DELIVERING END-TO-END SERVICES

56

IN A HYPER-CONNECTED WORLD November 2015 | www. tmforum.org Sponsored by: INSIGHTS RESEARCH DELIVERING END - TO - END SERVICES Free to tmforum members $495 where sold

-

Upload

ibrahim-jawad -

Category

Documents

-

view

229 -

download

5

description

DELIVERING END-TO-END SERVICES

Transcript of DELIVERING END-TO-END SERVICES

IN A HYPER-CONNECTED WORLD

November 2015 | www.tmforum.org

Sponsored by:

I N S I G H T S R E S E A R C H

DELIVERING END-TO-END SERVICES

Free to tmforum members $495 where sold

Are you ready to shape the future of digital business?Collaborate with these leading companies on Customer Centricity.

Get engaged in the community atwww.tmforum.org/customercentricity

TM

IoTSampleAd.indd 1 11/14/14 11:39 AM

3www.tmforum.org INSIGHTS RESEARCH

© 2015. The entire contents of this publication are protected by copyright. All rights reserved. The Forum would like to thank the sponsors and advertisers who have enabled the publication of this fully independently researched report. The views and opinions expressed by individual authors and contributors in this publication are provided in the writers’ personal capacities and are their sole responsibility. Their publication does not imply that they represent the views or opinions of TM Forum and must neither be regarded as constituting advice on any matter whatsoever, nor be interpreted as such. The reproduction of advertisements and sponsored features in this publication does not in any way imply endorsement by TM Forum of products or services referred to therein.

Page 4The big picture

Page 6Section 1Betting the business on digital services

Page 9Section 2Service providers speak: Why the Internet of Everything needs new business models

Page 15Section 3Shining the spotlight on business challenges

Page 20Section 4Navigating the operational roadblocks

Page 24Section 5Creating a global ecosystem

Page 31Section 6Make it happen: Six strategies for delivering digital services – and a ready-to-go toolkit

Page 38Sponsored features

This report is free for all employees of TM Forum member organizations to download by registering on our website. To purchase this report, non-members should contact [email protected]

Report author:Nancee RuzickaPresident and Founder, ICT Intuition [email protected]

Senior Director, Editorial:Annie [email protected]

Managing Editor:Dawn [email protected]

Editor, Digital Content:Sarah [email protected]

Manager, Content Production:Paul [email protected]

Business Development Director, Research & Publications:Mark [email protected]

Director, Solutions Marketing: Charlotte [email protected]

Senior Director, Content:Aaron Richard Earl [email protected]

Advisors:Nik Willetts, Deputy CEO & Chief Digital Officer, TM ForumCraig Bachmann, Senior Director, Open Digital Program, TM ForumRebecca Sendel, Senior Director, Customer Centricity Program, TM Forum

Report Design:thePAGEDESIGN

Published by:TM Forum240 Headquarters PlazaEast Tower, 10th FloorMorristown, NJ 07960-6628USAwww.tmforum.orgPhone: +1 973-944-5100Fax: +1 973-944-5110

ISBN: 978-1-939303-88-2

DELIVERING END-TO-END SERVICES IN A HYPER-CONNECTED WORLD

4 www.tmforum.orgINSIGHTS RESEARCH

DELIVERING END-TO-END SERVICES IN A HYPER-CONNECTED WORLD

Welcome to TM Forum’s first-ever Insights Research report focusing on the delivery of end-to-end services in digital ecosystems made up of many partners.

There is a distinction to be made between modernization, which is necessary for any business to keep current, improve its products and grow revenue, and transformation, which is a once-in-a-generation fundamental change to the identity of the business.

By 2020 the digital world will consist of tens of billions of devices, with an unlimited variety of applications delivered over highly scalable, virtualized infrastructure using distributed intelligence.

The move from communications service provider to digital service provider is transformational, and the ability of all digital service providers to configure and deliver end-to-end services seamlessly to millions of users accessing billions of devices will determine future success.

Communications have evolved from convenience to necessity. For customers, there is no longer fixed or wireless, voice, data or video – only devices and applications. Televisions, handsets, vehicles, sensors and any variety of ‘things’ are the devices, while voice, text, video, banking, spreadsheets, payroll, supply chain and more are applications in the cloud. Connectivity is transparent, and delivering reliable digital services requires the seamless integration of multiple partners and technology suppliers worldwide.

This report examines the progress and challenges associated with delivery of complex digital services in the Internet of Everything (IoE). While many efforts are underway or under consideration, very few digital service providers have completed the heavy lifting required to establish the foundation for digital services, nor have they defined a global ecosystem strategy or developed the necessary relationships with partners. All-in-all the delivery of end-to-end digital services remains a work in progress, but one that is ripe for innovation.

Transforming in a hyper-connected world

No longer just nice to have

The big picture

5www.tmforum.org INSIGHTS RESEARCH

We hope you enjoy the report and, most importantly, will find ways to use the concepts and recommendations detailed within. You can send your feedback to the TM Forum editorial team at [email protected].

Read this report to understand key issuesfor delivering end-to-end digital services

Read this report to understand:

What a digital service provider is.

Why the alternative business structures needed to sustain global ecosystems and partnerships are difficult to initiate and even more difficult to execute correctly.

What the most significant and difficult changes to the business and to operations will be for communications service providers transforming into digital service providers.

What the current state of play is in the IoE and the challenges associated with delivering the complex digital services required to make IoE successful for customers in any industry.

The role partners play in delivering IoE connectivity and how much progress has been made in developing partnerships.

Why security is so important.

What this means for you. What actions should you take now, and which tools will help you get there?

6 www.tmforum.orgINSIGHTS RESEARCH

DELIVERING END-TO-END SERVICES IN A HYPER-CONNECTED WORLD

SECTION 1

Betting the business on digital servicesMany industries are reinventing themselves by connecting users, customers, locations and things to move their organizations forward. Transportation, shipping, energy, healthcare, retail, safety, government, financial services and other verticals are anxious to embrace the opportunity the Internet of Everything (IoE) presents. To do this, they need solutions for digital communication.

Network technology has crossed the threshold from being value-added to mission-critical in most businesses. Business domains, supply chains and distribution have become even more diverse and far flung. That leaves business leaders to answer an important question: “Do we continue to invest in the

infrastructure and skills necessary to build, operate and maintain the required global critical infrastructure, or do we rely on digital service providers, some of whom have been making these investments and innovations for more than 100 years?”

BUILD OR BUY?

Enterprises can build their own global infrastructure

buy digital services from vetted providersOR

7www.tmforum.org INSIGHTS RESEARCH

Business as usual is almost impossible, given the number of products customers are demanding

For communications service providers, fundamental changes in infrastructure, competition and costs have always been the catalyst for restructuring the core business, but no change is more significant than the move to digital services.

Given the number of products that customers are demanding, the complexity of delivering and supporting each, combined with the need to ensure quality, ease-of-use and support, makes business-as-usual nearly impossible.

To that end, network operators are implementing business and technological changes to accommodate digital services business models.

Simultaneously organic, or native, digital service providers (companies like Microsoft, Amazon, Facebook and a fast-growing number of Internet of Things startups) are delivering services directly to end customers over existing communications networks.

