CREATE OR BUY OMPARATIVE ANALYSIS OF LIQUIDITY AND...

26

1 CREATE OR BUY: A COMPARATIVE ANALYSIS OF LIQUIDITY AND TRANSACTION COSTS FOR SELECTED U.S. ETFS MILAN BORKOVEC AND VITALY SERBIN October 25, 2012 Abstract Our examination of twelve popular Exchange Traded Funds (ETFs) reveals that ETFs exhibit qualitatively different liquidity and cost characteristics than common stocks. The limit order book for ETFs is deeper than that of common stocks with similar daily share volume, price, spread, and volatility characteristics, especially at price levels immediately surrounding the prevailing mid-quote. The differences in trading mechanisms and liquidity provision between ETFs and common stocks affect transaction costs. In order to reflect these differences, an appropriate transaction cost model should be properly calibrated and parameterized. In addition, it should also consolidate the entire accessible ETF liquidity on the secondary market and through the creation/redemption procedure. We demonstrate that looking at the cost estimates for trading the underlying constituents of ETFs provides additional clarity with respect to the “true” cost of an ETF. Finally, our comparison of ETF and basket costs in conjunction with a look at creation/redemption fees indicates the need for monitoring relative ETF liquidity, as the optimal switching points between trading an ETF and creating/redeeming vary widely across ETFs and trading styles. MILAN BORKOVEC is Head of Financial Engineering at ITG, 100 High Street, Boston MA 02110, Tel: (617) 692- 6733; e-mail: [email protected] VITALY SERBIN is Manager of Financial Engineering’s Portfolio Analytics Research Group at ITG, 100 High Street, Boston MA 02110, Tel: (617) 692-6746; e-mail: [email protected] [email protected] The information contained herein has been taken from trade and statistical services and other sources we deem reliable, but we do not represent that such information is accurate or complete, and it should not be relied upon as such. The analyses discussed herein are derived from aggregated ITG client data and are not meant to guarantee

-

Upload

vuongkhanh -

Category

Documents

-

view

213 -

download

1

Transcript of CREATE OR BUY OMPARATIVE ANALYSIS OF LIQUIDITY AND...

1

CREATE OR BUY: A COMPARATIVE ANALYSIS OF LIQUIDITY AND TRANSACTION COSTS FOR

SELECTED U.S. ETFS

MILAN BORKOVEC AND VITALY SERBIN

October 25, 2012

Abstract

Our examination of twelve popular Exchange Traded Funds (ETFs) reveals that ETFs exhibit qualitatively different liquidity and cost characteristics than common stocks. The limit order book for ETFs is deeper than that of common stocks with similar daily share volume, price, spread, and volatility characteristics, especially at price levels immediately surrounding the prevailing mid-quote. The differences in trading mechanisms and liquidity provision between ETFs and common stocks affect transaction costs. In order to reflect these differences, an appropriate transaction cost model should be properly calibrated and parameterized. In addition, it should also consolidate the entire accessible ETF liquidity on the secondary market and through the creation/redemption procedure. We demonstrate that looking at the cost estimates for trading the underlying constituents of ETFs provides additional clarity with respect to the “true” cost of an ETF. Finally, our comparison of ETF and basket costs in conjunction with a look at creation/redemption fees indicates the need for monitoring relative ETF liquidity, as the optimal switching points between trading an ETF and creating/redeeming vary widely across ETFs and trading styles.

MILAN BORKOVEC is Head of Financial Engineering at ITG, 100 High Street, Boston MA 02110, Tel: (617) 692-6733; e-mail: [email protected]

VITALY SERBIN is Manager of Financial Engineering’s Portfolio Analytics Research Group at ITG, 100 High Street, Boston MA 02110, Tel: (617) 692-6746; e-mail: [email protected]@itg.com

The information contained herein has been taken from trade and statistical services and other sources we deem reliable, but we do not represent that such information is accurate or complete, and it should not be relied upon as such. The analyses discussed herein are derived from aggregated ITG client data and are not meant to guarantee

Create or Buy: A Comparative Analysis of Liquidity and Transaction Costs for Selected U.S. ETFs

2

future performance or results. This report is for informational purposes and is neither an offer to sell nor a solicitation of an offer to buy any security or other financial instrument. This report does not provide any form of advice (investment, tax, or legal). No part of this report may be reproduced or retransmitted in any manner without permission. All trademarks, service marks, and trade names not owned by ITG are the property of their respective owners. The Frank Russell Company is not affiliated with ITG. Russell™ is a trademark of the Frank Russell Company. The Russell 1000®, Russell 2000®, and Russell 3000® indices are trademarks of the Frank Russell Company. Certain Index Data contained herein is the property of MSCI. Copyright © MSCI 2012. All Rights Reserved. Without prior written permission of MSCI, this information and any other MSCI intellectual property may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used to create any financial instruments or products or any indices. This information is provided on an "as is" basis, and the user of this information assumes the entire risk of any use made of this information. Neither MSCI nor any third party involved in or related to the computing or compiling of the data makes any express or implied warranties, representations or guarantees concerning the MSCI index-related data, and in no event will MSCI or any third party have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) relating to any use of this information. © 2012 Investment Technology Group. All rights reserved. Compliance # 50312-22030

Create or Buy: A Comparative Analysis of Liquidity and Transaction Costs for Selected U.S. ETFs

3

Attention to transaction cost considerations has risen in recent years in both

financial theory and practice. While for brokers and dealers transaction costs constitute

the bread and butter of their daily routine, the significance of transaction costs for buy

side market participants is often misunderstood or is interpreted too narrowly.

Traditionally, the impact of transaction costs, as applied to buy-side practices, is

summarized by one number: the difference between so-called “paper” and “net” returns.

The former refers to investment returns calculated without accounting for trading costs,

while the latter includes the cost of trading. In other words, the classical view of

transaction costs is that they eliminate part of the notional or “paper” return of an

investment strategy and, therefore, should be controlled at the trading stage. Some recent

papers demonstrate that accounting for transaction costs at the level of portfolio

construction could lead to better investment allocations. Borkovec et al. [2010] show that

cost-aware portfolio construction yields portfolios with higher net returns and lower

variances. Brandes, Domowitz and Serbin [2011] extend this evidence and show that the

inclusion of stock-specific transaction costs at the portfolio construction stage permits

higher turnover levels and allows portfolio manager to run larger portfolios without

facing detrimental cost effects.

Exchange-traded funds (ETFs) are relatively new investment tools that are similar

to mutual funds, but trade more like stocks. In contrast to mutual funds, ETFs can be

bought or sold at any time during the trading day. This is one of the main drivers of

ETF’s popularity and importance in the investment community. BlackRock [2011]

estimates that ETF turnover on all US exchanges, as a proportion of all equity turnover,

has been oscillating between 25 and 35% for most of the period between January 2008

and June 2011. Some of the most popular ETF strategies, including cash equitization and

hedging, rely on accurate index tracking, available liquidity and low cost. According to a

recent TABB Group report, see Berke [2009], “seven of the ten largest [ETFs] are broad

market indices, including the S&P500 index, the MSCI EAFE Index, the Russell2000

index and the Vanguard Total Stocks Market index. Together they hold 81% of the assets

in the top ten ETFs”. As important as it is, the tracking error of an ETF, with respect to a

broad market index, is only one of the top institutional priorities when it comes to

Create or Buy: A Comparative Analysis of Liquidity and Transaction Costs for Selected U.S. ETFs

4

selecting an ETF product. According to a Greenwich Associates [2011] survey, 61% of

institutional funds and 79% of asset managers cite liquidity as one of the top ETF

selection criteria. Managing the ETF trading process requires knowledge and effort from

investors. Failure to tap available ETF liquidity, or to fully understand the nature of ETF

costs, severely limits the usefulness of ETFs in a typical buy-side investment application.

