D2 2Initialbusinessmodels, market ... - 5g-pagoda.aalto.fi ·...

95

This project has received funding from the European Union’s Horizon 2020 research and innovation programme under grant agreement No 723172. D 2 . 2 Initial business models, market analysis and strategies for the adaptation of 5G!Pagoda concept Document Number D2.2 Status Final Work Package WP2 Deliverable Type Report Date of Delivery 30 June 2017 Responsible Device Gateway (DG) Contributors DG, Orange, Ericsson, Fokus, MI, UT, KDDI, Hitachi, NESIC Dissemination level CO This document has been produced by the 5GPagoda project, funded by the Horizon 2020 Programme of the European Community. The content presented in this document represents the views of the authors, and the European Commission has no liability in respect of the content.

Transcript of D2 2Initialbusinessmodels, market ... - 5g-pagoda.aalto.fi ·...

This project has received funding from the European Union’s Horizon 2020 research and innovation programme under grant agreement No 723172.

D2 .2 Initial business models, market analysis and strategies for the adaptation of 5G!Pagoda concept

Document Number D2.2

Status Final

Work Package WP2

Deliverable Type Report

Date of Delivery 30 June 2017

Responsible Device Gateway (DG)

Contributors DG, Orange, Ericsson, Fokus, MI, UT, KDDI, Hitachi, NESIC

Dissemination level CO

This document has been produced by the 5GPagoda project, funded by the Horizon 2020 Programme of the European Community. The content presented in this document represents the views of the authors, and the

European Commission has no liability in respect of the content.

D2.2 – Initial business models, market analysis, and strategies for the adaptation of 5G!Pagoda concept

5G!Pagoda Version 1.0.0 Page 2 of 95

Change History

Version Date Status Author (Company) Description

0.1 14.12.2016 Working Georges Haour, Eunah Kim (DG) ToC and structure description 0.15 30.01.2017 Working Georges Haour, Eunah Kim (DG) Added intro and foreword 0.2 13.02.2017 Working Georges Haour, Eunah Kim (DG) Updated foreword

0.25 24.02.2017 Working Georges Haour, Eunah Kim (DG), Nicklas Beijar (Ericsson) Added 5G and IoT

0.3 06.03.2017 Working Georges Haour, Eunah Kim (DG), Hiroshi Takezawa (NESIC)

Added market analysis and 5G dynamic slice impact

0.35 10.03.2017 Working Yoshiaki Kiriha (UT), Eunah Kim (DG)

Added use case market analysis and 5G dynamic slice impact

0.4 23.03.2017 Working

Lechosław Tomaszewski (Orange), Zaw Htike (KDDI), Daisuke Okabe (Hitachi), Eunah Kim(DG)

Added use case market analysis and 5G dynamic slice impact

0.5 11.04.2017 Working Yoshinori Kitatsuji (KDDI), Eunah Kim (DG) Added dynamic slice impact

0.55 30.04.2017 Working Georges Haour(DG), Eunah Kim (DG), Sébastien Ziegler (MI)

Updated market analysis and impact on dynamic slicing

0.6 18.05.2017 Working Yoshiaki Kiriha (UT), Zaw Htike (KDDI), Daisuke Okabe (Hitachi) Added adaptations of 5G!Pagoda

0.7 24.05.2017 Working Eleonora Cau (Fokus), Cédric Crettaz (MI), Georges Haour, Eunah Kim (DG)

Added market analysis, 5G!Pagoda adaptation, Added business opportunities

0.75 29.05.2017 Working Zaw Htike (KDDI) Added 5G!Pagoda adaptation

0.8 11.06.2017 Working

Eunah Kim (DG), Lechosław Tomaszewski (Orange), Nicklas Beijar (Ericsson), Christopher Hemmens (MI)

Added 5G!Pagoda adaptation, challenges of vendor, update of challenges on telcos, refinement of text.

0.9 15.06.2017 Working Sébastien Ziegler, Christopher Hemmens (MI), Georges Haour (DG), Nicklas Beijar (Ericsson)

Added analysis of the survey on partners’ exploitation plan

1.0 20.06.2017 Submitted to the consortium

Christopher Hemmens (MI), Georges Haour, Eunah Kim (DG) Overall text refinement

1.1 25.06.2017 Version 1.1 Eunah Kim (DG) Editorial corrections and applications of partners’ input

1.2 30.06.2017 Final Eunah Kim (DG), Sébastien Ziegler (MI)

Applying comments and overall update of the document.

D2.2 – Initial business models, market analysis, and strategies for the adaptation of 5G!Pagoda concept

5G!Pagoda Version 1.0.0 Page 3 of 95

AUTHORS

Full Name Affiliation Georges Haour, Eunah Kim Device Gateway SA Christopher Hemmens, Cédric Crettaz, Sébastien Ziegler

Mandat International

Nicklas Beijar Ericsson Lechosław Tomaszewski Orange Eleonora Cau Fokus Yoshinori Kitatsuji, Zaw Htike, Itsuro Morita, Phyo May Thet

KDDI

Akihiro Nakao, Yoshiaki Kiriha, Shu Yamamoto, Du Ping

UT

Daisuke Okabe, Kota Kawahara, Hidenori Inouchi

Hitachi

Hiroshi Takezawa, Kazuto Satou, Masato Yamazaki

NESIC

D2.2 – Initial business models, market analysis, and strategies for the adaptation of 5G!Pagoda concept

5G!Pagoda Version 1.0.0 Page 4 of 95

Executive Summary

After one year of project work, this deliverable provides inputs on the three components of task T 2.2, which are: 1) preliminary market data concerning 5G, IoT, and selected use cases in T2.1, 2) stakeholder analysis including their benefits and challenges, 3) initial business potential analysis and adaptation of 5G!Pagoda concepts by different stakeholders, and 4) surveying the paths envisaged by the partners to exploit the results of this project.

The market analysis described in the Section 3 does not simply provide general market studies, but it discusses how the dynamic slicing of 5G, the core focus of 5G!Pagoda project, can impact on the market movement. The consortium partners are thankfully consisted of key market players and active standardization actors, and the insights of the partners have been gathered in the process.

In the stakeholder discussion in the Section 4, we identifies major stakeholders involving each segment (5G, IoT, smart drive-‐assisted services, industrial factory management, ensuring QoS on demand, smart/virtual office, content delivery network as a service and advancement of medial services). This is done with special reference to the use cases selected in task T2.1. It also discusses the benefits in each stakeholder in general categories. In all cases, a crucial stakeholder is people, who may make or break the industry.

It is followed by discussing on challenges for telecom network operators, telecom vendors and manufacturers who have most influenced by the new technologies. In the section, it is not only pointing out challenges but also leads the discussion of opportunities using the challenges.

The business model analysis shows initial observation of dynamic slicing impacts on business. It also discusses the key factors, business types and cloud models on designing further business models. A particular emphasis has been put on telecommunication companies, which will be impacted heavily by 5G and dynamic slicing. It should be stressed that it includes initial strategies for adaptation of 5G!Pagoda concepts in each major stakeholder group, which is directly from the key industry partners giving their know-‐how, company direction and insight, instead of using broad and general market data.

Intensive survey analysis of partners’ initial exploitation plan is included in the Section 7. In order to develop and recommend any realistic and feasible business models in the next iteration, it is important to assess and clarify the specific assets and uniqueness of 5G!Pagoda technological outputs, and the survey on the initial exploitation plan has been used to identify the direction of exploitation plan and further paths on designing business models. According to our initial analysis, it appears that the most likely path to exploitation will be distributed between technology transfer to standardisation and/or individual exploitation of specific outputs by individual partners.

This “work in progress” must be seen as an iterative process. One of the objectives of the next phase is to concentrate on the key issue of this task, which consists of deeper assessing where and how dynamic slicing will impact business and markets, both in providing enhanced/new opportunities, as well as threats to certain established business positions. Given the rapid change and novelty of 5G, IoT and dynamic slicing, it is going to be a challenge to anticipate events for the foreseeable future.

