Detecting & Deterring Fraud: How to Prepare and … N...Detecting & Deterring Fraud: How to Prepare...

19

Detecting & Deterring Fraud: How to Prepare and Protect Against Fraud AFOA Conference – February 18, 2016 Presenters: Andrew Bourne (BDO Canada LLP) & Shannon Walker (WhistleBlower Security)

-

Upload

dangnguyet -

Category

Documents

-

view

225 -

download

0

Transcript of Detecting & Deterring Fraud: How to Prepare and … N...Detecting & Deterring Fraud: How to Prepare...

Detecting & Deterring Fraud: How to Prepare and Protect

Against Fraud

AFOA Conference – February 18, 2016

Presenters: Andrew Bourne (BDO Canada LLP) & Shannon Walker (WhistleBlower Security)

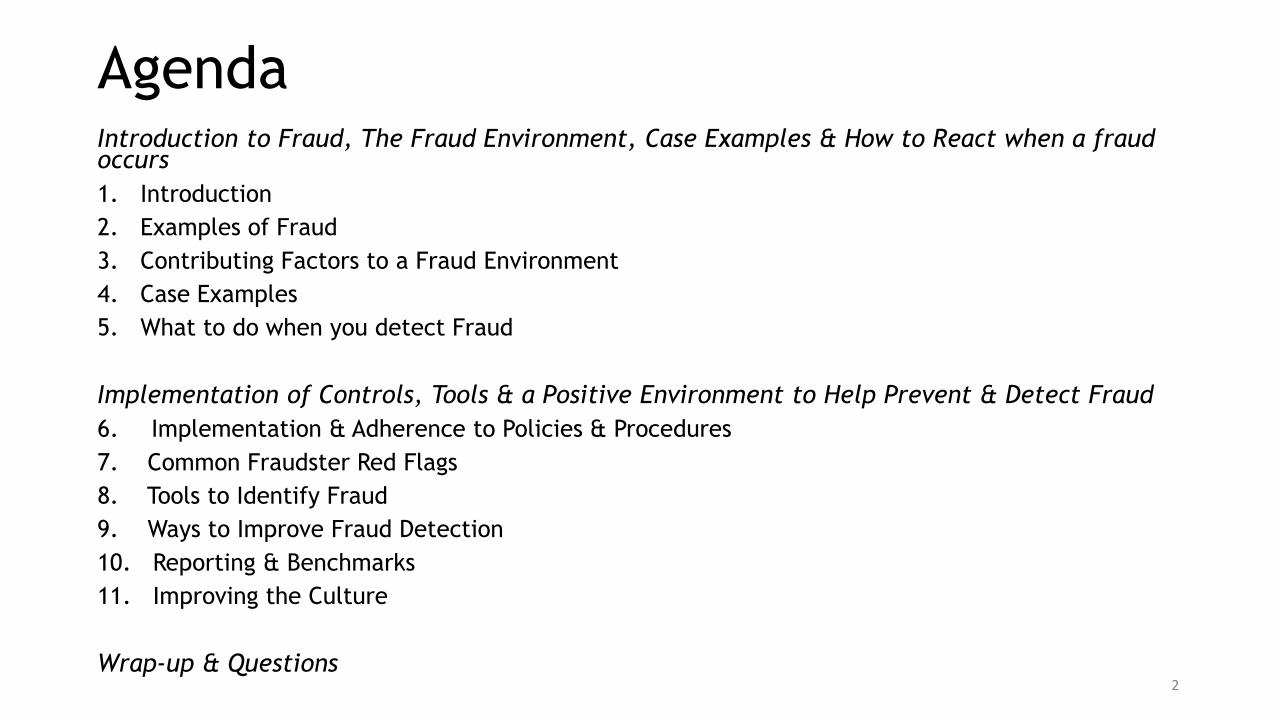

AgendaIntroduction to Fraud, The Fraud Environment, Case Examples & How to React when a fraud occurs

1. Introduction

2. Examples of Fraud

3. Contributing Factors to a Fraud Environment

4. Case Examples

5. What to do when you detect Fraud

Implementation of Controls, Tools & a Positive Environment to Help Prevent & Detect Fraud

