Debt Investor Update Full Year 2019 Strong performance in 2019 · Frequent benchmark issuer in EUR,...

22

Debt Investor Update Full Year 2019 Strong performance in 2019

Transcript of Debt Investor Update Full Year 2019 Strong performance in 2019 · Frequent benchmark issuer in EUR,...

Debt Investor Update Full Year 2019

Strong performance in 2019

2

Disclaimer

This presentation is not an offer or invitation to subscribe for or purchase any securities in any jurisdiction, including any jurisdiction of

the United States. Securities may not be offered or sold in the United States absent registration or pursuant to an available exemption

from registration under the U.S. Securities Act. Deutsche Pfandbriefbank AG (pbb) does not intend to conduct a public offering of

securities in the United States.

No warranty is given as to the accuracy or completeness of the information in this presentation. You must make your own

independent investigation and appraisal of the business and financial condition of pbb and its direct and indirect subsidiaries and their

securities. Nothing in this presentation shall form the basis of any contract or commitment whatsoever.

This presentation may only be made available, distributed or passed on to persons in the United Kingdom in circumstances in which

section 21(1) of the Financial Services and Markets Act 2000 does not apply.

This presentation may only be made available, distributed or passed on to persons in Australia who qualify as 'wholesale clients' as

defined in section 761G of the Australian Corporations Act.

This presentation is furnished to you solely for your information. You may not reproduce it or redistribute to any other person.

This presentation contains forward-looking statements based on calculations, estimates and assumptions made by the company’s top

management and external advisors and are believed warranted. These statements may be identified by such words as ‘may’, ‘plans’,

‘expects’, ‘believes’ and similar expressions, or by their context and are made on the basis of current knowledge and assumptions.

Various factors could cause actual future results, performance or events to differ materially from those described in these statements.

Such factors include general economic conditions, the conditions of the financial markets in Germany, in Europe, in the United States

and elsewhere, the performance of pbb’s core markets and changes in laws and regulations. No obligation is assumed to update any

forward-looking statements.

By participating in this presentation or by accepting any copy of the slides presented, you agree to be bound by the noted limitations.

Investor Update based on annual results 2019 (IFRS, pbb Group, audited), March 2020

Business model & strategy

pbb is a leading commercial real estate lender with a complementary

public investment finance business

LENDING FUNDING

Stable and well diversified

funding base

Pfandbrief (leading

issuer)

Senior unsecured bonds

(preferred/non-preferred)

Frequent benchmark issuer

in EUR, USD, GBP, SEK

and CHF plus private

placements

Retail deposits (online)

Specialised

on-balance sheet lender

European franchise,

complemented by the US

High risk standards and

focus on risk management

Key figures (IFRS) 31/12/19

Total assets € 56.8 bn

Total equity € 3.2 bn

RWA € 17.7 bn

CET1 ratio1 15.2%

Leverage ratio1 5.4%

RoE before taxes 6.9%

FTE 752

Pfandbrief-eligible

senior loans, REF portfolio:

avg. LTV 53%

Structuring expertise for

complex/large transactions

~150 deals p.a.

Avg. deal size € 50-60 mn

Long standing client

relationships

Real Estate Finance (REF)

Partner to professional national and international

real estate investors

One of the top commercial real estate finance

banks in Germany and Europe

Strategic portfolio – moderate growth targeted

Public Investment Finance (PIF)

Partner to public sector for project related

infrastructure investments2 and ECA guaranteed

export financing

Contribution business (earnings stabilisation,

cost/capital synergies)

Strategic portfolio in “hold” mode

50% 9% Germany USA

12%

Poland 4%

UK

11%

France

Sweden 3%

Austria 2%

8%

Czech Republic 1% Other Europe

46%

19%

16%

Mixed use 2%

Logistics/

storage

Office

Retail

Residential

Other 3% Hotel 5%

10%

Portfolio 31/12/19: € 29.8 bn (EaD)

52%

22%

14%

Nordics 2%

UK 2%

France Spain

Rest of World 1%

Germany

Austria 4%

Other Europe 4%

50%

27%

19%

PSE

Reg. Gov.

(incl. related)

Sov.

