DATATEC GROUP UNAUDITED RESULTS FOR THE SIX MONTHS ENDED 31AUGUST 2004 Jens Montanana CEO.

43

DATATEC GROUP UNAUDITED RESULTS FOR THE SIX MONTHS ENDED 31AUGUST 2004 Jens Montanana CEO

-

Upload

mitchell-white -

Category

Documents

-

view

213 -

download

0

Transcript of DATATEC GROUP UNAUDITED RESULTS FOR THE SIX MONTHS ENDED 31AUGUST 2004 Jens Montanana CEO.

DATATEC GROUP UNAUDITED RESULTS FOR

THE SIX MONTHS ENDED

31AUGUST 2004

Jens MontananaCEO

DATATEC GROUPTrading Environment

• General market conditions have remained stable, greater demand for

IT products and services is evident in the US and Asia-Pac, Europe

remains weak

• Latest results and guidance from the leading manufacturers such as

Cisco, IBM and HP have been mixed, while current performance seems

to be improving, the outlook remains uncertain

• Revenues met or exceeded expectations in all major divisions

• H1performance impacted by Westcon performance in Q2

DATATEC GROUPPerformance Highlights

• Continued strengthening of the balance sheet, cash position and

profitability

• Westcon’s revenues grew over 20%

• Logicalis’ first operating profit in three years

• Doubled size of consulting group with Analysys-Mason merger

• Westcon’s IPO process temporarily suspended due to environment

DATATEC GROUPRevenue

$1.25 B

1H 05

$1.13 B

1H 04 2H 04

$1.22 B

DATATEC GROUPRevenue By Regions

North America53.0%

South America1.2%

Europe36.5%

Asia6.2%

South Africa+ME3.1%

DATATEC GROUPGross Margin

$124.72 M

1H 05

$142.23 M

1H 04 2H 04

$133.19 M

DATATEC GROUPEBITDA

$10.25 M

1H 05

$12.32 M

1H 04 2H 04

$11.47 M

DATATEC GROUPTotal Headline Profit / (Loss) Per Share (Restated)

(6.29)(0.40)

US Cents

1H 04 2H 04 1H 05

0.10

DATATEC GROUPNet Cash

Cash position remains strong

Shows investment into working capital – revenue growth

$97.40 M

1H 05

$99.66 M

1H 04 2H 04

$88.70 M

DATATEC GROUPSegmental Analysis

Revenue

86%2%

12%

Gross Margin

67%

6%

27%

Westcon AMG Logicalis

EBITDA

73%

15%

*12%

* Excludes $1.68 M non trading EBT closure costs

DATATEC GROUPProspects

• Modest growth in corporate IT spend

• Improved operating profits from all subsidiaries

• Volatile tax rate

WESTCON GROUP RESULTS FOR THE

SIX MONTHS ENDED 31 AUGUST 2004

WESTCON GROUP Highlights

• Consolidated revenue grows 21.4% over comparable period

• Revenue increases across all divisions and geographic regions

• Unexpected drop in gross margins to 7.6% from 8.9% (mainly as a

result of Europe)

WESTCON GROUP Highlights

• FOREX losses declined

• SG&A decreased to 6.6% from 6.8%

• Non-recurring exceptional costs of $8 million

WESTCON GROUP Actions Initiated

• New Westcon Group CEO

• Reorganisation and streamlining of senior management

• Rationalisation of warehouse facilities in US and Europe

• Steps taken with key vendors to enhance margins

WESTCON GROUPHistorical Six Month Period Sales – US GAAP

(Includes intercompany revenue relating to non-Westcon group Datatec subsidiaries)

Mar-Aug Sep-Feb Mar-Aug Sep-Feb Mar-Aug Sep-Feb Mar-Aug2002 2003 2004 2005

931756 781 767

969903798

807842 880

1,0041,065

0

100

200

300

400

500

600

700

800

900

1,000

1,100

$

WESTCON GROUPConsolidated Sales by Vendor %

Cisco 51.7% 53.3% 57.0% 57.3%

Nortel 11.6% 10.6% 10.0% 11.3%

Avaya 11.5% 10.3% 8.8% 9.0%

Security 10.6% 11.1% 10.2% 9.0%

IP Devices 14.6% 14.7% 14.0% 13.4%

Total 100.0% 100.0% 100.0% 100.0%

(% of total revenue)

Vendor 2H03 1H04 2H04 1H05

Americas 58% 57% 54% 55%

Europe 37% 37% 40% 38%

Asia Pacific 5% 6% 6% 7%

Total 100% 100% 100% 100%

(% of total revenue)

