Data Centers 2015 - Welcome | Burke & Quick...

18

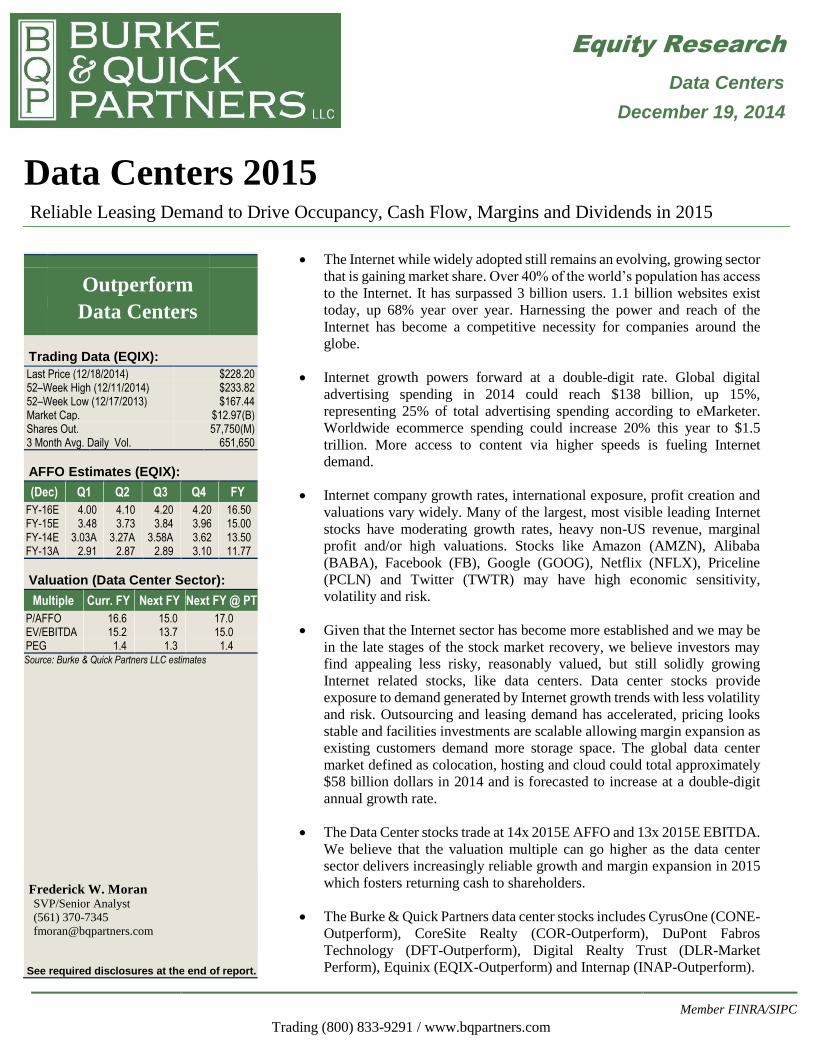

Trading (800) 833-9291 / www.bqpartners.com Member FINRA/SIPC Equity Research Data Centers December 19, 2014 Data Centers 2015 Reliable Leasing Demand to Drive Occupancy, Cash Flow, Margins and Dividends in 2015 The Internet while widely adopted still remains an evolving, growing sector that is gaining market share. Over 40% of the world’s population has access to the Internet. It has surpassed 3 billion users. 1.1 billion websites exist today, up 68% year over year. Harnessing the power and reach of the Internet has become a competitive necessity for companies around the globe. Internet growth powers forward at a double-digit rate. Global digital advertising spending in 2014 could reach $138 billion, up 15%, representing 25% of total advertising spending according to eMarketer. Worldwide ecommerce spending could increase 20% this year to $1.5 trillion. More access to content via higher speeds is fueling Internet demand. Internet company growth rates, international exposure, profit creation and valuations vary widely. Many of the largest, most visible leading Internet stocks have moderating growth rates, heavy non-US revenue, marginal profit and/or high valuations. Stocks like Amazon (AMZN), Alibaba (BABA), Facebook (FB), Google (GOOG), Netflix (NFLX), Priceline (PCLN) and Twitter (TWTR) may have high economic sensitivity, volatility and risk. Given that the Internet sector has become more established and we may be in the late stages of the stock market recovery, we believe investors may find appealing less risky, reasonably valued, but still solidly growing Internet related stocks, like data centers. Data center stocks provide exposure to demand generated by Internet growth trends with less volatility and risk. Outsourcing and leasing demand has accelerated, pricing looks stable and facilities investments are scalable allowing margin expansion as existing customers demand more storage space. The global data center market defined as colocation, hosting and cloud could total approximately $58 billion dollars in 2014 and is forecasted to increase at a double-digit annual growth rate. The Data Center stocks trade at 14x 2015E AFFO and 13x 2015E EBITDA. We believe that the valuation multiple can go higher as the data center sector delivers increasingly reliable growth and margin expansion in 2015 which fosters returning cash to shareholders. The Burke & Quick Partners data center stocks includes CyrusOne (CONE- Outperform), CoreSite Realty (COR-Outperform), DuPont Fabros Technology (DFT-Outperform), Digital Realty Trust (DLR-Market Perform), Equinix (EQIX-Outperform) and Internap (INAP-Outperform). Outperform Data Centers Trading Data (EQIX): Last Price (12/18/2014) $228.20 52–Week High (12/11/2014) $233.82 52–Week Low (12/17/2013) $167.44 Market Cap. $12.97(B) Shares Out. 57,750(M) 3 Month Avg. Daily Vol. 651,650 AFFO Estimates (EQIX): (Dec) Q1 Q2 Q3 Q4 FY FY-16E 4.00 4.10 4.20 4.20 16.50 FY-15E 3.48 3.73 3.84 3.96 15.00 FY-14E 3.03A 3.27A 3.58A 3.62 13.50 FY-13A 2.91 2.87 2.89 3.10 11.77 Valuation (Data Center Sector): Multiple Curr. FY Next FY Next FY @ PT P/AFFO 16.6 15.0 17.0 EV/EBITDA 15.2 13.7 15.0 PEG 1.4 1.3 1.4 Source: Burke & Quick Partners LLC estimates Frederick W. Moran SVP/Senior Analyst (561) 370-7345 [email protected] See required disclosures at the end of report.

Transcript of Data Centers 2015 - Welcome | Burke & Quick...

Trading (800) 833-9291 / www.bqpartners.com

Member FINRA/SIPC

Equity Research

Data Centers

December 19, 2014

Data Centers 2015 Reliable Leasing Demand to Drive Occupancy, Cash Flow, Margins and Dividends in 2015

The Internet while widely adopted still remains an evolving, growing sector

that is gaining market share. Over 40% of the world’s population has access

to the Internet. It has surpassed 3 billion users. 1.1 billion websites exist

today, up 68% year over year. Harnessing the power and reach of the

Internet has become a competitive necessity for companies around the

globe.

Internet growth powers forward at a double-digit rate. Global digital

advertising spending in 2014 could reach $138 billion, up 15%,

representing 25% of total advertising spending according to eMarketer.

Worldwide ecommerce spending could increase 20% this year to $1.5

trillion. More access to content via higher speeds is fueling Internet

demand.

Internet company growth rates, international exposure, profit creation and

valuations vary widely. Many of the largest, most visible leading Internet

stocks have moderating growth rates, heavy non-US revenue, marginal

profit and/or high valuations. Stocks like Amazon (AMZN), Alibaba

(BABA), Facebook (FB), Google (GOOG), Netflix (NFLX), Priceline

(PCLN) and Twitter (TWTR) may have high economic sensitivity,

volatility and risk.

Given that the Internet sector has become more established and we may be

in the late stages of the stock market recovery, we believe investors may

find appealing less risky, reasonably valued, but still solidly growing

Internet related stocks, like data centers. Data center stocks provide

exposure to demand generated by Internet growth trends with less volatility

and risk. Outsourcing and leasing demand has accelerated, pricing looks

stable and facilities investments are scalable allowing margin expansion as

existing customers demand more storage space. The global data center

market defined as colocation, hosting and cloud could total approximately

$58 billion dollars in 2014 and is forecasted to increase at a double-digit

annual growth rate.

The Data Center stocks trade at 14x 2015E AFFO and 13x 2015E EBITDA.

We believe that the valuation multiple can go higher as the data center

sector delivers increasingly reliable growth and margin expansion in 2015

which fosters returning cash to shareholders.

