Credit Card Accountability, Responsibility, and Disclosure Act of 2009 Credit CARD Act of 2009.

26

Credit Card Accountability, Responsibility, and Disclosure Act of 2009 Credit CARD Act of 2009

-

Upload

kelly-anis-lang -

Category

Documents

-

view

218 -

download

0

Transcript of Credit Card Accountability, Responsibility, and Disclosure Act of 2009 Credit CARD Act of 2009.

Credit Card Accountability, Responsibility, and Disclosure Act of 2009

Credit CARD Act of 2009

90 day Effective Date

• Section 101(a) Advance Notice of Rate Increase. Creditors must provide a 45-day advance notice of:– Rate increase unless exception applies (time expiration,

variable rate, workout arrangement)– “Significant change” to cardholder agreement with right to

cancel and pay off over time under permissible repayment method

• Section 106(b) Length of Billing Period. Creditors must adopt reasonable procedures to ensure that periodic statements are mailed or delivered no later than 21 days before the dues date.

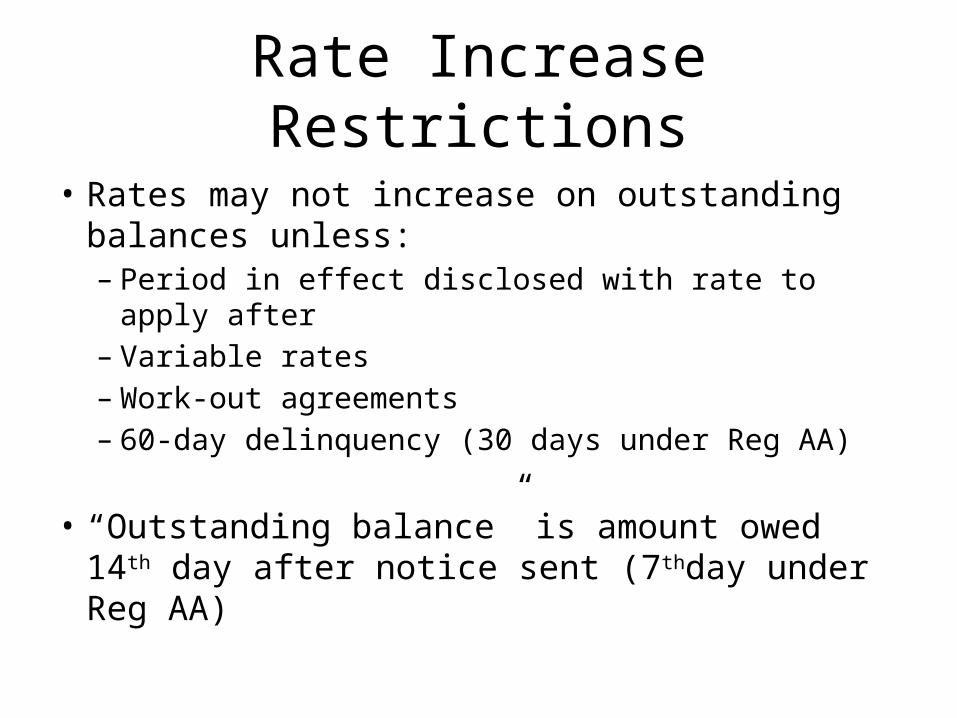

Rate Increase Restrictions

• Rates may not increase on outstanding balances unless:– Period in effect disclosed with rate to apply after– Variable rates– Work-out agreements– 60-day delinquency (30 days under Reg AA)

• “Outstanding balance” is amount owed 14th day after notice sent (7thday under Reg AA)

