Debtwire European CRE Finance Report Q1 2015

15

1Q15 EUROPEAN CRE FINANCE REPORT OVERVIEW 2 UK LOANS 3 GERMANY LOANS 4 NETHERLANDS LOANS 4 DEALS IN FOCUS 5 SOUTHERN EUROPE LOANS 6 LOAN PORTFOLIO SALES 7 LOAN PORTFOLIOS FOR SALE 9 IRISH CRE ANALYSIS 10 CRE FINANCING INDEX 11

-

Upload

thorsten-lederer- -

Category

Presentations & Public Speaking

-

view

219 -

download

0

Transcript of Debtwire European CRE Finance Report Q1 2015

1Q15

EUROPEAN CRE FINANCE REPORT

OVERVIEW 2

UK LOANS 3

GERMANY LOANS 4

NETHERLANDS LOANS 4

DEALS IN FOCUS 5

SOUTHERN EUROPE LOANS 6

LOAN PORTFOLIO SALES 7

LOAN PORTFOLIOS FOR SALE 9

IRISH CRE ANALYSIS 10

CRE FINANCING INDEX 11

EUROPEAN CRE FINANCE REPORT 1Q15

2

T he strong positive momentum seen in European commercial real estate lending throughout 2014 showed no signs of abating during the first quarter of 2015. In a sector characterised

by a high volume of investment deals, debt was widely available from a variety of lenders Including banks, institutional investors and private equity funds. Tight pricing was the key talking point of the quarter. In March, the

CBRE Capital Advisors’ Four Quadrants report showed that prime

lending margins were as low as 130 basis points and had arguably

reached a point of stabilisation, partly as a result of capital

adequecy regulations. Borrowers entered 2015 in a favourable

position, the research found, with the total cost of debt falling by

29% during 2014, due to margin compression and a decrease in

swap rates.

UK senior debt margins for prime property reached a low of 110 bps during the first quarter and

as tight as 60 bps in Germany, according to Debtwire’s pricing index. Lenders polled by this

news service said LTVs for UK senior debt were found at 60-65%, while in Germany senior LTVs

could go as high as 80%, at the end of the quarter.

The rise in bank lending against property was partially fuelled by low interest rates and partly by

quantitative easing. “QE has produced a swathe of global investors in the prime real estate

markets worldwide, in both equity and debt, who reference returns on real assets to corporate

bonds, and see value where there is a yield uplift which they consider a sufficient illiquidity

premium,” said Emma Huepfl, head of capital management for investment management firm

Laxfield Capital. “The secondary property market reflects property fundamentals more closely,

which in turn is more reflective of the local rather than international economy.”

“We are seeing gradually increasing numbers of requests for finance for secondary assets, and

lenders are getting more comfortable with lending in the better locations, where rents are ris-

ing, and we are still a good way off [from] over-supply,” Huepfl continued. Secondary margins

have come down significantly, to as low as 175 bps, according to one market source.

CBRE said that the proportion of debt in investment transactions remained far below the long-term average. The percentage of investment turnover funded by debt was 34% during 2014; a long way from the 69% seen in 2007, the market peak.

OVERVIEW

Tight pricing was the key

talking point of the

quarter

“We are seeing a variety of interesting capital in the [CRE] debt market,” said Huepfl. “More investors are agnostic about whether they invest in the equity or debt, and are actively seeking complex transactions, or stress in the capital structure where they can use their flexibility of capital to gain enhanced yield.” Lenders’ search for returns has led them into peripheral markets such as the Netherlands,

Spain, Italy and Ireland. In the Irish market, for instance, assets acquired through private equity

loan-to-own strategies started to come back for refinancing, with some domestic sponsors also

seeking finance opportunities.

The market for distressed debt continued to provide opportunities for new loan origination.

Loan-on-loan finance was increasingly available, market players said. For example, during the

first quarter, Citi provided a GBP 500m senior loan to Cerberus Capital Management for its

purchase of the GBP 1bn face-value Project Carlisle UK loan book from Nationwide for GBP

680m. The three-year loan (with two one-year extensions) carried a circa 300 bps margin. In a

February 2014 loan market report, Cushman & Wakefield said that loan-on-loan margins during

2013 had tightened to between 400 bps and 600 bps, with 300 bps seen in some instances.

Despite the competitive nature of the debt market with more lenders than ever to choose from,

existing lenders remained best positioned. “Incumbent lenders are in a good position to retain

business,” said one market participant, speaking in private. “We see a lot of deals go out to the

debt market, only to be refinanced by existing lenders. From a borrower’s perspective, it is often

easier to stay with a lender rather than have to start the documentation all over again with a

new party. Of course the lender still has to prove it is able to match the most competitive

terms.”

The syndication market was also active. The GBP 365m loan wrote by ING to finance the Safra

Group’s purchase of the Gherkin in the City of London was successfully placed with a number of

banks including three from Japan GBP 230m

was sold down to three of the banks, while a

fourth slice of less than GBP 50m was also

syndicated. In addition, Lloyds and Citigroup

went out to the market to sell down a portion

of the GBP 277m loan which they wrote to

The Peel Group and Legal & General, secured

by the MediaCityUK estate in Greater

Manchester.

