Craft Distilling 2016 white paper update - Axis of...

9

The U.S. Craft Distilling Market: 2016 Update © Michael Kinstlick, CEO, Coppersea Distilling, LLC No reproduction without permission. http://www.coppersea.com This brief is an update to the White Paper I released in April, 2012, “The U.S. Craft Distilling Market: 2011 and Beyond,” and the annual updates that followed. The original paper and subsequent updates are available here: http://bit.ly/HxUwj1.

Transcript of Craft Distilling 2016 white paper update - Axis of...

TheU.S.CraftDistillingMarket:2016Update

©MichaelKinstlick,CEO,CopperseaDistilling,LLC

Noreproductionwithoutpermission.http://www.coppersea.com

ThisbriefisanupdatetotheWhitePaperIreleasedinApril,2012,“TheU.S.CraftDistillingMarket:2011andBeyond,”andtheannualupdatesthatfollowed.Theoriginalpaperandsubsequentupdatesareavailablehere:http://bit.ly/HxUwj1.

IntroductionInearly2012,whenthenumberofUSCraftdistilleriesatyear-end2011hadonlyjustpassed200,IpredictedthatthenumberofUScraftdistillerieswouldreach1,000by2020.IcanconfidentlysaythatIwaswrongandthatbyyear-end2016thenumberofin-productionUScraftdistilleriescrossedthatmark.WebaseournumbersonarigorousanalysisofalllistingsintheADI’sannualdirectory,and,beginningwithlastyear’sreport,astatisticalsamplingoftheDSPlistingsintheTTB“Producers&Bottlers”fileavailableonline.Webelievethisproducesthemostaccurateestimateofthetruenumberofoperating,productioncraftdistilleriesintheUnitedStates.However,wealsoconcedethatitisstillanestimateandacknowledgethatthedynamismofthemarketmeansthatnewentrantsandexitswillchangethe“true”numberonadailybasis.Iamalsorigorousintryingtolimitmydefinitiontoproductiondistilleries,thosedistillingspiritfromrawingredients,notinfusingliqueursorAmari,orblendingfromspiritmadeelsewhere.Weestimatethattherewere1,043productioncraftdistilleriesattheendof2016.DSPListingsTherateofnewDSPformationcontinuedin2016atitsrecentannualrateof350/year.Chart1:DSPGrowthsince2010(fromTTBProducersandBottlersfile)

Lastyearweobservedthatapproximately60%ofnewDSPlistingseventuallygoontobecomeoperatingcraftentrants.(Othersarenon-craftfacilitiesfromthe“majors,”someare

wineriesorbreweriesthatmaywanttoprocessspirits,whileothersareintendedentrantswhonevergetpastthisstep.)Theadditionalyear’s“seasoning”onpreviousfilesshowsongoingentrantgrowthasexpected.Olderfiles(2011-13)showvirtuallynoadditionalentrants,suggestingthatthe“window”fornewDSPholderstogetintoproductionisapproximately2yearsafterfirstappearingbeforetheycanbedeemedtohavefallenbythewayside.

ProdCraft ProdCraft DSP Annual USCraft As% @60%final

FileDate Months Adds Rate Producers NewDSPs Unseen12/1/11 13 149 135 84 56% 8/1/12 8 122 180 78 64% 3/1/13 7 148 251 84 57% 6/1/14 15 413 325 192 46% 563/1/15 9 299 394 108 36% 712/1/16 11 324 346 68 21% 12612/1/16 10 302 358 16 5% 165Thefinalcolumnimpliesover400“expected”entrants,assumingthepoolofnewDSPlistingsfromthelatergroupsissimilartothoseprecedingand~60%goontobecomeproducers.However,wealsonotethattheannualrateofnewDSPsincreasessignificantly,andsochangingmarketopportunitiescouldcausetheultimatepercentageoflistingswhobecomeentrantstochange(seebelowformore).Soitishighlylikelythat150-175ofthose400+inthe“Unseen”columnarealreadyproducingas“hiddenentrants”andwillbecomeknownovertime.Andanother~250hadyettobeginproduction.Butitisalsotruethatofthe1300newDSPssince2013,morethan300willneverbecomeproducersatall.Chart2:DSPDropRate

