Debt Securities Market - World...

57

Transcript of Debt Securities Market - World...

Debt Securities Market

Reşat ADIGÜZEL

Chief Specialist

March 13, 2014

March 13, 2014 3

Borsa İstanbul A.Ş.

March 13, 2014 4

Legal Framework

Establishment Framework: Debt Securities Market (DSM) has been established as a government organisation based on Decree Law No: 91 (enacted on 1983) with the aim of (Article 3.1) :

- organising buy and sell activities of securities

- discovering security prices via secondary market transactions and

- publishing / registering security prices

Establishing a stock exchange is subject to the proposal of Capital Markets Board and approval of Ministry of Finance

Based on the Decree Law, Borsa İstanbul and Debt Securities Market by-laws were ruled within the Capital Markets Law legislation (No: 2499, enacted on 1981)

Current Framework: With the new Capital Markets Law (No: 6362, enacted on 2012) Borsa İstanbul became a joint-stock company in April 2013 with the 49% ownership of the Turkish Treasury. Borsa İstanbul and its members hold the remaining shares.

→ New by-laws and secondary regulations are being prepared and after the approval of the Capital Markets Law will be published soon.

March 13, 2014 5

Purpose of the Foundation

Debt Securities Market started to operate in 1991 to facilitate a transparent and reliable environment for secondary market trading of debt securities and related products

Due to Borsa İstanbul’s governmental structure and high public sector borrowing requirement, DSM’s first aim was to decrease cost of funding of internal borrowing

Vision: Providing efficient and competitive trading environment based on fairness and justice principles for all market participants

Tradable Asset Classes: Both government and corporate debt securities denominated in TL and foreign currency, securitized assets and income backed debt securities, lease certificates (aka Sukuk), Central Bank liquidity bills and other securities that are approved by Borsa İstanbul Board can trade on the Debt Securities Market

March 13, 2014 6

DSM – Sub-Markets

Outright Purchases and Sales Market

(June 17, 1991)

where secondary market transactions of fixed income

securities are conducted

Repo-Reverse Repo Market

(February 17, 1993)

where general collateral repo-reverse repo transactions are

conducted

Offerings Market for Qualified Investors

(May 17, 2010)

where corporate borrowing instruments are issued to

“qualified investors” as defined in the capital markets legislation

Repo Market for Specified Securities

(December 17, 2010)

where repo-reverse repo transactions with specified debt

securities are conducted

Interbank Repo-Reverse Repo Market

(January 7, 2011)

where general collateral repo-reverse repo transactions are

conducted only by the banks and only for their own portfolio

accounts

Equity Repo Market

(December 7, 2012)

where repo- reverse repo transactions are carried out with the equities that are traded on Borsa İstanbul Equity Market

(those included in BIST 30 Index)

March 13, 2014 7

Market Framework

Borsa İstanbul Debt Securities Market

Treasury / Corporate Firms

Primary Market Debt Issuance Capital Markets Board

(Regulatory Authority)

Central Bank of Turkey

Central Securities Depository

Banks / Brokerage Houses

Secondary Market Transactions (DSM / OTC)

İstanbul Settlement and Custody Bank

Central Securities Depository

March 13, 2014 8

Trading Framework

BİAŞ Members Banks

Brokerage Houses

BİAŞ

Debt Securities Market

İstanbul Settlement

and Custody Bank

Central

Securities

Depository

Central Bank of TR Investors

Domestic/ Foreign

Individual / Institutional

Real-time

communication

Trading Workstation

and/or API

DSM Trading System

March 13, 2014 10

DSM ASTS Characteristics

Borsa İstanbul Debt Securities Market uses "Automated Securities

Trading System" (ASTS) since August 1999

ASTS is an Electronic Trading Platform with the following

characteristics:

Secure connection via IP address restrictions (each member firm

have a range of IP address defined to connect to the system)

Alternative WAN connections using two separate ISP (Türk Telekom

and Turpak)

Disaster recovery site (Fail-over site) ready to replace Production site

in 4 hours with an expected of 1 minute data loss and starting at 50%

user capacity

Alternative ways of sending orders to Trading system:

Trading Workstation : full range of functionality

API connection : faster way of sending orders especially customer orders

(Automated Programming Interface)

March 13, 2014 11

DSM ASTS Characteristics

ASTS characteristics:

Order driven

Multiple price - continuous auction trading system

Auto matching process according to price/rate then time of orders

Different trading sessions are maintained by trading events (same

day trades vs forward day trades etc)

Repo deposit entry using Trader Workplaces (TW)

Margin deposit entry using TWs

Immediate screening of order/trade information and settlement

balances via TWs

Order withdraw/amend possible by members firms

Real-time risk management by continuously calculating cash

positions

Segregated surveillance module monitoring suspicious trades daily

and historically

March 13, 2014 12

ASTS Network Map

DSM

Trading System Engine

Member Firms’ Offices

İstanbul Settlement

and Custody Bank

Trading

Terminal (Multiuser)

Wide Area

Network

Alternative

connection with

2 different ISP

Real-time data

communication

Real-time data

communication

March 13, 2014 13

ASTS – Order Entry

March 13, 2014 14

ASTS – Order Book & MBO

March 13, 2014 15

ASTS – Market Watch

March 13, 2014 16

ASTS – Orders&Trades

March 13, 2014 17

ASTS – Cash Settlement Balance

March 13, 2014 18

ASTS – Security Settlement Balance

March 13, 2014 19

ASTS – Settlement Balance Aggregation

March 13, 2014 20

ASTS – Repo Deposit Entry

Primary Dealer System

March 13, 2014 22

Primary Dealer Sytem

As a part of increasing liquidity of debt instruments plan, Turkish

Treasury has adopted primary dealer system for government

debt securities since May 8, 2000

Turkish Treasury is the initiator of the Primary Dealer Program

that sets the rules and liabilities

Treasury determines and announces the Primary Dealer

members that are obliged to quote bid and offer prices in

benchmark securities in BİAŞ DSM Outright Purchases and

Sales Market

Primary dealership contract that is signed between assigned

primary dealer members and Treasury defines rules and

liabilities of counterparts for both primary and secondary market

transactions

March 13, 2014 23

Primary Dealer Sytem

Primary dealer system is an implementation of Trukish

Treasury for government debt securities that is carried out

in Borsa İstanbul DSM Outright Purchases and Sales

Market in order to increase the liquidity in the secondary

markets

Primary Dealer system is integrated into DSM ASTS

system in terms of order book, matching and settlement

balances calculation

There is no separate order book and therefore matching

mechanism for PD orders

PD trades are included member firm’s net settlement

balance calculations

March 13, 2014 24

Primary Dealer Sytem

PD bid and offer quotes are treated as regular orders that

go to normal order book of the related security and can

match with non-PD orders as well

PD quotes are conveyed to the market with PD account

code (see order entry window)

There is also an exclusive PD quote window that can be

used for mass quote order entry

There is an exclusive screen in data vendors where only

PD quotes are displayed in real-time

March 13, 2014 25

Primary Dealer Rights

According to the PD contract Clause 5; the rights of primary dealers are:

a) Primary Dealer has the right to use the title of “Turkish Primary Dealer”.

b) Primary Dealer is exempt from the collateral requirement for participation in auctions.

However, in case the Primary Dealer fails to meet its obligations after an auction, it will be

subject to the same penalties applied to other auction participants.

c) The Primary Dealer has the right to submit non-competitive bids before the auctions.

The total amount to be issued via accepting non-competitive bids cannot be more than

30% of the upper limit of the auction.

d) Primary Dealer has the right to submit option bids after an auction till 14.00 p.m. on the

issue date.

e) Treasury conducts cash operations in the money market with Primary Dealers.

f) Primary Dealer has the exclusive right to participate in “TAP” sales.

g) The Primary Dealer has the exclusive right to serve as an intermediary in “public

offerings”.

h) The Primary Dealer has the exclusive right to participate in Buy-back and Switching

auctions.

i) The Primary Dealers has right to participate in the Primary Dealership Consultation

Board with two representatives.

j) The Primary Dealer has right to borrow and lend securities at the Securities Lending

Market established at the Central Bank.

March 13, 2014 26

Primary Dealer Obligations I

According to the PD contract Clause 6; obligations of primary dealers are:

a) for primary market transactions;

- purchase a minimum amount of the issues programmed by the Treasury monthly (amount

calculated by Treasury)

- purchase a minimum amount of the issues programmed by the Treasury quarterly (amount

calculated by Treasury)

b) for secondary market transactions PD’s are obliged to enhance liquidity of benchmark securities.

