Deutsche Bank Energy & Utilities...

38

0 Deutsche Bank Energy & Utilities Conference Steve Snider President and Chief Executive Officer Michael Anderson Senior Vice President and Chief Financial Officer May 29, 2008

Transcript of Deutsche Bank Energy & Utilities...

0

Deutsche Bank Energy & Utilities Conference

Steve SniderPresident and ChiefExecutive Officer

Michael AndersonSenior Vice President and Chief Financial Officer

May 29, 2008

1

ForwardForward--Looking StatementsLooking StatementsAll statements in this presentation (and oral statements made regarding the subjects of this presentation) other than historical facts are forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements rely on a number of assumptions concerning future events and are subject to a number of uncertainties and factors that could cause actual results to differ materially from such statements, many of which are outside the control of Exterran Holdings, Inc. and Exterran Partners, L.P. (the “Companies”). Forward-looking information includes, but is not limited to: statements regarding the value and effect of the merger, including operating efficiencies, cost savings and synergies, and the Companies’ abilities to realize that value; the industry fundamentals, including the attractiveness of returns, stability of cash flows and demand dynamics, and the Companies’ abilities to realize the benefits thereof; the benefits realized by contract operations customers; the continuing international expansion of Exterran Holdings’ product lines; the continuation of industry growth drivers and the Companies’ abilities to take advantage of them; the Companies’ operational and financial strategies, and the Companies’ abilities to successfully effect those strategies; the Companies’ financial and operational outlook and ability to fulfill that outlook; demand for the Companies’ products and services and growth opportunities for those products and services; the ability of Exterran Holdings and Exterran Partners to complete a possible transaction and the expected benefits of such a transaction; and Exterran Holdings’ intention to offer and sell other assets to Exterran Partners over time.

While the Companies believe that the assumptions concerning future events are reasonable, they caution that there are inherent difficulties in predicting certain important factors that could impact the accuracy of the forward-looking information. The factors that could cause results to differ materially from those indicated by such forward-looking statements include, but are not limited to: changes in Exterran Holdings’ credit rating and the factors that impact its credit rating; the failure to realize anticipated synergies from the merger; changes in master limited partnership equity markets and overall financial markets that impact the effect of the drop-down of additional assets from Exterran Holdings to Exterran Partners; changes in tax laws that impact master limited partnerships, including drop-downs of additional assets to Exterran Partners; conditions in the oil and gas industry, including a sustained decrease in the level of supply or demand for natural gas and the impact on the price of natural gas; Exterran Holdings’ ability to timely and cost-effectively obtain components necessary to conduct the Companies’ business; changes in political or economic conditions in key operating markets, including international markets; the Companies’ abilities to timely and cost-effectively integrate their enterprise resource planning systems; changes in safety and environmental regulations pertaining to the production and transportation of natural gas; and, with respect to each of the Companies, the performance of the other entity.

These forward-looking statements are also affected by the risk factors, forward-looking statements and challenges and uncertainties described in the Companies’ Annual Reports on Form 10-K for the year ended December 31, 2007, and those set forth from time to time in the Companies’ filings with the Securities and Exchange Commission, which are currently available at www.exterran.com. Except as required by law, the Companies expressly disclaim any intention or obligation to revise or update any forward-looking statements whether as a result of new information, future events or otherwise.

2

COMPANY OVERVIEWCOMPANY OVERVIEW

3

Exterran Exterran –– New Organization with Market LeadershipNew Organization with Market Leadership

Global leader in full service natural gas compression

– Growing presence as premier provider of service and equipment for oil and gas production, processing and transportation

– Strategy focused on leadership in oil and gas infrastructure and surface production solutions

New company resulting from 2007 merger between Hanover Compressor and Universal Compression, formerly the two largest participants in the full service natural gas compression industry

$4.7 billion in market capitalization (NYSE: EXH)

Owns 51% of Exterran Partners (NASDAQ: EXLP)

Headquartered in Houston, Texas

1 As of May 23, 2008; based on EXH shares outstanding as of April 30, 2008.

1

4

Exterran Exterran –– Investment Merits Investment Merits

Global market leadership in product and service lines

Business model with stable cash flows and strong financial returns

Attractive long-term industry growth opportunities

– Primary drivers are growing natural gas production and expanding international energy infrastructure

