Demystifying Hedge Accounting

15

John Trefethen Director, Sales Travis Quast Director, Hedge Accounting

-

Upload

odin-soli -

Category

Economy & Finance

-

view

79 -

download

2

Transcript of Demystifying Hedge Accounting

John Trefethen

Director, Sales

Travis Quast

Director, Hedge Accounting

1www.DerivActiv.com Demystifying Hedge Accounting

• Founded 2004

• Leading, independent provider of valuations and hedge accounting

• Over 400 institutional clients globally

• 10+ years of hedge accounting experience

• Joined DerivActiv in 2006

• Previously worked for a MN-based Fortune 500 company

Travis QuastDirectorHedge Accounting

2www.DerivActiv.com Demystifying Hedge Accounting

• What is Hedge Accounting?

• A Tale of Two Case Studies

• “ABC Credit Union”

• “123 Credit Union”

• Top 3 Takeaways

3www.DerivActiv.com Demystifying Hedge Accounting

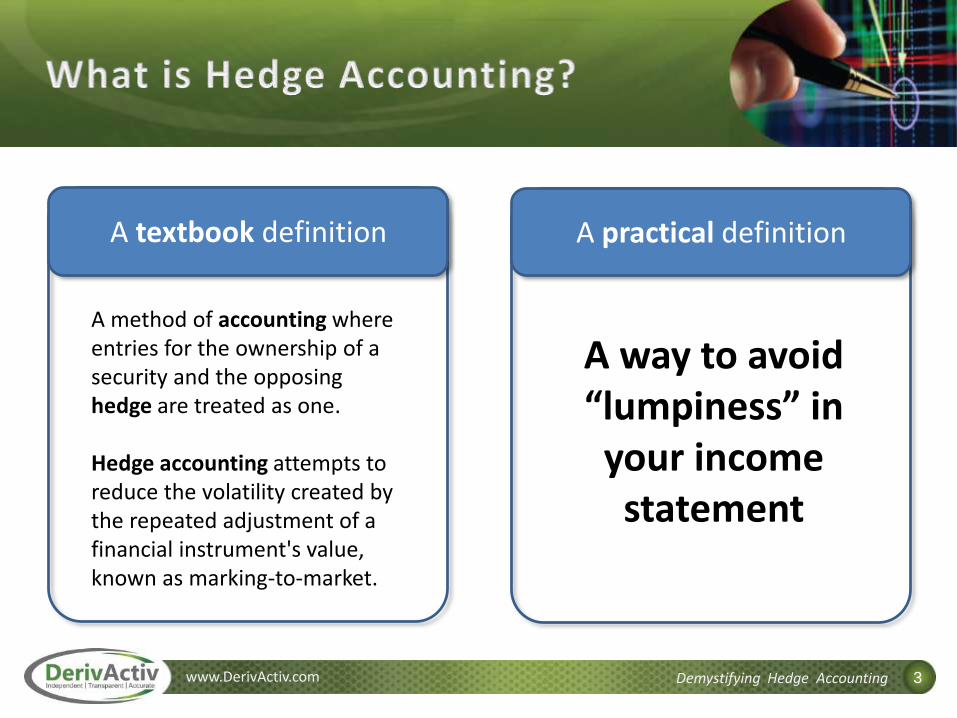

A textbook definition A practical definition

A method of accounting where entries for the ownership of a security and the opposing hedge are treated as one.

Hedge accounting attempts to reduce the volatility created by the repeated adjustment of a financial instrument's value, known as marking-to-market.

