Nedelcu & Cojocaru Gafica asistata de calculator prin AutoCAD Preview.pdf

Dear Student/Visitor

Don’t be fooled by ultra-low prices on the tax course offered by competitors. Our school doesn’t simply give you printed IRS publications to study, we pro-vide you with a complete and comprehensive study material written for serious tax students. You will gain comprehensive practice, using real scenarios, as you complete the quizzes along the course. Remember that you can email the instructor any question you may have during your study period. After completing the course, we will provide you with all of the information needed to register as a tax preparer in the State of California; we will also guide you through the CTEC application process. If you have any questions, please call our office at (818) 453-0674 or email us at [email protected] Feel free to browse the following course pages, it will give you a taste of the 60hr comprehensive self-study course.

Act Now! Become a Tax Preparer and earn extra income!

I Copyright©A&BOffice,IncomeTaxSchool-2010–AllRightsReserved

Federal Introduction 1GettingandStayingOrganized 3Itemizeddeductions 4Settinguparecordkeepingsystem 5AdditionalStudyMaterial6BigPicture 13

Chapter 1: General Material 14WhatIsaTaxPreparerandWhatIsHisRole 14WhoShouldFileaReturn15FilingRequirementsforMostTaxpayers 15DependentFilingRequirements 17WhichFormShouldbeUsed 18WhenTaxesMustbeFiled 21WheretoFile 21HowtoFile 21SocialSecurityNumber(SSN) 22MarriedFilingJoint,iftaxpayersonDecember31: 24MarriedFilingSeparately,ifonDecember31: 24HeadofHousehold,iftaxpayeronDecember31: 25QualifyingWidow(er)WithDependentChild,iftaxpayer:25PaidPreparer’sSignature 31

Chapter 2: Standard Deduction and Exemp-tions 35StandardDeduction 34StandardDeductionAmount 35Decedent’sfinalreturn 36HigherStandardDeductionforAge(65orOlder) 37HigherStandardDeductionforBlindness 37Spouse65orOlderorBlind 37HigherStandardDeductionforSalesTaxesOnNewMotorVehicles 37HigherStandardDeductionforNetDisasterLoss 37Exemptions 40DependentExemptions 40JointReturnTest41CitizenorResidentTest 42RelationshipTest42AgeTest 42ResidencyTest 43SupportTest(ToBeaQualifyingChild) 45SpecialTestforQualifyingChildofMoreThanOnePerson 45GrossIncomeTest 51TotalSupport 52Decedents 54Survivors 55TaxWithholding 56Tips 58TaxableFringeBenefits 58SickPay 58PensionsandAnnuities 58GamblingWinnings 58

UnemploymentCompensation 59FederalPayments 59BackupWithholding 60EstimatedTax 60WhentoPayEstimatedTaxes 61ReturnAssemblyandProcessing 61

Chapter 3: Income 64GrossIncome 64WagesandOtherCompensation 64IncomeofaChild 65ScholarshipandFellowships 65EmployerProvidedEducationalAssistanceProgram 65SickPay 66EmployerPaidDisabilityInsurancePremiums 66EmployerProvidedMealsandLodging 67CafeteriaPlans 67EmployerProvidedGroupTermLifeInsurance 67FringeBenefits 67Tips 69Interest 71Dividends 71CapitalGainsandLosses 71StateTaxRefunds 71Alimony 72ChildSupport 73BusinessIncome 73IncomefromRents,Royalties,Partnerships,Estates,andTrust 73UnemploymentCompensation 74Clergy 74CommunityPropertyIssues 75Bartering 76

Chapter 4: Interest and Dividend Income 81InterestIncome 81ConstructiveReceipt 81Form1099-INT 82Taxable/Nontaxable 84DividendsThatAreInterest 84GiftsforOpeningAccounts 84TreasuryBills 85SavingsBonds 85EducationSavingsBondProgram 86OriginalIssueDiscount 86Tax-ExemptInterest 87MunicipalBonds 87DividendIncome 87OrdinaryDividends 89HoldingPeriod 90MutualFunds 91ReturnofCapital 91InterviewingClients 92CommonInterviewMistakes 92CommonPreparationMistakes 93

Contents

1Copyright©A&BOffice,IncomeTaxSchool-2011–AllRightsReserved

IntroductionWelcometo A & B Office Income Tax Training School’s 60hrcoursetobecomeataxpreparer!

Wehavebeenteachingandhelpingstudentslikeyoulearntheincometaxbasicsandbecometaxprofessionalsforover18years.Asyouprobablyknow,Congressandpoliticalcandidatesengageinnever-endingdiscussionsaboutwaystotinkerwiththenation’staxlaws.Whereappropriatethroughoutthecourse,wehighlighthowanyresultingchangesintaxlawwillaffecttaxpreparersandyourclients.Thiscourseisupdatedannuallysincenewtaxformsmustbefiledeveryyearandeveryyeartaxlawschange.

Mostpeoplefindtaxestobeapain.Firstofall,everyonefacesthechoreofgatheringvariouscomplicated-lookingdocumentstocompletetheannualritualoffillingoutIRSForm1040(andwhateverformCaliforniamayrequire).Knowthatyoumayneedtobecomeacquaintedwithsomenewforms.Perhapsyouneedtofigureouthowtosubmitaquarterlytaxpaymentwhenyounolongerworkforacompanyandnowreceiveself-employmentincomefromindependentcontractwork.Maybeyousoldsomeinvestments(suchasstocks,mutualfunds,orrealestate)ataprofit(orloss),andyoumustcalculatehowmuchtaxyouowe;orhowmuchlosscanbewrittenoff.

A brief history of U.S. Income taxes.Federalincometaxeshaven’talwaysbeenacertainty.Intheearly20thcentury,peoplelivedwithoutbeingbotheredbythefederalincometax-orbytelevisions,microwaves,computers,voicemail,andallthoseothercomplications.Beginningin1913,Congresssetupasystemofgraduatedtaxrates,startingwitharateofonlyonepercentandgoinguptosevenpercent.Thistaxsystemwasenactedthroughthe16thAmendmenttotheConstitution,whichwassuggestedbyPresidentTeddyRoosevelt(aRepublican),andpushedthroughbyhissuccessor,PresidentWilliamH.Taft(anotherRepublican),andultimatelyratifiedbytwo-thirdsofthestates.Notethatwe,yourgoodauthors,areindependents,whichmeansthatwehappilytakeswipesatRepublicans,Democrats,andotherpoliticalpundits.

Infairness,wemusttellyouthatthe1913federalincometaxwasn’tthefirstU.S.incometax.PresidentAbrahamLincoln(Republican)signedaCivilWarincometaxin1861,whichwasabandonedadecadelater.Priorto1913,thevastmajorityoftaxdollarscollectedbythefederalgovernmentcamefromtaxesleviedongoods,suchasliquor,tobacco,andimports.Today,personalincometaxes,includingSocialSecuritytaxes,accountforabout.85percentoffederalgovernmentrevenue.In1913,theforms,instructions,andclarificationsfortheentirefederaltaxsystemwouldhavefilledjustonesmall,three-ringbinder!Thosewere,indeed,thegoodolddays.Sincethen,thankstoendlessrevisions,enhancements,andsimplifications,thefederaltaxlaws-alongwiththeIRSandcourtclarificationsofthoselaws-canfillseveraldumptrucks.SinceWorldWarII,thesizeofthefederaltaxcodehasswelledbymorethan400percent!And,accordingtotheTaxFoundation-anonprofit,nonpartisanpolicyresearchorganization-complyingwiththetaxlawscostseveryonemorethan$265billionannually.

FIGURING Out the U.S. Tax System:You’llpaymoreintaxesthanyouneedtoifyoudon’tunderstandthetaxsystem.Unfortunately,whenyoutrytoreadandmakesenseofthetaxlaws,youquicklyrealizethatyou’remorelikelytowinthelotterythanfigureoutsomepartsofthetaxcode!That’soneofthereasonsthattaxattorneysandaccountantsarepaidsomuch-tocompensatethemfortheirintenseandprolongedagonyofdecipheringthetaxcode!

Buthere’salittlesecrettomakeyoufeelmuchbetter:Youdon’tneedtoreadthedreadfultaxlaws.Mosttaxadvisorsdon’treadthelawthemselves.Instead,theyrelyuponsummariespreparedbyorganizationsandpeoplewhohaveaknackforexplainingthingsclearlyandmoreconciselythantheIRS. Ourcoursehelpsyoudiscoverhowthetaxsystemworksandhowtolegallymakethesystemworkforyou.

You will learn to reduce taxes.Thetaxsystemisbuiltaroundincentivestoencouragedesirablebehaviorandactivity.Homeownership,forexample,isconsideredgoodbecauseitencouragespeopletotakemoreresponsibilityformaintainingpropertiesandneighborhoods.Therefore,thegovernmentoffersallsortsoftaxbenefits(allowable deductions) toencouragepeopletoownhomes.Butifyoudon’tunderstandthesetaxbenefits,youprobablydon’tknowhowtotakefulladvantageofthem,either.Evenwhenyou’reanhonest,earnest,well-intentioned,andlaw-abidingcitizen,oddsarethatyoudon’tcompletelyunderstandthetaxsystem.

Sodon’tfeelinadequatewhenitcomestounderstandingthetaxsystem.You’renottheproblem-thecomplexityoftheincometaxsystemis.That’swhythroughoutthiscoursewehelpyouunderstandthebasicsofthetaxsystem.

14 Copyright©A&BOffice,IncomeTaxSchool-2011–AllRightsReserved

Chapter 1: General MaterialLearning Objective: In this chapter the student will learn to determine who should file a return, what filing status the taxpayer should use, and what forms to use. The student will also learn when returns are due, how to apply for an extension of time to file, and what form to use when filing an application for extension. Accounting periods and methods will be studied.