D2.2 – Initial business models, market analysis, and strategies for the adaptation of 5G!Pagoda concept

5G!Pagoda Version 1.0.0 Page 5 of 95

Table of Contents

1. Introduction ........................................................................................................................ 12

1.1. Objectives .................................................................................................................................... 12

1.2. Motivation and scope .................................................................................................................. 13

1.3. Relationships with other tasks in WP2 and other WPs .................................................................. 13

1.4. Structure of the document ........................................................................................................... 13

2. Foreword ............................................................................................................................ 15

2.1. Digital healthcare ......................................................................................................................... 15

2.2. Connected cars ............................................................................................................................ 16

2.3. Smart reality at fingertips ............................................................................................................. 16

2.4. The companies try to adapt to the digital revolution .................................................................... 17

2.5. The serious need for healthy debates ........................................................................................... 18

3. Market overview ................................................................................................................. 20

3.1. Market analysis and impact of 5G dynamic slicing ........................................................................ 20

3.1.1. 5G ......................................................................................................................................... 20

3.1.2. Application domains from the selected use cases .................................................................. 23

3.1.2.1 Massive IoT ..................................................................................................................... 23

3.1.2.2 Smart driving .................................................................................................................. 27

3.1.2.3 Smart manufacturing ..................................................................................................... 30

3.1.2.4 On-‐demand QoS support with mobility ......................................................................... 31

3.1.2.5 Smart/Virtual office ........................................................................................................ 32

3.1.2.6 Content Delivery Service ................................................................................................ 33

3.1.2.7 Advancement of medical services .................................................................................. 35

3.1.2.8 Handling disasters or very high concentration of people .............................................. 36

4. Multi-‐stakeholder analysis .................................................................................................. 38

4.1. Identified stakeholders in 5G!Pagoda use cases ........................................................................... 38

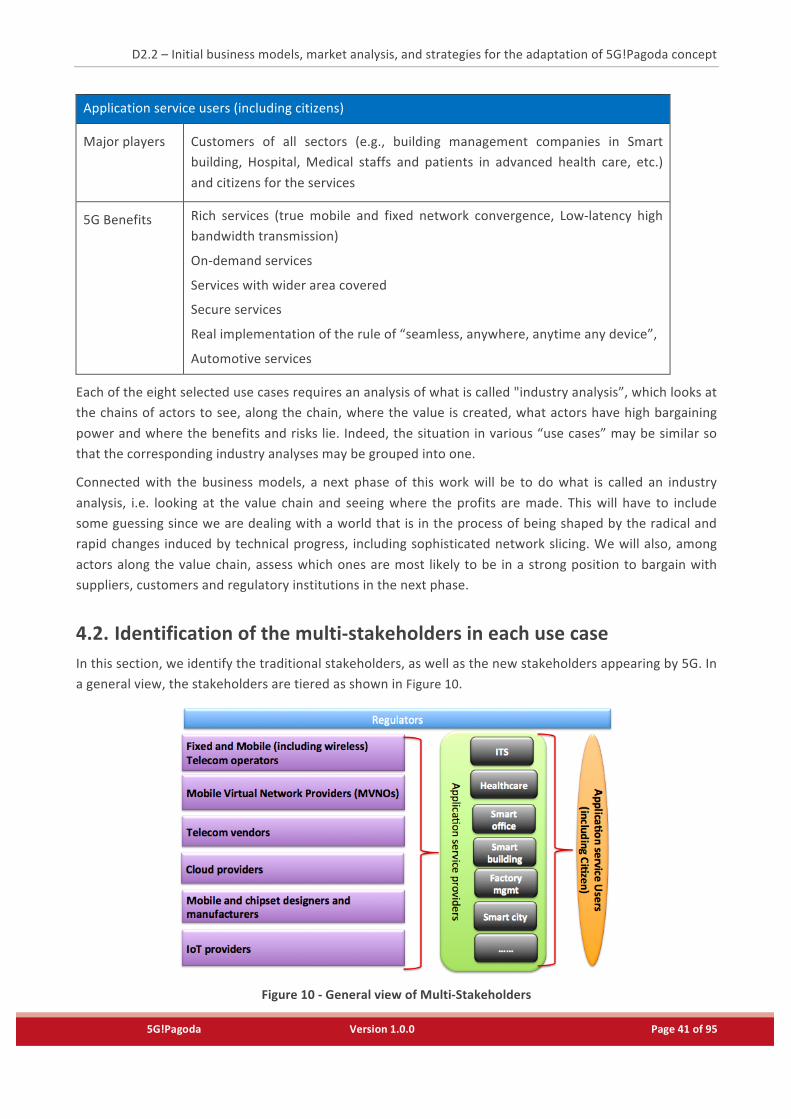

4.2. Identification of the multi-‐stakeholders in each use case .............................................................. 41

4.2.1. Massive IoT ........................................................................................................................... 42

4.2.2. Smart drive-‐assisted services ................................................................................................. 44

4.2.3. Industrial factory management .............................................................................................. 46

D2.2 – Initial business models, market analysis, and strategies for the adaptation of 5G!Pagoda concept

5G!Pagoda Version 1.0.0 Page 6 of 95

4.2.4. Ensuring QoS on demand ...................................................................................................... 46

4.2.5. The smart/virtual office ......................................................................................................... 47

4.2.6. Content delivery network as a service ................................................................................... 48

4.2.7. Advancement of medical services .......................................................................................... 49

5. Challenges for three key players ......................................................................................... 50

5.1. Specific challenges for the telecom network operators ................................................................. 50

5.2. Challenges to telecom vendors .................................................................................................... 53

5.3. Challenges to manufacturers ....................................................................................................... 54

6. Business model analysis ...................................................................................................... 55

6.1. Network slicing: a game-‐changer ................................................................................................. 55

6.2. Business model ............................................................................................................................ 56

6.2.1. Drivers and challenges of network slicing for the operators ................................................... 58

6.2.2. Business impact of network slicing ........................................................................................ 59

6.3. Business opportunities with 5G!Pagoda concepts ......................................................................... 61

6.4. Initial strategies for the adaptation of 5G!Pagoda concepts .......................................................... 62

6.4.1. Telecom operator (Orange) ................................................................................................... 62

6.4.2. Telecom operator (KDDI) ....................................................................................................... 64

6.4.3. Manufacturer (Hitachi) .......................................................................................................... 64

6.4.4. Telecom vendor (ERICSSON) .................................................................................................. 65

6.4.5. IoT platform provider (ERICSSON, DG) ................................................................................... 66

6.4.6. MVNO (NESIC) ....................................................................................................................... 67

6.4.7. IoT solution provider (DG) ..................................................................................................... 69

7. Initial Exploitation Strategy ................................................................................................. 70

7.1. Partners survey ............................................................................................................................ 71

7.2. Analysis of the survey .................................................................................................................. 71

7.2.1. Exploitable results ................................................................................................................. 71

7.2.2. Perceptions of market potential ............................................................................................ 72

7.2.3. IPR potential and strategy ..................................................................................................... 74

7.2.4. Exploitation strategy ............................................................................................................. 75

7.2.5. Specific results to be exploited .............................................................................................. 80

7.2.6. Freedom to use results .......................................................................................................... 82

D2.2 – Initial business models, market analysis, and strategies for the adaptation of 5G!Pagoda concept

5G!Pagoda Version 1.0.0 Page 7 of 95

7.3. Considerations on the exploitation strategy ................................................................................. 85

7.3.1. Comparative SWOT analysis .................................................................................................. 85

8. Legal, regulatory and corporate policy issues ...................................................................... 87

9. Future Steps ........................................................................................................................ 89

Appendix 1. Exploitation Plan Survey ........................................................................................ 90

D2.2 – Initial business models, market analysis, and strategies for the adaptation of 5G!Pagoda concept

