December 2013 - Total Training Solutionsttsmedia.ttstrain.com/AccountingO1213.pdf · FASB...

36

December 2013

Transcript of December 2013 - Total Training Solutionsttsmedia.ttstrain.com/AccountingO1213.pdf · FASB...

December 2013

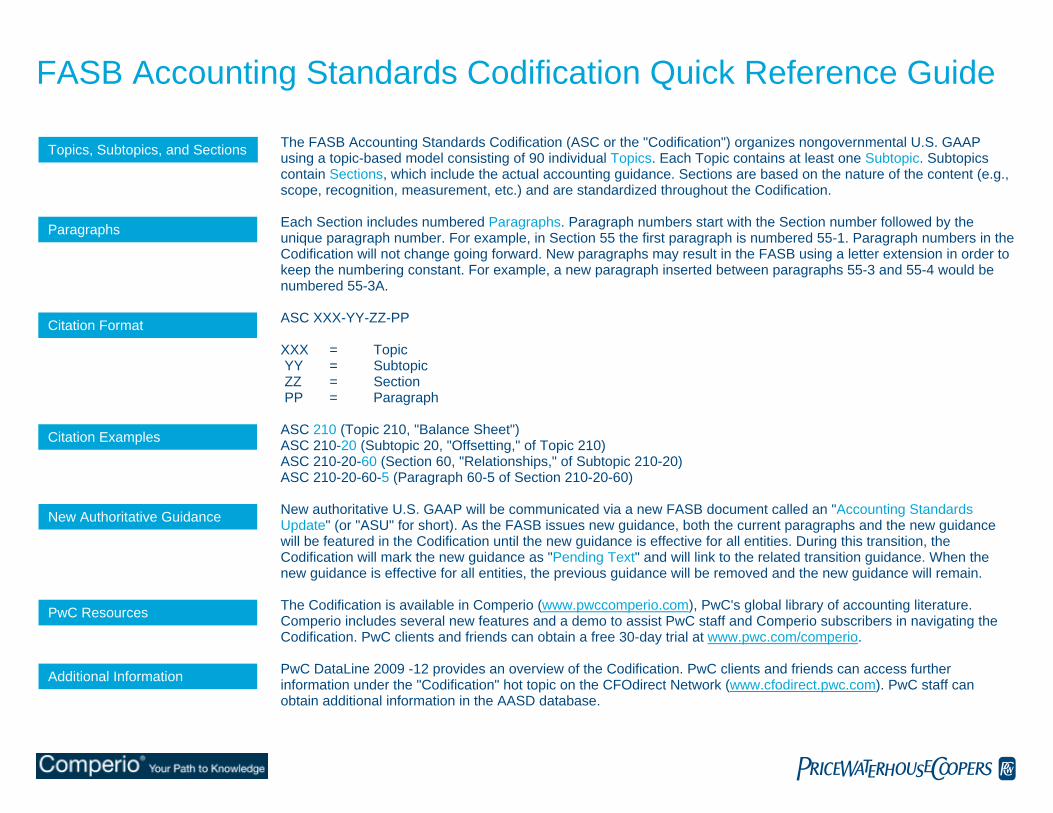

FASB Accounting Standards Codification Quick Reference Guide

The FASB Accounting Standards Codification (ASC or the "Codification") organizes nongovernmental U.S. GAAP using a topic-based model consisting of 90 individual Topics. Each Topic contains at least one Subtopic. Subtopics contain Sections, which include the actual accounting guidance. Sections are based on the nature of the content (e.g., scope, recognition, measurement, etc.) and are standardized throughout the Codification.

Topics, Subtopics, and Sections

Each Section includes numbered Paragraphs. Paragraph numbers start with the Section number followed by the unique paragraph number. For example, in Section 55 the first paragraph is numbered 55-1. Paragraph numbers in the Codification will not change going forward. New paragraphs may result in the FASB using a letter extension in order to keep the numbering constant. For example, a new paragraph inserted between paragraphs 55-3 and 55-4 would be numbered 55-3A.