Sector LTV (%)* Margin (bps)*

UK senior 60-65 110-225

UK mezz 60-80 500-900

Germany senior 60-80 60-175

Germany mezz 75-80 650-850

UK & German loan margins on prime property

*Figures are informal estimates by five European

bankers polled by Debtwire

EUROPEAN CRE FINANCE REPORT 1Q15

3

A t the prime end of the spectrum, the UK commercial real estate finance market remained busy and very competitive during the first quarter of 2015. Tight pricing continued to be a

major theme during the quarter, as it was during 2014 when prime margin compression was evident. However, some market participants argued that margins have reached a point of stabilisation, with no significant downward shift during the quarter. Borrowers did not seek higher LTVs, with potential interest rate rises and refinance risk limiting day-one leverage. Lenders were holding on tight on covenants too. Finance was widely available for buyers of prime London commercial property, with banks and alterna-tive lenders alike providing significant loans to finance major deals during the first three months. One example was Lloyds Bank Commercial Banking’s GBP 200m-plus loan to finance the purchase of the Tower Place office building in the City of London. The deal was an example of a major clearing bank providing debt for a well-heeled core buyer – in this case Chinese insurance firm Ping An – backed by a prime London office property. However, the quarter also saw several instances of lenders looking outside the prime space and into the regional and value-add sectors of the market to source deals. For some, this meant writing loans against some of the country’s prime regional office stock. In March, Lloyds and Citi provided GBP 277m, reflecting a 55% LTV, to the owners of the MediaCityUK scheme in Greater Manchester – The Peel Group and Legal & General. The 37-acre MediaCityUK is one of the country’s flagship developments of the last decade and is exactly the type of prime regional stock banks are eager to finance. But such opportunities do not appear too often. Regional portfolio transactions provided opportunities for lenders to gain exposure to UK prop-erty during the quarter. Wells Fargo and Royal Bank of Canada provided senior debt to Lone Star for its GBP 1bn purchase of retail, office, hotel, and residential property as well as student accommodation from two Moorfield funds. The circa GBP 600m five-year deal carried a margin in the high 200 bps, as reported. Another portfolio deal was Aviva Commercial Finance’s GBP 325.3m vendor finance to Kennedy Wilson Europe Real Estate to facilitate the GBP 503m sale of 180 mixed-use UK properties by Aviva. The 70% LTV deal was split into three tranches paying a weighted average margin of 207bps.

UK loan origination

Finance was widely available for

buyers of prime London commercial

property

Elsewhere, Barclays provided a GBP 96m whole loan to a Harbert Management Corporation subsidiary in January to finance 807,000 sq ft of UK business park properties. The 70% LTV loan was backed by properties bought from Arlington Business Parks and located in places such as Oxford, Leicester, Sunderland and Glasgow. Barclays also financed Oaktree and Patrizia’s GBP 127m purchase of the Citrus portfolio of UK properties, with a circa GBP 70m four-year loan alongside DRC Capital which provided GBP 24m of mezzanine debt. The collateral was 24 properties

located across the UK ranging from offices in the City of London to a distribution warehouse in Haverhill. Lenders also sought exposure to the London market, by financing less core properties. German

bank LBBW provided GBP 97m to refinance CLS’s Spring Gardens property, located in the

Vauxhall area of the city, south of the River Thames. Lenders also looked to finance value-add. A

good example is BNP Paribas’s GBP 90.4m loan to Tishman Speyer for 100 New Oxford Street.

The building is in the process of being bought by Tishman Speyer and is a scheme in the heart of

London with significant uplift potential (see deals in Focus).

Lenders also sought exposure to the London market by financing less core properties

EUROPEAN CRE FINANCE REPORT 1Q15

4

T he German property lending market has traditionally been one of the most competitive in Europe, both in terms of pricing and LTVs. The simple reason is that the country has too

many banks – from local savings banks to Landesbanken – willing to finance property. Plus the Pfandbrief market remains an easy and cheap way to refinance. Domestic banks have always preferred core properties. However, core properties accounted for only 40% of new business last year compared with 60% in 2013, according to the German property lenders index (Difi). The index rose by 10.2 points from the fourth quarter to 39.1 points, its highest level ever. German banks stretching further into non-core is potentially bad news for foreign banks. Non-core assets have normally been their preserve. For example, in the first quarter, both Bank of America Merrill Lynch and SEB wrote big tickets against non-prime assets.

BAML provided German property company IVG Immobilien with a EUR 470m loan for the SQUAIRE property outside Frankfurt. The loan represented a 70% LTV, with the margin coming in at less than 250 basis points. The refinancing of the property came after IVG failed to sell the asset following heavy marketing by CBRE. IVG sought around EUR 700m, compared with a book value of EUR 800m, but serious bids did not go beyond EUR 600m. It is suspended above the

railway tracks at Frankfurt airport, with KPMG as the main tenant. The big question is whether KPMG will remain in situ, its employees are rumoured to be unhappy about the location. SEB financed another difficult Frankfurt property. The Swedish bank provided a five-year loan to Blackstone for its purchase of the 257m tall Messeturm office tower for around EUR 250m. The 62,000 sq m property suffers from small floor plates and has a vacancy rate of around 30%. More importantly, the tower’s location is not prime sitting outside Frankfurt’s banking district. SEB syndicated parts of the loan to two other unnamed banks. Blackstone bought the MesseTurm around the same time as Pollux, a vacant office tower in Frankfurt’s banking district. Deutsche Bank financed that one.

