DEPARTMENT OF REGULATORY AGENCIES,...

110

DEPARTMENT OF REGULATORY AGENCIES, DIVISION OF REAL ESTATE CONSERVATION EASEMENT TAX CREDIT PROGRAM, AFTER CHANGES IN 2014 NOVEMBER 2016 PERFORMANCE AUDIT

Transcript of DEPARTMENT OF REGULATORY AGENCIES,...

DEPARTMENT OF REGULATORY AGENCIES, DIVISION OF REAL ESTATE

CONSERVATION EASEMENT TAX CREDIT PROGRAM, AFTER CHANGES IN 2014

NOVEMBER 2016 PERFORMANCE AUDIT

THE MISSION OF THE OFFICE OF THE STATE AUDITOR IS TO IMPROVE GOVERNMENT

FOR THE PEOPLE OF COLORADO

Representative Dan Nordberg – Chair Representative Dianne Primavera – Vice-Chair Senator Rollie Heath Representative Tracy Kraft-Tharp Senator Chris Holbert Senator Tim Neville Senator Cheri Jahn Representative Lori Saine

Dianne E. Ray State Auditor Monica Bowers Deputy State Auditor Jenny Page Audit Manager Christopher Harless Team Leader Kevin Amirehsani Staff Auditors Amber Spencer Torry van Slyke

AN ELECTRONIC VERSION OF THIS REPORT IS AVAILABLE AT WWW.COLORADO.GOV/AUDITOR

A BOUND REPORT MAY BE OBTAINED BY CALLING THE OFFICE OF THE STATE AUDITOR

303.869.2800

PLEASE REFER TO REPORT NUMBER 1561P WHEN REQUESTING THIS REPORT

LEGISLATIVE AUDIT COMMITTEE

OFFICE OF THE STATE AUDITOR

DIANNE E. RAY, CPA ——

STATE AUDITOR

OFFICE OF THE STATE AUDITOR 1525 SHERMAN STREET

7TH FLOOR DENVER, COLORADO

80203

303.869.2800

OFFICE

November 16, 2016

Members of the Legislative Audit Committee:

This report contains the results of a performance audit of Colorado’s Conservation Easement Tax Credit Program within the Division of Real Estate at the Department of Regulatory Agencies. The audit was conducted pursuant to Section 2-3-103, C.R.S., which authorizes the State Auditor to conduct audits of all departments, institutions, and agencies of state government, and Section 2-7-204(5), C.R.S., which requires the State Auditor to annually conduct performance audits of one or more specific programs or services in at least two departments for purposes of the SMART Government Act. This report presents our findings, conclusions, and recommendations, and the responses of the Division of Real Estate.

OF THE STATE AUDITOR

CONTENTS Report Highlights 1 CHAPTER 1 OVERVIEW 3

Conservation Easement Tax Credits 4 Claiming and Using Tax Credits 7 Administration 13 Major Program Changes 15 Program Funding 16 Audit Purpose, Scope, and Methodology 17

CHAPTER 2 ADMINISTRATION OF CONSERVATION EASEMENT TAX CREDITS 21

Timeliness of Application Reviews 23 RECOMMENDATION 1 39 Placeholder Certificate Process 42 RECOMMENDATION 2 50 Fee Setting and Fund Management 52 RECOMMENDATION 3 61 Communicating Review Standards to Appraisers 64 RECOMMENDATION 4 71 Effectiveness of the Tax Credit for Land Conservation 74 RECOMMENDATION 5 83 Policy Considerations 86

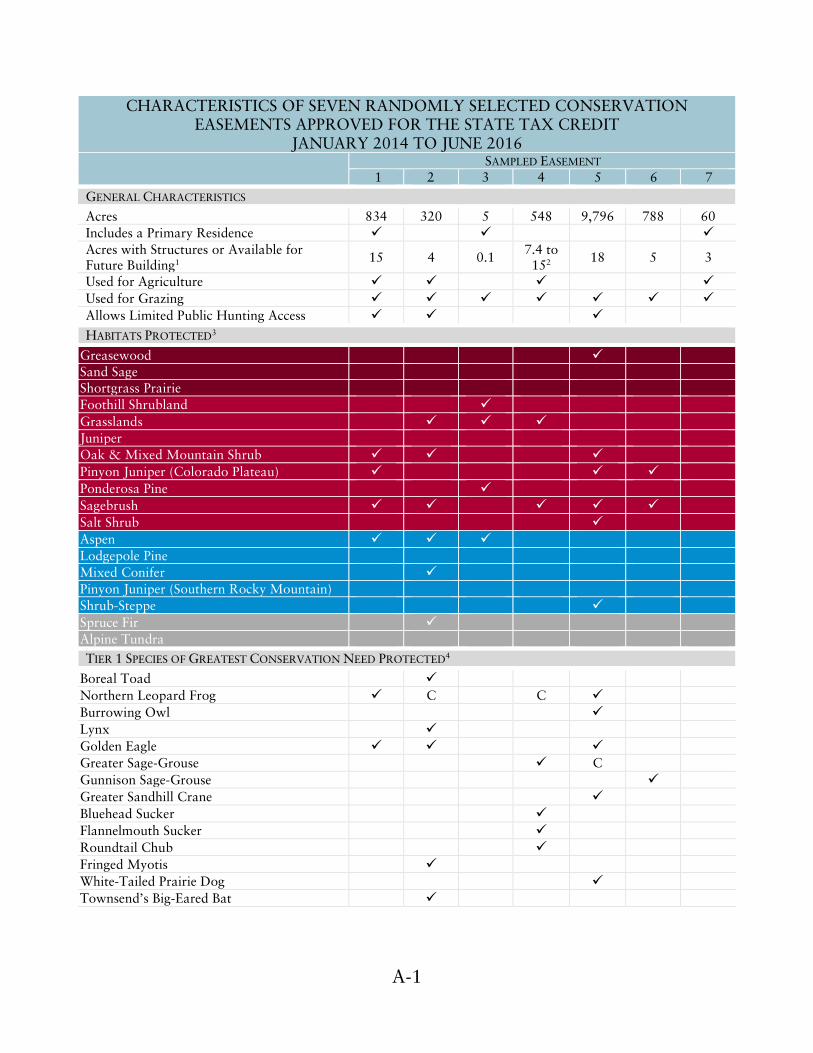

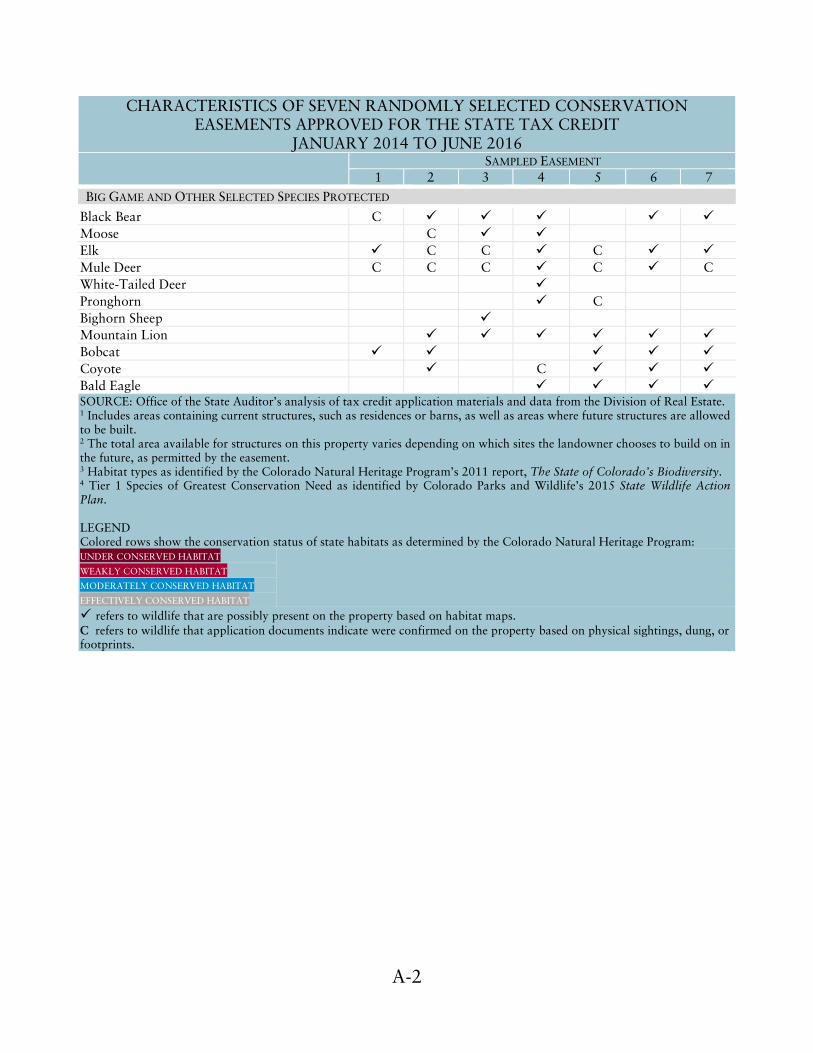

APPENDIX A Characteristics of Seven Randomly Selected Conservation Easements Approved for the State Tax Credit A-1

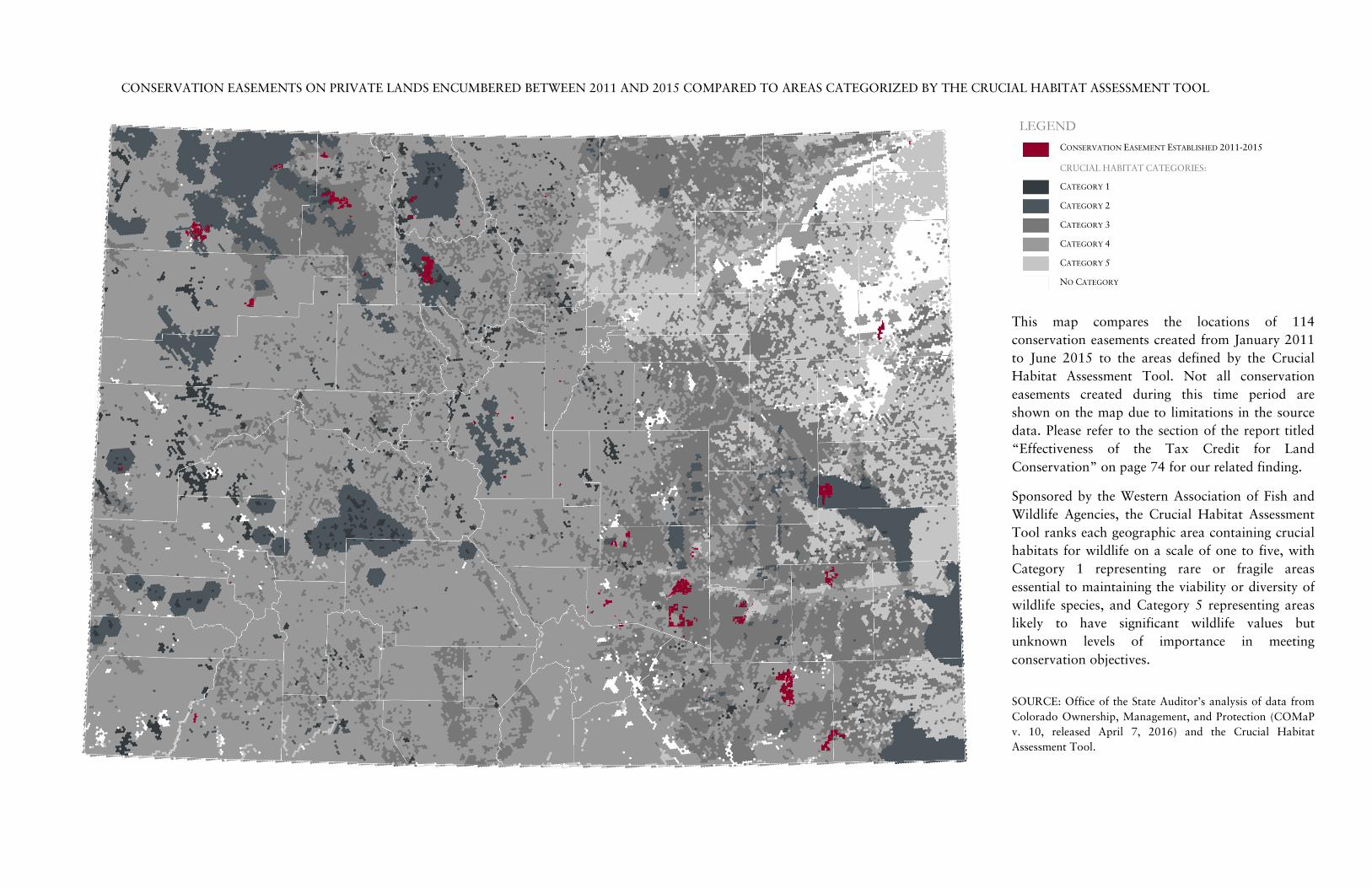

APPENDIX B

Conservation Easements on Private Lands Encumbered Between 2011 and 2015 Compared to Areas Categorized by the Crucial Habitat Assessment Tool B-1

