Critical Materials Report Quarterly Update: Dielectric ... · Quarterly Update: Dielectric...

14

Critical Materials Report Quarterly Update: Dielectric Precursors October 1, 2017 By Jonas Sundqvist, Ph.D., Sr. Analyst www.Techcet.com [email protected] +1 - 480 - 382 - 8336

Transcript of Critical Materials Report Quarterly Update: Dielectric ... · Quarterly Update: Dielectric...

Critical Materials Report Quarterly Update:

Dielectric PrecursorsOctober 1, 2017

By Jonas Sundqvist, Ph.D., Sr. [email protected]

+1-480-382-8336

Readers’ Note: This presentation represents the interpretation and analysis of information

generally available to the public or released by responsible agencies or individuals. Data was obtained from sources considered reliable. However, accuracy or completeness is not guaranteed. This report contains information generated by Techcet by way of primary and secondary market research methods.

The information contained in this presentation is for the use of TECHCET’s representatives and customers or prospective customers. It is considered confidential in nature and should not be shared with others outside of the aforementioned parties. Your cooperation is much appreciated.

[email protected] 10/1/2017

TECHCET CA LLC Copyright 2017 all rights reserved. TECHCET/CMC Confidential www.techcet.com 2

Confidential Information

OverviewOutlook semiconductor equipment market 2017/2018

Growth drivers for dielectric precursor

Forecast updated (Q4 2017)

3DNAND

EUV & DUV

DRAM Air Gaps

Future China demand today and 2020

[email protected] 10/1/2017 3TECHCET CA LLC Copyright 2017 all rights reserved.

TECHCET/CMC Confidential www.techcet.com

Outlook semiconductor equipment market 2017/2018

[email protected] 10/1/2017 4TECHCET CA LLC Copyright 2017 all rights reserved.

TECHCET/CMC Confidential www.techcet.com

In total, the semiconductor equipment market is expected toreach $70.4 billion in 2017, up 30.6% over 2016, according toVLSI Research. In 2018, the IC equipment market is projectedto hit $73.5 billion, up 4.4% over 2017, according to VLSIResearch.

Semiconductor equipment market growth. Data source: VLSI Research

“Silicon content in smartphones and other mobile devices isincreasing as vendors add greater functionality. Layering ontop of that are several emerging trends such as IoT, big data, AIand smart vehicles that are creating demand for greatercomputing power and expanding storage capacity.”- Arthur Sherman, vice president of marketing and business development at Applied Materials

Samsung 2017 spending: $14 billion – 3D NAND, $ 7 billion DRAM, and $5 billion Foundry

Growth drivers for ALD & CVD Metal and High-k precursors CAGR: 13% (2017) followed by 8% (2018)

3DNAND stacks moving to 64 layers driving demand for ALD & CVD precursors. New materials may be needed >128 layers.

DRAM recovery driven by smartphones and servers. Opening for EUV scaling to 10 nm announced by Samsung for 2019

2017 Record wafer fab equipment investment led by South Korea

IoT, automotive and industrial applications drive strong demand of legacy nodes on 200 mm

Early stage impact of 10 nm ramps followed by start of 7nm migration in 2018

China - Both global and local players driving Fab investments

[email protected] 10/1/2017 5TECHCET CA LLC Copyright 2017 all rights reserved.

TECHCET/CMC Confidential www.techcet.com

In 2017, South Korea will be the largest equipmentmarket for the first time. After maintaining the topspot for five years, Taiwan will place second, whileChina will come in third. All regions tracked willexperience growth, with the exception of Rest ofWorld (primarily Southeast Asia). [Semi.org, Dec2017]

Forecast (no significant changes since last quarter)

[email protected] 10/1/2017 6TECHCET CA LLC Copyright 2017 all rights reserved.