These facts, and the steady rise of ETF trading volume in the past decade, clearly suggest

the need to better understand the liquidity characteristics and trading costs of ETFs and

their underlying securities.

The purpose of this paper is to explore the liquidity and trading costs of a selected

group of ETFs that track popular U.S. equity indices. We adhere to the accepted

definition of liquidity as the “ability to transact quickly without exerting a material effect

on prices”1. It is important to bear in mind that by construction, the liquidity of an ETF is

closely tied to the liquidity of its underlying basket, since the net asset value (NAV) of an

ETF reflects the value of the underlying securities at any time. In other words, although

an ETF appears to “trade like a stock”, its liquidity is determined not only by supply and

demand for the ETF shares, but also by the liquidity of the underlying securities via the

creation/redemption mechanism. Not taking the creation/redemption process into

consideration when assessing the liquidity and trading cost of an ETF can severely

understate its true liquidity. As a result, it can inadvertently reduce the ETF universe

considered for inclusion into a portfolio and inflate the estimated implementation

shortfall cost of ETF trading in general.

This ETF-basket duality is only one corollary of the fact that ETFs are derivative

products whose liquidity and trading characteristics are affected by numerous factors not

commonly captured within a single security market microstructure framework. Another

distinguishing feature of ETFs is that their liquidity and price determination mechanism

can be strongly affected by trading activity in related derivate products such as futures

and options. Some ETF transactions, such as exchange for physicals (or EFPs), leave no

mark on the ETF price, and can often occur outside of an exchange altogether. While

those complications exist for common stocks as well, they are more pronounced for

ETFs, especially for those that track standard indexes, for which the trading volume in

futures, options and EFPs is typically much higher than for single stocks.

Create or Buy: A Comparative Analysis of Liquidity and Transaction Costs for Selected U.S. ETFs

5

Investigating the links between different derivatives markets in the context of

their effect on ETF trading costs is outside of the scope of this paper. We limit ourselves

to a more manageable task of documenting the differences between the liquidity profiles

of ETFs and single stocks from the point of view of an investor who is determined to

trade ETFs, and who wants to know if the trading practices that work for common stocks

still apply. We start by being agnostic about any links between ETFs and the underlying

baskets and treat ETFs as they were regular stocks. Later, we take an in-depth look at the

relationship between liquidity of ETFs in the secondary market and the liquidity of their

underlying baskets.

Our main findings are as follows.

ETFs exhibit qualitatively different liquidity and cost characteristics than common

stocks with comparable volume, volatility, spread and price levels. The limit order

book (LOB) for ETFs is deeper, especially at the levels immediately surrounding the

midquote. This is true even without accounting for implicit liquidity available via the

underlying basket.

The creation and redemption process is crucial for accessing the entire ETF liquidity.

The differences in trading mechanisms and liquidity characteristics result in disparate

transaction costs between ETFs and common stocks. Nevertheless, we see that the

liquidity in the secondary market remains an important determinant of ETF costs.

In order to reflect these differences, a good transaction cost model needs to be

properly calibrated and parameterized. Failure to do so may lead to inaccurate

estimates of ETF trading costs. For instance, the model design should reflect that the

permanent price impact costs of most ETF trades are significantly lower than the

price impact costs for a matched common stock. It also should reflect that ETF

liquidity is determined not only on the secondary market but also through other

means such as the creation/redemption process. In addition, the model calibration

should be performed on a subsample of a database which contains only ETF trades.

These points are illustrated utilizing the newly developed ITG’s Smart Cost Estimator

(SCE) model; however, they hold true for any quantitative transaction cost model.

Create or Buy: A Comparative Analysis of Liquidity and Transaction Costs for Selected U.S. ETFs

6

Looking jointly at the cost estimates of ETFs and the underlying baskets provides

additional clarity with respect to the “true” cost of an ETF. We argue that these cost

estimates can be utilized to derive upper and lower bounds of the “true” average

costs. These bounds could be interpreted as limits to arbitrage that could be

performed by authorized participants (APs).

The comparison of ETF and basket costs in conjunction with a look at

creation/redemption fees suggests that it is important to monitor relative ETF

liquidity, as the optimal switching points between trading an ETF and

creating/redeeming the underlying basket can vary widely across ETFs.

This paper is organized as follows. In the next section, we discuss ITG’s Limit

Order Book (LOB) database and present ITG’s Smart Cost Estimator (SCE) model.

Section 3 introduces the sample of ETFs used in this study, along with their basic trade-

related statistics. Section 4 presents the main results of our ETF liquidity and trading cost

analysis. Section 5 extends the analysis by comparing the costs of trading ETFs with the

cost of creation/redemption of the underlying basket of securities. Section 6 summarizes

our conclusions.

Transaction Cost Estimates and Data

Cost estimates for any security vary widely depending on a multitude of factors,

such as order size, time of day, prevailing market conditions (buy/sell imbalance,

volatility, volume and spread), the rebate structure of the exchange, and the desired

immediacy of order execution, among others. A good cost estimator should take most of

these factors into account, usually at the expense of making assumptions on the

functional form of the dependencies and on client preferences.

In order to abstract from the modeling assumptions, we begin by directly

examining the liquidity profiles of ETFs utilizing the consolidated LOB aggregated from

NYSE, NASDAQ, ARCA, BATS, as well as the NASDAQ OMX BX facility. The size

and distribution of LOB liquidity across different price levels reveals disparities between

ETFs and common stocks, and offers clues to the sources of differences in realized

Create or Buy: A Comparative Analysis of Liquidity and Transaction Costs for Selected U.S. ETFs

7

trading costs. In addition to measuring depth sizes at different price levels, we compute

the cost of instantaneous execution (“climbing the book”) as an aggregated liquidity

measure.

The proliferation of electronic trading results in the majority of large orders being

executed algorithmically via a strategy that usually aims at minimizing overall

implementation shortfall cost. In this paper, we use ITG’s newly developed Smart Cost

Estimator (SCE) model to simulate this process and to generate associated cost estimates.

SCE uses as its inputs the order attributes (size, date, and time stamp), security

characteristics (type, expected liquidity, volatility, and daily average spread), recently

observed market conditions (deviations of volatility, volume, and spread from historical

patterns), and the traders’ subjective market sentiment and its persistence (expressed

through the magnitude of trade imbalance). In contrast to a static trading cost estimator,

the SCE model has the capability to dynamically update execution trajectories based on

the market response to order flow and the observed market conditions. The SCE cost

estimates presented in this document are obtained under the assumption that the trader’s

subjective expectation of future trade imbalances is neutral (no directional prediction of

market sentiment).

The SCE model is calibrated for various market conditions using ITG’s Peer

Analysis™ database, which contains execution details for more than 33mln orders filled

by more than 140 institutional clients within the time period of March 2010 to February

2012. We define an order as a cluster of trades that occur on the same date, in the same

security and direction (buy, sell, short, or cover), have the same broker and client IDs,

and identical arrival time stamps corresponding to the time when the package was sent by

a trading desk to a broker for execution. This fairly standard methodology allows us to

identify the unit of analysis granular enough to distinguish the clusters of trades

performed by different brokers, or by the same broker on behalf of different ITG Peer

Analysis™ clients.