(incl. related)

Other 3%

Portfolio 31/12/19: € 7.1 bn (EaD)

1 Incl. full-year result, post proposed dividend 2019 2 incl. public housing, utilities and waste disposal, health care and nursing care properties, childcare and educational facilities

Debt Investors Considerable MREL buffer

Strong capital base

High quality cover pools

High portfolio quality and

risk standards

Strong operating

performance

Headquarter

Branches/Rep. Offices

USA

Regional presence (10 offices)

Investor Update based on annual results 2019 (IFRS, pbb Group, audited), March 2020 3

Pre-tax profit € mn (IFRS)

Highlights

Operating and financial overview

New business € bn (commitments, incl. extensions >1 y)

Net interest and commission income € mn (IFRS)

Note: Figures may not add up due to rounding 1 New definition: CIR = (GAE + net income from write-downs and write-ups on non-financial assets)/operating income 2 Taking into account AT1 coupon (pro-rata 2018: € 12 mn; 2019: € 17 mn)

General and admin. expenses € mn (IFRS)

Net income from risk provisioning € mn (IFRS)

Portfolio € bn (financing volumes)

1.8

4.2

2.6

2.4

2.4

2.6

4.7

2017

2.1

2.0

2018

2.1

2.6

2.0

2019

11.6 10.5

9.3

Q1

Q4

Q3

Q2

RoE b.t.

2017 2018 2019

7.3% 7.1%2 6.9%2

47 48 48

56 74 69

51 49 70

50 44

216

29

215

2017 2018 2019

204

Q2

Q3

Q4

Q1

73% 70% 72%

2018

12.1

24.9

13.8

2019

7.0

13.2

2017

26.8

6.4 6.3

27.1

45.7 46.4 45.5

VP PIF REF

Strategic

portfolio

Share of

strategic

portfolio

100 108 117

101 115 115

103 115 113

111 118 119

2017 2019

Q2

2018

Q3

Q4

415

Q1

456 464

43% 47% 44%

2018

45 44 46

47 44 47

49 48 48

58 57 61

199

Q4

2017 2018

Q2

2019

Q1

Q3

193 202

CIR1

-10 -14

-49

2017 2018 2019

Investor Update based on annual results 2019 (IFRS, pbb Group, audited), March 2020 4

Key drivers 2019:

New business volume stays on solid level while pbb remains highly

selective – in line with guidance of € 8.5-9.5 bn

REF – core portfolio with moderate growth strategy

Continued conservative approach

Avg. LTV 58%2

Cautious in UK and on Retail

Supplemented by USA, Office and Residential

Avg. REF gross interest margin stable at ~155 bp (2018: ~155 bp)

PIF – portfolio on hold with low new business volume

(2019: € 0.3 bn; 2018: € 1.0 bn)

New

bu

sin

es

s

(Com

mitm

ents

, in

cl.

exte

nsio

ns >

1ye

ar)

Note: Figures may not add up due to rounding 1 Legal maturities 2 New commitments; avg. LTV (extensions): 2019: 55%; 2018: 57% 3 Austria, Italy, Luxembourg, Netherlands, Switzerland

New business

REF new business volume of € 9.0 bn in line with guidance – avg. REF gross interest margin

stable at ~155 bp y-o-y

FY18 9M/19 FY19

Total volume (€ bn) 9.5 6.9 9.0

thereof:

Extensions >1 year 2.2 1.5 1.9

No. of deals 185 115 155

Avg. maturity (years)1 ~4.7 ~4.6 ~4.6

Avg. LTV (%)2 59 59 58

Avg. gross interest margin (bp) ~155 >150 ~155

FY19: € 9.0 bn FY19: € 9.0 bn

50%

22%

12%

7%

Office

Hotel/Leisure 2%

Retail

Logistics/

storage 7%

Mixed use/

other

Residential

Po

rtfo

lio

(E

aD

, B

asel III)

50%

12%

11%

9%

8%

Germany

UK

USA

France

Other

CEE 6%

Nordics 5%

46%

19%

16%

Residential

Office

Hotel 5%

Retail

Logistics/

storage 10%

Mixed use/other 4%

31/12/19: € 29.8 bn 31/12/19: € 29.8 bn

Regions Property types

47%

15%

12%

7%

8%

Germany

France

USA

Nordics 5%

CEE 6%

UK

Other 3

REF new business

24.9 26.8 27.1

4.0

1.9

3.8

2017

2.3

2.6

2.0

1.9

1.9 1.7

2018

2.1

2.5

2.5

2019

Q4

Q3

Q2

Q1

10.7 9.5 9.0

REF New business € bn (commitments, incl. extensions >1 yr)

Financing

volume

Investor Update based on annual results 2019 (IFRS, pbb Group, audited), March 2020 5

Portfolio

Continued high portfolio quality with an average LTV of 53%;

Non-performing loans up in 2019, but still on low level

REF Portfolio: Avg. weighted LTVs % (commitments)1

Non-performing loans € mn (EaD, Basel III)

0.6%

0.9%

0.6%

332 380 495

16

09/19 12/18

15

12/19

15 348 395

510

Workout2

Restructuring3

NPL

ratio4

Investor Update based on annual results 2019 (IFRS, pbb Group, audited), March 2020