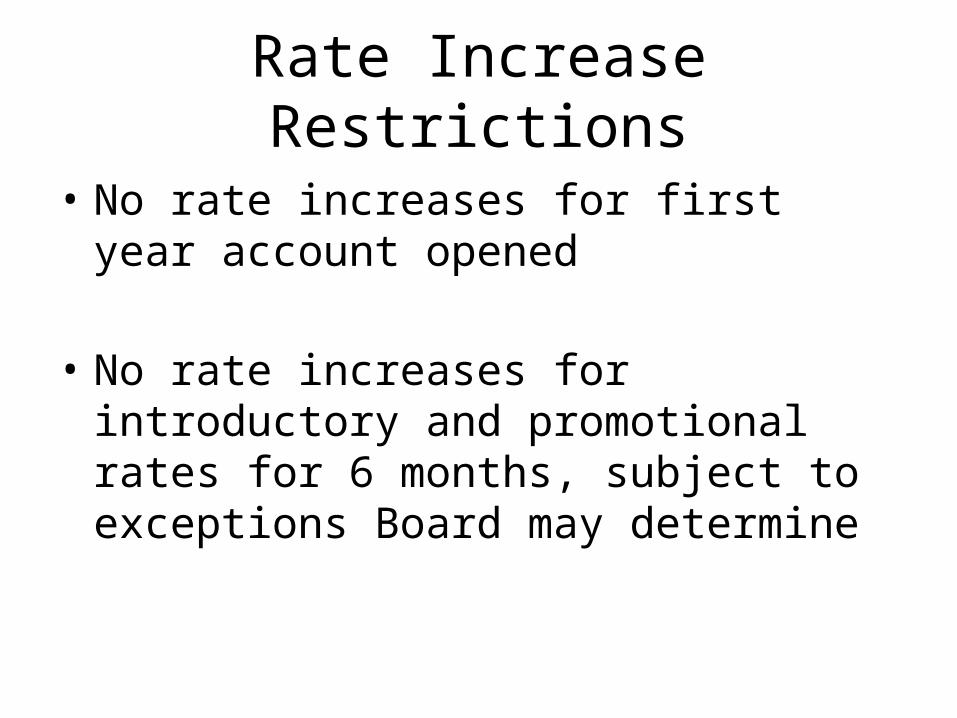

Rate Increase Restrictions

• No rate increases for first year account opened

• No rate increases for introductory and promotional rates for 6 months, subject to exceptions Board may determine

Interest Rate Reduction After Increase

• If increase rate based on certain factors must consider such factors when later considering rate reduction. Must:– Have “reasonable methodologies for assessing

factors– Review increases since Jan. 1, 2009 every 6 mos.– Reduce rate where indicated– Provide with 45 day advance notice reason for any

