Cost of Service Study Report - Modesto Irrigation District

94

Cost of Service Study Report November 19, 2018 DRAFT

Transcript of Cost of Service Study Report - Modesto Irrigation District

Cost of Service Study Report November 19, 2018

DRAFT

TABLE OF CONTENTS

EXECUTIVE SUMMARY ............................................................................................................. 1

A. Background .......................................................................................................................... 1 B. Cost of Service and Rate Design Process Overview ........................................................... 2 C. Revenue Requirements ........................................................................................................ 4 D. Cost of Service Results Compared to Current Revenue by Customer Class ....................... 4

I. INTRODUCTION ................................................................................................................... 1 A. Background .......................................................................................................................... 1

1. Generation and Power Supply ......................................................................................... 2 2. Transmission and Distribution ......................................................................................... 4

B. Cost of Service and Rate Design Process Overview ........................................................... 4 II. REVENUE REQUIREMENTS ............................................................................................... 6

A. Projected Energy Requirements .......................................................................................... 7 B. Operations and Maintenance Expenses ............................................................................... 7

1. Power Production ............................................................................................................ 8 2. Transmission .................................................................................................................. 10 3. Distribution .................................................................................................................... 11 4. Customer Accounts ........................................................................................................ 12 5. Administrative & General ............................................................................................. 12

C. Debt Service ...................................................................................................................... 13 D. Non-Rate Revenue ............................................................................................................. 13 E. Total Revenue Requirements ............................................................................................. 14

III. RATE REVENUE ............................................................................................................. 14 IV. COST OF SERVICE RESULTS ....................................................................................... 15

A. Functionalization of Revenue Requirement ...................................................................... 15 1. Production Function ...................................................................................................... 16 2. Transmission Function .................................................................................................. 16 3. Distribution Function ..................................................................................................... 16 4. Customer Service Function ........................................................................................... 16

B. Classification of Revenue Requirement ............................................................................ 17 V. ALLOCATION OF REVENUE REQUIREMENT .............................................................. 18

A. Class Allocation Factors .................................................................................................... 18 1. Demand Allocations ...................................................................................................... 18 2. Energy Allocations ........................................................................................................ 19

DRAFT

November 19, 2018 MRW & Associates, LLC ii

3. Customer Allocations .................................................................................................... 20 4. Direct Assignment Allocations ...................................................................................... 21