WESTCON GROUPConsolidated Sales by Geography

Region 2H03 1H04 2H04 1H05

Americas 499 401 432 439

Europe 711 604 509 486

Asia-Pac 118 128 124 129

Consolidated 1,328 1,132 1,065 1,054

WESTCON GROUP Headcount by Region

Region 2H03 1H04 2H04 1H05

WESTCON GROUPConsolidated Results – IFRS – As Reported

Sales $831 $860 $981 $1,044Gross Profit 73 76 86 79

Gross Profit % 8.8% 8.9% 8.8% 7.6%

SG&A 59 58 68 69SG&A % 7.1% 6.8% 6.9% 6.6%

EBITDA 14 18 18 10EBITDA % 1.7% 2.1% 1.9% 1.0%

Dep & Amort 25 11 13 5D&A % 3.0% 1.3% 1.3% 0.5%

Interest Exp, Net 1 1 3 3Int Exp % 0.2% 0.1% 0.4% 0.3%

Pre-tax Income (Loss) (12) 6 2 2Pre-tax % (1.5)% 0.7% 0.2% 0.2%

Note: Excludes Datatec Intercompany transactions

(US $, in millions) 2H03 1H04 2H04 1H05

WESTCON GROUPOperational Improvement Plan

• Plan to improve gross margins and return Europe to profitability by

applying the proven US model to Europe

• The plan will be implemented over the next two quarters and could

cost up to $4 million

(US $, in millions) 2H03 1H04 2H04 1H05

Accounts Receivable $236 $255 $311 $299

DSO (days) 51 54 60 53

Inventory $171 $175 $222 $204

Inventory Turns 9.0x 9.0x 7.8x 9.3x

Accounts Payable $278 $303 $364 $285

DPO (days) 66 70 77 55

Current Ratio 1.5 1.5 1.5 1.5

WESTCON GROUPConsolidated Balance Sheets – Working Capital – US GAAP

Note: DSO, DPO, and inventory turns calculated using trailing twelve month amounts.

(US $, in millions) 2H03 1H04 2H04 1H05

WESTCON GROUPConsolidated Balance Sheets – Capitalization – US GAAP

Cash $141 $133 $114 $99

Working Capital Debt 72 63 84 97

Datatec Intercompany Loan 35 35 38 38

Net (Debt) / Cash 34 36 (8) (36)

Equity 261 268 284 279

Debt to Capitalization 0.29 0.27 0.30 0.33

Liabilities to TNW 1.61 1.68 1.87 1.65

WESTCON GROUP Net Cash Trend - FY 2000 to Current

Note: Amounts noted on graph represent the average net debt during FY 01, 02, 03, 04 and 05 to date.

-$350,000,000

-$300,000,000

-$250,000,000

-$200,000,000

-$150,000,000

-$100,000,000

-$50,000,000

$0

$50,000,000

$100,000,000

Feb-00

May-00

Aug-00

Nov-00

Feb-01

May-01

Aug-01

Nov-01

Feb-02

May-02

Aug-02

Nov-02

Feb-03

May-03

Aug-03

Nov-03

Feb-04

May-04

Aug-04

Net Cash

($224,336,852)

($139,544,122)

($59,842,704)

($30,701,555)

($87,655,105)

WESTCON GROUPFuture Outlook

• Vendors increasingly committed to distribution

• Voice and convergence markets growing; traditional voice and data

switching and routing markets steady

• Customer base stable

• Group-wide program implemented to increase future operating

income performance

LOGICALIS GROUP RESULTS FOR THE

SIX MONTHS ENDED 31 AUGUST 2004

LOGICALISHighlights

• First operating profit recorded in over three years

• Revenues up 12% sequentially (2% on comparative basis)

• Margins steady

• Operating expenses tightly controlled

• US producing a stronger performance

• Working capital effectively managed (DSO at 41 days)

• Launched focused services division in UK

• Acquisition of STI in the USA completed 1 September 2004 – $90M

IBM partner

LOGICALISFinancial Performance - Summary

Notes: 1) Includes Datatec level inter-company transactions which eliminate on Datatec consolidation

2) The exceptional profit arises on the sale of the Australian and New Zealand operations