Note: Figures may not add up due to rounding 1 Based on performing investment loans only 2 Internal PD class 30: No signs that the deal will recover soon, compulsory measures necessary 3 Internal PD class 28+29: Payments more than 90 days overdue or criteria acc. to respective policy apply 4 NPL ratio = NPL volume / total assets 5 prior to the Brexit referendum in 2016

53%

58%

12/155

54%

12/13 09/19 12/19

64%

Avg. LTV:

Retail properties

19%

UK

16%

12%

28% 29%

16%

12/13

12/19

12/155

REF Portfolio:

Share of UK and retail properties reduced

% (EaD, Basel III)

6

54%

Germany Rest of

Europe

UK France

50%

USA Sweden Poland

09/19: Ø 54%

12/19: Ø 53%

53% 53% 52% 54% 56% 53% 51%

55% 58% 56% 56% 55%

09/19

12/19

Capital

Capitalisation remains strong – as expected and already communicated RWA increase

in Q4 due to LGD parameter recalibration; EBA and Basel IV anticipated

Basel III: Equity and capital ratios

(IFRS)

Note: Figures may not add up due to rounding 1 Incl. full-year result, post dividend 2018 2 Excl. interim result 3 Incl. full-year result, post proposed dividend 2019

Basel III: RWA

€ bn (IFRS) Key drivers Q4/19:

Risk weights geared to expected requirements from EBA and Basel IV

Recalibration of LGD parameters as of 31/12/2019 towards expected

Basel IV levels

Transfer of parts of the portfolio into standard approach (KSA),

predominantly affecting public sector assets

RWA increase in line with expected and communicated range of € 4-5 bn

(vs. Q2/19: € +4.1 bn; vs. Q3/19: € +3.4 bn)

14.6

12/18 06/19 12/19 09/19

13.6 14.3

17.7

SREP requirements 2020:

Requirements for CET1 and Own funds unchanged:

CET 1 ratio: 9.5% (2019: 9.5%)

Own funds ratio: 13.0% (2019: 13.0%)

Anticipated countercyclical buffer increased from 35bp to 45bp Capital ratios in %

12/181 09/192 12/193

CET 1 18.5 18.3 15.2

Tier 1 20.5 20.4 16.9

Own funds 24.9 24.8 20.4

Leverage ratio 5.3 5.1 5.4

Capital in € bn 12/181 09/192 12/193

CET 1 2.7 2.6 2.7

AT 1 0.3 0.3 0.3

Tier 2 0.6 0.6 0.6

Total Equity 3.6 3.6 3.6

+4.1 +3.4

Investor Update based on annual results 2019 (IFRS, pbb Group, audited), March 2020 7

SP4

Funding

Ambition level for Own Funds and Eligible Liabilities of more than 8 % TLOF (in € as of 31/12/2019)

AT1

capital and

bail-in stack

SNP

remaining

after 3 years ...5 years ...10 years

Subord.3

CET15

€ ~ 4.0 bn 8 % TLOF

€ ~ 15 bn

€ ~ 9.6 bn

€ ~ 3.6 bn

Substantial buffer for Senior Preferred

(SP) investors due to high volume of

capital instruments and Senior Non-

Preferred (SNP) liabilities

Existing Senior Non-Preferred liabilities

have long remaining terms

SP is expected to be the prevailing

senior product in the near-term, but

SNP will remain an element of pbb´s

funding strategy

pbb has a MREL-ambition level

of > 8 % TLOF

Regulatory requirements (SREP,

MREL etc.) are comfortably met

Own Funds and

Eligible Liabilities

€ ~ 8.5 bn

SNP2

> 1 Y

AT1

CET1

T2

Composition of

Liabilities (31/12/2019)

Rundown MREL1

(31/12/2019)

Other

1 pbb has set its ambition level at > 8% TLOF. As of 31 Dec 2019, MREL eligible items amounted to ~17% TLOF / ~48% RWA 2 MREL-eligible Senior Non-Preferred Debt >1Y according to legal maturities 3 Nominal amount of Tier 2 instruments; the capital stack

includes € 300 mn AT1 issuance callable in 2023 and € 300 mn T2 issuance callable in 2022 4 Senior Preferred, structured unsecured and corporate deposits (excl. protected deposits) 5 CET1 assumed to be constant

Investor Update based on annual results 2019 (IFRS, pbb Group, audited), March 2020 8