Several key SCE components and parameters are estimated and calibrated

separately for ETFs to reflect the distinct nature of those securities. For instance, the

permanent price impact, which is estimated directly from the ITG’s Peer Analysis™

Create or Buy: A Comparative Analysis of Liquidity and Transaction Costs for Selected U.S. ETFs

8

database, is significantly lower for ETFs than for common stocks. We also explicitly

incorporate the extra available liquidity of the underlying basket in our model. More

details on SCE’s methodology and definitions can be found in Borkovec et al. [2011].

ETF Universe

The sample of equity ETFs utilized for the study is selected on the basis of

practical relevance and ensuring a fair representation of different liquidity categories and

market segments. Where possible, we select ETFs which track the same index, but have

different liquidity characteristics (for instance, SPY, IVV, VOO and RSP track the

S&P500 index). There are twelve ETFs in our sample, all of them having US-only

constituents. Five ETFs track large cap indexes (S&P500 and Russell 1000), three mid-

cap indexes (S&P400 and MSCI US Mid Cap 450), and four small-cap indexes (S&P600,

Russell 2000, Russell Microcap and MSCI US Small Cap 1750). Our ETF sample also

allows for a comparison of trading costs across ETFs supplied by different vendors.

The liquidity categories utilized in the paper are based on the 21-day median daily

trading volume (MDV) in the secondary market. Exhibit 1 reports the thresholds used for

the classification and the selected ETFs falling into each liquidity group.

Exhibit 1. Liquidity Thresholds for ETFs

Liquidity Category MDV Thresholds Selected ETFs

Very Liquid > 10 mln shares SPY, IWM

Liquid 1.5..10 mln shares IVV, MDY

Medium Liquidity 0.2..1.5 mln shares VOO, IWB, RSP,

IJH, IJR, VB

Illiquid < 0.2 mln shares VO, IWC

Exhibit 2 provides descriptive and trade-related statistics for selected ETFs.

Overall, there appears to be a positive relationship between the fund’s inception year and

its secondary market volume, which supports the notion of a first-mover advantage. The

creation/redemption fees for all ETFs are $500, regardless of the number of units raised,

with a few exceptions. Those exceptions seem to be historical artifacts, as higher

Create or Buy: A Comparative Analysis of Liquidity and Transaction Costs for Selected U.S. ETFs

9

creation/redemption fees belong to ETFs which were incepted prior to 2000 (except for

Guggenheim’s RSP). Not surprisingly, the spread values of the ETFs are strongly

correlated with their corresponding liquidity group: very liquid ETFs have an average

spread of 1 cent, followed by average spreads for liquid ETFs of 1.43 cents, medium

liquidity ETFs of 1.62 cents and illiquid ETFs of 3.25 cents. Daily volatilities range

between 0.7 and 1.2%, and are roughly proportional to the volatilities of the underlying

indexes.

Exhibit 2. Summary Profiles for ETFs Selected

Price is the official closing price on February 28, 2012. MDV, daily volatility and spread are the 21-day median daily share volume, 60-day average historical daily volatility and the 5-day time-weighted average spread on February 28, 2012, respectively. The number of shares in one creation redemption unit for all ETFs in our sample is 50,000 shares with the exception of MDY (25,000 shares), VO and VB (both 100,000 shares). Creation/redemption fees for each ETF are gathered from SEC filing.

ETF Index Provider Inception Year

# Stocks

LiquidityGroup

MDV (‘000)

Price ($)

Volatility (%, day)

Spread(cents)

Creation/redempti

on fee SPY S&P500

Large Cap SSGA 1993 500 Very

Liquid 115,800 137.56 0.8 1.0 $3000

IVV S&P500 Large Cap

iShares 2000 500 Liquid 3,100 138.05 0.7 1.2 $500

VOO S&P500 Large Cap

Vanguard 2010 500 Medium Liquidity

370 62.93 0.8 1.6 $500

IWB Russell1000 Large Cap

iShares 2000 976 Medium Liquidity

1,070 76.29 0.8 1.1 $500

RSP S&P500 Equal Weights

Large Cap

Guggenheim

2003 500 Medium Liquidity

450 51.22 0.9 1.4 $2000

MDY S&P400 Mid Cap

SSGA 1995 400 Liquid 2,020 179.02 1.0 2.1 $3000

IJH S&P400 Mid Cap

iShares 2000 400 Medium Liquidity

680 98.29 1.0 2.1 $500

VO MSCI US Mid Cap 450 Index

Vanguard 2004 448 Illiquid 160 80.53 0.9 3.4 $500

IWM Russell2000 Small Cap

iShares 2000 1,944 Very Liquid

40,400 82.28 1.2 1.0 $500

IJR S&P600 Small Cap

iShares 2000 600 Medium Liquidity

1,180 75.5 1.2 1.1 $500

VB MSCI US Small Cap

1750 Small Cap

Vanguard 2004 1,732 Medium Liquidity

370 77.93 1.1 2.4 $500

IWC Russell Microcap

iShares 2005 1,373 Illiquid 110 50.55 1.2 3.1 $500

Create or Buy: A Comparative Analysis of Liquidity and Transaction Costs for Selected U.S. ETFs

10

A substantial part of this paper is devoted to the comparison of liquidity and cost

characteristics of ETFs and common stocks. In order to accomplish this comparison, we

use a matching technique introduced in Huang and Stoll [1996]2. For each ETF, we select

five stocks that come closest to an ETF in terms of their median daily dollar volume

(MDDV) , price, historical volatility and spread on February 27, 2012 (displayed in

Exhibit 2), as well as on September 26, 20113. The latter date, which represents different

market conditions, was added as a robustness check for the results discussed in the next

sections. The average VIX during the two-week period in 2011 was 37.6 (high volatility),

and, during the two-week period in 2012, 18.1 (normal volatility).

LOB and SCE Comparative Cost Analysis for ETFs and Common

Stocks

We characterize the liquidity profile of the ETFs in our sample by looking at the

cumulative depth sizes and “climbing the book” costs for various price levels and trade

sizes. We compare these quantities across ETFs, as well as between an ETF and its

matched common stocks.

The results presented in this section are based on two weeks of data that span the

ten-day window from February 27 until March 9, 20124. All LOB statistics are computed

25 times daily for each trading day in our sample period (every 15min from 9:45am to

4:00pm) and then averaged across the two week period. We utilize ITG’s SCE to

calculate the expected costs corresponding to an optimal execution schedule for different

trade sizes. We compare the costs of trading the ETFs on the secondary market with the

costs of acquiring/selling the baskets of underlying stocks. SCE cost estimates are

calculated daily assuming a trading horizon of one day (starting at 9:30am) and then

averaged across the ten-day window.

LOB Liquidity for ETFs and the Matched Common Stocks

Create or Buy: A Comparative Analysis of Liquidity and Transaction Costs for Selected U.S. ETFs

11

Exhibit 3 shows the ask side of the LOB for SPY, around 10:00am on February

28, 2012, where the ask price levels of the LOB are a step function of the depth. The

cumulative depth across the first ten levels corresponds to approximately 570K shares.

Exhibit 3

To put the distribution of liquidity of the LOB into perspective and to allow a

comparison across securities, we normalize the cumulative depth sizes by the median

daily share volume (MDV) and/or the unit size of the corresponding ETF. In the example

shown in Exhibit 3, the normalized LOB depth on the first ten levels is

570K/115,800K*100% = 0.49% of MDV or 570K/50K = 11.4 units (the MDV of SPY is

defined in Exhibit 2). Exhibit 4 presents a comprehensive summary of these results for

the twelve selected ETFs and the corresponding averages for the matched common

stocks.

