Depository Receipts Information Guide_Citigroup

58

Depositary Receipts Information Guide CitigroupGloba l Transaction Services

-

Upload

yasheshthakkar -

Category

Documents

-

view

221 -

download

0

Transcript of Depository Receipts Information Guide_Citigroup

8/8/2019 Depository Receipts Information Guide_Citigroup

http://slidepdf.com/reader/full/depository-receipts-information-guidecitigroup 1/58

Depositary ReceiptsInformation Guide

CitigroupGlobal Transaction Servic

8/8/2019 Depository Receipts Information Guide_Citigroup

http://slidepdf.com/reader/full/depository-receipts-information-guidecitigroup 2/58

Depositary Receipts Information Guide

Depositary Receipts (DRs) were created in 1927 to aid U.S. investors wishing to purchaseshares of Non-U.S. corporations. Since that time, DRs have grown into a widely accepted,

flexible instrument that enables issuers worldwide to access investors outside their homemarkets. The purpose of this Information Guide is to provide a clear overview of how theDR market works, helping issuers, investors and other market participants make informeddecisions related to cross border investing.

The information set forth herein is for information purposes only and does not constitute a recommendation, solicitation or offer by Citibank, N.A.,for the purchase or sale of any securities, nor shall this material be construed in any way as investment or legal advice or a recommendation, reference orendorsement by Citibank, N.A.

©2005 Citigroup Inc. All rights reserved. CITIGROUP and the Umbrella Device are trademarks and service marks of Citicorp or its affiliates and areused and registered throughout the world.

8/8/2019 Depository Receipts Information Guide_Citigroup

http://slidepdf.com/reader/full/depository-receipts-information-guidecitigroup 3/58

ContentsI. Introduction 2

II. Roles and Relationships in a DR Program 4

lll. Program Alternatives 8

lV. DR Enhancements 22

V. Issuance and Cancellation 24

Vl. Securities Regulations and Requirements 28

Vll. U.S. Listing Requirements 36

Vlll. DR Proxy Services 40

lX. Investor Relations 44

X. DR Terminology 48

Xl. Further Resources 54

8/8/2019 Depository Receipts Information Guide_Citigroup

http://slidepdf.com/reader/full/depository-receipts-information-guidecitigroup 4/58

l. IntroductionDepositary Receipts (DRs) were created in 1927 to aid U.S. investors who wished to purchase shares of Non-U.S.corporations. Since that time, DRs have grown into a widely accepted, flexible instrument that enables issuers worldwideto access investors outside their home markets.

The purpose of this Information Guide is to provide a clear overview of how the DR market works, helping issuers,investors and other market participants make informed decisions related to cross border investing.

A DR is a negotiable instrument issued by a U.S. depositary bank evidencing ownership of shares in a Non-U.S.corporation. Each DR denotes Depositary Shares (DSs) representing a specific number of underlying shares ondeposit with a custodian in the issuer’s home market. The term “DR” is commonly used to mean both the physicalcertificate and the security itself.

DRs are generally quoted and traded in $US and are subject to the trading and settlement procedures of the marketin which they trade. The ease of trading and settling DRs makes them an attractive investment option for investorswishing to purchase securities issued by companies outside the investor’s home market.

DRs are frequently identified by the markets in which they are available or the rules and regulations associated withthe structure.

>> American Depositary Receipts (ADRs) are DRs that are publicly available to investors in the U.S.>> Global Depositary Receipts (GDRs) are DRs that are offered to investors in two or more markets

outside the issuer’s home country, usually pursuant to Rule 144A and Regulation S under the SecuritiesAct of 1933.

DRs can be publicly offered, privately placed or issued pursuant to a global offering. The method of sale defines thesegment of investors that can purchase the securities. In the U.S., publicly offered securities are available to the broadestspectrum of investors and trade either on a national stock exchange or trading system (such as NYSE, Nasdaq or Amex)or in the Over-the-Counter (OTC) market. Privately placed securities are typically sold to Qualified Institutional Buyers(QIBs), including institutions that own and invest atleast $100 million in securities of non-affiliatesand registered broker-dealers that own or investon a discretionary basis at least $10 million insecurities of non-affiliates. A global offering usuallyhas a Rule 144A component as well as a placement

to non-U.S. investors pursuant to Regulation S.

2 >> Citigroup Depositary Receipt Services

ADRs listed on U.S. exchanges provide investors with the same level of information as any other U.S. security.

8/8/2019 Depository Receipts Information Guide_Citigroup

http://slidepdf.com/reader/full/depository-receipts-information-guidecitigroup 5/58

Information Guide << 3

Benefits of a DR Program

For Issuers

DRs enable issuers to>> Access capital outside the issuer’s home market

>> Build company visibility in the U.S. and internationally>> Broaden and diversify shareholder base

>> Expand opportunity to increase local share price as a resultof global demand/trading>> Enlarge the market for the company’s shares, potentially

increasing liquidity>> Adjust share price levels to those of peers through DR Ratio

>> Facilitate merger and aquisition activity through use asacquisition currency

>> Develop stock option plans and stock purchase plans forU.S. employees

For Investors

DRs aid investors by

>> Facilitating diversification into Non-U.S. securities>> Trading, clearing and settling in accordance with practices

of the investor’s home market

>> Eliminating cross border custody safekeeping charges>> Providing enhanced accessibility of research, and of price

and trading information

>> Allowing easy comparison to securities of similar companiestrading in the investor’s home market

>> Permitting dividend payments in $US and corporate actionnotifications in English

>> Allowing for lower dividend tax rates for exchange-listed ADRs,and for DRs where there exists a treaty between the U.S.and the issuer’s local market (applicable under the Jobs and

Growth Tax Relief Reconciliation Act of 2003)

DRs also may play a critical role in differenttypes of cross border transactions such asprivatizations and mergers and acquisitions.

PrivatizationsThe privatization of state-owned assets isan important undertaking for governmentsworldwide as they seek to restructuretheir economies and reduce fiscal deficits.Infrastructure and service enterprises suchas telecommunications, utilities, airlines

and petrochemicals are among those initiallytargeted for privatization.

DRs have been used successfully by governmentsseeking to privatize state-owned enterprises.Privatizations require a successful offering ofsecurities to investors, and DRs provide aneffective mechanism both to increase privateownership and to raise capital overseas.

Mergers and AcquisitionsDepositary Receipts can enhance the ease oftrading and settlement related to cross borderMergers and Acquisitions (M&A transactions),and they also can facilitate the execution ofcorporate actions such as payment of dividends,structuring of rights offerings and solicitationof votes. DRs enable issuers to address investordemands without the need to build an inde-pendent U.S. shareholder support infrastructureor to modify the equity issuance and tradingpatterns of the home market. Types of M&A

transactions that have made successful use ofDRs include spin-offs of Non-U.S. subsidiaries,equity-based acquisitions of U.S. businessentities and equity-based acquisitions of Non-U.S.business entities.

8/8/2019 Depository Receipts Information Guide_Citigroup

http://slidepdf.com/reader/full/depository-receipts-information-guidecitigroup 6/58

II. Roles and Relationships in a DR ProgramIn order to establish a DR program, the issuer develops a team of advisors that typically includes investment bankers,lawyers and accountants. The issuer also selects a depositary bank, a key partner that enlists the services of a custodianto handle the implementation of the program. The issuer and the depositary execute a Deposit Agreement that setsforth the terms of the DR program. Based upon this contract the depositary performs certain specified serviceson behalf of the issuer and the DR holders. Many of these same parties play key roles in the long-term developmentand day-to-day management of the issuer’s DR program. The depositary bank remains a critical liaison between theissuer and brokers and custodians, while the functions of lawyers and accountants becomes focused on periodicreporting. Generally, investment bankers are not involved with the ongoing management of a DR program unless theissuer is going back to the market.

The following pages show overviews of roles and responsibilities in establishment and ongoing management of aDR program.

4 >> Citigroup Depositary Receipt Services

8/8/2019 Depository Receipts Information Guide_Citigroup

http://slidepdf.com/reader/full/depository-receipts-information-guidecitigroup 7/58

Information Guide << 5

Brokers>> Submit required forms to become

a market maker in a security(for Level l programs), as needed

>> Make securities available to investors

Depositary>> Advise on DR facility structure>> Appoint custodian>> Assist with DR registration requirements

>> Coordinate with lawyers and investmentbankers to ensure that all implementationsteps are completed

>> Prepare and issue DRs>> Enlist market makers, if applicable>> Announce program establishment

to brokers and traders

Custodian>> Receive underlying shares>> Confirm deposit of underlying shares

Issuer>> Determine financial objectives>> Appoint depositary, lawyers, investment

bank and accountants>> Determine program type>> Obtain approval from board of

directors, shareholders and regulators,as needed

>> Provide financial information toaccountants

>> Develop investor relations plan

Investment Bankers>> Lead underwriting process>> Establish syndicate of participating banks>> Advise on capital structure>> Advise on type of DR structure>> Conduct due diligence>> Draft prospectus>> Obtain CUSIP number>> Obtain DTC, Euroclear and

Clearstream eligibility, as needed

>> Coordinate road show>> Organize book-building and line up

market makers>> Price and launch securities

Lawyers>> Advise on facility structure>> Negotiate Deposit Agreement>> Prepare appropriate registration

statements or establish exemptionswith SEC, as applicable

>> Prepare listing agreements to liston U.S. exchanges (Level II and Level III

DR facilities)>> Draft offering circular/prospectus

Accountants>> Prepare financial statements in

accordance with (or reconciled to)U.S. Generally Accepted AccountingPrinciples (U.S. GAAP) for SecuritiesAct registered securities (Level II andLevel III DR facilities)

Brokers

Depositary

Custodian

InvestmentBankers

Lawyers

Accountants

Issuer

Key Roles in Establishment of a DR Program

8/8/2019 Depository Receipts Information Guide_Citigroup

http://slidepdf.com/reader/full/depository-receipts-information-guidecitigroup 8/58

6 >> Citigroup Depositary Receipt Services

Brokers>> Make securities available to investors>> Execute and settle trades via

the depositary

Depositary>> Assists with DR registration

requirements>> Issues DRs>> Provides ongoing account management

support to the issuer>> Processes corporate actions and

dividend payments>> Offers value-added services such as

IR counsel.