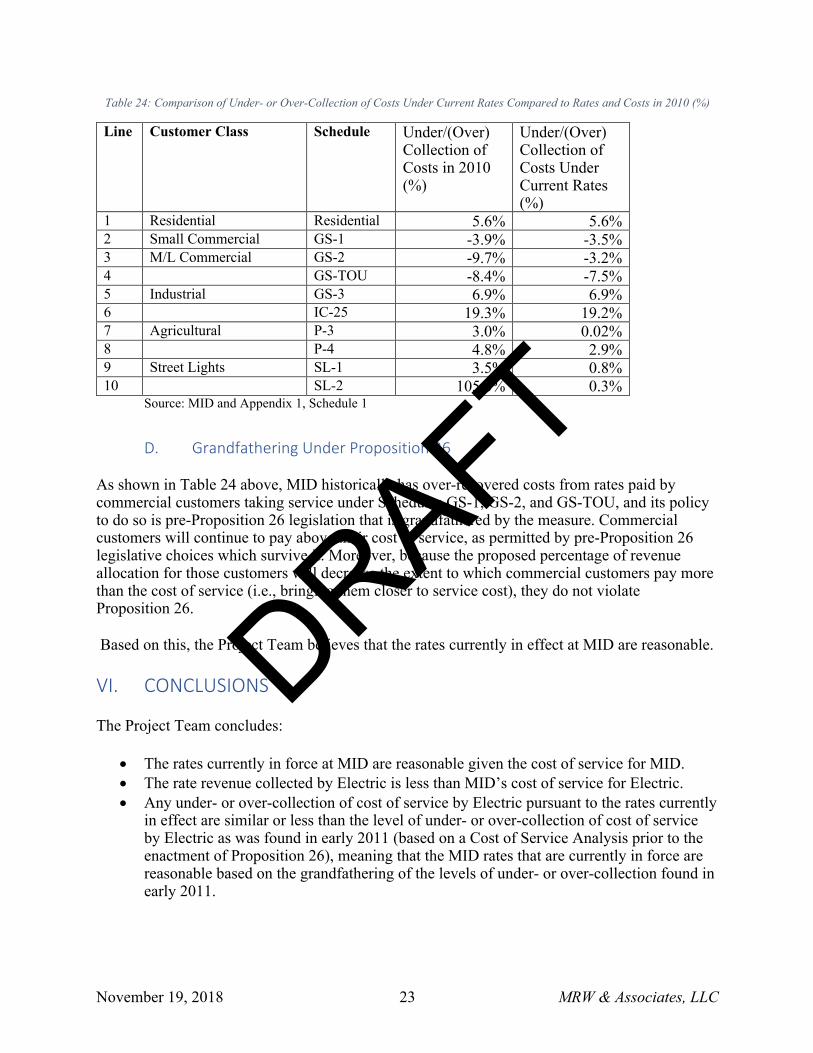

B. Cost of Service Results ...................................................................................................... 21 C. Cost of Service Results Compared to Current Revenue .................................................... 22 D. Grandfathering Under Proposition 26 ............................................................................... 23

VI. CONCLUSIONS ............................................................................................................... 23

LIST OF TABLES

Table 1: MID Revenue Requirements for Electric Compared to Rate Revenues ($) ...................... 4 Table 2: Cost of Service Compared to Rate Revenue by Customer Class ($) ................................ 5 Table 3: Comparison of Under- or Over-Collection of Costs Under Current Rates Compared to Rates and Costs in 2010 (%) ............................................................................................................ 6 Table 4: MID's Power Supply Resources as of December 31, 2017 ............................................... 3 Table 5: Electric's Transmission and Distribution Facilities ........................................................... 4 Table 6: Estimated Energy Requirements for MID ......................................................................... 7 Table 7: Total O&M for Electric Department for Test Year ($) ..................................................... 8 Table 8: O&M Expenses for Power Production ($) ........................................................................ 9 Table 9: MID's Purchased Power Costs ........................................................................................ 10 Table 10: Transmission O&M Expenditures ($) ........................................................................... 11 Table 11: Distribution O&M Expenses ($) ................................................................................... 12 Table 12: Customer Accounts O&M Expenditures ($) ................................................................. 12 Table 13: Administrative & General Expenditures ($) ................................................................. 13 Table 14: MID's Non-Rate Revenue for Electric ($) ..................................................................... 14 Table 15: MID’s Revenue Requirements for Electric ................................................................... 14 Table 16: Rate Revenue by Customer Class ($) ............................................................................ 15 Table 17: Functionalized Test Year Revenue Requirements ($) ................................................... 16 Table 18: Classification of MID's Electric Costs .......................................................................... 18 Table 19: Demand Allocation Factors ........................................................................................... 19 Table 20: Energy Allocation Factors ............................................................................................. 20 Table 21: Number of Customers by Schedule ............................................................................... 21 Table 22: Unbundled Revenue Requirements by Class ($) ........................................................... 21 Table 23: Cost of Service Compared to Rates ($) ......................................................................... 22 Table 24: Comparison of Under- or Over-Collection of Costs Under Current Rates Compared to Rates and Costs in 2010 (%) .......................................................................................................... 23

LIST OF FIGURES

Figure 1: Typical Cost of Service Process ....................................................................................... 3 Figure 2: Typical Cost of Service Process ....................................................................................... 6