To achieve this goal, PD member shall, on every trading day, quote bid and offer prices

continuously for benchmark securities specified by the Treasury. The quotations shall meet the

following criteria;

- The quotations shall be given on every trading day of BİAŞ, between 9:45-12:00 and 13:15 -

16:00

- The minimum size of quotations shall be 5 million TRY in nominal terms

- Bids and offers will be quoted in terms of prices for coupon-securities and the maximum

spread between bid and offer quotations will be 50 Kuruş (half of 1 TRY). For zero-coupon

securities, the quotations will be given in terms of simple-annual interest yield

Interest Rate Interval

(For Bid Quotations)

Maximum Spread Between

Bid and Offer Rates (Basis Points)

9.99 % and below 0.13

10.00 % - 19.99 0.25

20.00 % and above 0.50

March 13, 2014 27

Primary Dealer Obligations II

According to the PD contract Clause 6; obligations of primary dealers are:

b) for secondary market transactions;

- If the quotation sizes descend below 5 million TRY as a result of a transaction or the

quotations are called back for any reason, the Primary Dealer will renew the quotations in 5

minutes.

- The quotations shall be submitted with the “PY” account code (to differentiate between other

accounts).

- BİAŞ DSM monitors PD quotes every day in terms of time and quantity of quotations by a

daily report.

- In the calculation of the violations of quotation obligations, the average of the violations of all

Primary Dealers in terms of number and duration are calculated separately. The Primary

Dealer violates the obligation if both of the violations of Primary Dealer are above the

average of the violations of all Primary Dealers. If the monthly average violation in terms of

number is below 1, monthly average violations in terms of number are assumed to be 1.

- Primary Dealer is responsible for submitting detailed information on technical problems

faced during quotation process in the ISE Bonds and Bills Market for benchmark securities.

The information shall be submitted in 3 (three) working days to the ISE Bonds and Bills

Market and to the Undersecretariat.

March 13, 2014 28

Benchmark Securities

Benchmark securities are chosen by the Treasury by taking into account

the total issue size, the maturity and the trading volume in the secondary

markets.

Currently here are 9 benchmark securities selected by Treasury.

Primary Dealers have to select 6 benchmark securities out of 9 benchmark

securities consisting at least 4 fixed rate, 1 floating rate and 1 CPI indexed

security.

By informing the Treasury 1 week before, the primary dealer can change

the set of benchmark securities for the following 3 month period.

Benchmark securities lose their benchmark qualifications when there are

182 days remaining to their maturity. If necessary, by majority vote of

Primary Dealers and the approval of the Undersecretariat the benchmark

securities can be changed.

The Undersecretariat keeps the right to lift the quotation liability of the

Primary Dealer for a temporary period and to increase the maximum

spreads.

March 13, 2014 29

Primary Dealer Order Entry

Primary dealer system is an implementation of the Treasury in the secondary markets to

increase the liquidity

This system is carried out in Outright Purchases and Sales Market of BİST Debt

Securities Market

Automated Securities Trading System (ASTS), which runs in Debt Securities Market, has

a different order entry screen for PD quotations where buy and sell quotation can be

managed with a single window

Benchmark securities are all listed in the PD order entry window with buy and sell

spreads determined by the Treasury. Although PD members can change the spread, they

cannot lower it from the default value.

PD members, define the buy price/yield and quantity (minimum of 5 million TRY in

nominal). Sell price/yield is automatically calculated regarding the spread

PD members can choose to enter all orders (HEPSİ ==> button) or selected orders

(SEÇİLEN ==> button). Moreover, they can choose to cancel all orders (HEPSİ X button) or

selected orders (SEÇİLEN X button)

Primary dealer members can only have one buy/sell quotation for a benchmark security

(orders that are entered with a PY code in the account field). Therefore; if all or selected

orders are entered, previous outstanding PD orders are automatically cancelled by ASTS

Moreover, PD buy and sell orders for a given benchmark security cannot match. If

matching conditions are met for the same PD member then latest quotation is automatically

cancelled by ASTS. However, PD quotations can match other PD quotations, other PD’s

regular orders or non-PD member’s regular orders

March 13, 2014 30

Primary Dealer Order Entry Screen

March 13, 2014 31

Primary Dealer Quote Screen

March 13, 2014 32

Primary Dealer Benefits in DSM

Along with simple and easy-to-use PD quotation

management screen, PD members get an exchange trade

fee discount for their PD trades only

While a regular trade in DSM Outright Purchase and Sales

Market has a 0.1 / 10,000 exchange fee rate, PD trades has

a 0.075 / 10,000 exchange fee (applied on the value of the

trade)

