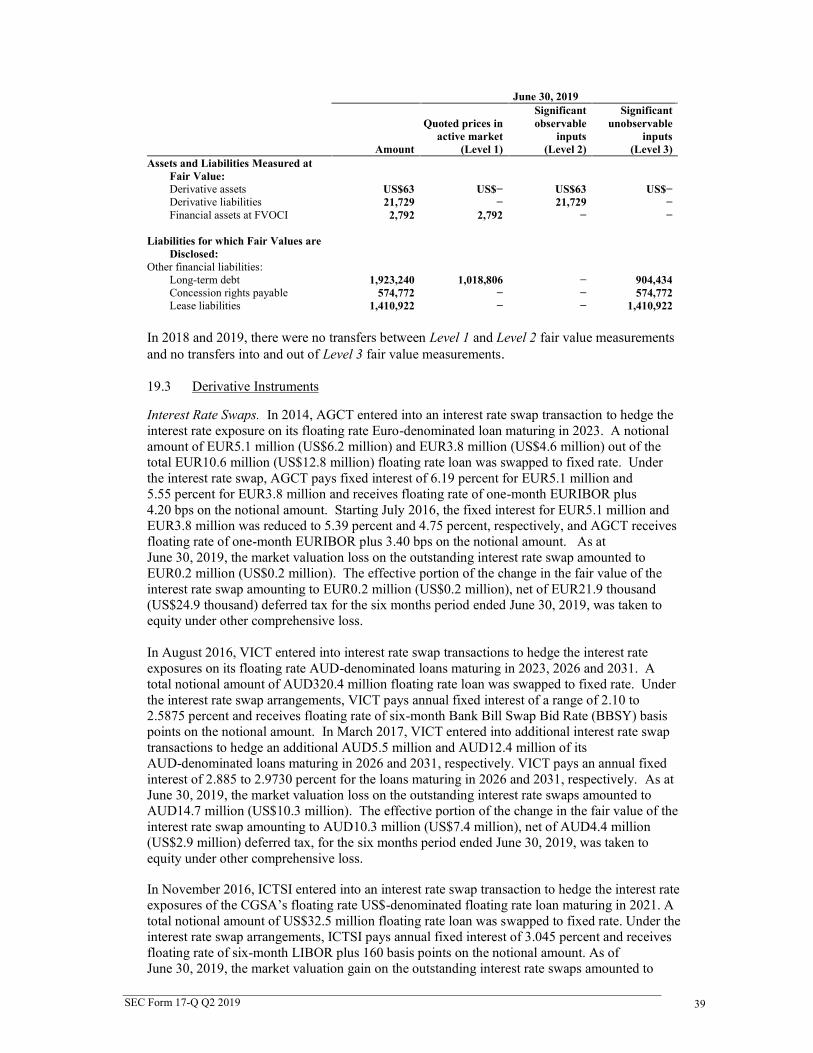

COVER SHEET - links.sgx.com

78

ICTSI Form 17-Q Q2 2019 1 4 7 2 1 2 SEC Registration Number I N T E R N A T I O N A L C O N T A I N E R T E R M I N A L S E R V I C E S , I N C . A N D S U B S I D I A R I E S (Company’s Full Name) I C T S I A D M I N I S T R A T I O N B U I L D I N G , M A N I L A I N T E R N A T I O N A L C O N T A I N E R T E R M I I N A L S O U T H A C C E S S R O A D , M A N I L A A (Business Address: No. Street City/Town/Province) Jose Joel M. Sebastian 245-4101 (Contact Person) (Company Telephone Number) 1 2 3 1 S E C 17 Q 0 4 Every 3 rd Thursday Month Day (Form Type) Month Day (Fiscal Year) (Annual Meeting) N/A (Secondary License Type, If Applicable) N/A Dept. Requiring this Doc. Amended Articles Number/Section Total Amount of Borrowings 1,378 as at June 30, 2019 US$332.9M US$1,535.1M Total No. of Stockholders Domestic Foreign To be accomplished by SEC Personnel concerned File Number LCU Document ID Cashier S T A M P S Remarks: Please use BLACK ink for scanning purposes. COVER SHEET

Transcript of COVER SHEET - links.sgx.com

ICTSI Form 17-Q Q2 2019

1 4 7 2 1 2SEC Registration Number

I N T E R N A T I O N A L C O N T A I N E R T E R M I N A L

S E R V I C E S , I N C . A N D S U B S I D I A R I E S

(Company’s Full Name)

I C T S I A D M I N I S T R A T I O N B U I L D I N G , M A

N I L A I N T E R N A T I O N A L C O N T A I N E R T E R MII N A L S O U T H A C C E S S R O A D , M A N I L AA

(Business Address: No. Street City/Town/Province)

Jose Joel M. Sebastian 245-4101(Contact Person) (Company Telephone Number)

1 2 3 1 S E C 17 Q 0 4 Every 3rd ThursdayMonth Day (Form Type) Month Day

(Fiscal Year) (Annual Meeting)

N/A(Secondary License Type, If Applicable)

N/ADept. Requiring this Doc. Amended Articles Number/Section

Total Amount of Borrowings

1,378as at June 30, 2019 US$332.9M US$1,535.1M

Total No. of Stockholders Domestic Foreign

To be accomplished by SEC Personnel concerned

File Number LCU

Document ID Cashier

S T A M P S

Remarks: Please use BLACK ink for scanning purposes.

COVER SHEET

ICTSI Form 17-Q Q2 2019

SECURITIES AND EXCHANGE COMMISSION

SEC FORM 17-Q

QUARTERLY REPORT PURSUANT TO SECTION 17 OF THESECURITIES REGULATION CODE AND SRC RULE 17(2)(b) THEREUNDER

1. For the quarterly period ended June 30, 2019

2. Commission identification number: 147212

3. BIR Tax Identification No. 000-323-228

1. Exact name of issuer as specified in its charter:INTERNATIONAL CONTAINER TERMINAL SERVICES, INC.

5. Province, Country or other jurisdiction of incorporation or organization: Philippines

6. Industry Classification Code: ___________________ (SEC Use Only)

7. Address of issuer’s principal office: ICTSI Administration Building, Manila InternationalContainer Terminal, South Access Road, Manila Postal Code: 1012

8. Registrant's telephone number, including area code: (632) 245-4101

9. Former name, former address, and former fiscal year: Not applicable

10. Securities registered pursuant to Sections 8 and 12 of the Code, or Sections 4 and 8 of the RSA.

Title of Each ClassNumber of shares outstanding

as at June 30, 2019

Common 2,013,633,338 Shares

11. Are any or all of the Securities listed on a Stock Exchange?Yes [x] No [ ]

If yes, state the name of such Stock Exchange and the class/es of securities listed therein:Philippine Stock Exchange Common shares

12. Indicate by check mark whether the issuer:

a) has filed all reports required to be filed by Section 17 of the Code and SRC Rule 17 thereunder orSections 11 of the RSA and RSA Rule 11(a)-1 thereunder, and Sections 26 and 141 of The CorporationCode of the Philippines during the preceding 12 months (or for such shorter period that the registrantwas required to file such reports).

Yes [x] No [ ]

(b) has been subject to such filing for the past 90 days. Yes [x] No [ ]

ICTSI Form 17-Q Q2 2019

TABLE OF CONTENTS

PART 1 – FINANCIAL INFORMATION........................................................................................ 1

Item 1. Financial Statements............................................................................................... 1

Consolidated Balance Sheet as at December 31, 2018, as Restated, andUnaudited Interim Consolidated Balance Sheet as at June 30, 2019....................... 3

Unaudited Interim Consolidated Statements of Income for theThree and Six Months Ended June 30, 2018 and 2019 ........................................... 4

Unaudited Interim Consolidated Statements of Comprehensive Income for theThree and Six Months Ended June 30, 2018 and 2019 ........................................... 5

Unaudited Interim Consolidated Statements of Changes in Equity for theSix Months Ended June 30, 2018 and 2019 ............................................................ 6

Unaudited Interim Consolidated Statements of Cash Flows for theSix Months Ended June 30, 2018 and 2019 ............................................................ 8

Notes to Unaudited Interim Condensed Consolidated Financial Statements ..................... 10

Item 2. Management’s Discussion and Analysis or Plan of Operations ............................ 41

PART II – OTHER INFORMATION ............................................................................................. 68

ANNEX 1 – Schedule of Aging of Receivables.............................................................................. 69

ANNEX 2 – Financial Soundness Indicators ................................................................................. 70

ANNEX 3 – List of Effective PFRS Standards and Interpretations .............................................. 71

ANNEX 4 – Map of Subsidiaries ................................................................................................... 74

SIGNATURES ................................................................................................................................ 75

ICTSI Form 17-Q Q2 2019 1

PART 1 – FINANCIAL INFORMATION

Item 1. Financial Statements

The consolidated balance sheet as at December 31, 2018, as restated, and the unaudited interimcondensed consolidated financial statements as at June 30, 2019 and for the three and six monthsended June 30, 2018 and 2019 and the related notes to unaudited interim condensed consolidatedfinancial statements of International Container Terminal Services, Inc. and Subsidiaries (collectivelyreferred to as “the Group”) are filed as part of this Form 17-Q on pages 2 to 40.

Operating segments are also reported in the notes to unaudited interim condensed consolidatedfinancial statements.

There are no other material events subsequent to the end of this interim period that have not beenreflected in the unaudited interim condensed consolidated financial statements filed as part of thisreport.

ICTSI Form 17-Q Q2 2019 2

International Container Terminal Services, Inc.and Subsidiaries

Unaudited Interim Condensed Consolidated Financial StatementsAs at June 30, 2019(with Comparative Figures as at December 31, 2018, as Restated)and for the Three and Six Months Ended June 30, 2018 and 2019

ICTSI Form 17-Q Q2 2019 3

INTERNATIONAL CONTAINER TERMINAL SERVICES, INC.AND SUBSIDIARIESUNAUDITED INTERIM CONSOLIDATED BALANCE SHEETSAs at June 30, 2019(With Comparative Figures as at December 31, 2018, as Restated)(In Thousands)

December 31, 2018(Restated - Note 3)

June 30, 2019(Unaudited)

ASSETSNoncurrent AssetsIntangibles (Note 5) US$1,965,647 US$2,002,010Property and equipment (Notes 3 and 6) 1,378,184 1,384,495Right-of-use assets (Note 3) 523,328 508,716Investment properties 7,439 7,315Investments in and advances to joint ventures and associates

(Notes 8 and 16) 381,188 447,547Deferred tax assets (Note 3) 248,062 266,156Other noncurrent assets (Notes 1, 7 and 19) 138,884 566,615

Total Noncurrent Assets 4,642,732 5,182,854Current AssetsCash and cash equivalents (Note 9) 447,079 295,585Receivables (Note 10) 120,424 109,653Spare parts and supplies 34,044 35,111Prepaid expenses and other current assets (Note 11) 71,465 91,477Derivative assets (Note 19) 426 60

Total Current Assets 673,438 531,886US$5,316,170 US$5,714,740

EQUITY AND LIABILITIESEquity Attributable to Equity Holders of the ParentCapital stock:

Preferred stock US$236 US$236Common stock 67,330 67,330

Additional paid-in capital (Note 15) 549,382 548,315Cost of shares held by subsidiaries (Note 15) (74,261) (74,261)Treasury shares (Note 15) (58,112) (53,746)Excess of acquisition cost over the carrying value of non-controlling

interests (Note 15) (142,555) (143,026)Retained earnings (Notes 3 and 15) 400,099 297,218Perpetual capital securities (Note 15) 1,153,615 1,018,513Other comprehensive loss - net (Notes 15 and 19) (155,505) (159,892)

Total equity attributable to equity holders of the parent 1,740,229 1,500,687Equity Attributable to Non-controlling Interests (Notes 1 and 15) 165,504 159,024

Total Equity 1,905,733 1,659,711Noncurrent LiabilitiesLong-term debt - net of current portion (Notes 12 and 19) 1,220,487 1,608,820Concession rights payable - net of current portion (Notes 5 and 19) 530,666 521,547Lease liabilities - net of current portion (Note 3) 1,122,563 1,143,042Deferred tax liabilities (Note 3) 57,883 64,471Other noncurrent liabilities (Notes 3 and 13) 32,716 40,365

Total Noncurrent Liabilities 2,964,315 3,378,245Current LiabilitiesLoans payable (Note 12) 35,718 31,568Accounts payable and other current liabilities (Notes 3, 14 and 16) 307,698 349,600Current portion of long-term debt (Notes 12 and 19) 50,848 227,633Current portion of concession rights payable (Notes 5 and 19) 10,603 10,902Current portion of lease liabilities (Note 3) 9,033 10,413Income tax payable 31,607 34,693Derivative liabilities (Note 19) 615 11,975

Total Current Liabilities 446,122 676,784Total Liabilities 3,410,437 4,055,029

US$5,316,170 US$5,714,740

See accompanying Notes to Unaudited Interim Condensed Consolidated Financial Statements.