DRAFT

November 19, 2018 MRW & Associates, LLC ES-1

EXECUTIVE SUMMARY

In December 2017, Bartle Wells Associates (Bartle Wells) was retained by the Modesto Irrigation District (MID) to perform an Electric Cost of Service (COS) and Revenue Allocation Study (Study) as part of a broader study of the cost of service for all of MID’s lines of business. Bartle Wells retained MRW & Associates, LLC (MRW) to assist with the Study. This report describes the analysis performed for the Electric line of service (Electric) and makes projections of the cost of service relative to the rate revenue recovered under current rates from the customers of Electric.1

The report consists of six sections. Following this Executive Summary, Section 1 provides the introduction for the Study. Section 2 discusses the development of the revenue requirement for the Test Year.2 Section 3 presents the rate revenue by customer class under present rates. Sections 4 and 5 discuss the estimated revenue requirement at various levels of aggregation (e.g., Electric, function, customer class). Section 6 presents conclusions.

A. Background

MID is a California irrigation district organized in 1887 under the provisions of the Irrigation District Law. MID has the powers under the Irrigation District Law to, among other things, provide irrigation and electric service. Under Irrigation District Law, MID has the powers of eminent domain, to contract, to construct works, to fix rates and charges for commodities or services furnished, to lease its properties and to incur indebtedness.

MID is governed by a Board of Directors, the five members of which are elected from separate electoral divisions within its irrigation district boundaries for staggered four year terms. MID’s operations are carried out under the direction of the General Manager who is in charge of MID’s operations in accordance with the Board of Director’s directives and policies.

MID is located in the San Joaquin Valley in Central California, approximately 90 miles east of San Francisco, California. MID began providing electric service in 1923, and since 1940 has provided all electric service within its original 160 square mile service area, which includes the major portion of Stanislaus County. Beginning in 1996, MID has also provided electric service on a competitive basis in portions of the service area of Pacific Gas & Electric Company (PG&E). California Assembly Bill 2638 (AB 2638), effective on January 1, 2001, added the 7.5 square mile Mountain House Community Services District in western San Joaquin County to MID’s exclusive electric service area and also designated a 400 square mile area in Southern San Joaquin County, Northern Stanislaus County and western Tuolumne County as MID’s non-exclusive electric service area. Pursuant to AB 2638, other than as set forth therein, MID is further prohibited from providing electric transmission or distribution service to retail customers in the service territory of PG&E. For the year ended December 31, 2017, MID served over

1 MID’s Fiscal Year (FY) runs from January 1 through December 31. All data contained in this report represents the MID FY unless otherwise stated. 2 The Test Year for the Study is 2018.

DRAFT

November 19, 2018 MRW & Associates, LLC ES-2

122,734 customers, had total retail sales of approximately 2.562 billion kWh and a peak demand of 697 MW.

To provide electric service within its service area, MID owns and operates an electric system that includes generation, transmission and distribution facilities. MID also purchases and sells power and transmission service and participates in pooling and other utility arrangements.

MID also supplies water for irrigation use in a portion of Stanislaus County and owns and operates a water treatment plant which supplies treated domestic water on a wholesale basis to the City of Modesto. MID’s irrigation system, as well as revenues from the sale of treated water, is operated and accounted for separately from Electric. Electric has no claim on the revenues of the irrigation or treated water systems.

MID’s last Electric Utility Rate Study was prepared in 2014. The MID Board approved a restructuring of electric rates in 2016 based in part on that study.

B. Cost of Service and Rate Design Process Overview

The COS and rate design process includes five steps as follows:

1. Determination of the Revenue Requirement – This first step examines the utility’s financial needs and determines the amount of revenue that must be generated from rates or non-rate revenue sources. The revenue requirement is determined on a “cash basis.” A “cash basis” analysis examines the cash obligations of the utility such as operations and maintenance (O&M) expenses, the Electric Utility’s allocated portion of MID’s administrative and general (A&G) expenses, debt service, and cash funded capital projects, and transfers to or from MID’s reserves.3

Discretionary Revenue is assigned at the discretion of the MID Board. Any Discretionary Revenue assigned to a customer class would have the effect of reducing that class’s revenue requirement and, as a result, that class’s Cost of Service.

