Demand Side Flexibility Annual Report 2016 - Power...

26

Demand Side Flexibility Annual Report 2016

-

Upload

truongkhanh -

Category

Documents

-

view

215 -

download

0

Transcript of Demand Side Flexibility Annual Report 2016 - Power...

Demand Side Flexibility Annual Report 2016

Executive summary

Demand side flexibility is the ability to change electricity output or demand in reaction to an external signal. The use of demand side flexibility tools such as demand side response, storage and distributed generation will be particularly important in the shift to a lower carbon future. Business customers can benefit financially by offering demand side flexibility services to market actors.

Power Responsive was set up to promote the participation of demand side flexibility in GB electricity markets. The Power Responsive Annual Report enables the Power Responsive Steering Group to account more widely for its work to electricity market actors, policy makers, and importantly to Industrial and Commercial (I&C) customers.

The annual report covers: Power Responsive work programme in Year 1 and priorities for Year 2 overview of demand side flexibility markets today and the perspectives

of different market actors initial metrics to assess progress year on year and gaps in the data

to address potential evolution of demand side markets in future.

Over the past year we have made some initial progress, including: Raising awareness – actively engaging with I&C customers to make them

aware of the opportunities and ways of taking part, including interviews, training, workshops and a survey.

Market making – working with market actors, I&C customers and policy makers, to develop a collective understanding of the opportunities, challenges and issues, so that they can begin to offer services/build up their customer base.

The contribution of demand side flexibility in GB electricity markets is currently small and mainly in balancing. But there is potential for gigawatts of demand side flexibility, saving billions in consumer value over time. Demand side flexibility will be needed in future to manage the system and market risks. So the opportunity and rewards to customers are likely to grow.

National Grid, as System Operator, has taken steps over the past year to improve information about Balancing services, making existing schemes more accessible and developing new schemes. Market actors are beginning to recognise the potential for demand side flexibility – incorporating it into their operations or developing new business models.

Customers who offer demand side flexibility generally do so to reduce their electricity costs and generate new revenue streams. Often this is done through an aggregator, with a focus on managing network charges, participating in Balancing services and the capacity market. Onsite/back-up generation provides much of the demand side flexibility today.

The focus of Power Responsive in Y2 will be on: wider and deeper customer engagement clearer information, simpler products,

strengthened customer confidence future evolution of demand side

flexibility markets.

The Power Responsive Steering Group is also developing a shared view of what success might look like for demand side flexibility in future and how markets might evolve.

d

e

Demand side responseDemand side response is intelligent energy usage. By knowing when to increase, decrease or shift their electricity consumption businesses and consumers will save on total energy costs and can reduce their carbon footprints.

Although in its infancy, demand side response is a reality. Together we can shape and share the possibilities created by demand side solutions.

Contents

Introduction 01

Report outline 01

1.0 Power Responsive programme 02

2.0 Demand side flexibility in GB electricity 03 markets today 2.1 Role of demand side flexibility 03 2.2 Current markets for demand side flexibility 04 2.3 System Operator steps to enable demand side participation 05 2.4 Electricity market actor views 06 2.5 Business customer views 07 2.6 Policy and regulatory context 09

3.0 Initial metrics for demand side flexibility 10 3.1 Context 10 3.2 Contracted markets – Balancing services 10 a. Total contribution to Balancing services 10 b. By demand side flexibility category 10 c. Contribution by Balancing service 11 3.3 Contracted markets – Capacity Market 12 3.4 Contracted markets – demand side providers 12 3.5 Self-dispatched activity 13 a. Transmission network cost management – TRIADs 13 b. Distribution network cost management 13 c. Wholesale market price signal 14 3.6 Areas for further analysis 14

4.0 Future development of demand side 15 flexibility markets

Annex A: Steering Group members 16

Annex B: Balancing services 17

Annex C: Glossary 18

Contact us 20

01

Our electricity system is changingIn response to climate change, with intermittent renewable energy and advances in technology, we are moving from a world where electricity once flowed one way along networks from a generator to homes and businesses, to one where it is now often produced locally and flows in multiple directions.

Introduction

Our electricity system is changing. In response to climate change, with intermittent renewable energy and advances in technology, we are moving from a world where electricity once flowed one way along networks from a generator to homes and businesses, to one where it is now often produced locally and flows in multiple directions. This means the system needs to be managed differently and more responsively.

Demand side flexibility is playing an increasingly important role in Britain’s electricity markets. Business customers can save money and earn revenues by using their power more flexibly and effectively without impacting on their normal day-to-day operations. Demand side flexibility can reduce costs to all customers and the system.

Power Responsive was set up in 2015 as a collaborative programme, facilitated by National Grid, working with business customers and the energy market to increase participation in various forms of demand side flexibility in Great Britain’s electricity markets.

For more information visit www.powerresponsive.com.

Report outline

This report considers the current role of demand side flexibility in GB electricity markets and the steps needed to enable greater participation in future. It covers:

Power Responsive work programme – delivery in Year 1 and priorities for Year 2 (Section 1).

The current contribution of demand side flexibility in different markets – balancing, capacity, wholesale, networks – including steps taken by National Grid, perspectives of different market actors and I&C customers, the policy and regulatory context (Section 2).

Initial metrics for the contribution of demand side flexibility today, from which to assess progress year on year, including gaps in the data to address (Section 3).

Future development of demand side flexibility markets – including a vision for 2025 and next steps for Power Responsive (Section 4).

The report has been written on behalf of the Power Responsive Steering Group by the environment charity Sustainability First, in collaboration with National Grid, who provided all the data analysis. It should not be taken as investment advice in demand side markets on the part of Sustainability First or National Grid. Steering Group members are listed in Annex A.

The report is addressed to those working in the electricity market, policy makers, and to Industrial and Commercial (I&C) customers – including businesses and public sector organisations, whose willing participation is fundamental to achieving cost-efficient delivery of flexibility to electricity markets.

It is designed for an informed audience. Balancing services are listed in Annex B. Terminology is explained in a glossary in Annex C. We have developed a separate fact-sheet for I&C customers.

Demand side response (DSR) is where levels of electricity demand are changed (increased, reduced or shifted) at a particular moment in time in response to an external signal (such as a change in price, or a message). Customers can decide whether to react to these signals or override them. National Grid uses the wider term demand side flexibility to include five categories of flexible response:

1. DSR by flexible load shifting (e.g. heating/cooling systems, business operations and appliances)

2. DSR by onsite generation3. DSR by onsite energy storage4. Distributed generation – for export5. Distributed energy storage – for export

02

Power Responsive programme1 .0Purpose, focus and oversight of Power Responsive. Delivery in Year 1 – awareness raising and market making. Plans for Year 2 – wider and deeper customer engagement; clearer information, simpler products and strengthened customer confidence; and future evolution of demand side flexibility markets.

Launched by National Grid in 2015, Power Responsive promotes different forms of demand side flexibility in electricity markets, aiming to address barriers to customer participation, with an initial focus on Industrial and Commercial (I&C) customers. The role for households and small and medium-sized enterprises is not considered in this report.

The Power Responsive Steering Group meets quarterly with representatives of the main interested parties – including electricity market actors, demand side providers, I&C customers from different sectors (transport, public, retail, water and industry), the Department for Business, Energy & Industrial Strategy (BEIS) and Ofgem. Current steering group members are listed in Annex A.

The steering group focus in Year 1 was on: awareness raising – of the existing markets and new opportunities for demand side flexibility; and market making – engaging with market actors, I&C customers and policy makers to develop a collective understanding of the opportunities, challenges and issues.

The group considered the current state of GB demand side flexibility in electricity markets, the perception and participation of customers and how demand side markets will evolve in the future. Each of these discussions was captured in a ‘market snapshot’ available at www.powerresponsive.com.

Activities in Year 1 included:

Raising awareness with I&C customers

Market making/ convening people

Developing simpler information & resources

Evolution of flexibility markets

In Year 2, Power Responsive will have a stronger emphasis on delivery – focusing on:

Customer engagement

Products, services and customer confidence

Evolution of flexibility markets

Actively engaging over 700 individuals and 370 businesses. Major sector-specific workshop on the National Health

Service estate with the Crown Commercial Service – involving 35 hospitals.

Training sessions and manual on demand side flexibility with the Major Energy Users’ Council – 120 businesses benefited.