5G!Pagoda Version 1.0.0 Page 8 of 95

List of Tables

Table 1 – List of Acronyms ....................................................................................................................... 10

Table 2 – Actors involved in the seven use cases selected in task D2.1 .................................................. 38

Table 3 – Partners' answer on exploitable results ................................................................................... 71

Table 4 – Perception of market potential ................................................................................................ 73

Table 5 – IPR potential and strategy ........................................................................................................ 74

Table 6 – Collective exploitation & Individual exploitation ..................................................................... 75

Table 7 – Exploitation Focus .................................................................................................................... 76

Table 8 – Joint commercial exploitation plans ........................................................................................ 77

Table 9 – Exploitation actions .................................................................................................................. 79

Table 10 -‐ Answers on results to be exploited ......................................................................................... 80

D2.2 – Initial business models, market analysis, and strategies for the adaptation of 5G!Pagoda concept

5G!Pagoda Version 1.0.0 Page 9 of 95

List of Figures

Figure 1 – Exploitation strategy for 5G!Pagoda ....................................................................................... 13

Figure 2 – Impact of the digital revolution on various sectors ................................................................ 18

Figure 3 – Security Decision-‐Makers have growing concerns about IoT initiatives ................................. 26

Figure 4 – Telecommunication cost ratio in various segments ............................................................... 28

Figure 5 – MRI's forecast for smart mobility ........................................................................................... 28

Figure 6 – Smart driving in Japan in 2030 (from Yano Economic Laboratories) ...................................... 29

Figure 7 – Boston Consulting Group's prediction on smart driving (2015) .............................................. 29

Figure 8 – Global Smart Office Market Industry (source: mordorintelligence.com) ............................... 32

Figure 9 – Content Delivery Service Revenue Forecast ........................................................................... 34

Figure 10 -‐ General view of Multi-‐Stakeholders ...................................................................................... 41

Figure 11 -‐ Stakeholders of 5G Telecom operators ................................................................................. 42

Figure 12 – Internet of Things for Business (source: Beecham research) ............................................... 43

Figure 13 – Stakeholders and key players of global smart city market ................................................... 44

Figure 14 – An Ecosystem of Winners of connected car ......................................................................... 45

Figure 15 – Pre-‐5G vs. 5G-‐based factory model ...................................................................................... 65

Figure 16 – MVNO subscribers in Japan (source: Mitsubishi Research Institute, Ltd.) ........................... 67

Figure 17 – Exploitable results of 5G!Pagoda .......................................................................................... 72

Figure 18 – Answers on Focus on exploitation ........................................................................................ 76

Figure 19 – Answers on the joint commercial exploitation plan ............................................................. 77

Figure 20 – Answers on the joint research activities ............................................................................... 78

Figure 21 – Answers on the joint standardization activities .................................................................... 78

Figure 22 – Category of exploitable results ............................................................................................. 81

Figure 23 – IPR policy ............................................................................................................................... 82

Figure 24 – Free exploitation to the partners .......................................................................................... 83

Figure 25 – Free exploitation to the 3rd party .......................................................................................... 83

Figure 26 – Survey results on business concerns in deploying M2M or IoT ............................................ 88

D2.2 – Initial business models, market analysis, and strategies for the adaptation of 5G!Pagoda concept

5G!Pagoda Version 1.0.0 Page 10 of 95

Abbreviations Throughout this document, the following acronyms are used.

Table 1 – List of Acronyms

Abbreviations Original terms

3GPP The Third Generation Partnership Project

5G system The Fifth Generation of Mobile Communications System

AaaS Asset as a Service

B2B2C Business to Business to Consumer

CDN Contents delivery network

CDNaaS CDN as a Service

E2E End to End

EBITDA Earnings Before Interest, Tax, Depreciation and Amortization

IaaS Infrastructure as a Service

IMT International Mobile Telecommunications

IoT Internet of Things

M2M Machine to Machine

MEC Mobile Edge Computing

MVNO Mobile Virtual Network Operator

NFVI Network Function Virtualization Infrastructures

NFVIaaS NFV Infrastructure as a Service

NGMN Next Generation Mobile Network Alliance

NSaaS Network Security as a Service

OaaS Operation as a Service

OSS Operational Support Systems

OTT Over-‐the-‐top content

RAN Radio access network

SDN Software Defined Networking

D2.2 – Initial business models, market analysis, and strategies for the adaptation of 5G!Pagoda concept

5G!Pagoda Version 1.0.0 Page 11 of 95

SDO Standards Development Organization

uRLLC ultra-‐reliable low latency communications

VMN Virtual Mobile Network

VNF Virtualized Network Function

XaaS Anything as a Service

D2.2 – Initial business models, market analysis, and strategies for the adaptation of 5G!Pagoda concept

5G!Pagoda Version 1.0.0 Page 12 of 95

1. Introduction

1.1. Objectives The objectives of WP2 are to define a set of reference use case scenarios for 5G!Pagoda with identification of their technical requirements (T2.1), to define target business models at work (T2.2) and to define 5G!Padoga architecture with descriptions of the specifications of different slices for different sectors (T2.3).

The general objective of task T2.2 is to explore marketing opportunities for dynamic network slicing, to analyse drivers and barriers for the adoption of the technology, and to explore viable business models. As stated in the description of action, this task is closely aligned with research and standardization activities and will evolve alongside the project.

The object of this deliverable is to present a first iteration of task T2.2's research and analysis. It identifies and outlines an initial set of market opportunities for 5G!Pagoda and analyses key drivers and barriers for the adoption of the technology among stakeholders in the whole value chain. A market overview of current and future commercial environments is provided. In order to define viable business models, realistic evaluations of the identified business models are derived and different marketing strategies are identified. In order to make realistic business models, legal, regulatory, and corporate policy issues associated with the 5G!Pagoda area are addressed and recommendations to cope with these issues are stated.

In the wording of the project proposal, for the D2.2 task, deliverables include three components:

• initial look at business models;

• preliminary market data;

• strategies for the exploitation by the partners of results of the project on dynamic slicing.

This work in progress will be complemented by a second iteration to be delivered by M30. From a research project perspective, it must be noted that the 5G!Pagoda project is a three-‐year project and most of the research results will come about in years 2 and 3, and according to the GANTT most outputs will not be finalized before M30.

At the same time, the technology landscape and 5G standardization are evolving very fast while the market and business prospects are unclear. The value of the results will thus depend a lot on the on-‐going evolution of technology and the markets.

In this context, we have chosen to focus this first deliverable on contextual analysis and a prospective view that will guide the exploitation strategy of task T6.3 which starts in M18. The second iteration, deliverable D2.4, due by M30, will extend and further detail the analysis according to the on-‐going developments and achievements of the project.

Our methodology has been chosen and adapted to this evolving market environment and to the integration with complementary tasks, namely task T6.3 on exploitation starting in M18. A coordinated strategy has been designed and adopted by tasks our task and task T6.3. Accordingly, the first iteration provides a high-‐level view that is expected to remain valid until the end of the project. It defines the overall context and framework. The second deliverable will be synchronized with the effective outputs of the project with a focus on supporting the exploitation strategy. It will also be adapted to T6.3's orientation and needs.

D2.2 – Initial business models, market analysis, and strategies for the adaptation of 5G!Pagoda concept

5G!Pagoda Version 1.0.0 Page 13 of 95

Figure 1 below illustrates the exploitation strategy for the 5G!Pagoda project as well as the relationships between tasks.

Figure 1 – Exploitation strategy for 5G!Pagoda

1.2. Motivation and scope This task aims at assessing the business implications of the developments expected as a result of the advent of 5G looking in particular at the eight uses case selected in task T2.1. As an initial version of the T2.2 results, it covers initial market analysis based on current market trends and forecasting. It includes a short conceptual description of the impact on 5G!Pagoda and includes initial strategies on the adaptation of 5G!Pagoda concepts from the different actors within the consortium partners. It also covers some initial observations on regulatory, societal and cooperation issues. These initial results will keep evolving until the end of the project according to market direction and 5G!Pagoda's exploitable results that will be carried out in the next phase (D2.4).