TECHCET/CMC Confidential www.techcet.com

2015 2016 2017 2018 2019 2020 2021CAGR [%] 20% 12% 13% 9% 8% 6%BTBAS 0.9 1.0 1.0 1.1 1.1 1.2 1.2DIPAS/BDEAS(SAM24) 5.9 7.0 8.0 9.1 10.2 11.5 12.8TSA 1.8 4.0 5.7 7.6 8.9 9.9 10.0HCDS 1.1 2.5 3.5 4.7 5.4 6.1 6.1TEOS 2.2 2.4 2.4 2.5 2.6 2.7 2.83MS, 4MS 4.2 4.5 4.6 4.8 5.0 5.2 5.4Low k, interconnect 4.6 4.9 5.1 5.3 5.5 5.7 5.9SOD 8.9 9.6 9.7 10.0 10.5 10.9 11.7

0.0

10.0

20.0

30.0

40.0

50.0

60.0

Reve

nues

(MU

SD)

Dielectric Precurssors

Q4 ModificationsTECHET latest Wafer forecast (december 2017 release)

Xpoint not implemented (will be in 2018 release)

2021 total revenue corrected downwards from USD 560 M to USD 660 M due to increased wafer starts in 3D NAND and DRAM yielding growth in :

- HCDS

- TSA

- DIPAS/BDEAS(SAM24)

[email protected] 10/1/2017 7TECHCET CA LLC Copyright 2017 all rights reserved.

TECHCET/CMC Confidential www.techcet.com

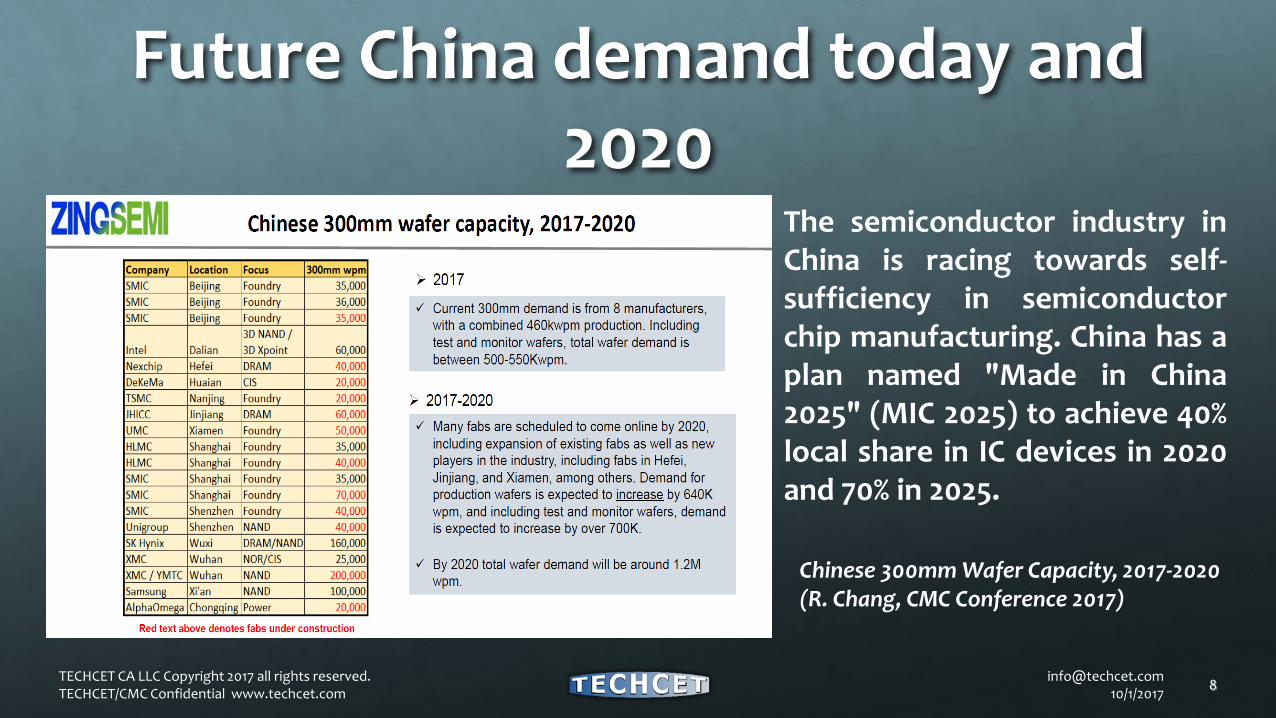

Future China demand today and 2020

The semiconductor industry inChina is racing towards self-sufficiency in semiconductorchip manufacturing. China has aplan named "Made in China2025" (MIC 2025) to achieve 40%local share in IC devices in 2020and 70% in 2025.

[email protected] 10/1/2017 8TECHCET CA LLC Copyright 2017 all rights reserved.