Paragraphs

ASC XXX-YY-ZZ-PP Citation Format XXX = Topic YY = Subtopic ZZ = Section PP = Paragraph ASC 210 (Topic 210, "Balance Sheet") Citation Examples ASC 210-20 (Subtopic 20, "Offsetting," of Topic 210) ASC 210-20-60 (Section 60, "Relationships," of Subtopic 210-20) ASC 210-20-60-5 (Paragraph 60-5 of Section 210-20-60) New authoritative U.S. GAAP will be communicated via a new FASB document called an "Accounting Standards Update" (or "ASU" for short). As the FASB issues new guidance, both the current paragraphs and the new guidance will be featured in the Codification until the new guidance is effective for all entities. During this transition, the Codification will mark the new guidance as "Pending Text" and will link to the related transition guidance. When the new guidance is effective for all entities, the previous guidance will be removed and the new guidance will remain.

New Authoritative Guidance

The Codification is available in Comperio (www.pwccomperio.com), PwC's global library of accounting literature. Comperio includes several new features and a demo to assist PwC staff and Comperio subscribers in navigating the Codification. PwC clients and friends can obtain a free 30-day trial at www.pwc.com/comperio.

PwC Resources

PwC DataLine 2009 -12 provides an overview of the Codification. PwC clients and friends can access further information under the "Codification" hot topic on the CFOdirect Network (www.cfodirect.pwc.com). PwC staff can obtain additional information in the AASD database.

Additional Information

pwc

ASC Topic List100 General Principles 105 Generally Accepted Accounting Principles 200 Presentation 205 Presentation of Financial Statements 210 Balance Sheet 215 Statement of Shareholder Equity 220 Comprehensive Income 225 Income Statement 230 Statement of Cash Flows 235 Notes to Financial Statements 250 Accounting Changes and Error Corrections 255 Changing Prices 260 Earnings Per Share 270 Interim Reporting 272 Limited Liability Entities 274 Personal Financial Statements 275 Risks and Uncertainties 280 Segment Reporting 300 Assets 305 Cash and Cash Equivalents 310 Receivables 320 Investments—Debt and Equity Securities 323 Investments—Equity Method and

Joint Ventures 325 Investments—Other 330 Inventory 340 Other Assets and Deferred Costs 350 Intangibles—Goodwill and Other 360 Property, Plant, and Equipment 400 Liabilities 405 Liabilities

410 Asset Retirement and Environmental Obligations

420 Exit or Disposal Cost Obligations 430 Deferred Revenue 440 Commitments 450 Contingencies 460 Guarantees 470 Debt 480 Distinguishing Liabilities from Equity 500 Equity 505 Equity 600 Revenue 605 Revenue Recognition 700 Expenses 705 Cost of Sales and Services 710 Compensation—General 712 Compensation—Nonretirement

Postemployment Benefits 715 Compensation—Retirement Benefits 718 Compensation—Stock Compensation 720 Other Expenses 730 Research and Development 740 Income Taxes 800 Broad Transactions 805 Business Combinations 808 Collaborative Arrangements 810 Consolidation 815 Derivatives and Hedging 820 Fair Value Measurements and Disclosures 825 Financial Instruments 830 Foreign Currency Matters

835 Interest 840 Leases 845 Nonmonetary Transactions 850 Related Party Disclosures 852 Reorganizations 855 Subsequent Events 860 Transfers and Servicing 900 Industry 905 Agriculture 908 Airlines 910 Contractors—Construction 912 Contractors—Federal Government 915 Development Stage Entities 920 Entertainment—Broadcasters 922 Entertainment—Cable Television 924 Entertainment—Casinos 926 Entertainment—Films 928 Entertainment—Music 930 Extractive Activities—Mining 932 Extractive Activities—Oil and Gas 940 Financial Services—Broker and Dealers 942 Financial Services—Depository and Lending 944 Financial Services—Insurance 946 Financial Services—Investment Companies 948 Financial Services—Mortgage Banking 950 Financial Services—Title Plant 952 Franchisors 954 Health Care Entities 958 Not-for-Profit Entities 960 Plan Accounting—Defined Benefit