1.3. Relationships with other tasks in WP2 and other WPs As stated in section 1.2, the market analysis is focused on selected use cases defined in D2.1 from T2.1. In addition, task T2.2 is bound by several interdependencies related to business models and exploitation strategies as indicated in Figure 1. There are two main interdependencies we can highlight:

• The market analysis and exploitation strategy is closely related to the output of the project.

• The market analysis is also closely related to task T6.3 in charge of exploitation. The initial exploitation strategy stated in deliverable D2.2 will contribute to guiding and focusing the market analysis work to be performed in D2.4.

1.4. Structure of the document Following this introductory section, the remaining part of the document is structured as follows:

• Section 2 states foreword,

D2.2 – Initial business models, market analysis, and strategies for the adaptation of 5G!Pagoda concept

5G!Pagoda Version 1.0.0 Page 14 of 95

• Section 3 analyses market data and impact on 5G dynamic slicing mechanism,

• Section 3 describes and analyses stakeholders,

• Section 4 discusses challenges of three major stakeholders,

• Section 6 describes business opportunities and adaptation of 5G!Pagoda concepts,

• Section 7 states initial exploitation strategies,

• Section 8 handles legal, regulatory and corporate policy issues, and

• Section 9 draws important concluding remarks and future work.

D2.2 – Initial business models, market analysis, and strategies for the adaptation of 5G!Pagoda concept

5G!Pagoda Version 1.0.0 Page 15 of 95

2. Foreword The world is at the threshold of a huge step-‐change in scale and speed in connectivity. This is due to the advent of 5G, which will provide roughly 100 times the capacity for transmission of information as compared with current 4G. At the same time, the expected exponential rise of connected objects will provide yet another level of connectivity. Some authors therefore speak of a “Digital Tsunami”. Although this industry is the object of much hype, it is clear that the digital revolution will continue to have a broad and profound impact on all aspects of human activity. People, governments and institutions are unprepared for this tsunami; this project should help improve the situation.

Not surprisingly, some aspects of the industry are negative, which should not be downplayed. If that were to happen, this would boomerang on the industry and on individual firms due to 1) loss of image and good will and 2) the possible triggering of the refusal of the technological change induced by 5G/IoT. Indeed, in recent times, the rapid pace of change has been poorly assimilated by the general public especially when other elements of the scene (geopolitics, economics, etc.) are changing at the same time. Staying away from the nostalgic “things were better before” lets us look at a few lights and shadows of this “brave new digital world”.

2.1. Digital healthcare Digital tools offer great opportunities for providing quality healthcare at a reasonable cost. The recent book by Dr. Eric Topol: “The patient will see you now” (Basic books, New York, 2015), provides a cogent vision of this large field.

Beyond the usual benefits of computer-‐aided surgical robots, such as the Vinci robot, telemedicine and tools for improved diagnostic, digital communications will be used a lot more in hospitals to improve effectiveness and efficiency. Also, there is great scope for keeping old people at home, which is the overwhelmingly preferred option when compared to retirement homes. This includes non-‐invasive sensors and user-‐friendly robots while making sure that older people live among diverse populations, for example, they could help pupils after school or read them stories or handle “hot lines”. Serious investment should be made to adapt housing to the health and needs of “seniors”. Part of the large financial resources of private healthcare companies should be mobilized to this end.

On the subject of productivity, information and computer technologies (ICTs) do not always have such a positive impact. As a low-‐key example, professionals, highly trained to take care of patients, spend expensive time on ICT-‐driven menial tasks such as scanning medical documents in order to mitigate the consequences of a computer/network failure. More dramatically, medical devices, such as insulin pump implants in a person, may be hijacked by a third party. The latter may thus trigger the release of a high quantity of insulin, killing the person, using a blue tooth connection. Similarly, tampering can also take place with pacemakers. So far, manufacturers of medical devices have provided low protection to such hacking because they did not think of it or decided that the cost did not justify the risk. Thinking the unthinkable is not easy.

D2.2 – Initial business models, market analysis, and strategies for the adaptation of 5G!Pagoda concept

5G!Pagoda Version 1.0.0 Page 16 of 95

2.2. Connected cars There is currently considerable hype – and much investment – concerning connected cars and driverless cars. This is because it concerns an object with which consumers have had a long love affair: automobiles. Also, the automotive industry is a substantial part of many countries' economy. Digital car technology has a number of difficult goals. First, it aims to reduce the number of victims in automobile accidents -‐ each year, more than a million people die on the world's roads. Certain counties, such as France, have managed to substantially reduce the number of traffic victims by a sustained, coherent set of measures, however, the digital car offers further improvement in this area. Given recent failures, however, driverless cars may not be on our roads before 2025.

Second, it aims to increase the amount of traffic that existing roads can handle -‐ one talks of an increase of 20 to 30%. Third, the car becomes a space for work and leisure. Finally, driverless cars greatly enhance the autonomy for handicapped people. One outstanding issue remains insurance -‐ in case of a car crash, the responsibility is not with the driver anymore, but then, with what or whom? The sensors, the hardware, the software, the road infrastructure? Fierce fights between experts are on the horizon. Obviously, the big economic impact will be that cars will then be leased and shared dramatically dropping the number of cars sold every year. Bad news for car-‐makers but good news for the environment. Later in this report, we’ll discuss the business aspects in this area.

2.3. Smart reality at fingertips Digital healthcare and connected cars, briefly discussed above, are pieces of a puzzle that can be named “smart reality”. There are already numerous such pieces available, many of them are often only seen and considered alone. Some of them may be reshaped according to coming technological advancements. Some of them may be made denser and more intense because technology enablers will make them affordable and their appearance on a massive scale will provide new opportunities and smart interactions between them. Some of them, currently missing, will be imagined and then created.

The idea of smart buildings, proposed in the 1970s, originates in automated manufacturing control systems and plant growth environment optimization systems. The smart building combines sensors and detectors into one, integrated management system managing facilities, installations and grids inside the building. With information coming from various sensors, the system can autonomously adapt to changes of environment inside and outside the building, optimizing its functionality, comfort, safety, security, operational costs and emissions. The idea of self-‐aware and self-‐managing building might have been perceived as futuristic in the 1970s, but nowadays it is common due to sensing, transmitting, computing and controlling technologies making it viable and affordable. This is especially true for the connected components of the smart building.

What if we think about expanding this “smartness” to cities, or regions, and, at the same time, aim to maximize the comfort of individual people? What if we expand self-‐awareness and self-‐management from air-‐conditioning, lighting, watering, access, safety and security, to other domains such as manufacturing, trade, logistics and supply chain, health, transportation and traffic, finance, information media and entertainment, etc.?

Telemedicine (including remote monitoring of human vital signs for early warning and diagnostics and automated calling for rescue, remote healthcare and consultations or even remote surgery) and connected

D2.2 – Initial business models, market analysis, and strategies for the adaptation of 5G!Pagoda concept

5G!Pagoda Version 1.0.0 Page 17 of 95

cars for road security improvement and active shaping of traffic for better use of road capacity, have been discussed above. In addition, existing fleet-‐tracking technologies might be developed, densified and reused for e.g. freight/luggage/shipment tracking and localization, inventory management, smart or assisted travelling, automated goods/shipment delivery, public transportation agility and adaptation etc. Existing remote sensing technologies may be densified in order to provide high spatial resolution metropolitan pollution sensing systems associated with e.g. traffic management systems and public systems for localized warning. Another scenario with multi-‐parametric and high spatial density-‐sensing/monitoring for natural disasters anticipation and emergency detection (terrorism, fires, traffic accidents etc.) may be considered. Current systems for energy and media management used in smart buildings may be expanded to smart electricity, water and gas grids allowing balanced production and utilization with inherent centralized remote charging. Many other currently available features can be rethought, redefined or re-‐engineered.

