636.32

1.7.3 Challenges

To ensure timely remittance of loan repayment to CBN by BOI;

1.7.4 Way Forward

Regular meetings with the Managing Agent (BOI) and Technical Adviser (AFC);

16

1.8 Nigeria Electricity Market Stabilisation Facility (NEMSF)

The Bank has established the Nigerian Electricity Market Stabilization Facility (NEMSF) in accordance with

Section 31 of the CBN Act, the Bank invested N213billion in a Refinancer – NESI Stabilization Strategy Ltd to

provide refinance for the NEMSF. The facility is aimed at putting the Nigerian Electricity Supply Industry (NESI)

on a route to economic viability and sustainability by facilitating the settlement of Legacy Gas Debts and payment

of outstanding obligations due to Market Participants, Service Providers and gas suppliers that accrued during the

Interim Rules Period (IRP Debts). NERC has also released a MYTO 2.1 and progressed the Industry from the

IRP to a Transition Electricity Market (TEM) Phase.

1.8.1 Disbursements

The total sum of N12.074 billion was approved and disbursed during the 2nd quarter, 2015 to nine (9) Market Participants under Nigeria Electricity Market Stabilisation Facility (NEMSF) as illustrated on the table below. Cumulatively, N64.755billion has so far been disbursed to 18 participants (Discos &

Gencos) in three batches from inception to June, 2015.

NEMSF Disbursements by Batches: Table 6

S/No NESI PARTICIPANT Cumulative No Amount Disbursed from April - June 2015

Cumulative Amount Disbursed

1. DISCOs 5 4,469,986.55 41,055,703,962.43

2. GENCOs 7 6,827,294,999.22 18,457,878,439.89

3. GASCOs 6 5,241,925,612.64 5,241,925,612.64

TOTAL 18 12,073,690,598.41 64,755,508,014.96

1.8.2 Challenges

Securing the buy-in of stakeholders on the Fund. Ensuring the GENCOs and DISCOs meet the disbursement criteria.

1.8.3 Way Forward Sensitization of stakeholders The Transaction Advisers should provide the necessary assistance to the GENCOs and DISCOs to

overcome the challenges;

PART TWO. FINANCIAL INCLUSION ACTIVITIES

Financial Inclusion is the delivery of financial services at affordable prices and terms to the generality of the populace especially the disadvantaged and low income segment of the society. The primary objective is to connect the unbanked population with the mainstream financial services. Pursuant to the implementation of the strategy, the following activities were executed: 2.1 ACTIVITIES

2.1.1 STATUS UPDATE FOR BANKERS’ COMMITTEE

The Department presented a status update on the progress of the Financial Inclusion at the 316th Bankers

Committee meeting in Lagos. The aim of the presentation was to intimate the Committee of the progress

recorded in the areas of pensions, credit and insurance.

Key comments that arose from the presentation included the following:

17

• That the Biometric Verification Number (BVN) which was hailed as a successful initiative was too narrow

in scope as it should have been extended to include the MFB’s rather than only the DMB’s due to the fact

that they play a critical role in Financial Inclusion.

• The need for more dispersion among financial service providers was emphasized to serve the rural areas

too.

2.1.2 2nd FINANCIAL INCLUSION TECHNICAL COMMITTEE MEETING

The 2nd meeting of the Financial Inclusion Technical Committee was held on 22nd April, 2015 to review the

progress of the National Financial Inclusion Strategy Implementation.

The following resolutions were taken;

That the Maiden edition of the Financial Inclusion Annual report was approved for presentation to the Steering Committee for approval before publication;

The expansion of Financial Inclusion working groups into four; Products, Channels, Special Interventions and Financial Literacy; and

To develop comprehensive monitoring and evaluation frameworks for the work plans of the working groups by the FI Secretariat.

2.1.3 7TH ANNUAL G24/AFI FINANCIAL INCLUSION ROUNDTABLE MEETING

The Department attended the 7th Annual G24/AFI Financial Inclusion Roundtable Meeting to discuss globally

relevant Financial Inclusion policy issues. The meeting focused on the promotion of the Financial Inclusion in line

with international standards.