Trading in the first half of FY2005 has produced an operating profit

US $000

Aug 2003 Feb 2004

Continuing Discontinued Total

Revenue 138,153 125,528 140,896 7,593 148,489

Gross profit 29,442 27,537 29,395 1,919 31,314

As % of revenue 21.3% 21.9% 20.9% 25.3% 21.1%

Operating expenses 28,530 28,811 27,666 1,662 29,328

As % of revenue 20.7% 23.0% 19.6% 21.9% 19.8%

EBITDA 912 (1,274) 1,729 257 1,986

As % of revenue 0.7% (1.0%) 1.2% 3.4% 1.3%

Operating profit/ (loss) (1,735) (4,047) 89 102 191

As % of revenue (1.3%) (3.2%) 0.1% 1.3% 0.1%

Exceptional profit - - - 44,853 44,853

Continuing

6 months to

Aug 2004

6 months to

LOGICALISRevenue (continuing operations)

North America comprises two-thirds of continuing operations(% of revenue)

Regions 1H04 2H04 1H05

UK 24.5% 27.9% 25.9%

Germany 1.9% 1.7% 1.6%

North America 70.2% 65.9% 67.8%

South America 3.4% 4.5% 4.7%

100.0% 100.0% 100.0%

LOGICALISRevenue Streams (continuing operations)

Revenue mix consistent

Note: Continuing operations exclude Australia and New Zealand

Product 77%

Prof Services8%

Maintenance7%

Managed Services

8%

1H04 1H05

Product 76%

Prof Services8%

Maintenance8%

Managed Services

8%

LOGICALISGross Margin % (continuing operations)

Gross margin percentages held relatively steady - mix change impact in US

Aug 2003

Feb 2004

Note: Continuing operations exclude Australia and New Zealand

5%

10%

15%

20%

30%

35%

UK Germany North America South America

Aug 200425%

Total

19.7% 19.4%

33.5%

21.3%

27.0%

20.4%

29.3%

21.9%

30.8%

18.1%

30.1%

20.9%

25.0%

23.5%

25.2%

6 months to

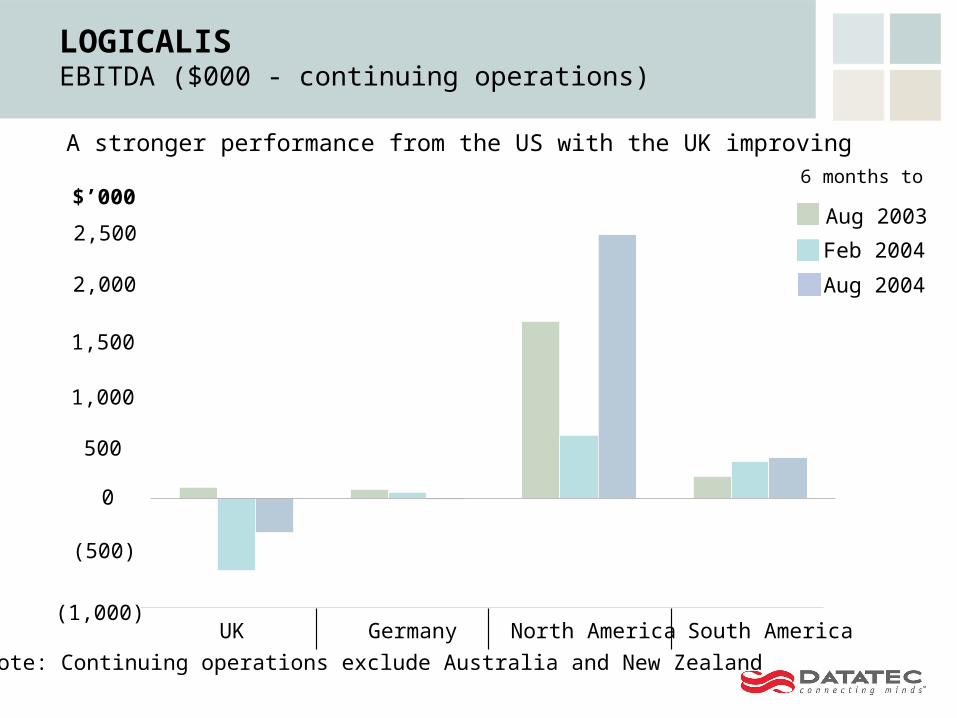

LOGICALISEBITDA ($000 - continuing operations)

A stronger performance from the US with the UK improving

Note: Continuing operations exclude Australia and New Zealand

$’000Aug 2003

Feb 2004

(1,000)

(500)

0

500

1,000

2,000

2,500

UK Germany North America South America

Aug 2004

1,500

6 months to

LOGICALISKey Financial Measures

Working capital remains effectively managed

Note: 1 Aug 2003 and Feb 2004 figures include Australia and New ZealandThese operations held net cash of $2M at Aug 2003 and $3M at Feb 2004

2 August 2004 net cash includes $41.7M after disposal of Australia/New Zealand operations and repayment of Datatec long term debt