Massive-‐coverage, high-‐density data, transmission networks, as key enablers for "smart reality", require:

• high data speeds,

• low latency,

• advanced mobility support (providing reliable connectivity for terminals in motion at high speed),

• high resolution of spatial positioning (horizontal and vertical, inside and outside buildings),

• high reliability,

• high agility and adaptability to specific use cases,

• high capacity in terms of volume of connected devices.

These features will be required in whole or part of a system, depending upon the specific individual needs. Such networks, satisfying the conditions listed above, will shortly come about with the advent of 5G.

2.4. The companies try to adapt to the digital revolution Existing firms must metamorphose themselves to adapt to this new reality. Although always profound, the digital revolution impacts various industries to different degrees: utilities or oil & gas can be said to be less drastically metamorphosed than media & entertainment, for example. Chemical companies must indeed learn to capitalize on these advances to manufacture and distribute “the digital way”, but their products themselves remain chemicals unchanged. In order to successfully negotiate such a revolution and achieve this, their activity in R&D Research and development has to be “digitalized”, not a trivial feat. Automotive companies are the most advanced in machine-‐to-‐machine communication. Plants, with modular manufacturing fully using robots and drones, are around the corner. Figure 2 illustrates the impact of the digital revolution in various business sectors. The sectors indicated close to the center are most likely to be affected by the digital revolution more than those in the outermost sectors.

In spite of the agreed upon enormous impact of digital on all walks of life, close to 45% of companies consider that this revolution is not a board issue. The power of human denial is enormous. On the other end of the scale, in 2015, close to 25% of firms were declared to be actively experimenting and proactively using the power of digital. The words “open-‐minded firms", "agility", "speed" and "quality of execution” pop up most often in the management literature.

D2.2 – Initial business models, market analysis, and strategies for the adaptation of 5G!Pagoda concept

5G!Pagoda Version 1.0.0 Page 18 of 95

On the manufacturing side, the production of smartphones in Asia’s plants, sometimes “black factories” i.e. without workers, may not ever be repatriated to the “west” because the latter does not have the necessary know-‐how.

On the other hand, new companies emerge and grow in order to leverage digital tools to offer new services such as Europe-‐born Skype or Airbnb. Their business models are not rocket science and many currently lose money, but their success depends heavily on access to large investments for fast growth and quality in execution. Their model is usually predicated on the accumulation of consumer habits and details, so as to provide high value, “targeted” marketing. However, things have been at a crude stage for years, for example, Internet messages to people in the Geneva area are written in German. In the attributes of speed and scale, the Chinese are unrivalled and this is particularly the case for the mobile Internet. The example of Tencent’s WeChat Pay is particularly remarkable. Close to 400 million Chinese are doing most of their payments with their mobile phone as of Spring 2017 [1]. Some problems of hacking and disruption have been reported, but, so far, apparently in a limited way.

Figure 2 – Impact of the digital revolution on various sectors

sectors close to the center are likely to be most affected [3]

2.5. The serious need for healthy debates Concerning this coming digital tsunami, we have to hold robust debates with lucidity. The media have a full role in this; will they be up to the task? Our governments must anticipate, or at least accompany, the process with light-‐footed but effective regulations, not self-‐serving bureaucracy. Consumers demand honesty and openness. The industry must inform and engage with the population at large about what 5G and IoT mean; their negative aspects must not be covered up. These include serious issues: security (the more connectivity, the more hacking is possible), privacy and the proper use of data, opaque systems (in

D2.2 – Initial business models, market analysis, and strategies for the adaptation of 5G!Pagoda concept

5G!Pagoda Version 1.0.0 Page 19 of 95

fact, in the case of “deep learning” in AI, the systems are opaque even to the authors of the software), and the very dense array of antennae required by 5G.

If these negative aspects are not responsibly addressed by the industry and the regulating bodies, impatient and demanding customers will rebel. Similarly, the world currently experiences a wave against globalization and free trade. Forgetting the downsides, these have been naively presented as panaceas. These days, when a group of people arrive at a refugee camp, one of the first things they ask for is access to Wi-‐Fi as well as electricity to recharge their cell phones. For them, a smartphone is as basic a resource for survival as food and water. This is a vivid reminder of the fact that we are fully immersed in a digital world. Currently, in the world, 150 million e-‐mails are sent every minute. However, we are about to reach the point where 50% of the world’s inhabitants are connected to the Internet, most of them securing this access via their cellular phones (e.g. “mobile internet”), which should, in fact, really be called “HC” – hand computers. This means that growth rates in the industry will begin to seriously decrease.

This explains why the industry is desperately racing ahead towards a new phase of a much more radically digital world after 2020, with all the relevant buzzwords. At that time, 5G is expected to be launched with the capability of transmitting truly massive amounts of data, roughly 100 times that of current 4G. In addition, we’ll witness the exponential growth of connected objects, the so-‐called IoT – the Internet of things. We are thus about to enter a truly new phase stepping up the impact of information technology in every aspect of human activity.

D2.2 – Initial business models, market analysis, and strategies for the adaptation of 5G!Pagoda concept

5G!Pagoda Version 1.0.0 Page 20 of 95

3. Market overview As already mentioned, the advent of 5G represents a much bigger step than going from 3G to 4G. Indeed, it comes with a hundredfold increase in the capacity of data transmission compared with the introduction of 4G. Furthermore, dynamic slicing provides a way to secure additional capacity for transmitting data. Indeed, the 5G and IoT dynamics are often coupled with other elements such as Big Data, Analytics, Artificial Intelligence (AI) and block-‐chain. This bundle constitutes a most powerful driver of change in every walk of life.

The numbers articulated to evaluate the markets in 2020-‐25 vary widely depending on the source. Much assessment and validating work in the present project will be needed to arrive at “responsible” numbers. The collective wisdom of the partners in this project is key in achieving this.

Market data given below must be taken with a grain of salt. Actors involved in the various market segments are 1) either an element of the value chain or 2) operate in the context of the business activities. This context includes several issues such as a host of societal, legal, regulatory, financial and geopolitical issues, which will make or break the markets more surely than the quality of the developed technology. Let us look at the forecast for the overall markets of 5G and IoT.

3.1. Market analysis and impact of 5G dynamic slicing This section provides market overview based on the current trends and prediction. In general, more statistics are available for IoT, largely because 5G is capable of enabling the development of data and information exchange. In addition to the market study, we give our thought on each market area how the dynamic slicing of 5G, the core focus of 5G!Pagoda project, can impact on the market movement.

3.1.1. 5G (1) Market analysis

As 5G is expected to be roughly 100 times faster than 4G, corresponding speeds are in the range of 1 to 10 GB per second with latency of 1 to 5ms and bandwidth of 6 to 30 GHZ [9]. Rapid speed is the crucial ingredient provided by 5G, but also, high bandwidth and low latency constitute substantial benefits. If everything goes well, customers will have the perception that they have infinite bandwidth and limitless data.

As a first step, it is useful to look at the market evolution of mobile telephones. A recent study [4] indicates that units sold worldwide in the first quarter of 2016 were 337.2 million (representing a value of $ 101.3 billion) compared to the first quarter of 2015, for which the respective numbers are 319.3 million (an increase of 6%) and $98.5 billion (an increase of 3%). Not surprisingly, the fastest growth is in China where the year-‐to-‐year value increased by 18%. Mobile telephones are increasingly seen as indispensable and an all-‐around medium for accessing data, information and images.

With regard to 5G, in order to avoid a "can't see the forest for the trees" situation, let us start with the general picture given by Geneva-‐based ITU (International Telecommunications Union). The target set by this organization is 10 Gbps mobile download speed with a latency of one millisecond [5]. Comparing 4G

D2.2 – Initial business models, market analysis, and strategies for the adaptation of 5G!Pagoda concept

5G!Pagoda Version 1.0.0 Page 21 of 95

and 5G, the ITU spells out significant improvements, especially in latency and data rate/capacity (see ITU vision IMT 2010, published in 2016).