REPORT

FOR FURTHER INFORMATION ABOUT THIS REPORT, CONTACT THE OFFICE OF THE STATE AUDITOR 303.869.2800 - WWW.COLORADO.GOV/AUDITOR

HIGHLIGHTS

KEY FINDINGS

The Division spent an average of 133 days on its initial reviews of conservation easement tax credit applications from January 2015 to June 2016, which exceeded the statutory 120-day average timeframe. Lengthy reviews are an inefficient use of Division resources and increase costs for some landowners.

In an effort to increase cash flow in 2014, the Division created a placeholder process to encourage landowners and non-landowners to prepay fees for preliminary advisory opinions in exchange for discounted fees on future tax credit applications. The Division improperly recorded 63 such prepayments and spent the money before receiving applications for the preliminary advisory opinions, resulting in unfunded liabilities through 2016. As of September 2016, about $48,000 in liabilities remained.

The Division has not collected sufficient revenue from application fees to cover its expenses associated with reviewing applications, partly due to flaws in its fee-setting methodology. Consequently, the Division has had difficulty funding Program staff positions and has a backlog of applications waiting to be reviewed.

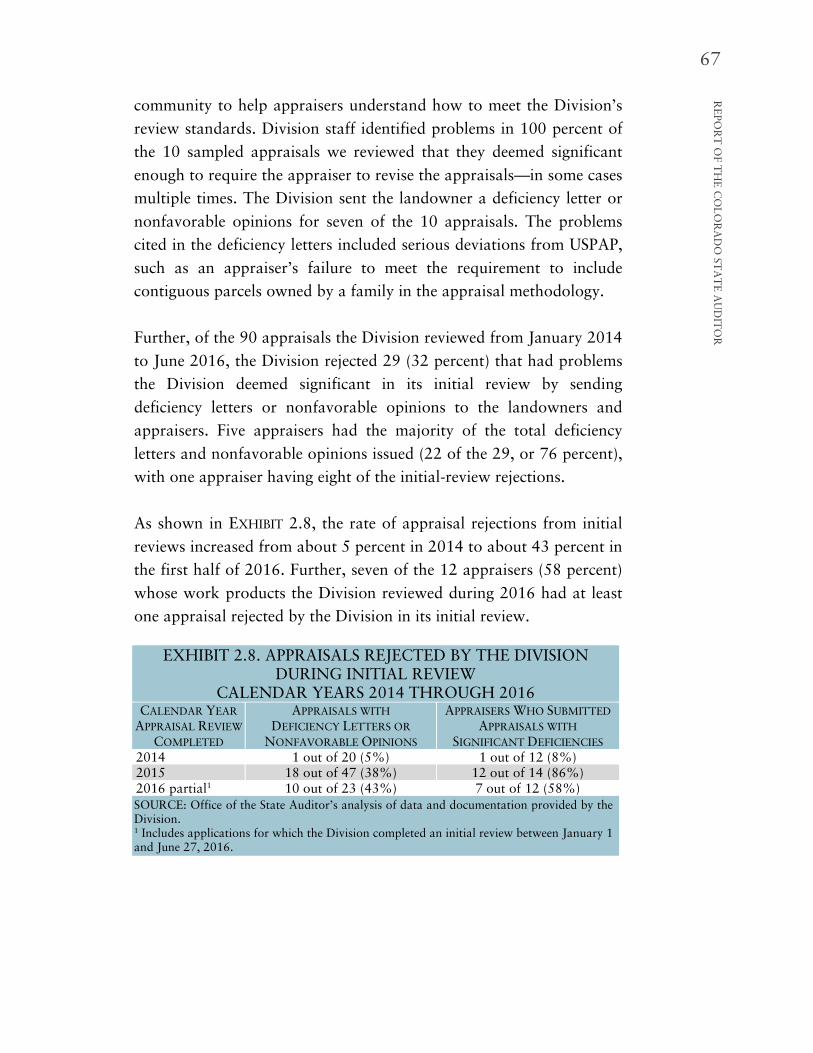

The Division identified problems with most conservation easement appraisals from January 2014 to June 2016, indicating the Division could improve its communication to help appraisers understand how to meet applicable standards.

Currently, no state agency reports on the types of lands, wildlife, or habitats being conserved by the Program, making it difficult for the public and policymakers to determine the benefits that the State has received from the Program in return for forgone tax revenue.

The Conservation Easement Oversight Commission may need authority from the General Assembly or legal guidance to set Program policies or direct outcomes, which would help ensure the Program addresses the State’s conservation needs effectively.

BACKGROUND

Colorado landowners are eligible for a state income tax credit when they donate a conservation easement on their land to a qualified organization, such as a land trust or local government.

In 2014, following the passage of Senate Bill 13-221, some Program administration shifted from the Department of Revenue to the Division. The Division instituted processes for reviewing applications for the conservation easement tax credit and for providing preliminary advisory opinions on whether proposed easement donations would qualify for the tax credit.

Since 2000 when the Program began, the State has issued almost $1 billion in tax credits for over 4,200 conservation easement donations on more than 1.7 million acres.

KEY RECOMMENDATIONS

The Division of Real Estate, within the Department of Regulatory Agencies, should: Implement timeliness goals and strategies to reduce the time it takes to review applications and issue decisions. Address the problems created by its placeholder process by either issuing refunds or continuing to track usage. Improve its fee-setting methods to ensure revenues are sufficient to cover the Program’s administrative costs. Better communicate review standards to appraisers and give landowners information on finding competent appraisers. Expand its public reporting on the specific conservation benefits the State receives from the Program. The Division of Real Estate agreed with these recommendations.

KEY CONCERNS The Division of Real Estate (Division) should improve its administration of the Conservation Easement Tax Credit Program (Program) by reviewing tax credit applications faster, improving its management of Program fees and resources,

and implementing strategies to help reduce the incidence of problems in conservation easement appraisals.

DEPARTMENT OF REGULATORY AGENCIES DIVISION OF REAL ESTATE

CONSERVATION EASEMENT TAX CREDIT PROGRAM, AFTER CHANGES IN 2014 PERFORMANCE AUDIT, NOVEMBER 2016

CHAPTER 1 OVERVIEW

A conservation easement is a legal agreement that restricts a landowner’s development and usage rights to preserve land for certain public benefits, such as open space, fish and wildlife habitats, outdoor recreation, or historical sites. Since 1976, Colorado statutes have allowed private landowners to donate a conservation easement on all or a portion of their land to a governmental entity or nonprofit organization, such as a land trust, to permanently limit how the land is used and protect its conservation value [Section 38-30.5-101 et seq., C.R.S.].

4

CO

NSE

RV

AT

ION

EA

SEM

EN

T T

AX

CR

ED

IT P

RO

GR

AM

, AFT

ER

CH

AN

GE

S IN

201

4, P

ER

FOR

MA

NC

E A

UD

IT –

NO

VE

MB

ER

201

6

The governmental entity or nonprofit organization that receives a conservation easement donation is known as a conservation easement holder, and it has the right to restrict the landowner from using the land in ways that would be inconsistent with the intended protection, such as building structures, diverting or damming streams, harvesting timber, or conducting surface mining. The landowner retains the ability to occupy, sell, or pass on the land to heirs, and may be allowed to use the property for traditional land uses, such as livestock grazing or farming, depending on the specific terms of the conservation easement. Conservation easements are viewed as desirable mechanisms for land preservation, because conservation-oriented parties, including governments and land trusts, can protect land without having to acquire full ownership of it. The specific conservation purposes being protected and any restrictions on the easement’s land are contained in the deed of conservation easement, which is maintained as part of local property records and the property title.

CONSERVATION EASEMENT TAX CREDITS

Landowners who donate a conservation easement to a governmental entity or nonprofit organization may qualify for federal and state tax benefits. Federal law [26 USC 170(h)] allows landowners to claim a federal income tax deduction for all or part of a donated conservation easement, which the tax code refers to as a “qualified conservation contribution.” Since 2000, Colorado statute [Section 39-22-522, C.R.S.] has allowed landowners to claim a state income tax credit for the same purpose. The state conservation easement tax credit is available to Colorado residents, C corporations, trusts, estates, and members of pass-through entities, such as partnerships, S corporations, and limited liability companies [Section 39-22-522(1), C.R.S.]. Regardless of whether a landowner receives a federal or state tax credit for a conservation

5

RE

POR

T O

F TH

E C

OL

OR

AD

O ST

AT

E A

UD

ITO

R

easement, the property remains on the local tax rolls for property tax purposes. To claim a state conservation easement tax credit, a landowner’s donation of a conservation easement must meet general federal requirements for a charitable contribution, plus specific requirements for a qualified conservation contribution, as described below:

CONSERVATION PURPOSE. State statute [Section 39-22-522(2), C.R.S.]

requires the conservation easement to be donated exclusively for one or more of the following conservation purposes outlined in federal statute [26 USC 170(h)(4)]:

Outdoor recreation or education for the general public. Protection of a relatively natural habitat or ecosystem. Preservation of open space (including farmland and forests) where

there is significant public benefit, and preservation is either for the general public’s scenic enjoyment or pursuant to a federal, state, or local governmental conservation policy.

Preservation of a historically important area or structure.

According to federal regulations [26 C.F.R. 1.170A-14(e)], the deed of conservation easement must prohibit uses of the land that are inconsistent with the established conservation purpose. For example, in Colorado a donated conservation easement would not qualify for the state tax credit if the easement purpose were to protect habitat for a threatened bird species but the easement deed did not prevent the landowner from using insect pesticides that would eliminate the species’ natural food source.

PERPETUITY OF RESTRICTIONS. The deed of conservation easement must ensure that the restrictions remain on the property forever, thereby creating a perpetual legal and financial obligation for current and future landowners to maintain the property in accordance with the easement’s terms and conditions [26 USC 170(h)(5)(a)].

