Dark Strategy - - EconIssues – Patrick A McNutt · Dark Strategy “Your words are ... what we...

22

HAPTER HAPTER 7 Dark Strategy “Your words are like the handiwork of my ancestor Daedalus; and if I were the sayer or propounder of them, you might say that this comes of my being his relation and that this is the reason why my arguments walk away and won’t remain fixed where they are placed.” Socrates 07 DS.indd 95 12/5/12 3:00:51 PM

Transcript of Dark Strategy - - EconIssues – Patrick A McNutt · Dark Strategy “Your words are ... what we...

h a p t e rhapter

7

Dark Strategy

“Your words are like the handiwork of my ancestor Daedalus; and if I were the sayer or propounder of them,

you might say that this comes of my being his relation and that this is the reason why my arguments walk away

and won’t remain fixed where they are placed.”Socrates

07 DS.indd 95 12/5/12 3:00:51 PM

CHAPTER SEvEn96

ompetitors know of each other’s existence. The zero- sum constraint is acute. In this context, type is not only about conduct and behaviour; it is also about making decisions, carrying them through and taking action. We may regard the courses of action open to management

as strategies of the firm. A strategy is one firm’s plan of action adopted in the light of management beliefs about the reactions of its competi-tors. In this scenario, for example, a firm’s pricing policy per se may not affect the shareholder value; it will, however, affect the shareholder value through the management’s reaction to the action of a competitor to the original pricing policy.

In other words, management must understand that action leads to a reaction that further requires a reply. Every action must have a (nash) reply. This hypothesis is maintained throughout the book. It simply means that management should not be surprised by events in time period t+1 that emanate from their action in time period t. As with our opening example in Chapter 1 on the possible launch of a gPhone ahead of the launch of an iPhone, the signal on the possibility of a gPhone in the market-as-a-game is called a moon-shot. A moon-shot is a signal that players deny, but if one player believes the moon-shot to be credible then they are observed as acting sooner than the cost technology or capacity may have facilitated at time period t. It is worth pointing out that the gPhone was launched only in September 2008. But was the iPhone released too soon, in the summer of 2007?

Answers to this type of question fall into the unknown of strategic behaviour, what we refer to as dark strategy. Will nokia enter the laptop market? Will Dell enter the smartphone market? These were challenging questions as at September 2009, answers to which could, in part, be accommodated within Framework Tn=3. By observing type, by understanding the convergence of technologies, players would be in a better position to consider the market that they should be in at time period t+1.

Mistake-proofingThe issue of launching ‘too soon’ depends on the inherent cost tech-nology of the player to ensure that they do not have capacity constraints

CC

07 DS.indd 96 12/5/12 3:00:51 PM

DARk STRATEgy 97

Chapter1 Strategic Reasoning

on the launch of the product. But a greater risk, in the absence of a nash reply, is that competitors can secure a second mover advantage by emulating the original players’ functionalities. nokia, for example, is in a strong position to secure a second mover advantage in the evolving smartphone market. By differentiating between music content with xPress models, focusing on the more professional users with n-series and E-series phones, and focusing on time period t+2 with mobile Internet, nokia can secure that competitive advantage provided Apple Inc are not surprised.

Player strategy is when management realise that they are in a game. In economics, rational man makes optimal choices guided by well-defined and stable preferences. There are preferences on costs – marginal cost pricing, ABC costing and incremental costs. Management are faced with a supply correspondence dilemma: on one hand there are competitors squared off against cyclical consumer preferences, the Penrose effect squared off against internal x-inefficiencies and costs squared off against price positioning. There will be capacity constraints in what is traditionally referred to as the short-run problem coupled with planning horizon issues in the long run. Making a decision has to translate into taking an action. It is not easy. For example, planned obsolescence, productivity and niche batch production characterise the production technology of many firms. Endogenous rivals whose type may be unknown at a given time period may emerge, and the nash premise becomes more acute — the essence of modern competition.

Belief System CV ≠ 0For management there are tensions between economic routine and argument and the desire to follow one’s own instinct in business matters. The company may have a smaller asset base but be generating greater pre-tax profits; hence it is making more profit from the same level of assets as its near-rival, and this will be reflected in the stock market as the company’s being observed to outperform its near-rival. It is important for management to learn the lesson that the best player in terms of profitability and performance measures is not necessarily the biggest player in the market. And the biggest player is not necessarily

07 DS.indd 97 12/5/12 3:00:52 PM

CHAPTER SEvEn98

the best. The belief system is captured by the conjectural variation [Cv] in the following way. If player A has a Cv = 0, then they do not expect a reaction from a competitor; conversely, with a non-zero Cv a player does expect a reaction to their action in a game.

It is this that distinguishes between knowing that a decision has to be made and knowing when and how to make that decision. knowing that a decision has to be made is referred to as making a decision; knowing when and how a decision has to be made is referred to as taking an action. The latter term is analogous to making a move as understood in game theory, that is, the players make their moves when they actually decide on the strategy to be adopted. In brief, a strategy is a string of moves or actions.

Therefore, management’s subjectivity is an essential property; it refers to management’s sense of past, present and future, which makes management at once a creature of history. Simon (1958) and the behav-ioural approach have argued that management are bounded rational in decision making, while Penrose (1958) has argued that management are limited in their abilities. Both subscribe to a view that management are exposed daily to complex information, reliant on subordinates to inform them of the precise usefulness of pieces of information. nonetheless, management must take the first step in decision making. In taking the first step they can apply their knowledge as management guided by ‘laws’ of individual behaviour and linked to other rival management by the game and to internal management by the organisational structure of the company. It is this coalescing of the links reminiscent of Poincare’s ‘collision of ideas’ that yields something new in a company and a degree of unpredictability for observers of patterns of behaviour. Simple ideas generate more complex ideas, and simple actions generate more complex actions, through a process of vertical blending, whereby the type of management blends with the type of player.

