COUNTY OF ROCKBRIDGE VIRGINIA

190

COUNTY OF ROCKBRIDGE, VIRGINIA COMPREHENSIVE ANNUAL FINANCIAL REPORT FOR THE FISCAL YEAR ENDED JUNE 30, 2016

Transcript of COUNTY OF ROCKBRIDGE VIRGINIA

COUNTY OF ROCKBRIDGE, VIRGINIA

COMPREHENSIVE ANNUAL FINANCIAL REPORT

FOR THE FISCAL YEAR ENDED JUNE 30, 2016

COUNTY OF ROCKBRIDGE, VIRGINIA

COMPREHENSIVE ANNUAL FINANCIAL REPORT

FOR THE FISCAL YEAR ENDED JUNE 30, 2016

Prepared by

Steven Bolster, Director of Fiscal Services

County of Rockbridge, Virginia

COUNTY OF ROCKBRIDGE, VIRGINIA

Comprehensive Annual Financial Report Fiscal Year Ended June 30, 2016

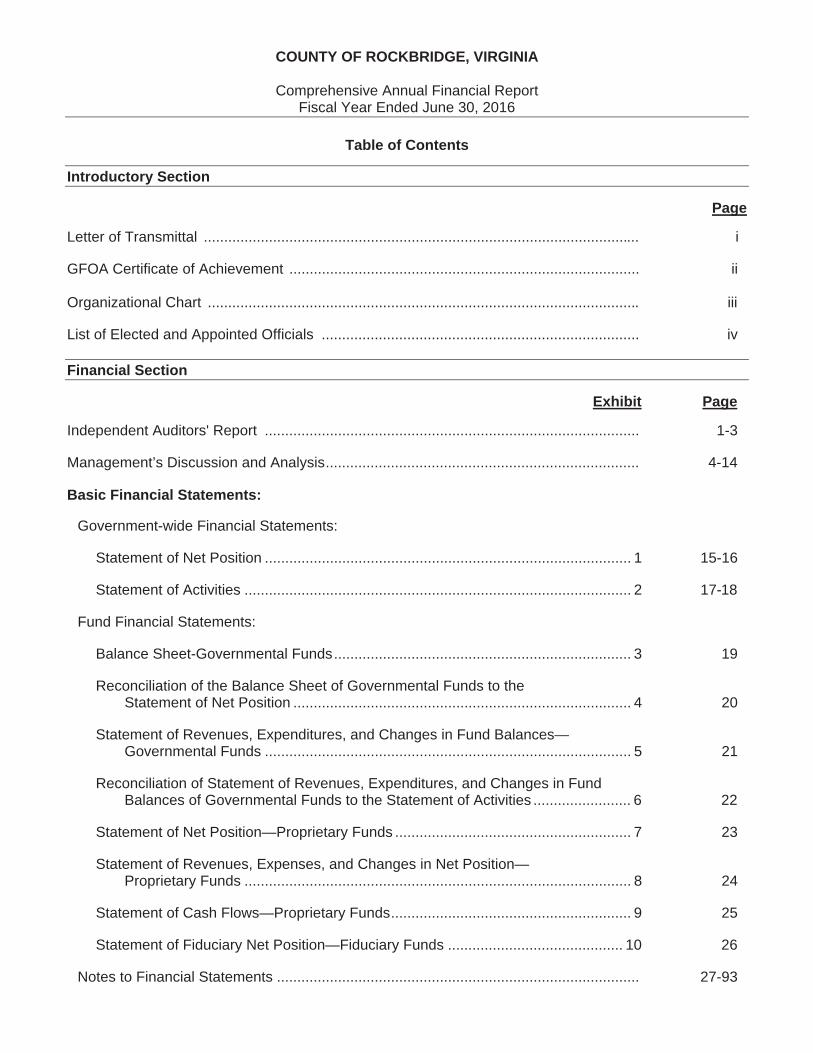

Table of Contents

Introductory Section

Page

Letter of Transmittal ........................................................................................................... i

GFOA Certificate of Achievement ...................................................................................... ii

Organizational Chart .......................................................................................................... iii

List of Elected and Appointed Officials .............................................................................. iv

Financial Section

Exhibit Page

Independent Auditors' Report ............................................................................................ 1-3

Management’s Discussion and Analysis ............................................................................. 4-14

Basic Financial Statements:

Government-wide Financial Statements:

Statement of Net Position .......................................................................................... 1 15-16

Statement of Activities ............................................................................................... 2 17-18

Fund Financial Statements:

Balance Sheet-Governmental Funds ......................................................................... 3 19

Reconciliation of the Balance Sheet of Governmental Funds to the Statement of Net Position ................................................................................... 4 20

Statement of Revenues, Expenditures, and Changes in Fund Balances— Governmental Funds .......................................................................................... 5 21

Reconciliation of Statement of Revenues, Expenditures, and Changes in Fund Balances of Governmental Funds to the Statement of Activities ........................ 6 22

Statement of Net Position—Proprietary Funds .......................................................... 7 23

Statement of Revenues, Expenses, and Changes in Net Position— Proprietary Funds ............................................................................................... 8 24

Statement of Cash Flows—Proprietary Funds ........................................................... 9 25

Statement of Fiduciary Net Position—Fiduciary Funds ........................................... 10 26

Notes to Financial Statements ......................................................................................... 27-93

COUNTY OF ROCKBRIDGE, VIRGINIA

Comprehensive Annual Financial Report Fiscal Year Ended June 30, 2016

Table of Contents (Continued)

Financial Section (Continued)

Exhibit PageRequired Supplementary Information:

Schedule of Revenues, Expenditures, and Changes in Fund Balances— Budget and Actual – General Fund ................................................................... 11 94

Schedule of Components of and Changes in Net Pension Liability and Related Ratios – Primary Government ........................................................................... 12 95

Schedule of Components of and Changes in Net Pension Liability and Related Ratios – Component Unit Rockbridge Regional Jail Commission .................... 13 96

Schedule of Components of and Changes in Net Pension Liability and Related Ratios – Component Unit School Board (nonprofessional) .............................. 14 97

Schedule of Employer’s Share of Net Pension Liability VRS Teacher Retirement Plan ................................................................................................ 15 98

Schedule of Employer Contributions ........................................................................ 16 99

Notes to Required Supplementary Information ........................................................ 17 100

Schedule of OPEB Funding Progress ...................................................................... 18 101

Other Supplementary Information:

Schedule of Revenues, Expenditures, and Changes in Fund Balances— Budget and Actual:

County Capital Projects Fund ............................................................................... 19 102

Other Capital Projects Fund ................................................................................. 20 103

Combining Statement of Fiduciary Net Position – Fiduciary Funds ................................ 21 104

Combining Statement of Changes in Assets and Liabilities – Agency Funds ................. 22 105

Discretely Presented Component Unit—School Board:

Combining Balance Sheet ....................................................................................... 23 106

Combining Statement of Revenues, Expenditures, and Changes in Fund Balances—Governmental Funds ...................................................................... 24 107

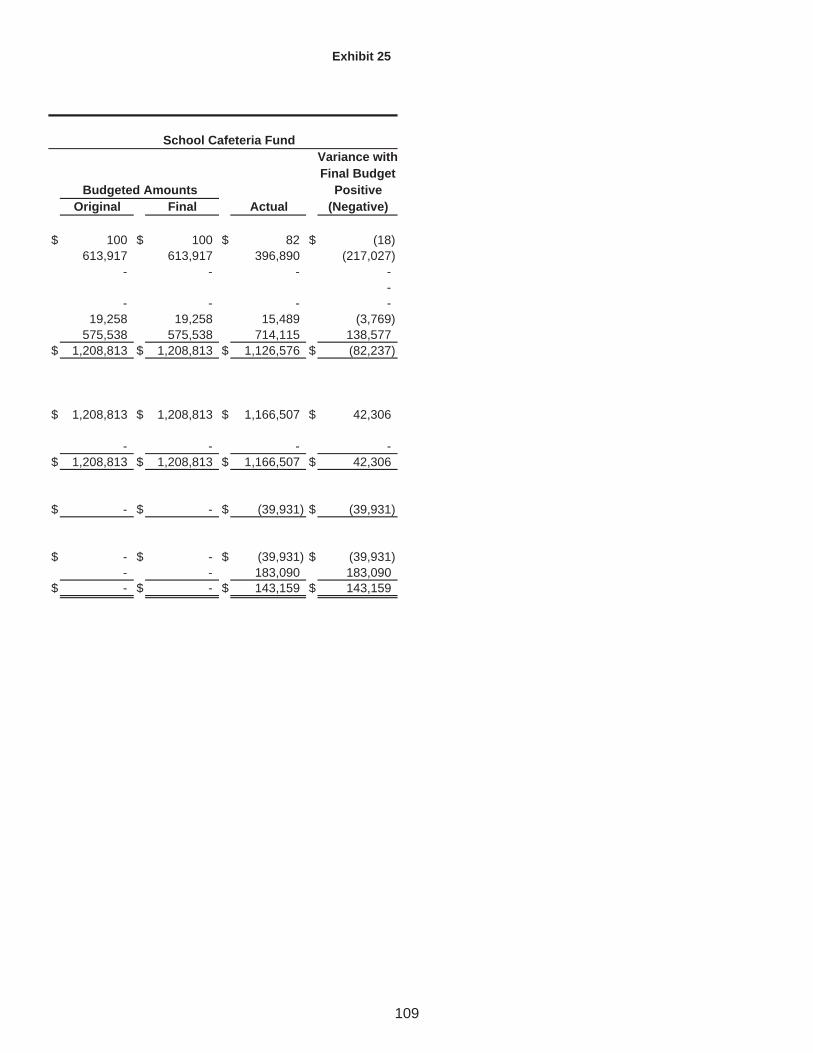

Schedule of Revenues, Expenditures, and Changes in Fund Balances—Budget and Actual .......................................................................... 25 108-109