6

CO

NSE

RV

AT

ION

EA

SEM

EN

T T

AX

CR

ED

IT P

RO

GR

AM

, AFT

ER

CH

AN

GE

S IN

201

4, P

ER

FOR

MA

NC

E A

UD

IT –

NO

VE

MB

ER

201

6

QUALIFIED EASEMENT HOLDER. The conservation easement must be donated to a qualified organization [26 USC 170(h)(3)]. State statute [Section 38-30.5-104(2), C.R.S.] requires the holder of a conservation easement to be a governmental entity or a nonprofit organization that is exempt under section 501(c)(3) of the federal Internal Revenue Code. Additionally, state statute [Section 12-61-724(8), C.R.S.] requires the receiver of the donation to be certified at the time of the donation by Colorado’s Department of Regulatory Agencies (Department), Division of Real Estate (Division). This certification is intended, in part, to ensure that the conservation easement holder has the resources and commitment to protect the conservation purposes of the donation. State statute [Section 12-61-724(1)(b), C.R.S.] requires the easement holder to assume stewardship responsibilities to ensure that the landowner abides by the easement’s terms and conditions.

QUALIFIED APPRAISAL AND APPRAISER. The amount of money that a landowner can claim as a tax credit for a conservation easement donation is based on the fair market value of the donation, as established by a qualified appraiser in a qualified appraisal [26 C.F.R. 1.170A-13(c)(3)(A) and Section 39-22-522(4)(a)(II.5), C.R.S.]. Federal regulations require the qualified appraisal for the conservation easement donation to be completed no more than 60 days prior to the donation and not later than the filing of the income tax return for the year of the donation [26 C.F.R. 1.170A-13(c)(3)(A)].

In Colorado, any individual who performs a conservation easement appraisal must be licensed as a certified general appraiser and comply with all state licensure and continuing education requirements established by the Board of Real Estate Appraisers (BOREA) [4 C.C.R., 725-4(4.1)(E)(1)]. The appraisal must be credible and performed in accordance with Uniform Standards of Professional Appraisal Practice (USPAP), which is a widely recognized industry standard [Section 12-61-727 (2)(a)(II), C.R.S.]. Further, conservation easement appraisers must complete a conservation easement update course every year [4 C.C.R., 725-2(6) and (7)].

7

RE

POR

T O

F TH

E C

OL

OR

AD

O ST

AT

E A

UD

ITO

R

CLAIMING AND USING TAX CREDITS

To claim a tax credit for a conservation easement donation, a landowner must first apply for a tax credit certificate from the Division. Once the application is approved, the Division issues a tax credit certificate that specifies a particular amount that the landowner can claim for a particular tax year. A “tax year” is the 12-month period covered by a particular tax return; for individuals, the tax year runs on a calendar year—January 1 to December 31. After receiving the tax credit certificate from the Division, the landowner must then submit the certificate to the Department of Revenue with a state income tax return for the year specified to claim the credit. If the landowner receives the tax credit certificate from the Division after the filing deadline for the tax year specified, the landowner may have to submit an amended return to claim the credit.

Unlike most other tax credits, a conservation easement tax credit does not have to be used by the taxpayer claiming the credit within the same tax year. Thus, it is important to distinguish between claiming the credit and using the credit. Landowners can claim a conservation easement tax credit for a donation made within that tax year and can claim only one donation per tax year [Section 39-22-522(6)(b), C.R.S.]. The landowner can use the credit to offset taxes owed during the year of the donation. If the value of the tax credit is greater than the landowner’s state income tax liability for the tax year in which the conservation easement is donated, the remaining value of the credit can be carried forward and used against income tax liabilities in each of the 20 succeeding tax years. The credit cannot be applied to tax years prior to the donation.

Colorado’s conservation easement tax credits are also transferable [Section 39-22-522(7), C.R.S.], meaning that after claiming a tax credit, landowners may sell the right to use the credit to another taxpayer, known as a transferee, for offsetting his or her income taxes. This option has generated an ancillary industry of “tax credit brokers” whom landowners hire to facilitate the sale of conservation easement tax credits to transferees for amounts that are less than their full value.

8

CO

NSE

RV

AT

ION

EA

SEM

EN

T T

AX

CR

ED

IT P

RO

GR

AM

, AFT

ER

CH

AN

GE

S IN

201

4, P

ER

FOR

MA

NC

E A

UD

IT –

NO

VE

MB

ER

201

6

TAX CREDIT CERTIFICATES ISSUED

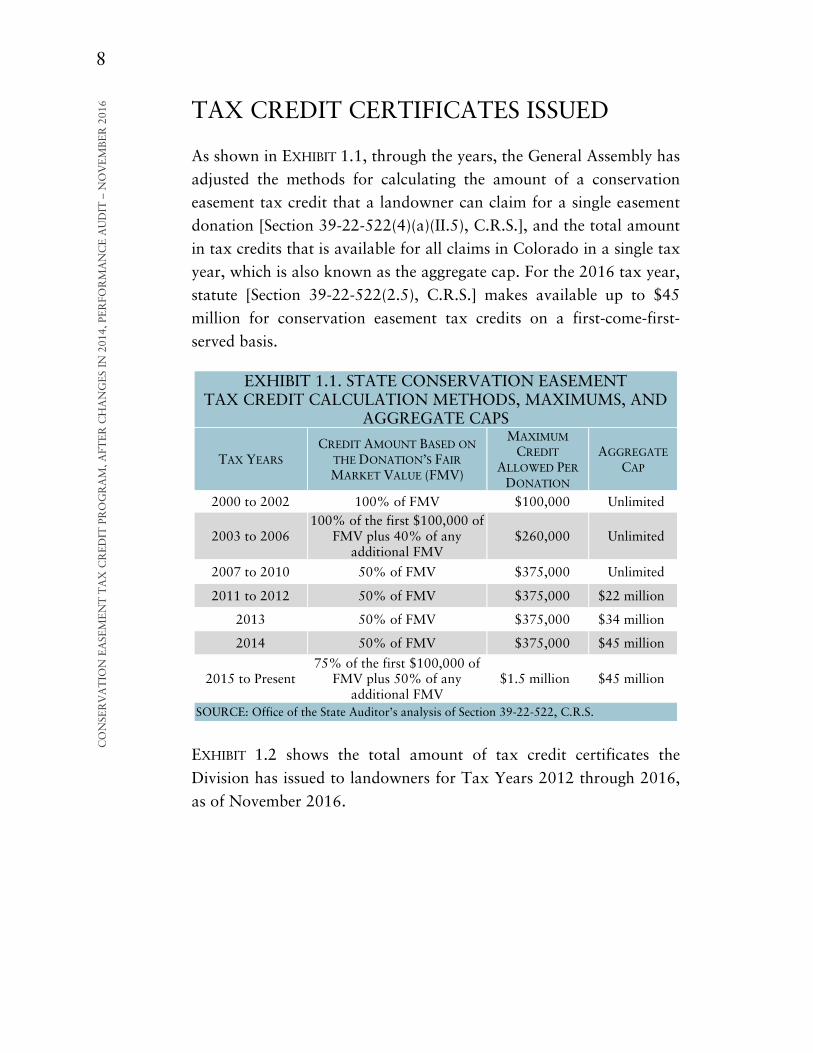

As shown in EXHIBIT 1.1, through the years, the General Assembly has adjusted the methods for calculating the amount of a conservation easement tax credit that a landowner can claim for a single easement donation [Section 39-22-522(4)(a)(II.5), C.R.S.], and the total amount in tax credits that is available for all claims in Colorado in a single tax year, which is also known as the aggregate cap. For the 2016 tax year, statute [Section 39-22-522(2.5), C.R.S.] makes available up to $45 million for conservation easement tax credits on a first-come-first-served basis.

EXHIBIT 1.1. STATE CONSERVATION EASEMENT TAX CREDIT CALCULATION METHODS, MAXIMUMS, AND

AGGREGATE CAPS

TAX YEARS CREDIT AMOUNT BASED ON

THE DONATION’S FAIR MARKET VALUE (FMV)

MAXIMUM CREDIT

ALLOWED PER DONATION

AGGREGATE CAP

2000 to 2002 100% of FMV $100,000 Unlimited

2003 to 2006 100% of the first $100,000 of

FMV plus 40% of any additional FMV

$260,000 Unlimited

2007 to 2010 50% of FMV $375,000 Unlimited

2011 to 2012 50% of FMV $375,000 $22 million

2013 50% of FMV $375,000 $34 million

2014 50% of FMV $375,000 $45 million

2015 to Present 75% of the first $100,000 of

FMV plus 50% of any additional FMV

$1.5 million $45 million

SOURCE: Office of the State Auditor’s analysis of Section 39-22-522, C.R.S.

EXHIBIT 1.2 shows the total amount of tax credit certificates the Division has issued to landowners for Tax Years 2012 through 2016, as of November 2016.

9

RE

POR

T O

F TH

E C

OL

OR

AD

O ST

AT

E A

UD

ITO

R

EXHIBIT 1.2. STATE CONSERVATION EASEMENT

TAX CREDIT CERTIFICATES ISSUED (IN MILLIONS) TAX YEARS 2012 THROUGH 20161

2012 2013 2014 2015 2016

Amount of Tax Credit Certificates Issued

$22.0 $28.2 $11.62 $5.32 $1.92

SOURCE: The Division of Real Estate’s website. 1 As of November 2016. 2 Additional credits may be issued for 2014, 2015, and 2016 because the Division was still reviewing applications for these tax years in September 2016.