A way to avoid “lumpiness” in

your income statement

4www.DerivActiv.com Demystifying Hedge Accounting

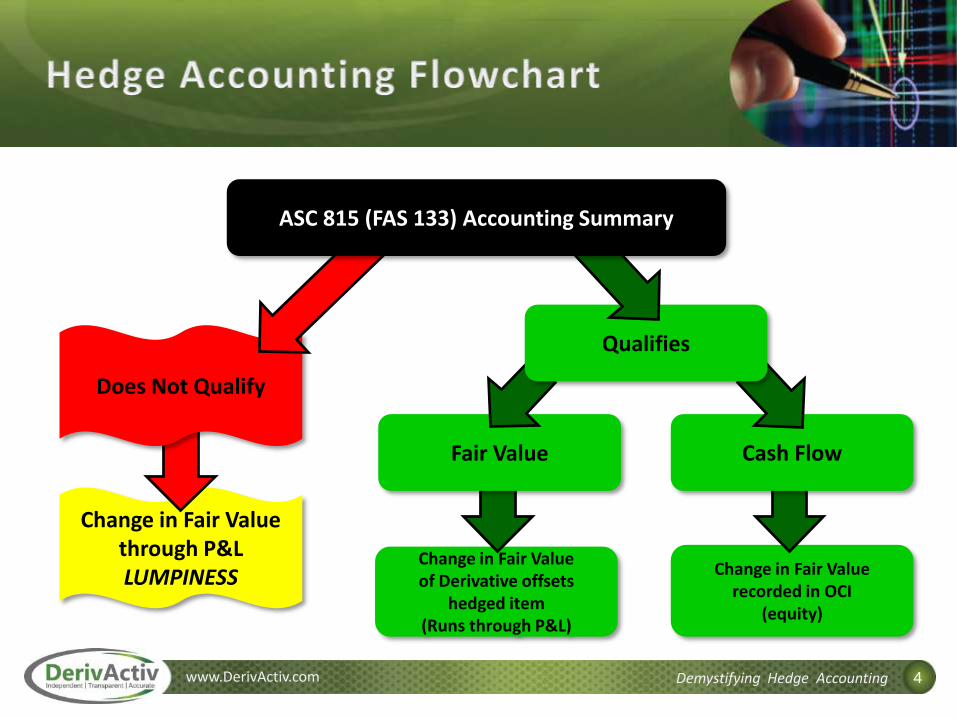

Change in Fair Valuerecorded in OCI

(equity)

Change in Fair Valueof Derivative offsets

hedged item(Runs through P&L)