Behaving Strategically From first principles we could define the economics of strategy as a combination of the Penrose effect (PE) and the nash premise (nP). The latter simply requires a player to have a reply function, anticipating

07 DS.indd 98 12/5/12 3:00:52 PM

DARk STRATEgy 99

the likely reaction from the player’s action. In their pursuit of growth, for example, management come to realise that a growth rate implies specific costs of growth and trade-offs. In Mueller’s (1972) life cycle interpretation of firm growth, desired growth is often limited by both internal and external constraints. Internally, there are Penrose limitations on the ability of management to achieve growth, and this is coupled with external constraints in a zero-sum market where growth of the firm slows down. Management do not wish this to happen.

Costs are committed to maximising growth, and management inse-curity about the impact of the zero-sum constraint could push their motives so far as to dilute the market value of the company suffi-ciently to create a reverse risk of takeover. Understanding the type of management of the competitor becomes crucial in this story. Once management take cognizance of a rival competitor’s interdependence, management have become a player in a game and decisions are said to be strategic. Management behave strategically when they come to understand that each and every decision is followed by an action that is observed by the market participants. This gives us a definition of the strategy equation:

S = PE + nP

It is a combination of minimising the Penrose effect and ensuring one has a response to any reaction to one’s initial decision in a game. The Penrose effect can be minimised by understanding type, and with a non-zero conjectural variation the player has anticipated a reaction. Ideally, we as third party observers — the fact finders — would like to understand how the decision was achieved and, for each alternative in the decision-making process, to understand why it was rejected, and by whom. In other words, we need to understand the context of the decision-making behaviour. The management of competitors would like to know this as well, but particularly they would need to understand the history of the actions for each of the market participants in the decision-making process. The play of a firm consists of a detailed description of the firm’s activities in carrying out its move. This is discussed in Chapter 9 through the reaction functions. If A and B were to move to a price

07 DS.indd 99 12/5/12 3:00:52 PM

CHAPTER SEvEn100

war, for example, their play would be a description of their actions, but the intriguing question is how they made the decision to engage in a price war.

It is by knowing when and how to make a decision for each player that a description may be forthcoming. But rivals will do everything to keep one another guessing. Interpreting management as participants in a game is nothing new. However, in this book we have approached management as participants from a different angle by introducing the significance of type in understanding management behaviour and company strategy in product and service markets, in local, national and global markets. The focus on type is a key driver to understanding actual, observable behaviour. The behaviour translates into a conflict of subjective outcomes in a non-cooperative market wherein management as individuals compete against each other for market share; however, they keep each other guessing on the next action.

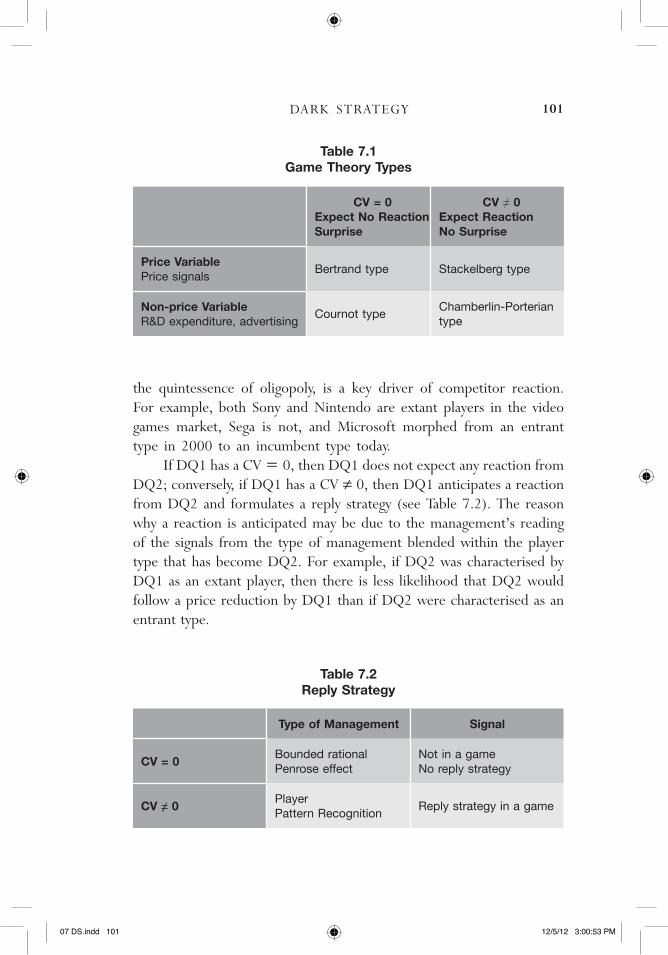

Key Decision Makers: Decision QuantumThe blending of management type and player type creates a decision quantum (DQ), that is, the individual or group of individuals that make decisions or take action or both. The blending of management type and player type is supported by the property of conjectural variation (Cv). The earliest models of oligopolistic behaviour assumed that firms formed expectations about the reactions (or variations) of other firms, called conjectural variations. The Cournot, Bertrand and Stackelberg models can be interpreted as conjectural variation types (see Table 7.1). The quantum is composed of management type and firm, as they morph into one game-playing entity, the player. If a player per se finds itself in a market with fewer than five competitors, it behoves management to identify each rival as a type of player. At its simplest, all players are incumbents in the smallest bounded market and any new player wishing to enter that market is an entrant type. Post-entry, the entrant type evolves into an incumbent type and the blending of management type with entrant-turned-incumbent player type begins to unfold. The player is an extant (still existing) type. This becomes more acute in a market where the number of players is less than five, where interdependence,

07 DS.indd 100 12/5/12 3:00:53 PM

DARk STRATEgy 101

the quintessence of oligopoly, is a key driver of competitor reaction. For example, both Sony and nintendo are extant players in the video games market, Sega is not, and Microsoft morphed from an entrant type in 2000 to an incumbent type today.