What Is a Tax Preparer and What Is His RoleAtaxpayermayfindthatthemostefficientandcosteffectivemannerinwhichtocomplywithfilingatimelyandaccuratetaxreturnistoemploytheservicesofaprofessionaltaxpreparer.Becausethetaxpayerisstillrespon-siblefortheaccuracyofhistaxreturn,heshouldbesurehehaschosenaneducatedprofessionaltoassisthim.Ataxpayershouldalsorememberthefollowing:

“Anyonemaysoarrangehisaffairsthathistaxesshallbeaslowaspossible;heisnotboundtochoosethatpat-ternwhichwillbestpaythetreasury;thereisnotevenapatrioticdutytoincreaseone’staxes.”

ThisquoteisfromtheinfluentialU.S.CourtofAppealsjudgeandnotedjudicialphilosopher,LearnedHand,whoisexpressinghisviewsonourdutyastaxpayerstopayour“fairandlegitimate”shareoftaxes.Aprofessionalpre-parermostlikelywillshareU.S.CourtofAppealsJudgeLearnedHand’sviews.

a) Goal:toattainleastlegitimatetax(minimizetax) b) Worksforthetaxpayer,nottheIRS(donotaudit).(TheTaxReliefActof1997doesrequirethat preparersofreturnswithEarnedIncomeCreditexercise“duediligence”inpreparingEarnedIn- comeCredit(EIC)returns.SeeChapter5forfurtherexplanation.)However,taxpayersmaybe audited,inwhichcase,theywillberequiredtosubstantiateentriesontheirtaxreturns. c) Interprets"gray"areastotheadvantageofthetaxpayer,nottheIRS d) Isassertiveandasksthetaxpayermanyquestionssothatnoincomeordeductionsandcreditsare overlooked e) Maintainstaxpayer'sinformationincompleteconfidence f) Meetsrequirementsforcompetenceandprofessionalstanding: -Awarenessofalltaxlawsaffectingindividuals -Abilitytoresearchandinterpretthetaxlaws -Athoroughandefficientinterviewtechnique -Genuinerespectandconcernforthetaxpayer g) Ifataxpayerpreparesareturnthatisnotinaccordancewiththetaxlaworasksapreparerto prepareareturnthatisnotproper,theprofessionalpreparershouldtellthetaxpayerthecorrect waytoreporttheitemandadvisehimtocomplywiththetaxlawsandregulations.Thepreparer isundernoobligationtoreportthetaxpayertoeithertheIRSortheState.However,thepre- parerisexpectedtotellthetruthifaskedbyarepresentativeofeitherthefederalorstategovern- ment. h) Thetaxpreparershouldneverprepareareturnincorrectlymerelybecausethetaxpayerinsistson it. i) Preparersshouldalwaysbealerttofraud.Ifaclientisvaguewithanswerstoquestionsorpro- videsanswersthataresuspicious,thetaxpreparershouldbeassertiveandaskadditional questions.Ifthepreparerisnotcomfortablepreparingareturnforthetaxpayer,heshouldexplain hispositiontothetaxpayerandrefusetopreparethereturn.

Apreparerissubjecttoa$1,000(or,ifgreater,50%oftheincomederivedwithrespecttotheincome)fineperreturnforanunderstatementoftaxpayer’sliabilityduetoanunrealisticposition.Understatementduetopreparer’swillfulorrecklessconductorintentionaldisregardofrulesispunishablebyafineof$5,000(or,ifgreater,50%oftheincomederivedwithrespecttotheincome)perreturn.

11Copyright©A&BOffice,IncomeTaxSchool-2011–AllRightsReserved

Form 1040 (The Long Form - 77 lines)BecauseForms1040Aand1040EZareeasiertocompletethanForm1040,youshoulduseoneofthemunlessForm1040allowsyoutopaylesstax.Butifyoudon’tqualifyforfilingForm1040Aor1040EZ,youmustuseForm1040.Thisformistheonethateverybodylovestohate.Ifyouitemizeyourdeductions,claimahostoftaxcredits,ownrentalproperty,areself-employed,orsellastockorbond,you’restuck-welcometotheworldofthe1040. IfyouthinktheonlyfactorthatmightpreventyoufromusingaForm1040Aisthatyou’vealwaysitemizedyourdeductionsinthepast,doScheduleA,ItemizedDeductions,first.It’sareasonablyeasyformtocomplete,andifyourdeductionsdon’tadduptoyourstandarddeduction,you’reoffthe1040hook.Ifyou’redepressedbecauseyouhavetousethesimplerformslastyearand,youwanttobeabletodeductmoreandhavemorefavorableadjustmentstoyourincomeinthefuture,allisnotlost.Ataminimum,youcanmakethingsbetterfor2011byplanningahead.

Form

1040A 2010U.S. Individual Income Tax ReturnDepartment of the Treasury—Internal Revenue Service

OMB No. 1545-0074

IRS Use Only—Do not write or staple in this space. (99)

Name, Address, and SSN See separate instructions.

P R I N T

C L E A R L Y

Your first name and initial Last name

Your social security number

If a joint return, spouse’s first name and initial Last name Spouse’s social security number

Home address (number and street). If you have a P.O. box, see instructions. Apt. no.▲ Make sure the SSN(s) above

and on line 6c are correct.

City, town or post office, state, and ZIP code. If you have a foreign address, see instructions. Checking a box below will not change your tax or refund.Presidential

Election Campaign ▶ Check here if you, or your spouse if filing jointly, want $3 to go to this fund . . . . . . ▶ You Spouse

Filing status Check only one box.

1 Single2 Married filing jointly (even if only one had income)3 Married filing separately. Enter spouse’s SSN above and

full name here. ▶

4 Head of household (with qualifying person). (See instructions.)If the qualifying person is a child but not your dependent, enter this child’s name here. ▶

5 Qualifying widow(er) with dependent child (see instructions)

Exemptions 6a Yourself. If someone can claim you as a dependent, do not check box 6a.

b Spousec Dependents:

(1) First name Last name

(2) Dependent’s social security number

(3) Dependent’s relationship to you

(4) ✓ if child under age 17 qualifying for child tax credit (see

page 16)If more than six dependents, see instructions.

} Boxes checked on 6a and 6bNo. of children on 6c who: • lived with you

• did not live with you due to divorce or separation (see instructions)

Dependents on 6c not entered above

d Total number of exemptions claimed.

Add numbers on lines above ▶

Income Attach Form(s) W-2 here. Also attach Form(s) 1099-R if tax was withheld. If you did not get a W-2, see page 20. Enclose, but do not attach, any payment. Also, please use Form 1040-V.

7 Wages, salaries, tips, etc. Attach Form(s) W-2. 7

8a Taxable interest. Attach Schedule B if required. 8ab Tax-exempt interest. Do not include on line 8a. 8b

9a Ordinary dividends. Attach Schedule B if required. 9ab Qualified dividends (see instructions). 9b

10 Capital gain distributions (see instructions). 1011a IRA

distributions. 11a11b Taxable amount

(see instructions). 11b12a Pensions and

annuities. 12a12b Taxable amount

(see instructions). 12b

13 Unemployment compensation and Alaska Permanent Fund dividends. 1314a Social security

benefits. 14a14b Taxable amount

(see instructions). 14b

15 Add lines 7 through 14b (far right column). This is your total income. ▶ 15Adjusted gross income

16 Educator expenses (see instructions). 1617 IRA deduction (see instructions). 1718 Student loan interest deduction (see instructions). 18

19 Tuition and fees. Attach Form 8917. 1920 Add lines 16 through 19. These are your total adjustments. 20

21 Subtract line 20 from line 15. This is your adjusted gross income. ▶ 21For Disclosure, Privacy Act, and Paperwork Reduction Act Notice, see separate instructions. Cat. No. 11327A Form 1040A (2010)

13Copyright©A&BOffice,IncomeTaxSchool-2011–AllRightsReserved

Big Picture Nowthatyouunderstandforms1040,1040Aand1040EZ,itremainsnecessarytofirstsimplifyourfederalincometaxstructuresothatyoucanseewhereeachtransactionfitsinthebigpicture.Movingforwardyouwillknowinadvancewherethetransactionbelongs.Forexample,willtheactionincreasetheincome,reducethetax,orincreasetherefundand/orpayment?Inotherwords,weencourageyoutocarefullystudyeachtaxsituationinordertostimulateyourmindandskills-you’llbebetterpreparedtohandlespecialissueswhentheyarise.

Income Fromallsources.wages,interest,dividends,alimony received,businessincome,capitalgains,IRAdistributions, pensions,rentalincome,socialsecuritybenefits,otherincome,etc. (lines7through21). XXX

Less Adjusted to Income Educatorexpenses,movingexpenses,onehalf ofself-employmenttax,Alimony,IRAcontribution, studentinterestloan,tuitionandfees,penaltyonearly withdrawalofsavingsandothers(lines23through36). (XXX)

Adjusted Gross Income (AGI) (1) XXX

Tax and Credits: Less:StandardorItemizeddeductions(line40) (XXX) Less:Exemptionforeachperson(line42) (XXX) Taxable Income XXX Tax(line44) XXX Plus:AlternativeMinimumTax(line45) XXX Plus;Othertaxes.Self-employment,unreportedsocialsecurity, additionaltaxonIRA’s,others(lines56through59) XXX

Less:Childanddependentcare(2),educationcredits,child taxcredit,plusothers(lines47through53) (XXX) Less:Payments: Withheldfromemployers,makingworkpay(3) estimatedpay- ments,earnedincomecredit(EIC),additionalchildtaxcredit(2), americanopportunitycredit,first-timehomebuyer,excess socialsecurity,andothers(lines61through71) (XXX)

Refund or Amount you Owe XXX

(1)Thisisanimportantline.Youwillneeditfrequently(forreference)whenpreparingoranalyzingtaxreturns.(2)Noticethatchildanddependentcarecreditshaveadoubleeffectonareturn.Onewhenreducingthe tax,andtheotherisarefundtothetaxpayer.(3)Youwillfrequentlynoticethatthisisarefundablecredit.TheMakingWorkPaytaxcredit,normallyamaximumof $400forworkingindividualsand$800forworkingmarriedcouples,isreducedbytheamountofanyEconomic RecoveryPayment($250pereligiblerecipientofSocialSecurity).

