CPA 1 Hour CPE Class

24

THE AFFORDABLE HOUSING TAX CREDIT PROGRAM Presented by Dauby O’Connor & Zaleski, LLC and Midwest Housing Equity Group

-

Upload

midwest-housing-equity-group-inc -

Category

Documents

-

view

772 -

download

0

Transcript of CPA 1 Hour CPE Class

THE AFFORDABLE

HOUSING TAX CREDIT

PROGRAM

Presented by Dauby O’Connor & Zaleski, LLC and Midwest Housing Equity Group

Panelists

Jeff LathropDauby O’Connor & Zaleski, LLC

Jim RiekerMidwest Housing Equity Group, Inc.

Background

The Tax Reform Act of 1986 signed by President Reagan Curbed tax shelters and introduced Section 42

Pre-1986 multifamily housing developments sold to individual investors

Post-1986 Section 42 multifamily housing developments sold to corporate investors

Market for LIHTC was very slim 1987-1989 with tax credits rotting on the vine

The Omnibus Budget Reconciliation Act of 1993 signed by President Clinton – made the LIHTC permanent From 1987 through August 1993, the LIHTC program was subject to

various sunsets

Tax Credit Pricing

1987

1991

1995

1999

2003

2007

2009

0

0.2

0.4

0.6

0.8

1

1.2 Initially investors were any

corporation looking for a good return

Many corporate controllers/ treasurers were skeptical of an unproven product LIHTC

Result – pricing was in the mid .40 range in 1987-1988 producing 20%+ IRR

Early in mid-1990s – Financial institutions embrace LIHTC

Banks, GSE’s – fair return plus Community Reinvestment Act (CRA) credit

Tax Credit Pricing

1987

1991

1995

1999

2003

2007

2009

0

0.2

0.4

0.6

0.8

1

1.2 2000-2007 – Substantially all

of the LIHTC purchased by financial institutions and GSE’s

2008 – Sub-Prime mortgage crisis followed by full scale financial meltdown – Investors retreat Housing and Economic

Recovery Act of 2008 intended to boost returns bringing non-financial investors to the LIHTC market

2009 – Many 2007 and 2008 deals unfunded and little prospect for 2009 American Recovery &

Reinvestment Act intended to jumpstart the LIHTC industry

Legislative Movements

HERA of 2008 The Housing and Economic Recovery Act of 2008 signed by President

Bush on July 30, 2008

ARRA of 2009 The American Recovery & Reinvestment Act of 2009 signed by

President Obama on February 17, 2009

HERA of 2008

Temporary provisions: Increase in-state LIHTC allocation authority by 10% = .20 (per capita)

for 2008 and 2009 In 2010 credit authority returns to the 2008 amount $2.00 indexed for

inflations

Additional $11 billion nationally of Tax-Exempt Housing Bonds in 2008 (additional 38.6% for each state)

Authority to issue bonds may be carried forward to 2010

Temporarily fix at 9% the credit rate for new construction and substantial rehabilitation costs

Effective for buildings placed into service after July 30, 2008 and before December 31, 2013

The 9% credit as it is called was the rate in 1987 that provided on a present value basis 70% of new construction or rehabilitation costs; thereafter, the rate was adjusted monthly based on prevailing interest rates. The rate in July 2008 was 7.93%; the November 2009 rate is 7.76%. This provision increases credits otherwise allocable for these properties by 13% to 15%.

HERA of 2008 (continued)

Permanent provisions: Alternative Minimum Tax (AMT) Relief

LIHTC offset AMT for buildings placed into service after December 31, 2007. AMT was an issued for many smaller C corporations.

Example: Widely used C Corp. with $5M of taxable income and no other AMT adjustments could use $700,000 in LIHTC under prior law; now is can use $1,581,250 (an increase of 83%)

HUD Moderate Rehabilitation projects are no longer prohibited from participation in the LIHTC program. Effective for buildings placed into service after July 30, 2008.

The 10-year hold provision for acquisition credits is no longer applicable to federally or state assisted buildings. HUD Section 8, 221(d)3, 221(d)4, 236 and RD section 515 properties and similarly assisted properties under various state programs.

Verify with state HFA for guidance respective as each state’s interpretation may vary

Allowable Related Party interest in subsequent ownership is increased to 50% from 10%.

This will facilitate acquisition rehabilitation projects where the GP remains in the acquiring LP

HERA of 2008 (continued)

Permanent provisions (continued): 30% basis boost previously allowed for properties located in qualified

census tracts or difficult to develop areas is allowed for any project that needs additional credits to be financially feasible as determined by the state housing finance agencies. Apples to projects placed in service after July 30, 2008. Does not apply to Tax Exempt bond financed properties.