Pension Plans 962 Plan Accounting—Defined Contribution

Pension Plans

965 Plan Accounting—Health and Welfare Benefit Plans

970 Real Estate—General 972 Real Estate—Common Interest

Realty Associations 974 Real Estate—Real Estate Investment Trusts 976 Real Estate—Retail Land 978 Real Estate—Time-Sharing Activities 980 Regulated Operations 985 Software 995 U.S. Steamship Entities

ASC Section List 05 Overview and Background 10 Objectives 15 Scope and Scope Exceptions 20 Glossary 25 Recognition 30 Initial Measurement 35 Subsequent Measurement 40 Derecognition 45 Other Presentation Matters 50 Disclosure 55 Implementation Guidance and Illustrations 60 Relationships 65 Transition and Open Effective Date Information 70 Grandfathered Guidance 75 XBRL Definitions S99 SEC Materials

Note: In addition to Section S99, an "S" preceding any Section number denotes SEC content. Example: 260-10-S55

Selected Accounting Standards and Where They Now Reside* Accounting Standard General FASB Codification Topic Accounting Standard General FASB Codification Topic Accounting Standard General FASB Codification Topic Accounting Standard General FASB Codification Topic

FAS 5 ASC 450 Contingencies FAS 115 ASC 320 Investments—Debt and Equity Securities

FAS 141(R) ASC 805 Business Combinations FAS 165 ASC 855 Subsequent Events

FAS 13 ASC 840 Leases FAS 123(R) ASC 718 Compensation—Stock Compensation FAS 142 ASC 350 Intangibles—Goodwill and Other FAS 168 ASC 105 Generally Accepted Accounting Principles

FAS 52 ASC 830 Foreign Currency Matters FAS 128 ASC 260 Earnings Per Share FAS 143 ASC 410 Asset Retirement and Environmental Obligations

ARB 51 / FIN 46(R) / FAS 160 / FAS 167***

ASC 810 Consolidation

FAS 57 ASC 850 Related Party Disclosures FAS 130 ASC 220 Comprehensive Income FAS 144 ASC 360 Property, Plant, and Equipment APB 18 ASC 323 Investments—Equity Method and Joint Ventures

FAS 87; 88, and 106

ASC 715 Compensation—Retirement Benefits FAS 131 ASC 280 Segment Reporting FAS 146 ASC 420 Exit or Disposal Cost Obligations APB 28 ASC 270 Interim Reporting

FAS 95 ASC 230 Statement of Cash Flows FAS 133 ASC 815 Derivatives and Hedging FAS 150 ASC 480 Distinguishing Liabilities from Equity APB 29 ASC 845 Non Monetary Transfers

FAS 109 / FIN 48 ASC 740 Income Taxes FAS 140 / FAS 166**

ASC 860 Transfers and Servicing FAS 157 ASC 820 Fair Value Measurements and Disclosures

FIN 45 ASC 460 Guarantees

* Use the Cross-Reference Tool in Comperio for specific details on where the prior standards now reside within the Codification.

** FAS 166 has not yet been Codified. It is anticipated that this standard will primarily be incorporated into ASC 860 Transfers and Servicing.

*** FAS 167 has not yet been Codified. It is anticipated that this standard will be primarily incorporated into ASC 810 Consolidation.

© 2009 PricewaterhouseCoopers LLP. All rights reserved. “PricewaterhouseCoopers” refers to PricewaterhouseCoopers LLP, a Delaware limited liability partnership, or, as the context requires, the PricewaterhouseCoopers global network or other member firms of the network, each of which is a separate and independent legal entity.

