CREATE AND SUSTAIN A CULTURE OF MAXIMIZED ... 1 CREATE AND SUSTAIN A CULTURE OF MAXIMIZED VALUE AND...

25

11/2/2010 1 CREATE AND SUSTAIN A CULTURE OF MAXIMIZED VALUE AND PERFORMANCE Why is Growing a Business and Building Value Complicated? • Competing Goals Maximize Profits WHY IS GROWING A BUSINESS AND BUILDING VALUE COMPLICATED?

Transcript of CREATE AND SUSTAIN A CULTURE OF MAXIMIZED ... 1 CREATE AND SUSTAIN A CULTURE OF MAXIMIZED VALUE AND...

11/2/2010

1

CREATE AND SUSTAIN A CULTURE OF MAXIMIZED VALUE AND PERFORMANCE

Why is Growing a Business and Building Value Complicated?

• Competing Goals

Maximize Profits

WHY IS GROWING A BUSINESS AND BUILDING VALUE COMPLICATED?

11/2/2010

2

Why is Growing a Business and Building Value Complicated?

• Competing Goals

Maximize Profits

Cash Available for Taxes/Distributions

WHY IS GROWING A BUSINESS AND BUILDING VALUE COMPLICATED?

Why is Growing a Business and Building Value Complicated?

• Competing Goals

Maximize Profits

Cash Available for Taxes/Distributions

Grow Business

WHY IS GROWING A BUSINESS AND BUILDING VALUE COMPLICATED?

11/2/2010

3

Why is Growing a Business and Building Value Complicated?

• Competing Goals

Maximize Profits

Cash Available for Taxes/Distributions

Grow Business

Regulatory Compliance

WHY IS GROWING A BUSINESS AND BUILDING VALUE COMPLICATED?

Why is Growing a Business and Building Value Complicated?

• Competing Goals

Maximize Profits

Cash Available for Taxes/Distributions

Grow Business

Regulatory Compliance

Attracting and Compensating Best and Brightest

WHY IS GROWING A BUSINESS AND BUILDING VALUE COMPLICATED?

11/2/2010

4

Why is Growing a Business and Building Value Complicated?

• Competing Goals

Maximize Profits

Cash Available for Taxes/Distributions

Grow Business

Regulatory Compliance

Attracting and Compensating Best and Brightest

Getting All of the Key People on the Same Set of Objectives

WHY IS GROWING A BUSINESS AND BUILDING VALUE COMPLICATED?

Who are Stakeholders?

Internal

Where they come from?

Owners/Investors

Stockholders

Internal Employees

External Business Partners

External Banks/Lending Institutions

Community

Why is Growing a Business and Building Value Complicated?

External

11/2/2010

5

Why is Growing a Business and Building Value Complicated?

• Key Stakeholders

Owners/Investors

Employees

Who Drives the Business – Key Stakeholders?

Why is Growing a Business and Building Value Complicated?

Understand Success

How Do We Get Owners and Employees to Work

with the Same Attitudes and Drive to Success?

11/2/2010

6

Why is Growing a Business and Building Value Complicated?

Understand Success

Effects of Success

How Do We Get Owners and Employees to Work

with the Same Attitudes and Drive to Success?

Why is Growing a Business and Building Value Complicated?

Understand Success

Effects of Success

Understand the Drivers of Success

How Do We Get Owners and Employees to Work

with the Same Attitudes and Drive to Success?

11/2/2010

7

Why is Growing a Business and Building Value Complicated?

Understand Success

Effects of Success

Understand the Drivers of Success

Work as one with much to gain or lose

How Do We Get Owners and Employees to Work

with the Same Attitudes and Drive to Success?

Why is Growing a Business and Building Value Complicated?

Clear Strategic Objectives

ACHIEVING A WIN/WIN WITH

OWNERS/EXECUTIVE/KEY EMPLOYEES

11/2/2010

8

Why is Growing a Business and Building Value Complicated?

Clear Strategic Objectives

Simplify the Metrics for Success

ACHIEVING A WIN/WIN WITH

OWNERS/EXECUTIVE/KEY EMPLOYEES

Why is Growing a Business and Building Value Complicated?

Clear Strategic Objectives

Simplify the Metrics for Success

Put Together a Long Term Incentive Plan That

Rewards Long Term Thinking

ACHIEVING A WIN/WIN WITH

OWNERS/EXECUTIVE/KEY EMPLOYEES

11/2/2010

9

Why is Growing a Business and Building Value Complicated?