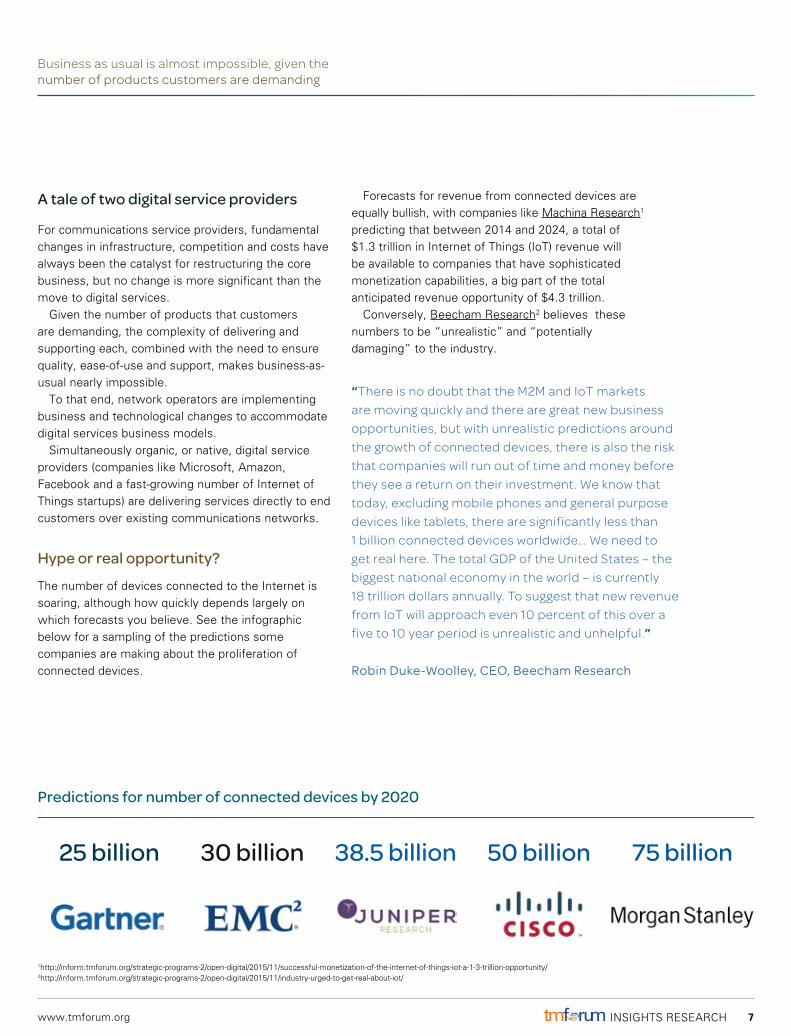

The number of devices connected to the Internet is soaring, although how quickly depends largely on which forecasts you believe. See the infographic below for a sampling of the predictions some companies are making about the proliferation of connected devices.

Forecasts for revenue from connected devices are equally bullish, with companies like Machina Research1 predicting that between 2014 and 2024, a total of $1.3 trillion in Internet of Things (IoT) revenue will be available to companies that have sophisticated monetization capabilities, a big part of the total anticipated revenue opportunity of $4.3 trillion.

Conversely, Beecham Research2 believes these numbers to be “unrealistic” and “potentially damaging” to the industry.

A tale of two digital service providers

Hype or real opportunity?

“There is no doubt that the M2M and IoT markets are moving quickly and there are great new business opportunities, but with unrealistic predictions around the growth of connected devices, there is also the risk that companies will run out of time and money before they see a return on their investment. We know that today, excluding mobile phones and general purpose devices like tablets, there are significantly less than 1 billion connected devices worldwide… We need to get real here. The total GDP of the United States – the biggest national economy in the world – is currently 18 trillion dollars annually. To suggest that new revenue from IoT will approach even 10 percent of this over a five to 10 year period is unrealistic and unhelpful.”

Robin Duke-Woolley, CEO, Beecham Research

1http://inform.tmforum.org/strategic-programs-2/open-digital/2015/11/successful-monetization-of-the-internet-of-things-iot-a-1-3-trillion-opportunity/2http://inform.tmforum.org/strategic-programs-2/open-digital/2015/11/industry-urged-to-get-real-about-iot/

Predictions for number of connected devices by 2020

25 billion 30 billion 38.5 billion 50 billion 75 billion

8 www.tmforum.orgINSIGHTS RESEARCH

DELIVERING END-TO-END SERVICES IN A HYPER-CONNECTED WORLD

Many service providers recognize that their current operational mindset is closer to that of a utility than a retailer. Their business is not built to compete but rather to deliver ubiquity, consistency and quality. Every customer gets the same service the same way, and quality is universally high, regardless of cost. Changing that culture to one of tiered quality, service level agreements, product variety and one that accepts that “the customer is always right” in a competitive global marketplace is a lot to overcome.

We’ll discuss this more in the next sections, where we provide the detailed results of our research.

Despite the discrepancies in market projections, it’s clear there is a huge opportunity for both native digital service providers and communications service providers looking to become digital providers. The native providers have an advantage because their businesses are already software-defined and operating in the cloud. This means they can create and retire services rapidly, and increasingly they are controlling the relationship with the customer.

In an effort to compete more effectively, communications service providers are divesting the product business from the regulated infrastructure business. Structurally separating this new end-to-end services business from the core network infrastructure business, centralizing product management and aligning product development efforts across the business will improve time to market for new services, reduce costs and improve customer experience.

How to become a digital service provider

“Expanding expectations and rapid delivery, all while maintaining a long-term competitive cost structure in a perceived commodity industry, requires transformation. Growing threats from traditional, non-related industries present long-term challenges.”

North American communications service provider

of respondents to our survey are considering or completing the creation of a separate digital services business

82%

9www.tmforum.org INSIGHTS RESEARCH

SECTION 2

Service providers speak: Why the Internet of Everything needs new business models

Details of how we conducted our primary research for this report and with whom

WHO?

40 SERVICE PROVIDERSWhile the majority of companies were telecommunications service providers, we also have included responses from enterprises that represent connected car, digital health, retail, social media and IT services.

HOW?

ONLINE SURVEY AND TELEPHONE INTERVIEWS

WHERE? TYPE OF SERVICE PROVIDER

Source: TM Forum, 2015

LATIN AMERICA/CARIBBEAN EUROPE/RUSSIA

GLOBAL NORTH AMERICA

ASIA/PACIFICMIDDLE EAST/AFRICA

68% Telecommunications

20% IT

5% Online retail

3% Media & Social media

2% Connected car

2% Digital health

10 www.tmforum.orgINSIGHTS RESEARCH

DELIVERING END-TO-END SERVICES IN A HYPER-CONNECTED WORLD

To describe their digital services organizations, respondents were asked to characterize them as one of four types:

n End-to-end digital service providers offer products that include devices, connectivity, content and support services (for example, TV programming, eBooks, supply chain management, home health monitoring, energy management, telematics), often delivered using partners and a retail ecosystem. Retail solutions can also include exposure of fulfillment, assurance and billing/settlements functionality for self-care and channel/partner support.

n Digital enablers offer integration of connectivity, infrastructure, hosting, content, applications, integration or professional services that enable others to become retailers of end-to-end digital services. This includes one or more components of an end-to-end digital service but cannot be sold as turn-key and requires components from partners.

How do you deliver services?

End-to-end digital service provider

n Digital suppliers provide components, bandwidth, rack space, collocation facilities, power, cooling, switches, security, operations, maintenance and data center infrastructure that are often accompanied by strict service level agreements, performance and quality requirements. Service providers that sell only bandwidth services (vLAN, carrier Ethernet) and data center or hosting facility operators are here defined as suppliers.

n Digital global alliance brokers maintain arrangements and negotiate settlements with global suppliers for access, connectivity, payment processing and physical presence in markets worldwide.

Digitalenabler

Digitalsupplier

Digital global alliance broker

47.5% 42.5% 25% 15%

TM Forum IoE survey respondents fall into four categories

11www.tmforum.org INSIGHTS RESEARCH

Most service providers are starting with connected vehicles, homes and smart energy

The majority of survey respondents serve fewer than 5 million customers which is indicative of the market overall (see Figure 2-1). In addition, some of the largest network operators in the world, which are making great strides in delivering digital services, also provided their input. The individuals surveyed represent executives, marketing, technical and business leaders who are working to define, market, deliver and support end-to-end digital services for their retail and business customers.