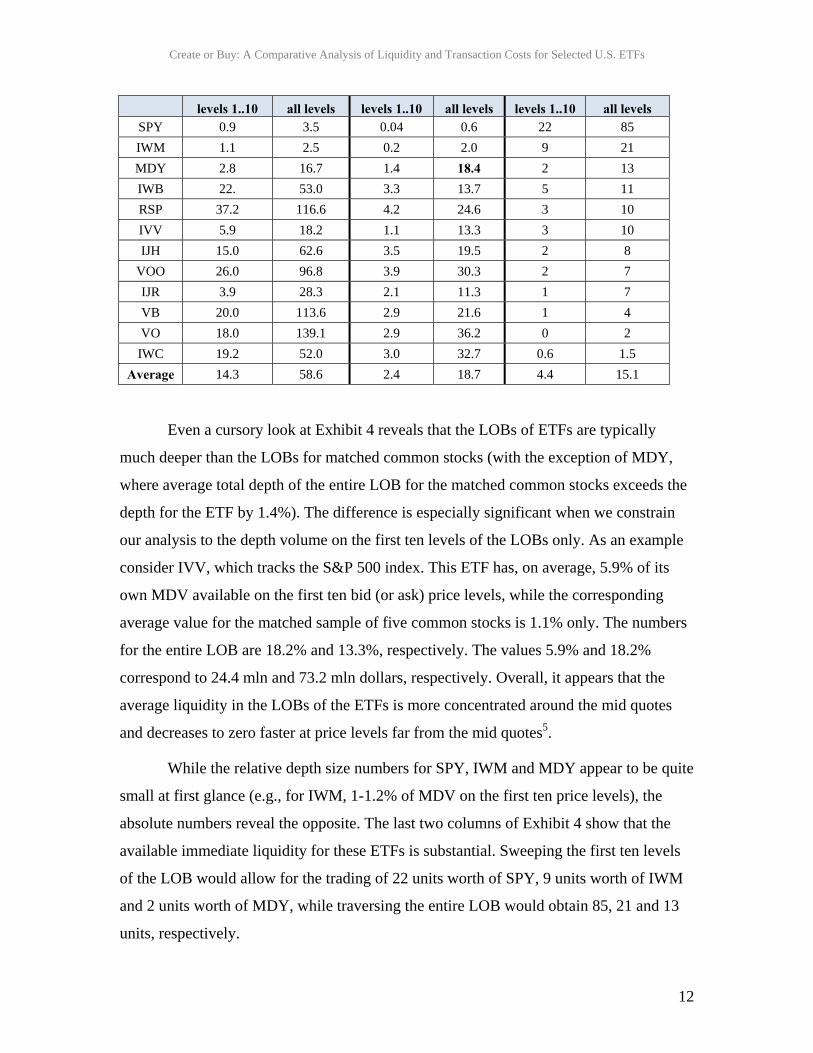

Exhibit 4: LOB Liquidity for ETFs and Matched Common Stocks

The rows are sorted in descending order by the number of units that can be raised by sweeping the entire LOB.

ETF

Cumulative Visible Depth, as % of MDV, ETF

Cumulative Depth, as % of MDV, matched

common stock

Average # of ETF Units that can be raised

Create or Buy: A Comparative Analysis of Liquidity and Transaction Costs for Selected U.S. ETFs

12

levels 1..10 all levels levels 1..10 all levels levels 1..10 all levels SPY 0.9 3.5 0.04 0.6 22 85

IWM 1.1 2.5 0.2 2.0 9 21

MDY 2.8 16.7 1.4 18.4 2 13

IWB 22. 53.0 3.3 13.7 5 11

RSP 37.2 116.6 4.2 24.6 3 10

IVV 5.9 18.2 1.1 13.3 3 10

IJH 15.0 62.6 3.5 19.5 2 8

VOO 26.0 96.8 3.9 30.3 2 7

IJR 3.9 28.3 2.1 11.3 1 7

VB 20.0 113.6 2.9 21.6 1 4

VO 18.0 139.1 2.9 36.2 0 2

IWC 19.2 52.0 3.0 32.7 0.6 1.5

Average 14.3 58.6 2.4 18.7 4.4 15.1

Even a cursory look at Exhibit 4 reveals that the LOBs of ETFs are typically

much deeper than the LOBs for matched common stocks (with the exception of MDY,

where average total depth of the entire LOB for the matched common stocks exceeds the

depth for the ETF by 1.4%). The difference is especially significant when we constrain

our analysis to the depth volume on the first ten levels of the LOBs only. As an example

consider IVV, which tracks the S&P 500 index. This ETF has, on average, 5.9% of its

own MDV available on the first ten bid (or ask) price levels, while the corresponding

average value for the matched sample of five common stocks is 1.1% only. The numbers

for the entire LOB are 18.2% and 13.3%, respectively. The values 5.9% and 18.2%

correspond to 24.4 mln and 73.2 mln dollars, respectively. Overall, it appears that the

average liquidity in the LOBs of the ETFs is more concentrated around the mid quotes

and decreases to zero faster at price levels far from the mid quotes5.

While the relative depth size numbers for SPY, IWM and MDY appear to be quite

small at first glance (e.g., for IWM, 1-1.2% of MDV on the first ten price levels), the

absolute numbers reveal the opposite. The last two columns of Exhibit 4 show that the

available immediate liquidity for these ETFs is substantial. Sweeping the first ten levels

of the LOB would allow for the trading of 22 units worth of SPY, 9 units worth of IWM

and 2 units worth of MDY, while traversing the entire LOB would obtain 85, 21 and 13

units, respectively.

Create or Buy: A Comparative Analysis of Liquidity and Transaction Costs for Selected U.S. ETFs

13

The distribution of the visible liquidity across multiple price levels of the LOB

indicates substantial differences between ETFs and common stocks. Yet, the evidence

above is mute on another important liquidity component: the spread. Therefore, we

combine the depth and spread values on all levels of the LOB and use the implied cost of

instantaneous execution as an aggregate measure of liquidity. As before, we compare this

liquidity metric across ETFs and across the matched common stocks. Exhibit 5 below

summarizes the results.

Exhibit 5: Instantaneous Average Costs for Trading ETFs and the Matched Sample

of Common Stocks

The rows are sorted in ascending order of the instantaneous costs in the second column (marked with ▲), i.e. the implied instantaneous costs of trading $1mln worth of each ETF on the secondary market. The “NA” values indicate that there is insufficient available visible depth in the LOB on average to execute the specified quantity.

ETF

Cost of immediate execution $1mln, bp

Cost of immediate execution $10mln, bp

ETF ▲ Matched ETF Matched

SPY 0.4 2.5 0.8 33.9 IWM 0.6 3.0 2.7 58.7 IVV 0.9 3.6 1.6 98.2 IWB 1.4 3.9 5 93.3 MDY 1.5 5.9 3.9 NA VOO 1.6 29.7 53 NA IJH 1.8 6.5 8.1 NA RSP 2.7 14.8 21.1 NA VB 3.4 6.2 63.8 NA IJR 3.6 23.5 40.9 NA VO 5.7 82.6 105.7 NA IWC NA 176.6 NA NA

The evidence from Exhibit 5 substantiates our earlier findings on the differences

in liquidity between ETFs and common stocks. Perhaps, the “NA” values tell the most

compelling story. For instance, trading instantaneously $10mln is possible, on average,

for all but one ETF (IWC). However, trading the same dollar amount for the matched

stocks exhausts the LOB liquidity for the majority of matched common stocks. The

differences in actual costs can be staggering: trading instantaneously $10mln in IVV

costs only 1.6bp, while the similar instantaneous trade for the matched common stocks

would cost nearly 100bp.