Clear Strategic Objectives

Simplify the Metrics for Success

Put Together a Long Term Incentive Plan That

Rewards Long Term Thinking

Make Key Players Partners in Success

ACHIEVING A WIN/WIN WITH

OWNERS/EXECUTIVE/KEY EMPLOYEES

The Key Elements in Building Value

1) Expectations

2) Traditional Methods

a) Profit – Annually/Quarterly/Monthly – EPS (Earnings Per Share)

b) Project/Investment Returns

c) Cash Flow

d) Problem

Too much emphasis on the short term

Profits can be manipulated

Does not take into consideration building value and long term results

THE KEY ELEMENTS IN BUILDING VALUE

11/2/2010

10

DEFINITIONS TO EVA

NOPAT

WACC

Invested Capital

Definitions to EVA

DEFINITIONS TO EVA

Net Operating Profit After Taxes NOPAT

WACC

Invested Capital

Definitions to EVA

11/2/2010

11

DEFINITIONS TO EVA

Net Operating Profit After Taxes NOPAT

Weighted Average Cost of Capital WACC

Invested Capital

Definitions to EVA

DEFINITIONS TO EVA

Net Operating Profit After Taxes NOPAT

Weighted Average Cost of Capital WACC

Equity & Debt

Invested Capital

Definitions to EVA

11/2/2010

12

Definitions to EVA

Measured by market value of the business

less accumulated equity on Balance Sheet.

MVA = MARKET VALUE ADDED

Value of Business to others (market) – Equity of Owners =

Market Value Added

Definitions to EVA

Measured in absolute dollars by

taking the net Operating Profit

after tax and subtracting (the cost

of capital x the invested capital.)

EVA = ECONOMIC VALUE ADDED

11/2/2010

13

Definitions to EVA

EVA Calculation ($Millions)

Sales $2,436

Cost of Sales 1,700

Sales General & Admin Cost 400

Taxes 134

NOPAT 202

Invested Capital 1,500

X WACC 12%

Capital Charge 180

Economic Value Added 22

NOPAT (Net Operating Profit After Tax)

WACC x Cost of Capital (WACC=The % of Interest /Aggregate Loan Rates)

Definitions to EVA

• Earn more than your WACC on all that you do

You must earn more than what it cost to get your

money

• Consistently grow NOPAT

Investors won’t pay more tomorrow for

a company that is smaller

THE SECRETS OF VALUE CREATION

11/2/2010

14

Definitions to EVA

• Making EVA grow makes MVA grow

Over twice a powerful as making only EPS grow

• High EVA over time produces high MVA

The Price/Book Ratio goes up

THE CONNECTION

Why is Growing a Business and Building Value Complicated?

What is WACC “Weighted

Average Cost of Capital”

All the assets you use are paid for from the right side

of the balance sheet

UNDERSTANDING THE ELEMENTS

11/2/2010

15

Why is Growing a Business and Building Value Complicated?

The Two Sources

of Money

Debt and Equity

UNDERSTANDING THE ELEMENTS

Why is Growing a Business and Building Value Complicated?

UNDERSTANDING THE ELEMENTS

The Cost of Equity = What Investors Could Earn

by Investing Elsewhere (It’s Opportunity Cost)

11/2/2010

16

Why is Growing a Business and Building Value Complicated?

UNDERSTANDING THE ELEMENTS

The Cost of Equity = What Investors Could Earn

by Investing Elsewhere (It’s Opportunity Cost)

Why is Growing a Business and Building Value Complicated?