ICTSI Form 17-Q Q2 2019 4

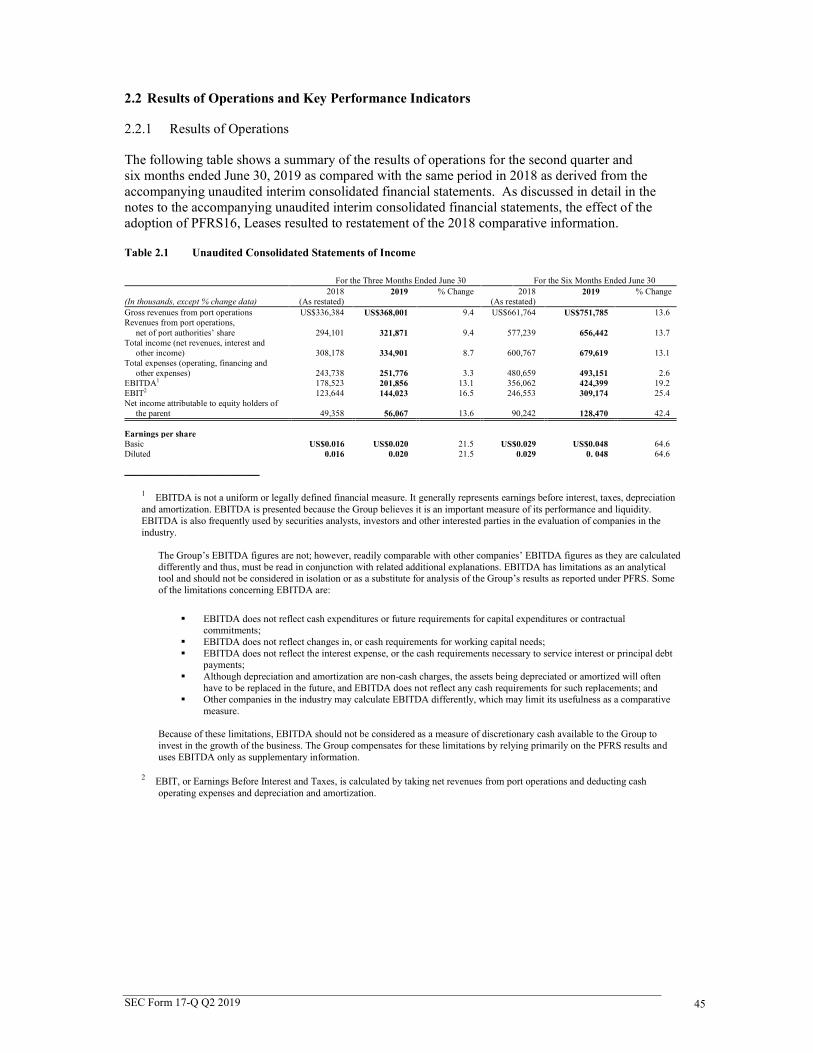

INTERNATIONAL CONTAINER TERMINAL SERVICES, INC.AND SUBSIDIARIESUNAUDITED INTERIM CONSOLIDATED STATEMENTS OF INCOME(In Thousands, Except Per Share Data)

For the Three Months Ended June 30 For the Six Months Ended June 302018

(Restated - Note 3) 20192018

(Restated - Note 3) 2019

INCOMEGross revenues from port operations US$336,384 US$368,001 US$661,764 US$751,785Foreign exchange gain (Note 3) 133 1,319 2,163 2,881Interest income (Notes 9 and 16) 6,353 6,999 12,161 13,101Other income (Note 13) 7,591 4,712 9,204 7,195

350,461 381,031 685,292 774,962

EXPENSESPort authorities’ share in gross revenues

(Notes 3 and 16) 42,283 46,130 84,525 95,343Manpower costs (Notes 15 and 16) 54,655 59,519 107,214 116,831Equipment and facilities-related expenses

(Notes 3 and 16) 29,034 27,934 55,146 54,891Depreciation and amortization (Note 3) 54,879 57,833 109,509 115,225Administrative and other operating expenses

(Note 16) 31,889 32,562 58,817 60,321Interest expense and financing charges on

borrowings (Notes 5, 6 and 12) 25,746 27,976 53,697 53,739Interest expense on concession rights payable

(Note 5) 8,970 9,986 17,038 19,995Interest expense on lease liabilities (Note 3) 26,050 25,859 53,131 51,786Equity in net loss of joint ventures and an

associate (Note 8) 7,578 6,266 16,036 12,398Foreign exchange loss (Note 3) 1,748 516 3,760 2,081Other expenses 3,189 3,325 6,311 5,884

286,021 297,906 565,184 588,494

CONSTRUCTION REVENUE(EXPENSE)

Construction revenue 26,475 41,039 33,702 79,487Construction expense (26,475) (41,039) (33,702) (79,487)

– – – –

INCOME BEFORE INCOME TAX 64,440 83,125 120,108 186,468

PROVISION FOR (BENEFIT FROM)INCOME TAX

Current 17,578 20,786 36,744 44,634Deferred (Note 3) (9,345) (2,226) (20,540) (4,236)

8,233 18,560 16,204 40,398

NET INCOME US$56,207 US$64,565 US$103,904 US$146,070

Attributable ToEquity holders of the parent (Note 3) US$49,358 US$56,067 US$90,242 US$128,470Non-controlling interests 6,849 8,498 13,662 17,600

US$56,207 US$64,565 US$103,904 US$146,070

Earnings Per Share (Notes 3 and 17)Basic US$0.016 US$0.020 US$0.029 US$0.048Diluted 0.016 0.020 0.029 0.048

See accompanying Notes to Unaudited Interim Condensed Consolidated Financial Statements.

ICTSI Form 17-Q Q2 2019 5

INTERNATIONAL CONTAINER TERMINAL SERVICES, INC.AND SUBSIDIARIESUNAUDITED INTERIM CONSOLIDATED STATEMENTS OFCOMPREHENSIVE INCOME(In Thousands)

For the Three Months Ended June 30 For the Six Months Ended June 302018

(Restated – Note 3) 20192018

(Restated – Note 3) 2019

NET INCOME FOR THE PERIOD US$56,207 US$64,565 US$103,904 US$146,070

OTHER COMPREHENSIVE INCOMEItems to be reclassified to profit or loss in

subsequent periodsExchange differences on translation of foreign

operations’ financialstatements (Notes 3 and 15) (44,247) (309) (41,528) 5,647

Net change in unrealized mark-to-market valuesof derivatives (Notes 15 and 19) (2,328) (14,968) 128 (19,409)

Net unrealized mark-to-market gain on available-for-sale investments (Note 15) – (5,928) 88 (66)

Share in other comprehensive gain (loss) of anassociate (Note 15) (2,564) 2,773 (4,191) 2,713

Income tax relating to components of othercomprehensive income(Notes 15 and 19) 206 4,460 (500) 5,363

(48,933) (13,972) (46,003) (5,752)Items not to be reclassified to profit or loss in

subsequent periodsShare in other comprehensive gain (loss) of an

associate (Note 15) (1) – 89 –Actuarial gains (losses) on defined benefit plans -

net of tax (Note 15) 63 – 50 (113)(48,871) (13,972) (45,864) (5,865)

TOTAL COMPREHENSIVE INCOME FORTHE PERIOD US$7,336 US$50,593 US$58,040 US$140,205

Attributable ToEquity holders of the parent (Note 3) US$9,346 US$45,853 US$49,744 US$124,083Non-controlling interests (2,010) 4,740 8,296 16,122

US$7,336 US$50,593 US$58,040 US$140,205

See accompanying Notes to Unaudited Interim Condensed Consolidated Financial Statements.

SEC Form 17-Q Q2 2018 666 6

INTERNATIONAL CONTAINER TERMINAL SERVICES, INC.AND SUBSIDIARIESUNAUDITED INTERIM CONSOLIDATED STATEMENTS OF CHANGES IN EQUITYFOR THE SIX MONTHS ENDED JUNE 30, 2018 and 2019(In Thousands)

Attributable to Equity Holders of the Parent

PreferredStock

CommonStock

AdditionalPaid-inCapital

(Note 15)

PreferredShares Held

by aSubsidiary

(Note 15)

CommonShares Held

by aSubsidiary

(Note 15)

TreasuryShares

(Note 15)

Excess ofAcquisition

Cost over theCarryingValue of

Non-controlling

Interests(Note 15)

RetainedEarnings(Note 15)

PerpetualCapital

Securities(Note 15)

OtherCompre-

hensiveLoss - net

(Notes 3, 15and 19) Total

Non-controlling

Interests(Notes 1 and

15)Total

Equity

Balance at December 31, 2017 US$236 US$67,330 US$547,853 (US$72,492) (US$1,769) (US$15,059) (US$142,555) US$819,668 US$761,341 (US$256,622) US$1,707,931 US$164,638 US$1,872,569Effect of PFRS 16 adoption

(Note 3) – – – – – – – (470,156) – 126,860 (343,296) – (343,296)Balance at December 31, 2017,

as restated 236 67,330 547,853 (72,492) (1,769) (15,059) (142,555) 349,512 761,341 (129,762) 1,364,635 164,638 1,529,273Total comprehensive income for the

period – – – – – – – 90,242 – (40,498) 49,744 8,296 58,040Issuance of perpetual capital

securities (Note 15) – – – – – – – – 392,274 – 392,274 – 392,274Share-based payments (Note 15) – – 2,086 – – – – – – – 2,086 – 2,086Issuance of treasury shares – – (2,277) – – 2,277 – – – – – – –Acquisition of ICTSI common

shares (Note 15) – – – – – (6,090) – – – – (6,090) – (6,090)Cash dividends (Note 15) – – – – – – – (97,584) – – (97,584) (11,184) (108,768)Distributions on perpetual capital

securities (Note 15) – – – – – – – (27,774) – – (27,774) – (27,774)Balance at June 30, 2018 US$236 US$67,330 US$547,662 (US$72,492) (US$1,769) (US$18,872) (US$142,555) US$314,396 US$1,153,615 (US$170,260) US$1,677,291 US$161,750 US$1,839,041

SEC Form 17-Q Q2 2018 777 7

Attributable to Equity Holders of the Parent

PreferredStock

CommonStock

AdditionalPaid-inCapital

(Note 15)

PreferredShares Held

by aSubsidiary

(Note 15)

CommonShares Held

by aSubsidiary

(Note 15)

TreasuryShares

(Note 15)

Excess ofAcquisition

Cost over theCarryingValue of

Non-controlling

Interests(Note 15)

RetainedEarnings(Note 15)

PerpetualCapital

Securities(Note 15)

OtherCompre-

hensiveLoss - net

(Notes 3, 15and 19) Total

Non-controlling

Interests(Notes 1 and

15)Total

Equity

Balance at December 31, 2018 US$236 US$67,330 US$549,382 (US$72,492) (US$1,769) (US$58,112) (US$142,555) US$882,814 US$1,153,615 (US$314,753) US$2,063,696 US$165,504 US$2,229,200Effect of PFRS 16 adoption

(Note 3) – – – – – – – (482,715) – 159,248 (323,467) – (323,467)Balance at December 31, 2018,

as restated 236 67,330 549,382 (72,492) (1,769) (58,112) (142,555) 400,099 1,153,615 (155,505) 1,740,229 165,504 1,905,733Total comprehensive income for the

period – – – – – – – 128,470 – (4,387) 124,083 16,122 140,205Share-based payments (Note 15) – – 3,299 – – – – – – – 3,299 – 3,299Issuance of treasury shares – – (4,366) – – 4,366 – – – – – – –Cash dividends (Note 15) – – – – – – – (194,228) – – (194,228) (15,073) (209,301)Acquisition of non-controlling

interests (Note 15) – – – – – – (471) – – – (471) (7,529) (8,000)Redemption of perpetual capital

securities (Note 15) – – – – – – – (4,584) (135,102) – (139,686) – (139,686)Distributions on perpetual capital

securities (Note 15) – – – – – – – (32,539) – – (32,539) – (32,539)Balance at June 30, 2019 US$236 US$67,330 US$548,315 (US$72,492) (US$1,769) (US$53,746) (US$143,026) US$297,218 US$1,018,513 (US$159,892) US$1,500,687 US$159,024 US$1,659,711

See accompanying Notes to Unaudited Interim Condensed Consolidated Financial Statements.