Custodian>> Receives underlying shares.>> Confirms deposit of underlying shares>> Holds shares in custody for the account

of depositary in the home market>> Disseminates corporate action and

proxy information to depositary

Issuer>> Communicates with depositary

about DR program and potentialprogram changes

Investment Bankers>> Generally not involved in ongoing

management of DR program unless theissuer is going back to the market

Lawyers>> Prepare appropriate registration

statements or establish exemptionswith the SEC, as applicable

Accountants>> Support the issuer in terms of

periodic reporting

Brokers

Depositary

Custodian

InvestmentBankers

Lawyers

Accountants

Issuer

Key Roles in Ongoing Development of a DR Program

8/8/2019 Depository Receipts Information Guide_Citigroup

http://slidepdf.com/reader/full/depository-receipts-information-guidecitigroup 9/58

Information Guide << 7

The Role of the Investor Relations Firm

An additional influencer in both the establishment and ongoing management of a DR program may be an investorrelations (IR) firm, a resource well versed in IR best practices in the market where securities are being offered.Specific IR functions may include:

>> Developing a strategic IR plan>> Coordinating ownership analysis and investor targeting>> Refining messages to the investment community>> Providing road show and presentation advice

The issuer should make a proactive decision as to whether IR needs are best met by an internal IR professional, anexternal IR firm with specific expertise in the market(s) where securities are being offered, or a combination of both.

The Depository Trust & Clearing Corporation and Depositary ReceiptsThe Depository Trust & Clearing Corporation (DTCC), through its subsidiaries, provides clearance, settlement andinformation services for equities, corporate and municipal bonds, government and mortgage-backed securities andOver-the-Counter credit derivatives. DTCC’s depository (DTC) also provides custody and asset servicing for morethan two million securities issues from the United States and 100 other countries and territories.

DTC was created in 1973 in response to Wall Street’s “paperwork crisis” to maintain (or immobilize) physical certifi-cates in a central location, record changes of ownership using “book-entry accounting” (where no certificates changehands), and facilitate settlement electronically. Another step toward eliminating paper in securities processing wastaken in 1982, when DTC distributed the first paperless Book Entry Only (BEO) issues. BEO, which began as a wayto deal with the high volume of municipal bond issues, has since been expanded to address other issues, includingDepositary Receipts.

Instead of issuing certificates evidencing ownership to investors, BEO ownership is, from an investor’s perspective,represented by credits to the investor’s account with the investor’s bank or broker. With BEO, the issuer’s securitiesissued in certificate form are safekept by DTC or are, such as in the case of many DR programs, represented by amaster certificate for all outstanding securities held in DTC.

Ownership positions and transactions in each security—including purchases, sales, and interest or principal payments—are reflected initially in DTC’s records and thereafter in the records of thousands of participating banks and brokersin the U.S. The physical securities that are underlying these positions are deposited for safekeeping at DTC (or at acustodian designated by DTC) by participants, and are registered in DTC’s nominee name, Cede & Co. Participantownership is reflected on the electronic records of DTC under an individual participant account number.

DTC plays a crucial role in the DR securities environment, working closely with depositaries to:>> Facilitate the issuance and cancellation of DRs and transfer and delivery of DRs to the broker

>> Expedite the distribution of dividends to investors on the payable date>> Manage the handling of corporate actions that many issuers undertake>> Provide for custody, safekeeping and settlement to ensure the safety and soundness of DR transactions

Information provided courtesy of DTCC

8/8/2019 Depository Receipts Information Guide_Citigroup

http://slidepdf.com/reader/full/depository-receipts-information-guidecitigroup 10/58

lll. Program AlternativesMost issuers use Depositary Receipts to reach investors in the U.S., the largest and most liquid securities market inthe world. Issuers may select the type of DR program best suited to meet their objectives. Issuer priorities may includeexpanding its shareholder base, gaining increased recognition of the company name and its products and/or servicesin the global markets, and using DRs as a vehicle for raising capital.

Issuers can use DRs to access large institutional investors that may be prohibited or limited by their charter or byregulation from investing in Non-U.S. securities purchased in the issuer’s home market. U.S. investors may prefer

to purchase DRs rather than shares in the issuer’s home market because the DRs trade, clear and settle accordingto U.S. market conventions.

Setting the RatioA primary step in establishing a DR program is determining the ratio of underlying shares to Depositary Shares (DSs),the securities represented by a DR. DSs are established as a multiple or fraction of the underlying shares and the ratiocan influence the price trading range. In setting the ratio, the issuer should consider:

>> Industry peers: To the extent that securities of companies in the issuer’s industry generally trade in a certainprice range, the issuer may want to conform to industry norms in the market where the DR will be listed;

>> Exchange options: Each exchange has average price ranges for the shares listed and, generally speaking,issuers may want to conform to that range;

>> Investor appeal: U.S. institutional and retail investors are more likely to buy shares which they perceive aswell priced and valued fairly.

While many DR programs are established with a 1:1 ratio (one underlying share equals one DS), current DR programs haveratios ranging from 100,000:1 to 1:100. The depositary will work with issuers to determine the most appropriate ratio atthe inception of the DR program. The ratio can be adjusted at a future date to address changes in market conditions.

Types of Depositary Receipt ProgramsIn the U.S., DRs can be:

>> Traded Over-the-Counter (OTC) through the OTC Bulletin Board and/or the Pink Sheets (Level l)>> Listed on a U.S. exchange: the New York Stock Exchange (NYSE) or the American Stock Exchange (Amex),

or quoted on the Nasdaq Stock Market (Nasdaq) (Level ll)>> Issued as a public offering of securities on a U.S. exchange (Level lll)>> Privately placed with QIBs in the Rule 144A market (RADR)

In Non-U.S. markets, DRs can be:>> Privately placed outside the U.S. with Non-U.S. persons. (Reg S) Note that Reg S programs are often

offered in global markets along with 144A programs in the U.S. market.>> Issued to raise capital via a global offering. (GDRs, RADR and Reg S offerings)

8 >> Citigroup Depositary Receipt Services

8/8/2019 Depository Receipts Information Guide_Citigroup

http://slidepdf.com/reader/full/depository-receipts-information-guidecitigroup 11/58

Over-the-Counter Exchange TradedLevel l Level ll

Description Unlisted program in the U.S. Listed program on a recognized

U.S. exchange

Trading Quoted in the Pink Sheets NYSE, Amex or Nasdaq

and/or on the OTC Bulletin Board

Program Alternatives Guide

Information Guide << 9

Public Offering Private Placement-U.S. Private Placement- GlobalLevel lll Rule 144A ADR (RADR) Global Depositary Receipt (GDR)

Description Offered and listed Private placement in the Global private placement in

on a recognized U.S. U.S. to Qualified Institutional two or more markets outside the

exchange Buyers (QIBs) issuer’s home market

May include RADR and/or

Reg S* offering

Trading NYSE, Amex or Nasdaq Quoted on PORTAL in the U.S. London Stock Exchange,

Luxembourg Stock Exchange for

non-U.S. component, and/or

PORTAL if there is a U.S. tranche

Broaden Shareholder Base with Existing Shares

*Note that Reg S programs are often offered in global markets along with 144A programs in the U.S. market

Raise Capital with New Shares

8/8/2019 Depository Receipts Information Guide_Citigroup

http://slidepdf.com/reader/full/depository-receipts-information-guidecitigroup 12/58

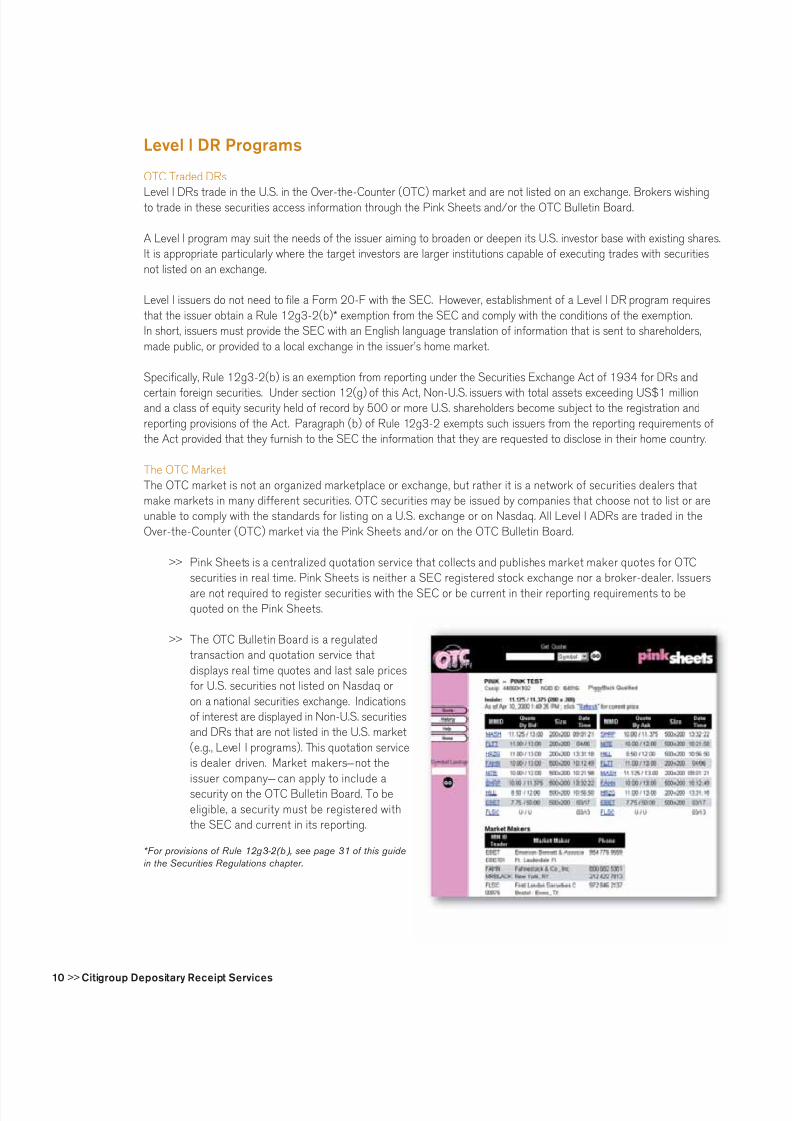

Level l DR Programs

OTC Traded DRs

Level l DRs trade in the U.S. in the Over-the-Counter (OTC) market and are not listed on an exchange. Brokers wishingto trade in these securities access information through the Pink Sheets and/or the OTC Bulletin Board.