German loan origination

Core properties accounted for only 40% of new business last year

D omestic lenders are making a comeback in the Netherlands. While FGH and SNS Propertize remain burdened by their legacy loans, ABN Amro and ING are stepping up their lending

activities, albeit on a selective basis. However, ABN Amro recently noted that foreign financiers retain a dominant position in major deals. It listed Royal Bank of Canada and Deutsche Hypo as well as non-banks such as debt funds, as the main players. In January, ING provided EUR 140m of debt to a secondary office portfolio bought by Valad on behalf of an unidentified investor. The five-year senior loan was made at around 210 basis points, and 60% LTV. The portfolio, sold by Unibail-Rodamco, consists of three buildings in Rotterdam, one in Almere, one in Delft and one in Zoetermeer. The biggest building in the portfolio is the 33,442 sq m Central Plaza in Rotterdam, which also has 480 parking spaces. The Dutch residential sector saw plenty of lending activity in the first quarter. Investors see potential upside from a liberalization of social housing sector and increasing demand for houses due to a continuing fall in home prices. In February, ING took part in a consortium of three banks to provide a EUR 331m loan for the EUR 578m purchase of 5,500 residential units in the Netherlands by German Investor PATRIZIA Immobilien for its Wohnmodul I vehicle. The three banks are each taking a third of the debt, paying an all-in interest rate of 2%. Deutsche Hypo acted as mandated lead arranger, agent and bookrunner, ING Real Estate Finance as MLA and pbb as co-arranger. Interestingly, the loan came out of ING Germany as the Dutch bank’s cost of capital is lower there. ING’s retail savings services have been successful in Germany, leading to a surplus of cash to allocate. Dutch residential is also on ABN Amro’s menu. The bank financed two acquisitions by Round Hill

Capital. The private equity firm completed on two Dutch residential portfolios totalling 958 units

across approximately 84,600 sq m for a combined value of approximately EUR 98m. It has also

completed on a 976 unit Propertize portfolio that Round Hill which it agreed to acquire for EUR

89m in December. Round Hill is currently looking for debt for its EUR 365m purchase of the WIF

portfolio. Although the deal was agreed last year, it still has not closed as the Dutch interior

minister needs to give his approval. Meanwhile, a number of social housing corporations –

which sold their stock to WIF in return for a stake in the fund – are objecting to the deal, arguing

refinancing is a better alternative than an outright sale.

Netherlands loan origination

Domestic lenders are making a

comeback in the Netherlands

EUROPEAN CRE FINANCE REPORT 1Q15

5

BNP Paribas backs London value-add BNP Paribas took what most observers would probably agree was a calculated gamble on the West End of London during the quarter. The French bank wrote a GBP 90.4m, six-year senior loan to property investor Tishman Speyer for the purchase of 100 New Oxford Street; a mixed-use office and retail block close to the Centre Point tower on the eastern edge of the West End. The deal was a good example of a lender gaining exposure to value-add opportunities in the increasingly tight London market. The 103,500 sq ft 100 New Oxford Street building is a bit of a fixer-upper. Sold by Canada Pension Plan Investment Board and Hermes Real Estate in a deal expected to close in May, Hermes is in the process of refurbishing elements of the building before it changes hands. Three floors are currently being revamped. Vacancy in the building – which Tishman stated was around 50% back in January - is also being tackled, with office and retail space under offer when Debtwire reported the loan in February. The associated financing reflected the asset management potential of the building. BNP Paribas’s loan was structured pre-

dominantly as acquisition finance, alongside a GBP 5m tranche intended to cover costs while the existing vacancy is filled up.

The pricing of the loan reflected the value-add status. The margin was written at 175bps over Libor from day one, although

it is due to reduce to below 150bps once the majority of the building is leased.

V&D refinancing target missed Dutch department store V&D is causing financiers a headache. The ailing retail chain just about survived in the first quarter thanks to a rescue package in which landlords, banks and the owner, Sun Capital, pulled together. Sun Capital desperately needs a new formula to bring customers back to the former icon of the Dutch high street. V&D’s concept of offering everything to anybody no longer works. Retail spending is sluggish, an increasing number of consumers are buying online. Meanwhile, landlord IEF Capital missed a February refinancing target of around EUR 200m due to the problems at V&D. IEF Capital is gradually refinancing a EUR 1bn retail property portfolio whose loan – securitised in Leo Mesdag – matures in 2016. In addition to V&D stores, the portfolio contains stores let to loss-making Hema, a Dutch version of M&S, and upmarket department store Bijenkorf. The latter is the only one out of the three doing well after adopting the shop-in-shop concept. To avoid balloon risk at maturity, last year IEF asked CMBS noteholders for permission for a staged refinancing. The

bondholders reluctantly agreed after IEF Capital promised to inject EUR 40m of fresh equity. But that was before problems

with V&D came to a head. V&D accounts for 18% of rental income in the Leo Mesdag CMBS. Under the refinancing deal, IEF

Capital agreed that V&D should not account for more than 25% of the property pool to be refinanced at any one time. This

could be more problematic at the next refinancing date in August, when IEF has to refinance EUR 400m or more.

Loan size GBP 90.4m

Lender BNP Paribas Corporate and Institutional

Banking

Borrower Tishman Speyer

Term 6 years

Acquisition price c. GBP 130.00m

Margin 175 bps (to reduce to sub-150bps)

Loan size EUR 1bn

Lender Leo Mesdag CMBS

Borrower IEF Capital

Country Netherlands

Asset type Retail

DEALS IN FOCUS

EUROPEAN CRE FINANCE REPORT 1Q15

6

T he search for returns has led lenders outside of the core European markets of the UK, France and Germany and into peripheral geographies including Spain and Italy. However,

each country has its individual challenges and market participants said that it can be difficult to source the right deals. During the first quarter of 2015, there were a few examples of banks providing debt finance outside core Europe. Italy is a geography which almost every market player claims to be looking at, although a limited number seemed to be closing deals. In March, Debtwire reported that Bank of America Merrill Lynch (BAML) was lined up by Cerberus Capital Management to finance its EUR 230m purchase of a portfolio of seven public-sector leased buildings in Italy from the Fondo Immobili Pubblici (FIP) fund. Once the deal clos-es, BAML will provide a loan with a circa 65% LTV with a margin of just less than 300 basis points. It seems that the lender’s relationship with, or confidence in, the sponsor is paramount in Italian

deals. In BAML’s case it is lending to a borrower with a strong track record in opportunistic

European investment. Previous deals in the country have included Deutsche Bank financing

Blackstone’s acquisition drive, providing loans that were subsequently securitised.