The availability of 5G is likely to be first localized; it will then unroll slowly. In terms of overall markets, the advent of 5G will trigger vast and rapidly growing added value through services and products, primarily through the Internet of things, which will be discussed in the following section. For the latter, for example, Cisco estimates that, by 2020 [6], more than 50 billion objects will be connected. The corresponding economic added value is estimated to be close to $2 trillion across all sectors [7]. Forecasts, however, range from 16 billion (Ericsson) to more than 30 billion (IDC) connected objects by 2020-‐21.

South Korea (5G Forum) has invested $1.4 billion and is planning to launch commercial 5G in 2019 [7]. Japan, where 5GMF was established in 2014, intends to realize the commercial stage of 5G for the Tokyo Olympics, in 2020 [7].

Enabling technologies for 5G are [7] as follows:

• Wireless networks

• Optical networks

• Network management

• Effective systems

• Software

(2) Impact on 5G with slicing mechanism

As network slicing is one of the fundamental enablers of 5G technology (together with NFV and SDN concepts and the global trend of telecommunication network architecture cloudification), its implementation conditions implementation of 5G itself, especially the demands of the separation of traffic belonging to different profiles of services and processing these traffic fractions within network architectures matched to essential service requirements (e.g. IP traffic break-‐out point location dependent on maximum latency limit). The promises of 5G technologies and expectations regarding them are commonly known, especially the impact of 5G on the global economy and on civilization. Additionally, as the densification of the network will demand high investment costs, the pressure on optimizing utilization of currently owned resources will grow. That’s why all techniques increasing infrastructure flexibility, versatility, reusability and agility will play very important roles during the 5G roll-‐out.

It is expected that network slicing will be brought into common usage by 5G implementation, however, it disrupts the current “market puzzle”, which is currently under a lot of pressure and highly sensitive.

The telecom ecosystem has changed irreversibly over the last three decades. The value chain initially containing three segments (distribution, end-‐user devices and “network = service”) and often being covered even by one player (network operator) has been converted to the 7-‐segments model of distribution (physical and on-‐line), end-‐user devices, network access, network core, enablers (e.g. advertising platforms, billing & payment systems, cloud computing, web hosting and CDN), content & service providers and content producers. As was mentioned in Section 5.1, the implementation of the “all-‐IP” paradigm with coincidental separation of basic connectivity and services has capsized the position of traditional network operators fighting for survival with OTT service providers and with network access providers (offering alternative access technologies for IP connectivity, e.g. Cable TV operators, local WiFi

D2.2 – Initial business models, market analysis, and strategies for the adaptation of 5G!Pagoda concept

5G!Pagoda Version 1.0.0 Page 22 of 95

operators) and breached the customers' base. It was further strengthened by state regulators’ pressure (promoting new operators, imposing asymmetric interconnected fees).

According to the forecast of Tera Consulting, the economic transformation of the telecom ecosystem will mean the total growth of the entire market (slightly more than doubling between 2014 and 2025). However, the distribution of revenues in segments is going to change dramatically, growing especially in higher segments. In 2014, the access segment part is 46% of total, while core and enablers’ parts are about 5% and service/content providers’ part is 13%. In 2025, the access segment is expected to have only 26%, the core part less than 2%, enablers almost 30% and service/content providers part almost 27%.

The technical implementation and opening a market offer of orchestrated network slicing based on NFV shall redefine the value chain again, adding the 2nd dimension to the chain and punching a wedge between underlying infrastructure and functions of network access/core, enablers’ and service/content providers’ segments. This trend will also affect the situation of network operators and change the aforementioned distribution of revenues further (e.g. operators of orchestrators, offering orchestrated services built with 3rd parties’ components, will strengthen the “enablers” segment).

New roles are going to appear:

• “Infrastructure provider” selling the “bare metal” devices (computing and storage nodes) and “naked media” (optic fibres, copper lines) or physical access (radio-‐head or fixed access-‐head devices) offering everybody infrastructural resources for last-‐mile access and scattered edge-‐computing. The latter will be spatially densified according to maximum transmission latency limits lowering (e.g. implementation of augmented reality services). The most extreme case would be implementation of a common single network infrastructure utilised by all operators and only one radio network shared by all operators. In such a scenario, the gravity of inter-‐operator competition would shift to services, as data rate and coverage differentiation will have disappeared. In case of a joint-‐venture company owned by a group of all network operators, the extremely deep cooperation between partners would be needed, but the gain on reduction of CAPEX spent on the network build. On the other side, the spectrum auctions would become pointless (one network, one license per country, one applicant) – resistance of the regulatory authority to such an extreme scenario is feasible.

• “XaaS services broker/integrator” offering various levels of services assembled from components delivered by 3rd party owners/sellers. Such an actor wouldn’t be just a dealer or reseller due to the active role of the operator of orchestrator, unbundling packages of offered and delivered services and then actively designing and delivering the new bundle composing the service requested by served customers. Probably, the relations will be multilateral and some “infrastructure providers” will be interested in expanding their offers with the offers of others and putting up the synergic, orchestrated offer for sale, thus becoming IaaS service integrators.

• “NSaaS customer” embedding the operated network into a specific wider industrial context. The main example is vertical industry (automotive, manufacturing, media grids, health sector, public safety, ITS, freight tracking and management etc.). They already use transmission, connectivity, communication, positioning or cloud services, but equipped with network slicing technology and orchestration they will become more self-‐reliant and “operator-‐like”, having a separated, secured network and their own control over its quality and reliability, thus being able to take the sole E2E responsibility for their services nested in the telecommunications network.

D2.2 – Initial business models, market analysis, and strategies for the adaptation of 5G!Pagoda concept

5G!Pagoda Version 1.0.0 Page 23 of 95

The technologies of orchestration and network slicing bring opportunities and threats to network operators. They shall rethink themselves in the future “orchestrated network slicing reality” and find their position in the future shape of the value chain. They will probably not avoid mutual sharing of resources and exposing network management APIs, still wanting to be able to gain such access to the common market of infrastructure and networks. They will need to get maximum internal benefits of network slicing and function virtualization and migrate to more profitable segments of the value chain, keeping proper balance between profits and losses entailed by this common market.

3.1.2. Application domains from the selected use cases The transformational power of 5G is considerable, but yet, it is fairly unknown. Indeed, it will vary from country to country and, mainly, from one industrial sector to another. Of course, early on, the clear winners will be those companies involved in building infrastructure, as well as the chip manufacturers. The companies on the losing side will be a broad mix of companies -‐ the business of which will be impacted and displaced by the digital tsunami. Within the ICT sector, likely losers include cable-‐makers as well as gaming consoles.

The release of 3GPP-‐15 is expected for 2018 for fixed wireless, while 3GPP-‐16 is expected in 2020 for mobile Internet and massive IoT. Indeed, the advent and growth of 5G is predicated on the development of software. On the 5G and IoT scenes, dynamic slicing brings considerable added potential for an enormous range of use cases and customized applications.

It is generally accepted that two sectors will represent the biggest share of this dynamic: healthcare and advanced manufacturing [11]. We now turn to a brief overview of the market potential for the various use cases selected in task T2.1, listed below:

• Massive IoT

• Autonomous (driver-‐less) cars, or smart driving

• Factory management

• QoS on demand

• Smart/Virtual office

• Contents Delivery Networks

• Advanced medical services

• Disaster handling

We will now look at a couple of these sectors, beginning with IoT and followed by autonomous cars.

