Cross-border business – Hong Kong as a preferred ... · Cross-border business – Hong Kong as a...

29

IYER PRACTICE Singapore vs Hong Kong Cross-border business – Hong Kong as a preferred jusrisdiction SINGAPORE | HONGKONG 20 YEARS IN PRACTICE Sanjay Iyer 4 September 2014

Transcript of Cross-border business – Hong Kong as a preferred ... · Cross-border business – Hong Kong as a...

IYER PRACTICE Singapore vs Hong Kong

Cross-border business – Hong Kong as a preferred jusrisdiction

SINGAPORE | HONGKONG20 YEARS IN PRACTICE

Sanjay Iyer4 September 2014

IYER PRACTICE Singapore vs Hong Kong

General Background

Tax

Tax Treaties

AGENDA

SINGAPORE | HONGKONG20 YEARS IN PRACTICE

GENERAL BACKGROUND

IYER PRACTICE Singapore vs Hong Kong

General Factor Hong KongEase of Company Formation 4 daysTime Zone GMT + 8 hoursBusiness Language EnglishForeign Exchange Controls NoneAvailability of Service Providers PlentifulEconomically and Politically Stable VeryLegal System Common lawWorld Bank Survey:Ease of Doing Business 2Starting a Business 5Registering Property 89Getting Credit 3Protecting Investors 3Paying Taxes 4Trading Across Borders 2Enforcing Contracts 9Resolving Insolvency 19

4

IYER PRACTICE Singapore vs Hong Kong

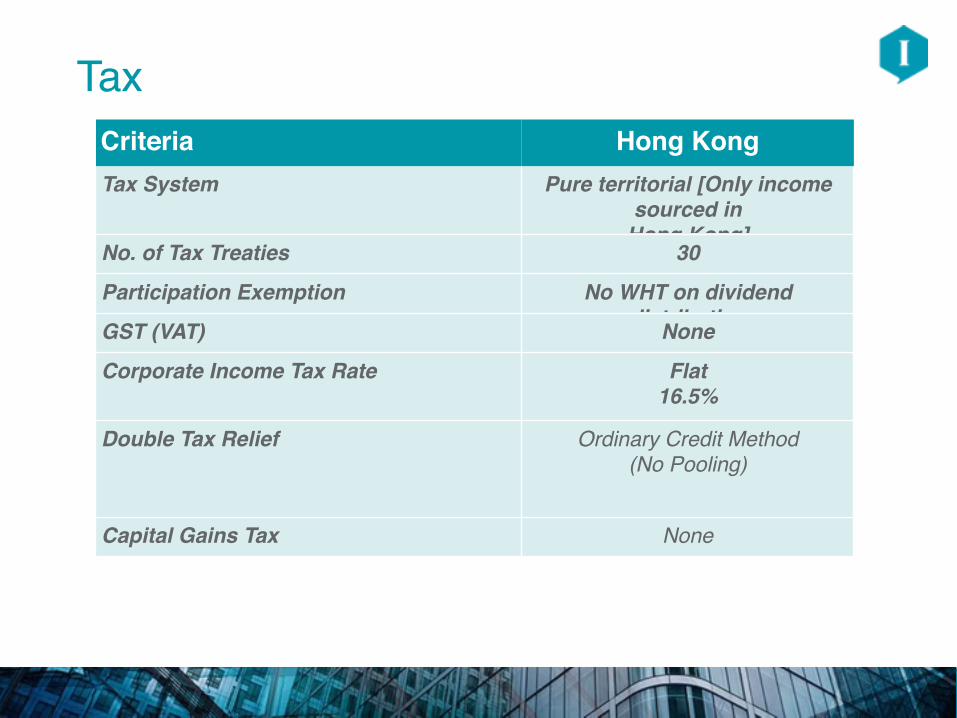

Criteria Hong KongTax System Pure territorial [Only income

sourced in Hong Kong]

No. of Tax Treaties 30

Participation Exemption No WHT on dividend distributionGST (VAT) None

Corporate Income Tax Rate Flat 16.5%

Double Tax Relief Ordinary Credit Method(No Pooling)

Capital Gains Tax None

5

Tax

IYER PRACTICE Singapore vs Hong Kong

• Setting up– Minimum one director (natural, can be non-resident)– Resident Company Secretary (Corporate or Individual)– Local Registered Office (No PO Box)– No definition of tax residence (as per DTA) [Inc (HK); M&C (O/S)]– Minimum share capital – HK$1– Business registration certificate– No restriction on foreign ownership

• Ongoing requirements– Audit – AGM/Annual Return– Profits tax return (Must always be filed)

Setting Up and Ongoing Requirements

6

TAX FACTORS

7

IYER PRACTICE Singapore vs Hong Kong

Dividend Income

8

Dividend income (Received)

✓ Hong Kong sourced income - Exempt from taxation

✓ Foreign sourced income - Exempt even if remitted

Dividend Income (Paid)