March 13, 2014 33

Primary Dealer - Trading Statistics

% Share of Traded Value

Year Primary Dealer OPS Market % of OPS

2010 12,089 574,270 2.11

2011 24,103 499,761 4.82

2012 19,612 397,905 4.93

2013 25,989 376,163 6.91

Traded Value (Million USD)

2010 - 2013 PD Trade Statistics

March 13, 2014 34

Primary Dealer System – Future Agenda

Introduce market maker system system where selected

members will give two-way quotations for corporate

securities

As in government securities market maker system,

members will be liable for certain securities that are elected

as benchmark securities

Security ISIN code and member ID will be correlated in the

reference database so that two-way quotations will be

monitored continuously

Market members will have privileges regarding market

transactions and issues

Exchange Trade Fees &

Taxes

March 13, 2014 36

Fee Schedule

On-Exchange Transaction Fee Outright Purchases&Sales 0.1 / 10,000

Repo-Reverse Repo 0.05 / 10,000 x Repo Duration

Primary Deal OPS Trades 0.075 / 10,000

For same day value trades after 14:00

• Outright Purchases&Sales 0.2 / 10,000

• Repo-Reverse Repo 0.1 / 10,000 x Repo Duration

Off-Exchange Registration Fee (OTC Trades) Outright Sales&Purchases 0.2 / 10,000

Repo-Reverse Repo 0.1 / 10,000 x Repo Duration

Listing Fee % 0.1 of the nominal issue amount (Min 1,000 TRY / Max 10,000 TRY)

Annual Quotation Fee ¼ of the Listing Fee

March 13, 2014 37

Taxes

Outright Purchases and Sales

Interest income is subject to 10% withholding tax

Repo-Reverse Repo Transactions

Repo revenues obtained from repo transactions are subject to

15% withholding tax. This tax is paid to the Turkish Treasury by

the repo member on behalf of reverse repo side -obtainer of the

repo revenue ( value date 2 amount is the net of

principal+interest-tax )

Exceptions

Pension funds, investment trusts and exchange trading funds

are exempt from withholding taxes stated above

Market Figures

March 13, 2014 39

Market Members

Brokerage

Houses Banks Total

Outright Purchases and

Sales Market 81 42 123

Repo-Reverse Repo

Market 48 40 88

Repo Market For

Specified Securities 36 27 63

Equity Repo Market 26 2 28

Foreign Securities

Market 5 13 18

As of February 28, 2014

March 13, 2014 40

Outstanding Securities

* As of February 28, 2014

** Stripped securities are counted as single issue

Type Number Issue Nominal (Million USD)

Government Securities 49 181,629

Public Lease Certificates 6 5,592

Corporate Bonds 169 6,383

Bank Bills 65 8,711

Commercial Paper 14 410

Asset-Backed Securities 64 412

Corporate Lease Certificates 9 354

Structured Debt Securities 4 6

Total 380 202,711

Issue Q

92,00%

Issue #

85,52%

March 13, 2014 41

DSM - Historical Traded Value Figures

Outright Purchases

and Sales Market

Offerings Market for

Qualified Investors

Repo-Reverse

Repo Market

Interbank Repo

Market

Repo with Specified

Securities MarketEquity Repo Market Total Daily Average

Million US$ Million US$ Million US$ Million US$ Million US$ Million US$ Million US$ Million US$