Extensive national media coverage and trade media coverage, raising awareness of the benefits of demand side flexibility.

Two major Power Responsive conferences (held in June 2015 and

June 2016). 200-plus people attended the 2016 conference. Conference in Scotland in October 2016. Two chief-executive level discussions in May 2015 and May 2016.

Power Responsive website. Published 20 business customer case studies. Infographic on current demand side opportunities and markets. Short ‘How-to’ guide for business customers.

Power Responsive vision to 2025. Metrics for assessing market development year on year.

Awareness raising and clearer information. Deepen engagement with sector-specific I&C customers. Widen engagement to other flexible technologies (e.g. storage). Ongoing national and trade media engagement. Simpler Balancing products, and ensuring they are

easier to access. Refresh the Shared Services Framework. Supporting development by the Association for Decentralised

Energy (ADE) of a voluntary market-led code of conduct for demand side providers.

What success looks like for demand side flexibility in electricity markets today and in the future?

Boundaries and intersects for networks (transmission and distribution) and markets (balancing, capacity, wholesale and networks).

Future market arrangements and the transition.

Future evolution?The group considered the current state of GB demand side flexibility in electricity markets, the perception and participation of customers and how demand side markets will evolve in the future.

03

Demand side flexibility in GB electricity markets today2.0The role of demand side flexibility in GB electricity markets today and potential in future. National Grid changes to balancing products and services. Current perspectives of different electricity market actors and I&C customers on demand side flexibility. The policy and regulatory context.

2.1 Role of demand side flexibility

There is growing recognition of the important role that demand side flexibility can play in electricity markets. It reduces the need for new conventional generation and network infrastructure; supports the integration of growing intermittent generation; and helps suppliers to manage market risk.

Policy makers and the energy sector envisage that the scale and value of demand side flexibility is likely to grow in the future as part of a smarter system and with technological advances. But there are many uncertainties making it difficult to model the future potential for demand side flexibility1.

BEIS and Ofgem recently released a joint call for evidence on a smart, flexible energy system2. The National Infrastructure Commission estimated that ‘smart power’ – interconnection, storage and flexible demand – could save consumers up to £8bn a year by 20303.

National Grid estimates that increasing flexibility (interconnection, storage and DSR) could deliver up to £2bn of consumer value per year by 2030. National Grid has set an aspiration for 30–50% of balancing capability from demand side sources by 2020. The Association for Decentralised Energy estimates potential for demand side response of 9.8 GW by 20204.

1 Frontier Economics with Lane Clark and Peacock and Sustainability First (October 2015) Future potential for DSR in GB.

2 BEIS and Ofgem (November 2016) Smart, flexible energy system: A call for evidence.

3 National Infrastructure Commission (March 2016) Smart Power.

4 Association for Decentralised Energy (July 2016) Flexibility on demand: Giving customers control to secure our electricity system.

04

.

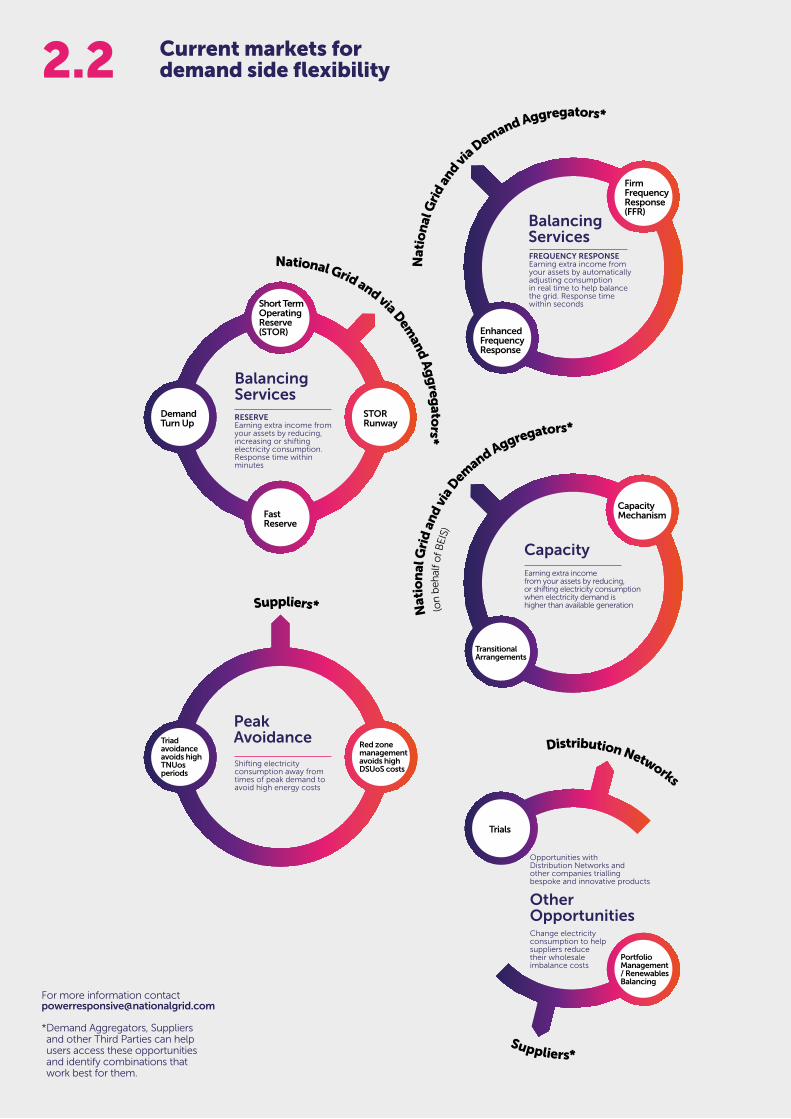

Current markets for demand side flexibility2.2

DemandTurn Up

Trials

PortfolioManagement/ RenewablesBalancing

STORRunway

EnhancedFrequencyResponse

TransitionalArrangements

Triadavoidanceavoids highTNUosperiods

Red zonemanagementavoids highDSUoS costs

CapacityMechanism

FirmFrequencyResponse(FFR)

FastReserve

Short TermOperatingReserve(STOR)

National Grid and via Demand A

gg

regato

rs*

Nat

ion

al G

rid

and via D

emand Aggregators*

Nat

ion

al G

rid

and

via

Dem

and Aggregators*(o

n b

ehal

f of B

EIS)

Suppliers*

Distribution Networks

Suppliers*

For more information contact [email protected]

* Demand Aggregators, Suppliers and other Third Parties can help users access these opportunities and identify combinations that work best for them.

BalancingServicesRESERVE Earning extra income from your assets by reducing, increasing or shifting electricity consumption. Response time within minutes

Earning extra income from your assets by reducing, or shifting electricity consumption when electricity demand is higher than available generation

Shifting electricity consumption away from times of peak demand to avoid high energy costs

Opportunities with Distribution Networks and other companies trialling bespoke and innovative products

Change electricity consumption to help suppliers reduce their wholesale imbalance costs

FREQUENCY RESPONSE Earning extra income from your assets by automatically adjusting consumption in real time to help balance the grid. Response time within seconds

BalancingServices

PeakAvoidance

Other Opportunities

Capacity

05

System Operator steps to enable demand side participation

National Grid as the System Operator is currently the largest procurer of demand side flexibility services to help balance the electricity system on a second-by- second basis. They are incentivised to deliver an efficient system, ensuring thereis sufficient reserve electricity available on different timescales, at least cost toconsumers, and where possible, procured through competitive tenders. Annex B lists current Balancing services. Annex C explains each service in the glossary.

National Grid launched Power Responsive as a programme of work to promote the benefits of participation in demand side flexibility in electricity markets – including for Balancing and wider opportunities.

National Grid’s role, as facilitator, is leading engagement activity and working to improve Balancing Service offers to increase participation, remove barriers and create a more level playing field for demand and supply side providers.

2.3

Year 1: Developments to Improve Accessibility Clearer information on Balancing products & services

New Balancing products

Changes to existing Balancing service

Year 2: Focus on ‘Simplicity’National Grid undertook a questionnaire in October 2016 and received feedback from 115 flexibility providers on specific elements that can be simplified and clarified in Balancing Services. Feedback suggested that the complexity and number of Balancing Services markets and adjustments is acting as a barrier to entry. In Year 2, National Grid will work to address these issues, building on the steps already taken above, with a focus on:

Simplifying the suite of Balancing products and services

Shared services

Future market evolution

The programme of simplification will be progressed with stakeholders through the Power Responsive Steering Group and subgroups – the Demand Side Response Providers Forum and Storage Working Group as well as with energy and customer trade associations – with the aim of developing options that can be implemented within existing frameworks and within a 12-month timeframe.