A Level l program may suit the needs of the issuer aiming to broaden or deepen its U.S. investor base with existing shares.It is appropriate particularly where the target investors are larger institutions capable of executing trades with securitiesnot listed on an exchange.

Level l issuers do not need to file a Form 20-F with the SEC. However, establishment of a Level l DR program requiresthat the issuer obtain a Rule 12g3-2(b)* exemption from the SEC and comply with the conditions of the exemption.In short, issuers must provide the SEC with an English language translation of information that is sent to shareholders,made public, or provided to a local exchange in the issuer’s home market.

Specifically, Rule 12g3-2(b) is an exemption from reporting under the Securities Exchange Act of 1934 for DRs and

certain foreign securities. Under section 12(g) of this Act, Non-U.S. issuers with total assets exceeding US$1 millionand a class of equity security held of record by 500 or more U.S. shareholders become subject to the registration andreporting provisions of the Act. Paragraph (b) of Rule 12g3-2 exempts such issuers from the reporting requirements ofthe Act provided that they furnish to the SEC the information that they are requested to disclose in their home country.

The OTC MarketThe OTC market is not an organized marketplace or exchange, but rather it is a network of securities dealers thatmake markets in many different securities. OTC securities may be issued by companies that choose not to list or areunable to comply with the standards for listing on a U.S. exchange or on Nasdaq. All Level I ADRs are traded in theOver-the-Counter (OTC) market via the Pink Sheets and/or on the OTC Bulletin Board.

>> Pink Sheets is a centralized quotation service that collects and publishes market maker quotes for OTCsecurities in real time. Pink Sheets is neither a SEC registered stock exchange nor a broker-dealer. Issuers

are not required to register securities with the SEC or be current in their reporting requirements to bequoted on the Pink Sheets.

>> The OTC Bulletin Board is a regulatedtransaction and quotation service thatdisplays real time quotes and last sale pricesfor U.S. securities not listed on Nasdaq oron a national securities exchange. Indicationsof interest are displayed in Non-U.S. securitiesand DRs that are not listed in the U.S. market(e.g., Level I programs). This quotation serviceis dealer driven. Market makers–not theissuer company– can apply to include asecurity on the OTC Bulletin Board. To beeligible, a security must be registered withthe SEC and current in its reporting.

*For provisions of Rule 12g3-2(b), see page 31 of this guidein the Securities Regulations chapter.

10 >> Citigroup Depositary Receipt Services

8/8/2019 Depository Receipts Information Guide_Citigroup

http://slidepdf.com/reader/full/depository-receipts-information-guidecitigroup 13/58

Activity Week* Key Parties Involved

Establish Program Launch Team

Begin planning for ongoing investor relations program

Submit Form 12g3-2(b) exemption request to SEC for approval

Negotiate Deposit Agreement and prepare Form F-6 registration

statement

Submit Deposit Agreement and Form F-6 to SEC

Amend as necessary and receive SEC approval

Complete all requirements for trading and settlement (prepare

certificates, request CUSIP number, obtain DTC eligibility)

Distribute announcement to brokers and investors via e-mail and fax

Depositary solicits market makers

Trading Begins

*The time frames provided for establishing new programs are indicative only. Establishment can take as littleas nine weeks but time frames may vary due to regulators’ involvement and individual program specifics.

Steps to Establish an Over-the-Counter Traded DR Program(Level l)

1 2 3 4 5 6 7 8 9 I s s u e

r

D e p o

s i t a r y

L e g a l C o u n s e l

B r o k e r s

I R F i r

m

Information Guide << 11

8/8/2019 Depository Receipts Information Guide_Citigroup

http://slidepdf.com/reader/full/depository-receipts-information-guidecitigroup 14/58

12 >> Citigroup Depositary Receipt Services

Level ll DR Programs

Exchange-Listed DRsListing on one of the U.S. national exchanges such as the New York Stock Exchange (NYSE), the American StockExchange (Amex), or the National Association of Securities Dealers Automated Quotation System (Nasdaq) canpromote more active trading in DRs than a Level l and increase the issuer’s visibility within the U.S. Level ll, exchange-listed DRs are more widely covered by the U.S. financial media and analysts, providing investors with increasedinformation about the issuer and its securities.

To list its DRs, the issuer must comply with the individual exchange’s requirements, and issuers must register under the

Securities Act of 1933 and report under the Securities Exchange Act of 1934 by filing the initial registration statementand periodic reports. Non-U.S. issuers that are listing their securities must reconcile all financial statements to U.S.Generally Accepted Accounting Principles (U.S. GAAP). Financial reporting for individual business segments need not bereconciled to U.S. GAAP. Listing securities exempts Non-U.S. issuers from complying with various state securities regulations.

Exchange-Listing ConsiderationsBoth the NYSE and Amex are auction-based markets with specialists who are responsible for maintaining a fair andorderly market in the securities they manage. Exchange specialists facilitate trading in a particular DR program by providingan informed point of contact on the trading floor and maintaining a market in a particular security. Other members of theexchange go to the specialist to transact or leave an order. The resulting concentration of orders allows investors to tradedirectly with other investors. The issuer appoints its own specialist at both the NYSE and the Amex.

The Nasdaq Stock Market is an electronic market that collects and disseminates quotations from competing dealers.The Nasdaq Stock Market offers real-time trade reporting and is organized around a system of multiple market makerslinked by computers. Vendor terminals (including Reuters and Bloomberg) carry comprehensive quote and last saleinformation to traders, fund managers and brokers worldwide. Traders in the U.S. enter bid and offer prices via computerusing the Nasdaq network. Non-U.S. traders retrieve Nasdaq data from vendor terminals and execute orders throughNational Association of Securities Dealers (NASD) -member firms. All issuers must have at least two market makersquoting its stock.

8/8/2019 Depository Receipts Information Guide_Citigroup

http://slidepdf.com/reader/full/depository-receipts-information-guidecitigroup 15/58

Activity Week* Key Parties Involved

Establish Program Launch Team

Begin planning for ongoing investor relations program

Prepare and submit Form 20-F for SEC approval

Submit Exchange Listing Application and Agreement

and receive approval from exchange

Negotiate and submit Deposit Agreement and Form F-6

registration statement

Complete all requirements for trading and settlement

(prepare certificates, request CUSIP number, obtain DTC eligibility)

Receive SEC comments on Deposit Agreement and

amend as needed

Receive SEC approval

Distribute announcement to brokers and investors via e-mail and fax

Trading Begins

*The time frames provided for establishing new programs are indicative only. Establishment can take as littleas fifteen weeks but time frames may vary due to regulators’ involvement and individual program specifics.

Information Guide << 13

Steps to Establish an Exchange Traded DR Program(Level ll)

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 I s s u e

r

D e p o

s i t a r y

L e g a l C o u n s e l

A c c o

u n t a n t s

I R F i r m

B r o k e r s

8/8/2019 Depository Receipts Information Guide_Citigroup

http://slidepdf.com/reader/full/depository-receipts-information-guidecitigroup 16/58

14 >> Citigroup Depositary Receipt Services

Level lll DR Programs

U.S. Public Offering of DRsIn a Level lll program, the issuer offers new shares to U.S. investors in DR form. A public offering provides the issuerwith the ability to raise capital by accessing the broadest US investor base. In order to conduct an initial public offeringin the U.S., the issuer must: 1) submit Form F-1 to the SEC to register the underlying securities to be offered; 2) fullyreconcile its financial statements to U.S. GAAP (or include U.S. GAAP financials); and 3) with the depositary, submit formF-6 to the SEC to register the DRs. In establishing a Level lll DR program, the issuer also selects an investment bank toadvise on and underwrite the offering and to market the DRs to U.S. investors. After the offering has been completed,the program is maintained as a listed facility and generally can accept ongoing deposits from investors. An issuer may also

raise capital in subsequent offerings. In such a follow-on offering, the issuer will file a Form F-2 or Form F-3 with the SEC.

8/8/2019 Depository Receipts Information Guide_Citigroup

http://slidepdf.com/reader/full/depository-receipts-information-guidecitigroup 17/58

Information Guide << 15

Activity Week* Key Parties Involved

Establish Program Launch Team

Begin planning for U.S. road show and ongoing investor

relations program

Prepare and submit Prospectus, Form F-1 and Form 20-F

(or Form 8-A, a shorter version of 20-F) for SEC approval**

Submit Exchange Listing Application and Agreement

and receive approval from exchange

Negotiate and submit Deposit Agreement and Form F-6

registration statement

Complete all requirements for trading and settlement

(prepare certificates, request CUSIP number, obtain

DTC eligibility)

Receive SEC comments on Prospectus and Deposit

Agreement and amend documents accordingly

Receive SEC approval

Sign Deposit Agreement and print final Prospectus

Closing Day

Underwriter delivers cash proceeds to issuer

Depositary’s custodian receives underlying shares

Depositary delivers ADRs to underwriter

Distribute announcements to brokers and investors

via e-mail and fax

Trading Begins

*The time frames provided for establishing new programs are indicative only. Establishment can take as little

as fifteen weeks but time frames may vary due to regulators’ involvement and individual program specifics.