During the quarter, ING provided a EUR 63m five-year loan secured by Credit Suisse’s Milan

offices. In this case, the loan was written to a holding company incorporated in the Qatar

Financial Centre. The property securing the facility is an 11,000 sq m prime office building locat-

ed in Via Santa Margherita 3 in Milan, bought by Qatar Investment Authority in the second

quarter of last year from Tishman Speyer for EUR 108m, according to Knight Frank’s Milan Office

Market Outlook research. Using that purchase price, ING’s loan reflected circa 58% loan-to-

value.

The Spanish market looks set to provide lenders with significant opportunities during 2015.

According to Savills’ Spain Investment Market Report in February 2015, the retail investment

volume for 2014 was more than EUR 2.3bn, in line with 2006’s figures. Offices were in the

region of EUR 2.8bn. SOCIMIs were lauded as one of the main factors in the market upturn,

accounting for almost a third of total investment volume last year.

Southern Europe loan origination

Italy is a geography which almost every

market player claims to be looking at

During the quarter Allianz Real Estate wrote a EUR 133.6m ten-year loan to Spanish SOCIMI

Merlin Properties to finance its acquisition of the Marineda Shopping Centre in A Coruña. It is

Spain’s second largest commercial and leisure complex and the borrower is one of the country’s

most active real estate investment trusts.

Italy – a fertile ground for securitisation

The arbitrage between CMBS and bilateral lending is most pronounced in jurisdictions where finance is not readily available, or in size. Italy is proving to be one of these geographies and was the setting for two new deals during the quarter. Bank of America Merrill Lynch launched its Taurus 2015-IT in January, which investors welcomed due to its straightforward structure and strong sponsors. The EUR 286.39m deal securitised three loans and featured three tranches. All the notes have a February 2020 expected maturity. The multi-borrower deal read like a roll-call of some of the most active private equity investors in the Italian sector. It comprised the EUR 101m Calvino loan sponsored by Cerberus, the EUR 85m Fashion District loan sponsored by Blackstone and the EUR 115m Globe loan, sponsored by Orion Capital Managers. The EUR 206m A-class priced at 150bps (from initial price thoughts around 140bps), while the

EUR 23m B-class priced at 190bps (from IPTs at 180bps), and the EUR 34.3m C tranche priced at

250bps, in line with the IPTs.

More than 20 investors bought into the deal, of which 79% went to the UK. Dutch investors took 10%, Italians 6% and investors in other jurisdictions took the remaining 5%. Asset managers were the largest group with 80%, insurance companies and pension funds took up 10% and hedge funds and banks the remaining 10%. Just two investors bought the privately placed TIBET CMBS backed by super prime retail space in Milan. The EUR 203m deal — launched by Banca IMI and Cairn Capital — refinances an existing syndicated loan for sponsor Giuseppe Statuto and consists of four rated tranches. The EUR 105m A, EUR 27m B and EUR 10m C notes were placed with one investor while class D went to a second. The margins ranged from 165bps for the A tranche to 415bps for the BB rated D tranche.

EUROPEAN CRE FINANCE REPORT 1Q15

7

T he first quarter of 2015 was relatively quiet in the European loan portfolio space, following a frenzy of business at the tail end of 2014. Cushman & Wakefield’s corporate finance team

said that a record-breaking EUR 80.6bn of CRE loans and real estate-owned (REO) properties were sold last year across Europe. This year is tipped to be huge once again for loan sales (C&W predicts EUR 60-70bn of CRE loan and REO transactions), suggesting the first quarter may be the calm before the storm. Last year saw huge volumes traded in Ireland, but the first quarter was quieter. In March, Per-manent TSB said it had sold EUR 1.5bn of non-core loans – known in the market as Projects Munster and Leinster – to a vehicle funded by Deutsche Bank and funds affiliated with Apollo Global Management. The loans were sold for EUR 800m, a 47% discount to face value. Permanent TSB is preparing for sale the final portion of its non-core Irish loans; the EUR 900m Project Connacht containing buy-to-let mortgages and CRE loans, the Irish Independent recently reported. The National Asset Management Agency (NAMA) closed the sale of Project Boyne to Deutsche

Bank. The portfolio with a face value of EUR 287m sold for around EUR 95m. Boyne was not a

huge portfolio by Irish loan market standards, but was typical of the mid-sized single borrower

portfolios that NAMA is expected to bring to the market in the coming months. Boyne related to

the entrepreneur William Smyth and contained debt secured by property including serviced

offices in Dublin.

NAMA spent the quarter preparing new portfolios, including the EUR 8bn-plus Project Arrow, a

granular portfolio to contain loans written to in the region of 500 borrowers. Other banks such

as Lloyds Banking Group and Ulster Bank, the Irish arm of Royal Bank of Scotland, still have the

remainder of their Irish loan books to offload, and more sales are expected. As one debt special-

ist told this news service recently: “If you are a bank and have a tail, it’s worth getting it into the

market now. Good assets will appreciate. The tail won’t”.

Loan sales have been thin on the ground in Germany. Last year, they fell 45% compared with

the year before, according to Cushman & Wakefield. But there are signs the flow is increasing

once again. In the first quarter, Goldman Sachs and Wells Fargo sold two loan portfolios.