ICTSI Form 17-Q Q2 2019 8

INTERNATIONAL CONTAINER TERMINAL SERVICES, INC.AND SUBSIDIARIESUNAUDITED INTERIM CONSOLIDATED STATEMENTS OF CASH FLOWS(In Thousands)

For the Six Months Ended June 302018

(Restated – Note 3) 2019

CASH FLOWS FROM OPERATING ACTIVITIESIncome before income tax US$120,108 US$186,468Adjustments for:

Depreciation and amortization 109,509 115,225Interest expense on:

Borrowings (Notes 5, 6 and 12) 53,697 53,739Lease liabilities (Note 3) 53,131 51,786Concession rights payable (Note 5) 17,038 19,995

Equity in net loss of joint ventures and an associate (Note 8) 16,036 12,398Share-based payments (Note 15) 2,075 2,258Interest income (Notes 9 and 16) (12,161) (13,101)Unrealized foreign exchange loss (gain) 171 (1,248)Loss (gain) on sale of property and equipment 171 (89)

Operating income before changes in working capital 359,775 427,431Decrease (increase) in:

Receivables 5,780 9,510Spare parts and supplies (664) (1,404)Prepaid expenses and other current assets (1,887) (20,637)

Increase (decrease) in:Accounts payable and other current liabilities (5,357) (4,753)Pension liabilities 57 878

Cash generated from operations 357,704 411,025Income taxes paid (33,198) (37,337)Net cash provided by operating activities 324,506 373,688CASH FLOWS FROM INVESTING ACTIVITIESAcquisitions of:

Intangible assets (Notes 1 and 5) (83,852) (75,781)Property and equipment (Notes 1 and 6) (42,428) (41,136)

Increase in other noncurrent assets (2,264) (431,164)Additional subscription and acquisition of shares in a joint

venture and an associate (Note 8) – (50,081)Payments of concession rights (Note 5) (38,109) (9,202)Interest received 2,693 4,399Decrease (increase) in advances to joint ventures (Notes 8 and 16) (4,735) 3,593Net proceeds from sale of property and equipment 234 1,055Net cash used in investing activities (168,461) (598,317)

SEC Form 17-Q Q2 2018 999 9

For the Six Months Ended June 302018

(Restated – Note 3) 2019

CASH FLOWS FROM FINANCING ACTIVITIESNet proceeds from:

Long-term borrowings (Note 12) 31,319 590,756Issuance of perpetual capital securities 392,274 –Short-term borrowings (Note 12) 39,726 –

Payments of:Dividends (Note 15) (110,622) (207,648)Interest on borrowings and concession rights payable

(Notes 5 and 12) (66,935) (66,945)Long-term borrowings (Note 12) (183,057) (29,012)Interest on lease liabilities (Note 3) (25,028) (24,814)Short-term borrowings (Note 12) (66,283) (3,990)Lease liabilities (Note 3) (532) (3,399)

Redemption of perpetual capital securities (Note 15) – (139,686)Distributions on perpetual capital securities (Note 15) (27,774) (32,539)Acquisition of non-controlling interest (Note 15) – (8,000)Increase in other noncurrent liabilities (983) (1,148)Acquisition of ICTSI common shares (Note 15) (6,090) –Net cash provided by (used in) financing activities (23,985) 73,575

EFFECT OF EXCHANGE RATE CHANGES ON CASH ANDCASH EQUIVALENTS (9,949) (440)

NET INCREASE (DECREASE) IN CASH AND CASHEQUIVALENTS 122,111 (151,494)

CASH AND CASH EQUIVALENTS AT BEGINNING OF PERIOD 279,427 447,079

CASH AND CASH EQUIVALENTS AT END OF PERIOD (Note 9) US$401,538 US$295,585

See accompanying Notes to Unaudited Interim Condensed Consolidated Financial Statements.

SEC Form 17-Q Q2 2019 1010

INTERNATIONAL CONTAINER TERMINAL SERVICES, INC.AND SUBSIDIARIESNOTES TO UNAUDITED INTERIM CONDENSED CONSOLIDATED FINANCIALSTATEMENTS

1. Corporate Information

1.1 General

International Container Terminal Services, Inc. (ICTSI or the Parent Company) wasincorporated in the Philippines and registered with the Philippine Securities and ExchangeCommission (SEC) on December 24, 1987. The registered office address of the Company isICTSI Administration Building, MICT South Access Road, Manila. ICTSI’s common shareswere listed with the Philippine Stock Exchange (PSE) on March 23, 1992 at an offer price ofP=6.70. ICTSI has 2,013,633,338 common shares outstanding held by 1,378 shareholders onrecord as at June 30, 2019.

1.2 Port Operations

ICTSI and subsidiaries (collectively referred to as “the Group”) entered into various concessionsof port operations which include development, management, and operation of containerterminals and related facilities around the world. As at August 13, 2019, the Group is involvedin 32 terminal concessions and port development projects in 18 countries worldwide. There areeleven terminal operations, including an inland container terminal and a barge terminal in thePhilippines, two each in Indonesia, Papua New Guinea (PNG) and Brazil, one each in China,Ecuador, Poland, Georgia, Madagascar, Croatia, Pakistan, Mexico, Honduras, Iraq, Argentina,Colombia, Democratic Republic (DR) of Congo, and Australia; and an existing concession toconstruct, develop and operate a port in Tuxpan, Mexico.

Concessions for port operations entered into, acquired, developed and terminated by ICTSI andsubsidiaries for the last two years are summarized below:

Umm Qasr, Iraq. ICTSI, through its wholly owned subsidiary, ICTSI (M.E.) DMCC [formerlyICTSI (M.E.) JLT] (ICTSI Dubai), and General Company for Ports of Iraq (GCPI) signed onApril 10, 2014 the Contract for the Construction and Operation of Three New Quays andManagement and Operation of Quay No. 20 (“Contract”) in the Port of Umm Qasr (“Port”) inIraq. The Contract grants ICTSI the rights to: (a) manage and operate the existing containerfacility at Berth 20 of the Port for a period of 10 years, (b) build in three phases, under abuild-operate-transfer (BOT) scheme, a new container and general cargo terminal in the Port fora concession period of 26 years, and (c) provide container and general cargo terminal services inboth components. On March 1, 2016, an addendum to the Contract (“First Addendum”) wassigned by the parties granting ICTSI, through ICTSI Dubai, the right to manage and operate anadditional existing Quay No. 19 for a total of 13 years, with the first three years for thecompletion of rehabilitation works. Also, the First Addendum extended the original term for themanagement and operation of Quay No. 20 from 10 to 13 years. On March 26, 2017, a secondaddendum to the Contract (“Second Addendum”) was signed by the parties granting ICTSI,through ICTSI Dubai, the right to manage and operate Quay No. 21 co-terminus with theContract and the First Addendum. The Second Addendum extended the term for themanagement and operation of Quay No. 19 and 20 from 13 to 21 years.

SEC Form 17-Q Q2 2019 1111

ICTSI commenced trial operations at Berth 20 in September 2014 and full-fledged commercialoperations in November 2014. ICTSI commenced commercial operations of Berth 19 inJune 2016. The rehabilitation works for Berth 21 are on-going and it has started operations inthe third quarter of 2018.

Phase 1 of the expansion project (Berth 27) under the BOT scheme has 250 meters of berth withan estimated capacity of 300,000 TEUs. The facility will have 600 meters of quay with anestimated capacity of 900,000 TEUs. Berth 27 was completed and fully operational in the firstquarter of 2017.

On October 22, 2017, ICTSI signed an agreement with GCPI for the Phase 2 of expansiondevelopment of the Port. The Phase 2 expansion project will involve development of two newberths, Berths 25 and 26, including a 20-hectare yard area. This expansion will increase thePort’s container handling capacity by 600,000 TEUs to 1,200,000 TEUs and its capability tohandle large container vessels of up to 10,000 TEUs. The development of this phase of theexpansion project is on-going and is expected to be completed in the third quarter of 2019.

Port of Melbourne, Australia. On May 2, 2014, ICTSI, through its subsidiary in Australia,Victoria International Container Terminal Ltd. (VICT), signed a contract in Melbourne with Portof Melbourne Corporation for the design, construction, commissioning, operation, maintainingand financing of the Webb Dock Container Terminal (Terminal) and Empty Container Park(ECP) at Webb Dock East (WDE) in the Port of Melbourne. The Contract grants VICT therights to: (a) design, build and commission the new Terminal at berths WDE 4 and WDE 5,(b) design, build and commission the new ECP at WDE, and (c) operate the Terminal and ECPuntil June 30, 2040. Initially, VICT was 90% owned by ICTSI through ICTSI Far East Pte. Ltd.(IFEL), a wholly owned subsidiary, and 10% by Anglo Ports Pty Limited (“Anglo Ports”). OnFebruary 4, 2015, IFEL acquired the 10% non-controlling interest from Anglo Ports and became100% owner of VICT. On January 7, 2016, IFEL’s ownership interest in VICT was transferredto another subsidiary, ICTSI Oceania B.V. (IOBV), making IOBV the new 100% owner ofVICT.

Phase 1 of the Terminal and the ECP with capacities of 350,000 TEUs and 250,000 TEUs,respectively, commenced commercial operations in the second quarter of 2017. Phase 2 of theTerminal commenced commercial operations in the first quarter of 2018 and has increased thecapacity to 1,000,000 TEUs.

Davao, Philippines. On April 21, 2006, the Philippine Ports Authority (PPA) granted DavaoIntegrated Port and Stevedoring Services Corporation (DIPSSCOR) a ten-year contract for cargohandling services at Sasa Wharf, Port of Davao in the Philippines that expired onApril 20, 2016. Thereafter, the PPA granted DIPSSCOR a series of hold-over authority on atemporary basis over the cargo handling services at Sasa Wharf, Port of Davao. OnFebruary 22, 2018, the PPA issued Administrative order (AO) No. 04-2018 directing all PortManagers of the PPA to grant hold-over authorities to cargo handling service providers withcontracts due to expire in 2018, for six months, unless earlier terminated by the PPA or uponaward of a new terminal management contract in accordance with PPA AO No. 03-2016 entitled“Port Terminal Management Regulatory Framework”. On June 11, 2018, the hold-overauthority was issued by the PPA with a validity of six months starting February 26, 2018 untilthe award of a new contract by the PPA, whichever is earlier, unless cancelled or revoked forreason by the PPA during the validity of the hold-over authority. On November 12, 2018, thehold-over authority was issued by the PPA with a validity of six months startingAugust 26, 2018 or until the award of a new contract by the PPA, whichever is earlier, unlesscancelled or revoked for reason by the PPA during the validity of the hold-over authority. As ofAugust 13, 2019, DIPSSCOR has not received a new hold-over authority.