** For subsequent offerings (where all the steps may not apply), prepare and submit Form F-2 or Form F-3.

Steps to Conduct a Public Offering of DRs(Level lll)

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 I s s u e r

D e p o s i t a r y

L e g a l C o u n s e l

A c c o u n t a n t s

I n v e s t m e n t B a n k

I R F i r m

B r o k e r s

8/8/2019 Depository Receipts Information Guide_Citigroup

http://slidepdf.com/reader/full/depository-receipts-information-guidecitigroup 18/58

16 >> Citigroup Depositary Receipt Services

Private Placements and Global Offerings

Rule 144A Depositary Receipts (RADRs)Rule 144A DRs, or RADRs, are DRs that are privately placed in the U.S. RADRs are traded pursuant to Rule 144Awhich, adopted in 1990, greatly increased the liquidity of privately placed securities by allowing Qualified InstitutionalBuyers (QIBs) to resell these securities privately to other QIBs without a holding requirement or other formalities.

Generally, QIBs are institutional investors who are willing and able to do their own research. The SEC has exempted sales toQIBs from certain of the disclosure and reporting requirements designed to protect individual investors, such as prospectusdelivery and periodic financial reporting.

Rule 144A enables issuers to access more readily the U.S. institutional capital markets:>> Securities offered in the Rule 144A market do not have to be registered under the Securities Act of 1933.

Issuers of Rule 144A securities do not have to comply with the periodic reporting requirements of the SecuritiesExchange Act of 1934 but do have an obligation to make certain financial disclosures to investors. Thisobligation can be satisfied by compliance with the information exemption available pursuant to Rule 12g3-2(b)of the Securities Exchange Act of 1934.

>> The reduced registration and reporting requirements associated with Rule 144A securities enable issuers ofRADRs to raise capital in the U.S. private market at a cost comparable to that of raising capital in the Euromarkets.

>> The time required to complete a U.S. equity private placement is less than with a registered offering.>> A Rule 144A offering can be made with any class of shares that is not (i) listed on a U.S. securities exchange or

quoted on a U.S. automated interdealer quotation system, or (ii) issued by a company that is required to registeras an “investment company.”

>> Trading of RADRs is facilitated by PORTAL, the NASD’s quotation system for Rule 144A securities.

A private placement of DRs may enable Non-U.S. issuers to assess investor appetite for their securities before listing orpublicly offering their DRs to the full spectrum of investors.

A potential limitation to a Rule 144A ADR is that the issuer is prohibited from any type of promotion of the program in U.S.media, so visibility opportunities are less than those associated with listed programs.

Regulation S (Reg S) Depositary ReceiptsA Reg S Depositary Receipt Program is a private placement in global markets other than the U.S. Market. Regulation Sclarifies the conditions under which offers and sales of securities outside the U.S. are exempt from SEC registrationrequirements. Regulation S was adopted by the SEC in 1990 in conjunction with the adoption of Rule 144A. In many

ways, the structure of Reg S programs mirrors that of the 144A ADR programs. Reg S and 144A, taken together, cansignificantly enhance the liquidity of a private placement or global offering.

Global Depositary Receipts (GDRs)GDRs allow an issuer to raise capital simultaneously in two or more markets through a global offering. GDRs use a globalsettlement convention linking DTC with Euroclear and Clearstream to provide global clearing and settlement via theDTC/Euroclear/Clearstream Bridge.

8/8/2019 Depository Receipts Information Guide_Citigroup

http://slidepdf.com/reader/full/depository-receipts-information-guidecitigroup 19/58

Information Guide << 17

Global offerings allow issuers to access shareholders in capital markets outside the issuer’s home market. If the DRs areoffered in the U.S. and Europe, the clearing link between DTC, Euroclear and Clearstream eases settlement and promotesincreased liquidity through cross border trading.

GDRs can be issued in either the public or private markets in the U.S. or other countries. Most GDRs include aU.S. tranche, which can be privately placed under Rule 144A or placed in a registered offering, and an internationaltranche placed pursuant to Reg S outside the U.S., typically in the Euromarkets. GDRs placed in Europe are generallylisted on the Luxembourg or London Exchanges or quoted on SEAQ* International.

The evolution of region-specific DRs evidences the flexibility of the GDR structure, allowing issuers to select the investorbase they wish to access and broaden their investor base into new markets. An issuer could establish a GDR program that

taps only European, Asian and/or Latin American investors and does not offer shares in the US. Over time, the GDR pro-gram could be enhanced to reach additional markets and investors.

Side-by-Side FacilitiesOnce an issuer has raised capital in the U.S. private markets (using RADRs or GDRs), the same class of shares can bemade available to all investors in the U.S. through publicly traded DRs. To “upgrade” its DR program in this manner, theissuer establishes a Level l DR program that trades concurrently with the privately placed shares in compliance with SECrules that prevent “leakage” of 144A securities into the Level l program. This facility, developed to broaden access tointernational investors as an issuer’s needs evolve and to improve liquidity in an issuer’s stock, is called a side-by-side facility.A side-by-side facility makes the issuer’s DRs available to all investors, including individual and non-QIB institutionalinvestors. The side-by-side Level l DR program is established under the same Rule 12g3-2(b) exemption that the issuermay have already obtained for the RADRs.

The publicly traded Level l DR facility may already be in place when a RADR or GDR program is established. Certainconditions relating to activities in the U.S. market must be met to ensure that there are no conflicts with the SEC provisionsrelated to private placements and Reg S offerings.

*SEAQ (Stock Exchange Automated Quotation System) is the London Stock Exchange’s service for mid-cap securities and the mostliquid AIM (Alternative Investment Market) securities. The service is based on two-way continuous quotes, offered by competingmarket makers.

8/8/2019 Depository Receipts Information Guide_Citigroup

http://slidepdf.com/reader/full/depository-receipts-information-guidecitigroup 20/58

Activity Week** Key Parties Involved

Establish Program Launch Team

Prepare Offering Circular and Deposit Agreement

File Rule 12g3-2(b) exemptive application with SEC, if applicable

Notify local stock exchange of intention to offer

Contact Euroclear, Cedel and DTC regarding eligibility for their

respective book-entry systems

Print preliminary Offering Circular

Apply to Nasdaq for eligibility in the PORTAL system

Confirm that SEC has added the issuer to its list of foreign private issuers

claiming Rule 12g3-2(b) exemption, if applicable

Sign Deposit Agreement

Print final Offering Circular

Closing Day

Placement Agent delivers cash proceeds to issuer

Depositary’s custodian receives underlying shares

Depositary delivers RADR/GDR securities to underwriter through DTC

Closing Day + 40 Days***

Sign Level l DR Deposit Agreement, file form F-6 with SEC

Depositary delivers DRs upon receipt of underlying shares

*This chart focuses on a typical Rule 144A/Reg S offering, which requires no SEC registration.

**The time frames provided for establishing new programs are indicative only. Establishment can take as little as seven weeks

but time frames may vary due to regulators’ involvement and individual program specifics.

***If a “side-by-side” facility is being established.

Steps to Conduct a RADR/GDR* Program

1 2 3 4 5 6 7 I s s u e r

D e p o s i t a r y

L e g a l C o u n s e

l

A c c o u n t a n t s

I n v e s t m e n t B a n k

I R F i r m

B r o k e r s

18 >> Citigroup Depositary Receipt Services

8/8/2019 Depository Receipts Information Guide_Citigroup

http://slidepdf.com/reader/full/depository-receipts-information-guidecitigroup 21/58

DR ConversionsIn many instances, investors wish to convert DRs from one program to another program with the same class of underlyingordinary shares. However, certain conversions are restricted. The following is a general guideline of what conversions mightbe possible for an investor.

Information Guide << 19

Acceptable DR Conversions

Type of Security Held Type of Security the Acceptability of Conversion

by the Investor Investor PrefersRule 144A DR (RADR) Reg S GDR Acceptable (with certification papers). Provided the

underlying ordinary shares are the same class,

conversion is possible

Rule 144A DR (RADR) Level I or Level II ADR Not Acceptable, unless pursuant to an exchange

offer or a special certification process

Reg S GDR Rule 144A DR (RADR) Acceptable (with certification papers).

Provided the underlying ordinary shares are the

same, conversion is possible.