Highlights from the meeting included;

That significant progress was recorded globally on financial inclusion; The need to support policies on financial inclusion for women in view of their high global financial

inclusion rate; and, The need for sustained global collaboration to address gaps through appropriate measures; and Challenges in the implementation of proportionate AML/CFT and Basel 11 and 111 requirements

highlighted. 2.1.4 EXTRAORDINARY MEETING OF THE FINANCIAL INCLUSION TECHNICAL COMMITTEE

An extraordinary meeting of the Financial Inclusion Technical Committee was held on 19th May, 2015. The aim of the meeting was to discuss the details of the Working Group work plans before presentation to the Financial Inclusion Steering Committee meeting scheduled for May 26, 2015. Highlights from the meeting included;

That the FIS should go beyond measuring number of adults using different products to include frequency of usage under the monitoring framework for Financial Inclusion working groups;

The Products Working Group should drill down on sustainability and risks involved in product

development;

Financial Literacy activities of all Working Groups should be transferred to the Financial Literacy working

group;

FIS should include Federal Ministry of Youth Development as NFIS stakeholder;

The Nigerian Stock Exchange should be included in the Financial Literacy working group

18

FIS should work with SEC to coordinate the development of their strategy including organizing stakeholder engagements to get their buy in; and

Work plans revised and recommended for approval by Steering Committee.

2.1.5 MEETING WITH THE WORLD BANK

The Department hosted a team from the World Bank on the 6th of May, 2015 to discuss areas of cooperation

between the Bank and the Financial Inclusion Secretariat. Discussions centred on capacity building for the

Secretariat and other financial service providers that promote financial inclusion.

The following resolutions were taken:

That in collaboration with the Federal Government of Nigeria, the Development Bank of Nigeria has been

approved to wholesale-lend to SMEs in the country.

That the World Bank was currently working with OFISD to pilot the World Bank Housing Credit Project

with 5 MFBs.

That the Secretariat will come up with specific capacity building programs around MSME finance for a

follow-up meeting.

2.1.6 WORKSHOP WITH HEADS OF STRATEGY OF DEPOSIT MONEY BANKS

A workshop was organized by the Department for Deposit Money Banks in CBN, Lagos within the period. The

workshop was aimed at discussing progress made by DMBs in fostering financial inclusion across the nation.

Presentations were made by CBN departments as well as all the DMBs present.

Key outcomes of the workshop were as follows:

That the CBN will not give a time frame for accounts migration between the three tiers in the Tiered K-Y-

C requirements;

That the CBN should reexamine revisit the guide to bank charges with a view to increase Commissions to

Agents as an incentive to adoption of agent banking;

That there should be increased awareness on Mobile and Agent Banking to the public;

That continuous effort should be made to address Infrastructural challenges hindering POS and Mobile

channels penetration;

That DMBs should adopt MFBs for the purpose of on-lending to MSMEs; and

That there should be technical assistance to illustrate the business cases of financial inclusion to

convince stakeholders to embrace the various interventions.

2.1.7 THE 6TH AFI FINANCIAL INCLUSION STRATEGY PEER LEARNING GROUP MEETING

The Department represented the Bank at the 6th Financial Inclusion Strategy Peer Learning Group meeting which was held in Kuala Lumpur from the 8th to 12th June, 2015. One of the objectives of the meeting was to facilitate peer learning on the different approaches to financial inclusion strategy development and implementation across the network.

The key take aways from the meeting include;

To develop and implement Financial Inclusion Strategies by engaging of all stakeholders especially the financial services providers.

To engage the Public Private collaborations, which are key to successful implementation of National Financial Inclusion Strategies.

19

To facilitate the understanding of the National Economic Plan of a country.

To harness the grant provided by the Alliance for Financial Inclusion (AFI) on policy and knowledge exchange to support AFI member institutions conduct research, develop and implement financial inclusion strategies/innovative policy solutions for financial inclusion.