SEC Form 17-Q Q2 2019 1212

South Cotabato, Philippines. On February 20, 2006, the PPA granted South Cotabato IntegratedPort Services, Inc. (SCIPSI) a ten-year contract for the exclusive management and operation ofarrastre, stevedoring, and other cargo handling services, except porterage, at Makar Wharf, Portof General Santos, General Santos City in the Philippines that expired on February 19, 2016.Thereafter, the PPA granted SCIPSI a series of hold-over authority on a temporary basis over thecargo handling services at Makar Wharf, Port of General Santos. On February 22, 2018, thePPA issued AO No. 04-2018 directing all Port Managers of the PPA to grant hold-overauthorities to cargo handling service providers with contracts due to expire in 2018, for sixmonths, unless earlier terminated by the PPA or upon award of a new terminal managementcontract in accordance with PPA AO No. 03-2016. On June 21, 2018, the hold-over authoritywas issued by the PPA with a validity of six months starting February 25, 2018 until the awardof a new contract by the PPA, whichever is earlier, unless cancelled or revoked for reason by thePPA during the validity of the hold-over authority. On October 19, 2018, the hold-overauthority was issued by the PPA with a validity of six months starting August 25, 2018 or untilthe award of a new contract by the PPA, whichever is earlier, unless cancelled or revoked forreason by the PPA during the validity of the hold-over authority. As of August 13, 2019,SCIPSI has not received a new hold-over authority.

Cavite Gateway Terminal, Philippines. On April 21, 2017, ICTSI, through its wholly-ownedsubsidiary, Cavite Gateway Terminal (CGT), in partnership with the Philippine Department ofTransportation, project launched the country’s first container roll-on roll-off barge terminal inTanza, Cavite. CGT will facilitate off-the-roads seaborn transport of containers between Port ofManila and Cavite and service industrial locators in Cavite area. CGT’s barge terminal willhave an annual capacity of 115,000 TEUs, which is equivalent to 140,000 fewer truck trips oncity roads each year. CGT formally commenced commercial operations in November 2018.

Motukea and Lae, Papua New Guinea. In September 2017, ICTSI received a notification fromPNG Ports Corporation Limited (PNGPCL), a PNG state-owned enterprise, of the confirmationby the Independent Consumer and Competition Commission in PNG with respect to the two25-year agreements signed by ICTSI’s PNG subsidiaries, Motukea International TerminalLimited (MITL) and South Pacific International Container Terminal Limited (SPICTL), withPNGPCL for the operation, management and development of the two international ports inMotukea and Lae in PNG. SPICTL and MITL were allowed by PNGPCL to take over the portfacilities and begin operations at the Port of Lae in February 2018 and at the Port of Motukea inMay 2018, respectively. The terminal operating agreements (TOA) and other related contractstook effect on June 1, 2018 after all the parties have complied with the agreed conditionsprecedent.

ICTSI, through its subsidiaries, ISPL, MITL and SPICTL entered into Subscription andShareholders Agreements (SSA) with the impacted communities (IC) for the management andgovernance of and the further transfers and/or issues of shares of MITL and SPICTL. The SSAsbecame effective upon the effectivity of the TOAs. Within one year from the effectivity date ofthe SSAs and upon the required written notification by ICTSI, through ISPL, the ICs have theright to subscribe up to 30% of the total initial shares of MITL and SPICTL. Pre-emptive rightson additional subscriptions are available to all shareholders.

On August 8, 2019, ISPL entered into agreements with the local Tatana and Barunicommunities, represented by Noho-Mage Holdings Limited, for the latter to acquire a 30% stakeof MITL.

As of August 13, 2019, the ICs for SPICTL have not exercised their right to subscribe pendingthe finalization of the capital structure of SPICTL.

SEC Form 17-Q Q2 2019 1313

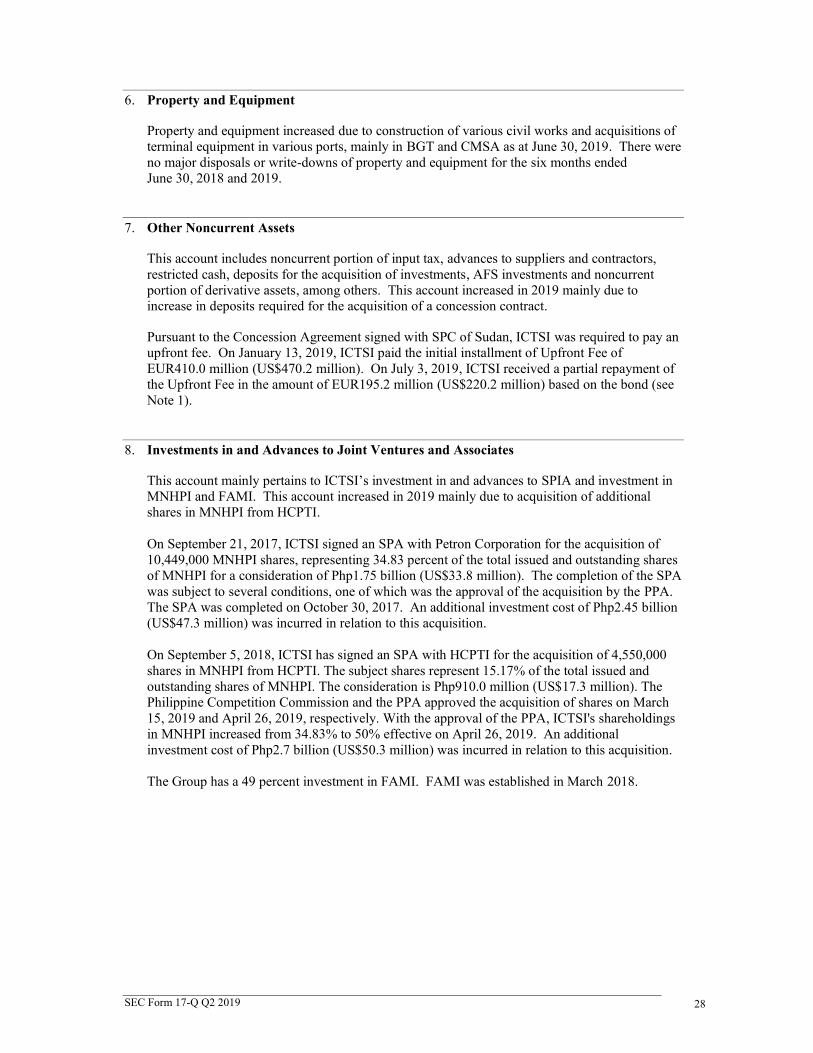

Manila North Harbor, Philippines. On September 21, 2017, the Board of ICTSI granted theauthority to acquire shares in MNHPI. On the same date, ICTSI signed a Share PurchaseAgreement (SPA) with Petron Corporation for the acquisition of 10,449,000 MNHPI shares,representing 34.83% of the total issued and outstanding shares of MNHPI for a consideration ofPhp1.75 billion (US$33.8 million). The completion of the SPA was subject to severalconditions, one of which was the approval of the acquisition by the Philippine Ports Authority(PPA) which was obtained on October 20, 2017. The SPA was completed on October 30, 2017.An additional investment cost of Php2.45 billion (US$47.3 million) was incurred in relation tothis acquisition.

On September 5, 2018, ICTSI has signed an SPA with Harbour Centre Port Terminal, Inc.(HCPTI) for the acquisition of 4,550,000 shares in MNHPI from HCPTI. The subject sharesrepresent 15.17% of the total issued and outstanding shares of MNHPI. The consideration isPhp910.0 million (US$17.3 million). The Philippine Competition Commission and the PPAapproved the acquisition of shares on March 15, 2019 and April 26, 2019, respectively. With theapproval of the PPA, ICTSI's shareholdings in MNHPI increased from 34.83% to 50% effectiveon April 26, 2019. An additional investment cost of Php2.7 billion (US$50.3 million) wasincurred in relation to this acquisition.

Port of Tanjung Priok, Indonesia. On November 2, 2017, PT ICTSI Jasa Prima Tbk (IJP), anICTSI subsidiary in Indonesia, signed a Conditional Share Purchase Agreement with PTSamudera Terminal Indonesia for the purchase of IJP’s interest in PT Perusahaan Bongkar MuatOlah Jasa Andal (OJA), subject to certain conditions. As of August 13, 2019, the conditionsprecedent have not yet been fulfilled.

Port of Port Sudan, Sudan. On January 3, 2019, ICTSI, through its wholly-owned subsidiaryICTSI Middle East DMCC, signed a Concession Agreement (‘the Agreement’) with Sea PortsCorporation (SPC) of Sudan to operate, manage, and develop the South Port Container Terminal(SPCT) at the Port of Sudan, Republic of the Sudan for 20 years. The Port of Sudan is the onlymajor modern port in the Republic of the Sudan and serves as the international gateway for morethan 95% of country’s cargo flows.

Pursuant to the Agreement, ICTSI is required to pay: (a) an upfront fee of EUR530.0 million ininstallments of EUR410.0 million (US$467.2 million) and five other installments each in theamount of EUR24.0 (US$27.3 million) from the third to the seventh operation year; (b) fixedmonthly fee; and (c) royalty fee during the concession period. The Agreement is secured by asovereign guarantee by the Republic of the Sudan. On January 13, 2019, ICTSI paid the initialinstallment of upfront fee of EUR410.0 million (US$470.2 million, the “Upfront Fee”) andshown as part of “Other noncurrent assets” (see Note 7). In February 2019, ICTSI establishedAfrica Gateway Terminal (AGT), a Sudanese entity, to operate the container terminal.

On January 8, 2019, the Ministry of Finance and Economic Planning (the “Ministry”) issued abond (the “Refund Bond”), which was subsequently amended, wherein it agreed to refund theUpfront Fee in case ICTSI is unable to take over operations by April 7, 2019.

On August 7, 2019, due to the ongoing political instability in the Republic of the Sudan and thefailure of the Sudanese government to turn over SPCT on or before April 7, 2019, the SudaneseMinistry sent ICTSI a letter confirming: (1) the remittance of EUR195.2 million as partialrepayment of the Upfront Fee under the terms of the Refund Bond and (2) that the balance willbe repaid as soon as possible.

ICTSI is in continuous discussion with the Sudanese Government for the repayment schedule ofthe balance of the Upfront Fee and the status of the Concession Agreement following a letterfrom SPC regarding its cancellation which ICTSI disputes. ICTSI reserves and continues toreserve its rights under the Concession Agreement.

SEC Form 17-Q Q2 2019 1414

ICTSI, has an excellent track record of managing and making significant investments incontainer terminal infrastructure and is committed to making the Port of Sudan a leading portand strategic gateway to Africa, benefitting all of its stakeholders.

Port of Rio de Janeiro City, Federative Republic of Brazil. On July 19, 2019, ICTSI, through itswholly-owned subsidiary ICTSI Americas B.V, signed a Share Purchase Agreement with BorealEmpreendimentos e Participações S.A. (Boreal) to acquire 100% of the shares of Libra TerminalRio S.A. (Libra Rio), which holds the concession rights to operate, manage and develop thecontainer terminal Terminal de Contêineres 1 (T1Rio) in the port of Rio de Janeiro City,Federative Republic of Brazil. The concession of T1Rio commenced in 1998 and was extendedin 2011 until 2048. Transfer of the facilities to ICTSI management is expected to take place inthe fourth quarter of 2019, once all conditions precedent and all required regulatory approvalshave been obtained.

