“Current and Pending Management Implications of Current Market Conditions on Private and...

31

MANAGEMENT IMPLICATIONS OF CURRENT AND FORECASTED MARKET CONDITIONS

-

Upload

forest-landowners-association -

Category

Environment

-

view

458 -

download

2

Transcript of “Current and Pending Management Implications of Current Market Conditions on Private and...

MANAGEMENT IMPLICATIONS OF

CURRENT AND FORECASTED

MARKET CONDITIONS

CURRENT

LOCATIONS

AND

SERVICE AREA

United States

HQ in Albany, GA

19 offices in 12 states

137 employees

South America

HQ in MVD, UY

Operations in 2 countries

Incorporated in 5 countries

45 employees

F&W SERVICES

Forest management

Forestland accounting

Forestland inventory

Forestland acquisition support, Financial analysis, Resource studies

Forestland database development / management, Mapping, Harvest scheduling

Real estate sales

Fiber supply logistics

Forest certification program development, management and support, Audits, Pre-audits

Environmental assessments, Wetland delineation, and Land-use permitting

WHAT WE WILL TALK ABOUT

Background

Déjà vu (all over again)

What does this mean for a landowner/forester?

PLANTING ACRES AND POTENTIAL IMPACTS

Harper, R. A., Hernandez, G., Arseneault, J., Bryntesen, M., Enebak, S., & Overton, R. P. (2013). Forest

Nursery Seedling Production in the United States - Fiscal Year 2012. Tree Planters' Notes, 56(2),

72-77.

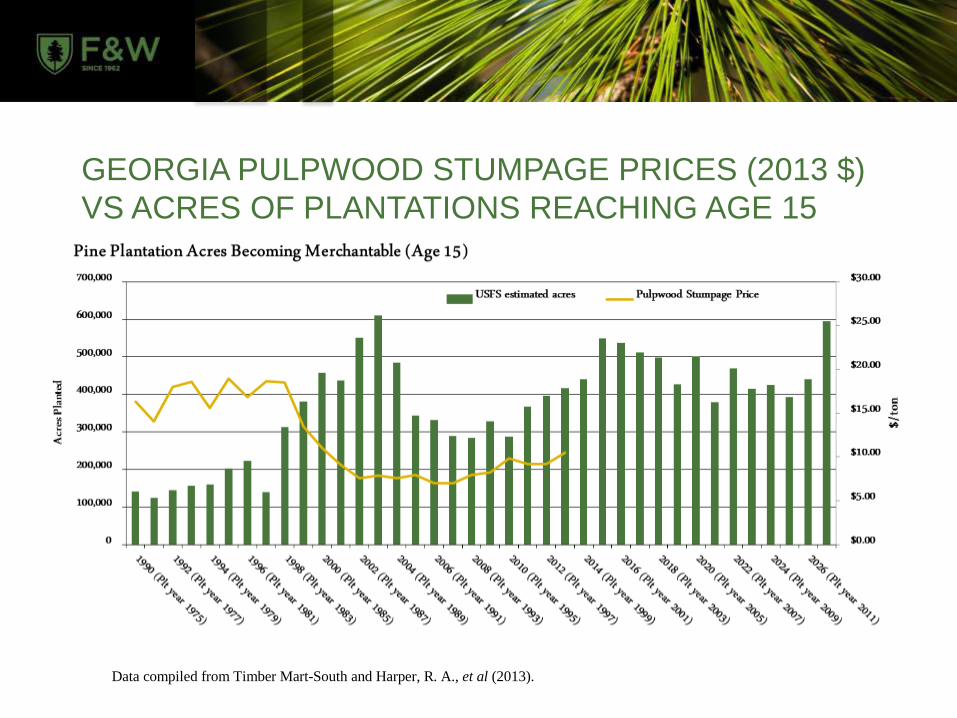

GEORGIA PULPWOOD STUMPAGE PRICES (2013 $)

VS ACRES OF PLANTATIONS REACHING AGE 15

Data compiled from Timber Mart-South and Harper, R. A., et al (2013).

