D.A. Davidson Ninth Annual Engineering & …s2.q4cdn.com/910306481/files/doc_presentations/2010/D.A....

17

Bill Utt – Chairman, President and CEO Sue Carter - Senior Vice President and CFO September 28, 2010 D.A. Davidson Ninth Annual Engineering & Construction Conference Page 1 of 16

Transcript of D.A. Davidson Ninth Annual Engineering & …s2.q4cdn.com/910306481/files/doc_presentations/2010/D.A....

Bill Utt – Chairman, President and CEO

Sue Carter - Senior Vice President and CFO

September 28, 2010

D.A. Davidson Ninth AnnualEngineering & Construction Conference

Page 1 of 16

Forward Looking StatementsThis presentation contains “forward-looking statements.” All statements other than statements of historical fact are, or may be deemed to be, forward-looking statements. Forward-looking statements include statements about the benefits of the split-off, the discussions of KBR’s business strategies and KBR’s expectations concerning future operations, profitability, liquidity and capital resources. You can generally identify forward-looking statements by terminology such as “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,”“forecast,” “goal,” “intend,” “may,” “objective,” “plan,” “potential,” “predict,” “projection,” “should” or other similar words. These statements relate to future events or future financial performance and involve known and unknown risks, uncertainties and other factors that may cause actual results, levels of activity, performance or achievements to differ materially from those in the future that are implied by these forward-looking statements. Many of these factors cannot be controlled or predicted. These risks and other factors include those described under “Risk Factors” in KBR’s Annual Report on Form 10-K dated February 25, 2010, Forms 10-Q, recent Current Reports on Forms 8-K, and other Securities and Exchange Commission filings. Those factors, among others, could cause KBR’s actual results and performance to differ materially from the results and performance projected in, or implied by, the forward-looking statements. As you read and consider this presentation, you should carefully understand that the forward-looking statements are not guarantees of performance or results. KBR cautions you that assumptions, beliefs, expectations, intentions and projections about future events may and often do vary materially from actual results. Therefore, KBR cannot assure you that actual results will not differ materially from those expressed or implied by forward-looking statements.

The forward-looking statements included in this presentation are made only as of the date of this document. New risks and uncertainties arise from time to time, and KBR cannot predict those events or their impact. KBR assumes no obligation to update any forward-looking statements after the date of this presentation as a result of new information, future events or developments, except as required by the federal securities laws.

Page 2 of 16

KBR – A Leading Global E&C Provider

* For contracts that contain both fixed-price and cost-reimbursable components, KBR classifies the components as either fixed-price or cost-reimbursable according to the composition of the contract, except for smaller contracts that are characterized on the predominate component.

» Revenue: Full Year 2009 - $12.1 Billion; 2009 Fortune 500 Company #193Full Year 2008 - $11.6 Billion; Fortune 500 Company #234

» Backlog: June 30, 2010 - $12.4 Billion (79% reimbursable / 21% fixed-price)*June 30, 2009 - $12.3 Billion (79% reimbursable / 21% fixed-price)*

» Headquarters in Houston, Texas

» 100+ years of operating history

» ~42,000 employees; 45+ countries

» Extensive service capabilities:

• Engineering, procurement, construction, commissioning, and start-up (EPC-CS) to global hydrocarbons, power, industrial, minerals, and infrastructure customers