As we outlined in Section 1, the IoE opportunity for digital service providers is potentially huge. We asked survey respondents which Internet of Things or machine-to-machine services they offer now and which they intend to offer in two years’ and five years’ time. The results are shown in Figure 2-2.

Service providers are prioritizing delivery of IoE services based on their specific customers, regions and expertise. For the early services including energy, connected home, smart city and digital health, the number of service providers delivering services to each sector now, versus two or five years from now, is evenly split. This indicates the varying priorities of providers.

While not all digital service providers are entering every market, most are starting with connected vehicles, connected home or smart energy. As with any product, digital services require a valid business case, quantifiable revenue opportunity and review of risk.

They are delaying going to market in areas like smart agriculture, telematics for insurance and wearables while they wait for demand to increase, the variety and cost of unique devices to drop, and/or the standardization of interfaces so that delivering services becomes less risky and costly.

Figure 2-1: Number of customers served

Source: TM Forum, 2015

Smart energy

Connected home

Smart city

Digital health

Connected vehicle

Wearables

Insurance telematics

Smart agriculture

0% 20% 40% 60% 80% 100%

Now Next 2 years Next 5 years

Sizing the service providers

Which smart services do you offer?

Figure 2-2: Deployment of IoE services

Source: TM Forum, 2015

Waiting for a market

Fewer than 5 million 5 million to 25 million 25 million to 50 million 50 million to 100 million 100 million to

150 million More than 150 million

42.5%

25.0%

17.5%

2.5%

5.0%

7.5%

Making connections

NOW

Connected vehicles

LATER

Connected home

Smart energy

Smart agriculture

Telematics for insurance

Wearables

12 www.tmforum.orgINSIGHTS RESEARCH

DELIVERING END-TO-END SERVICES IN A HYPER-CONNECTED WORLD

For communications service providers, offering digital services requires a change in operating processes, systems and likely even personnel. They need to shift from an approach that delivers the same service to every customer to a strategy that delivers a unique product to every customer.

The daily operation and management of the infrastructure, service and partner assets required to deliver thousands of unique digital services will become a continuous challenge to ensure quality of the service, product performance and customer satisfaction. Efficient operations and economies of scale dictate that standardized processes, applications, networks, data models and interfaces be adopted.

Customers are unique

Business priorities today include changes to organizations, processes, services, partner relationships and operations

Execution and optimization

Figure 2-3: Progress on execution and optimization

Source: TM Forum, 2015

Business leaders are currently emphasizing the execution of their digital services strategies, and they are re-engineering processes and implementing back-office systems to support delivery of digital services. Our research shows that more than 80 percent of service providers are either considering or doing both (see Figure 2-3).

Process changes are especially risky for digital service providers since many have not focused on process in the past and are often ill prepared to engage in the type of overarching analysis and mapping required to define an entirely new process. Existing functions are so embedded in the culture and operations of their businesses that it becomes very

Done

In progress

Seriously considering

Considering

Not now

7.5%

Execution of digital services strategy Process re-engineering/optimization

7.5%

12.5%

22.5% 50.0%

7.7%10.3%

15.4%

23.1%

43.6%

13www.tmforum.org INSIGHTS RESEARCH

Systems implement processes and incorrect processes prevent change

difficult to step out of the tactical world and suddenly become strategic. However, as leading digital service providers know, systems implement processes and if they get the processes wrong nothing will change.

AT&T recognizes this, which is why the company has embarked on a multi-year transformation3 of its operational and business support systems (OSS/BSS) to support network virtualization and the IoE. AT&T is using TM Forum’s Frameworx4 suite of tools and best practices (see page 29) along with some of its own frameworks and processes, to transform the entire software delivery lifecycle from service concept through to measuring customer experience.

Transformation at AT&T

“The goal is to provide reduced cycle time to the end customer with new market offerings. More than anything else, it’s about providing them features and services – fast. A lot of the work we’re doing internally is to automate provisioning, service assurance efforts, ticketing, fault detection. Those are all software IT projects. If we can do them faster, we can actually provide the end customer reduced cycle time for obtaining services from AT&T.”

Sorabh Saxena, Senior Vice President, Software Development and Engineering, AT&T Services

We asked survey respondents to indicate what kinds of business changes are underway to support new business models. The results are shown in Figure 2-4.

As we noted in Section 1, a large majority of communications service providers (82 percent) are either already separating or considering separating the expensive, regulated network business to compete with over-the-top (OTT) providers.

Companies with trusted brands can design, sell and bill for connected products, professional services, secure transaction processing and content, while remaining competitive with companies without expensive network infrastructure.

Out with the old

Figure 2-4: Changes to support new business models

Source: TM Forum, 2015

3http://inform.tmforum.org/features-and-analysis/featured/2014/10/technology-transformation-att-sets-stage-virtualization/4https://www.tmforum.org/tm-forum-frameworx/

Align product development across internal & external assets

Centralize end-to-end product management

Create professional services groups

Create industry-specific sales and support groups

Create global partner strategy for industry-specific solutions

Create new business unit/structural separation

Create global partner strategy for support

Create global partner strategy for infrastructure

Create global partner strategy for content

0% 20% 40% 60% 80% 100%

Not now Considering Seriously considering In progress Done

14 www.tmforum.orgINSIGHTS RESEARCH

DELIVERING END-TO-END SERVICES IN A HYPER-CONNECTED WORLD

Transformation requires disconnecting online and automated order management, customer care, and support from specific silos of systems to enable management of relationships with global partners and suppliers.

Engaging with partners that provide infrastructure, content and support needs service providers to implement and optimize end-to-end processes for product development, order management, customer support, service delivery, billing, settlements and assurance. They must also make the on- and off-boarding processes simple and secure.

For example, nearly 45 percent of communications service providers we surveyed have already forged or are in the process of creating global infrastructure partnerships, and another 20 percent are seriously considering it. More than a quarter have also started building global partnerships for customer support and content, although close to 40 percent of respondents said they are not yet working on or considering content deals.

It takes two to tango

Delivering Internet of Everything (IoE) connectivity and complex digital services requires pre-integration of partners and applications. To that end, companies are taking steps in their local markets to align product development across their internal assets and those of their partners. Close to 60 percent of respondents said they have already or are working on aligning product development, while another 20 percent are seriously considering it.

Toward this end, service providers also are establishing professional services organizations and creating sales and support groups with the unique knowledge and skills required to target specific industries and customers.

B2B2X Step-by-step Partnering Guide5

Learn about the 5 stages of building and scaling partnerships

Pre-integration is required

5https://www.tmforum.org/open-digital-ecosystem-2/#b2b2x

Grab your partner

Most service providers are already creating or seriously considering global partnerships for

64% Infrastructure

57% Support

Content 51% While a majority of the service providers surveyed want to pursue centralized digital services business strategies and 30-40 percent are actively implementing changes, the data also shows that less than a quarter have actually completed their efforts. And when the discussion turns to global strategies for infrastructure, content and support partnerships, only 5 percent or fewer have defined those strategies and relationships. But the efforts are well underway and are starting to deliver some results.

We’ll examine the role of partnerships in more detail in Section 5.

Streamline for simplicity

aligning product development internally

50% establishing professional services

creating industry-specific sales and support

47.5%

57.5%

15www.tmforum.org INSIGHTS RESEARCH

SECTION 3

Shining the spotlight on business challenges

Native digital providers already operate in the cloud, and virtualization technology is now enabling network operators to evolve from traditional suppliers of separate, network-dependent services into cloud providers. But the transformation comes with significant challenges, most of which are business and operational roadblocks rather than technological.