The definition of federal subsidy no longer includes “or any below market federal loan” allowing HOME, RD and section 515 projects to utilize the 9% credit for new construction or substantial rehabilitation costs. Tax Exempt bond financed projects are still limited to the 4% tax credit.

Federal Grants received after construction no longer reduce tax credit basis – relief for IRP financed deals and other properties receiving federal operating subsidies.

Allowable eligible basis for community service facilities increased to 25% of total cost up to $15M; plus 10% of total cost in excess of $15M.

HERA of 2008 (continued)

Permanent provisions (continued): Minimum threshold to qualify for substantial rehabilitation is

increased to $6,000 per unit or 20% of acquisition basis from $3,000 or 10%. Indexed for inflation going forward.

LIHTC bond posting requirement is eliminated provided investor agrees to extend statute of limitations to three years after IRS notification.

Extends the time period to satisfy the 10% cost incurred test necessary for carryover to 1 year from 6 months.

Tax Exempt Bond rules now mirror LIHTC rules – Next available unit, Full time student, and Single room occupancy.

Tenant re-certifications no longer required for 100% LIHTC properties.

Example

Change in Maximum Credits due to 9% and Basis Boost:

Adjusted Eligible Basis 10,000,000 10,000,000

X 130% Basis Boost 100% 130%

X Applicable Percentage 7.94% 9.00%

= Total Annual Credits 794,0001,170,000

X 10 Years (Total Credits) 7,940,000 11,700,000

47.35% Increase

Obviously, HERA put substantially more resources on the table to attract other non-financial investors back into the LIHTC market.

ARRA of 2009

Not withstanding the tremendous resources included in the HERA legislation to boost the LIHTC industry, many 2007 and most 2008 allocated properties had not closed due to the frozen LIHTC market. In response to this, ARRA included provisions to “jump start” stalled projects. Section 1602: Grants to States for Low-Income Housing Projects in

Lieu of Low-Income Housing Credits aka the “Credit Exchange Program”

State HFA’s have the ability to exchange eligible LIHTC allocations with Treasury for $0.85 per dollar of credit allocation exchanged. The proceeds from the exchange are to be used by the HFA to provide funds to projects with or without an allocation of LIHTC in the form of grants or forgivable loans.

ARRA of 2009 (continued)

The amount of LIHTC an HFA may exchange for $0.85 is equal to the following: 100% of the state housing credit ceiling for 2009 attributable to

unused and returned credits from the 2008 housing credit ceiling plus any amount of state housing credit ceiling returned in 2009. (This provisions applies to 2007 and 2008 allocations).

40% of the state housing credit ceiling for 2009 attributable to the 2009 ceiling including any amounts reallocated from other states with unallocated credits. Amounts exchanged under this provision serve to reduce the state’s 2009 credit ceiling.

ARRA of 2009 (continued)

Grants or loans received by the project from exchange funds are not includable in taxable income and do not reduce basis. Treat as tax exempt interest income. Treatment at the state level may vary

Funds received cannot exceed 85% of the amount Recipients of exchange funds must demonstrate a good faith effort to obtain private equity commitments. Good faith effort is determined by each state HFA.

of buildings eligible basis including any increase for buildings located in high cost areas. Direct tracing is not required.

Funds received under this program must be expended by December 31, 2011 – originally this date was December 31, 2010

ARRA of 2009 (continued)

Funds may be used in a development with Tax Exempt bond financing

Exchange does not mean one for one – funds obtained by a HFA from credits returned by one project may be used to fund other projects.

Eligible buildings must not be placed into service prior to 2009; however, substantially complete buildings are eligible. In this case, exchange funds can be used to repay equity or construction loans.

State HFA’s must provide a recapture provision on any sub-award to assure compliance.

ARRA of 2009 (continued)

Title VII – Tax Credit Assistance Program (TCAP) Appropriated $2.25 billion under the HOME Investment Partnerships

program for a grant program to provide funds for capital investments in Low-Income Housing Tax Credit projects.

Eligible projects are those receiving LIHTC award under Section 42(h) or 1400N during the period October 1, 2006 through September 30, 2009.

Funds are intended to address funding gaps created by diminished investor demand for LIHTC.

TCAP funds may be used for eligible basis items.

Most HOME requirements do not apply, except for environmental review. Other cross cutting federal requirements do apply – Davis Bacon, Fair Housing, Accessibility and others.