– Growing Total Solutions business and build-own-operate projects

Successful track record of redeploying North American cash flow into growing international sector

– We believe the master limited partnership (MLP) enhances strategy through access to lower cost of capital

5

Breadth of ProductBreadth of Product

Leading service solutions company, with expertise incompression, production and processing equipment

Processing and TreatingProduction

Compression

CrudeWellFluid

H2 O for Disposal

NGLLiquid Fractionation

GasGas Compression

Gas Metering

Gas Processing

Gas Dehydration

Gas Treating(H2 S / CO2 Disposal)

Crude Dehydration

DesaltingSeparationHeating

WaterTreatment

CrudeDistillation

Topping Plant

6

Product Mix Product Mix –– 1Q 20081Q 2008

Three Months ended March 31, 2008

1Q 2008 Gross Margin Mix

PRODUCT LINE ($ millions) Operating Revenue

GrossMargin

Gross Margin %

North American Contract Operations $199 $111 56%International Contract Operations 120 81 67%Aftermarket Services 84 17 20%Fabrication 337 73 22%Total $740 $282 38%

1 See Addendum II for information on gross margin

1

Aftermarket Services

6%

Fabrication26%

Int'l Contract Operations

29%

North American Contract Operations

39%

7

PRODUCT LINESPRODUCT LINES

8

Contract Operations Contract Operations -- CompressionCompression

Wellhead

• Enable natural gas production

• Maintain reservoir pressure

Gathering & Processing

• Deliver natural gas to processing facilities

• Pressurize natural gas into and out of processing plants

Pipelines & Storage

• Move natural gas long distances

• Inject and withdraw natural gas from storage facilities

Distribution

• Move natural gas into industrial and rural locations

• Deliver natural gas to city gates

• LNG

Compression is a “must-run” service required at each phase of the natural gas production and transportation cycle

9

Reasons for Customer Outsourcing to ExterranReasons for Customer Outsourcing to Exterran

OPERATING EXPERTISE

Superior run-time

Lower operating costs

CAPITAL COST

Eliminate hard asset investments

Refocus capital

ASSET MANAGEMENT

Outsource asset management

Eliminate reapplication risk

CUSTOMER BENEFITSEnhanced production or

transportation volumes

Improved cash flow

Better ROIC

10

0

5

10

15

20

1990 1992 1994 1996 1998 2000 2002 2004

Contract Contract Operations Operations -- CompressionCompression

Total Production

Source: Energy Information Administration

Conventional and other Unconventional

Unconventional production from tight sands, coalbed methane and shale gas is boosting compression demand

(Trillion cubic feet)

Evolving U.S. Natural Gas Market

% Unconventional Production

15%

44%

11

Contract Contract OperationsOperationsNorth America and International Revenue Growth

1 The merger of Hanover Compressor Company with Universal Compression Holdings, Inc. into the new combined company, Exterran Holdings, Inc., was completed on August 20, 2007. Hanover was the acquirer for accounting purposes and, as a result, Exterran Holdings’ financial statements include Universal’s results for only the periods following the merger’s completion. Periods prior to the merger reflect only Hanover’s results.

1

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

2003 2004 2005 2006 2007

North America International

($ millions)

Strategy to offer more Total Solutions projects under long-term contracts expected to enhance international contract operations growth