• Defense, logistics, and contingency support for defense services

Page 3 of 16

KBR Operates in 45 Countries

Edmonton

Calgary

Houston

Monterrey

Arlington

MMM

GreenfordLeatherhead

Moscow

Atyrau

Baku

Dubai

CairoAlgiers

Angola

Lagos

Johannesburg

BaghdadKuwait City China

SingaporeJakarta

Perth

Brisbane

SydneyAdelaide Canberra

Melbourne

Gothenburg

Abu Dhabi

DhahranNew Delhi

BirminghamAtlanta

Wilmington

Raleigh / Charlotte

Page 4 of 16

Gas Monetization

LNG remains robust

Skikda LNG progressing well

Gorgon LNG execution is strong

Pluto 2 and 3 FID expected mid-2011

Inpex Ichthys FID expected 2nd half of 2011

Browse LNG Basis of Design

Improving Gas Monetization margins

Tangguh/Yemen LNG projects complete; negotiating final close out on Tangguh

Escravos GTL and Skikda LNG will have reducing impact over the next year

Double-digit margins not unrealistic over time

Page 5 of 16

Oil & Gas

Capturing opportunities

FEEDs being converted to detailed engineering, design, and implementation

Strong level of global offshore activity with several excellent opportunities in Caspian and West Africa over next 18 months

Expand service offerings from engineering to project execution

Energo Engineering acquisition

Expands KBR’s offshore capabilities in areas of integrity management and advanced structural engineering

Page 6 of 16

Downstream

Saudi Arabia projects progressing well

FEED activities continue on Ras Tanura Integrated project

Yanbu EPC packages awarded

KBR staffing up EPC project offices in support of Aramco GES Plus initiative

African refinery projects moving forward

Lobito project negotiations for first phases for EPCm continue

PetroSA FEED expected to commence later this year

Page 7 of 16

North America Government & DefenseLogCAP Updates and Outlook

Expect 2011 revenue at approximately second half of 2010 levels

Once troop level at 50,000 levels, expect our staffing to remain reasonable consistent through end of 2011

Received $60 million in prior period award fees during second quarter of 2010

Positive breakthroughs on DCAA and other legacy LogCAP issues

Life After LogCAP

Replacing LogCAP work by diversifying customer base, building on logistical expertise, and expanding geographically

New customers including NATO, Air Force Civil Engineering Agency, National Reconnaissance Office

Turkey and Spain base operations award by U.S. Air Force Page 8 of 16

Infrastructure, Government, and PowerInternational Government & Defense

Continued support for U.K. Ministry of Defence and NATO in Afghanistan; newly acquired NATO contract ramped up

Building on U.K. based logistics and life support and consultancy and training capabilities in Australia to expand services within the Asia-Pacific region

Infrastructure & MineralsSlow ramp up for infrastructure spending in the U.S., Australia, and the U.K.

Middle East infrastructure activity improving based on stabilized oil price

Minerals markets strengthening; recent Hope Downs 4 EPCm award

Power & IndustrialDemand for new electric generating capacity still lagging

Industrial markets experiencing strong volume of early stage prospects Page 9 of 16

ServicesU.S. construction markets

Continued moderate activity for small to mid-size capital projects

Only now seeing the beginnings of a return of larger construction projects

Increasing activity in Alberta oil sands region

Strong Building Group activity this year with sanctioned projects moving forward

Industrial Services

Large DuPont construction, maintenance and services project began mobilized earlier this year