6. Implementation & Adherence to Policies & Procedures

7. Common Fraudster Red Flags

8. Tools to Identify Fraud

9. Ways to Improve Fraud Detection

10. Reporting & Benchmarks

11. Improving the Culture

Wrap-up & Questions2

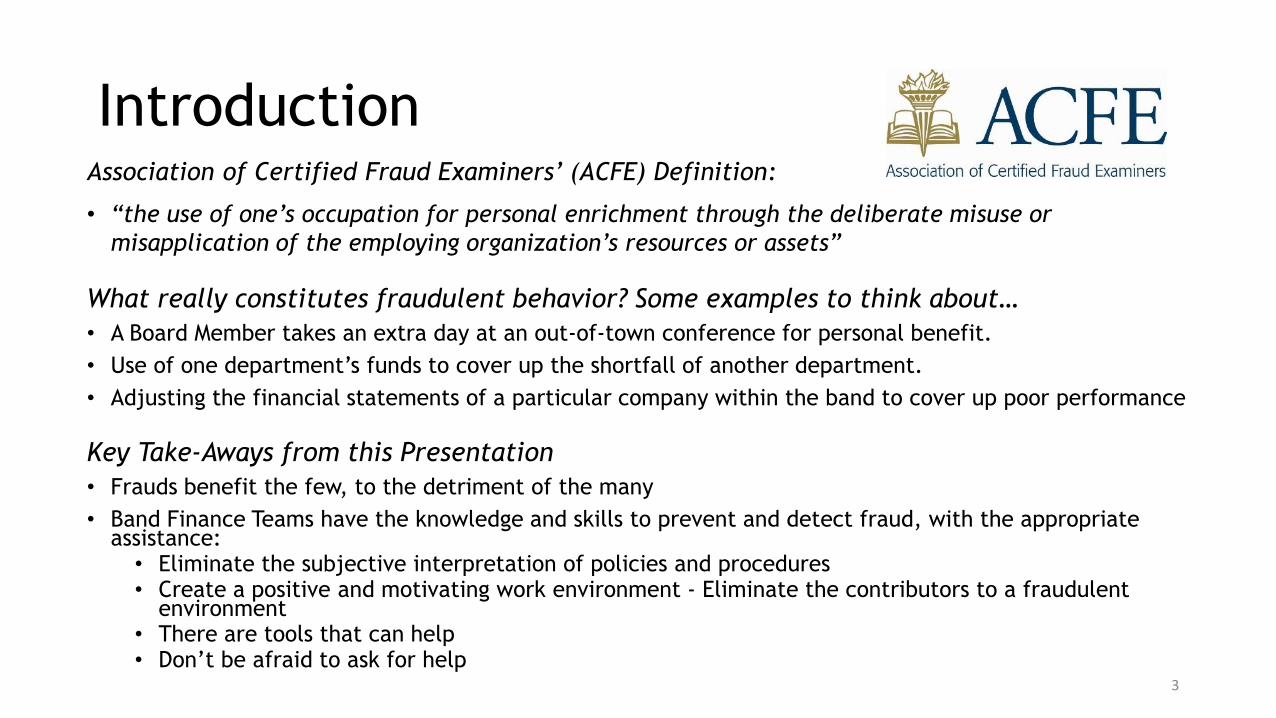

IntroductionAssociation of Certified Fraud Examiners’ (ACFE) Definition:

• “the use of one’s occupation for personal enrichment through the deliberate misuse or

misapplication of the employing organization’s resources or assets”

What really constitutes fraudulent behavior? Some examples to think about…

• A Board Member takes an extra day at an out-of-town conference for personal benefit.

• Use of one department’s funds to cover up the shortfall of another department.

• Adjusting the financial statements of a particular company within the band to cover up poor performance

Key Take-Aways from this Presentation

• Frauds benefit the few, to the detriment of the many

• Band Finance Teams have the knowledge and skills to prevent and detect fraud, with the appropriate assistance:• Eliminate the subjective interpretation of policies and procedures• Create a positive and motivating work environment - Eliminate the contributors to a fraudulent