12

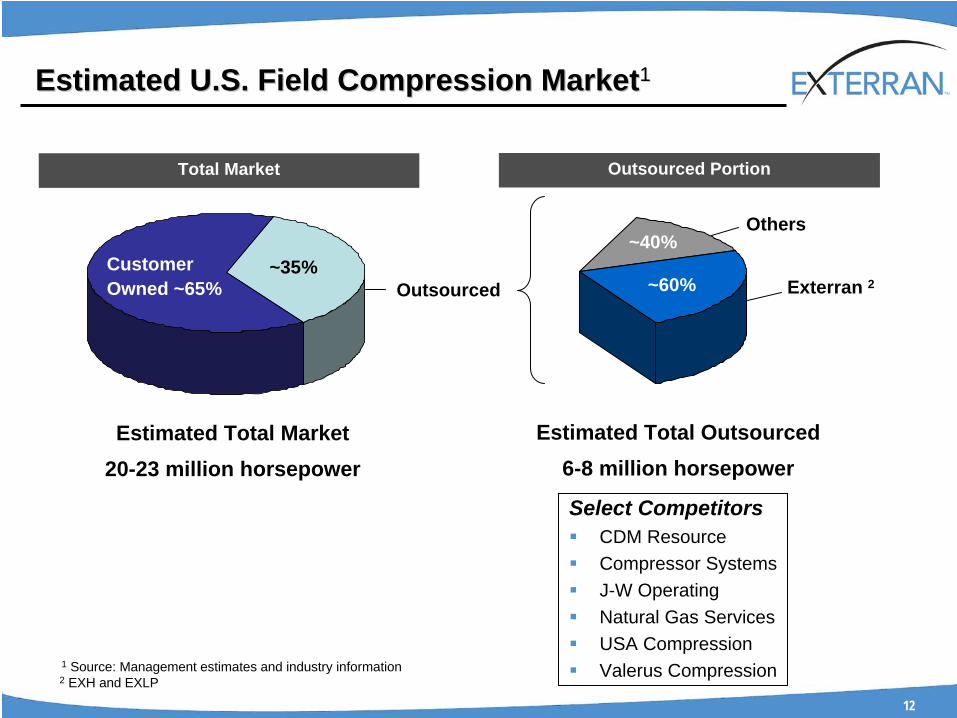

Estimated U.S. Field Compression MarketEstimated U.S. Field Compression Market11

1 Source: Management estimates and industry information

CustomerOwned ~65% Outsourced

Estimated Total Market20-23 million horsepower

Estimated Total Outsourced6-8 million horsepower

Select CompetitorsCDM ResourceCompressor SystemsJ-W OperatingNatural Gas ServicesUSA CompressionValerus Compression

Total Market Outsourced Portion

Others

~35%~40%

~60% Exterran 2

2 EXH and EXLP

13

$0

$50

$100

$150

$200

$250

$300

2003 2004 2005 2006 2007

($ millions)

Aftermarket ServicesAftermarket Services

Aftermarket Services Revenue1

Provides services for customer-owned equipment– Operations, service, maintenance and parts sales

Allows Exterran to generate revenue from customer-owned equipment– Potential interim step to convert customers to outsourced model

Expanding international network through small acquisitions

1 The merger of Hanover Compressor Company with Universal Compression Holdings, Inc. into the new combined company, Exterran Holdings, Inc., was completed on August 20, 2007. Hanover was the acquirer for accounting purposes and, as a result, Exterran Holdings’ financial statements include Universal’s results for only the periods following the merger’s completion. Periods prior to the merger reflect only Hanover’s results.

14

FabricationFabrication

Fabrication Backlog (Third Party Sales Only)1

Designs, engineers, fabricates and sells natural gas compressors and equipment used in the production, treating and processing of oil and gasFabricates equipment for contract compression fleet and Total Solutions contract operationsBelleli Energy provides equipment for refineries, petrochemical facilities, desalination plants and tank farms

$643 Belleli Energy

$354 Compression

$276 Production & Processing

1 The merger of Hanover Compressor Company with Universal Compression Holdings, Inc. into the new combined company, Exterran Holdings, Inc., was completed on August 20, 2007. Hanover was the acquirer for accounting purposes and, as a result, Exterran Holdings’ financial statements include Universal’s results for only the periods following the merger’s completion. Periods prior to the merger reflect only Hanover’s results.

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

6/03 12/03 6/04 12/04 6/05 12/05 6/06 12/06 6/07 12/07

($ millions)

Backlog of $1.3 billionat 3/31/08:

15

Total Solutions ProjectsTotal Solutions Projects

Project under construction in Oman

Bundles two or more Exterran products and servicesIntegrated product offering demand is particularly strong in Eastern Hemisphere and Latin America Strategy to capture more of these projects in the form of contract operations rather than sale

16

Selected Total Solutions Projects in ExecutionSelected Total Solutions Projects in Execution

1 As of March 31, 2008

Note: EPF denotes Early Production Facility

Processing(US)

Processing(US)

Compression(Mexico)

Compression(Brazil)

Compression(Venezuela)

Processing(Venezuela)

Processing(Venezuela)

EPF(Gabon)

Processing(Kazakhstan)

Compression(Russia)

Processing(Pakistan)

Processing(Oman)Compression

(Oman)