Statement of Fiduciary Net Position – Fiduciary Fund ............................................. 26 110

COUNTY OF ROCKBRIDGE, VIRGINIA

Comprehensive Annual Financial Report Fiscal Year Ended June 30, 2016

Table of Contents (Continued)

Financial Section (Continued)

Exhibit PageOther Supplementary Information: (continued)

Discretely Presented Component Unit—School Board: (continued)

Statement of Changes in Fiduciary Net Position – Fiduciary Fund ......................... 27 111

Schedule PageSupporting Schedules:

Schedule of Revenues—Budget and Actual—Governmental Funds ............................ 1 112-116

Schedule of Expenditures—Budget and Actual—Governmental Funds ........................ 2 117-120

Statistical Section

Table Page

Net Position by Component .............................................................................................. 1 121-122

Changes in Net Position ................................................................................................... 2 123-126

Governmental Activities Tax Revenues by Source ........................................................... 3 127

Fund Balances of Governmental Funds ........................................................................... 4 128-129

Changes in Fund Balances of Governmental Funds ........................................................ 5 130-131

General Governmental Tax Revenues by Source ............................................................ 6 132

Assessed Value and Estimated Actual Value of Taxable Property ................................... 7 133-134

Property Tax Rates ........................................................................................................... 8 135

Property Tax Levies and Collections ................................................................................ 9 136

Principal Property Taxpayers .......................................................................................... 10 137

Ratios of Outstanding Debt by Type ............................................................................... 11 138-139

Ratio of Net General Bonded Debt to Assessed Value and Net Bonded Debt per Capita ................................................................................................................... 12 140

Pledged-Revenue Coverage ........................................................................................... 13 141

Demographic and Economic Statistics ........................................................................... 14 142

Principal Employers ........................................................................................................ 15 143

Full-time Equivalent County Government Employees by Function ................................. 16 144-145

COUNTY OF ROCKBRIDGE, VIRGINIA

Comprehensive Annual Financial Report Fiscal Year Ended June 30, 2016

Table of Contents (Continued)

Statistical Section (continued)

Table Page

Operating Indicators by Function .................................................................................... 17 146-147

Capital Asset Statistics by Function ................................................................................ 18 148-149

Schedule of the City of Lexington’s and Buena Vista’s Share of Certain General Government Expenditures .......................................................................................... 19 150-151

Compliance Section

Independent Auditors’ Report on Internal Control over Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance with Government Auditing Standards ..................................... 152-153

Independent Auditors’ Report on Compliance for Each Major Program and on Internal Control over Compliance Required by the Uniform Guidance .......................................... 154-155

Schedule of Expenditures of Federal Awards ..................................................................... 156-157

Schedule of Findings and Questioned Costs ...................................................................... 158

INTRODUCTORY SECTION

County of Rockbridge Organizational Chart

Revision Date 12/2015 *The Rockbridge County Solid Waste Authority is a blended component unit of the County

Board of Supervisors

Building

Permits

Erosion/Stormwater

Management

Building Maintenance

PreschoolFIre and EMS

Emergency/HazMat

Management

Fleet ServicesSolid Waste*

Landfill Operattions

Recycling

Community Outreach

Parks and RecreationFiscal Services

Information Technology

Central Accounting

Accounts Payable

Rental Assistance

Community Development

Planning and Zoning

GIS

Economic Development

Human Resources

County Attorney

County Administrator

Citizens

Constitutional Offices Clerk of Circuit Court

Commissioner of Revenue Commonwealth Attorney

Sheriff Treasurer

State and Local Offices Circuit Court

Cooperative Extension Electoral Board/Registrar

General District Court Health Department

Magistrate Probation Office Social Services

Environmental Sciences Public Library

Boards and Commissions

iii

COUNTY OF ROCKBRIDGE, VA

BOARD OF SUPERVISORS

John M. Higgins, ChairmanDavid W. Hinty, Jr., Vice Chairman

Ronnie R. CampbellRussell L. Ford

Albert W. Lewis, Jr.

ROCKBRIDGE COUNTY APPOINTED OFFICIALS

County Administrator……………………………………………………………………..…………………Spencer H. SuterCounty Attorney……………………………………………………………………………….………………Vickie L. Huffman

COUNTY SCHOOL BOARD

David B. McDaniel, ChairmanAlbert “Jay” Lewis II, Vice Chairman

Kevin BrooksLaura C. Hoofnagle

Laurie Strong

SCHOOL DIVISION APPOINTED OFFICIALS

Superintendent of Schools………………………………………………………………..…………………Dr. Jack DonaldClerk of the School Board………………………………………………………………………………Rhonda Humphries

LEGISLATIVE ELECTION

Judge of the Circuit Court…….…………………………………….……..…………………Honorable Anita D. FilsonJudge of the General District Court………………………………………………Honorable Gordon F. SaundersJudge of the Juvenile & Domestic District Court…………….…………………Honorable Laura L. Dascher

CONSTITUTIONAL OFFICERS

Clerk of the Circuit Court……………………………………………………………..…………………D. Bruce PattersonCommonwealth’s Attorney………………………….……………………………………………………….……Chris BilliasCommissioner of the Revenue………………….…………………………………..…………………David C. WhitesellSheriff…………………………………………………………………………………………………………Christopher J. BlalockTreasurer……………………………………………………………..………………………………………….…Betty S. Trovato

iv

FINANCIAL SECTION

1

ROBINSON, FARMER, COX ASSOCIATES CERTIFIED PUBLIC ACCOUNTANTS A PROFESSIONAL LIMITED LIABILITY COMPANY

INDEPENDENT AUDITORS' REPORT

TO THE HONORABLE MEMBERS OF THE BOARD OF SUPERVISORS COUNTY OF ROCKBRIDGE, VIRGINIA

Report on the Financial Statements

We have audited the accompanying financial statements of the governmental activities, the business-type activities, the discretely presented component units, each major fund and the aggregate remaining fund information of the County of Rockbridge, Virginia, as of and for the year ended June 30, 2016, and the related notes to the financial statements, which collectively comprise the County’s basic financial statements as listed in the table of contents.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditors’ Responsibility

Our responsibility is to express opinions on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America; the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States; and the Specifications for Audits of Counties, Cities, and Towns,issued by the Auditor of Public Accounts of the Commonwealth of Virginia. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditors’ judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinions.

2

Opinions

In our opinion, the financial statements referred to above present fairly, in all material respects, the respective financial position of the governmental activities, the business-type activities, the discretely presented component units, each major fund and the aggregate remaining fund information of the County of Rockbridge, Virginia, as of June 30, 2016, and the respective changes in financial position, and, where applicable cash flows thereof for the year then ended in accordance with accounting principles generally accepted in the United States of America.

Change in Accounting Principle

As described in Note 1 to the financial statements, in 2016, the County adopted new accounting guidance, GASB Statement 79 Certain External Investment Pools and Pool Participants, and No. 82 Pension Issues – an amendment of GASB Statements No. 67, No. 68, and No. 73. Our opinion is not modified with respect to this matter.

Other Matters

Required Supplementary Information

Accounting principles generally accepted in the United States of America require that the management’s discussion and analysis, budgetary comparison information, and schedules related to pension and OPEB funding on pages 4-14, 94, 95-101, respectively, be presented to supplement the basic financial statements. Such information, although not a part of the basic financial statements, is required by the Governmental Accounting Standards Board, who considers it to be an essential part of financial reporting for placing the basic financial statements in an appropriate operational, economic, or historical context. We have applied certain limited procedures to the required supplementary information in accordance with auditing standards generally accepted in the United States of America, which consisted of inquiries of management about the methods of preparing the information and comparing the information for consistency with management’s responses to our inquiries, the basic financial statements, and other knowledge we obtained during our audit of the basic financial statements. We do not express an opinion or provide any assurance on the information because the limited procedures do not provide us with sufficient evidence to express an opinion or provide any assurance. The budgetary comparison information has been subjected to the auditing procedures applied in the audit of the basic financial statements and, in our opinion, is fairly stated in all material respects in relation to the basic financial statements taken as a whole.

Other Information

Our audit was conducted for the purpose of forming opinions on the financial statements that collectively comprise the County of Rockbridge, Virginia’s basic financial statements. The introductory section, other supplementary information, and statistical section, are presented for purposes of additional analysis and are not a required part of the basic financial statements. The schedule of expenditures of federal awards is presented for purposes of additional analysis as required by Title 2 U.S. Code of Federal Regulations (CFR) Part 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards(Uniform Guidance), and is also not a required part of the financial statements. The other supplementary information and the schedule of expenditures of federal awards are the responsibility of management and were derived from and relate directly to the underlying accounting and other records used to prepare the basic financial statements. Such information has been subjected to the auditing procedures applied in the audit of the basic financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the financial statements or to the basic financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America. In our opinion, other supplementary information and the schedule of expenditures of federal awards are fairly stated in all material respects in relation to the basic financial statements as a whole.

3

The introductory and statistical sections have not been subjected to the auditing procedures applied in the audit of the basic financial statements and, accordingly, we do not express an opinion or provide any assurance on them.

Other Reporting Required by Government Auditing Standards

In accordance with Government Auditing Standards, we have also issued our report dated December 18, 2016, on our consideration of the County of Rockbridge, Virginia’s internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the County of Rockbridge, Virginia’s internal control over financial reporting and compliance.

Staunton, Virginia December 18, 2016

4

Management’s Discussion and Analysis

As management of the County of Rockbridge, Virginia, we offer the readers of the County’s financial statements this narrative. The narrative provides an overview and analysis of our financial activities for the fiscal year ending June 30, 2016.

