Could US Shale Gas Revolution be Repeated in Europe – a ... · Could US Shale Gas Revolution be...

45

SEE Upstream Bucharest 3.04.2014 Could US Shale Gas Revolution be Repeated in Europe – a Case Study of Poland Paweł Poprawa The Energy Studies Institute, Warsaw

Transcript of Could US Shale Gas Revolution be Repeated in Europe – a ... · Could US Shale Gas Revolution be...

SEE Upstream Bucharest 3.04.2014

Could US Shale Gas Revolution be Repeated in Europe

– a Case Study of Poland

Paweł Poprawa The Energy Studies

Institute, Warsaw

shale gas in USA

shale gas in USA

decrease of gas price in US due to increasing

shale gas supply

since 2009 – split of prices of oil and gas

shale / tight oil in USA

• currently – 6,5 % of US oil production • projection for 2016-2020 – 15-20 %

shale gas impact on US economy

• recently shale gas stands for ~ 40 % US gas production, while shale oil stands for 6,5 % US oil production • cumulative annual shale gas / oil investments in US is in a range of ~100 bln USD/year • US limited gas import – export of LNG gas; US become the biggest gas producer in the World

• decrease of gas price in USA in 2008-2009 – big nominal profit for economy and individual consumers

• cheap gas in USA – attracts gas consuming industry; US chemical industry turning back to US

• investment of 1 mln USD/year creates 14 jobs (direct – 4, indirect – 4,5, induced – 5,5); 600+ thousand new jobs

can it be reproduced in Europe ?

North America – an shale gas/oil exploration analogue

North America vs Europe – geological setting

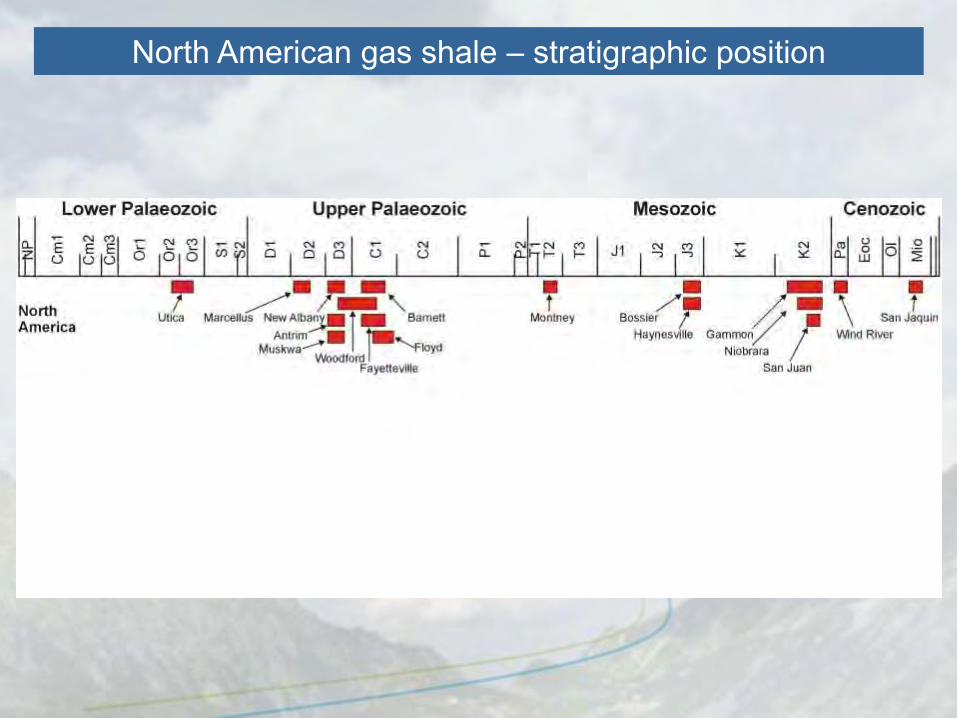

North American gas shale – stratigraphic position

North American & European gas shale – stratigraphic position

shale gas resources – Europe vs North America

(EIA 2013)

shale oil resources – Europe vs North America

(EIA 2013)

potential shale gas basins in Europe

shale gas in Europe – pro vs contra

• breaks the historical division into less developed, unreliable exporters vs developed consumers – different geographic distribution of resources