✓ No dividend withholding tax

Shareholder

Hong Kong

InvestmentN

o dividend w

ithholding tax

Dividend incom

e exempt

IYER PRACTICE Singapore vs Hong Kong

Interest Income

9

Interest income (Received)

✓ Hong Kong sourced income – Exempt unless earned from carrying on such a business (financial institution)

✓ Foreign sourced income - Exempt from taxation even if remitted

Interest Income (Paid)

✓ No interest withholding tax

✓ BUT no deduction

Shareholder

Hong Kong

LoanN

o interest w

ithholding tax

Interest income exem

pt

IYER PRACTICE Singapore vs Hong Kong

Royalty Income

10

Royalty income (Received)

✓ Hong Kong sourced income – Exempt unless earned from carrying on such a business

✓ Foreign sourced income - Exempt from taxation

Royalty Income (Paid)

✓ 30% of 16.5% gross✓ 100% of 16.5% (associated

company & previously owned by a person carrying on business in Hong Kong)

✓ Deemed source in Hong Kong (deductible

✓ Unless reduced by treaties)

Shareholder

Hong Kong

Investment

30% of 16.5%

gross; 100%

of 16.5%, deem

ed sourced in H

K, unless reduced by treaties

Royalty income exem

pt

IYER PRACTICE Singapore vs Hong Kong

Other Payments to Non-Residents

No withholding tax on payments but required to report IRD in tax return

11

IYER PRACTICE Singapore vs Hong Kong

Tax Incentives

12

IYER PRACTICE Singapore vs Hong Kong 13

Hong Kong Outside

Hong Kong Activities

• Exempt income in Hong Kong?

Offshore Claim

IYER PRACTICE Singapore vs Hong Kong

• Territorial tax system

• Person will not be subject to profits tax unless:

✓ Business must be carried on in Hong Kong

✓ Profits must arise in or be derived from Hong Kong

14

Inland Revenue Ordinance

IYER PRACTICE Singapore vs Hong Kong

Operations Test

• “All profits from business transacted in Hong Kong, whether directly or through an agent”

✓ “What the taxpayer has done to earn profit in question” and “where has he done it”?

• Focus of the effective causes of profit

✓ Where is the geographical location of the taxpayer’s profit producing activities?

✓ Commercial answer: Practical realities?

[ING Baring, Hang Seng Bank]

15

Case Law

IYER PRACTICE Singapore vs Hong Kong

• DIPN 21: Locality of profits – cases don’t cover all situations

• Evidence:

– Expenses (Travelling/hotel)

– Agents (Agency agreement)

• Advance Rulings available

• Subject to tax overseas?

16

Hong Kong IRD Position

IYER PRACTICE Singapore vs Hong Kong

Capital Gains

• No Capital Gains Tax

• Tax if trading in nature

• Badges of Trade

• No Safe Harbour

17

IYER PRACTICE Singapore vs Hong Kong

• Intention at time of purchase

• Period of ownership

• Frequency of similar transactions

• Reasons for sale

• Means of financing the acquisition

18

Badges of Trade

TAX TREATIES

19

IYER PRACTICE Singapore vs Hong Kong

Tax Treaties

• 30 full tax treaties concluded, 28 in force

• 1 full treaty pending

• No limitation of relief provisions

20

IYER PRACTICE Singapore vs Hong Kong

Reducing HK Withholding Tax

• Royalties only

• Obtain reduced withholding (royalties only) in Hong Kong✓ Take a tax position (in tax return)

✓ Provide COR in residence jurisdiction

✓ Provide details of transaction

21

IYER PRACTICE Singapore vs Hong Kong

• Company incorporated or constituted in Hong Kong

• Company incorporated or constituted outside Hong Kong but managed or controlled in Hong Kong

22

Certificate of Residence Status

IYER PRACTICE Singapore vs Hong Kong

Hong Kong – India Treaty

• Signed a limited double taxation treaty in 2003 (exempting shipping companies and airlines)

• In April 2010, India specified HK as a ‘specified territory’

• Two rounds of DTA negotiations in late 2010 and 2011

• Talks concluded unsuccessfully

• New government in India – policy action increase in FDI – might result in a treaty