environment• There are tools that can help• Don’t be afraid to ask for help

3

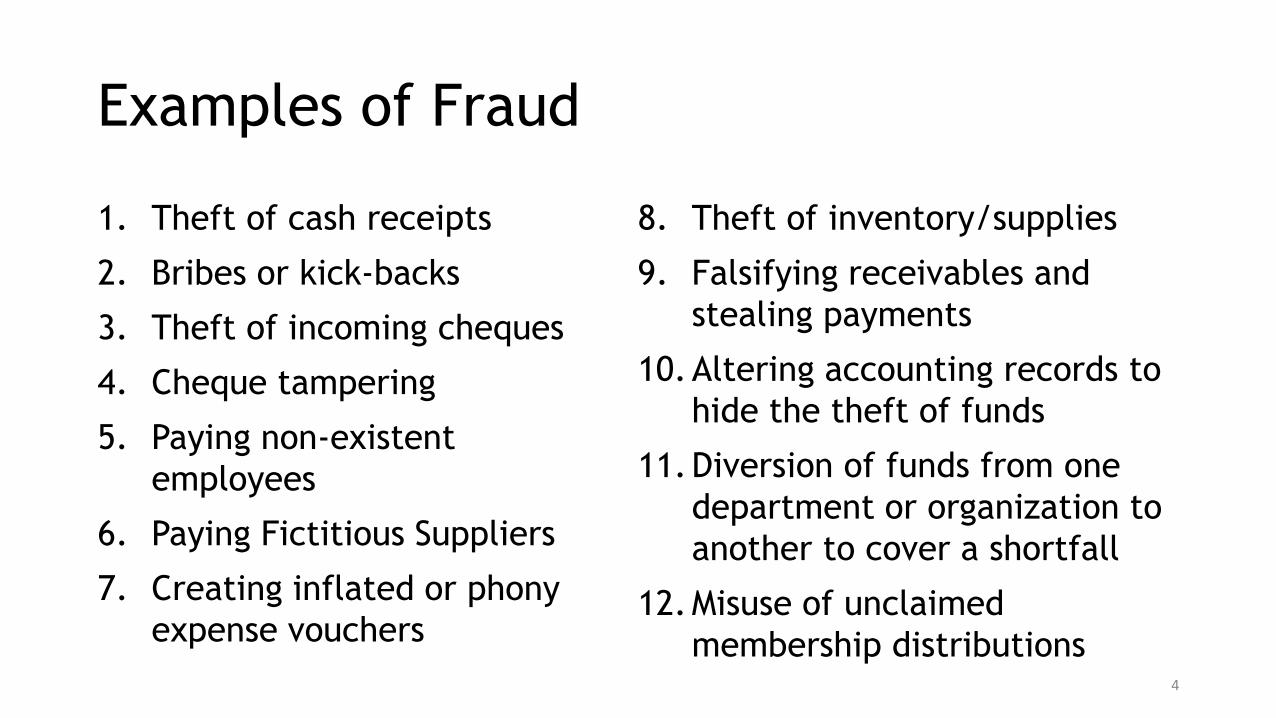

Examples of Fraud

1. Theft of cash receipts

2. Bribes or kick-backs

3. Theft of incoming cheques

4. Cheque tampering

5. Paying non-existent

employees

6. Paying Fictitious Suppliers

7. Creating inflated or phony

expense vouchers

8. Theft of inventory/supplies

9. Falsifying receivables and

stealing payments

10.Altering accounting records to

hide the theft of funds

11.Diversion of funds from one

department or organization to