3.1.2.1 Massive IoT

(1) Overall market figure

The Internet of Things, according to Cisco, will represent, by 2020 [6], more than 50 billion connected objects. The corresponding economic value is estimated to be close to $2 trillion across all sectors [7]. Gartner estimates that Internet of Things devices will constitute 13.5 billion connected devices by 2020

D2.2 – Initial business models, market analysis, and strategies for the adaptation of 5G!Pagoda concept

5G!Pagoda Version 1.0.0 Page 24 of 95

[34]. These devices will thus surpass mobile phones as the largest category of connected devices in 2018 [27]. Between 2015 and 2021, IoT is expected to increase at a compounded annual growth rate (CAGR) of 23 % [27]. In addition to the uncertainty in the estimation, these numbers also vary depending on what is counted as an IoT device. By 2025, IoT may represent a business volume between $3.9 trillion and $11.1 trillion a year [36].

(2) IoT in Mobile Networks

At the end of 2015, millions of IoT devices were connected using mobile subscriptions [6]. Cellular IoT is expected to experience the highest rates of growth among the different categories of connected devices reaching 1.5 billion in 2021 [27].

GSM/EDGE will continue to be an important alternative for Massive IoT [27]. Today, around 70 percent of cellular IoT devices support only GSM [27]. Cost reductions achieved by reducing complexity and limiting modem functionality will make LTE an increasingly viable option. This enables new low latency applications [27]. 5G networks can enable a wide range of use cases for IoT -‐ greater capacity will allow more devices to be connected and lower energy requirements will prolong battery lives more than 10 times [27]. Coverage for cellular machine-‐type communication (MTC) will support IoT applications in more remote locations such as within buildings and in underground locations [28]. Network system improvements, such as sleep mode, will support battery lifetimes beyond 10 years for remote cellular devices [27].

(3) Edge Computing

In terms of data processing, the edge cloud (or “fog” computing) concept has an important role for IoT. One reason for providing network intelligence closer to the data source is that most data will be too noisy or expensive to be carried all the way to the cloud [29]. The amount of data can be reduced by compressing, filtering, and aggregating it near the network edge [33]. Analytics, image recognition and machine control can also be provided at the network edge in order to avoid transporting the raw data to the cloud and instead only collect the important features from the data. For example, in the automatic analysis of surveillance video, the interested features could be extracted near the camera device itself, and only the resulting summarized data from the analysis, or alarms, will be sent to the central cloud. Another motivation for edge processing is the reduction of latency. Control loops collecting data from (typically multiple) sensors must react quickly to the data and send back actuation commands to the device based on the determined action. This motivates running application servers at the network edge.

(4) Applications and use cases

Companies are focused on IoT as a driver of incremental revenue streams based on new products and services. Businesses are also embracing IoT to improve productivity and save costs, such as capex, labour, and energy [29]. While the initial drive of IoT will come from lower device costs and the availability of connectivity, the creation of new services not limited to connectivity requires enablers from cloud computing, big data management, security, logistics and other network-‐enabled capabilities [32].

IoT creates opportunities for several vertical industries, including the health, automotive, and energy sectors as well as homes and buildings [32]. Applications include smart wearables, video surveillance, smart meters and digital health monitors [26][32]. In [29], the application area is divided into connected wearable devices, connected cars, connected homes, connected cities, and the industrial internet, where the latter covers industries including transportation, oil and gas, and health care.

D2.2 – Initial business models, market analysis, and strategies for the adaptation of 5G!Pagoda concept

5G!Pagoda Version 1.0.0 Page 25 of 95

The connected health consumer segment is estimated to have the fastest growth of connections between 2015 and 2020 (from 144 million to 729 million) [26]. For example, future clothes may integrate ultra-‐light, low power sensors to measure various environmental and health attributes like pressure, temperature, heart rate, blood pressure, body temperature, breathing rate and volume, and skin moisture [32]. Smart cities provide services for gas, water and electricity metering as well as environmental monitoring (pollution, temperature, humidity, and noise), light control, and vehicle traffic control [32]. Video surveillance may be supported in mobile environment such as on aircrafts, drones, cars, and security personnel [32]. The Consumer Electronics Association estimates only 10% of new homes in the United States currently utilize home automation [29]. The connected home segment will have the largest volume of connections: nearly half of all connections (2.4 billion in 2015, 5.8 billion by 2020) [26]. This is in line with [29], which expects that home automation to be at the vanguard of IoT adoption.

Western Europe will add the most connections led by growth within the connected car segment [27]. A connected car is counted here as one device, though it may have hundreds of sensors.

(5) Applications requirements for business growth

IoT devices differ significantly in terms of capabilities, power consumption and cost. IoT also poses a range of requirements on the reliability, security, latency, throughput of the network. The real impact in IoT will be felt at a later date. The true transformational role of this field will be felt after the “stovepipes” solutions have been implemented. The scope is huge, for example, in the area of energy, reducing the consumption of industry and home appliances at peak demand times will produce handsome savings. Figure 3 is a chart regarding concerns on the part of industry, from Forrester’s Global Business Security survey in 2016. As it shown in the Figure, security and privacy concerns are increasing and impact on business decision on adaptation of IoT.

IoT devices can be roughly divided into two main segments: Massive IoT and Critical IoT. Massive IoT is characterized by a high number of connections, where the data volume per connection is relatively low. Low-‐cost and low-‐energy consumption is required. Examples include smart buildings, transport logistics, fleet management, smart meters and agriculture. Many of the Massive IoT devices will not be directly connected to the mobile network, but rather through things will be connected through capillary networks, i.e. short-‐range radio networks connecting to the mobile network via IoT gateways [27]. A large group of the massive IoT devices are immobile and do not require features like handovers and location updates, which have been critical in serving mobile phones [30]. On the other hand, the connections may be very dense geographically -‐ up to 200,000 connections per square kilometre [30].

Critical IoT connections are characterized by requirements for ultra-‐reliability and availability with very low latency [27]. Examples include traffic safety, autonomous cars, industrial applications, remote manufacturing and healthcare including remote surgery [27]. Service, such as autonomous driving or remote controlled robots, requires latency in the order of milliseconds -‐ less than 5 ms for intelligent traffic monitoring (ITS) and less than 1 ms for control of motion [30].

The requirements of both Massive IoT and Critical IoT differ substantially from mobile broadband.

D2.2 – Initial business models, market analysis, and strategies for the adaptation of 5G!Pagoda concept

5G!Pagoda Version 1.0.0 Page 26 of 95

Figure 3 – Security Decision-‐Makers have growing concerns about IoT initiatives

(6) Impact on 5G with slicing mechanism

VNFs are being placed in different locations (edge or core cloud) depending on the purpose of the slice. For a massive IoT slice, scalability is the main criteria. A simpler, light-‐duty 5G Core without mobility management may be sufficient [30]. In a Critical IoT slice, the 5G Core and application servers, such as vehicle communication servers (V2X), are placed in the edge in order to minimize the transmission delay [30]. Some network functions like charging and policy control can be essential in one slice but unnecessary in other slices [30]. Operators can customize network slices the way they want [30].

Operators can provide network slices with different performance characteristics to offer optimal support for different types of services for different types of customer segments [28]. Separation of core networks provides flexibility and allows the network control to be optimized for different types of traffic and priorities. In particular, it allows giving higher priority to massive IoT traffic compared to smart phone

D2.2 – Initial business models, market analysis, and strategies for the adaptation of 5G!Pagoda concept

5G!Pagoda Version 1.0.0 Page 27 of 95

traffic. Network congestion and failures caused by a large number of M2M devices could impact the communication of higher-‐priority smart phone traffic. Separation between the traffic classes improves reliability and performance by reducing the impact of failures and isolating the network from each other [NTT]. In contrast to traditional QoS methods, separation also protects the core network elements and services. Additionally, cost reduction is possible by adjusting the service levels to suit the traffic characteristics and priority levels of the devices.