In preparing our analysis of the electric revenues from present rates and the development of the revenue requirement, the Project Team relied upon MID’s historical audited data, the 2018 Budget, records of operation, customer billing data, and other detailed information and data compiled and provided by the MID’s management and staff.

2. Functionalization and Sub-functionalization of Costs – The revenue requirement is then assigned to the particular function or sub-function of the utility. Electric utilities like Electric typically have power supply, transmission, distribution, and customer services functions. Power Supply sub-functions may include utility-owned generation or short- and long-term purchased power from contracts or the wholesale power market. In MID’s case, Electric incurs costs related to hydroelectric generation that is controlled by Irrigation, resulting in an inter-departmental transfer from Electric to Irrigation. Transmission and Distribution sub-functions may include distribution infrastructure by voltage, metering, billing, collection, etc. In MID’s case, Electric uses right-of-way

3 At the present time, MID has a single set of reserves that are used for both Electric and Irrigation.

DRAFT

November 19, 2018 MRW & Associates, LLC ES-3

associated with Irrigation’s canals for siting some of its transmission and distribution facilities, resulting in an inter-departmental transfer from Electric to Irrigation. Customer sub-functions include billing and collections, customer service, meter reading, etc.

3. Classification of Costs – Once costs are functionalized, costs are then classified based on the underlying nature of the costs. Of particular importance is the determination of fixed versus variable costs. Fixed costs remain a financial obligation of the utility regardless of the amount of energy produced whereas variable costs fluctuate based on system energy requirements. Also, fixed and variable costs are associated with utility requirements to meet customer demand, energy, and customer service needs.

4. Allocation of Costs – Once costs are classified, costs are then allocated to the various customer classes. Allocation factors align with cost classification. So, demand-related costs are allocated on measures of class demand such as class contribution to the system coincident peak (CP). Energy allocation factors are based on energy consumed by customers. Customer allocation factors are based on various allocators, such as the number of customers.

These first four steps in the COS process are depicted in the figure below.

Figure 1: Typical Cost of Service Process

5. Rate Design – The fifth, and final, step is rate design, which translates COS results into rates for each customer class. The rate design establishes tariffs for each group of customers in order to fully recover all revenue requirements allocated to each customer group. Tariffs may include per-customer charges, demand charges, energy charges, or other charges. For this report, the Project Team did not propose revisions to MID’s rate design.

DRAFT

November 19, 2018 MRW & Associates, LLC ES-4

C. Revenue Requirements

The Project Team developed the Test Year Revenue Requirement for Electric based on the 2018 Budget with adjustments for unusual or one-time expenses or revenues. For this analysis, the Project Team used MID’s COSA model after carefully reviewing the structure and assumptions in the model. The Project Team discussed any adjustments to expenses, revenues, model structure or assumptions with MID staff.

After developing the costs of service for MID, the Project Team compared the expected rate revenue at present rates and non-rate revenues for the Test Year against the cost of service in the Test Year. MID staff provided rate revenue for the Test Year.

Based on the costs and revenues for the Test Year, the Project Team compared costs and revenues to determine any under- or over-recovery of costs based on present rates.

Table 1: MID Revenue Requirements for Electric Compared to Rate Revenues ($)

Line Category Amount 1 O&M 290,106,182 2 Capital Expenses(1) 6,465,234 3 Debt Service & Debt Service Coverage(2) 94,613,189 4 Subtotal 391,184,604 5 Less Non-Rate Revenue -11,743,023 7 Less Discretionary Revenue -9,030,000 8 Revenue Requirement 370,411,582 9 Test Year Projected Rate Revenues 356,802,380 10 Over (Under) Recovery of Costs (13,609,202) 11 Over (Under) Recovery of Costs (3.8%)

Please note the total amounts shown in the table may not sum due to rounding. Also note that this table does not include any transfers either to or from MID reserves.