Goldman Sachs’ asset manager, Archon, sold Project Wagner, a EUR 650m portfolio of 600 loans

to EOS Group for around EUR 100m. Wells Fargo sold a EUR 60m loan portfolio secured against

Loan portfolio sales

This year is also tipped to be a

huge one for loan sales

10 German nursing homes to Bank of America Merrill Lynch. Commerzbank is launching a EUR 800m sale of loans made by Eurohypo, and Helaba has started to market a EUR 500m loan sale under the name Project Aurora. Contrary to their European peers, German banks resisted large loan

sales so as to avoid painful write-downs. But with the market improving and investors hungrier for riskier assets in Germany, they may have been proven right to wait after all. Dutch banks were also slow to sell down their loan books, but the few deals have generated a lot of investor interest. FGH and HSH sold a loan secured against an office portfolio, called Project Omega, to Archon and Valad. The properties were bought at the top of the market by Dutch investor and asset manager Ping Properties. ING sold a loan secured against another Ping Properties portfolio, Project Ogon. ING sold Ogon for around EUR 60m to Apollo Global Management compared with a face value of EUR 100m and a EUR 70m guide price. Although the loans involve the same borrower, the sales were different. There was no longer a role for Ping Properties following the sale of Omega, whereas it continues to be the owner and asset manager of Ogon. Meanwhile, FGH is still touting around a EUR 250m Dutch loan portfolio through PWC. The portfolio consists of loans secured by office properties bought by German fund manager Wölbern Invest. Southern Europe was quiet for loan sales in the first quarter. Just before year-end SAREB confirmed loan sales with a combined face value of EUR 847m had been sold to various buyers including Cerberus and Hayfin Capital Management. Attention in Spain in the first quarter was mostly fixated on Project Gaudi, a circa EUR 750m portfolio held by German bad bank FMS Wertmanagement. As this report went to press, Colony Capital and Oaktree Capital Management were the final two parties shortlisted to buy the portfolio for between 60 and 70 cents in the Euro. The UK had a quiet quarter. In February, Kennedy Wilson Europe Real Estate bought eight loans

secured by Park Inn hotels leased to Rezidor Hotel Group and located across the UK for GBP

61.5m. Market observers do not expect the UK market to be a major focus of NPL sales during

the course of 2015.

The Southern European market was quiet in terms of loan sales

EUROPEAN CRE FINANCE REPORT 1Q15

8

LOAN PORTFOLIO SALES

Date reported

Portfolio name

Seller(s) Buyer(s) CUR Sale price

(m) Property

type No. of

properties Country

Original face value (m)

Seller’s financial advisor

Notes

09-Jan-15 Project Omega FGH Bank, HSH Nordbank

Goldman Sachs EUR Office 24 Netherlands

The property transaction had a volume of EUR 109m, ac-cording to an entry in the Dutch land registry

13-Jan-15 Project Boyne National Asset Management Agency

Deutsche Bank EUR 95.00 Office, retail,

residential Ireland 287.00 JLL

The purchase price reflects a discount to par value of around 67%

14-Jan-15 National Asset Management Agency

Invel Real Estate Partners

GBP Retail,

residential UK, Italy c.140.00

The collateral is located in Liverpool, South East London and the Italian island of Sardinia

16-Jan-15 Project Wagner

Archon Group EOS Group EUR c. 100.00 Real estate Germany 650.00 KPMG

16-Jan-15 Project Helios Wells Fargo Bank of America

Merrill Lynch EUR 60.00 Care home 10 Germany 80.00 Ernst & Young

BAML bought the loans at an 11% to 12% discount to the outstanding balance of EUR 60m

11-Mar-15 Project Ogon ING Apollo Global Management

EUR 60.00 Office Netherlands Cofiton EUR 100m outstanding bal-ance, the bank had sought a price of around EUR 70m

11-Mar-15 Projects Munster and Leinster

Permanent TSB Deutsche Bank/

Apollo Global Management

EUR 800.00 CRE and

buy-to-let residential

c.1,600 Ireland 1500 Morgan Stanley

PTSB confirmed the buyer on 26 March.

31-Mar-15 PVE Capital EUR c. 183.00 Residential Italy 408 Purchase price is based on information that portfolio sold for 45 cents in the Euro

EUROPEAN CRE FINANCE REPORT 1Q15

9

Project Arrow: Ireland’s National Asset Management Agency (NAMA) has instructed

Cushman & Wakefield and partner firm Lisney to sell loans with a face value of EUR

8.4bn, relating to up to 500 borrowers and secured by around 3,000 properties. Around

half of the collateral is residential, with the remainder made up of CRE (20%), land

(20%) and other types including hotels (10%). The portfolio was yet to be launched as

the report went to press.

Project Milner: NAMA, through Cushman & Wakefield, is aiming to sell a EUR 778m

face-value NPL portfolio relating to Irish entrepreneur Gerry Barrett, secured by ten

properties including three Irish hotels, plus retail assets.

Project Lee: The circa EUR 300m portfolio, which is being sold by NAMA, contains debt

secured by the Mahon Retail Park in Mallow, County Cork, among other assets. The

debt relates to Cork-based developer Owen O’Callaghan.

Project Connacht: In March, the Irish Independent reported that Permanent TSB was

preparing to sell its remaining EUR 900m of Irish non-core loans including buy-to-let

mortgages and CRE debt.