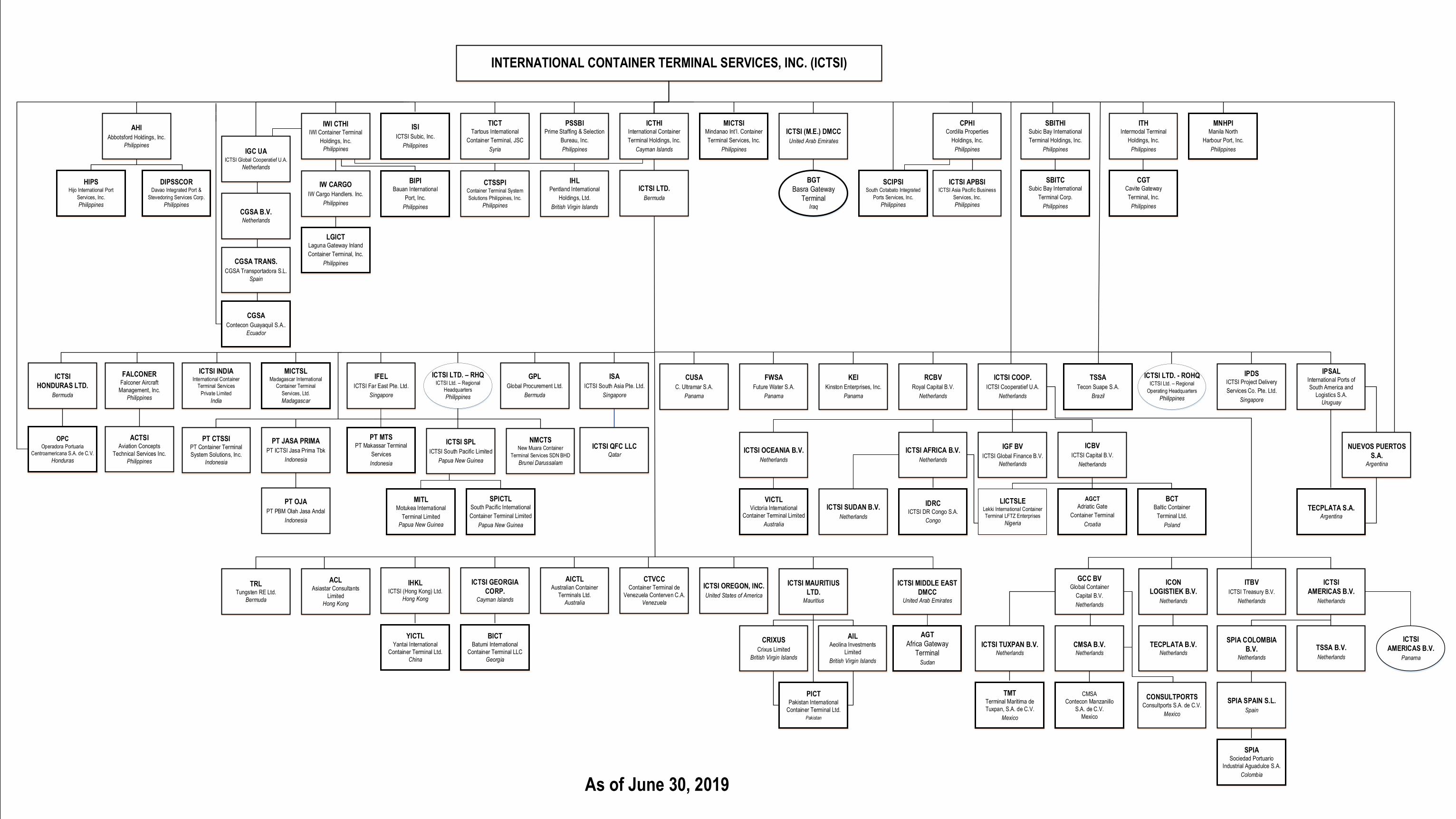

1.3 Subsidiaries and Joint Ventures

Percentage of OwnershipPlace of Nature of Functional December 31, 2018 June 30, 2019Incorporation Business Currency Direct Indirect Direct Indirect

Subsidiaries:AsiaInternational Container Terminal Holdings, Inc.

(ICTHI) and SubsidiariesCayman Islands Holding Company US Dollar 100.00 – 100.00 –

ICTSI Ltd. Bermuda Holding Company US Dollar – 100.00 – 100.00ICTSI Mauritius Ltd. Mauritius Holding Company US Dollar – 100.00 – 100.00Aeolina Investments Limited British Virgin

IslandsHolding Company US Dollar – 100.00 – 100.00

Pakistan International Container Terminal(PICT)

Pakistan Port Management Pakistani Rupee – 64.53 – 64.53

IFEL Singapore Holding Company US Dollar – 100.00 – 100.00New Muara Container Terminal Services

Sdn Bhd (NMCTS)Brunei Port Management Brunei Dollar – 100.00 – 100.00

IJP and Subsidiaries Indonesia Maritimeinfrastructure andlogistics

US Dollar – 80.16 – 80.16

OJA Indonesia Port Management US Dollar – 80.16 – 80.16PT Makassar Terminal Services, Inc. (MTS) Indonesia Port Management Indonesian

Rupiah– 95.00 – 95.00

PT Container Terminal Systems SolutionsIndonesia

Indonesia Software Developer US Dollar – 100.00 – 100.00

ICTSI (Hong Kong) Limited Hong Kong Holding Company US Dollar – 100.00 – 100.00Yantai International Container Terminals,

Limited (YICT)China Port Management Renminbi – 51.00 – 51.00

Pentland International Holdings, Ltd. British VirginIslands

Holding Company US Dollar – 100.00 – 100.00

ICTSI Georgia Corp. Cayman Islands Holding Company US Dollar – 100.00 – 100.00Global Procurement Ltd. Bermuda Holding Company US Dollar – 100.00 – 100.00ICTSI Honduras Ltd. Bermuda Holding Company US Dollar – 100.00 – 100.00ICTSI Ltd. Regional Headquarters Philippines Regional

HeadquartersPhilippine Peso – 100.00 – 100.00

International Container Terminal Services(India) Private Limited

India Port Management Indian Rupee – 100.00 – 100.00

Container Terminal de Venezuela ContervenCA (CTVCC)

Venezuela Holding Company US Dollar – 95.00 – 95.00

ICTSI Africa (Pty) Ltd. (c) South Africa BusinessDevelopmentOffice (BDO)

South AfricanRand

– – – –

Australian International Container TerminalsLimited (AICTL)

Australia Port Management Australian Dollar – 70.00 – 70.00

Mindanao International Container TerminalServices, Inc. (MICTSI)

Philippines Port Management Philippine Peso 100.00 − 100.00 −

Abbotsford Holdings, Inc. Philippines Holding Company Philippine Peso 100.00 – 100.00 –Hijo International Port Services, Inc. (HIPS) Philippines Port Management Philippine Peso – 65.00 – 65.00DIPSSCOR Philippines Port Management Philippine Peso – 96.95 – 96.95IWI Container Terminal Holdings, Inc. (IWI

CTHI, formerly ICTSI Warehousing, Inc.)Philippines Warehousing Philippine Peso 100.00 – 100.00 –

IW Cargo Handlers, Inc. Philippines Port EquipmentRental

US Dollar – 100.00 – 100.00

Container Terminal Systems SolutionsPhilippines, Inc.

Philippines Software Developer US Dollar – 100.00 – 100.00

Bauan International Port, Inc. (BIPI) (f) Philippines Port Management Philippine Peso – 60.00 – 80.00Prime Staffers and Selection Bureau, Inc. Philippines Manpower

RecruitmentPhilippine Peso 100.00 – 100.00 –

ICTSI Subic, Inc. (ICTSI Subic) Philippines Port Management US Dollar 100.00 – 100.00 –Subic Bay International Terminal Holdings,

Inc. (SBITHI)Philippines Holding Company US Dollar 83.33 – 83.33 –

SEC Form 17-Q Q2 2019 1515

Percentage of OwnershipPlace of Nature of Functional December 31, 2018 June 30, 2019Incorporation Business Currency Direct Indirect Direct Indirect

Subic Bay International Terminal Corporation(SBITC)

Philippines Port Management US Dollar – 83.33 – 83.33

Cordilla Properties Holdings, Inc. Philippines Holding Company Philippine Peso 100.00 − 100.00 −SCIPSI Philippines Port Management Philippine Peso 35.70 14.38 35.70 14.38ICTSI Dubai United Arab

EmiratesBDO US Dollar 100.00 − 100.00 −

ICTSI Capital B.V. (ICBV) The Netherlands Holding Company US Dollar – 100.00 – 100.00Icon Logistiek B.V. The Netherlands Holding Company US Dollar – 100.00 – 100.00Royal Capital B.V. (RCBV) The Netherlands Holding Company US Dollar – 75.00 – 75.00ICTSI Cooperatief U.A. The Netherlands Holding Company US Dollar 1.00 99.00 1.00 99.00Global Container Capital, B.V. The Netherlands Holding Company US Dollar – 100.00 – 100.00ICTSI Treasury B.V. (ITBV) The Netherlands Holding Company US Dollar – 75.00 – 75.00IABV The Netherlands Holding Company US Dollar – 100.00 – 100.00ICTSI Africa B.V. The Netherlands Holding Company US Dollar – 100.00 – 100.00ICTSI Sudan B.V. (formerly ICTSI Cameroon

B.V.)The Netherlands Holding Company US Dollar – 100.00 – 100.00

CMSA B.V. The Netherlands Holding Company US Dollar – 100.00 – 100.00Tecplata B.V. The Netherlands Holding Company US Dollar – 100.00 – 100.00SPIA Colombia B.V. The Netherlands Holding Company US Dollar – 100.00 – 100.00TSSA B.V. The Netherlands Holding Company US Dollar – 100.00 – 100.00CGSA B.V. The Netherlands Holding Company US Dollar – 100.00 – 100.00SPIA Spain S.L. Spain Holding Company US Dollar – 100.00 – 100.00CGSA Transportadora S.L. Spain Holding Company US Dollar – 100.00 – 100.00Crixus Limited British Virgin

IslandsHolding Company US Dollar – 100.00 – 100.00

VICT Australia Port Management Australian Dollar – 100.00 – 100.00Asia Pacific Port Holdings Private Ltd. (c) Singapore Holding Company US Dollar – – – –ICTSI Global Finance B.V. (IGFBV) The Netherlands Holding Company US Dollar – 75.00 – 75.00IOBV The Netherlands Holding Company US Dollar – 100.00 – 100.00ICTSI Tuxpan B.V. The Netherlands Holding Company US Dollar – 100.00 – 100.00ICTSI Asia Pacific Business Services, Inc.