If DQ1 has a Cv = 0, then DQ1 does not expect any reaction from DQ2; conversely, if DQ1 has a Cv ≠ 0, then DQ1 anticipates a reaction from DQ2 and formulates a reply strategy (see Table 7.2). The reason why a reaction is anticipated may be due to the management’s reading of the signals from the type of management blended within the player type that has become DQ2. For example, if DQ2 was characterised by DQ1 as an extant player, then there is less likelihood that DQ2 would follow a price reduction by DQ1 than if DQ2 were characterised as an entrant type.

Table 7.2Reply Strategy

Type of Management Signal

CV = 0Bounded rational Penrose effect

Not in a gameNo reply strategy

CV ≠ 0PlayerPattern Recognition

Reply strategy in a game

Table 7.1Game Theory Types

CV = 0 Expect No Reaction Surprise

CV ≠ 0 Expect Reaction No Surprise

Price Variable Price signals

Bertrand type Stackelberg type

Non-price Variable R&D expenditure, advertising

Cournot typeChamberlin-Porterian type

07 DS.indd 101 12/5/12 3:00:53 PM

CHAPTER SEvEn102

Our treatment here is concerned with management acting only as DQs rather than as individuals, each DQ attempting to predict the actions of other DQs but not cooperating explicitly with them. This really is about management team interaction. It assumes no cooperation, but the outcome may sometimes be interpreted as implicit cooperation between the DQs. Take the example of DQ1 reducing price with a Cv ≠ 0; DQ2 follows with Cv ≠ 0, and DQ1 replies in what appears to a fact finder as a sequencing of price tumbles.

Players will either adopt a binary approach or not. In the Marris type, there is an inherent threat of takeover, and it is this threat that influences management to take action, for example, to engage in share buy-back or payment of generous dividends. There is empirical evidence to support the view that share price movements are correlated with dividend payments. Competitors would observe and may infer a Marris-type strategy based on an aggressive dividend policy within the company. An aggressive dividend policy carries with it the opportunity cost of funds not spent on more R&D, as well as lower growth for the company and the possibility of reduced future dividends. The business model works until the company is no longer on a balanced growth path, that is, unable to differentiate products or to innovate due to lack of funds at a time when the share price is increasing in the expectation of a change to the business model.

It is useful to address the issue of risk as understood from the premise that management are risk-averse but that being risk-averse does not preclude the taking of risks. In the context of game strategy there is a burden of loss in the interpretation of strategy in the context of actually playing the game with rival management. Otherwise, the interpretation of risk falls back on the issue of whether it is judicious for management to play the game. Indeed, it may be the case that management do opt not to play or that the understanding of type is wholly inappropriate for some managements and their respective firms. The latter could define management who, in effect, increase volume in order to maximise sales revenue, cut prices and largely ignore the presence of other firms. It may be a Baumol type.

The management philosophy known as kaizen has captured the attention of management over the past 30 years. It is a generic term

07 DS.indd 102 12/5/12 3:00:53 PM

DARk STRATEgy 103

incorporating numerous management techniques with a promise of increased productivity coupled with a reduction in inventories, errors and lead times with radical realignment of the production technology. Described by Imai (1986) as “the basic philosophical underpinning for the best in Japanese management”, kaizen has emerged as a process-oriented, customer-driven strategy for corporate success (1986). It has given management the capability to quickly adopt and adapt their manu-facturing processes to changing customer and market requirements. Management terms such as TQM, JIT, kamban and the 5-S programme are process-oriented concepts.

Poka-yoke and the nth RootThere is a lesser-known term that goes to the heart of our discussion of type and strategy: known as mistake-proofing or ‘poka-yoke’, it is adaptable as a concept to understand management type and risk (see Table 7.3 on the following page). Management by nature are risk-averse, but being risk-averse, does not preclude the taking of risks. Indeed, the risk, however quantified, has an opportunity cost of real resources, and the management team has to balance that cost with the possible gains. gains from, say, launching a new product, exciting an episodic price war or relocating a plant may be forthcoming. The risk element is to be interpreted in terms of management as a player finally adopting a contingency plan to complement whatever motive is driving their action. The strategy adopted is observed by competitors as an action. So, for example, whether or not to launch a new product is a binary choice: launch the product or do not launch the product, in the latter case parking its launch until later. Either way, the competitor can interpret the action and draw inferences about the type of management. If the expected return for not launching the product, E(r

A), is greater than

the expected return for launching the product, E(rB), management take

the risk and delay the product launch at this juncture. To understand this, we need to realise that the E(r

A) is computed as

the nth-root of the different risks as perceived by the player. If a player decides not to launch a product, the opportunity cost of lost revenue, for example, is a risk r

1 that has to be balanced against the opportunity

07 DS.indd 103 12/5/12 3:00:54 PM

CHAPTER SEvEn104

cost of resources devoted to producing a product that might fail, r2,

resources that could be used elsewhere within the firm, r3, or indeed in

R&D expenditure on a different type of product, r4. But one additional

factor in computing that risk is the likely reaction from a competitor. If a player, for example, adopts a strategy, call it strategy 1 (S

1), then we

would ordinarily associate a risk, r1, with that strategy play. However,

in order to integrate poka-yoke into that strategy, we would have to associate a row vector of risks, R, such that R = (r

1, r

2, … r

n); and for

each ri there is an expected return E(r

i), so that management as a player

adopting a poka-yoke position in trying to ensure mistake-proofing compute the nth-root of √{E(r

1) + E(r

2) + E(r

3) + … + E(r

n). The

action that is S1 is contingent on r

1 with an nth-root expected return.