Funding

Increased funding volumes in line with plan

High share of foreign currencies reducing derivative volume

9

0.5

0.8

1.1

0.3

0.7

Public

3.6

2.9

Mortgage Public Unsecured

2.1

Mortgage

1.9

<0.1

1.7

Unsecured

3.6

1.6

2.9

0.3

2019: € 6.7 bn

Tenor (av, yrs)3

6.7 16.1 5.9

15 21 74 Spread (av, bp)2

Note: Figures may not add up due to rounding 1 Excl. retail deposit business 2 vs. 3M Euribor 3 Initial weighted average maturity 4 Excl. AT1 issuance 5 Initial weighted average maturity of term deposits

New long-term funding1

€ bn

Pfandbrief Pfandbrief

2018: € 5.2 bn4

7.6 20 6.4

6 0 42

Private placements

Benchmark issuances

Senior Unsecured

€ 1.25 bn Senior Preferred raised with two €-Benchmarks (4y

and 5y)

CHF-Benchmark 125 mn Senior Preferred issued (4y)

GBP-Benchmark 250 mn issued (3y). pbb was the first

German bank issuing a Senior Preferred Benchmark in

Sterling.

Strong private placement activity including € 1.6 bn and

SEK 2.5 bn Senior Preferred as well as € 128 mn Senior Non-

Preferred

pbb direkt

Total volume reduced to € 2.8 bn (12/18: € 3.0 bn) to optimize

funding costs

Average maturity5 increased to 4.2 years (12/18: 4.0 yrs)

Funding structure and liquidity

ALM profile and liquidity position remain comfortable

(NSFR >100%; LCR >150%)

Pfandbriefe

Pfandbrief volume dominated by Benchmarks

€ 1.55 bn Mortgage Pfandbriefe issued, comprising two

€ 500 mn Benchmarks (5y and 6y) and several taps

$ 650 mn 3y Mortgage Pfandbrief issued as Benchmark

With SEK 3.7 bn (3y and 4y) pbb is the largest Pfandbrief

issuer in SEK

One existing Public Sector Pfandbrief Benchmark tapped with

€ 250 mn

Investor Update based on annual results 2019 (IFRS, pbb Group, audited), March 2020

10

Funding

Investment opportunities

Pfandbrief Investments

One of the largest Pfandbrief issuers with 16 € benchmarks outstanding and a strong presence in the GBP, SEK and USD market

Benchmarks issued with maturities up to 2035

Very low weighted average LTV of 34.28% in the Mortgage Cover Pool (based on market value)

Private Placements starting with € 1 mn and maturities up to 30 years

Available currencies: EUR, GBP, SEK, USD

Unsecured Investments

2 € senior preferred and 3 € senior non preferred benchmarks outstanding

Private Placements starting with € 1 mn and maturities up to 30 years

Available currencies (e.g. EUR, GBP, SEK, USD, CHF, NOK, YEN, CZK)

Senior “preferred” (rated A-) and “non preferred” (rated BBB-) products

Focus on the development of the funding franchise

New debt product “Senior Preferred” opens the access to a larger investor base.

Co-operation with Origin for the MTN placement and Deposit Solutions for our retail deposit brand pbb direkt in order to

stream line internal processes.

Investor Update based on annual results 2019 (IFRS, pbb Group, audited), March 2020

Outlook 2020

Note: Figures may not add up due to rounding 1 Incl. extensions > 1 year 2 Incl. full-year result, post (proposed) dividend

Operating trends 2018 2019 Guidance 2020

Real Estate Finance (REF)

New business volume1 (€ bn) 9.5 9.0 € 8.0-9.0 bn

Avg. gross margin (bp) ~155 ~155 Slightly lower

Financing volume (€ bn) 26.8 27.1 Moderate increase (strategic portfolio)

Public Investment Finance (PIF)

Avg. gross margin (bp) >60 >80 Stable (strategic portfolio in “hold” mode)

Financing volume (€ bn) 6.4 6.3

Value Portfolio (VP)

Financing volume (€ bn) 13.1 12.1 < € 11.5bn (non-strategic portfolio in run-down mode)

Income statement (IFRS, EUR mn) 2018 2019 Guidance 2020

Net interest and commission income 456 464 Largely stable

Loan-loss provisions -14 -49 Stable; 15-20bp EL on REF financing volume

General administrative expenses -193 -202 Stable

Pre-tax profit 215 216 € 180-200 mn

Key ratios (%) 2018 2019 Guidance 2020

RoE before taxes 7.1 6.9 5.5-6.5%

RoE after taxes 5.9 5.7 4.0-5.0%

CIR 44.2 43.5 Slightly higher

CET1 ratio2 18.5 15.2 Significantly above SREP requirement of 9.5% + countercyclical buffer of

0.45% (2019: 9.5% + 0.35%)

Investor Update based on annual results 2019 (IFRS, pbb Group, audited), March 2020 11