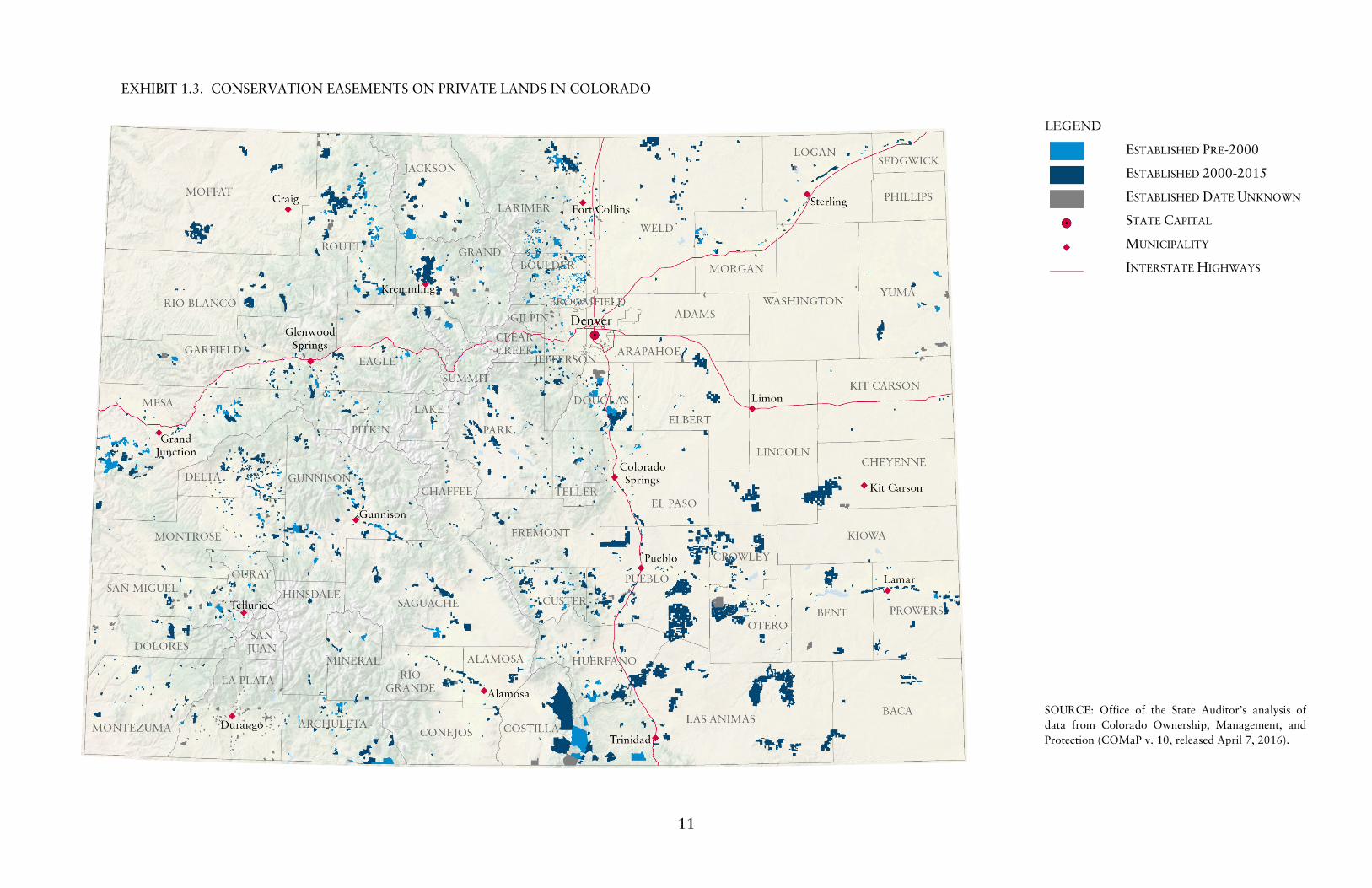

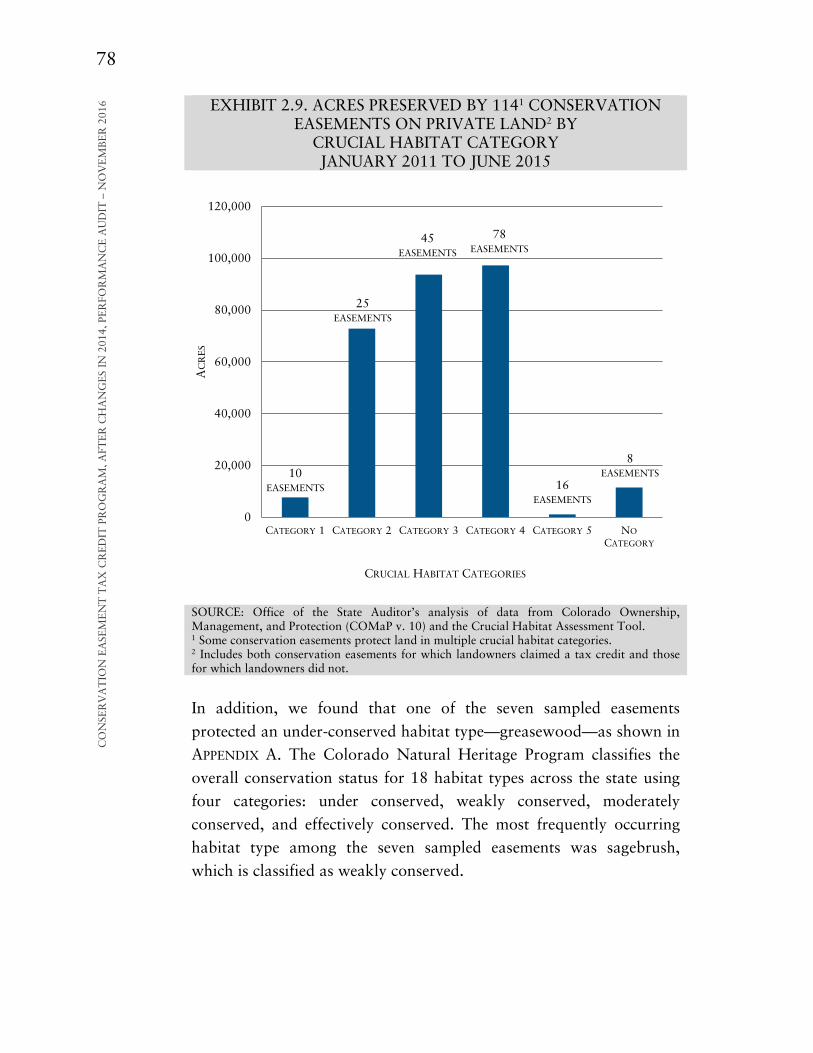

Between January 2000, when the tax credit was created, and September 2016, landowners claimed or were approved to claim $965 million in state tax credits on over 4,200 conservation easement donations, covering more than 1.7 million acres. EXHIBIT 1.3 shows conservation easements on private lands in Colorado, including easements that garnered the tax credit and those that did not, as of June 2015, according to the most current data available from the Colorado Ownership, Management, and Protection (COMaP) service, which is a resource sponsored by Colorado State University that maps all protected lands in the state. The map in EXHIBIT 1.3 is segmented to show easements established before 2000 and those established after 2000, when the conservation easement tax credit was created.

11

LEGEND

ESTABLISHED PRE-2000

ESTABLISHED 2000-2015

ESTABLISHED DATE UNKNOWN

STATE CAPITAL

MUNICIPALITY

INTERSTATE HIGHWAYS

EXHIBIT 1.3. CONSERVATION EASEMENTS ON PRIVATE LANDS IN COLORADO

SOURCE: Office of the State Auditor’s analysis of data from Colorado Ownership, Management, and Protection (COMaP v. 10, released April 7, 2016).

13

RE

POR

T O

F TH

E C

OL

OR

AD

O ST

AT

E A

UD

ITO

R

ADMINISTRATION

The Division is primarily responsible for administering Colorado’s Conservation Easement Tax Credit Program (Program), although other state agencies and entities have responsibilities related to conservation easement donations and tax credits, as described below.

DIVISION OF REAL ESTATE. The Division receives and reviews applications for conservation easement tax credits to determine whether (1) the conservation easement is a qualified conservation contribution with a conservation purpose that is recognized by state and federal law and (2) the appraisal is credible and complies with state and federal requirements [Sections 12-61-727(3)(a) and (b), C.R.S.]. After reviewing an application and determining that the easement is qualified under state and federal law and the appraisal is credible, the Division issues a tax credit certificate to the landowner, which entitles the landowner to claim the credit on a state income tax return. The Division also oversees the total aggregate cap for the tax credit. In addition, the Division, in consultation with the Conservation Easement Oversight Commission (Commission), issues conservation easement holder certifications to entities, such as land trusts, that want to receive conservation easement donations that will be used for the tax credit. The Division is also responsible for regulating real estate professionals doing business in Colorado, including real estate appraisers, real estate brokers, and mortgage loan originators. The Division works with BOREA, the Real Estate Commission, and the Board of Mortgage Loan Originators to administer licensing and continuing education requirements, investigate complaints, and take disciplinary action against licensees for noncompliance with applicable requirements.

CONSERVATION EASEMENT OVERSIGHT COMMISSION. The Commission

is a Type 2, nine-member commission that makes the final determination about whether a donated conservation easement is a qualified charitable contribution, as defined by the federal Internal

14

CO

NSE

RV

AT

ION

EA

SEM

EN

T T

AX

CR

ED

IT P

RO

GR

AM

, AFT

ER

CH

AN

GE

S IN

201

4, P

ER

FOR

MA

NC

E A

UD

IT –

NO

VE

MB

ER

201

6

Revenue Code, and therefore qualifies for the state tax credit. The Commission also advises the Division about whether to certify conservation easement holders. The Commission members represent a number of different stakeholder interests. By statute [Section 12-61-725(1), C.R.S.], the Great Outdoors Colorado Trust Fund, Department of Agriculture, and Department of Natural Resources each have a permanent member on the Commission, and the Governor appoints the remaining six members for 3-year terms. The six gubernatorial appointments must represent (1) a land trust, (2) a local government agency concerned with open space or land conservation, (3) a land trust or a local government agency concerned with open space or land conservation, (4) an individual who is competent and qualified to analyze the conservation purpose of conservation easements, (5) a certified general appraiser with conservation easement appraisal experience, and (6) a landowner who has donated a conservation easement in Colorado. No more than three of the Governor’s appointees serving at the same time may be from the same political party.

BOARD OF REAL ESTATE APPRAISERS. BOREA is a Type 1, seven-member board that establishes rules regarding licensure, continuing education, and experience requirements for real estate appraisers in Colorado. BOREA also reviews complaints against certified general appraisers who accept a conservation easement appraisal assignment and has the power to take disciplinary action, including revocation of licensure and fines. BOREA’s membership comprises three licensed appraisers, one county assessor, one banker with experience in mortgage lending, one representative of an appraisal management company, and one member of the general public. All members are appointed by the Governor with confirmation by the State Senate for 3-year terms.

DEPARTMENT OF REVENUE. As the State’s tax authority, the Department of Revenue is responsible for administration, collection, audit, enforcement, and other activities pertaining to Colorado’s tax laws. The Department of Revenue’s Taxpayer Service Division is

15

RE

POR

T O

F TH

E C

OL

OR

AD

O ST

AT

E A

UD

ITO

R

responsible for processing tax filings, including all conservation easement tax credit claims. For credits claimed on or after January 1, 2014, the Department of Revenue’s responsibility includes such tax compliance matters as ensuring the individual or entity claiming a credit is a Colorado resident with income tax liabilities, that the full value of the credit has not already been used, and that the credit is not being claimed for multiple donations [Section 39-22-522(3.6)(b), C.R.S.]. The Department of Revenue is authorized to disallow a conservation easement tax credit that does not meet these requirements but is not authorized to disallow a claim based on the requirements under the jurisdiction of the Division and Commission. When the Department of Revenue disallows the use of a credit, statute [Sections 39-22-522.5(2) and (6), C.R.S.] provides taxpayers a process to protest the disallowance in an administrative hearing or bypass the hearing and protest in district court.

MAJOR PROGRAM CHANGES

The Program has undergone the following major changes:

2000: The conservation easement tax credit is created for

landowners donating conservation easements to qualified organizations. The Department of Revenue is solely responsible for determining whether tax credit claims meet the State’s statutory requirements. The General Assembly also makes the tax credit transferrable to other taxpayers through passage of House Bill 00-1348.

2008: Due to abuses of the Program, largely associated with

appraisals, the General Assembly passes House Bill 08-1353, which vests the Division with responsibility for reviewing appraisals of conservation easements for which tax credits will be claimed. The legislation also requires any entity wishing to receive conservation easement donations that will be used to claim a state tax credit to become certified by the Division. Finally, the legislation creates the Commission to advise the Division on whether to approve applications for holder certification and advise

16

CO

NSE

RV

AT

ION

EA

SEM

EN

T T

AX

CR

ED

IT P

RO

GR

AM

, AFT

ER

CH

AN

GE

S IN

201

4, P

ER

FOR

MA

NC

E A

UD

IT –

NO

VE

MB

ER

201

6

the Department of Revenue on whether conservation easement donations meet federal and state requirements. The Department of Revenue retains final authority for allowing or disallowing claims for the conservation easement tax credit. The Commission’s advisory role vis-à-vis the Department of Revenue continued for tax credits claimed on conservation easement donations made through 2013 but was replaced by the application review process that was created by Senate Bill 13-221 for donations made on or after January 1, 2014.

2011: The total amount of money available for conservation

easements is capped for each calendar year, following passage of House Bill 10-1197. The Division is vested with responsibility for managing the cap.

2014: Following passage of Senate Bill 13-221, which addressed the audit recommendations from the Office of the State Auditor’s 2012 performance audit of the Program, the Program is restructured, making the Division and Commission responsible for reviewing and approving applications for tax credits and the Department of Revenue responsible for ensuring compliance with all other tax laws related to the claim or use of tax credits. As a result of this change, tax credit claims are certified by the Division and Commission before the taxpayer files a tax return. Senate Bill 13-221 also creates an option for landowners to request a preliminary advisory opinion from the Commission and the Division on an easement’s conservation purpose and the appraisal’s credibility prior to completing a donation transaction and recording the easement [Section 12-61-727(14), C.R.S.].