(APBS)Philippines Business Process

OutsourcingUS Dollar – 100.00 – 100.00

ICTSI Ltd. Regional Operating Headquarters Philippines Regional OperatingHeadquarters

US Dollar – 100.00 – 100.00

ICTSI Project Delivery Services Co. Pte. Ltd. Singapore Port Equipment Saleand Rental

US Dollar – 100.00 – 100.00

ICTSI QFC LLC Qatar Holding Company US Dollar – 100.00 – 100.00ICTSI South Asia Pte. Ltd. Singapore Holding Company US Dollar – 100.00 – 100.00Laguna Gateway Inland Container

Terminal, Inc. (LGICT)Philippines Port Management Philippine Peso – 60.00 – 60.00

ICTSI Middle East DMCC United ArabEmirates

Holding Company US Dollar – 100.00 – 100.00

ICTSI Global Cooperatief U.A. The Netherlands Holding Company US Dollar 99.00 1.00 99.00 1.00Consultports S.A. de C.V. Mexico BDO Mexican Peso – 100.00 – 100.00Asiastar Consultants Limited (a) Hong Kong Management

ServicesUS Dollar – 100.00 – 100.00

CGT Philippines Port Management Philippine Peso – 100.00 – 100.00Intermodal Terminal Holdings, Inc. Philippines Holding Company Philippine Peso 100.00 – 100.00 –ICTSI Americas B.V. (Multinational

Headquarters) (a)Panama BDO US Dollar – 100.00 – 100.00

ICTSI South Pacific Limited (a) Papua New Guinea Holding Company Papua NewGuinean Kina

– 100.00 – 100.00

MITL (a) Papua New Guinea Port Management Papua NewGuinean Kina

– 100.00 – 100.00

SPICTL (a) Papua New Guinea Port Management Papua NewGuinean Kina

– 100.00 – 100.00

Tungsten RE Ltd. (a) Bermuda Insurance Company US Dollar – 100.00 – 100.00Europe, Middle East and Africa (EMEA)Tartous International Container

Terminal, Inc. (TICT)Syria Port Management US Dollar 100.00 – 100.00 –

Madagascar International Container TerminalServices, Ltd. (MICTSL)

Madagascar Port Management Euro – 100.00 – 100.00

Baltic Container Terminal Ltd. (BCT) Poland Port Management US Dollar – 100.00 – 100.00Adriatic Gate Container Terminal (AGCT) Croatia Port Management Euro – 51.00 – 51.00Batumi International Container Terminal LLC

(BICTL)Georgia Port Management US Dollar – 100.00 – 100.00

Lekki International Container TerminalServices LFTZ Enterprise (LICTSLE)

Nigeria Port Management US Dollar – 100.00 – 100.00

ICTSI DR Congo S.A. (IDRC) DR Congo Port Management US Dollar – 52.00 – 52.00ICTSI (M.E.) DMCC Iraq Branch (ICTSI Iraq) Iraq Port Management US Dollar – 100.00 – 100.00AGT (e) Sudan Port Management Euro – – – 100.00AmericasContecon Guayaquil, S.A. (CGSA) Ecuador Port Management US Dollar 51.00 49.00 51.00 49.00Contecon Manzanillo S.A. (CMSA) Mexico Port Management US Dollar 1.00 99.00 1.00 99.00Tecon Suape, S.A. (TSSA) Brazil Port Management Brazilian Real – 100.00 – 100.00ICTSI Oregon, Inc. (ICTSI Oregon) U.S.A. Port Management US Dollar − 100.00 − 100.00C. Ultramar, S.A. Panama Holding Company US Dollar – 100.00 – 100.00Future Water, S.A. Panama Holding Company US Dollar – 100.00 – 100.00Kinston Enterprise, Inc. Panama Holding Company US Dollar – 100.00 – 100.00International Ports of South America and

Logistics SAUruguay Holding Company US Dollar − 100.00 − 100.00

Tecplata S.A. (Tecplata) Argentina Port Management US Dollar − 100.00 − 100.00Nuevos Puertos S. A. Argentina Holding Company US Dollar 4.00 96.00 4.00 96.00

SEC Form 17-Q Q2 2019 1616

Percentage of OwnershipPlace of Nature of Functional December 31, 2018 June 30, 2019Incorporation Business Currency Direct Indirect Direct Indirect

Operadora Portuaria Centroamericana,S.A. (OPC)

Honduras Port Management US Dollar 30.00 70.00 30.00 70.00

Terminal Maritima de Tuxpan, S.Ade C.V (TMT)

Mexico Port Management Mexican Peso – 100.00 – 100.00

CMSA Servicios PortuariosSA De CV (a)

Mexico Manpower Services Mexican Peso – 100.00 – 100.00

CMSA Servicios Profesionales Y DeEspecialistas SA De CV (a)

Mexico Manpower Services Mexican Peso – 100.00 – 100.00

Joint Ventures:Sociedad Puerto Industrial Aguadulce SA

(SPIA)Colombia Port Management US Dollar – 46.30 – 46.30

Falconer Aircraft Management, Inc. (FAMI) (d) Philippines AircraftManagement

Philippine Peso – 49.00 – 49.00

Associates:MNHPI (b) Philippines Port Management Philippine Peso 34.83 – 50.00 –Asiaview Realty and Development Corporation

(ARDC)Philippines Realty Philippine Peso – 49.00 – 49.00

(a) Established in 2017(b) Acquired as an associate on October 30, 2017 and additional shares were purchased effective on April 26, 2019(c) Deregistered in 2017(d) Established in 2018(e) Established in February 2019 and has not yet started commercial operations as of August 13, 2019(f) Percentage of ownership increased to 80% on April 10, 2019 due to acquisition of minority shares (see Note 15.7)

2. Basis of Preparation and Statement of Compliance

2.1 Basis of Preparation

The consolidated balance sheet as at December 31, 2018, as restated, and the unaudited interimcondensed consolidated financial statements as at June 30, 2019 and for the three and six monthsended June 30, 2018 and 2019 have been prepared on a historical cost basis, except for financialassets at fair value through other comprehensive income (FVOCI) and derivative financialinstruments which have been measured at fair value. The unaudited interim condensedconsolidated financial statements are presented in United States dollar (US dollar, USD or US$),the Parent Company’s functional and presentation currency. All values are rounded to thenearest thousand US dollar unit, except when otherwise indicated. Any discrepancies in thetables between the listed amounts and the totals thereof are due to rounding. Accordingly,figures shown as totals may not be an arithmetic aggregation of the figures that precede them.

2.2 Statement of Compliance

The unaudited interim condensed consolidated financial statements have been prepared inaccordance with Philippine Accounting Standard (PAS) 34, Interim Financial Reporting.Accordingly, the interim condensed consolidated financial statements do not include all theinformation and disclosures required in the annual audited consolidated financial statements, andshould be read in conjunction with the Group’s audited annual consolidated financial statementsas at and for the year ended December 31, 2018.

3. Summary of Significant Accounting Policies

3.1 Basis of Consolidation

The unaudited interim condensed consolidated financial statements of the Group include theaccounts of ICTSI and its subsidiaries where the Parent Company has control. Control isachieved when the Group is exposed, or has rights, to variable returns from its involvement withthe investee and has the ability to affect those returns through its power over the investee.

SEC Form 17-Q Q2 2019 1717

Specifically, the Group controls an investee if and only if the Group has: Power over the investee (i.e., existing rights that give it the current ability to direct the

relevant activities of the investee), Exposure, or rights, to variable returns from its involvement with the investee, and The ability to use its power over the investee to affect its returns.

When the Group has less than a majority of the voting or similar rights of an investee, the Groupconsiders all relevant facts and circumstances in assessing whether it has power over an investee,including: The contractual arrangement with the other vote holders of the investee, Rights arising from other contractual arrangements, and The Group’s voting rights and potential voting rights.

The Group re-assesses whether or not it controls an investee if facts and circumstances indicatethat there are changes to one or more of the three elements of control.

Subsidiaries. Subsidiaries are entities controlled by the Parent Company. Subsidiaries areconsolidated from the date of acquisition or incorporation, being the date on which the Groupobtains control, and continue to be consolidated until the date such control ceases.

Non-controlling Interests. Non-controlling interests represent the portion of profit or loss andnet assets in PICT, MTS, AICTL, CTVCC, SBITC, SBITHI, BIPI, DIPSSCOR, YICT, SCIPSI,RCBV, AGCT, IJP, OJA, ITBV, HIPS, IGFBV, IDRC and LGICT not held by the Group andare presented separately in the unaudited interim consolidated statement of income and theunaudited interim consolidated statement of comprehensive income, and interim consolidatedbalance sheet separate from equity attributable to equity holders of the parent.

An acquisition, transfer or sale of a non-controlling interest is accounted for as an equitytransaction. No gain or loss is recognized in an acquisition of a non-controlling interest. Thedifference between the fair value of the consideration and book value of the share in the netassets acquired is presented under “Excess of acquisition cost over the carrying value ofnon-controlling interests” account within the equity section of the unaudited interimconsolidated balance sheet. If the Group loses control over a subsidiary, it: (i) derecognizes theassets (including goodwill) and liabilities of the subsidiary, the carrying amount of any non-controlling interest and the cumulative translation differences recorded in equity; (ii) recognizesthe fair value of the consideration received, the fair value of any investment retained and anysurplus or deficit in the unaudited interim consolidated statement of income; and (iii) reclassifiesthe Parent Company’s share of components previously recognized in other comprehensiveincome to the unaudited interim consolidated statement of income or retained earnings, asappropriate.

Transactions Eliminated on Consolidation. All intragroup transactions and balances includingincome and expenses, and unrealized gains and losses are eliminated in full.

Accounting Policies of Subsidiaries. The financial statements of subsidiaries are prepared forthe same reporting period or year using uniform accounting policies as those of the ParentCompany.

Functional and Presentation Currency. The unaudited interim condensed consolidated financialstatements are presented in US dollar, which is ICTSI’s functional and presentation currency.Each entity in the Group determines its own functional currency, which is the currency that bestreflects the economic substance of the underlying events and circumstances relevant to thatentity, and items included in the financial statements of each entity are measured using thatfunctional currency.

SEC Form 17-Q Q2 2019 1818

At the reporting date, the assets and liabilities of subsidiaries whose functional currency is notUS dollar are translated into the presentation currency of ICTSI using the Bloomberg closingrate at balance sheet date and, their unaudited interim statements of income are translated at theBloomberg weighted average daily exchange rates for the period. The exchange differencesarising from the translation are taken directly to the unaudited interim consolidated statement ofcomprehensive income. Upon disposal of the foreign entity, the deferred cumulative translationamount recognized in the unaudited interim consolidated statement of comprehensive incomerelating to that particular foreign operation is recognized in the unaudited interim consolidatedstatement of income.

The following rates of exchange have been adopted by the Group in translating foreign currencyincome statement and balance sheet items as at and for the six months ended June 30:

2018 2019Closing Average Closing Average

Foreign currency to 1 unit of US dollar:Argentine peso (AR$) 28.93 21.63 42.48 41.46Australian dollar (AUD) 1.35 1.30 1.42 1.42Brazilian real (BRL or R$) 3.88 3.43 3.85 3.84Chinese renminbi (RMB) 6.62 6.37 6.87 6.79Colombian peso (COP) 2,931.61 2,848.75 3,211.36 3,188.99Croatian kuna (HRK) 6.32 6.13 6.51 6.57Euro (EUR or €) 0.86 0.83 0.88 0.89Georgian lari (GEL) 2.45 2.47 2.85 2.70Honduran lempira (HNL) 24.03 23.70 24.59 24.48Hong Kong dollar (HKD) 7.85 7.84 7.81 7.84Indian rupee (INR) 68.47 65.74 69.03 70.03Indonesian rupiah (IDR or Rp) 14,330.00 13,748.00 14,126.00 14,194.00Iraqi dinar (IQD) 1,187.58 1,187.44 1,182.28 1,190.32Malagasy ariary (MGA) 3,374.57 3,246.22 3,651.00 3,609.19Mexican peso (MXN) 19.91 19.07 19.22 19.15Pakistani rupee (PKR or Rs) 121.58 114.33 159.52 143.43Papua New Guinean kina (PGK) 3.29 3.25 3.39 3.37Philippine peso (P=) 53.34 51.95 51.24 52.22Polish zloty (PLN) 3.74 3.49 3.73 3.80Singaporean dollar (SGD) 1.36 1.33 1.35 1.36Sudanese pound (SDG) - - 45.23 46.76

Revenue from Contracts with Customers. The Group applied the following judgements thatsignificantly affect the determination of the amount and timing of revenue from contracts withcustomers: Identifying performance obligations

The Group provides port services, mainly cargo handling, to its customers. The Group hasdetermined that each of the services are capable of being distinct.

Determining the transaction priceThe Group determined that the transaction price is in accordance with the tariff ratespublished by port authorities in certain jurisdictions or agreed rates with the customers.

Determining the timing of satisfaction of port servicesThe Group concluded that the revenue for port operations is to be recognized when theservices are rendered.

Definition of Default and Credit-impaired Financial Assets. The Group defines a financialinstrument as in default, which is fully aligned with the definition of credit-impaired, when acustomer is more than 120 days past due on its contractual obligations. However, in certaincases, the Group may also consider a financial asset to be in default when internal or externalinformation indicates that the Group is unlikely to receive the outstanding contractual amountsin full.