FASB Accounting Standards Codification Quick Reference GuideFinancial Instruments Supplement*

* This is a supplement to PwC's primary Codification Quick Reference Guide, which is available on the CFOdirect Network (www.cfodirect.pwc.com), in Comperio, and the firm's internal AASD database.** This table highlights the primary location of prior standards within the Codification. Use the Cross-Reference Tool in Comperio for specific details on where the prior standards now reside within the Codification.

Presentation and Financial Statement Accounts—ASC Topic/Subtopic List200 Presentation

260 Earnings Per Share260-10 Overall

300 Assets

305 Cash and Cash Equivalents305-10 Overall942-305 Financial Services—Depositary and Lending946-305 Financial Services—Investment Companies

310 Receivables310-10 Overall310-20 Nonrefundable Fees and Other Costs310-30 Loans and Debt Securities Acquired with

Deteriorated Credit Quality310-40 Troubled Debt Restructurings by Creditors940-310 Financial Services—Brokers and Dealers942-310 Financial Services—Depository and Lending944-310 Financial Services—Insurance946-310 Financial Services—Investment Companies948-310 Financial Services—Mortgage Banking

320 Investments—Debt and Equity Securities940-320 Financial Services—Broker and Dealers942-320 Financial Services—Depository and Lending944-320 Financial Services—Insurance946-320 Financial Services—Investment Companies

323 Investments—Equity Method andJoint Ventures

323-10 Overall323-30 Partnerships, Joint Ventures, and Limited

Liability Entities323-740 Income Taxes946-323 Financial Services—Investment Companies970-323 Real Estate—General974-323 Real Estate Investment Trusts

325 Investments—Other325-10 Overall325-20 Cost Method Investments325-30 Investments in Insurance Contracts325-40 Beneficial Interests in Securitized

Financial Assets940-325 Financial Services—Broker and Dealers942-325 Financial Services—Depository and Lending944-325 Financial Services—Insurance

400 Liabilities

405 Liabilities405-10 Overall405-20 Extinguishment of Liabilities405-30 Insurance-Related Assessments940-405 Financial Services—Broker and Dealers942-405 Financial Services—Depository and Lending944-405 Financial Services—Insurance946-405 Financial Services—Investment Companies

440 Commitments440-10 Overall

450 Contingencies450-10 Overall450-20 Loss Contingencies450-30 Gain Contingencies

460 Guarantees460-10 Overall

470 Debt470-10 Overall470-20 Debt with Conversion and Other Options470-30 Participating Mortgage Loans470-40 Product Financing Arrangements470-50 Modifications and Extinguishments470-60 Troubled Debt Restructuring by Debtors942-470 Financial Services—Depository and Lending944-470 Financial Services—Insurance970-470 Real Estate—General

480 Distinguishing Liabilities from Equity480-10 Overall

500 Equity

505 Equity505-10 Overall505-20 Stock Dividends and Stock Splits505-30 Treasury Stock505-50 Equity-Based Payments to Non-Employees505-60 Spinoffs and Reverse Spinoffs942-505 Financial Services—Depository and Lending944-505 Financial Services—Insurance946-505 Financial Services—Investment Companies

Selected Accounting Standards and Where They Now Reside**Loans Securities/Other Investments Distinguishing Liabilities vs. Equity Liabilities

Accounting Standard FASB Codification Accounting Standard FASB Codification Accounting Standard FASB Codification Accounting Standard FASB CodificationFAS 65 ASC 948-310 FAS 115/FAS 124 ASC 320 FAS 150 ASC 480 FAS 5 ASC 450SAB 109 (Topic 5: DD) ASC 815-10-S99-1 FAS 155 ASC 815-15-25 ASR 268 ASC 480-10-S99-3A FAS 6 ASC 470-10

APB 18 ASC 323-10-35 FAS 133 ASC 815 FAS 78 ASC 470-10FIN 45 ASC 460

EITF 04-5 ASC 810-25 and 55 EITF D-98 ASC 480-10-S30 and S55 FTB 79-3 ASC 470-10-45-2 and 50-3EITF 02-14 ASC 323-10-55 FSP APB 14-1 ASC 470-20 ARB 43 ASC 440-10, 450-20,