• challenges existing structure of gas supplies (e.g. Gasprom, Northstream, Southstream, North Africa, Norway)

• competition with other energy producers – nuclear power plants (France), renewable energy (Germany/EU), coal (Poland)

• local communities & green activist, in some countries also politicians, concerns about environment impact

• for countries with high coal & lignite position in energy mix – a realistic alternative allowing for reduction of CO2 emission

• countries dependent on monopolistic gas supplier desire alternative (Central & Eastern Europe)

challenges for shale gas exploration in Europe

• EU strategy, regulatory framework & political acceptance

• technology and know-how transfer from North America

• availability of drilling & seismic service (protected market)

• availability of qualified / certified stuff

• drilling and production cost

• property right structure

• environmental concerns

• geological challenges – differences to N. American basins

• scale of required financial resources

drilling rigs (June 2012) rigs required in Poland in positive scenario: 250-300

Source: Energy Economist

Source: Carl T. Montgomery and Michael B.

Smith, NSI Technologies

availability of drilling, frack & seismic service (protected market)

hydraul. fracturing equipment (December 2012) required frack teams in Poland in positive scenario: 30-50

shale gas & oil in Poland

concessions for shale gas exploration – early 2007

2007 prospective regions

concessions for shale gas exploration – late 2010

2010 2007

ConocoPhillips, Chevron, Nexen, Total, (ExxonMobil, ENI, Marathon, Talisman); Polish Oil & Gas Company, Orlen, Lotos, etc.

burial depth (m)

(after: Poprawa, 2010)

Depth to the bottom of the Llandovery Lower Silurian (m)

average recent burial depth – US vs Poland bu

rial d

epth

(m)

after: US Energy Information Administration, 2011

drilling cost per well – US vs Poland pr

oduc

tion

wel

l cos

t (M

M P

LN)

after: US Energy Information Administration, 2011

thermal maturity (% Ro)

(after: Poprawa, 2010)

Thermal maturity (% VRo) of the Lower Silurian

BALTIC BASIN lack of major tectonic deformations, some normal faulting of the Silurian –Precambrian, partly induced during flexure of the lower plate in front of the Caledonian orogen

grey colors: Carboniferous

brown colors: Devonian

blue colors: Silurian

(Krzywiec, 2010, in press)

Precambrian

Cambrian

Ordovician

Silurian

Zechstein

Triassic

Jurassic

LUBLIN BASIN (SE PART) system of thin- and thick-skinned reverse faults/thrusts developed during Late Carboniferous inversion

(Krzywiec, 2009)

grey colors: Carboniferous

brown colors: Devonian

blue colors: Silurian

Żarnowiec IG 1

TOC distribution in a section and the net pay thickness

Total Organic Carbon contents – US vs Poland

Montey shale – av. TOC ~1.5 %

contradicting recoverable shale gas resources assessments for Poland

contradicting recoverable shale oil resources assessments for Poland

successful play – data usually available in Europe

shale gas production costs

www.pgi.gov.pl

Państwowy Instytut Geologiczny Państwowy Instytut Badawczy

recent stage of shale gas exploration

19

80

19

85

19

90

19

95

20

00

20

05

20

10

Barnett

Marcellus

Woodford

Fayetteville

Haynesville

Eagle Ford

Exploration Development Mature

East European Craton

USA

POLAND

After: Halliburton (modified)

First concession in Poland First exploration well in Poland

Explor.