1. Clearer information on current Balancing products and services.

2. More regular updates including data.3. Historic information.4. More regular forward projections of commercial

requirements.

5. Demand Turn Up (DTU) – to increase/shift electricity use to times of day when levels of renewable generation are high. 300MW procured.

6. Enhanced Frequency Response (EFR) – a new faster frequency response product (<1 second), suited to electricity storage but open to all types of provider. 201 MW procured.

7. Demand Side Balancing Reserve – temporary tender for demand side providers to participate in offering capacity over winter peak periods; in lieu of capacity market/transitional arrangements starting.

8. Offering customers the flexibility to be unavailable for some windows of Short Term Operating Reserve (STOR) (e.g. so they can participate in Triad Avoidance), whilst through a premium service, incentivising those who can commit to being available for all windows.

9. Enabling participation of providers with smaller loads (<10 MW) e.g. through STOR runway and Firm Frequency Response (FFR) bridging.

Simplifying the current suite of Balancing products and services.

Improving market information of Balancing Services. Making improvements based on feedback from

the questionnaire.

Feeding lessons from trial with Western Power Distribution on shared benefits of DTU into a future shared services framework.

Considering the future shape of GB markets for demand side flexibility.

06

Electricity market actor views2.4Based on discussions at the Power Responsive Steering Group, the current perspectives of different market actors are:

Transmission Network Operators (TNOs) – operate, maintain and build networks to transport electricity nationwide. The current structure of transmission charges offers one of the strongest signals for half-hourly settled customers to manage their electricity use at times of system peak. Winter 2015–16 saw the highest ever response of Triad avoidance from customers.

Distribution Network Operators (DNOs) – run and maintain safe and reliable regional distribution systems to transport electricity to homes and businesses. Demand side flexibility can be used to manage local network restrictions – reducing stress at peak times, supporting planned or unplanned network outages, and deferring or avoiding network reinforcement. DNOs have gained significant experience through innovation trials, and are looking to incorporate this learning into day-to-day operations. Some DNOs are supporting development of demand side flexibility markets through innovative approaches to ‘value stacking’ – adding up all the bits of incremental value to be obtained in each segment of the electricity market. A key activity here is developing processes to ensure transmission and distribution network requirements are optimised (and avoid unintended consequences).

Suppliers – to date, have been less active in demand side response. But due to the increased wholesale price volatility, suppliers are beginning to offer products to manage their exposure to market risk and the costs of being out of balance. Business models are changing for some suppliers toward aggregation and ‘virtual power plant’ models – where different power sources and demand side activities are aggregated to give a reliable power supply. There are also new disruptive market entrants. Suppliers are well placed to combine the demand side value-stack for their customers. They can help customers to reduce their electricity costs by offering time-of-use (TOU) tariffs and also by offering customer alerts for Triad management.

Aggregators – can help facilitate customer access to a range of demand side flexibility services by aggregating many small demand side volumes from their contracted customers. Aggregators currently do not trade or supply power, but act as an active third party. The role of aggregators has grown in terms of the number of operators, the number of schemes they participate in and the scale of their customer participation. Aggregators focus particularly on contracted markets, as they cannot directly access potential benefits for their customers in the wholesale markets, because they are not Balancing and Settlement Code (BSC) signatories. Suppliers and third-party intermediaries can also offer similar services to aggregators – so we use the term ‘demand side providers’.

Load Response Providers – changing electricity demand onsite in response to a signal e.g. industrial process, lighting and appliances. Some customers are beginning to offer load response services through frequency and potentially for Triads. But it is relatively early days. There are currently challenges to making the commercial case for upfront investment in load response equipment and processes.

Onsite generators – much demand side flexibility is currently provided by back-up/onsite generation. There is significant potential for more onsite generation to participate in demand side markets and the challenge for Power Responsive is to encourage customers to make this flexibility available.

Storage operators – making the commercial case for storage is currently challenging, but the picture is becoming clearer at grid scale.

Market actors and customers are beginning to recognise the opportunities for demand side flexibility and they are developing capability to actively participate. The BEIS and Ofgem call for evidence identifies specific steps that could be taken to improve the case and remove barriers – in particular for aggregators, electricity storage providers, and considering the transition from DNO to Distribution System Operator (DSO)5.

5 BEIS and Ofgem (November 2016) Smart, flexible energy system: A call for evidence.

Avoiding peak energy usageThe BEIS and Ofgem identified specific steps that could be taken to improve the case and remove barriers – in particular for aggregators, electricity storage providers, and considering the transition from DNO to Distribution System Operator (DSO)5.

07

Business customer views

Business customer perspective on opportunities and challenges of taking part in demand side flexibility today, based on discussions at the Power Responsive Steering Group, interviews and workshops.

2.5

Cultural

Regulatory (role of parties) Commercial (incentives)

Structural (costs)

Lack of awareness of the opportunity. Difficulties gathering information about schemes and

how to participate. Customer confusion about various options available and

relative value. Perception business processes are not suitable.

Market complexity and scheme design. On-site generation connections at distribution level –

time and expense. Challenge for customers of engaging in policy development

and finding trusted advice.

Commercial viability – value proposition and uncertain payback. Contract terms and length – technical requirements may not fit

with business customer characteristics. Non-core business/other business drivers and competing priorities. Existing corporate environmental schemes/commitments.

Staff resourcing and getting buy-in ‘in-house’. Concerns about disruption to business-as-usual operations.

Many I&C customers have already achieved savings through energy efficiency and are now seeking opportunities to save money and generate revenue through demand side flexibility. The level of engagement varies by sector and available assets. The major driver is financial benefit, enabled by new

technology (e.g. metering and automation), whilst ensuring there is no significant impact on business operations. Many customers work with aggregators because current markets for demand side response are seen as complex, or their volumes are too small to access products directly.

Bath NHS Foundation Trust uses its existing two 800kW standby diesel generators to participate in Short Term Operating Reserve (STOR) and Triad management, combining essential testing of the generators with overall benefits of £40,000/MW for 2015–16.

Bernard Matthews found that by shifting the lighting for their livestock by one hour to avoid peak times, they saved £40,000 whilst maintaining comfort levels.

Water companies are major power users. United Utilities is involved in winter peak avoidance, Short Term Operating Reserve (STOR) and Frequency Response, using flexibility from its water/waste water pumping and waste water aeration processes. Over the next five years it intends to offer up to 50 MW of demand side response subject to it being commercially viable.

Sainsbury’s sends a warning to all stores during Triads to reduce electricity use, with automatic turn down of air handling units via onsite Building Management Systems. The business also offers dynamic frequency response through heating, ventilation and air conditioning (HVAC) systems and fridges.

For some customers, it can be confusing to navigate the many different demand side products available. There are also commercial challenges to an individual business due to uncertainty on paybacks and a reliance on multiple revenue streams. Customers and demand side providers want to see surety of return. Senior management buy-in and cross-business commitment is often required.

Confidence is critical to the success of demand side flexibility, therefore industry standards are needed – the ADE is working to develop a voluntary industry Code of Conduct for demand side providers.

Power Responsive has taken steps to raise awareness and gain a better appreciation of the challenges customers face, so that these can be addressed. We have produced a short guide for customers on steps to participate in DSR. Potential barriers to customer participation The following barriers have been identified based on discussions at the Power Responsive Steering Group, incorporating points from the BEIS & Ofgem Call for Evidence (Table 6).

Examples of businesses benefiting from demand side flexibility:

Avoiding peak energy usageBernard Matthews found that by shifting the lighting for their livestock by one hour to avoid peak times, they saved £40,000 whilst maintaining comfort levels

08

Headlines from Energyst survey6 212 responses, 191 completed the survey. 187 specified their industry sector: 56% I&C; 25% public sector; 9% manufacturing; remainder in food and drink, finance and retail.

Headlines from Ofgem DSR survey7 Survey of I&C consumers (>100) and DSR procurers (>80 but only 30 completed most questions). Of customers – industrial 42%, commercial 16%, public sector 8%, remainder cross-sector.