12 Investor Update based on annual results 2019 (IFRS, pbb Group, audited), March 2020

Funding / Debt Investor Relations

Götz Michl +49 (0)6196 9990 2931

Silvio Bardeschi + 49 (0)6196 9990 2934

Funding Desk [email protected]

Webpage: www.pfandbriefbank.com/investors/debt-investors.html

Contact details

© Deutsche Pfandbriefbank AG

Parkring 28

85748 Garching/Germany

+49 (0) 89 28 80-0

www.pfandbriefbank.com

Appendix

13 Investor Update based on annual results 2019 (IFRS, pbb Group, audited), March 2020

Key figures

pbb Group

Income statement (€ mn) 2017 Q1/18 Q2/18 Q3/18 Q4/18 2018 Q1/19 Q2/19 Q3/19 Q4/19 2019

Net interest income 407 107 113 114 116 450 116 113 112 117 458

Net fee and commission income 8 1 2 1 2 6 1 2 1 2 6

Net income from fair value measurement -5 - 4 -2 -11 -9 -2 -5 5 -5 -7

Net income from realisations 45 9 6 8 9 32 6 10 15 17 48

Net income from hedge accounting -1 -1 -1 1 - -1 -1 - -2 1 -2

Net other operating income -1 -4 -5 -3 5 -7 -1 -1 2 3 3

Operating Income 453 112 119 119 121 471 119 119 133 135 506

Net income from risk provisioning -10 4 4 -17 -5 -14 -1 1 -10 -39 -49

General and administrative expenses -199 -44 -44 -48 -57 -193 -46 -47 -48 -61 -202

Expenses from bank levies and similar dues -28 -21 -1 -1 -2 -25 -21 -1 -1 -1 -24

Net income from write-downs and write-ups on non-

financial assets -14 -3 -4 -4 -4 -15 -4 -4 -5 -5 -18

Net income from restructuring 2 - - - --9 -9 1 1 1 - 3

Pre-tax profit 204 48 74 49 44 215 48 69 70 29 216

Income taxes -22 -9 -14 -10 -3 -36 -8 -10 -14 -5 -37

Net income 182 39 60 39 41 179 40 59 56 24 179

Key ratios (%) 2017 Q1/18 Q2/18 Q3/18 Q4/18 2018 Q1/19 Q2/19 Q3/19 Q4/19 2019

CIR1 47.0 42.0 40.3 43.7 50.4 44.2 42.0 42.9 39.8 48.9 43.5

RoE before tax 7.3 6.7 9.5 6.3 5.5 7.1 6.0 9.0 9.2 3.4 6.9

RoE after tax 6.5 5.4 7.6 4.9 5.1 5.9 4.9 7.6 7.3 2.7 5.7

Balance sheet (€ bn) 12/17 03/18 06/18 09/18 12/18 12/18 03/19 06/19 09/19 12/19 12/19

Total assets 58.0 57.6 57.8 57.3 57.8 57.8 60.3 60.1 59.8 56.8 56.8

Equity 2.9 3.0 3.2 3.2 3.3 3.3 3.3 3.2 3.2 3.2 3.2

Financing volume 45.7 46.3 45.9 45.7 46.4 46.4 47.1 46.4 46.3 45.5 45.5

Regulatory capital ratios2 12/17 03/18 06/18 09/18 12/18 12/18 03/19 06/19 09/19 12/19 12/19

RWA (€ bn) 14.5 14.2 13.7 13.5 14.6 14.6 14.3 13.6 14.3 17.7 17.7

CET 1 ratio – phase in (%) 17.6 18.84 19.45 19.75 18.53 18.53 18.86 19.47 18.37 15.28 15.28

Personnel 12/17 03/18 06/18 09/18 12/18 12/18 03/19 06/19 09/19 12/19 12/19

Employees (FTE) 744 733 747 747 750 750 743 746 750 752 752

Note: annual results 2017, 2018 and 2019 audited, interim results unaudited (Q1/Q3 2018 and 2019), interim results Q2 2018 and 2019 reviewed 1 CIR = (GAE + net income from write-downs and write-ups on non-financial assets)/operating income 2 Basel III transition rules 3 Incl. full-year result, post dividend 2018 4 Post dividend for 2017, incl. interim result Q1/18, post max. calc. dividend acc. to ECB methodology 5 Incl. interim result Q1/18, post max. calc. dividend acc. to ECB methodology 6 Excl. interim result, post dividend 2018 7 Excl. interim result 8 Incl. full-year result, post proposed dividend 2019

Investor Update based on annual results 2019 (IFRS, pbb Group, audited), March 2020 14