Financial Highlights

Government-wide Financial Statements

The combined total assets of the County of Rockbridge, Virginia exceeded its liabilities by $41,749,479 (net position) at the close of the most recent fiscal year. Of the total net position, $37,366,546 is associated with governmental activities and $4,382,933 is associated with business-type activities. Of the net governmental activities net position, $23,911,471 may be used to meet the government’s ongoing obligations to creditors and citizens. There is $232,779 presented under governmental activities which are restricted to ensure the availability of funds for specific functions, programs and anticipated liabilities (ex., capital projects and fire services). These restricted accounts are also displayed on the Balance Sheet of Government Funds. Of the business-type activities net position, $366,856 is unrestricted and available to meet the business-type activity’s obligations. For the year ending June 30, 2016, the governmental activities’ assets include $10,068,860 in taxes receivable while $9,364,953 is reflected as deferred inflows of resources. This is shown as part of compliance with GASB requirements. The $10,068,860 in taxes receivable are booked in the first half of calendar year 2016, but because of twice-a-year tax billing, second half real estate taxes of $8,874,382 are not due until December 2016, and are shown as a deferred revenue. When compared to the net position at year’s end June 30, 2015, the total combined net position increased by $1,837,493 (up 4.6%).

Fund Financial Statements

As of the close of the fiscal year June 30, 2016, the County’s governmental funds reported a combined ending fund balance of $27,192,421. This is an increase of $1,620,036 as compared with the previous fiscal year. The increase in fund balance is associated with collecting higher than estimated general property taxes, other local taxes, use of money and property revenue, and recovered costs. The total unassigned fund balance reported as $20,713,488, or 76.17%, is available for spending at the government’s discretion and for projected capital improvement projects.

At the fiscal year end, unassigned fund balance for the General Fund was $20,713,488 or 51.41% of total General Fund expenditures. This is a 3.28 percentage point decrease in fund balance to expenditure ratio compared to year ending June 30, 2015, but well within the County’s fund balance policy, which requires a 20% unassigned fund balance to expenditures ratio.

In FYE 2016, the Board of Supervisors authorized the re-designation of the Courthouse Construction Fund to the Construction Projects Fund. In an effort to proactively establish dedicated fund sources for existing and future projects, this capital fund, reflected under County Capital Projects Fund in exhibit 3, will account for new construction and major upgrades to County facilities that are approved or planned for in the Capital Improvement Program (CIP). During FYE 2016, the Board authorized the transfer of over $3M from the General Fund to the Construction Project Fund to source the purchase and renovation of a vacant building for a new regional 911 Center. The County will also use the fund balance to pay for approved FYE 2017 CIP projects (new staffed collection centers - $542.5K; County administration building HVAC upgrade - $350K; & Fleet Services facility improvements - $75K). Additionally, the Board approved the creation of a new Capital Purchases Fund to source and account for procurement of vehicles in FYE 2017 and beyond. The Board approved the transfer of nearly $520K into this new fund in FYE 2016. The Capital Purchases Fund is also included under County Capital Projects Fund in exhibit 3.

The School Capital Projects Fund and Broadband Technology Fund are combined under Other Capital Projects Fund in exhibit 3. The combined fund balance is down $235,434 compared to FYE 2015. Ninety-seven percent of the $199,105 balance can be used to source improvements to Maury River Middle School.

5

Overview of the Financial Statements

This discussion and analysis is intended to serve as an introduction to the County’s basic financial statements. These statements include three components: 1) government-wide financial statements, 2) fund financial statements, and 3) notes to the financial statements. This report also contains other supplementary information in addition to the basic financial statements themselves.

Local government accounting and financial reporting originally focused on funds that were designed to enhance and demonstrate fiscal accountability. Now, and in accordance with GASB 34, fund statements are accompanied by government-wide financial statements, to ensure objectives of operational accountability will also be met. These objectives will provide financial statement users with confirmation from the government that public monies have been used to comply with public decisions, and to confirm that operating objectives were met efficiently and effectively and can be met in the future.

Government-wide Financial Statements

Government-wide financial statements provide users with a general overview of County finances. The statements include all assets and liabilities using the accrual basis of accounting. All current year revenue and expenses are taken into account regardless of when cash is received or paid. Both the financial overview and accrual accounting factors are used in the reporting of a private-sector business. Two financial statements are used to present this information: 1) the statement of net position and 2) the statement of activities.

The statement of net position presents all of the County’s permanent account assets, liabilities and net position. The difference between assets and liabilities is reported as net position. Increases or decreases in net position may serve as a useful indicator of whether the financial position of the County is improving or deteriorating. Other non-financial factors such as changes in restricted accounts will also need to be considered to determine the overall financial position of the County.

The statement of activities presents information showing how the government’s net position changed during the fiscal year. The statement is focused on the gross and net cost of various government functions that are supported by general tax and other revenue. The statement of activities presents expenses before revenues, emphasizing that in government, revenues are generated for the express purpose of providing services rather than as an end in themselves.

The government-wide financial statements separate governmental activities and business-type activitiesof the County. Governmental activities are principally supported by taxes and intergovernmental revenues. They include general government administration; judicial administration; public safety; public works; health and welfare; parks, recreation and cultural; community development; and transfers to other funds. Business-type activities recover all or a significant portion of their costs through user fees and charges. The County shows the Rockbridge County Solid Waste Authority as a business-type activity.

The government-wide financial statements include, in addition to the primary government, five component units: 1) the Rockbridge County School Board, 2) the Rockbridge Area Social Services Board, 3) the Rockbridge Regional Jail Commission, and 4) the Rockbridge County Public Service Authority. Although the component units are legally separate entities, the County is accountable or financially accountable for them. A primary government is accountable for an organization if the primary government appoints a majority of the organization’s governing body. A primary government is financially accountable if, in addition, either the government is able to impose its will on the organization or the organization is capable of imposing specific financial burdens on the primary government. For example, the primary government may approve debt issuances, rate structures, and/or provide significant funding for operations of the component unit.

6

Fund Financial Statements

The fund financial statements present only major or significant funds. A fund is a group of related accounts used to maintain control over resources that are segregated for specific activities or objectives. Fund accounting is used to ensure and demonstrate compliance with finance-related legal requirements. The County’s funds can be divided into three categories: governmental funds, proprietary funds, and fiduciary funds.

Governmental funds

Governmental funds are used to account for essentially the same functions, or services, reported as governmental activities in the government-wide financial statements. Whereas the government-wide financial statements are prepared on the accrual basis of accounting, the governmental fund financial statements are prepared on the modified accrual basis of accounting. The focus of modified accrual reporting is on near-term inflows and outflows of financial resources and the balance of financial resources available at the end of the fiscal year. Since the governmental funds focus is narrower than that of the government-wide financial statements, reconciliation between the two methods is provided at the bottom of the governmental fund balance sheet and the governmental fund statement of revenues, expenditures, and changes in fund balances.

Proprietary funds

There are two types of proprietary funds: enterprise funds, which are established to account for the delivery of goods and services to the public and internal service funds that account for the delivery of goods and services to other departments or agencies of the government. Proprietary funds use accrual basis accounting, similar to private sector business.

The Rockbridge County Solid Waste Authority is a blended component unit/business-type activity of the County of Rockbridge. The Authority’s financial statements are shown as a proprietary/enterprise fund in the County’s fund financial statements. The Authority owns the only permitted landfill site within the County of Rockbridge. The Authority has a separate annual financial report that provides more financial details.

Fiduciary funds

Fiduciary funds account for assets held by the government as a trustee or agent for another organization or individual. The County is responsible for ensuring that the assets reported in these funds are used for their intended purposes. Fiduciary funds are not reflected in the government-wide financial statement because the funds are not available to support the County’s own activities.

Notes to the financial statements

These notes provide additional information that is needed to fully understand the data provided in the government-wide and fund financial statements.

Government-wide Financial Analysis

Net Position

As noted, net position may serve as a useful indicator of a government’s financial position. For the County of Rockbridge, combined total assets exceeded liabilities by $41,749,479 at the end of the fiscal year.

The County’s net position is divided into three categories: (1) invested in capital assets, net of related debt, (2) restricted, and (3) unrestricted. A comparative analysis has been provided below.

7

2015, 2015, 2015,2016 as restated 2016 as restated 2016 as restated

Current and other assets $ 38,875,554 $ 37,104,120 $ 11,699,642 $ 4,355,758 $ 50,575,196 $ 41,459,878Capital Assets 72,070,826 75,444,596 4,276,356 3,340,357 76,347,182 78,784,953Total Assets $ 110,946,380 $ 112,548,716 $ 15,975,998 $ 7,696,115 $ 126,922,378 $ 120,244,831

Deferred Outflowsof Resources $ 2,077,918 $ 1,636,013 $ 59,812 $ 54,022 $ 2,137,730 $ 1,690,035

Long-term liabilities $ 64,066,423 $ 65,548,154 $ 10,502,943 $ 3,442,104 $ 74,569,366 $ 68,990,258Other liabilities 2,226,376 2,431,797 1,105,017 783,199 3,331,393 3,214,996Total liabilities $ 66,292,799 $ 67,979,951 $ 11,607,960 $ 4,225,303 $ 77,900,759 $ 72,205,254

Deferred Inflowsof Resources $ 9,364,953 $ 9,714,767 $ 44,917 $ 102,859 $ 9,409,870 $ 9,817,626

Net Position:Net investment in

capital assets $ 13,222,296 $ 14,218,888 $ 2,592,481 $ 2,166,784 $ 15,814,777 $ 16,385,672Unrestricted (deficit) 23,911,471 21,080,229 366,856 44,453 24,278,327 21,124,682Restricted 232,779 1,190,894 1,423,596 1,210,738 1,656,375 2,401,632Total net position $ 37,366,546 $ 36,490,011 $ 4,382,933 $ 3,421,975 $ 41,749,479 $ 39,911,986

COUNTY OF ROCKBRIDGE'S NET POSITIONJune 30, 2016

Governmental Activities Business-type Activities Total

Governmental Activities

For the County, investment in capital assets (i.e., land, buildings, machinery, and equipment), net of related outstanding debt used to acquire those assets is $13,222,296 which represents 35.39% of total net position. The County uses these capital assets to provide services to citizens; therefore, these assets are not available for future spending. Although the County’s investment in its capital assets is reported net of related debt, it should be noted that the resources needed to repay this debt must be provided from other sources, since the capital assets themselves cannot be used to liquidate these liabilities. It is of note that a portion of the capital assets is used to encourage economic development and in turn may produce future revenue for operations in either fees or sale of property.