Across the strategy set, S, there are S1 to S

n, and the strategy with the

maximum return as computed with the nth-root formula is the adopted strategy. The choice is binary, that is, management as a player will choose strategies from a set of strategies and can refer back to historic E(r) for any related strategy.

Burden of Loss StandardThe complexity of the strategy set mirrors the complexity of playing the game; there is a burden of loss standard that impinges on manage-ment in adopting mistake-proofing or ‘poka-yoke’. In other words, the burden of loss standard requires management to minimise the firm’s exposure to loss. In many respects the interpretation of strategy is in the context of actually playing the game with rival management,

Table 7.3Poka-yoke

Make a Decision Take an Action

Knowing thatNo error in the game No surprise signal

Poka-yokeMoon-shot is credible

Knowing how Knowing when

Poka-yoke Lost first mover advantage

No error in the game No surprise Nash reply

07 DS.indd 104 12/5/12 3:00:54 PM

DARk STRATEgy 105

while the interpretation of risk falls back on the issue of whether it is judicious for management to play the game. Making a decision, and knowing that a decision has to be made, are crucial. As noted, it may be the case that management decide not to play a game per se but proceed with business. Whether this happens or not depends on management type, technology and time. In a world where manage-ment can influence rivals’ actions by their type, a reliance on profit maximisation or shareholder value as the key driver of management behaviour may no longer seem reasonable. Making a decision, and knowing that a decision has to be made, is crucial.

Management in oligopoly markets find themselves coming closer to the rhythm and pattern of real price movements. Prices are no longer arbitrarily guided by a march towards the Holy grail of a perfectly competitive price. Rather, prices fall into a pattern that pervades the market for products, and management have to redeem themselves through their behaviour in the firm. Management’s rational nature can help management decide to accept the reality or to change the pattern of observed behaviour through their own actions and reac-tions in the market. The economic price standards appear arbitrary or are imposed by institutions without any reference to the right reason or the preferences of management. There are price opposites of the perfectly competitive equilibrium, for example a cartel-like price, which can be turned into a negative signal (quaternity) when included with monopoly and dominant positions. So in this view, the business world management, robbed of their rationality, must avoid a cartel price or monopoly position because otherwise their behaviour will be constrained and retarded by external factors.

Strategy SetA fact finder may observe play in a market by observing management actions, but for management the situation is more complex. Observed behaviour may not be repeated, or, as in our fictitious example, player A may not have expected a reaction from B because in the past B did not react. This is a crucial point in understanding the relevance of management type to a meaningful and pragmatic definition of strategy.

07 DS.indd 105 12/5/12 3:00:54 PM

CHAPTER SEvEn106

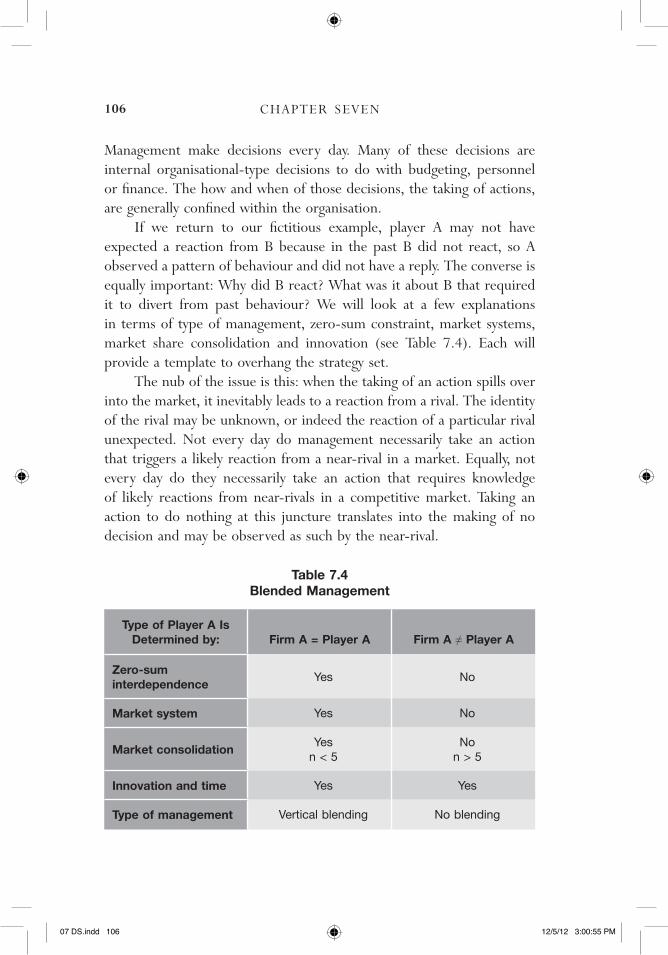

Management make decisions every day. Many of these decisions are internal organisational-type decisions to do with budgeting, personnel or finance. The how and when of those decisions, the taking of actions, are generally confined within the organisation.

If we return to our fictitious example, player A may not have expected a reaction from B because in the past B did not react, so A observed a pattern of behaviour and did not have a reply. The converse is equally important: Why did B react? What was it about B that required it to divert from past behaviour? We will look at a few explanations in terms of type of management, zero-sum constraint, market systems, market share consolidation and innovation (see Table 7.4). Each will provide a template to overhang the strategy set.

The nub of the issue is this: when the taking of an action spills over into the market, it inevitably leads to a reaction from a rival. The identity of the rival may be unknown, or indeed the reaction of a particular rival unexpected. not every day do management necessarily take an action that triggers a likely reaction from a near-rival in a market. Equally, not every day do they necessarily take an action that requires knowledge of likely reactions from near-rivals in a competitive market. Taking an action to do nothing at this juncture translates into the making of no decision and may be observed as such by the near-rival.