Processing(Egypt)

Compression(Russia)

Processing(Kurdistan)

Contract OperationsSales

Processing(Kazakhstan)

Power(Peru)

Offshore Compression(Brazil)

Processing(Kazakhstan)

Compression(Brazil)

Processing(US)

Processing(Brazil)

Compression(Brazil)Compression

(Brazil)

1

17

MARKET OVERVIEWMARKET OVERVIEW

18

26

6

67

0

50

100

3,535

1,234

116

-

2,000

4,000

6,000

8,000

10,000

12,000

~35%

~65%

Global Growth OpportunitiesGlobal Growth Opportunities

CustomerOwned ~65%Annual Gas Production (TCF) Exterran Contracted Horsepower (000s) *

Source of gas production data: Energy Information Administration* At March 31, 2008

The international market, encompassing the majority of natural gas production, is largely untapped by contract operations

– Ability to provide production and processing equipment improves Exterran’s international position

U.S. & Canada Eastern HemisphereLatin America

Eastern Hemisphere Opportunity

19

Expanded Worldwide CoverageExpanded Worldwide Coverage

Fabrication LocationsOther Major International Locations

(multiple locations)

20

Industry Growth DriversIndustry Growth Drivers

Growing worldwide gas demandInternational expansion of gas infrastructureTrend towards outsourcing/build-own-operateDeclining reservoir pressuresIncreasing unconventional gas production in the United States

Natural Gas Demand – Historical and Projected

Source: Energy Information Administration

0

20

40

60

80

100

120

140

160

180

1980 1990 2000 2004 2010 2015 2020 2025 2030

Cubi

c Fe

et (i

n Tr

illio

ns)

United States International

21

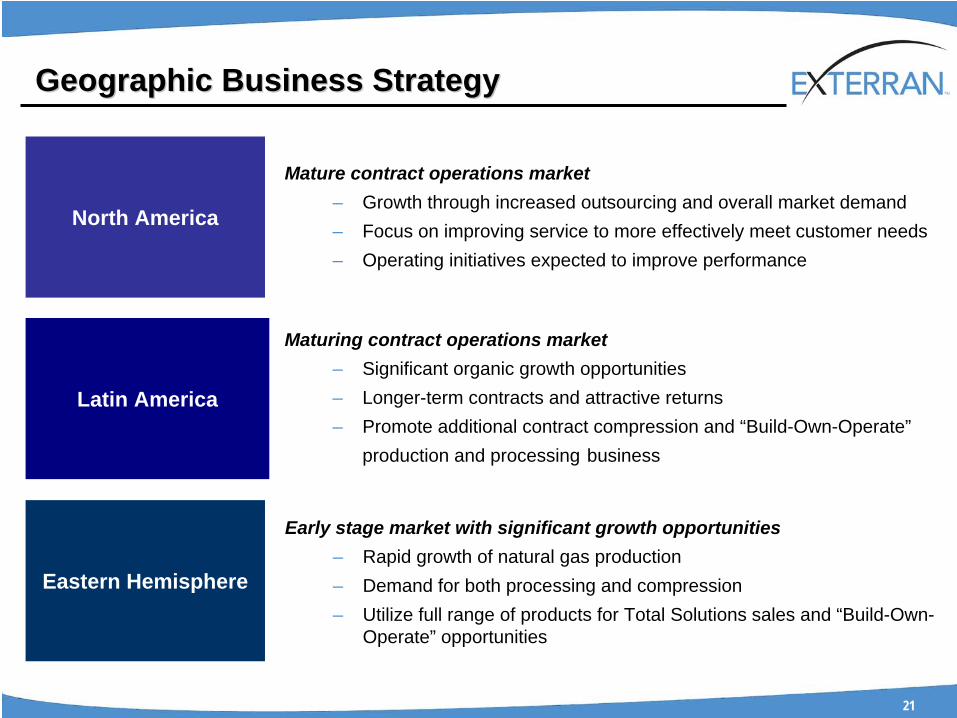

Geographic Business StrategyGeographic Business Strategy

Eastern Hemisphere

Maturing contract operations market– Significant organic growth opportunities– Longer-term contracts and attractive returns– Promote additional contract compression and “Build-Own-Operate”

production and processing business

Latin America

Mature contract operations market– Growth through increased outsourcing and overall market demand– Focus on improving service to more effectively meet customer needs– Operating initiatives expected to improve performance