another to cover a shortfall

12.Misuse of unclaimed

membership distributions4

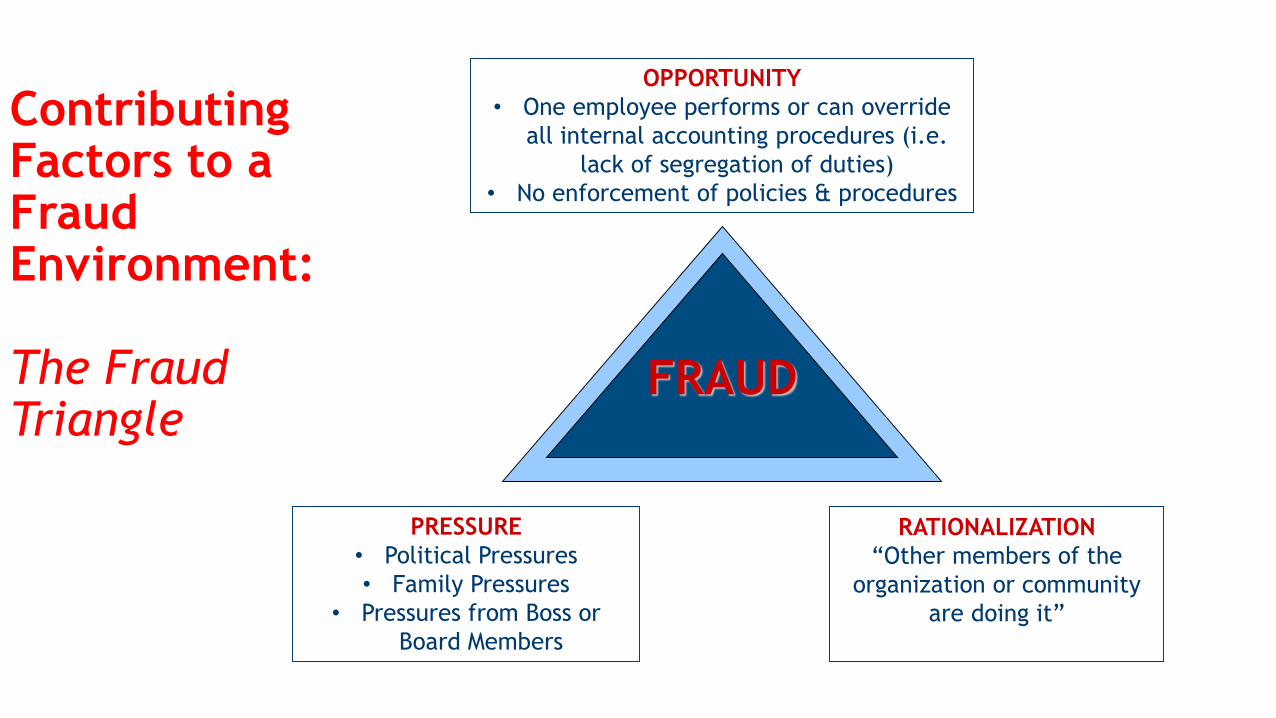

Contributing Factors to a Fraud Environment:

The Fraud Triangle

FRAUD

OPPORTUNITY

• One employee performs or can override

all internal accounting procedures (i.e.

lack of segregation of duties)

• No enforcement of policies & procedures

PRESSURE

• Political Pressures

• Family Pressures

• Pressures from Boss or

Board Members

RATIONALIZATION

“Other members of the

organization or community

are doing it”