TECHCET/CMC Confidential www.techcet.com

Chinese 300mm Wafer Capacity, 2017-2020 (R. Chang, CMC Conference 2017)

Logic fab ramp forecast according to TrendForce(April 2017)

[email protected] 10/1/2017 9TECHCET CA LLC Copyright 2017 all rights reserved.

TECHCET/CMC Confidential www.techcet.com

Demand for High-k/Metal Gate precursors in China will rice starting 2018 (e.g. Hf, Ti, Ta )

Note: On the right is provided the corresponding technology and precursor demand for ALD assessed by TECHCET

China regional activities

[email protected] 10/1/2017 10TECHCET CA LLC Copyright 2017 all rights reserved.

TECHCET/CMC Confidential www.techcet.com

Region Fabs ALD/CVD Equipment

Other Precursors Part of Sino Fund / RMB

Beijing SMIC Naura, Beijing Xiantec

Air Liquide, Versum Materials, Entegris

32 B

Shanghai Hynix Wuxi, TSMC, SMIC, CSMC, Samsung, Grace*, ASMC

AMECLead Micro

Zing Semi, Wafer Works, Anji Microelectronics Co

Air Liquide, Versum Materials, Entegris

50 B

Xian Samsung Spectrum Materials, Entegris

30 B

Liaoning Intel Dalian Piotech Ltd. Versum Materials 10 BNanjing Tsinghua, TSMC Air Liquide 60 BHunan (TBB) 5 BSichuan Texas Instrument*

GlobalFoundries12 B

Wuhan (TBB) 30 BXiamen UMC 60 BGuangdong (TBB) Versum Materials 15 BShenzhen SMIC (TBB) 10 B

China Regional Funding, and Locations of Established 300mmFabs and ALD/CVD Precursor Companies

[email protected] 10/1/2017 11TECHCET CA LLC Copyright 2017 all rights reserved.