PROGRAM FUNDING

For Fiscal Years 2014 through 2017, the Division was appropriated 5.8 full-time equivalent (FTE) staff to administer the Program—3.5 FTEs were for reviews of applications for tax credit certificates and preliminary advisory opinions and 1.3 FTEs were for administering the holder certification process.

17

RE

POR

T O

F TH

E C

OL

OR

AD

O ST

AT

E A

UD

ITO

R

The Division’s and Commission’s administration of the Program is entirely cash funded by application fee revenues from landowners applying for conservation easement tax credits or preliminary advisory opinions, and from entities applying to become certified conservation easement holders. Our audit did not review the Division’s processes or funding for certifying easement holders. For the application review function, the Division has collected, on average, about $205,000 in fees each year and expended an average of about $201,000 each year. We discuss the Division’s fees and funding for this function in detail in CHAPTER 2.

AUDIT PURPOSE, SCOPE, AND METHODOLOGY

We conducted this audit pursuant to Section 2-3-103, C.R.S., which authorizes the State Auditor to conduct audits of all departments, institutions, and agencies of state government, and Section 2-7-204(5), C.R.S., the State Measurement for Accountable, Responsive, and Transparent Government (SMART) Act. This audit was conducted in response to a request from the former Executive Director of the Department of Regulatory Agencies. We appreciate the assistance provided by the management and staff of the Department of Regulatory Agencies and Division of Real Estate during this audit. The key objective of the audit was to evaluate Program operations and the effectiveness of Division and Commission processes since the structural changes included in Senate Bill 13-221 took effect in January 2014. The audit also reviewed the extent to which the Division’s processes and changes addressed the concerns in our 2012 performance audit of the Program. This audit did not review the Department of Revenue’s processes, conservation easement donations made prior to January 2014, or processes for certifying conservation easement holders. We performed our audit fieldwork from March to September 2016.

18

CO

NSE

RV

AT

ION

EA

SEM

EN

T T

AX

CR

ED

IT P

RO

GR

AM

, AFT

ER

CH

AN

GE

S IN

201

4, P

ER

FOR

MA

NC

E A

UD

IT –

NO

VE

MB

ER

201

6

We conducted this performance audit in accordance with generally accepted government auditing standards. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions based on our audit objectives. We believe that the evidence obtained provides a reasonable basis for our findings and conclusions based on our audit objectives.

To accomplish the audit objective, we performed the following audit work:

Analyzed Division electronic data and documentation on

conservation easement tax credit certificate applications and preliminary advisory opinion applications.

Examined Program fee collection and revenue and expenditure

data from the Colorado Financial Reporting System (COFRS) and Colorado Operations Resource Engine (CORE).

Reviewed various sources of information related to land conservation in Colorado, including the Division’s most recent annual report for the Program; Colorado Ownership, Management, and Protection (COMaP); the Colorado Department of Natural Resources’ 2015 edition of the State Wildlife Action

Plan; the Trust for Public Land’s 2009 report, A Return on Investment: The Economic Value of Colorado’s Conservation

Easements; and the Colorado Natural Heritage Program’s 2011 report, The State of Colorado’s Biodiversity.

Interviewed management and staff of the Department of Regulatory Agencies and the nine members of the Commission, and communicated with members of the land conservation community regarding their experiences working with the Division and Commission.

We relied on sampling to support some of our audit work. Specifically, we selected a random sample of 10 of the 62 conservation

19

RE

POR

T O

F TH

E C

OL

OR

AD

O ST

AT

E A

UD

ITO

R

easements for which landowners had received a tax credit certificate, a deficiency letter, or an opinion between January 2014 and March 2016. We designed our sample to provide sufficient and appropriate evidence for the purpose of evaluating Division and Commission application review processes. We planned our audit work to assess the effectiveness of those internal controls that were significant to our audit objectives. Our conclusions on the effectiveness of those controls, as well as specific details about the audit work supporting our findings, conclusions, and recommendations, are described in CHAPTER 2 of this report.

CHAPTER 2 ADMINISTRATION OF

CONSERVATION EASEMENT TAX CREDITS

Since the State established the conservation easement tax credit in 2000, Colorado has witnessed a marked increase in the conservation of privately owned lands. To date, the State has assisted landowners in protecting over 4,200 parcels of land by allowing them to claim about $965 million in tax credits through the State’s Conservation Easement Tax Credit Program (Program).

22

CO

NSE

RV

AT

ION

EA

SEM

EN

T T

AX

CR

ED

IT P

RO

GR

AM

, AFT

ER

CH

AN

GE

S IN

201

4, P

ER

FOR

MA

NC

E A

UD

IT –

NO

VE

MB

ER

201

6 Given the amount of tax revenue the State has forgone and will forgo through conservation easement tax credits, it is important that the Program operates effectively, efficiently, and according to statutory intent. For example, as outlined in Section 12-61-727, C.R.S., the Division of Real Estate (Division) must process each application for a conservation easement tax credit in a timely manner, ensure the appraisal supporting the landowner’s requested tax credit amount is credible, and ensure its overall administration of the Program is fiscally sound and transparent. In addition, the Division and the Conservation Easement Oversight Commission (Commission) must ensure each conservation easement donation has a conservation purpose in compliance with federal and state requirements. Overall, we found that the Division has procedures and internal controls in place to ensure that appraisals accompanying tax credit applications are credible, that the conservation easement donation has a qualifying conservation purpose, and that Commissioners and Program staff avoid conflicts of interest when making decisions regarding appraisal credibility and conservation purpose of easement donations. Specifically:

The Division has implemented processes intended to ensure that appraisals are reviewed in a consistent manner using relevant criteria and that appraisers are referred to the Board of Real Estate Appraisers (BOREA) for investigation when significant issues with appraisal credibility are identified. Our audit work indicated that these processes were working as intended.

The Division has implemented controls intended to ensure that Program staff possess appropriate qualifications, education, and experience to review conservation easement applications for compliance with federal and state requirements for the tax credit. Our audit work indicated that these controls were working as intended.

The Division has implemented controls intended to ensure Program staff and members of the Commission abide by

23

RE

POR

T O

F TH

E C

OL

OR

AD

O ST

AT

E A

UD

ITO

R

Department policies and state regulations to avoid possible conflicts of interest. Specifically, all Program staff and Commission members annually sign agreements to disclose conflicts of interest and recuse themselves from tax credit certificate application reviews, discussions, and votes when they have a real or perceived conflict of interest regarding specific applications. Our audit work indicated that these controls are working as intended.

We also identified areas where the Division should improve Program operations related to the timeliness of its application reviews, accounting and fiscal management of the placeholder certificate process, fee setting and cash fund management, communication of its appraisal review standards to appraisers, and public reporting of Program information. Further, we identified matters for policymakers to consider regarding the role and authority of the Commission. The remainder of CHAPTER 2 describes these findings and our recommendations.

TIMELINESS OF APPLICATION REVIEWS A landowner seeking a Colorado conservation easement tax credit certificate begins the process by submitting to the Division an application for either a tax credit certificate or a preliminary advisory opinion on whether a potential easement donation may qualify for a tax credit. The Division reviews submitted applications to determine whether the landowner’s conservation easement donation, or proposed donation, has a conservation purpose that qualifies for the tax credit and whether the conservation easement appraisal is credible. In order for the Division to consider a tax credit certificate application complete, statute [Section 12-61-727(5), C.R.S.] requires that the application include documentation supporting the conservation purpose of the easement and an appraisal of the easement’s value, among other information. The Division requires applications for preliminary advisory opinions to include similar documentation. If the

24

CO

NSE

RV

AT

ION

EA

SEM

EN

T T

AX

CR

ED

IT P

RO

GR

AM

, AFT

ER

CH

AN

GE

S IN

201

4, P

ER

FOR

MA

NC

E A

UD

IT –

NO

VE

MB

ER

201

6 Division does not receive a complete application, it communicates with the landowner and appraiser, as appropriate, to obtain the information needed to make the application complete. Upon receipt of an application with all required supporting documentation, Division staff send the landowner a letter stating that the application is deemed complete. Division staff track each application in an electronic database and review completed applications in the order received using checklists to assess whether each potential easement donation meets applicable state and federal requirements for conservation purpose and appraisal credibility. Staff note on the checklists any problems they have identified with an application. Once staff complete their review of the application, they write two detailed reports summarizing their analyses—one on the conservation purpose of the easement and one on the appraisal. In each report, staff note any significant deficiencies or problems that they have identified. Staff also prepare 1-page summaries of each report in which they recommend: (1) full approval or a favorable opinion, (2) denial or a nonfavorable opinion, (3) approval or a favorable opinion if certain conditions are met, or (4) issuance of a deficiency letter to the landowner explaining the deficiencies identified. The Commission has final authority for deciding whether the conservation purpose of an easement donation meets the qualifications for a state tax credit, and it has delegated its approval authority to the Division whenever staff identify no problems related to a donation’s or proposed donation’s conservation purpose. Thus, if Division staff identify no problems with an application, the Division issues a tax credit certificate, or a favorable preliminary advisory opinion, which indicates that if the landowner applies for the tax credit, the Division has not identified a reason to deny it. When Division staff identify problems with an application, either the Commission or the Division Director reviews the problems and decides what action to take. For problems with the conservation purpose of a donation, such as undefined building envelopes (areas

25

RE

POR

T O

F TH

E C

OL

OR

AD

O ST

AT

E A

UD

ITO

R

where building can occur within an easement) that could undermine the conservation values present on the property, Division staff send the application and their conservation purpose checklist, report, summary, and recommendations to the Commission. The Commission reviews the materials provided by staff and votes on whether to approve the tax credit certificate, have the Division staff issue a deficiency letter to the landowner, or issue a favorable or nonfavorable preliminary advisory opinion. For problems with appraisals, the Division Director reviews the Division staff’s checklists, reports, summaries, and recommendations and makes the final decision regarding appraisal credibility. When staff identify significant problems with the appraisal, such as inadequate support for the conclusions in the appraisal, the Division Director may send the landowner a deficiency letter explaining the problems, ask the landowner to obtain a second appraisal (for tax credit certificate applications), or issue a nonfavorable opinion (for preliminary advisory opinion applications). If the landowner resolves all problems related to a tax credit certificate application to the satisfaction of the Commission and Division Director, the Division sends the landowner a tax credit certificate, and if not, the Division sends the landowner a letter of denial. During the period we reviewed, January 2014 through June 2016, the Division received a total of 71 complete conservation easement tax credit applications and 65 complete preliminary advisory opinion applications.

WHAT AUDIT WORK WAS PERFORMED, WHAT WAS THE PURPOSE, AND HOW WERE THE RESULTS OF THE WORK MEASURED?

We analyzed information on the time it took between the Division’s receipt of a complete application to its issuance of a tax credit certificate or an opinion, for the 71 complete tax credit certificate

26

CO

NSE

RV

AT

ION

EA

SEM

EN

T T

AX

CR

ED

IT P

RO

GR

AM

, AFT

ER

CH

AN

GE

S IN

201

4, P

ER

FOR

MA

NC

E A

UD

IT –

NO

VE

MB

ER

201

6 applications and 65 complete preliminary advisory opinion applications the Division received from January 2014 through June 2016 (the audit period). We examined the Division’s application file documentation and electronic data for a random sample of 10 of the 62 conservation easements for which landowners had received a tax credit certificate, deficiency letter, or opinion as of March 2016. The sample included seven tax credit applications and seven preliminary advisory opinion applications that landowners submitted for these 10 easements. We also listened to recorded audio of Commission meetings and reviewed meeting minutes, interviewed the nine Commissioners, and obtained anecdotal information about the review process from members of the land conservation community. Additionally, we conducted a survey of 96 landowners who had applied for conservation easement tax credit certificates or preliminary advisory opinions during the audit period and received responses from 58 landowners (60 percent). The purpose of the audit work was to determine whether the Division reviews applications for tax credit certificates and preliminary advisory opinions, and issues decisions, in accordance with the time frames established in statute and rule. Although statute and rules do not establish a firm deadline for the Division’s overall review process, they do specify the average time in which reviews should be made, as well as deadlines for the applicant’s responses and the Division’s final decisions. These timeframes and deadlines are as follows:

120 DAYS, ON AVERAGE, FOR THE DIVISION’S INITIAL REVIEW. Statute states that the Division shall either approve an application and issue a tax credit certificate to the landowner, or mail a letter to the landowner documenting potential deficiencies in the application, within an average of 120 days from the date a completed application is received [Sections 12-61-727(7)(a) and (10), C.R.S.]. Division rules further require the Division to review applications for preliminary advisory opinions and issue either a favorable or nonfavorable opinion within an average of 120 days [4 C.C.R., 725-4(4.4)(G)]. According to the Division, statute establishes an average time frame, and not a firm deadline, because

27

RE

POR

T O

F TH

E C

OL

OR

AD

O ST

AT

E A

UD

ITO

R

some applications are complex and require extensive Division review.