3.1.2.2 Smart driving

(1) Market analysis

Much of the data here comes from Frost Sullivan’ Global 2015 study [9], which included Nissan, PSA, Ericsson, Mazda and Bosch. Commercialization planned as follows:

• South Korea 2020

• USA 2025

• Japan 2020, pegged on the Olympic Game

The study concludes that consumers will have to pay in order to have the option of 5G available. This option is expected to increase the cost of a vehicle by $200. Interestingly, the study does not articulate a single prediction on the number of driverless vehicles expected to be on the roads

The autonomous car elicits much enthusiasm from consultancy firms to ridiculous lengths -‐ the obscure “Grand View” [8] consultancy pontificates that, in 2024, 138,089 driverless cars will be sold. Given the fact that this kind of forecast has a 50% error of margin, it is unnecessary to go to that level of precision, which constitutes part of the exquisite charm of market studies. Alphabet (ex-‐Google), Tesla, Ford, GM and VW/Bosch are all active in this area. Volvo, now owned by the Chinese Chery, makes similar noises on this issue.

In 2015, another pundit claimed that there will be 10 million self-‐driving cars on the road by 2020 [10]! On this glamorous issue, it is probably realistic to remain in the camp of a somewhat conservative stand since there are so many technical, practical, legal and ethical issues. Our regulatory environment will NOT be ready for a while as many crucial issues are outstanding requiring a minimum of societal consensus.

In Japan, towards the era of IoT/Big Data/AI, private sector lead organization ”IoT Acceleration Consortium” was established on October 23, 2016, in order to promote the utilization of IoT in industry, government and academia. Under this umbrella, Technology Development WG (Smart IoT Acceleration Forum) is promoting a mart mobility project, which tackles research and development of future mobility systems (Smart driving, Autonomous Robots, Drones) thanks to 5G capabilities. According to a Japanese document (http://www.soumu.go.jp/main_content/ 000397783.pdf), written by the Mitsubishi Research Institute (MRI), transportation, i.e. vehicle tracking, connected cars and ITS, and industrial segments (remote control and operation of large factories), are indeed anxiously waiting for the advent of 5G because their application depends heavily on the availability of the appropriate telecommunication infrastructure. The anticipated average communication cost in the total cost of ownership is around 10-‐30% and is compared below with the situation in other sectors.

D2.2 – Initial business models, market analysis, and strategies for the adaptation of 5G!Pagoda concept

5G!Pagoda Version 1.0.0 Page 28 of 95

Figure 4 – Telecommunication cost ratio in various segments

Concerning smart driving, all automotive companies in Japan plan to commercialize automatic driving cars by around 2020. Moreover, Mitsubishi Research Institute predicts that the Japanese market, including robotics, advanced services using drones, and smart driving & ITS will grow from 1.6 trillion yen (2015) to 9.7 trillion yen (2035). One Yen is roughly equivalent to 9 US cents at current market rates so 1.6 trillion yen represents about $14.4 billion.

Figure 5 – MRI's forecast for smart mobility

According to https://japan.zdnet.com/article/35095221/, the Japanese consulting firm Yano Economic laboratory (https://www.yano.co.jp/press/pdf/1633.pdf) predicts that smart-‐driving-‐ready cars will increase to 23 million for assisted driving, 28 million for partial autopilot, 18 million for full auto-‐pilot, and 2

D2.2 – Initial business models, market analysis, and strategies for the adaptation of 5G!Pagoda concept

5G!Pagoda Version 1.0.0 Page 29 of 95

million for fully autonomous vehicles. Each corresponds to autonomous driving levels 1, 2, 3, and 4 defined by NHTSA (National Highway Traffic Safety Administration). Of course, this evolution depends a lot on the autonomous capabilities of the car. However, ITS-‐related communication capabilities in 5G are also greatly expected for innovation. The ultra-‐reliability and low-‐latency capabilities in 5G are key to realizing drive assistance and partial or full autopilot in this automotive segment as well as in remote industrial operations and new drone-‐based services.

Figure 6 – Smart driving in Japan in 2030 (from Yano Economic Laboratories)

The Boston Consulting Group has reported a similar estimation (http://www.bcg.co.jp/documents/ file197533.pdf). The figures below state that around 30 million (18.4+12) cars on levels 2 and 3 will be on the market and the total size of the market will grow to $77 billion worldwide.

Figure 7 – Boston Consulting Group's prediction on smart driving (2015)

In conclusion, a note of warning: the hype around driverless cars does not mean that it will be around in a big way soon. The gross, recent failures (autonomous cars going through red lights, getting overturned,

D2.2 – Initial business models, market analysis, and strategies for the adaptation of 5G!Pagoda concept

5G!Pagoda Version 1.0.0 Page 30 of 95

hitting somebody" venture capitalist, John Doerr, who stated that “Segway was to be bigger than the internet”!. These bizarre miscalculations are reported in the book “Driverless: intelligent cars and the road ahead”, by Hod Lipson and Melba Kurman (MIT Press, 2016)

(2) Impact on 5G with slicing mechanism

In order for network infrastructure to provide real-‐time and highly reliable and secure capabilities to share huge volume of ITS information, it is necessary for information-‐networking infrastructure to provide an isolated slicing mechanism. Especially in the case of supporting (semi-‐)automatic driving since a communication delay and failure may cause car accidents. It is demanding to provide high-‐quality communication avoiding the effects from other traffic. In order to deal with this, end-‐to-‐end (i.e. from cars to mobile edge servers and cloud servers) network slicing mechanism is one of anticipating and promising technologies. Thanks to the isolation capability in network slicing, ITS service providers are able to control various type of traffic (for example, car navigation, congestion information, real-‐time driving status information, real-‐time driving control commands) according to the demanding quality of services avoiding interference.

3.1.2.3 Smart manufacturing

(1) Market analysis

In the business-‐to-‐business activity of industrial manufacturing, sometimes called “smart manufacturing”, the impact of advanced ICTs is already large and is expected to be enormous in the near future. It is critically important in achieving vastly enhanced flexibility, effectiveness and efficiency. Japan is leading the way in this sophisticated, modular manufacturing. For example, Toyota is using block-‐chain to improve and secure its automotive supply chain [9].

As this is not a customer-‐focused industry, it is probably implemented more smoothly. In fact, in Japan and some areas of Shenzhen, this revolution is fully at work. Certain plants have NO workers in sight, as far as one can see. For example, most iPads are produced in “black plants”, i.e., on premises without any workers so no lighting is required. On the other hand, in such plants, the investments in IT infrastructure are enormous [6].

The market numbers for this business segment are also there and, not surprisingly, differ wildly depending on the source. More time is needed to reach meaningful (tentative) conclusions in this area. At this stage, let us only mention the optimistic anticipation by General Electric, to the effect that advanced manufacturing (with internet of things and machine to machine communications, etc.) presents the potential of adding $500 billion each year to the global economy [7].

The report "Smart Factory Market” by Markets & Markets, indicates that smart factory market size, in terms of value, is expected to reach $74.8 billion by 2022 at a growth rate of 10.4% between 2016 and 2022. The emergence of smart factories can be seen from the period of change toward cohesive control of the machineries, processes, and resources with local intelligence. The increasing focus on saving energy & improving process efficiency along with the integration of engineering and manufacturing by the adoption of IoT is expected to foster the growth of the smart factory market [23].

(2) Impact on 5G with slicing mechanism

D2.2 – Initial business models, market analysis, and strategies for the adaptation of 5G!Pagoda concept

5G!Pagoda Version 1.0.0 Page 31 of 95

With the growth of device and service technology, cyber-‐attacks, which target infrastructure systems, have been confirmed in several industrial facilities. For example, in a threat to a car factory, 13 factories were shut down by a viral infection in August 2005. In addition, a reduction in processing capability of the car product line was reported in 2011. It was also reported that in a semiconductor factory, the product line was stopped by a viral infection [24].

In a typical car-‐assembly plant, it is generally expected that each minute of stopping the line costs two million yen per minute. If the damage requires an average of one hour to be fixed, this translates into a loss of 120 million yen [25]. It is hoped that the risks presented by the cyber-‐attacks may be minimized by disconnecting the slice that is caught in the attack and avoid it influencing the whole system.

3.1.2.4 On-‐demand QoS support with mobility

(1) Market analysis