131Copyright©A&BOffice,IncomeTaxSchool-2011–AllRightsReserved

Chapter 6: Child Care and Others Credits

Learning Objective: Students will explore Child Tax Credit, Child Care Credit, Credit for the Elderly and Dis-abled, the Additional Child Tax Credit, Education Credits and the requirements for qualification. Form 2441, Child and Dependent Care Expenses, Schedules 2, 3, Form 8863, Education Credits, and Form 1040 Schedule R, Credit for the Elderly or Disabled, will be mastered. Form 8812, Additional Child Tax Credit, will be examined.

Child Tax Credit

Thechildtaxcreditisanonrefundablecredit.Mosttaxpayerswhohavechildrenunderage17areeligibleforthechildtaxcredit.Theamountofcreditis$1,000perqualifyingchild.Ifthetaxpayerwasunabletoclaimthefullchildtaxcredit,hemaybeeligibleforanadditionalchildtaxcredit(discussedlater).Thechildtaxcreditislimitedbythetaxpayer’staxliabilityandmodifiedAGI.

Qualifying Child Forpurposesofthechildtaxcredit,aqualifyingchildis—

1. Underage17attheendof2010 2. AcitizenorresidentoftheUnitedStates 3. Didnotprovideoverhalfofhisownsupportfor2010 4. Livedwiththetaxpayerformorethanhalfof2010 5. Hasoneofthefollowingrelationshipstothetaxpayer: • Sonordaughter • Stepsonorstepdaughter • Adoptedchild* • Brotherorsister • Stepbrotherorstepsister • Anydescendantofanyoftheabove(forexample,grandchild**),or • Eligiblefosterchild

Note:*Anadoptedchildplacedwiththetaxpayerbyanauthorizedplacementagencyforlegaladoptionisanadoptedchildeveniftheadoptionisnotfinal.

**Agrandchildisconsideredtobeanydescendentofthetaxpayer’sson,daughter,oradoptedchildandincludesgreat-grandchildren,greatgreat-grandchildren,etc.

Form 1040 (2010) Page 2

Tax and Credits

38 Amount from line 37 (adjusted gross income) . . . . . . . . . . . . . . 38

39a Check if:

{ You were born before January 2, 1946, Blind.

Spouse was born before January 2, 1946, Blind.} Total boxes

checked ▶ 39a

b If your spouse itemizes on a separate return or you were a dual-status alien, check here ▶ 39b

40 Itemized deductions (from Schedule A) or your standard deduction (see instructions) . . 40

41 Subtract line 40 from line 38 . . . . . . . . . . . . . . . . . . . 41

42 Exemptions. Multiply $3,650 by the number on line 6d . . . . . . . . . . . . 42

43 Taxable income. Subtract line 42 from line 41. If line 42 is more than line 41, enter -0- . . 43

44 Tax (see instructions). Check if any tax is from: a Form(s) 8814 b Form 4972 . 44

45 Alternative minimum tax (see instructions). Attach Form 6251 . . . . . . . . . 45

46 Add lines 44 and 45 . . . . . . . . . . . . . . . . . . . . . ▶ 46

47 Foreign tax credit. Attach Form 1116 if required . . . . 47

48 Credit for child and dependent care expenses. Attach Form 2441 48

49 Education credits from Form 8863, line 23 . . . . . 49

50 Retirement savings contributions credit. Attach Form 8880 50

51 Child tax credit (see instructions) . . . . . . . . 51

52 Residential energy credits. Attach Form 5695 . . . . 52

53 Other credits from Form: a 3800 b 8801 c 53

54 Add lines 47 through 53. These are your total credits . . . . . . . . . . . . 5455 Subtract line 54 from line 46. If line 54 is more than line 46, enter -0- . . . . . . ▶ 55

Other Taxes

56 Self-employment tax. Attach Schedule SE . . . . . . . . . . . . . . . 56

57 Unreported social security and Medicare tax from Form: a 4137 b 8919 . . 57

58 Additional tax on IRAs, other qualified retirement plans, etc. Attach Form 5329 if required . . 58

59 a Form(s) W-2, box 9 b Schedule H c Form 5405, line 16 . . . . 59

60 Add lines 55 through 59. This is your total tax . . . . . . . . . . . . . ▶ 60

Payments 61 Federal income tax withheld from Forms W-2 and 1099 . . 61

62 2010 estimated tax payments and amount applied from 2009 return 62

63 Making work pay credit. Attach Schedule M . . . . . . . 63 If you have a qualifying child, attach Schedule EIC.

64a Earned income credit (EIC) . . . . . . . . . . 64a

b Nontaxable combat pay election 64b

65 Additional child tax credit. Attach Form 8812 . . . . . . 65

66 American opportunity credit from Form 8863, line 14 . . . 66

67 First-time homebuyer credit from Form 5405, line 10 . . . 67

68 Amount paid with request for extension to file . . . . . 68

69 Excess social security and tier 1 RRTA tax withheld . . . . 69

70 Credit for federal tax on fuels. Attach Form 4136 . . . . 70

71 Credits from Form: a 2439 b 8839 c 8801 d 8885 71 72 Add lines 61, 62, 63, 64a, and 65 through 71. These are your total payments . . . . ▶ 72

73 If line 72 is more than line 60, subtract line 60 from line 72. This is the amount you overpaid 73Refund 74a Amount of line 73 you want refunded to you. If Form 8888 is attached, check here . ▶ 74a

Direct deposit? See instructions.

▶

▶

b Routing number ▶ c Type: Checking Savings

d Account number

75 Amount of line 73 you want applied to your 2011 estimated tax ▶ 75 Amount You Owe

76 Amount you owe. Subtract line 72 from line 60. For details on how to pay, see instructions ▶ ▶76

77 Estimated tax penalty (see instructions) . . . . . . . 77

Third Party Designee

Do you want to allow another person to discuss this return with the IRS (see instructions)? Yes. Complete below. No

Designee’s name ▶

Phone no. ▶

Personal identification number (PIN) ▶

Sign Here Joint return? See page 12. Keep a copy for your records.

Under penalties of perjury, I declare that I have examined this return and accompanying schedules and statements, and to the best of my knowledge and belief, they are true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge.

Your signature Date Your occupation Daytime phone number

Spouse’s signature. If a joint return, both must sign.

▲

Date Spouse’s occupation

Paid Preparer Use Only

Print/Type preparer’s name Preparer’s signature Date Check if self-employed

PTIN

Firm’s name ▶ Firm's EIN ▶

Firm’s address ▶ Phone no.

Form 1040 (2010)

138 Copyright©A&BOffice,IncomeTaxSchool-2011–AllRightsReserved

Child and Dependent Care (Form 2441 With 1040; Schedule 2 with 1040A)

Anonrefundablecreditofupto35%oftheexpensesincurredforthecareofaqualifieddependentisallowedwhentheexpendituresareworkrelated.Thepercentageofcreditgoesdownasincomegoesupwith20%ofeligibleexpensesasthesmallestamountallowed.Expensesarelimitedto$3,000foroneand$6,000fortwoormorequalifieddependents.

Forexample,ifataxpayerandhisspouseeachmade$50,000andtheypaid$3,600forchildcareforonechild,theywouldbealloweda$600credit.

Taxpayer’sincome $50,000 Spouse’sincome $50,000 Total $100,000

Incomesover$43,000arelimitedtoa20%deduction.Ofthe$3,600thatwasspentonchildcare,themaximumonwhichthecreditisfiguredis$3,000,so $3,000 x.20 $600

Inordertoclaimthecredit,allthefollowingtestsmustbemet: • Onajointreturn,bothparentsMUSThaveearnedincome.(SeeRulesforStudent- SpouseorSpouseDisabledinthePub.17,Chapter32.) • Careprovider’sSSNoremployeridentificationnumber(EIN),aswellasthenameand address,mustbeprovided. • CaremustbeforoneormorequalifiedpersonswhosenameandSocialSecurityNumber mustappearontheForm2441,ChildandDependentCareExpenses,orSchedule2, ChildandDependentCareExpensesforForm1040AFilers. • Taxpayer(andspouseifmarried)mustpaymorethanhalfthecosttokeepupahomein whichheandthequalifiedpersonlived. • Expensesmustbeincurredsothatthetaxpayercouldworkorlookforwork.Ifmarried, spousemustalsobeworkingorlookingforwork.Expensesforovernightcamportrans- portationcannotbeusedtofigurethecredit. • FilingstatusgenerallycannotbeMarriedFilingSeparate(seeJointReturnTestlater).If thecouplelivedapartthelastsixmonthsoftheyearthenonecouldfileasHeadof

Form 2441Department of the Treasury Internal Revenue Service (99)

Child and Dependent Care Expenses

▶ Attach to Form 1040, Form 1040A, or Form 1040NR.

▶ See separate instructions.

1040A . . . . . . . . . . 1040

2441

◀. . . . . . . . . .

1040NR

OMB No. 1545-0074

2010Attachment Sequence No. 21

Name(s) shown on return Your social security number

Part I Persons or Organizations Who Provided the Care—You must complete this part. (If you have more than two care providers, see the instructions.)

1 (a) Care provider’s name

(b) Address (number, street, apt. no., city, state, and ZIP code)

(c) Identifying number (SSN or EIN)

(d) Amount paid (see instructions)

Did you receive dependent care benefits?

No ▶ Complete only Part II below.