Create or Buy: A Comparative Analysis of Liquidity and Transaction Costs for Selected U.S. ETFs

14

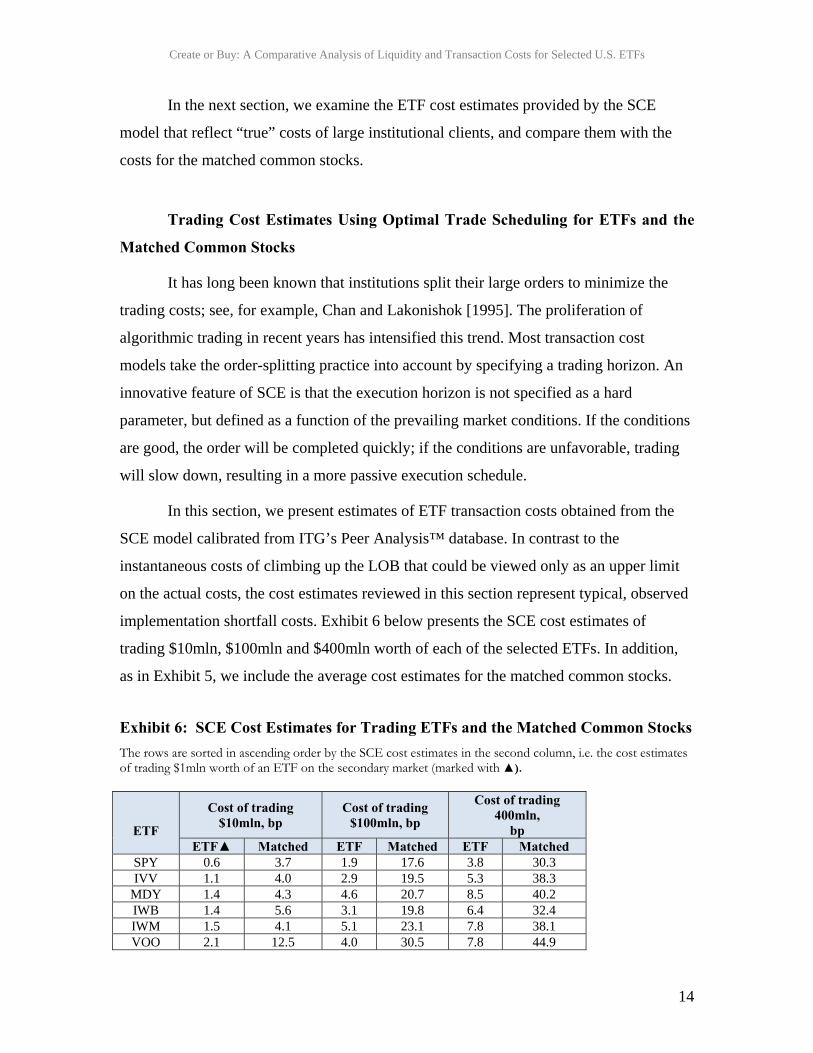

In the next section, we examine the ETF cost estimates provided by the SCE

model that reflect “true” costs of large institutional clients, and compare them with the

costs for the matched common stocks.

Trading Cost Estimates Using Optimal Trade Scheduling for ETFs and the

Matched Common Stocks

It has long been known that institutions split their large orders to minimize the

trading costs; see, for example, Chan and Lakonishok [1995]. The proliferation of

algorithmic trading in recent years has intensified this trend. Most transaction cost

models take the order-splitting practice into account by specifying a trading horizon. An

innovative feature of SCE is that the execution horizon is not specified as a hard

parameter, but defined as a function of the prevailing market conditions. If the conditions

are good, the order will be completed quickly; if the conditions are unfavorable, trading

will slow down, resulting in a more passive execution schedule.

In this section, we present estimates of ETF transaction costs obtained from the

SCE model calibrated from ITG’s Peer Analysis™ database. In contrast to the

instantaneous costs of climbing up the LOB that could be viewed only as an upper limit

on the actual costs, the cost estimates reviewed in this section represent typical, observed

implementation shortfall costs. Exhibit 6 below presents the SCE cost estimates of

trading $10mln, $100mln and $400mln worth of each of the selected ETFs. In addition,

as in Exhibit 5, we include the average cost estimates for the matched common stocks.

Exhibit 6: SCE Cost Estimates for Trading ETFs and the Matched Common Stocks

The rows are sorted in ascending order by the SCE cost estimates in the second column, i.e. the cost estimates of trading $1mln worth of an ETF on the secondary market (marked with ▲).

ETF

Cost of trading $10mln, bp

Cost of trading $100mln, bp

Cost of trading 400mln,

bp ETF▲ Matched ETF Matched ETF Matched

SPY 0.6 3.7 1.9 17.6 3.8 30.3 IVV 1.1 4.0 2.9 19.5 5.3 38.3

MDY 1.4 4.3 4.6 20.7 8.5 40.2 IWB 1.4 5.6 3.1 19.8 6.4 32.4 IWM 1.5 4.1 5.1 23.1 7.8 38.1 VOO 2.1 12.5 4.0 30.5 7.8 44.9

Create or Buy: A Comparative Analysis of Liquidity and Transaction Costs for Selected U.S. ETFs

15

RSP 2.2 11.6 6.2 29.2 9.7 43.2 IJR 2.5 5.8 8.0 21.7 12.6 36.3 IJH 2.6 6.1 7.4 21.9 11.3 36.2 VB 4.8 13.8 10.9 35.3 14.8 51.9 VO 5.0 16.2 9.1 38.4 11.1 56.7 IWC 9.2 20.2 17.6 48.2 29.9 70.4