The Burke & Quick Partners data center stocks includes CyrusOne (CONE-

Outperform), CoreSite Realty (COR-Outperform), DuPont Fabros

Technology (DFT-Outperform), Digital Realty Trust (DLR-Market

Perform), Equinix (EQIX-Outperform) and Internap (INAP-Outperform).

Outperform

Data Centers

Trading Data (EQIX): Last Price (12/18/2014) $228.20 52–Week High (12/11/2014) $233.82 52–Week Low (12/17/2013) $167.44 Market Cap. $12.97(B) Shares Out. 57,750(M) 3 Month Avg. Daily Vol. 651,650

AFFO Estimates (EQIX):

(Dec) Q1 Q2 Q3 Q4 FY

FY-16E 4.00 4.10 4.20 4.20 16.50 FY-15E 3.48 3.73 3.84 3.96 15.00 FY-14E 3.03A 3.27A 3.58A 3.62 13.50 FY-13A 2.91 2.87 2.89 3.10 11.77

Valuation (Data Center Sector):

Multiple Curr. FY Next FY Next FY @ PT

P/AFFO 16.6 15.0 17.0 EV/EBITDA 15.2 13.7 15.0 PEG 1.4 1.3 1.4 Source: Burke & Quick Partners LLC estimates

Frederick W. Moran SVP/Senior Analyst

(561) 370-7345

See required disclosures at the end of report.

December 19, 2014

Burke & Quick Partners, LLC.

Equinix, Inc. Page 2 of 18 Frederick W. Moran

Investment Thesis

The Burke & Quick Partners research universe of data center stocks includes

CyrusOne (CONE-Outperform), CoreSite Realty (COR-Outperform), DuPont

Fabros Technology (DFT-Outperform), Digital Realty Trust (DLR-Market

Perform), Equinix (EQIX-Outperform) and Internap (INAP-Outperform). We

believe that the sector of data centers stocks will outperform for the following

reasons:

1) Internet growth powers forward at a double-digit rate. Global digital

advertising spending in 2014 could reach $138 billion, up 15%. Worldwide

ecommerce spending could increase 20% this year to $1.5 trillion.

2) More content at faster speed is fueling Internet demand. Internet traffic and

data storage demand has blossomed over the last few years and could

sustain strong growth for many more years.

3) Today, data centers capture less than 20% of all data storage. As companies

experience the superior reliability, speed and pricing of outsourced

offerings demand should blossom allowing market share gains.

4) Outsourcing and leasing demand has accelerated, pricing looks stable and

facilities investments are scalable allowing margin expansion as existing

customers demand more storage space.

5) The global data center market defined as colocation, hosting and cloud

could total approximately $58 billion dollars in 2014 and is forecasted to

increase at a double-digit annual growth rate.

6) REIT structures shields from most corporate income tax. Dividends are

yielding between 3% and 5% annually and will likely grow with free cash

generation.

7) Given that the Internet sector is more established and we may be in the late

stages of the stock market recovery, we believe investors may look to less

risky, reasonably valued, but still solidly growing Internet related stocks.

8) The Data Center stocks trade at 14x 2015E AFFO and 13x 2015E EBITDA.

9) We believe that the valuation multiple of data centers can go higher as the

sector proves increasingly reliable growth and margins expand which

fosters returning cash to shareholders. The stocks could prove rewarding

and outperform.

Internet growth powers

forward at a double-digit

rate

More content at faster

speed is fueling demand

Data Centers capture less

than 20% of all data

storage

REIT structures shields

from most corporate

income tax

Investors may look to less

risky Internet related stocks

Increasingly reliable growth

and margin expansion

Leasing demand has

accelerated

$58 billion dollars in 2014

Data centers stocks could

outperform

December 19, 2014

Burke & Quick Partners, LLC.

Equinix, Inc. Page 3 of 18 Frederick W. Moran

The Data Center Industry

Data centers are buildings that house servers and related hardware. Data centers

require four things: power, space, bandwidth (fiber) and cooling. They are

typically located in large metropolitan markets where these resources are readily

available. The major US data center markets are Silicon Valley, New York,

Northern Virginia, Dallas, Miami, Chicago and Los Angeles. The primary

European markets are London, Frankfurt, Amsterdam and Paris. The top locations

in Asia are Hong Kong, Tokyo, Singapore and Sydney.

Different markets are driven by different customers, and the differences are

predictable. Silicon Valley has many Internet content and software-as-a-service

companies. New York has a sizable financial contingent complementing

generally smaller Internet companies and European telecommunications

companies. Northern Virginia is primarily telecoms, Internet companies and

government. Miami hosts many Latin American companies.

The global data center demand is growing annually at a double-digit pace while

supply rises mid-single digits. Data center construction typically takes about one

year. Over the past year demand have accelerated. Pricing has held steady. Pricing

typically starts to move up once 70% of capacity is reached in any one center. At

70%, space is still available but not easily accessible for expansion by an existing

customer.

Businesses across Internet commerce, advertising and content, data center

demand remain robust with sustained revenue growth. Internet traffic should

growth over 20% per year through 2018 according to Cisco.

The biggest concerns of data center customers are capacity, connectivity, power

and uptime. Other concerns include cooling, computing power, tech support,

security and speed of expansion, which are equally important but somewhat easier

to duplicate. Customers are typically charged rental space, power utilization fees

and service costs.

The main reasons for purchasing new servers are normal demand driven needs

for increases in capacity, upgrades to old servers and new server purchases for

new applications. All three of these drivers should increase demand for either data

center capacity and/or power utilization.

Addressable Market

Worldwide IT spending is on pace to total $3.8 trillion in 2014, a 3.2% increase

from 2013 spending, according to the latest forecast by Gartner, Inc. International

Data Corporation (IDC) Worldwide Black Book projects worldwide IT spending

will increase by 4.1% in constant currency this year down from last year’s growth

of 4.5%. Forrester estimates Global Tech Purchases will rise 3.3% in 2014.

IT will not be outsourced completely. However, a significant amount of IT

infrastructure could be outsourced to data center providers over time. Another

indicator of the addressable market for IT infrastructure is total IT hardware

expenditures. IT infrastructure providers replace internal data centers, which

represent a significant portion of IT hardware costs. IT infrastructure is becoming

an increasingly larger portion of hardware costs as applications are delivered over

networks instead of individual desktops. IDC says the top priority of Chief

Data Center demand is

growing annually at a mid-

teens pace

Capacity, connectivity,

power and uptime

Data centers are buildings

that house servers and

related hardware

Worldwide IT spending is

on pace to total $3.8 trillion

in 2014, a 3.2% increase

December 19, 2014

Burke & Quick Partners, LLC.

Equinix, Inc. Page 4 of 18 Frederick W. Moran

Information Officers is reducing costs. Sharing infrastructure via outsourcing is

the most compelling way to reduce this capital and operating expense.

Growth Drivers

Data Center revenue growth has been about 15% annually. Growth is maintained

as companies recognize the efficiency inherent in sharing infrastructure. Cost

savings of as much as 50%, coupled with more flexibility, drive corporations to

outsource. Faster broadband speeds and improving technology also contribute to

IT outsourcing growth. Roughly 85% of servers are on the premises of the

company utilizing them.

Blossoming Internet communications is a primary contributor to data center

growth. The evolution of Internet communications as the primary means of

communication for both companies and individuals is a core driver of IP and data

center growth. This is evident in the consumption of Internet media, content and

information, represented by Google, Facebook, Netflix and YouTube.

Ecommerce is another contributor, best exemplified by the market share gains of

online commerce companies like Amazon. Ecommerce spending sustains 20%

growth while retail grows at a mid-single digits pace.

Consumer Internet consumption continues to increase rapidly. According to

eMarketer, 75% of online users watch digital videos. However, Nielsen believes

the average online user watches less than four hours of online video per month.

We believe as broadband speed increases, the consumption of online video will

grow rapidly. The list goes on – gaming, peer-2-peer, rich media advertising – all

should contribute to an explosion in usage that requires greater server capacity

and drives data center demand and revenue.

Beyond consumer-driven IP growth, corporations are relying increasingly on IP

for communicating. Email, instant messaging, and voice are currently delivered

via the Internet. In addition, software and applications such as customer

relationship management are utilized via the Internet and housed remotely at data

centers. Increasing real-time business requirements and storage needs add to

demand. Electronic trading is also growing rapidly and adding to network and

server demands.