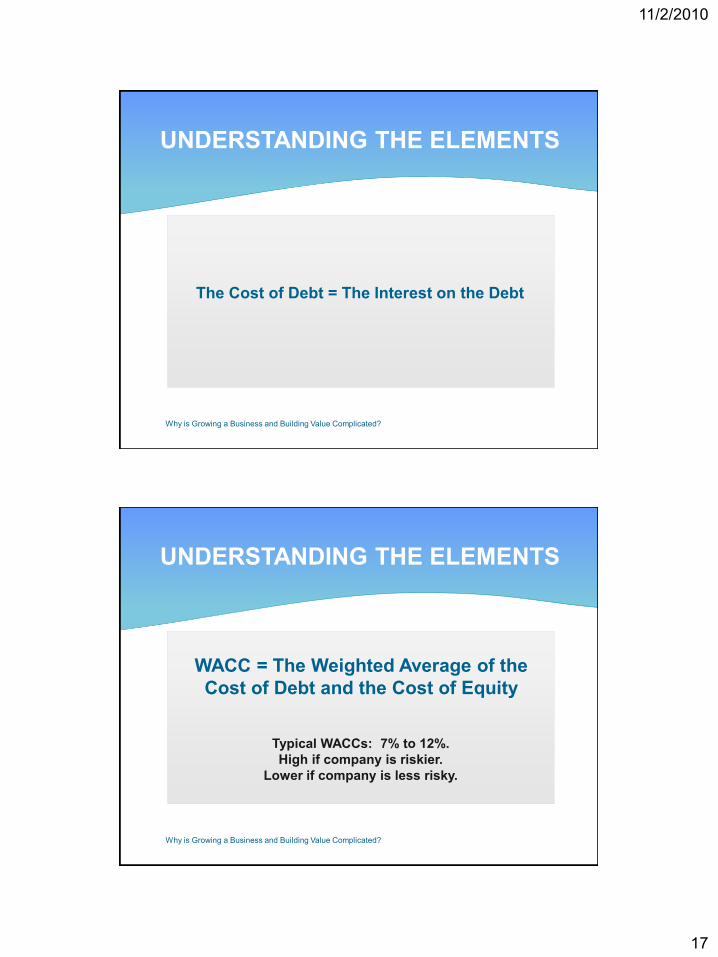

The Cost of Debt = The Interest on the Debt

UNDERSTANDING THE ELEMENTS

11/2/2010

17

Why is Growing a Business and Building Value Complicated?

The Cost of Debt = The Interest on the Debt

UNDERSTANDING THE ELEMENTS

Why is Growing a Business and Building Value Complicated?

WACC = The Weighted Average of the

Cost of Debt and the Cost of Equity

UNDERSTANDING THE ELEMENTS

Typical WACCs: 7% to 12%.

High if company is riskier.

Lower if company is less risky.

11/2/2010

18

The Secrets of Value Creation

Earn More than your WAAC on all that you do

You must earn more than what it costs to get

your money

Consistently grow NOPAT

Investors won’t pay more tomorrow for

a company that is smaller

THE SECRETS OF VALUE CREATION

Strategic Planning Directives

Make NOPAT go up

Earn more than WACC on all that you do

New Capital Projects should earn more than WACC

Get rid of operations that do not earn your WACC

STRATEGIC PLANNING DIRECTIVES

11/2/2010

19

HOW IT WORKS NET OPERTING PROFIT AFTER TAXES (NOPAT) CALCULATION:

Sales $25,000,000

Cost of Sales <210,000>

Gross Margin $24,790,000

Total Operating Expense <$21,603,000>

Income from Operations before Taxes 3,870,000

Taxes 53,000

NOPAT (Net Operating Profit After Tax) $3,817,000

INVESTED CAPITAL (IC) CALCULATION:

Total Assets 26,100,000

Less: Accounts Payable <687,000>

Less: Other Current Liabilities (Non Debt) <1,430,000>

INVESTED CAPITAL $23,983,000

RETURN ON INVESTED CAPITAL AT END OF YEAR:

NOPAT $3,817,000

Invested Capital @ End of Year 23,983,000

NOPAT/IC 15.90%

ECONOMIC VALUE ADDED (EVA) CALCULATION:

NOPAT $3,817,000

Less Capital Charge:

Invested Capital @ End of Year $23,983,000

X Cost of Capital (assumed 10%) x10%

Capital Charge $2,398,300

Calculated EVA (difference EVA less Capital Charge) $1,418,700

YEAR TO YEAR EFFECT

BASIC ECONOMIC VALUE TARGET ANALYSIS

XYZ COMPANY

2008 2009 2010 2011 2012 2013

Actual Actual Forecast Proforma Proforma Proforma

Economic Value Added 1,418,700 1,178,900 1,567,524 1,969,500 2,417,500 2,807,500

Change 338,200 <239,800> 518,624 400,000 450,000 390,000

Recommended Targets

(Used Graduated Increase)

20% Growth in EVA 1,600,000 2,000,000 2,400,000 2,800,000

11/2/2010

20

Take away points

To Make your company worth more tomorrow:

Grow NOPAT

Earn more than WACC on all that you do

Get rid of operations that earn less than WACC

TAKE AWAY POINTS

INCENTIVE PLAN

Incentive plan

1. Shareholder/Owners

Have a stake in growing business as the more it grows the more their investment is worth.