Reg S GDR Level I or Level II ADR Usually acceptable after a 40-day restricted period

Level I or Level II ADR Rule 144A DR (RADR) Acceptable (with certification papers)

Level I or Level II ADR Reg S GDR Acceptable (with certification papers)

8/8/2019 Depository Receipts Information Guide_Citigroup

http://slidepdf.com/reader/full/depository-receipts-information-guidecitigroup 22/58

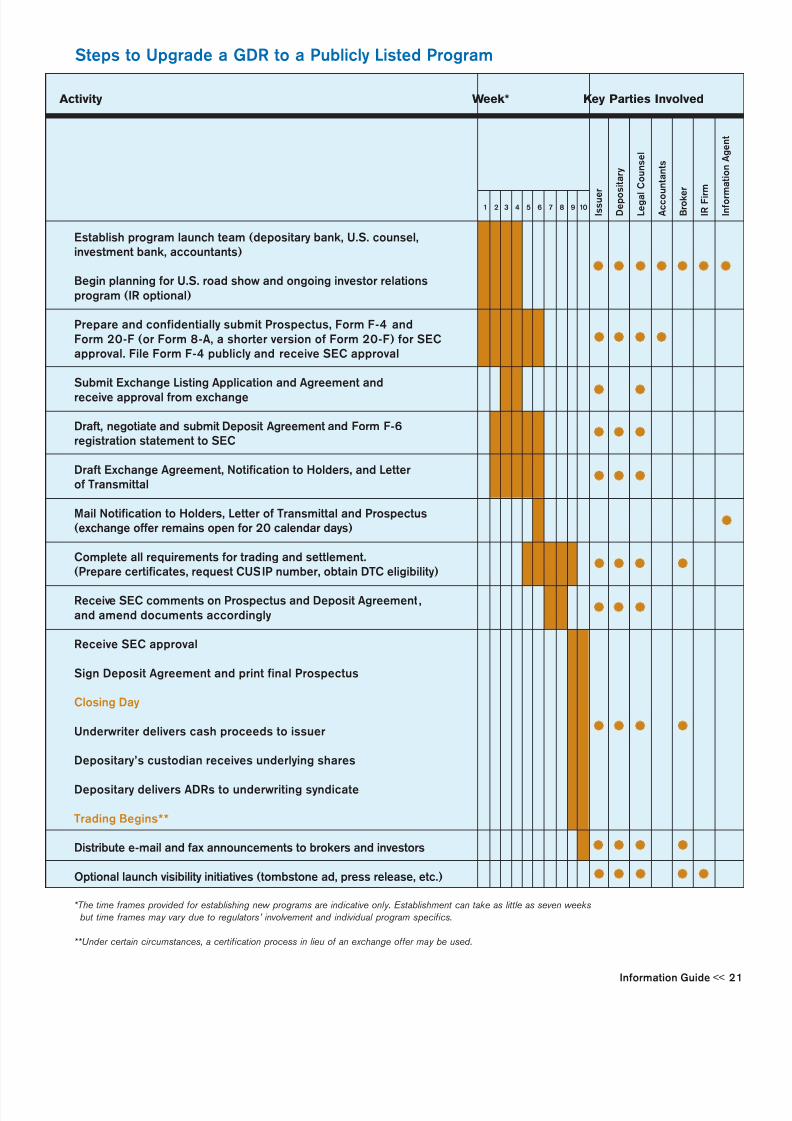

Upgrading a GDR to a Publicly Listed ProgramA Non-U.S. company may decide to list its DRs subsequent to its global Rule 144A and Reg S offering. Although the RegS tranche easily can be moved to a listed facility 40 days after the Reg S offer, a Rule 144A tranche cannot. Furthermore,a Rule 144A facility cannot actively coexist with a listed program. In order to upgrade the Rule 144A facility to a listedprogram, the issuer first needs to file a form F-4 registration statement pursuant to the 1933 Act. After the F-4 registra-tion statement is filed, a registered exchange offer with the QIBs may be undertaken. Under certain circumstances, andif the Rule 144A program is “seasoned” (i.e. if the two-year period since the last deposit by the company or any of itsaffiliates in the Rule 144A program has expired), the issuer may opt for a private exchange using a certification processrather than a registered exchange under the 1933 Act.

20 >> Citigroup Depositary Receipt Services

8/8/2019 Depository Receipts Information Guide_Citigroup

http://slidepdf.com/reader/full/depository-receipts-information-guidecitigroup 23/58

Steps to Upgrade a GDR to a Publicly Listed Program

1 2 3 4 5 6 7 8 9 10 I s s u e

r

D e p o

s i t a r y

L e g a l C o u n s e l

A c c o

u n t a n t s

B r o k e r

I R F i r m

I n f o r m a t i o n A g e n t

Information Guide << 21

Activity Week* Key Parties Involved

Establish program launch team (depositary bank, U.S. counsel,investment bank, accountants)

Begin planning for U.S. road show and ongoing investor relationsprogram (IR optional)

Prepare and confidentially submit Prospectus, Form F-4 andForm 20-F (or Form 8-A, a shorter version of Form 20-F) for SECapproval. File Form F-4 publicly and receive SEC approval

Submit Exchange Listing Application and Agreement and

receive approval from exchange

Draft, negotiate and submit Deposit Agreement and Form F-6registration statement to SEC

Draft Exchange Agreement, Notification to Holders, and Letterof Transmittal

Mail Notification to Holders, Letter of Transmittal and Prospectus(exchange offer remains open for 20 calendar days)

Complete all requirements for trading and settlement.(Prepare certificates, request CUSIP number, obtain DTC eligibility)

Receive SEC comments on Prospectus and Deposit Agreement,and amend documents accordingly

Receive SEC approval

Sign Deposit Agreement and print final Prospectus

Closing Day

Underwriter delivers cash proceeds to issuer

Depositary’s custodian receives underlying shares

Depositary delivers ADRs to underwriting syndicate

Trading Begins**

Distribute e-mail and fax announcements to brokers and investors

Optional launch visibility initiatives (tombstone ad, press release, etc.)

*The time frames provided for establishing new programs are indicative only. Establishment can take as little as seven weeksbut time frames may vary due to regulators’ involvement and individual program specifics.

**Under certain circumstances, a certification process in lieu of an exchange offer may be used.

8/8/2019 Depository Receipts Information Guide_Citigroup

http://slidepdf.com/reader/full/depository-receipts-information-guidecitigroup 24/58

22 >> Citigroup Depositary Receipt Services

lV. DR EnhancementsIn recent years a number of innovations have made DRs an increasingly flexible and attractive corporate finance toolfor Non-U.S. issuers.

Some innovations involve new structures designed to access additional markets or investors, such as AmericanDepositary Debentures (ADDs) and American Depositary Notes (ADNs). Others are transaction-based and use DRsto further the issuer’s goals in acquisitions, privatizations or debt financing. Still others satisfy investor relations oremployee benefits objectives by offering Dividend Reinvestment, Employee Stock Purchase and Stock Option plans.

The ability to tailor a program to meet individual issuer needs demonstrates the versatility of DRs.

American Depositary Debentures (ADDs) and American Depositary Notes (ADNs)ADDs and ADNs are debt securities issued in the U.S. that represent, respectively, debentures or notes of the issuerdeposited with the depositary’s custodian in the issuer’s home market. In either case, the issuer establishes a DRfacility under a deposit agreement with the depositary to provide for the issuance of ADDs or ADNs against thedeposit of debentures or notes. ADDs and ADNs are quoted in U.S. dollars and represent the right to receive a fixedprincipal amount of the debt represented by the securities deposited with the custodian in the issuer’s home market,irrespective of the currency in which the debt is denominated. Interest and other payments made by the issuer on thedebentures or notes will be converted to U.S. dollars and distributed by the depositary to the holders of the correspon-ding ADDs or ADNs.

ADDs and ADNs may be listed for public trading on the U.S. exchanges. Public offers of debt securities in the U.S.

are subject to the requirements of the Trust Indenture Act of 1939, and the indenture or other agreement amongthe issuer, the debt holders and the trustee for the debt holders must comply with its terms. Public offers of debtsecurities in the U.S. must comply with the registration and reporting requirements of the U.S. securities laws.

Exchangeable Bonds or NotesExchangeable Bonds or Notes are debt instruments issued by a company (not necessarily an ADR issuer) which mayconvert into an ADR of that issuer or another issuer, usually an affiliate of the issuing company.

American Depositary Warrants (ADWs)Warrants typically entitle the holder to purchase a specified number of shares for a specified price over a specifiedperiod of time in the local market. ADWs issued against deposited warrants generally entitle the holders to purchasea corresponding specified number of American Depositary Shares (ADSs) representing the issuer’s shares depositedin its DR facility for a specified price in $US over the same specified period of time provided under the terms of the

issuer’s warrants. Certain ADWs have been structured as stock appreciation warrants which provide investors theopportunity to exercise their ADWs for ADSs upon the occurrence of certain events or upon triggering a certain strikeprice specified under the terms of the issuer’s appreciation warrants.

Embedded Restricted Securities (ERS)Embedded Restricted Securities are restricted securities embedded into an exchange-listed program. This structureis used when an existing exchange-listed issuer needs to issue restricted ADRs. The restricted securities are listed onthe exchange but are segregated from the registered ADRs for securities law purposes.

8/8/2019 Depository Receipts Information Guide_Citigroup

http://slidepdf.com/reader/full/depository-receipts-information-guidecitigroup 25/58

Information Guide << 23

N SharesThe N Share structure was created to assist issuers in developing markets in accessing international investorswhile retaining control over ownership in the home market. N shares are not listed in the home market and cannotbe purchased by local investors. N shares are created by the issuer to provide a means of raising capital amonginternational investors.

Alternative Structures

New York Registry Shares (NYRSs)A New York Registry Share (NYRS) Program is a mechanism for holding, trading and settling transfers of shares ofNon-U.S. issuers in New York. The structure is typically used by Dutch issuers where local law allows share registrationto occur outside of the Netherlands. Thus, a NYRS issuer company’s share capital is equivalent to the sum of theDutch and U.S. registers.

DR programs and NYRS programs serve the samepurpose: to support the holding, trading and settlingin the U.S. of equity securities of Non-U.S. issuers.The most notable differences lie in the legal andservicing aspects of these structures, such as:

>> Absence of the custodial function from

NYRS programs>> Difference in fee structures>> No “ratio” between local shares and NYRSs

The differences between DR and NYRS programsare transparent to many U.S. investors who tradein Non-U.S. equity securities. From an issuer pointof view, factors influencing the selection of onestructure over another might include greater issuerinvolvement needed for implementation and

maintenance of NYRS programs, and the relative ease with which DR programs can be amended or terminatedby agreement with the depositary.