60 DAYS FOR THE APPLICANT’S RESPONSE PERIOD. In cases where the Division or the Commission has identified potential deficiencies in an application for a tax credit certificate, statute specifies that the landowner applicant has 60 days after the mailing date of the Division’s letter to address the potential deficiencies identified and provide the Division with additional information or documentation that the Division deems necessary to make a final determination regarding the application [Section 12-61-727(7)(b), C.R.S.].

90 DAYS FOR THE DIVISION’S SECONDARY REVIEW. Statute specifies that, once the landowner submits additional information to address the deficiencies noted in the Division’s letter, the Division has 90 days to review it and make a final determination regarding the application [Section 12-61-727(7)(c), C.R.S.].

Statute states that the prescribed deadlines “may be extended upon mutual agreement between the [Division] Director and the Commission and the landowner” [Section 12-61-727(7)(d), C.R.S.].

WHAT PROBLEM DID THE AUDIT WORK IDENTIFY?

We found that the Division’s reviews of completed applications for tax credit certificates and preliminary advisory opinions were often not timely.

UNTIMELY INITIAL REVIEWS

TAX CREDIT CERTIFICATE APPLICATIONS. We found that the Division exceeded the 120-day statutory limit for the average time spent on initial reviews of tax credit certificate applications that the Division received since January 2015, spending an average of 133 days for

28

CO

NSE

RV

AT

ION

EA

SEM

EN

T T

AX

CR

ED

IT P

RO

GR

AM

, AFT

ER

CH

AN

GE

S IN

201

4, P

ER

FOR

MA

NC

E A

UD

IT –

NO

VE

MB

ER

201

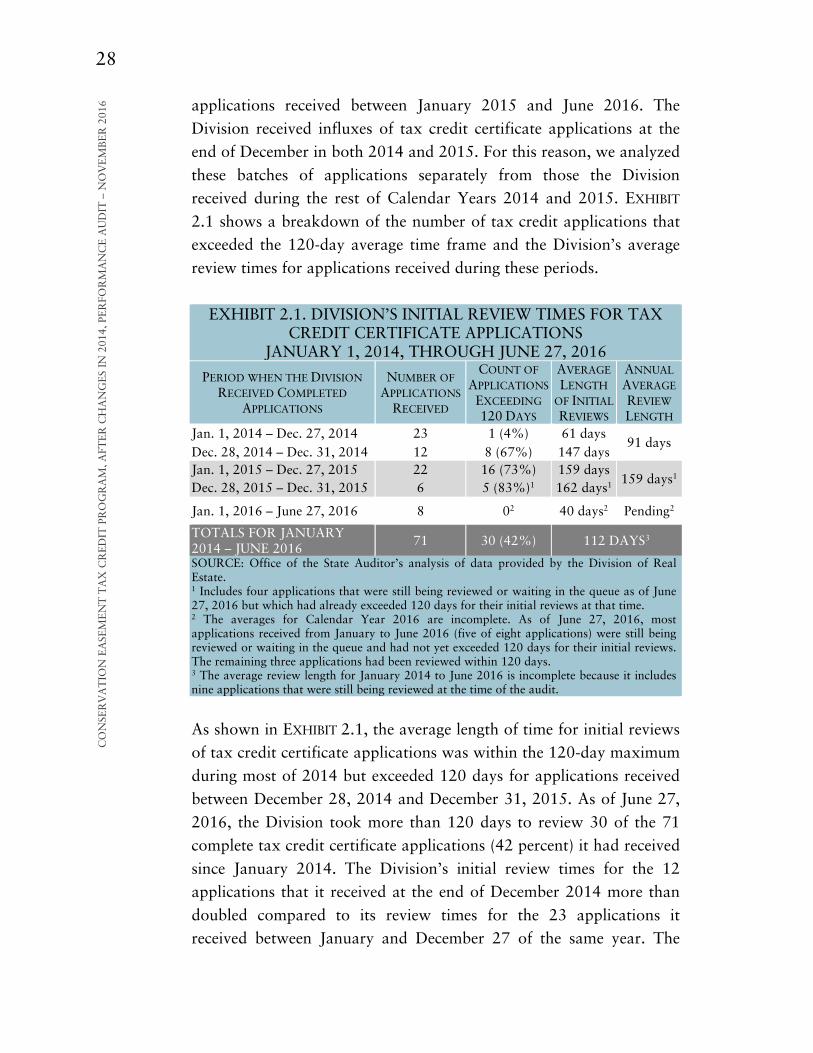

6 applications received between January 2015 and June 2016. The Division received influxes of tax credit certificate applications at the end of December in both 2014 and 2015. For this reason, we analyzed these batches of applications separately from those the Division received during the rest of Calendar Years 2014 and 2015. EXHIBIT 2.1 shows a breakdown of the number of tax credit applications that exceeded the 120-day average time frame and the Division’s average review times for applications received during these periods.

EXHIBIT 2.1. DIVISION’S INITIAL REVIEW TIMES FOR TAX CREDIT CERTIFICATE APPLICATIONS

JANUARY 1, 2014, THROUGH JUNE 27, 2016

PERIOD WHEN THE DIVISION RECEIVED COMPLETED

APPLICATIONS

NUMBER OF APPLICATIONS

RECEIVED

COUNT OF APPLICATIONS EXCEEDING 120 DAYS

AVERAGE LENGTH

OF INITIAL REVIEWS

ANNUAL AVERAGE REVIEW LENGTH

Jan. 1, 2014 – Dec. 27, 2014 23 1 (4%) 61 days 91 days

Dec. 28, 2014 – Dec. 31, 2014 12 8 (67%) 147 days Jan. 1, 2015 – Dec. 27, 2015 22 16 (73%) 159 days

159 days1 Dec. 28, 2015 – Dec. 31, 2015 6 5 (83%)1 162 days1

Jan. 1, 2016 – June 27, 2016 8 02 40 days2 Pending2

TOTALS FOR JANUARY 2014 – JUNE 2016

71 30 (42%) 112 DAYS3

SOURCE: Office of the State Auditor’s analysis of data provided by the Division of Real Estate. 1 Includes four applications that were still being reviewed or waiting in the queue as of June 27, 2016 but which had already exceeded 120 days for their initial reviews at that time. 2 The averages for Calendar Year 2016 are incomplete. As of June 27, 2016, most applications received from January to June 2016 (five of eight applications) were still being reviewed or waiting in the queue and had not yet exceeded 120 days for their initial reviews. The remaining three applications had been reviewed within 120 days. 3 The average review length for January 2014 to June 2016 is incomplete because it includes nine applications that were still being reviewed at the time of the audit.

As shown in EXHIBIT 2.1, the average length of time for initial reviews of tax credit certificate applications was within the 120-day maximum during most of 2014 but exceeded 120 days for applications received between December 28, 2014 and December 31, 2015. As of June 27, 2016, the Division took more than 120 days to review 30 of the 71 complete tax credit certificate applications (42 percent) it had received since January 2014. The Division’s initial review times for the 12 applications that it received at the end of December 2014 more than doubled compared to its review times for the 23 applications it received between January and December 27 of the same year. The

29

RE

POR

T O

F TH

E C

OL

OR

AD

O ST

AT

E A

UD

ITO

R

Division’s longest initial review took 274 days, from February to November 2015. As of June 2016, the Division had not completed its initial review for five of the eight applications that it had received since January 2016, and therefore, it was too early to determine whether the Division’s average review times for these applications would follow past trends.

PRELIMINARY ADVISORY OPINIONS. We found that the Division spent an average of 124 days on initial reviews of applications for preliminary advisory opinions received between January 1, 2014 and June 27, 2016, which exceeds the 120-day average time frame set in rule. EXHIBIT 2.2 shows the number of preliminary advisory opinion applications for which the Division initial review times exceeded 120 days and the average length of initial reviews for applications received during three time periods. As of the end of our fieldwork in June 2016, the Division had not completed its initial review of the 17 applications that it had received since November 1, 2015, and therefore, EXHIBIT 2.2 breaks out these applications separately.

EXHIBIT 2.2. DIVISION’S INITIAL REVIEW TIMES FOR PRELIMINARY ADVISORY OPINION APPLICATIONS

JANUARY 1, 2014, THROUGH JUNE 27, 2016

PERIOD WHEN THE DIVISION RECEIVED COMPLETED

APPLICATIONS

NUMBER OF APPLICATIONS

RECEIVED

COUNT OF APPLICATIONS EXCEEDING 120 DAYS

AVERAGE LENGTH OF

INITIAL REVIEWS

Jan. 1, 2014 – Dec. 31, 2014 26 0 (0%) 51 days

Jan. 1, 2015 – Oct. 31, 2015 22 18 (82%) 168 days

Nov. 1, 2015 – June 27, 2016 17 13 (76%)1 145 days1

TOTALS FOR JANUARY 2014 – JUNE 2016 65 31 124 DAYS

SOURCE: Office of the State Auditor’s analysis of data provided by the Division of Real Estate. 1 As of June 27, 2016, all 17 preliminary advisory opinion applications received since November 2015 were still being reviewed or waiting in the queue, and 13 of these applications had already exceeded 120 days for their initial reviews. The remaining four applications had not yet exceeded 120 days.

As shown in EXHIBIT 2.2, the average length of time for initial reviews of preliminary advisory opinion applications was within 120 days during 2014 but exceeded 120 days for applications received after

30

CO

NSE

RV

AT

ION

EA

SEM

EN

T T

AX

CR

ED

IT P

RO

GR

AM

, AFT

ER

CH

AN

GE

S IN

201

4, P

ER

FOR

MA

NC

E A

UD

IT –

NO

VE

MB

ER

201

6 January 1, 2015. The Division took more than 120 days to issue preliminary advisory opinions on 18 of the 22 preliminary advisory opinion applications (82 percent) that it received between January and October 2015; the Division’s longest review was 282 days during this period. As of June 2016, a total of 13 of the 17 applications that have been pending since November 2015 had already been in the Division’s queue for more than the 120-day maximum set by Division rule.