2.1.8 2ND FINANCIAL INCLUSION WORKING GROUP MEETINGS

The Department organized the 2nd meeting of the Financial Inclusion Working Groups within the period. The

working groups were as follows:

Financial Inclusion Products Working Group – created to develop new products to foster financial

inclusion.

Financial Inclusion Channels Working Group – created to improve service delivery channels to improve

the level of financial inclusion in the country.

Financial Inclusion Special Interventions Working Group – created to focus on improve financial services

to women, youths and people living with disabilities.

2.1.9 FINANCIAL LITERACY WORKING GROUP INAUGURAL MEETING

The inaugural meeting of the Financial Literacy Working Group was held on the 24 th of June, 2015 at the

International Training Institute, Maitama. The aim of the meeting was to focus on modalities for creating

awareness on the output of the other working groups and to define policy propositions for adopting best practices

on financial literacy programme for Nigeria.

2.1.10 Challenges

Lack of appropriate visibility amongst certain stakeholders on the targets of the National Financial Inclusion Strategy

Low adoption of Agent Banking and inadequate dispersion of agents particularly in rural areas.

2.1.11 Going Forward

Concerted efforts to implement stakeholder engagement meetings planned for 2015.

Implementation of the Work Plans for the four Financial Inclusion Working Groups.

Capacity building for industry stakeholders, training scheduled to hold in July 2015

Engagement on planned research studies on critical financial inclusion initiatives to support NFIS implementation.

Leverage harmonized sensitization campaign to reach out to State governments across the nation of including financial inclusion to their policy directions.

PART THREE: ENTREPRENEURSHIP DEVELOPMENT INITIATIVES

3.1 Entrepreneurship Development Centres (EDCs)

The Entrepreneurship Development Centres were initiated by the Bank to unleash the entrepreneurial spirit of

youths to own/set up their own businesses, create employment and reduce poverty. During the period under

review, a number of activities were carried out;

3.1.1 Activities

a) During the period under review, the Department attended the MSME Conference week organized by Shield Academy Partners (the implementing Agency for the CBN South – South Entrepreneurship Development new centre) themed “Redefining and Redistributing Nigeria’s Wealth base.

20

The following were discussed at the Conference;

Accelerating Entrepreneurship Development and the Economic Outlook for 2015 and beyond;

From oil to soil: Rebranding agribusiness for the younger generation

From import to export: exploring new frontiers in Technology, tourism and textiles

b) Hosted the 22nd regular meeting of the CBN-EDC Governing Council in the period under review. The following were discussed at the meeting;

That the implementing Agencies should come up with strategies to enable the EDCs graduates access

the MSMEDF through their signed up Participating Financial Institutions.

To forestall hostilities within the community hosting the CBN-EDCs, the IAs were encouraged to host

Town hall meetings with the youth of the Community periodically to high light the importance of the EDC

programme in their localities.

c). In the quarter under review the existing EDCs located in North-East (Maiduguri), North-Central (Makurdi) and South-South (Calabar) had trained 2,632 Participants.

540 participants trained in North-East

509 participants trained in North-Central

745 participants trained in the South-South

Cumulatively from inception, 14,219 participants were trained, 10,427 jobs were created while 4,358 accessed a total of N742.513 funds as loan to start their businesses.

The 2 new EDC’s {located in North-West (Kano) and South-West (Ibadan); and one outreach Center located in the North-Central (Minna) had trained 894 out of a target of 1,350 participants. This represents 62.22% of the target (64.99% male and 35.01% female).

192 participants ( 154 male, 38 female) were trained in North-West

334 participants ( 110 male, 224 female) trained in South-West

368 participants (317 male, 51 female) trained in the North-Central outreach centre. Cumulatively from inception in January, 2015, 894 participants were trained under the EDCs while 492 jobs were

created.

3.1.2 Challenges Keeping to the timeline and securing stakeholders buy-in. Keeping to timeline in selecting consultants to operate the centres. Identifying the financing products for the EDC Graduates to key-in.