23

IYER PRACTICE Singapore vs Hong Kong

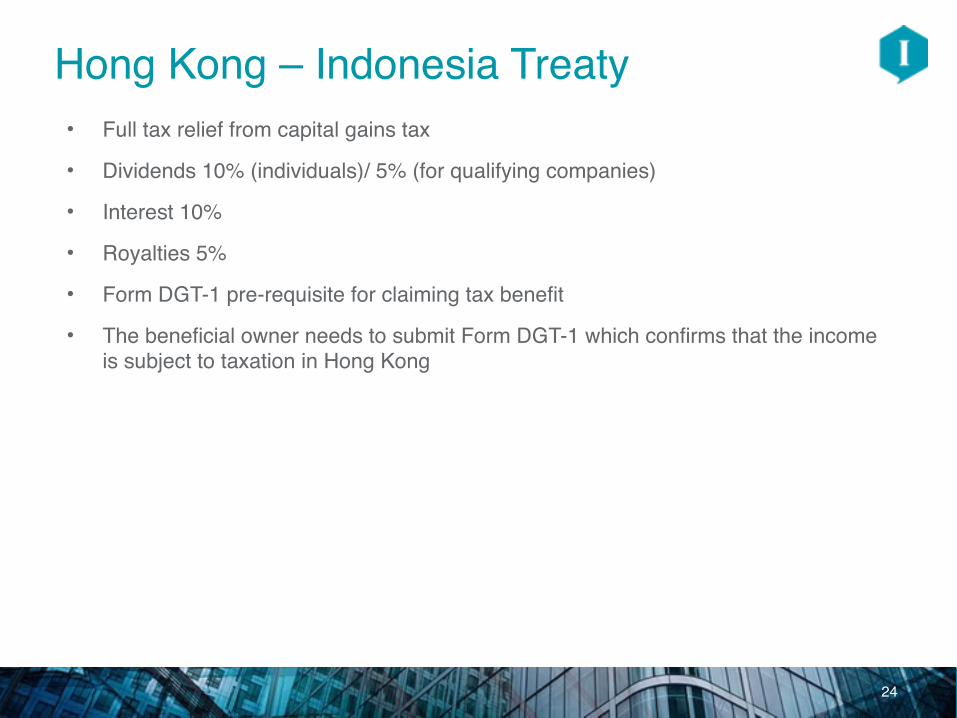

Hong Kong – Indonesia Treaty• Full tax relief from capital gains tax

• Dividends 10% (individuals)/ 5% (for qualifying companies)

• Interest 10%

• Royalties 5%

• Form DGT-1 pre-requisite for claiming tax benefit

• The beneficial owner needs to submit Form DGT-1 which confirms that the income is subject to taxation in Hong Kong

24

IYER PRACTICE Singapore vs Hong Kong

Hong Kong – Indonesia Treaty• Issues:

✓ Hong Kong tax system is territory based, therefore a Hong Kong recipient of dividends from Indonesia will not be able to obtain a Form DGT-1

✓ Therefore, suffer withholding @ 20% or potential adjustments and penalties

✓ DGT Form requires certification of tax residency from relevant tax authority

✓ Subject to tax requirement in DGT-1

✓ Uncertainty as to claiming CGT DTA relief

25

IYER PRACTICE Singapore vs Hong Kong

Hong Kong – China Treaty• Full tax relief from capital gains tax in respect of the disposal of non “land rich”

companies if under 25% owned, otherwise 10%

• Dividends 10% (individuals)/ 5% (for qualifying companies)

• Interest 7%

• Royalties 7%

• For dividend income, numerous requirements need to be met (Circular 81)

• Non-residents need to provide proof that DTA relief requirements are met (Circular 124)

• Assessing whether beneficial ownership requirements met (Circular 124)

• Different rules for different local tax authorities

26

IYER PRACTICE Singapore vs Hong Kong

Hong Kong – China Treaty

• State Administration of Taxation of Mainland China has set out procedures for obtaining Certificate of Tax Residency (‘CTR’) in Hong Kong

• Announcement 53 – China tax authority to issue a referral letter to the IRD to facilitate the application of CTR

• To submit the referral letter and application form to obtain the CTR

• The CTR issued would distinguish whether the entity is incorporated or constituted under the HK laws or under foreign jurisdiction laws

• The CTR would entitle the taxpayer benefits under the treaty in Mainland China

• Whether an entity qualifies as a tax resident in Hong Kong is still an issue, especially for Companies incorporated abroad

27

IYER PRACTICE Singapore vs Hong Kong

Hong Kong – China Treaty• Circular 81 requires following conditions to be satisfied:

✓ The recipient of the dividend must be Hong Kong tax resident

✓ The recipient of dividend must be the beneficial owner

✓ The dividend must qualify as dividend under the tax laws of China

✓ The recipient must satisfy the minimum ownership requirement

✓ Any other condition that SAT may impose

• Ultimately onus is on the HK resident to prove that they satisfy the conditions to claim DTA relief

• Local tax authorities continuously change their views on the application of law

28

IYER PRACTICE Singapore vs Hong Kong

• International & Domestic Tax

• Company Formation & Administration

• Trusts & Foundations

• Immigration & HR

• Funds & Family Offices

• Accounting & Financial Reporting

The insight to be your trusted adviser

29

Unit 29E, 29/F Admiralty Centre Tower 118 Harcourt Road, AdmiraltyHong Kong

Sanjay IyerEmail [email protected] +852 2529 9952Mobile +852 9355 3495