Credit Reports - slcolibrary.org · acct) Identify Accounts that Build Credit ... 30 days late on...

26

Credit Reports This program is made possible by a grant from the FINRA Investor Education Foundation through Smart Investing@your library®, a partnership with the American Library Association. http://www.slcolibrary.org/smartinvesting

-

Upload

nguyendang -

Category

Documents

-

view

215 -

download

0

Transcript of Credit Reports - slcolibrary.org · acct) Identify Accounts that Build Credit ... 30 days late on...

Credit Reports

This program is made possible by a grant from the FINRA Investor Education Foundation through Smart Investing@your library®, a partnership with the American

Library Association.

http://www.slcolibrary.org/smartinvesting

What will we discuss?

Receiving a free copy of your credit report.

What information is in your credit report.

How can you dispute inaccuracies in your report.

Credit Scores

Credit Reports vs. Credit Scores

Your CREDIT REPORT provides details about your borrowing history.

This is like a report card.

Your CREDIT SCORE summarizes the info in your report. Scores range between 300-850.

This is like your GPA.

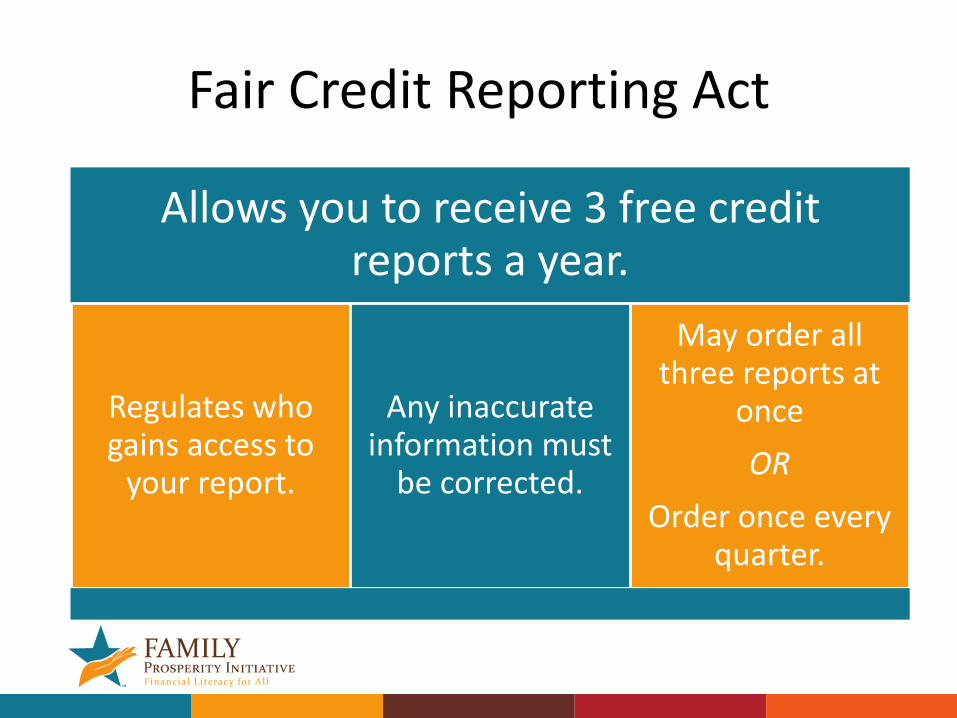

Fair Credit Reporting Act

Allows you to receive 3 free credit reports a year.

Regulates who gains access to

your report.

Any inaccurate information must

be corrected.

May order all three reports at

once

OR

Order once every quarter.