Internet data traffic has increased more than fivefold over the last 5 years and

could increase threefold over the next 5 years according to Cicso Systems. Cisco

Systems, which is the largest manufacturer of IP equipment, believes IP traffic

will grow at a compound annual growth rate of over 20% through 2018.

While IP traffic is growing rapidly, IT continues to be complex and ever-

changing. Coupling this with recent technology improvements such as

virtualization and faster broadband speed creates an attractive environment for

outsourcing IT to data centers. Given as much as 80%–90% of computing

capacity on dedicated servers goes unused at any given time, virtualization

enables unused capacity to be utilized.

Data Center revenue

growth has been about

15% per year

Internet consumption

continues to increase

rapidly

Internet data traffic grew

increased more than

fivefold over the last 5

years

December 19, 2014

Burke & Quick Partners, LLC.

Equinix, Inc. Page 5 of 18 Frederick W. Moran

REITS

REITS are Real Estate Investment Trusts. Companies with this tax structure can

be of higher relative value than non-REIT companies because profits are largely

shielded from corporate income tax. That savings can be passed along to the

shareholders in the form of dividend. Often REITs have fairly high dividend. The

publicly traded data center REITs have dividends ranging from 3% to 5%

annually.

To qualify as a REIT a company must have at least 75% of its assets in real estate,

75% of income must come from real estate, 90% of pre-tax income must be

distributed to shareholders, no more than 50% of the stock can be owned by five

or fewer individuals, and the company cannot own more than 10% of a tenant.

Today, most of the publicly traded Data Centers have a REIT structure. All would

likely qualify because data centers are physical buildings that rent space to clients

housing servers to store and transmit data.

Risks

Macro-Economic and Interest Rates

Data center demand can fluctuate depending on economic conditions. Rising

interest rates can hurt data center stocks in a number of different ways. First, rising

interest rates make the dividend yield of REITs less attractive because alternatives

including risk free treasuries become a more viable alternative. Second, the cost

of borrowings of both existing variable loans and future loans can impair bottom-

line profits including AFFO. Third, rising interest rates lessen the present value

of future cash flow.

Competition and Pricing

Communications real-estate and hosting services are highly fragmented and

competitive sectors.

Pricing may be pressured over time as data centers compete with large companies

that have greater resources, such as Microsoft, IBM, EDS, AT&T and Amazon.

These companies have the ability to invest materially more capital in their

businesses. They also could lower pricing given they have greater scale.

Historically data center industry colocations contracts have averaged 2-3 years,

but more recently contracts have spanned 3-7 years. While pricing pressure and

potential margin erosion is a threat to the business opportunity, the outstripping

of demand versus supply has allowed stable pricing in 2014.

Virtualization and Potential Pricing Power Deterioration

Virtualization is a broad IT term referring to the abstraction of computing

resources to perform multiple tasks. As much as 80%–90% of computing capacity

on dedicated servers goes unused at any given time. Cloud computing is a hot

REITS are Real Estate

Investment Trusts

Pricing may be pressured

Rising interest rates can

hurt data centers

Recently contracts have

spanned 3-7 years

Most of the publicly traded

Data Centers are REITs

December 19, 2014

Burke & Quick Partners, LLC.

Equinix, Inc. Page 6 of 18 Frederick W. Moran

area within virtualization. Cloud computing refers to computing resources made

accessible as scalable, on-demand services over a network. Cloud computing

combines virtualization, service-orientation, elasticity, multi-tenancy and pay-as-

you-go billing. Adopters of cloud computing seek to capture improved cost

efficiencies, accelerated innovation cycles, faster time-to-market deployment,

and scalability on-demand.

Virtualization enables colocation clients to occupy less space because server

efficiency improves. Customers can now run multiple applications or projects on

a single or group of shared servers, as opposed to dedicating individual servers

for each project or task. This can result in lower colocation revenue per customer

for the group but might aid cloud revenue.

Virtualization is an example of how technological advancement might impact the

colocation business negatively. In general, as server hardware advances, the

amount of physical space required to power the same computing capacity could

lessen. If technological advancements overwhelm the trend of growing IP traffic,

then colocation demand and pricing could decline.

Availability of and Access to Credit

Data Center development requires meaningful, substantial upfront spending to

construct and build facilities. Availability of capital is critical to future growth.

Should lending markets tighten, facility development could suffer.

Dependence on a Limited Number of Large Enterprise Clients

Liquidity crises and customer bankruptcies add to churn. Recent signs point to

steady improvement in the economy, the consumer, credit and the economy, but

demand can be sensitive to any change in these variables.

Publicly Traded Data Center Operators

CyrusOne Inc.

CyrusOne (CONE) operates 25 Data Centers. It serves 656 customers including

141 of the Fortune 1000. CyrusOne seeks to serve as the preferred global data

center provider to the global Fortune 1000. Its 25 facilities comprise 1.2 million

colocation square feet. While its customer base is fairly diversified, two of

CyrusOne’s largest sectors are Energy and IT, each representing roughly 30% of

revenue. The company headquarters is located just north of Dallas, Texas at 1649

West Frankford Road, Carrollton, Texas 75007.

CyrusOne should sustain strong business momentum in 2015 as it has already

constructed enough data center building shell to allow for nearly a doubling of

total company capacity, its latest facility in Phoenix was built in an industry

record 107 days, year to date new lease signings are at record levels and

management led by CEO Gary Wojtaszek appears focused on both operational

and stock performance.

Virtualization enables

colocation clients to occupy

less space

CyrusOne operates 25

Data Centers comprising

1.2 million square feet

serving 656 customers

Availability of capital is

critical

Churn

Has enough data center

building shell to allow for

nearly a doubling of total

company capacity

December 19, 2014

Burke & Quick Partners, LLC.

Equinix, Inc. Page 7 of 18 Frederick W. Moran

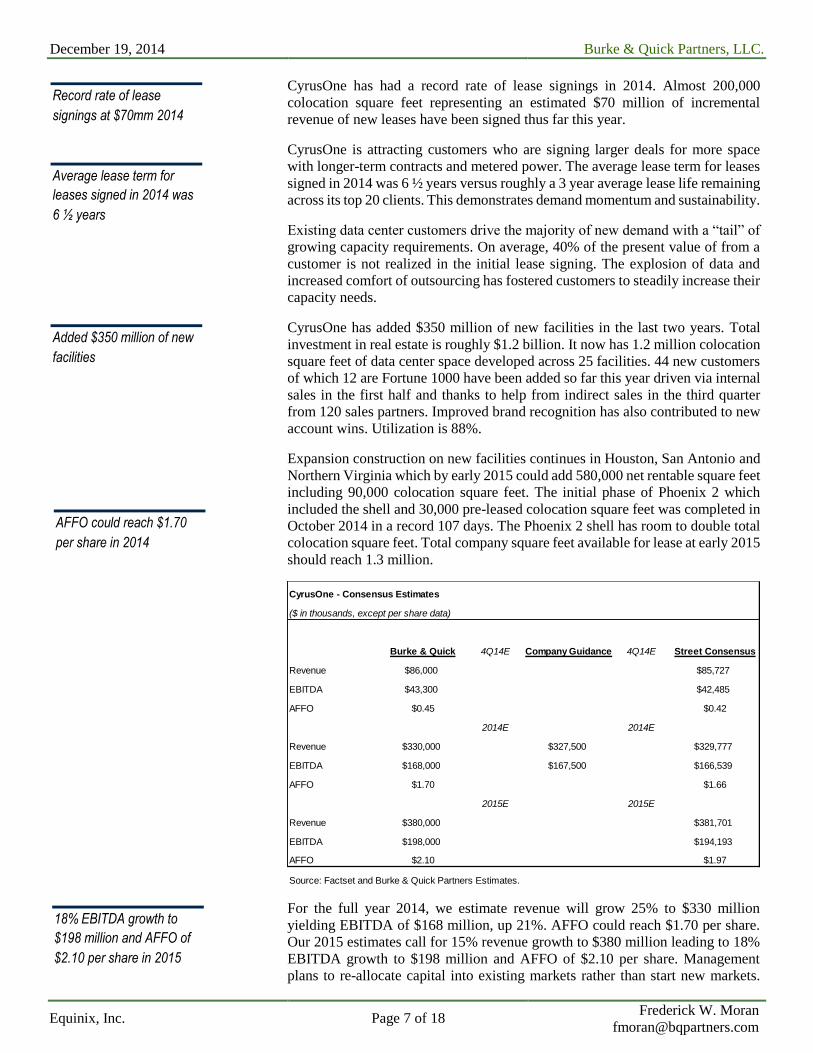

CyrusOne has had a record rate of lease signings in 2014. Almost 200,000

colocation square feet representing an estimated $70 million of incremental

revenue of new leases have been signed thus far this year.