SEC Form 17-Q Q2 2019 1919

The criteria above have been applied to all financial instruments held by the Company and areconsistent with the definition of default used for internal credit risk management purposes. Thedefault definition has been applied consistently to calculate Company’s expected loss.

An instrument is considered to be no longer in default (i.e. to have cured) when it no longermeets any of the default criteria.

Measurement of Expected Credit Losses (ECL). ECLs are derived from unbiased andprobability-weighted estimates of expected loss, and are based on the difference between thecontractual cash flows due in accordance with the contract and all the cash flows that the Groupexpects to receive, discounted at the original effective interest rate, or an approximation thereof.The expected cash flows will include cash flows from the sale of collateral held or other creditenhancements that are integral to the contractual terms.Leases. At the inception of the lease, the Group assesses whether a contract is, or contains, alease. This assessment involves the exercise of judgment about whether it depends on aspecified asset, whether the Group obtains substantially all the economic benefits from the use ofthe asset and whether the Group has the right to direct the use of the asset.

The Group recognizes a right-of-use (ROU) asset and a lease liability at the commencement ofthe lease. The ROU assets are measured at cost, less any accumulated depreciation andimpairment losses, and adjusted for any remeasurement of lease liabilities. The cost of ROUasset includes the present value of lease payments (including upfront fees and periodic fixedpayments), plus initial direct cost and the cost of obligations to refurbish the assets, less anylease incentives received.

The ROU is depreciated on a straight-line basis over the shorter of the lease term or the usefullife of the underlying asset. The ROU is subject to test for impairment if there are indicators forimpairment.

The lease payments include fixed payments (including in-substance fixed payments) less anylease incentives receivable, variable lease payments that depend on an index or a rate, andamounts expected to be paid under residual value guarantees. The lease payments also includethe exercise price of a purchase option reasonably certain to be exercised by the Group andpayments of penalties for terminating a lease, if the lease term reflects the Group exercising theoption to terminate. The variable lease payments that do not depend on an index or a rate arerecognized as expense in the period on which the event or condition that triggers the paymentoccurs.

Lease liabilities are measured at the present value of lease payments to be made over the leaseterm.

In calculating the present value of lease payments, the Group uses the incremental borrowingrate at the lease commencement date if the interest rate implicit in the lease is not readilydeterminable. After the commencement date, the amount of lease liabilities is increased to reflectthe accretion of interest and reduced for the lease payments made. In addition, the carryingamount of lease liabilities is remeasured if there is a modification, a change in the lease term, achange in the in-substance fixed lease payments or a change in the assessment to purchase theunderlying asset.

The Group has elected not to recognize ROU assets and liabilities for leases with terms of lessthan or equal to 12 months, or for leases of low value assets. The payments for such leases arerecognized in the statement of income on a straight-line basis over the lease term.

SEC Form 17-Q Q2 2019 2020

3.2 Changes in Accounting Policies

3.2.1 New and Amended Standards Adopted in 2019

The accounting policies adopted for the unaudited interim condensed consolidated financialstatements are consistent with those followed in the preparation of the Group’s annualconsolidated financial statements as at and for the year ended December 31, 2018 except that theGroup has adopted the following new and amended standards starting January 1, 2019:

Amendments to PFRS 9, Prepayment Features with Negative CompensationUnder PFRS 9, a debt instrument can be measured at amortized cost or at fair value throughother comprehensive income, provided that the contractual cash flows are ‘solely paymentsof principal and interest on the principal amount outstanding’ (the SPPI criterion) and theinstrument is held within the appropriate business model for that classification. Theamendments to PFRS 9 clarify that a financial asset passes the SPPI criterion regardless ofthe event or circumstance that causes the early termination of the contract and irrespective ofwhich party pays or receives reasonable compensation for the early termination of thecontract. The amendments should be applied retrospectively and are effective fromJanuary 1, 2019, with earlier application permitted. The adoption of these amendments didnot result in any significant impact on the unaudited interim condensed consolidatedfinancial statements.

PFRS 16, LeasesPFRS 16 sets out the principles for the recognition, measurement, presentation anddisclosure of leases and requires lessees to account for all leases under a single on-balancesheet model similar to the accounting for finance leases under PAS 17, Leases. The standardincludes two recognition exemptions for lessees - leases of ‘low-value’ assets and short-termleases (i.e., leases with a lease term of 12 months or less). At the commencement date of alease, a lessee shall recognize a liability to deliver lease payments (i.e., the lease liability)and an asset representing the right to use the underlying asset during the lease term (i.e., theright-of-use asset). Lessees are required to separately recognize the interest expense on thelease liability and the depreciation expense on the right-of-use asset.

Lessees shall be required to remeasure the lease liability upon the occurrence of certainevents (e.g., a change in the lease term, a change in future lease payments resulting from achange in an index or rate used to determine those payments). The lessee generallyrecognizes the amount of the remeasurement of the lease liability as an adjustment to theright-of-use asset.

Lessor accounting under PFRS 16 is substantially similar as compared with the accountingunder PAS 17. Lessors will continue to classify all leases using the same classificationprinciple as in PAS 17 and distinguish between two types of leases: operating and financeleases.

PFRS 16 also requires lessees and lessors to provide more disclosures than under PAS 17.

PFRS 16 supersedes PAS 17 Leases, Philippine Interpretation IFRIC 4 Determining whetheran Arrangement contains a Lease, Standard Interpretations Committee (SIC)-15 OperatingLeases-Incentives and SIC-27 Evaluating the Substance of Transactions Involving the LegalForm of a Lease.

The Group adopted PFRS 16 using the full retrospective method of adoption with the date ofinitial application of January 1, 2019. The Group also elected to use the recognitionexemptions for lease contracts that, at the commencement date, have a lease term of12 months or less and do not contain a purchase option (‘short-term leases’), and leasecontracts for which the underlying asset is of low value (‘low-value assets’).

SEC Form 17-Q Q2 2019 2121

The effect of adoption of PFRS 16 are as follows (amounts in thousands):

Impact on the consolidated balance sheet as at December 31, 2018

Increase(decrease)

AssetsProperty and equipment - net US$136Right-of-use assets - net 523,328Deferred tax assets 89,775Total Assets 613,239

EquityRetained earnings (482,715)Cumulative translation adjustments 159,248Total Equity (323,467)

LiabilitiesAccounts payable and other current liabilities (1,621)Current portion of lease liabilities 9,033Lease liabilities - net of current portion 1,122,563Deferred tax liabilities (46,464)Other noncurrent liabilities (146,805)Total Liabilities US$936,706

Impact on the consolidated statements of income

Increase (decrease)For the three

months endedJune 30, 2018

For the sixmonths endedJune 30, 2018

Port Authorities' share in gross revenues (US$5,497) (US$11,754)Equipment and facilities-related expenses (21,268) (44,779)Depreciation and amortization 6,924 14,276Interest expense on lease liabilities 26,050 53,131Income before income tax (6,209) (10,874)Benefit from deferred income tax (1,970) (3,450)Net income (US$4,239) (US$7,424)

Attributable to equity holders of the parent (US$4,239) (US$7,424)

Impact on earnings per share

Increase (decrease)For the three

months endedJune 30, 2018

For the sixmonths endedJune 30, 2018

BasicDiluted

(US$0.002)(US$0.002)

(US$0.004)(US$0.003)

Impact on the consolidated statement of cash flows for the six months ended June 30, 2018

Increase (decrease)Net cash flows from operating activities US$25,560Net cash flows from financing activities (25,560)

SEC Form 17-Q Q2 2019 2222

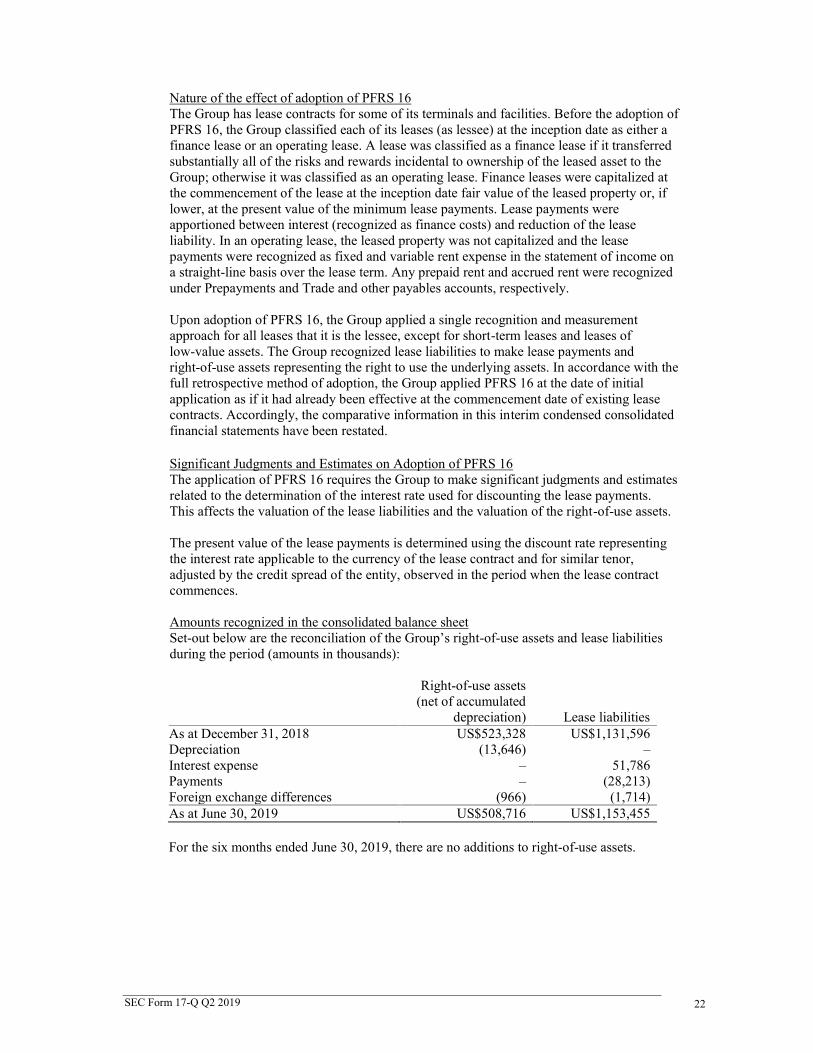

Nature of the effect of adoption of PFRS 16The Group has lease contracts for some of its terminals and facilities. Before the adoption ofPFRS 16, the Group classified each of its leases (as lessee) at the inception date as either afinance lease or an operating lease. A lease was classified as a finance lease if it transferredsubstantially all of the risks and rewards incidental to ownership of the leased asset to theGroup; otherwise it was classified as an operating lease. Finance leases were capitalized atthe commencement of the lease at the inception date fair value of the leased property or, iflower, at the present value of the minimum lease payments. Lease payments wereapportioned between interest (recognized as finance costs) and reduction of the leaseliability. In an operating lease, the leased property was not capitalized and the leasepayments were recognized as fixed and variable rent expense in the statement of income ona straight-line basis over the lease term. Any prepaid rent and accrued rent were recognizedunder Prepayments and Trade and other payables accounts, respectively.

Upon adoption of PFRS 16, the Group applied a single recognition and measurementapproach for all leases that it is the lessee, except for short-term leases and leases oflow-value assets. The Group recognized lease liabilities to make lease payments andright-of-use assets representing the right to use the underlying assets. In accordance with thefull retrospective method of adoption, the Group applied PFRS 16 at the date of initialapplication as if it had already been effective at the commencement date of existing leasecontracts. Accordingly, the comparative information in this interim condensed consolidatedfinancial statements have been restated.

Significant Judgments and Estimates on Adoption of PFRS 16The application of PFRS 16 requires the Group to make significant judgments and estimatesrelated to the determination of the interest rate used for discounting the lease payments.This affects the valuation of the lease liabilities and the valuation of the right-of-use assets.