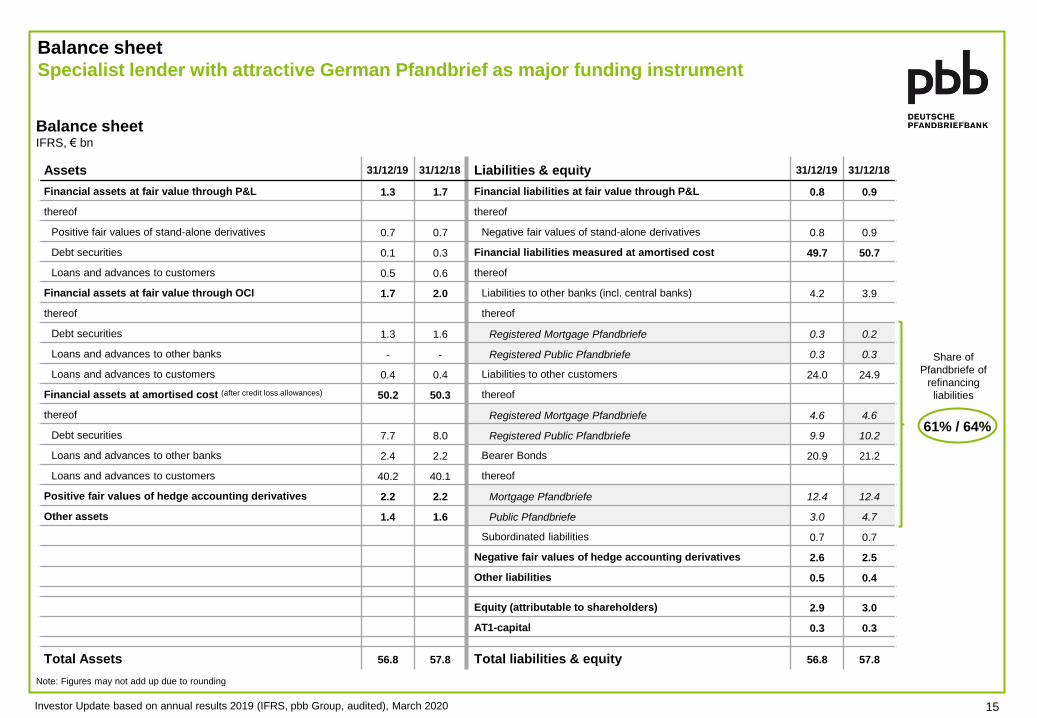

Balance sheet

Specialist lender with attractive German Pfandbrief as major funding instrument

Balance sheet IFRS, € bn

Note: Figures may not add up due to rounding

Assets 31/12/19 31/12/18 Liabilities & equity 31/12/19 31/12/18

Financial assets at fair value through P&L 1.3 1.7 Financial liabilities at fair value through P&L 0.8 0.9

thereof thereof

Positive fair values of stand-alone derivatives 0.7 0.7 Negative fair values of stand-alone derivatives 0.8 0.9

Debt securities 0.1 0.3 Financial liabilities measured at amortised cost 49.7 50.7

Loans and advances to customers 0.5 0.6 thereof

Financial assets at fair value through OCI 1.7 2.0 Liabilities to other banks (incl. central banks) 4.2 3.9

thereof thereof

Debt securities 1.3 1.6 Registered Mortgage Pfandbriefe 0.3 0.2

Loans and advances to other banks - - Registered Public Pfandbriefe 0.3 0.3

Loans and advances to customers 0.4 0.4 Liabilities to other customers 24.0 24.9

Financial assets at amortised cost (after credit loss allowances) 50.2 50.3 thereof

thereof Registered Mortgage Pfandbriefe 4.6 4.6

Debt securities 7.7 8.0 Registered Public Pfandbriefe 9.9 10.2

Loans and advances to other banks 2.4 2.2 Bearer Bonds 20.9 21.2

Loans and advances to customers 40.2 40.1 thereof

Positive fair values of hedge accounting derivatives 2.2 2.2 Mortgage Pfandbriefe 12.4 12.4

Other assets 1.4 1.6 Public Pfandbriefe 3.0 4.7

Subordinated liabilities 0.7 0.7

Negative fair values of hedge accounting derivatives 2.6 2.5

Other liabilities 0.5 0.4

Equity (attributable to shareholders) 2.9 3.0

AT1-capital 0.3 0.3

Total Assets 56.8 57.8 Total liabilities & equity 56.8 57.8

61% / 64%

Share of

Pfandbriefe of

refinancing

liabilities

Investor Update based on annual results 2019 (IFRS, pbb Group, audited), March 2020 15