470-10, 505-20

Classification

EITF 03-16 ASC 323-30-15 and 35 EITF 86-30 ASC 470-10-45-1 and 55-3thru 6

FAS 91 ASC 310-20 FAS 91 ASC 310-20 APB 14 ASC 470-20 FAS 84 ASC 470-20SOP 01-6 ASC 310-10, 835-30 EITF 96-15 ASC 320-10-35, 830-20-35 EITF 98-5 ASC 470-20 APB 26 ASC 470-50SOP 03-3 ASC 310-30 FAS 157 ASC 820 EITF 00-27 ASC 470-20 AIN-APB 26 ASC 470-20-40-4 and

470-50-15-3 and 40-5FAS 157 ASC 820 FAS 159 ASC 825-10-25 APB 21 ASC 835-30

Recognition

FAS 159 ASC 825-10-25FAS 5 ASC 450 FSPFAS 115-1/124-1 ASC 320-10-35 FAS 15 ASC 470-60FAS 114 ASC 310-40 FSPFAS 115-2/124-2 ASC 320-10-65 EITF 02-04 ASC 470-60-55SAB 102 (Topic 6:L) ASC 310-10-S99-4 SOP 03-3 ASC 310-30 EITF 96-19 ASC 470-50-40/55FAS 15 ASC 310-40 EITF 99-20 ASC 325-40-15, 35, and 55 EITF 06-6 ASC 470-50-40-12, 40-15

thru 16

Impairment/Other Events

EITF 01-07 ASC 310-20-35-11 FAS 141R ASC 805 EITF 98-14 ASC 470-50-40, 45, and 55

FASB Accounting Standards Codification Quick Reference GuideFinancial Instruments Supplement*

* This is a supplement to PwC's primary Codification Quick Reference Guide, which is available on the CFOdirect Network (www.cfodirect.pwc.com), in Comperio, and the firm's internal AASD database.** This table highlights the primary location of prior standards within the Codification. Use the Cross-Reference Tool in Comperio for specific details on where the prior standards now reside within the Codification.

Broad Transactions—ASC Topic/Subtopic List800 Broad Transactions

815 Derivatives and Hedging815-10 Overall815-15 Embedded Derivatives815-20 Hedging—General815-25 Fair Value Hedges815-30 Cash Flow Hedges815-35 Net Investment Hedges815-40 Contracts in Entity's Own Equity815-45 Weather Derivatives944-815 Financial Services—Insurance

820 Fair Value Measurementsand Disclosures

820-10 Overall820-820 Financial Services—Brokers and Dealers

825 Financial Instruments825-10 Overall825-20 Registration Payment Arrangements942-825 Financial Services—Depository and Lending944-825 Financial Services—Insurance

830 Foreign Currency Matters830-10 Overall830-20 Foreign Current Transactions830-30 Translation of Financial Statements830-230 Statement of Cash Flows830-740 Income Taxes946-830 Financial Services—Investment Companies

835 Interest

840 Leases840-10 Overall840-20 Operating Leases840-30 Capital Leases840-40 Sale and Leaseback Transactions974-840 Real Estate—Real Estate Investment Trusts978-840 Real Estate—Time-Sharing Activities

860 Transfers and Servicing860-10 Overall860-20 Sales of Financial Assets860-30 Secured Borrowing and Collateral860-40 Transfers to Qualifying Special

Purposes Entities860-50 Servicing Assets and Liabilities

ASC Section List05 Overview and Background10 Objectives15 Scope and Scope Exceptions20 Glossary25 Recognition30 Initial Measurement35 Subsequent Measurement40 Derecognition45 Other Presentation Matters50 Disclosure55 Implementation Guidance and Illustrations60 Relationships65 Transition and Open Effective Date Information70 Grandfathered Guidance75 XBRL DefinitionsS99 SEC Materials