During the year ending June 30, 2016, total governmental liabilities decreased by $1,687,152. While accounts payable increased by $89,130, the remaining liability categories dropped when compared to FYE 2015. This results mainly from making scheduled debt-service payments.

The restricted net position represents resources that are subject to external or internal restrictions on how they may be used. The restricted net position for fiscal year 2016 included assets restricted by external constraints. For fiscal year 2016, the restricted assets meet the reserve requirements for debt service, and provide for capital improvements to the Maury River Middle School.

The unrestricted net position is $23,911,471, which is 63.99% of total net position, may be used to meet the government’s ongoing obligations to citizens and creditors.

At the end of the fiscal year, the County’s governmental activities realized decreases in two of the three categories of combined total net position. The changes in net position include a decrease in net investment in capital assets of $996,592. Restricted assets decreased in the amount of $958,115 while unrestricted assets were higher by $2,831,242. For the year ending June 30, 2016, the combined total net position increased by $876,535 from last fiscal year.

Business-type Activities

The business-type activities/enterprise fund (landfill and recycling) net position increased by $960,958 resulting from increased tipping fees generating additional cash for future landfill expansion procurement, funds from a revenue bond executed in June 2016, and the value of heavy-duty equipment purchased in

8

FYE 2016. The Authority’s total net position invested in capital assets at the end of the past three years has grown significantly with the procurement of heavy-duty equipment and the on-going stages of developing a new piggy-back lined landfill. The Authority uses capital assets to provide services to its customers, so these assets are not available for future spending.

Changes in Net Position

The following table presents the revenues and expenses of the governmental and business-type activities. Following the table is a brief highlight and discussion on key elements of Rockbridge County’s change in net position.

2015, 2015, 2015,2016 as restated 2016 as restated 2016 as restated

Revenues:Program revenues:Charges for services $ 2,165,018 $ 2,404,454 $ 2,098,447 1,578,750 $ 4,263,465 $ 3,983,204 Operating grants 2,381,742 2,424,462 23,300 23,046 2,405,042 2,447,508 Capital grants 41,945 273,913 - - 41,945 273,913 General Revenues:Property taxes 24,775,816 24,210,212 - - 24,775,816 24,210,212 Other taxes 9,009,065 8,619,694 - - 9,009,065 8,619,694 Use of money and property 113,017 57,337 11,162 3,413 124,179 60,750 Other 833,978 943,636 25,869 8,927 859,847 952,563 Grants and contributions not restricted to specific programs 2,749,809 2,732,823 - - 2,749,809 2,732,823 Total Revenues $ 42,070,390 $ 41,666,531 $ 2,158,778 $ 1,614,136 $ 44,229,168 $ 43,280,667

Expenses:GeneralGeneral Govt. Admin $ 2,888,023 $ 2,294,804 $ - $ - $ 2,888,023 $ 2,294,804 Judicial administration 1,363,768 1,283,097 - - 1,363,768 1,283,097 Public safety 7,165,176 6,492,719 - - 7,165,176 6,492,719 Public works 3,257,681 2,879,018 1,647,771 1,435,346 4,905,452 4,314,364 Health and welfare 1,641,027 1,330,106 - - 1,641,027 1,330,106 Education 15,794,029 14,980,144 - - 15,794,029 14,980,144 Parks, recreation, and culture 1,431,206 1,289,331 - - 1,431,206 1,289,331 Community development 2,933,943 3,088,793 - - 2,933,943 3,088,793 Non-departmental 1,780,693 1,757,409 - - 1,780,693 1,757,409 Interest on long-term debt 2,488,358 2,449,604 - - 2,488,358 2,449,604 Total expenses $ 40,743,904 $ 37,845,025 $ 1,647,771 $ 1,435,346 $ 42,391,675 $ 39,280,371

Increase (decrease) in netposition before transfers $ 1,326,486 $ 3,821,506 $ 511,007 $ 178,790 $ 1,837,493 $ 4,000,296

Transfers (449,951) (220,708) 449,951 220,708 - - Increase (decrease) net position $ 876,535 $ 3,600,798 $ 960,958 $ 399,498 $ 1,837,493 $ 4,000,296 Net position - beginning as restated 36,490,011 32,889,213 3,421,975 3,022,477 39,911,986 35,911,690 Net position - ending $ 37,366,546 $ 36,490,011 $ 4,382,933 $ 3,421,975 $ 41,749,479 $ 39,911,986

COUNTY OF ROCKBRIDGE'S CHANGES IN NET POSITIONJune 30, 2016

Governmental Activities Business-type Activities Total

Note: Net position as reported at June 30, 2015 is restated to record additional advances to/from participating entities. Specifically, the Rockbridge County General Fund transferred funding to the Rockbridge County Solid Waste Authority to source due diligence efforts associated with the lateral expansion of current operations.

9

Governmental Activities

Governmental activities increased the County’s net position by $876,535. Key elements relating to FYE 2016 activities compared to the prior fiscal year will be discussed below.

Revenues increased by $403,859. The following table provides a breakdown on the various revenues sources as of June 30, 2016.

Type Overall total % 1. Property taxes 58.89% 2. Other local taxes 21.41% 3. Non-restricted grants and contributions 6.54% 4. Operating and capital grants 5.76% 5. Charges for services 5.15% 6. Other general revenues 1.98% 7. Use of money and property 0.27%

Component changes from FYE 2015, as restated, to FYE 2016 include:

The largest source of revenues is general property taxes at $24,775,816. General property tax collections rose by $565,604. The Board approved a two-cent increase to the real property tax rate in calendar year 2016 contributing to higher revenues in the June 2016 billing cycle. In addition, public service corporation, personal property, and machinery and tools taxes increased as a result of higher value growth and/or collection levels.

Other local taxes increased by $389,371. Sales, meals, occupancy, and bank franchise taxes continued a positive trend in receipts collected, a reflection of on-going tourism and economic development efforts in the County.

Non-restricted grants or contributions increased by $16,986 as state-shared revenues for mobile home titling and motor vehicle rentals came in higher than projected.

Operating and capital grants dropped by $274,688. This reflects the final stages of a grant reimbursement linked to the completion of the Greenhouse Village water and sewer infrastructure system for a low-to-moderate income housing development began in FYE 2014.

Charges for services decreased by $239,436 due to the one-time permit fees collected in FYE 2015 for the Washington and Lee University housing and natatorium projects which generated over $300,000 in service revenues.

Other revenues were lower by $109,658 resulting from miscellaneous collections (sale of supplies, patron refunds/rebates, and loan proceeds) coming in lower than anticipated.

Use of money and property rose by $55,680. A combination of ongoing income from County property rentals and a new investment methodology by the Treasurer contributed to the revenue increase.

The following table reflects the distribution of FYE 2016 governmental expenditures. For the year, the Board of Supervisors’ expenditure priorities were to maintain improvements in education, public safety, public works, health and welfare, and economic development. In addition, the Board approved a 2% cost-of-living adjustment and step increases to eligible employees, effective July 1, 2015, with a goal of retaining and attracting a quality workforce via competitive compensation. Overall expenses increased by $2,898,879 over the same period in FYE 2015. As shown, education expenses account for 38.76% of total expenses. When combined with public safety, public works, health and welfare, and community development, expenditures for these five categories are 75.58% of the $40,743,904 in total expenses.

10

Type Overall total % 1. Education 38.76% 2. Public Safety 17.59% 3. Public Works 8.00% 4. Community Development 7.20% 5. General Government Administration 7.09% 6. Long-term debt interest 6.11% 7. Non-departmental 4.37% 8. Health and Welfare 4.03% 9. Parks, Recreation, and Cultural 3.51% 10. Judicial Administration 3.35%

Component changes from FYE 2015 to FYE 2016 include:

Education expenses increased by $813,885. The asset allocation from the General Fund to the School Fund was approximately $1.6 million more in FYE 2016 compared to FYE2015. The primary driver to the upward change is that debt service on school board debt financed assets rose by over $416K as a result of the financing of the Maury River Middle School renovation. Assets for the School Division are recorded by the County and then reclassified back to the School Division as the debt on the assets is paid. In FYE 2016, the net amount of assets/accumulated depreciation transferred back to the School Division was $2,701,922. While the asset allocation increased expenses by $1.6 million, the operating transfers to the School Board decreased by approximately $746,000.