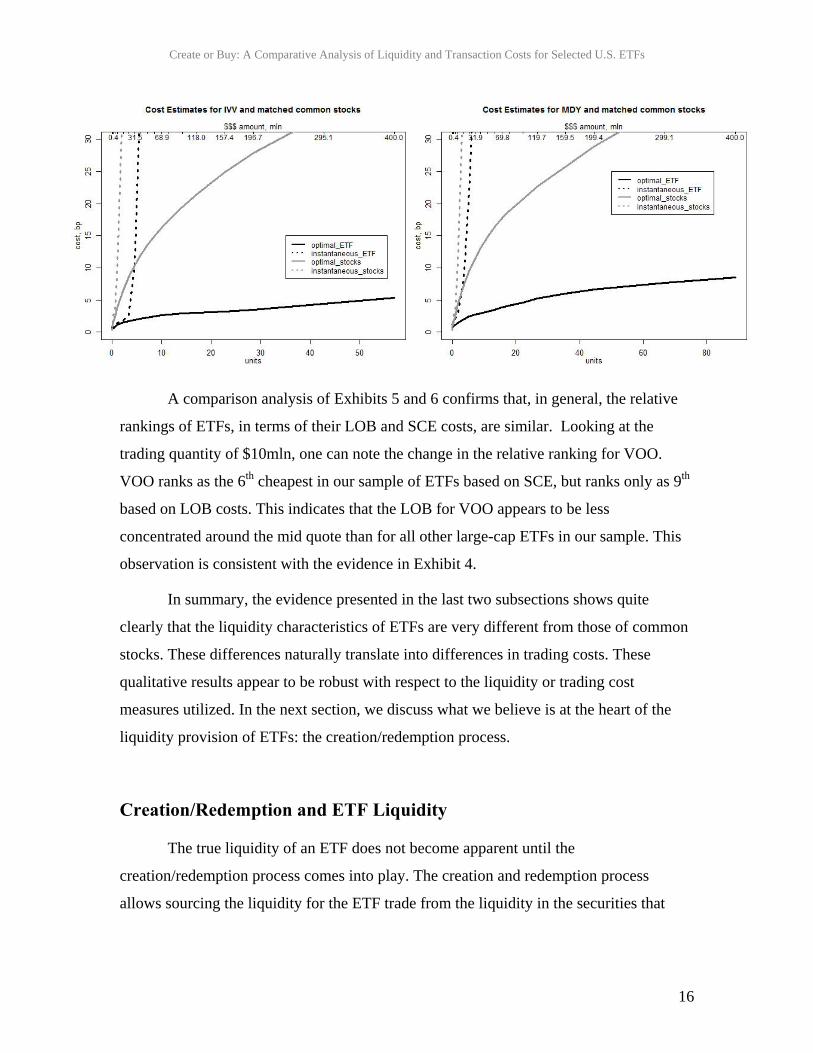

It is obvious that across all ETFs and trade quantities, the SCE cost estimates for

the selected ETFs are lower than those for the matched common stocks. Exhibit 7 below

illustrates this for IVV and MDY. The chart contains SCE cost estimates for those two

ETF and for the matched common stocks. In order to link these results with the previous

section, the chart also includes the instantaneous costs of climbing up the LOB from

Exhibit 5. Exhibits 6 and 7 show clearly that it is essential for pre-trade models to

recognize the different nature of ETFs. Failure to do so could lead to situations where the

cost estimates of trading ETFs optimally across the whole day are higher than the

instantaneous costs of climbing the LOB which is, indeed, impossible6.

We believe that the arbitrage mechanism available to authorized participants

(APs) is largely behind the lower ETF costs. For example, whenever an ETF is getting

overbought in the secondary market, an AP who closely watches the discrepancy between

the IOPV and the ETF price could start selling the ETF short and buying stocks in

underlying basket. We discuss the ETF-basket liquidity link and the creation/redemption

mechanism in Section 5.

Exhibit 7 also visualizes quite vividly that the immediate liquidity would come at

a steep price. For example, trading instantaneously 5 units of IVV would cost over 30bp,

while the SCE cost estimate for this ETF is only around 2-3bp.

Exhibit 7

The black solid lines represent the optimal costs of trading an ETF, while the grey solid lines show the average optimal cost (across stocks) of trading a matched common stock. The black dashed lines illustrate the cost of the instantaneous trade of an ETF; while the dashed grey lines represent the average cost (across stocks) of the instantaneous trade of a matched common stock. The lower horizontal axis depicts the number of ETF units, while the upper horizontal axis shows the corresponding dollar amount (in millions).

Create or Buy: A Comparative Analysis of Liquidity and Transaction Costs for Selected U.S. ETFs

16

A comparison analysis of Exhibits 5 and 6 confirms that, in general, the relative

rankings of ETFs, in terms of their LOB and SCE costs, are similar. Looking at the

trading quantity of $10mln, one can note the change in the relative ranking for VOO.

VOO ranks as the 6th cheapest in our sample of ETFs based on SCE, but ranks only as 9th

based on LOB costs. This indicates that the LOB for VOO appears to be less

concentrated around the mid quote than for all other large-cap ETFs in our sample. This

observation is consistent with the evidence in Exhibit 4.

In summary, the evidence presented in the last two subsections shows quite

clearly that the liquidity characteristics of ETFs are very different from those of common

stocks. These differences naturally translate into differences in trading costs. These

qualitative results appear to be robust with respect to the liquidity or trading cost

measures utilized. In the next section, we discuss what we believe is at the heart of the

liquidity provision of ETFs: the creation/redemption process.

Creation/Redemption and ETF Liquidity

The true liquidity of an ETF does not become apparent until the

creation/redemption process comes into play. The creation and redemption process

allows sourcing the liquidity for the ETF trade from the liquidity in the securities that

Create or Buy: A Comparative Analysis of Liquidity and Transaction Costs for Selected U.S. ETFs

17

comprise the underlying basket. Consequently, ETFs tracking the same index should

have, in principle, very similar market impact costs.

Exhibit 8 below examines the liquidity of the basket of the underlying securities

for the selected ETFs. Different panels show the liquidity for ETFs tracking large-, mid-

and small-cap indices. SCE cost estimates for trading ETFs on the secondary market are

depicted by solid lines. SCE cost estimates for the baskets of underlying constituents are

shown by dashed lines and include creation/redemption fees. We assume that the ETF

creation/redemption costs are a lump-sum payment (see Exhibit 2) independent of the

quantities raised.

Displaying on the same chart the trading cost estimates for ETFs and the

underlying baskets of securities within a given market cap segment sheds light on the

relationship between the liquidity of an ETF and its basket. The charts confirm that

sourcing liquidity from the underlying baskets of securities for alternative ETFs that

passively track the same index have nearly identical costs. The dashed lines for SPY and

VOO (two ETFs tracking the S&P500 index) on the chart for large-cap ETFs in Exhibit 8

converge as the order size increases and the lump-sum creation/redemption fees become

less relevant. The creation/redemption cost estimates for IWB, which tracks the Russell

1000 large-cap index, are comparable with those tracking the S&P500 index. The basket

cost estimates for RSP which tracks the equally-weighted S&P 500 index (not shown) are

slightly higher than those for all other large-cap ETFs, reflecting the fact that less-liquid

securities from the index would have to be accumulated in the same proportions as more

liquid securities. At the same token, the ranking of the cost estimates for large-cap ETFs

on the secondary market (solid lines) is different from the ranking of the cost estimates

for the corresponding baskets.

The optimal switching point between trading an ETF and using the

creation/redemption mechanism differs widely for the selected ETF universe. For

instance, SPY, with its abundant secondary market liquidity, does not appear to benefit

from creation/redemption up to 15 units, corresponding to approximately a $100mln trade

size. On the other hand, Vanguard’s VOO ETF, which was launched relatively recently in

2010, and which has identical underlying basket, is lagging with respect to IVV and SPY

Create or Buy: A Comparative Analysis of Liquidity and Transaction Costs for Selected U.S. ETFs

18

in terms of secondary market volume. Therefore, investors who trade VOO appear to be

better off taking advantage of the creation/redemption process for quantities as small as 2

units, corresponding to a $6mln trade size.

Exhibit 8

The solid lines represent the optimal costs of trading an ETF while the dashed lines illustrate the optimal cost of trading the basket of stocks necessary for creation/redemption (with the creation/redemption fees added on top). All costs are displayed for the number of ETF units indicated on the horizontal axis.

Similar to VOO, the chart for mid-cap ETFs in Exhibit 8 shows that another ETF

by Vanguard, VO (tracking the MSCI US Mid Cap 450 index), appears to be competitive

against the more established MDY, provided by SSGA. With a median daily volume of

Create or Buy: A Comparative Analysis of Liquidity and Transaction Costs for Selected U.S. ETFs

19

only 160K shares against 2mln shares of MDY on the secondary market, Vanguard

compensates by tracking a slightly broader mid-cap index (450 vs. 400 stocks in the

basket) and setting a low creation/redemption fee ($500 vs. $3000). As a result, for trade

quantities of 10 units or more, creation/redemption costs for VO are, essentially, in line

with the secondary market costs for MDY.