We asked survey respondents to indicate the most significant business challenges they face in executing their strategies for defining and delivering end-to-end digital services. The results are shown in Figure 3-1.

Given that the majority of survey respondents are communications service providers, it’s not surprising that culture and mindset tops the list of challenges. In fact, only 10 percent of respondents said culture is not an issue.

It’s also not surprising that defining a digital services strategy is perceived as a challenge – nearly all respondents cited it as a significant or potential issue – since this is a new world for network operators.

Moving to cloud-based technologies and virtualization brings challenges, mostly operational and business

Figure 3–1: Business challenges in the Internet of Everything

Source: TM Forum, 2015

Culture/mindset

Security/privacy

Standards (or lack of )

Cost

Process/organizational changes

Definition of digital services strategy

Regulatory

Organizational/cultural issues

Leadership and ongoing support

Availability of technology and support solutions

0% 20% 40% 60% 80% 100%

Not an issue May be a concern Significant challenge

16 www.tmforum.orgINSIGHTS RESEARCH

DELIVERING END-TO-END SERVICES IN A HYPER-CONNECTED WORLD

Number two among the challenges in our survey is security, which also is no surprise. The need to develop secure software and components becomes even more apparent with IoE and cloud, where multiple third-party providers work together to deliver mission-critical services.

Financial services, hospitality, and retail businesses are still the primary targets of data breaches because of their wealth of information and also due to their wide physical distribution. However as other industries begin to deploy connected devices across large geographies, there will be millions of new access points for hackers to exploit.

To address security, controls must be designed into components, devices, operations and applications. There are methods for including security in all these stages of development. However, go-to-market urgency and short-term cost savings often mean that security is overlooked until late in the day. This must change so that security is designed in from the ground up.

One key consideration is which traffic gets filtered. Most enterprises filter only the traffic coming into the organization, not outbound traffic. Yet if a remote device has been compromised and is being used to collect unauthorized data, it can be detected by monitoring outbound traffic and stopped. Millions of connected devices will have predictable traffic patterns, which should make anomalies easy to spot – so long as someone is looking.

Closely related to the issue of culture is leadership. When the economy is booming and revenues abound, leadership is less critical to the perceived success of a business. However, when a service provider is faced with a perfect storm of large and start-up competitors, exploding demand and a challenging economy, strong leadership is essential.

Some companies believe they already have the necessary leadership to transform to digital service providers, while others are bringing in new blood from other industries including retail.

For example, BT has tapped technology and business leadership from the finance and

Worries about security Security and privacy in the Internet of Everything

The importance of leadership and support

A recent TM Forum Catalyst project6 showed how to design security into a hybrid or virtualized environment

6http://inform.tmforum.org/features-and-analysis/featured/2015/06/catalyst-unified-api-enables-operators-to-offer-security-as-a-service/

Taking the lead

92.5%say security is a significant challenge or may be a concern

67.5%say leadership is a significant challenge or may be a concern

17www.tmforum.org INSIGHTS RESEARCH

Each digital service provider will find its own way, but foundational efforts must come from leaders

manufacturing sectors, while T-Mobile USA hired a CIO who worked for retailers like Avon, Barnes & Noble and Chico’s.

Although each digital service provider will find its own way through the transformation minefield, there are long-term foundational efforts that must originate in the executive suite. Without strong leadership in these areas, the transition won’t be successful.

Investment and planning: The clearest indicator of commitment to transformation is the allocation of budget and definition of a strategic plan for change to every part of the business. As executives develop digital service strategies and set investment priorities, it is critical to communicate that change is coming and that everyone is obligated to make it happen.

Teaching the message: Communicating the intent, plan, successes, failures and progress is critical to changing the culture. Training that reinforces key strategies and intent is important, as is ‘practicing what you preach’. And any product or service innovation that is offered to customers should be used internally.

Relentless execution: Leadership has a tendency to lose focus once a major effort is underway and projects are being executed, but that’s when executives need to remain engaged. The CEO of a large North American digital service provider conducts monthly reviews of projects to ensure that each stays on track and delivers the intended customer and business benefits. On- and off-boarding partners will be a continuous challenge and one that digital service providers must continuously refine and manage.

In addition to concerns about culture and strategy, there are organizational challenges associated with the structuring of the business, as well as the processes

3 key leadership roles

and staffing required to develop innovative solutions and execute the sale and delivery of new digital services to a variety of customers.

Service providers, like every other business, are facing a shortage of critical skills as the demand for experienced developers, data scientists and engineers is increasing.

For companies venturing into adjacent and connected industries like automotive or healthcare, there is also a need for personnel with experience in those industries who understand the unique needs of the business and which services are valued at what price.

Lack of critical skills

The skill sets required to configure, operate and maintain existing products and infrastructure are very different from what is required to deliver complex digital services. Automation is essential to reduce costs, ensure accuracy and improve time to market.

Alternatively, outsourcing of legacy infrastructure or product management might better control the costs associated with operating and maintaining legacy products. However, demand for the highly skilled engineering, IT, operations and support personnel required to deliver transformation remains unsatisfied and is cited as a significant risk by nearly half of the digital service provider executives included in this research.

“Culture, skill set and a willingness to work on each are the major challenges that face our industry.”

Asian communications service provider

Staffing and skills shortages are an issue for IoE

87.5%say the shortage of skills is a significant challenge or may be a concern

18 www.tmforum.orgINSIGHTS RESEARCH

DELIVERING END-TO-END SERVICES IN A HYPER-CONNECTED WORLD

While digital service providers spend a lot of time and money to support the volume of traffic, devices, users, data and applications in today’s networks, the explosion in mobile data only hints at the problems that will be magnified by virtualization and the IoE.

Tons of transactions: Service providers already handle trillions of transactions and millions of health and status events from network elements, IT elements, customer devices, services, applications and users. In ten years, the number of IoE devices is estimated to be ten times the number of existing mobile devices, which means the volume of data, number of connections and operational events increase by orders of magnitude.

Not just the network: To support the IoE, OSS/BSS also has to scale – not only to manage hundreds of thousands of subscribers but also to accommodate hundreds of unique service instantiations. When millions of end-point devices, servers, storage and applications are added that must be delivered in a secure multi-tenant fashion, scale and complexity are multiplied.

Deliver the data: In the IoE, data will be collected and delivered to a wide variety of applications that can make use of it. There will be many variables associated with delivering data for each customer, including collection frequency, volume, storage, parsing and correlation. Policies will have to be applied to dynamically direct when data is collected, how often and where it is sent.

Signs of things to come

Big changes to operations

Nobody rides for free: Each participating provider, partner and business will want to be paid. The challenges that exist around accurately collecting transaction data, billing multiple parties, reconciling payments to numerous providers, revenue assurance and fraud are monumental. Existing OSS/BSS are rapidly being replaced and upgraded to add flexibility, but not all solutions will be capable of meeting the demands of multi-tenant digital services across various industry verticals.

We’ll look at operational challenges in more detail in the next section.

Volume equals complexity, and digital service providers are managing more connections, more transactions and more users across a larger variety of networks than ever before. This translates to rapidly rising costs when it comes to support calls, training, maintenance and operations – costs that could quickly outpace any revenue gains.

Manage your money

Escalating costs associatated with IoE

92.5%say the escalating cost of delivering digital services is a significant challenge or may be a concern

KG

19www.tmforum.org INSIGHTS RESEARCH

Ensure capital expenditure contributes to the success of the digital services strategy

Willingness to invest in transformation and ensure that each capital expenditure contributes to the digital services strategy is critical for demonstrating commitment and ensuring success. Executive oversight is required to maintain the vision of transformation and reinforce the desired corporate culture.