80% of customers are contracted via an aggregator although some also contract directly with National Grid (20%) and through their DNO (10%).

Around three-quarters (76%) turn on standby generators or switch to onsite generation. 59% also decrease consumption; 24% increase consumption.

Generating income from assets was the main reason for participation (85%) followed by avoiding peak network charges (40%).

Almost nine in ten DSR providers (86%) said they are satisfied with the outcome of DSR participation.

Reasons cited for dissatisfaction include scheme instability and revenue uncertainty; increased CO2 emissions from turning on diesel generators; and poor response and support from DNOs.

One-third of respondents participate in DSR. They currently provide around 350 MW of demand reduction with over 400 MW of technically and commercially viable additional demand reduction potentially available.

Translated to GB scale, the survey responses suggest a far greater untapped flexibility potential (c.3 GW for reducing demand and c.2 GW for increasing demand as a rough estimate).

DSR providers typically have higher electricity consumption and peak demand.

A diversity of sources of potential flexibility are available – motors and pumps most flexible, then lighting but this is infrequently used.

Regardless of DSR provision, two-thirds of respondents have on-site generation.

Three-quarters of respondents contacted about flexibility by suppliers, aggregators, National Grid, DNOs or others. Aggregators are most prevalent in procuring DSR.

6 http://theenergyst.com/dsr/

7 https://www.ofgem.gov.uk/publications-and-updates/industrial-commercial-demand-side-response-gb-barriers- and-potential

DSR Providers Almost nine in ten DSR providers said they are satisfied with the outcome of DSR participation

Generating Income Generating income from assets was the main reason for participation (85%) followed by peak network charges (40%)

Business customer views

86% 85%

09

Policy and regulatory context

How policy and regulation are working towards delivery of demand side flexibility markets – including balancing, capacity, wholesale and networks.

BEIS and Ofgem recognise the contribution that demand side flexibility can offer alongside low carbon, distributed and conventional generation. Market arrangements are still largely designed for an ‘old world’ model – a static system where electricity flows from power centres across the transmission network, to distribution networks, and then to customers, rather than dynamic, multi-way flows from distributed generation, storage and responsive customers. Policy makers are, therefore, working collaboratively, including with Power Responsive, to enable a smarter energy system in the future. Since Power Responsive began in early 2015, there have been some significant developments to support demand side flexibility in the I&C sector, including:

sharper signal in the wholesale markets for imbalance following Ofgem’s decision to move to a single cash-out price.

rollout of advanced meters in businesses

more cost-reflective pricing for suppliers and potentially customers with the extension of mandatory half-hourly settlement to business customers (load profile classes 5–8)

the introduction of the Capacity Market’s Early Auction to incentivise capacity to be available in the short term, prior to the first Capacity Market delivery year

better knowledge of I&C customer perception and participation through major surveys – Ofgem and Energyst.

Current work in the following areas is also likely to impact on demand side flexibility:

BEIS and Ofgem Call for Evidence and forthcoming plan on a smart, flexible energy system.

Ofgem’s review of charging arrangements for embedded generators (‘embedded benefits’)8 and associated follow-up targeted charging review.

Ofgem’s plans for a view on future distribution charging reform, signalled in the Call for Evidence.

Ofgem review of System Operator (SO) incentive arrangements; review of certain Capacity Market rules.

Code modification DCP228 impacting Distribution Use of System (DUoS) charges.

European Network Codes – UK implementation.

Government’s work in relation to the outcome of the EU referendum9.

2.6

8 Ofgem (July 2016) Open Letter: Charging arrangements for embedded generation.

9 On 23 June, the EU referendum took place and the people of the United Kingdom voted to leave the European Union. The Government states that until exit negotiations are concluded, the UK remains a full member of the European Union and all the rights and obligations of EU membership remain in force. During this period the Government will continue to negotiate, implement and apply EU legislation. The outcome of these negotiations will determine what arrangements apply in relation to EU legislation in future once the UK has left the EU.

10

Initial metrics for demand side flexibility3.03.1 Context A key challenge for Power Responsive in Year 1 was to draw together data and analysis on the development of demand side flexibility in electricity markets, setting out baseline metrics to assess progress against year on year.

3.2 Contracted markets – Balancing services Balancing services is the most established market for demand side flexibility today. This covers frequency response and reserve services.

a. Total contribution to Balancing services

b. By demand side flexibility category

In future it will be important to develop metrics for the total contribution of demand side flexibility to electricity markets (including value and volume). But this is not currently feasible, because the way of measuring participation in each market differs. Therefore, we have looked separately at: Contracted markets – such as

balancing and capacity – where good data is available

Self-dispatched activity – such as in the wholesale markets and also customer

self-management of their network charges (through peak avoidance) – where there is limited data.

National Grid is working to improve reporting of data on Balancing services and products. For self-dispatched activity considerable gaps remain in the data available. Developing metrics and further data analysis will be a focus for Power Responsive, working with BEIS, Ofgem and Trade Associations in Year 2 – so that the full extent of demand side activity can be assessed across all markets.

The schemes are detailed in Annex B. There are different schemes offering opportunities for different types of demand side participation. Large and energy-intensive industrial customers have engaged with these markets for many years, and wider businesses are beginning

to take part, often via aggregators, suppliers or third-party intermediaries. Many Balancing services were developed with traditional generation in mind, so National Grid is considering ways to ensure a ‘level playing field’ between supply and demand side providers.

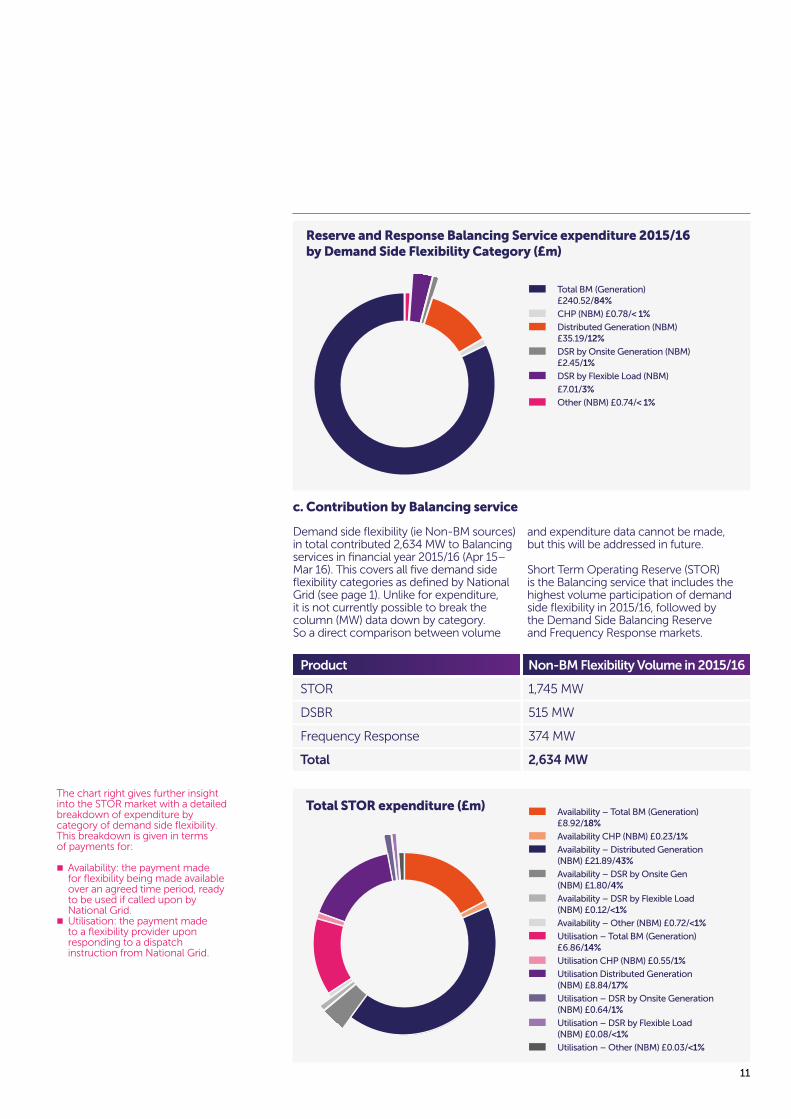

Demand side flexibility constituted 16% of total spend on Balancing services (reserve and response)10 during financial year 2015/16 (Apr 15–Mar 16). The chart

shows this split between BM (balancing mechanism) generation sources and Non-BM sources; i.e. all types of demand side flexibility.