Table 7.4Blended Management

Type of Player A Is Determined by: Firm A = Player A Firm A ≠ Player A

Zero-sum interdependence

Yes No

Market system Yes No

Market consolidationYes

n < 5No

n > 5

Innovation and time Yes Yes

Type of management Vertical blending No blending

07 DS.indd 106 12/5/12 3:00:55 PM

DARk STRATEgy 107

Today, for the majority of companies, the management team has to evaluate the risks associated with market participation. They can indeed integrate and adopt mistake-proofing or a ‘poka-yoke’ into their decision making: management evaluate the risks, decide to play the game and become players, and thus proceed to adopt strategies accordingly.

The important element in all of this is that management are risk-averse, implying that they evaluate the risks, take the risk with the greatest expected return and enter the market as strategic players. non-participation, or admission that strategic behaviour is inapplicable to one’s firm, is, in and of itself, a strategic decision, whether the management wish to concede that point or not to the other market rival participants. It is the nature of the market-as-a-game that another firm will interpret that decision strategically — it may signal, for example, old traditional management styles, it may suggest a possibility of poaching market share, it may signal a lack of R&D expenditures or whatever. But the management who opt not to participate have to take some responsibility for that decision should it inevitably leave the firm exposed to the vagaries of strategic game play, playing catch-up in a rapidly changing business world. This would be close to the concept of short-termism and could probably best characterise a type traditionally referred to as ‘risk-averse management’.

Z or Third VariableThe importance of poka-yoke is to minimise errors by identifying a mistake. Ellsberg (1961) has shown that individuals express preferences for bets with known probabilities over bets with unknown probabilities. In order to minimise opportunity cost in any trade-off between variables X and y, management have a third variable, Z, so that they are prepared to trade different pairs of X and y provided Z remains at least constant in time period t and increases in time period t+1. Pairs of X and y, for all n variables, (X1,y1) … (Xn,yn), translate into a business strategy: more profits and less revenues, or less costs and more profits. A business strategy requires action. Rational management prefer strategies yielding higher values for Z, and are indifferent between strategies yielding equal values. If by lowering costs in time period t management can realise a

07 DS.indd 107 12/5/12 3:00:55 PM

CHAPTER SEvEn108

higher value of Z, then the observed strategy will be a lowering of costs. keeping to type affords management a degree of certainty, a probability that the trade-off between X and y will deliver a Z-result.

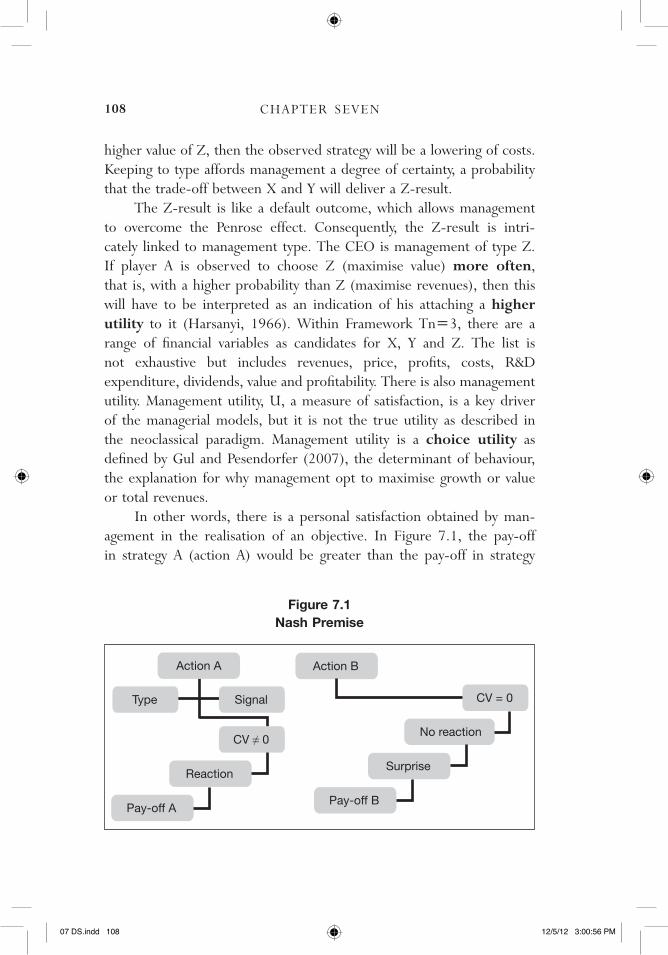

The Z-result is like a default outcome, which allows management to overcome the Penrose effect. Consequently, the Z-result is intri-cately linked to management type. The CEO is management of type Z. If player A is observed to choose Z (maximise value) more often, that is, with a higher probability than Z (maximise revenues), then this will have to be interpreted as an indication of his attaching a higher utility to it (Harsanyi, 1966). Within Framework Tn=3, there are a range of financial variables as candidates for X, y and Z. The list is not exhaustive but includes revenues, price, profits, costs, R&D expenditure, dividends, value and profitability. There is also management utility. Management utility, U, a measure of satisfaction, is a key driver of the managerial models, but it is not the true utility as described in the neoclassical paradigm. Management utility is a choice utility as defined by gul and Pesendorfer (2007), the determinant of behaviour, the explanation for why management opt to maximise growth or value or total revenues.

In other words, there is a personal satisfaction obtained by man- agement in the realisation of an objective. In Figure 7.1, the pay-off in strategy A (action A) would be greater than the pay-off in strategy

Figure 7.1 Nash Premise

Action A

Signal

CV ≠ 0

Reaction

Pay-off A

Action B

CV = 0

No reaction

Surprise

Pay-off B

Type

07 DS.indd 108 12/5/12 3:00:56 PM

DARk STRATEgy 109

B (action B) if the non-zero Cv was correct. Management are not surprised by the reaction of a competitor; although it is critical to be in a position to identify competitors, the near rival, that competitor who has the greatest probability of reacting first to one’s action, is the main competitor. In other words, in a business framework described by technology and time, the identity of the nearest rival becomes more critical and more difficult in the absence of understanding signalling of player type. A first response would be to construct a critical timeline of competitor signals over a period of time.