To reduce operational costs – and to meet the demand for connectivity in the IoE – automation must become the norm. This is something native digital providers like Microsoft already understand.

“Extreme automation is required. In 5G, there’s no way we can do this unless everything is completely automated – everything has to be software defined… When you’re operating at hyperscale, there is no choice.”

Eric Troup, Chief Technical Officer, Worldwide Communications and Media Industries, Microsoft

To read an interview with Troup about the Operations Center of the Future, visit TM Forum Inform7

Finally, the availability of virtualized network functions and standards-based OSS/BSS solutions capable of supporting the rapid creation and retirement of digital services is also a concern for service providers. In fact, the lack of standards, which we will discuss in more detail in Section 5, ranked third among challenges in our survey.

The right tools for the job

7http://inform.tmforum.org/strategic-programs-2/customer-centricity/2015/10/microsofts-eric-troup-automation-is-crucial-in-the-opcf/8https://www.tmforum.org/strategic-program/apis/

Availability of technology & support solutions for IoE

Today, many suppliers’ solutions remain proprietary or rely on legacy processes and silos. And while OSS/BSS vendors are making strides toward implementation of open interfaces and standardized platforms, too much variety still exists.

Cloud platforms are proprietary to each vendor and do not interoperate. Multiple mobile operating systems cannot seamlessly share data and proprietary versions of application interfaces are everywhere.

Data collected from IoE devices is ideally intended for use by multiple applications and business units, which also means that interfaces must be open, available and secure across the user’s organization, not just the digital service provider.

API Zone8

TM Forum offers 10 open, REST-based APIs (with 11 more under development) to manage services end to end and throughout their lifecycle in a multi-partner environment

82%say availability of technology and support solutions is a significant challenge or may be a concern

20 www.tmforum.orgINSIGHTS RESEARCH

DELIVERING END-TO-END SERVICES IN A HYPER-CONNECTED WORLD

SECTION 4

Navigating the operational roadblocks

Many operational challenges threaten to derail the emerging Internet of Everything (IoE). From defining services to delivering and supporting services unique to multiple industries, the integration and interoperability challenges that service providers have been working around or avoiding for years are exposed.

Defining and delivering end-to-end services for IoE require process efficiencies and automation that enable:

n first-use provisioning; n over-the-air software updates; n seamless network handoffs between operators; andn interoperability from the device to the cloud

then the network, and back again, regardless of infrastructure.

We asked survey respondents to indicate the most significant operational challenges they face in executing their strategies for end-to-end digital services. The results are shown in Figure 4-1.

Figure 4-1: Most significant operational challenges for IoE

Source: TM Forum, 2015

Security management and assurance

Definition of digital services technology strategy

Product/service definition & management

Partner ecosystem management

Cost

Customer care

Billing/revenue assurance

Product/service delivery

Product/service assurance

Sales/marketing

Virtualization

0% 20% 40% 60% 80% 100%

Not an issue May be a concern Significant challenge

21www.tmforum.org INSIGHTS RESEARCH

It is not surprising that security, the number-two business challenge (see page 16), ranks as the top operational challenge. Partnerships bring a great deal of added complexity to security and privacy, and it’s clear that for the foreseeable future figuring out how to ensure both end to end operationally and how to deal with breaches contractually will be focuses for digital service providers. We’ll discuss this more in the next section on partnerships.

Defining a digital services technology strategy also ranks high as an operational challenge. Close to half the respondents cite it as a significant challenge and another 40 percent saying it may be a concern.

Delivering turn-key, end-to-end IoE services requires the implementation of a centralized, data-driven architecture which relies on integrating the component-based catalog and automated fulfillment.

Creating operational efficiencies needs operational and business support system (OSS/BSS) functionality to bridge the gaps between existing systems, new virtualized solutions and partners’ platforms to deliver end-to-end services.

In the end, it’s all about automation and creating a single view of the customer and services across the business.

Service definition is a significant challenge or concern for almost 83 percent of respondents, but there are steps service providers can take to address this issue, from creating consistent views of subscribers to tracking the progress of orders.

IoE services demand a centralized, data-driven architecture, reliant on integrated catalog and automated fulfillment

Developing a technology strategy

Defining a technology strategy for digital services

Instant help with managing NFVTo learn more about what it takes to deliver end-to-end services in virtualized and hybrid networks, see our Extra Insights primer NFV: Can it be managed? 9

9https://www.tmforum.org/resources/research-and-analysis/nfv-can-it-be-managed-blueprint-for-end-to-end-management/

Defining and delivering digital services

1. Create a consistent, horizontal view of the subscriber across customer relationship management, infrastructure and OSS/BSS

2. Reduce the time it takes to define a new offer, including mapping and testing, by implementing a data-driven, rather than process-driven, strategy

3. Give customers the flexibility to customize offers using self-care

4. Apply rules, policies and thresholds to ensure the accuracy of orders and reduce fallout levels across all order and fulfillment channels

5. Track the progress of the order through fulfillment, activation and initial use

5 ways to improve the development of digital services

85%say defining a technology strategy for digital services is a significant challenge or may be a concern

22 www.tmforum.orgINSIGHTS RESEARCH

DELIVERING END-TO-END SERVICES IN A HYPER-CONNECTED WORLD

Virtually speaking

Interestingly, virtualization does not present nearly as big a challenge as service delivery for respondents. This may imply that virtualized functions have been isolated from existing operating processes, which does not bode well for defining and delivering end-to-end digital services at scale.

Alternatively, it may be that the integration of virtualized functions into existing networks and services is not underway or that virtual functions have not been activated to an extent that it affects operations. In either case it is important to integrate virtualization with existing solutions and operations platforms under a single management umbrella to enable end-to-end service delivery.

Customer-facing functions are also proving problematic as support personnel need specialized industry knowledge and training to support critical business customers. Likewise, service level agreements (SLAs) for connected applications and infrastructure become much more stringent and the penalties much more severe.

You need a planFor more about how service provider plan to develop a single management umbrella, see our Extra Insights primer Building the Operations Center of the Future10

10https://www.tmforum.org/resources/research-and-analysis/building-the-digital-operations-center-of-the-future/

Quality is the top task

65%percent say virtualization is as a significant challenge or concern,

Only

90%

95% say service delivery is

while

of survey respondents say service assurance is either a significant challenge or concern,

Close to

79% percent cite customer care as a challenge or concern

and

23www.tmforum.org INSIGHTS RESEARCH

Even though Internet of Things (IoT) devices typically use the mobile network, unlike mobile phones, dongles and tablets, the devices themselves may not move. As mobile networks are not as reliable as fixed networks, this creates a challenge. For example, a sensor on a storm sewer pump cannot go around the corner to get a better signal in bad weather.

Digital service providers must deliver SLAs to ensure reliable connectivity and diversity for critical devices under adverse operating conditions, which might mean hard-wired access. The more stringent the SLA, the more expensive for the business – but losing contact with a critical sensor during an emergency would be infinitely more costly.

Providing guaranteed availability is difficult and expensive, but is something that enterprise customers are willing to pay for, based on the value of the asset, and the importance of its safety and security.

How to get better performanceFind out more about how service providers plan to ensure quality in virtualized and hybrid networks in our Quick Insights report Virtualization: How to manage performance11

IoT devices present challenges for service providers when it comes to ensuring service level agreements

If digital service providers are to implement the increasingly complex processes and automation required to deliver advanced digital services, a new layer of expertise and staffing is required to support customers. Customers like self-care, but the self-care portals have to empower customers to achieve their goals, rather than just display billing information.

A collection of apps to monitor home security or remote systems isn’t enough either. At some point customers want a consolidated view of their services and apps, regardless of provider or partner.