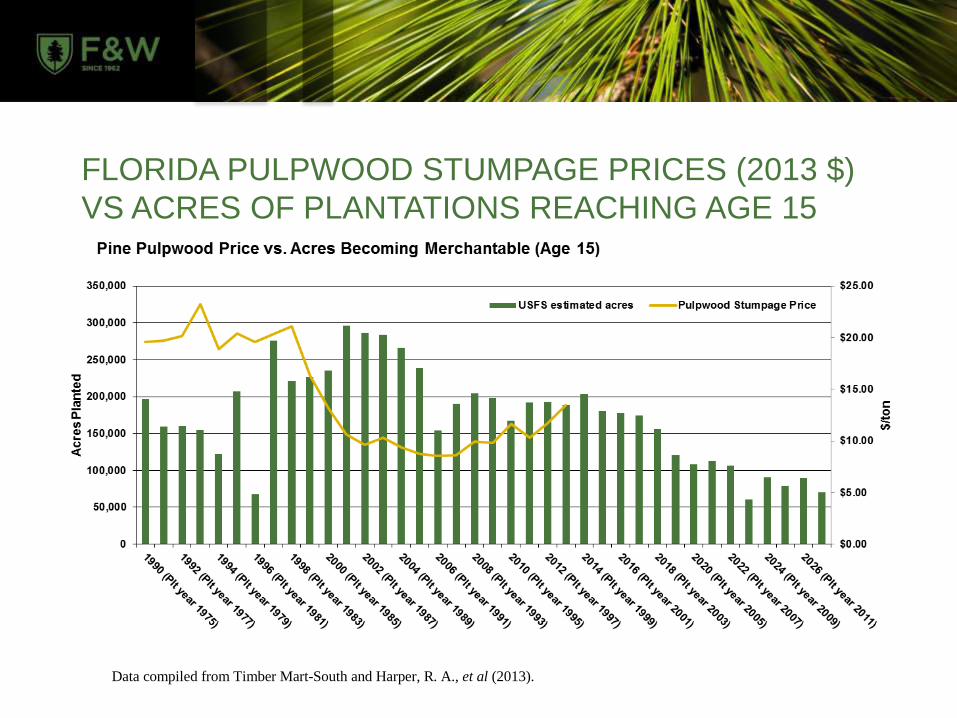

FLORIDA PULPWOOD STUMPAGE PRICES (2013 $)

VS ACRES OF PLANTATIONS REACHING AGE 15

Data compiled from Timber Mart-South and Harper, R. A., et al (2013).