1991 312 312 2.29

1992 2,406 2,406 9.58

1993 10,728 4,794 15,522 63.10

1994 8,832 23,704 32,536 128.60

1995 16,509 123,254 139,763 554.62

1996 32,737 221,405 254,142 1,008.50

1997 35,472 374,384 409,856 1,626.41

1998 68,399 372,201 440,601 1,762.40

1999 83,842 589,267 673,109 2,714.15

2000 262,941 886,732 1,149,673 4,580.37

2001 37,297 627,244 664,541 2,647.57

2002 67,256 480,725 547,982 2,165.94

2003 144,422 701,545 845,967 3,383.87

2004 262,596 1,090,476 1,353,072 5,369.33

2005 359,371 1,387,221 1,746,591 6,876.34

2006 270,183 1,770,337 2,040,520 8,129.56

2007 278,873 1,993,283 2,272,156 9,016.49

2008 239,367 2,274,077 2,513,444 10,013.72

2009 269,977 1,929,031 2,199,008 8,726.22

2010 297,710 27 2,010,217 101 2,308,055 9,232.22

2011 291,088 151 1,744,291 408,465 5,065 2,449,059 9,680.08

2012 199,791 663 2,077,008 1,530,927 5,302 3,813,692 15,073.88

2013 214,967 780 1,655,482 1,742,184 10,525 0.03 3,623,940 14,495.76

2014 02 28 20,796 162 204,320 434,916 996 0.00 661,189 15,742.60

March 13, 2014 42

DSM - Daily Average Traded Value

Daily Average - Million USD

As of February 28, 2014

March 13, 2014 43

DSM vs OTC

Total Traded Value - % Share

As of February 28, 2014

March 13, 2014 44

DSM vs OTC

Sub-Markets - % Share

Outright Transactions

Repo Transactions

As of February 28, 2014

55.34

39.46 40.79

45.42 44.66

60.54

59.21 54.58

0.00

20.00

40.00

60.00

80.00

100.00

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

DSM OTC

92.12 91.83

91.56

7.88 8.17

8.44

0.00

20.00

40.00

60.00

80.00

100.00

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

DSM OTC

March 13, 2014 45

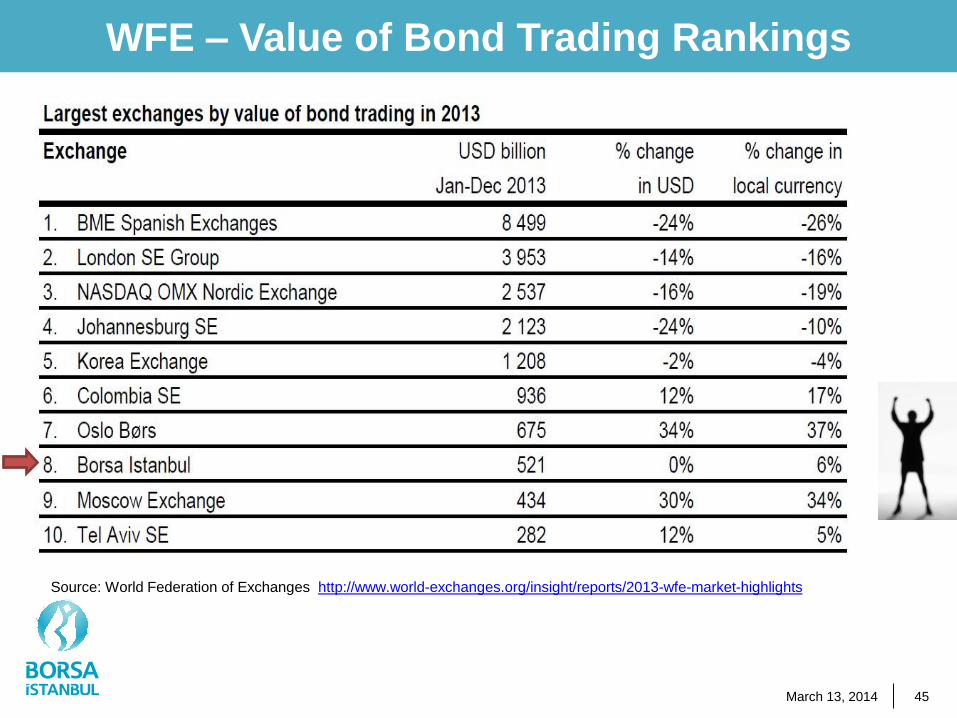

WFE – Value of Bond Trading Rankings

Source: World Federation of Exchanges http://www.world-exchanges.org/insight/reports/2013-wfe-market-highlights

March 13, 2014 46

WFE - Global Bonds Trading Rankings

2012-2007 – Billion USD

Source: World Federation of Exchanges http://www.world-exchanges.org/statistics

Value Rank Value Rank Value Rank Value Rank Value Rank Value Rank

BME Spanish Exchanges 11.132 1 17.412 1 11.030 1 8.181 1 6.839 1 5.863 1

London SE Group 4.575 2 5.394 2 4.022 2 5.120 2 6.567 2 3.603 2

NASDAQ OMX Nordic 3.031 3 2.674 4 2.620 3 2.257 3 2.924 3 2.798 3

…

Borsa İstanbul 520 7 518 8 446 8 401 7 390 5 467 5

2007Exchange

2012 2011 2010 2009 2008

What’s Behind These Figures ?