Global Registered Shares (GRSs)The first Global Registered Share (GRS) program was established by DaimlerChrysler AG in 1998 as a means totrade the company’s shares directly on the NYSE in a manner fully fungible with the German-traded shares. Througha New York-based transfer agency arrangement, direct share registration is coordinated with the company’s homemarket registrar. At this writing, there are three other GRS program in existence: Germany’s Celanese AG, DeutscheBank AG and Switzerland-based UBS AG. Key differences between GRSs and DRs lie in issues of fee structure andcontrol. Many Canadian and Israeli issuers list their ordinary shares directly on U.S. exchanges using a similar structure.

The differences between DR and NYRS programs are transparentto many U.S. investors.

8/8/2019 Depository Receipts Information Guide_Citigroup

http://slidepdf.com/reader/full/depository-receipts-information-guidecitigroup 26/58

DR Issuance Process

Investor contacts broker and requests the purchaseof a DR issuer company’s shares. If existing DRs of thatcompany are not available, the issuance process begins.

To issue new DRs, the broker contacts a local brokerin the issuer’s home market.

The local broker purchases ordinary shares on anexchange in the local market.

Ordinary shares are deposited with a local custodian.

The local custodian instructs the depositary to issueDRs that represent the shares received.

The depositary issues DRs and delivers them inphysical form or book entry form through DTC/Euroclear/Clearstream (as applicable).

The broker delivers DRs to the investor or credits

the investor’s account.

Investor

DR Broker

DTC/Euroclear/Clearstream

Depositary

Local Broker

Local StockMarket

Local Custodian

V. Issuance and Cancellation Acquiring a DR

Based upon availability and market conditions, an investor may acquire a DR by either purchasing existing DRsor purchasing shares in an issuer’s home market and arranging for the creation of new DRs .

New DRs are created once the underlying shares are deposited with the depositary’s custodian in the issuer’s homemarket. The depositary then issues DRs, which represent the shares on deposit, to the investor or to the investor’s

broker. This is referred to as an issuance of DRs.

24 >> Citigroup Depositary Receipt Services

1

7

1

2

3

4

5

6

7

6

2

3

4

5

Typically, for an issuance of Rule 144A DRs and Reg S DRs, the broker must submit certification papersto the depositary bank.

8/8/2019 Depository Receipts Information Guide_Citigroup

http://slidepdf.com/reader/full/depository-receipts-information-guidecitigroup 27/58

Information Guide << 25

DR Cancellation Process

The investor instructs the broker to cancel DRs.

The broker delivers the DRs to the depositary forcancellation and instructs the depositary to deliverthe ordinary shares to a local custody account.

The depositary cancels the DRs and instructs the localcustodian to release and deliver the underlying sharesto the seller’s broker in the issuer’s home market.

The local custodian delivers the underlying ordinaryshares as instructed to the local broker. The localbroker safekeeps the ordinary shares or deliversthem to or on behalf of the new investor.

Investor

DR Broker

Depositary

Local Custodian

Local Broker

Selling a DR

Based upon demand and market conditions, an investor may sell a DR in the market in which it trades, or the investormay cancel the DR and sell the ordinary share in its home market.

Upon receipt of investor instructions to cancel DRs, the broker delivers DRs to the depositary for cancellation andinstructs the depositary to deliver the ordinary shares to a local custody account. The depositary cancels the DRs and

instructs the local custodian to release and deliver the underlying shares to the seller’s broker in the issuer’s home market.The broker may then either safekeep or sell the ordinary shares in the local market.

1

2

3

4

1

2

3

4

Typically, for cancellation of Rule 144A DRs, the broker must submit certification papers to the depositary bank.For cancellation of Reg S DRs, certification papers are generally required for the first 40 days after the closing.

8/8/2019 Depository Receipts Information Guide_Citigroup

http://slidepdf.com/reader/full/depository-receipts-information-guidecitigroup 28/58

Liquidity

For many DR market participants, liquidity—the consistent breadth and depth of U.S. exchange trading activity—is considered the best measure for long term success of a DR program. Without the ability to move into and out ofpositions of sufficient size, U.S. institutions are reluctant to add the security to their managed portfolios. Likewise,brokers prefer to deal in liquid issues, and both sell-side and buy-side analysts prefer to cover liquid issues, with U.S.standards of financial disclosure providing an important added protection. Liquidity is a “virtuous cycle,” which isdifficult to establish, but once established through a strong investor relations (IR) effort combined with the resourcesand support of the depositary bank and other partners, tends to maintain strong momentum.

A U.S.-traded ADR’s liquidity generally is comparable to the liquidity of underlying shares in the issuer’s home market.For most securities, the supply of ADRs is not constrained solely by U.S. trading volumes. U.S. investors wishing tobuild positions in an ADR (or their U.S. brokers) can create new ADRs by purchasing shares in the issuer’s homemarket and following the issuance process outlined previously in this chapter.

The ADR float constantly fluctuates in response to investor demand. The number of ADRs outstanding increasesor decreases as a result of investor requests for ADR issuances and cancellations.

Citigroup research has shown historically that having an ADR program may actually enhance an issuer company’sliquidity—a phenomenon termed the “uplift effect.” By having two pools of liquidity (the home market through theordinary shares and the U.S. market through the ADRs) and two sets of buyers and sellers, the issuer is more likelyto get the benefit of the more positive sentiment.

26 >> Citigroup Depositary Receipt Services

Citigroup Liquid DR Indices

Citigroup Depositary Receipt Services has developed Liquid DR Indices which are an excellent gauge of internationalinvestor sentiment towards non-U.S. markets.

Liquid DRs by definition attract the most interest from investors. The countries included in the four regional CitigroupLiquid DR Indices account for over 98% of global (excluding U.S.) market capitalization.

Citigroup Liquid DR Indices are distinctive in that they:>> Provide a timely gauge of international investor sentiment towards Non-U.S. markets at end of day, because

all of their constituent stocks trade in the U.S. and/or London time zones.>> More completely capture U.S. and international investor sentiment towards the Indian, Korean andTaiwanese markets by including London traded GDRs, unlike other DR indices.

>> Achieve highly correlated returns to MSCI benchmarks with only a fraction of the number of securities.

The Indices are available on Bloomberg (Tickers CLDRAPAC, CLDREAS, CLDREPAC, CLDRLAT) and the CitigroupDR home page at www.citigroup.com/adr.

8/8/2019 Depository Receipts Information Guide_Citigroup

http://slidepdf.com/reader/full/depository-receipts-information-guidecitigroup 29/58

Exceptions to Standard Issuance and Cancellation

Limited Two-Way MarketsWhile most countries and issuers allow issuance and cancellation into and out of DR facilities at any time (a “two-waymarket”), several countries and issuers maintain restrictions on issuance of DRs (a “limited two-way market”). In alimited two-way market, after withdrawal and sale of ordinary shares from the DR facility, the shares are subject tolimitations on redeposit into the DR facility. Deposits may only occur up to a certain limit. Once that limit is reached,the DR facility is closed for re-issuance. In contrast, in a free two-way market, foreign investors may purchase at anytime outstanding ordinary shares in the local market for deposit into the DR facility.

Three key markets that typically have limited two-way programs but that may benefit from relaxed restrictions areKorea, Taiwan and India.

How relaxed restrictions may benefit issuers and investors:>> Increased possibility for immediate issuance of DRs>> Enhanced liquidity over time. Ability to issue and cancel the company’s DRs potentially enhances trading

activity. Specifically, associated advantages are higher investor demand and higher valuation.>> Decreased risk due to lower share price volatility. Due to larger pool of a company’s stock, changes

in supply and demand yield smaller price changes.>> Broadened opportunity for Non-U.S. investment in local market

DR PremiumThe DR Premium is the differential between the ordinary share price in the local currency and the price of the DR,which is quoted and traded in $US. Historically, when the U.S. market outperforms the Non-U.S. market, the premiumgrows. When the local market outperforms the U.S. market, the premium shrinks.

The limited two-way market promotes cross border liquidity up to a point, but does not significantly reduce the size ofthe DR premium compared to a one-way market. Under a free two-way market, the effect of the higher performingmarket on the size of the DR premium is minimized. International investors will sometimes buy at a premium becauseNon-U.S. ownership of ordinary shares is limited, and DRs are the only way to own a particular security.

Information Guide << 27

8/8/2019 Depository Receipts Information Guide_Citigroup

http://slidepdf.com/reader/full/depository-receipts-information-guidecitigroup 30/58