Fair Value Cash Flow

Change in Fair Value through P&LLUMPINESS

Qualifies

Does Not Qualify

ASC 815 (FAS 133) Accounting Summary

5www.DerivActiv.com Demystifying Hedge Accounting

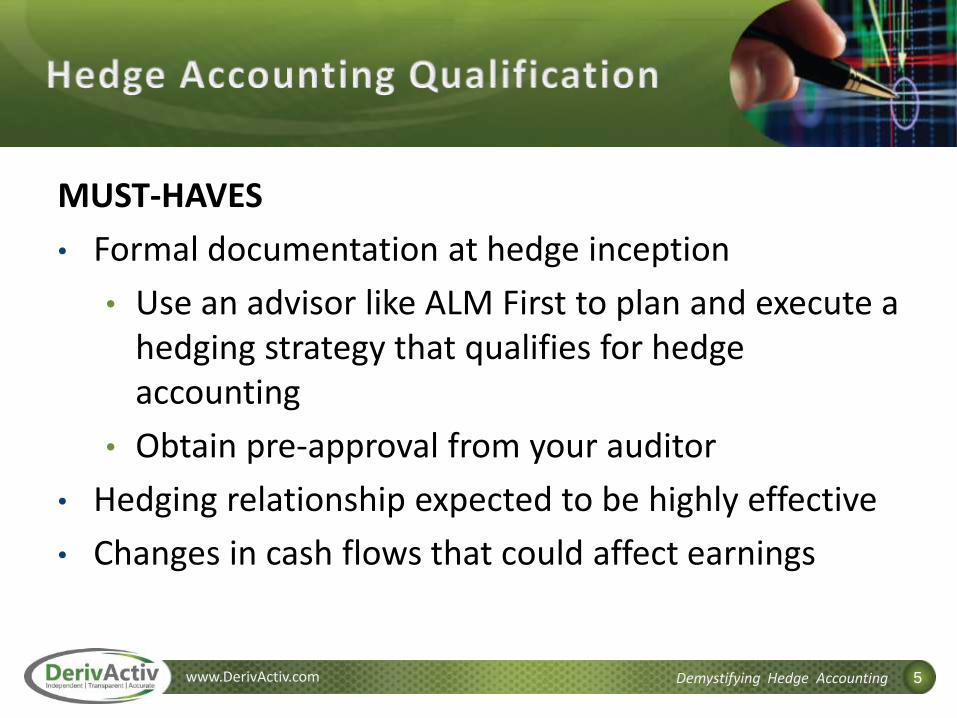

MUST-HAVES

• Formal documentation at hedge inception

• Use an advisor like ALM First to plan and execute a hedging strategy that qualifies for hedge accounting

• Obtain pre‐approval from your auditor

• Hedging relationship expected to be highly effective

• Changes in cash flows that could affect earnings

6www.DerivActiv.com Demystifying Hedge Accounting

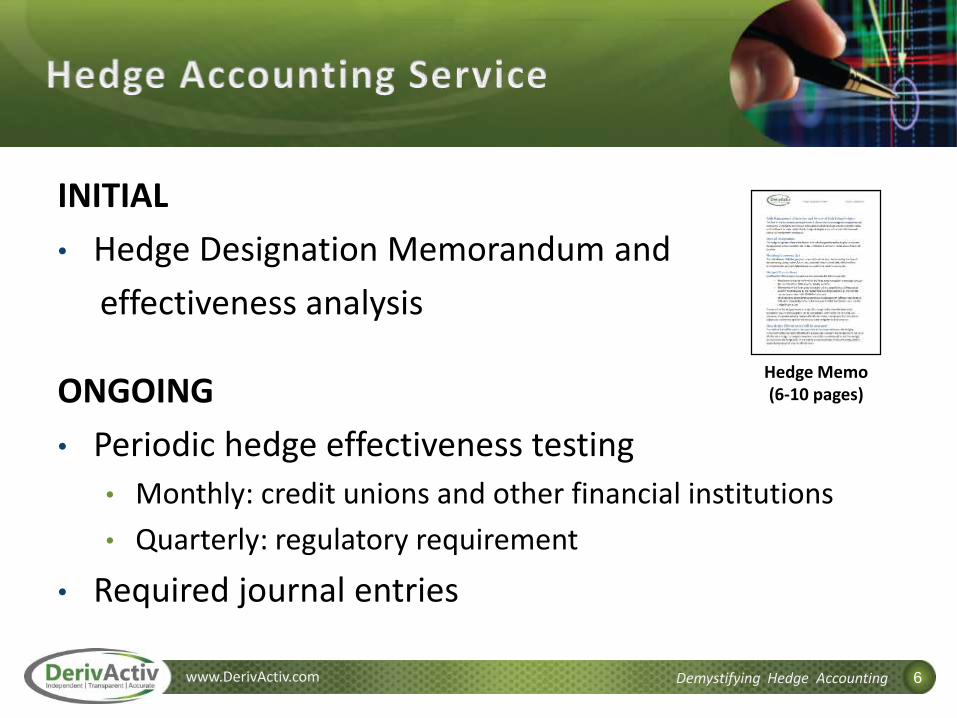

INITIAL

• Hedge Designation Memorandum and

effectiveness analysis

ONGOING

• Periodic hedge effectiveness testing

• Monthly: credit unions and other financial institutions

• Quarterly: regulatory requirement

• Required journal entries

Hedge Memo(6-10 pages)