Turnaround activity picking upPage 10 of 16

KBR Financials and Backlog

Page 11 of 16

Creating a More Profitable Backlog

100

105

110

115

120

125

130

135

140

145

150

155

Perf

orm

ance

Inde

x

Job Income Backlog

Revenue Backlog

2006 2007 2008 2009

Less impact from legacy projects

Less impact from LogCAP project

Success from risk focus on new projects

Pursuit of selective projects

Page 12 of 16

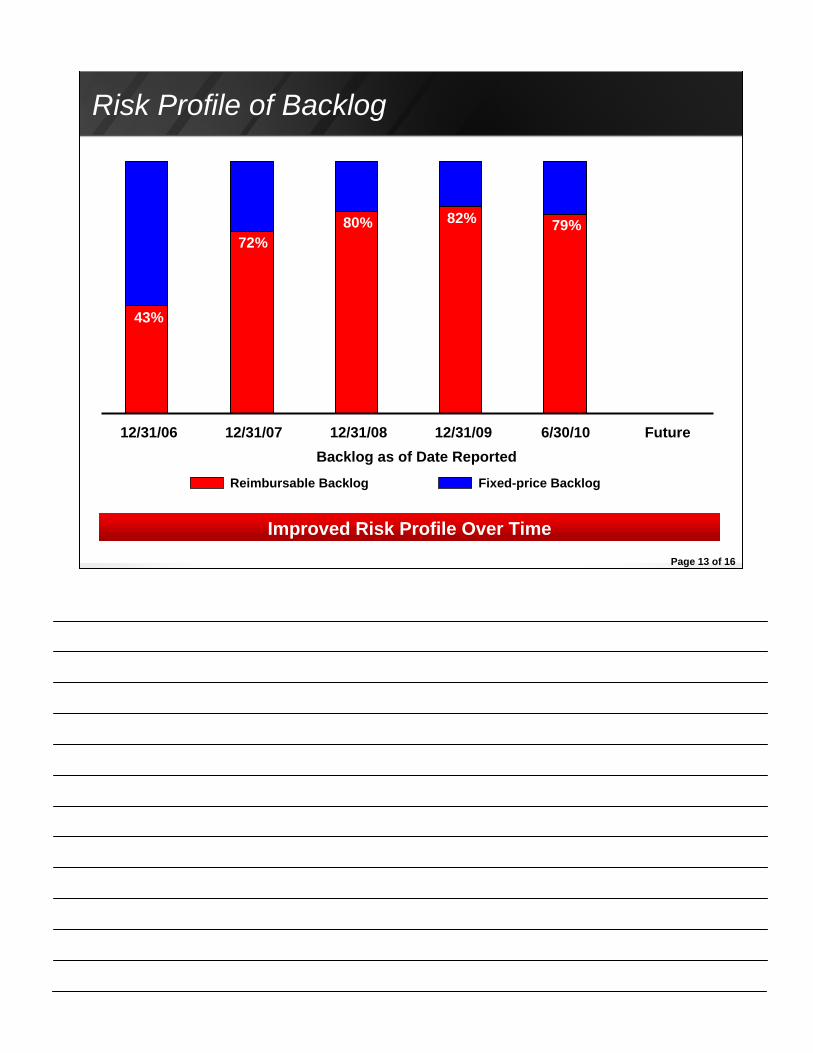

Risk Profile of Backlog

43%

12/31/06

Fixed-price BacklogReimbursable Backlog

12/31/07 12/31/08 12/31/09 6/30/10Backlog as of Date Reported

72%80% 82% 79%

Future

Improved Risk Profile Over Time Page 13 of 16

Cash and Cash Equivalents $1,235

Joint Venture Cash $267

Operating / Discretionary Cash $968

Effective Cash Deployment

Operating Requirements

Dividends $32 M

Capex with ERP $70 - $80 M

Share Repurchase* Up to $220 M

Pension Contribution $30 - $40 M

Acquisitions $36 M - ??

June 30, 2010 ($ millions)

Full Year 2010 Outlook

Effective and Thoughtful Cash Deployment in 2010*Assumes 10 million shares repurchased pursuant to authorization at an average purchase share price of $22 per share Page 14 of 16

Working Capital Management

Focused on reducing general business accounts receivable

Managing accounts payable

Resolution of unbilled receivables on uncompleted contracts

Collecting on past disputes (EPC 1)

Government Business

As LogCAP work declines, less working capital requirements

Diligently working to resolve disputed withhold amounts

Award fees

Page 15 of 16

KBR Investment Thesis

• KBR is a growth company across a broad based and diverse series of businesses

• Optimism for acceleration in new orders around growth opportunities across markets

• Ample opportunities to replace declining LogCAP work

• Strong balance sheet with emphasis on cash management

• Patience, prudence, and thoughtfulness in managing KBR’s cash balances

Page 16 of 16

We Deliver