CyrusOne is attracting customers who are signing larger deals for more space

with longer-term contracts and metered power. The average lease term for leases

signed in 2014 was 6 ½ years versus roughly a 3 year average lease life remaining

across its top 20 clients. This demonstrates demand momentum and sustainability.

Existing data center customers drive the majority of new demand with a “tail” of

growing capacity requirements. On average, 40% of the present value of from a

customer is not realized in the initial lease signing. The explosion of data and

increased comfort of outsourcing has fostered customers to steadily increase their

capacity needs.

CyrusOne has added $350 million of new facilities in the last two years. Total

investment in real estate is roughly $1.2 billion. It now has 1.2 million colocation

square feet of data center space developed across 25 facilities. 44 new customers

of which 12 are Fortune 1000 have been added so far this year driven via internal

sales in the first half and thanks to help from indirect sales in the third quarter

from 120 sales partners. Improved brand recognition has also contributed to new

account wins. Utilization is 88%.

Expansion construction on new facilities continues in Houston, San Antonio and

Northern Virginia which by early 2015 could add 580,000 net rentable square feet

including 90,000 colocation square feet. The initial phase of Phoenix 2 which

included the shell and 30,000 pre-leased colocation square feet was completed in

October 2014 in a record 107 days. The Phoenix 2 shell has room to double total

colocation square feet. Total company square feet available for lease at early 2015

should reach 1.3 million.

For the full year 2014, we estimate revenue will grow 25% to $330 million

yielding EBITDA of $168 million, up 21%. AFFO could reach $1.70 per share.

Our 2015 estimates call for 15% revenue growth to $380 million leading to 18%

EBITDA growth to $198 million and AFFO of $2.10 per share. Management

plans to re-allocate capital into existing markets rather than start new markets.

CyrusOne - Consensus Estimates

($ in thousands, except per share data)

Burke & Quick 4Q14E Company Guidance 4Q14E Street Consensus

Revenue $86,000 $85,727

EBITDA $43,300 $42,485

AFFO $0.45 $0.42

2014E 2014E

Revenue $330,000 $327,500 $329,777

EBITDA $168,000 $167,500 $166,539

AFFO $1.70 $1.66

2015E 2015E

Revenue $380,000 $381,701

EBITDA $198,000 $194,193

AFFO $2.10 $1.97

Source: Factset and Burke & Quick Partners Estimates.

AFFO could reach $1.70

per share in 2014

Added $350 million of new

facilities

Record rate of lease

signings at $70mm 2014

Average lease term for

leases signed in 2014 was

6 ½ years

18% EBITDA growth to

$198 million and AFFO of

$2.10 per share in 2015

December 19, 2014

Burke & Quick Partners, LLC.

Equinix, Inc. Page 8 of 18 Frederick W. Moran

We speculate another roughly 200,000 csf could be added in 2015. The plan is to

spend less capital in 2015 with a higher return.

CyrusOne has long-term debt of $555 million plus $14 million of capital lease

obligations and cash of $30 million. Net debt to annualized EBITDA stands at 3x.

CyrusOne pays a $0.21 per share quarterly dividend.

CyrusOne trades below peers despite superior market positioning and growth

potential. Using 17x 2015E AFFO and 15x EBITDA, we maintain our per share

price target for CyrusOne of $36.

CoreSite Realty Corporation

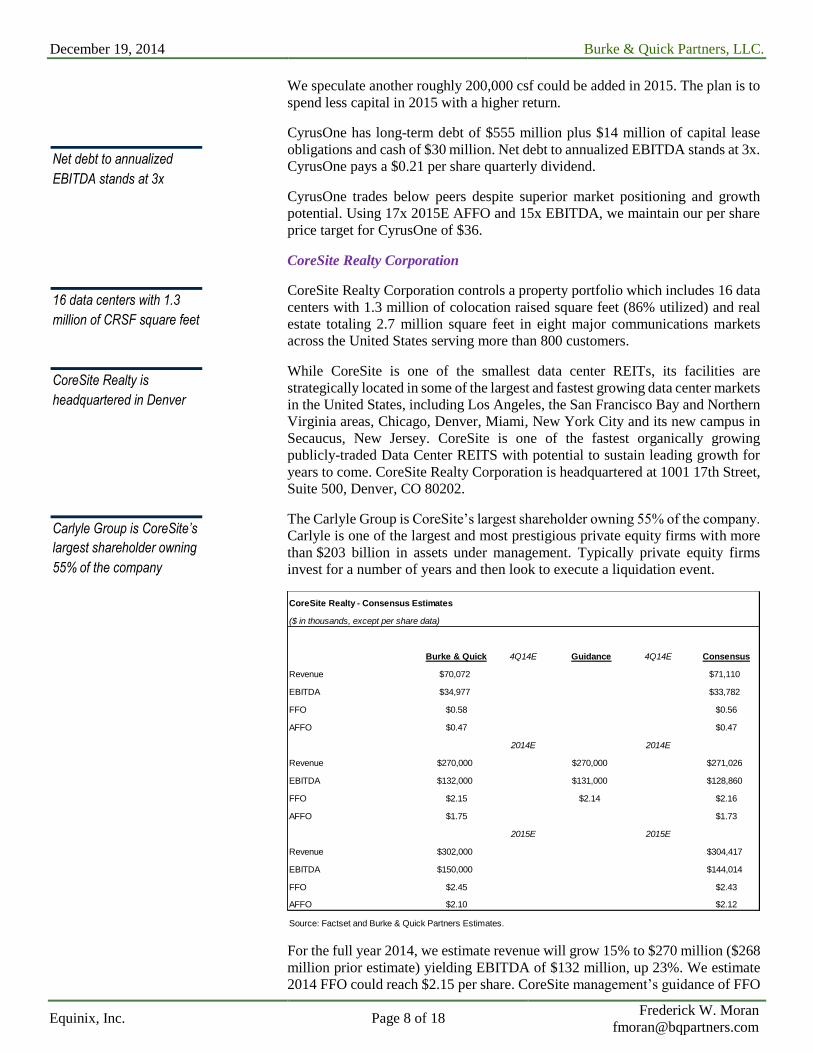

CoreSite Realty Corporation controls a property portfolio which includes 16 data

centers with 1.3 million of colocation raised square feet (86% utilized) and real

estate totaling 2.7 million square feet in eight major communications markets

across the United States serving more than 800 customers.

While CoreSite is one of the smallest data center REITs, its facilities are

strategically located in some of the largest and fastest growing data center markets

in the United States, including Los Angeles, the San Francisco Bay and Northern

Virginia areas, Chicago, Denver, Miami, New York City and its new campus in

Secaucus, New Jersey. CoreSite is one of the fastest organically growing

publicly-traded Data Center REITS with potential to sustain leading growth for

years to come. CoreSite Realty Corporation is headquartered at 1001 17th Street,

Suite 500, Denver, CO 80202.

The Carlyle Group is CoreSite’s largest shareholder owning 55% of the company.

Carlyle is one of the largest and most prestigious private equity firms with more

than $203 billion in assets under management. Typically private equity firms

invest for a number of years and then look to execute a liquidation event.

For the full year 2014, we estimate revenue will grow 15% to $270 million ($268

million prior estimate) yielding EBITDA of $132 million, up 23%. We estimate

2014 FFO could reach $2.15 per share. CoreSite management’s guidance of FFO

CoreSite Realty - Consensus Estimates

($ in thousands, except per share data)

Burke & Quick 4Q14E Guidance 4Q14E Consensus

Revenue $70,072 $71,110

EBITDA $34,977 $33,782

FFO $0.58 $0.56

AFFO $0.47 $0.47

2014E 2014E

Revenue $270,000 $270,000 $271,026

EBITDA $132,000 $131,000 $128,860

FFO $2.15 $2.14 $2.16

AFFO $1.75 $1.73

2015E 2015E

Revenue $302,000 $304,417

EBITDA $150,000 $144,014

FFO $2.45 $2.43

AFFO $2.10 $2.12

Source: Factset and Burke & Quick Partners Estimates.