3.1.3 Going Forward

Engaging the would-be host State governments to operate under the Tripartite Agreement. Continue to sensitize the National, State and community on effective advocacy and prudent use of the

funds. The Bank and the Implementing Agencies (IAs) to continually explore areas of financial linkage for the

EDC graduates.

3.2. MSME DEVELOPMENT FUND (MSMEDF)

3.2.1 Activities

21

a). The sum of N8.118 billion was approved and disbursed to sixty two (62) PFI/States under the MSMEDF

Commercial Component within the 2nd quarter 2015, bringing the wholesale amount disbursed to N48.592 billion under the MSMEDF Commercial Component since inception. (Table 3)

Table 7 – MSMEDF Commercial Component Activity Summary: 2nd Quarter, 2015

Wholesale Fund Wholesale Amount 198 Billion

Wholesale Amount Disbursed in 2nd

Quarter, 2015

8,118.93

Cumulative Wholesale Amount

Disbursed to Date

48,592.70

Wholesale Balance as at end of 2nd

Quarter, 2015

149,407.30

b). Meeting with various Stakeholders Several meetings on stakeholders’ engagement were held during the period which includes;

Quintessential Business Women Association (QBWA), the Office of the Special Adviser to the president on Ethics and Value, the Nigerian Association of Federal Civil Servants Cooperatives, International Finance Corporation (IFC), the Federal Ministry of Women Affairs and Development, Bankers Committee and the Stakeholders of S-SPV and MFBs in Abia State. The discussions for all the meetings were centered on strategies to increase access to the MSME Development Fund.

c) Post Disbursement Verification Exercises Conducted In the 2nd Quarter, 2015 The Department conducted post disbursement verification exercises in thirteen (13) states during the

period, namely; Kebbi, Jigawa, Cross River, Sokoto, Bauchi, Benue, Gombe, Adamawa, Abia, Anambra, Akwa Ibom, Kwara and Ondo States. Some of the findings from the exercises which has been duly communicated to the MFBs, SPVs and DFO’s include;

Repayment schedule not properly communicated to beneficiaries Interest charged upfront Multiple borrowing was discovered The PFIs still had some undisbursed balances ranging from N15m to N50m Some PFIs in the State charged excess COT on clients Undisbursed funds ranging from N15m to N50m

3.2.2 Challenges

To emphasize prompt repayment to ensure fund tunnelling Secure the buy-in of State Govts/FCT in respect of MSMEDF Lack of loan processing software Inadequate staff complement to process application Low uptake of the fund

3.2.3 Going Forward

Ensure that MSMEDF funds are promptly disbursed to the projects Continue to collaborate with the Stakeholders on the way forward Deployment of FINO & BICS software Continue to engage more women to participate in MSMED fund

22

3.3 Microfinance Management

3.3.1 ACTIVITIES a). RURAL FINANCE INSTITUTION (RUFIN) CAPACITY BUILDING PROGRAMME The inauguration exercise for the 12 RUFIN implementing States was held from April 27 to May 7, 2015 at the CBN branches in the respective states. The RUFIN Strategic Implementation Committee was set up to assure the continuity of the programmes for enhanced and sustainable micro-financing activities Nigeria after the exit of the programme. The Committee consists of: i). Rural Finance Institution Building Programme (RUFIN) ii). State Chapter of Association of Non-Bank Microfinance Institutions of

Nigeria (ANMFIN) iIi). State Chapter of National Association of Microfinance Bank (NAMB) iv). Federal Department of Cooperatives/State Field Offices v) Bank of Agriculture vi). Branch Managers of RUFIN Partnering Financial Institutions and, vii). Head, Development Finance Office, Central Bank of Nigeria in the State The Terms of Reference of the Committee include: i) Meetings with partnering financial institutions (PFIs) and Ape Associations on quarterly basis. ii) Identify, nurture and encourage clients to participate under the programme. iii) Involve in capacity building exercise of RUFIN –Mentored PFIs and State Chapters of Apex Associations

on record keeping, loan appraisal, disbursement, monitoring, loan recovery, reporting, etc. v) Link clients in the rural areas to PFIs and encourage financial institutions to lend to rural dwellers to

enhance financial inclusion. vi) Make recommendations to CBN/RUFIN for policy formulation and decision making. Some of the recommendations made by the Committee include:

i. Meeting in the first week of the first month of the quarter and reports are to be sent to the Head Office on or before Friday of the second week.