If digital service providers are to implement the complex processes and automation required to deliver advanced services, a new layer of expertise and staffing is required11https://www.tmforum.org/resources/research-and-analysis/virtualization-how-to-manage-performance/

24 www.tmforum.orgINSIGHTS RESEARCH

DELIVERING END-TO-END SERVICES IN A HYPER-CONNECTED WORLD

SECTION 5

Creating a global ecosystem

From the smallest to the largest, digital service providers recognize that they need ecosystems of partners and a wide variety of business models to deliver competitive services efficiently and profitably.

Simply put, digital service providers cannot do this alone. The complexity and overhead associated with owning the network, building the services and supporting customers is too much for any one company, but suppliers, enablers and retailers can partner to expand and become stronger businesses.

We asked survey respondents about the role partnerships play in their strategies (see Figure 5-1).

As systems are upgraded, modified or replaced, service providers believe they will be in a better position to work with partners over the next two years, and that partners’ roles will become more

Figure 5-1: Role of partners now and in the future

Source: TM Forum 2015

Partners will play a substantial role

Partners will play a primary and critical role

Partners will play a minor or ad hoc role

Partners will play no role

0% 20% 40% 60% 80% 100%

Now Next 2 years Next 5 years

25www.tmforum.org INSIGHTS RESEARCH

51% say partnerships will play a minor role or no role in five years

substantial. There is a shift at the five-year mark, however, that seems to indicate a possible move away from partnerships.

Possible reasons for reducing reliance on partnerships in the future could include:

n Differentiation – digital service providers may initially go to market with partners but intend to acquire or make exclusive arrangements with those who provide popular or revenue-generating services and differentiation.

n Specialization – digital service providers cannot be all things to all customers. As Internet of Everything (IoE) customers demand higher and higher levels of integration and complex features, service providers may need to focus on a specific industries or sectors to deliver desired levels of service.

n Security – always at the top of the list of concerns, security to many digital service providers means closing the door to partners once the desired application, feature or functionality can be brought in-house.

n Standardization – as standards for interfaces and data structures are put in place either intentionally or by default, there will be a natural consolidation and fewer partners to consider.

n Cloud and platform strategies – digital service providers and partners are defining cloud and platform strategies to make interfaces and interactions with partners more transparent. As with standardization, the end result will be fewer unique partnering arrangements.

n Inability to predict – so many changes are underway at once, resulting in acquisitions, divestitures, mergers and other business and operational challenges, that predicting what will happen in five years may simply be too difficult.

We asked respondents whether they have defined an ecosystem platform for global partnerships and developed the necessary integration standards. Less than 9 percent have done so, but most are working on it (see Figure 5-2).

Developing the ecosystem platform

Figure 5-2: Progress on defining platforms and standards for global ecosystems

Source: TM Forum, 2015

Yes

Working on it

No

60.0%

8.6%

31.4%

More than one third of companies surveyed are working to deliver a partner-friendly environment; more than half are developing partner channels for sales, shipping, delivery and support. Overall, a majority have either completed or are in the process of completing much of the foundational work to transform their businesses from that of communication service provider to digital service provider.

Digital service providers cannot build entire ecosystems on their own – they need partners

26 www.tmforum.orgINSIGHTS RESEARCH

DELIVERING END-TO-END SERVICES IN A HYPER-CONNECTED WORLD

67.5% Organizational restructuring/organizational changes

59% Operational leadership changes

55.3% Implementation of virtualized environments

57% Digital service strategy execution

51.3% Product development emphasis

57.5% Talent and skills development/acquisition

59% Implementation of back office to deliver digital services

How respondents are building the foundation for digital services

It won’t be easy

In the near term digital service providers must establish alliances that enable them to deliver seamless global services, much like airlines have created global alliances to help passengers travel wherever they want to go under one umbrella. But doing so isn’t easy.

Operators that own networks are regulated by the countries where they operate and/or are restricted to regions where they are licensed. Each faces considerable regulatory and legal restrictions, which creates a minimum requirement for infrastructure partners.

Some IoE services are based on GSM networks while others use CDMA. Widespread LTE or Wi-Fi infrastructure might help overcome those differences, but many offerings will rely on older, widely deployed 3G and even 2G networks. Upgrading them will need massive investment. In addition, devices or sensors on the move – such as on trucks, containers and packages – will involve network handoffs to stay connected. Some companies could deliver a global virtual private network, but they too would have to rely on multiple networks run by many partners.

Some companies could deliver a global virtual private network, but they too would have to rely on multiple networks run by many partners

27www.tmforum.org INSIGHTS RESEARCH

When asked specifically about partnership challenges, security unsurprisingly tops the list again (see Figure 5-3). Beyond that, however, are the practical and tactical challenges associated with finding the right partners and integrating them into operational processes.

There are instances where service providers are trying to delay the introduction of partners. This is not because of competitive concerns: The biggest obstacle for digital service providers is that current business processes, practices and systems cannot meet the dynamic requirements of on-boarding partners, product and order management, settlements, assurance and security.

Service providers are used to contract management, but moving from contract to settlements is a different story. Adding partners to the product development process and including third-party components in the product catalog is difficult if the catalog is not open or flexible enough to accommodate a wide variety of complex elements, rules and workflow.

On the customer-facing side of the business, partners need payment without introducing opportunities for fraud or security breaches. Also, partners’ products or components must be included in the product catalog, sales and care processes.

If a customer is having a problem with a partner’s component, the service provider still has to take the call, find the problem and fix it. That puts additional pressure on customer relationship management (CRM) and care systems, and on the training and supervision of support personnel – all of which raises costs.

Transforming processes

Respondents see integration issues as a significant challenge or concern

For product catalogs

For billing and settlement systems

For CRM

86%97%94%

There are instances where service providers are trying to delay the introduction of partners

Highlighting the difficulties Figure 5-3: Challenges for partners

Source: TM Forum, 2015

Security

Identifying the right partners

Integration into billing, settlements and revenue assurance

Integration into service delivery and fulfillment

Integration into CRM, sales and customer care

Integration into product development and product catalog

Contract management

Performance management

Interoperability with existing infrastructure

Cost

0% 20% 40% 60% 80% 100%

Not an issue May be a concern Significant challenge

28 www.tmforum.orgINSIGHTS RESEARCH

DELIVERING END-TO-END SERVICES IN A HYPER-CONNECTED WORLD

n Provide open interfaces for rapid network, IT and OSS/BSS integration

n Offer fair pricing and automated demand management to monetize capacity

n Ensure security as user information is shared globally and the number of mobile financial and business transactions explodes

n Support standards that encourage network sharing, spectrum availability and global alliances

4 ways to be a better partner for digital services

Operating physical, virtual, cloud and partner components securely across geographies and systems is a task service providers are just starting to understand

Implementing a component-based environment in which to create products enables digital service providers to independently model products, connectivity and even changes. By using pre-defined components, processes, rules and workflows, products are consistently defined and delivered across the business, regardless of the underlying systems or partners.

On the activation side, by basing the automation of the fulfillment workflow on defined product components greatly reduces the time needed to deliver a new product or service.

Even once a partner’s product is included in the catalog and integrated into a service offering, there is no guarantee that it will work with existing infrastructure, service delivery or fulfillment processes and systems. As CRM, sales, order and offer management are aligned with partners and providers, the bottleneck moves to fulfillment.

Activating and operating physical, virtual, cloud and partner components securely across geographies and systems is another daunting task, which digital service providers are only beginning to understand.

Many potential partners do not have the IT staff and/or in-house expertise to put a partnership with a digital service provider in place. Certifications and testing must be performed once the necessary interfaces and integrations have been completed. And, once completed, every change or update to applications or infrastructure elements must be verified with regression testing. This typically results in modifications to partners’ software or systems.