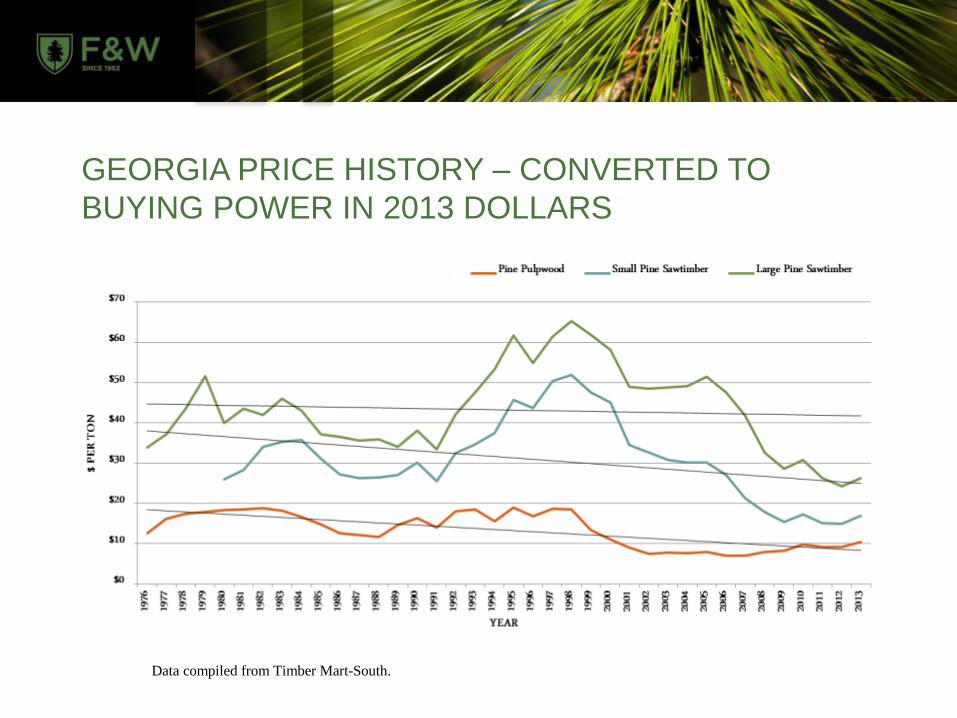

GEORGIA PRICE HISTORY – CONVERTED TO

BUYING POWER IN 2013 DOLLARS

Data compiled from Timber Mart-South.

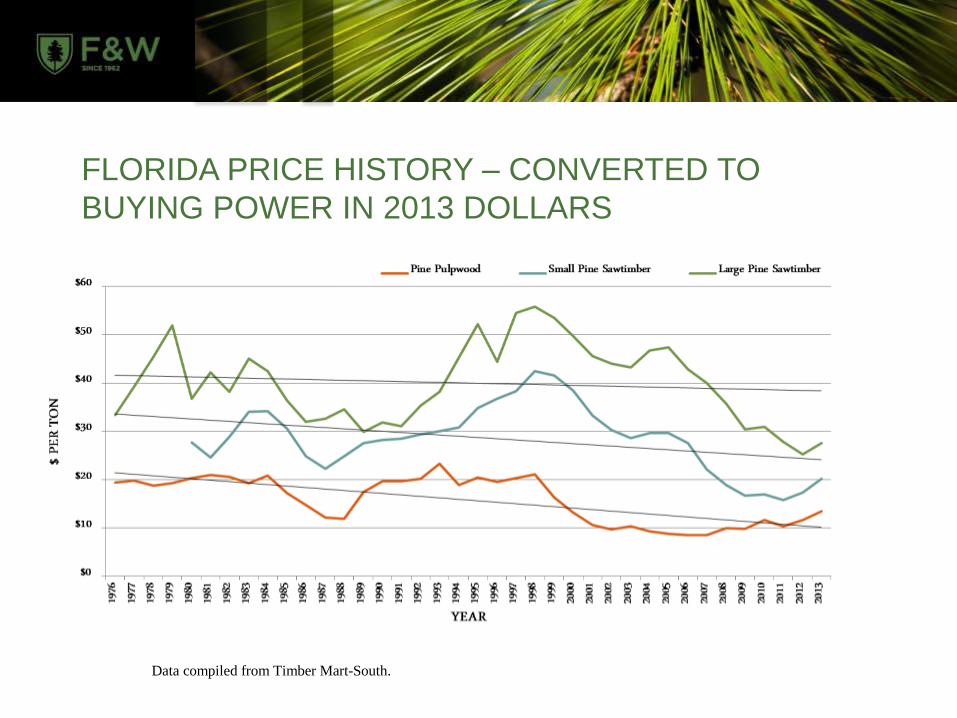

FLORIDA PRICE HISTORY – CONVERTED TO

BUYING POWER IN 2013 DOLLARS

Data compiled from Timber Mart-South.