increase

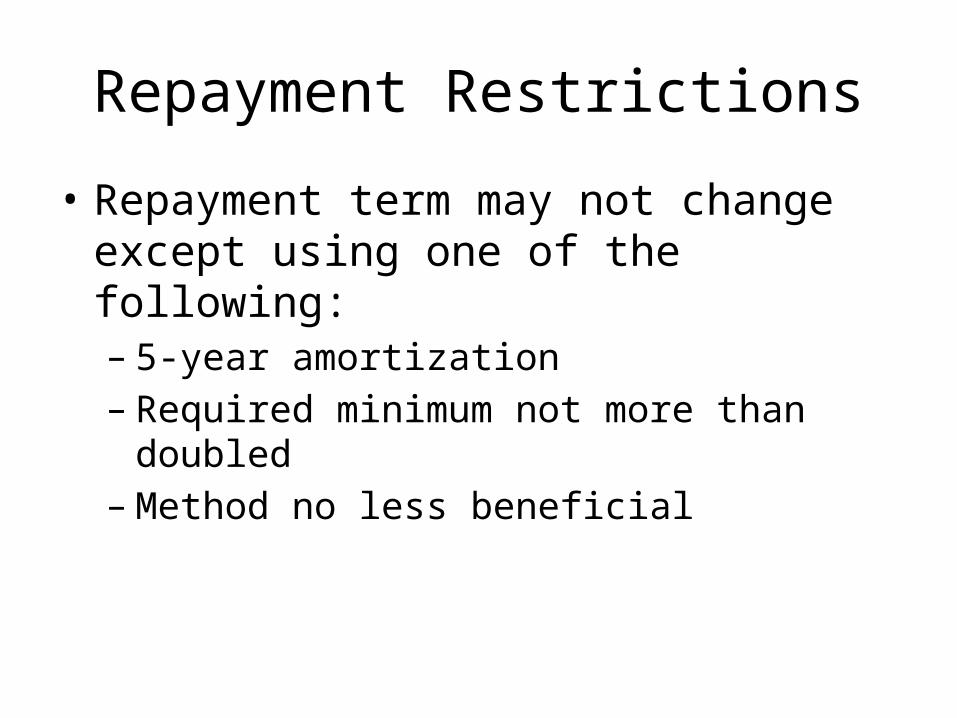

Repayment Restrictions

• Repayment term may not change except using one of the following:– 5-year amortization– Required minimum not more than doubled– Method no less beneficial

Interest-free Period Restrictions

• Prohibits:– Two-cycle billing– One-cycle billing

Over-the Limit Fees

• Card issuers may not charge OTL fees unless the customer opts in

• Statements with such fees must provide notice of right to rescind opt-in

• One OTL fee per cycle• Regulations to prevent manipulation of credit

limits designed to increase OTL fees or other penalty fees

Fee Limits on Payments

• Issuers may not impose fee for payment regardless of method

• Fees permitted for expedited payment service “by a service representative of the creditor”

Limitations on Penalty Fees

• Penalty fees (late payment, over-the-limit, and others) must be:– Reasonable and– Proportional

* No civil liability

Repayment Restrictions

• Repayment term may not change except using one of the following:– 5-year amortization– Required minimum not more than doubled– Method no less beneficial

Payment Allocation

• After minimum payment amount, payments must apply to balance with highest rate first (high to low)

• For deferred interest plans, entire amount in excess of minimum must be applied during the last two billing cycles preceding expiration date of deferred interest period

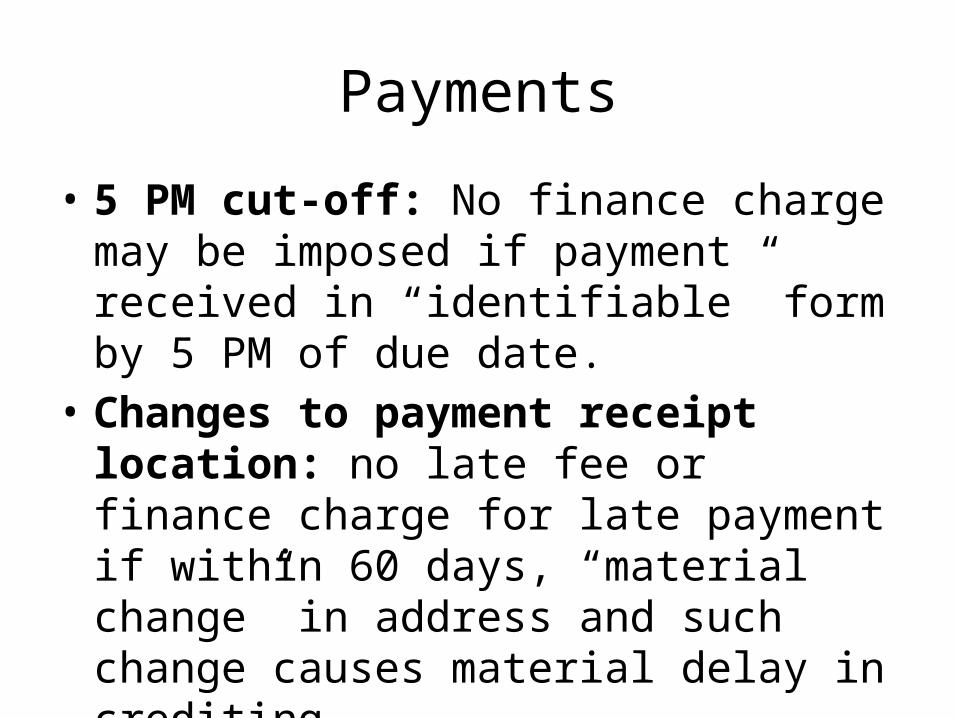

Payments

• 5 PM cut-off: No finance charge may be imposed if payment received in “identifiable” form by 5 PM of due date.

