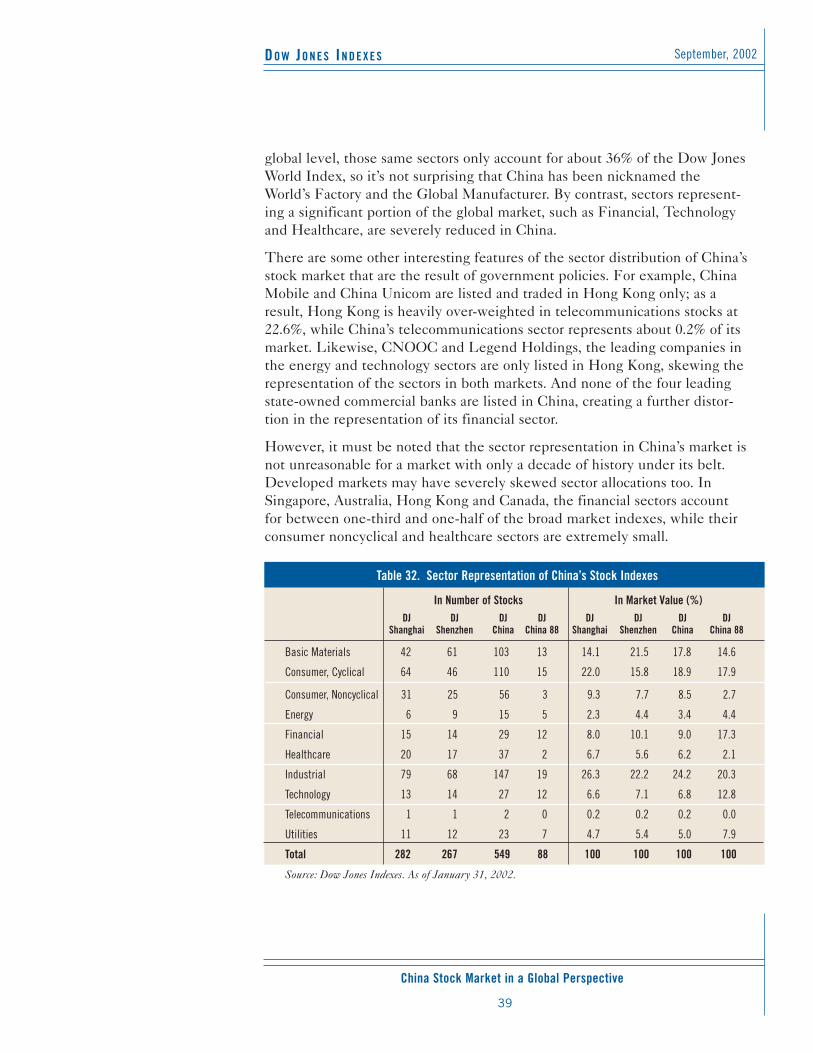

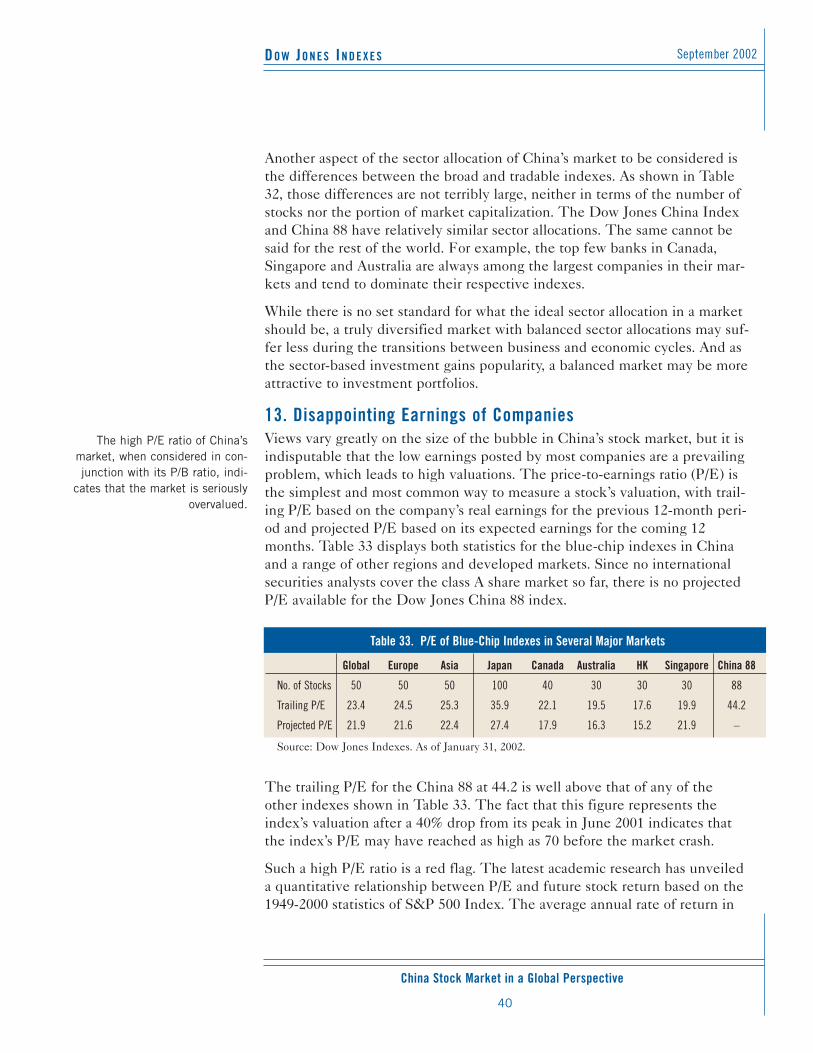

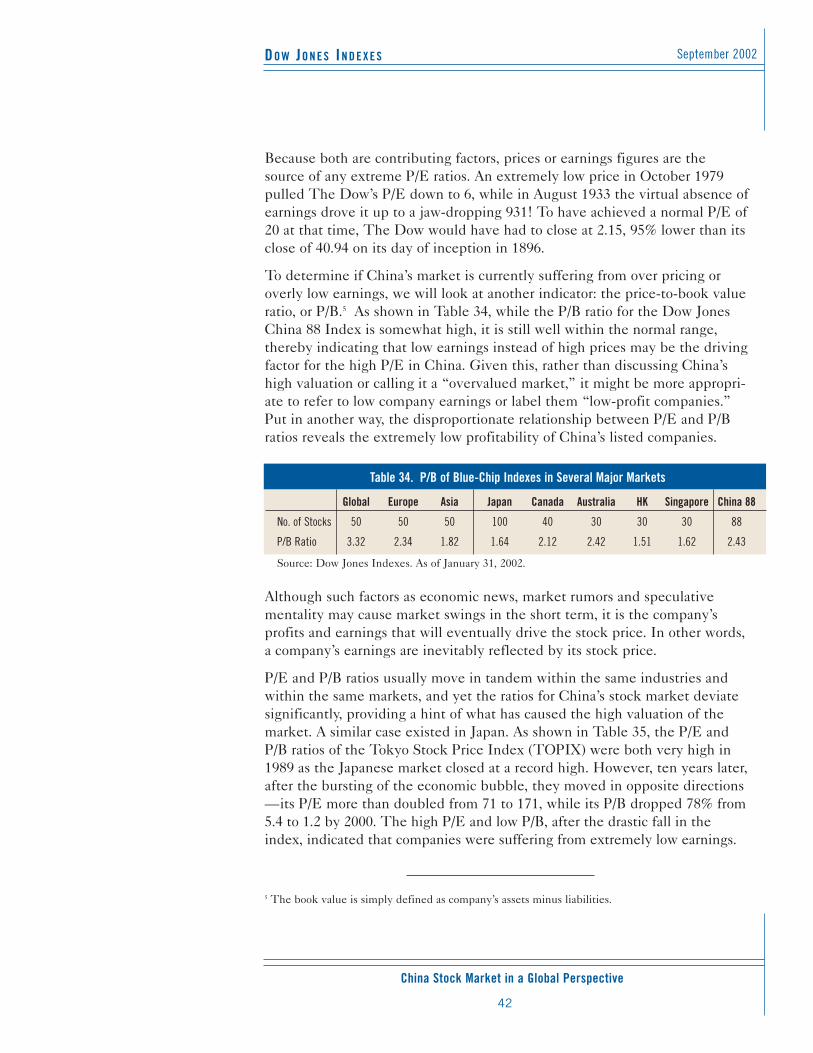

D J INDEXES EPTEMBER CHINA STOCK MARKET IN A GLOBAL PERSPECTIVE

48

Research Report by Sheldon Gao, PhD. Senior Director, Dow Jones Indexes 609-520-4114 [email protected] D OW J ONES I NDEXES CHINA STOCK MARKET IN A GLOBAL PERSPECTIVE S EPTEMBER 2002 Executive Summary China’s stock market has experienced amazing growth since establishing its two exchanges in 1990, although the growth has been uneven and irregular, and the market remains in the early stages of its development. This report seeks to identify the key characteristics of China’s market and how they combine to form the most dynamic and intriguing developing market in the world. The current structure of China’s market is one of its key obstacles to further develop- ment. There are very few stocks that would fit the definition of “blue-chip” trad- ing on China’s mainland exchanges. Whereas most developed markets are domi- nated by a limited number of large-cap stocks, China’s market is cramped by a multitude of small-cap stocks. This feature allows for increased speculation and higher turnover for both investors and indexes, among other problems. A related matter is the reliance of China’s market on external expansion, that is, expansion through the issuance of new shares rather than the appreciation in value of existing stocks. Since these shares generally do not experience sustained growth, often because of market manipulation, they contribute to the dominance of smaller size stocks in China’s market. Ultimately, the current structure is a major obstacle to the creation of viable index-related products in China. Another issue is the fact that, despite the tremendous growth of the stock market, China’s companies are not operating at a high level of profitability. They are plagued by poor earnings and low dividend yields. China’s companies need to increase their profitability if they are to compete in global markets. Finally, government seems to have too much influence on the market. It keeps a tight control on the issuance of IPOs, and, as a result of widespread government hold- ings, many listed companies in China have very low free-float ratios. Meanwhile, due at least in part to the unusual market structure, market manipulation and speculation are common. The solution is simply a matter of strengthening controls in certain areas while relaxing them in others in order to foster an environment in which China’s stock market can continue to thrive.

Transcript of D J INDEXES EPTEMBER CHINA STOCK MARKET IN A GLOBAL PERSPECTIVE

Research Report bySheldon Gao, PhD.Senior Director, Dow [email protected]

DO W JO N E S IN D E X E S

CHINA STOCK MARKET IN A GLOBAL PERSPECTIVE

SE P T E M B E R 2002

Execut ive Summary

China’s stock market has experienced amazing growth since establishing its twoexchanges in 1990, although the growth has been uneven and irregular, and themarket remains in the early stages of its development. This report seeks to identifythe key characteristics of China’s market and how they combine to form the mostdynamic and intriguing developing market in the world.

The current structure of China’s market is one of its key obstacles to further develop-ment. There are very few stocks that would fit the definition of “blue-chip” trad-ing on China’s mainland exchanges. Whereas most developed markets are domi-nated by a limited number of large-cap stocks, China’s market is cramped by amultitude of small-cap stocks. This feature allows for increased speculation andhigher turnover for both investors and indexes, among other problems.

A related matter is the reliance of China’s market on external expansion, that is,expansion through the issuance of new shares rather than the appreciation invalue of existing stocks. Since these shares generally do not experience sustainedgrowth, often because of market manipulation, they contribute to the dominanceof smaller size stocks in China’s market. Ultimately, the current structure is amajor obstacle to the creation of viable index-related products in China.

Another issue is the fact that, despite the tremendous growth of the stock market,China’s companies are not operating at a high level of profitability. They areplagued by poor earnings and low dividend yields. China’s companies need toincrease their profitability if they are to compete in global markets.

Finally, government seems to have too much influence on the market. It keeps a tightcontrol on the issuance of IPOs, and, as a result of widespread government hold-ings, many listed companies in China have very low free-float ratios. Meanwhile,due at least in part to the unusual market structure, market manipulation andspeculation are common. The solution is simply a matter of strengthening controlsin certain areas while relaxing them in others in order to foster an environment inwhich China’s stock market can continue to thrive.

DO W JO N E S IN D E X E S

China Stock Market in a Global Perspective

September 2002

2

CON

TEN

TSCH

ARTS

AND

TAB

LES

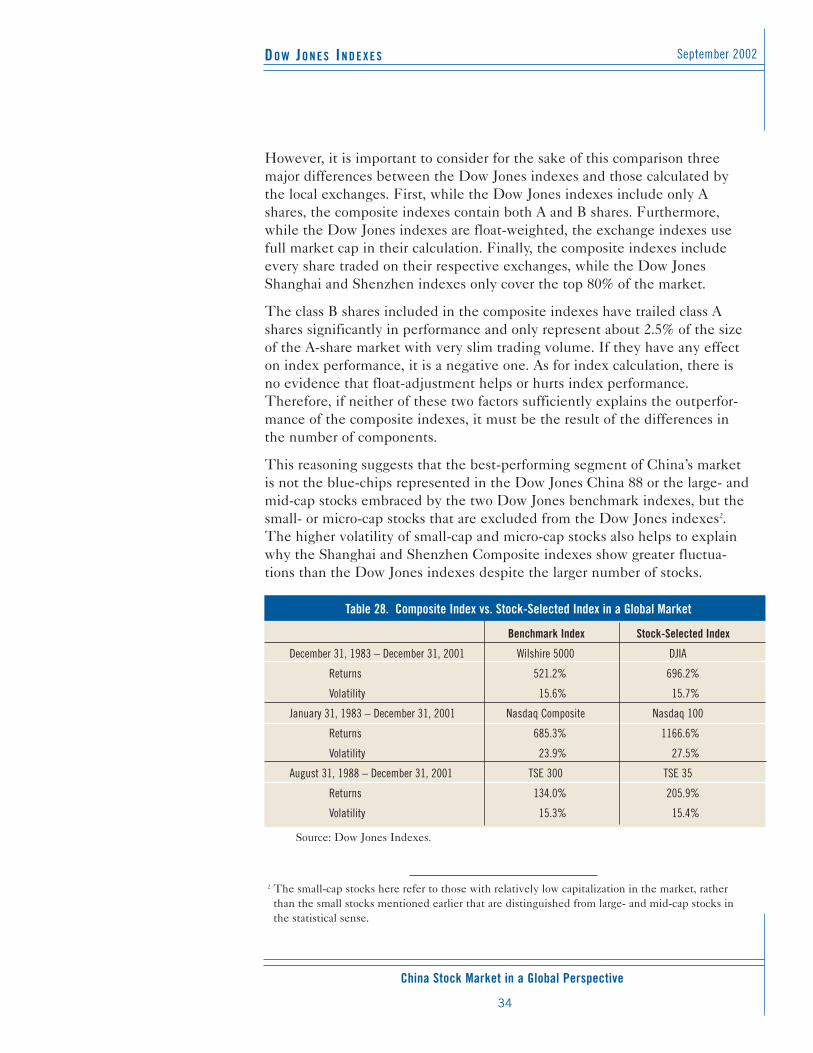

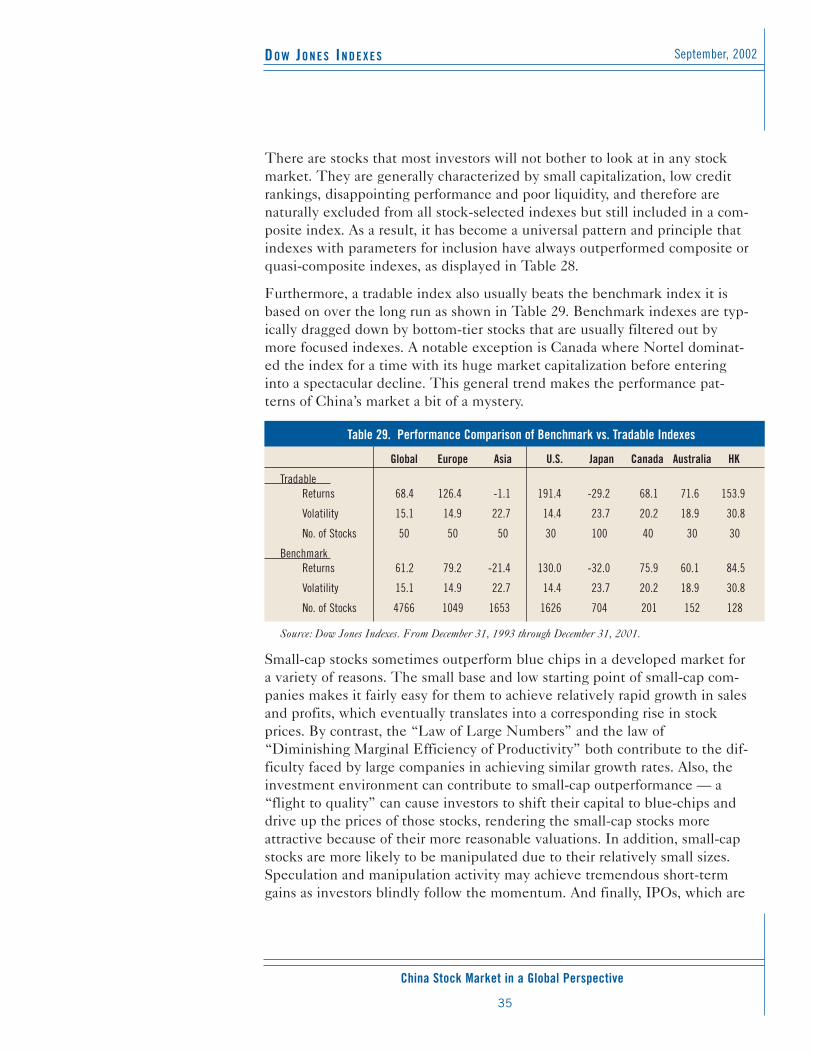

4 Introduction6 Abnormal Performance9 Tremendous Volatility

12 Insulated Market 14 Substantial Government Ownership 17 Irregular Expansion 19 Influence of IPOs 21 Typical Emerging Market24 Pyramid Structure30 Unstable Core33 Outperformance of Micro Stocks36 Incredible Speculation38 Manufacturing Orientation40 Disappointing Earnings of Companies44 Low Dividend Yield47 Conclusions

6 Performance of Major Indexes Worldwide (1994—2001)7 First Eight Years of the Dow Jones China Index8 Ten Biggest Up and Down Days in the China Market 8 Crucial Role of the Ten Best Days in the China Market9 Performance of China Indexes in Domestic and Overseas Markets

10 Volatility of Major Indexes Worldwide (1994—2001)11 Bull and Bear Markets in China (1994—2001)11 Bull and Bear Markets in the U.S. and China (1896—2001)13 Annual Return of Major Indexes Worldwide 13 Correlation Between Major Indexes Worldwide14 Tracking Error Between Major Indexes Worldwide15 Float Ratios of Major Stock Markets Worldwide15 Free-Float Ratios of the China Market (%)

DO W JO N E S IN D E X E S

China Stock Market in a Global Perspective

September, 2002

3

16 Float Ratio vs. Stock Return in China’s Market16 Government Ownership in the U.S. and Japan 18 Stock Market Expansions in the U.S. and China 19 The Role of IPOs in the U.S. and China Stock Markets20 IPO Change vs. Index Performance in China’s Market23 Shareholder Statistics in the U.S. and Japan Stock Markets24 Correlation Between Major China Indexes25 Market Concentration Measured by % of Stocks 26 Market Concentration Measured by # of Stocks 26 Market Coverage of Dow Jones Country Titans Indexes 27 Market Coverage of China Stocks (January 31, 2002)27 Comparison of Market Concentration in China and Rest of the World28 Tracking Error Between Major China Indexes29 Stock Number: Dow Jones Global Indexes and China Indexes30 Turnover Rate of Blue-Chip Indexes in Market Value 31 Turnover of Blue-Chip Indexes in Number of Stocks 32 Benchmark vs. Blue-Chip Indexes in China 33 Performance Comparison of China Indexes (1994 – 2001)34 Composite Index vs. Stock-Selected Index in a Global Market35 Performance Comparison of Benchmark vs. Tradable Indexes37 Turnover Comparison of Several Stock Exchanges 38 Comparison of Sector Representation 39 Sector Representation of China’s Stock Indexes40 P/E of Blue-Chip Indexes in Several Major Markets42 P/B of Blue-Chip Indexes in Several Major Markets43 P/E and P/B of TOPIX in Japan43 Ratio of Stock Market Capitalization Over GDP in China44 Summary of Index Payout Percentage Over the Past Two Years45 Payout Ratio and Dividend Yield of Some Blue-Chip Indexes47 Comparison of Several New Emerging Markets

CHAR

TSAN

DTA

BLE

S(C

ON

TIN

UED

)

DO W JO N E S IN D E X E S

China Stock Market in a Global Perspective

September 2002

4

IntroductionChina’s stock market has experienced tremendous growth and developmentin the ten years since the inceptions of the Shanghai Stock Exchange(December 19, 1990) and the Shenzhen Stock Exchange (December 1, 1990).The number of listed companies reached 1,160 at the end of 2001 — up fromonly 10 companies in the early 1990s — with a total market capitalization of525.6 billion USD. In addition, more than 65 million investment accounts areon record as of the end of 2001.

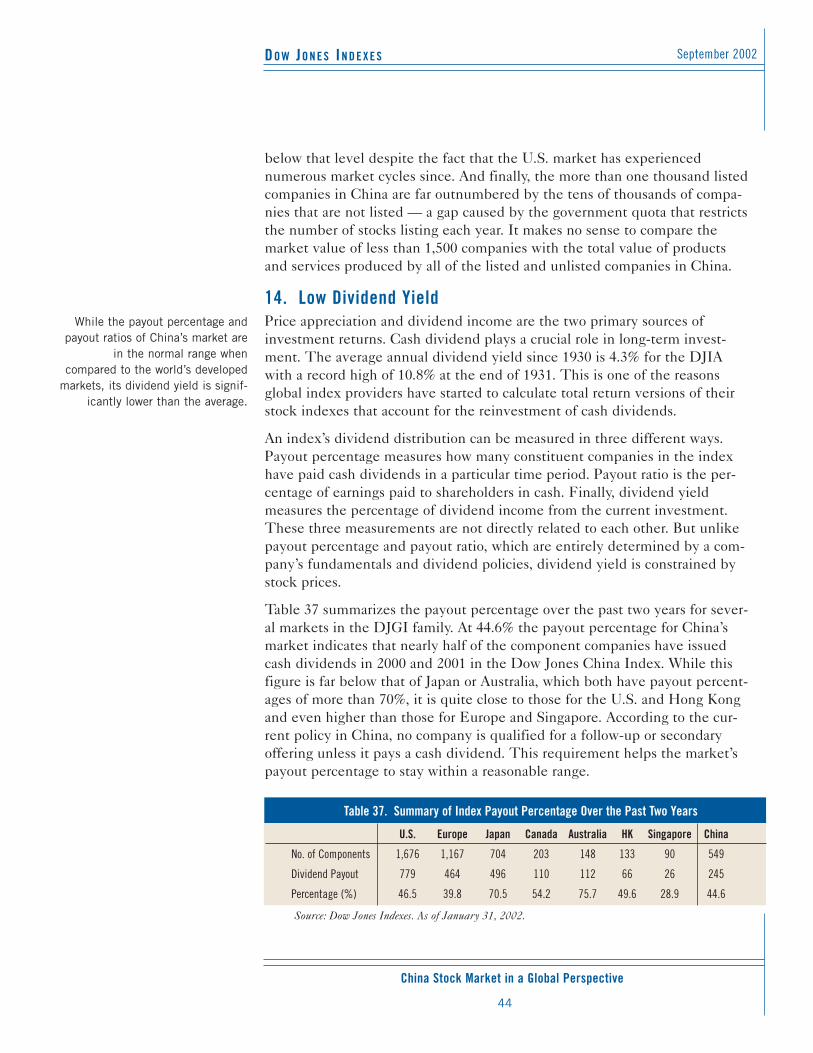

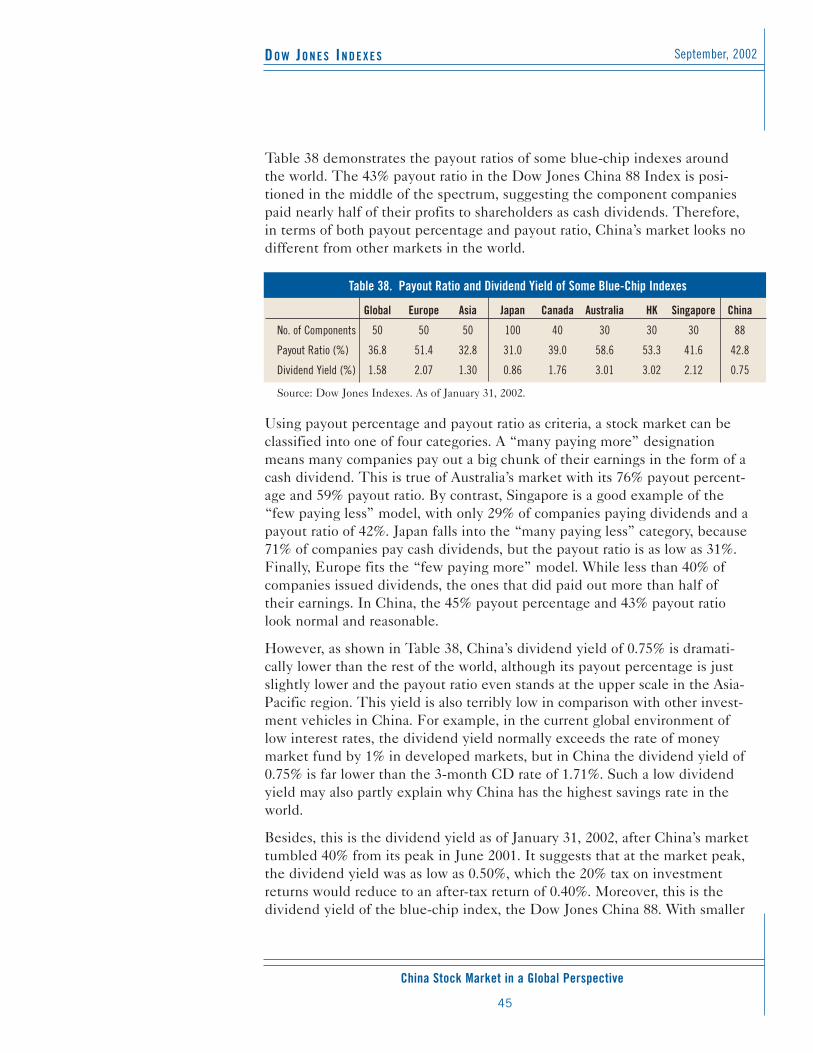

However, two sets of phenomena have been identified in media reports. Oneis the rapid growth of the stock market: almost 1,200 listed companies,swelling numbers of stock investors and the generally upward trend of thelocal stock indexes all indicate that the basic shape of a large country’s stockmarket has formed. The other set of phenomena also deserves the sameattention: an incomplete corporate-governance structure, inadequate regula-tory capacity, intrinsic structural defects of the market, ferocious marketmanipulators and all kinds of traps. In other words, China’s market is still inthe early stages of development. Building a solid foundation and appropriatestructure is pivotal to the consistent long-term growth of China’s financialmarket.

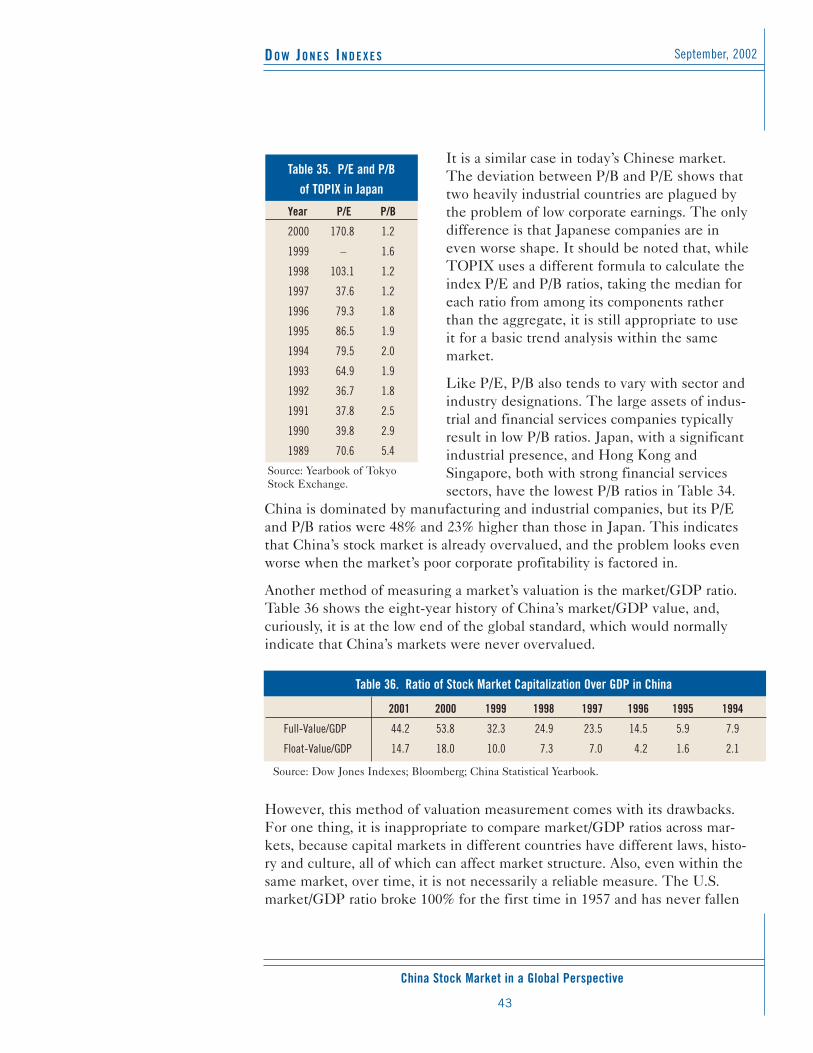

People have been trying to understand this paradox, but have failed to figureout precisely the growth and decline of these two components. This hasmade it difficult to unravel the mystery of China’s stock market. For instance,how high is the price-to-earning ratio (P/E) in China’s market and what kindof stocks have been the driving power of the market? Furthermore, is China’smarket ready for financial derivative products?

On May 26, 1996, the one-hundredth anniversary of the Dow Jones IndustrialAverage (DJIA), Dow Jones & Company introduced its China index series.The first China index series developed by a global index provider, it consistsof four indexes. The Dow Jones Shanghai and Shenzhen Indexes cover about80% of the market capitalization of the Shanghai and Shenzhen Stockexchanges, respectively. The Dow Jones China Index, the composite of theDow Jones Shanghai and Shenzhen indexes, tracks the general trends inChina’s stock market. The Dow Jones China 88 Index, a tradable indexdesigned specifically for investment products and derivatives, is made up ofthe 88 largest and most liquid stocks. With a base value of 100 as of the basedate of December 31, 1993, for each of its indexes, the series includes onlyclass A shares, which are restricted to domestic Chinese investors.

China’s stock market has grownwith amazing rapidity since the

establishment of its two exchangesin 1990. However, that growth has

been extremely irregular and hasnot followed traditional models of

stock-market development. In manyways, it is still in the early stages

of development.

DO W JO N E S IN D E X E S

China Stock Market in a Global Perspective

September, 2002

5

Since the Dow Jones China index series is constructed according to the samerules and concepts as the Dow Jones Global Indexes (DJGI), it provides aunique platform from which to make a direct comparison between China’smarket and major developed markets worldwide.

Using the DJGI and the Dow Jones China Index series as tools, this articlescrutinizes China’s stock market from a global perspective by comparing itsstructural characteristics and movement patterns with those of other marketsaround the world.

DO W JO N E S IN D E X E S

China Stock Market in a Global Perspective

September 2002

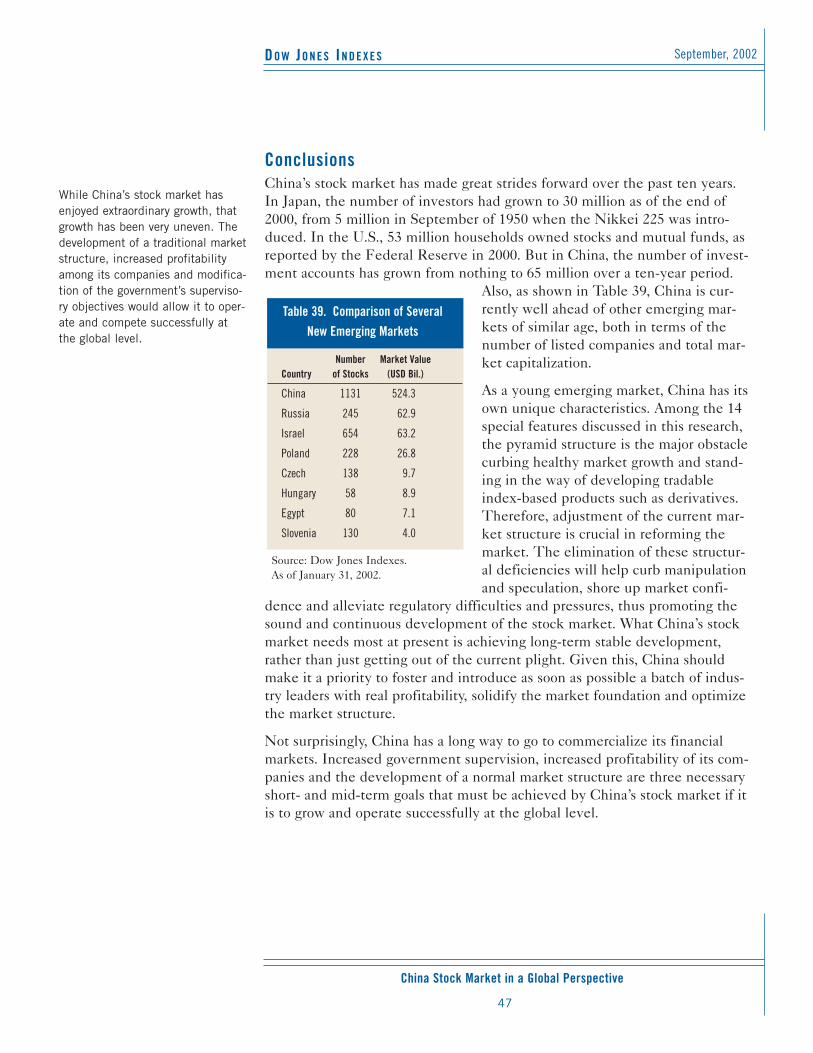

6

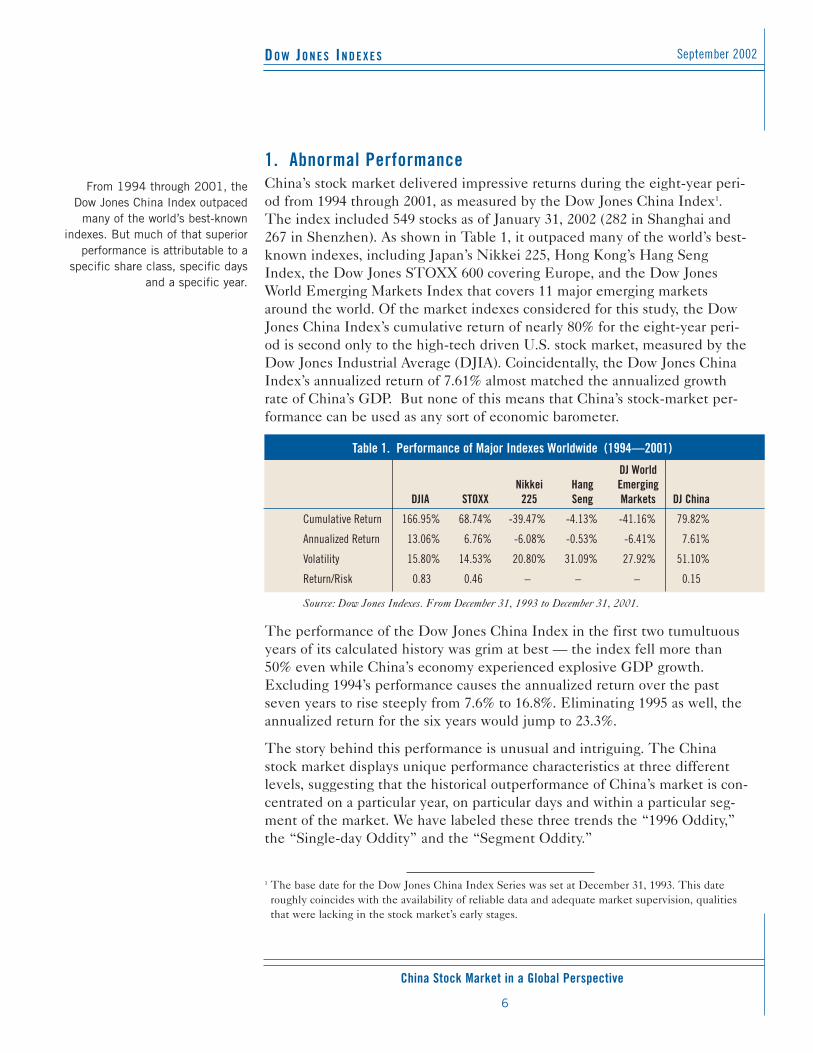

1. Abnormal PerformanceChina’s stock market delivered impressive returns during the eight-year peri-od from 1994 through 2001, as measured by the Dow Jones China Index1.The index included 549 stocks as of January 31, 2002 (282 in Shanghai and267 in Shenzhen). As shown in Table 1, it outpaced many of the world’s best-known indexes, including Japan’s Nikkei 225, Hong Kong’s Hang SengIndex, the Dow Jones STOXX 600 covering Europe, and the Dow JonesWorld Emerging Markets Index that covers 11 major emerging marketsaround the world. Of the market indexes considered for this study, the DowJones China Index’s cumulative return of nearly 80% for the eight-year peri-od is second only to the high-tech driven U.S. stock market, measured by theDow Jones Industrial Average (DJIA). Coincidentally, the Dow Jones ChinaIndex’s annualized return of 7.61% almost matched the annualized growthrate of China’s GDP. But none of this means that China’s stock-market per-formance can be used as any sort of economic barometer.

The performance of the Dow Jones China Index in the first two tumultuousyears of its calculated history was grim at best — the index fell more than50% even while China’s economy experienced explosive GDP growth.Excluding 1994’s performance causes the annualized return over the pastseven years to rise steeply from 7.6% to 16.8%. Eliminating 1995 as well, theannualized return for the six years would jump to 23.3%.

The story behind this performance is unusual and intriguing. The Chinastock market displays unique performance characteristics at three differentlevels, suggesting that the historical outperformance of China’s market is con-centrated on a particular year, on particular days and within a particular seg-ment of the market. We have labeled these three trends the “1996 Oddity,”the “Single-day Oddity” and the “Segment Oddity.”

From 1994 through 2001, the Dow Jones China Index outpaced

many of the world’s best-knownindexes. But much of that superior

performance is attributable to aspecific share class, specific days

and a specific year.

Table 1. Performance of Major Indexes Worldwide (1994—2001)

DJ WorldNikkei Hang Emerging

DJIA STOXX 225 Seng Markets DJ China

Cumulative Return 166.95% 68.74% -39.47% -4.13% -41.16% 79.82%

Annualized Return 13.06% 6.76% -6.08% -0.53% -6.41% 7.61%

Volatility 15.80% 14.53% 20.80% 31.09% 27.92% 51.10%

Return/Risk 0.83 0.46 – – – 0.15

Source: Dow Jones Indexes. From December 31, 1993 to December 31, 2001.

1 The base date for the Dow Jones China Index Series was set at December 31, 1993. This dateroughly coincides with the availability of reliable data and adequate market supervision, qualitiesthat were lacking in the stock market’s early stages.

DO W JO N E S IN D E X E S

China Stock Market in a Global Perspective

September, 2002

7

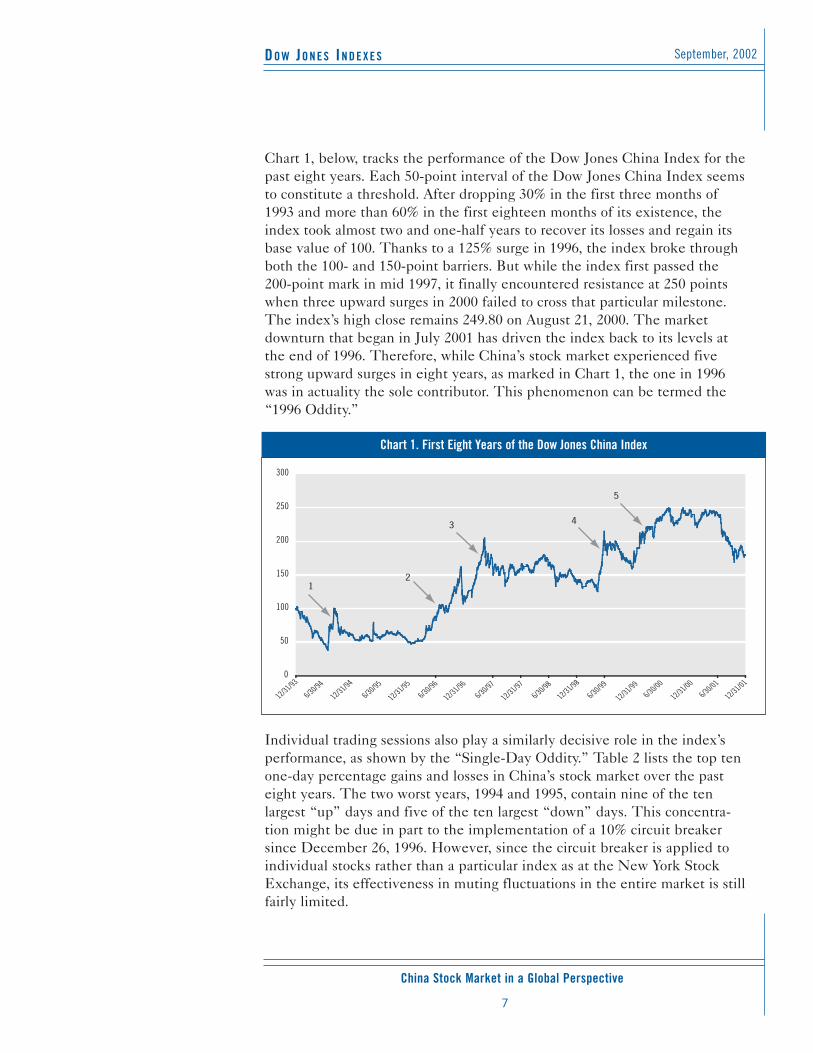

Chart 1, below, tracks the performance of the Dow Jones China Index for thepast eight years. Each 50-point interval of the Dow Jones China Index seemsto constitute a threshold. After dropping 30% in the first three months of1993 and more than 60% in the first eighteen months of its existence, theindex took almost two and one-half years to recover its losses and regain itsbase value of 100. Thanks to a 125% surge in 1996, the index broke throughboth the 100- and 150-point barriers. But while the index first passed the200-point mark in mid 1997, it finally encountered resistance at 250 pointswhen three upward surges in 2000 failed to cross that particular milestone.The index’s high close remains 249.80 on August 21, 2000. The marketdownturn that began in July 2001 has driven the index back to its levels atthe end of 1996. Therefore, while China’s stock market experienced fivestrong upward surges in eight years, as marked in Chart 1, the one in 1996was in actuality the sole contributor. This phenomenon can be termed the“1996 Oddity.”

Individual trading sessions also play a similarly decisive role in the index’sperformance, as shown by the “Single-Day Oddity.” Table 2 lists the top tenone-day percentage gains and losses in China’s stock market over the pasteight years. The two worst years, 1994 and 1995, contain nine of the tenlargest “up” days and five of the ten largest “down” days. This concentra-tion might be due in part to the implementation of a 10% circuit breakersince December 26, 1996. However, since the circuit breaker is applied toindividual stocks rather than a particular index as at the New York StockExchange, its effectiveness in muting fluctuations in the entire market is stillfairly limited.

0

50

100

150

200

250

300

12

5

3 4

12/31/93

6/30/94

12/31/94

6/30/95

6/30/96

6/30/97

6/30/98

12/31/99

12/31/00

12/31/95

12/31/96

12/31/97

12/31/98

6/30/996/30/00

6/30/01

12/31/01

Chart 1. First Eight Years of the Dow Jones China Index

DO W JO N E S IN D E X E S

China Stock Market in a Global Perspective

September 2002

8

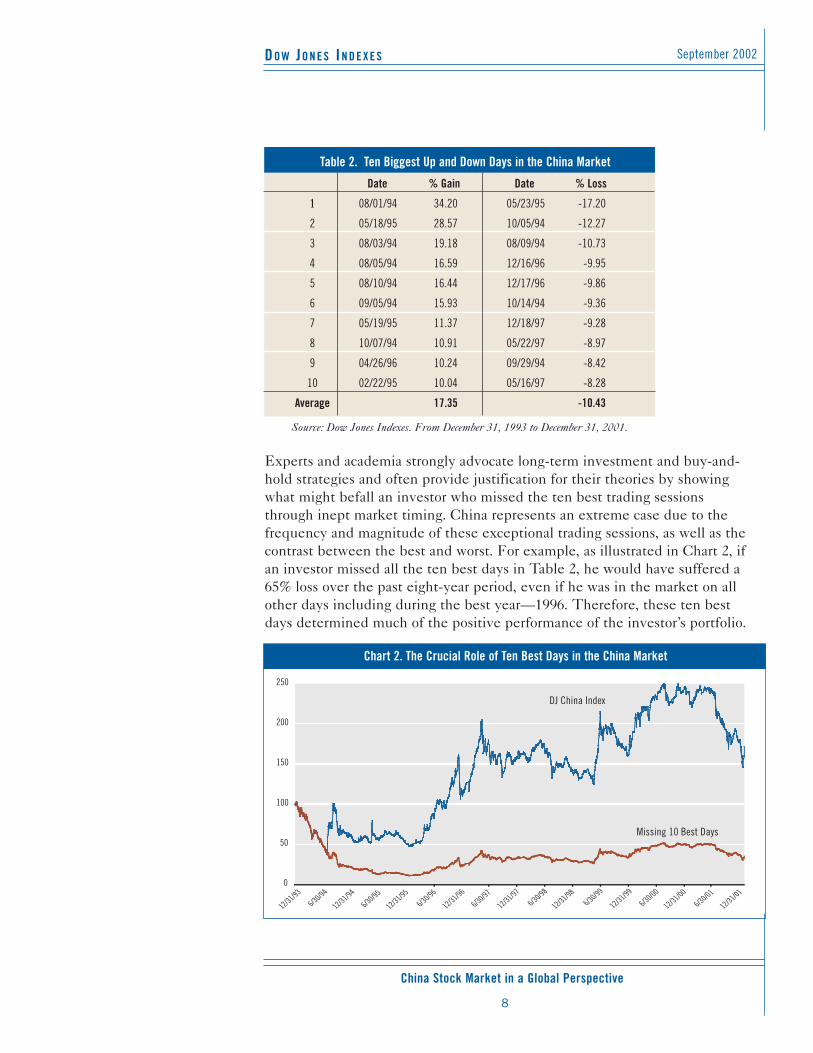

Experts and academia strongly advocate long-term investment and buy-and-hold strategies and often provide justification for their theories by showingwhat might befall an investor who missed the ten best trading sessionsthrough inept market timing. China represents an extreme case due to thefrequency and magnitude of these exceptional trading sessions, as well as thecontrast between the best and worst. For example, as illustrated in Chart 2, ifan investor missed all the ten best days in Table 2, he would have suffered a65% loss over the past eight-year period, even if he was in the market on allother days including during the best year—1996. Therefore, these ten bestdays determined much of the positive performance of the investor’s portfolio.

0

50

100

150

200

250

Missing 10 Best Days

DJ China Index

12/31/93

6/30/94

12/31/94

6/30/956/30/96

6/30/976/30/98

6/30/99

6/30/00

6/30/01

12/31/95

12/31/96

12/31/97

12/31/98

12/31/99

12/31/00

12/31/01

Chart 2. The Crucial Role of Ten Best Days in the China Market

Table 2. Ten Biggest Up and Down Days in the China Market

Date % Gain Date % Loss

1 08/01/94 34.20 05/23/95 -17.20

2 05/18/95 28.57 10/05/94 -12.27

3 08/03/94 19.18 08/09/94 -10.73

4 08/05/94 16.59 12/16/96 -9.95

5 08/10/94 16.44 12/17/96 -9.86

6 09/05/94 15.93 10/14/94 -9.36

7 05/19/95 11.37 12/18/97 -9.28

8 10/07/94 10.91 05/22/97 -8.97

9 04/26/96 10.24 09/29/94 -8.42

10 02/22/95 10.04 05/16/97 -8.28

Average 17.35 -10.43

Source: Dow Jones Indexes. From December 31, 1993 to December 31, 2001.

DO W JO N E S IN D E X E S

China Stock Market in a Global Perspective

September, 2002

9

China’s stock market displayedextreme volatility during the eight

years from 1994 through 2001: anaverage of 51.10% for the Dow

Jones China Index versus 15.80%for the Dow Jones IndustrialAverage. Bear markets also

occurred much more frequently inthe Dow Jones China Index but

were of shorter duration than thoseregistered by the DJIA.

At the market level, deviations among the performances of China’s indexescovering different segments and serving different investor groups also reflectthe unusual nature of China’s stock market. We call this “Segment Oddity.”In addition to the aforementioned four A-share stock indexes, Dow Jones alsodeveloped the Dow Jones China Offshore Index, which covers all shares ofChinese companies with non-RMB denominations that are available to globalinvestors such as class B and H shares and red-chips traded in Hong Kong.With a base value of 100 as of December 31, 1991, this index covers 80% ofthe total universe and of each sector and had 59 components as of April 30,2002.

As demonstrated in Chart 3, in contrast to the approximately 80% gain on theDow Jones China Index, the Dow Jones China Offshore Index fell 35% overthe same eight-year period, or 5.24% per year on the average. Worse still, the30-stock China Free Trade Stock Index derived from the Morgan StanleyCapital International (MSCI) China-Free Index tumbled more than 87% inthe same time period.

2. Tremendous Volatility It is a generally accepted premise in the investment world that higher returnis accompanied by higher volatility. The efficient-frontier curve, whichreflects this intrinsic relationship, is also the foundation for modern invest-ment portfolio theory. These rules hold true in China, despite the uniquenature of its stock market.

As shown below in Table 3, along with fairly impressive returns over the pasteight years, China’s stock market also demonstrates exceptionally high

12/1/936/1/94

12/1/946/1/95

6/1/966/1/97

6/1/98

6/1/996/1/00

6/1/0112/1/95

12/1/96

12/1/97

12/1/98

12/1/99

12/1/0012/1/01

0

50

100

150

200

250

DJ China Index

MSCI China-Free Index

DJ China Offshore Index

Chart 3. Performance of China Indexes in Domestic and Overseas Markets

DO W JO N E S IN D E X E S

China Stock Market in a Global Perspective

September 2002

10

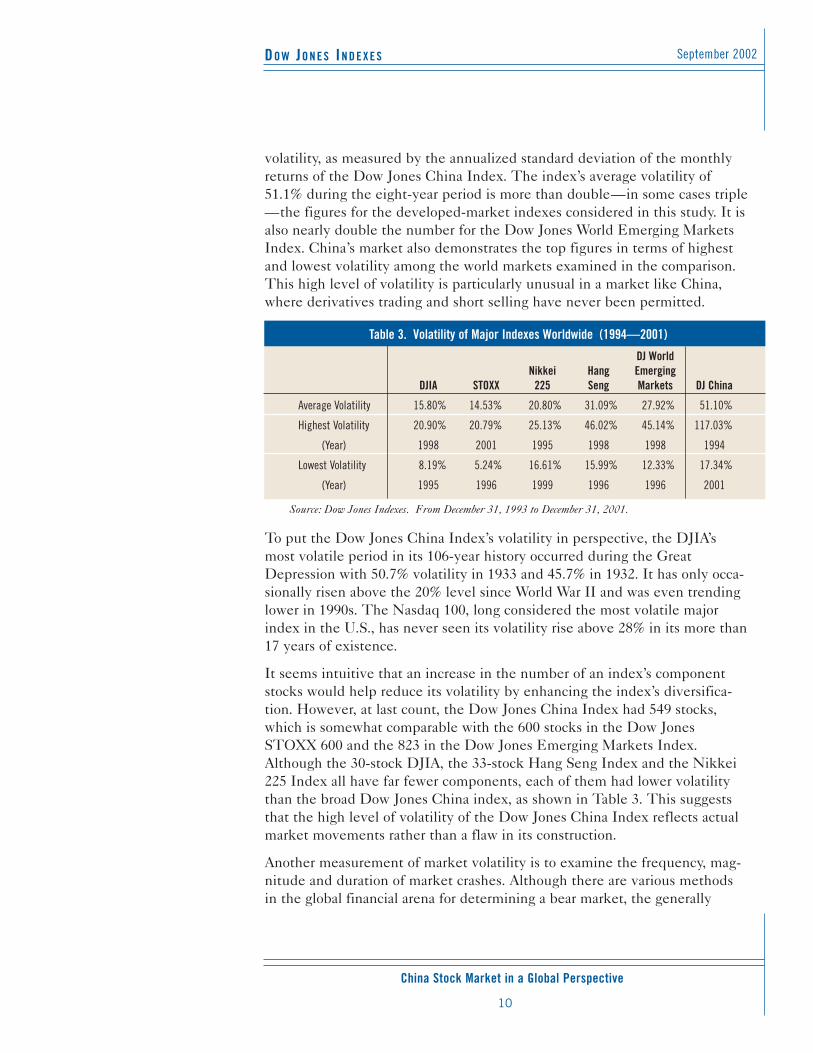

volatility, as measured by the annualized standard deviation of the monthlyreturns of the Dow Jones China Index. The index’s average volatility of51.1% during the eight-year period is more than double—in some cases triple—the figures for the developed-market indexes considered in this study. It isalso nearly double the number for the Dow Jones World Emerging MarketsIndex. China’s market also demonstrates the top figures in terms of highestand lowest volatility among the world markets examined in the comparison.This high level of volatility is particularly unusual in a market like China,where derivatives trading and short selling have never been permitted.

To put the Dow Jones China Index’s volatility in perspective, the DJIA’smost volatile period in its 106-year history occurred during the GreatDepression with 50.7% volatility in 1933 and 45.7% in 1932. It has only occa-sionally risen above the 20% level since World War II and was even trendinglower in 1990s. The Nasdaq 100, long considered the most volatile majorindex in the U.S., has never seen its volatility rise above 28% in its more than17 years of existence.

It seems intuitive that an increase in the number of an index’s componentstocks would help reduce its volatility by enhancing the index’s diversifica-tion. However, at last count, the Dow Jones China Index had 549 stocks,which is somewhat comparable with the 600 stocks in the Dow JonesSTOXX 600 and the 823 in the Dow Jones Emerging Markets Index.Although the 30-stock DJIA, the 33-stock Hang Seng Index and the Nikkei225 Index all have far fewer components, each of them had lower volatilitythan the broad Dow Jones China index, as shown in Table 3. This suggeststhat the high level of volatility of the Dow Jones China Index reflects actualmarket movements rather than a flaw in its construction.

Another measurement of market volatility is to examine the frequency, mag-nitude and duration of market crashes. Although there are various methodsin the global financial arena for determining a bear market, the generally

Table 3. Volatility of Major Indexes Worldwide (1994—2001)

DJ WorldNikkei Hang Emerging

DJIA STOXX 225 Seng Markets DJ China

Average Volatility 15.80% 14.53% 20.80% 31.09% 27.92% 51.10%

Highest Volatility 20.90% 20.79% 25.13% 46.02% 45.14% 117.03%

(Year) 1998 2001 1995 1998 1998 1994

Lowest Volatility 8.19% 5.24% 16.61% 15.99% 12.33% 17.34%

(Year) 1995 1996 1999 1996 1996 2001

Source: Dow Jones Indexes. From December 31, 1993 to December 31, 2001.

DO W JO N E S IN D E X E S

China Stock Market in a Global Perspective

September, 2002

11

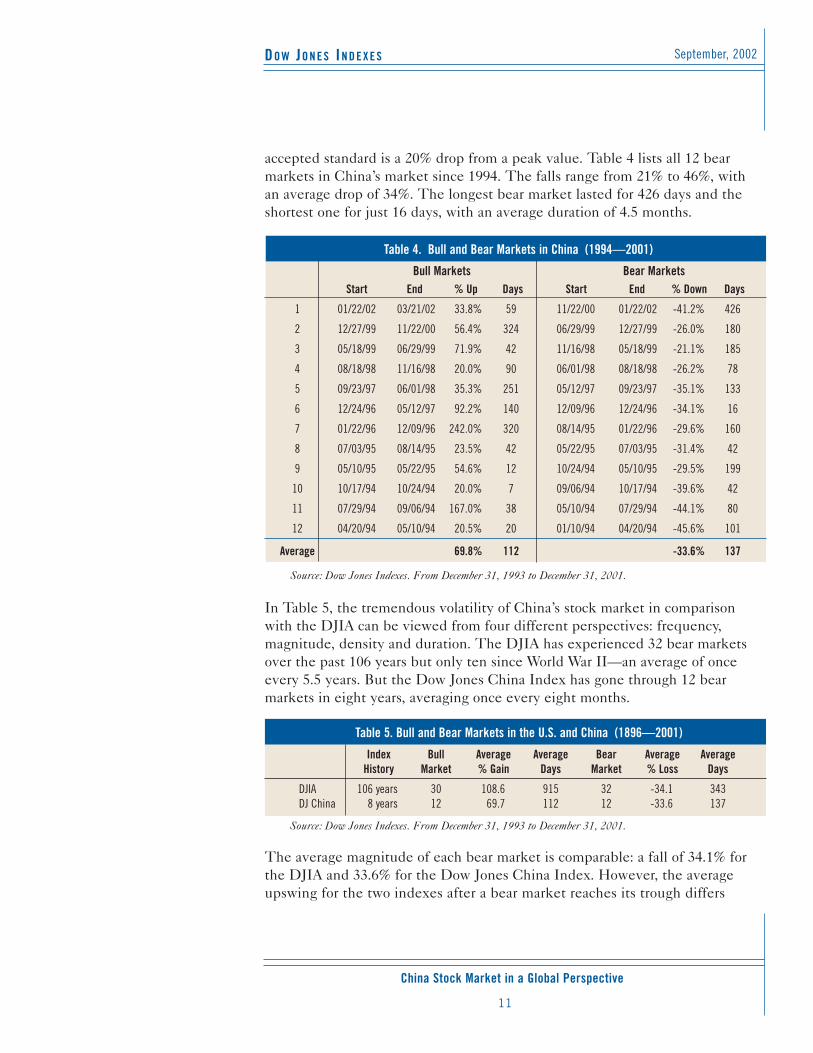

accepted standard is a 20% drop from a peak value. Table 4 lists all 12 bearmarkets in China’s market since 1994. The falls range from 21% to 46%, withan average drop of 34%. The longest bear market lasted for 426 days and theshortest one for just 16 days, with an average duration of 4.5 months.

In Table 5, the tremendous volatility of China’s stock market in comparisonwith the DJIA can be viewed from four different perspectives: frequency,magnitude, density and duration. The DJIA has experienced 32 bear marketsover the past 106 years but only ten since World War II—an average of onceevery 5.5 years. But the Dow Jones China Index has gone through 12 bearmarkets in eight years, averaging once every eight months.

The average magnitude of each bear market is comparable: a fall of 34.1% forthe DJIA and 33.6% for the Dow Jones China Index. However, the averageupswing for the two indexes after a bear market reaches its trough differs

Table 4. Bull and Bear Markets in China (1994—2001)

Bull Markets Bear MarketsStart End % Up Days Start End % Down Days

1 01/22/02 03/21/02 33.8% 59 11/22/00 01/22/02 -41.2% 426

2 12/27/99 11/22/00 56.4% 324 06/29/99 12/27/99 -26.0% 180

3 05/18/99 06/29/99 71.9% 42 11/16/98 05/18/99 -21.1% 185

4 08/18/98 11/16/98 20.0% 90 06/01/98 08/18/98 -26.2% 78

5 09/23/97 06/01/98 35.3% 251 05/12/97 09/23/97 -35.1% 133

6 12/24/96 05/12/97 92.2% 140 12/09/96 12/24/96 -34.1% 16

7 01/22/96 12/09/96 242.0% 320 08/14/95 01/22/96 -29.6% 160

8 07/03/95 08/14/95 23.5% 42 05/22/95 07/03/95 -31.4% 42

9 05/10/95 05/22/95 54.6% 12 10/24/94 05/10/95 -29.5% 199

10 10/17/94 10/24/94 20.0% 7 09/06/94 10/17/94 -39.6% 42

11 07/29/94 09/06/94 167.0% 38 05/10/94 07/29/94 -44.1% 80

12 04/20/94 05/10/94 20.5% 20 01/10/94 04/20/94 -45.6% 101

Average 69.8% 112 -33.6% 137

Source: Dow Jones Indexes. From December 31, 1993 to December 31, 2001.

Table 5. Bull and Bear Markets in the U.S. and China (1896—2001)

Index Bull Average Average Bear Average AverageHistory Market % Gain Days Market % Loss Days

DJIA 106 years 30 108.6 915 32 -34.1 343DJ China 8 years 12 69.7 112 12 -33.6 137

Source: Dow Jones Indexes. From December 31, 1993 to December 31, 2001.

DO W JO N E S IN D E X E S

China Stock Market in a Global Perspective

September 2002

12

The isolation of China’s stock market can be attributed to the

government’s currency shield andthe existence of separate share

classes for foreign and domesticinvestors. In comparison with othermarkets, China displays low corre-

lation and high tracking error.

significantly: a 108.6% rise for the DJIA but only a 69.7% rise for the DowJones China Index. During the Depression, the DJIA experienced two bear markets every yearin three consecutive years from 1931 through 1933—its densest concentra-tion of bear-market occurrences ever. By contrast, as demonstrated in Table4, China’s market witnessed a bear market three times in 1994, and two timeseach in 1995, 1996 and 1999.

Finally, a bull market is much longer than a bear market in the U.S.—915 vs.343 days, but a bull market is even shorter than a bear market in China—112vs. 137 days. Put another way, while the average length of a bear market inthe U.S. is almost three times that of one in China—343 vs. 137 days—thebull market in the U.S. is more than eight times longer that in China—915vs. 112 days.

Volatility is generally a negative characteristic as far as financial investmentsare concerned. It plays havoc with compound earnings, for one thing, but alsoencourages a speculative mentality in investors who are led to make short-term bets rather than long-term investments.

As a developing market, China’s economy is growing at a very fast pace,allowing its stock market to deliver strong returns, despite its extreme volatil-ity. The Dow Jones China Index rose 49% in 2000—the last time the DJIAexperienced such gains for a calendar year was 1933. And while the DJIA’srecord percentage increase for a calendar year is 81.7% in 1915, the DowJones China Index far outstrips that figure with a 125% rise in 1996.

3. Insulated Market In China, class A shares—the shares restricted to domestic investors—arelisted on either the Shanghai or Shenzhen exchanges and are denominated inRenminbi (RMB), which are not freely convertible to any international cur-rencies. Chinese investors cannot buy shares listed in Hong Kong and over-seas, and foreign investors are not allowed to trade class A shares. The class Bshares that were created specifically for foreign investors have been availableto local Chinese investors since Spring 2001, but their market hardly com-pares with that of the A shares. The number of class B shares, 112, is lessthan 10% the number of A-shares (1,160), and the B-share market’s total mar-ket value is only 2.4% of the A-share market’s value. The long-term perform-ance of the B-share market also lags far behind that of the A-share market.

Market segregation and the currency shield helped China to protect its econ-omy and markets during the Asian economic crisis of 1997 and the globalfinancial turmoil of 1998, but they remain a barrier between China’s capitalmarkets and international investors. The astonishing degree of this insulationis revealed in an index-performance comparison.

DO W JO N E S IN D E X E S

China Stock Market in a Global Perspective

September, 2002

13

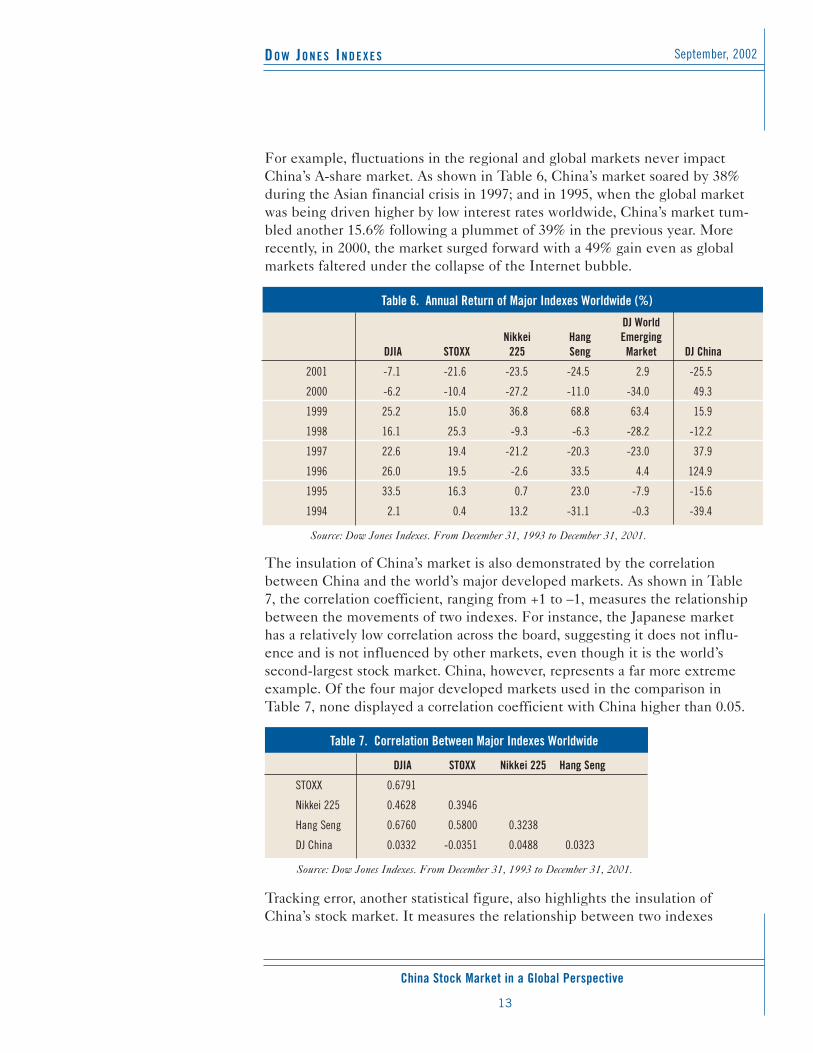

For example, fluctuations in the regional and global markets never impactChina’s A-share market. As shown in Table 6, China’s market soared by 38%during the Asian financial crisis in 1997; and in 1995, when the global marketwas being driven higher by low interest rates worldwide, China’s market tum-bled another 15.6% following a plummet of 39% in the previous year. Morerecently, in 2000, the market surged forward with a 49% gain even as globalmarkets faltered under the collapse of the Internet bubble.

The insulation of China’s market is also demonstrated by the correlationbetween China and the world’s major developed markets. As shown in Table7, the correlation coefficient, ranging from +1 to –1, measures the relationshipbetween the movements of two indexes. For instance, the Japanese markethas a relatively low correlation across the board, suggesting it does not influ-ence and is not influenced by other markets, even though it is the world’ssecond-largest stock market. China, however, represents a far more extremeexample. Of the four major developed markets used in the comparison inTable 7, none displayed a correlation coefficient with China higher than 0.05.

Tracking error, another statistical figure, also highlights the insulation ofChina’s stock market. It measures the relationship between two indexes

Table 6. Annual Return of Major Indexes Worldwide (%)

DJ WorldNikkei Hang Emerging

DJIA STOXX 225 Seng Market DJ China

2001 -7.1 -21.6 -23.5 -24.5 2.9 -25.5

2000 -6.2 -10.4 -27.2 -11.0 -34.0 49.3

1999 25.2 15.0 36.8 68.8 63.4 15.9

1998 16.1 25.3 -9.3 -6.3 -28.2 -12.2

1997 22.6 19.4 -21.2 -20.3 -23.0 37.9

1996 26.0 19.5 -2.6 33.5 4.4 124.9

1995 33.5 16.3 0.7 23.0 -7.9 -15.6

1994 2.1 0.4 13.2 -31.1 -0.3 -39.4

Source: Dow Jones Indexes. From December 31, 1993 to December 31, 2001.

Table 7. Correlation Between Major Indexes Worldwide

DJIA STOXX Nikkei 225 Hang Seng

STOXX 0.6791

Nikkei 225 0.4628 0.3946

Hang Seng 0.6760 0.5800 0.3238

DJ China 0.0332 -0.0351 0.0488 0.0323

Source: Dow Jones Indexes. From December 31, 1993 to December 31, 2001.

DO W JO N E S IN D E X E S

China Stock Market in a Global Perspective

September 2002

14

Due to widespread governmentownership, China has a very lowfloat ratio, averaging just under30% from 1993 through 2001.

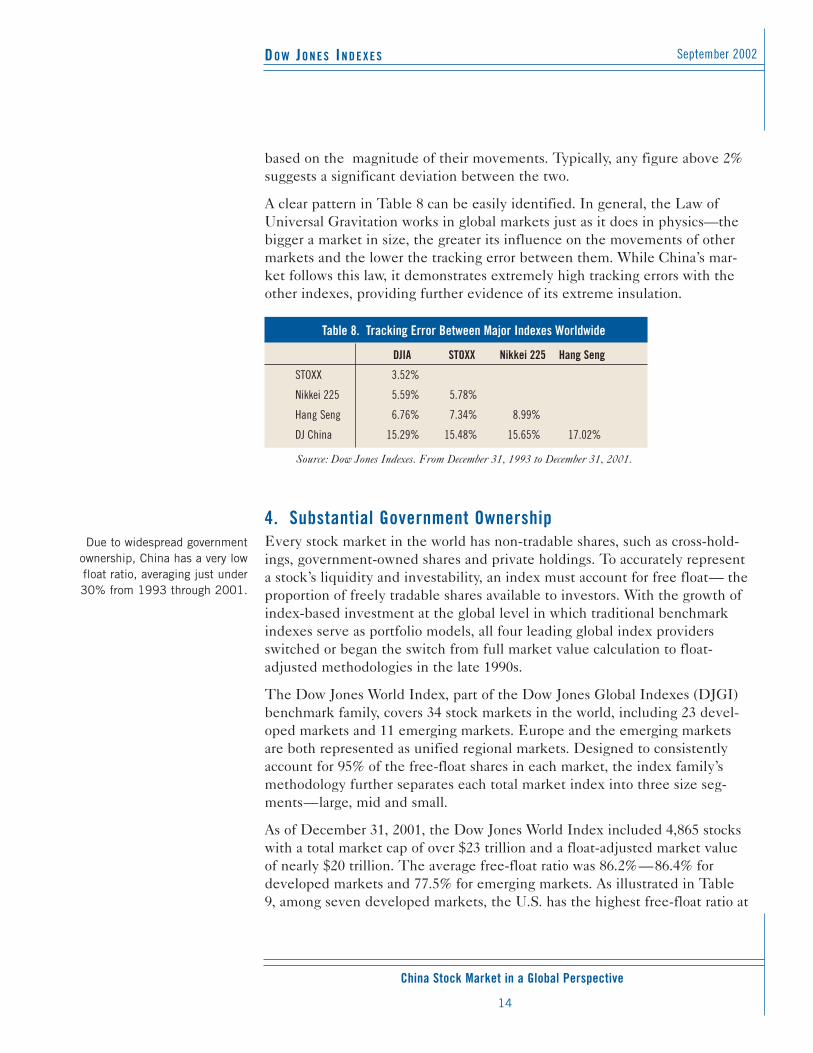

based on the magnitude of their movements. Typically, any figure above 2%suggests a significant deviation between the two.

A clear pattern in Table 8 can be easily identified. In general, the Law ofUniversal Gravitation works in global markets just as it does in physics—thebigger a market in size, the greater its influence on the movements of othermarkets and the lower the tracking error between them. While China’s mar-ket follows this law, it demonstrates extremely high tracking errors with theother indexes, providing further evidence of its extreme insulation.

4. Substantial Government Ownership Every stock market in the world has non-tradable shares, such as cross-hold-ings, government-owned shares and private holdings. To accurately representa stock’s liquidity and investability, an index must account for free float— theproportion of freely tradable shares available to investors. With the growth ofindex-based investment at the global level in which traditional benchmarkindexes serve as portfolio models, all four leading global index providersswitched or began the switch from full market value calculation to float-adjusted methodologies in the late 1990s.

The Dow Jones World Index, part of the Dow Jones Global Indexes (DJGI)benchmark family, covers 34 stock markets in the world, including 23 devel-oped markets and 11 emerging markets. Europe and the emerging marketsare both represented as unified regional markets. Designed to consistentlyaccount for 95% of the free-float shares in each market, the index family’smethodology further separates each total market index into three size seg-ments—large, mid and small.

As of December 31, 2001, the Dow Jones World Index included 4,865 stockswith a total market cap of over $23 trillion and a float-adjusted market valueof nearly $20 trillion. The average free-float ratio was 86.2%—86.4% fordeveloped markets and 77.5% for emerging markets. As illustrated in Table9, among seven developed markets, the U.S. has the highest free-float ratio at

Table 8. Tracking Error Between Major Indexes Worldwide

DJIA STOXX Nikkei 225 Hang Seng

STOXX 3.52%

Nikkei 225 5.59% 5.78%

Hang Seng 6.76% 7.34% 8.99%

DJ China 15.29% 15.48% 15.65% 17.02%

Source: Dow Jones Indexes. From December 31, 1993 to December 31, 2001.

DO W JO N E S IN D E X E S

China Stock Market in a Global Perspective

September, 2002

15

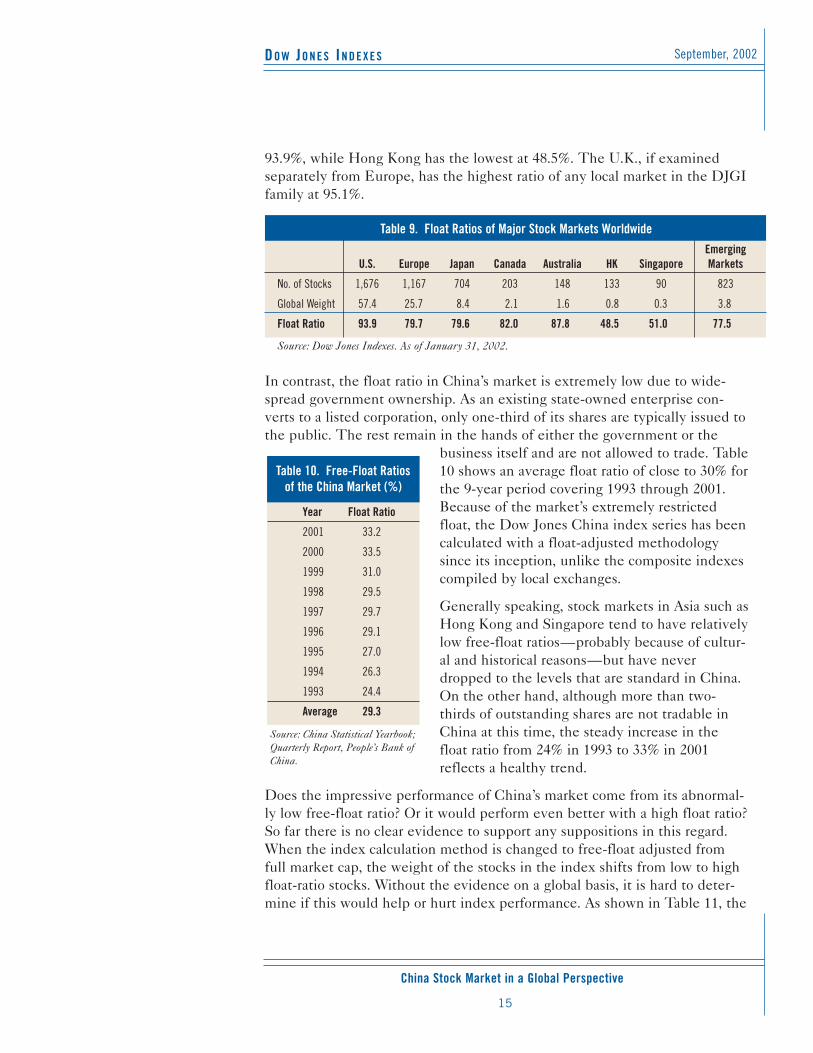

93.9%, while Hong Kong has the lowest at 48.5%. The U.K., if examinedseparately from Europe, has the highest ratio of any local market in the DJGIfamily at 95.1%.

In contrast, the float ratio in China’s market is extremely low due to wide-spread government ownership. As an existing state-owned enterprise con-verts to a listed corporation, only one-third of its shares are typically issued tothe public. The rest remain in the hands of either the government or the

business itself and are not allowed to trade. Table10 shows an average float ratio of close to 30% forthe 9-year period covering 1993 through 2001.Because of the market’s extremely restrictedfloat, the Dow Jones China index series has beencalculated with a float-adjusted methodologysince its inception, unlike the composite indexescompiled by local exchanges.

Generally speaking, stock markets in Asia such asHong Kong and Singapore tend to have relativelylow free-float ratios—probably because of cultur-al and historical reasons—but have neverdropped to the levels that are standard in China.On the other hand, although more than two-thirds of outstanding shares are not tradable inChina at this time, the steady increase in thefloat ratio from 24% in 1993 to 33% in 2001reflects a healthy trend.

Does the impressive performance of China’s market come from its abnormal-ly low free-float ratio? Or it would perform even better with a high float ratio?So far there is no clear evidence to support any suppositions in this regard.When the index calculation method is changed to free-float adjusted fromfull market cap, the weight of the stocks in the index shifts from low to highfloat-ratio stocks. Without the evidence on a global basis, it is hard to deter-mine if this would help or hurt index performance. As shown in Table 11, the

Table 9. Float Ratios of Major Stock Markets WorldwideEmerging

U.S. Europe Japan Canada Australia HK Singapore Markets

No. of Stocks 1,676 1,167 704 203 148 133 90 823

Global Weight 57.4 25.7 8.4 2.1 1.6 0.8 0.3 3.8

Float Ratio 93.9 79.7 79.6 82.0 87.8 48.5 51.0 77.5

Source: Dow Jones Indexes. As of January 31, 2002.

Year Float Ratio

2001 33.2

2000 33.5

1999 31.0

1998 29.5

1997 29.7

1996 29.1

1995 27.0

1994 26.3

1993 24.4

Average 29.3

Table 10. Free-Float Ratios of the China Market (%)

Source: China Statistical Yearbook; Quarterly Report, People’s Bank ofChina.

DO W JO N E S IN D E X E S

China Stock Market in a Global Perspective

September 2002

16

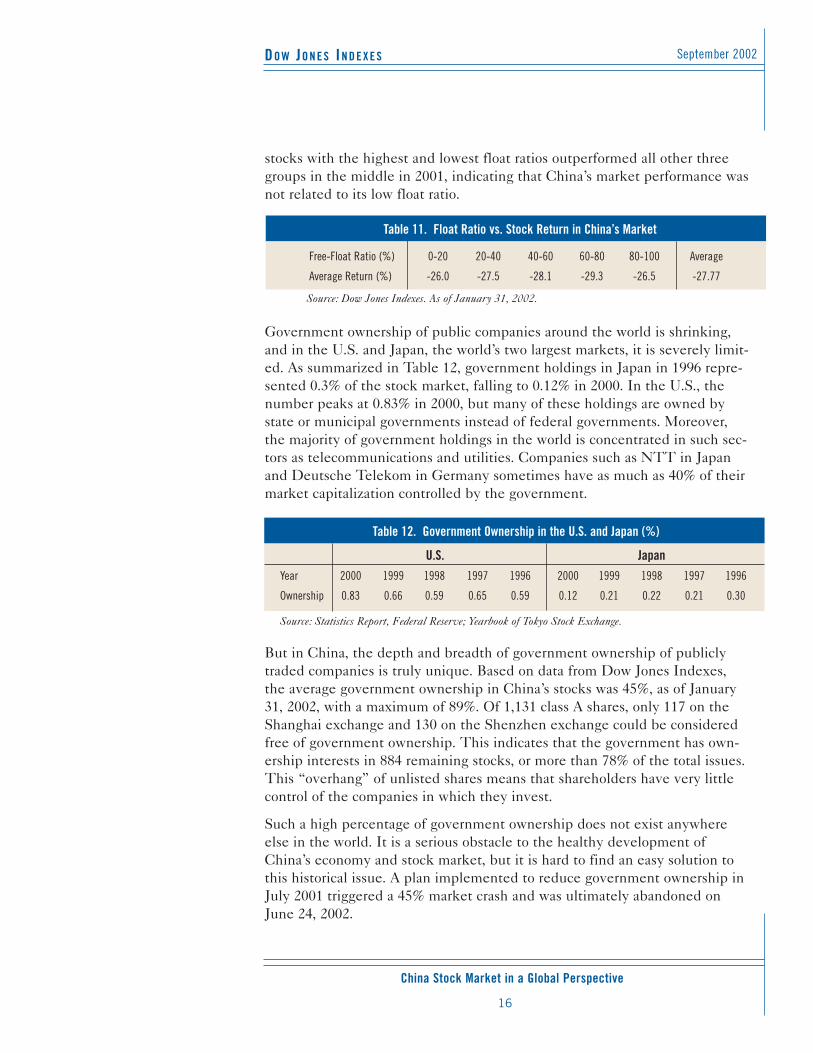

stocks with the highest and lowest float ratios outperformed all other threegroups in the middle in 2001, indicating that China’s market performance wasnot related to its low float ratio.

Government ownership of public companies around the world is shrinking,and in the U.S. and Japan, the world’s two largest markets, it is severely limit-ed. As summarized in Table 12, government holdings in Japan in 1996 repre-sented 0.3% of the stock market, falling to 0.12% in 2000. In the U.S., thenumber peaks at 0.83% in 2000, but many of these holdings are owned bystate or municipal governments instead of federal governments. Moreover,the majority of government holdings in the world is concentrated in such sec-tors as telecommunications and utilities. Companies such as NTT in Japanand Deutsche Telekom in Germany sometimes have as much as 40% of theirmarket capitalization controlled by the government.

But in China, the depth and breadth of government ownership of publiclytraded companies is truly unique. Based on data from Dow Jones Indexes,the average government ownership in China’s stocks was 45%, as of January31, 2002, with a maximum of 89%. Of 1,131 class A shares, only 117 on theShanghai exchange and 130 on the Shenzhen exchange could be consideredfree of government ownership. This indicates that the government has own-ership interests in 884 remaining stocks, or more than 78% of the total issues.This “overhang” of unlisted shares means that shareholders have very littlecontrol of the companies in which they invest.

Such a high percentage of government ownership does not exist anywhereelse in the world. It is a serious obstacle to the healthy development ofChina’s economy and stock market, but it is hard to find an easy solution tothis historical issue. A plan implemented to reduce government ownership inJuly 2001 triggered a 45% market crash and was ultimately abandoned onJune 24, 2002.

Table 11. Float Ratio vs. Stock Return in China’s Market

Free-Float Ratio (%) 0-20 20-40 40-60 60-80 80-100 Average

Average Return (%) -26.0 -27.5 -28.1 -29.3 -26.5 -27.77

Source: Dow Jones Indexes. As of January 31, 2002.

Table 12. Government Ownership in the U.S. and Japan (%)

U.S. JapanYear 2000 1999 1998 1997 1996 2000 1999 1998 1997 1996

Ownership 0.83 0.66 0.59 0.65 0.59 0.12 0.21 0.22 0.21 0.30

Source: Statistics Report, Federal Reserve; Yearbook of Tokyo Stock Exchange.

DO W JO N E S IN D E X E S

China Stock Market in a Global Perspective

September, 2002

17

While most stock markets grow primarily through the appreciation

of stock values, China’s marketgrowth mainly has been the result

of new share issuances, or externalexpansion.

Like all other economic phenomena, the valuation of a stock market isdependent on the equilibrium of supply and demand. A sudden boom insupply—in this case, the availability of stocks for trading—inevitably leads toa market drop if demand fails to increase accordingly. There is the possibilitythat a shift from full market-cap weighting to float-adjusted weighting by anindex provider could cause a disturbance in the marketplace by flooding themarket with shares as investors shift their portfolios to reflect the indexes.Faced with an explosion of available shares, any market would be at risk of acollapse. For example, if all family-owned shares were put on the market inHong Kong, float shares would almost double, an effect the Hong Kong mar-ket would find hard to bear. A case in point is the Tracker Fund of HongKong, the first exchange-traded fund (ETF) in the Asia Pacific. It was origi-nally created as a vehicle for the Hong Kong government to unload theshares it bought during the financial turmoil in 1998 to maintain market sta-bility. Since its launch in November 1999, the Hong Kong market has alwaysdropped significantly before its quarterly issuance.

5. Irregular Expansion There are only two modes for the growth of stock market size. One is theissuance of new shares such as IPOs, secondary offerings and follow-up offer-ings, and the other is the appreciation of existing stocks. The former is con-sidered external expansion, while the latter is viewed as internal growth.While both are driving factors for the growth of any stock market, the rapidgrowth of China’s market primarily has relied on external expansion. In mostcases worldwide, the opposite has been the true.

Every index has a divisor, which can be adjusted to filter out the impact fromcomponent changes and corporate actions such as stock splits and spin-offs inorder to maintain the continuity and consistency of the index. With a divisorin position, the performance of a benchmark index that covers a consistentportion of a market—say 80%—can be used as an indicator of the market’sinternal growth; the growth difference between the index and the total valueof the stock market measures the market’s external expansion. Since IPOsare not immediately included in stock indexes, their value would be includedin the value of the entire stock market but not in the value of the index.However, external expansion does not necessarily mean that market itself hasexpanded in size. Often the introduction of new IPOs just means more stockscompeting for the same amount of money, while a lot of mergers and acquisi-tions might cause the market’s size to contract even as more IPOs are issued.

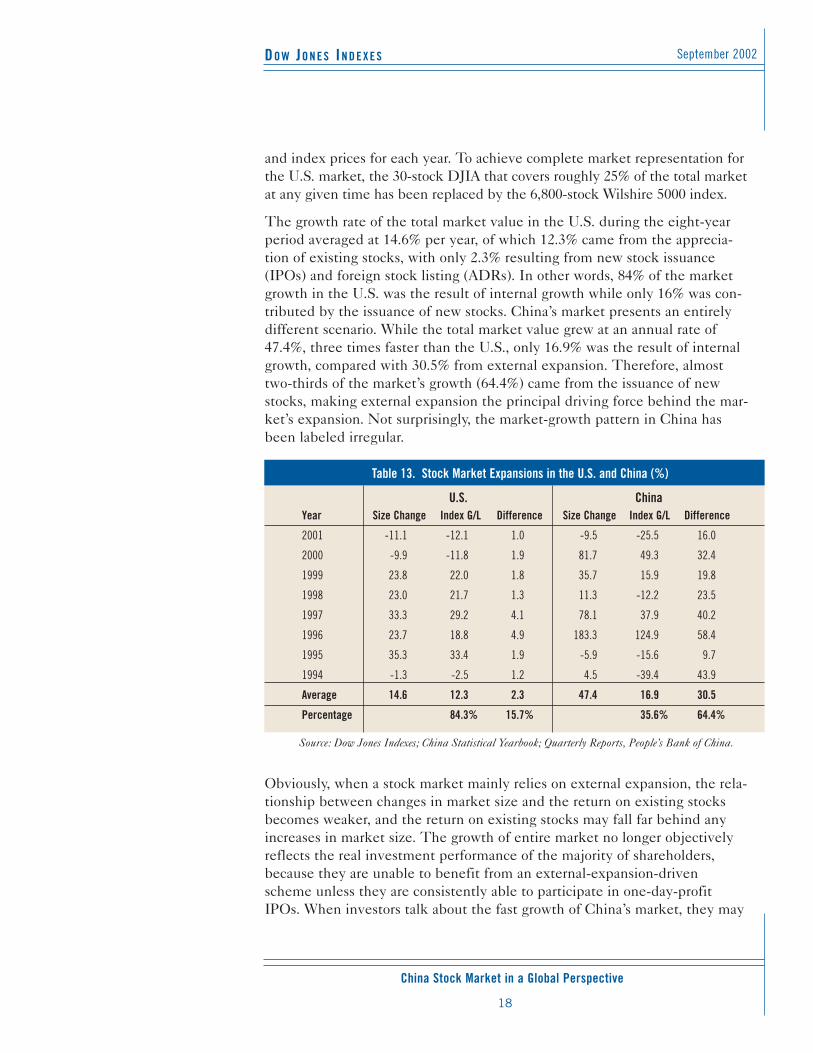

Table 13 compares the internal growth and external expansion of the U.S.and China markets during an eight-year period. The “Size Change” and“Index Gain/Loss” represent the changes in the total market capitalization

DO W JO N E S IN D E X E S

China Stock Market in a Global Perspective

September 2002

18

and index prices for each year. To achieve complete market representation forthe U.S. market, the 30-stock DJIA that covers roughly 25% of the total marketat any given time has been replaced by the 6,800-stock Wilshire 5000 index.

The growth rate of the total market value in the U.S. during the eight-yearperiod averaged at 14.6% per year, of which 12.3% came from the apprecia-tion of existing stocks, with only 2.3% resulting from new stock issuance(IPOs) and foreign stock listing (ADRs). In other words, 84% of the marketgrowth in the U.S. was the result of internal growth while only 16% was con-tributed by the issuance of new stocks. China’s market presents an entirelydifferent scenario. While the total market value grew at an annual rate of47.4%, three times faster than the U.S., only 16.9% was the result of internalgrowth, compared with 30.5% from external expansion. Therefore, almosttwo-thirds of the market’s growth (64.4%) came from the issuance of newstocks, making external expansion the principal driving force behind the mar-ket’s expansion. Not surprisingly, the market-growth pattern in China hasbeen labeled irregular.

Obviously, when a stock market mainly relies on external expansion, the rela-tionship between changes in market size and the return on existing stocksbecomes weaker, and the return on existing stocks may fall far behind anyincreases in market size. The growth of entire market no longer objectivelyreflects the real investment performance of the majority of shareholders,because they are unable to benefit from an external-expansion-drivenscheme unless they are consistently able to participate in one-day-profitIPOs. When investors talk about the fast growth of China’s market, they may

Table 13. Stock Market Expansions in the U.S. and China (%)

U.S. ChinaYear Size Change Index G/L Difference Size Change Index G/L Difference

2001 -11.1 -12.1 1.0 -9.5 -25.5 16.0

2000 -9.9 -11.8 1.9 81.7 49.3 32.4

1999 23.8 22.0 1.8 35.7 15.9 19.8

1998 23.0 21.7 1.3 11.3 -12.2 23.5

1997 33.3 29.2 4.1 78.1 37.9 40.2

1996 23.7 18.8 4.9 183.3 124.9 58.4

1995 35.3 33.4 1.9 -5.9 -15.6 9.7

1994 -1.3 -2.5 1.2 4.5 -39.4 43.9

Average 14.6 12.3 2.3 47.4 16.9 30.5

Percentage 84.3% 15.7% 35.6% 64.4%

Source: Dow Jones Indexes; China Statistical Yearbook; Quarterly Reports, People’s Bank of China.

DO W JO N E S IN D E X E S

China Stock Market in a Global Perspective

September, 2002

19

IPOs represent a larger proportionof the market capitalization of

China’s stock market than in otherworld markets. The direction of the

stock market in any given yearseems to be closely linked to

whether the number of IPOs in thatyear has increased or decreased

from the previous year. An increasein IPOs is accompanied by a rise in

the index and vice versa.

be focusing on the change of its total market value but ignoring the means bywhich it has grown. In reality, extreme external expansion distorts percep-tions of a marketplace because it has little relation to the actual investmentreturns of long-term shareholders.

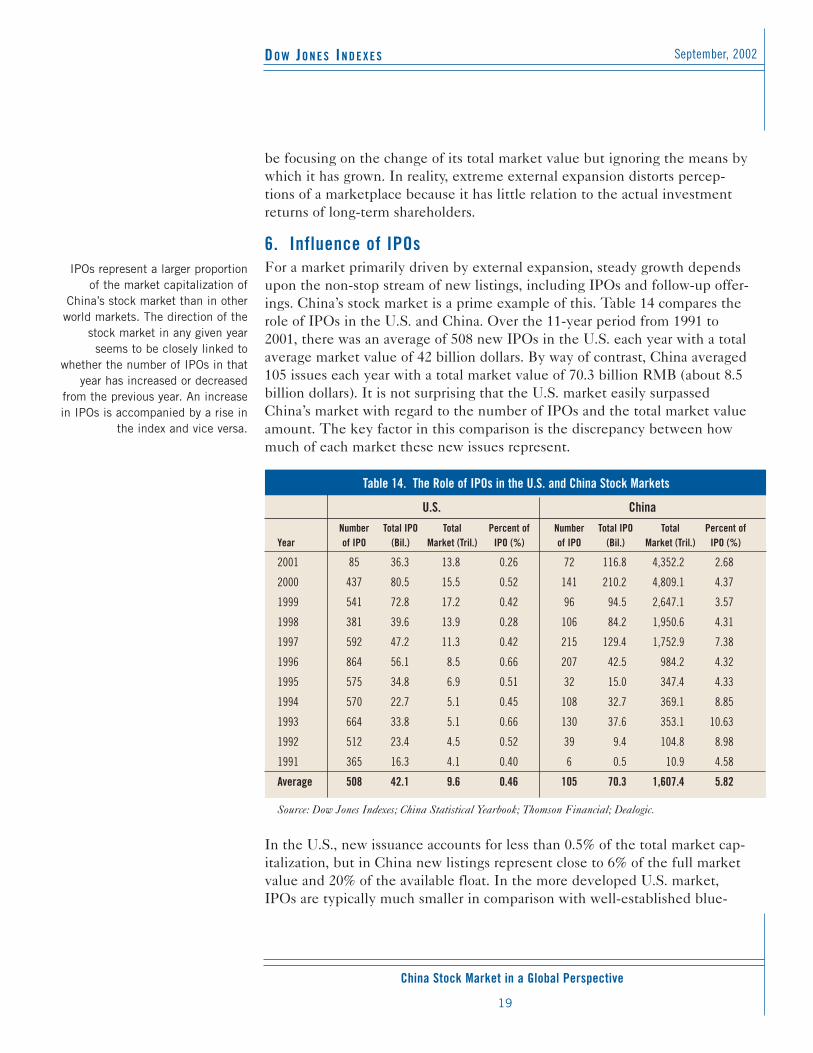

6. Influence of IPOs For a market primarily driven by external expansion, steady growth dependsupon the non-stop stream of new listings, including IPOs and follow-up offer-ings. China’s stock market is a prime example of this. Table 14 compares therole of IPOs in the U.S. and China. Over the 11-year period from 1991 to2001, there was an average of 508 new IPOs in the U.S. each year with a totalaverage market value of 42 billion dollars. By way of contrast, China averaged105 issues each year with a total market value of 70.3 billion RMB (about 8.5billion dollars). It is not surprising that the U.S. market easily surpassedChina’s market with regard to the number of IPOs and the total market valueamount. The key factor in this comparison is the discrepancy between howmuch of each market these new issues represent.

In the U.S., new issuance accounts for less than 0.5% of the total market cap-italization, but in China new listings represent close to 6% of the full marketvalue and 20% of the available float. In the more developed U.S. market,IPOs are typically much smaller in comparison with well-established blue-

Table 14. The Role of IPOs in the U.S. and China Stock Markets

U.S. ChinaNumber Total IPO Total Percent of Number Total IPO Total Percent of

Year of IPO (Bil.) Market (Tril.) IPO (%) of IPO (Bil.) Market (Tril.) IPO (%)

2001 85 36.3 13.8 0.26 72 116.8 4,352.2 2.68

2000 437 80.5 15.5 0.52 141 210.2 4,809.1 4.37

1999 541 72.8 17.2 0.42 96 94.5 2,647.1 3.57

1998 381 39.6 13.9 0.28 106 84.2 1,950.6 4.31

1997 592 47.2 11.3 0.42 215 129.4 1,752.9 7.38

1996 864 56.1 8.5 0.66 207 42.5 984.2 4.32

1995 575 34.8 6.9 0.51 32 15.0 347.4 4.33

1994 570 22.7 5.1 0.45 108 32.7 369.1 8.85

1993 664 33.8 5.1 0.66 130 37.6 353.1 10.63

1992 512 23.4 4.5 0.52 39 9.4 104.8 8.98

1991 365 16.3 4.1 0.40 6 0.5 10.9 4.58

Average 508 42.1 9.6 0.46 105 70.3 1,607.4 5.82

Source: Dow Jones Indexes; China Statistical Yearbook; Thomson Financial; Dealogic.

DO W JO N E S IN D E X E S

China Stock Market in a Global Perspective

September 2002

20

chip companies. However, in the still-developing China market, companieslaunching IPOs can be significantly larger than many that have been tradingfor some time. This is partly due to the fact that currently China’s marketlacks a stable core of blue-chip companies.

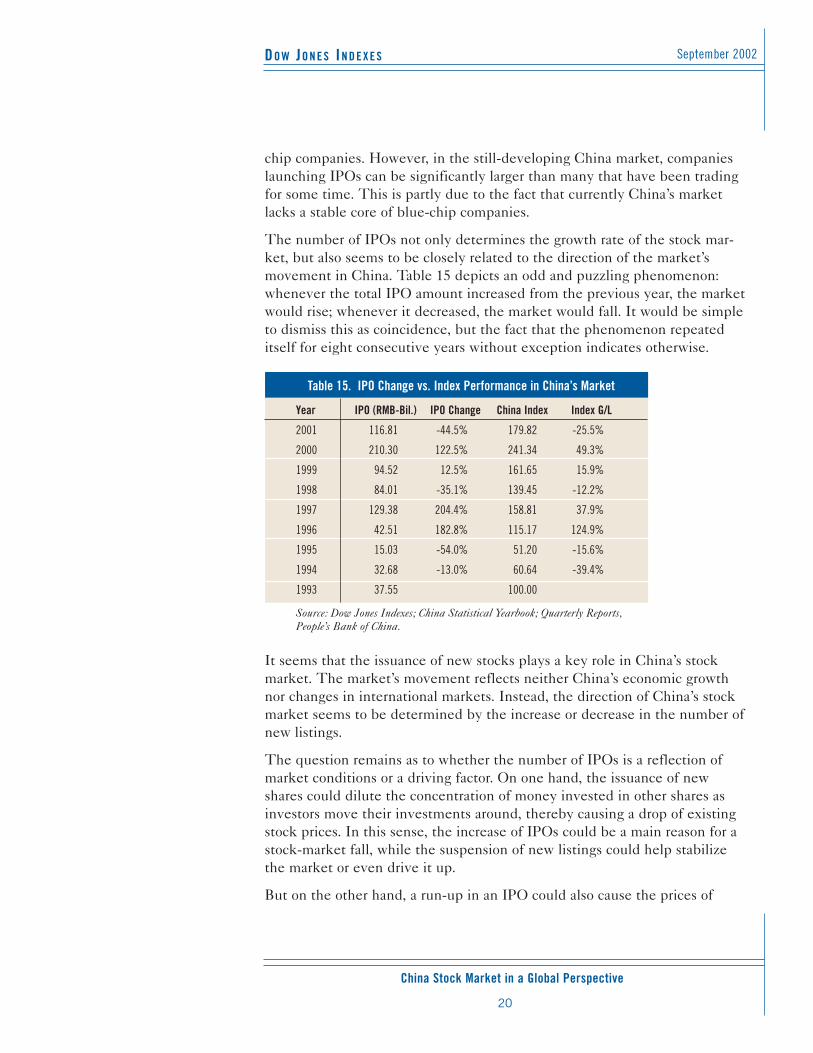

The number of IPOs not only determines the growth rate of the stock mar-ket, but also seems to be closely related to the direction of the market’smovement in China. Table 15 depicts an odd and puzzling phenomenon:whenever the total IPO amount increased from the previous year, the marketwould rise; whenever it decreased, the market would fall. It would be simpleto dismiss this as coincidence, but the fact that the phenomenon repeateditself for eight consecutive years without exception indicates otherwise.

It seems that the issuance of new stocks plays a key role in China’s stockmarket. The market’s movement reflects neither China’s economic growthnor changes in international markets. Instead, the direction of China’s stockmarket seems to be determined by the increase or decrease in the number ofnew listings.

The question remains as to whether the number of IPOs is a reflection ofmarket conditions or a driving factor. On one hand, the issuance of newshares could dilute the concentration of money invested in other shares asinvestors move their investments around, thereby causing a drop of existingstock prices. In this sense, the increase of IPOs could be a main reason for astock-market fall, while the suspension of new listings could help stabilizethe market or even drive it up.

But on the other hand, a run-up in an IPO could also cause the prices of

Table 15. IPO Change vs. Index Performance in China’s Market

Year IPO (RMB-Bil.) IPO Change China Index Index G/L

2001 116.81 -44.5% 179.82 -25.5%

2000 210.30 122.5% 241.34 49.3%

1999 94.52 12.5% 161.65 15.9%

1998 84.01 -35.1% 139.45 -12.2%

1997 129.38 204.4% 158.81 37.9%

1996 42.51 182.8% 115.17 124.9%

1995 15.03 -54.0% 51.20 -15.6%

1994 32.68 -13.0% 60.64 -39.4%

1993 37.55 100.00

Source: Dow Jones Indexes; China Statistical Yearbook; Quarterly Reports,People’s Bank of China.

DO W JO N E S IN D E X E S

China Stock Market in a Global Perspective

September, 2002

21

China is a typical emerging marketin many ways, including its large

number of small-cap stocks, itslarge number of share classes, the

dominance of retail investors, itstwo-exchange structure and thestrict regulation of IPOs by the

government.

other related stocks to be pulled along as well, because price rallies in IPOsare usually not limited to the first trading session but can last for severalweeks or even months. In the case of a very large IPO that gains immediateadmission to the index, the adjustment of the divisor on the first trading daycan certainly filter out its impact on the index, but continuous price increasesduring the following days will inevitably push the index up. In addition, theIPO effect may also have some positive impact on existing stock prices—arise in the tide lifts every boat in the sea. From this perspective, an increasein the number of IPOs may help boost an index.

Whatever the answer, nowhere else is this correlation between the number ofIPOs and market movements so sharply defined. The effect of IPOs onChina’s stock market mainly depends on if IPOs effectively attract assets tothe stock market or if they are competing with existing stocks for limitedcapital. In the case of the former, the stock market would be stimulated bythe new listings, but if the IPOs are competing for limited capital, the marketwould suffer as a result. In truth, the reality probably lies somewherebetween these two extreme examples, but the question remains as towhether the market is stimulated by new listings or whether the new listingsare the result of an invigorated stock market.

7. Typical Emerging MarketBoth of China’s exchanges are recent creations established in December1990. There were no laws to govern corporations until 1994, and there wereno laws to regulate securities until 1999. Open-ended mutual funds were cre-ated as recently as 2000, and a draft of investment company law is not sched-uled to be submitted to Congress until 2003. Not surprisingly, China demon-strates many of the features that are characteristic of emerging markets. Theyare not only seen in the primary IPO market for public offerings but also inthe secondary stock-trading market. These features can be summarized intofive major points.

First, there is an overwhelming number of share classes to confuse investors.Besides class A shares, which are restricted to domestic investors, and the Bshares trading in China for foreign investors, there are several additionalclasses available to global investors and denominated in hard currencies. The H, N, L and S shares are listed in Hong Kong, New York, London andSingapore, respectively. If foreign-currency financing is the sole purpose,ADRs or GDRs can be readily created, even if the RMB is non-convertible.They are simpler and more flexible and effective in terms of raising capital inhard currencies. Also, they put domestic and international investors on thesame platform, thus eliminating differences between them. The DeutscheBank and the United Bank of Switzerland (UBS) even created another brand-

DO W JO N E S IN D E X E S

China Stock Market in a Global Perspective

September 2002

22

new share class in 2001 by issuing “global shares” denominated in multiplecurrencies.

Many of China’s blue-chip companies are listed only on overseas exchangesand are not available to local investors. Although foreign listing is a common-ly chosen option for companies in countries such as South Africa and Israel,China’s implementation of this practice far outstrips that of any other country.China Mobile, China Unicom, CNOOC, and Legend are all leading Chinesecompanies as well as components of the Hang Seng Index. But while main-land Chinese are the customers, suppliers, producers and even employees ofthese companies, they are unable to invest in them. As can be seen later, thisstrange issue creates many structural drawbacks for China’s stock market.

Secondly, the Chinese government strictly regulates initial public offerings.While regulations and government supervision are necessary for the success-ful and fair operation of any stock market, China represents an extreme case.The government sets the quota for new listings each year, selects the quali-fied companies based on provincial and sector allocation, and — until 2001 —even determined where the new stocks would list. China is the only countryin which the government completely controls the size of the stock market,the pace of issue and the allocation of resources. Also, under current laws inChina, no company is allowed to list without three years of continuous prof-itability. As a result, only a few of the listed companies in China are youngand dynamic enterprises. This has led to the criticism that the stock marketfavors state-owned companies over entrepreneurial ventures.

Another consequence of the overseas listing of China’s large companies is thepredominance of small-cap stocks, in both absolute size and in relation to therest of the world. The low free-float ratio in China makes the situation evenworse. For instance, the Dow Jones Emerging Market Index includes 12 mar-kets—South Korea, Taiwan, Malaysia, Indonesia, the Philippines, Thailand,South Africa, Mexico, Brazil, Chile, Colombia and Venezuela—and covers95% of the combined market value. According to the parameters of thisindex, the cutoff lines between large and mid-cap, and mid and small-capstocks are 1.2 billion and 210 million dollars respectively, as of December 31,2001. Based upon this standard, only one company listed in China can beclassified as a large stock—Shenzhen Development Bank (Sinopec andChina Merchants Bank have big full but limited float market capitalization),and 130 qualify as mid-cap stocks. The remaining 1,000-plus companies, or88% of the total number, are small-cap or micro-cap companies.

The dominance of small stocks in China also can be measured by the averagetrading price of all stocks. As of February 28, 2002, 326 stocks, or 9%, of the3,3736 stocks trading on the Nasdaq stock market had a closing price under

DO W JO N E S IN D E X E S

China Stock Market in a Global Perspective

September, 2002

23

$1, meeting the definition of a “junk stock.” At the same time, China’s mar-ket had a total of 521.8 billion shares outstanding with a full market value of$525.6 billion dollars. This translates into an average price of $1.007 dollarper share, compared with $34 and $23 at the NYSE and Nasdaq, respectively.

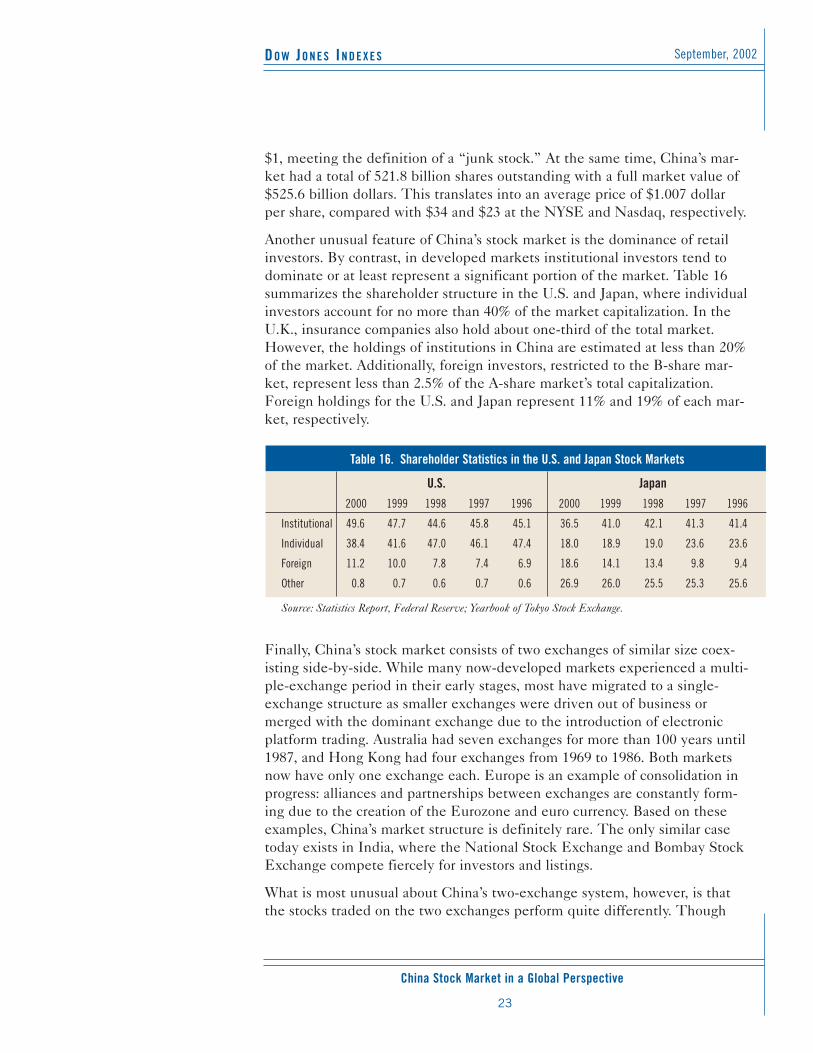

Another unusual feature of China’s stock market is the dominance of retailinvestors. By contrast, in developed markets institutional investors tend todominate or at least represent a significant portion of the market. Table 16summarizes the shareholder structure in the U.S. and Japan, where individualinvestors account for no more than 40% of the market capitalization. In theU.K., insurance companies also hold about one-third of the total market.However, the holdings of institutions in China are estimated at less than 20%of the market. Additionally, foreign investors, restricted to the B-share mar-ket, represent less than 2.5% of the A-share market’s total capitalization.Foreign holdings for the U.S. and Japan represent 11% and 19% of each mar-ket, respectively.

Finally, China’s stock market consists of two exchanges of similar size coex-isting side-by-side. While many now-developed markets experienced a multi-ple-exchange period in their early stages, most have migrated to a single-exchange structure as smaller exchanges were driven out of business ormerged with the dominant exchange due to the introduction of electronicplatform trading. Australia had seven exchanges for more than 100 years until1987, and Hong Kong had four exchanges from 1969 to 1986. Both marketsnow have only one exchange each. Europe is an example of consolidation inprogress: alliances and partnerships between exchanges are constantly form-ing due to the creation of the Eurozone and euro currency. Based on theseexamples, China’s market structure is definitely rare. The only similar casetoday exists in India, where the National Stock Exchange and Bombay StockExchange compete fiercely for investors and listings.

What is most unusual about China’s two-exchange system, however, is thatthe stocks traded on the two exchanges perform quite differently. Though

Table 16. Shareholder Statistics in the U.S. and Japan Stock Markets

U.S. Japan2000 1999 1998 1997 1996 2000 1999 1998 1997 1996

Institutional 49.6 47.7 44.6 45.8 45.1 36.5 41.0 42.1 41.3 41.4

Individual 38.4 41.6 47.0 46.1 47.4 18.0 18.9 19.0 23.6 23.6

Foreign 11.2 10.0 7.8 7.4 6.9 18.6 14.1 13.4 9.8 9.4

Other 0.8 0.7 0.6 0.7 0.6 26.9 26.0 25.5 25.3 25.6

Source: Statistics Report, Federal Reserve; Yearbook of Tokyo Stock Exchange.

DO W JO N E S IN D E X E S

China Stock Market in a Global Perspective

September 2002

24

China’s stock market lacks trulyblue-chip stocks and so is

dominated by a large number ofsmaller capitalization stocks, givingit a pyramid structure. By contrast,developed markets tend to be dom-

inated by a small number of largeblue-chip stocks, giving them a

funnel-shaped structure.

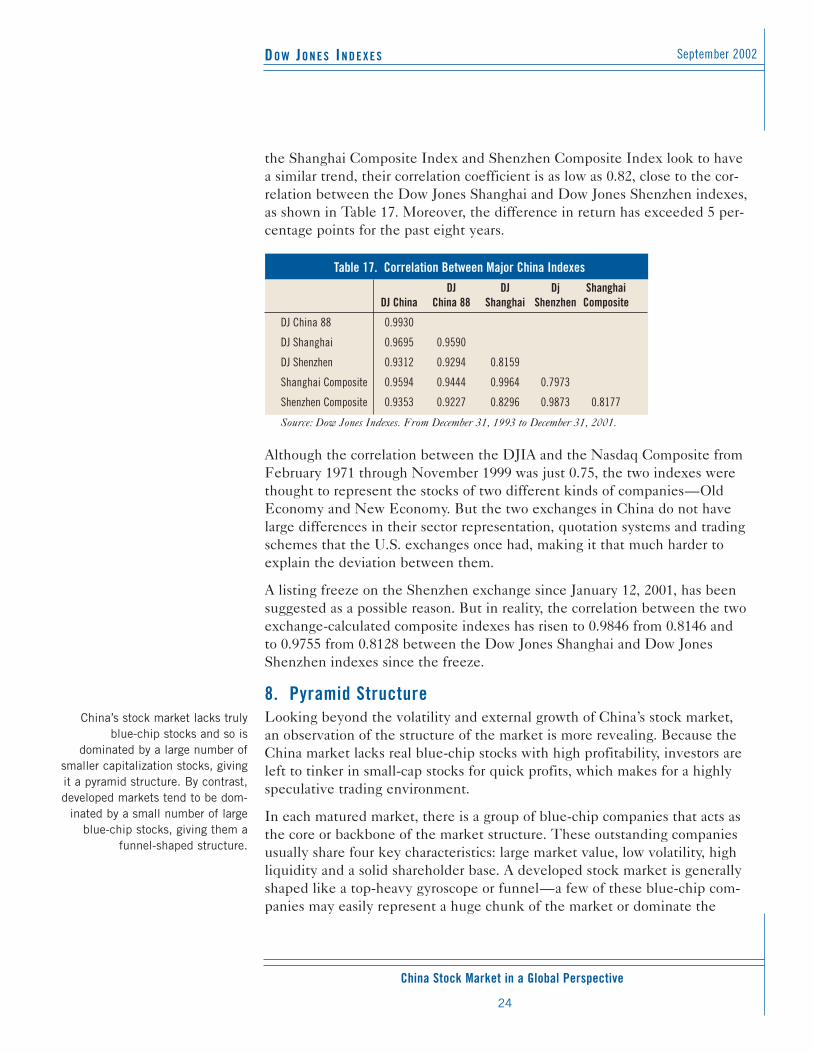

the Shanghai Composite Index and Shenzhen Composite Index look to havea similar trend, their correlation coefficient is as low as 0.82, close to the cor-relation between the Dow Jones Shanghai and Dow Jones Shenzhen indexes,as shown in Table 17. Moreover, the difference in return has exceeded 5 per-centage points for the past eight years.

Although the correlation between the DJIA and the Nasdaq Composite fromFebruary 1971 through November 1999 was just 0.75, the two indexes werethought to represent the stocks of two different kinds of companies—OldEconomy and New Economy. But the two exchanges in China do not havelarge differences in their sector representation, quotation systems and tradingschemes that the U.S. exchanges once had, making it that much harder toexplain the deviation between them.

A listing freeze on the Shenzhen exchange since January 12, 2001, has beensuggested as a possible reason. But in reality, the correlation between the twoexchange-calculated composite indexes has risen to 0.9846 from 0.8146 andto 0.9755 from 0.8128 between the Dow Jones Shanghai and Dow JonesShenzhen indexes since the freeze.

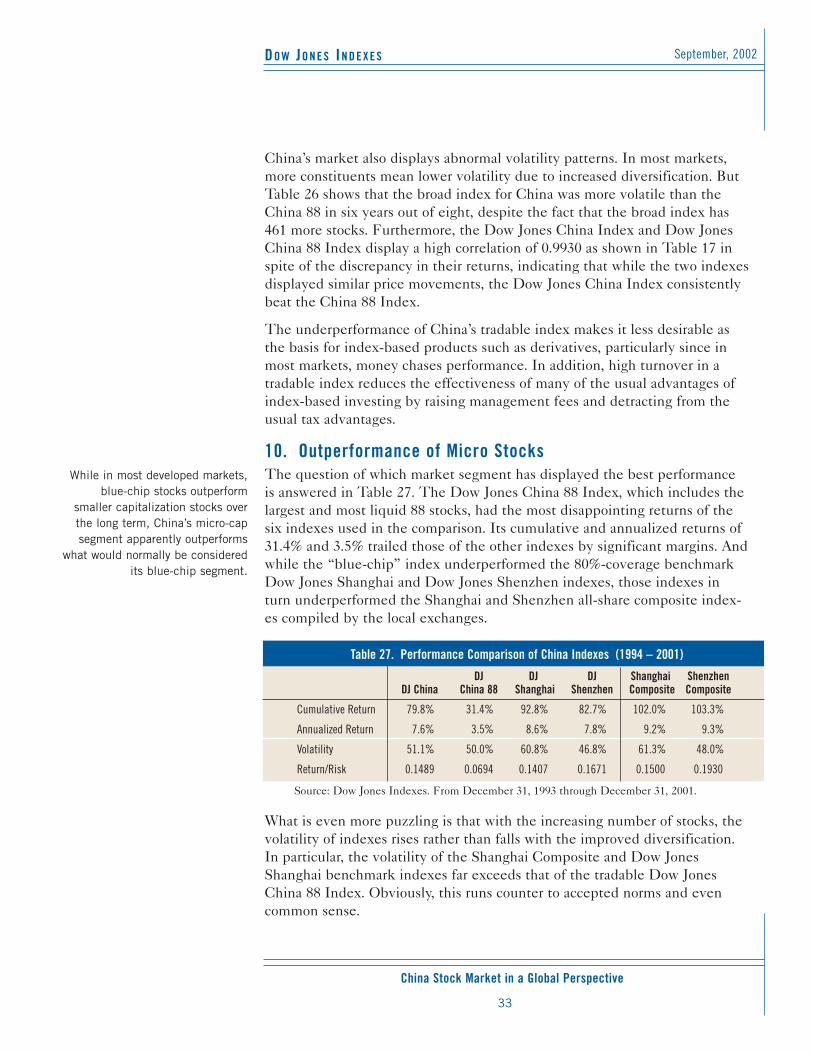

8. Pyramid StructureLooking beyond the volatility and external growth of China’s stock market,an observation of the structure of the market is more revealing. Because theChina market lacks real blue-chip stocks with high profitability, investors areleft to tinker in small-cap stocks for quick profits, which makes for a highlyspeculative trading environment.

In each matured market, there is a group of blue-chip companies that acts asthe core or backbone of the market structure. These outstanding companiesusually share four key characteristics: large market value, low volatility, highliquidity and a solid shareholder base. A developed stock market is generallyshaped like a top-heavy gyroscope or funnel—a few of these blue-chip com-panies may easily represent a huge chunk of the market or dominate the

Table 17. Correlation Between Major China IndexesDJ DJ Dj Shanghai

DJ China China 88 Shanghai Shenzhen Composite

DJ China 88 0.9930

DJ Shanghai 0.9695 0.9590

DJ Shenzhen 0.9312 0.9294 0.8159

Shanghai Composite 0.9594 0.9444 0.9964 0.7973

Shenzhen Composite 0.9353 0.9227 0.8296 0.9873 0.8177

Source: Dow Jones Indexes. From December 31, 1993 to December 31, 2001.

DO W JO N E S IN D E X E S

China Stock Market in a Global Perspective

September, 2002

25

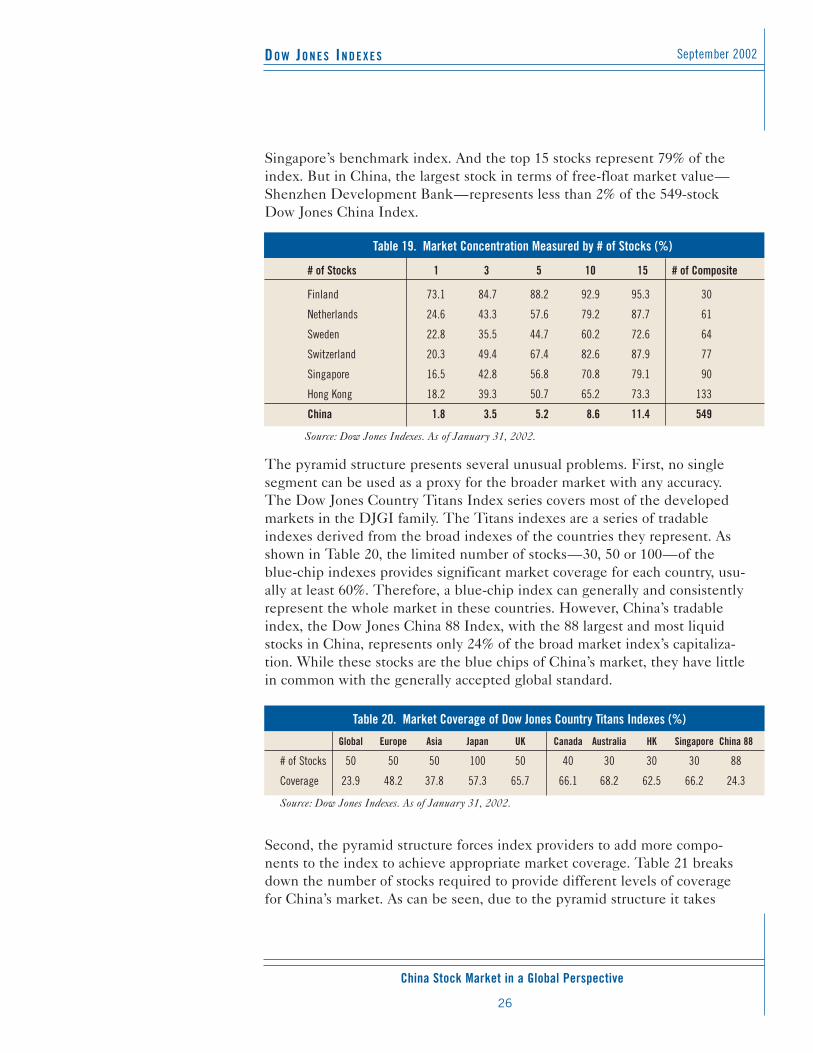

benchmark index’s movement. Meanwhile, the numerous small-cap compa-nies at the bottom are relatively insignificant. A typical example is Nokia. Asingle company represents roughly 73% of Finland’s total market value. InHong Kong, HSBC and China Mobile, combined, account for almost half ofthe Hang Seng Index. But such is not the case in China. Without true blue-chip companies in the A-share market, the market structure resembles a pyra-mid, and with the increasing number of listed companies, the aggregate mar-ket value accumulates slowly as more shares compete for a limited amount ofmoney.

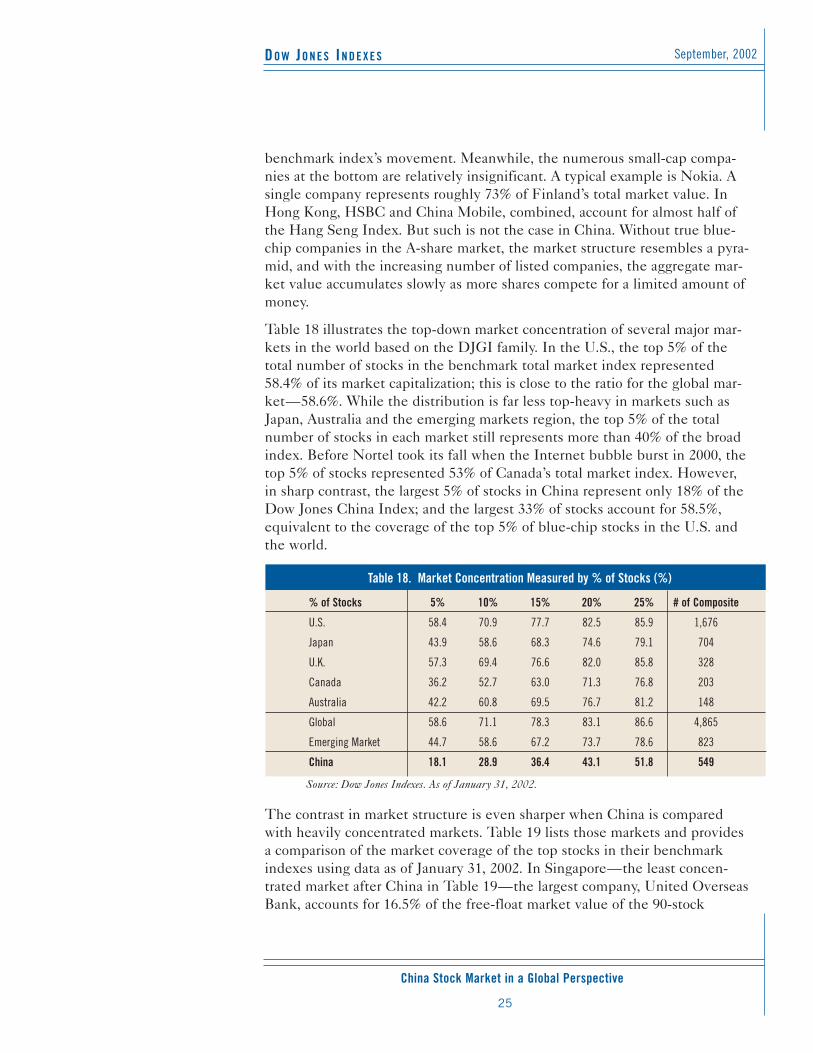

Table 18 illustrates the top-down market concentration of several major mar-kets in the world based on the DJGI family. In the U.S., the top 5% of thetotal number of stocks in the benchmark total market index represented58.4% of its market capitalization; this is close to the ratio for the global mar-ket—58.6%. While the distribution is far less top-heavy in markets such asJapan, Australia and the emerging markets region, the top 5% of the totalnumber of stocks in each market still represents more than 40% of the broadindex. Before Nortel took its fall when the Internet bubble burst in 2000, thetop 5% of stocks represented 53% of Canada’s total market index. However,in sharp contrast, the largest 5% of stocks in China represent only 18% of theDow Jones China Index; and the largest 33% of stocks account for 58.5%,equivalent to the coverage of the top 5% of blue-chip stocks in the U.S. andthe world.

The contrast in market structure is even sharper when China is comparedwith heavily concentrated markets. Table 19 lists those markets and providesa comparison of the market coverage of the top stocks in their benchmarkindexes using data as of January 31, 2002. In Singapore—the least concen-trated market after China in Table 19—the largest company, United OverseasBank, accounts for 16.5% of the free-float market value of the 90-stock

Table 18. Market Concentration Measured by % of Stocks (%)

% of Stocks 5% 10% 15% 20% 25% # of Composite

U.S. 58.4 70.9 77.7 82.5 85.9 1,676

Japan 43.9 58.6 68.3 74.6 79.1 704

U.K. 57.3 69.4 76.6 82.0 85.8 328

Canada 36.2 52.7 63.0 71.3 76.8 203

Australia 42.2 60.8 69.5 76.7 81.2 148

Global 58.6 71.1 78.3 83.1 86.6 4,865

Emerging Market 44.7 58.6 67.2 73.7 78.6 823

China 18.1 28.9 36.4 43.1 51.8 549

Source: Dow Jones Indexes. As of January 31, 2002.

DO W JO N E S IN D E X E S

China Stock Market in a Global Perspective

September 2002

26

Singapore’s benchmark index. And the top 15 stocks represent 79% of theindex. But in China, the largest stock in terms of free-float market value—Shenzhen Development Bank—represents less than 2% of the 549-stockDow Jones China Index.

The pyramid structure presents several unusual problems. First, no singlesegment can be used as a proxy for the broader market with any accuracy.The Dow Jones Country Titans Index series covers most of the developedmarkets in the DJGI family. The Titans indexes are a series of tradableindexes derived from the broad indexes of the countries they represent. Asshown in Table 20, the limited number of stocks—30, 50 or 100—of theblue-chip indexes provides significant market coverage for each country, usu-ally at least 60%. Therefore, a blue-chip index can generally and consistentlyrepresent the whole market in these countries. However, China’s tradableindex, the Dow Jones China 88 Index, with the 88 largest and most liquidstocks in China, represents only 24% of the broad market index’s capitaliza-tion. While these stocks are the blue chips of China’s market, they have littlein common with the generally accepted global standard.

Second, the pyramid structure forces index providers to add more compo-nents to the index to achieve appropriate market coverage. Table 21 breaksdown the number of stocks required to provide different levels of coveragefor China’s market. As can be seen, due to the pyramid structure it takes

Table 20. Market Coverage of Dow Jones Country Titans Indexes (%)

Global Europe Asia Japan UK Canada Australia HK Singapore China 88

# of Stocks 50 50 50 100 50 40 30 30 30 88

Coverage 23.9 48.2 37.8 57.3 65.7 66.1 68.2 62.5 66.2 24.3

Source: Dow Jones Indexes. As of January 31, 2002.

Table 19. Market Concentration Measured by # of Stocks (%)

# of Stocks 1 3 5 10 15 # of Composite

Finland 73.1 84.7 88.2 92.9 95.3 30

Netherlands 24.6 43.3 57.6 79.2 87.7 61

Sweden 22.8 35.5 44.7 60.2 72.6 64

Switzerland 20.3 49.4 67.4 82.6 87.9 77

Singapore 16.5 42.8 56.8 70.8 79.1 90

Hong Kong 18.2 39.3 50.7 65.2 73.3 133

China 1.8 3.5 5.2 8.6 11.4 549

Source: Dow Jones Indexes. As of January 31, 2002.

DO W JO N E S IN D E X E S

China Stock Market in a Global Perspective

September, 2002

27

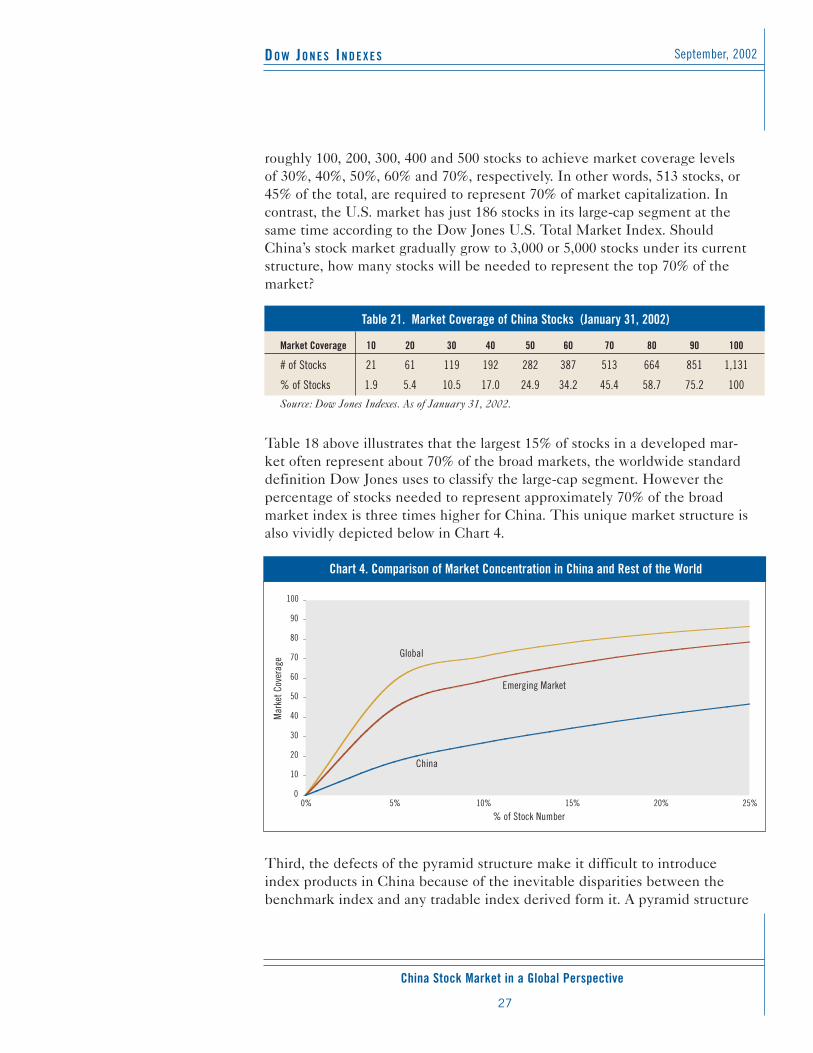

roughly 100, 200, 300, 400 and 500 stocks to achieve market coverage levelsof 30%, 40%, 50%, 60% and 70%, respectively. In other words, 513 stocks, or45% of the total, are required to represent 70% of market capitalization. Incontrast, the U.S. market has just 186 stocks in its large-cap segment at thesame time according to the Dow Jones U.S. Total Market Index. ShouldChina’s stock market gradually grow to 3,000 or 5,000 stocks under its currentstructure, how many stocks will be needed to represent the top 70% of themarket?

Table 18 above illustrates that the largest 15% of stocks in a developed mar-ket often represent about 70% of the broad markets, the worldwide standarddefinition Dow Jones uses to classify the large-cap segment. However thepercentage of stocks needed to represent approximately 70% of the broadmarket index is three times higher for China. This unique market structure isalso vividly depicted below in Chart 4.

Third, the defects of the pyramid structure make it difficult to introduceindex products in China because of the inevitable disparities between thebenchmark index and any tradable index derived form it. A pyramid structure

Table 21. Market Coverage of China Stocks (January 31, 2002)

Market Coverage 10 20 30 40 50 60 70 80 90 100

# of Stocks 21 61 119 192 282 387 513 664 851 1,131

% of Stocks 1.9 5.4 10.5 17.0 24.9 34.2 45.4 58.7 75.2 100

Source: Dow Jones Indexes. As of January 31, 2002.

0

10

20

30

40

50

60

70

80

90

100

0% 5% 10% 15% 20% 25%

% of Stock Number

Mar

ket C

over

age Global

Emerging Market

China

Chart 4. Comparison of Market Concentration in China and Rest of the World

DO W JO N E S IN D E X E S

China Stock Market in a Global Perspective

September 2002

28

increases the likelihood that these indexes will diverge from each other sig-nificantly because the blue-chip stocks that generally dictate the direction ofthese indexes are simply not present.

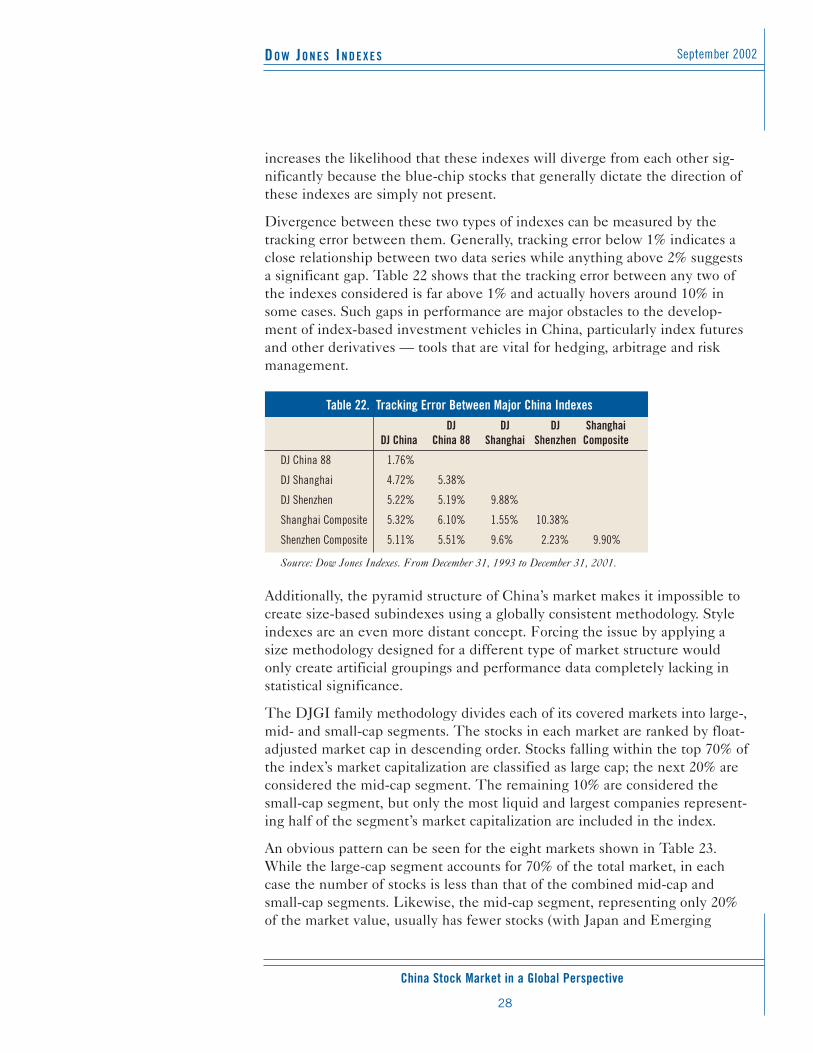

Divergence between these two types of indexes can be measured by thetracking error between them. Generally, tracking error below 1% indicates aclose relationship between two data series while anything above 2% suggestsa significant gap. Table 22 shows that the tracking error between any two ofthe indexes considered is far above 1% and actually hovers around 10% insome cases. Such gaps in performance are major obstacles to the develop-ment of index-based investment vehicles in China, particularly index futuresand other derivatives — tools that are vital for hedging, arbitrage and riskmanagement.

Additionally, the pyramid structure of China’s market makes it impossible tocreate size-based subindexes using a globally consistent methodology. Styleindexes are an even more distant concept. Forcing the issue by applying asize methodology designed for a different type of market structure wouldonly create artificial groupings and performance data completely lacking instatistical significance.

The DJGI family methodology divides each of its covered markets into large-,mid- and small-cap segments. The stocks in each market are ranked by float-adjusted market cap in descending order. Stocks falling within the top 70% ofthe index’s market capitalization are classified as large cap; the next 20% areconsidered the mid-cap segment. The remaining 10% are considered thesmall-cap segment, but only the most liquid and largest companies represent-ing half of the segment’s market capitalization are included in the index.

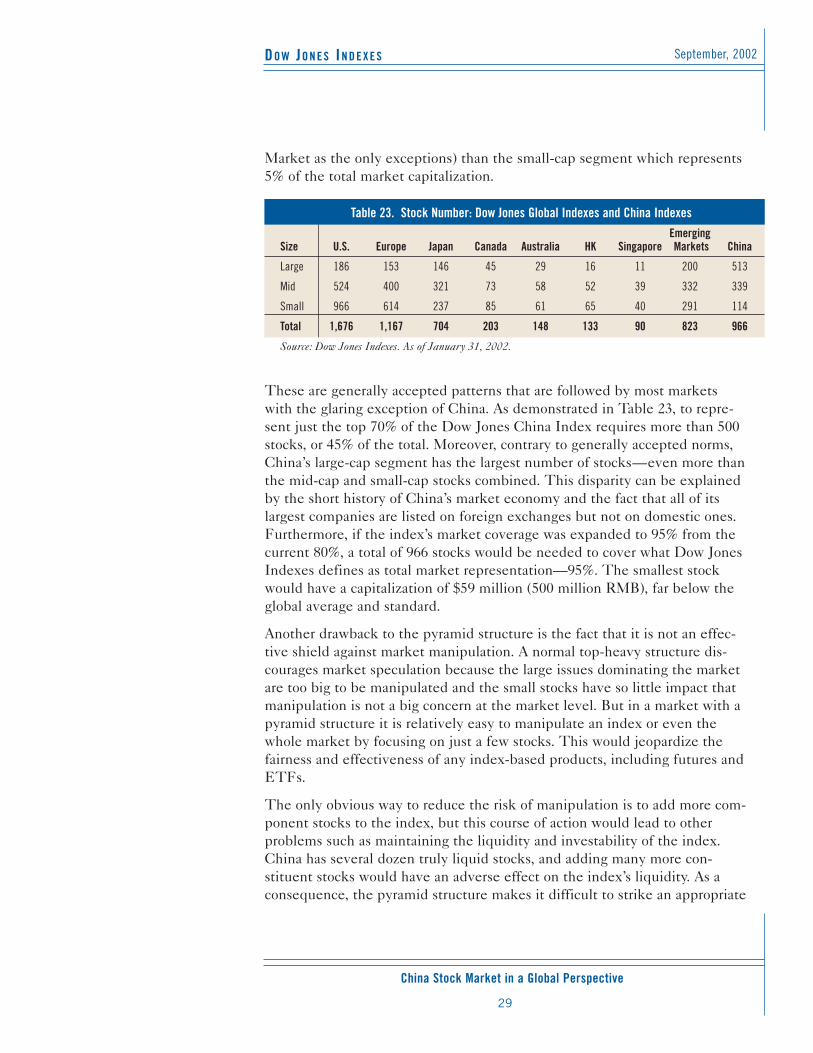

An obvious pattern can be seen for the eight markets shown in Table 23.While the large-cap segment accounts for 70% of the total market, in eachcase the number of stocks is less than that of the combined mid-cap andsmall-cap segments. Likewise, the mid-cap segment, representing only 20%of the market value, usually has fewer stocks (with Japan and Emerging

Table 22. Tracking Error Between Major China IndexesDJ DJ DJ Shanghai

DJ China China 88 Shanghai Shenzhen Composite

DJ China 88 1.76%

DJ Shanghai 4.72% 5.38%

DJ Shenzhen 5.22% 5.19% 9.88%

Shanghai Composite 5.32% 6.10% 1.55% 10.38%

Shenzhen Composite 5.11% 5.51% 9.6% 2.23% 9.90%

Source: Dow Jones Indexes. From December 31, 1993 to December 31, 2001.

DO W JO N E S IN D E X E S

China Stock Market in a Global Perspective

September, 2002

29

Market as the only exceptions) than the small-cap segment which represents5% of the total market capitalization.

These are generally accepted patterns that are followed by most marketswith the glaring exception of China. As demonstrated in Table 23, to repre-sent just the top 70% of the Dow Jones China Index requires more than 500stocks, or 45% of the total. Moreover, contrary to generally accepted norms,China’s large-cap segment has the largest number of stocks—even more thanthe mid-cap and small-cap stocks combined. This disparity can be explainedby the short history of China’s market economy and the fact that all of itslargest companies are listed on foreign exchanges but not on domestic ones.Furthermore, if the index’s market coverage was expanded to 95% from thecurrent 80%, a total of 966 stocks would be needed to cover what Dow JonesIndexes defines as total market representation—95%. The smallest stockwould have a capitalization of $59 million (500 million RMB), far below theglobal average and standard.

Another drawback to the pyramid structure is the fact that it is not an effec-tive shield against market manipulation. A normal top-heavy structure dis-courages market speculation because the large issues dominating the marketare too big to be manipulated and the small stocks have so little impact thatmanipulation is not a big concern at the market level. But in a market with apyramid structure it is relatively easy to manipulate an index or even thewhole market by focusing on just a few stocks. This would jeopardize thefairness and effectiveness of any index-based products, including futures andETFs.

The only obvious way to reduce the risk of manipulation is to add more com-ponent stocks to the index, but this course of action would lead to otherproblems such as maintaining the liquidity and investability of the index.China has several dozen truly liquid stocks, and adding many more con-stituent stocks would have an adverse effect on the index’s liquidity. As aconsequence, the pyramid structure makes it difficult to strike an appropriate

Table 23. Stock Number: Dow Jones Global Indexes and China IndexesEmerging

Size U.S. Europe Japan Canada Australia HK Singapore Markets China

Large 186 153 146 45 29 16 11 200 513

Mid 524 400 321 73 58 52 39 332 339

Small 966 614 237 85 61 65 40 291 114

Total 1,676 1,167 704 203 148 133 90 823 966

Source: Dow Jones Indexes. As of January 31, 2002.

DO W JO N E S IN D E X E S

China Stock Market in a Global Perspective

September 2002

30

China’s stock market lacks a dominant core of blue-chip stocks.

This problem is closely linked tohigh turnover in market indexes

and rampant market speculation.These factors are serious obstacles

to the creation of viable index-based products.

balance between market coverage and stock liquidity.

Finally, the pyramid structure also makes index-based investing particularlydifficult in China. With limited capital and assets under management, mostmutual funds and other institutional investors in China do not have enoughmoney or resources to hold the vast number of stocks required for indexreplication over a long period of time. Accordingly, the creation of ETFsremains a distant possibility as long as only a few financial institutions canafford a large basket of stocks.

9. Unstable CoreThe “core-satellite” structure is another model that is typical of the world’sstock markets. In this construct, the core of the index is composed of blue-chip stocks with long histories of performance that seldom experience anydramatic changes. The satellites are those companies sliding in and out of theindex because of insufficient size or liquidity and poor or unstable fundamen-tals.

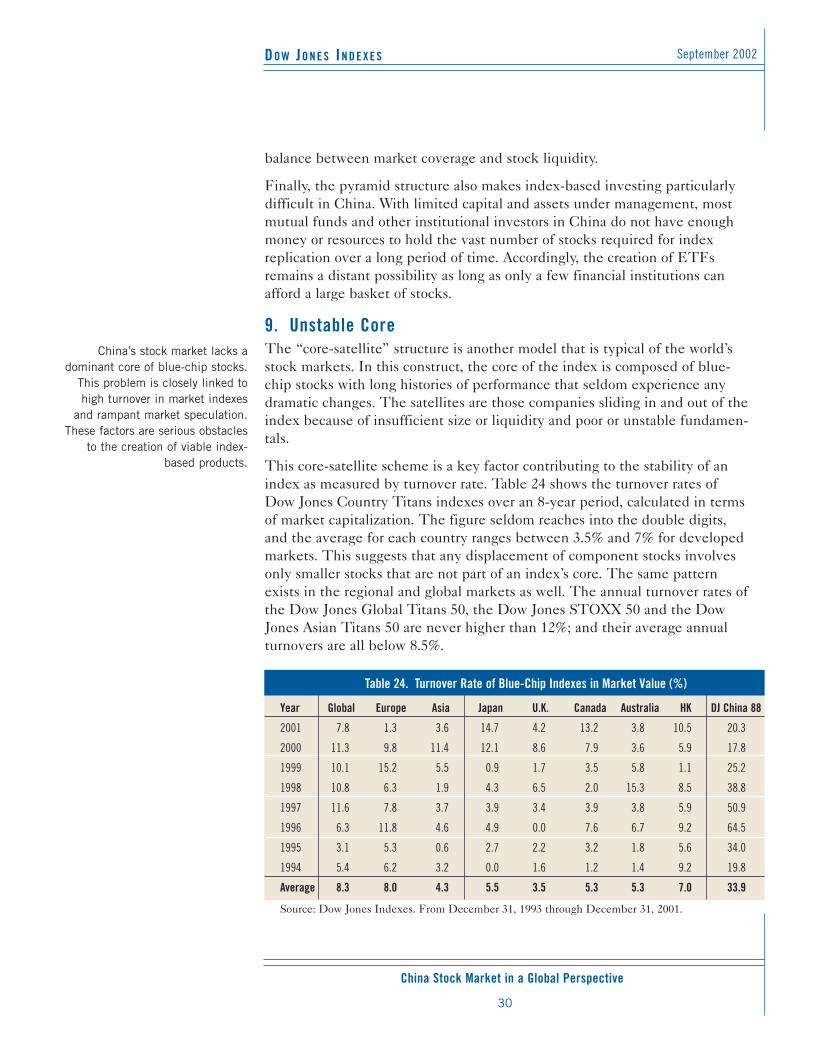

This core-satellite scheme is a key factor contributing to the stability of anindex as measured by turnover rate. Table 24 shows the turnover rates ofDow Jones Country Titans indexes over an 8-year period, calculated in termsof market capitalization. The figure seldom reaches into the double digits,and the average for each country ranges between 3.5% and 7% for developedmarkets. This suggests that any displacement of component stocks involvesonly smaller stocks that are not part of an index’s core. The same patternexists in the regional and global markets as well. The annual turnover rates ofthe Dow Jones Global Titans 50, the Dow Jones STOXX 50 and the DowJones Asian Titans 50 are never higher than 12%; and their average annualturnovers are all below 8.5%.

Table 24. Turnover Rate of Blue-Chip Indexes in Market Value (%)

Year Global Europe Asia Japan U.K. Canada Australia HK DJ China 88

2001 7.8 1.3 3.6 14.7 4.2 13.2 3.8 10.5 20.3

2000 11.3 9.8 11.4 12.1 8.6 7.9 3.6 5.9 17.8

1999 10.1 15.2 5.5 0.9 1.7 3.5 5.8 1.1 25.2

1998 10.8 6.3 1.9 4.3 6.5 2.0 15.3 8.5 38.8

1997 11.6 7.8 3.7 3.9 3.4 3.9 3.8 5.9 50.9

1996 6.3 11.8 4.6 4.9 0.0 7.6 6.7 9.2 64.5

1995 3.1 5.3 0.6 2.7 2.2 3.2 1.8 5.6 34.0

1994 5.4 6.2 3.2 0.0 1.6 1.2 1.4 9.2 19.8

Average 8.3 8.0 4.3 5.5 3.5 5.3 5.3 7.0 33.9

Source: Dow Jones Indexes. From December 31, 1993 through December 31, 2001.

DO W JO N E S IN D E X E S

China Stock Market in a Global Perspective

September, 2002

31

However, this pattern does not manifest in China because there is no blue-chip core—unless it is a highly unstable one—that can provide a focus pointfor medium and small stocks. As shown in Table 24, the average annualturnover rate in China during this eight-year period was nearly 34% with alow of 17.8% in 2000. That low is still higher than the highest turnover levelfor any of the other markets used in the comparison. This high turnover can-not be explained by the replacement of small-cap satellite stocks but rathermust involve the replacement of what would normally be considered corestocks if China had a standard market structure.

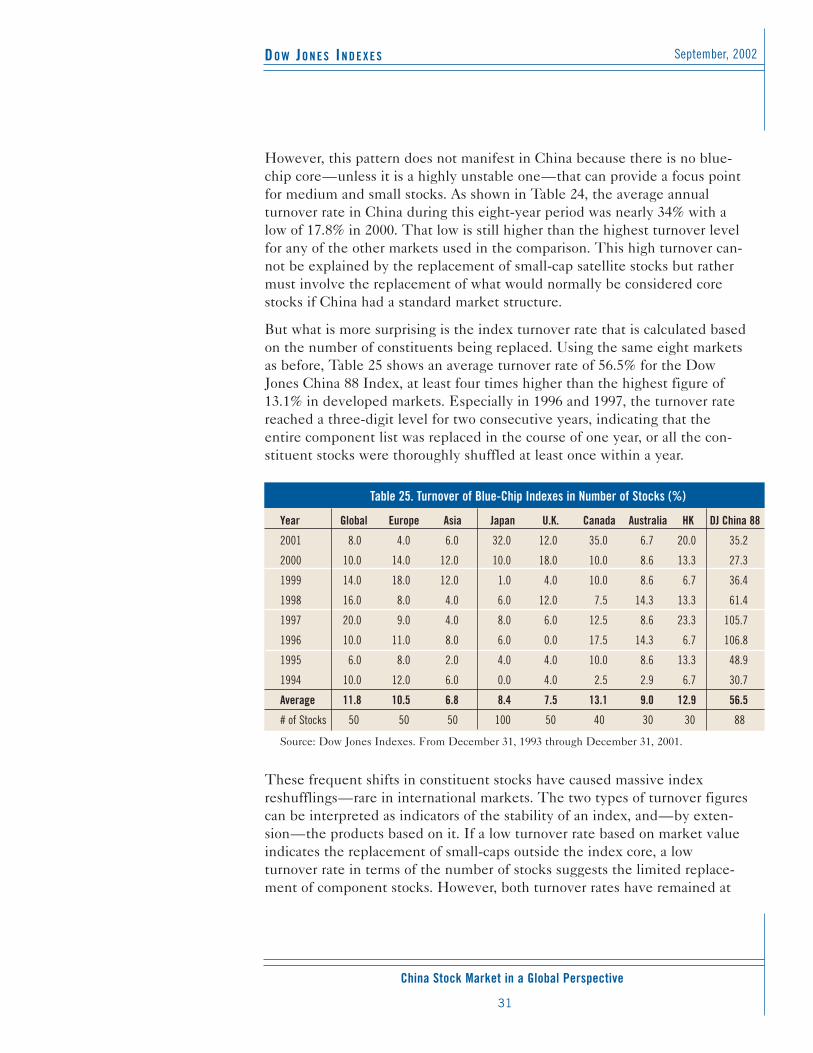

But what is more surprising is the index turnover rate that is calculated basedon the number of constituents being replaced. Using the same eight marketsas before, Table 25 shows an average turnover rate of 56.5% for the DowJones China 88 Index, at least four times higher than the highest figure of13.1% in developed markets. Especially in 1996 and 1997, the turnover ratereached a three-digit level for two consecutive years, indicating that theentire component list was replaced in the course of one year, or all the con-stituent stocks were thoroughly shuffled at least once within a year.

These frequent shifts in constituent stocks have caused massive indexreshufflings—rare in international markets. The two types of turnover figurescan be interpreted as indicators of the stability of an index, and—by exten-sion—the products based on it. If a low turnover rate based on market valueindicates the replacement of small-caps outside the index core, a lowturnover rate in terms of the number of stocks suggests the limited replace-ment of component stocks. However, both turnover rates have remained at

Table 25. Turnover of Blue-Chip Indexes in Number of Stocks (%)

Year Global Europe Asia Japan U.K. Canada Australia HK DJ China 88

2001 8.0 4.0 6.0 32.0 12.0 35.0 6.7 20.0 35.2

2000 10.0 14.0 12.0 10.0 18.0 10.0 8.6 13.3 27.3

1999 14.0 18.0 12.0 1.0 4.0 10.0 8.6 6.7 36.4

1998 16.0 8.0 4.0 6.0 12.0 7.5 14.3 13.3 61.4

1997 20.0 9.0 4.0 8.0 6.0 12.5 8.6 23.3 105.7

1996 10.0 11.0 8.0 6.0 0.0 17.5 14.3 6.7 106.8

1995 6.0 8.0 2.0 4.0 4.0 10.0 8.6 13.3 48.9

1994 10.0 12.0 6.0 0.0 4.0 2.5 2.9 6.7 30.7

Average 11.8 10.5 6.8 8.4 7.5 13.1 9.0 12.9 56.5

# of Stocks 50 50 50 100 50 40 30 30 88

Source: Dow Jones Indexes. From December 31, 1993 through December 31, 2001.

DO W JO N E S IN D E X E S

China Stock Market in a Global Perspective

September 2002

32

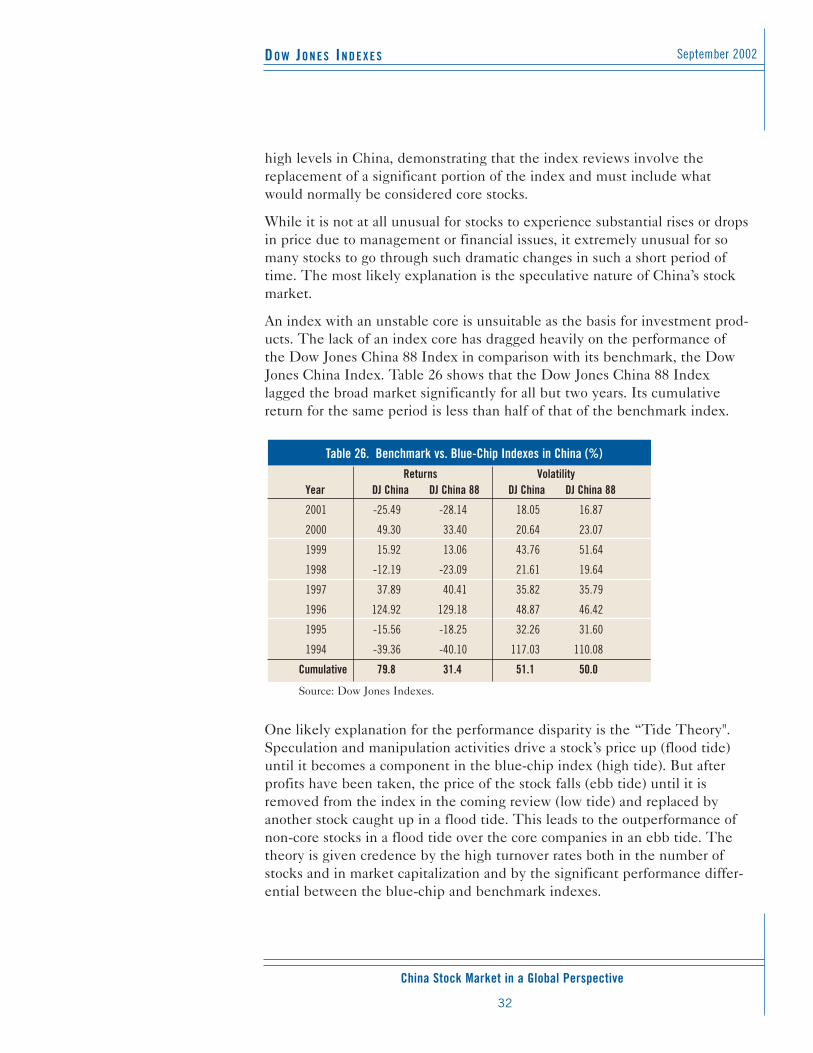

high levels in China, demonstrating that the index reviews involve thereplacement of a significant portion of the index and must include whatwould normally be considered core stocks.