Case Examples

6

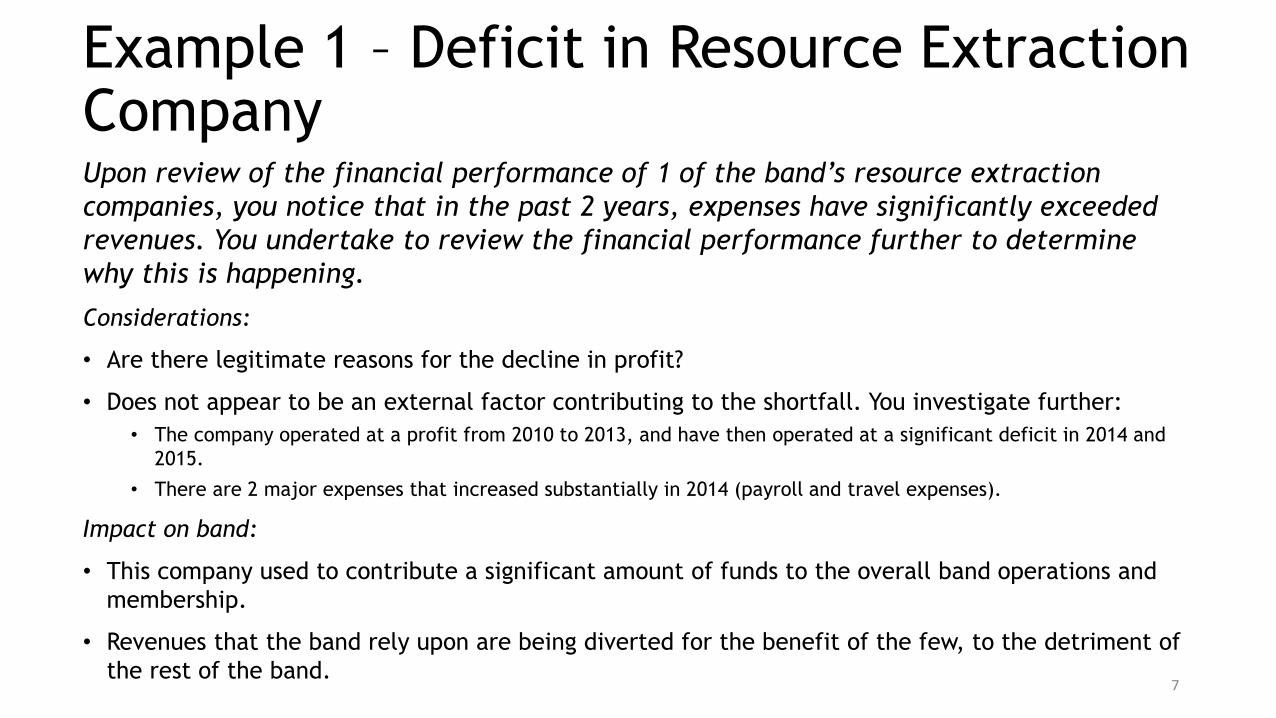

Example 1 – Deficit in Resource Extraction CompanyUpon review of the financial performance of 1 of the band’s resource extraction

companies, you notice that in the past 2 years, expenses have significantly exceeded

revenues. You undertake to review the financial performance further to determine

why this is happening.

Considerations:

• Are there legitimate reasons for the decline in profit?

• Does not appear to be an external factor contributing to the shortfall. You investigate further:

• The company operated at a profit from 2010 to 2013, and have then operated at a significant deficit in 2014 and

2015.

• There are 2 major expenses that increased substantially in 2014 (payroll and travel expenses).

Impact on band:

• This company used to contribute a significant amount of funds to the overall band operations and

membership.

• Revenues that the band rely upon are being diverted for the benefit of the few, to the detriment of

the rest of the band.7

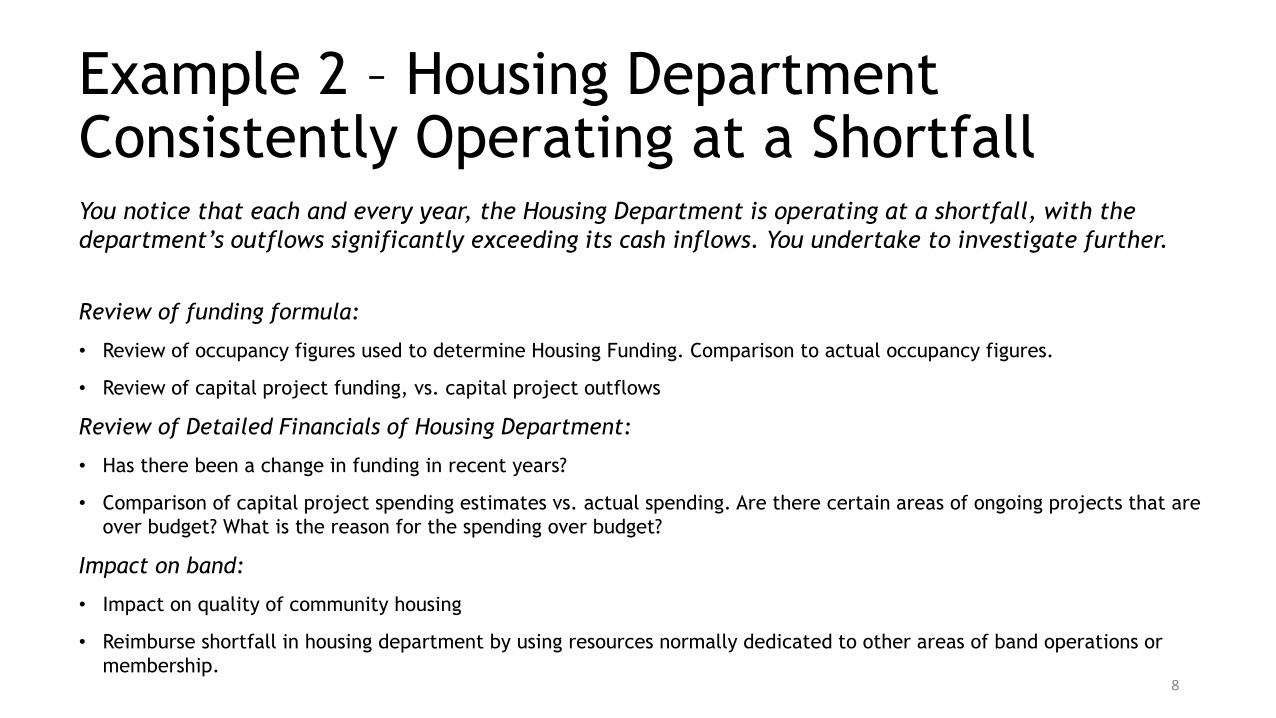

Example 2 – Housing Department Consistently Operating at a ShortfallYou notice that each and every year, the Housing Department is operating at a shortfall, with the