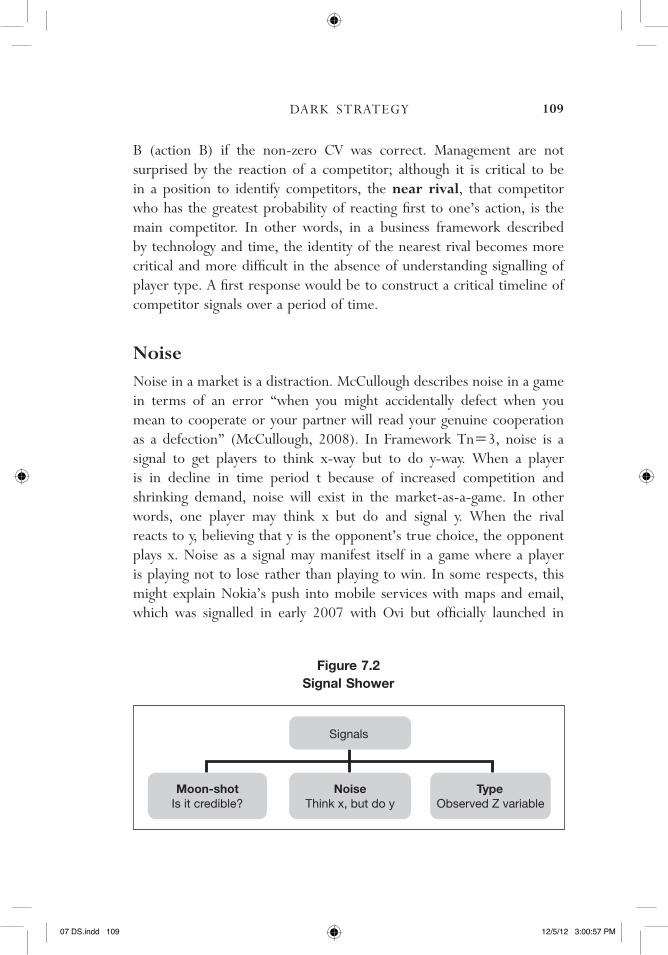

Noisenoise in a market is a distraction. McCullough describes noise in a game in terms of an error “when you might accidentally defect when you mean to cooperate or your partner will read your genuine cooperation as a defection” (McCullough, 2008). In Framework Tn=3, noise is a signal to get players to think x-way but to do y-way. When a player is in decline in time period t because of increased competition and shrinking demand, noise will exist in the market-as-a-game. In other words, one player may think x but do and signal y. When the rival reacts to y, believing that y is the opponent’s true choice, the opponent plays x. noise as a signal may manifest itself in a game where a player is playing not to lose rather than playing to win. In some respects, this might explain nokia’s push into mobile services with maps and email, which was signalled in early 2007 with Ovi but officially launched in

Figure 7.2Signal Shower

Signals

Moon-shotIs it credible?

NoiseThink x, but do y

TypeObserved Z variable

07 DS.indd 109 12/5/12 3:00:57 PM

CHAPTER SEvEn110

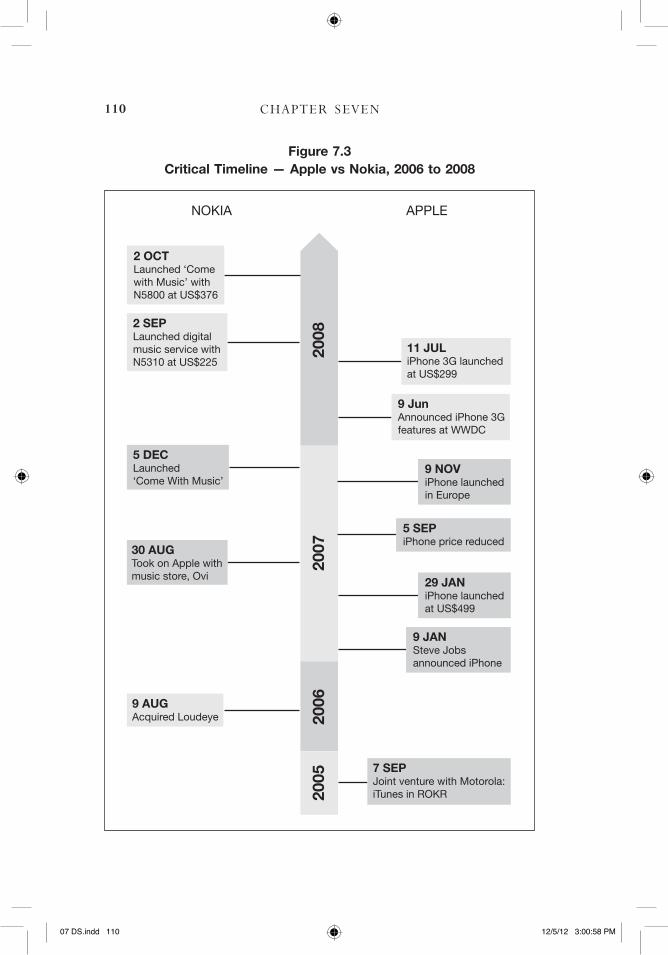

Figure 7.3Critical Timeline — Apple vs Nokia, 2006 to 2008

NOKIA APPLE

9 AUGAcquired Loudeye

5 DECLaunched ‘Come With Music’

30 AUGTook on Apple with music store, Ovi

2 OCTLaunched ‘Come with Music’ with N5800 at US$376

2 SEPLaunched digital music service with N5310 at US$225

7 SEPJoint venture with Motorola: iTunes in ROKR

9 NOViPhone launched in Europe

5 SEPiPhone price reduced

29 JANiPhone launched at US$499

9 JANSteve Jobs announced iPhone

11 JULiPhone 3G launched at US$299

9 JunAnnounced iPhone 3G features at WWDC

2007

2008

2005

2006

07 DS.indd 110 12/5/12 3:00:58 PM

DARk STRATEgy 111

early 2009 as Ovi Maps and Ovi Mail. Ovi has been described in tech-nology magazines as “a hub that integrates mobile services between handsets and PCs” (The Economist, 6 December 2008).

nokia has a reputed worldwide market share of 40 per cent in handsets. In order to protect that market share — so that it does not fall, say, to 30 per cent — nokia is creating noise by signalling a stra-tegy that focuses not on growth of handsets per se but on the services it provides.