Project Gaudi: German bad bank FMS Wertmanagement mandated Cushman & Wake-

field to sell EUR 750m across 18 loans secured by Spanish (and some Portuguese) col-

lateral. Notable properties include the Hotel Arts de Barcelona as well as the Penha

Longa Hotel & Resort in Cascais, Portugal. The portfolio contains 18 loans, roughly

equally divided between performing, sub-performing and non-performing. At the time

of writing, Colony and Oaktree had been shortlisted.

SELECTED LOAN PORTFOLIOS FOR SALE

Eurohypo loans: Commerzbank is selling a EUR 800m German portfolio and a EUR 3bn pan-European portfolio of loans, written by Eurohypo (now called Hypotheke bank Frankfurt). Four private equity firms (Cerberus, Colony, Oaktree and Lone Star) are thought to be through to the second round of the pan-European sale, with second round bids due by the end of April. The same parties are also thought to be in the race for the German book.

Project Tristan: Goldman Sachs’ asset manager Archon has instructed KPMG to sell a

circa EUR 800m loan portfolio consisting of around 700 loans, secured by CRE across Germany.

FGH Bank loans: The Dutch bank is selling a circa EUR 250m loan portfolio backed by

Dutch offices. PwC has been mandated to sell the loans. The portfolio comprises loans secured by office properties bought by German fund manager Wölbern Invest, which filed for insolvency in 2013.

Project Aurora: Lazard is selling a EUR 500m NPL portfolio on behalf of an unidentified bank. Sources told Debtwire that the seller is believed to be Helaba.

EUROPEAN CRE FINANCE REPORT 1Q15

10

I reland’s commercial real estate market is at an interesting juncture. Since 2012, US private equity firms have

pounced upon loan portfolios secured by real estate. The prime part of the market has experienced a significant recovery in the intervening years, putting Ireland on core investors’ radar. “Ireland can no longer be classified as a distressed market. It has reached the point where private equity firms are not the leading bidders for single assets,” said Adrian Trueick, Irish in-vestment property director with Knight Frank. Private equity funds are still keen to invest. Real estate loans with a face value of EUR 20bn were traded during 2014, according to research by Lisney. However, there has not yet been an overwhelming volume of properties put back onto the market. “We sense that the key occupancy markets are still relatively early in the cycle,” said Peter Collins, Dublin-based managing director of Kennedy Wilson Europe. “By and large we are holders of property and we still see a lot of upside potential because we are essentially real estate operators.” Although NPL buyers are not clambering for the exits, some higher quality properties have been

sold. In February, Hibernia REIT bought the Garda headquarters at Dublin’s Harcourt Square for

EUR 70m from a subsidiary of Starwood Capital. Starwood had acquired loans secured by the

property through the purchase of NAMA’s Project Aspen loan portfolio in 2013.

Local property consultants admit that it is difficult to guess what the Irish CRE investment

market will look like once the private equity frenzy has died down. Last year’s investment

volumes were unprecedented. Lisney recorded EUR 4.4bn of investment turnover, up from EUR

180m just three years earlier.

“The real question is will there be enough capital to deal with the unwinding of loans and assets

which takes place in 2016 and 2017,” said John Moran, managing director of JLL’s Irish

operation. “Who are the secondary buyers? Will the market remain international or revert to a

Irish CRE An opportunistic market matures (This is an abridged version of a feature published by Debtwire on 4 March 2015)

Ireland can no longer be

classified as a distressed market

more domestic nature? It is hard to know where our normal level is.” As occupier demand and rents in the prime Dublin market recover, core buyers including REITs, institutions and European funds are entering the fray. In February, NAMA sold the adjacent 4 and 5 Grand Canal Square office buildings – Facebook’s EMEA HQ – for EUR 232m, a net initial yield of just more than 4%, hardly the type of return to attract opportunistic money. The buyer was Union Investment, the investment management arm of Germany’s DZ Bank. Prime Dublin office rents increased by 36% to EUR 45 per sq ft during 2014, according to Lisney,

and further growth to more than EUR 50 per sq ft is expected by many agents. Office yields in

the Irish capital have come in from 6% at the end of 2013 to 4.75% at the end of 2014.

“The office market has definitely shifted towards the core buyers, so a lot of the opportunistic players are looking at retail,” said Johnny Horgan, head of capital markets for CBRE in Ireland. Central Dublin shops might yield 4%, but provincial shopping centres can provide investors with running yields of over 7%, Horgan added. The sell-off of Ireland’s CRE debt is not over yet. Cushman & Wakefield Corporate Finance said

in the last quarter of 2014 that it was tracking EUR 21.7bn of live loan sales, of which 21% were

in Ireland. Market sources said that Ulster Bank is working up another large loan sale to follow

the Projects Aran and Achill which were sold last year. NAMA is working up plans for the sale of

Project Arrow through Cushman & Wakefield and Lisney; a EUR 8.4bn face value portfolio of

loans predominantly secured by Irish property relating to around 500 borrowers.

“In the NPL and debt arena there are still plenty of opportunity funds looking for exposure. Some are express-ing the view that the market has become too expensive from a value perspective, but they keep bidding,” said one agent. The financing market provides opportunities for debt

players eager for exposure to the Irish recovery, local

agents argued. The Irish debt market is not functioning efficiently at the moment, although

more banks and non-traditional lenders are looking for opportunities, sources said.