It is helpful to understand the extent to which demand side flexibility is provided by load shifting, generation and/or electricity storage. The assumption is that much demand side flexibility today is provided by onsite/back-up generation. Of the 16% share of demand side flexibility by expenditure in Balancing services –

3% is load response, 1% is demand connected generation (e.g. standby/ back-up), 12% is generation for export, and 1% other. The onsite/back-up generation and generation for export categories both contain all kinds of small generators, including combined heat and power (CHP) and emergency generators.

10 This figure does not include Ancillary Services (such as Blackstart or reactive power), Demand Side Balancing Reserve or Supplementary Balancing Reserve.

Reserve and Response Balancing service expenditure (£m) 2015/16

Generation Balancing Support (BM) £240.52/84%

Total (NBM) £46.16/16%

11

c. Contribution by Balancing service

Demand side flexibility (ie Non-BM sources)in total contributed 2,634 MW to Balancing services in financial year 2015/16 (Apr 15–Mar 16). This covers all five demand side flexibility categories as defined by National Grid (see page 1). Unlike for expenditure, it is not currently possible to break the column (MW) data down by category. So a direct comparison between volume

and expenditure data cannot be made, but this will be addressed in future.

Short Term Operating Reserve (STOR) is the Balancing service that includes the highest volume participation of demand side flexibility in 2015/16, followed by the Demand Side Balancing Reserve and Frequency Response markets.

The chart right gives further insight into the STOR market with a detailed breakdown of expenditure by category of demand side flexibility. This breakdown is given in terms of payments for: Availability: the payment made

for flexibility being made available over an agreed time period, ready to be used if called upon by National Grid.

Utilisation: the payment made to a flexibility provider upon responding to a dispatch instruction from National Grid.

Product Non-BM Flexibility Volume in 2015/16

STOR 1,745 MW

DSBR 515 MW

Frequency Response 374 MW

Total 2,634 MW

Reserve and Response Balancing Service expenditure 2015/16 by Demand Side Flexibility Category (£m)

Availability – Total BM (Generation) £8.92/18%

Availability CHP (NBM) £0.23/1%

Availability – Distributed Generation (NBM) £21.89/43%

Availability – DSR by Onsite Gen (NBM) £1.80/4%

Availability – DSR by Flexible Load (NBM) £0.12/<1%

Availability – Other (NBM) £0.72/<1%

Utilisation – Total BM (Generation) £6.86/14%

Utilisation CHP (NBM) £0.55/1%

Utilisation Distributed Generation (NBM) £8.84/17%

Utilisation – DSR by Onsite Generation (NBM) £0.64/1%

Utilisation – DSR by Flexible Load (NBM) £0.08/<1%

Utilisation – Other (NBM) £0.03/<1%

Total STOR expenditure (£m)

Total BM (Generation) £240.52/84%

CHP (NBM) £0.78/< 1%

Distributed Generation (NBM) £35.19/12%

DSR by Onsite Generation (NBM) £2.45/1%

DSR by Flexible Load (NBM)

£7.01/3%

Other (NBM) £0.74/< 1%

12

Contracted markets – Capacity Market3.3The Capacity Market (CM) aims to ensure that there is sufficient capacity available in the electricity market to meet projected levels of future demand – ensuring security of electricity supply by providing payment to existing and prospective generators and demand side providers, in return for a commitment to provide capacity during a system stress event.

As the Delivery Body for Electricity Market Reform, National Grid runs the main T-4 auction annually, buying capacity for four years ahead of delivery. In the 2015 T-4 auction, ~450 MW of unproven DSR was contracted for £18k per MW for delivery in 2019/20.

Two further auctions exist; the T-1 auction runs one year ahead of delivery as a top-up to secure volume. The first auction, which is known as the “Early Auction”, takes place on 31 January 2017, and is for delivery in Winter 2017/18. The DSR Transitional Arrangements auction offers targeted support to DSR to encourage enterprise and increase levels of participation in the intervening years 2016–2018. In the Transitional Arrangements auction, ~475 MW was contracted for £27.5k per MW for delivery in 2016/17.

It is not currently possible to break the data down by National Grid’s five demand side flexibility categories – as the technology for the majority of DSR is not yet known and also a like-for-like comparison cannot be made as the CM’s definition of DSR is based on demand reduction against an end user’s consumption11.

Some contractual issues remain for demand side providers, in particular contract duration and the requirement for bid bonds. The Government is also considering the role of new diesel farms in the CM and emissions from distributed generation. Reports by IPPR12 and Green Alliance13 suggest that the CM is focused on large power stations at the expense of demand side flexibility.

BEIS has indicated openness to looking at future market design and to considering where there are any existing process barriers to DSR participation that could be addressed without removing transparency or undermining delivery assurance.

One potential measure for future market development will be the number of demand side providers. The number of ‘active’ demand side providers in balancing markets in 2015 was 13. We define ‘active’

demand side providers as aggregators that had a live agreement with National Grid at any point during the year. There were 10 live aggregators in 2014.

11 CM definition of DSR means the activity of reducing the metered volume of imported electricity of one or more customers below a baseline, by a means other than a permanent reduction in electricity use. Therefore new diesel farms (not linked to a customer site) are included under National Grid’s five demand side flexibility categories but not the CM definition of DSR.

12 IPPR (Mar 2016) Incapacitated.13 Green Alliance (Oct 2016) Smart

Investment: Valuing flexibility in the UK electricity market.

3.4 Contracted markets – demand side providers

Contracted future capability –DSR Volume (MW)

Contracted future capability –DSR Spend (£ million)

£4

£0

£2

£6

£8

£10

£12

£14

Delivery Year2016/17

2015 DSR Transitional Auction

Delivery Year2018/19

2014 T-4 Auction

Delivery Year2019/20

2015 T-4 Auction

Tota

l Sp

en

d (

£ m

illio

n)

Proven DSR Contracted Volume (MW)

Unproven DSR Contracted Volume (MW)

Delivery Year2016/17

2015 DSR Transitional Auction

Co

ntr

acte

d V

olu

me

(M

W)

500

400

450

350

300

250

200

150

100

50

0

Delivery Year2018/19

2014 T-4 Auction

Delivery Year2019/20

2015 T-4 Auction

Proven DSR Contracted Volume (MW)

Unproven DSR Contracted Volume (MW)

13

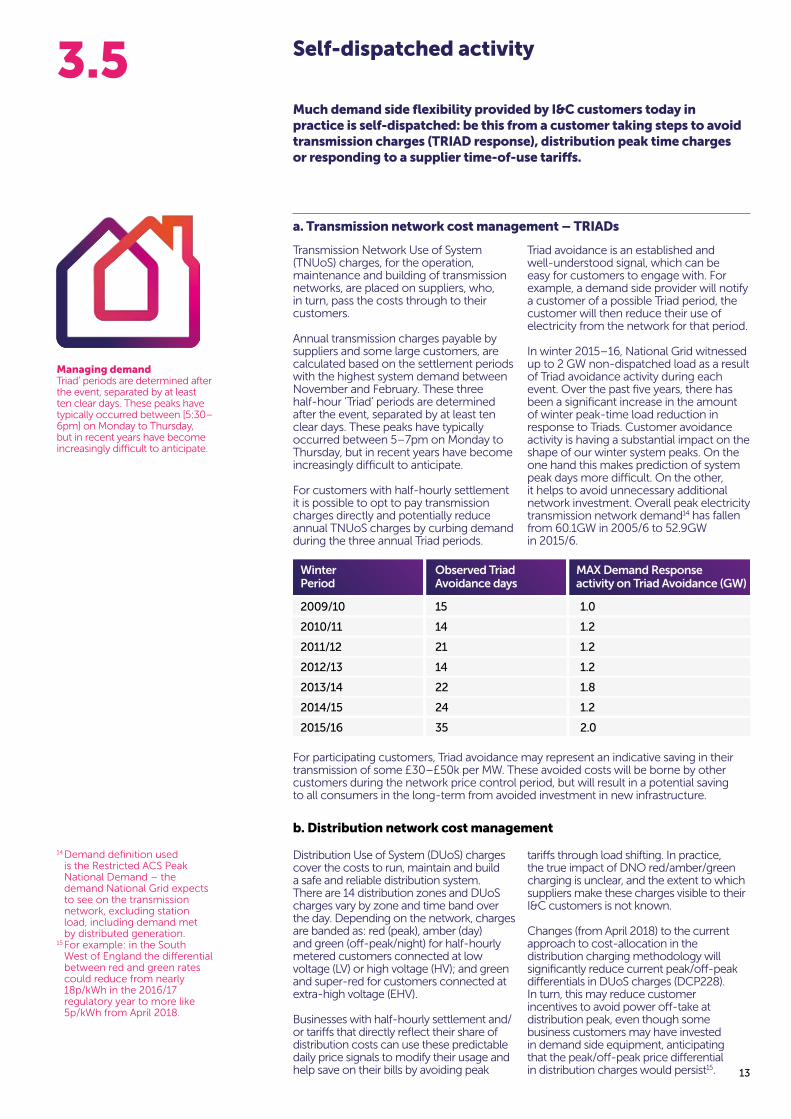

Self-dispatched activity3.5Much demand side flexibility provided by I&C customers today in practice is self-dispatched: be this from a customer taking steps to avoid transmission charges (TRIAD response), distribution peak time charges or responding to a supplier time-of-use tariffs.