North America

Early stage market with significant growth opportunities– Rapid growth of natural gas production– Demand for both processing and compression– Utilize full range of products for Total Solutions sales and “Build-Own-

Operate” opportunities

22

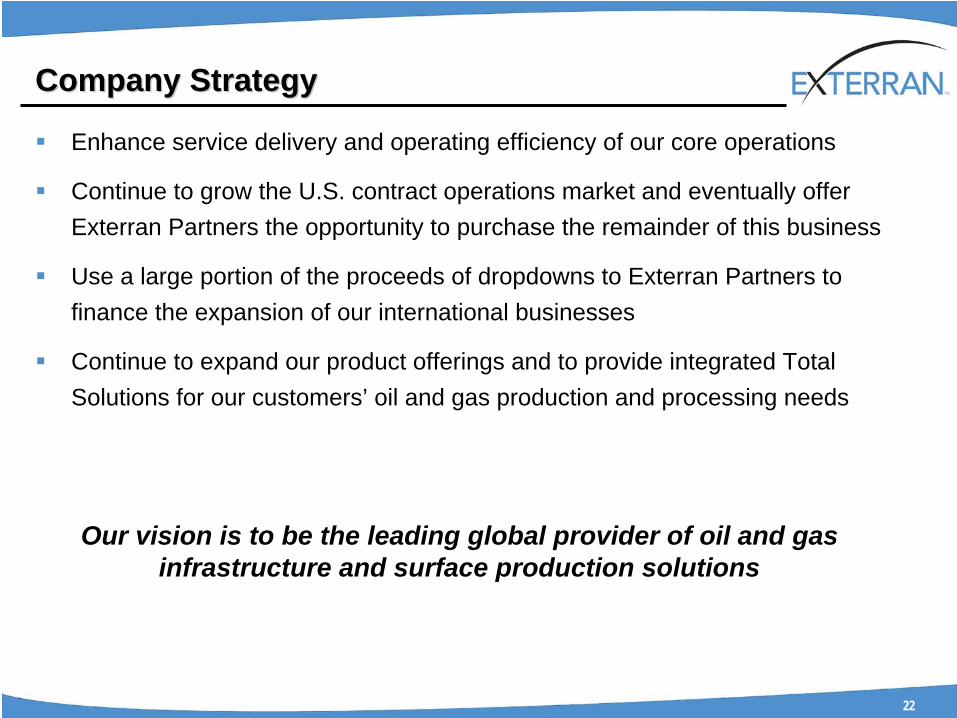

Company StrategyCompany Strategy

Enhance service delivery and operating efficiency of our core operations

Continue to grow the U.S. contract operations market and eventually offer Exterran Partners the opportunity to purchase the remainder of this business

Use a large portion of the proceeds of dropdowns to Exterran Partners to finance the expansion of our international businesses

Continue to expand our product offerings and to provide integrated Total Solutions for our customers’ oil and gas production and processing needs

Our vision is to be the leading global provider of oil and gas infrastructure and surface production solutions

23

FINANCIAL OVERVIEWFINANCIAL OVERVIEW

24

Financial OverviewFinancial Overview

Stable and growing cash flow business

Positive earnings momentum from merger of Hanover & Universal

Refinanced capital structure provides flexibility and low cost

Operating cash flow generation provides capital for international expansion

MLP drop-down strategy enhances cash flow and valuation of EXH

25

Historical Financial OverviewHistorical Financial Overview

1 The merger of Hanover Compressor Company with Universal Compression Holdings, Inc. into the new combined company, Exterran Holdings, Inc., was completed on August 20, 2007. Hanover was the acquirer for accounting purposes and, as a result, periods prior to the merger reflect only Hanover’s results.

2 Periods reflect December 31st year-end, except as otherwise noted. Exterran reports EBITDA, as adjusted; see Addendum II.3 EBITDA, as adjusted, is $212.5 million and $211.2 million for 4Q07 and 1Q08, respectively; see Addendum II.