28 >> Citigroup Depositary Receipt Services

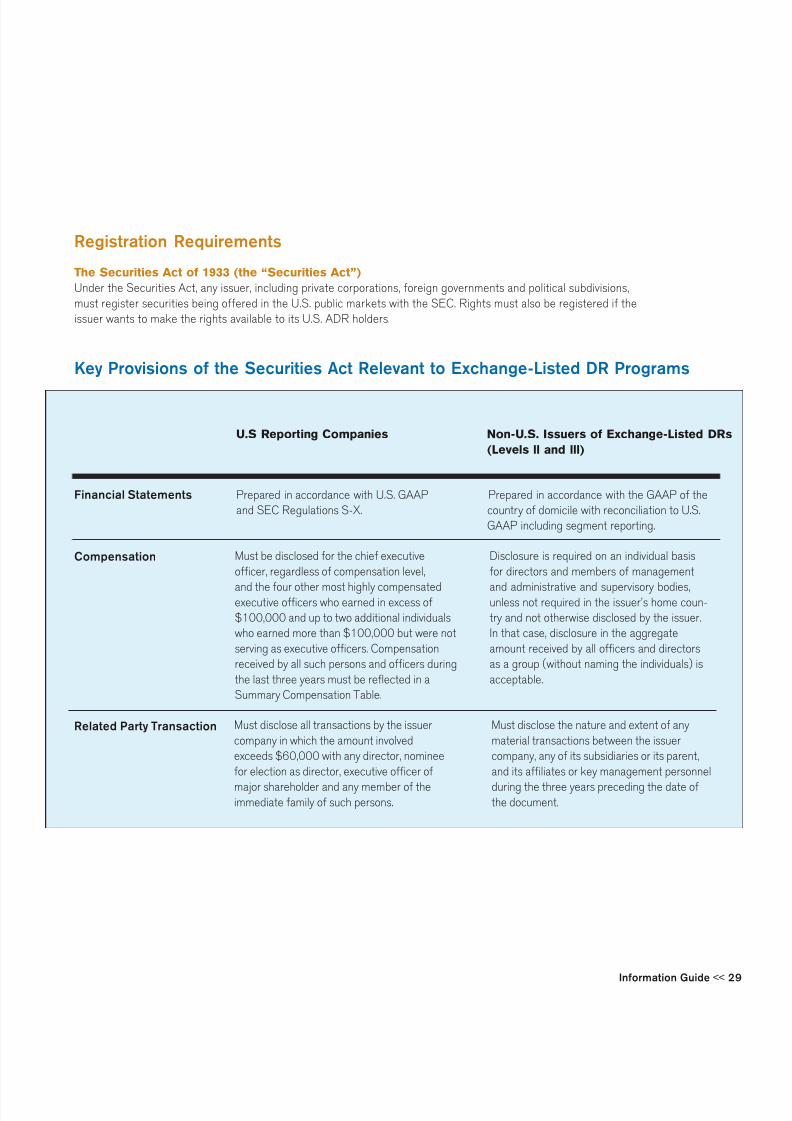

Vl. Securities Regulations and RequirementsIssuers of Depositary Receipts must comply with the regulations of the markets in which their DRs are issued.This section provides a general overview of the regulations which apply in the United States.

The Securities and Exchange Commission (SEC) was created as an independent agency of the U.S. government toenforce federal securities laws governing securities offerings, trading practices and persons dealing in the securitiesmarkets. The SEC protects U.S. investors by requiring disclosure of material facts concerning issuers making publicofferings of securities. The SEC is empowered to issue regulations and enforce provisions of both federal securities

laws and its own regulations.

In addition to the securities regulations discussed in this chapter there may be additional U.S. regulations and/orBlue Sky Securities Laws of individual states within the U.S. that apply to certain issuers. In most instances the federalsecurities laws override the individual states’ securities laws. The issuer’s legal counsel works with the issuer todetermine which regulations apply, and takes steps to ensure compliance with the requirements.

Two key U.S. securities laws with which DR issuers must comply are:>> The Securities Act of 1933, as amended (the “Securities Act”)>> The Securities Exchange Act of 1934, as amended (the “Exchange Act”)

In short, the primary intention of the Securities Act is to provide investors with full and fair disclosure of material infor-mation regarding an issuer in connection with the offer and sale of its securities. The Exchange Act is different in that

its primary intention is to provide investors trading securities of an issuer in the secondary market with access to fulland fair disclosure of material information regarding an issuer on an ongoing basis.

8/8/2019 Depository Receipts Information Guide_Citigroup

http://slidepdf.com/reader/full/depository-receipts-information-guidecitigroup 31/58

U.S Reporting Companies Non-U.S. Issuers of Exchange-Listed DRs

(Levels ll and lll)

Financial Statements Prepared in accordance with U.S. GAAP Prepared in accordance with the GAAP of theand SEC Regulations S-X. country of domicile with reconciliation to U.S.

GAAP including segment reporting.

Compensation

Related Party Transaction

Key Provisions of the Securities Act Relevant to Exchange-Listed DR Programs

Information Guide << 29

Registration Requirements

The Securities Act of 1933 (the “Securities Act”)

Under the Securities Act, any issuer, including private corporations, foreign governments and political subdivisions,must register securities being offered in the U.S. public markets with the SEC. Rights must also be registered if theissuer wants to make the rights available to its U.S. ADR holders.

Disclosure is required on an individual basisfor directors and members of management

and administrative and supervisory bodies,unless not required in the issuer’s home coun-try and not otherwise disclosed by the issuer.In that case, disclosure in the aggregateamount received by all officers and directorsas a group (without naming the individuals) isacceptable.

Must be disclosed for the chief executiveofficer, regardless of compensation level,

and the four other most highly compensatedexecutive officers who earned in excess of$100,000 and up to two additional individualswho earned more than $100,000 but were notserving as executive officers. Compensationreceived by all such persons and officers duringthe last three years must be reflected in aSummary Compensation Table.

Must disclose all transactions by the issuercompany in which the amount involvedexceeds $60,000 with any director, nomineefor election as director, executive officer of

major shareholder and any member of theimmediate family of such persons.

Must disclose the nature and extent of anymaterial transactions between the issuercompany, any of its subsidiaries or its parent,and its affiliates or key management personnel

during the three years preceding the date ofthe document.

8/8/2019 Depository Receipts Information Guide_Citigroup

http://slidepdf.com/reader/full/depository-receipts-information-guidecitigroup 32/58

U.S Reporting Companies Non-U.S. Issuers of Exchange-Listed DRs

(Levels ll and lll)

Financial Statements Prepared in accordance with U.S. GAAPand SEC Regulation S-X.

Compensation Must be disclosed for the chief executive officer,regardless of compensation level, and for each ofthe other most highly compensated executiveofficers who earned in excess of $100,000

and up to two additional individuals who earnedmore than $100,000 but were not serving asexecutive officers. Compensation received byall such persons and officers during the lastthree years must be reflected in a SummaryCompensation Table.

Related Party Transaction Must disclose all transactions in which theamount involved exceeds $60,000 by thecompany with any director, executive officeror major shareholder.

The Securities Exchange Act of 1934 (the “Exchange Act”)

The Exchange Act regulates public trading of securities through standards of fair dealing by brokers, dealers andissuers, and requires certain reports to be filed with the SEC to ensure full and fair disclosure of financial datamaterial to investment decisions. Issuers of unlisted DRs can obtain an exemption from reporting requirements underlisting of DRs on an exchange, and/or registration under the Securities Act of a public offering in the U.S.

Key Provisions of the Exchange Act Relevant to Exchange-Listed DR Programs

30 >> Citigroup Depositary Receipt Services

Prepared in accordance with the GAAP of thecountry of domicile with reconciliation to U.S.GAAP, but with no segment reporting.

Disclosure is required on an individual basis fordirectors and members of management andadministrative and supervisory bodies, unlessnot required in the issuer’s home country and

not otherwise disclosed by the issuer. In thatcase, disclosure in the aggregate amountreceived by all officers and directors as a group(without naming the individuals) is acceptable.

Must disclose the nature and extent of anymaterial transactions between the issuercompany, any of its subsidiaries or its parentand its affiliates, or key management personnelduring the one year preceding the date of thedocument.

8/8/2019 Depository Receipts Information Guide_Citigroup

http://slidepdf.com/reader/full/depository-receipts-information-guidecitigroup 33/58

Information Guide << 31

Rule 12g3-2(b)

This rule sets forth an exemption from reporting under the Securities Exchange Act of 1934 (the “Exchange Act”) forAmerican Depositary Receipts and certain other Non-U.S. securities.

Under Section 12(g) of the Act, a Non-U.S. issuer with total assets exceeding US$1 million and a class of equity securityheld of record by 500 or more U.S. shareholders becomes subject to the registration and reporting provisions of the Act.

Paragraph (b) of Rule 12g3-2 exempts such an issuer from the reporting requirements of the Exchange Act providedthat the issuer furnishes to the SEC the information that it is requested to disclose in its home country. Key provisions ofParagraph (b) include that in order to be exempt, an issuer—or a government official or agency of the country of the

issuer’s domicile or in which it is incorporated or organized—must furnish to the SEC information dating from thebeginning of its last fiscal year that it:

a. has made or is required to make public pursuant to the law of the country of its domicile or in which it isincorporated or organized,

b. has filed or is required to file with a stock exchange on which its securities are traded and which was madepublic by such exchange of this section, or

c. has distributed or is required to distribute to its security holders.

8/8/2019 Depository Receipts Information Guide_Citigroup

http://slidepdf.com/reader/full/depository-receipts-information-guidecitigroup 34/58

32 >> Citigroup Depositary Receipt Services

Reports to be Filed with the SEC byCompanies Registered Under the Exchange Act

U.S. Reporting Companies Non-U.S. Issuers of Exchange-

Listed DR Programs

TYPE OF REPORTS TO TIME OF FILING REPORTS TO TIME OF FILING

REPORT BE FILED BE FILED

Annual Report 10-K Within 90 days following 20-F Six months following closeclose of fiscal year of fiscal year

Quarterly Report 10-Q Within 45 days following Exempt 1 Exempt 1

close of each of the firstthree-quarters of the fiscal year

Current Report 8-K Within a certain time (5/15 days) 6-K 2,3 Promptly after any information

following the occurrence of certain or documentation required todesignated events be furnished on Form 6-K

has been filed with a stockexchange in the issuer’s homecountry, distributed tostockholders or made publicin the home country

Proxy Statement Preliminary and Preliminary proxy material, 10 Exempt 4 Exempt 4

Definitive Proxy days prior to mailing; definitiveproxy material, at time of firstmailing to stockholders

Directors, Forms 3, 4 or 5 Form 3 (statement of beneficial Exempt 5 Exempt 5

Officers and ownership), 10 days afterBeneficial becoming a director, officer orOwners 10% holder; Form 4 (statement

of changes in beneficial ownership),within 10 days of the last day of themonth in which a change occurred;Form 5 (annual statement ofownership transactions), within 45days after the issuer’s fiscal year end

1 Regulation 240.13a-13(b)2 under the Exchange Act exempts foreign private issuers from the requirements to file quarterly reports on Form 10-Q

if they are required to file 6-K reports pursuant to Section 240.13a-16 of the Exchange Act.

2 While 8-K reports filed by U.S. reporting companies subject the issuers to the liability provisions of Section 18 of the Exchange Act, Rule 240.13a-16(c)

under the Exchange Act exempts from such provisions reports filed on Form 6-K by foreign issuers.