Motorola’s launch of the clamshell mobile phone design in the 1990s may well have been noise in the emerging game for dominance in handsets.

Noise in a Tumbling PriceIn the market for mobile phones, both price and non-price character-istics are important in the game. Price falls can signal a Baumol type, and if players believe that there is a Baumol type in a game, price should not fall below the trigger price because net total revenue accruing to any player would fall. A rival, observing no price fall, believes that no player is a Baumol type. So no player reduces price and no player knows that there is a Baumol type, so no player moves on reducing price. This is a paradox.

If a player knows that the rival believes that the player is not a Baumol type, then price will not be increased above the trigger price because net total revenue accruing to the player would fall. Consequently, it is only when the player knows that the rival knows that the player is a Baumol type that the player will reduce price, but it is the action of reducing price (if present price is above the trigger price) that reveals the true identity of the player as a Baumol type.

Within the elastic range, a high prevailing price can be maintained to maximise profits in a concentrated market with fewer than five players. Any action by a player to reduce price (in order to recoup lost revenues) could be interpreted as a price signal from a Baumol type and is unlikely to precipitate a price reaction, if the rival knows that the player is a Baumol type, and price should only fall to the level of the Baumol type’s trigger price floor (refer to Figure 3.2 in Chapter 3).

07 DS.indd 111 12/5/12 3:00:59 PM

CHAPTER SEvEn112

yet, if no player reduces price, prices will not tumble. For example, nokia and Apple could succumb to this paradox of a tumbling price, in that as price falls in order to compete, the trigger price, activated by changing fickle consumer preferences for more functionalities, embeds a sequentially lower bound on the market price. As the game unfolds, the market price could fall to zero. The n97, for example, was launched in the United kingdom in October 2008 at zero price. As that happens, a greater demand for functionalities is creating an inelastic demand that would warrant a price increase in time. Identifying patterns in observed signals is necessary in order for each player to isolate a rival’s strategy as a string of price moves across the CTL. It is imperative that patterns are identified in the market-as-a-game, wherein innovation, rapid product development, technology and the demand for functionalities define the game dimension.

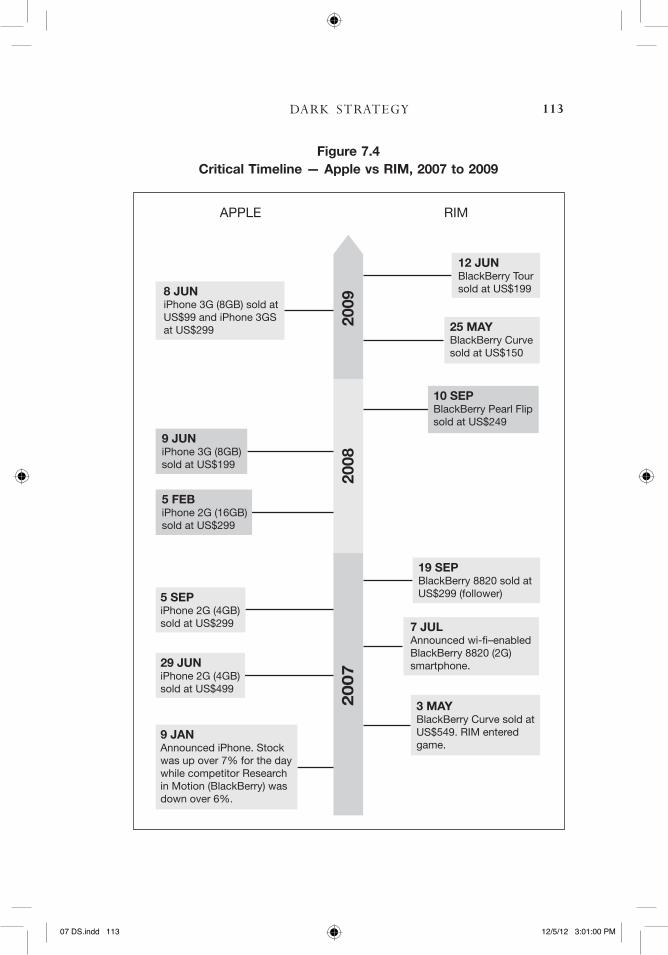

The significance of technology is reflected in the Apple versus RIM critical timeline in 2009 (see Figure 7.4). The competing products are differentiated by functionality (2g or 3g), but not by network. The market-as-a-game exhibits a range of observations, for example, Sony Ericsson smartphones target games fans, and in a bid to distinguish itself from rival mobile firms, Sony Ericsson is used PlayStation technology for its 2009 products. The HTC Touch was popular in Asia because it was cheaper than the iPhone and can be used on a variety of cellular networks.

The Mistakes of Dark StrategyManagement are used to dealing with incomplete information, and they make decisions daily out of uncertainty. Increasingly, new technology is presenting new challenges to management, and decision making is constrained by the kinetic equation dT/dt = –1. Across their suite of products and services there is at least one product or service market that is evolving into a market-as-a-game, and thus it behoves manage-ment to play the signalling game. Dark strategy facilitates mistake- proofing in the market-as-a-game that management already believe in, and the critical issue is the observed action of a competitor.