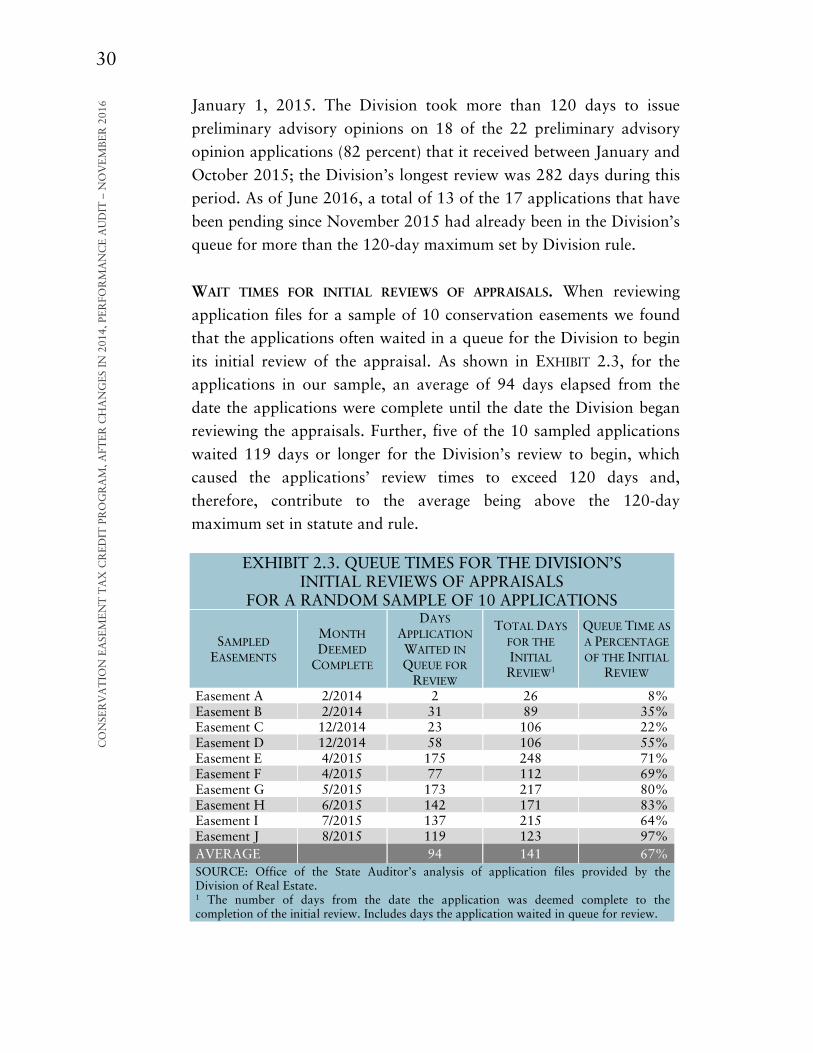

WAIT TIMES FOR INITIAL REVIEWS OF APPRAISALS. When reviewing

application files for a sample of 10 conservation easements we found that the applications often waited in a queue for the Division to begin its initial review of the appraisal. As shown in EXHIBIT 2.3, for the applications in our sample, an average of 94 days elapsed from the date the applications were complete until the date the Division began reviewing the appraisals. Further, five of the 10 sampled applications waited 119 days or longer for the Division’s review to begin, which caused the applications’ review times to exceed 120 days and, therefore, contribute to the average being above the 120-day maximum set in statute and rule.

EXHIBIT 2.3. QUEUE TIMES FOR THE DIVISION’S INITIAL REVIEWS OF APPRAISALS

FOR A RANDOM SAMPLE OF 10 APPLICATIONS

SAMPLED EASEMENTS

MONTH DEEMED

COMPLETE

DAYS APPLICATION WAITED IN QUEUE FOR

REVIEW

TOTAL DAYS FOR THE INITIAL REVIEW1

QUEUE TIME AS A PERCENTAGE OF THE INITIAL

REVIEW

Easement A 2/2014 2 26 8% Easement B 2/2014 31 89 35% Easement C 12/2014 23 106 22% Easement D 12/2014 58 106 55% Easement E 4/2015 175 248 71% Easement F 4/2015 77 112 69% Easement G 5/2015 173 217 80% Easement H 6/2015 142 171 83% Easement I 7/2015 137 215 64% Easement J 8/2015 119 123 97% AVERAGE

94 141 67%

SOURCE: Office of the State Auditor’s analysis of application files provided by the Division of Real Estate. 1 The number of days from the date the application was deemed complete to the completion of the initial review. Includes days the application waited in queue for review.

31

RE

POR

T O

F TH

E C

OL

OR

AD

O ST

AT

E A

UD

ITO

R

Based on our sample review, the initial review period for appraisals would be shorter if applications did not sit in a queue. Once the Division began reviewing these sampled applications, it took from 4 to 83 days, or 48 days on average, to complete the initial reviews.

SECONDARY REVIEWS

We found that the Division exceeded the 90-day time limit for nine of the 19 applications (47 percent) for which it conducted secondary reviews as of September 2016. For all nine that exceeded the 90-day limit, the Division received consent from the landowners to extend the deadlines and so was not out of compliance with statute. Secondary reviews ranged from 29 days to 320 days, with an average of 119 days.

WHY DID THE PROBLEM OCCUR?

Overall, we identified six main reasons for the Division’s untimely application processing for the Conservation Easement Tax Credit Certificate Program, as described below.

LACK OF ANALYSIS TO ENSURE STAFFING ADDRESSES APPLICATION

SURGES. First, we found that the Division has not analyzed staff workload capacity, which is the number of applications staff can process in a given period. Had the Division conducted such analysis, the resulting information could have helped the Division determine whether it needed to adjust staffing levels in response to the surges in tax credit certificate applications it received in December 2014 and December 2015. Although the Division was appropriated 3.5 FTE staff positions for reviewing applications through Senate Bill 13-221, the Division was using only 2.25 FTE staff in January 2015 to review applications, which it does not believe was sufficient to manage the workload. The Division reported to us that it did not hire staff to fill the additional FTE position because revenue from application fees was not sufficient to fund the position. We discuss the Division’s difficulty in setting fees to fully cover costs in the section titled “Fee Setting and Fund Management.”

32

CO

NSE

RV

AT

ION

EA

SEM

EN

T T

AX

CR

ED

IT P

RO

GR

AM

, AFT

ER

CH

AN

GE

S IN

201

4, P

ER

FOR

MA

NC

E A

UD

IT –

NO

VE

MB

ER

201

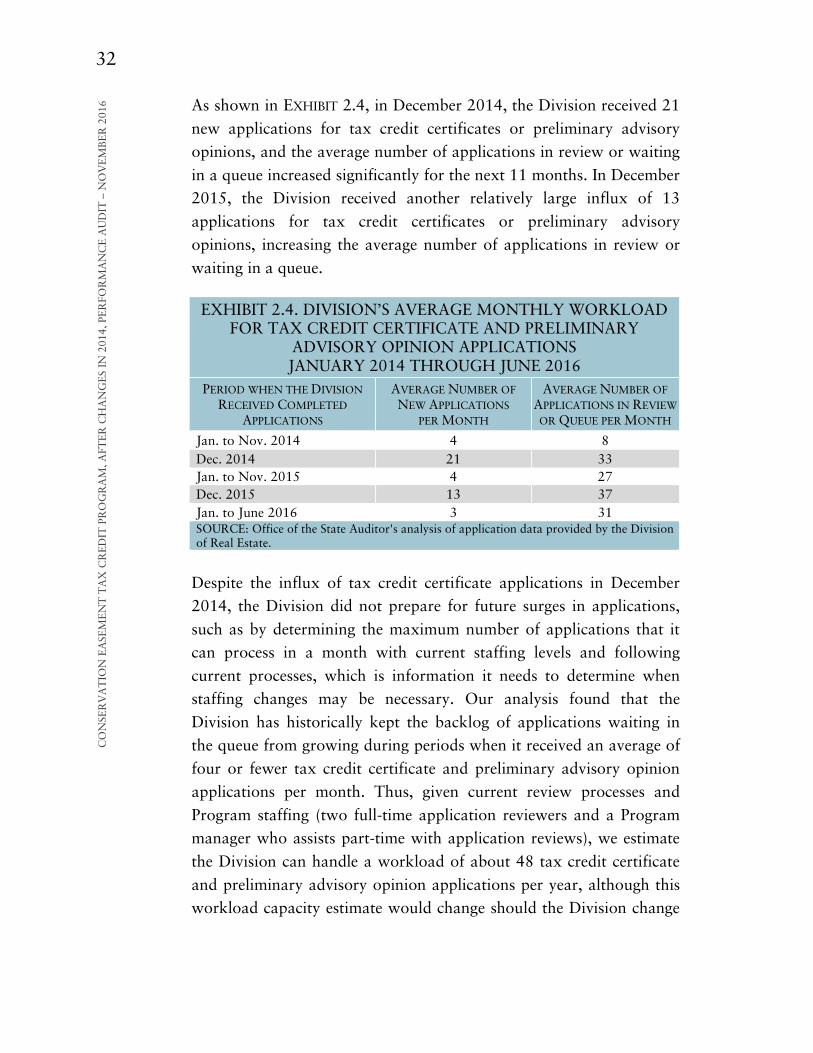

6 As shown in EXHIBIT 2.4, in December 2014, the Division received 21 new applications for tax credit certificates or preliminary advisory opinions, and the average number of applications in review or waiting in a queue increased significantly for the next 11 months. In December 2015, the Division received another relatively large influx of 13 applications for tax credit certificates or preliminary advisory opinions, increasing the average number of applications in review or waiting in a queue.

EXHIBIT 2.4. DIVISION’S AVERAGE MONTHLY WORKLOAD FOR TAX CREDIT CERTIFICATE AND PRELIMINARY

ADVISORY OPINION APPLICATIONS JANUARY 2014 THROUGH JUNE 2016

PERIOD WHEN THE DIVISION RECEIVED COMPLETED

APPLICATIONS

AVERAGE NUMBER OF NEW APPLICATIONS

PER MONTH

AVERAGE NUMBER OF APPLICATIONS IN REVIEW OR QUEUE PER MONTH

Jan. to Nov. 2014 4 8 Dec. 2014 21 33 Jan. to Nov. 2015 4 27 Dec. 2015 13 37 Jan. to June 2016 3 31 SOURCE: Office of the State Auditor's analysis of application data provided by the Division of Real Estate.

Despite the influx of tax credit certificate applications in December 2014, the Division did not prepare for future surges in applications, such as by determining the maximum number of applications that it can process in a month with current staffing levels and following current processes, which is information it needs to determine when staffing changes may be necessary. Our analysis found that the Division has historically kept the backlog of applications waiting in the queue from growing during periods when it received an average of four or fewer tax credit certificate and preliminary advisory opinion applications per month. Thus, given current review processes and Program staffing (two full-time application reviewers and a Program manager who assists part-time with application reviews), we estimate the Division can handle a workload of about 48 tax credit certificate and preliminary advisory opinion applications per year, although this workload capacity estimate would change should the Division change

33

RE

POR

T O

F TH

E C

OL

OR

AD

O ST

AT

E A

UD

ITO

R

its staffing and/or processes. The Division received more than 48 applications in both 2014 and 2015; hence the backlog. Second, although the Division hired part-time external contractors to review applications and manage the backlog for about $21,000 in October 2015, the backlog persisted. We estimate that the addition of one full-time equivalent (FTE) staff for reviewing applications, at the cost of about $77,000 annually, would increase the Division’s capacity for reviewing applications by about 40 percent and eliminate the backlog within about 21 months, assuming the Division makes no other changes to the review process and receives the same rate of new applications going forward. As of August 2016, the Division still had one open FTE staff position that it has never filled due to insufficient revenue from application fees. Our RECOMMENDATION 3 includes improvements that should help the Division address its difficulties with funding its costs, thereby allowing the Division to hire another staff to review applications.