Transmission Network Use of System (TNUoS) charges, for the operation, maintenance and building of transmission networks, are placed on suppliers, who, in turn, pass the costs through to their customers.

Annual transmission charges payable by suppliers and some large customers, are calculated based on the settlement periods with the highest system demand between November and February. These three half-hour ‘Triad’ periods are determined after the event, separated by at least ten clear days. These peaks have typically occurred between 5–7pm on Monday to Thursday, but in recent years have become increasingly difficult to anticipate.

For customers with half-hourly settlement it is possible to opt to pay transmission charges directly and potentially reduce annual TNUoS charges by curbing demand during the three annual Triad periods.

Triad avoidance is an established and well-understood signal, which can be easy for customers to engage with. For example, a demand side provider will notify a customer of a possible Triad period, the customer will then reduce their use of electricity from the network for that period.

In winter 2015–16, National Grid witnessed up to 2 GW non-dispatched load as a result of Triad avoidance activity during each event. Over the past five years, there has been a significant increase in the amount of winter peak-time load reduction in response to Triads. Customer avoidance activity is having a substantial impact on the shape of our winter system peaks. On the one hand this makes prediction of system peak days more difficult. On the other, it helps to avoid unnecessary additional network investment. Overall peak electricity transmission network demand14 has fallen from 60.1GW in 2005/6 to 52.9GW in 2015/6.

For participating customers, Triad avoidance may represent an indicative saving in their transmission of some £30–£50k per MW. These avoided costs will be borne by other customers during the network price control period, but will result in a potential saving to all consumers in the long-term from avoided investment in new infrastructure.

Distribution Use of System (DUoS) charges cover the costs to run, maintain and build a safe and reliable distribution system. There are 14 distribution zones and DUoS charges vary by zone and time band over the day. Depending on the network, charges are banded as: red (peak), amber (day) and green (off-peak/night) for half-hourly metered customers connected at low voltage (LV) or high voltage (HV); and green and super-red for customers connected at extra-high voltage (EHV).

Businesses with half-hourly settlement and/or tariffs that directly reflect their share of distribution costs can use these predictable daily price signals to modify their usage and help save on their bills by avoiding peak

tariffs through load shifting. In practice, the true impact of DNO red/amber/green charging is unclear, and the extent to which suppliers make these charges visible to their I&C customers is not known.

Changes (from April 2018) to the current approach to cost-allocation in the distribution charging methodology will significantly reduce current peak/off-peak differentials in DUoS charges (DCP228). In turn, this may reduce customer incentives to avoid power off-take at distribution peak, even though some business customers may have invested in demand side equipment, anticipating that the peak/off-peak price differential in distribution charges would persist15.

b. Distribution network cost management

a. Transmission network cost management – TRIADs

Winter Observed Triad MAX Demand Response Period Avoidance days activity on Triad Avoidance (GW) 2009/10 15 1.0

2010/11 14 1.2

2011/12 21 1.2

2012/13 14 1.2

2013/14 22 1.8

2014/15 24 1.2

2015/16 35 2.0

Managing demandTriad’ periods are determined after the event, separated by at least ten clear days. These peaks have typically occurred between [5:30–6pm] on Monday to Thursday, but in recent years have become increasingly difficult to anticipate.

14 Demand definition used is the Restricted ACS Peak National Demand – the demand National Grid expects to see on the transmission network, excluding station load, including demand met by distributed generation.

15 For example: in the South West of England the differential between red and green rates could reduce from nearly 18p/kWh in the 2016/17 regulatory year to more like 5p/kWh from April 2018.

14

The within-day wholesale market baseload-peak price differential does not currently appear to be a strong driver of demand side flexibility. Some I&C customers have two rate (day/ night-time) tariffs from their suppliers, but this has declined with the growth of flexible contracts. Suppliers typically aggregate shape and balancing risk across their portfolio. With sharper cash-out signals and half-hourly settlement for more customers, supplier products are emerging to support balancing via demand side actions.

Wholesale prices are also becoming more volatile: periods of low prices (caused by renewables generating whenever practicable) interspersed by ‘needle-spikes’ when flexible plant is unexpectedly needed. To date, these price signals are not thought to be driving demand side flexibility behaviours in the wholesale markets. But, in the future, they could be expected to do so.

c. Wholesale market price signal

1.0

1.7

1.6

1.5

1.4

1.2

1.1

1.3

1.9

1.8

Jan 2014 Jul 2014 Jan 2015 Jul 2015

Rat

io

Peaks-o�peaks ratio Linear (Peaks-o�peaks ratio)Peaks-baseload ratio Linear (Peaks-baseload ratio)

Technical potential for demand side flexibility – including by sector and sub-sector.

Customers and assets – number of participating customers, participation by business sector, customer route to market, types of participating asset and visibility of network and other non-energy charges in business customer end-bills.

Network charges and effectiveness of signals to customers – detailed analysis of customer participation in Triads and response to DUoS signals.

Benefits to customers and the system overall – value to participating customers, benefits to all consumers and to the system overall, and carbon abatement implications.

3.6 Areas for further analysis We have identified a number of gaps where further data gathering and analysis could prove valuable to a better understanding of demand side markets today and in future:

Daily peaks-offpeaks/Peaks-baseload ratio based on volume-weighted trades and indices

Source: ICIS

Future development of demand side flexibility markets

In this report, we have begun to pull together a picture of what we know today about the role of demand side flexibility in GB electricity markets. What has emerged is a patchwork. Positive steps are being taken and business customers are beginning to be more aware and engaged. But challenges remain. We will continue to engage business customers and now storage stakeholders in our second year.

Through Power Responsive we have set out a collaborative vision to 2025 for a consumer-empowered future that delivers innovative, cost-effective, low-carbon energy solutions. To achieve this, we need to create consumer value by facilitating access to functioning markets for all parties; both existing and new players.

In Year 2, Power Responsive will focus its efforts on delivering improvements to demand side flexibility markets today. This means looking in the round at products and services and the costs and benefits for customers of participating – making better use of existing assets and investing in new assets where appropriate. It is important that when we make changes to markets, including approaches to network charges, we do so holistically, rather than fixing each issue in turn.

We will look ahead at what success might look like in future, how we get there – making a smooth transition – and how we measure our progress. Developing metrics through data gathering and analysis will be a priority.

We are grateful to all those who have contributed to Power Responsive in its first year. We are particularly grateful to Steering Group members. We look forward to contributing to the ongoing work of BEIS and Ofgem on their Smart Energy Plan and continued work with policy makers, market actors, I&C customers and electricity storage players through Power Responsive in Year 2.