3 Regulation 240.13a-11(b) under the Exchange Act exempts foreign private issuers that file reports on Form 6-K from filing any current reports on Form 8-K.

4 Regulation 240.3a-12.3(b) under the Exchange Act exempts foreign private issuers from the proxy regulations.

5 Regulation 240.3a-12.3(b) exempts a foreign private issuer’s directors and officers from reporting on Forms 3, 4 or 5.

8/8/2019 Depository Receipts Information Guide_Citigroup

http://slidepdf.com/reader/full/depository-receipts-information-guidecitigroup 35/58

Information Guide << 33

Other Relevant Securities Law ProvisionsIn recent years, there have been two significant legislative moves to heighten corporate governance compliance by issuersin the U.S., impacting Non-U.S. issuers in different ways. These include:

>> Regulation Fair Disclosure (Regulation FD), enacted in 2000>> Sarbanes-Oxley Act, enacted in 2002

Regulation Fair Disclosure (Regulation FD)Regulation FD was enacted in 2000 to address the SEC’s concerns regarding the integrity of the capital market,unfair advantage to corporate insiders and loss of public confidence in the fairness of the markets. Regulation FDprovides that whenever an issuer selectively discloses material non-public information to persons expected topurchase or sell securities, the issuer must make public disclosure either simultaneously or promptly.

Regulation FD applies to reporting issuers in the U.S. (primarily companies having securities listed on a U.S. exchange), andit technically excludes Non-U.S. private issuers and Non-U.S. governments. However, it is relevant to DR issuers in that:

>> The anti-fraud provisions and insider trading laws of the U.S. apply to the disclosure practices of Non-U.S.companies which have securities listed on an exchange in the U.S.

>> Selective disclosure may become the basis for a private enforcement action under those laws.>> The SEC has identified selective disclosure as “bearing a close resemblance” to insider trading.

For these reasons, many Non-U.S. companies with securities trading in the U.S. (including DR issuers) have voluntarilyopted to comply with the requirements of Regulation FD.

8/8/2019 Depository Receipts Information Guide_Citigroup

http://slidepdf.com/reader/full/depository-receipts-information-guidecitigroup 36/58

Sarbanes-Oxley Act

The Sarbanes-Oxley Act of 2002 was signed into law on July 30, 2002 to address the SEC’s concerns regardingcorporate responsibility and accountability, financial disclosure, accounting and auditing standards, and liability associatedwith violations of securities laws. The Sarbanes-Oxley Act provides broad amendments and additions to the SecuritiesAct, the Exchange Act and other laws in response to breaches in corporate governance.

There is no provision in the Sarbanes-Oxley Act itself that universally exempts Non-U.S. issuers. However, in adoptingrules to implement the law, the SEC has applied certain exemptions for Non-U.S. companies. With respect to depositaryreceipts, issuers of Level l programs are exempt because they are generally exempt from reporting under the ExchangeAct. However, issuers of Level ll and Level lll DR programs must comply with the Sarbanes-Oxley Act.

The table below highlights the provisions of the Sarbanes-Oxley Act that may impact DR issuers.

Selected Provisions of the Sarbanes-Oxley Act Applicableto Non-U.S. IssuersUnless otherwise noted in the table, there are no statutory exemptions for non-U.S. issuers.

Provision Section Description

Audit Committee Requirements 301 All listed companies must maintain independent audit committees that areresponsible for employment, compensation and oversight of auditors.

There are limited exemptions for foreign private issuers.

Certification of Financial Disclosure 302 & 906 Section 302 requires CEOs and CFOs to certify for each annual, semi-

annual or quarterly report “filed or submitted” to the SEC the following:>> he/she has reviewed the filing>> there are no material misstatements or omissions>> it is a fair presentation of financial condition>> he/she has responsibility for internal controls and their effectiveness>> he/she has disclosed to auditors and the Audit Committee any

control deficiencies and fraud, and corrective actions takenconcerning control weaknesses or deficiencies

Section 906 requires CEOs and CFOs to certify for all Exchange Actreports containing financials that:>> the financials comply with Exchange Act requirements>> the financials are a fair representation of the financial condition

and reports of operation

Further, Section 906 provides for criminal penalties for failure tocomply including:>> fines of $1 million to $5 million>> imprisonment from 10 to 20 years

34 >> Citigroup Depositary Receipt Services

8/8/2019 Depository Receipts Information Guide_Citigroup

http://slidepdf.com/reader/full/depository-receipts-information-guidecitigroup 37/58

Provision Section Description

Unlawful Influence on 303 Section 303 prohibits any officer, director or other persons under

Conduct of Audits their direction from taking any action to fraudulently influence, coerce,manipulate or mislead auditors for purposes of rendering financialstatements to be materially misleading.

CEO/CFO Forfeiture of 304 Section 304 provides that if an issuer is required to prepare an accountingBonuses and Profits restatement due to material noncompliance by the issuer with the financial

reporting requirements of the securities laws as a result of misconduct,the CEO/CFO of the issuer will be required to reimburse the issuer companyfor any bonus/equity-based or incentive-based compensation/profitsreceived or realized during the 12 months following the public issuance orfiling of the relevant financial document.

Officer and Director 305 Section 305 provides that the SEC has power to bring action against a

Bars and Penalties person “unfit” to serve as officer/director and to obtain applicable equitablerelief appropriate and necessary to benefit investors.

Prohibition on Insider 306 Section 306 provides that directors and executive officers are prohibitedTrading During Pension Fund from buying, selling or otherwise transferring equity securities (acquiredBlackout Periods in connection with employment) during any blackout period for a

self-directed pension plan.

SEC has provided exemptions for certain transactions (e.g., DRIPs,advance election).

Enhanced Financial 401 Section 401 provides for certain adjustments to GAAP financials, includingDisclosures that all annual and quarterly financials filed with the SEC must disclose all

material off-balance sheet transactions, arrangements, obligations andrelationships with unconsolidated entities that may have material currentor future effect on financials.

All GAAP financials must contain all corrective adjustments identified by RPAF.

There are limited exceptions for foreign private issuers on prohibitionsto use non-GAAP items.

Prohibition and Personal Loans 402 Section 402 provides that issuers are prohibited from extending or renewingcredit in the form of personal loans to any director or executive officer (exceptfor consumer loans generally available to the general public on market terms).

Audit Committee Financial 407 Section 407 requires an issuer to disclose in annual/quarterly reportsExpert whether or not (and if not, why not) its audit committee comprises at least

one member that is a “financial expert.”

Foreign private issuers must make this disclosure in their Form 20-F filings.

Information Guide << 35

8/8/2019 Depository Receipts Information Guide_Citigroup

http://slidepdf.com/reader/full/depository-receipts-information-guidecitigroup 38/58

36 >> Citigroup Depositary Receipt Services

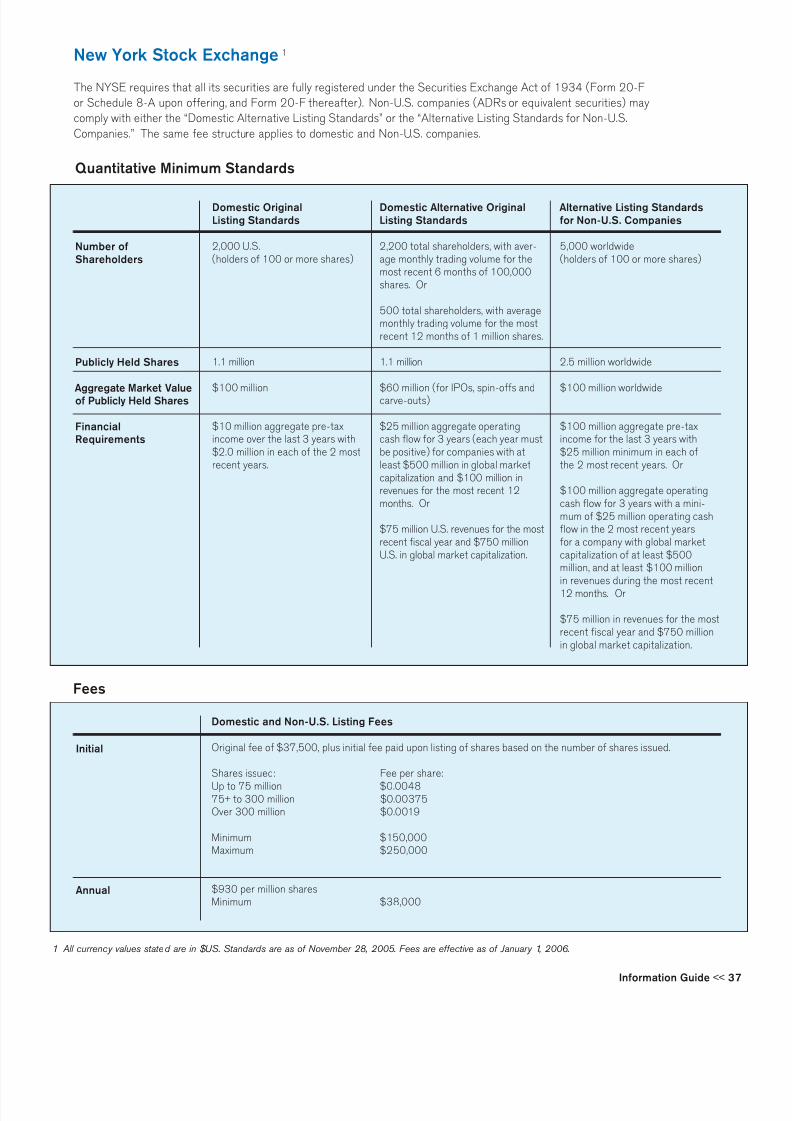

Web Directory for U.S. Listing Requirements