Notes:

(1) Capital Expenses represent certain capital expenditures that are assumed to be paid out of current revenues. Other capital expenditures are assumed to be financed and are reflected in the Debt Service and Debt Service Coverage line item.

(2) Debt Service & Debt Service Coverage reflect the annual total principal and interest paid on existing and new debt as well as an allowance for debt service coverage.

As is seen from this table, MID’s current rates under-recover MID’s costs for Electric by $13,609,202 or 3.8%. Note that this table does not include any transfers either to or from MID reserves.

D. Cost of Service Results Compared to Current Revenue by Customer Class

The Project Team developed customer class-specific estimates of cost of service for the Test Year. To do this, the Project Team functionalized the revenue requirement into four functions (i.e., Production, Transmission, Distribution, and Customer Service), classified costs into three categories (i.e., Energy, Demand, and Customer), and then allocated those costs to each of

DRAFT

November 19, 2018 MRW & Associates, LLC ES-5

MID’s customer classes.4 These customer class-specific costs were then compared to rate revenue for each class. The following table presents these results.

Table 2: Cost of Service Compared to Rate Revenue by Customer Class ($)

Line Customer Class

Schedule Cost of Service

[a]

Test Year Rate

Revenues [b]

Difference ($)

[c] = [a]-[b]

Difference (%)

[d]=[c]/[b]

1 Residential Residential 164,434,962 155,733,609 8,701,353 5.6% 2 Small

Commercial GS-1 22,164,937 22,958,570 (793,634) -3.5%

3 M/L Commercial

GS-2 73,878,168 76,301,128 (2,422,960) -3.2%

4 GS-TOU 4,501,940 4,867,789 (365,850) -7.5% 5 Industrial GS-3 60,917,991 56,993,098 3,924,893 6.9% 6 IC-25 27,875,594 23,387,304 4,488,289 19.2% 7 Agricultural P-3 12,448,157 12,445,627 2,530 0.02% 8 P-4 2,194,078 2,131,909 62,169 2.9% 9 Street Lights SL-1 1,292,278 1,281,709 10,569 0.8% 10 SL-2 703,478 701,636 1,842 0.3% 11 Total 370,411,582 356,802,380 13,609,202 3.8%

Table 2 shows that all customer classes except for tariffs serving Small and Medium/Large Commercial customers are paying less than their costs of service (i.e., Test Year rate revenues are less than Cost of Service).