NEW DEMAND - FLORIDA AND GEORGIA MILL

ANNOUNCEMENTS & NEW OPENINGS

Klausner Lumber – Suwannee Co., FL – 350mmbf

capacity – due to open 4th Quarter 2014

Interfor, a Canadian company, has purchased

sawmills in Eatonton, Perry, Preston, Swainsboro, and

Thomaston, Georgia

New pellet mills have been announced by Enova in

Wilkinson and Warren Counties

Pellet mill announced at former LP OSB site in Athens

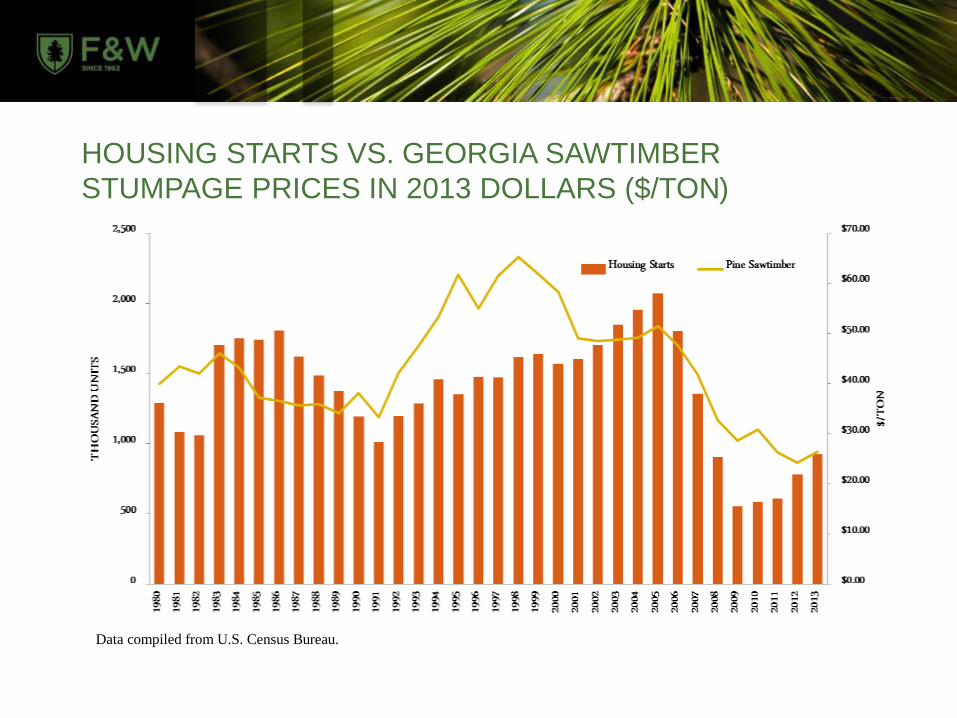

HOUSING STARTS VS. GEORGIA SAWTIMBER

STUMPAGE PRICES IN 2013 DOLLARS ($/TON)

Data compiled from U.S. Census Bureau.

HOUSING STARTS VS. FLORIDA SAWTIMBER STUMPAGE

PRICES IN 2013 DOLLARS ($/TON)

Data compiled from U.S. Census Bureau.

SOUTHERN LUMBER PRODUCTION IN THE SOUTH

Barynin, P., & Abeysekera, C. (2013, December). RISI North American 15-Year Timber Forecast.

SOFTWOOD DEMAND IN THE SOUTH

Barynin, P., & Abeysekera, C. (2013, December). RISI North American 15-Year Timber Forecast.

FOREIGN COMPETITION?

IT COMES AND GOES…

SAO PAULO, Aug 12, 2014 17:13:00 (RISI) - The Brazilian

pulp and paper sector's profitability is inadequate,

according to major producers who took part in the

CEO/Executive Panel Discussion, promoted on Aug. 12 at

RISI's Latin American Pulp and Paper Outlook Conference,

in São Paulo, Brazil. The executives commented on the

current low prices for bleached eucalyptus kraft (BEK)

pulp, as well as on the high production costs faced by the

companies as the main factors impacting the companies'

performance.

WHERE DOES THE WOOD COME FROM?

Recent survey of F&W managers in Georgia reports

73% of harvests are from planted stands

A 2008 Georgia survey of loggers reported 80% of

harvests from planted stands

If true, then plantations are carrying a big load…

The 2013 FIA data reports 37% of forested acres are planted

and 63% are natural in Georgia

HOW MUCH WOOD DO WE USE (GEORGIA

COMPARISON)?