CoreSite Realty is

headquartered in Denver

16 data centers with 1.3

million of CRSF square feet

Net debt to annualized

EBITDA stands at 3x

Carlyle Group is CoreSite’s

largest shareholder owning

55% of the company

December 19, 2014

Burke & Quick Partners, LLC.

Equinix, Inc. Page 9 of 18 Frederick W. Moran

calls for a range of $2.12 to $2.16. Our AFFO estimate which deducts recurring

capital spending is $1.70 per share.

Our 2015 financial projections call for 12% revenue growth to $302 million

leading to 14% EBITDA growth to $150 million. 2015 FFO could reach $2.46

per share and AFFO $2.10 per share.

For CoreSite Realty, debt to EBITDA stands at roughly 2x. Including preferred

obligations of $115 million the ratio jumps to 3x. CoreSite Realty offers shielded

free cash generation thanks to its favorable REIT tax status. A $0.42 quarterly

dividend currently yields over 4% annually. Using 20x 2015E AFFO and 15x

EBITDA, our price target for CoreSite is $41.

DuPont Fabros Technology, Inc.

DuPont Fabros Technology, Inc. owns, develops, operates and manages data

centers. It leases access on a triple-net wholesale basis. Its portfolio includes 11

facilities in 4 major markets totaling 2.8 gross square feet and 1.4 million

wholesale computer room square feet (CRSF) offering 240 megawatts of critical

load. It has heavy exposure to Northern Virginia via a 6 facility campus in

Ashburn, a facility in Reston and one in Bristow; all in an area that is one of the

two most fiber dense areas in the U.S. We believe DuPont Fabros is the largest

Data Center provider in Northern Virginia. The portfolio was 97% leased (93%

if you include “not stabilized” properties.

DuPont Fabros serves Internet industry leaders, including Microsoft, Facebook,

Yahoo! and Rackspace. In total, DuPont Fabros serves 34 customers with 100

different lease expirations and an average remaining lease term of 6.1 years. The

top 4 clients represent 61% of annual base rent. Investment grade or equivalent

large enterprises represent 77% of revenue. The company is structured as a Real

Estate Investment Trust (REIT). DuPont Fabros is headquartered in our Nation’s

capital just four blocks from the White House at 1212 New York Avenue, NW,

Suite 900, Washington, D.C 20005.

Yahoo! has begun a multi-year shift of its servers away from DuPont to its

company-owned Buffalo, NY based facility which offers it company specific tax

advantages. Yahoo! entered into a tri-party sublease agreement with one of

DuPont Fabros’ existing large customers for 13.65 MW expiring in 4.55 MW

tranches in 2017-2019 in its ACC$ data center. Yahoo! will pay through the

remainder of its lease. Then the sublease customer has contracted to continue at

lower current market pricing levels, so that the entire lease now terminates in

2019.

Management has extended its CEO succession plan in an effort to hasten a near-

term resolution. The company plans to hire a candidate to immediately assume

the role of CEO and President. Current CEO Fateh will support the successor and

remain on the Board.

Given DuPont’s facilities are almost at full capacity, 97% leased, and

management has taken a methodical approach to new facility development,

growth may be somewhat hindered as pricing typically does not outpace inflation.

For the full year 2014, we estimate revenue will grow 11% to $417 million

yielding EBITDA of $268 million, up 10%. AFFO could reach $2.50 per share.

Dividend yields over 4%

AFFO could reach $2.50

per share in 2014 and

$2.70 in 2015

11 facilities in 4 major

markets with heavy

exposure to Northern VA

2015 AFFO $2.10

Average remaining lease

term of 6.3 years

Yahoo! entered into a tri-

party sublease agreement

97% leased

December 19, 2014

Burke & Quick Partners, LLC.

Equinix, Inc. Page 10 of 18 Frederick W. Moran

Our 2015 estimates call for 7% revenue growth to $447 million leading to

EBITDA of $290 million, up 8%, and AFFO of $2.70 per share, up 8%

Performance might be boosted by two projects currently under development

including Santa Clara SCA Phase 11B offering 9.1 megawatts which is currently

50% pre-leased and expected to deliver in early 2Q15 and Chicago CH2 Phase 1

offering 7.1 megawatts expected 3Q15.

DuPont Fabros has long-term debt of $965 million. Debt maturities begin in 2018,

2019 and balloon with $600 million due in 2021. Net debt to annualized EBITDA

stands at 3.5x. Cash flow coverage of interest is almost 6x. Preferred stock adds

$351 million to liabilities.

DuPont Fabros offers shielded free cash generation thanks to its favorable REIT

tax status. It pays a $0.42 quarterly dividend yielding 5% annually. The dividend

was increased 5 times over the last 11 quarters. The payout ratio is less than 65%

of AFFO.

Digital Realty Trust

Digital Realty Trust, Inc. is one of the 20 largest publicly-traded U.S. real estate

investment trusts (REIT) and the biggest that specifically focuses on

infrastructure for the digital economy. Digital Realty offers data center solutions

by building and leasing facilities throughout the world via 130 properties. Its

portfolio is located in 30 markets throughout North America, Europe, Asia and

Australia. The properties aggregate 24.5 million square feet including

approximately 1.3 million square feet of space under active development and 1.4

million square feet of space held for future development.

Digital Realty offers data center and colocation service to over 600 clients via

over 2,000 leases. Its clients include domestic and international companies across

multiple industry verticals, of all sizes, ranging from financial services, cloud and

information technology services, to manufacturing, energy, gaming, life sciences,

DuPont Fabros - Consensus Estimates

($ in thousands, except per share data)

Burke & Quick 4Q14E Guidance 4Q14E Consensus

Revenue $107,385 $106,249

EBITDA $68,388 $71,056

FFO $0.62 $0.62 $0.62

AFFO $0.62 $0.66

2014E 2014E

Revenue $417,000 $415,000 $415,003

EBITDA $268,000 $271,498

FFO $2.42 $2.40 $2.41

AFFO $2.50 $2.51

2015E 2015E

Revenue $447,000 $443,758

EBITDA $290,000 $290,336

FFO $2.60 $2.56

AFFO $2.70 $2.66

Source: Factset and Burke & Quick Partners Estimates.

Net debt to annualized

EBITDA stands at 3.5x

DLR is one of 20 largest

publicly-traded U.S. REITs

24.5 million square feet

DFT’s dividend yields 5%.

It was increased 5 times

over the last 11 quarters

December 19, 2014

Burke & Quick Partners, LLC.

Equinix, Inc. Page 11 of 18 Frederick W. Moran

health care, and consumer products. Digital Realty Trust has been a publicly

traded stock for ten years generating positive year over year growth in both

dividends and FFO per share every one of those years. It is headquartered at Four

Embarcadero Center, Suite 3200, San Francisco, CA 94111.

Digital Realty’s management mentioned its plans for potential assets sales over

the next few quarters. It could strengthen the balance sheet ensuring the

company’s investment grade debt rating while supporting the dividend and

possibly sparking an extra one-time dividend.

Digital Realty’s pricing disciple combined with increased rent per square foot

should allow mid-single digit revenue and EBITDA growth. For the full year

2014, we estimate that revenue could reach $1.62 billion, up 9%. EBITDA could

hit $935 million, up 6%. Core funds from operations (CFFO) could reach $4.90

per share in 2014 and adjusted funds from operations (AFFO) could be $3.75. In

2015, we estimate CFFO of $5.00 and AFFO of $4.00.

Digital Realty offers shielded free cash generation thanks to its favorable REIT

tax status. It has provided 10 consecutive years of dividend increases. The last

authorized quarterly cash dividend of $0.83 per share to common stockholders

was paid on September 30, 2014. A $0.83 quarterly dividend currently yields 5%

annually.

Digital Realty Trust trades above the data center group despite slower growth

likely due to its size and high dividend yield. Using 18x AFFO and 15x EBITDA,

we maintain a price target of $70 for Digital Realty Trust.