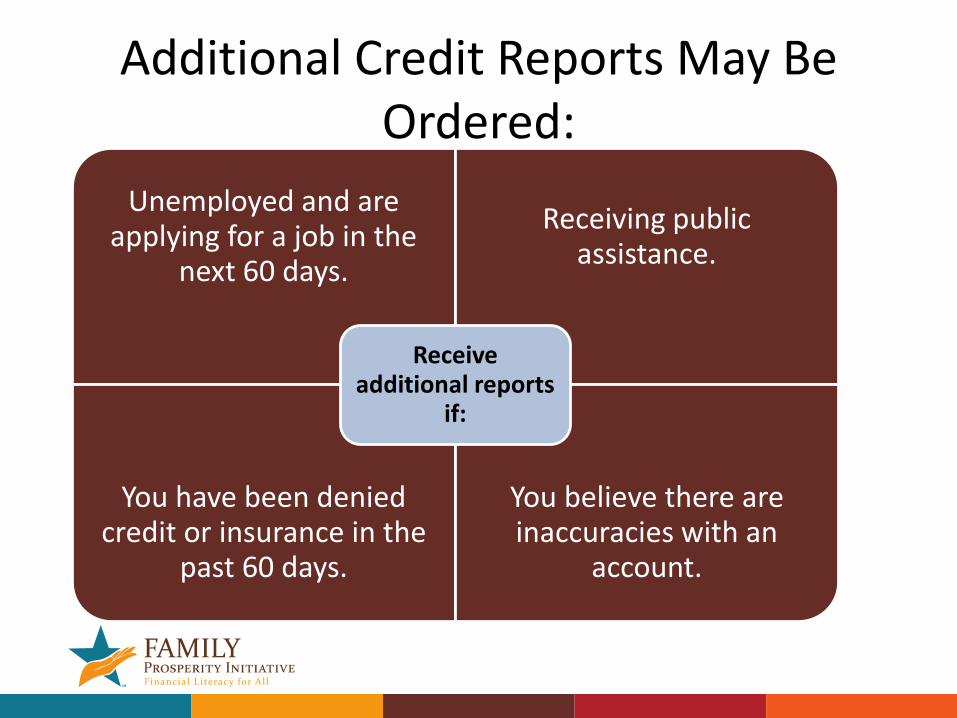

Additional Credit Reports May Be Ordered:

Unemployed and are applying for a job in the

next 60 days.

Receiving public assistance.

You have been denied credit or insurance in the

past 60 days.

You believe there are inaccuracies with an

account.

Receive additional reports

if:

Ordering Free Copies of Your Report

www.annualcreditreport.com

Phone: 1-877-322-8228

Mail: Annual Credit Report Services

PO BOX 105281

Atlanta GA 30348-5281

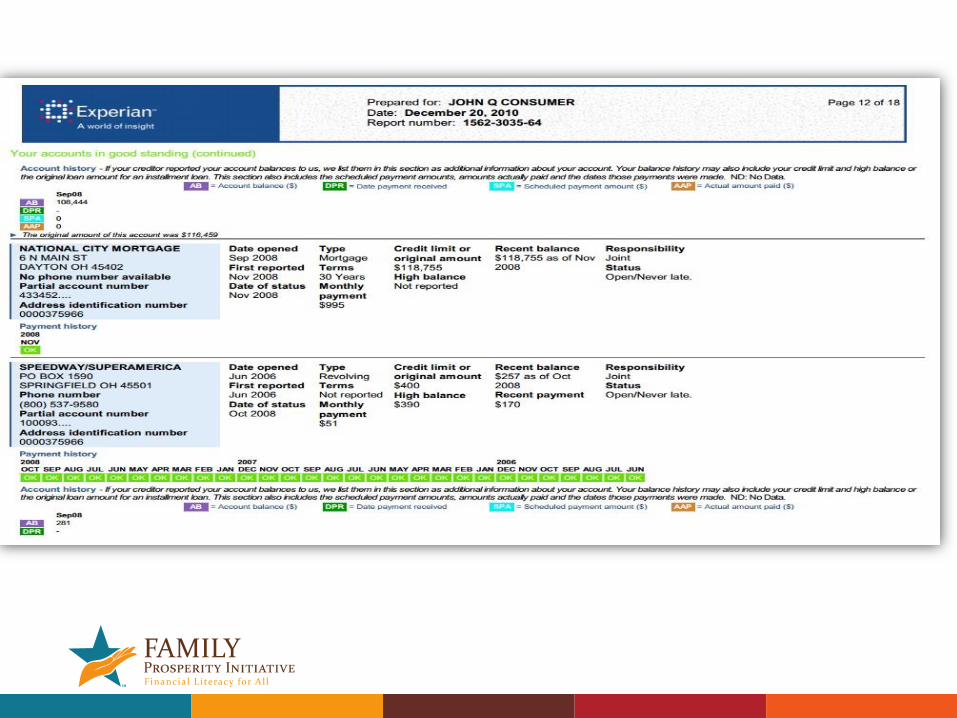

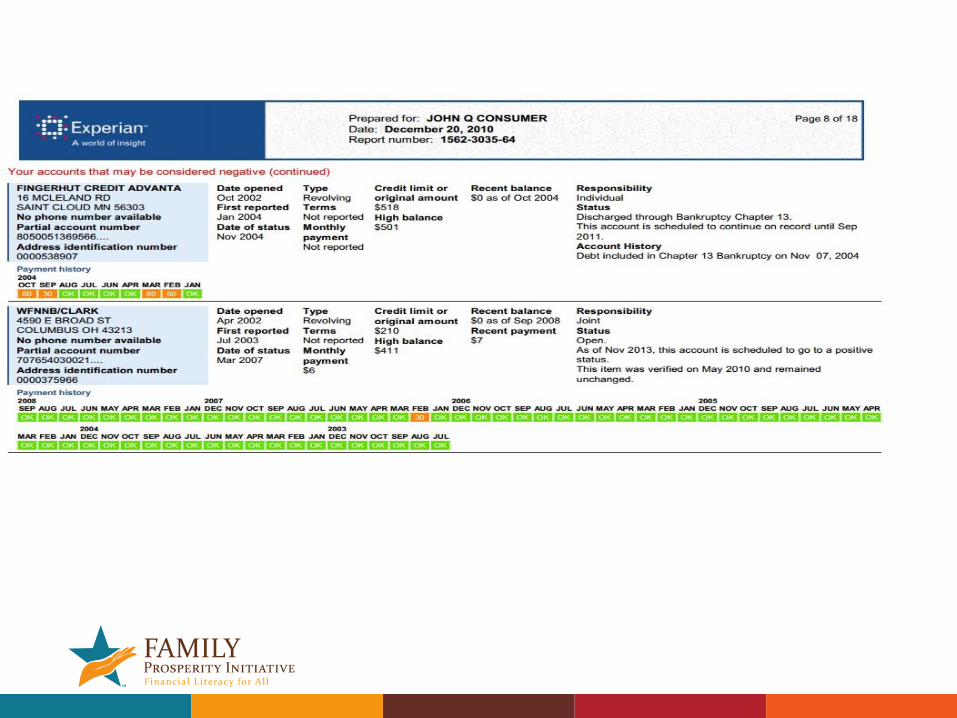

What Information is in Your Credit Report?