The sell-off of Ireland’s CRE debt is not over yet

EUROPEAN CRE FINANCE REPORT 1Q15

11

CRE FINANCING INDEX

Date reported

Asset(s) Lender(s) Borrower(s) CUR Loan

size (m) LTV (%)

Margin Loan

length (y)

Country Asset type Notes

05-Jan-15 Six Dutch offices ING Valad Europe EUR c.84.00 c. 60 c. 210bps 5 Netherlands Office Purchase made by Valad Europe on behalf of an unidentified investor

16-Jan-15 Building 7 at Chiswick Park

BNP Paribas Corporate and Industrial Banking

Blackstone Real Estate Partners Europe III

GBP 76.50 3 UK Office The 331,000 sq ft building was under construction at the time the loan was closed

20-Jan-15 Silberturm, Jurgen-Ponto-Platz 1

ING Real Estate Finance Korean Samsung SRA Management Group

EUR c. 450.00 <85bps Germany Office ING syndicated part of the loan

23-Jan-15 Emperor Portfolio Barclays Harbert Management Corporation

GBP 96.00 70 UK Office Whole loan to finance 807,000 sq ft portfolio of business park properties

23-Jan-15 Tower place Lloyds Bank Commercial Banking

Ping An Life Insurance GBP c.200.00 >60 5 UK Office The 385,000 sq ft tower was sold to Ping An by Deutsche Asset and Wealth Management

28-Jan-15 Brettenham House DRC Capital, Standard Life Investments

Draco Property GBP 65.00 5 UK Office, retail

The senior portion of the loan has been placed with Standard Life Investments. It refinanced existing debt

28-Jan-15 Residential units BNP Paribas Powerhouse France EUR 793.50 France Residential

The refinancing comprises a EUR 206m corporate facility provided to Powerhouse France and a EUR 588.5m senior mortgage facility provided to its subsidiary, SAFRAN

30-Jan-15 Citrus portfolio Barclays, DRC Capital Oaktree Capital Management, Patrizia Immobilien

GBP c. 94.00 c.75 4 UK

Office, industrial/logistics,

leisure, mixed use

The loan is structured as a senior and a mezzanine tranche, with Barclays providing the senior finance DRC provided EBP 24m it confirmed.

EUROPEAN CRE FINANCE REPORT 1Q15

12

CRE FINANCING INDEX (cont’d)

Date reported

Asset(s) Lender(s) Borrower(s) CUR Loan

size (m) LTV (%)

Margin Loan

length (y)

Country Asset type Notes

02-Feb-15 180 mixed-use UK assets

Aviva Commercial Real Estate Finance

Kennedy Wilson Europe Real Estate

GBP 325.30 70 blended 207bps

3, 5 and 8 year

tranches UK Mixed use

The senior vendor finance is split into three-year floating-rate (33%), five-year fixed-rate (20%) and eight-year fixed-rate (47%) tranches

03-Feb-15 HSBC St Modwen GBP 100.00 5 UK Revolving

credit facility Replaced a GBP 75m facility which was due to expire January 2016

11-Feb-15 UK-wide mixed use portfolio

Wells Fargo, Royal Bank of Canada Capital Markets

Lone Star GBP c.600.00 C.60 high 200bps 5 UK

Office, retail, hotels,

residential, other

Lone Star bought a UK portfolio from two Moorfield funds for GBP 1bn.

12-Feb-15 5,500 Dutch residential units

Deutsche Hypo, ING Real Estate Finance, pbb Deutsche Pfandbriefbank

PATRIZIA Immobilien EUR 331.00 Netherlands Residential The three banks are each taking a third of the debt. All-in interest rate of 20%

12-Feb-15 100 New Oxford Street, London

BNP Paribas Corporate and Industrial Banking

Tishman Speyer GBP 90.40 C.70 c.175bps 5 UK Office, retail

The loan term can be increased by one year. The margin is due to decrease to sub-150bps once the majority of the building is leased

18-Feb-15 Five hotels Legal & General Private client GBP 75.00 78 20 UK Hotels Hotels are located at London’s Gatwick and Stanstead airports

25-Feb-15 Unsecured

Bank of China Limited, Barclays Bank Plc, Credit Agricole Corporate and Investment Bank, Handelsbanken, Royal Bank of Scotland Group Plc, Santander Global Banking and Markets, The Bank of Tokyo-Mitsubishi UFJ Ltd

British Land GBP 485.00 90bps 5 UK Unsecured revolving credit facility. The loan can be extended to a maximum period of seven years

26-Feb-15 Marshes Shopping Centre

Bank of Ireland Kennedy Wilson Europe Real Estate

EUR 264.00 212.5bps Ireland Retail The loan replaced a EUR 195.8m Bank of Ireland facility which had been agreed in June 2014

EUROPEAN CRE FINANCE REPORT 1Q15

13

CRE FINANCING INDEX (cont’d)

Date reported

Asset(s) Lender(s) Borrower(s) CUR Loan

size (m) LTV (%)

Margin Loan

length (y)