department’s outflows significantly exceeding its cash inflows. You undertake to investigate further.

Review of funding formula:

• Review of occupancy figures used to determine Housing Funding. Comparison to actual occupancy figures.

• Review of capital project funding, vs. capital project outflows

Review of Detailed Financials of Housing Department:

• Has there been a change in funding in recent years?

• Comparison of capital project spending estimates vs. actual spending. Are there certain areas of ongoing projects that are

over budget? What is the reason for the spending over budget?

Impact on band:

• Impact on quality of community housing

• Reimburse shortfall in housing department by using resources normally dedicated to other areas of band operations or

membership.8

Example 3 – Inappropriate Controls over Membership Distribution PaymentsBased on your review of the Membership Distribution Account, you notice that there are

multiple cheques being written to the same band members for the same membership

distribution. You undertake to investigate further.

Multiple payments being made to the same members of the community

• Source of funds – stale dated cheques due to inappropriate tracking of membership (members no longer in

community)

Inappropriate controls in distribution account

• No tracking of stale dated cheques

• No segregation of duties – same individual performing the account reconciliation is cutting cheques

• Membership department not keeping up appropriately with membership figures

Impact on Band

• Band funding being used to benefit small number of individuals, instead of the greater community

9

What to do when you detect fraud?

Some Important Considerations:

• What area of the organization is impacted? How long has it been going on for?

• Who is perpetrating the fraud? Is there collusion?

• What steps can be undertaken to stop the fraud from continuing?

• Involve band legal counsel, when possible

• Consider suspending employee, pending an investigation

• What message, if any, needs to be communicated to the rest of the organization/community/overall band membership?

Potential avenues for recovery:• Normally limited funds available for recovery from the perpetrator

• Misappropriation of funds normally leads to the band having to fund the shortfall from other areas of the band

operations/membership.

• Does the band have an Insurance Policy to assist in the recovery of misappropriated funds?

Establish greater internal controls and fraud deterrence tools to prevent the same

occurrence in the future.

10

Implementation of Controls, Tools & a Positive Environment to Help Prevent & Detect Fraud