Equinix

Equinix Inc. builds and operates data center facilities across the United States,

Europe and Asia. It operates 101 data centers in 32 markets across 15 countries

in the Americas, EMEA, and Asia-Pacific on five continents. In total it controls

Digital Realty - Consensus Estimates

($ in millions, except per share data)

Burke & Quick 4Q14E Guidance 4Q14E Consensus

Revenue $415,778 $413,448

EBITDA $232,359 $233,650

CFFO $1.19 $1.23

AFFO $0.89 $0.95

2014E 2014E

Revenue $1,620,000 $1,619,342

EBITDA $935,000 $927,993

CFFO $4.90 $4.93 $4.91

AFFO $3.75 $3.74

2015E 2015E

Revenue $1,720,000 $1,703,372

EBITDA $980,000 $977,564

CFFO $5.00 $5.09

AFFO $4.00 $3.99

Source: Factset and Burke & Quick Partners Estimates.

100 data centers in 32

markets across 15

countries

Potential assets sales over

the next few quarters

Pricing disciple

10 consecutive years of

dividend increases

December 19, 2014

Burke & Quick Partners, LLC.

Equinix, Inc. Page 12 of 18 Frederick W. Moran

3.8 million square feet of colocation space. The company headquarters is located

at One Lagoon Drive, 4th Floor, Redwood City, CA 94065.

Equinix has filed for REIT tax status. It is scheduled to convert into a REIT at the

start of 2015. Employing a REIT structure will shield it from most corporate

income tax. The introduction of a regular dividend will be required in order to

comply with being a REIT.

The conversion to a REIT could boost valuation as shielding future corporate

income taxation results in incremental shareholder value creation in the form of

dividends.

Inclusion in REIT indexes could broaden Equinix’s shareholder base and further

enhance valuation. After Equinix converts to a REIT on 1/1/2015. In our opinion,

it will likely get reviewed and included into the two leading REIT indices RMZ

and FTSE/NAREIT. We expect this to occur mid to late in the first quarter of

2015.

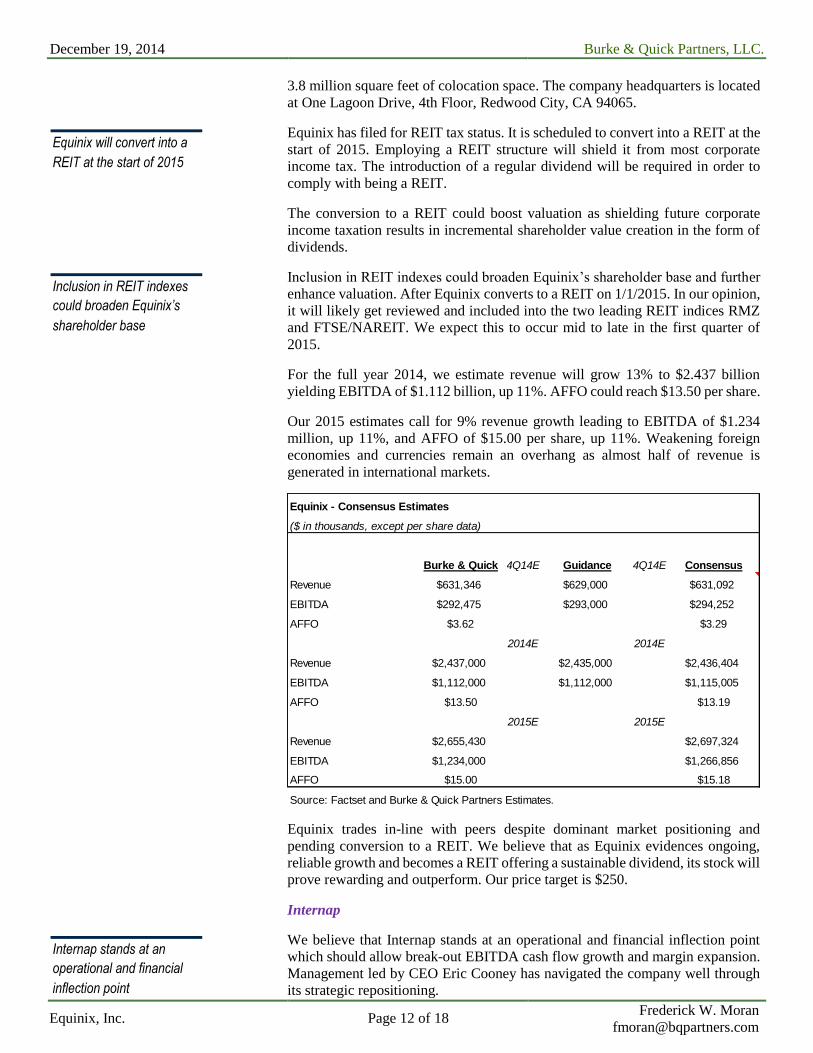

For the full year 2014, we estimate revenue will grow 13% to $2.437 billion

yielding EBITDA of $1.112 billion, up 11%. AFFO could reach $13.50 per share.

Our 2015 estimates call for 9% revenue growth leading to EBITDA of $1.234

million, up 11%, and AFFO of $15.00 per share, up 11%. Weakening foreign

economies and currencies remain an overhang as almost half of revenue is

generated in international markets.

Equinix trades in-line with peers despite dominant market positioning and

pending conversion to a REIT. We believe that as Equinix evidences ongoing,

reliable growth and becomes a REIT offering a sustainable dividend, its stock will

prove rewarding and outperform. Our price target is $250.

Internap

We believe that Internap stands at an operational and financial inflection point

which should allow break-out EBITDA cash flow growth and margin expansion.

Management led by CEO Eric Cooney has navigated the company well through

its strategic repositioning.

Equinix - Consensus Estimates

($ in thousands, except per share data)

Burke & Quick 4Q14E Guidance 4Q14E Consensus

Revenue $631,346 $629,000 $631,092

EBITDA $292,475 $293,000 $294,252

AFFO $3.62 $3.29

2014E 2014E

Revenue $2,437,000 $2,435,000 $2,436,404

EBITDA $1,112,000 $1,112,000 $1,115,005

AFFO $13.50 $13.19

2015E 2015E

Revenue $2,655,430 $2,697,324

EBITDA $1,234,000 $1,266,856

AFFO $15.00 $15.18

Source: Factset and Burke & Quick Partners Estimates.

Equinix will convert into a

REIT at the start of 2015

Inclusion in REIT indexes

could broaden Equinix’s

shareholder base

Internap stands at an

operational and financial

inflection point

December 19, 2014

Burke & Quick Partners, LLC.

Equinix, Inc. Page 13 of 18 Frederick W. Moran

Growth has accelerated thanks to new data center launches and the acquisition of

iWeb. Having spent roughly $300 million over the last few years building out 16

company owned data centers which are at only a 60% data center capacity

utilization rate, Internap has room to meaningfully add customers without

spending heavily on facilities expansion.

Data center service now represents 73% of total company revenue, up from 60%

only two years ago. The core owned data centers alone represent 59% of revenue

versus 42% two years ago. Core owned data center revenues grew 16% on an

organic basis in 3Q14.

Mario Gabelli’s GAMCO, Gabelli Funds and associated entities stand as

Internap’s largest shareholder owning roughly 10.1 million shares (down from a

peak of 10.5 million) or 18.6% (prior 19.3%) of the company. According to a

Form 13-D filed with the SEC on November 18, 2014,

http://ir.internap.com/sec.cfm, Gabelli sold a net of roughly 400,000 shares of

Internap between 9/19/14 and 11/18/14 at prices ranging from $6.55 per share to

$8.17 per share.

We speculate that Gabelli has traded around his core position in Internap likely

for tax planning and/or short-term trading reasons. Gabelli’s investment style

often uncovers unrecognized value through investing in companies that sell below

private market value while waiting patiently to see the value get recognized. We

believe Gabelli remains positioned for the long-term especially given the recent

impressive operating results and potential for break-out margin improvement

ahead Internap reported accelerating growth and expanding margins in its 3Q14

financial results and guided to higher than expected 4Q14 EBITDA.

Internap - Consensus Estimates

($ in thousands, except per share data)

Burke & Quick 4Q 2014 Consensus

Revenue $85,000 $84,518

EBITDA $21,984 $21,768

AFFO $0.21

2014

Revenue $335,696 $335,372

EBITDA $78,000 $77,176

AFFO $0.66

2015

Revenue $355,000 $350,967

EBITDA $90,000 $88,931

AFFO $0.90

Source: Factset and Burke & Quick Partners Estimates.