To make partnerships profitable using virtualized infrastructure to deliver complex digital services, digital service providers need an end-to-end strategy, architecture and operational processes. There is no shortage of technology; proper implementation of the right technology is what will make all the difference.

From components to fulfillment

Ensuring services end to end

29www.tmforum.org INSIGHTS RESEARCH

As we discussed in Section 4, there are big operational challenges associated with delivering digital services, and partnerships magnify them. Close to half the respondents to our survey are in the process of implementing the necessary OSS/BSS platforms to handle services delivered through partnerships (see Figure 5-4).

A horizontal OSS/BSS architecture that abstracts infrastructure from services, services from customers and customers from products creates a more open environment for partners. A layered approach that is vertically integrated will deliver timely and consistent information throughout the business and implement end-to-end processes while enabling automation across service areas and silos.

For all their efforts, service providers recognize that OSS/BSS transformation cannot and will not occur overnight. Billions have been spent on existing systems, and critical data is scattered throughout the business. Orchestration layers abstract functionality from systems and infrastructure while enabling digital service providers to leverage existing infrastructure, OSS/BSS solutions and data.

In addition, development of global ecosystems for delivering digital services may well be delayed while providers identify industry and corporate standards for IT and OSS/BSS solutions which can be consistently applied worldwide.

Best-of-breed deployments are giving way to global platform standards and ecosystem solutions that enable digital service providers to specify infrastructure, system and integration standards that ensure consistency and interoperability. However, those solutions are not imminent and agreement on global standards is even further behind.

In the interim, digital service providers must rely on solutions that accommodate existing processes, systems and data while providing the additional capabilities foe delivering reliable and secure digital services anywhere in the world.

Billions have been spent on OSS/BSS and critical data is scattered across the business

Preparing the back office

Standards need work

92.5% say lack of standards is a significant challenge or may be a concern

Figure 5-4: Implementation of OSS/BSS for digital services

Source: TM Forum 2015

Done In progress Seriously considering Considering Not now

48.7%

5.1%

15.4%

20.5%

10.3%

30 www.tmforum.orgINSIGHTS RESEARCH

DELIVERING END-TO-END SERVICES IN A HYPER-CONNECTED WORLD

You’re not aloneFor more details about the Forum’s vision for the digital ecosystem including a look at Catalyst projects addressing the challenges, see our Extra Insights publication Collaborate to Innovate12

Figure 5-5: TM Forum’s vision for partnering

Source: TM Forum, 2015

TM FO

RUM

DIG

ITAL B

AC

KPLAN

E

DEVICE

STORE

COMPUTE NETWORK

12https://www.tmforum.org/resources/research-and-analysis/collaborate-to-innovate-a-universal-approach-to-winning-in-the-digital-world/

How to ensure provisioning or settlements across multiple providers’ networks and partners’ systems is far from certain. The number and variety of systems and interfaces in use makes rapid activation, billing, revenue assurance and automation of global end-to-end operating processes extremely difficult.

Fundamental problems include:

n defining and implementing common infrastructure, n virtualization, n application and service element interfaces,andn common data models and common operating

procedures across the business and aligned with partners.

By consolidating OSS/BSS, participating in standards bodies and insisting on implementation of specific transformational processes as part of OSS/BSS procurements, they will be able to ensure that OSS/BSS, IT, infrastructure and integration system suppliers deliver operational solutions that meet service providers’ requirements.

TM Forum has defined a vision for how best to represent the necessary elements of an open digital ecosystem and enable definition and implementation of a global digital services strategy (see Figure 5-5).

The service realization layer at the top represents where services are delivered to and experienced by customers.

The middle layer is the services platform and can be seen as an extension of the platform as a service, cloud-based model that is sold as a service to other businesses to enable them to offer their own services to customers. This layer ultimately shapes the digital ecosystem as it affects what partners can offer.

The bottom layer comprises infrastructure providers

that deliver and support compute, storage, network resources and devices. Those involved in the infrastructure layer are facing the biggest technological and organizational upheaval in a generation in the form of virtualization.

Some elements of this proposed architecture for the digital ecosystem run across all three of the layers forming a ‘backplane’. These backplane functions contribute the foundational assets, models and definitions that allow ecosystem partners to interact in a standardized way, enable scale, deliver a common view across the processes and simplify integration.

The qualities that service providers have built into the network – scalability, reliability, availability, performance and quality – must now be built into the IT infrastructure, applications, customer portals, care centers, retail outlets and devices that are the foundation for IoE partnerships and a connected economy.

A starting point

31www.tmforum.org INSIGHTS RESEARCH

Separate digital service offerings from expensive,regulated network construction and operations

SECTION 6

Make it happen: Six strategies for delivering digital services – and a ready-to-go toolkitIn the burgeoning Internet of Everything (IoE), digital service providers of all kinds must develop partnerships to deliver the complex services customers are demanding. No single company can do it alone.

Communications service providers in particular face numerous and difficult challenges as they transform their companies to compete in a hyper-connected world. They are faced with changing their culture and business processes, all while managing costs, complying with regulations and turning a profit.

Following are six key takeaways from this report that will help digital service providers succeed in an increasingly connected and competitive world.

Over-the-top providers like Amazon, Facebook and Microsoft have built very successful businesses without operating networks of their own.

Communications service providers need to follow their lead and separate digital services offerings from expensive, regulated network construction and operations. This will allow them to compete around products rather than bandwidth, coverage or speed.

The result is that companies with trusted brands can design, sell and bill for connected products, professional services, secure transaction processing and content while remaining competitive with

1. Go over the top

32 www.tmforum.orgINSIGHTS RESEARCH

DELIVERING END-TO-END SERVICES IN A HYPER-CONNECTED WORLD

companies that are not encumbered by expensive network infrastructure. Separation of regulated network infrastructure encourages infrastructure deployment because the amount of capacity deployed will be based on demand, rather than competition, and suppliers will be rewarded equally.

We’re all consumers and the concept of becoming a retailer is not foreign to individuals, millions of whom sell through Alibaba, Amazon and eBay. However, a company needs substantial cultural and mindset changes to become a digital retailer.

Our survey data reveals that business challenges are of the greatest concern to digital service providers. The people who recognize these challenges must initiate business adjustments, so that service providers’ business and operating strategies, and solutions can deliver end-to-end services to customers regardless of industry, location, application or device.

Some of the issues around moving into retail were explored in the recent TM Forum Omnishop proof-of-concept Catalyst project (see page 31).

Culture, mindset, organizational structure and leadership are all critical to making end-to-end, global digital services work. Business leaders must clearly communicate that digital services transformation affects every single part of the business and all staff.

Continuous communication of IoE strategies, their progress, future plans and expected results will make the changes less disruptive and promote cooperation.

This communication of expectations combined with relentless execution of a clearly defined strategy are essential to achieving the fundamental business transformation to make digital services flexible and profitable.

Transformation is seldom neat, and establishing global ecosystems and collaborative platforms for end-to-end digital services are no exception. Successful initiatives usually start as small proof-of-concept tests or lab

67%of service providers are restructuring or making organizational changes

Making changes

2. Become a retailer

90%of those surveyed are concerned about culture and mindset

Culture and mindset concerns

3. Leaders must lead

4. Commit to change and stay engaged

Continuous communication of IoE strategies, their progress, future plans and expected results will make the changes less disruptive and promote cooperation

33www.tmforum.org INSIGHTS RESEARCH

Potential benefits to service providers from this retail proof of concept include dynamic partnerships

Catalyst13 projects are TM Forum’s rapid-fire proof-of-concept projects, aimed at tackling real-world problems and finding pragmatic solutions for their adoption. The Omnishop Catalyst was demonstrated at TM Forum’s Catalysts InFocus event, held in Dallas at the beginning of November 2015.