• Changes to payment receipt location: no late fee or finance charge for late payment if within 60 days, “material change” in address and such change causes material delay in crediting

Periodic Statements

• Due date must be same day each month• Billing statements must be sent 21 days prior

to due date

Ability to Repay

• Card issuers may not open account unless the card issuer considers “the ability of the consumer to make the required payments under the terms of such account.”

* No civil liability

“Fee Harvester” Cards

• No additional fees (other than penalty fees) from credit line if fees exceed 25 percent of total credit line in first year of account

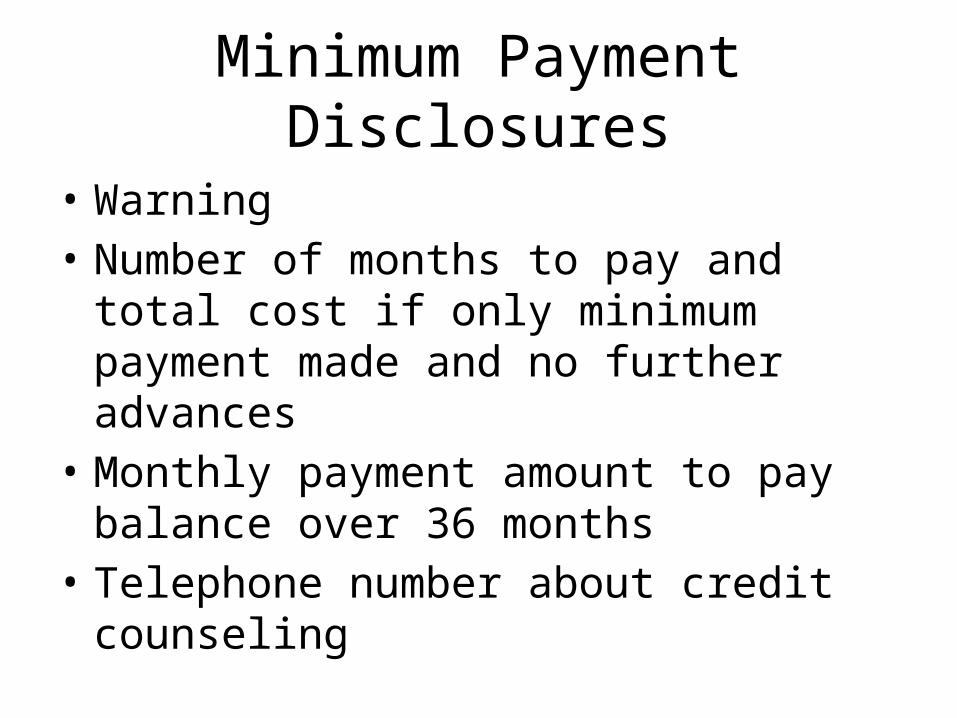

Minimum Payment Disclosures

• Warning• Number of months to pay and total cost if only

minimum payment made and no further advances

• Monthly payment amount to pay balance over 36 months

• Telephone number about credit counseling

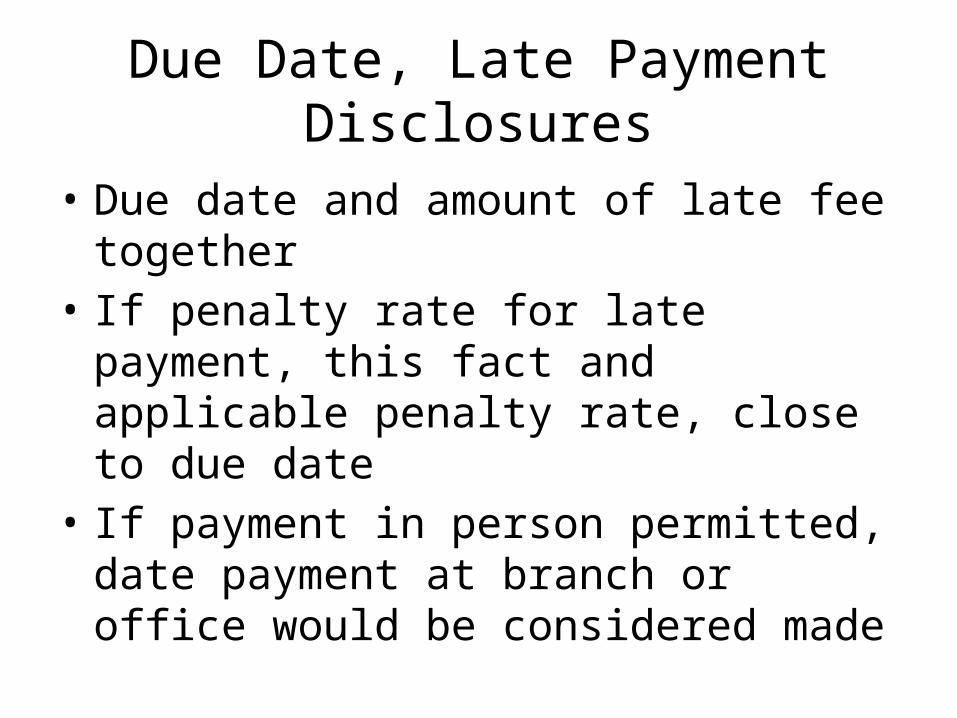

Due Date, Late Payment Disclosures

• Due date and amount of late fee together• If penalty rate for late payment, this fact and

applicable penalty rate, close to due date• If payment in person permitted, date payment

at branch or office would be considered made

“Renewal” Disclosures

• If any term changed since date of last renewal without prior disclosures 30 days prior to renewal disclose:– Date account will expire if not renewed– Information about APR, annual fee, interest-free

period, calculation method– Method to terminate continued credit availability

Internet Posting of Agreements

• Issuers must post on website agreement between issuer and consumer

• Provide Board every agreement on website• Board to establish website as central

repository for all agreements

Restrictions on Young Consumers

• For those under 21:• Written application• Application must include:

– Signature of an eligible co-signer or – Information showing “independent means” to repay