Markets

Low interest rate environment continues to support and prolong CRE cycle – slowing

economic growth and individual market risks require even more cautious approach

1 Source: Property Market Analysis

European and US CRE investment volumes remain on

solid levels

Investment volumes recovered in Q2 and Q3 after a

weak Q1, which was driven by slowing economic

growth, high prices, challenges in sourcing suitable

properties, interest rate increases in the US and

(geo)political uncertainties

Commercial real estate investments in Europe

reached € 65 bn in Q3/19, 1.5% above Q3/18 and

above 10-year average

Solid take up levels, office vacancy remains on

low level

But: yields for prime office properties at historical

lows in most core markets which increases

valuation risks; yields on UK retail properties

already increasing with significant valuation

discounts to follow

US CRE transaction volume reached $ 157 bn in Q3,

slightly below y-o-y number – limited room for further

growth

Slowing economic growth and individual market risks

(e.g. Brexit, retail sector, co-working space, corona virus,

etc.) urge continued higher caution – pbb remains highly

selective, especially on

UK (in most property types)

Retail (structural change/online business)

temporarily also hotel

European CRE Investment volume

(€ bn)

Retail prime yields

in %

Development retail rents

2010 = 100

Office prime yields

in %

Office vacancy

in %

Development office rents

2010 = 100

0

50

100

150

200

250

300

0

30

60

90

2006Q1

2007Q1

2008Q1

2009Q1

2010Q1

2011Q1

2012Q1

2013Q1

2014Q1

2015Q1

2016Q1

2017Q1

2018Q1

2019Q1

Quarter total (LHS) 12 month rolling total (RHS)

2019

Q3

0

5

10

15

20

25

2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Paris: Central Frankfurt London: Central

2,5

3,5

4,5

5,5

6,5

7,5

2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Paris: Central Frankfurt London: Central

2,0

3,0

4,0

5,0

6,0

7,0

2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Paris Berlin London

70

80

90

100

110

120

130

140

2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Paris: Central Frankfurt London: Central

60

80

100

120

140

160

2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Paris Berlin London

Investor Update based on annual results 2019 (IFRS, pbb Group, audited), March 2020 16

REF Portfolio

Shift in composition

Regions

31/12/2019 / Total: € 29.8 bn1

Note: Figures may not add up due to rounding 1 EaD, Basel III 2 prior to the Brexit referendum in 2016

31/12/2013 / Total: € 22.2 bn1

54%

16%

9%

8%

6%

UK

Germany CEE

Nordics

France

Other 6%

Investor Update based on annual results 2019 (IFRS, pbb Group, audited), March 2020 17

31/12/20152 / Total: € 25.8 bn1

47%

19%

12%

9%

7%

Germany France

UK

CEE

Nordics Other 5%

33%

29%

16%

10%

Office

Residential

Retail

Logistics/

Storage 4%

4%

Hotel Other 4%

Mixed use

50%

12%

11%

9%

Nordics

Germany

Other 8%

UK

France

CEE

USA

3% 6%

46%

19%

16%

10% 2%

Office

Retail

Residential

5% Logistics/

Storage

Hotel

Mixed use Other 3%

31%

28%

22%

8% Office

Retail

2%

Mixed use

5%

Residential

Hotel

Logistics/

Storage

Other 5%

Property types

Po

rtfo

lio

(E

aD

, B

asel II

I)

13.8

12/17 12/18 12/19

13.2 12.1

-12%

Note: Figures may not add up due to rounding

New business & segment reporting

VP: Run-down of non-strategic Value Portfolio continued in line with strategy

31/12/19: € 15.6 bn 31/12/19: € 15.6 bn

Regions Borrower classification

38%

27%

12%

6%

France Austria

Poland 1%

Germany

5%

Italy

Spain

Hungary 1%

4%

Other

Europe

6%

Other Rest

of World

60%

28%

7%

FI

Sov.

(incl. related)

Reg. Gov.

(incl. related)

4%

Supra PSE <1%

€ bn

Fin

an

cin

g v

olu

me

Investor Update based on annual results 2019 (IFRS, pbb Group, audited), March 2020 18

Mortgage

Lending Value (Yield 6.2%)

€ 65 mn

Difference

e.g. 35%

19

Pfandbrief refinancing

ISCR and the effect of the Mortgage Lending Value – very simplified example!

Loan

Pfandbrief

issued

€ 33 mn

OC e.g. 15%

Pfandbrief

Collateral

(Coverpool)

€ 39 mn

Borrower’s

Equity

€ 45 mn

Loan (Yield 7.3%)

€ 55 mn

Refinancing

55%

LTV

max.