Note: In addition to Section S99, an "S" preceding anySection number denotes SEC content.Example: ASC 260-10-S55

Selected Accounting Standards and Where They Now Reside**Derivatives Hedging Other Broad Transactions

Accounting Standard FASB Codification Accounting Standard FASB Codification Accounting Standard FASB CodificationDefinition FAS 133, par. 6, 9 ASC 815-10-15 Eligibility/ DIG G2 ASC 815-20-55-111 Example 8 Transfers FAS 140/FAS 166*** ASC 860, ***Not yet codified

FSPEITF 00-19-2 ASC 825-20 Designation DIG G13 ASC 815-20-55-88 Example 4 FAS 156 ASC 860-50-35 and 860-50-50-5Scope exceptions FAS 133, par. 10 ASC 815-10-15 FAS 133, par. 20c, 28c ASC 815-20-25-94 Consolidations FIN 46R/FAS 167*** ASC 810, ***Not yet codified

FAS 133, par. 11a ASC 815-10-15-74 FAS 133, par. 29 ASC 815-20-25-15 ARB 51 ASC 810-10EITF 07-5 ASC 815-40-15 FAS 133, par. 32 ASC 815-30-40-1 thru 3 FAS 160 ASC 810-10-65-1EITF 00-19 ASC 815-40 FAS 133, par. 40a ASC 815-20-25-61 EITF 96-16 ASC 810-10-25-1 thru 14DIG A6DIG A10

ASC 815-10-55ASC 815-10-15

Hedge effectivenessand ineffectiveness

FAS 133, par. 68DIG G20

ASC 815-20-25-102 thru 117ASC 815-20-25-126, 55-209,

EITF 04-5 ASC 810-20-25-1 thru 20, and810-20-55-1 thru 16

DIG A12 ASC 815-10-55-99 thru 110 and 35-33 EITF 85-12 ASC 810-10-25-15DIG C12 ASC 815-10-15-39 FAS 133, par. 120c ASC 815-25-55-53 Example 9 Leasing FAS 13 ASC 840

Embedded FAS 133, par. 12, 13, 61 ASC 815-15-25 FAS 138 FV Example ASC 815-25-55-72 Example 11 FAS 98 ASC 840-40Derivatives DIG B16 ASC 815-15-25-42 thru 43, DIG G7 Method 1 ASC 815-30-35-16 EITF 97-10 ASC 840-40-55

and 815-15-55-13 DIG G7 Method 2 ASC 815-30-35-25 EITF 01-8 ASC 840-10-15/55DIG B38 ASC 815-10-15-107 thru 109 DIG G7 Method 3 ASC 815-30-35-31 EITF 00-13 ASC 360-20-15/55DIG B39 ASC 815-15-25-37 thru 39, and DIG H8 ASC 815-35-35 Foreign FAS 52 ASC 830

815-15-55-25 DIG E7 ASC 815-20-35 Currency EITF D-55 ASC 830-10-45-12 and 830-10-55-24EITF D-109 ASC 815-10-S99-3 Matters

The Codification is available in Comperio (www.pwccomperio.com), PwC’s global library of accounting literature. Comperio includes several new features and a demo to assistPwC staff and Comperio subscribers in navigating the Codification. PwC clients and friends can obtain a free 30-day trial at www.pwc.com/comperio. Questions about topicscontained in this document should be directed to your PwC engagement team or members of the Financial Instruments team in the National Professional Services Group.

PwC Resources

12/17/2013

Accounting For Lenders Supplement #1

Jeffery Johnson BANKERS INSIGHT GROUP, LLC

ACCOUNTING ASSUMPTIONS

Accounting principles and assumptions are the essential guidelines under which businesses

prepare their financial statements. These principles guide the methods and decisions for a

business over a short and long term. For both internal and external reporting purposes, it is

important to understand the concepts presented below because they serve as a guideline to the

analysis of financial reporting issues.