Tax Credit Syndicator - MHEG

Non-profit organization established in 1993 at the request of Governor Ben Nelson - rural areas underserved

Mission: Change lives for a better tomorrow by promoting the development and sustainability of quality affordable housing

Service area today includes Nebraska, Kansas, Iowa and Oklahoma

MHEG Profile

Our developments range from 6 to over 200 units and include: single family homes

multi-unit and multi-building complexes

duplexes

historical renovations

specialty needs developments: elderly, assisted living, transitional homeless facilities, and developmentally disabled residents

Number of Developments: 241 Number of Counties Represented: 104

Number of Housing Units: 6,517 Number of Cities Represented: 127

Equity raised: $570 million Current as of

10/31/09

Fund Investment Structure

MHEGTax Credit Syndicator

NF XIV, L.P.Owned 99.99% by

InvestorsOwned 00.01% by MHEG

Investors

NIFATax Credits

Project BLower Tier Partnership

LP/LLC

Owned .01% by Developer/GP

Owned 99.99% by Fund

Project ALower Tier Partnership

LP/LLC

Owned .01% by Developer/GP

Owned 99.99% by Fund

Project CLower Tier Partnership

LP/LLC

Owned .01% by Developer/GP

Owned 99.99% by Fund

CRA Bank Benefits for Banks

Shortage- Allows for CRA credit regardless of project locations as long as it is within the fund’s trade territory (i.e. a Grand Island bank can receive credit for a project in Omaha)*

Regulators do vary on the scope of inclusion. Please check with your Regulator for their interpretation.

See OCC report dated 2/08– further adopted by FDIC and Federal Reserves

By purchasing tax credits in a MHEG fund banks can potentially fulfill the Investment portion of the CRA exam, typically the most difficult portion for most banks to meet, as well as opportunities to meet the lending and service tests.

All documentation that the Examiners require is provided by MHEG.

Typical Deal Structure

Soft Debt / GP Equity

25%*Hard Debt< 20%

Tax Credit Equity 55% (70% with basis

boost)

* Funded By: AHP HOME TCAP Exchange Developer Fee Various Contributions Certain Grants

What is the Real Risk?

Ownership risks of multifamily low-income rental housing pools

Mitigated by MHEG’s investment policies, ongoing management and financial oversight, as well as MHEG’s financial strength

Compliance risk Mitigated by MHEG’s continuing compliance practices and

oversight

Changes in current law Highly improbable any law change would affect any current

investments

Reputation Risk We take “the high road”, we know that we represent our

fund participants who are financial pillars of their communities

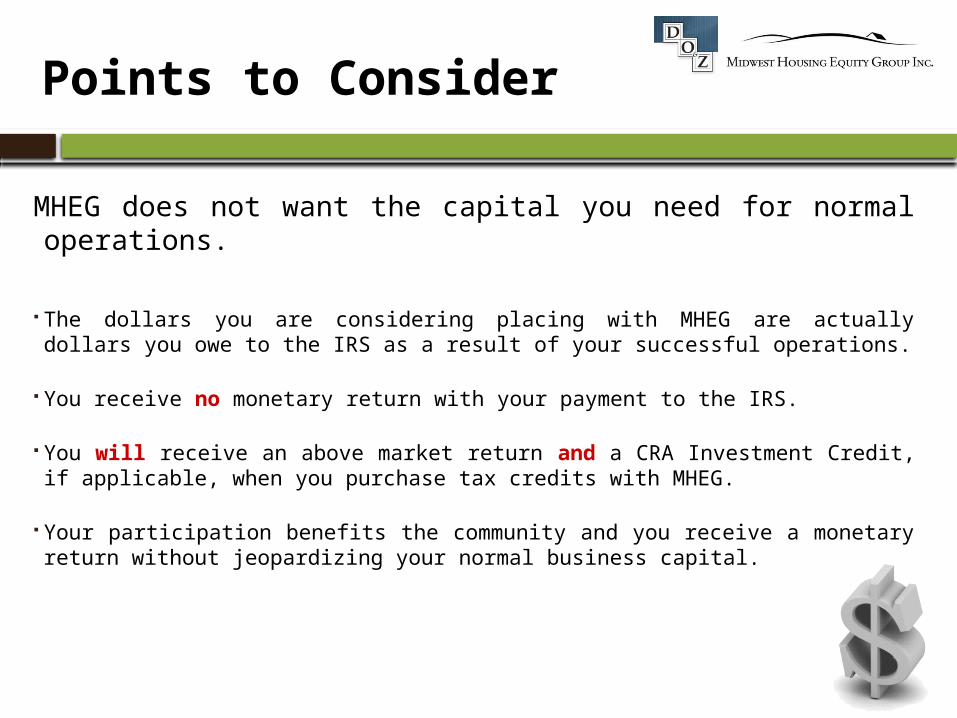

Points to Consider

MHEG does not want the capital you need for normal operations.

The dollars you are considering placing with MHEG are actually dollars you owe to the IRS as a result of your successful operations.

You receive no monetary return with your payment to the IRS.

You will receive an above market return and a CRA Investment Credit, if applicable, when you purchase tax credits with MHEG.

Your participation benefits the community and you receive a monetary return without jeopardizing your normal business capital.

Questions???