Credit Report

Inquiries

Personal Information

Late payment Information

Public Records

Trade Lines or Credit

Information

What is NOT on your report

NOT on your credit report

Current Medical Bill Payments

Savings and Checking Account

Information

Current Utility Bill Payments

Current Rent payments

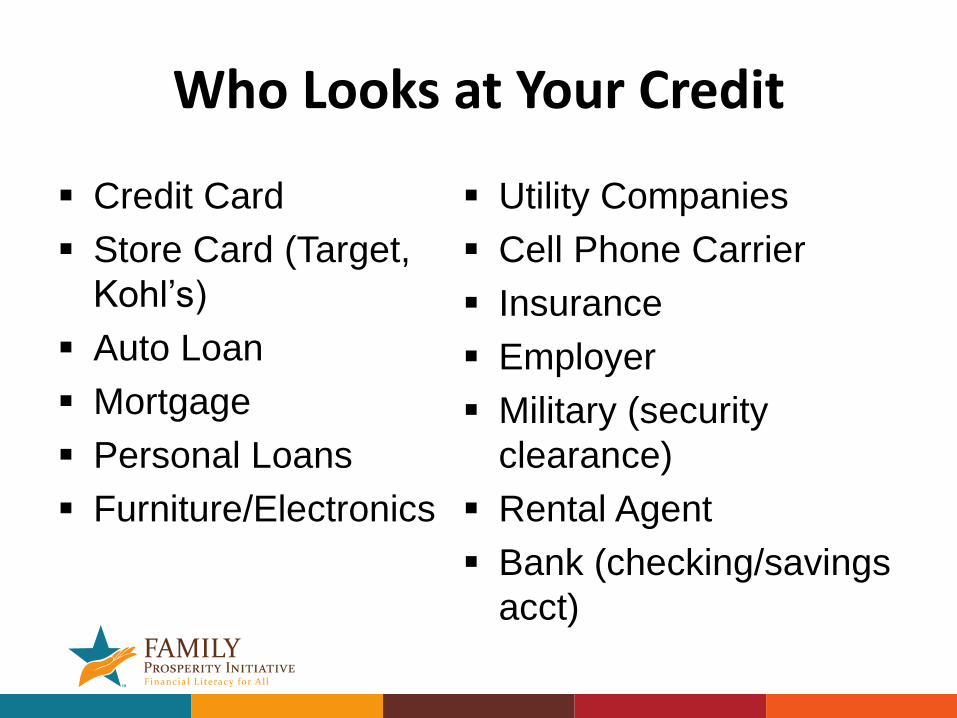

Who Looks at Your Credit

Credit Card

Store Card (Target,

Kohl’s)

Auto Loan

Mortgage

Personal Loans

Furniture/Electronics

Utility Companies

Cell Phone Carrier

Insurance

Employer

Military (security

clearance)

Rental Agent

Bank (checking/savings

acct)

Identify Accounts that Build Credit

Credit Card

Utility Companies

Cell Phone Carrier

Store Card

Personal Loan

Bank (checking/saving accounts)

Furniture/Electronics Loan

Insurance

Employer

Mortgage

Military (security clearance)

Rental Agent

Auto Loan

Payday Loans

Title Loan

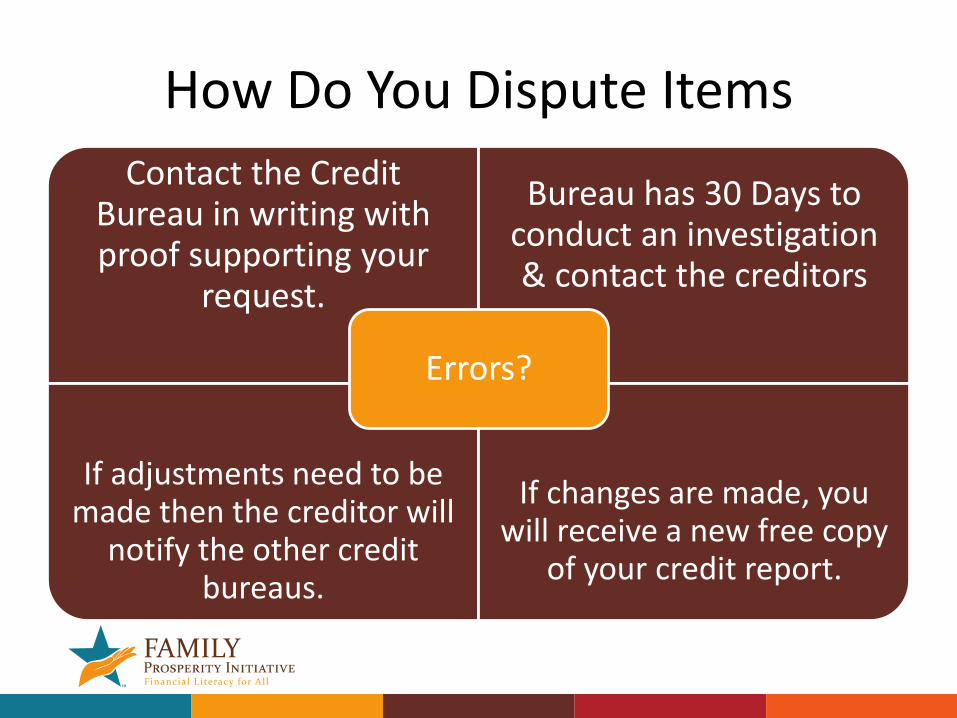

Disputing the Credit Report

How Do You Dispute Items

Contact the Credit Bureau in writing with proof supporting your

request.