EBITDA, as adjusted 1,2

3

$223$289

$420

$621

$317

$847

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

2003 2004 2005 2006 2007 6 Mos Ended3/31/08

Annualized

($ millions)

26

First Quarter ResultsFirst Quarter Results

1 The merger of Hanover Compressor Company with Universal Compression Holdings, Inc. into the new combined company, Exterran Holdings, Inc., was completed on August 20, 2007. Hanover was the acquirer for accounting purposes and, as a result, periods prior to the merger reflect only Hanover’s results.

2 See Addendum II for information on EBITDA, as adjusted, and gross margin.

($ millions except per share data) 2008 2007 Growth

Revenue and other income $740 $448 65%

Gross margin 2 $282 $155 82%

EBITDA, as adjusted 2 $211 $118 79%

Diluted EPS $0.73 $0.71 3%

Backlog $1,273 $773 65%

Three Months Ended 1March 31,

27

Historical Financial OverviewHistorical Financial Overview

1 The merger of Hanover Compressor Company with Universal Compression Holdings, Inc. into the new combined company, Exterran Holdings, Inc., was completed on August 20, 2007. Hanover was the acquirer for accounting purposes and, as a result, periods prior to the merger reflect only Hanover’s results.

2 Periods reflect December 31st year-end, except as otherwise noted. Exterran reports EBITDA, as adjusted; see Addendum II.3 For the 2007 and 3/31/08 periods, the calculation is based upon annualized EBITDA, as adjusted, for 4Q07 and 1Q08, respectively; see

Addendum II.

Debt to EBITDA, as adjusted 1,2

8.00

5.694.66

3.26 2.75 2.75

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

2003 2004 2005 2006 2007 3/31/20083 3

28

Capital StructureCapital Structure

($ millions)

1 Excludes effect of interest rate swap agreements and amortization of debt issuance costs.2 Approximately $357 million of letters of credit outstanding at March 31, 2008.3 Facility size based upon May 2008 facility expansion.

March 31, 2008 Debt Structure(as modified)

Debt structure provides low cost, financial flexibility and significant credit availability

Funded FacilityType Amount Size Rate1 Maturity Rating

Senior Secured Revolver $365 $850 2 L+82.5 2012 BB+/Ba2Senior Secured Term Loan 800 800 L+82.5 2013 BB+/Ba2ABS Notes 800 1,000 L+82.5 2012 n/aConvertible Notes 144 144 4.75% 2014 BB/N/aEXLP Secured Revolver 217 433 3 L+100 2011 n/aShort-Term Debt - - various various n/a

$2,326 $3,227

29

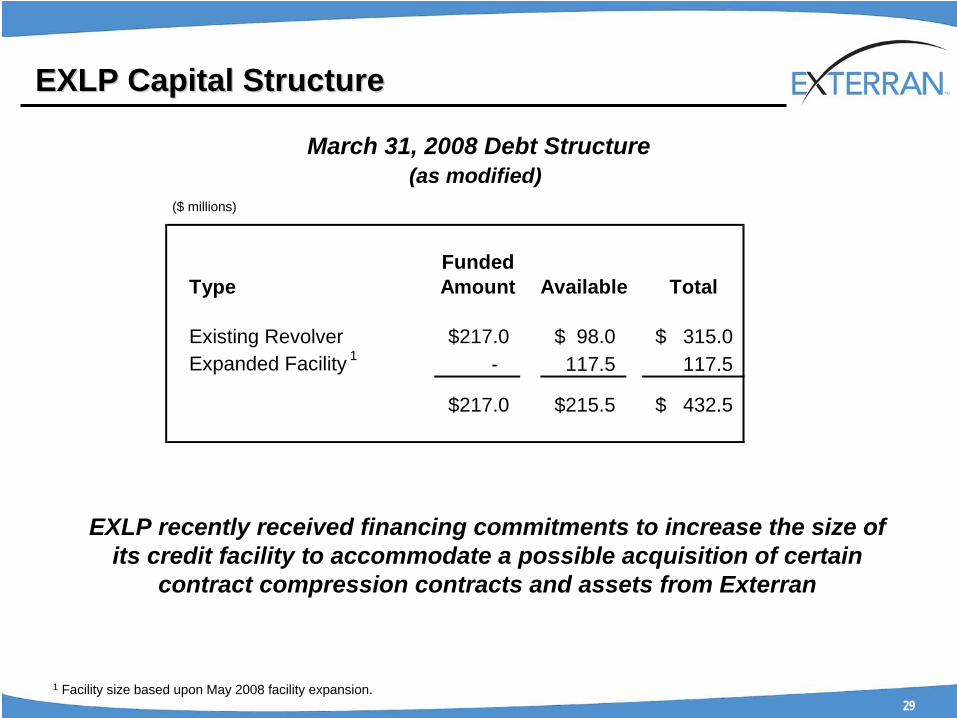

EXLP Capital StructureEXLP Capital Structure

($ millions)