Economic Entity Assumption

Under the economic entity assumption, an economic activity can be identified to a separate entity

accountable for that activity. In other words, this assumption states that businesses must keep

their transactions separate from their owners’, business units’ or other businesses’ transactions.

For example, the business activities of the neighborhood coffee house are to be kept separate

from the financial activities of its owners or managers. The financial statements for the coffee

house will only reflect the revenue and expenses for the coffee house. Thus, it is possible to

compare the financial statements of this coffeehouse with its competitors’ reports, since these

statements should be reported separately under the economic entity assumption. Important to

note, a separate entity does not necessary mean a legal entity. For example, financial statements

for a parent company and its subsidiaries (i.e. separate legal entities) can be presented together

(i.e. consolidated financial statements).

Revenue Recognition Principle

Under this principle revenue is to be recorded when it is realized (or realizable), and when it is

earned and not when it is received. Revenue is realized when goods or services are exchanged, is

realizable when assets received can be converted to cash, and is earned when all necessary

requirements are met entitling the company to the benefits represented by the revenue (e.g.

services performed).

For example, suppose a neighborhood coffee house orders 100 coffee mugs from a coffee

wholesaler in June. The coffee house takes delivery of the new mugs in July and pays for the

order in August. The wholesaler does not recognize the revenue from this sale in June, when the

order was placed, or in August, when the cash was received. For recording purposes, the

revenue is recognized by the wholesaler in July, when the coffee mugs were delivered to the

coffeehouse.

This principle is used for the recognition of revenue for both goods and services. For example, if

an attorney is hired with an agreed upon retainer fee of $2,500 in May, and the services are not

performed until July, the attorney does not recognize the revenue until July. The attorney must

earn the income before it can be recorded as such, even though he/she received cash for the

service at an earlier date.

Historical Cost Principle

The historical cost principle deals with the valuation of both assets and liabilities. The value at

the time of acquisition is used to value most assets and liabilities. For example, say the coffee

wholesaler purchased an office building in 1990 for $1.2 million. Over time this asset has most

likely appreciated in value. However, in accordance with the cost principle, the original

(historical) price of the building is what is recorded as the cost of the building in the books of the

business.

Note that another basis for valuing elements of financial statements is coming into play. The

new basis is fair value. With the convergence of global standards, fair value is used more in the

United States to value elements of financial statements.

Matching Principle

This principle mandates that the expenses of a business need to line up with its revenue. The

expense or cost of doing business is recorded in the same period as the revenue that has been

generated as the result of incurring that cost. In the case of the coffee wholesaler, when the 100

coffee mugs were delivered in July they changed from being a part of inventory (asset) to a cost

of goods sold entry (expense) in the month that the revenue from the sale was recognized. At

this point, the difference between the revenue and expense is determined as the gross profit from

the sale.

Full Disclosure Principle

This principle states that all past, present and future information that may have had an impact on

the financial performance of the company needs to be fully disclosed. The historical

performance of a company is readily available, but examining the numbers does not always

provide the entire financial picture of a company. Sometimes there are alternative situations that

need to be reported. Pending or current lawsuits are one example of a transaction that could

severely impact a company’s bottom line. In addition, incomplete financial transactions or any

other conditions that could impact the company’s performance must also be disclosed. Most of

these transactions are disclosed in the footnotes to the financial statements.

Periodicity

An entity’s life can be subdivided into time periods for purposes of reporting its

economic activities.

![INTERMEDIATE - preview.kingborn.netpreview.kingborn.net/920000/4344e7e68c624fa98fe9d9d76dffe1c1.pdf · FASB CODIFICATION FASB Codification References [1] FASB ASC 350-10-05. [Predecessor](https://static.fdocuments.net/doc/165x107/5b892df67f8b9a770a8cf6c0/intermediate-fasb-codification-fasb-codification-references-1-fasb-asc-350-10-05.jpg)