7www.DerivActiv.com Demystifying Hedge Accounting

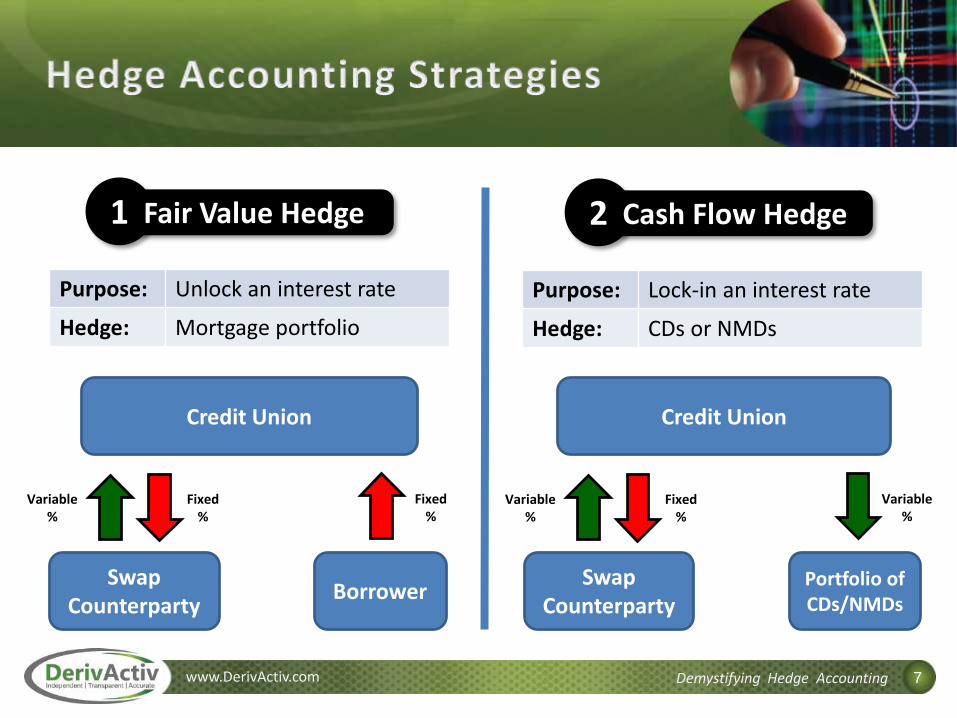

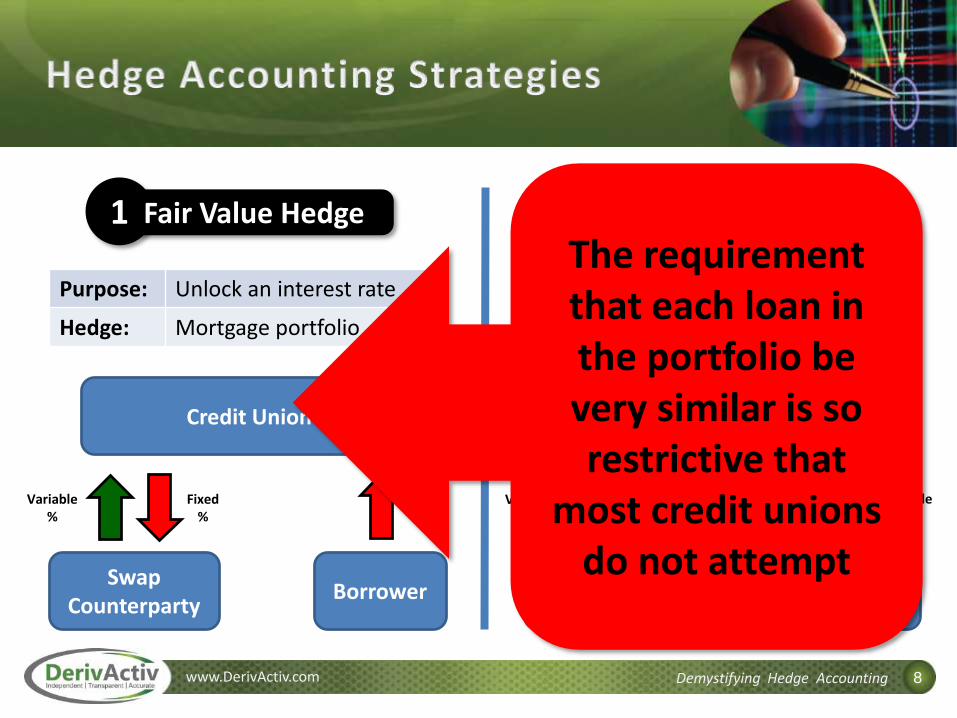

1 Fair Value Hedge 2 Cash Flow Hedge

Purpose: Unlock an interest rate

Hedge: Mortgage portfolio

Purpose: Lock-in an interest rate

Hedge: CDs or NMDs

Swap Counterparty

Credit Union

Borrower

Fixed%

Fixed%

Variable%

Swap Counterparty

Credit Union

Portfolio of CDs/NMDs

Variable%

Fixed%

Variable%

8www.DerivActiv.com Demystifying Hedge Accounting

1 Fair Value Hedge 2 Cash Flow Hedge

Purpose: Unlock an interest rate

Hedge: Mortgage portfolio

Purpose: Lock-in an interest rate

Hedge: CDs or NMDs

Swap Counterparty

Credit Union

Borrower

Fixed%

Fixed%

Variable%

Swap Counterparty

Credit Union

Portfolio of CDs/NMDs

Variable%

Fixed%

Variable%

The requirement that each loan in the portfolio be very similar is so restrictive that