Public Safety reflects an increase of $672,457. The County’s procurement of a vacant building ($375K) for renovation into a regional communications (911) and emergency operations center (EOC) occurred under this category. In addition, seven volunteer fire departments were approved for a 15% increase in the operational contribution while the variable pay amount was also increased by 15% (up a combined total of ~$82K). Furthermore, the Board funded $54K for contracted services to cover annual inspections of all fire apparatus pumps, aerial ladders, ground ladders, self contained breathing apparatus, and hoses. The Board also approved targeted increases for the contribution towards two volunteer rescue squads at 15% while two others received an additional 5% to account for additional consumables used at their respective facilities that are housing a contracted ambulance service. The overall squad contributions are up ~$52K. Lastly, the County cost-share costs for the regional jail function rose by ~$60K based on the number of Rockbridge County citizens housed in the facility each month and an increase in overall per capita incarceration costs.

Public Works increased by $378,663. This category pays the County’s cost-share for the landfill operation. The cost per ton tipping fee increased by approximately $14 per ton in FYE 2016 as part of two-year plan to build surplus cash to assist the Rockbridge County Solid Waste Authority with future capital procurement efforts and development of a budget stabilization fund. The combination of the higher tipping fee and actual tonnage generated this upward change.

Community Development decreased by $154,850. The County had previously secured a $262,650 community development grant to provide water and sewer infrastructure for a primarily low- and moderate-income person’s subdivision which was substantially completed in FYE 2015.

General government administration increased by $593,219. Approximately $303,000 of the increase is due to the completion of the general reassessment which began in FYE 2016. In addition, the County developed and funded all costs associated with a new human resources position ($78K). The Board also approved procuring hardware and software updates for the municipal financial management modules required for efficient operations and reporting. Lastly, professional engineering services linked to space-needs analysis, environmental assessment, and facility design for a new 911 center were accounted for in this category.

Long-term debt interest payments are up $38,754 based on current debt payment schedules. Non-departmental was up $23,284 resulting from an increase in the Modified Voluntary

Settlement of Annexation and Immunity payment from Rockbridge County to Lexington City.

11

Health and Welfare reflects an increase of $310,921 primarily because the County’s cost-share funding for the Comprehensive Services Act program was higher than the prior fiscal year due to increased cases involving Rockbridge County residents.

Parks, Recreation and Cultural increased by $141,875 due in part to the funding of higher cost-share for the regional library and talking books program for the elderly and disabled; converting a part-time parks and recreation position into full-time status; and providing the regional recreation organization with additional capital funding originally planned for FYE 2017.

Judicial Administration rose by $80,671 reflecting the unscheduled replacement of the courthouse security system (over $67K) and the full-year, County funding of a new position within the Clerk of the Circuit Court department.

Business-type Activities

The business-type activities/enterprise fund (landfill and recycling) net position increased by $960,958. Tipping fee revenues for FYE 2016 increased by $519,697 resulting from the final step in a 2-year plan to raise charges for services to generate additional surplus in FYEs 2015 and 2016. The additional surplus cash will offset future construction costs and equipment procurement related to cell 1 of the lateral expansion of the landfill. In addition, landfill staff continue to extract scrap metal from the working face of the active cell while recycling materials collected at staffed centers are compacted in preparation for transporting. Each commodity is sold on the recyclable materials market. The Authority realized nearly $12,450 in additional revenue from selling these resources during the fiscal year. Lastly, an improved methodology of investing closure/post-closure funds resulted in a $7,749 improvement in investment income compared to FYE 2015.

Expenditures realized a $212,425 increase compared to FYE 2015. The four primary drivers are: 1) interest expense and bond issue cost ($130,047), 2) depreciation ($71,447), 3) contractual services ($36,347), and 4) personnel costs ($29,658). These individual categories grew due to the following respective factors: 1) new revenue bond and lease-purchase financing, 2) depreciating additional equipment purchased later in FYE 2015 and earlier in FYE 2016, 3) new hauling contract which incorporated transporting recycling stream to buyers beyond County limits, and 4) compensation increases for full and part-time employees.

Transfers from the Rockbridge County General Fund supported the county recycling program accounted for under the Authority. The County transfers funding to subsidize the recycling program. During FYE 2016, the transfer to the Recycling Fund totaled $459,051. The RCSWA conveyed a 6.05 acre plat to the County for the purpose of building a law enforcement shooting range and training facility – resulting in a transfer out of $9,100.

Financial Analysis of the Government’s Funds

As previously mentioned, the County uses fund accounting to ensure and demonstrate compliance with finance-related legal requirements.

Governmental funds

The focus of the County’s governmental funds is to provide information on near-term inflows, outflows, and balances of financial resources. Such information is useful in assessing the County’s financing requirements. Unassigned fund balance may serve as a useful measure of a government’s net resources available for spending at the end of the fiscal year.

At the end of the fiscal year, the County’s total governmental funds reported combined ending fund balances of $27,192,421, an increase of $1,620,036 over the prior fiscal year. The increase is associated with assets growing by $1,792,330 when compared to FYE 2015. This total is impacted by positive changes in cash and cash equivalents (up $1,841,651), taxes receivables (up $276,920), and advances to other entities (up $566,177). In addition, due to other government liabilities dropped $63,337 compared to FYE 2015. Lastly, school carryover increased by $167,393 as a result of unexpended funds and were restricted to source future School Board capital projects.

12

The General Fund is the chief operating fund of the County. As of June 30, 2016, unassigned fund balance of the General Fund was $20,713,488. This is a decrease in unassigned fund balance of $1,143,081 compared with the previous fiscal year. The total fund balance of the General Fund is $22,903,794. This is a decrease over the previous year by $2,234,052, a result of the aforementioned transfer of previously gained surplus to fund planned capital projects.

As a measure of the General Fund’s liquidity, it is useful to compare both unassigned fund balance and total fund balance to total fund expenditures. Unassigned fund balance represents 51.41% of total General Fund expenditures, which includes transfers to the School Board component unit of $12,998,898 for operational support. The Board of Supervisors financial policy is to maintain a minimum of 20% unassigned fund balance to expenditures ratio. Total fund balance represents 56.84% of total General Fund expenditures.

Proprietary funds

The County’s proprietary fund statements provide the same type of information found in the government-wide financial statements, but in more detail.

The Rockbridge County Solid Waste Authority (RCSWA) owns and the County operates a permitted landfill that was targeted for closure on December 31, 2014. A 2014 request for permit extension to June 30, 2017 received Virginia Department of Environmental Quality (VA DEQ) approval. Part of the fund balance will be used to meet landfill closure requirements of the VA DEQ. The net funds associated with financing these requirements are restricted. This restricted fund balance will support landfill operations and equipment purchases as needed. Other factors concerning the finances of this fund were discussed in the County’s business-type activities section of this summary. Net position of the landfill fund at the end of the year was $4,324,996 while the recycling fund net position is $57,937. Additional detail is provided in the RCSWA financial report.

General Fund Budgetary Highlights

The difference between the original budgeted appropriations and the final, amended-budget appropriations was a $399,263 increase. This is 0.96% of the total original budget. The actual expenditures were $1,513,334 below the final appropriation total. This total is 3.62% below the final budget. The major components of these appropriation changes are:

Carryover funding from FYE 2015 CIP projects that remained in progress at the start of FYE 2016.

The Board of Supervisors authorized funding a space-needs analysis related to constructing a co-located, regional communications (911) and emergency operations center (EOC).

The Board approved the first-year request to fund the Dabney S. Lancaster Community College “The Dabney Promise” scholarship program, which supports eligible, County residents in meeting their educational needs.

The Board authorized funding an environmental assessment, and later design development, of a vacant building procured for a new 911 Center and EOC.

A Virginia Community Development Block Grant approved to support the completion of an infrastructure project for a low-to-moderate income family housing project carried over into FYE 2016 for final completion.

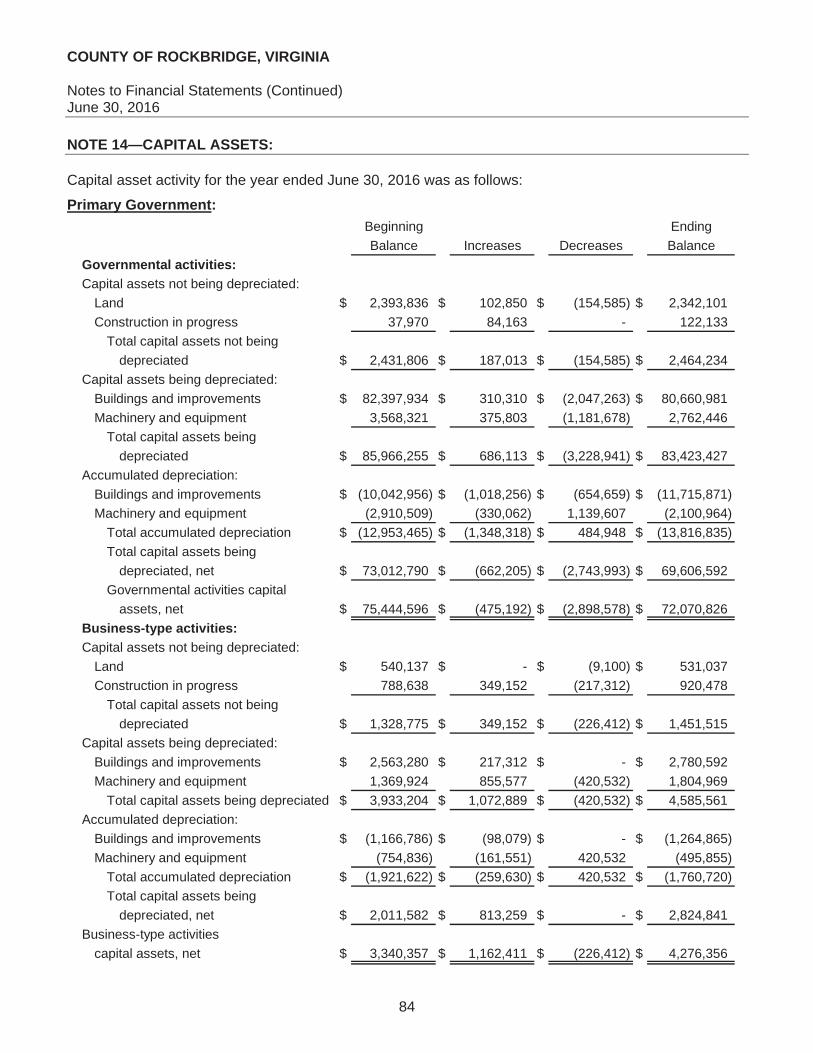

Capital Asset and Debt Administration

Capital assets The County’s investment in capital assets for its governmental activities as of June 30, 2016 was $72,070,826 (net of accumulated depreciation). This investment in capital assets includes land, buildings and systems, and machinery and equipment. This is a decrease of $3,373,770 from the previous fiscal year, or 4.47%. The primary change in capital assets is the result of depreciation.