ii. NAMB & ANMFIN would should with their members in the state to present position papers of happenings in the field and that will form part of working documents for the Committee in the state.

iii. The training manuals produced by RUFIN should be made available to the Committee to serve as a part of her working documents.

b). CONTRIBUTION OF $1.5 MILLION BY RUFIN

RUFIN partnered with NIRSAL in the deployment of $1.5million. The fund will serve as guarantee that would be domiciled and managed by NIRSAL. The guidelines and modalities for the operation of the Fund were approved by Management during the period. The $1.5 million contribution by RUFIN would increase the capacity of microfinance institutions access to MSMEDF and other available funds.

C) 10TH IFAD/RUFIN RURAL BUSINESS PLAN TRAINING

The Department attended the 10th IFAD/RUFIN Supervision Mission training on Rural Business Plan in Lafia and

Nasarawa State within the period. The programme was aimed at training the institutions/trainers on how to

develop a sustainable rural business plan. Other participants at the event included; ANMFIN, NAMB, Select

RUFIN Microfinance Banks and Non-Bank Microfinance Institutions.

23

The Supervision Mission also paid a visit to the Bank and met with the 3 Implementing Departments (Research,

Other Financial institutions and Development Finance Departments), Information Technology, Legal Services,

Banking and Payment Systems Departments, the Micro, Small and Medium Enterprises Development Fund

Office and NIRSAL. Discussions centred on the implementation of the activities on the approved Annual Work

Plan & Budget for the remaining part of the year.

Some of the recommendations of the Mission include:

CBN should lead the Rural Business Plan(RBP) through NAMB and ANMFIN

Regulation of Non-Bank MFIs should be promoted

CBN should develop a follow-up mechanisms and formats to track State level progress on RBP implementation.

d) NATIONAL MICROFINANCE POLICY CONSULTATIVE COMMITTEE (NMFPCC) A meeting of the National Microfinance Policy Consultative Committee (NMFPCC) was held during the period in review to discuss on issues and way forward for the NMFPCC. The following decisions were reached;

That the Committee would hold meetings on a quarterly basis;

That Technical Working group were to be constituted to tackle and review issues and proffers solutions for the Committee’s consideration;

To conduct an evaluation of service providers and review the curriculum of the Certification programme for MFBs;

That the NDIC would collaborate with NAMB to verify claims by its clients; and,

That the ANMFIN would submit a proposal for the establishment of a Microfinance Act to CBN for its consideration.

e). DATABASE FOR NON-BANK MICROFINANCE INSTITUTIONS

The Department in conjunction with the Information Technology Department of the Bank developed a software

application that will drive the database of the activities of Non-Bank Microfinance Institutions (NB-MFIs) in

Nigeria. The focus of the application is to enable DFD keep an adequate record and seamlessly update records

of NON-Bank-MFIs towards monitoring and effectively managing the growth of the sector, as well as provide

reliable inputs for policy formulation and decision making. The application can be accessed via ‘applications’ on

the Banknet.

Training had been done in six geo-political zones of the country, which focused on how to operate the database

as well as the features of the modules on the application. Errors or some features were highlighted to be

corrected on the application and the ITD had effected the corrections. Finally, a Sign-Off of User’s Manual and

Guide had been done and the application will go live in May, 2015.

Questionnaire for update and validation of data on the database was forwarded to the DFOs. This will be used to

validate existing data on non-bank MFIs and also update information on the database.

3.3.2. Challenges

Implementation of recommendations of the RUFIN Mission Team and outstanding activities for the year.