2. Key Members of Management Team

a)Need to know the connection between short term profits and long term growth.

b)They need a long term Incentive Program that makes them partners in long term growth.

c)Multiyear incentive based on growth to include earnings and investment.

Connecting the Key Stakeholders to the

Concept of Growing Value Over the Long Run.

11/2/2010

21

Bonus Plan Design

Pay target bonuses to Key Associates if the EVA target

for the year is met, and

Pay more if EVA is bigger than last year

Pay more if return on invested capital is greater than

target return

BONUS PLAN DESIGN

BONUS PLAN DESIGN

Bonus Plan Design

Bonus Plan

Needs to be based on long term

performance

Reasons

a)Prevent Manipulated Profits

b)Think Strategically on Capital

Purchases

Unproductive Assets

Bonus Plan Design

11/2/2010

22

4 4

3 3

2 2

A targeted annual ROIC is established

Each participant will have a bonus pool account set up in his/her name

Key personnel who have the greatest impact on the decisions that affect ROIC will be

invited to participate.

Based on the target rate of Return on Invested Capital, each amount calculated on the

actual return over or under will be added or reduced from the total of the Bonus Bank.

Details of Plan

DETAILS OF PLAN

1 1

BONUS PLAN DESIGN

Bonus Plan Design

Target Return

WACC & Risk Factor

Weighted Average Cost of Capital

Cost of Debt 6%

Return on Investment 8%

WACC = 6.7%

Risk = 5.3%

Target Return 12%

Bonus Plan Design

11/2/2010

23

YEAR TO YEAR EFFECT XYZ Company

Strategic Bonus Program

Year A Year B Year B Year D Cumulative

NOPAT 1,337,498 1,417,748 1,332,683 1,665,854

Invested Capital @ End of Year 12,672,400 12,925,848 13,701,399 13,838,413

NOPAT/IC (Calculated) 10.6% 11.0% 9.7% 12.0%

NOPAT/IC (Minimum Base) 10.0% 10.0% 10.0% 10.0%

NOPAT 1,337,498 1,417,748 1,332,683 1,665,854

NOPAT/IC 10.6% 11.0% 9.7% 12.0%

Dollars exceeding (under) base 70,258 125,163 (37,457) 282,012 439,977

Dollars available

First dollar 70,258 100,000 (37,457) 100,000

20% of remainder - 5,033 - 36,402

Bonus Dollars Earned 70,258 105,033 (37,457) 136,402 274,236

Assumptions:

1) ROIC return on invested Capital over target:

First $100,000 into Bonus pool at Dollar for Dollar

Over $100,000, 20% of each dollar into Bonus Pool

2) ROIC Return less than target:

, First $100,000 deducted from Bonus pool at Dollar for Dollar

20% of each dollar over $100,000 taken away from Bonus Pool

3) Percentage of participation based on each individuals base pay as a percent of all eligible participants

Net Wages Earned Year A Year B

Net Base Wages

Percent of

Bonus

Dollars

Bonus Pool Net

Carry Forward

Bonus Pool Dollars

Earned Year A

Total

Accumulated

Dollars

Year A

Distribution (1/3

of pool)

Bonus Pool Net

Carry Forward

Bonus Pool Dollars

Earned Year A

Total Accumulated

Dollars

Year B Distribution

(1/3 of pool)

Bonus Pool Net

Carry Forward

Key Employees

Employee A $98,500.00 21.0% 20,987.63 14,745.49 35,733.12 11,911.04 23,822.08 22,043.86 45,865.94 15,288.65 30,577.30

B $67,615.00 14.4% 14,406.89 10,121.99 24,528.89 8,176.30 16,352.59 15,131.94 31,484.53 10,494.84 20,989.68

C $93,000.00 19.8% 19,815.73 13,922.14 33,737.87 11,245.96 22,491.92 20,812.98 43,304.90 14,434.97 28,869.93

D $77,002.00 16.4% 16,407.00 11,527.23 27,934.23 9,311.41 18,622.82 17,232.70 35,855.53 11,951.84 23,903.68

E $78,851.00 16.8% 16,800.97 11,804.03 28,605.00 9,535.00 19,070.00 17,646.50 36,716.50 12,238.83 24,477.67

F $54,356.00 11.6% 11,581.76 8,137.12 19,718.88 6,572.96 13,145.92 12,164.63 25,310.55 8,436.85 16,873.70

TOTAL ALL $469,324.00 100.0% 100,000.00 70,258 170,258 56,753 113,505 105,033 218,538 72,846 145,692

Year C Year D

Bonus Pool Dollars

Earned

Total

Accumulated

Dollars

Year C

Distribution (1/3

of pool)