1H04 2H04 1H05

Deferred Revenue ($000) 18,467 20,224 17,506

Inventory ($000) 16,250 16,766 11,622

Inventory Turns (excluding spares stock) 17 14 17

Accounts Receivable ($000) 46,902 48,097 37,138

DSO Days 47 43 41

Accounts Payable ($000) 40,376 42,568 37,667

DPO Days 71 73 79

Net Cash ($000) 18,026 25,797 64,991

Americas 490 469 448 452

Europe 280 226 211 207

Asia-Pac 330 344 324 -

Consolidated 1,100 1,039 983 659

LOGICALIS Headcount by Region

Region 2H03 1H04 2H04 1H05

LOGICALIS Key Product Vendors (Product Revenue %)

HP and Cisco remain our dominant vendors – Cisco stronger in first half of FY2005

Note: Continuing operations

IBM

EMCOthers

HPCisco

Sep-02 Feb-03 Aug-03

Feb-04 Aug-04

%

0

10

20

30

40

50

LOGICALISRecent Important Wins

• US – Exxon Mobile – large IBM win ($1.5M)

• US – Swiss Re Insurance – new customer for IBM solutions ($1.5M)

• US – LA County Sheriff – strong municipal reference story ($7.0M)

• UK – Haringey Council – won against 3Com and another Cisco partner

($943K)

• UK – Canada Life – VOIP single converged network structure ($808K)

• UK/South America – Major cross border education project won in UK,

delivered by South American operations ($909K)

• South America – Multi-country contract with major oil company ($1.6M)

LOGICALISProspects

• Acquisition of STI in USA will yield benefits

- improves critical mass

- creates a better balanced business

• UK services division gaining momentum

• South American operations now stable after difficult economic times

• Markets remain challenging and competitive

• Seeking to make further acquisitions, but based on strict criteria

• Cautiously optimistic for continuing performance improvement

ANALYSYS MASON GROUP

ANALYSYS MASON GROUPOverview

Analysys MasonGroup

Consultancy

Contact Centre & Change MgtConsultants

AnalysysConsulting

Analysys Research

MasonCommunications

Catalyst IT Partners

TelecommunicationsConsultants &

Implementation

IndependentTelecommunications

research

Strategic Telecommunications

Consultants

The Analysis Mason Group is an umbrella consultancy powerhouse

• Created in August 2004 with a projected first year turnover of £35m

• 300 staff based in 4 UK offices (London, Cambridge, Edinburgh and Manchester) and France, Ireland, Italy, Spain and the USA

• Management own 14% (max of 24% in future)

ANALYSYS MASON GROUPHighlights

• Significant recovery since Mason restructured in Jan 04

• Telecoms operators now spending again on consultancy services

• Rate pressures of recent years beginning to ease

• Mason turnover + 12% on 1H04

• After reductions in infrastructure cost, Mason EBITDA + 53% on 1H04

• Charge to close Employee Benefit Trust (EBT) due to AMG merger

• Annualised integration savings of approx £400k which will only

impact next financial year

ANALYSYS MASON GROUPFinancial Performance

£000 % £000 % £000 % £000 %Turnover 9,598 895 0 10,493Cost of sale 6,848 572 0 7,420Gross profit 2,750 28.7% 323 36.1% 0 0.0% 3,073 29.3%Operating costs 1,993 267 29 2,289EBITDA 757 7.9% 56 6.3% -29 0.0% 784 7.5%Depreciation 66 8 0 74PBIT 691 7.2% 48 5.4% -29 0.0% 710 6.8%

Interest paid/(received) 10 -4 18 24Profit before tax 681 7.1% 52 5.8% -47 0.0% 686 6.5%

Note - The above results excludes the Mason EBT closure.

Mason Analysys AMG Company AMG Consolidated1H05 1H05 1H05 1H05

1H05 Performance (6 mths Mason – 1mth Analysys)

ANALYSYS MASON GROUPJoint Bids

• Development Agency - a regional planning instrument and toolkit

• Development Agency - commercial and technical options for a

national broadband network

• Development Agency - commercial and technical due diligence

• Ofcom - allocating available spectrum within VHF band III and

L-Band

• Ofcom - Cost Benefit assessment of Ultra Wide Band

ANALYSYS MASON GROUPProspects

• Steady recovery taking place in Telecoms sector

• Increasing demand from operators across a range of issues

including; implementation, support, business planning,

consolidation and triple play (voice, data & TV)

• Continuing global diversification

• Identifying new cross-selling opportunities among the new Group’s

existing clients

• Should achieve further growth in revenues and margins in the

second half