The present value of the lease payments is determined using the discount rate representingthe interest rate applicable to the currency of the lease contract and for similar tenor,adjusted by the credit spread of the entity, observed in the period when the lease contractcommences.

Amounts recognized in the consolidated balance sheetSet-out below are the reconciliation of the Group’s right-of-use assets and lease liabilitiesduring the period (amounts in thousands):

Right-of-use assets(net of accumulated

depreciation) Lease liabilitiesAs at December 31, 2018 US$523,328 US$1,131,596Depreciation (13,646) –Interest expense – 51,786Payments – (28,213)Foreign exchange differences (966) (1,714)As at June 30, 2019 US$508,716 US$1,153,455

For the six months ended June 30, 2019, there are no additions to right-of-use assets.

SEC Form 17-Q Q2 2019 2323

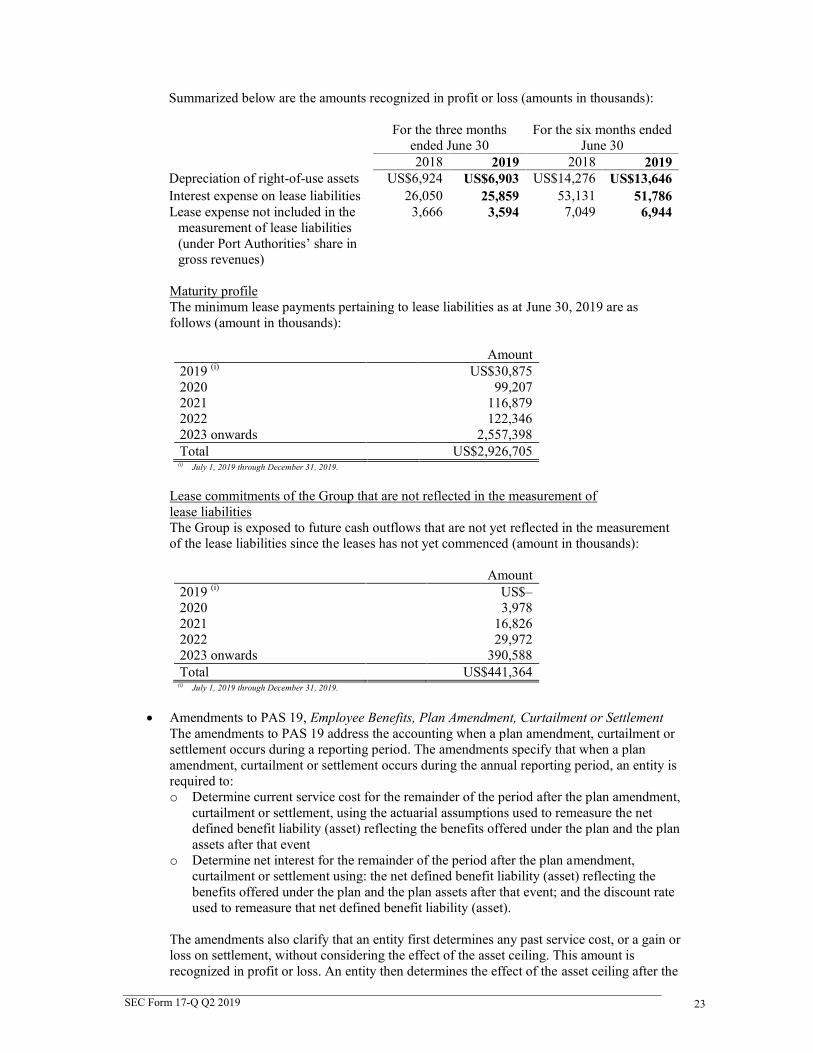

Summarized below are the amounts recognized in profit or loss (amounts in thousands):

For the three monthsended June 30

For the six months endedJune 30

2018 2019 2018 2019Depreciation of right-of-use assets US$6,924 US$6,903 US$14,276 US$13,646Interest expense on lease liabilities 26,050 25,859 53,131 51,786Lease expense not included in the

measurement of lease liabilities(under Port Authorities’ share ingross revenues)

3,666 3,594 7,049 6,944

Maturity profileThe minimum lease payments pertaining to lease liabilities as at June 30, 2019 are asfollows (amount in thousands):

Amount2019 (i) US$30,8752020 99,2072021 116,8792022 122,3462023 onwards 2,557,398Total US$2,926,705

(i) July 1, 2019 through December 31, 2019.

Lease commitments of the Group that are not reflected in the measurement oflease liabilitiesThe Group is exposed to future cash outflows that are not yet reflected in the measurementof the lease liabilities since the leases has not yet commenced (amount in thousands):

Amount2019 (i) US$–2020 3,9782021 16,8262022 29,9722023 onwards 390,588Total US$441,364

(i) July 1, 2019 through December 31, 2019.

Amendments to PAS 19, Employee Benefits, Plan Amendment, Curtailment or SettlementThe amendments to PAS 19 address the accounting when a plan amendment, curtailment orsettlement occurs during a reporting period. The amendments specify that when a planamendment, curtailment or settlement occurs during the annual reporting period, an entity isrequired to:o Determine current service cost for the remainder of the period after the plan amendment,

curtailment or settlement, using the actuarial assumptions used to remeasure the netdefined benefit liability (asset) reflecting the benefits offered under the plan and the planassets after that event

o Determine net interest for the remainder of the period after the plan amendment,curtailment or settlement using: the net defined benefit liability (asset) reflecting thebenefits offered under the plan and the plan assets after that event; and the discount rateused to remeasure that net defined benefit liability (asset).

The amendments also clarify that an entity first determines any past service cost, or a gain orloss on settlement, without considering the effect of the asset ceiling. This amount isrecognized in profit or loss. An entity then determines the effect of the asset ceiling after the

SEC Form 17-Q Q2 2019 2424

plan amendment, curtailment or settlement. Any change in that effect, excluding amountsincluded in the net interest, is recognized in other comprehensive income.

The amendments apply to plan amendments, curtailments, or settlements occurring on orafter the beginning of the first annual reporting period that begins on or afterJanuary 1, 2019, with early application permitted. The Group adopted the amendmentseffective January 1, 2019 and will apply on future plan amendments, curtailments, orsettlements.

Amendments to PAS 28, Long-term Interests in Associates and Joint VenturesThe amendments clarify that an entity applies PFRS 9 to long-term interests in an associateor joint venture to which the equity method is not applied but that, in substance, form part ofthe net investment in the associate or joint venture (long-term interests). This clarification isrelevant because it implies that the expected credit loss model in PFRS 9 applies to suchlong-term interests.

The amendments also clarified that, in applying PFRS 9, an entity does not take account ofany losses of the associate or joint venture, or any impairment losses on the net investment,recognized as adjustments to the net investment in the associate or joint venture that arisefrom applying PAS 28, Investments in Associates and Joint Ventures.

The amendments should be applied retrospectively and are effective from January 1, 2019,with early application permitted. The amendments did not have a significant impact on theunaudited interim condensed consolidated financial statements.

Philippine Interpretation IFRIC-23, Uncertainty over Income Tax TreatmentsThe interpretation addresses the accounting for income taxes when tax treatments involveuncertainty that affects the application of PAS 12, Income Taxes, and does not apply to taxesor levies outside the scope of PAS 12, nor does it specifically include requirements relatingto interest and penalties associated with uncertain tax treatments.

The interpretation specifically addresses the following:o Whether an entity considers uncertain tax treatments separatelyo The assumptions an entity makes about the examination of tax treatments by

taxation authoritieso How an entity determines taxable profit (tax loss), tax bases, unused tax losses,

unused tax credits and tax rateso How an entity considers changes in facts and circumstances

An entity must determine whether to consider each uncertain tax treatment separately ortogether with one or more other uncertain tax treatments. The approach that better predictsthe resolution of the uncertainty should be followed.

The Group adopted the amendments and shall continue to assess the impact in accordancewith the requirements of the said amendments.

SEC Form 17-Q Q2 2019 2525

4. Segment Information

A segment is a distinguishable component of the Group that is engaged either in providing typesof services (business segment) or in providing the services within a particular economicenvironment (geographic segment).

The Group operates principally in one industry segment, which is cargo handling and relatedservices. ICTSI has organized its business into three geographical segments:

Asia - includes Manila International Container Terminal (MICT), BIPI, DIPSSCOR,SCIPSI, SBITC, ICTSI Subic, HIPS, MICTSI, LGICT, CGT and MNHPI in the Philippines;YICT in China; OJA, and MTS in Indonesia; VICT in Australia; NMCTS in Brunei; PICTin Pakistan; MITL and SPICTL in PNG; and AICTL, ICTHI, ICTSI Ltd. and other holdingcompanies and those companies incorporated in The Netherlands for the purpose ofsupporting the funding requirements of the Group;

EMEA - includes BCT in Poland, BICTL in Georgia, AGCT in Croatia, MICTSL inMadagascar, LICTSLE in Nigeria, TICT in Syria, IDRC in DR Congo, ICTSI Iraq in Iraqand AGT in Sudan; and

Americas - includes TSSA in Brazil, CGSA in Ecuador, SPIA in Colombia, Tecplata inArgentina, CMSA, TMT, CMSA Servicios Portuarios SA De CV and CMSA ServiciosProfesionales Y De Especialistas SA De CV in Mexico, OPC in Honduras and ICTSIOregon in Oregon, U.S.A.

Management monitors the operating results of its operating unit separately for making decisionsabout resource allocation and performance assessment. The Group evaluates segmentperformance based on contributions to gross revenues, which is measured consistently withgross revenues from port operations in the interim condensed consolidated statements of income.

Financing is managed on a group basis and centralized at the Parent Company level or at theentities created solely for the purpose of obtaining funds for the Group. Funding requirementsthat are secured through debt are recognized as liabilities of the Parent Company or of the entityissuing the debt instrument, classified under the geographical region of Asia and are notallocated to other geographical segments where funds are eventually transferred and used.The table below presents financial information on geographical segments as ofDecember 31, 2018 (restated) and as of June 30, 2019 (unaudited) and for the three and sixmonths June 30, 2018 (unaudited and restated) and 2019 (unaudited):

2018 (Restated - Note 3)As at and for the Three Months Ended June 30 As at and for the Six Months Ended June 30

Asia EMEA Americas Consolidated Asia EMEA Americas Consolidated

Volume (a) 1,253,784 384,809 750,122 2,388,715 2,495,093 772,190 1,446,972 4,714,255

Gross revenues US$161,697 US$71,461 US$103,226 US$336,384 US$316,735 US$140,439 US$204,590 US$661,764Capital expenditures (b) 33,165 16,616 18,000 67,781 57,952 37,707 40,347 136,006Other information:

Segment assets (c) 3,092,967 512,643 1,462,498 5,068,108 3,092,967 512,643 1,462,498 5,068,108Segment liabilities (d) 2,416,649 145,107 759,191 3,320,947 2,416,649 145,107 759,191 3,320,947

2019 (Unaudited)As at and for the Three Months Ended June 30 As at and for the Six Months Ended June 30Asia EMEA Americas Consolidated Asia EMEA Americas Consolidated

Volume (a) 1,354,478 456,377 752,389 2,563,244 2,653,248 890,664 1,498,004 5,041,916

Gross revenues US$182,711 US$78,753 US$106,537 US$368,001 378,959 154,274 218,552 US$751,785Capital expenditures (b) 33,211 12,257 22,080 67,548 55,215 33,916 32,662 121,793Other information:

Segment assets (c) 2,973,382 1,008,948 1,466,254 5,448,584 2,973,382 1,008,948 1,466,254 5,448,584Segment liabilities (d) 3,058,530 138,385 758,950 3,955,865 3,058,530 138,385 758,950 3,955,865

SEC Form 17-Q Q2 2019 2626

(a) Measured in TEUs.

(b) Capital expenditures include amount disbursed for the acquisition of port facilities and equipment classified as intangibles under IFRIC 12 andproperty and equipment as shown in the unaudited interim consolidated statement of cash flows.