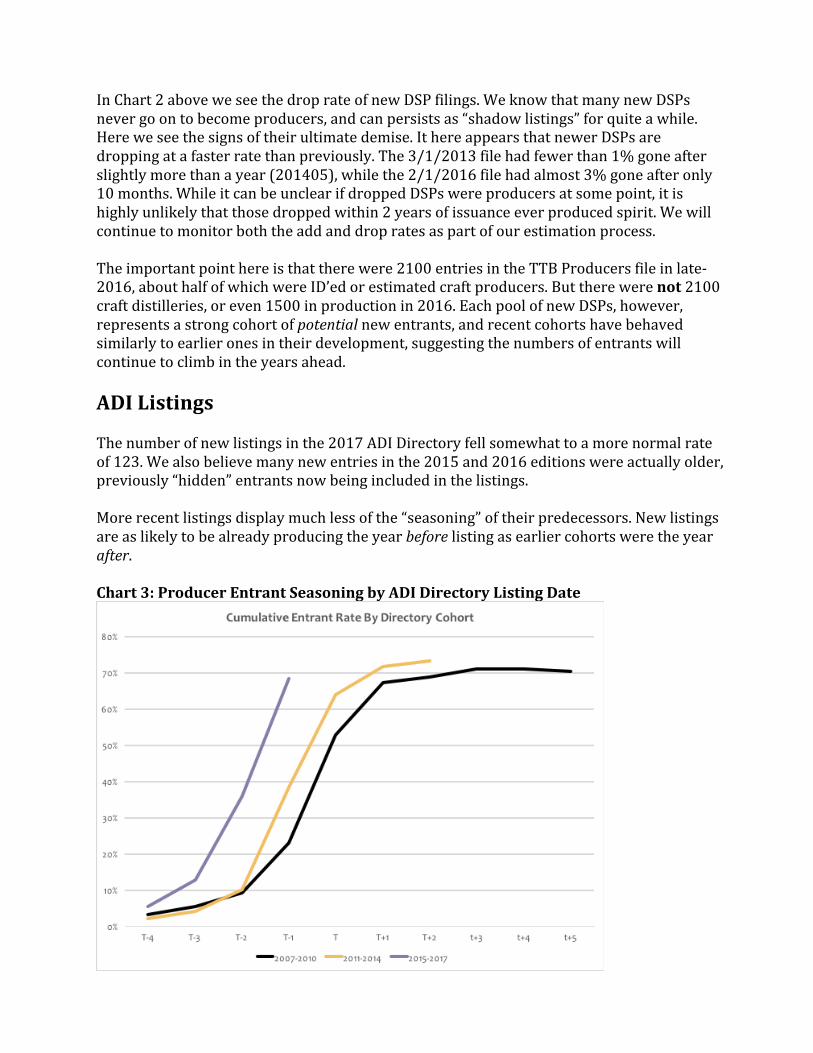

InChart2aboveweseethedroprateofnewDSPfilings.WeknowthatmanynewDSPsnevergoontobecomeproducers,andcanpersistsas“shadowlistings”forquiteawhile.Hereweseethesignsoftheirultimatedemise.IthereappearsthatnewerDSPsaredroppingatafasterratethanpreviously.The3/1/2013filehadfewerthan1%goneafterslightlymorethanayear(201405),whilethe2/1/2016filehadalmost3%goneafteronly10months.WhileitcanbeunclearifdroppedDSPswereproducersatsomepoint,itishighlyunlikelythatthosedroppedwithin2yearsofissuanceeverproducedspirit.Wewillcontinuetomonitorboththeaddanddropratesaspartofourestimationprocess.Theimportantpointhereisthattherewere2100entriesintheTTBProducersfileinlate-2016,abouthalfofwhichwereID’edorestimatedcraftproducers.Buttherewerenot2100craftdistilleries,oreven1500inproductionin2016.EachpoolofnewDSPs,however,representsastrongcohortofpotentialnewentrants,andrecentcohortshavebehavedsimilarlytoearlieronesintheirdevelopment,suggestingthenumbersofentrantswillcontinuetoclimbintheyearsahead.ADIListingsThenumberofnewlistingsinthe2017ADIDirectoryfellsomewhattoamorenormalrateof123.Wealsobelievemanynewentriesinthe2015and2016editionswereactuallyolder,previously“hidden”entrantsnowbeingincludedinthelistings.Morerecentlistingsdisplaymuchlessofthe“seasoning”oftheirpredecessors.Newlistingsareaslikelytobealreadyproducingtheyearbeforelistingasearliercohortsweretheyearafter.Chart3:ProducerEntrantSeasoningbyADIDirectoryListingDate