Yes ▶ Complete Part III on the back next.Caution. If the care was provided in your home, you may owe employment taxes. If you do, you cannot file Form 1040A. For details, see the instructions for Form 1040, line 59, or Form 1040NR, line 58.

Part II Credit for Child and Dependent Care Expenses2 Information about your qualifying person(s). If you have more than two qualifying persons, see the instructions.

(a) Qualifying person’s name

First Last

(b) Qualifying person’s social security number

(c) Qualified expenses you incurred and paid in 2010 for the

person listed in column (a)

3 Add the amounts in column (c) of line 2. Do not enter more than $3,000 for one qualifying person or $6,000 for two or more persons. If you completed Part III, enter the amount from line 31 . . . . . . . . . . . . . . . . . . . . . . . . . . 3

4 Enter your earned income. See instructions . . . . . . . . . . . . . . . 4 5 If married filing jointly, enter your spouse’s earned income (if your spouse was a student

or was disabled, see the instructions); all others, enter the amount from line 4 . . . . 5 6 Enter the smallest of line 3, 4, or 5 . . . . . . . . . . . . . . . . . . 6 7 Enter the amount from Form 1040, line 38; Form

1040A, line 22; or Form 1040NR, line 37. . . . . 7 8 Enter on line 8 the decimal amount shown below that applies to the amount on line 7

If line 7 is:

OverBut not over

Decimal amount is

$0—15,000 .35

15,000—17,000 .34

17,000—19,000 .33

19,000—21,000 .32

21,000—23,000 .31

23,000—25,000 .30

25,000—27,000 .29

27,000—29,000 .28

If line 7 is:

OverBut not over

Decimal amount is

$29,000—31,000 .27

31,000—33,000 .26

33,000—35,000 .25

35,000—37,000 .24

37,000—39,000 .23

39,000—41,000 .22

41,000—43,000 .21

43,000—No limit .20

8 X .

9 Multiply line 6 by the decimal amount on line 8. If you paid 2009 expenses in 2010, see the instructions . . . . . . . . . . . . . . . . . . . . . . . . . 9

10 Tax liability limit. Enter the amount from the Credit Limit Worksheet in the instructions. . . . . . . 10

11 Credit for child and dependent care expenses. Enter the smaller of line 9 or line 10 here and on Form 1040, line 48; Form 1040A, line 29; or Form 1040NR, line 46 . . . . 11

For Paperwork Reduction Act Notice, see your tax return instructions. Cat. No. 11862M Form 2441 (2010)

286 Copyright©A&BOffice,IncomeTaxSchool-2011–AllRightsReserved

Chapter 15: Self-Employment Income Learning Objective: This chapter examines self-employment income. Sole proprietorships, statutory employees, Form 1040 Schedule C, Profit or Loss from Business, C-EZ, SE, Self-Employment Tax, and Form 8829, Expenses for Business Use of Your Home are emphasized. We will also examine the health insurance deduction taken as an adjustment to income as well as other deductions that may be partially deductible on Schedule C and partially deductible on Schedule A, Itemized Deductions.

Sole Proprietor Asthenamestates,asoleproprietorissomeonewhoownsanunincorporatedbusinessbyhimself.However,ifyouarethesolememberofadomesticlimitedliabilitycompany(LLC),youarenotasoleproprietorifyouelecttotreattheLLCasacorporation.AsoleproprietorreportstheincomeandexpensesfromhisbusinessonaScheduleC,ProfitorLossfromaBusiness.Oneisself-employedifhe— • Conductsatradeorbusinessasasoleproprietor. • Isanindependentcontractor. • Isinbusinessforhimselfinanyotherway.

Self-employmentcanincludeworkinadditiontoregularfull-timebusinessactivities.Italsoincludescertainpart-timeworkdoneathomeorinadditiontoaregularjob.

Husband and Wife Businesses Itispossibleforeitherthehusbandorthewifetobetheownerofthesoleproprietorbusiness.Whenonlyonespouseistheowner,theotherspousecanworkinthebusinessasanemployee.

Inthepastahusbandandwifecouldnotbesoleproprietorsofthesamebusiness.Iftheywerejointowners,theywerepartnersandwouldhavetofileapartnershipreturn,Form1065,U.S. Partnership Return of Income.

WiththeSmallBusinessandWorkOpportunityTaxActof2007,amarriedcouplewhofilesajointtaxreturncanelecttoconducttheirbusinessactivitiesasaqualifiedjointventure(atradeorbusinessentityinwhichthehus-bandandwifemateriallyparticipateinsuchventure).Thespousesmustdividetheitemsofincome,gain,loss,deduction,creditandexpensesinaccordancewiththeirrespectiveinterestsinsuchventure.AseparateScheduleCmustbepreparedforeachandbothincludedinthejointreturn.ThisiseffectivefortaxyearsbeginningafterDecember31,2006.Seethe1040ScheduleCinstructionsformoredetailedinformation.

Independent Contractor Onewhoownsabusinessisanindependentcontractor.Thisstatusentitleshimtocertainfavorabletaxbenefits(andfullresponsibilityforemploymenttaxes).Theindependentcontractorcanitemizeallhisbusinessexpenses,

SCHEDULE C (Form 1040)

Department of the Treasury Internal Revenue Service (99)

Profit or Loss From Business (Sole Proprietorship)

▶ Partnerships, joint ventures, etc., generally must file Form 1065 or 1065-B. ▶ Attach to Form 1040, 1040NR, or 1041. ▶ See Instructions for Schedule C (Form 1040).

OMB No. 1545-0074

2010Attachment Sequence No. 09

Name of proprietor Social security number (SSN)

A Principal business or profession, including product or service (see instructions) B Enter code from pages C-9, 10, & 11

▶

C Business name. If no separate business name, leave blank. D Employer ID number (EIN), if any

E Business address (including suite or room no.) ▶

City, town or post office, state, and ZIP code

F Accounting method: (1) Cash (2) Accrual (3) Other (specify) ▶

G Did you “materially participate” in the operation of this business during 2010? If “No,” see instructions for limit on losses Yes No

H If you started or acquired this business during 2010, check here . . . . . . . . . . . . . . . . . . . . ▶

Part I Income 1 Gross receipts or sales. Caution. See instructions and check the box if:

• This income was reported to you on Form W-2 and the “Statutory employee” box on that form was checked, or

• You are a member of a qualified joint venture reporting only rental real estate income not subject to self-employment tax. Also see instructions for limit on losses.

} . . ▶

1

2 Returns and allowances . . . . . . . . . . . . . . . . . . . . . . . . . 2

3 Subtract line 2 from line 1 . . . . . . . . . . . . . . . . . . . . . . . . 3

4 Cost of goods sold (from line 42 on page 2) . . . . . . . . . . . . . . . . . . . 4

5 Gross profit. Subtract line 4 from line 3 . . . . . . . . . . . . . . . . . . . . 5

6 Other income, including federal and state gasoline or fuel tax credit or refund (see instructions) . . . . 6 7 Gross income. Add lines 5 and 6 . . . . . . . . . . . . . . . . . . . . . ▶ 7

Part II Expenses. Enter expenses for business use of your home only on line 30. 8 Advertising . . . . . 8

9 Car and truck expenses (see instructions) . . . . . 9

10 Commissions and fees . 10

11 Contract labor (see instructions) 11

12 Depletion . . . . . 12

13 Depreciation and section 179 expense deduction (not included in Part III) (see instructions) . . . . . 13

14 Employee benefit programs (other than on line 19) . . 14

15 Insurance (other than health) 15

16 Interest:

a Mortgage (paid to banks, etc.) 16a

b Other . . . . . . 16b

17 Legal and professional services . . . . . . 17

18 Office expense . . . . . . 18

19 Pension and profit-sharing plans . 19

20 Rent or lease (see instructions):

a Vehicles, machinery, and equipment 20a

b Other business property . . . 20b

21 Repairs and maintenance . . . 21

22 Supplies (not included in Part III) . 22

23 Taxes and licenses . . . . . 23

24 Travel, meals, and entertainment:

a Travel . . . . . . . . . 24a

b Deductible meals and entertainment (see instructions) . 24b

25 Utilities . . . . . . . . 25

26 Wages (less employment credits) . 26

27 Other expenses (from line 48 on page 2) . . . . . . . . 27

28 Total expenses before expenses for business use of home. Add lines 8 through 27 . . . . . . ▶ 28

29 Tentative profit or (loss). Subtract line 28 from line 7 . . . . . . . . . . . . . . . . . 29

30 Expenses for business use of your home. Attach Form 8829 . . . . . . . . . . . . . . 30

31 Net profit or (loss). Subtract line 30 from line 29.

• If a profit, enter on both Form 1040, line 12, and Schedule SE, line 2, or on Form 1040NR, line 13 (if you checked the box on line 1, see instructions). Estates and trusts, enter on Form 1041, line 3.

• If a loss, you must go to line 32.} 31

32 If you have a loss, check the box that describes your investment in this activity (see instructions).

• If you checked 32a, enter the loss on both Form 1040, line 12, and Schedule SE, line 2, or on Form 1040NR, line 13 (if you checked the box on line 1, see the line 31 instructions). Estates and trusts, enter on Form 1041, line 3.

• If you checked 32b, you must attach Form 6198. Your loss may be limited.

} 32a All investment is at risk.

32b Some investment is not at risk.

For Paperwork Reduction Act Notice, see your tax return instructions. Cat. No. 11334P Schedule C (Form 1040) 2010

347Copyright©A&BOffice,IncomeTaxSchool-2011–AllRightsReserved

Chapter 19: Ethics and Responsibilities Of Tax Professionals

Learning Objectives: Describe an ethical environment. Identify the paid preparer’s responsibilities. Discuss requirements to maintain confidentiality. List matters connected with the practice before the Internal Revenue Service. Identify specifics related to Circular 230. Discuss the AICPA Statements on Standards for Tax Services.