Update and validation of information on the MFI Database by DFOs

24

3.3.3 Going Forward

Commence implementation of recommendations by the various implementing Departments. Implementation of outstanding activities on the 2015 Annual Work Plan and Budget.

Consistent update of information by the DFOs

4.1 Commodity Promotion Activities

4.1.1 Achievements

a). INTER – AGENCY MEETING ON MYCOTOXIN CONTROL IN NIGERIA (PAMYCON) The Department participated in an Inter-Agency meeting hosted by Raw Materials Research & Development Council with other stakeholder within the period. The meeting deliberated on strategies for reducing mycotoxins (poisonous chemical compounds) contamination in food and animal feedstock while focus was on Aflatoxin which is a form of mycotoxin. The Strategies include:

To enhance stakeholder’s awareness and demand for aflatoxin safe food and feed through improved

communication and awareness creation, strengthen capacity for aflatoxin sampling and risk

assessment;

To improve the crop management and post-harvest handling practices to mitigate aflotoxin

contamination in food and feed through enhanced use of available technology for crop production,

harvesting and processing; and

To create an enabling policy and regulatory environment for controlling aflatoxin in food and feed

.Strengthen farmers association and value chain actors as a driving force for market related initiatives.

b). ANNUAL POULTRY SUMMIT

The Department attended the Annual Poultry Summit organized Poultry Association of Nigeria within the

period in Lagos to deliberate on the importance of poultry to the socio-economic development of the country.

Strategies to further strengthened and reposition the poultry industry for export was also developed.

Some of the decisions that formed the communiqué include:

The need to bring the attention of the Government and the Federal Ministry of Agriculture and Rural Development to the contribution of poultry production towards the Gross Domestic Product (GDP) of the Nigerian economy.

Developing a National Policy on Poultry to achieve the Nigerian Poultry Vision 2013-2023 on becoming one of the world’s great poultry producing nations.

That as part of incentives to promote the expansion of the industry, reduction in tariffs, corporate tax and an increase in investor’s tax credit from 2014-2023 be granted to all Poultry farmers

The need for the association to work with other commodity associations such as Maize and Soya bean Associations, the Research National Strategic Grain Reserve to ensure a synergy for adequate supply of quality raw materials for feed at competitive prices.

The Summit reiterates the urgent need to resuscitate the “An Egg a Day” School Feeding Programme as enshrined in the UBE Commission Act not only to promote the consumption of poultry products, but to ensure improved health to school children and increase school enrolment

c). The National Survey on Agricultural Exportable Commodity Statistics in Nigeria (CCAECS)

COG approved the conduct of the National Survey on Agricultural Exportable Commodities Statistics in Nigeria for year 2013/14 and 2014/15 surveys. Members of the Committee on Agricultural Exportable Commodity include

25

the National Bureau of Statistics (NBS), the Federal Ministry of Agriculture and Rural Development (FMA&RD and the Federal Ministry of Industry, Trade and Investment and Central Bank of Nigeria.

The Agricultural Exportable Commodity Committee met on June 9 and 18th June, 2015 to deliberate on the modalities and timelines for the National Survey on Agricultural Exportable Commodities Statistics in Nigeria earlier approved by the COG for year 2013/14 and 2014/15 considering its relevance to national planning and economic development.

Deliberations centered on:

Action plan for the survey

The scope of the survey

The Budget

Financial contributions of the collaborating agencies to the funding of the survey to ensure sustainability

Review of the questionnaire for the survey

Training

4.2 OTHERS: 4.2.1 Achievements Conducted the inaugural edition of the 2015 DFD Seminar Series titled: “Nigeria Electricity Market

Stabilization Fund (NEMSF): CBN Power Sector Issues Resolution Initiative”.

Delivered presentations to students’ representatives from a variety of Tertiary Institutions on educational visit

to the Bank. The presentation titled “Development Finance: An Instrument for Economic Growth and Wealth

Creation” is a routine presentation as part of the package for students on educational visit to the Bank.

Compiled by: Board Matters & Publications Office, Development Finance Department, Central Bank of Nigeria, Abuja. JUNE, 2015