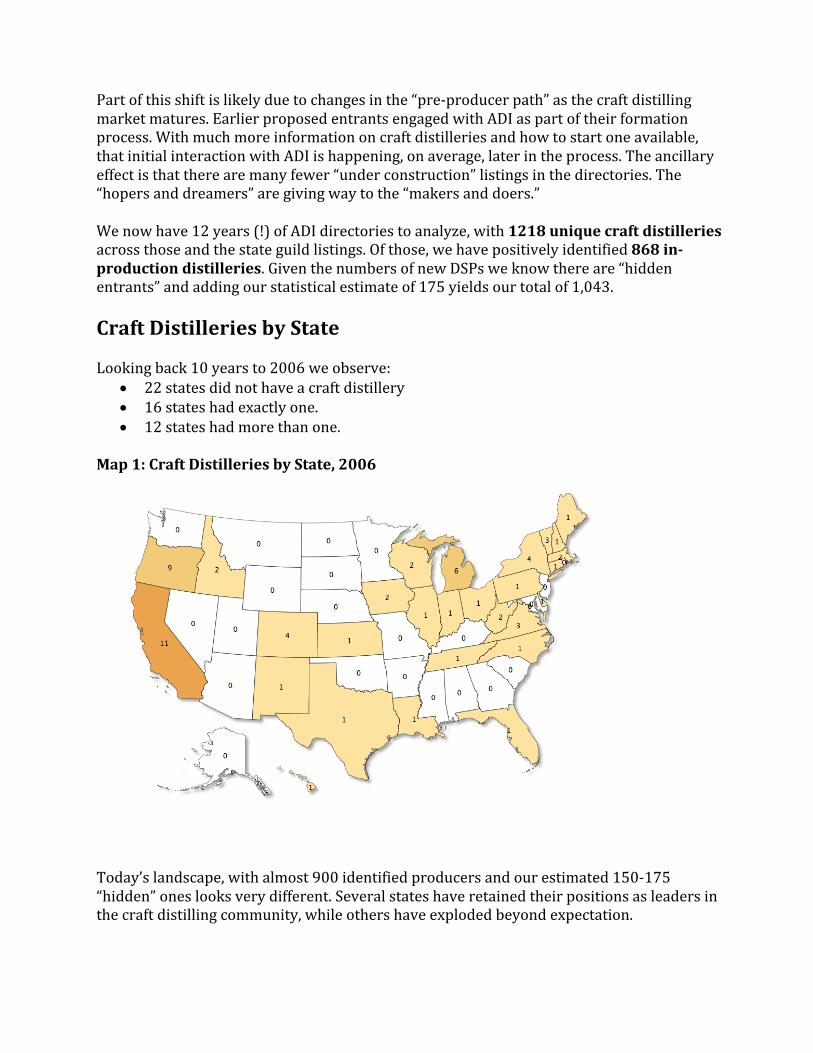

Partofthisshiftislikelyduetochangesinthe“pre-producerpath”asthecraftdistillingmarketmatures.EarlierproposedentrantsengagedwithADIaspartoftheirformationprocess.Withmuchmoreinformationoncraftdistilleriesandhowtostartoneavailable,thatinitialinteractionwithADIishappening,onaverage,laterintheprocess.Theancillaryeffectisthattherearemanyfewer“underconstruction”listingsinthedirectories.The“hopersanddreamers”aregivingwaytothe“makersanddoers.”Wenowhave12years(!)ofADIdirectoriestoanalyze,with1218uniquecraftdistilleriesacrossthoseandthestateguildlistings.Ofthose,wehavepositivelyidentified868in-productiondistilleries.GiventhenumbersofnewDSPsweknowthereare“hiddenentrants”andaddingourstatisticalestimateof175yieldsourtotalof1,043.CraftDistilleriesbyStateLookingback10yearsto2006weobserve:

• 22statesdidnothaveacraftdistillery• 16stateshadexactlyone.• 12stateshadmorethanone.

Map1:CraftDistilleriesbyState,2006

Today’slandscape,withalmost900identifiedproducersandourestimated150-175“hidden”oneslooksverydifferent.Severalstateshaveretainedtheirpositionsasleadersinthecraftdistillingcommunity,whileothershaveexplodedbeyondexpectation.