Thiscourseisdesignedtohelpthetaxprofessionalunderstandtherulesandregulationsgoverningthetaxprofes-sionandthepracticalapplicationoftheserulesinthedailyoperationoftheirbusinesses.Thecoursealsoillus-tratesthecompliancerequirementsofTreasuryDepartmentCircular230asitappliestoEnrolledAgents,CPAsandAttorneysintheirpracticebeforetheInternalRevenueService(IRS);AICPAStatementsonStandardsforTaxServices;andtheIRSrequirementsconcerningduediligence,confidentialityofclientinformation,andprofes-sionalconduct.

Ethics,asdefinedinFunk&WagnallsStandardCollegeDictionary,are“theprinciplesofrightconduct,especial-lywithreferencetoaspecificprofession.”TheAmericanHeritageDictionarydefinesethicsas“Therulesorstan-dardsgoverningtheconductofthemembersofaprofession.”Mostpeoplewoulddefineethicsas“doingtherightthing,”whichleadsonetobelievethatindividualswillasamatterofcommonsenseandconscienceinstinctivelyreactinanethicalmannerinallsituations.AsevidencedbythefinancialscandalsatEnron,Tyco,WorldCom,AdelphiaandArthurAndersenthisisnotalwaystrue.“Doingtherightthing”wasnotthebasisforthedecisionsmadebytheleadersoftheseorganizations.Thepublichasbecomegenerallydisillusionedanduntrustingofthebusinesscommunity.

Professionalorganizations,businessschools,andregulatoryagencieshavereactedtothisdeclineinthepublictrustbyreviewingtheirCodesofConductandincreasingtheeducationalrequirementsoftheirmembersand/orstudents.TheTreasuryDepartmenthasrecentlyrevisedCircular230torequireallAttorneys,CertifiedPublicAc-countants,EnrolledAgentsandEnrolledActuariestoannuallycomplete16hoursofcontinuingeducationinclud-ing2hoursofethicsorprofessionalconduct.Traditionaltrainingprogramshaveconcentratedoncompliancewiththelaws,regulations,andpoliciesoftheorganizationandthusmanypeoplehavebasedtheirdecisionsonthelegalityoftheissuesratherthanthemorality.Justbeinglegaldoesnotmakeitright!

SupremeCourtJusticePotterStewartdefinedethicsas“knowingthedifferencebetweenwhatyouhavearighttodo,andwhatistherightthingtodo.”Recognizing“therightthingtodo”andactuallydoingitinareallife,practicalsituationarenotnecessarilythesamething.ArieReshefsaidthat“Businessethicsistheapplicationandadaptationofethicalconsiderationstothedecisionsofbusinessorganizations.”Itisnownecessaryfororganiza-tionstoadopttrainingprogramsandstandardsofconductthatclearlyestablishacompleteunderstandingoftheprinciples,values,andethicalbehaviorsexpectedfromtheirmembers.

How Can You Develop an Ethical Environment? Communicationisthekeytorealizingconsistentapplicationoftheorganization’sethicalrulesandstandards.Members,students,employees,andmanagersmustrealizethatethicalbehaviorisexpected,willberewarded,andistheresponsibilityofeveryoneintheorganization.

OrganizationscancommunicatetheseexpectationsthroughformaldocumentssuchasaCodeofEthics,StandardsofConduct,ethicstrainingcourses,oreventhecorporateMissionStatement.However,unlesstheprescribedbehaviorsaredemonstratedintheday-to-dayactionsoftheindividuals(fromthePresidenttothemaintenancestaff)thewrittenidealsandvalueswillnottranslatetoautomaticbehaviors.Inhisbook,MakingEthicalDeci-sions,MichaelJosephsonstates“Trustworthiness.Respect.Responsibility.Fairness.Caring.Citizenship.TheSixPillarsofCharacterareethicalvaluestoguideourchoices.Thestandardsofconductthatariseoutofthosevaluesconstitutethegroundrulesofethics,andthereforeofethicaldecision-making.”Guidelinessuchasthese

1Copyright©A&BOffice,IncomeTaxSchool-2011–AllRightsReserved

Chapter 1: Quizzes KarlaWhite(age37,SSN245-45-5778)andherdaughter,Nancy(age9,SSN245-98¬7412)livedwith Karla’smotherallyear.Usingthefollowinginformation,determineifKarlapaidmorethanhalfofthe costofmaintainingahome. Expenses paid by Karla Expenses paid by Karla’s mother Electric $2149 MortgageInterestExpense $3202 Water 480 PropertyTaxes 798 Repairs 1500 Food 600 Food 2600 PropertyInsurance 280 Telephone 576

1. AnswerthefollowingquestionbasedontheCostofMaintainingaHouseholdWorksheetyou completedforKarlaWhite:WhatisthetotalamountpaidbytheTaxpayer?

a)$4,880 c)$12,185 b)$7,305 d)$7,405

2.AnswerthefollowingquestionbasedontheCostofMaintainingaHouseholdWorksheetyou completedforKarlaWhite:WhatisthetotalamountpaidbyOthers?

a)$12,185 c)$0 b)$4,880 d)$12,035

3.AnswerthefollowingquestionbasedontheCostofMaintainingaHouseholdWorksheetyou completedforKarlaWhite:WhatisthetotalcostfortheTaxpayerandOthers? a)$12,185 c)$4,880 b)$7,305 d)$7,300

Cost of Maintaining a Household

ExpensesPaid AmountTaxPayerPaid AmountPaidByOthers TotalCostPropertyTaxesMortgageInterestExpenseRentUtilityChargesUpkeep&RepairsPropertyInsuranceFoodConsumedonPremisesOtherHouseholdExpensesTotalsMinusTotalAmountPaidbyTaxPayerAmountPaidbyOthers

Note:Ifthetotalamountpaidbythetaxpayerismorethantheamountallotherpaidthenthetaxpayermeetstherequirementsofpay-ingmorethanhalfthecostofkeepingupthehome.

Copyright © A & B Office, Income Tax School - 2011 – All Rights Reserved 21

Chapter 4: Quizzes

1. Which of the following are taxable (use an X to identify taxable items)?

2. Complete a Federal Return for James and Ileana Galeano James (age 50, DOB: 4/15/60, SSN 334-55-4455) and Ileana (age 44, DOB: 3/25/66, SSN 355-55-4444). The Galeano’s are married and lived together for the whole tax year. They have one child, Ana, who is 18 years old, DOB: 6/23/92. Ana’s SSN is 400-11-0001. They all live at 100 Alberta St., Your City, Your State – Your Zip. Neither James nor Ileana wishes to designate $3 of their taxes for the Presidential Election Campaign Fund. They did not receive any Recovery payment in 2010 (Schedule M).

James is a manager for an auto repair shop.

Ileana is a homemaker. They rent their house.

James and Ileana have a savings account. Also, they received dividends during the year. Complete the correct income tax return for the Galeanos.

Item Taxable NontaxableOrdinary dividends paid by Exxon. (Over $1,500)Municipal Bond Interest ( Over $1,500)Ordinary Dividends paid by Do-minion Resources (Over $1,500)Interest paid by New Haven Savings Bank (Over $1,500)Interest paid by Wachovia (In-terest of less than $1,500)

CORRECTED (if checked)Payer’s RTN (optional)PAYER’S name, street address, city, state, ZIP code, and telephone no. OMB No. 1545-0112

Interest Income

PAYER’S federal identification number RECIPIENT’S identification number

RECIPIENT’S name

Street address (including apt. no.)

City, state, and ZIP code

Account number (see instructions)

$Department of the Treasury - Internal Revenue ServiceForm 1099-INT

Copy BFor Recipient

This is important taxinformation and is

being furnished to theInternal Revenue

Service. If you arerequired to file a return,a negligence penalty orother sanction may beimposed on you if thisincome is taxable and

the IRS determines thatit has not been

reported.

(keep for your records)

Form 1099-INTInterest on U.S. Savings Bonds and Treas. obligations3

$Federal income tax withheld Investment expenses54

$$Foreign tax paid6

$Specified private activitybond interest

9Tax-exempt interest8

Foreign country or U.S.possession

7

$

Early withdrawal penalty2

$

Interest income1

$ 09Prudential Insurance Co. of AmericaPO Box 1228Your City, Your State-Your ZIP

439.82

13-5554444 334-55-4455

James and Ileana Galeano

100 Alberta St.

Your City, Your State-Your ZIP

11 12

(keep for your records)

Nonemployee compensation

CORRECTED (if checked)OMB No. 1545-0115Rents1PAYER’S name, street address, city, state, ZIP code, and telephone no.

$2 Royalties

$Other income3

RECIPIENT’S identificationnumber

PAYER’S federal identificationnumber

5 Fishing boat proceeds 6 Medical and health care payments

$ $RECIPIENT’S name Substitute payments in lieu of

dividends or interest87

$$9Street address (including apt. no.) 10 Crop insurance proceeds

City, state, and ZIP code

Gross proceeds paid toan attorney

14Excess golden parachutepayments

13Account number (see instructions)

$16 State tax withheld 17 State/Payer’s state no.

$Department of the Treasury - Internal Revenue Service

18 State income

$

$$ $

4

$ $

Payer made direct sales of$5,000 or more of consumerproducts to a buyer(recipient) for resale �

Form 1099-MISC

Form 1099-MISC

MiscellaneousIncome

$

Copy BFor Recipient

This is important taxinformation and isbeing furnished to

the Internal RevenueService. If you are

required to file areturn, a negligence

penalty or othersanction may be

imposed on you ifthis income is

taxable and the IRSdetermines that it

has not beenreported.