Bonus Pool Net

Carry Forward

Bonus Pool Dollars

Earned

Total Accumulated

Dollars

Year C Distribution

(1/3 of pool)

Bonus Pool Net

Carry Forward

Key Employees

Employee A (7,861.31) 22,715.98 7,571.99 15,143.99 28,627.66 43,771.64 14,590.55 29,181.10

B (5,396.37) 15,593.31 5,197.77 10,395.54 19,651.36 30,046.90 10,015.63 20,031.27

C (7,422.36) 21,447.58 7,149.19 14,298.39 27,029.16 41,327.54 13,775.85 27,551.69

D (6,145.55) 17,758.13 5,919.38 11,838.76 22,379.56 34,218.32 11,406.11 22,812.21

E (6,293.12) 18,184.55 6,061.52 12,123.03 22,916.95 35,039.98 11,679.99 23,359.99

F (4,338.17) 12,535.53 4,178.51 8,357.02 15,797.82 24,154.84 8,051.61 16,103.22

TOTAL ALL (37,457) 108,235 36,078 72,157 136,402 208,559 69,520 139,039

11/2/2010

24

The Morey Organization ROIC Incentive Individualized Worksheet

Overall Assumptions:

1) ROIC return on invested Capital over target:

First $100,000 into Bonus pool at Dollar for

Dollar

Over $100,000, 20% of each dollar into

Bonus Pool

2) ROIC Return less than target:

First $100,000 deducted from Bonus pool at

Dollar for Dollar

20% of each dollar over $100,000 taken

away from Bonus Pool

3) Percentage of participation based on each

individuals base pay as a percent of all eligible

participants

Prepared for: Employee A

Percent of Bonus Dollars 21.0%

ROIC Bonus Program Scenario

Year A

NOPAT 1,337,498

Invested Capital @ End of Year 12,672,400

NOPAT/IC (Calculated) 10.55%

NOPAT/IC (Minimum Base) 10.00%

NOPAT 1,337,498

NOPAT/IC 10.55%

Dollars exceeding (under) base 70,258

Dollars available

First dollar 70,258

20% of remainder -

Bonus Dollars Earned Overall 70,258

Individualized Results for A:

Bonus Dollars Earned by Individual 14,745

Redistribution of 50% of monies due to new participants -

Starting or Prior Year Balance carried forward 20,988

Accumulated balance 35,733

Annual distribution for 2009 Year (1/3 of accumulated balance) (11,911)

Net carryforward 23,822

The Morey Organization ROIC Incentive Individualized Worksheet

Prepared for: Employee B

Projected % of 2009 Bonus Dollar Earnings for B 14.4%

ROIC Bonus Program Scenario 2009

NOPAT 1,337,498

Invested Capital @ End of Year 12,672,400

NOPAT/IC (Calculated) 10.55%

NOPAT/IC (Minimum Base) 10.00%

NOPAT 1,337,498

NOPAT/IC 10.55%

Dollars exceeding (under) base 70,258

Dollars available

First dollar 70,258

20% of remainder -

Bonus Dollars Earned Overall 70,258

Individualized Results for B:

Bonus Dollars Earned by Individual 10,122

Redistribution of 50% of monies due to new participants -

Starting or Prior Year Balance carried forward 14,407

Accumulated balance 24,529

Annual distribution for 2009 Year (1/3 of accumulated balance) (8,176)

Net carryforward 16,353

Overall Assumptions:

1) ROIC return on invested Capital over target:

First $100,000 into Bonus pool at Dollar

for Dollar

Over $100,000, 20% of each dollar into

Bonus Pool

2) ROIC Return less than target:

First $100,000 deducted from Bonus pool

at Dollar for Dollar

20% of each dollar over $100,000 taken

away from Bonus Pool

3) Percentage of participation based on each

individuals base pay as a percent of all eligible

participants

11/2/2010

25

Conclusion

MAKE YOUR KEY PLAYERS PARTNERS IN

SUCCESSFULLY GROWING THE BUSINESS

QUESTIONS AND ANSWER PERIOD

CONCLUSION

THANK YOU!