Softwood Hardwood

FIA Avg. Annual Removals

in Georgia (2009-2013)

37,972,648 10,041,189

TPO Timber Receipts in

Georgia

36,444,580 6,944,518

% Difference 4% 31%

FIA Avg. Annual Removals - the average amount of volume removed each year during the five-year period (2009-2013)

TPO - the total volume of roundwood products from all sources, plus the volume of byproducts recovered from mill

residues (equals roundwood product drain)

UNCERTAINTY IN THE NUMBERS

Forest Inventory Assessment (FIA) – a federally

funded inventory of state lands

Timber Product Outputs (TPO) – a federally funded

assessment of roundwood receipts and production

from mills

Comprehensive Statewide Forest Inventory Analysis

and Study (CSFIAS) – a state funded effort to fine

tune the FIA data with GIS

HOW MANY ACRES DO WE HAVE (FLORIDA

COMPARISON)?

Planted Acres Natural Acres Total Acres

2013 FIA Data 4,751,650 12,520,145 17,271,795

2013 SCFIAS Data 5,621,569 11,260,923 16,882,492

Difference

SCFIAS/FIA (%)

118% 90% 98%

FIA – Forest Inventory and Analysis program of the U.S. Forest Service. Permanent plots are measured

on a rotating basis annually (1/5 each year in Florida). Measures the status and trends in multiple

variables.

CSFIAS – Comprehensive Statewide Forest Inventory Analysis and Study. The State of Florida analyzes

FIA plot data in a stratified approach with GIS imagery to report on the timber resource.

WHAT DO THESE DISCREPANCIES MEAN?

We have data sources that aren’t reconciled.

Could lead to mistakes in mill openings/closings

Hard to plan for the future when you don’t know what

you have today.

LUMBER PRICES VS. GEORGIA SAWTIMBER STUMPAGE

PRICES IN 2013 DOLLARS ($/TON)

Data compiled from Timber Mart-South and Random Lengths.

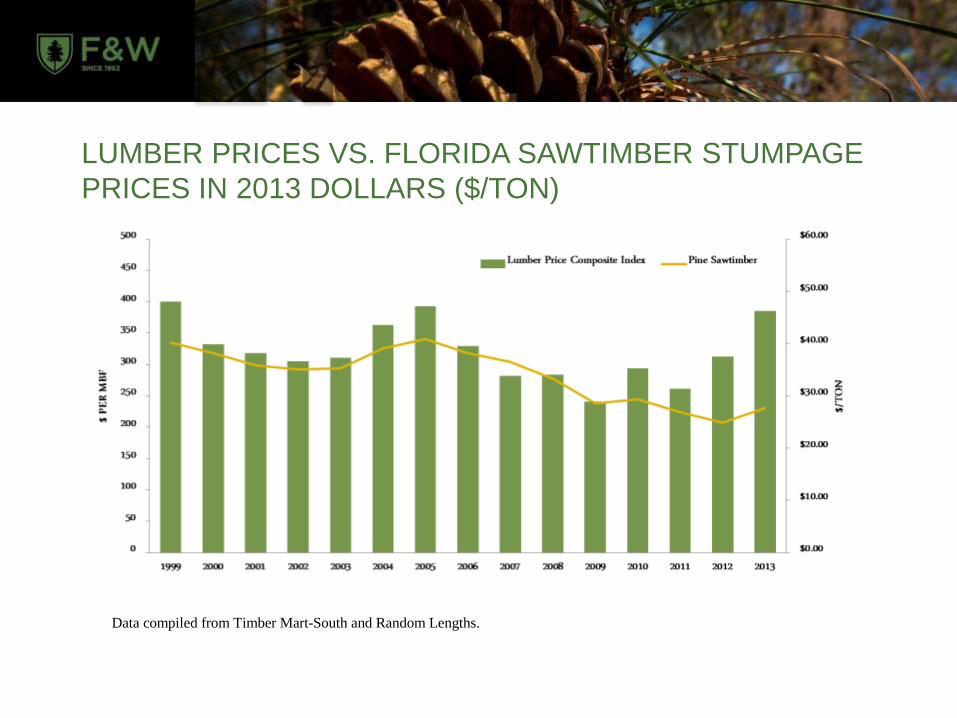

LUMBER PRICES VS. FLORIDA SAWTIMBER STUMPAGE

PRICES IN 2013 DOLLARS ($/TON)

Data compiled from Timber Mart-South and Random Lengths.