1 Facility size based upon May 2008 facility expansion.

EXLP recently received financing commitments to increase the size of its credit facility to accommodate a possible acquisition of certain

contract compression contracts and assets from Exterran

FundedType Amount Available Total

Existing Revolver 217.0$ 98.0$ 315.0$ Expanded Facility 1 - 117.5 117.5

217.0$ 215.5$ 432.5$

March 31, 2008 Debt Structure(as modified)

30

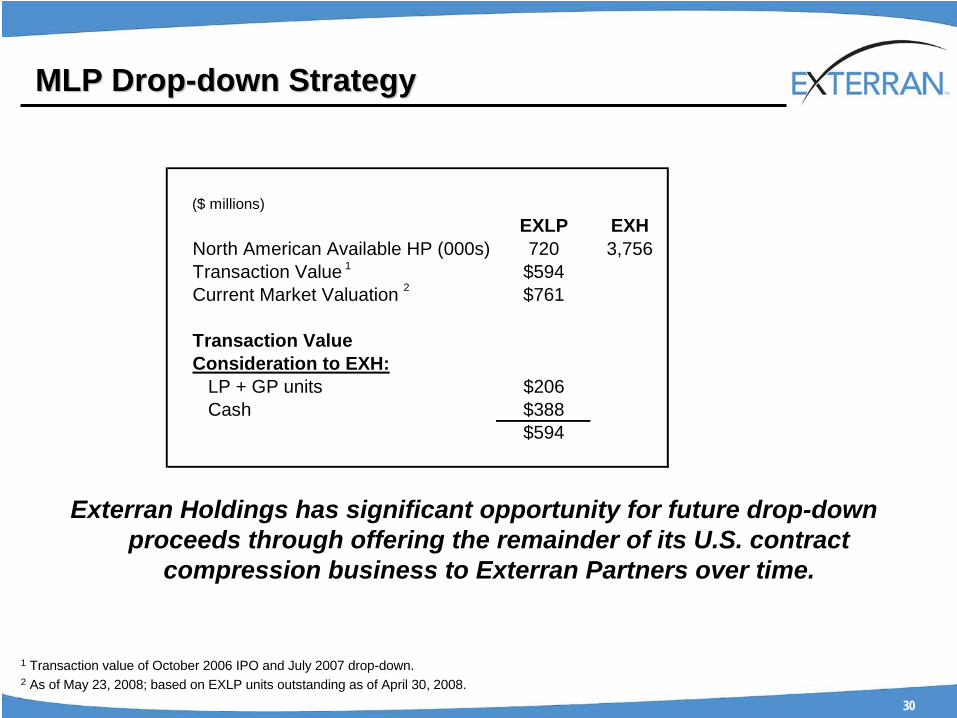

MLP DropMLP Drop--down down StrategyStrategy

Exterran Holdings has significant opportunity for future drop-down proceeds through offering the remainder of its U.S. contract

compression business to Exterran Partners over time.

1 Transaction value of October 2006 IPO and July 2007 drop-down.2 As of May 23, 2008; based on EXLP units outstanding as of April 30, 2008.

2

1

($ millions)EXLP EXH

North American Available HP (000s) 720 3,756Transaction Value $594Current Market Valuation $761

Transaction ValueConsideration to EXH: LP + GP units $206 Cash $388

$594

31

Exterran Exterran –– Investment Merits Investment Merits

Global market leadership in product and service lines

Business model with stable cash flows and strong financial returns

Attractive long-term industry growth opportunities

– Primary drivers are growing natural gas production and expanding international energy infrastructure

– Growing Total Solutions business and build-own-operate projects

Successful track record of redeploying North American cash flow into growing international sector

– We believe the MLP enhances strategy through access to lower cost of capital

32

APPENDIXAPPENDIX

Results Results -- ExterranExterran

Addendum I

4Q07 1Q08Revenues:

North America contract operations 203.0$ 199.1$ International contract operations 111.4 119.9 Aftermarket services 102.3 84.2 Fabrication 436.7 336.9 Revenue 853.4$ 740.1$

Expenses:North America contract operations 86.3$ 88.3$ International contract operations 40.4 39.4 Aftermarket services 82.6 66.9 Fabrication 362.4 263.7

571.7$ 458.3$

Gross Margin:North America contract operations 116.7$ 110.8$ International contract operations 71.0 80.5 Aftermarket services 19.7 17.2 Fabrication 74.3 73.2

281.7$ 281.7$

($ millions)

1 See Addendum II for information on gross margin

1

NonNon--GAAP Financial MeasuresGAAP Financial Measures

EBITDA, as adjusted, a non-GAAP measure, is defined as income from continuing operations plus income taxes, interest expense (including debt extinguishment costs and gain or loss on termination of interest rate swaps), depreciation and amortization expense, impairment charges, merger and integration expenses, minority interest, excluding non-recurring items, and extraordinary gains or losses.

Gross margin, a non-GAAP measure, is defined as total revenue less cost of sales (excluding depreciation and amortization).

Management believes disclosure of EBITDA, as adjusted, and gross margin, when viewed with our GAAP results and accompanying reconciliations, provide a more complete understanding of our performance than GAAP results alone. Management uses EBITDA, as adjusted, and gross margin as supplemental measures to review current period operating performance, comparability measures and performance measures for period to period comparisons. In addition, EBITDA, as adjusted, is used by management as a valuation measure.

Addendum II-A

NonNon--GAAP Financial Measures (cont.)GAAP Financial Measures (cont.)

Addendum II-B

1

1 The merger of Hanover Compressor Company with Universal Compression Holdings, Inc. into the new combined company, Exterran Holdings, Inc., was completed on August 20, 2007. Hanover was the acquirer for accounting purposes and, as a result, Exterran Holdings’ financial statements include Universal’s results for only the periods following the merger’s completion. Periods prior to the merger reflect only Hanover’s results.

($ millions)1Q07 4Q07 1Q08

Reconciliation of GAAP to Non-GAAP Financial Information:Income from continuing operations 25.4$ 58.5$ 49.0$ Depreciation and amortization 49.5 85.8 90.5 Fleet impairment - - 1.5 Interest expense 28.3 35.0 33.2 Merger and integration expenses 0.3 9.3 4.4 Minority interest - 3.9 2.6 Provision for income taxes 14.4 20.0 30.0

EBITDA, as adjusted 117.9 212.5 211.2

Selling, general and administrative 49.9 89.7 89.6 Equity in (income) loss of non-consolidated affiliates (5.7) (5.5) (6.1) Other (income) expense (7.6) (15.0) (13.0) Gross margin 154.6$ 281.7$ 281.7$

Addendum II-C

1NonNon--GAAP Financial Measures (cont.)GAAP Financial Measures (cont.)

1 The merger of Hanover Compressor Company with Universal Compression Holdings, Inc. into the new combined company, Exterran Holdings, Inc., was completed on August 20, 2007. Hanover was the acquirer for accounting purposes and, as a result, Exterran Holdings’ financial statements include Universal’s results for only the periods following the merger’s completion. Periods prior to the merger reflect only Hanover’s results.

($ millions) 2003 2004 2005 2006 2007

Reconciliation of GAAP to Non-GAAP Financial Information:

Income (loss) from continuing operations (117.5)$ (54.1)$ (37.1)$ 85.7$ 34.6$ Depreciation and amortization 159.3 165.1 172.6 175.9 252.7 Fleet impairment - - - - 61.9 Impairment of investment in non-consolidated affiliate - - - - 6.7 Impairment of goodwill 35.5 - - - - Securities related litigation settlement 43.0 (4.2) - - - Interest expense 99.0 157.2 147.0 123.5 130.1 Debt extinguishment costs - - 7.3 5.9 70.2 Merger and integration expenses - - - - 46.7 Minority interest - - - - 6.3 Provision (benefit) for income taxes 3.6 24.8 27.7 28.8 11.9 EBITDA, as adjusted 222.9$ 288.8$ 317.5$ 419.8$ 621.1$

Year Ended December 31,