Gabelli sold a net of

roughly 400,000 shares

Gabelli remains positioned

for the long-term

Data center service now

represents 73% of total

company revenue

Invested $300mm

launching new data centers

December 19, 2014

Burke & Quick Partners, LLC.

Equinix, Inc. Page 14 of 18 Frederick W. Moran

We estimate Internap will produce $336 million of revenue, $78 million

EBITDA, $36 million of recurring free cash flow and $0.66 per share of AFFO

in 2014. After all capital requirements Internap may “burn” roughly $24 million

in cash in 2014.

On a recent investor conference call management confirmed they believe that the

new margin levels can be sustained and extended further. We suspect that as

EBITDA margins rise thanks to an increasing percentage of growth coming from

the core owned data centers, Internap’s valuation gap relative to its peers could

improve.

In 2015, EBITDA could grow 15% to $90 million producing $0.90 per share in

AFFO and/or recurring free cash flow per share.

Internap has long-term debt of $293 million, $54 million in capital lease

obligations and working capital of negative $4 million. Net debt to EBITDA

stands above 4x. The company’s goal is to reduce leverage ½ a turn every year

until it hits 3x.

Internap trades at only 8x 2015E AFFO and EBITDA, a substantial discount to

the group. Using 11x 2015E AFFO of $0.90 and 10x EBITDA of $90 million, our

price target is $10. Our rating on Internap is Outperform.

Valuation

The Data Center sector trades at 14x 2015E AFFO and 13x 2015E EBITDA with

a double-digit rate of annual growth. With a recurring business model and

infrastructure that has strategic value, we believe the multiple can go higher.

Internap trades at only 8x

EBITDA could grow 15% to

$90 million in 2015

$78 million EBITDA 2014

Margins can be sustained

and extended further

December 19, 2014

Burke & Quick Partners, LLC.

Equinix, Inc. Page 15 of 18 Frederick W. Moran

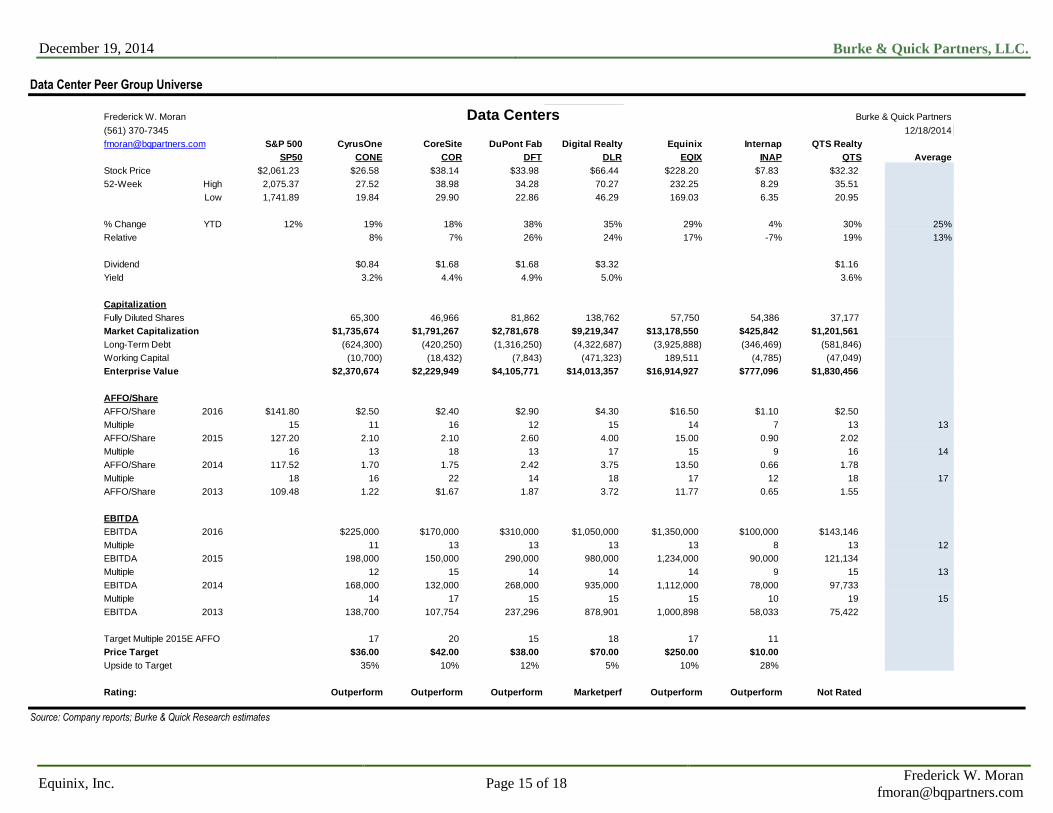

Data Center Peer Group Universe

Source: Company reports; Burke & Quick Research estimates

Frederick W. Moran Data Centers Burke & Quick Partners

(561) 370-7345 12/18/2014

[email protected] S&P 500 CyrusOne CoreSite DuPont Fab Digital Realty Equinix Internap QTS Realty

SP50 CONE COR DFT DLR EQIX INAP QTS Average

Stock Price $2,061.23 $26.58 $38.14 $33.98 $66.44 $228.20 $7.83 $32.32

52-Week High 2,075.37 27.52 38.98 34.28 70.27 232.25 8.29 35.51

Low 1,741.89 19.84 29.90 22.86 46.29 169.03 6.35 20.95

% Change YTD 12% 19% 18% 38% 35% 29% 4% 30% 25%

Relative 8% 7% 26% 24% 17% -7% 19% 13%

Dividend $0.84 $1.68 $1.68 $3.32 $1.16

Yield 3.2% 4.4% 4.9% 5.0% 3.6%

Capitalization

Fully Diluted Shares 65,300 46,966 81,862 138,762 57,750 54,386 37,177

Market Capitalization $1,735,674 $1,791,267 $2,781,678 $9,219,347 $13,178,550 $425,842 $1,201,561

Long-Term Debt (624,300) (420,250) (1,316,250) (4,322,687) (3,925,888) (346,469) (581,846)

Working Capital (10,700) (18,432) (7,843) (471,323) 189,511 (4,785) (47,049)

Enterprise Value $2,370,674 $2,229,949 $4,105,771 $14,013,357 $16,914,927 $777,096 $1,830,456

AFFO/Share

AFFO/Share 2016 $141.80 $2.50 $2.40 $2.90 $4.30 $16.50 $1.10 $2.50

Multiple 15 11 16 12 15 14 7 13 13

AFFO/Share 2015 127.20 2.10 2.10 2.60 4.00 15.00 0.90 2.02

Multiple 16 13 18 13 17 15 9 16 14

AFFO/Share 2014 117.52 1.70 1.75 2.42 3.75 13.50 0.66 1.78

Multiple 18 16 22 14 18 17 12 18 17

AFFO/Share 2013 109.48 1.22 $1.67 1.87 3.72 11.77 0.65 1.55

EBITDA

EBITDA 2016 $225,000 $170,000 $310,000 $1,050,000 $1,350,000 $100,000 $143,146

Multiple 11 13 13 13 13 8 13 12

EBITDA 2015 198,000 150,000 290,000 980,000 1,234,000 90,000 121,134

Multiple 12 15 14 14 14 9 15 13

EBITDA 2014 168,000 132,000 268,000 935,000 1,112,000 78,000 97,733

Multiple 14 17 15 15 15 10 19 15

EBITDA 2013 138,700 107,754 237,296 878,901 1,000,898 58,033 75,422

Target Multiple 2015E AFFO 17 20 15 18 17 11

Price Target $36.00 $42.00 $38.00 $70.00 $250.00 $10.00

Upside to Target 35% 10% 12% 5% 10% 28%

Rating: Outperform Outperform Outperform Marketperf Outperform Outperform Not Rated

December 19, 2014

Burke & Quick Partners, LLC.

Equinix, Inc. Page 16 of 18 Frederick W. Moran

DISCLOSURES: ANALYST CERTIFICATION I, Frederick W. Moran, hereby certify that the views expressed in this research report accurately reflect my personal views about the subject securities and issuers. I also certify that no part of my compensation was, is, or will be, directly or indirectly, related to the specific recommendations or views expressed in this research report.

DISCLOSURES Additional information available upon request.

“This report was prepared by Burke & Quick Partners, LLC. (BQP)”

BQP is a Member of FINRA and SIPC.