A quick look at small-cap ETFs shows that liquidity considerations regarding the

underlying securities of an ETF are important. All small-cap ETFs presented in Exhibit

10 track different indices: IWM tracks the Russell 2000, VB – MSCI US 1750, and IWC

– Russell Microcap index. The slopes and intercepts of the dashed lines corresponding to

these ETFs reflect perfectly the differences in liquidity between the underlying securities

of these indexes. For instance, the basket costs for VB which tracks the narrower index

(S&P 1750), starts a bit lower than the basket costs for IWM, which tracks the Russell

2000 index. However, as the trade quantities increase, the basket costs for IWM increases

at a slower rate than the basket costs for VB, as larger trade volume is spread among

more securities. The illiquidity of the stocks belonging to the Russell Microcap index

places the creation/redemption costs for IWC well above the other three ETFs. Taking the

creation/redemption fees into consideration does not change the relative ranking of small-

cap ETFs as much as it did for large-cap ETFs.

Exhibit 9 below presents a more detailed cost breakdown for three selected trade

quantities: $10mln, $100mln and $400mln. The ETFs are sorted in ascending order by

the SCE cost estimates of creating/redeeming $10mln worth of each ETF. Note that the

ranking of an ETF changes as the quantity traded is varied. For instance, SPY’s

underlying stocks are very liquid securities, but the ETF itself also has one of the highest

creation/redemption costs ($3,000, regardless of the number of units created).

Consequently, SPY ranks only 10th when trading $10mln via creation/redemption.

However, due to “economies of scale” and the abundant liquidity in its underlying

securities, SPY moves from 10th to 4th position (still lagging after three other large-cap

ETFs) when it comes to creating/redeeming $400mln worth of the underlying basket.

Exhibit 9: SCE Cost Estimates for Trading ETFs and Creation/Redemption Costs

Create or Buy: A Comparative Analysis of Liquidity and Transaction Costs for Selected U.S. ETFs

20

The rows are sorted in ascending order by the cost of creating/redeeming $10mln worth of each ETF, taking fees into account (marked with ▲).

ETF

SCE, $10 mln SCE, $100 mln SCE, $400 mln

ETF Basket Basket +

cr/rdm fee▲ ETF Basket

Basket + cr/rdm fee

ETF Basket Basket +

cr/rdm fee VOO 2.1 1.3 1.9* 4 1.6 1.7* 7.8 2.4 2.4*

IVV 1.1 1.3 1.9 2.9 1.6 1.7* 5.3 2.4 2.4*

IWB 1.4 1.4 2.0 3.1 1.6 1.7* 6.4 2.4 2.4*

VO 5 2.1 2.7* 9.1 2.7 2.8* 11.1 4.6 4.6*

IJH 2.6 2.3 22..99 77..44 3.7 3.8* 11.3 7.5 7.5*

VB 4.8 3.1 33..77** 1100..99 4.1 4.2* 14.8 6.9 6.9*

IJR 2.5 3.2 3.8 8 6.2 6.3* 12.6 13.2 13.2

RSP 2.2 1.7 4.2 6.2 2 2.2* 9.7 3.1 3.2*

IWM 1.5 3.7 4.3 5.1 5.1 5.2 7.8 8.9 8.9

SPY 0.6 1.3 5.1 1.9 1.6 1.9 3.8 2.4 2.5*

MDY 1.4 2.3 6.1 4.6 3.7 4.0* 8.5 7.5 7.6*

IWC 9.15 9.2 9.8 17.6 16.1 16.2* 29.9 25.1 25.1*

As has been previously demonstrated in Exhibit 8, the trading costs of ETFs still

depend to a large extent on their secondary market volumes and liquidity. The cells with

asterisks indicate the instances when creation/redemption is cheaper than trading the

same quantity on the secondary market. The number of ETFs for which

creation/redemption is cheaper for the same trade amount grows from 3 for a $10mln

trade to 10 for a $400mln trade. However, the creation/redemption mechanism is not a

magic cure that would substantially enhance the liquidity of all ETFs. The numbers

presented in Exhibit 9 for some liquid ETFs (IWM, SPY, MDY) suggest that sourcing

liquidity from the underlying securities can only partially alleviate the burden of high

trading costs on the secondary market. In particular, for MDY and SPY,

creation/redemption starts to get cheaper only for extremely large trade quantities

($400mln), while for IWM, trading on the secondary market appears to be cheaper,

regardless of the trade amount.

Earlier in the paper we mention that the arbitrage mechanism via

creation/redemption ensures that the costs of trading an ETF on the secondary market are

substantially lower than the costs of trading a common stock with comparable volume,

spread, volatility and price characteristics. However, the evidence in Exhibits 8 and 9

Create or Buy: A Comparative Analysis of Liquidity and Transaction Costs for Selected U.S. ETFs

21

suggests that creation/redemption arbitrage does not completely reduce the gap between

the secondary market costs and the basket costs for large order sizes. We believe that

there are several reasons behind this. First, trading an ETF basket usually involves higher

commissions and other implicit costs, simply because there are more shares traded7,

which can make it harder to execute this strategy successfully. Second, securities in the

basket often need to be accumulated in a non-discretionary fashion (e.g. via market

orders) in order to ensure that the ETF can be created or redeemed at the end of the day.

The cost estimates that were presented so far are based on SCE’s default trade imbalance

function, which maps own trading into aggregated order flow and is estimated using

ITG’s Peer Analysis™ data. Since many client orders stored in the Peer Analysis™

database are executed opportunistically, it is possible that the resulting cost estimates are

biased downwards to some extent8.

Despite the caveats discussed above, we believe that the cost estimates for the

underlying baskets of stocks provide additional clarity with respect to the “true” average

costs of large ETF orders. The joint analysis of ETF and basket cost estimates presents

the user with a realistic range of possible outcomes. For most ETFs and larger order

sizes, the costs of trading the basket (illustrated by the dashed lines in Exhibit 8) define a

lower limit on the costs of ETF trading. These costs correspond to the hypothetical

situation, in which there are no implicit fees other than creation/redemption fees, and the

execution implementation is a mix of opportunistic and non-discretionary trading. One

can observe that the difference between transaction cost estimates for an ETF and for the

underlying basket becomes wider when the ETF’s secondary market liquidity and the

liquidity of underlying securities are disparate. For instance, VOO trades only 370K

shares daily; however, it tracks a very liquid S&P500 index. On the other hand, for an

ETF with abundant liquidity on the secondary market, such as SPY or IWM, the

transaction cost uncertainty band becomes much narrower, possibly indicating that the

creation/redemption process is less practical.

Exhibit 10:

The black solid lines represent the optimal costs of trading an ETF, while the black (grey) dashed lines depict the cost of trading the underlying basket of stocks necessary for creation/redemption using a mix of

Create or Buy: A Comparative Analysis of Liquidity and Transaction Costs for Selected U.S. ETFs

22

market and limit orders (market orders) only. The lower horizontal axis shows the number of ETF units, while the upper horizontal axis represents the corresponding dollar amount (in millions).