most credit unions do not attempt

9www.DerivActiv.com Demystifying Hedge Accounting

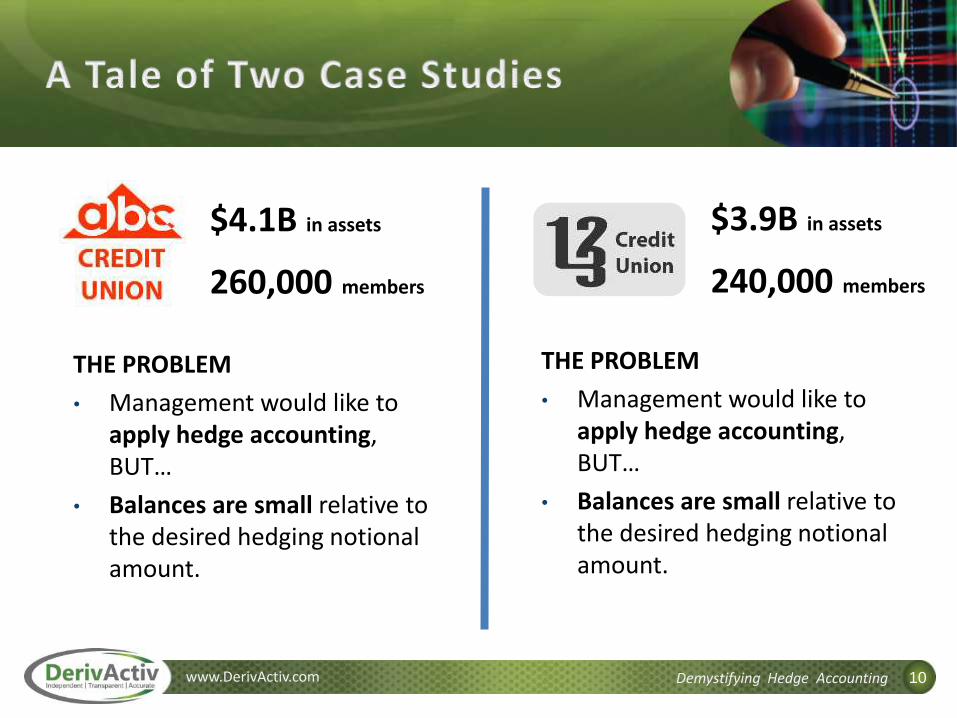

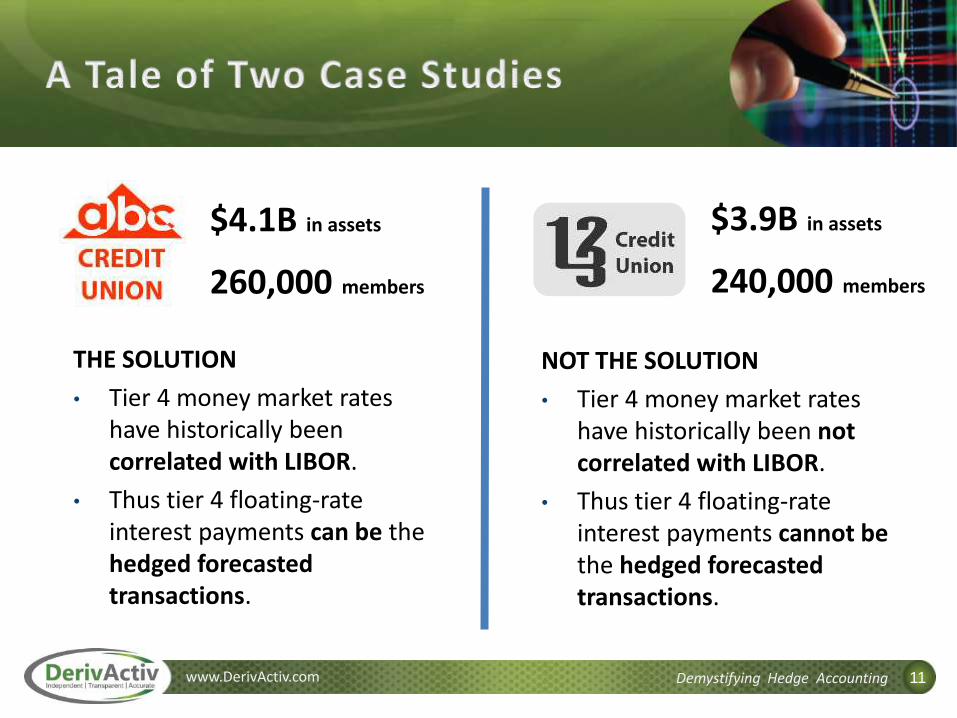

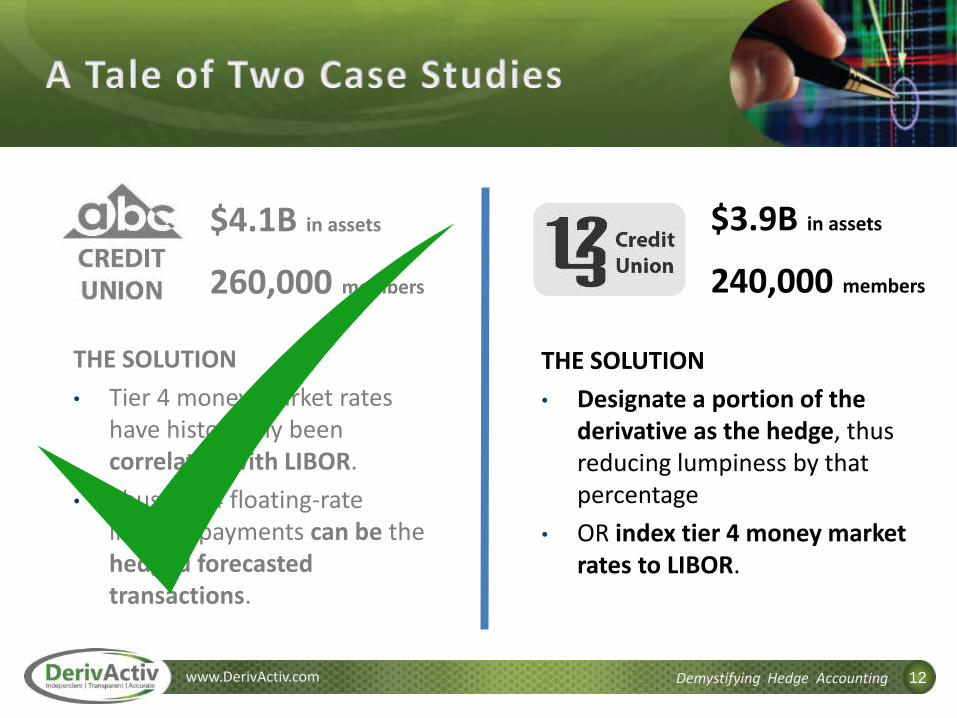

$4.1B in assets

260,000 members

THE SITUATION

• “ABC Credit Union” desires to hedge its portfolio of CDs by entering into a pay-fixed, receive-floating cash flow hedge.

$3.9B in assets

240,000 members

THE SITUATION

• “123 Credit Union” desires to hedge its portfolio of CDs by entering into a pay-fixed, receive-floating cash flow hedge.

10www.DerivActiv.com Demystifying Hedge Accounting

$4.1B in assets

260,000 members

THE PROBLEM

• Management would like to apply hedge accounting, BUT…

• Balances are small relative to the desired hedging notional amount.

$3.9B in assets

240,000 members

THE PROBLEM

• Management would like to apply hedge accounting, BUT…

• Balances are small relative to the desired hedging notional amount.

11www.DerivActiv.com Demystifying Hedge Accounting

$4.1B in assets

260,000 members

THE SOLUTION