Federal income tax withheld

Section 409A income15bSection 409A deferrals15a

$ $

10

Copyright © A & B Office, Income Tax School - 2011 – All Rights Reserved 22

Page 5 of 12 of Form W-2 6 Part 6The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

1

Retirementplan

Third-party sick pay

Statutoryemployee

6

2

Employer’s name, address, and ZIP code

Allocated tips7

Advance EIC payment

8

109

Wages, tips, other compensation Federal income tax withheld

Social security tax withheldSocial security wages

12a11

Employer’s state ID number

43

Employer identification number (EIN)

Medicare wages and tips

Social security tips

13

5

Control number

Employee’s first name and initial Nonqualified plans

Medicare tax withheld

15

14

1716

Other

18

Employee’s address and ZIP code

State income taxState State wages, tips, etc. Locality name

Copy B—To Be Filed With Employee’s FEDERAL Tax Return.This information is being furnished to the Internal Revenue Service.

Department of the Treasury—Internal Revenue Service

Form

Dependent care benefits

See instructions for box 12

b

c

d

e

f

W-2 Wage and TaxStatement 2 00 9

Last nameCode

12bCode

12cCode

19Local wages, tips, etc. 20Local income tax

12dCode

Safe, accurate,FAST! Use

Visit the IRS websiteat www.irs.gov/efile.

Suff.

Employee’s social security numbera

OMB No. 1545-0008334-55-4455

53-0320351 37591.19 4638.65

Ray's Body & Engine Repair2002 Sunny Dr.Your City, Your State-Your Zip

37591.19 2330.65

37591.19 545.07

0000000

James Galeano

100 Alberta St

Your City, Your State-Your Zip SDI $ 413.50

YS 415415238 37591.19 1879.55

a Employee’s social security number

OMB No. 1545-0008

Safe, accurate, FAST! Use

Visit the IRS website at www.irs.gov/efile

b Employer identification number (EIN)

c Employer’s name, address, and ZIP code

d Control number

e Employee’s first name and initial Last name Suff.

f Employee’s address and ZIP code

1 Wages, tips, other compensation 2 Federal income tax withheld

3 Social security wages 4 Social security tax withheld

5 Medicare wages and tips 6 Medicare tax withheld

7 Social security tips 8 Allocated tips

9 Advance EIC payment 10 Dependent care benefits

11 Nonqualified plans 12a See instructions for box 12Co d e

12bCo d e

12cCo d e

12dCo d e

13 Statutory employee

Retirement plan

Third-party sick pay

14 Other

15 State Employer’s state ID number 16 State wages, tips, etc. 17 State income tax 18 Local wages, tips, etc. 19 Local income tax 20 Locality name

Form W-2 Wage and Tax Statement 2010

Department of the Treasury—Internal Revenue Service

Copy B—To Be Filed With Employee’s FEDERAL Tax Return. This information is being furnished to the Internal Revenue Service.

CORRECTED (if checked)PAYER’S name, street address, city, state, ZIP code, and telephone no.

RECIPIENT’S identificationnumber

PAYER’S federal identificationnumber

RECIPIENT’S name

Street address (including apt. no.)

City, state, and ZIP code

Account number (see instructions)

Dividends andDistributions

Department of the Treasury - Internal Revenue ServiceForm 1099-DIV (keep for your records)

Copy B

This is importanttax information

and is beingfurnished to the

Internal RevenueService. If youare required tofile a return, a

negligencepenalty or other

sanction may beimposed on youif this income istaxable and theIRS determines

that it has notbeen reported.

For Recipient

Unrecap. Sec. 1250 gain

OMB No. 1545-0110Total ordinary dividends1a

$1b Qualified dividends

$Total capital gain distr.2a

Collectibles (28%) gainSection 1202 gain 2d2c

$3

5 Investment expenses

Noncash liquidationdistributions

9Cash liquidationdistributions

8

$

$

2b

$ $

Nondividend distributions

Form 1099-DIV

$

76

$

Foreign tax paid Foreign country or U.S. possession

$

$4 Federal income tax withheld$

09Merrett Link441 W. Main St.Your City, Your State-Your ZIP

110.00

12-1511443 334-55-4455

James and Ileana Galeano

100 Alberta St

Your City, Your State-Your ZIP 11 12

(keep for your records)

Nonemployee compensation

CORRECTED (if checked)OMB No. 1545-0115Rents1PAYER’S name, street address, city, state, ZIP code, and telephone no.

$2 Royalties

$Other income3

RECIPIENT’S identificationnumber

PAYER’S federal identificationnumber

5 Fishing boat proceeds 6 Medical and health care payments

$ $RECIPIENT’S name Substitute payments in lieu of

dividends or interest87

$$9Street address (including apt. no.) 10 Crop insurance proceeds

City, state, and ZIP code

Gross proceeds paid toan attorney

14Excess golden parachutepayments

13Account number (see instructions)

$16 State tax withheld 17 State/Payer’s state no.

$Department of the Treasury - Internal Revenue Service

18 State income

$

$$ $

4

$ $

Payer made direct sales of$5,000 or more of consumerproducts to a buyer(recipient) for resale �

Form 1099-MISC

Form 1099-MISC

MiscellaneousIncome

$

Copy BFor Recipient

This is important taxinformation and isbeing furnished to

the Internal RevenueService. If you are

required to file areturn, a negligence

penalty or othersanction may be

imposed on you ifthis income is

taxable and the IRSdetermines that it

has not beenreported.

Federal income tax withheld

Section 409A income15bSection 409A deferrals15a

$ $

10

FDIA1312 01/08/11

Department of the Treasury ' Internal Revenue Service

Form 1040A U.S. Individual Income Tax Return (99) 2010 IRS Use Only ' Do not write or staple in this space.

Boxeschecked on6a and 6b . . . . .

No. of childrenon 6c who:

? livedwith you . . . . . .

? did notlive withyou due todivorce orseparation (seeinstructions) . . .

Dependentson 6c notentered above . .

Add numbersGon lines above

6 a Yourself. If someone can claim you as a dependent, do not check box 6a . . . . . . . . . . . . Exemptions

b Spouse . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

c Dependents:

(1) First name Last name

(2) Dependent'ssocial security

number

(3) Dependent'srelationship

to you

(4) bifchild under

age 17qual for

child tax cr(see instrs)

If more than sixdependents,see instructions.

d Total number of exemptions claimed . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Income7 Wages, salaries, tips, etc. Attach Form(s) W-2 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

8 a Taxable interest. Attach Schedule B if required . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8 a

b Tax-exempt interest. Do not include on line 8a . . . . . . . . . . . . . . . . . . . . . . 8 b

9 a Ordinary dividends. Attach Schedule B if required . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9 a

Attach Form(s)W-2 here. Alsoattach Form(s)1099-R if taxwas withheld. b Qualified dividends (see instructions) . . . . . . . . . . . . . . . . . . . . . . . 9 b

10 Capital gain distributions (see instructions) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

11 a IRA distributions . . . . . . . . . . . . . . . 11 a 11 b Taxable amount . . . . . . 11 b

12 a Pensions and annuities . . . . . . . . 12 a 12 b Taxable amount . . . . . . 12 b

13 Unemployment compensation and Alaska Permanent Fund dividends

(see instructions) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

14 a Social securitybenefits . . . . . . . . . . . . . . . . . . . . . . . 14 a 14 b Taxable amount . . . . . . 14 b

If you did notget a W-2,see instructions.

Enclose, butdo not attach,any payment.Also, pleaseuse Form 1040-V. 15 GAdd lines 7 through 14b (far right column). This is your total income . . . . . . . . . . . . . . . . . . . 15

Your first name and initial Last name OMB No. 1545-0074

Your social security numberName,Address,and SSN

If a joint return, spouse's first name and initial Last name Spouse's social security number

Home address (number and street). If you have a P.O. box, see instructions. Apartment no.See separateinstructions

JMake sure the SSN(s)above and on line 6care correct.

City, town or post office. If you have a foreign address, see instructions. State ZIP code

PresidentialElectionCampaign G

1 Single 4 Head of household (with qualifying person). (See instructions.)Filingstatus 2 Married filing jointly (even if only one had income) If the qualifying person is a child but not your dependent,

3 Married filing separately. Enter spouse's SSN above and Genter this child's name here

Gfull name here 5 Qualifying widow(er) with dependent childCheck onlyone box. (see instructions)

GCheck here if you, or your spouse if filing jointly, want $3 to go to this fund (see instructions) . . . . You Spouse

16 Educator expenses (see instructions) . . . . . . . . . . . . . . . . . . . . . . . 16

17 IRA deduction (see instructions) . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

18 Student loan interest deduction (see instructions) . . . . . . . . . . . . 18

19 Tuition and fees. Attach Form 8917 . . . . . . . . . . . . . . . . . . . . . . . . 19

Adjustedgrossincome

20 Add lines 16 through 19. These are your total adjustments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

21 GSubtract line 20 from line 15. This is your adjusted gross income . . . . . . . . . . . . . . . . . . . . . 21

BAA For Disclosure, Privacy Act, and Paperwork Reduction Act Notice, see separate instructions. Form 1040A (2010)

Checking a box below willnot change your

tax or refund

JAMES GALEANO 334-55-4455

ILEANA GALEANO 355-55-4444

5210 ALBERTA ST

LOS ANGELES CA 90060

X

X

X2

1

3

37,591.440.

110.

38,141.

38,141.