– Opt-in to prescreened offers– Prohibition against limit increases without

cosigner

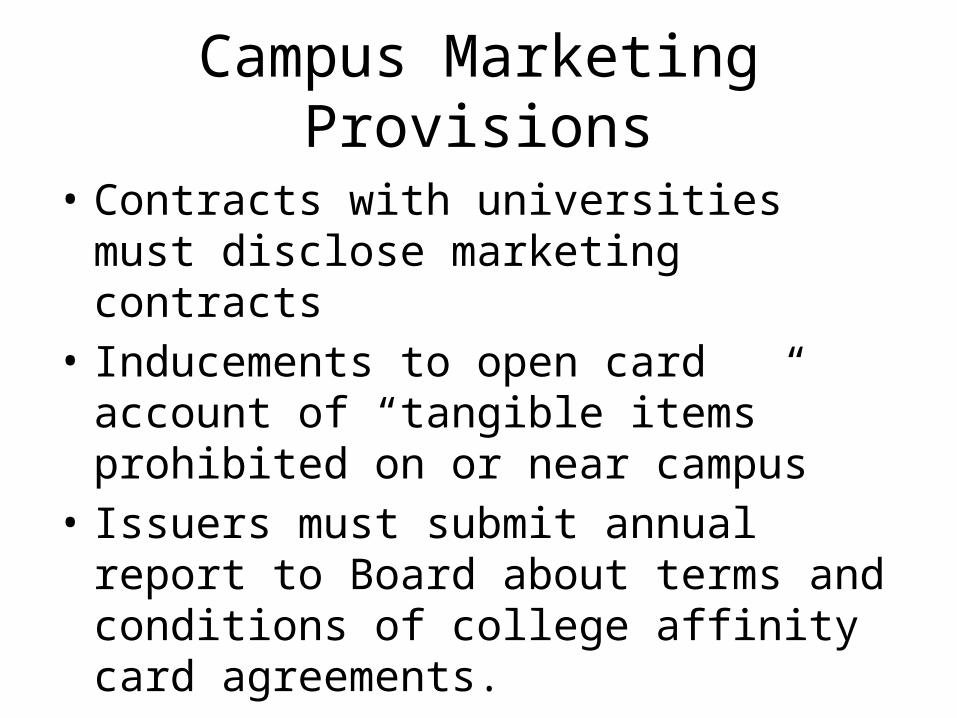

Campus Marketing Provisions

• Contracts with universities must disclose marketing contracts

• Inducements to open card account of “tangible items” prohibited on or near campus

• Issuers must submit annual report to Board about terms and conditions of college affinity card agreements.

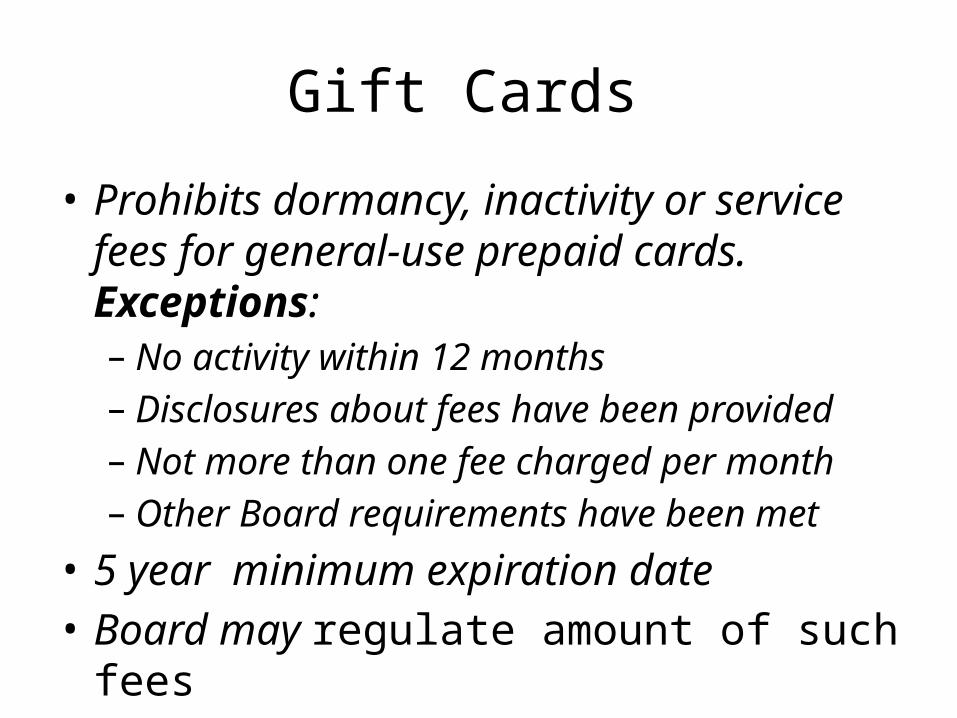

Gift Cards

• Prohibits dormancy, inactivity or service fees for general-use prepaid cards. Exceptions:– No activity within 12 months– Disclosures about fees have been provided– Not more than one fee charged per month– Other Board requirements have been met

• 5 year minimum expiration date• Board may regulate amount of such fees

Credit CARD Act Effective Dates

• Generally 9 months after enactment• Exceptions:– 90 days for advance notices of change in terms

and length of billing period– 15 months for interest rate reduction, reasonable

penalty fees, gift cards

Increase in Penalties

• Increases the minimum statutory damages to $500 and maximum to $5,000

• Increased damages without any specific limit if established pattern or practice of such violation

Selected Studies

• Interchange fees• Review of consumer credit card market• Whether reduced credit limits or higher interest

rates based on location or identify of merchant, credit transactions of consumer, and identify of mortgage lender

• Review of use of credit cards by small businesses and terms of agreements

• Marketing of products (e.g., debt cancellation)