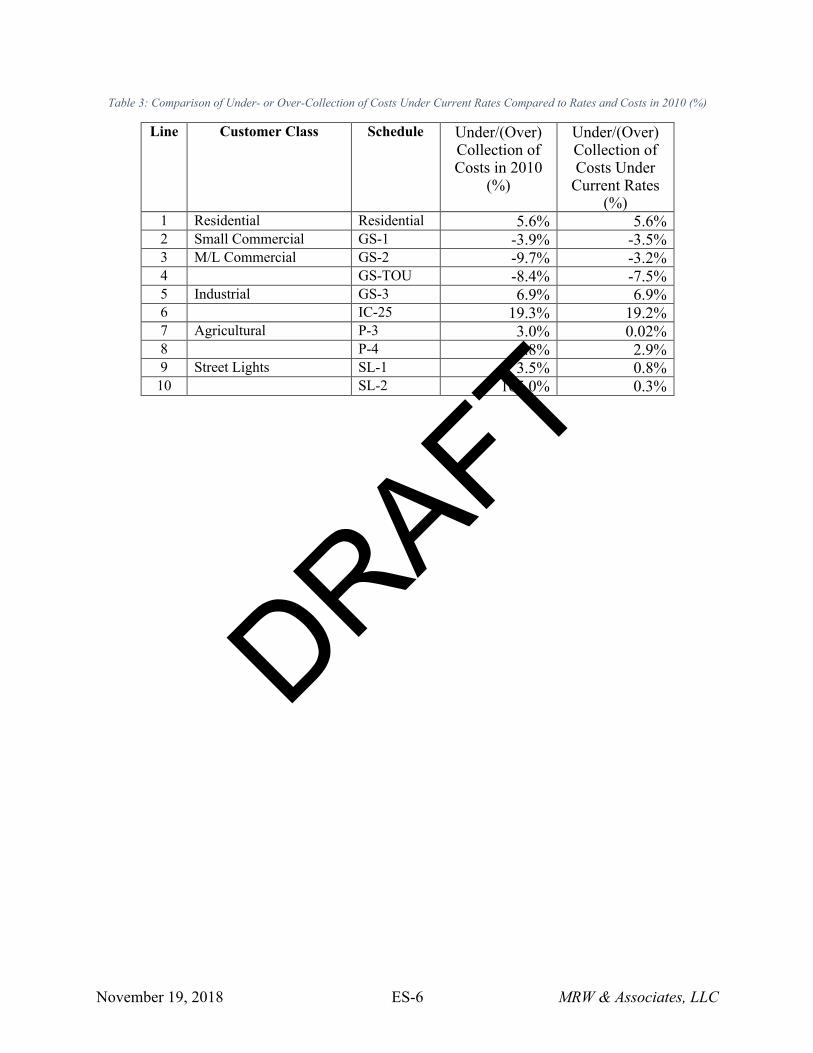

The levels of under- or over-collection for each customer class on a percentage basis are, on an absolute value basis, less than was found in late 2010, meaning that the current MID rates are “closer” to cost of service than what was found in 2010. The following table presents the level of under- or over-collection in late 2010 and under MID’s current rates.

As shown in Table 3 below, MID historically has over-recovered costs from rates paid by commercial customers taking service under Schedules GS-1, GS-2, and GS-TOU, and its policy to do so is pre-Proposition 26 legislation that is grandfathered by the measure. Commercial customers will continue to pay above their cost of service, as permitted by pre-Proposition 26 legislative choices which survive it. Moreover, because the proposed percentage of revenue allocation for those customers will decrease the extent to which commercial customers pay more than the cost of service (i.e., bringing them closer to service cost), they do not violate Proposition 26.

Based on this, the Project Team believes that the rates currently in effect at MID are reasonable.

4 For this study, “customer class” is the same as rate schedule.

DRAFT

November 19, 2018 MRW & Associates, LLC ES-6

Table 3: Comparison of Under- or Over-Collection of Costs Under Current Rates Compared to Rates and Costs in 2010 (%)

Line Customer Class Schedule Under/(Over) Collection of Costs in 2010

(%)

Under/(Over) Collection of Costs Under

Current Rates (%)

1 Residential Residential 5.6% 5.6% 2 Small Commercial GS-1 -3.9% -3.5% 3 M/L Commercial GS-2 -9.7% -3.2% 4 GS-TOU -8.4% -7.5% 5 Industrial GS-3 6.9% 6.9% 6 IC-25 19.3% 19.2% 7 Agricultural P-3 3.0% 0.02% 8 P-4 4.8% 2.9% 9 Street Lights SL-1 3.5% 0.8% 10 SL-2 105.0% 0.3%

DRAFT

November 19, 2018 MRW & Associates, LLC 1

I. INTRODUCTION

In December 2017, Bartle Wells Associates (Bartle Wells) was retained by the Modesto Irrigation District (MID) to perform an Electric Cost of Service (COS) and Revenue Allocation Study (Study) as part of a broader study of the cost of service for all of MID’s lines of business. Bartle Wells retained MRW & Associates, LLC (MRW) to assist with the Study.