13

The County’s investment in capital assets for its proprietary funds is $4,276,356, an increase of $935,999 from the previous year. This is a result of the completion of a new office building, procurement of additional heavy-duty equipment, and on-going, lateral expansion efforts at the landfill during the fiscal year.

2016 2015 2016 2015 2016 2015

Land $ 2,342,101 $ 2,393,836 $ 531,037 $ 540,137 $ 2,873,138 $ 2,933,973Buildings and systems 68,945,110 72,354,978 1,515,727 1,396,494 70,460,837 73,751,472Machinery & equipment 661,482 657,812 1,309,114 615,088 1,970,596 1,272,900Construction in progress 122,133 37,970 920,478 788,638 1,042,611 826,608 Total $ 72,070,826 $ 75,444,596 $ 4,276,356 $ 3,340,357 $ 76,347,182 $ 78,784,953

Governmental Activities Business-type Activities Total

COUNTY OF ROCKBRIDGE'S CAPITAL ASSETSNet of Depreciation

Additional information on the County’s capital assets can be found in the Note 14 to the financial statements.

Long-term debt

At the end of fiscal year 2016, the County had the following outstanding debt:

2016 2015 2016 2015 2016 2015

General Obligation Bonds $ 42,453,194 $ 43,604,236 $ - $ - $ 42,453,194 $ 43,604,236Revenue Bonds 16,745,000 17,390,000 7,264,710 724,462 24,009,710 18,114,462Literary Loans 1,075,000 1,255,000 - - 1,075,000 1,255,000Capital Leases - - 916,590 449,111 916,590 449,111Compensated Absences 335,203 301,028 36,716 32,291 371,919 333,319Net pension liability 3,292,026 2,849,890 301,416 260,935 3,593,442 3,110,825OPEB Obligation 166,000 148,000 3,000 3,000 169,000 151,000Landfill closure liability - - 1,980,511 1,972,305 1,980,511 1,972,305Total long-term obligations $ 64,066,423 $ 65,548,154 $ 10,502,943 $ 3,442,104 $ 74,569,366 $ 68,990,258

COUNTY OF ROCKBRIDGE'S LONG-TERM OBLIGATIONS

Governmental Activities Business-type Activities Total

The County’s total long-term debt includes the Rockbridge County School Board debt and the business-type activities debt. For the year, the total, combined long-term debt increased by $5,579,108. The County completed an advance refunding of the former 2007 courthouse loan, which generated an estimated net present value savings of $613,354, an 11.96% change. On May 25, 2016, the Solid Waste Authority executed a revenue bond of $5,710,000, with $856,329 premium, to finance the development of a new landfill cell. In addition, the Authority completed a $681,832 lease-purchase of an articulated haul truck and excavator as part of planned CIP efforts. The governmental and business-type activities’ compensated absences, net pension liability, and OPEB obligation and are included in the long-term debt to meet GASB requirements. These categories changed as follows: 1) compensated absences (rose $38,600); 2) net pension liability (increased $482,617); and 3) OPEB obligation (grew $18,000).

Additional information on the County’s long-term debt can be found in Note 7 to the financial statements.

14

Economic Factors and Next Year’s Budgets and Rates

The Rockbridge County population was 22,307 as of the April 1, 2010 U.S. Census. The Weldon Cooper Institute’s July 1, 2015 population estimate reflects 22,163, a decrease of 144 (0.65%). Minimal change in population has occurred over the past decade and no substantial change is anticipated in the next fiscal year.

For the fiscal year ending June 30, 2016, the unemployment rate for the Commonwealth and Rockbridge County were 4.0% and 4.5% respectively. During the progress of this management discussion and analysis report, the October 2016 unemployment rate rose to 4.1% for the state and 4.8% in the County. Overall, local efforts by the Board of Supervisors to fund a variety of economic development initiatives continue in an effort to generate new business inquiries and interest.

The Board of Supervisors fiscal year 2017 budget priorities include limiting overall expenditures in all areas except education, “safety net” programs, public safety, solid waste management, emergency communications, and economic development. These activities may require increased funding compared to prior years. Additionally and primarily, the Board’s goals include meeting all mandates, debt services, and legal obligations.

In FYE 2016 the Board of Supervisors continued its annual support of educational programs. The County student population continues to remain consistent at approximately 2,600. The County’s restricted funding which sourced the local supplement to offset increasing Virginia Retirement System increases over the past several years was depleted at FYE 2016. The Board committed to increase the local operational transfer in FY 2017 by $232,000 (or one penny on the real estate tax rate).

The County continues to tackle capital improvement projects through long-term planning and funding. Projects include the ongoing efforts to construct a new regional 911 center, development of additional staffed collection center sites, completion of major upgrades to the County’s administration building, building a Sheriff Office shooting range classroom facility, and procuring new voting equipment. Additionally, debt service commitments will involve financing a “piggyback” lined landfill and the next phase of a regional radio system upgrade (subscriber units). Decisions on these and other funding decisions were guided by the Board’s mission, vision and values statements, which drive strategic plans and funding priorities.

The County’s commitment to improve the regional Central Dispatch operations involves a cost-share (with our regional governmental partners) commitment to replace the 911 Center’s computer aided dispatch system. This one-time capital improvement within the 911 Center budget, in addition to other approved expenditures, increased the County’s contribution to this critical service by $238,201.

The Board of Supervisors chose to use $427,250 in unassigned fund balance and $147,450 in restricted accounts to fund one-time and carryover capital efforts to provide a limited level of budget stabilization. As result of increased debt service, expanded public safety services, and higher personnel costs, the real property tax rate was increased to $0.735 per $100.00 of assessed valuation i.e. a two cent increase). The personal property rate of $4.25 remained unchanged from the prior year.

All of these factors were considered in preparing the County’s budget for the 2017 fiscal year.

Requests for Information

This financial report is designed to provide readers with a general overview of the County of Rockbridge finances. Questions concerning any of the information provided in this report or requests for additional financial information should be addressed to the Rockbridge County Administrator, 150 S. Main Street, Lexington, Virginia 24450.

BASIC FINANCIAL STATEMENTS

GOVERNMENT-WIDE FINANCIAL STATEMENTS

County of Rockbridge, VirginiaStatement of Net Position

Governmental Business-typeActivities Activities Total

ASSETSCash and cash equivalents $ 21,084,279 $ 1,614,827 $ 22,699,106 Investments - - - Receivables (net of allowance for uncollectibles):

Taxes receivable 10,068,860 - 10,068,860 Accounts receivable 725,451 67,360 792,811

Internal balances (115,923) 115,923 - Due from component units 2,016,342 - 2,016,342 Due from other governmental units 993,921 - 993,921 Inventories 104,915 - 104,915 Advances to other entities 3,819,848 - 3,819,848 Prepaid items - - - Restricted assets:

Cash and cash equivalents 177,861 9,901,532 10,079,393 Net pension asset - - - Capital assets (net of accumulated depreciation):

Land 2,342,101 531,037 2,873,138 Buildings and improvements 68,945,110 1,515,727 70,460,837 Machinery and equipment 661,482 1,309,114 1,970,596 Utility plant and equipment - - - Construction in progress 122,133 920,478 1,042,611

Total assets $ 110,946,380 $ 15,975,998 $ 126,922,378

DEFERRED OUTFLOWS OF RESOURCESDeferred charge on refunding $ 1,424,664 $ - $ 1,424,664 Items related to measurement of net pension liability 38,832 3,556 42,388 Pension contributions subsequent to measurement date 614,422 56,256 670,678

Total deferred outflows of resources $ 2,077,918 $ 59,812 $ 2,137,730

LIABILITIESAccounts payable $ 365,590 $ 33,828 $ 399,418 Advances from participating entities - 74,292 74,292 Capital advances from Rockbridge County - 957,773 957,773 Accrued interest payable 810,327 39,124 849,451 Due to primary government - - - Performance deposits 149,187 - 149,187 Due to other governments 899,741 - 899,741 Unearned revenue 1,531 - 1,531 Deposits payable - - - Long-term liabilities:

Due within one year 2,313,339 347,744 2,661,083 Due in more than one year 61,753,084 10,155,199 71,908,283

Total liabilities $ 66,292,799 $ 11,607,960 $ 77,900,759

DEFERRED INFLOWS OF RESOURCESDeferred revenue-property taxes $ 8,874,382 $ - $ 8,874,382 Items related to measurement of net pension liability 490,571 44,917 535,488

Total deferred inflows of resources $ 9,364,953 $ 44,917 $ 9,409,870

NET POSITIONNet investment in capital assets $ 13,222,296 $ 2,592,481 $ 15,814,777 Restricted

Fire funds 53,912 - 53,912 Rental assistance 1,006 - 1,006 Capital projects 168,890 - 168,890 Debt service 8,971 1,423,596 1,432,567

Unrestricted 23,911,471 366,856 24,278,327 Total net position $ 37,366,546 $ 4,382,933 $ 41,749,479

The notes to the financial statements are an integral part of this statement.