Exhibit 10 offers a more detailed, graphical representation of the effect of

different trading styles on the market order flow and, ultimately, on the trading costs for

IJH and VB. In addition to SCE’s default trade imbalance function, which corresponds to

a mix of opportunistic and non-discretionary trading (dashed dark-grey line), we compute

the basket costs assuming that the stocks in the basket are traded only via market orders

(dashed light-grey line). The data points marked on Exhibit 10 correspond to the numbers

highlighted in bold in Exhibit 9. Both charts in Exhibit 10 demonstrate that the

creation/redemption mechanism can substantially reduce implementation shortfall costs,

particularly for large quantities, when the liquidity diversification effect for the

underlying large cap constituents becomes apparent. However, the cost savings can be

realized only if the trading is properly implemented. Trading the underlying basket only

via market orders would have a substantial adverse effect on trading costs. In order to

make optimal trading decisions, it is thus important to assess market conditions that affect

the liquidity and trading costs of ETFs and their underlying baskets in real-time9.

Create or Buy: A Comparative Analysis of Liquidity and Transaction Costs for Selected U.S. ETFs

23

Conclusions

We examine liquidity and trading cost characteristics for twelve equity ETFs that

track small-cap, mid-cap and large-cap US market indices, and compare them with their

counterparts for matched common stocks with similar MDDV, spread, historical

volatility and price levels. Our analysis reveals that ETFs and matched common stocks

exhibit different liquidity characteristics. The LOBs of ETFs are deeper and more

concentrated around the prevailing mid quotes. The costs of instantaneous execution

(climbing up the book) are significantly lower for ETFs than for the matched common

stocks. At the same time, we present empirical evidence that the LOBs of ETFs are quite

volatile. The number of ETF units that can be raised by climbing the LOB at any

particular moment of time can change dramatically within a single trading day.

Our findings confirm that the creation and redemption mechanism is crucial for

the liquidity provision of ETFs. For many (but not all) ETFs studied, the costs of

creation/redemption are lower than the costs of acquiring/selling the ETF in the

secondary market across a wide range of notional trade quantities. Our conclusions hold

when creation/redemption fees are taken into account. Nevertheless, we see that the

liquidity in the secondary market remains an important determinant of ETF costs. For

instance, $10mln of SPY can be traded instantaneously at a cost of less than 1bp, whereas

trading the same quantity via creation/redemption would cost over 4bp. For some liquid

ETFs, the costs of trading the underlying basket remain higher than secondary market

costs throughout the entire practical range of trade quantities. Overall, it appears that the

arbitrage mechanism associated with the creation/redemption mechanism is likely to keep

in check the difference between secondary market costs and the costs of trading the

basket. However, for some ETFs (VO, VOO, RSP), we observe noticeable differences

between these two cost estimates for larger order sizes. We offer several reasons that

explain the cost differences.

We also argue that a properly estimated and calibrated transaction cost model can

serve as a useful tool for measuring and analyzing ETF liquidity and trading costs. The

model design should reflect the fact that the permanent price impact costs of most ETF

trades are significantly lower than the price impact costs for matched common stock.

Create or Buy: A Comparative Analysis of Liquidity and Transaction Costs for Selected U.S. ETFs

24

Model parameters should be estimated and calibrated using the ETF-only sub-universe of

trading data and incorporate liquidity available through the creation/redemption

mechanism. Provided that proper care has been taken in building a transaction cost

model, its cost estimates for ETF trades on the secondary market and for its underlying

basket can serve as upper and lower bands for the actual ETF transaction costs.

The comparison of ETF and basket costs, in conjunction with a look at

creation/redemption fees, indicates the need for monitoring relative ETF liquidity, as the

optimal switching points between trading an ETF and creating/redeeming can vary

widely across ETFs. For instance, the low creation/redemption fees for two ETFs of

Vanguard (VOO, VO) appear to make them very attractive options for

creation/redemption, as soon as the trade sizes exceed two ETF units. These low fees

seem to compensate for the lack of liquidity on the secondary market relative to the

competitors’ ETFs that track similar indices. On the other hand, the relatively steep

creation/redemption fees for SPY and IWM, combined with the abundant liquidity of

ETF shares on the secondary market, make the creation or redemption mechanism for

those ETFs suboptimal across the entire range of trade sizes of practical relevance.

Endnotes

The authors would like to thank Charlie Behette, Doug Clark, Ian Domowitz, Laura Tuttle, Konstantin

Tyurin, Olav Van Genabeek and Ian Williams for their support, comments, and suggestions. Any opinions

expressed herein reflect the judgment of the individual authors at this date and are subject to change, and do

not necessarily represent the opinions or views of Investment Technology Group, Inc.

1 See, for instance, Warsh [2007]. 2 Davies and Kim [2007] provide an extensive list of papers using similar matching techniques. 3 For instance, the five stocks matched to IWB are: ECL, PGN, ED, ETR and ADP. 4 We use an alternative two-week period between September 26 and October 7, 2011 to run robustness

checks. The results are qualitatively very similar and available upon request.5The finding is consistent with

the CFTC and SEC Report [2010]. 6 Note that a big chunk of the solid grey line lies above the dashed black line for IVV, 7 For example, creation/redemption of 1 unit of IWB requires trading ~95,000 shares of underlying stocks

(while only 50,000 shares of ETF itself).

Create or Buy: A Comparative Analysis of Liquidity and Transaction Costs for Selected U.S. ETFs

25

8 For instance, the price impact costs for individual securities in the basket are not independent of each

other. Once an AP starts actively accumulating securities in the basket, the price impact costs of other

securities from the same basket are likely to go up as well. 9 See, for example, Borkovec et al. [2011].

Create or Buy: A Comparative Analysis of Liquidity and Transaction Costs for Selected U.S. ETFs

26

References

Berke, Laura. “The Optimal Implementation. ETFs, Futures and Swaps.” TABB Group

Report, 2009.

Borkovec, Milan, I. Domowitz, B. Kiernan and V. Serbin. “Portfolio Optimization and

the Cost of Trading.” Journal of Investing, 19 (2010), pp. 63-76.

Borkovec, Milan, K. Tyurin, Q. Fang, and J. Cheng. “What Does It Take to Work Large

Orders in Real Time? Introducing ITG Smart Cost Estimator.” ITG Technical Report,

2011.

Brandes, Yossi, I. Domowitz, and V. Serbin. “Transaction Costs and Equity Portfolio

Capacity Analysis.” In B. Scherer and K. Winston, ed., The Oxford Handbook of

Quantitative Asset Management, Oxford University Press, 2011, pp. 398-420.

Chan, Louis K.C., and J. Lakonishok. “The Behavior of Stock Prices Around Institutional

Trades.” Journal of Finance 50 (1995), pp. 1147-1174.

Davies, Ryan and S. Kim. “Using Matched Samples to Test for Differences in Trade

Execution Costs.” Journal of Financial Markets 12 (2009), pp. 173-202.

Fuhr, Deborah. “ETF Landscape. Industry Highlights.” BlackRock Report, 2011.

“Findings Regarding the Market Events of May 6, 2010.” CFTC and SEC Report,

September 2010.

Huang, Roger and H. Stoll. "Dealer versus auction markets: A paired comparison of

execution costs on NASDAQ and the NYSE." Journal of Financial Economics 41 (1996),

pp. 313-357.

“Institutional Demand for Exchange-Traded Funds Continues to Climb.” Greenwich

Associates Report, May 2011.

Warsh, Kevin. “Market Liquidity: Definitions and Implications.” Speech at the Institute

of International Bankers Annual Washington Conference, 2007, available at

http://www.federalreserve.gov/newsevents/speech/warsh20070305a.htm.