SUPPLY DISRUPTION IN THE PNW FROM THE

MOUNTAIN PINE BEETLE

The B.C. Ministry of Forests, Lands and Natural Resource Operations estimates that the mountain pine beetle has now killed a cumulative total of 710 million cubic metres of timber since the current infestation began. (approx 710 million tons)

The cumulative area of B.C. affected to some degree (red-attack and grey-attack) is estimated at 18.1 million hectares. (45 million acres)

Newly attacked lodgepole pine trees turn red about one year after infestation. Trees can stay in the red-attack stage for two to four years before turning grey as they lose their needles.

In terms of area, 4.6 million hectares of red-attack were surveyed in 2011. This is compared to 7.8 million hectares and 6.3 million hectares in the two preceding years.

The amount of habitat available to the beetle has begun to diminish as the beetle has already attacked most of the mature lodgepole pine in the Central Plateau region.

(from the BC Ministry of forests)

CANADIAN PRODUCERS ARE MOVING SOUTH

The latest WOOD MARKETS annual survey of the “Top 20” Canadian and U.S. softwood lumber producers shows modest gains in both countries in 2013 as lumber demand continues to rise in the U.S. and in key export markets. U.S. softwood lumber shipments increased 5.1% to 30.0 billion bf, whereas Canadian production rebounded from minimal gains in 2012 to record an increase of 4.0% to 23.5 billion bf. Corporate acquisitions were again a big part of the story as the Canadian buying frenzy continued in the U.S. South – more than 25 mills have been purchased by Canadian firms in the South that all started in the mid-2000s!

Wood Markets Monthly International Report Press Release

DÉJÀ VU (ALL OVER AGAIN)

This reminds me of the late 80’s, early 90’s

We had been through a long period of declining

housing starts, declining stumpage prices

There had been a huge supply disruption in the NW

…causing industry to move to the South

…and we were on the cusp of an incredible 15 year

“golden period” for landowners in the South.

THE ONLY DIFFERENCE IS…

It feels like we’re working hard but not making progress…

THE ONLY DIFFERENCE IS…

It feels like we’re working hard but not making progress…

…SO WHAT NOW?

We should be in a period of slowly rising sawtimber prices, with occasional fits and spurts.

Inventory issues associated with tree planting of late 80’s, early 90’s will be a damper, but won’t overcome rising demand.

Pulpwood prices should stay strong with increasing demand from pellet mills offsetting decreased roundwood consumption by mills as sawmill residues increase.

HOW SHOULD I MANAGE?

Management decisions usually center around these

variables:

Rotation length

Trees per acre to plant

To thin or not to thin

Silvicultural inputs

AFTER RUNNING SOME BORING FINANCIAL

CALCULATIONS, WE FOUND THAT…

The old “standby” management style of planting 500 to 700 trees per acre, thinning once or twice, and cutting at 25 to 35 still works, but… If you assume pw prices are going up a lot, it pays to plant more

trees, cut sooner without thinning, and…

If you assume st prices are going way up, it pays to plant fewer trees, carry longer, and thin once or twice…

But if you assume you don’t know what market conditions will be at the time you harvest, the old standby mitigates that risk – we believe the market risk adjusted return is equal to or better than committing to a single product rotation

SUMMARY

Times are getting better, but this won’t be like the 90’s.

Consider lagging sawtimber harvests some…

…but if you have non-productive or poorly stocked stands replant them now.

It’s time to thin!

We have to grow more volume on fewer acres.

Plantations are probably carrying the load.

We need to support state and federal agencies as they upgrade data to our current needs.