Primary Government

June 30, 2016

15

Exhibit 1

Component ComponentComponent Unit Unit

Unit Rockbridge Rockbridge Component Rockbridge Regional Public

Unit Area Social Jail ServiceSchool Board Services Commission Authority

$ 140,179 $ 398,186 $ 200 $ 4,045,992 - - - 1,017,863

- - - - 51,474 7,928 15,392 429,659

- - - - - - - -

814,451 517,406 332,289 - 36,137 - - 59,380

- - - - 590,751 3,385 - -

- - - 59,920 - 3,237 - 40,528

117,555 - - 389,259 18,089,990 - 3,154,991 67,698

1,875,090 14,342 33,408 173,830 - - - 23,720,661- - - 129,349

$ 21,715,627 $ 944,484 $ 3,536,280 $ 30,134,139

$ - $ - $ - $ - 20,617 - 13,166 -

2,327,179 94,393 208,323 30,013 $ 2,347,796 $ 94,393 $ 221,489 $ 30,013

$ 141,954 $ 228,650 $ 43,410 $ 348,718 - - - - - - - - - - - -

1,310,941 633,801 71,600 - - - - - - 64,454 - - - - - - - - - 59,920

42,458 16,781 42,223 918,550 28,477,540 50,344 1,306,847 11,251,529

$ 29,972,893 $ 994,030 $ 1,464,080 $ 12,578,717

$ - $ - $ - $ - 2,742,379 218,796 166,330 56,937

$ 2,742,379 $ 218,796 $ 166,330 $ 56,937

$ 20,082,635 $ 14,342 $ 3,188,399 $ 12,370,263

- - - - - - - - - - - - - - - -

(28,734,484) (188,291) (1,061,040) 5,158,235 $ (8,651,849) $ (173,949) $ 2,127,359 $ 17,528,498

16

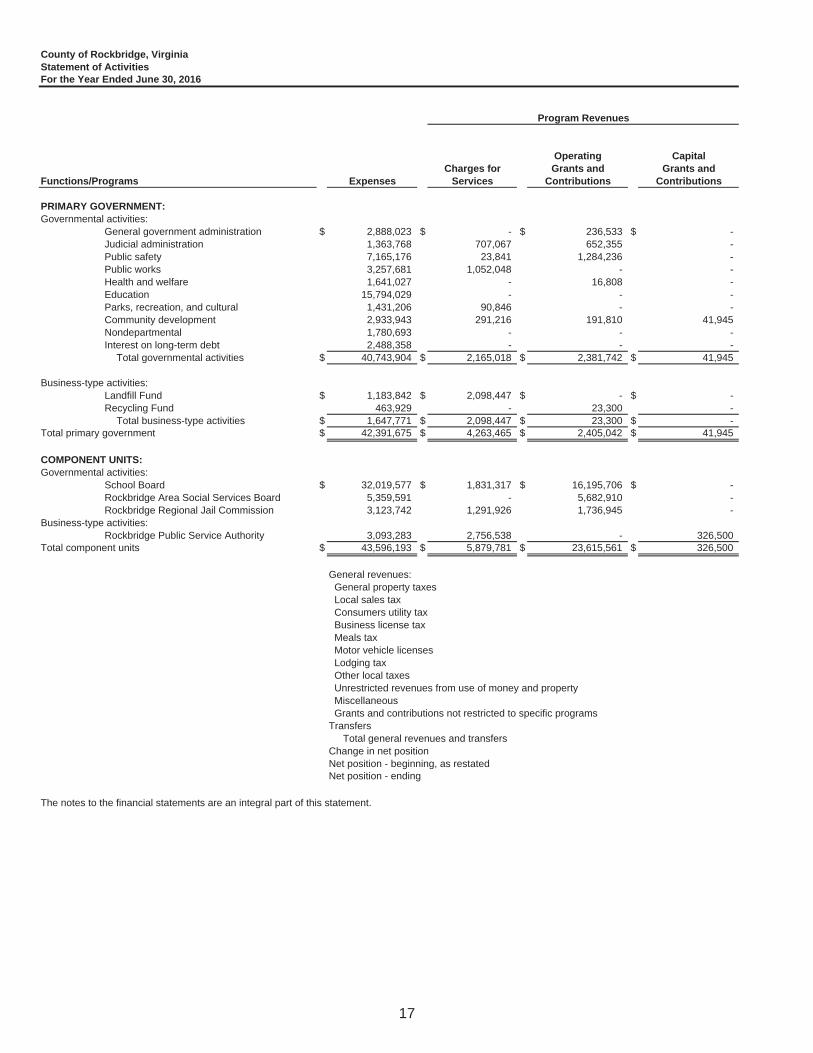

County of Rockbridge, VirginiaStatement of ActivitiesFor the Year Ended June 30, 2016

Operating CapitalCharges for Grants and Grants and

Functions/Programs Expenses Services Contributions Contributions

PRIMARY GOVERNMENT:Governmental activities:

General government administration $ 2,888,023 $ - $ 236,533 $ - Judicial administration 1,363,768 707,067 652,355 - Public safety 7,165,176 23,841 1,284,236 - Public works 3,257,681 1,052,048 - - Health and welfare 1,641,027 - 16,808 - Education 15,794,029 - - - Parks, recreation, and cultural 1,431,206 90,846 - - Community development 2,933,943 291,216 191,810 41,945 Nondepartmental 1,780,693 - - - Interest on long-term debt 2,488,358 - - -

Total governmental activities $ 40,743,904 $ 2,165,018 $ 2,381,742 $ 41,945

Business-type activities:Landfill Fund $ 1,183,842 $ 2,098,447 $ - $ - Recycling Fund 463,929 - 23,300 -

Total business-type activities $ 1,647,771 $ 2,098,447 $ 23,300 $ - Total primary government $ 42,391,675 $ 4,263,465 $ 2,405,042 $ 41,945

COMPONENT UNITS:Governmental activities:

School Board $ 32,019,577 $ 1,831,317 $ 16,195,706 $ - Rockbridge Area Social Services Board 5,359,591 - 5,682,910 - Rockbridge Regional Jail Commission 3,123,742 1,291,926 1,736,945 -

Business-type activities:Rockbridge Public Service Authority 3,093,283 2,756,538 - 326,500

Total component units $ 43,596,193 $ 5,879,781 $ 23,615,561 $ 326,500

General revenues: General property taxes Local sales tax Consumers utility tax Business license tax Meals tax Motor vehicle licenses Lodging tax Other local taxes Unrestricted revenues from use of money and property Miscellaneous Grants and contributions not restricted to specific programsTransfers

Total general revenues and transfersChange in net positionNet position - beginning, as restatedNet position - ending

The notes to the financial statements are an integral part of this statement.

Program Revenues

17

Exhibit 2

Net (Expense) Revenue andChanges in Net Position

Component Unit Component Unit Component Unit Component UnitRockbridge Rockbridge Rockbridge

Area Regional PublicGovernmental Business-type School Social Jail Service

Activities Activities Total Board Services Commission Authority

$ (2,651,490) $ - $ (2,651,490) $ - $ - $ - $ - (4,346) - (4,346) - - - -

(5,857,099) - (5,857,099) - - - - (2,205,633) - (2,205,633) - - - - (1,624,219) - (1,624,219) - - - -

(15,794,029) - (15,794,029) - - - - (1,340,360) - (1,340,360) - - - - (2,408,972) - (2,408,972) - - - - (1,780,693) - (1,780,693) - - - - (2,488,358) - (2,488,358) - - - -

$ (36,155,199) $ - $ (36,155,199) $ - $ - $ - $ -

$ - $ 914,605 $ 914,605 $ - $ - $ - $ - - (440,629) (440,629) - - - -

$ - $ 473,976 $ 473,976 $ - $ - $ - $ - $ (36,155,199) $ 473,976 $ (35,681,223) $ - $ - $ - $ -

$ - $ - $ - $ (13,992,554) $ - $ - $ - - - - - 323,319 - - - - - - - (94,871) -

- - - - - - (10,245) $ - $ - $ - $ (13,992,554) $ 323,319 $ (94,871) $ (10,245)

$ 24,775,816 $ - $ 24,775,816 $ - $ - $ - $ - 2,720,814 - 2,720,814 - - - - 1,488,723 - 1,488,723 - - - -

849,796 - 849,796 - - - - 1,439,665 - 1,439,665 - - - -

540,217 - 540,217 - - - - 1,636,776 - 1,636,776 - - - -

333,074 - 333,074 - - - - 113,017 11,162 124,179 97 - 19 39,671 833,978 25,869 859,847 82,127 - 14,028 34,298

2,749,809 - 2,749,809 15,710,645 - - 185,342 (449,951) 449,951 - - - - -

$ 37,031,734 $ 486,982 $ 37,518,716 $ 15,792,869 $ - $ 14,047 $ 259,311 876,535 960,958 1,837,493 1,800,315 323,319 (80,824) 249,066

36,490,011 3,421,975 39,911,986 (10,452,164) (497,268) 2,208,183 17,279,432 $ 37,366,546 $ 4,382,933 $ 41,749,479 $ (8,651,849) $ (173,949) $ 2,127,359 $ 17,528,498

Primary Government

18

FUND FINANCIAL STATEMENTS

County of Rockbridge, Virginia Exhibit 3Balance SheetGovernmental Funds

County OtherCapital Capital

General Projects ProjectsFund Fund Fund Total

ASSETSCash and cash equivalents $ 16,908,595 $ 4,143,632 $ 32,052 $ 21,084,279Receivables (net of allowance

for uncollectibles):Taxes receivable 10,068,860 - - 10,068,860Accounts receivable 725,451 - - 725,451