Bureau has 30 Days to conduct an investigation & contact the creditors

If adjustments need to be made then the creditor will

notify the other credit bureaus.

If changes are made, you will receive a new free copy

of your credit report.

Errors?

Additional Help on Correcting Your Report?

File an online complaint:

http://bit.ly/KR48P9

Sample dispute letter:

http://bit.ly/2dutOkz

www.ftc.gov

idtheft.utah.gov/

consumerfinance.gov

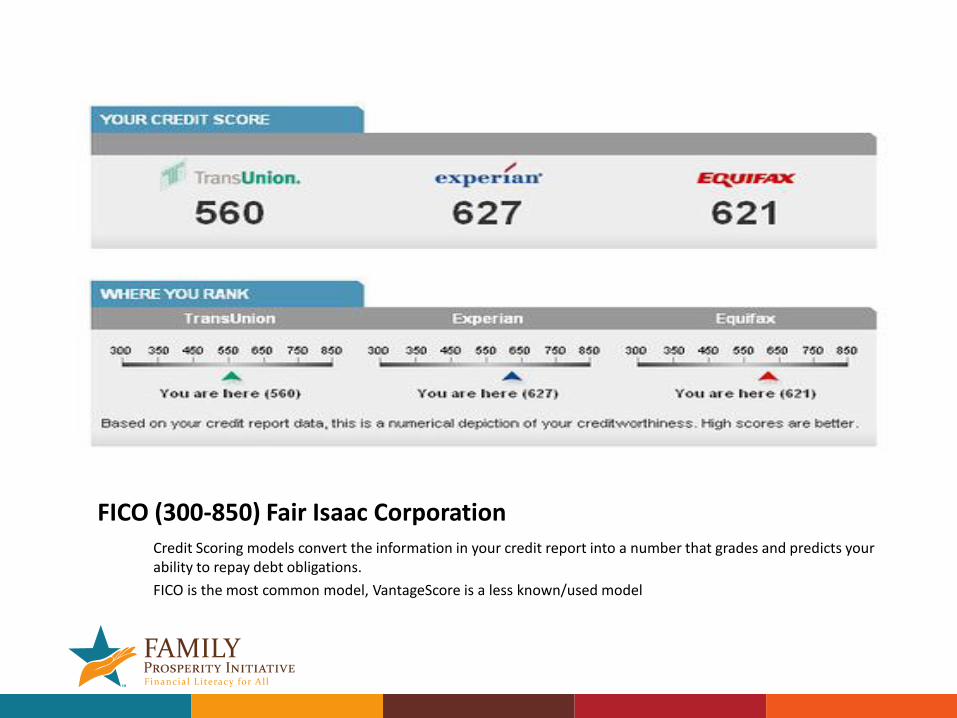

CREDIT SCORES

Credit Scores

Score Range What does that mean? 300-629 Poor Credit Hard to get a loan, may

have to pay high % rates

630-689 Average Credit Easier to qualify for a loan; May have a higher % rate

690-719 Good Credit Can qualify for credit, but not the best rates

720-850 Excellent Credit Qualify for lower % rates and rewards cards

Interest Rate Comparison

Loan Type Credit Rating Interest Rate

Auto Loan (Used) Best 2.99-3.60%

Auto Loan (Used) Middle 4-7.99%

Auto Loan (Used) Poor 8-25%

FICO (300-850) Fair Isaac CorporationCredit Scoring models convert the information in your credit report into a number that grades and predicts your ability to repay debt obligations.