• Tier 4 money market rates have historically been correlated with LIBOR.

• Thus tier 4 floating-rate interest payments can be the hedged forecasted transactions.

$3.9B in assets

240,000 members

NOT THE SOLUTION

• Tier 4 money market rates have historically been not correlated with LIBOR.

• Thus tier 4 floating-rate interest payments cannot be the hedged forecasted transactions.

12www.DerivActiv.com Demystifying Hedge Accounting

$4.1B in assets

260,000 members

THE SOLUTION

• Tier 4 money market rates have historically been correlated with LIBOR.

• Thus tier 4 floating-rate interest payments can be the hedged forecasted transactions.

$3.9B in assets

240,000 members

THE SOLUTION

• Designate a portion of the derivative as the hedge, thus reducing lumpiness by that percentage

• OR index tier 4 money market rates to LIBOR.

13www.DerivActiv.com Demystifying Hedge Accounting

1) GET RID OF LUMPINESS

• Take advantage of hedge accounting!

2) PLAN AHEAD

• Use an advisor like ALM First to plan and execute a hedging strategy to get terms that will qualify for hedge accounting.

• Obtain pre‐approval from your auditor for any new hedging strategy.

3) DO IT RIGHT

• Beware of widely publicized “shortcut” and “critical terms match” methods, which have led to numerous restatements.

• Quantitative methods in which hedge effectiveness is assessed and measured are much safer.

14www.DerivActiv.com Demystifying Hedge Accounting

John TrefethenDirector, [email protected]

Minneapolis || New York || Panama City

www.DerivActiv.com

866-200-9012

Travis QuastDirector, Hedge [email protected]

![Demystifying Hedge Funds: A Design PrimerEd. 2] Demystifying Hedge Funds: A Design Primer 325 that even might threaten the financial stability of the markets.? But, like those clubs](https://static.fdocuments.net/doc/165x107/61295b7dec886b24c863857e/demystifying-hedge-funds-a-design-primer-ed-2-demystifying-hedge-funds-a-design.jpg)

![Forex Hedge Accounting Treatment[1]](https://static.fdocuments.net/doc/165x107/5534f67255034625198b45d7/forex-hedge-accounting-treatment1.jpg)