ANA GALEANO 400-11-0001 Daughter

Form 1040A (2010) Page 2

22 Enter the amount from line 21 (adjusted gross income) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

23 a Check You were born before January 2, 1946, Blind

if: Spouse was born before January 2, 1946, BlindTotal boxes

Gchecked . 23a

Tax, credits,andpayments

b If you are married filing separately and your spouse itemizes deductions,Gsee instructions and check here . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23b

24 Enter your standard deduction (see instructions) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

25 Subtract line 24 from line 22. If line 24 is more than line 22, enter -0- . . . . . . . . . . . . . . . . . . . . 25

26 Exemptions. Multiply $3,650 by the number on line 6d . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

27 Subtract line 26 from line 25. If line 26 is more than line 25, enter -0-. This is yourGtaxable income . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

28 Tax, including any alternative minimum tax

(see instructions) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

29 Credit for child and dependent care expenses. Attach Form 2441 . . . . . . . . . . 29

30 Credit for the elderly or the disabled. Attach Schedule R . . . . . 30

31 Education credits from Form 8863, line 23 . . . . . . . . . . . . . . . . . . 31

32 Retirement savings contributions credit. Attach Form 8880 . . . 32

33 Child tax credit (see instructions) . . . . . . . . . . . . . . . . . . . . . . . . . . 33

34 Add lines 29 through 33. These are your total credits . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34

35 Subtract line 34 from line 28. If line 34 is more than line 28, enter -0- . . . . . . . . . . . . . . . . . . . . 35

36 Advance earned income credit payments from Form(s) W-2, box 9 . . . . . . . . . . . . . . . . . . . . . . . 36

37 GAdd lines 35 and 36. This is your total tax . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37

38 Federal income tax withheld from Forms W-2 and 1099 . . . . . . 38

2010 estimated tax payments and amount applied from39

2009 return . 39

40 Making work pay credit. Attach Schedule M . . . . . . . . . . . . . . . . . 40

41 a Earned income credit (EIC) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41 a

bNontaxable combat pay election. 41b

42 Additional child tax credit. Attach Form 8812 . . . . . . . . . . . . . . . . 42

43 American opportunity credit from Form 8863, line 14 . . . . . . . . . 43

44 GAdd lines 38, 39, 40, 41a, 42, and 43. These are your total payments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44

45 If line 44 is more than line 37, subtract line 37 from line 44.This is the amount you overpaid . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45Refund

46 a GAmount of line 45 you want refunded to you. If Form 8888 is attached, check here . . 46 a

G bRoutingnumber . . . . . . . . . . G c Type: Checking Savings

Direct deposit?See instructionsand fill in 46b,46c, and 46d orForm 8888.

G dAccountnumber . . . . . . . . . .

47 Amount of line 45 you want applied to your 2011estimated tax . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47

Amountyou owe

48 Amount you owe. Subtract line 44 from line 37. For details on how to pay,Gsee instructions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48

49 Estimated tax penalty (see instructions) . . . . . . . . . . . . . . . . . . . . 49

Do you want to allow another person to discuss this return with the IRS (see instructions)? . . . . . . . . . . Yes. Complete the following. NoThird partydesignee

Designee'sname G

Phoneno. G

Personalidentificationnumber (PIN) G

If you havea qualifyingchild, attachSchedule EIC.

Signhere

Under penalties of perjury, I declare that I have examined this return and accompanying schedules and statements, and to the best of my knowledge and belief, theyare true, correct, and accurately list all amounts and sources of income I received during the tax year. Declaration of preparer (other than the taxpayer) is based on allinformation of which the preparer has any knowledge.

Your signature Date Your occupation Daytime phone number

Joint return?See instructions.

Spouse's signature. If a joint return, both must sign. Date Spouse's occupationKeep a copyfor your records.

A

Print/Type preparer's name Preparer's signature Date Check G if PTIN

self-employed

Firm's name G

Paidprepareruse only

Firm's addressG Firm's EIN G

Phone no.

Form 1040A (2010)

FDIA1312 01/08/11

JAMES & ILEANA GALEANO 334-55-445538,141.

11,400.26,741.10,950.

15,791.

1,578.

1,578.

1,578.4,639.

800.387.

5,826.

4,248.4,248.

XXXXXXXXX

XXXXXXXXXXXXXXXXX

X

MANAGER AUTO SHOP (071) 457-8988

HOMEMAKER

Income Tax StudentX

2609 OLIVE ST

HUNTINGTON PARK CA 90255

Qualifying Child Information Child 1 Child 2 Child 3

1 Child's name First name Last name First name Last name First name Last name

If you have more than three qualifyingchildren, you only have to list three to getthe maximum credit . . . . . . . . . . . . . . . . . . . . . . . . .

2 Child's SSN

The child must have an SSN as defined in theinstructions for Form 1040A, lines 41a and41b, or Form 1040, lines 64a and 64b, unlessthe child was born and died in 2010. If yourchild was born and died in 2010 and did nothave an SSN, enter 'Died' on this line andattach a copy of the child's birth certificate,death certificate, or hospital medical records. . .

3 Child's year of birth Year Year Year

If born after 1991 AND the child wasyounger than you (or your spouse, iffiling jointly), skip lines 4a and 4b; goto line 5.

If born after 1991 AND the child wasyounger than you (or your spouse, iffiling jointly), skip lines 4a and 4b; goto line 5.

If born after 1991 AND the child wasyounger than you (or your spouse, iffiling jointly), skip lines 4a and 4b; goto line 5.

4 a Was the child under age 24 at the end of2010, a student, and younger than you (oryour spouse, if filing jointly)? . . . . . . . . . . . . . . . . . Yes. No. Yes. No. Yes. No.

Go to line 5. Continue. Go to line 5. Continue. Go to line 5. Continue.

bWas the child permanently and totallydisabled during any part of 2010? . . . . . . . . . . . . . Yes. No. Yes. No. Yes. No.

Continue. The childis not aqualifying child.

Continue. The childis not aqualifying child.

Continue. The childis not aqualifying child.

5 Child's relationship to you

(for example, son, daughter, grandchild,niece, nephew, foster child, etc) . . . . . . . . . . . . . .

6 Number of months child lived with you in theUnited States during 2010

? If the child lived with you for more thanhalf of 2010 but less than 7 months,enter '7'.

? If the child was born or died in 2010 andyour home was the child's home for theentire time he or she was alive during2010, enter '12' . . . . . . . . . . . . . . . . . . . . . . . . . . months months months

Do not enter more than12 months.

Do not enter more than12 months.

Do not enter more than12 months.

FDIA7401 11/04/10

SCHEDULE EIC OMB No. 1545-0074

(Form 1040A or 1040)

Earned Income CreditQualifying Child Information 2010

Department of the TreasuryInternal Revenue Service (99)

Complete and attach to Form 1040A or 1040only if you have a qualifying child.

AttachmentSequence No. 43

Name(s) shown on return Your social security number

Before you begin: ? See the instructions for Form 1040A, lines 41a and 41b, or Form 1040, lines 64a and64b, to make sure that (a) you can take the EIC and (b) you have a qualifying child.

? Be sure the child's name on line 1 and social security number (SSN) on line 2 agree with the child's socialsecurity card. Otherwise, at the time we process your return, we may reduce or disallow your EIC. If the name orSSN on the child's social security card is not correct, call the Social Security Administration at 1-800-772-1213.

? If you take the EIC even though you are not eligible, you may not be allowed to take the credit for up to 10 years. See theinstructions for details.CAUTION!

? It will take us longer to process your return and issue your refund if you do not fill in all lines that apply for each qualifying child.

BAA For Paperwork Reduction Act Notice, see your tax return instructions. Schedule EIC (Form 1040A or 1040) 2010

JAMES & ILEANA GALEANO 334-55-4455

ANA GALEANO

400-11-00011992

Daughter

12

SCHEDULE M OMB No. 1545-0074

(Form 1040A or 1040) Making Work Pay Credit 2010Department of the TreasuryInternal Revenue Service (99)

G Attach to Form 1040A or 1040. G See separate instructions. AttachmentSequence No. 166

Name(s) shown on return Your social security number

Important: Check the 'No' box on line 1a and see the instructions if:

(a) You have a net loss from a business,

(b) You received a taxable scholarship or fellowship grant not reported on a Form W-2,

(c) Your wages include pay for work performed while an inmate in a penal institution,

(d) You received a pension or annuity from a nonqualified deferred compensation plan or a nongovernmentalsection 457 plan, or

(e) You are filing Form 2555 or 2555-EZ.

7 Is the amount on line 5 more than the amount on line 6?

No. Skip line 8. Enter the amount from line 4 on line 9 below.

Yes. Subtract line 6 from line 5 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

8 Multiply line 7 by 2% (.02) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

9 Subtract line 8 from line 4. If zero or less, enter -0- . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

10 Did you (or your spouse, if filing jointly) receive an economic recovery payment in 2010? You may havereceived this payment in 2010 if you did not receive an economic recovery payment in 2009 but you receivedsocial security benefits, supplemental security income, railroad retirement benefits, or veterans disabilitycompensation or pension benefits in November 2008, December 2008, or January 2009 (see instructions).

No. Enter -0- on line 10 and go to line 11.

Yes. Enter the total of the payments you (and your spouse, if filing jointly) received in 2010.Do not enter more than $250 ($500 if married filing jointly) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

11 Making work pay credit. Subtract line 10 from line 9. If zero or less, enter -0-. Enter the result here and onForm 1040, line 63; or Form 1040A, line 40 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

*If you are filing Form 2555, 2555-EZ, or 4563 or you are excluding income from Puerto Rico, see instructions.

BAA For Paperwork Reduction Act Notice, see your tax return instructions. Schedule M (Form 1040A or 1040) 2010

FDIA8501 09/20/10

1 a Do you (and your spouse if filing jointly) have 2010 wages of more than $6,451 ($12,903 if married filing jointly)?

Yes. Skip lines 1a through 3. Enter $400 ($800 if married filing jointly) on line 4 and go to line 5.

No. Enter your earned income (see instructions) . . . . . . . . . . . . . . . . . . . . . . . . . . . 1 a

b Nontaxable combat pay included on line 1a(see instructions) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1 b

2 Multiply line 1a by 6.2% (.062) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

3 Enter $400 ($800 if married filing jointly) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

4 Enter the smaller of line 2 or line 3 (unless you checked 'Yes' on line 1a) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

5 Enter the amount from Form 1040, line 38*, or Form 1040A, line 22 . . . . . . . . . . . . . 5

6 Enter $75,000 ($150,000 if married filing jointly) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

Caution: To take the making work pay credit, you must include your social security number (if filing a joint return, the number of either you oryour spouse) on your tax return. A social security number does not include an identification number issued by the IRS. Only theSocial Security Administration issues social security numbers.