60%

MV € 100 mn

Valuation

19 Investor Update based on annual results 2019 (IFRS, pbb Group, audited), March 2020

minus

€ 1.1 mn interest payment p.a.

for a € 55 mn loan

at 2% interest rate

€ 2.9 mn excess cash

€ 4.0 mn rent

= ~ 360% ISCR

€ 1.1 mn interest

€ 4.0 mn rent p.a. at 4% property yield

results in a market

value of € 100 mn

Interest Service Cover Ratio Loan - to - Value Ratio

20 Investor Update based on annual results 2019 (IFRS, pbb Group, audited), March 2020

Cover Pools

Mortgage Cover Pool

Cover Funds by Region € bn (nominal)

Note: Figures may not add up due to rounding 1 Excl. additional cover assets (substitute collateral) 2 Incl. logistics, hotels, other commercially used buildings as well as building land

Cover Funds By Property Type as of 31/12/2019

Cover Funds By Region as of 31/12/2019

46%

13%

11%

10%

8%

6% 2%

Germany

Switzerland 1%

3% CEE

UK

USA

France

Nordic countries

Benelux

Austria Spain

42%

19%

19%

20%

Office

Retail/Shopping

Residential

Other2

Mortgage cover pool (Nominal) 31/12/2019

Pfandbriefe outstanding € 16.6 bn

Cover funds € 19.7 bn

Over-collateralisation (Nominal / NPV) 18.5% / 20.2%

No. of loans 2,030

No. of properties 3,518

Payments ≥90 days overdue € 0.2 mn

Weighted average LTV (based upon the market value) 34.28% 2.6

Spain France Benelux

Nordic

countries

Austria

0.2

UK Germany USA CEE

2.3

Switzerland

2.0

8.1 8.0

0.6

1.8 1.9 1.3

1.8 1.3 1.2 1.0

0.6 0.4 0.3 0.2 0.2 0.1

30/09/2019 Total: € 18.3 bn1

31/12/2019 Total: € 17.6 bn1

21

Cover Pools

Public Sector Cover Pool

Cover Funds by Region € bn (nominal)

Note: Figures may not add up due to rounding

Cover Funds by Counterparty Type as of 31/12/2019

Cover Funds by Region as of 31/12/2019

39%

26%

22%

Germany

Supra 1% Portugal 1%

Austria

2%

France

Canada 1%

4%

Italy

Spain

UK 1%

Benelux 1%

Japan 1%

Nordic countries 1%

CEE 1%

46%

35%

8%

11%

Central governments

Regional authorities

Local authorities

Other debtors

Public sector cover pool (Nominal) 31/12/2019

Pfandbriefe outstanding € 10.8 bn

Cover funds € 14.3 bn

Over-collateralisation (Nominal / NPV) 32.7% / 29.7%

No. of loans / bonds 586

Payments ≥90 days overdue -

Investor Update based on annual results 2019 (IFRS, pbb Group, audited), March 2020

0.1

Austria Germany France

0.2

5.1

Japan Benelux

0.1

Spain Italy

0.6

Portugal Nordic

countries

Supra UK CEE Canada

0.1

5.5

0.1

4.0

0.1

3.7

3.0 3.1

0.5 0.3 0.3 0.3

0.1 0.2 0.2 0.2 0.2 0.1 0.1 0.1 0.2

30/09/2019 / Total: € 14.2 bn

31/12/2019 / Total: € 14.3 bn

Mandated Ratings

Bank ratings S&P

Long-term A-

Outlook/Trend Negative

Short-term A-2

Stand-alone rating1 bbb

Long Term Debt Ratings

“Preferred” senior unsecured Debt2 A-

“Non-preferred” senior unsecured Debt3 BBB-

Subordinated Debt BB+

Pfandbrief ratings Moody’s

Public Sector Pfandbrief Aa1

Mortgage Pfandbrief Aa1

Disclaimer:

The rating information published in this presentation and on our web site are a service for our investors. The information does not necessarily represent the opinion of Deutsche Pfandbriefbank AG.

Ratings should not serve as a substitute for individual analysis. The information provided should not be seen as a recommendation to buy, hold or sell securities. Deutsche Pfandbriefbank AG does not

assume any liability, including for the completeness, timeliness, accuracy and selection of such information, or for any potential damages which may occur in connection with this information.

The rating agencies may alter or withdraw their ratings at any time. The rating of an individual security issued by Deutsche Pfandbriefbank AG may differ from the ratings shown above or an individual

security might not be rated at all. For the evaluation and usage of the rating information (including the rating reports), please refer to the respective rating agencies’ pertinent criteria and explanations,

terms of use, copyrights and disclaimers, which are to be considered.

Note: The above list does not include all ratings 1 Stand-alone credit profile 2 "Senior Unsecured Debt" 3 "Senior Subordinated Debt"

Investor Update based on annual results 2019 (IFRS, pbb Group, audited), March 2020 22