• Implementation & Adherence to Policies & Procedures

• Tools to Detect Fraud

• Encouraging & Nurturing Strong & Positive Organizational

Culture

• Reporting, Metrics & Benchmarks for Improved Behaviour &

Engagement

11

Policy and Procedures

• Examine existing corporate culture

& identify any recent breaches

• Create clear, concise and

straightforward Code of Conduct &

Whistleblower Policy

• Non-Retaliatory language is a must

12

Policy & Procedures

• Walk the Walk and Speak the Speak

all the way to the middle

• Identify the risks and draft policy

to ensure support of the risks

• Set clear expectations and

outcomes & train, train, train

13

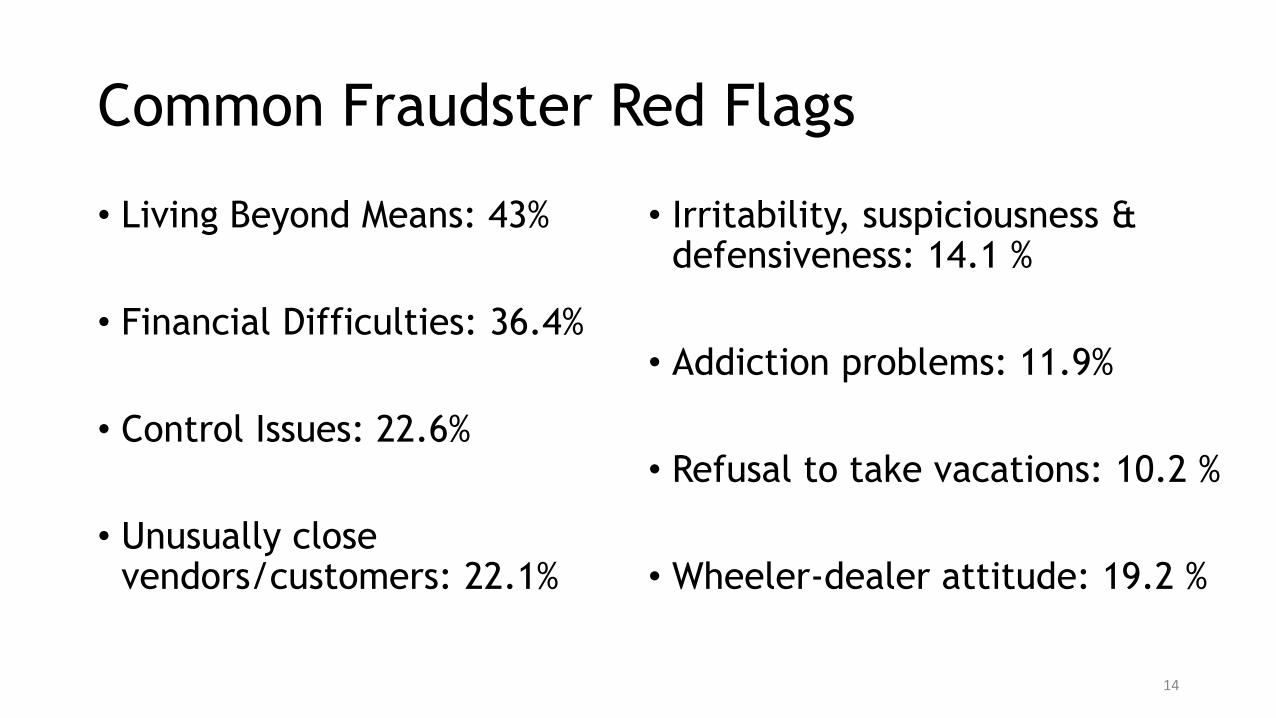

Common Fraudster Red Flags

• Living Beyond Means: 43%

• Financial Difficulties: 36.4%

• Control Issues: 22.6%

• Unusually close vendors/customers: 22.1%

• Irritability, suspiciousness & defensiveness: 14.1 %

• Addiction problems: 11.9%

• Refusal to take vacations: 10.2 %

• Wheeler-dealer attitude: 19.2 %

14

Tools to Identify Fraud

• Hotlines are the best method to detect fraud

• Better you are at collecting and responding to tips, the better you are at detecting and limiting losses

• Ethics Training (red flag training)

• Management leads by example and sets “Tone at the Top”

• Educate members about fraud, how to detect it, how to prevent it, how to report it

15

10 Ways To Improve Fraud Detection1. Use a Hotline

WhistleBlower tips are the most common fraud detection technique

2. Multiple Report Mechanisms

Whether by phone, email, web portal, mail or fax, all stakeholders can report on fraud

3. Outsourced Hotline

Third-party anonymous hotlines ensure employees feel safe and secure when reporting

4. Training Employees

Train on what fraud looks like, what to look our for and how to report it

5. Train Again

Most of us need a little repetition. It’s okay. Keep the training going all the time and use

real-life scenarios to put it in context for your employees 16

Improving Fraud Detection6. Fraud Triangle

Look for behavioral traits, red flags

7. Reduce Opportunity

Segregate sensitive duties amongst more than one employee

8. Protect Assets

From petty cash to company issued credit cards, reconcile everything

9. Spot Audit

Implement spot audit programs and conduct random audits on particular sensitive areas

10. Policies

Get your policies in place, make them available, and ensure all employees from the top down, obey them. 17

Reporting and Benchmarks

• Establish benchmarks before launching your ethics program

• Measure employee engagement and satisfaction

• Identify an Ethics Champion Advocate

• Use sanitized case studies to share with staff

• Reward and acknowledge improved behavior

• Re-measure employee engagement

18

Fraud Prevention – Improving The Culture

• Create a structure that discourages and eliminates fraud

• Craft policies and procedures that prevent fraud

• Management leads by example and sets “Tone at the Top”

• Educate employees about fraud, how to detect it, how to prevent it, how to report it

• Live the Speak Up Way!19