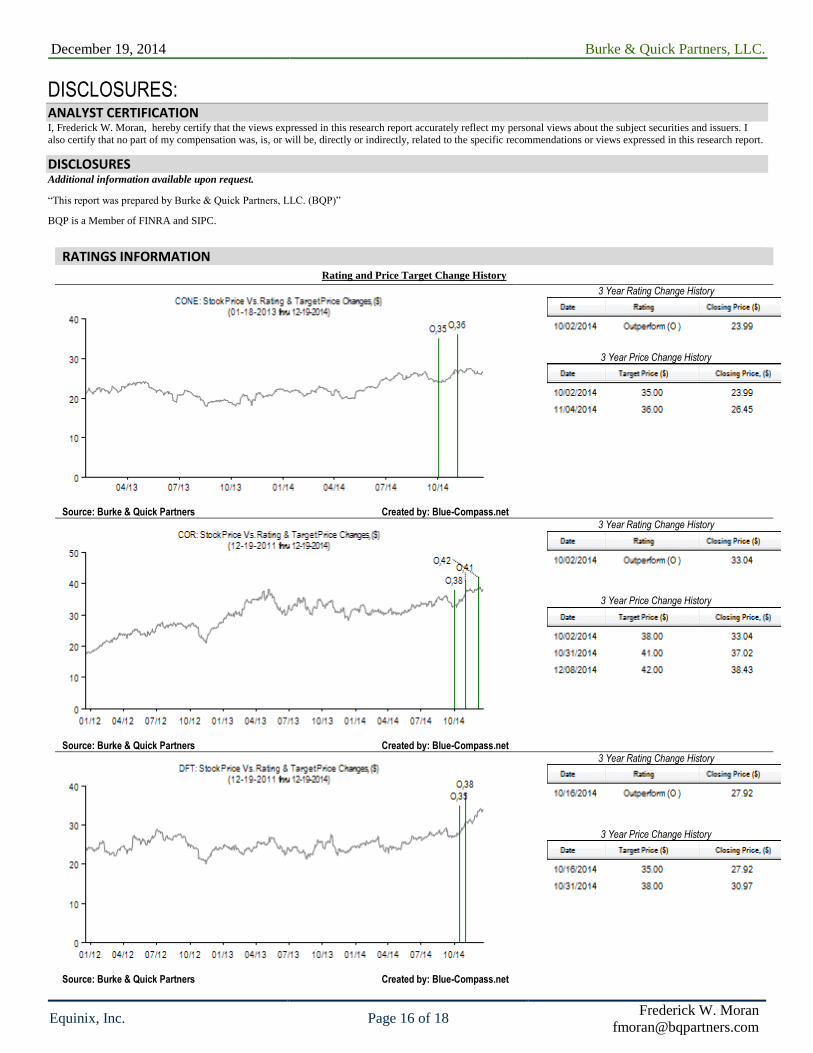

RATINGS INFORMATION Rating and Price Target Change History

Source: Burke & Quick Partners Created by: Blue-Compass.net

3 Year Rating Change History

3 Year Price Change History

Source: Burke & Quick Partners Created by: Blue-Compass.net

3 Year Rating Change History

3 Year Price Change History

Source: Burke & Quick Partners Created by: Blue-Compass.net

3 Year Rating Change History

3 Year Price Change History

December 19, 2014

Burke & Quick Partners, LLC.

Equinix, Inc. Page 17 of 18 Frederick W. Moran

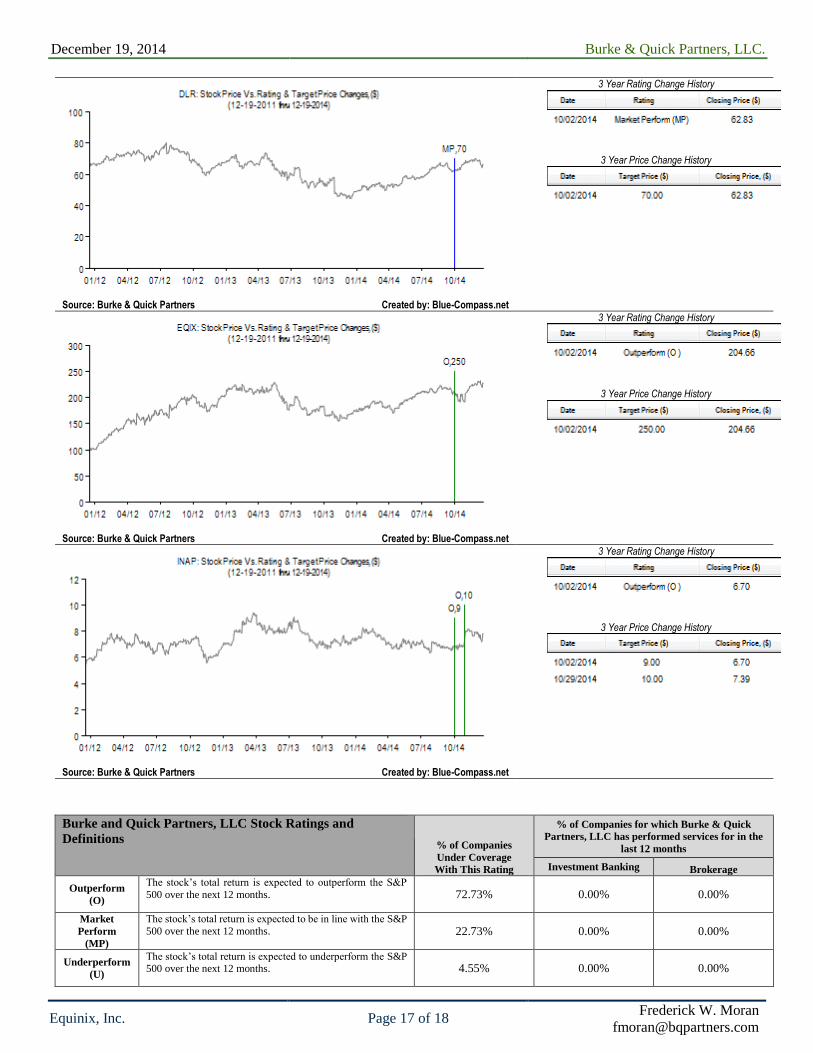

Source: Burke & Quick Partners Created by: Blue-Compass.net

3 Year Rating Change History

3 Year Price Change History

Source: Burke & Quick Partners Created by: Blue-Compass.net

3 Year Rating Change History

3 Year Price Change History

Source: Burke & Quick Partners Created by: Blue-Compass.net

3 Year Rating Change History

3 Year Price Change History

Burke and Quick Partners, LLC Stock Ratings and

Definitions % of Companies

Under Coverage

With This Rating

% of Companies for which Burke & Quick

Partners, LLC has performed services for in the

last 12 months

Investment Banking Brokerage

Outperform

(O)

The stock’s total return is expected to outperform the S&P

500 over the next 12 months. 72.73% 0.00% 0.00%

Market

Perform

(MP)

The stock’s total return is expected to be in line with the S&P

500 over the next 12 months. 22.73% 0.00% 0.00%

Underperform

(U)

The stock’s total return is expected to underperform the S&P 500 over the next 12 months. 4.55% 0.00% 0.00%

December 19, 2014

Burke & Quick Partners, LLC.

Equinix, Inc. Page 18 of 18 Frederick W. Moran

Covered Not

Rated

(CNR)

The stock is covered by the firm but ratings and estimates are

not issued.

![Untitled-1 [myibd.investors.com]INVESTOR'S BUSINESS DAILY How To Find & Own America' Greatest Opportunities s Priceline.com (PCLN) Weekly Chart Sell when goes through channel line](https://static.fdocuments.net/doc/165x107/5e645e76bfa20601136faa71/untitled-1-myibd-investors-business-daily-how-to-find-own-america-greatest.jpg)

![paos.colorado.eduwhan/ATOC5051/Class... · o7Y hbZ3l_¦ WzhioMoO ]Tl W#lnZ3yQ pCln[)Z ^OZ3g ldaic_]wh abkRlnZJr>gn]wldaioOkmo> ^OoOg#lnabcJabl }ZJ Ke$]wldaioOk o7^OZJgzln[Z\Z3kKldaig](https://static.fdocuments.net/doc/165x107/5ec4175830439636b965a184/paos-whanatoc5051class-o7y-hbz3l-wzhiomoo-tl-wlnz3yq-pclnz-oz3g.jpg)