time from beginning of exploration to development and mature production: US vs Poland

shale gas exploration in Poland – majors

2014

shale gas exploration in Poland – independents

shale gas exploration in Poland – Polish national operators

slow exploration

Administrative procedures: • permit for drilling a well in Poland 9-12 months, in Pennsylvania

up to 45 days Regulatory regime & political support: • Poland – high political support is appreciated, but discussion on

new regulations created uncertainty for the investors • Poland – some of proposed new taxation models unrealistic • UE – lack of political support plus bureaucratic regime Difficult geological results of first exploration wells Currently it is more difficult for independents to gather money for drilling Companies internal issues (e.g. Talisman)

current stage of shale gas exploration in Poland

• shale gas: some 55 wells were drilled; including ~46 vertical ones; 9 lateral wells with multi-fracturing and well test • tight gas: 6 vertical wells 3 fractured • coming 2-3 years some ~100-150 fractured wells expected to be drilled (> 1.5 bln $)

experiences in Poland

21 exploration companies

- financial potential - human potential - technical experience - technology availability

Majors: Chevron, Total, Nexen, ConocoPhillips, (ExxonMobil, MarathonOil, Talisman, ENI)

Polish National Companies: PGNiG, Orlen Upstream, Lotos, Independents: 3Legs Resources, Petrolinvest S.A., Wisent Oil&Gas,

San Leon, Realm Energy, Cuadrilla, Dart Energy, BNK, Emfesz, Basgas

79 exploration companies

Abraxas Petroleum, Alta Mesa Holdings, Anadarko, Apache Copr., Aruba Petroleum, Aurora Resources, Austin Exploration, BHP Biliton, BP, Cabot Oil&Gas, Carrizo Oil&Gas, Chaparral Energy, Chesapeak Energy, Cinco Resources, Clayton

Williams Energy, Comstock Resources, Conoco Phillips, CNOOC, Crimson Exploration, Devon Energy, Eagle Ford Oil&Gas Corp., El Paso, Enduring

Resources, Enerjex Resources, EOG resources, Escondido Resources, Espada Operating, Exxon-XTO, Forest Oil, GAIL, GeoResources, Goodrich Petroleum,

Global Petroleum, Hess Corporation, Hilcorp, Hunt Oil, Jadela Oil, KNOC, Laredo Energy, Lewis Energy Group, Lonestar Resources, Lucas Energy, Magnum Hunter

Resources, Marathon Oil, Marubeni Corporation, Matador Resources, Mitsui, Murphy Oil, Newfield Exploration, Penn Virginia Corp, Peregrine Petroleum,

PetroHawk, PetroQuest, Pioneer Natural Resources, Plains Exploaration&Production, Redemption Oil&Gas, Reliance Industries, Riley

Exploration, Rock Oil Company, Rosetta Resources, San Isidro Development, Sanchez Energy, Sandstone Energy, Saxon Oil Company, Shell, SM Energy, Statoil,

Strand Energy, Strike Energy, Swift Energy, Talisman Energy, Texon Petroleum, Tidal Petrloeum, TXCO Resources, Unit Corporation, U.S. Energy Corp., Weber

Energy, WEJCO E&P, ZaZa Energy

experiences in Eagle Ford

social acceptance in Poland

Early dialog with local communities: • industry • government and local administration together with experts

Environment monitoring projects: • government – publicly available reports • academic institution – publicly available reports • cooperation with US and Canadian public administration • new wells demonstrate safe Support also related to: • HC tax in 60 % for local administration • political context – alternative to Russian gas

could „shale revolution” be repeated in Europe / Poland

alternative

Source: Der Spiegel, January 2009

• need to proof geological potential (numerous drillings; high costs)

• need to reduce production costs (mainly drilling and fracturing); roughly by half

• bureaucratic and regulatory barriers; EU regulations

• need to develop technical service (drilling, fracturing, waist utilization)

• need to free gas market in Poland

• adjust fiscal regime • requires political acceptance • requires social acceptance • need to proof that technology is

safe for environment

first shale gas drilling pad in Poland (2010, Łebień LE-1 well)

thank you