FICO is the most common model, VantageScore is a less known/used model

Impact on Your FICO ScoreConsumer A Consumer B Consumer C

Beginning FICO Score 680 720 780

What happens after:

30 days late on mortgage 600-620 630-650 670-690

90 days late on mortgage 600-620 610-630 650-670

Short sale/deed-in-lieu/settlement (no deficiency balance)

610-630 605-625 655-675

Short sale (with deficiency balance) Still owe money on mortgage

575-595 570-590 620-640

Foreclosure 575-595 570-590 620-640

Bankruptcy 530-550 525-545 540-560

Research was conducted on select consumer profiles, FICO Banking Analytics Blog

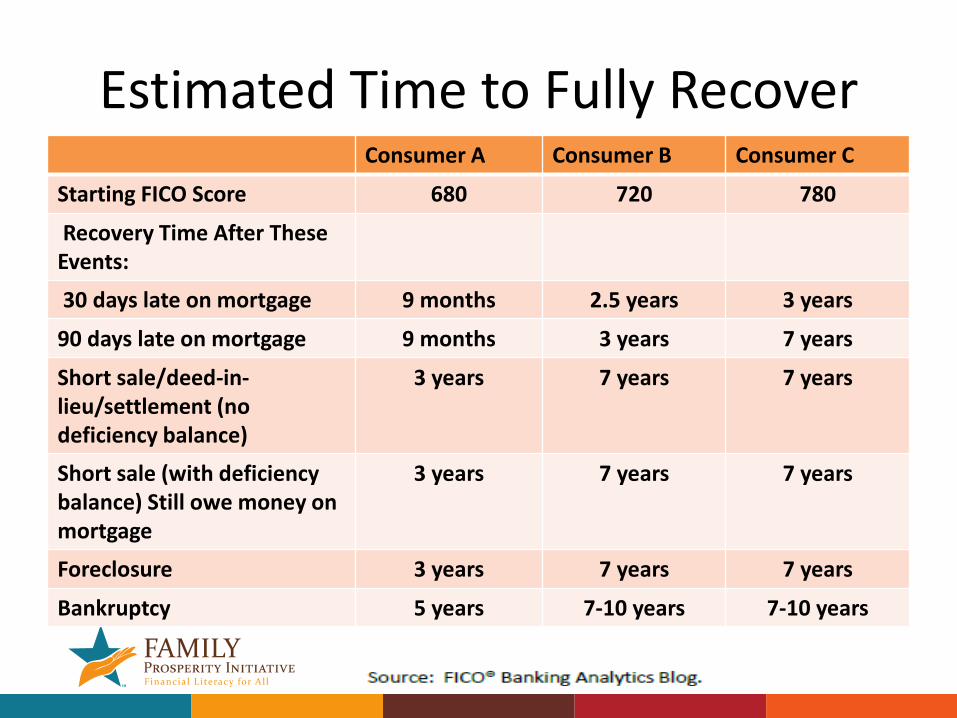

Estimated Time to Fully RecoverConsumer A Consumer B Consumer C

Starting FICO Score 680 720 780

Recovery Time After These Events:

30 days late on mortgage 9 months 2.5 years 3 years

90 days late on mortgage 9 months 3 years 7 years

Short sale/deed-in-lieu/settlement (no deficiency balance)

3 years 7 years 7 years

Short sale (with deficiency balance) Still owe money on mortgage

3 years 7 years 7 years

Foreclosure 3 years 7 years 7 years

Bankruptcy 5 years 7-10 years 7-10 years

How long will the information stay on my Credit Report?

Type of Account How Long Will It Stay?

Open accounts in good standing (paid on time) Forever

Closed accounts in good standing 10 years

Late/missed payments 7 years

Collections 7 years

Civil Judgments 7 years

Chapter 7 Bankruptcy 10 years

Chapter 13 Bankruptcy 7 years

Unpaid tax liens 10 years

Paid tax liens 7 years

Credit inquiries 2 years

Payment History35%

Amounts Owed30%

Credit Age 15%

Credit Inquiries 10%

Types of Credit10%

FICO Score

Payment History

Amounts Owed

Length of Credit History

New Credit

Types of Credit

Thank [email protected]@slcolibrary.org

This program is made possible by a grant from the FINRA Investor Education Foundation through Smart investing@your library®, a partnership with the American Library Association.

http://www.slcolibrary.org/smartinvesting