Cathy McClayChair, Power Responsive Steering Group

4.0

15

16

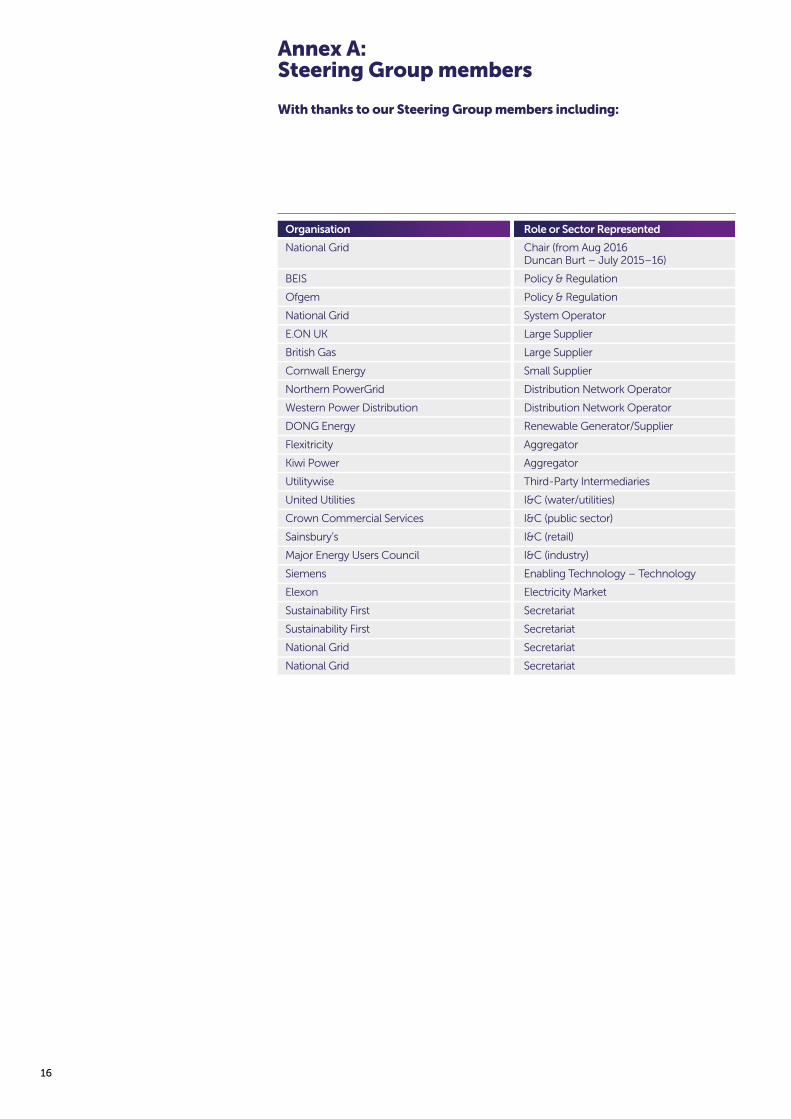

Annex A: Steering Group members

With thanks to our Steering Group members including:

Organisation Role or Sector Represented

National Grid Chair (from Aug 2016 Duncan Burt – July 2015–16)

BEIS Policy & Regulation

Ofgem Policy & Regulation

National Grid System Operator

E.ON UK Large Supplier

British Gas Large Supplier

Cornwall Energy Small Supplier

Northern PowerGrid Distribution Network Operator

Western Power Distribution Distribution Network Operator

DONG Energy Renewable Generator/Supplier

Flexitricity Aggregator

Kiwi Power Aggregator

Utilitywise Third-Party Intermediaries

United Utilities I&C (water/utilities)

Crown Commercial Services I&C (public sector)

Sainsbury’s I&C (retail)

Major Energy Users Council I&C (industry)

Siemens Enabling Technology – Technology

Elexon Electricity Market

Sustainability First Secretariat

Sustainability First Secretariat

National Grid Secretariat

National Grid Secretariat

Include Thank You message incl. to others we have collaborated with

17

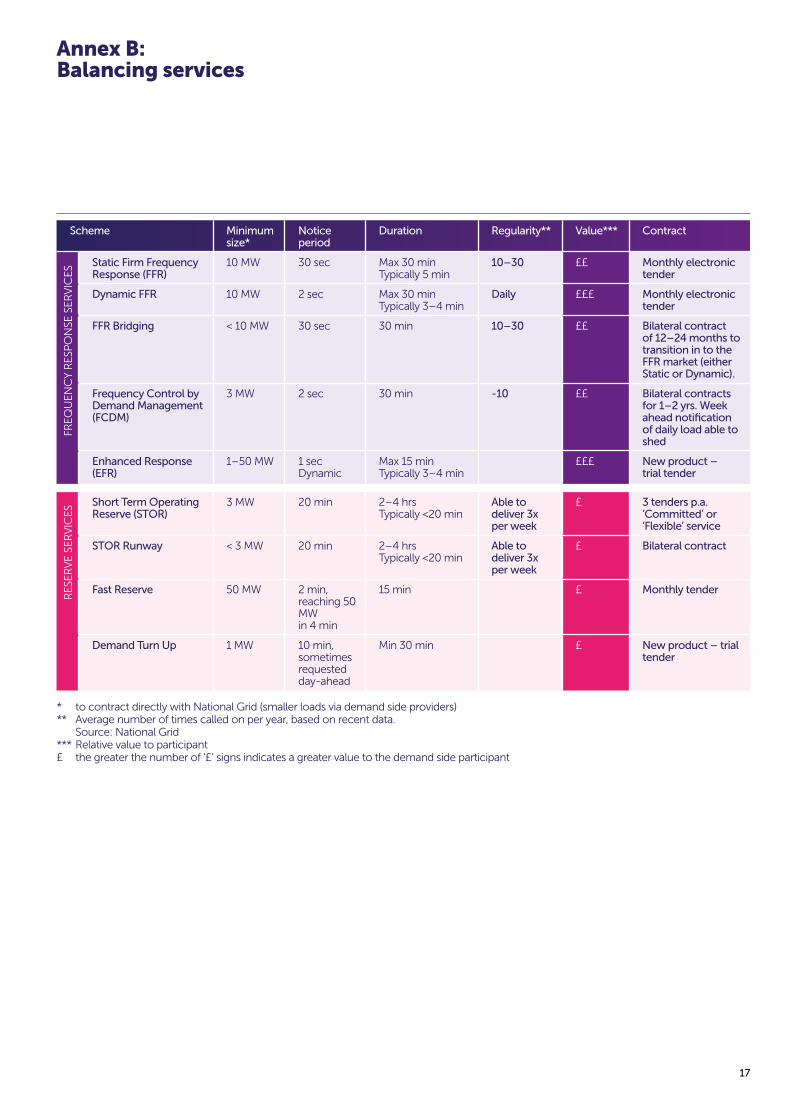

Annex B: Balancing services

Scheme Minimum size*

Notice period

Duration Regularity** Value*** Contract

FREQ

UEN

CY

RES

PO

NSE

SER

VIC

ES

Static Firm Frequency Response (FFR)

10 MW 30 sec Max 30 min Typically 5 min

10–30 ££ Monthly electronic tender

Dynamic FFR 10 MW 2 sec Max 30 min Typically 3–4 min

Daily £££ Monthly electronic tender

FFR Bridging < 10 MW 30 sec 30 min 10–30 ££ Bilateral contract of 12–24 months to transition in to the FFR market (either Static or Dynamic).

Frequency Control by Demand Management (FCDM)

3 MW 2 sec 30 min -10 ££ Bilateral contracts for 1–2 yrs. Week ahead notification of daily load able to shed

Enhanced Response (EFR)

1–50 MW 1 sec Dynamic

Max 15 min Typically 3–4 min

£££ New product – trial tender

RES

ERV

E SE

RV

ICES

Short Term Operating Reserve (STOR)

3 MW 20 min 2–4 hrs Typically <20 min

Able to deliver 3x per week

£ 3 tenders p.a. ‘Committed’ or ‘Flexible’ service

STOR Runway < 3 MW 20 min 2–4 hrs Typically <20 min

Able to deliver 3x per week

£ Bilateral contract

Fast Reserve 50 MW 2 min, reaching 50 MW in 4 min

15 min £ Monthly tender

Demand Turn Up 1 MW 10 min, sometimes requested day-ahead

Min 30 min £ New product – trial tender

* to contract directly with National Grid (smaller loads via demand side providers)** Average number of times called on per year, based on recent data. Source: National Grid*** Relative value to participant£ the greater the number of ‘£’ signs indicates a greater value to the demand side participant