This report describes the analysis performed for the Electric line of service (Electric) and makes projections of the cost of service relative to the rate revenue recovered under current rates from the customers of Electric.5 The report consists of six sections and an Executive Summary. Following the Executive Summary, this section provides the introduction for the Study. Section 2 discusses the development of the revenue requirement for the Test Year.6 Section 3 presents the rate revenue by customer class under present rates. Sections 4 and 5 discuss the estimated revenue requirement at various levels of aggregation (e.g., Electric, function, customer class). Section 6 presents conclusions. Appendices are attached containing schedules and other information supporting the information contained in this report.

Regular reviews of the performance of a utility’s rates are an integral part of the management of any utility and failure to monitor the rates can result in the need for significant rate actions. The Project Team recommends that, going forward, MID continue to regularly monitor and review the performance of its adopted rates and perform rate adjustments in a timely manner to preserve the financial integrity of the Electric Utility.

The analysis performed by the Project Team was designed to consider the foreseeable, known, and measurable adjustments during the Study Period. The goal was to provide MID management with information related to the degree to which costs at different levels of aggregation are being fully recovered by current rates. As with any forecast, assumptions were made and MID should note that the actual expenses and revenues may differ from the projected expenses and revenues outlined in this report due to unforeseen changes such as system growth, inflation, etc.

A. Background

MID is a California irrigation district organized in 1887 under the provisions of the Irrigation District Law. MID has the powers under the Irrigation District Law to, among other things, provide irrigation and electric service. Under Irrigation District Law, MID has the powers of eminent domain, to contract, to construct works, to fix rates and charges for commodities or services furnished, to lease its properties and to incur indebtedness.

MID is governed by a Board of Directors, the five members of which are elected from separate electoral divisions within its irrigation district boundaries for staggered four year terms. MID’s operations are carried out under the direction of the General Manager who is in charge of MID’s operations in accordance with the Board of Director’s directives and policies.

5 MID’s Fiscal Year (FY) runs from January 1 through December 31. All data contained in this report represents the MID FY unless otherwise stated. 6 The Test Year for the Study is 2018.

DRAFT

November 19, 2018 MRW & Associates, LLC 2

MID is located in the San Joaquin Valley in Central California, approximately 90 miles east of San Francisco, California. MID began providing electric service in 1923, and since 1940 has provided all electric service within its original 160 square mile service area, which includes the major portion of Stanislaus County. Beginning in 1996, MID has also provided electric service on a competitive basis in portions of the service area of Pacific Gas & Electric Company (PG&E). California Assembly Bill 2638 (AB 2638), effective on January 1, 2001, added the 7.5 square mile Mountain House Community Services District in western San Joaquin County to MID’s exclusive electric service area and also designated a 400 square mile area in Southern San Joaquin County, Northern Stanislaus County and western Tuolumne County as MID’s non-exclusive electric service area. Pursuant to AB 2638, other than as set forth therein, MID is further prohibited from providing electric transmission or distribution service to retail customers in the service territory of PG&E. For the year ended December 31, 2017, MID served over 122,734 customers, had total retail sales of approximately 2.562 billion kWh and a peak demand of 697 MW.

To provide electric service within its service area, MID owns and operates an electric system that includes generation, transmission and distribution facilities. MID also purchases and sells power and transmission service and participates in pooling and other utility arrangements.

MID also supplies water for irrigation use in a portion of Stanislaus County and owns and operates a water treatment plant which supplies treated domestic water on a wholesale basis to the City of Modesto. MID’s irrigation system, as well as revenues from the sale of treated water, is operated and accounted for separately from Electric. Electric has no claim on the revenues of the irrigation or treated water systems.

MID’s last Electric Utility Rate Study was prepared in 2014. The MID Board approved a restructuring of electric rates in 2016 based in part on that study.