Strategy is a string of moves. Dark strategy refers to how manage-ment act, having observed the moves of a competitor while being aware

07 DS.indd 112 12/5/12 3:00:59 PM

DARk STRATEgy 113

Figure 7.4Critical Timeline — Apple vs RIM, 2007 to 2009

APPLE RIM

5 FEBiPhone 2G (16GB) sold at US$299

29 JUNiPhone 2G (4GB) sold at US$499

5 SEPiPhone 2G (4GB) sold at US$299

9 JANAnnounced iPhone. Stock was up over 7% for the day while competitor Research in Motion (BlackBerry) was down over 6%.

8 JUNiPhone 3G (8GB) sold at US$99 and iPhone 3GS at US$299

9 JUNiPhone 3G (8GB) sold at US$199

3 MAYBlackBerry Curve sold at US$549. RIM entered game.

25 MAYBlackBerry Curve sold at US$150

10 SEPBlackBerry Pearl Flip sold at US$249

7 JULAnnounced wi-fi–enabled BlackBerry 8820 (2G) smartphone.

19 SEPBlackBerry 8820 sold at US$299 (follower)

12 JUNBlackBerry Tour sold at US$199

2008

2009

20

07

07 DS.indd 113 12/5/12 3:01:00 PM

CHAPTER SEvEn114

that the competitor not only observes the action as a reaction but also knows that management are observing them. The sequence of observed moves can be plotted as a CTL as illustrated by Figures 7.3 and 7.4. The key to unlocking a sustainable competitive advantage is in deter-mining a pattern in the observed moves, a pattern that management believe will be repeated if they act. By plotting a CTL as the game unfolds, management will see a pattern emerging, and they will see a string of moves that defines the strategy of a competitor. Management could also use the pattern to engage in a process called backward induction, whereby they plot, based on their belief system about competitors, the likely future outcome should they act now. It is as if Apple Inc in 2007 in Figure 7.4 could have predicted the likely reaction from Blackberry in 2008, and, with that knowledge in the market-as-a-game, play the game differently in 2007 to obtain a competitive advantage.

Near-rival CompetitorThere are many competitors in the market but the one that is more likely to react first in the market-as-a-game is referred to as the near-rival competitor. Management who adopt dark strategy are secure in the market-as-a-game. Security in Framework Tn=3 is ascribed to management who avoid the three mistakes of strategy. In a signalling game, secure management is convinced that they will persuade the competitor to choose the correct action and the competitor trusts the secure management sufficiently to act. The duration of the signal-ling cycle at t = T will depend on whether Player B, the competitor, expects Player A to prefer Player B to act if signalled. A near-rival is that competitor who will not hesitate to act if its only alternative is to acquiesce with Player A. In other words, a near-rival is that competitor who, with positive probability, will react first at t = k < T to the action from Player A at t = k. However, if at t = k < T, competitor C does not react and it is the case that Player A knows that the competitor C knows that reaction will at least lead to tumbling prices and a possible zero-price equilibrium at t = T, then Player A can assume that competitor C is not a near-rival at t = k < T.

07 DS.indd 114 12/5/12 3:01:00 PM

DARk STRATEgy 115

First Mistake: Zero-Price OutcomeThe type of a player that is signalled embodies some, but not all, of the decision-relevant private information. Player type is signalled by all players, allowing any one player to observe a common signal in the action of an individual player and to retain a private signal as noise or a moon-shot.

The private signal allows management the flexibility to react. Both technology and time are significant due to the curse of differentiation created by technology and the dT/dt = –1 kinetic equation respectively (see Chapters 1 and 2). A small but non-zero number of players of Bertrand type with Cv = 0 proceed to reduce price in the belief that there will be no reaction from a near-rival — but there is a reaction. This is a mistake that reflects a lack of understanding of the game and could result in a zero-price equilibrium outcome. If a player incurs such a mistake, then the player could update their belief system on hindsight. To this mistake, dark strategy ascribes a solution in the origin of management beliefs.

Second Mistake: Failed ExecutionA second mistake occurs with a Stackelberg type player with a non-zero Cv but fails in the execution of the strategy. The executable strategy should weigh more in favour of the signals than any prior signal on observed action. In the Razr example, any Reduction in Price in 2004 should have discounted a 4gB iPod at $199 at t = T. Management are in a Bayesian game (vives, 2005), when the weight attached by management to prior observed actions at t = T is greater than that attached to the signals at t = T. Bayesian type management see what they want to see and ignore the signals. To this mistake, dark strategy ascribes a solution in significance of signals.

The demise of Motorola’s Razr is a good example of the second mistake, where Motorola management took the fashionable, highly inelastic US$400 Razr mobile phone in early 2000 (t = k), mass produced it and flooded the market with it at a lower price. Sales fell sharply, although Motorola are in the ascendancy in 2012 with the recently launched Motorola Razr i Smart phone.

07 DS.indd 115 12/5/12 3:01:01 PM

CHAPTER SEvEn116

Third Mistake: Lagged DifferentiationThe third mistake of dark strategy occurs when management adopt new technology or product functionalities at time period t = k < T and they either rush to mass produce at t = T and the product fails or the firm experiences excess capacity at t = T when consumers baulk at the new product and sales fall below optimal production levels. Consumers have time-dependent preferences: they do not know what they want at t = T, but if it is available at time period t = k < T, then they will buy it but in insignificant numbers until the technology has gained an externality in use. To this mistake, dark strategy ascribes a solution in playing a game not to lose (second mover advantage) rather than in playing to win. With x per cent market share at t = k < T, a player plays not to lose in order to avoid (x – 1)% at t = T. Management, too, often play to win (x + 1)% at t = k < T, but end up with (x – 1)%.

07 DS.indd 116 12/5/12 3:01:01 PM