Advances to other entities 3,819,848 - - 3,819,848Due from other funds 1,837 - - 1,837Due from component units 2,016,342 - - 2,016,342Due from other governmental units 993,921 - - 993,921Inventories 104,915 - - 104,915Restricted assets:

Cash and cash equivalents 8,971 - 168,890 177,861Total assets $ 34,648,740 $ 4,143,632 $ 200,942 $ 38,993,314

LIABILITIESAccounts payable $ 311,480 $ 54,110 $ - $ 365,590Due to other governments 899,741 - - 899,741Due to other funds 115,923 - 1,837 117,760Performance deposits 149,187 - - 149,187Unearned revenue 1,531 - - 1,531

Total liabilities $ 1,477,862 $ 54,110 $ 1,837 $ 1,533,809

DEFERRED INFLOWS OF RESOURCESUnavailable revenue-property taxes $ 10,267,084 $ - $ - $ 10,267,084

FUND BALANCESNonspendable:

Inventories $ 104,915 $ - $ - $ 104,915Total nonspendable $ 104,915 $ - $ - $ 104,915

Restricted:Debt service and bond covenants $ 8,971 $ - $ - $ 8,971Capital projects - - 168,890 168,890Rental assistance 1,006 - - 1,006Fire program 53,912 - - 53,912

Total restricted $ 63,889 $ - $ 168,890 $ 232,779Assigned:

Garage $ 165,469 $ - $ - $ 165,469Industrial property 603,193 - - 603,193School carryover 607,395 - - 607,395Convenience centers 12,075 - - 12,075Partnership 82,097 - - 82,097Recreation 10,000 - - 10,000Revenue recovery 541,273 - - 541,273Capital projects funds - 4,089,522 30,215 4,119,737

Total assigned $ 2,021,502 $ 4,089,522 $ 30,215 $ 6,141,239

Unassigned $ 20,713,488 $ - $ - $ 20,713,488Total unassigned $ 20,713,488 $ - $ - $ 20,713,488

Total fund balances $ 22,903,794 $ 4,089,522 $ 199,105 $ 27,192,421Total liabilities, deferred inflows of resources and fund balances $ 34,648,740 $ 4,143,632 $ 200,942 $ 38,993,314

The notes to the financial statements are an integral part of this statement.

June 30, 2016

19

County of Rockbridge, Virginia Exhibit 4

Amounts reported for governmental activities in the statement of net position are different because:

Total fund balances per Exhibit 3 - Balance Sheet - Governmental Funds $ 27,192,421

72,070,826

902,131

614,422

(63,413,254)

Net position of governmental activities $ 37,366,546

The notes to the financial statements are an integral part of this statement.

Capital assets used in governmental activities are not financial resources and, therefore, arenot reported in the funds.

Other long-term assets are not available to pay for current-period expenditures and, therefore,are deferred in the funds.

Long-term liabilities, including bonds payable, are not due and payable in the current periodand, therefore, are not reported in the funds.

Reconciliation of the Balance Sheet of Governmental FundsTo the Statement of Net PositionJune 30, 2016

Pension contributions subsequent to the measurement date will be a reduction to the net pension liability in the next fiscal year and, therefore, are not reported in the funds.

20

County of Rockbridge, Virginia Exhibit 5

County OtherCapital Capital

Projects ProjectsGeneral Fund Fund Total

REVENUESGeneral property taxes $ 24,843,541 $ - $ - $ 24,843,541Other local taxes 9,009,065 - - 9,009,065Permits, privilege fees,

and regulatory licenses 275,060 - - 275,060Fines and forfeitures 445,370 - - 445,370Revenue from the use of

money and property 112,157 - 860 113,017Charges for services 1,444,588 - - 1,444,588Miscellaneous 833,978 - - 833,978Recovered costs 469,735 - - 469,735Intergovernmental:

Commonwealth 4,965,583 - - 4,965,583Federal 207,913 - - 207,913

Total revenues $ 42,606,990 $ - $ 860 $ 42,607,850

EXPENDITURESCurrent:

General government administration $ 2,117,583 $ - $ - $ 2,117,583Judicial administration 1,472,432 - - 1,472,432Public safety 7,403,041 - - 7,403,041Public works 3,312,600 - - 3,312,600Health and welfare 1,639,246 - - 1,639,246Education 13,082,282 - - 13,082,282Parks, recreation, and cultural 1,427,654 - - 1,427,654Community development 2,808,451 - - 2,808,451Nondepartmental 1,780,693 - - 1,780,693

Capital projects - 477,000 9,825 486,825Debt service:

Principal retirement 2,502,118 - - 2,502,118Interest and other fiscal charges 2,746,012 - - 2,746,012

Total expenditures $ 40,292,112 $ 477,000 $ 9,825 $ 40,778,937

Excess (deficiency) of revenues over(under) expenditures $ 2,314,878 $ (477,000) $ (8,965) $ 1,828,913

OTHER FINANCING SOURCES (USES)Transfers in $ 9,100 $ 4,566,522 $ - $ 4,575,622Transfers out (4,799,104) - (226,469) (5,025,573)Issuance of refunding bonds 4,985,000 - - 4,985,000Premium on refunding bonds issued 835,950 - - 835,950Payment to refunded bond escrow agent (5,579,876) - - (5,579,876)

Total other financing sources (uses) $ (4,548,930) $ 4,566,522 $ (226,469) $ (208,877)

Net change in fund balances $ (2,234,052) $ 4,089,522 $ (235,434) $ 1,620,036Fund balances - beginning, as restated 25,137,846 - 434,539 25,572,385Fund balances - ending $ 22,903,794 $ 4,089,522 $ 199,105 $ 27,192,421

The notes to the financial statements are an integral part of this statement.

Statement of Revenues, Expenditures, and Changes in Fund BalancesGovernmental FundsFor the Year Ended June 30, 2016

21

County of Rockbridge, Virginia Exhibit 6

Net change in fund balances - total governmental funds $ 1,620,036

(3,177,114)

The net effect of various miscellaneous transactions involving capital assets (i.e., sales, trade-ins, anddonations) is to increase (decrease) net position. (196,656)

565,113

2,377,178

(312,022)

Change in net position of governmental activities $ 876,535

The notes to the financial statements are an integral part of this statement.

Some expenses reported in the statement of activities do not require the use of current financial resources and,therefore are not reported as expenditures in governmental funds.

For the Year Ended June 30, 2016

Reconciliation of Statement of Revenues, Expenditures, and Changes in Fund Balances of Governmental Fundsto the Statement of Activities

Amounts reported for governmental activities in the statement of activities are different because:

Governmental funds report capital outlays as expenditures. However, in the statement of activities the cost ofthose assets is allocated over their estimated useful lives and reported as depreciation expense. This is theamount by which the capital outlays exceeded depreciation in the current period.

Revenues in the statement of activities that do not provide current financial resources are not reported asrevenues in the funds.

The issuance of long-term debt (e.g. bonds, leases) provides current financial resources to governmentalfunds, while the repayment of the principal of long-term debt consumes the current financial resources ofgovernmental funds. Neither transaction, however, has any effect on net position. Also, governmental fundsreport the effect of premiums, discounts, and similar items when debt is first issued, whereas these amountsare deferred and amortized in the statement of activities. This amount is the net effect of these differences inthe treatment of long-term debt and related items.

22

County of Rockbridge, Virginia Exhibit 7Statement of Net PositionProprietary Funds

Enterprise EnterpriseFund Fund

Landfill RecyclingFund Fund Total

ASSETSCurrent assets:

Cash and cash equivalents $ 1,614,827 $ - $ 1,614,827 Accounts receivable 67,360 - 67,360 Due from other funds 115,923 - 115,923

Total current assets $ 1,798,110 $ - $ 1,798,110 Noncurrent assets:

Restricted assets:Cash and cash equivalents $ 9,901,532 $ - $ 9,901,532 Total restricted assets $ 9,901,532 $ - $ 9,901,532

Capital assets, net of accumulated depreciation:Land $ 531,037 $ - $ 531,037 Buildings and improvements 1,391,744 123,983 1,515,727 Machinery and equipment 1,255,612 53,502 1,309,114 Construction in progress 920,478 - 920,478 Total capital assets $ 4,098,871 $ 177,485 $ 4,276,356 Total noncurrent assets $ 14,000,403 $ 177,485 $ 14,177,888Total assets $ 15,798,513 $ 177,485 $ 15,975,998

DEFERRED OUTFLOWS OF RESOURCESItems related to measurement of net pension liability $ 2,278 $ 1,278 $ 3,556 Pension contributions subsequent to measurement date 36,039 20,217 56,256

Total deferred outflows of resources $ 38,317 $ 21,495 $ 59,812

LIABILITIESCurrent liabilities:

Accounts payable $ 28,340 $ 5,488 $ 33,828 Initial advances from participating entities 74,292 - 74,292 Capital advances from Rockbridge County 957,773 - 957,773 Accrued interest payable 39,124 - 39,124 Bonds payable - current portion 65,334 - 65,334 Capital lease payable - current portion 273,231 - 273,231 Compensated absences-current portion 6,406 2,773 9,179

Total current liabilities $ 1,444,500 $ 8,261 $ 1,452,761Noncurrent liabilities:

Compensated absences - net of current portion $ 19,220 $ 8,317 $ 27,537 Net OPEB obligation 3,000 - 3,000 Net pension liability 193,094 108,322 301,416 Closure and post-closure liability 1,980,511 - 1,980,511 Bonds payable - net of current portion 7,199,376 - 7,199,376 Capital lease payable - net of current portion 643,359 - 643,359