Preferential trade agreements AND MULTILATERAL LIBERALIZATION

WOrld Trade repOrT 2011

122

This section considers to what extent conclusions about deep preferential trade agreements (PTAs) and production networks, reached in Section C, are supported by evidence. The evidence presented includes an examination of the magnitude of preferential tariff rates, the coverage and contents of the agreements, econometric evidence on the relationship between production networks and deeper PTAs and the integration experience of specific PTAs.

d. anatomy of preferential trade agreements

II – tHe Wto AnD PReFeRentIAL tRADe AGReements

123

D. A

nA

tom

y o

F PR

eFe

Re

ntIA

L

tRA

De

AG

Re

em

en

ts

Contents 1. ArelowertariffsstillimportantforPTAs? 124

2. PatternsinthecontentofPTAs 128

3. ProductionnetworksanddeepPTAs 145

4. Africanregionalcooperation:lessonsfromdeepintegration? 151

5. Conclusions 153

Appendixtables 157

Some key facts and findings

• MFN tariffs are low and equal to 4 per cent on average in 2009.

• Most “sensitive” sectors remain “sensitive” in PTAs. Approximately

66 per cent of tariff lines with MFN rates above 15 percentage points

have not been reduced in PTAs.

• If the preferential access enjoyed by other exporters is taken into

account, less than 13 per cent of preferential trade benefits from a

competitive advantage exceeding 2 percentage points.

• Signing deep integration PTAs increases trade in production

networks by almost 8 per cent on average. In addition, high levels

of trade in production networks raise the likelihood of signing

deep agreements.

WOrld Trade repOrT 2011

124

1. ArelowertariffsstillimportantforPTAs?

TariffshaveprogressivelyfallensincetheestablishmentoftheGeneralAgreementonTariffsandTrade(GATT)in 1948. The pre-GATT average tariff among majortrading countries was between 20 and 30 per cent.1Since then, unilateral liberalization, eight rounds ofmultilateraltradenegotiationsandnumerousPTAshavesignificantly reduced the tariffs applied by WTOmembers.In2009,theaverageappliedtariffacrossallproductsandcountrieswasamere4percent.

The process of most-favoured nation (MFN)liberalization (i.e. the reduction of tariffs on an MFNbasis for all WTO members) accelerated in the late1980sand1990s,whenappliedtariffswerereducedinmany developing countries. The rates applied bydevelopedcountrieswerealready low,ataround6percent on average by the end of the 1980s. Theycontinued to decline subsequently, to an average ofapproximately 3 per cent in 2009. Average appliedtariffshavebeenfallinginallregions(seeFigureD.1).InSouth-CentralAmerica,theaveragetariffratefellfromover30percentatthebeginningofthe1990stolessthan10percenttenyearslater.Overthesameperiod,tariffsinEastAsiadroppedfromaround15-20percenttosome6percentin2009.Similarly,inAfrica,appliedMFNtariffsfellfromanaveragerateofroughly30percent to some 12 per cent in 2009. The reduction of

tariffs was more pronounced in West Asia, where theaverageMFNappliedtariffratefellfromanaverageofabout45percenttobelow15percent.

Tariff reductionshavenotoccurredat thesamepacein all sectors. Significant tariff barriers still exist inagriculture and some manufacturing sectors. MostMFN tariff reductions took place in manufacturedgoods,however,withparticularemphasisonpartsandcomponents (see Figure D.2). The latter trendaccompaniedthedevelopmentofproductionnetworks.

Despitevarianceintariffratesaroundtheaverage,lowaverage MFN rates suggest that the scope forexchangingpreferentialmarketaccessisunlikelytobeextensive. A similar conclusion is suggested by thedataontradeflows.AsseeninSectionB,theshareofMFN duty-free trade in total trade is estimated at52 per cent in 2008 (excluding trade within the EU),andover70percentoftotal tradeoccursatanMFNtariffrateofbelow5percent.

Moreover,PTAscannotbesatisfactorilyexplainedbyadesire to remove tariff peaks (i.e. relatively highertariffs).Most“sensitive”sectorswithhighertariffsalsotend to retain higher tariffs in PTAs. As shown inFigureD.3,forexample,tarifflinessubjecttoanMFNrate above 15 per cent continue to be subject torelatively high rates in PTAs. According to the 2007datareportedinthefigure,approximately66percent

FigureD.1: mFn tariff trends in developing countries by region (Percentage)

Note: Inorder toavoidsampleselectionbias,figureshavebeencalculated forabalancedsub-sampleofcountries ineach regionandmissingdatahavebeeninterpolated.Inthissubsample,EastAsiacomprises13economies(Australia;KingdomofBahrain;China;HongKong,China; Indonesia;Japan;RepublicofKorea;Malaysia;NewZealand;Philippines;Singapore;Thailand;andChineseTaipei);WestAsiacoversfourcountries(Bangladesh;India;SriLanka;andNepal);SouthandCentralAmericaismadeupof12countries(Argentina;thePlurinationalStateofBolivia;Brazil;Chile;Colombia;Cuba;Ecuador;Paraguay;Peru;TrinidadandTobago;Uruguay;andtheBolivarianRepublicofVenezuela);andAfricaincludes11countries(BurkinaFaso;Côted’Ivoire;Algeria;Ghana;Morocco;Nigeria;Rwanda;Tunisia;Tanzania;SouthAfrica;andZimbabwe).Thedatausedinthefigurearesimpleaveragesofad valoremlinesinallsectors.

Source:CalculationsbasedonTrainsdatabase,WITS.

Sim

ple

aver

age

(at t

he p

rodu

ct le

vel)

1990 1995 2000 2005 2010

50

40

30

20

10

0

Africa South and Central America

East Asia West Asia

II – tHe Wto AnD PReFeRentIAL tRADe AGReements

125

D. A

nA

tom

y o

F PR

eFe

Re

ntIA

L

tRA

De

AG

Re

em

en

ts

ofthetariffsabovethisratehavenotbeenreducedatall throughPTAs.Thismeans that “preferential” ratesarenolowerthanMFNrates.

Recent work has emphasized that the value of aparticular preferential tariff must be gauged in thecontextofanimportingcountry'soveralltariffpolicy.2

Thus, in a world of numerous PTAs, the advantageconferred by a preferential tariff to a given exporterdoesnotdependonlyon that rate,butalsoon tariffsfaced by competing suppliers from other countries inthesamemarket.

Inordertoaccountfortheactualadvantageprovidedbypreferences, Low et al. (2009) use the concept of a“competition-adjusted”preferencemargin,calculatedasthepercentage-pointdifferencebetweentheweighted

averagetariff rateapplied to therestof theworldandthepreferential rateappliedtothebeneficiarycountry,where weights are represented by trade shares in thepreference-grantingmarket(seeBoxD.1).

Unlike a traditional preference margin which was thebasis of the analysis in Section B, this competition-adjusted preference margin can assume positive aswell as negative values. A negative value indicatesthat, in a specific market, a certain country facesworse market conditions than its trade competitors.3Competition-adjusted preference margins emphasizethefactthatPTAscanresultfromthedesiretoavoidnegative discrimination rather than to benefit from apositive preference margin. This is the underlyingargument for theso-called “dominoeffect” toexplaintheproliferationofPTAs(seeSectionC).

FigureD.2: World mFn applied tariff trends (Percentage)

Note:Underlyingdataaretrade-weightedaveragesofad valoremrates.

Source:Trainsdatabase,WITS.

FigureD.3: Preferential reductions of tariff rates above 15 per cent, 2007

Note:“PreferentialequalMFN”denotestheshareoftarifflinesattheHS-6levelwithanMFNrateabove15percentthathavenotbeenreducedunderPTAs.“PreferentialbelowMFN”denotestheshareoftarifflinesthathavebeenatleastpartiallyreduced.

Source:CalculationsbasedontheFugazzaandNicita(2010)database,coveringthePTAsof85countries,accountingfor90percentofworldtrade.

MF

N a

pplie

d ta

riff

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008

10

9

8

7

6

5

4

3

2

1

0

Parts and components All products

Preferential below MFN34 per cent

Preferential equal MFN 66 per cent

WOrld Trade repOrT 2011

126

BoxD.1:measurement of the value of preferences

Traditionally, the valueofapreferencemargin forabeneficiarycountryhasbeenmeasuredsimplyas thedifference in terms of percentage points between the MFN rate and the preferential tariff. Or, expressedformally:

Traditionalpreferencemargin= jik

MFNik TT ,,

where MFNikT , istheMFNrateappliedbycountrykonproduct iand j

ikT , isthepreferentialrateappliedto

countryj.Bydefinitionthismargincanonlybepositive.

Alimitationofthismeasureofthevalueofthepreferenceisthatitcannotaddressthequestionwhethertheputative advantage of a preference effectively helps the beneficiary to export to the preference-givingcountry.Sincenumerousandoverlappingpreferentialtradeagreementsexistaroundtheworld,theMFNratedoesnotprovideanappropriatebasisforcalculatingthepreferencemargin.Onthecontrary,thevalueofapreferenceforonecountrywillultimatelydependontheadvantage/disadvantage ithasvis-à-vis theothercountriescompetinginthesamemarket.

The “competition-adjusted” preference margin proposed by Low et al. (2009) addresses this concern bymeasuringthevalueofapreferenceasthepercentage-pointdifferencebetweentheweightedaveragetariffrateappliedtotherestoftheworldandthepreferentialrateappliedtothepreferentialagreementpartner,where weights are represented by trade shares in the preference granting market. The formula for thismeasureisexpressedasfollows:

Competition-adjustedpreferencemarginforproducti= jik

wik TT ,,

where

vivk

v

vikivk

wik X

TXT

,

,,

, is theexport-weighted(X intheformuladenotesexportsofv intok)average

tariff imposedbycountrykonallotherexportingcountriesv (excludingcountry j) in respectofproduct i.Equivalently,theformulacapturesweightedtariffimposedbykonimportsfromallothercountriesbutj.As

before, jikT ,

isthepreferentialrateappliedtocountryj.Thiscompetition-adjustedpreferencemargincanbepositiveornegative,dependingonwhetherexportersofgood i fromcountry jbenefit frommarketaccessconditionsmoreorlessfavourablethantheothertradingpartnersofcountrykinthesamemarket.

In order to measure the overall level of advantage or disadvantage that a beneficiary under a PTA faces inenteringanothermarket in thepreferentialarea,FugazzaandNicita (2010)estimated theoverall value toacountryofpreferencesintermsofthedegreeofresponsivenessofimportdemandtovariationsinprice(priceelasticity of import demand), taking into account the trade share of the country concerned. Under thisspecification of the value of the preference, which the authors call the “relative preference margin” (RPM),preferencemarginsarethusweightedbytherelevantimportdemandelasticityandbytheexportshareofthepreference-receivingcountry.Therationaleforincludingtheseelementsinthepreferencemargincalculationisthat a preference margin is more or less valuable to the exporting country depending on the elasticity ofdemandintheimportingcountryandontheexportcapabilityoftheexportingcountry.Whenimportdemandiselastic,agivenpreferencemargingivesrisetolargerincreasesinimportdemandthanwhentheimportdemandisinelastic.Inaddition,apreferenceismorevaluabletoanexporterthehigherthelevelofexports.

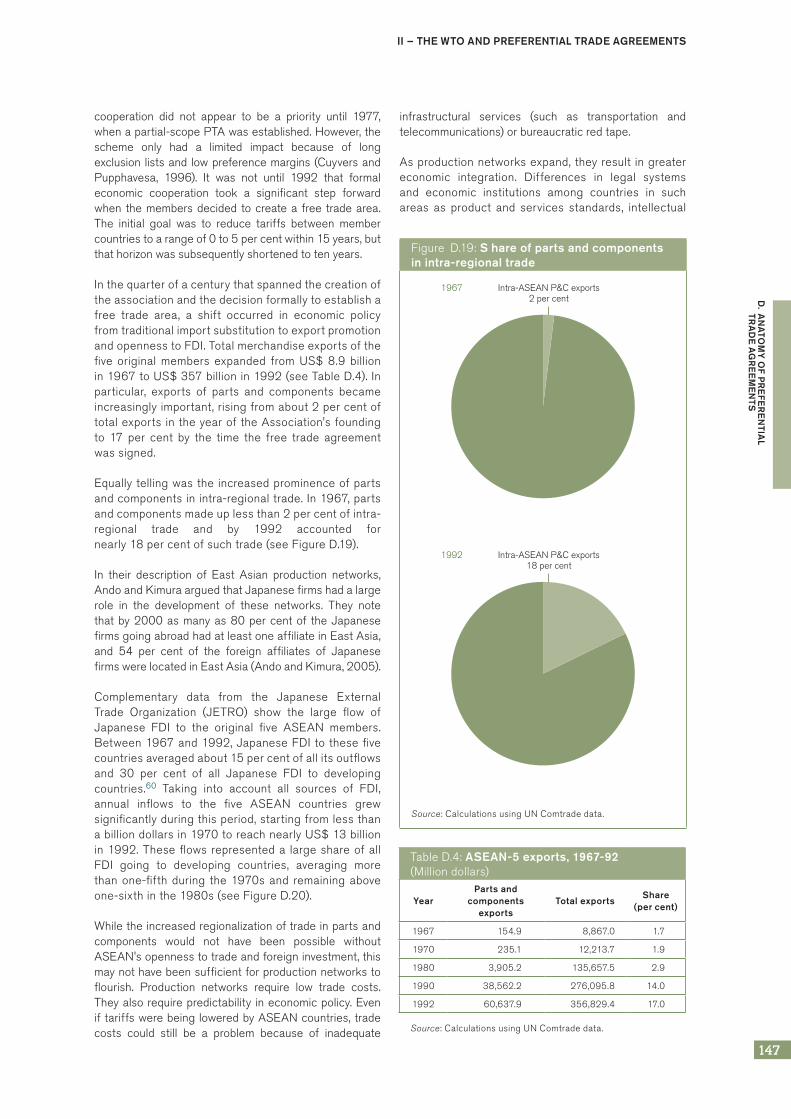

TheformulafortheRPMis:

kj

X

TTXRPM

iikijk

i

jik

wikkiijk

jk

,

,,

,,,

whereεisanestimateofthepriceelasticityofdemandforanimport,andtheothervariablesaredefinedasabove.

II – tHe Wto AnD PReFeRentIAL tRADe AGReements

127

D. A

nA

tom

y o

F PR

eFe

Re

ntIA

L

tRA

De

AG

Re

em

en

ts

TableD.1showsthedistributionofcompetition-adjustedpreference margins at the Harmonized System (HS)6-digit level for the years 2000 and 2007. Thedistribution is highly concentrated, falling within therange of –2 per cent and +2 per cent. In 2007, over87 per cent of trade fell inside this range. Exceptperhaps for highly demand-elastic goods that areparticularlyresponsivetopricechanges,thesenumberssuggestthattodaytariffpreferencesareunlikelytobeasole reason,or insomecasesnotevenamajorone,forcountriesenteringPTAs.

A limitation of using competition-adjusted preferencemargins as a measure of the value of preferences isthattheydonottakeintoaccountthefactthatimportsofsomegoodscanbemoreresponsivethanotherstochanges in price. A reduction of the tariff on a goodwhose demand is inelastic (i.e. not very sensitive topricechanges)willhaveasmallerimpactontheoverallvolume of trade than a reduction of the samemagnitude for demand-elastic goods. Even a lowpreference margin may trigger significant changes inthe volume of trade when the import demand for thegood is elastic. In these circumstances, even lowpreferencemarginsmightleadtotheestablishmentofPTAs. Applying product-specific price elasticities toproducts,FugazzaandNicita(2010)defineanindexofthe overall advantage/disadvantage that exporters incountryA face incountryB (seeBoxD.1).This indexaccords lower weights to competition-adjustedpreference margins that are less sensitive to pricechanges(inelasticgoods)thanthosethataresensitive(elasticgoods).

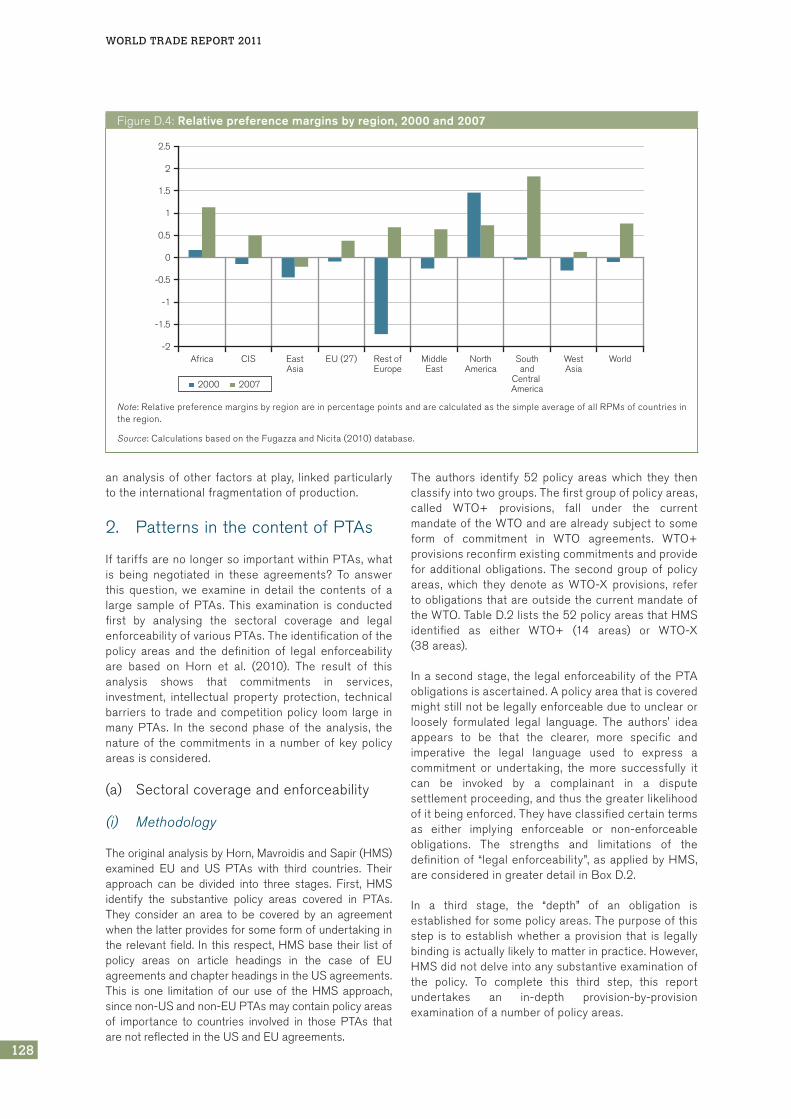

Data based on this relative preference margin (RPM)index was calculated for a sample of 85 countriescovering90percentoftradebetween2000and2008.As shown in Figure D.4, RPMs improved on averageacrossall regionsbetween2000and2007, except inNorthAmerica,wheretheinitialcompetitiveadvantageof the region has been eroded by the proliferation of

PTAs in other areas. In general, PTAs have helpedcountriestooffsetorreducethenegativediscriminationthey suffer vis-à-vis non-PTA trading partners. Forexample, countries in South and Central Americasignificantlyimprovedtheirconditionsofmarketaccessbetween 2000 and 2007, mainly because of thenumerousPTAstheysignedoverthatperiod.

Figure D.4 shows that on average RPMs were below1 per cent in 2007. Africa and South and CentralAmericahadRPMsinexcessofthisaverage.FugazzaandNicita(2010)calculatedthata1percentchangein the RPM would have a trade impact of 0.34 percent.4 This implies that a rise or fall of 2 per cent intrade would require a change in the RPM of at least5percentagepoints.ElSalvadoristheonlycountryinthe sample covered by the Fugazza and Nicitadatabase that satisfies these conditions. This findingreinforces our conclusion that limited scope remainsforthepursuitofpreferencesinPTAs.

In sum, the proliferation of PTAs between 2000 and2007 has improved the conditions of market accessfor signatory countries. To a large extent, theimprovement has been due to the reduction in thenumber of instances where relative preferencemargins were negative (i.e. cases where a countryfaces worse market conditions than its tradecompetitors). One may argue, therefore, that PTAshave in part restored a “level-playing field” for thosecountries that facedworseconditionsofaccess thanothers. Whether or not adjusted for tariffs faced byother suppliers, the overall level of tariffs faced byexporters is low, as is the volume of trade for whichpreference margins are significant.5 Low averagebenefits accruing from preferential tariffs on trademay nevertheless conceal larger effects for someproducts and countries, and this should be borne inmindinthecontextofthebroaderconclusionreachedin this report that preferential tariffs are no longer amajorconsiderationinPTAformation.Wenowturnto

Table D.1: share of tariff lines and trade by level of competition-adjusted preference margin, 2000 and 2007 (Percentage)

Competition-adjusted preference margin

2000 2007

tL covered trade covered tL covered trade covered

<–30 0.2 0.0 0.1 0.0

–30;–15 1.1 0.3 0.5 0.1

–15;–5 7.1 3.4 4.6 2.3

–5;–2 9.3 5.8 6.3 3.5

–2;2 72.4 77.8 79.0 87.3

of which MFN = 0 9.2 18.5 25.3 42.5

2;5 5.7 7.6 5.6 4.5

5;15 3.7 4.1 3.1 2.0

15;30 0.4 0.9 0.6 0.2

>30 0.1 0.1 0.1 0.0

Source:CalculationsbasedontheFugazzaandNicita(2010)database,coveringthePTAsof85countries,accountingfor90percentofworldtrade.

WOrld Trade repOrT 2011

128

ananalysisofother factorsatplay, linkedparticularlytotheinternationalfragmentationofproduction.

2. PatternsinthecontentofPTAs

IftariffsarenolongersoimportantwithinPTAs,whatis being negotiated in these agreements? To answerthis question, we examine in detail the contents of alarge sampleofPTAs. Thisexamination is conductedfirst by analysing the sectoral coverage and legalenforceabilityofvariousPTAs.Theidentificationofthepolicy areas and the definition of legal enforceabilityare based on Horn et al. (2010). The result of thisanalysis shows that commitments in services,investment, intellectual property protection, technicalbarriers to tradeandcompetitionpolicy loom large inmany PTAs. In the second phase of the analysis, thenatureof thecommitments inanumberofkeypolicyareasisconsidered.

(a) Sectoralcoverageandenforceability

(i) Methodology

TheoriginalanalysisbyHorn,MavroidisandSapir(HMS)examined EU and US PTAs with third countries. Theirapproach can be divided into three stages. First, HMSidentify the substantive policy areas covered in PTAs.They consider an area to be covered by an agreementwhenthelatterprovidesforsomeformofundertakingintherelevantfield. In this respect,HMSbasetheir listofpolicy areas on article headings in the case of EUagreementsandchapterheadingsintheUSagreements.This is one limitation of our use of the HMS approach,sincenon-USandnon-EUPTAsmaycontainpolicyareasof importance to countries involved in those PTAs thatarenotreflectedintheUSandEUagreements.

The authors identify 52 policy areas which they thenclassifyintotwogroups.Thefirstgroupofpolicyareas,called WTO+ provisions, fall under the currentmandateoftheWTOandarealreadysubjecttosomeform of commitment in WTO agreements. WTO+provisionsreconfirmexistingcommitmentsandprovideforadditionalobligations.Thesecondgroupofpolicyareas, which they denote as WTO-X provisions, refertoobligationsthatareoutsidethecurrentmandateoftheWTO.TableD.2liststhe52policyareasthatHMSidentified as either WTO+ (14 areas) or WTO-X(38areas).

Inasecondstage, the legalenforceabilityof thePTAobligationsisascertained.Apolicyareathatiscoveredmightstillnotbelegallyenforceableduetounclearorloosely formulated legal language. The authors' ideaappears to be that the clearer, more specific andimperative the legal language used to express acommitment or undertaking, the more successfully itcan be invoked by a complainant in a disputesettlementproceeding,andthusthegreaterlikelihoodofitbeingenforced.Theyhaveclassifiedcertaintermsas either implying enforceable or non-enforceableobligations. The strengths and limitations of thedefinitionof“legalenforceability”,asappliedbyHMS,areconsideredingreaterdetailinBoxD.2.

In a third stage, the “depth” of an obligation isestablishedforsomepolicyareas.Thepurposeofthisstep is toestablishwhetheraprovision that is legallybindingisactuallylikelytomatterinpractice.However,HMSdidnotdelveintoanysubstantiveexaminationofthe policy. To complete this third step, this reportundertakes an in-depth provision-by-provisionexaminationofanumberofpolicyareas.

FigureD.4: Relative preference margins by region, 2000 and 2007

Note:RelativepreferencemarginsbyregionareinpercentagepointsandarecalculatedasthesimpleaverageofallRPMsofcountriesintheregion.

Source:CalculationsbasedontheFugazzaandNicita(2010)database.

Africa CIS EastAsia

EU (27) Rest ofEurope

MiddleEast

NorthAmerica

Southand

Central America

WestAsia

World

2.5

2

1.5

1

0.5

0

-0.5

-1

-1.5

-2

2000 2007

II – tHe Wto AnD PReFeRentIAL tRADe AGReements

129

D. A

nA

tom

y o

F PR

eFe

Re

ntIA

L

tRA

De

AG

Re

em

en

ts

TableD.2: Wto+ and Wto-x policy areas in PtAsWto+ areas Wto-x areas

PTAindustrialgoods Anti-corruption Health

PTAagriculturalgoods Competitionpolicy Humanrights

Customsadministration Environmentallaws Illegalimmigration

Exporttaxes IPR Illicitdrugs

SPSmeasures Investmentmeasures Industrialcooperation

Statetradingenterprises Labourmarketregulation Informationsociety

Technicalbarrierstotrade Movementofcapital Mining

Countervailingmeasures Consumerprotection Moneylaundering

Anti-dumping Dataprotection Nuclearsafety

Stateaid Agriculture Politicaldialogue

Publicprocurement Approximationoflegislation Publicadministration

TRIMSmeasures Audiovisual Regionalcooperation

GATS Civilprotection Researchandtechnology

TRIPS Innovationpolicies SMEs

Culturalcooperation Socialmatters

Economicpolicydialogue Statistics

Educationandtraining Taxation

Energy Terrorism

Financialassistance Visaandasylum

Source:Hornetal.(2010).

BoxD.2:Legal enforceability

For thepurposeofclassifyingprovisions inPTAsas “legallyenforceable”or “non-enforceable”,Hornetal.(2010)focusontwovariablesrelatingtodisputesettlement:(a)theactualterminologyofaprovision,andinparticularwhetheraprovision“specifiesatleastsomeobligationthatisclearlydefinedandlikelyeffectivelytobindtheparties”,asdistinguishedfromvagueundertakingsthatare“notlikelytobesuccessfullyinvokedbyacomplainantinadisputesettlementproceeding”;and(b)whethertheagreement“explicitlystatesthatdisputesettlementisnotavailablefortheprovision”underthePTA.

Although these two variables constitute a solid starting point, there are a number of other variables –includingthoserelatedtodisputesettlement–thatcouldalsohaveabearingonthe“legalenforceability”ofobligationsarisingunderPTAs.TheHMSstudy,however,focusessolelyonthetextofPTAs,andnotontheireffectsorimplementation.

Whetherornottheactualterminologyofaprovisionestablishesalegallyenforceableobligationisaquestionoftreatyinterpretation.Animportantconsiderationisthereforetheapproachtotreatyinterpretationadoptedin the PTA. For example, in the context of WTO dispute settlement proceedings, the Appellate Body hasrepeatedlyemphasizedtheprincipleof“effectiveness”intreatyinterpretation,whichprovidesallofthetermsoftheWTOagreementswitha“legallyoperativemeaning”.TheAppellateBodyhasfoundonmorethanoneoccasionthattheterm“should”,inthesamewayas“shall”,cangiverisetoalegalobligation.

The tradition of treaty interpretation stems from the Vienna Convention on the Law of the Treaties 1969(VCLT).TheVCLTisa legal instrumentcodifiedbytheUNInternationalLawCommission. Itsetsoutrulesrecognizedascustomary international law.Forpresentpurposes, therelevantrulesoftreaty interpretationarelaiddowninArticles31-33oftheConvention.Article31oftheVCLTestablishesfourelementsthathavetobecombinedintheinterpretationofatreaty.Atreatyhastobeinterpreted:i)ingoodfaith;ii)withintheordinarymeaningofitsterms;iii)initsspecificcontext;andiv)inthelightofitsobjectandpurpose.6PTAsarerecognizedastreatiesunderinternationallawandhavetobeinterpretedinaccordancewiththerulesoftheVCLT.7

Thestrongfocusontheuseof legal languageinaPTAisreferredtoasatextualor literal interpretation.8The languageofaprovision reveals its intentionand theextent towhich itdeclares legalobligationsandrights.9The languagealsohelps todefinedemarcationsand thescopeofWTO law indisputesettlement

WOrld Trade repOrT 2011

130

The analysis conducted here extends HMS's originalanalysisof14EUand14USPTAstoatotalof96PTAs.Of these, 33 involve the EU and 11 involve the UnitedStates. The sample covers some recently concludedEPAs by the EU, with Cameroon and CARIFORUM, forexample,aswellasEuromedagreements.The42otherPTAswereconcludedbyregionaltradingblocsandmajortrading powers, such as the Association of SoutheastAsianNations(ASEAN),China,theEuropeanFreeTradeAgreement (EFTA), India and the Southern CommonMarket (MERCOSUR). PTAs from Africa (such asCOMESA and ECOWAS) and the Middle East (such asthe GCC and PAFTA) are also included in the analysis.ThesampleofPTAswaschosenprimarilyonaccountofthevolumeoftradewithinthePTA,butalsoincludedtheinitial set of PTAs examined in the HMS study (seeAppendixTableD.1foradetailedlistofthePTAscovered).

The HMS study only covers PTAs concluded by WTOmembers, signedby thepartiesandmostlynotified totheWTOasofOctober2008.Itconsidersagreementssignedbothbeforeandafter thecreationof theWTO,

butexcludesthosewherepartnersarenotmembersoftheWTO.Threeagreementsthathavebeensignedbutthatarenotyetratifiedwerealsoincludedinthestudy.HMSfurtherrestrictstheselectionofPTAsinitsstudytothoseconcludedunderArticleXXIVoftheGATTorArticleVoftheGeneralAgreementonTradeinServices(GATS).AgreementsnotifiedundertheEnablingClausearenot taken intoaccount.All thePTAsconsidered inthe HMS study are free trade agreements, except forEU-Turkey,whichisacustomsunion.

Thesampleusedinthisreportalsoincludesagreementsin which not all partners are members of the WTO.Somenon-notifiedagreementsarecovered,butallarein force. The sample covers the period from 1958 to2010. PTAs notified under the Enabling Clause areincludedalongwithothersnotifiedunderGATTArticleXXIVandGATSArticleV.Eighty-twooftheagreementscovered are free trade agreements, 12 are customsunions and two are partial scope agreements.14 Fouramong the EC agreements are enlargementagreements.

proceedings.Inthisrespect,treatylanguagealsorevealsthoseareasthathavenotbeennegotiatedwithintheframeworkoftheWTO.10Theprocessofenforcement,however,makesuseofotherapproachesinWTOdisputesettlement.Threeaspectsofthelegalenforceabilityofaprovisionarementionedbelow,inadditiontothetextualapproach.

First, obligations arising under the WTO agreements may have a bearing on the legal enforceability ofobligationsunderPTAs.HMSconsiderprovisionscarvedoutfromdisputesettlementproceedingsasbeingnon-enforceable.TotheextentthataprovisionofaPTAaddressesanareathatisalsodirectlyorindirectlycoveredbyoneormoreobligationsundertheWTOagreements, it remainstobeseenwhetheraPTAcandepriveapartyof its rightofaccess to theWTOdisputesettlement system. Inotherwords, the fact thatdispute settlement may not be available in respect of that provision under the PTA would not necessarilyprecludeapartyfromhavingrecoursetoWTOdisputesettlementproceduresinrespectofthecorrespondingobligation(s) under the WTO agreements. This complex and unsolved legal question leaves open whetherandtowhatextentrulesofconflictleadingtotheenforcementofaprovisionunderaPTAcanoverridetheWTOdisputesettlementsystem.11

Secondly,totheextentthattheconceptoflegalenforceabilityislinkedtothepossibilityofapplyingcounter-measurestogiveforcetoPTAobligations,rightsandobligationsunderWTOagreementslimitingtheuseoftrade counter-measures may also have a bearing on the enforceability of certain PTAprovisions.AnotherrelatedissuereferstotheenforceabilityofWTO-Xprovisions.Towhatextent is itpossibletomakeuseoftradecounter-measurestoenforcethosepolicyareasnotcoveredbytheWTO(Marceau,2009)?Thescopeandlimitationsoftherelevantlawstillneedtobeclarified.12

Thirdly,non-legalconsiderationsareanimportantfactorwhendeterminingtheenforceabilityofobligationsintradeagreements.Thisapproachencompassespoliticalfactorsasrelevantintheprocessoflegaldrafting,thusleadingtotheadoptionoflooselyformulatedlegallanguage.Itdoesnot,however,takeexternalpoliticalfactorsintoconsiderationthatmightbeimportantfortheactualenforcementofaprovisioninpractice.13AsHMS acknowledge, “provisions may be enforced not only through a formal judicial dispute settlementmechanism,butalsothroughmorepoliticalmeans”.Inotherwords,thefactthatparticularobligationsmaybecarved out from dispute settlement procedures does not necessarily mean that parties cannot seek toenforcesuchobligations throughpoliticalordiplomaticmeans.However, the reverse isalso true.The factthatparticularobligationsarenotcarvedoutfromdisputesettlementproceduresdoesnotnecessarilymeanthatlegalenforcementthroughdisputesettlementproceedingsisalwaysarealisticandviableoption.

Thevastmajorityofprovisionsinregionalandbilateraltradeagreementsareneverthesubjectofanydisputesettlementproceedings,evenwherea right to invokeproceedingsexists. Inanutshell,provisions thatarelegallyenforceableintheorymaybedifficulttoenforceinpractice,whetheronaccountofpoliticalfactors,resourceconstraints,orothernon-legalconsiderations.

II – tHe Wto AnD PReFeRentIAL tRADe AGReements

131

D. A

nA

tom

y o

F PR

eFe

Re

ntIA

L

tRA

De

AG

Re

em

en

ts

The majority of the EU's PTAs are concluded withneighbouring countries, whereas those of the UnitedStates tend to be more widely spread geographically.Included in the coverage are ten PTAs concluded byJapan, seven by China, five by Australia, five by theRepublic of Korea and four by India. The sample covers18majortradingblocs.TheanalysisheredepartsslightlyfromtheHMSapproachinthatcertainobligationscoveredmaynotbe thesubjectofadedicatedarticleorchapter.Provisionsintheareasof“visaandasylum”or“informationsociety”,forexample,areoftennotexplicitlymentionedasanarticleorchapterheading,but in thecontextofotherprovisions.Anothernotableexampleisexporttaxeswhere,unlike HMS, this report considers “customs duties onexports”assynonymouswithexporttaxes.Finally,itshouldbe noted that the analysis relates to the version of thetradeagreementasitwassignedornotifiedtotheWTO.Thismeansitwillnotcapturesubsequentchangestoanagreement, such as the addition of new areas ofcooperationorastrengtheningofexistingprovisions.

(ii) Empirical evidence on PTA content by income, policy area and over time

Figure D.5 shows that the average number of WTO+areas coveredbyPTAshasbeen increasingover time.From1958to2010,theproportionoflegallyenforceableprovisionswasveryclosetothetotalnumberofsectorscovered. As described above, WTO+ areas are thosecovered by existing WTO agreements. The patternobserved suggests that deepening commitments intheseareas,i.e.goingbeyondcommitmentsintheWTO,continuetobeamajordrivingforceforrecentPTAs.

Incontrast,thepatternovertimeofWTO-Xprovisionsisless clear (see Figure D.6). It is certainly the case thatPTAscomingintoforcesince2000covermoreWTO-Xareasthanagreementsestablishedearlier,andthatmoreof them are legally enforceable. However, the gap

betweenareascoveredthatarelegallyenforceableandthose that are not is still higher for WTO-X provisionsthanforWTO+provisions.Hornetal.(2010)characterizeWTO-Xprovisionsas largely regulatory innature.Usingthis interpretation, and even accounting for the smallerproportion of these areas that are enforceable, thegrowth in the average number of WTO-X provisions inrecentPTAsisatestimonytothegrowingimportanceofbehindthebordermeasuresinPTAs.

Which specific policy areas figure prominently inpreferentialtradeagreements?FigureD.7presentsthenumber of PTAs in the sample with specific WTO+provisions. As expected, all of the 96 agreementscontainprovisionsrelatingtoindustrialandagriculturaltariffs.However,an increasingly largenumberofPTAsnowgobeyondmerchandisetariffs,includingprovisionson technical barriers to trade, services, intellectualpropertyandtrade-relatedinvestmentmeasures.FigureD.7alsoshows thateven if oneexamineseachof theWTO+ areas individually, there is not much of a gapbetweencoverageandlegalenforceability.

The main policy areas covered by WTO-X provisionsare competition policy, intellectual property rights,investmentandmovementofcapital (seeFigureD.8).These are also the policy areas that are most oftenlegallyenforceableinPTAs.Thenextlargestgroupofpolicy areas with legally enforceable provisions(present in about one-third of the agreements) areenvironmental laws, labour market regulations andmeasures on visa and asylum. The remaining legallyenforceablepolicyareasappearinlessthantenoftheagreements. So while there appears to have been asignificant increase in new policy areas in PTAs, thepicturethatemergesfromFigureD.8ismorenuanced.Only a handful of truly important areas are affected,whereimportanceisjudgedbywhethertheprovisionscanbeenforcedbythepartiestotheagreement.

Figure D.5: Covered and enforceable Wto+ provisions over time

Source:WTOSecretariat.

Figure D.6: Covered and enforceable Wto-x provisions over time

Source:WTOSecretariat.

Num

ber o

f WTO

+ p

rovi

sion

s (a

vera

ge)

1958-79 1980-89 1990-99 2000-10

12

10

8

6

4

2

0

Covered Enforceable

Num

ber o

f WTO

-X p

rovi

sion

s (a

vera

ge)

1958-79 1980-89 1990-99 2000-10

12

10

8

6

4

2

0

Covered Enforceable

WOrld Trade repOrT 2011

132

To investigate possible differences among PTAssigned between categories of countries – that is,developed-developed, developed-developing anddeveloping-developing – the average number ofprovisionsinthesePTAcategoriesarecompared(seeFigureD.9).PTAsbetweendevelopedanddevelopingcountries contain on average a higher number oflegally enforceable WTO+ provisions compared withPTAs between trading partners with similar levels ofincome (i.e. among developed or among developingcountries). How might this be explained? Barriersaffecting goods and services are generally higher in

developing than in developed countries. DevelopedcountriesmightusePTAswithdevelopingcountriestoobtaindeeperlevelsofcommitmentsthanthosemadein the WTO. In exchange, developing countries mightacquirefullerandgreatersecurityofmarketaccesstothelargeeconomiesoftheirPTApartners.

As shown in the second panel of Figure D.9, PTAsbetweendevelopedanddevelopingcountriesalsocovera higher average number of WTO-X provisions thanPTAsbetweentwodevelopedcountriesorbetweentwodevelopingcountries.However,mostoftheseprovisions

FigureD.7: number of agreements covering Wto+ provisions

Source:WTOSecretariat.

FigureD.8: number of agreements covering Wto-x provisions

Source:WTOSecretariat.

Num

ber o

f PTA

s

Indu

stria

l tar

iffs

Agr

icul

tura

l tar

iffs

Cus

tom

s

AD

CV

M

Exp

ort t

ax

TBT

GAT

S

TRIP

S

Sta

te a

id

Pub

lic p

rocu

rem

ent

SP

S

STE

s

TRIM

S

100

90

80

60

40

70

50

30

20

10

0

Sector covered Legally enforceable

Num

ber o

f PTA

s

IPR

Agr

icul

ture

Ene

rgy

Cul

tura

l coo

pera

tion

Info

rmat

ion

soci

ety

Hum

an ri

ghts

Eco

nom

ic p

olic

y di

alog

ue

Mon

ey la

unde

ring

Dat

a pr

otec

tion

Illeg

al im

mig

ratio

n

Taxa

tion

Pub

lic a

dmin

istr

atio

n

Nuc

lear

saf

ety

Civ

il pr

otec

tion

Com

petit

ion

polic

y

Mov

emen

t of c

apita

l

Reg

iona

l coo

pera

tion

Indu

stria

l coo

pera

tion

Fina

ncia

l ass

ista

nce

Env

ironm

enta

l law

s

Edu

catio

n an

d tr

aini

ng

Visa

and

asy

lum

Con

sum

er p

rote

ctio

n

Sta

tistic

s

Inve

stm

ent

Res

earc

h an

d te

chno

logy

Labo

ur m

arke

t reg

ulat

ion

Soc

ial m

atte

rs

SM

EA

ppro

xim

atio

n of

legi

slat

ion

Pol

itica

l dia

logu

e

Illic

it dr

ugs

Ant

i-cor

rupt

ion

Aud

iovi

sual

Min

ing

Hea

lth

Terr

oris

m

Inno

vatio

n po

licie

s

100

90

60

40

50

30

20

10

0

Sector covered Legally enforceable

II – tHe Wto AnD PReFeRentIAL tRADe AGReements

133

D. A

nA

tom

y o

F PR

eFe

Re

ntIA

L

tRA

De

AG

Re

em

en

ts

are not legally enforceable. Agreements betweendevelopedcountriesonaveragehaveahighernumberof enforceable provisions, with PTAs betweendeveloping countries having the smallest number ofenforceable WTO-X provisions. The pattern betweendeveloped and developing countries observed in theportionofFigureD.9dealingwithWTO-Xprovisionsisconsistent with the argument made by HMS thatdeveloped countries are seeking to “export” theirregulatory regimes to developing countries. The factthat most of these WTO-X provisions are not legallyenforceable may suggest limited success in theseefforts, or perhaps that the process of regulatoryconvergenceinalegallybindingsenseisagradualone.

It may at first appear surprising that agreementsbetween developing countries include WTO-X policyareas. However, this pattern becomes moreunderstandablegiventhatmanyofthesePTAstypicallyinvolve upper or middle-income developing countriessuch as Chile, the Republic of Korea and Singapore.They may have the same interest in exporting theirregulatoryregimesasdevelopedcountries.

Overall, this analysis leads to two main conclusions.First, where WTO+ provisions are encountered inPTAs, involving any combination of developed ordeveloping countries, agreements have generallyserved to strengthen rules and commitment levelscompared with the WTO agreements. The fact thatthese are policy areas already covered by the WTOhas made it easier to give legal force to the relevantprovisions.Secondly,inspiteoftheapparentexplosionof new WTO-X issues covered by PTAs, the areasembodying legally enforceable and thereforesubstantive commitments in PTAs are relatively few,and are to be found predominantly in the fields ofinvestment, competition policy, intellectual propertyrights,andthemovementofcapital.

(b) PTAcommitmentsinselectedpolicyareas

(i) Services

Services obligations are usually included incomprehensive PTAs that cover not only trade ingoods, but also, for example, investment, intellectualproperty, e-commerce and competition. Out of 85notifications under Article V of the GATS,15 a littlemore than one-third of the agreements follow astructure that is close to that of the GATS, with asimilarsetofobligations(nationaltreatment,domesticregulation, etc.) that apply to the four modes ofsupply,16 and rely on a GATS-type “positive-listmodality” for the scheduling of liberalizationcommitments.17 A positive-list approach means thattheobligationsstipulatedintheagreementapplyonlyto those services sectors listed in WTO members'schedulesofcommitments (andsubject to limitationsinscribed), while a negative-list approach means thatobligations intheagreementapplyfullytoallsectors,subject only to explicitly listed reservations. In otherwords, inapositive listapproachonlywhat is listediscovered,whereasinanegativelistapproacheverythingiscoveredapartfromwhatislisted.

Almost half of the services PTAs notified follow adifferentstructure,whichisclosertotheapproachusedintheNorthAmericanFreeTradeAgreement(NAFTA)than to that of the GATS.18 Such agreements use anegative-list modality for the scheduling ofcommitments,andservicestradeiscoveredbydifferentsets of obligations. These include a chapter on cross-borderservicestradefocusingonmode1(cross-bordersupply), mode 2 (consumption abroad) and mode 4(movementofnaturalpersons),achapteroninvestmentcovering all sectors, including services, and separatechaptersontelecommunications,financialservicesandthetemporaryentryofbusinesspersons.19

FigureD.9: number of Wto+ and Wto-x provisions

Source:WTOSecretariat.

Num

ber o

f WTO

+ p

rovi

sion

s (a

vera

ge)

Developed Developed-Developing

Developing

15

10

5

0

Covered EnforceableN

umbe

r of W

TO-X

pro

visi

ons

(ave

rage

)

Developed Developed-Developing

Developing

12

10

8

6

4

2

0

WTO+ provisions WTO-X provisions

WOrld Trade repOrT 2011

134

Overtime,anumberofagreementshave innovated interms of their structure, combining elements of boththe original NAFTA and GATS-type models.20 Anumber of services PTAs, whether positive-list ornegative-list, also include some additional sector-specific provisions, contained in annexes to relevantchapters. Examples of these are recognition forprofessional services in various PTAs, provisionsspecifictoexpressdeliveryservicesinUSagreements,and maritime services in the agreement between theEUandtheCaribbeanForum(CARIFORUM).

Aside from innovations in architecture and market-openingmodalities,mostservicesPTAstendtoshareabroadcommonality,amongthemselvesandwiththeGATS,intermsofabasicsetofdisciplinesrelatingtotrade in services. These include national treatment(the principle of giving others the same treatment asone’s own nationals), market access, domesticregulation obligations, exceptions, definitions andscope.Intheareaof“rules”,forwhichnegotiationsareprovided for under the GATS, namely safeguards,subsidies andprocurement, PTAs have tendednot togo further. The same is true for most agreements inregardtodomesticregulationandtransparencyissues.Important exceptions exist here, however, as somecountries have gone beyond GATS provisions. TheseincludeanecessitytestondomesticregulationintheSwitzerland-JapanPTA,oradditionalservices-specificprovisionsontransparencyinUSagreements.21

How much more market access than under the GAts?

Inadditiontoarchitecturalandrules-relateddifferencesin the services provisions in PTAs, a key issue is theextent of market-opening commitments – that is, thelevel of access guaranteed for foreign services andservices suppliers (market access and nationaltreatmentobligations).Studieshavefoundthat,overall,services commitments in PTAs go beyond GATScommitments currently in force.22 Some studies alsoshow that PTA commitments go further than GATSoffers tabled so far in theDohaDevelopmentAgenda(DDA).23GATS+commitmentsinPTAstaketheformofbothnewbindingsorcommitments inservicessectorsuncommitted under the GATS and better bindings insectorsalreadycommittedundertheGATS.

Thevalueofservicescommitments inPTAs is largelybasedonthefactthattheyguaranteeaminimumleveloftreatment–oftenabetteronethanthatguaranteedundertheGATS.Thisisimportantformode3(foreigncommercialpresence),wherethesupplyinvolveslargeinvestments abroad, and for mode 1 (cross-bordersupply),wherethecurrentlackofrestrictionsinvarioussectorsmaynotlastastechnologicaladvancesleadtogreater trade, and competitive pressures, via thatmode.24 It isalso important formode4(movementofnaturalpersons),wheremeasuresaffectingtemporaryentrycanrapidlybereversed.

PTA commitments are not expected to lead to manyoccurrences of “real liberalization” – i.e. removal ofapplied restrictions. At the same time, although suchinformation is not readily discernible from PTAs,evidence suggests that some PTAs have, in certaininstances,directlyledtotheremovalofcertainappliedrestrictions, for example the phasing out of themonopolyintheinsurancesectorinCostaRicaandtheopeningoftheinsurancesectortoforeignbranchesinAustralia,theDominicanRepublicorChile.25

FigureD.1026highlightsdifferencesbetweenservicescommitmentsintheWTOandinPTAsbyfocusingontheproportionofservicessubsectorsthataresubjecttomarketaccess/nationaltreatmentcommitments.OnthebasisofdataforalargenumberofPTAs,thefigureshows that members involved in PTAs have, onaverage, undertaken commitments on a greaterproportion of services subsectors than they have intheGATS, or even than theyhave so far proposed intheir current GATS offers in the Doha DevelopmentAgenda(DDA).Thistrendisclearinbothmodes1and3,representingmorethan80percentofthevalueofworld trade in services. Levels of sectoral coverageachieved in PTAs are, on average, similar fordeveloping and developed countries included in thesample. The contrast with the GATS, however, isgreaterfordevelopingcountries,whosecommitmentstend to apply to a more limited set of servicessubsectorsatthemultilaterallevel.

Figure D.11 presents a more complete picture ofGATS+ commitments in PTAs by showing theproportion of subsectors where commitmentsundertaken by WTO members in PTAs go beyond

Figure D.10: sector coverage in PtAs in comparison with GAts commitments and DDA offers (Percentage)

Note:SeeAppendixTableD.3forthelistofPTAscovered.

Source: Updated from Roy et al. (2008) on the basis of anexpandeddataset.

Ave

rage

% o

f sub

sect

ors

com

mitt

ed

for m

embe

rs re

view

ed

Mode 1 Mode 3

100

80

60

40

90

70

50

30

20

10

0

GATS With GATS offer With PTA

II – tHe Wto AnD PReFeRentIAL tRADe AGReements

135

D. A

nA

tom

y o

F PR

eFe

Re

ntIA

L

tRA

De

AG

Re

em

en

ts

Figure D.11: Proportion of services subsectors subject to new or improved commitments in PtAs, compared to GAts (by member) (Percentage)

Note:GATSstandshereforGATScommitmentsandDDAoffers.Blue:subsectorscommittedunderGATS;red:subsectorscommittedunderGATSbutboundat abetter levelof treatmentunderPTAs;green: subsectorscommittedunderPTAs thatwereuncommittedunderGATS.Covers each member’s “best” PTA commitment across all the PTAs it is party to. Covers modes 1 and 3. See Box A.1. The legend of theacronymsforthemembersisprovidedinAppendixTableD.2.

Source:UpdatedfromRoyetal.(2007),onthebasisofexpandeddataset.

0 2010 30 40 50 60 70 80 90 100

Subsectors committed under GATS that are not further improved

Subsectors committed under GATS that are further improved in PTAs

Subsectors that are newlycommitted in PTAs

ARG

ATG

AUS

BHR

BLZ

BRA

BRB

BRN

CAN

CHE

CHL

CHN

COL

CRI

DMA

DOM

EC

GRD

GTM

GUY

HND

IDN

IND

ISL

JAM

JOR

JPN

KNA

KOR

LCA

LIE

MAR

MEX

MYS

NIC

NOR

NZL

OMN

PAK

PAN

PER

PHL

PRY

SGP

SLV

SUR

CHT

THA

TTO

URY

USA

VCT

VNM

WOrld Trade repOrT 2011

136

those inGATSschedulesofcommitmentsandoffers.This captures not only those instances where PTAsinclude new bindings in subsectors that wereuncommitted in theGATS,butalsobindingsatbetterlevelsofaccessinPTAsforthosesubsectorsalreadysubject to commitments under the GATS and DDAoffers.TheunderlyingPTAinformationrepresentsthePTA inwhich thememberconcernedhasundertakenthe highest level of binding – it is not an average ofbindingsinallPTAswithservicescommitments.Thesedata underscore the magnitude of GATS+commitments in PTAs, both among developing anddevelopedmembers.

The overall trend of significant GATS+ commitmentsobservedinmanyPTAsalsoembodieslargevariationsamong parties. Some exhibit spectacularimprovementsoverwhatiscommittedorofferedunderthe WTO, particularly in the case of a number ofdevelopingcountriesinLatinAmerica.Others,suchasASEAN countries (other than Singapore), showrelatively more limited GATS+ commitments in PTAs.Moreover,alargenumberofthosemembersthathavemade more significant GATS+ commitments havesubmitted relatively limited offers in the servicesnegotiationsintheDDA.

Thelevelofservicescommitmentsofindividualpartiesto PTAs also varies significantly among agreements.Singapore's services commitments, for example, varynotably in its agreements with the United States,Japan, and other ASEAN countries. Importantvariations can also be observed in the PTAcommitments of Australia, Chile and the Republic ofKorea.CommitmentsbytheUnitedStates,incontrast,do not vary significantly among PTAs, except for itsagreementwithJordan,whichwasbasedontheGATS(seeAppendixFigureD.1).

No simple or single reason explains why PTAcommitmentsaredifferentamong thePTAssignedbyvarious countries, or why PTA commitments aregenerally more far-reaching than those offered in theGATS. It has been argued that factors such asreciprocity (within services, but also among otherissues) as well as the respective economic size andimportanceofthepartiesinvolvedhaveplayedarole.27For example, the United States always obtains bettercommitmentsoverallonmodes1and3fromitstradingpartners than the commitments these countriesundertake in PTAs with other countries. In AppendixFigureD.1,thisisapparentinthePTAcommitmentsofChile,theRepublicofKorea,AustraliaandSingapore.

The type of liberalization modalities used in the PTA isalso a factor, as agreements using negative list28modalitieshave tended,onaverage, to result ingreatercommitmentsthanpositivelistones.Thismay,ofcourse,beduetothefactthatgovernmentswhicharereadytoassume more commitments are more comfortable withthenegativelistapproach.29Althoughnotinvestigatedin

the context of services PTAs, the nature of politicalregimes may also play a role in influencing levels ofGATS+ commitments that governments are ready toundertakeinapreferentialcontext.30

Figure D.12 shows GATS and PTA commitments bysectorformodes1and3.Overall,servicescommitmentsat the sectoral level in PTAs are more numerous thanthose inGATSsectors.Sectors thathaveprovedmoredifficult at the multilateral level (e.g. audiovisual,education)havealsoattractedlessGATS+commitmentsthan sectors such as telecommunications or financialservices. However, PTA commitments for the formerhavestillgonesignificantlybeyondGATScommitments.QualitativeanalysisofPTAcommitmentsinanumberofsectors also highlights this point.31 Nevertheless, themore sensitive sectors for larger trading partners havebeen subject to little or no improvement in PTAs(e.g. maritime transport for the United States oraudiovisualservicesfortheEuropeanUnion).

As for differences according to the level ofdevelopmentamongparties,theGATS+commitmentsof developed economies tend to be more limitedoverall in PTAs in view of the higher levels of GATScommitments in these countries. For developedcountries,GATS+commitments largely take the formofbetterlevelsofbindingsforsectorsalreadycoveredunder the GATS. The GATS+ commitments ofdeveloping countries are spread across all sectors,withparticularlysignificantadvancesinsuchareasasbusiness, environmental services, distribution,education and postal-courier services. Overall, PTAshavenarrowedthegapincommitmentlevelsbetweendevelopedanddevelopingcountries.

GATS+ commitments are more significant in cross-border supply (mode 1) and commercial presence(mode 3) than they are in respect of the temporarymovement of natural persons (mode 4). Mode 4commitments are essentially defined in a cross-sectoral manner in both the GATS and PTAs. PTAshave on the whole made notable improvements overtheGATS,althoughtoalesserextentinsuchimportantcategories of natural persons as “independentprofessionals”and“contractualservicesuppliers”.32

ThescaleofGATS+commitmentsvariessignificantlyfromonemembertoanother.AccordingtoStephensonandDelourme(2010),Australia,Canada,theEuropeanUnion and Japan have undertaken some significantGATS+commitments in some recentPTAs.33On theother hand, most United States PTAs on services,includingallthosenotifiedtotheWTOafter2003,donotgobeyondGATSonmode4.ThesameistrueforanumberofPTAcommitmentsbydevelopingcountries.However,thebroadersectoralcoverageofmostPTAsmeans that, at a minimum, GATS-type mode 4commitments are extended to many previouslyuncommittedsectors.34

II – tHe Wto AnD PReFeRentIAL tRADe AGReements

137

D. A

nA

tom

y o

F PR

eFe

Re

ntIA

L

tRA

De

AG

Re

em

en

ts

Bilateral investment treaties (BITs) also cover issuesrelevant tomode3.AlthoughthemajorityofBITsarelimited to post-establishment investor rights, somealso includecommitmentson investments in servicessectors with respect to the establishment phase.35ThisisparticularlythecasewithBITsconcludedbytheUnitedStates.

Finally,PTAsaresometimesGATS-minus, inthattheycontaincommitmentsthatprovideforlessthanwhatisbound under the GATS, either by excluding sectors(e.g. financial services in certain PTAs) or by listinglimitationsnotforeseeninGATScommitments.36

(ii) Investment

Thetradeand investment literature–see, forexample,Helpman (1984); Markusen (1984); Brainard (1993);Brainard (1997) and Markusen (1998) – allows us toinfer what provisions in trade agreements, and ininvestment chapters in particular, will be needed tofacilitateinternationalproductionnetworks.Akeyinsightof this literature is that what gives the multinationalenterprise itscompetitiveedge in internationalmarketsisitsfirm-specificassets–humancapital(managementor technical experts) and intellectual property, such aspatentsorblueprints.HenceprovisionsinPTAsthatgive

ample protection to these assets will encourage moreFDI flows and production sharing. Examples of suchprovisions are protection against expropriation or acommitment to compensate investors in the case ofexpropriation.

Allowingfreermovementofcorporatepersonnelwouldbe another critical ingredient in PTAs motivated byproductionsharing.Anotherprovisionthatmayimproveinvestor confidence is having the right to invoke thePTA'sdisputesettlementmechanism.Finally,reducingbarriers to investmentwill allowmoreenterprises theopportunity to establish a production facility in aforeignlocation.

What are investment provisions in PtAs commonly about?

SeveralstudieshaveanalysedinvestmentprovisionsinPTAs–see,forexample,Deeetal.(2006);Dee(2008);Houdeetal. (2007);Kotschwar (2009)andBergeretal.(2010).Forthepurposeofthisreport,theKotschwarstudywillbeused.Itisbasedonanexaminationoftheinvestment chapters or provisions in 52 PTAs. Thesample of PTAs includes 22 free trade agreementsamongcountriesoftheAmericas.Twoagreementsarefrom the 1980s, 13 from the 1990s, and 33 from

FigureD.12: GAts+ commitments in PtAs by sector, modes 1 and 3 (Percentage)

Note:GATSstandshereforGATScommitmentsandDDAoffers.Doneonthebasisofeachmember’s“best”PTAcommitmentacrossallthePTAsitispartyto.

Source:UpdatedfromRoyetal.(2007),onthebasisofexpandeddataset.

Members with commitments under GATS, without improvement in PTAs

Members improving upon GATS commitments in PTAs

Members committing for first time through PTAs

100

70

50

20

90

80

60

40

30

10

70

50

20

90

80

60

40

30

10

0

Tele

com

Tour

ism

Pos

tal-c

ourie

r

Pro

fess

iona

l

Insu

ranc

e

Mar

itim

e tr

ansp

ort

Env

ironm

enta

l

Hea

lth a

nd s

ocia

l

Dis

trib

utio

n

Edu

catio

n

Com

pute

r

Con

stru

ctio

n

Aud

iovi

sual

Ban

king

and

fina

ncia

l

Tele

com

Tour

ism

Pos

tal-c

ourie

r

Pro

fess

iona

l

Insu

ranc

e

Mar

itim

e tr

ansp

ort

Env

ironm

enta

l

Hea

lth a

nd s

ocia

l

Dis

trib

utio

n

Edu

catio

n

Com

pute

r

Con

stru

ctio

n

Aud

iovi

sual

Ban

king

and

fina

ncia

l

100

0

Mode 1 Mode 3

WOrld Trade repOrT 2011

138

2000 onwards. Seventeen agreements in the samplepaircountriesof theAmericaswithothersoutside theregion, including eight with Asian countries, six withcountries in the Middle East and three with Europeanpartners. Eight agreements are between Asiancountries, twoagreements amongEuropeancountriesor groups (European transition agreements), and oneeach involving Europe-Africa, Europe-Asia, Europe-Middle East and Africa-Africa. More than 30 specificfeatures of the investment chapters in theseagreementswereexaminedinKotschwar's2009study.

OnepotentialshortcomingoftheapproachtakenheretoexamineinvestmentprovisionsinPTAsisthattheseagreements are not the sole avenue for makinginternational commitments in investments. Over thepast20years,therehasbeenanexplosionofbilateralinvestment treaties (BITs). The United NationsConference on Trade and Development (UNCTAD)estimates that the total number of BITs increasedmorethansix-foldduringthe1990s,withtheirnumberrisingfrom385in1989tosome2,750bytheendof2009.37 One reason why investment and trade havebeen regulated by distinct treaties is becauseinvestmentandtradedisciplinesfocusedon“differentbut complementary objectives” (DiMascio andPauwelyn,2008).Tradeagreementsseekto increasetradingopportunitiesandinvestmentagreementsseektoprotectandpromoteforeigninvestment.

Even though PTAs increasingly include investmentrules, theirnumbersarestilldwarfedby theBITs.Forinstance, UNCTAD's BITs database reports that 82BITsweresignedin2009,whichexceedsthenumberof PTAs containing investment provisions notified tothe WTO that year.38 BITs have clearly been animportantvehicleforguaranteeinginvestorprotection(Adlung and Molinuevo, 2008). Baldwin (2010)considers the explosion of BITs in the 1990s as animportant means by which emerging markets wereable to attract offshored manufacturing jobs andfactories. Thus, it could be argued that BITs andinvestmentchapters inPTAsplay largelysimilar rolesinthespreadofinternationalproductionnetworks.

Kotschwar'sstudyidentifiesanumberofkeyelementsin the investment provisions of PTAs, includingcoverage, non-discrimination, standards of treatment,investor protection, temporary movement andnationalityofseniorpersonnel,anddisputesettlement.Eachoftheseisconsideredbrieflybelow.

Coverage

Thecoverageoftheinvestmentchapterdependsonhowinvestmentisdefinedandwhatdisciplinesarecontainedin the chapter. Investment may be defined in either abroad,asset-basedway(includingbothFDIandportfolioinvestment)ormorenarrowlyusinganenterprise-basedapproach(comprisingtheestablishmentoracquisitionofa business enterprise). Investment disciplines may be

dividedbetweentheinvestmentandserviceschaptersofanagreement.Asaconsequence, interactionsbetweenthemaremoreprevalent,andaregovernedeitherintheinvestmentortheserviceschapter(Houdeetal.,2007).Alternatively, investmentdisciplinesarecontainedintheinvestment chapter and there is limited interaction withtheserviceschapter.39

Principle of non-discrimination

A key mechanism for opening up investmentopportunitiesinaPTAistheapplicationoftheprincipleofnon-discriminationtoforeigninvestors.Theextentofopening depends upon how broadly investment isdefined in the agreement (i.e. the range of assets towhichnon-discriminationapplies),whethertheprincipleis applied to the entire lifetime of the investment (pre-andpost-establishment),andthenumberofreservations.There are two broad approaches for determiningreservations:thenegativelistandpositivelistapproach,asexplainedearlier.Ingeneral,anegativelistapproachislikelytoyieldgreaterinvestmentopportunities.

Standard of treatment

Beyondnon-discrimination,investmentprovisionsalsospecify other standards of treatment of foreigninvestors. These include such standards as fair andequitable treatment under international law, andfreedomintransferringpaymentsabroad.

Investor protection

Most investment chapters contain provisionsstipulating that investors are protected or will becompensated in the event that the host countrynationalizesorexpropriatesaninvestment.

Senior management and personnel

MostPTAsprovideforthetemporaryentryofmanagersand key personnel of a foreign investor. Someagreements allow hiring of top managerial personnelregardless of nationality, while other agreements holdthattheforeigninvestormaynotstipulatethenationalityofamajorityoftheboardofdirectors.

Dispute settlement

Whilemanyinvestmentchapters inPTAsnowcontainprovisionsondisputesettlement,disputesarehandledin a variety of ways. Some PTAs provide for thesettlement of disputes through coordination andnegotiation;otherscontainprovisiononlyforstate-to-state settlement of disputes. However, some PTAs,such as NAFTA, now allow investor-state disputesettlement. An investor that is a national of a PTAmembermaysubmittointernationalarbitrationaclaimthat a PTA member (state) has breached obligationsundertheinvestmentprovisionsofthePTA.

II – tHe Wto AnD PReFeRentIAL tRADe AGReements

139

D. A

nA

tom

y o

F PR

eFe

Re

ntIA

L

tRA

De

AG

Re

em

en

ts

Kotschwar'ssampleofPTAsisusedtoprovideamoredetailedanalysisof thoseelementsof theagreementsthatmightbeseenasessentialforproductionnetworks.FigureD.13showsthatalargeproportionofthesampleofthePTAs(between60and70percent)haveadopteda negative list approach to investment commitments.MFN and national treatment have also been widelyguaranteedtoforeigninvestorswhowishtoestablishapresence, or acquire or resell holdings. Investorprotectionguaranteesarewrittenintomostagreements,andprivateinvestorsarefrequentlygrantedtherighttodisputesettlement.Ingeneral,theinvestmentprovisionsin these PTAs appear to be rather open, although noattemptwasmade in theKotschwarstudy to testhowmuch these provisions actually affected FDI flows.Some econometric evidence is available, however,showing that FDI flows respond to provisions in theinvestment chapters of PTAs. See Dee et al. (2006),Dee(2008)andBergeretal.(2010).

Patterns over time

TheagreementsinKotschwar'ssamplespanfromtheearly 1980s to around 2009. Using the total numberofprovisionsintheinvestmentchapterasanindicatorof investment openness, later agreements appear tobe more open than earlier ones (see Figure D.14).40This trend is the same even if a narrower set ofprovisionsintheinvestmentchapterareused,suchasonlythoselimitedtoMFNandnationaltreatment.

Are there families of investment provisions?

KotschwarfindsthatPTAsaregroupedroughlyaroundtwo hubs: a NAFTA-type hub, which includesagreements among countries in the Americas andincreasingly in the Asia-Pacific region, and theEuropean-stylehub.ShecharacterizesallthePTAsin

FigureD.14: total number of provisions in investment chapter over time

Source:CalculatedfromKotschwar(2009).

1982

Tota

l num

ber o

f pro

visi

ons

1987 1993 1998 2004 2009

18

14

10

4

16

12

8

6

2

0

FigureD.13: Proportion of PtAs with selected provisions in investment chapter (Percentage)

Source:CalculatedfromKotschwar(2009).

Negative listapproach

Establishment Acquisition Post-establishment

MFN and national treatment

Resale Investor protection

Investor accessto disputesettlementmechanism

80

60

40

20

0

WOrld Trade repOrT 2011

140

the sample involving the three NAFTA members(Canada, Mexico and the United States) with theirrespectivepartnersintheAmericasas“encompassing”,since they apply the four modalities that determineinvestment conditions: establishment, acquisition,post-establishment operations and resale. They alsocover such disciplines as MFN treatment, nationaltreatment, anddispute settlement.Eightyper centormore also cover transparency, protection againstdenialofbenefitsandrestrictionoftransfers,minimumlimitations on the nationality of management and theboardof directors, noperformance requirements andguaranteesagainstexpropriation.

The United States leads the way in designingparticularly comprehensive PTAs. In Asia, Kotschwarfinds that Singapore and Australia’s agreements aremorecomprehensive,butotheragreementshavescantcoverage. In interregional agreements, she finds thatthe coverage is somewhat lower due to the limitedcoverageofdisciplinesintheEU-MexicoandEU-Chileagreements,aswellas in theChile-ChinaFreeTradeAgreement (FTA), the P-4 Agreement (Australia,BruneiDarussalam,ChileandSingapore),andtheUS-JordanFTA.

Kotschwarobservesthattheagreementssignedamongdeveloped economies tend to go beyond provisions atthe multilateral level. This is most obvious where theyinclude separate investment chapters that go beyondservices,coverallinvestmentphases,employanegativelist approach, and have little or no limitations on thenationality of board members and management. Ageographic divide exists with respect to limitations onperformance requirements. United States agreements(except for US-Israel) restrict performancerequirements. Singapore agreements (except for US-SingaporeandJapan-Singapore)donot.

A similar division is seen in terms of transparencyrequirements.AgreementsintheAmericastendtoaddprior comment and publication obligations to theGATS, and establish national enquiry points. Asianagreements, by and large, do not. Australianagreements (with the United States and withSingapore) incorporateGATS-styledenialofbenefits.Amongagreements that includeAsianmembers,onlya handful adopt tougher-than-GATS treatment. All ofthesearewithcountriesintheAmericas(Chile-Korea,Mexico-Japan, US-Korea and US-Singapore).Agreements with Australia or Israel do not containinvestor-state dispute settlement mechanisms exceptfortheSingapore-Australiaagreement–allSingaporeagreementsincorporatethiselement.

Asforagreementsbetweendevelopedanddevelopingcountries,thoseintheAmericasallcontainaseparateinvestment chapter or incorporate a BIT. EUagreements with developing countries generally donot. PTAs among developing countries varyconsiderably in content and approach. Agreements

signed by Chile and Mexico with other developingcountries look much more like the agreementsinvolving developed countries than those signedamong other developing countries, such asMERCOSUR. These latter agreements tend to openmarketsmoregradually.

(iii) Technical barriers to trade

In a world where tariff barriers have progressivelyfallen,non-tariffbarriers to tradehaveacquiredmoresignificance. As noted above, many PTAs includenorms on technical barriers to trade (TBT) and agrowingnumberincludeTBTprovisions.

Data reported here on TBT provisions in PTAs aretakenfromastudybyPiermartiniandBudetta(2009)of 70 PTAs that differ in terms of geographicalcharacteristics,levelofdevelopmentandtheextentofintra-regional trade. Fifty-eight of the 70 PTAssurveyedcontainedTBTprovisions.Thestudyemploysa template that maps TBT provisions in terms of theintegration approach chosen for standards, technicalregulations and conformity assessment procedures(i.e. harmonization or mutual recognition),improvements in transparency, institutions ormechanisms to administer the agreement and solvedisputes, and the possibility of cooperation amongregionalpartnersonstandards-related issuesbeyondtrade objectives and technical assistance. Since thisdatabase primarily41 relies on the legal texts of theagreements, it does not allow an assessment of theactualextentofimplementationoftheprovisions.

What are tBt provisions in PtAs commonly about?

The most common provisions in PTAs (occurring inover 50 per cent of the 58 PTAs included in thePiermartini and Budetta study that contain TBTprovisions) are mutual recognition of conformityassessment, harmonization of technical regulations,transparencyprovisions, andprovisions that establishinstitutionalmachinerysuchasacommittee,abodyora network for standard-related matters (seeFigure D.15). Harmonized standards, harmonizedconformity assessment procedures and disputesettlementprovisionswerefoundinmorethan40percentoftheagreementscontainedinthesampleof58PTAs. Provisions dealing with the mutual recognitionof regulations and standards, common policies,technical assistance and metrology occurred in lessthan30to40percentoftheagreements.

Mutual recognition means that countries agree torecognize each other's regulations, standards orconformity assessmentproceduresasequivalent, thusfacilitating the unimpeded flow of goods into partnermarkets. Like mutual recognition, harmonization ofregulationsandstandardsisasteptowardsmoreopentrade. Both mutual recognition and harmonization

II – tHe Wto AnD PReFeRentIAL tRADe AGReements

141

D. A

nA

tom

y o

F PR

eFe

Re

ntIA

L

tRA

De

AG

Re

em

en

ts

promote transparency and trade opening by reducingthecoststoexportersofmonitoringdestinationcountrypolicy changes. These arrangements also provideexporters with easier access to information about thepreferencesofconsumersinpartnercountries.42

The advantage of harmonization relative to mutualrecognition in termsof itseffectsontrade is thatwithharmonizationproductsproducedindifferentcountriesare more similar (more homogeneous) and thereforebetter substitutes from the point of view of producersand consumers. This, in turn, may facilitate trade byimproving consumer confidence about the quality ofimported goods. In enhancing compatibility betweenimported and domestically produced goods,harmonizationmakes iteasier forconsumers tomatchproducts.Itisalsolikelytoincreasecompetition,reduceprices and increase trade. However, harmonizationinvolves more arduous negotiations and carries higherregulatorycoststhanmutualrecognition.

Finally, strengthening cooperation on the institutionalset-up for the standards regime is a step towardsfurther trade opening because it is likely to promotetheeffective implementationofmeasures. Ingeneral,the gap between law and practice will depend oninstitutionsandadministrativeprocedures.

Who integrates tBt provisions the most?

Agreementssignedbetweencountriessimilarintermsof levels of development, technology, environmentalrequirementsandpreferencesare likely tobedeeperin termsofTBT integrationthanthosebetweenmoredissimilarcountries.Thisisbecausecountriesthatare

alike tend to share similar policy objectives andtherefore similar types of standards. In addition,countries at a higher level of development are morelikely to trust one another's conformity assessmentsand standards than countries at a lower level ofdevelopment.

In order to understand the overall level of TBTintegration, PTAs have been ranked on the basis ofprovisions that go beyond WTO commitments(i.e.WTO+integration).FigureD.16showstheaverage

FigureD.15: Percentage of PtAs by tBt provision

Note:Percentagesarerelativetothe58PTAsinthesamplecontainingTBTprovisions.MRdenotesmutualrecognitionandHarm.meansharmonization.

Source:Authors’calculationsonPiermartiniandBudetta(2009)database.

MR

sta

ndar

ds

MR

tech

nica

lre

gula

tions

MR

con

form

ityas

sess

men

t

Har

m. s

tand

ards

Har

m. t

echn

ical

regu

latio

ns

Har

m. c

onfo

rmity

asse

ssm

ent

Tran

spar

ency

Adm

inis

trat

ive

bodi

es

Dis

pute

set

tlem

ent

mec

hani

sms

Com

mon

pol

icy

Tech

nica

l ass

ista

nce

Met

rolo

gy

80

50

30

70

40

20

10

0

FigureD.16: Average degree of tBt integration by level of development

Note:The“North”consistsoftheEU,EFTAcountries,Australia,New Zealand, the United States, Canada and Japan.AgreementswithnoTBTprovisionsareincluded.

Source:Authors’calculationsbasedonPiermartiniandBudetta(2009)database.

16

12

8

14

10

6

4

2

0South-South

Num

ber o

f WTO

+ T

BT

prov

isio

ns (a

vera

ge)

North-North North-South

WOrld Trade repOrT 2011

142

levelofWTO+integrationachievedbyPTAsclassifiedaccordingtothelevelofdevelopmentandsimilarityoftheirmembercountries.InlinewiththepredictionthatadeeperlevelofintegrationislikelytobeachievedinPTAs among countries with a similar level ofdevelopment and higher incomes, agreementsbetween developed countries (the North) display thehighest degree of TBT integration on average. PTAsbetweendevelopingcountries(theSouth)scoremorehighly than agreements between a developed and adeveloping country, confirming the proposition thatintegrationismorelikelyamongsimilarcountries.

Are there families of PtAs in the context of tBt integration?

TableD.3showspatternsofTBTintegrationbyregion.The most common provisions (defined as those thatoccurredinover60percentofthecases)areshadedin green, the least common (those occurring in lessthan40percentofcases)areshadedinblue,andtherest(occurringbetween40and60percentofcases)are shaded in red. While mutual recognition ofconformity assessment is common across the board,significant differences are discernible in relation toothermeasuresadoptedinPTAs.

AmajordifferenceexistsbetweenEU-typeandNorthAmerican-type agreements in terms of the choicebetween harmonization and mutual recognition as avehicle for TBT integration. PTAs involving the EUtypically prefer harmonization, while North Americanagreements tend to prefer mutual recognition. Inaddition, TBT provisions in PTAs in North America,EastAsiaandSouth-CentralAmericamainlyfocusonintroducingtransparencyrequirementsanddevelopinginstitutionalbodies,whileEUandAfricanagreementsbarelyconsidertheseissues.

PTAs that harmonize standards are likely to featurehub-and-spoke characteristics, with a larger partnerrepresenting the hub to whose standards the spokeswill conform. This tendency can result in standardsbecoming a barrier to trade and integration amongmajorregionalgroupings.43

(iv) Competition policy

Thepresenceofmonopolies, cartelsandother formsofprivateanti-competitivepracticescan frustrate thebenefits of trade, investment and services reform.These market features prevent multinationalenterprises from taking full advantage of differencesin costs among countries through fragmentingproduction. The adoption of competition policy is inmany ways a natural complement to the reduction oftrade, investment and services barriers. While thelatter reduce or eliminate policy-created distortions,competition policy dilutes or prevents the abuse ofmarket power. As noted by many commentators, thestillborn 1948 Havana Charter of the InternationalTrade Organization included provisions on restrictivebusiness practices, testifying to the recognition bynegotiators of the link between trade opening andcompetitionlaw.

Thefollowinganalysisofcompetitionrules inPTAs isbasedonrecentresearchbySilva(2004);Brusiketal.(2005); Anderson and Evenett (2006); Solano andSennekamp (2006); Teh (2009) and Dawar andHolmes (2010). Many studies of competition rules inPTAs have focused only on the competition policychapters of agreements. However, as Anderson andEvenett (2006)haveemphasized,competition-relatedprovisionsalsoappearinotherprovisions.Intheirview,thesesector-specificcompetitionprovisionsmayhavestrongerpro-competitiveeffectsthanthecompetition

TableD.3: Patterns of tBt integration across regions (percentage of PtAs by provision and region)

Provisions eunorth

Americaeast Asia

south Central America

Africa

MRstandards 13 7 8 6 0

MRtechnicalregulations 13 40 31 41 0

MRconformityassessment 67 73 69 76 70

Harm.standards 80 20 31 47 60

Harm.technicalregulations 73 27 54 59 50

Harm.conformityassessment 80 20 31 47 60

Transparencyrequirements 20 67 62 65 20

Administrativebody 20 67 62 76 40

Disputesettlementbody 20 33 46 47 20

Commonpolicy 7 0 15 6 20

Technicalassistance 40 40 23 65 40

Metrology 47 13 8 47 60

Note:MRreferstomutualrecognitionandHarm.toharmonization.

Source:CalculationsonPiermartiniandBudetta(2009)database.

II – tHe Wto AnD PReFeRentIAL tRADe AGReements

143

D. A

nA

tom

y o

F PR

eFe

Re

ntIA

L

tRA

De

AG

Re

em

en

ts

policy chapter itself, assuming that the tradeagreement even has one. The authors also drawattentiontowhattheyrefertoas“horizontalprinciples”relating to thenon-discrimination,procedural fairnessandtransparencyprovisionsintheagreements.

Transparency requires the publication of lawspromoting fair competition and addressing anti-competitive practices. Procedural fairness requiresthat administrative proceedings are consistent,impartial and reasonable and that it is possible torevieworappealanydecisionstakeninadministrativeproceedings.AndersonandEvenett(2006)arguethatthese horizontal principles have a bearing oncompetitionlawandpolicy.

Confirming the hypothesis of Anderson and Evenett,the study by Teh (2009) documents how a largenumberofPTAsincludecompetitiondisciplinesinthechapters on investment, services (intelecommunications, maritime transport and financialservices), government procurement and intellectualproperty.Basedonhissampleof74PTAs,FigureD.17shows the proportion of PTAs which containcompetition-relatedelements in theotherchaptersoftheagreements.MorethanaquarterofthePTAs,forexample, have provisions that guard against majortelecommunications suppliers engaging in anti-competitive practices. About one-fifth of the PTAshave an intellectual property (IP) chapter preventingabuse or anti-competitive behaviour by IP rightsholders.

As has been argued in this report, infrastructuralservices, investments, and intellectual propertyprotectionare likely tobecentral ingredientsofwell-functioningproductionnetworkingarrangements.Theapplication of competition rules in these areascomplements the reduction of trade and otherregulatorybarriers.