Map2:CraftDistilleriesbyState,2016

California’ssheersizehaskeptitnearthefront,andColorado,NewYork,andOregonhavesimilarlymaintainedtheirrole.TheSoutheasternstateswithastronghistoricalassociationwithfolkdistilling(ie.,moonshining)havegrowntheirnumbersmorerecently,butithastakenchangestoProhibition-eralawsatthestateleveltoacceleratethosedevelopments.TheincredibleoutlierhereisWashington,whichwentfromZEROcraftdistilleries10yearsagotoalmost100todayandthemostinthecountry.MarketGrowth&TrendsWewerethefirsttopresentthedatashowingthecraftdistillerymarketfollowingontheheelsofthecraftbeermarketwithabouta20-yearlag.Lastyearwestartedexploringthequestionof“exits.”Althoughwearen’tpresentingupdatedanalysisthisyear,webelievethatmarginalproducersarealreadystartingtofadeintothebackground.Whenadistillerygetsup-and-runningtheyusuallymakesomefanfareonFaceBookortheirwebsite.Whentheyquietlyceaseoperations,itcantakesometimebeforetheevidenceisclear:firstalackofsocialmediaupdates,thenanexpiredwebsite,andfinallyapulledDSP.Thecraftbeermarketstartedseeingexitsintheearly-90s,justasthecraftdistillerymarketisnow.Thenthenumberofnewentrantscontinuedtodominateuntilthelate-90s/early-00swhenexitswentup&entrantsdeclinedandpredictionswereforthe“endofcraftbeer.”Andthenthenumberofbreweriestripledafter2010.Sowhilewebelievethenumberofcraftdistilleryexitswillaccelerate,wealsobelievethenumberofnewentrantswaitinginthepipelinewillcontinuetodominateforseveralyears.Andthatbroadermarkettrendsaroundsmallerbrandswillcontinuetosupportthecraftdistillers.

Chart4:Revisions&HiddenEntrants

Wesawextraordinarygrowthinnumbersofidentifiedcraftproducersoverthelasttwoyearsoftheanalysis.Partofthatisduetothenaturalgrowthinthemarketandpartwasdueto“catchup”inoursourcesandmethods.Therewereabout200newlistingsintheADIDirectoriesin2015and2016;webelievethatthiswasaone-timeanomalyastheADIsoughttolistentrantsithadmissed.Thisyearsawonly123newdirectorylistings,andweexpectWearenowaccountingforthose“hidden”producerswehavereasonablestatisticalassuranceareoutthere,buthavenotyetpositivelyidentified,andweexpectthiswillproducemuchsmallerrevisionsgoingforward.ComparisonwithCraftBrewingMarketAsnotedpreviously,aftertorridinitialgrowththecraftbeermarketsawaperiodofconsolidationand“churn”betweenentrants&exitsbeforefindingnewenergyandskyrocketingagain.

Chart5:CraftDistillersvs.CraftBrewers(fromIndustryFoundingDate)

Thegrowthfrom1200breweries10yearsagoto5000todayhasbeenunprecedented,especiallygiventhebroadavailabilityofexcellentproducts.Moremicrobreweriesalonehaveopenedinthepast2yearsthantherearecraftdistilleriesinoperationtoday.ConclusionAfterdecadesofconsolidationtoahandfulofplayers,socialmoresaroundalcoholconsumption,consumerdesiresformoreflavorfulandhand-craftedproducts,andchangesinregulationjump-startedthecraftbeermovement40yearsago.Thosechangesfoundtheirwaytothespiritsbusinessandsimilarlyimpelledthecraftdistilleryboom.Wearealreadyseeingthenaturaloutcomeofarapidlygrowingmarketofyoungstart-upsinexitsanddroppedDSPs.Butwhiletheremaybeconsolidationamongweakerentrantswithlessproductdifferentiation,thereisnoreasontobelievewehavereached“peakcraft”inthespiritsmarket.Inthecraftbeermarket,theearly-00’sconsolidationdidn’tmeanalackofnewentrants,onlythatthenumberofexitsexceededentrantsforawhile.Ittookthecraftbeermarket15yearstogofrom1000entrantsto2000,andonly5yearsfromthereto5000.

Arecent(Sept2017)TTBProducersandBottlersfileshowedanincreaseofover350listings,implyinganannualrateofover400,and250newentrants(togowiththe400alreadynoted)assumingthesame60%entryrate.Thisrobustpipelineofpotentialnewentrantssuggestscontinuedgrowthinnumbers,likelytobesomewhatoffsetbyexitsandclosingsgoingforward.Althoughthecraftdistillerymarkethasexperiencedtorridgrowth,Ibelievethenextphasewillbesomewhatmodulatedasthemarketandconsumersabsorbandprocessallthenewentrants.