Caution: You cannot take the making work pay credit if you can be claimed as someone else's dependent or if you are a nonresident alien.

JAMES & ILEANA GALEANO 334-55-4455

X

800.

38,141.

150,000.

X

800.

X

0.

800.

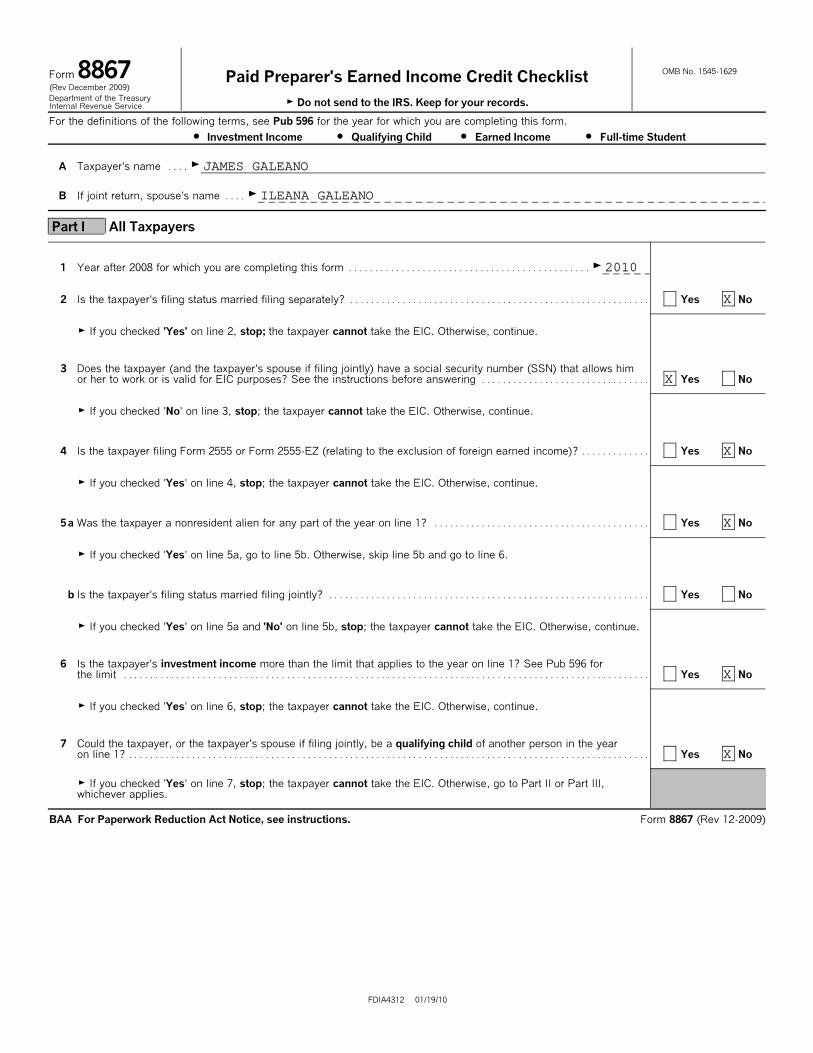

Form 8867(Rev December 2009)

Paid Preparer's Earned Income Credit Checklist OMB No. 1545-1629

Department of the TreasuryInternal Revenue Service G Do not send to the IRS. Keep for your records.

For the definitions of the following terms, see Pub 596 for the year for which you are completing this form.

? Investment Income ? Qualifying Child ? Earned Income ? Full-time Student

A GTaxpayer's name . . . .

B GIf joint return, spouse's name . . . .

Part I All Taxpayers

1 GYear after 2008 for which you are completing this form . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

2 Is the taxpayer's filing status married filing separately? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Yes No

G If you checked 'Yes' on line 2, stop; the taxpayer cannot take the EIC. Otherwise, continue.

3 Does the taxpayer (and the taxpayer's spouse if filing jointly) have a social security number (SSN) that allows himor her to work or is valid for EIC purposes? See the instructions before answering . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Yes No

G If you checked 'No' on line 3, stop; the taxpayer cannot take the EIC. Otherwise, continue.

FDIA4312 01/19/10

6 Is the taxpayer's investment income more than the limit that applies to the year on line 1? See Pub 596 forthe limit . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Yes No

G If you checked 'Yes' on line 6, stop; the taxpayer cannot take the EIC. Otherwise, continue.

7 Could the taxpayer, or the taxpayer's spouse if filing jointly, be a qualifying child of another person in the yearon line 1? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Yes No

G If you checked 'Yes' on line 7, stop; the taxpayer cannot take the EIC. Otherwise, go to Part II or Part III,whichever applies.

4 Is the taxpayer filing Form 2555 or Form 2555-EZ (relating to the exclusion of foreign earned income)? . . . . . . . . . . . . . Yes No

G If you checked 'Yes' on line 4, stop; the taxpayer cannot take the EIC. Otherwise, continue.

5 a Was the taxpayer a nonresident alien for any part of the year on line 1? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Yes No

G If you checked 'Yes' on line 5a, go to line 5b. Otherwise, skip line 5b and go to line 6.

b Is the taxpayer's filing status married filing jointly? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Yes No

G If you checked 'Yes' on line 5a and 'No' on line 5b, stop; the taxpayer cannot take the EIC. Otherwise, continue.

BAA For Paperwork Reduction Act Notice, see instructions. Form 8867 (Rev 12-2009)

JAMES GALEANO

ILEANA GALEANO

2010

X

X

X

X

X

X

Caution. If there is more than one child, complete lines 8 through14 for one child before going to the next column.

8 Child's name . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

9 Is the child the taxpayer's son, daughter, stepchild, foster child,brother, sister, stepbrother, stepsister, or a descendant of anyof them? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Yes No Yes No Yes No

Form 8867 (Rev 12-2009) Page 2

G If you checked 'No' on line 13a, go to line 14. Otherwise, go toline 13b.

b Enter the child's relationship to the other person(s) . . . . . . . . . . . . . . . . .

Yes No Yes No Yes Noc Under the tiebreaker rules, is the child treated as the taxpayer'squalifying child? See the instructions before answering . . . . . . . . . . . . . . Don't know Don't know Don't know

G If you checked 'Yes' on line 13c, go to line 14. If you checked'No,' the taxpayer cannot take the EIC based on this child andcannot take the EIC for taxpayers who do not have a qualifyingchild. If there is more than one child, see the Note at the bottom ofthis page. If you checked 'Don't know,' explain to the taxpayer that,under the tiebreaker rules, the taxpayer's EIC and other tax benefitsmay be disallowed. Then, if the taxpayer wants to take the EICbased on this child, complete lines 14 and 15. If not, and there areno other qualifying children, the taxpayer cannot take the EIC,including the EIC for taxpayers without a qualifying child; do notcomplete Part III. If there is more than one child, see the Note atthe bottom of this page.

Part II Taxpayers With a Child Child 1 Child 2 Child 3

12 Was the child (at the end of the year on line 1) '

?Under age 19 and younger than the taxpayer (or the taxpayer'sspouse if the taxpayer files jointly),

?Under age 24, a full-time student, and younger than the taxpayer(or the taxpayer's spouse if the taxpayer files jointly), or

?Any age and permanently and totally disabled? . . . . . . . . . . . . . . . . . . . Yes No Yes No Yes No

G If you checked 'Yes' on lines 9, 10, 11, and 12, the child is thetaxpayer's qualifying child; go to line 13a. If you checked 'No' online 9, 10, 11, or 12, the child is not the taxpayer's qualifyingchild; see the instructions for line 12.

13 a Could any other person check 'Yes' on lines 9, 10, 11, and 12 forthe child? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Yes No Yes No Yes No

10 Is either of the following true?

??

The child is unmarried, orThe child is married and can be claimed as the taxpayer'sdependent and is not filing a joint return (or is filing it only as aclaim for refund) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Yes No Yes No Yes No

11 Did the child live with the taxpayer in the United States for over halfof the year? See the instructions before answering . . . . . . . . . . . . . . . . . Yes No Yes No Yes No

14 Does the qualifying child have an SSN that allows him or herto work or is valid for EIC purposes? See the instructionsbefore answering . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Yes No Yes No Yes No

G If you checked 'No' on line 14, the taxpayer cannot take the EICbased on this child and cannot take the EIC for taxpayers who donot have a qualifying child. If there is more than one child, see theNote at the bottom of this page. If you checked 'Yes' on line 14,continue.

15 Are the taxpayer's earned income and adjusted gross income eachless than the limit that applies to the taxpayer for the year on line1? See Pub 596 for the limit . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Yes No

G If you checked 'No' on line 15, stop; the taxpayer cannot takethe EIC. If you checked 'Yes' on line 15, the taxpayer can take theEIC. Complete Schedule EIC and attach it tothe taxpayer's return. If there are two or three qualifying childrenwith valid SSNs, list them on Schedule EIC in the same order asthey are listed here. If the taxpayer's EIC was reduced or disallowedfor a year after 1996, see Pub 596 to see if Form 8862 must befiled. Go to line 20.

Note. If you checked 'No' on line 13c or 14 but there is more thanone child, complete lines 8 through 14 for the other child(ren) (butfor no more than three qualifying children). Also do this if youchecked 'Don't know' on line 13c and the taxpayer is not taking theEIC based on this child.

BAA FDIA4312 01/19/10 Form 8867 (Rev 12-2009)

JAMES & ILEANA GALEANO 334-55-4455

ANA

X

X

X

X

X

Daughter

X

X

X