18

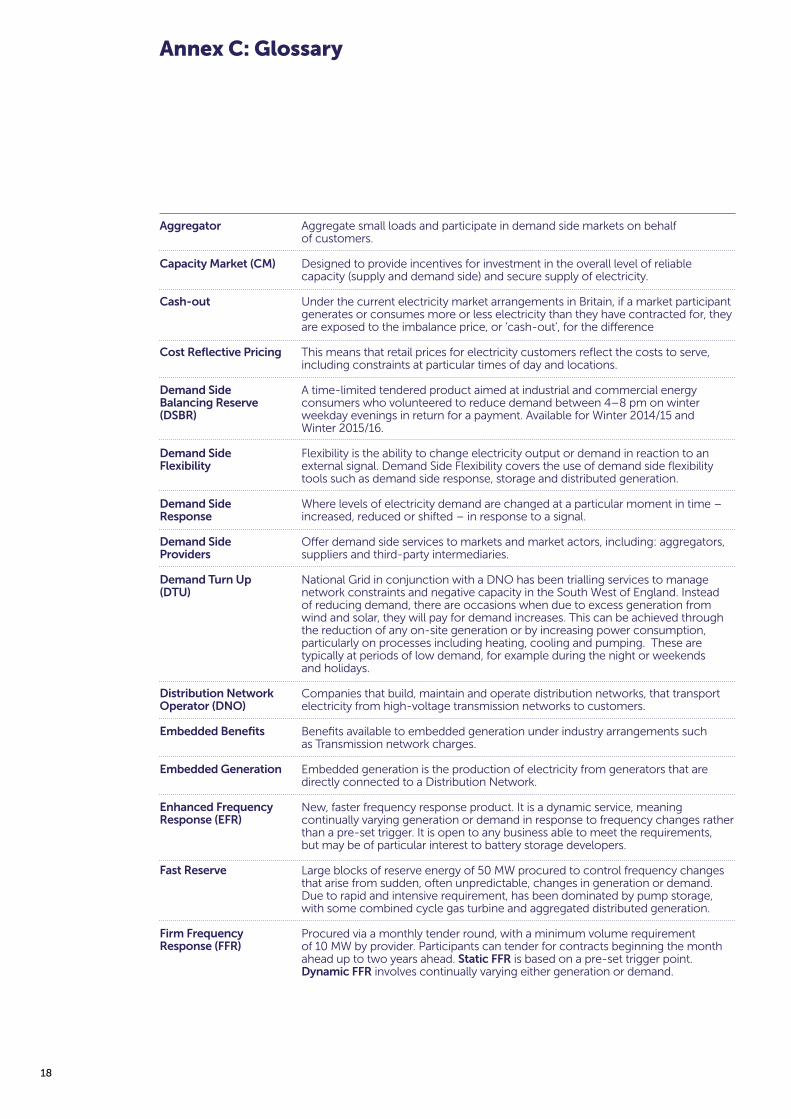

Annex C: Glossary

Aggregator

Capacity Market (CM)

Cash-out

Cost Reflective Pricing

Demand Side Balancing Reserve (DSBR)

Demand Side Flexibility Demand Side Response Demand Side Providers

Demand Turn Up (DTU)

Distribution Network Operator (DNO)

Embedded Benefits

Embedded Generation

Enhanced Frequency Response (EFR)

Fast Reserve

Firm Frequency Response (FFR)

Aggregate small loads and participate in demand side markets on behalf of customers. Designed to provide incentives for investment in the overall level of reliable capacity (supply and demand side) and secure supply of electricity. Under the current electricity market arrangements in Britain, if a market participant generates or consumes more or less electricity than they have contracted for, they are exposed to the imbalance price, or ‘cash-out’, for the difference This means that retail prices for electricity customers reflect the costs to serve, including constraints at particular times of day and locations. A time-limited tendered product aimed at industrial and commercial energy consumers who volunteered to reduce demand between 4–8 pm on winter weekday evenings in return for a payment. Available for Winter 2014/15 and Winter 2015/16. Flexibility is the ability to change electricity output or demand in reaction to an external signal. Demand Side Flexibility covers the use of demand side flexibility tools such as demand side response, storage and distributed generation.

Where levels of electricity demand are changed at a particular moment in time – increased, reduced or shifted – in response to a signal. Offer demand side services to markets and market actors, including: aggregators, suppliers and third-party intermediaries. National Grid in conjunction with a DNO has been trialling services to manage network constraints and negative capacity in the South West of England. Instead of reducing demand, there are occasions when due to excess generation from wind and solar, they will pay for demand increases. This can be achieved through the reduction of any on-site generation or by increasing power consumption, particularly on processes including heating, cooling and pumping. These are typically at periods of low demand, for example during the night or weekends and holidays. Companies that build, maintain and operate distribution networks, that transport electricity from high-voltage transmission networks to customers. Benefits available to embedded generation under industry arrangements such as Transmission network charges. Embedded generation is the production of electricity from generators that are directly connected to a Distribution Network. New, faster frequency response product. It is a dynamic service, meaning continually varying generation or demand in response to frequency changes rather than a pre-set trigger. It is open to any business able to meet the requirements, but may be of particular interest to battery storage developers. Large blocks of reserve energy of 50 MW procured to control frequency changes that arise from sudden, often unpredictable, changes in generation or demand. Due to rapid and intensive requirement, has been dominated by pump storage, with some combined cycle gas turbine and aggregated distributed generation.

Procured via a monthly tender round, with a minimum volume requirement of 10 MW by provider. Participants can tender for contracts beginning the month ahead up to two years ahead. Static FFR is based on a pre-set trigger point. Dynamic FFR involves continually varying either generation or demand.

19

Annex C: Glossary

FFR bridging

Frequency Control by Demand Management (FCDM)

Frequency Response

Half-Hourly Settlement

Industrial and Commercial (I&C) Customers

Reserve Services

Short Term Operating Reserve (STOR)

Supplemental Balancing Reserve (SBR)

System Operator (SO) Time-of-use (TOU)tariffs

Third-Party Intermediaries (TPI)

Transmission Network Operator (TNO)

Triad Avoidance

Virtual Power Plant

A bilateral agreement for businesses unable to meet 10 MW threshold, to build volume over 1–2 years, paid an agreed fee per MW.

Service that helps prevent dramatic falls in frequency by automatically interrupting the demand of customers that use large amounts of electricity (more than 3 MW) when the frequency falls below a trigger point of 49.7Hz.

System frequency is a continuously changing variable that is determined and controlled by the second-by-second balance between system demand and total generation. National Grid must maintain a frequency of +/- 1% of 50Hz at all times, so procures frequency services in readiness to manage fluctuations in electricity demand or generation from forecast volumes or to withstand faults to the network or connected generation.

The electricity settlement process places incentives on suppliers to buy energy to meet their customers’ demand in each half hour of the day. With advanced meters, businesses customers are increasingly able to have their electricity consumption settled on a half-hourly basis.

This refers to large business customers of electricity, including those manufacturing goods and those serving customers. We include public sector organisations in this category.

In order to deal with unforeseen changes in demand or lack or generation, National Grid requires access to additional sources of power in the form of generation or demand reduction. The response time and duration is typically longer for reserve services than frequency.

Is a service for the provision of additional active power from generation and/or demand side response. STOR is needed because at certain times of the day National Grid needs reserve power in the form of either generation and/or demand reduction in order to be able to deal with actual demand being greater than forecast demand and/or plant failure.

SBR is targeted at generators who would otherwise be closed, mothballed or generally unavailable to the market, and would only be used as a last resort by the system operator after all commercial balancing actions have been taken.

Manages the national electricity system on a second-by-second basis to ensure supply meets demand and maintain a steady frequency.

Energy companies charge different amounts for electricity depending on the time of day it is used.

Are organisations or individuals that give energy-related advice, aimed at helping customers to buy energy and/or manage their energy needs.

Companies that build, maintain and operate transmission networks, transporting electricity at a high-voltage across the country.

Reducing consumption at periods where peak winter national demand is forecast, in order to proportionally reduce TNUoS (Transmission Network Use of System) charge.

A system that integrates several types of power sources, (e.g. microCHP, wind-turbines, small hydro, photovoltaics, back-up generation, demand side response and batteries) so as to give a reliable overall power supply.

20

Turn debate into action be Power Responsive

Power Responsive is a practical platform to galvanise businesses, suppliers, policy makers and others to shape demand side flexibility collaboratively and deliver it in practice at scale by 2020. Together, we can shape and share the possibilities created by demand side solutions.

Find out more atwww.powerresponsive.comTel: 01926 654611

With thanks to Sustainability First for their continued contribution to the Power Responsive programme of work.

21

22 www.powerresponsive.com