LACK OF PERFORMANCE GOALS AND MONITORING OF REVIEW

TIMELINESS. The Division has not established achievable performance goals for how long applications can wait in a queue or for how long staff should spend reviewing applications. In its strategic plans for Fiscal Years 2014 and 2015, the Division included a goal of 60 days for the total processing time from when an application is deemed complete until it sends a final decision to the landowner. However, the 60-day goal did not distinguish queue wait times from review times and was unachievable given that the average time for initial reviews was at least double that between December 2014 and June 2016. The Division did not establish a timeliness goal for Fiscal Year 2016 and has not set goals for reducing the backlog of applications waiting in queue. Further, the Division does not track sufficient information in a central location to monitor the timeliness of reviews. Although the Division tracks the dates when applications are deemed complete and when it sends deficiency letters to landowners in its database, the Division does not track when reviewers actually begin reviewing applications in

34

CO

NSE

RV

AT

ION

EA

SEM

EN

T T

AX

CR

ED

IT P

RO

GR

AM

, AFT

ER

CH

AN

GE

S IN

201

4, P

ER

FOR

MA

NC

E A

UD

IT –

NO

VE

MB

ER

201

6 its database. Thus, the Division is unable to readily calculate the length of wait times and review times and is unable to analyze trends in processing times, which is necessary information for planning staffing levels and gauging the efficiency of its review processes.

APPRAISALS THAT DO NOT MEET DIVISION STANDARDS. The Division reported to us that it takes staff longer to review appraisals that have significant deficiencies that call into question the appraisals’ credibility. Indeed, through our file review of a sample of 10 conservation easements, we found that staff often request more than one revision and engage in multiple back-and-forth exchanges with the appraisers to address deficiencies, which adds time to the review process. Our recommendations in the section titled “Communicating Review Standards to Appraisers” are aimed at reducing the incidence of conservation easement appraisals that fail to meet the Division’s standards.

INEFFICIENT APPLICATION REVIEW PROCEDURES. In June 2016, the Division conducted a Lean review and found that it could streamline two application review procedures that add considerable time to the processing of applications, which we also identified as being inefficient. First, Division staff reported that they often spend a considerable amount of time reviewing title commitment exceptions, which are legal restrictions on the property rights of the landowner and include items such as liens, public utility easements, and rights to drainage ditches. Title commitment exceptions can be numerous for any given property; for example, one conservation easement donation had 135 exceptions, each of which was reviewed by Division staff, per Division policy. This review by Division staff is often unnecessary because it duplicates work that certified conservation easement holders are required to do under state regulations to ensure that any liens or encumbrances are addressed and the conservation purposes will be ensured in perpetuity [4 C.C.R., 725-4(2.1)(B)(2)]. In October 2016, the Division reported to us that it changed its procedures to rely more on the title reviews conducted by easement holders so that staff only review title exceptions that could have an impact on the value or conservation purpose of an easement donation. The Division found

35

RE

POR

T O

F TH

E C

OL

OR

AD

O ST

AT

E A

UD

ITO

R

that it could save at least 15 hours of staff review time per application (a savings of about 75 percent of the review time) by changing its procedures in this way. Second, both the Division’s Lean review and our audit found that the reports staff compose for their application reviews are lengthy and time-consuming to prepare. According to Division staff, the reports, particularly for appraisal reviews, are often repetitive and sometimes take weeks to write and revise. In October 2016, the Division reported to us that it has developed a template for more concise reports. The Division estimated that it can save about 20 hours of staff time on about one-half of the appraisals it reviews by using this more concise report format.

INFREQUENT USE OF SETTLEMENTS. Statute [Section 12-61-727(12)(d),

C.R.S.] gives the Division the option to compromise with a landowner regarding deficiencies in an application “including the amount of the tax credit certificate to be issued.” Applying this compromise option could be an efficient mechanism when deficiencies are not severe enough to change the valuation of the easement to such an extent that the tax credit amount would be affected. However, the Division has offered to compromise with only two of the 19 landowners to whom it sent deficiency letters between January 2014 and June 2016. Further, of the 12 appraisals during this period for which the Division sent deficiency letters and later approved a revised appraisal, six changed the valuation of the easement upon revision and only three changed the valuation sufficiently to affect the amount of tax credit the landowner could claim. The Division may be able to reduce the review time on more applications if it exercises its option to settle when it has sufficient information to support a negotiated settlement or when the appraisal has deficiencies that do not significantly affect the valuation of the easement. For example, if the appraisal valued the easement at $3.5 million and the landowner was claiming the maximum $1.5 million tax credit, a revision in the appraisal would have to reduce the valuation by $550,000 (16 percent) to affect the amount the landowner could claim for a tax credit. In such a scenario, if a revision is not likely to change the value that much, or at all, and

36

CO

NSE

RV

AT

ION

EA

SEM

EN

T T

AX

CR

ED

IT P

RO

GR

AM

, AFT

ER

CH

AN

GE

S IN

201

4, P

ER

FOR

MA

NC

E A

UD

IT –

NO

VE

MB

ER

201

6 the deficiencies identified are not fundamental to the credibility of the appraisal, the Division could eliminate its request for a revised appraisal and secondary review by offering to settle with the landowner for the tax credit amount claimed. The Division could send a deficiency letter that explains the landowner’s options to either address the deficiencies identified in the appraisal or accept a denial and subsequent settlement. We estimate that eliminating secondary reviews for some applications could save an average of 130 days per application.

NO MECHANISMS FOR ENCOURAGING LANDOWNERS TO SUBMIT

APPLICATIONS EARLIER IN THE YEAR. The Division has not established submission deadlines or other mechanisms to encourage landowners to submit their applications at times of the year other than December. Currently, two factors tend to encourage taxpayers to submit applications late in the year. First, tax filing deadlines likely play a role in the surges of applications the Division has received in December of each year. To be eligible to receive a tax credit for a given tax year, a landowner must first record the deed of conservation easement with the appropriate county office by December 31 of that year, obtain a tax credit certificate, and file his or her tax return by April 15 of the following year (or October 15 if a filing extension is granted). The process of donating a conservation easement to a certified land trust is lengthy, and landowners often submit their tax credit certificate applications to the Division after recording conservation easements late in the year to meet tax deadlines. Given the average length of review times for tax credit certificate applications, a landowner who submits an application on December 31 is unlikely to receive a decision from the Division by the April 15 tax-filing deadline. Second, the Division revises its application fee amounts annually, publicly informing the Commission of the upcoming changes in December and making the changes effective January 1. The Division increased application fees in 2015 and 2016, so in those years landowners had an incentive to submit applications before January 1 to avoid paying the increased fee amount. If the Division set application submission deadlines earlier in the year, it could

37

RE

POR

T O

F TH

E C

OL

OR

AD

O ST

AT

E A

UD

ITO

R

incentivize submissions at different times and help spread the application review workload more evenly across the year. For example, after improving its processes and reducing the backlog of applications, the Division could set an application deadline of September 15 for landowners who wish to receive a tax credit certificate prior to the April 15 tax-filing deadline. This would give the Division about 210 days to process the application from start to finish, including resolving any noted deficiencies. To ensure that such a deadline is workable and appropriately balances the Division’s priorities with the needs of landowners, the Division may need to obtain input from industry stakeholders, including those who serve on the Commission.

WHY DOES THIS PROBLEM MATTER?

ADDED TIME AND COSTS FOR LANDOWNERS. Statute includes review process time frames to help ensure the application process is timely for landowners. Each step in the review process adds time that landowners must wait to receive a tax credit certificate for filing a tax return. During the audit review period, the Division’s total processing time, from the date it deemed an application complete until it mailed the tax credit certificate to the landowner ranged from 4 days to 328 days, with an average of 131 days. We identified three landowners (of the 58 who applied for preliminary advisory opinions) who submitted applications for tax credit certificates before the Division finished reviewing their preliminary advisory opinion applications, because the Division’s review process was taking longer than they expected. All three landowners had applied for preliminary advisory opinions to determine whether their conservation easement transactions would qualify for the state tax credit but abandoned their applications and did not receive opinions. When applicants abandon their preliminary advisory opinion applications, the application process can be wasted time for the applicant and the Division. Because the Division does not track the time staff spend reviewing preliminary advisory opinion applications, we could not determine the staff resources spent on these reviews prior to the applicants abandoning them. Recognizing the cost to landowners that can be caused by prolonged processing times, the

38

CO

NSE

RV

AT

ION

EA

SEM

EN

T T

AX

CR

ED

IT P

RO

GR

AM

, AFT

ER

CH

AN

GE

S IN

201

4, P

ER

FOR

MA

NC

E A

UD

IT –

NO

VE

MB

ER

201

6 Division agreed to reduce the fee for tax credit certificate applications for six landowners who had applied for preliminary advisory opinions from August to October 2015, including two of the three who abandoned their applications before applying for a tax credit certificate. The third landowner was already promised a discount due to the placeholder certificate process we discuss in the next section. In addition, landowners may incur additional costs when the Division is not timely in processing an application. For example, some landowners must file extensions for their tax filings, which causes an additional burden and may increase their costs for professional tax services.

INEFFICIENT USE OF STAFF RESOURCES. When Division staff spend time working with appraisers to correct deficiencies in appraisals that do not affect the valuation of the easement, it is an inefficient use of staff resources. For example, such time could be spent completing substantive reviews of more applications or developing appraisal course materials or guidance on the Division’s review standards, as we recommend in RECOMMENDATION 4.

DISCONTENT IN THE LAND CONSERVATION COMMUNITY. Members of the conservation easement community, including landowners, land trust representatives, and appraisers expressed their concerns to us during the audit regarding the length of the process. In addition, 73 percent (36 out of 49) of participants in our survey who responded to a question on the Division’s timeliness disagreed or strongly disagreed with the statement that “the Division processed their applications in a reasonable amount of time.” During our audit we found that this discontent strained relations between the conservation community and the Division, and between the Commission and the Division, which at times led to miscommunication and breakdowns in collaboration.

39

RE

POR

T O

F TH

E C

OL

OR

AD

O ST

AT

E A

UD

ITO

R

RECOMMENDATION 1

The Division of Real Estate (Division) should implement strategies to reduce the length of time it takes to review applications for conservation easement tax credits and preliminary advisory opinions and to issue its decisions by: A Implementing an ongoing process for analyzing the number of

applications that have been processed and are in a queue, and using this information to evaluate the sufficiency of available staffing resources. The Division should then use the results of this evaluation to seek additional staff resources, if needed.

B Setting goals for the timeliness of application reviews and for

reducing the backlog of applications waiting in queue, and monitoring performance toward such goals and statutory timelines.

C Continuing to identify and implement strategies for improving the

efficiency of application reviews. D Increasing the use of the settlement option for deficiencies in

appraisals when the Division has sufficient information to support a negotiated settlement or when such deficiencies are unlikely to affect the value of the tax credit claimed or the credibility of the appraisal.

E Implementing mechanisms to encourage landowners to submit

applications throughout the year, such as setting deadlines for landowners who want to receive decisions on their applications by a certain date.

40

CO

NSE

RV

AT

ION

EA

SEM

EN

T T

AX

CR

ED

IT P

RO

GR

AM

, AFT

ER

CH

AN

GE

S IN

201

4, P

ER

FOR

MA

NC

E A

UD

IT –

NO

VE

MB

ER

201

6

RESPONSE

DIVISION OF REAL ESTATE

A AGREE. IMPLEMENTATION DATE: JULY 2017 AND ONGOING.

The Division understands the importance of analyzing and tracking the resources necessary to process the tax credit certificate applications received. In late Spring 2016, the Division initiated a LEAN project specific to the tax credit certificate application portion of the Conservation Easement Program. One of the recommendations that resulted from the LEAN project was to establish a procedure for tracking the time spent performing specific assignments and workloads. As a result, the Division is now using a Google-based software solution for tracking, and will use such information to seek additional staff resources, if needed. The Division is tracking when applications have been deemed complete, when the 120-day deadline occurs, and internal target deadlines for completion of the appraisal and conservation purpose reviews. The Division is also tracking information that is specific to each application to ensure that staff is consistently informed of each application's progress.

B AGREE. IMPLEMENTATION DATE: JULY 2017.