TECHCET/CMC Confidential www.techcet.com

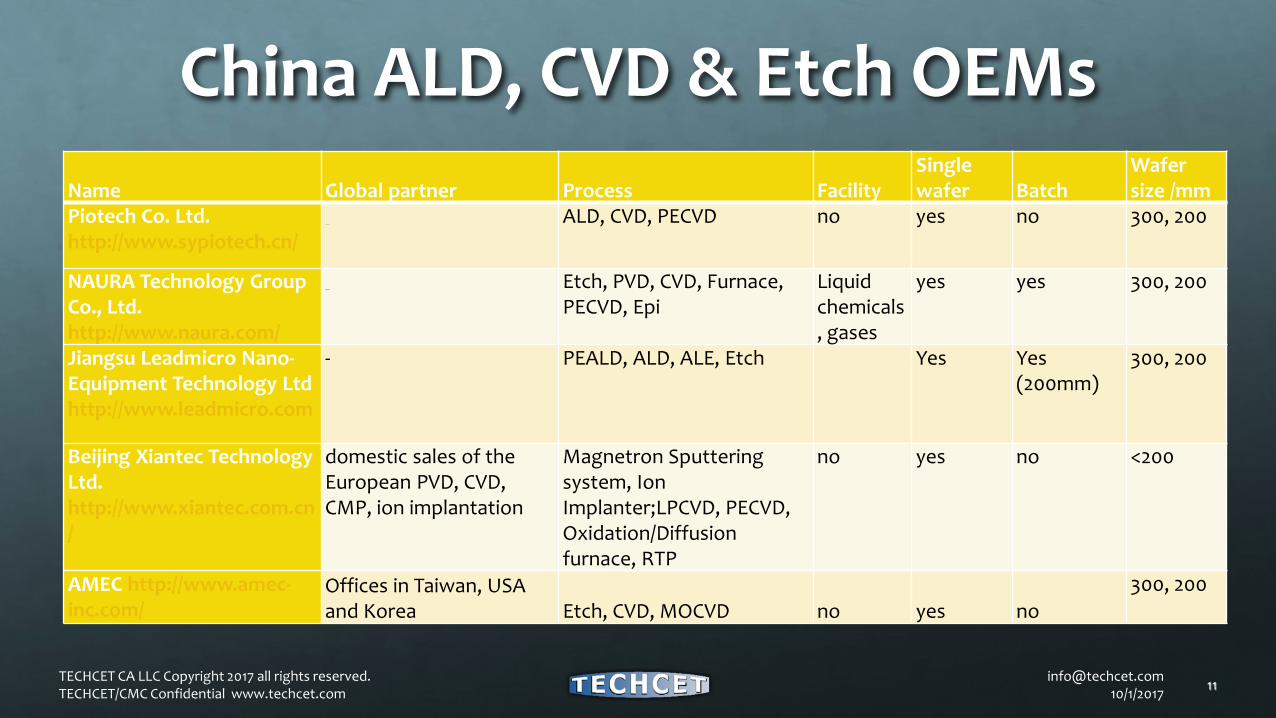

Name Global partner Process FacilitySingle wafer Batch

Wafer size /mm

Piotech Co. Ltd. http://www.sypiotech.cn/

ALD, CVD, PECVD no yes no 300, 200

NAURA Technology Group Co., Ltd. http://www.naura.com/

Etch, PVD, CVD, Furnace, PECVD, Epi

Liquid chemicals, gases

yes yes 300, 200

Jiangsu Leadmicro Nano-Equipment Technology Ltdhttp://www.leadmicro.com

- PEALD, ALD, ALE, Etch Yes Yes (200mm)

300, 200

Beijing Xiantec Technology Ltd. http://www.xiantec.com.cn/

domestic sales of the European PVD, CVD, CMP, ion implantation

Magnetron Sputtering system, Ion Implanter;LPCVD, PECVD, Oxidation/Diffusion furnace, RTP

no yes no <200

AMEC http://www.amec-inc.com/

Offices in Taiwan, USA and Korea Etch, CVD, MOCVD no yes no

300, 200

China ALD, CVD & Etch OEMs

[email protected] 10/1/2017 12TECHCET CA LLC Copyright 2017 all rights reserved.

TECHCET/CMC Confidential www.techcet.com

Name Global partner Process FacilityZillion-Tek http://www.zillion-tek.com/en/product.php

Kojundo, CS, Veeco ALD, CVD Gas mixing, scrubbers

Wonik IPS http://www.ips.co.kr

Wonik IPS ALD, CVD Gas; Liquid delivery panels as subsystems

AIR LIQUIDE China Holding Co., Ltd. http://www.airliquide.com

Air Liquide ALD, CVD Gas; Liquid delivery panels as subsystems

Entegris (Shanghai) Microelectronics Trading Co., Ltd. http://www.entegris.com

Entegris ALD, CVD Gas; Liquid delivery panels as subsystems

KC Tech Co., Ltd. (KC TECH China) http://www.kctech.com/

KC Tech Co., Ltd. ALD, CVD Gas; Liquid delivery panels as subsystems

Shanghai Gentech Co., Ltd. http://www.gentech-online.com/index.php?a=lists&catid=78

ALD, CVD Gas; Liquid delivery panels as subsystems

China Gas, Precursor and Facility

China ConclusionsToday the priority in China is focused on building the fabs rather than building up the complete infrastructure for materials, equipment and technology.

With respect to wafer processing equipment there are two leading China OEMs for Etch, CVD and some ALD activity as well and those areAMEC (Mainly Etch) and NAURA. These companies rely on expertise from ex- Applied and Lam employees returning home to China.

There is a supply issue currently, partly also due to China's local regulation and enforcement, which is currently not very well synchronized.

The difference in regulation and enforcement in each province will also slow down the investment to actual achievable situation.

There are contradictory enforcement actions between economic development and environmental protection regulation and enforcement. For example, in Greater Shanghai Area, dangerous goods are generally prohibited to enter. Only very specialized licensed players might or might not be able to handle the delivery on a regular basis.

Customers right now will purchase the equipment much more quickly, as they announced the fab buildup speed. Material supply will not be able to keep up to this announcement speed. So, it will force the announcement speed to gradually slow down or spread out the implementation time, and consequently put pressure on the rate of production ramp. The ramp schedule is not likely to go as originally planned for the first half of the year.

Regulation implementation and enforcement will not be able to catchup to the ramp-up schedule.

[email protected] 10/1/2017 13TECHCET CA LLC Copyright 2017 all rights reserved.

TECHCET/CMC Confidential www.techcet.com

Pertinent feedback from Industry Interviews

Thank [email protected]

+49 (0) 152 0294 3083

[email protected] 10/1/2017

TECHCET CA LLC Copyright 2017 all rights reserved. TECHCET/CMC Confidential www.techcet.com 14