Country Asset type Notes

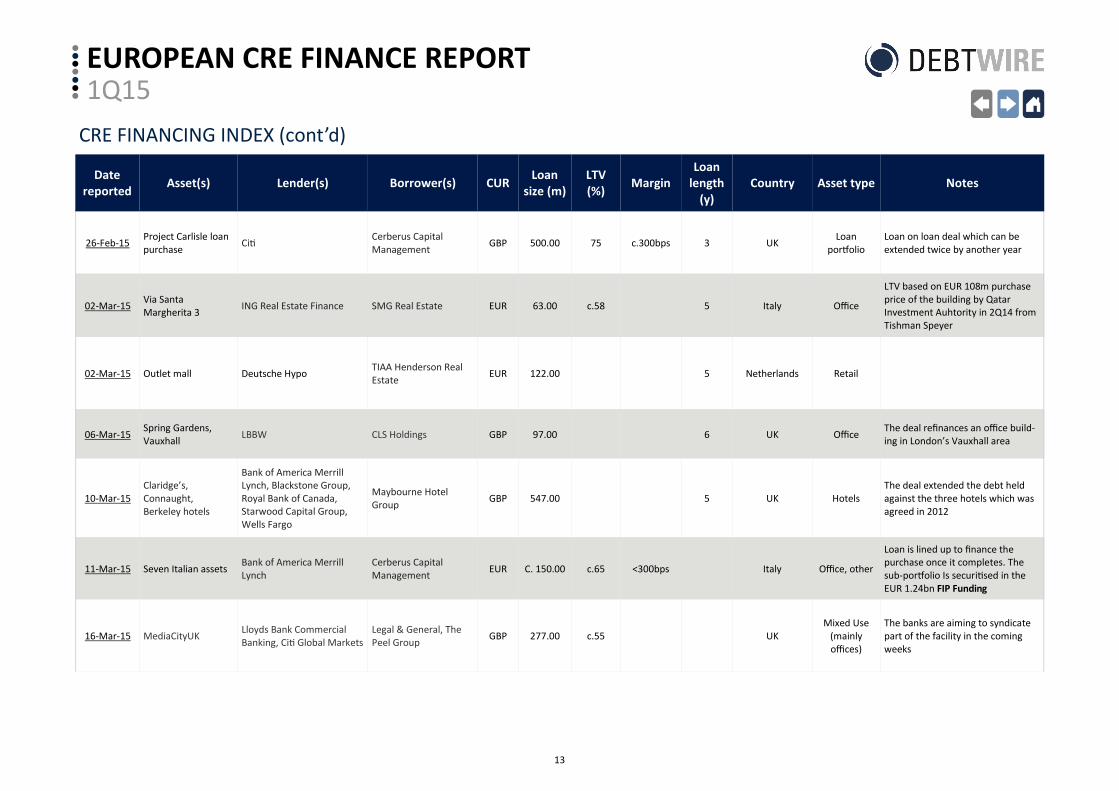

26-Feb-15 Project Carlisle loan purchase

Citi Cerberus Capital Management

GBP 500.00 75 c.300bps 3 UK Loan

portfolio Loan on loan deal which can be extended twice by another year

02-Mar-15 Via Santa Margherita 3

ING Real Estate Finance SMG Real Estate EUR 63.00 c.58 5 Italy Office

LTV based on EUR 108m purchase price of the building by Qatar Investment Auhtority in 2Q14 from Tishman Speyer

02-Mar-15 Outlet mall Deutsche Hypo TIAA Henderson Real Estate

EUR 122.00 5 Netherlands Retail

06-Mar-15 Spring Gardens, Vauxhall

LBBW CLS Holdings GBP 97.00 6 UK Office The deal refinances an office build-ing in London’s Vauxhall area

10-Mar-15 Claridge’s, Connaught, Berkeley hotels

Bank of America Merrill Lynch, Blackstone Group, Royal Bank of Canada, Starwood Capital Group, Wells Fargo

Maybourne Hotel Group

GBP 547.00 5 UK Hotels The deal extended the debt held against the three hotels which was agreed in 2012

11-Mar-15 Seven Italian assets Bank of America Merrill Lynch

Cerberus Capital Management

EUR C. 150.00 c.65 <300bps Italy Office, other

Loan is lined up to finance the purchase once it completes. The sub-portfolio Is securitised in the EUR 1.24bn FIP Funding

16-Mar-15 MediaCityUK Lloyds Bank Commercial Banking, Citi Global Markets

Legal & General, The Peel Group

GBP 277.00 c.55 UK Mixed Use

(mainly offices)

The banks are aiming to syndicate part of the facility in the coming weeks

EUROPEAN CRE FINANCE REPORT 1Q15

14

CRE FINANCING INDEX (cont’d)

Date reported

Asset(s) Lender(s) Borrower(s) CUR Loan

size (m) LTV (%)

Margin Loan

length (y)

Country Asset type Notes

18-Mar-15 Unspecified Aviva Commercial Finance Shaftesbury GBP 130 3.2% fixed

interest rate

15 UK Unspecified Shaftesbury has cancelled a GBP 100m RCF with Nationwide.

26-Mar-15 Middlebrook Park, Bolton

TIAA Henderson Real Estate Orbit Developments GBP 100 20 UK Retail,

business park Loan was provided in January.

30-Mar-15 Unspecified Lloyds, Santander, RBS, HSBC, Citi, Sabadell, Bank of China, UBS

Land Securities GBP 1255 75bps 5 UK Unspecified

Secured revolving credit facility. Stepped margin increases depends on utilisation amount. Facility length can be extended for seven years.

EUROPEAN CRE FINANCE REPORT 1Q15

15

Debtwire ABS Research

Ortenca Aliaj, CRE Database Manager +44 (0)20 7010 6265, [email protected] Arijeet Das, ABS Analyst +44 (0)20 7010 6287, [email protected]

Debtwire ABS Editorial

Bert Erik ten Cate, Associate Editor, Commercial Real Estate +44 (0)20 7010 6249, [email protected] Daniel Cunningham, Senior Reporter, UK Property Finance +44 (0)20 7010 5106, [email protected]

Managing Team

Chris Haffenden, Editor +44 (0)20 7059 6189, [email protected]

Chris Dammers, Deputy Editor +44 (0)20 7010 6328, [email protected]

Disclaimer: We have obtained the information provided in this report in good faith from sources which we consider to be reliable, but we do not independently verify the information. The information is not intended to provide tax, legal or investment advice. We shall not be liable for any mistakes, errors, inaccuracies or omissions in, or incompleteness of, any information contained in this report. All such liability is excluded to the fullest extent permitted by law. Data has been derived from investor reports, press releases, presentations and DW intelligence.