The Catalyst was championed by Liberty Global and led by Infosys, with participants from Salesforce, IBM, Zira and ESRI. It showcased a reference implementation for ‘shop’ journeys which span call center agents, other customer-facing, and dealer-facing channels.

The team is leveraging and extending TM Forum standards, tools and best practices from its Frameworx suite and the Omnichannel Introductory Guide14. The Catalyst is taking an innovative approach, which abstracts the back-end complexities, federates information from diverse back-end ecosystems, and offers consistent capabilities across channels. This facilitates seamless transfer of context from one channel to another, in real time.

Benefits to the service provider inlcude:

n enabling omnichannel experience at reduced cost by reusing service providers’ existing and legacy IT systems;

n facilitating new dynamic digital partnerships by allowing third party channels to integrate to the Omnishop commerce framework;

n supporting business agility (evolving offerings, business models, partners, and channels); and

n simplifying customer experience by allowing customers to buy bundled offers of any service, in a simple,flawless transaction.

The demonstration included some use-case scenarios which showed how to realize an omnichannel shopping

experience, looking at how traditional and digital-age products from different service lines and partners can be bundled together. It also showed how these defined use cases apply to different channels, such as call centers, kiosks, online, social media and others, based on business rules.

The Catalyst demonstrated the concept of omnichannel merchandising where the customer can use various channels to act on a campaign,

Concepts such as federated catalog and order management are realized through an omnichannel enablement layer.

Subsequent phases of this Catalyst will explore a mechanism to replace ‘saved’ shopping carts to improve the conversion rate. The next step would be to incorporate feedback and learnings from the demonstration, and extend a solution to other business processes and service delivery scenarios.

Selling the retail concept

13https://www.tmforum.org/collaboration/catalyst-program/ 14http://bit.ly/OmnichannelIntroGuide

browse the offer,

create a shopping basket,

interact with customer service rep,

place an order, and

fulfill the order across different back-end stacks/partners.

34 www.tmforum.orgINSIGHTS RESEARCH

DELIVERING END-TO-END SERVICES IN A HYPER-CONNECTED WORLD

trials that gain critical mass rapidly, often with little regard for interoperability or security standards.

Digital service providers can ensure that the digital services coming to market deliver on the promise of a connected economy by selecting and validating platforms against industry guidelines, establishing friendly partnering policies and promoting capabilities to potential participants.

The are real opportunities to increase revenues, reduce costs and better serve customers –provided that the development, planning and execution of strategy are undertaken with the focus on business outcomes.

Complex digital services must not appear complex to customers. Automation, interoperability and clear interfaces and operating processes between partners are required to ensure that end-to-end services are defined, delivered and supported securely, accurately and profitably.

When the integration of infrastructure, systems and partners seems overwhelming, it becomes even more important to remember that they are just tools to implement strategy and process.

Finally, service providers of all kinds must collaborate to develop the global platform standards and ecosystem solutions that will enable them to ensure consistency and interoperability in the IoE.

TM Forum is defining a vision for how best to represent the necessary elements of an open digital ecosystem and enable definition and implementation of a global digital services strategy.

This work is detailed in our Extra Insights publication Collaborate to Innovate15. We also offer many other tools digital service providers can use to build partnerships, transform operations, virtualize networks and ensure customer experience.

While strong leadership and many business and operational changes are fundamental to delivering digital services end to end, many service providers are definitely making progress. As our research shows, they are, indeed, setting up the necessary partnerships to serve customers in a hyper-connected world.

Perhaps the most worthwhile thing we can do now is to ‘keep calm and carry on’, never losing sight of the business outcomes we are striving to achieve.

5. Build products customers want

6. Collaborate to innovate

In summary

When the integration of infrastructure, systems and partners seems overwhelming, it is even more important to remember that they are just tools to implement strategy and process

15https://www.tmforum.org/resources/research-and-analysis/collaborate-to-innovate-a-universal-approach-to-winning-in-the-digital-world/

35www.tmforum.org INSIGHTS RESEARCH

TM FORUM TOOLKITS

AGILE & VIRTUALIZED

REST APIsTM Forum offers ten open, REST APIs (with 11 more under development) to manage services end to end and throughout their lifecycle in a multi-partner environment.

End-to-End Virtualization Management: Impact on E2E Service Assurance and SLA Management for Hybrid NetworksThis information guide looks at the challenges and impacts on end-to-end service assurance and management of service level agreements in a hybrid physical/virtualized environment.

ZOOM NFV Security Fabric OverviewThis information guide outlines the TM Forum view on where the security fabric needs to be to support virtualized services.

OPEN & PARTNER EFFECTIVELY CUSTOMER CENTRICITY

Digital Services ToolkitCurrently under development, this toolkit will help companies rapidly address business problems using a collection of interlinked assets based on Frameworx.

Online B2B2X Step-by-Step Partnering GuideThis guide explains the five stages required to build a partner relationship. Each stage provides key concepts, strategy and approach, worksheets, examples and exit criteria to enable streamlined and repeatable implementation.

Customer Experience Management Solution SuiteThis set of tools consists of six components: a guidebook, more than 550 metrics, a maturity model, a lifecycle model, more than 10 implementation use cases and an ROI model.

Big Data Analytics Solution SuiteThis set of tools includes a big data reference model, a guidebook containing 65 use cases and 1700+ pre-defined metrics.

RESEARCH & PUBLICATIONS

Extra InsightsCollaborate to innovate: A universal approach to winning in the digital worldBuilding the Operations Center of the FutureNFV: What does it take to be agile? Transforming operations for the digital ecosystemNFV: Are you prepared? Operations and procurement readinessNFV: Can it be managed? Blueprint for end-to-end management

Insights ResearchCustomer experience and analytics in a digital worldVirtualization: When will NFV cross the chasm?

Quick InsightsVirtualization: How to manage performanceDigital services: Developing successful business models and roles

TM Forum toolkits help service providers build successful digital partnerships

https://www.tmforum.org/resources/standard/tr211-online-b2b2x-partnering-step-by-step-guide-r15-0-0/

36 www.tmforum.orgINSIGHTS RESEARCH

DELIVERING END-TO-END SERVICES IN A HYPER-CONNECTED WORLD

Since February 2015, hundreds of individuals from nearly 300 member companies have used TM Forum’s agile collaboration and development platform across 13 distinct projects to deliver the new features in Frameworx 15, working within the Forum’s three strategic programs: Agile Business and IT, Open Digital Ecosystem and Customer Centricity.

Agile Business & ITTM Forum’s Agile Business and IT Program helps enterprises continuously optimize their IT and business operations. New features come from the ZOOM (Zero-touch Orchestration, Operations and Management) project which has identified and verified the key transformation drivers and challenges – validated by studies and Collaboration Community reviews. They include:

n A novel, dynamic policy-based approach to end-to-end SLA management for hybrid operations, underpinned by the world’s first information model for the hybrid environment.

n A catalog approach to creating services through internal (make) service components and external (buy/rent) activities, supported by a federated catalog model, a comprehensive UML catalog model in the Information Framework, as well as DevOps and agile product lifecycle management. This enables service providers to assemble a wide range of services across the digital ecosystem with maximum commercial flexibility.

n A Procurement Survival Kit based on procurement patterns, ecosystem partner management, NFV procurement packaging, federated catalogs and maturity models.

COLLABORATIVE R&D MAKES DIGITAL BUSINESS REAL WITH FRAMEWORX 15

Open Digital EcosystemTM Forum’s Open Digital Ecosystem Program helps service providers, enterprises and technology suppliers create and manage complex, innovative services by establishing the right tools, APIs, standards and best practices. Key features from this program in Frameworx 15 provide organizations with the actionable information needed to accelerate R&D and time-to-market while reducing risk: