CW African cement markets

19

Cement and Clinker Price Markers: Med Basin, Persian Gulf-Arabian Sea and East Africa African cement markets overview Webinar presentation CW Group LLC | T: +1-702-866-9474 | F: +1-928-832-4762 | Connecticut, USA March 18, 2021

Transcript of CW African cement markets

Cement and Clinker Price

Markers: Med Basin, Persian

Gulf-Arabian Sea and East

Africa

African cement markets

overview

Webinar presentation

CW Group LLC | T: +1-702-866-9474 | F: +1-928-832-4762 | Connecticut, USA

March 18, 2021

Presenters

2

Juliana VieiraBusiness Analyst

M:+351 918 285 753

▪ Lead analyst on CW’s Trade Prices Report (GCTRP).

Responsible for the qualitative and quantitative analysis for CW

Research's price and volume assessments in the building

material and heavy industrial sectors. 5+ years of experience in

cement sector

▪ Degree in International Business from ESPM, Rio de Janeiro,

Brazil

Wanderson

TeixeiraJunior Business Analyst

M:+351 930 636 142

▪ Executes quantitative analysis for CW Research's price and

volume assessments in the building material and heavy industrial

sectors. Experience of more than two years in the construction

industry

▪ Degree in International Relations from La Salle, Rio de Janeiro,

Brazil

Agenda

▪ Introduction to CW Group

▪ African cement markets highlights

− Macro-economic analysis

− Regional construction market overview

− Cement market overview

− Capacity drivers and prospects

− Trade and pricing dynamics

− On-going impact of Covid-19

3

4

About the CW Group

CEMENT, BUILDING

MATERIALS &

CONSTRUCTION

STEEL, METALS &

MINING

CHEMICALS DRY BULK CARGO,

PORTS AND

INFRASTRUCTURE

POWER, ENERGY

AND SOLID FUELS

Seasoned expertsBusiness &

technicalNetwork & access Proprietary data

STRATEGY AND M&A

ADVISORYBUSINESS DECISION

SUPPORTMEDIA & MEETINGS

Strategic advisory

Management consulting

M&A advice

Transaction support

Due diligence

Syndicated market /

industry study reports

Reference forecasts

Data and chart-books

Commodity price

assessments

Market reporting services

Newsletters

Online data access

Publications

Meetings

Advisory Research Media

Client Confidential Information

5

African cement market highlights

What does it include

6

▪ A comprehensive review of the dynamic cement market, covering cement volume trends in detail, analyzing trade flows, historical cement demand and production, the competitive landscape as well as demand drivers, including macro economic and construction sector dynamics, for the country

▪ Scope of the report:

– Executive summary

– Country assessments: population, GDP, GDP per capita, FDI

– Construction sector overview and projects outlook

– Cement sector: sector overview, numerical perspective on cement, import and exports, incumbent operations and new capacity

– Cement prices (ex-works, retail and imports)

– Competitive dynamics

– 5 year historical and outlook

– Company profiles

For more details visit:

https://www.cwgrp.com/bmweek-reports/product/303-algeria-cement-market-forecast-report-2020-edition

https://www.cwgrp.com/research/research-products/product/93-ethiopia-cement-market-report-and-forecast

https://www.cwgrp.com/coalweek-reports/product/314-democratic-republic-of-congo-drc-cement-market-forecast-report-2021-edition

https://www.cwgrp.com/cemweek-reports/product/304-kenya-cement-market-forecast-report-2020-edition

https://www.cwgrp.com/cemweek-reports/product/305-tanzania-cement-market-forecast-report-2020-edition

https://www.cwgrp.com/research/research-products/product/68-uganda-cement-market-and-forecast-report

Source: CW Research

Client Confidential Information

7

Macro-economic analysis

The IMF projects a strong rebound in economic growth for the select

group of countries with the singular exception of Ethiopia

GDP 2021E (current prices, USD bn)

Algeria (USD 155 bn)

Algeria’s economy, is highly

dependent on hydrocarbons

GDP is expected to have a growth

at a CAGR of 3 percent from 21E-

26F

Ethiopia (USD 92 bn)

Ethiopia’s GDP is expected to

increase at a CAGR of 8 percent

from 21E-26F

The government aims to make the

country a lower-middle-income by

2025

Kenya (USD 106 bn)

Kenya has been placed as one of

the fastest growing economies in

Sub-Saharan Africa, with an

estimated economic growth of 6

percent in 2020

Uganda (USD 41 bn)

Uganda’s economy is highly

dependent on the service and

agriculture sectors

Tanzania (USD 68 bn)

Tanzania’s GDP growth is dependent on reforms

to improve busines environment but also on the

post-pandemic economic recovery

DRC (USD 50 bn)

DRC economy is heavily dependent on

the industrial sector

The 2019-23 Strategic Development

Plan aims to improve the economy

Source: IMF, CW Research

Tanzania and Uganda were the only ones to see an yearly increase in

foreign direct investment in 2019

Source: CW Research

FDI Inflow (USD bn)

▪ Ethiopia and DRC remain one of the largest FDI recipients

▪ However, Ethiopia witnessed the biggest decline in FDI inflows in 2019 amongst the select markets

▪ The average FDI inflows to the countries was USD 1.5 billion in 2019

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

2015 2017 2019

Algeria DRC Ethiopia Kenya Tanzania Uganda

Mega-infrastructure investment is expected to boost cement demand

in the region over the forecast period

10

Algeria DRC Ethiopia

Total

Source: CW Research

Note: Only selected projects

▪ Highway of the Haust-

Plateaux

▪ Tafoulk

▪ Sonatrach

▪ BirSeba Phase II & Mouiat

Outlad Messaoud Field

Development

▪ Inga III Hydropower Project

▪ “Kitoko Smart City” Project

Phase I

▪ Kinshasa Solar City

▪ Busanga Hydropower Damn

Project

▪ Lapsset Project

▪ Bishoftu Airport

▪ Grand Ethiopian

Renaissance Dam US

▪ Addis Ababa-Djibouti

Railway Modernization

Project

USD 45.7 bnUSD 20.6 bnUSD 14.7 bn

11

Kenya Tanzania Uganda

Source: CW Research

Note: Only selected projects

Total USD 14.7 bnUSD 51.5 bnUSD 41.0 bn

▪ Uganda Standard Gauge

Railway

▪ KLA Bus Rapid Transit

▪ Kabaale International Airport

▪ Katosi Water Treatment

Plant Project

▪ Kampala Flyover

Construction and Road

Upgrading Project

▪ Likong’o-Mchinga LNG

▪ Standard Gauge Railway

Phases I & II

▪ Tanzania & Uganda pipeline

project

▪ Julius Nyerere Hydropower

Project

▪ Konza Technology City

▪ The LAPSSET Corridor

Program

▪ Lamu Port Project

▪ Nairobi Mombasa Highway

Expansion Project

▪ Standard Gauge Railway

Phase II

The USD 30 bn Likong’o-Mchinga LNG plant in Tanzania is the

single largest investment for the countries in discussion

Client Confidential Information

12

Select African cement markets

Cement manufacturers are expanding production capacity in order to

meet demand led by mega-infrastructure projects

13

Capacity additions (mn tons)

0.0 1.0 2.0 3.0 4.0 5.0 6.0

Tanzania

Algeria

DRC

Kenya

Uganda

Ethiopia

2021E-2026F

▪ Abay Industrial Development Share Company is

expected to commission in 2021E an integrated plant

▪ Uganda’s cement market to witness capacity addition

and upgrade until 2026F

▪ Kenya cement capacity is expected to witness additions

from National Cement and Mombasa Cement and a

new player, Nairobi Business Ventures

▪ DRC cement capacity is estimated to see the entrance

of not only several new players as the reopening of the

former CINAT

▪ Algeria is expected to commission a new cement plant

by 2022F

▪ Two new cement manufacturers are set to enter

Tanzania’s cement market by 2026F

Source: CW Research

0.0 5.0 10.0 15.0 20.0 25.0 30.0

Algeria

Ethiopia

Tanzania

Kenya

Uganda

DRC

2016 2018 2020 2021E

Most countries are expected to see an increase in utilization rates as

manufacturers ramp up production

14

Cement production 2016-2021E (mn tons)

▪ From 2016-2021E, Algeria and Kenya are the only markets expected to see a decline in cement production

▪ For the next five years, Kenya is expected to have the smallest growth in production while Uganda is set to see the

highest growth

59%

50%

53%

70%

51%

44%

Utilization rates

16-21E (avg):

Source: CW Research

15

Despite the economic impact of the pandemic, cement demand

remains robust due to sustained government investment

Source: CW Research

Cement demand outlook: 5 year growth (% CAGR)

0% - 3%

+12 %

Legend:

3% - 6%

Algeria’s sustained public spending in

infrastructure is expected to drive

cement demand, to increase at a

CAGR of 2%

Increasing cement demand in the

DRC is expected to be catered by

additional capacities as manufacturers

are unable to supply demand

Mega infrastructure projects estimated

to boost cement demand in Ethiopia

Uganda’s additional capacity

expected to spur housing and

real estate development within

the region

Kenya cement demand expected

to be catered by the additional

capacities coming online,

increase in exports

Tanzania cement market growth

upon mega infrastructures

investments in the country

16

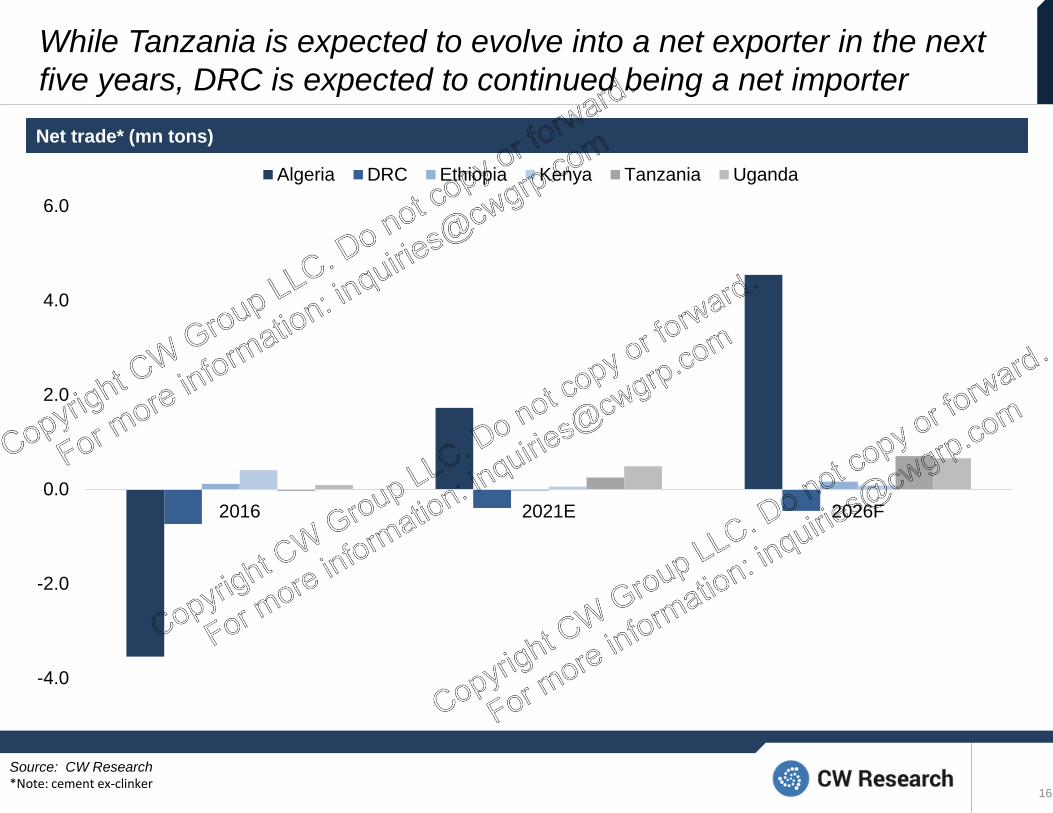

While Tanzania is expected to evolve into a net exporter in the next

five years, DRC is expected to continued being a net importer

Source: CW Research*Note: cement ex-clinker

Net trade* (mn tons)

-4.0

-2.0

0.0

2.0

4.0

6.0

2016 2021E 2026F

Algeria DRC Ethiopia Kenya Tanzania Uganda

$0

$60

$120

$180

Algeria Ethiopia Tanzania Kenya DRC Uganda

2016 2018 2020 2021E

Ex-works prices to see a wide variation in the region with Algeria

having the lowest while Uganda has the highest prices

17

Cement prices (USD/ ton)Cement ex-works prices (USD/ ton)

-6%

-2% -1%

0% 1%

-3%

Source: CW Research

CAGR 16-21E

Closing remarks

▪ Infrastructure investments are expected to boost the

construction sector across regional markets in Africa,

therefore increasing cement demand in the next five

years

▪ All of the markets are expected to have additional

capacities coming online in the next five years, with

Algeria and Tanzania witnessing the biggest additions

▪ In the next five years, demand is expected to see a rise

in all six countries, with DRC seeing the biggest increase

▪ Ex-works prices are expected to witness a slight decline

from 2016-2021E, with the exception of the DRC

18Source: CW Research

About CW ResearchCW Research is a leader in syndicated and data-driven market research solutions. The company offers independent

perspectives on multiple industrial market segments(e.g., cement, metals & minerals, and specialty chemicals) and

deep functional expertise in market intelligence, sourcing intelligence, commodity pricing intelligence.

CW Research also provides custom industry and competitive research programs for operating companies, financial

analysts, consultants, governments, suppliers and many others as well as tailored studies together with CW Advisory.

For more information: research.cwgrp.com.

Contacts

CW Group LLCPO Box 5263, Greenwich,

CT 06831 USA

T: +1-702-866-9474

F: +1-928-832-4762

www.cwgrp.com

Juliana Vieira

Business Analyst

Wanderson Teixeira

Junior Business Analyst

Liviu Dinu

Market Services &

Marketing Consultant