March 13, 2014 48

Trading Platform

Secure and steady connection

Multi-function (from order entry to settlement balance view)

Multi-asset and currency

Real-time risk and collateral management

Portfolio, customer, funds and PD accounts to select from

Order cancellation possible at the disposal of the member (untill

order match)

Trade cancellation possible upon counterparties’ request (subject

to approval of Borsa İstanbul)

Change of account type upon request of counterparties (only from

funds to portfolio)

User management via different roles (firm manager, trader etc)

and levels of authority within a firm

Real-time order and trade information dissemination (anonymous

– no member or account id)

March 13, 2014 49

High Issue Volume

Treasury periodically (monthly/quarterly) announces its

domestic borrowing strategy stating financing program and

issue calender since 2001

Having a transparent debt management service lets the

market members as well as investors to rationalize their

needs and expectations

As of February, 2014, there are 55 outstanding government

securities with an average maturity of 5,7 years and total

issue nominal value of 185 billion USD

As of February, 2014, total number of corporate securities

is 325 with outstanding nominal value equal to 17 billion

USD and average maturity of 1,5 years

March 13, 2014 50

Coordination with regulatory authorities

Coordination with Treasury, Central Bank and Capital Markets

Board, is a crucial part of secondary market success

Borsa İstanbul and regulatory authorities periodically meet to

revise the needs of the markets and take necessary acts to

improve market efficiency

Treasury is the main supplier of the debt instruments

Central Bank is a member of the market that acts as price/rate

regulatory agency. Moreover, it acts as the Treasury agency

for debt issuance and provides depository account services

for government securities

Capital Markets Board, defines the legal framework of the

market and is responsible for conducting the Capital Markets

Law. It gives licences for security trading and repo

transactions

March 13, 2014 51

Cooperation with market participants

• Market is the playground for the members hence they

ought to have a word on its functioning

• Borsa İstanbul periodically meets with its members under

the framework of Membership Relations Committee

• Representatives of members attend the Committee

meetings and express their views on the working of the

market. They may also convey their suggestions/demands

for new products, ease of operation or deduction in fees

etc

• Upon the request of the members, Borsa İstanbul

considers the legal and operational workplan of the request

and conduct the project

March 13, 2014 52

Presence of the Central Bank

Central Bank of Turkey is a natural member of Debt

Securities Market in order to attain it’s main role of

maintaining price stability

It plays a regulatory role for price fluctuations, mainly in

repo markets. It sets upper and lower rates and places its

orders at the boundaries

All short-term cash needs of market members are

eventually met without any unexpected price changes

(lender of the last resort)

Having Central Bank at each side of the market, generally

lets the market members to borrow/lend money between

them at the rates within the price coridor

March 13, 2014 53

Lessons learned from past crisis

• Russian and Asian financial crises, as well as Turkey’s own

financial crises of 1994 and 2001 have increased the need

of safe trading, clearing and settlement

• Crisis acted like a test for the smooth functioning of the

market and showed the deficiencies

• New rules and risk management tools are designated and

enforced

• Protection of investors’ rights as well as safe trading

environment has became primary criteria rather than

trading volume

Future agenda

March 13, 2014 55

DSM Future Agenda

Considering the potential of Turkey due to its geographical

position, cultural heritage and stable growth rates there is still

way to go. DSM agenda has the following items to be

performed:

Opening ˝Committed Transactions Market of Sukuk˝ where Islamic

financial instruments are used

Introducing market maker system for corporate securities that will

enhance trading liquidity of these securities

Opening ˝Auction Market˝ where security issues can take place with

different issue methods such as single price, floating price within a range

and multi price

Opening ˝OTC Negotiated Deal Screen˝ where OTC trades will be

reported with counterparts mutually confirming trade details

Forming joint trading platforms with neighboor exchanges such as Balkan

countries, Turkic republics as well as with US, Europe and/or Far East

exchanges to enhance alternative ways of accessing trading platform and

to attrack new investors from all around the world