1. Generation and Power Supply

Electric provides power to its customers through a combination of MID-owned generation, purchase power contracts, and market purchases. The following table summarizes all of MID’s power supply resources as of the end of 2017.

DRAFT

November 19, 2018 MRW & Associates, LLC 3

Table 4: MID's Power Supply Resources as of December 31, 2017

Historical - Year Ending

December 31, 2017

Source Capacity

Available (MW) Actual Energy

(GWh) Percent of

Total Energy Generating Facilities:

Don Pedro/Stone Drop (Hydro) ................................... 62.3 277.5 10.7% Woodland 1 (Combustion Turbine) .............................. 49.0 152.9 5.9 Woodland 2 (Combustion and Steam Turbines) .......... 83.0 200.4 7.7 Woodland 3 (Reciprocating Engine) ........................... 49.0 65.3 2.5 Ripon Generation Station ............................................. 96.0 89.3 3.4 McClure (Combustion Turbine, 2 units) ...................... 122.0 4.7 0.2

Total(1) ......................................................................... 461.3 790.1 30.3% Purchased Power:

M-S-R PPA San Juan(2) ................................................ 75.0 502.2 19.3% Lodi Energy Center(3) ................................................... 30.0 77.8 3.0 Renewables ...................................................................

Wind(4) ..................................................................... 206.2 427.6 16.4 New Hogan(5) .......................................................... 2.1 11.9 0.5 Methane Digester .................................................... 0.8 0.9 0.0 McHenry Solar Project ........................................... 25.0 62.4 2.4

City and County of San Francisco (Hetch Hetchy)(6) ...................................................... 25.0 106.9 4.1

Western Area Power Administration (WAPA)(6) ......... 6.0 37.2 1.4 Other Purchases(7) ......................................................... 206.5 588.0 22.6 Total(1) ......................................................................... 576.6 1,814.8 69.7%

Total Energy Resources (Generation + Load Reduction + Purchases)(9) ...................................... 1,037.9 2,605.0 100.00% Load: District System Requirement for Retail ............................ 696.5 2,583.3 99.2% Wholesale Power Sales:(8)

Other Sales .................................................................. 0.0 21.7 0.8% Total Capacity and Energy Sold at Wholesale ........ 0.0 21.7 0.8%

Total (Retail + Wholesale)(1)(9) .......................................... 1,037.9 2,605.0 100.0% ____________________________ (1) Totals may not add due to rounding. (2) M-S-R PPA ceased to have an ownership interest in the San Juan Unit No. 4 effective December 31, 2017. (3) MID’s share of the output of the Lodi Energy Center is sold into the CAISO energy markets. Replacement energy is purchased

for delivery to MID as needed. (4) Capacity shown is total contract capacity. Represents energy sold to MID at the project bus from the High Winds Project (50

MW), located in Solano County, California, and the Big Horn Project (25 MW) located in Klickitat County, Washington and also includes delivery of the output of the 98.7 MW from the Star Point Wind Project, located in Sherman County, Oregon and 32.5 MW of the Big Horn II Project. Actual capacity delivery at the project will be less than the total contract capacity.

(5) Delivery of output for MID’s benefit from the New Hogan Project commenced on June 1, 2010 and is scheduled similarly to the wind projects that are located within the CAISO. Although the plant has two generators with 3.0 MW of capacity, only 2.1 MW is shown because both units cannot operate at the same time (2.1 MW is the capacity of the larger unit).

(6) WAPA and Hetch Hetchy Class 1 capacity are daily firm only. (7) Other Purchases include firm and non-firm short-term resources from various sources such as SMUD, BPA, PowerEx, and

CAISO, among others. Also include reserves consistent with prudent utility practices. Direct load control (10 MW) and interruptible retail contracts (16.4 MW) count towards planning reserves.

(8) Wholesale sales from the MID system are made on a short-term basis. This does not include sales made from Lodi Energy Center, San Juan, High Winds, Shiloh or New Hogan as output from those resources is sold directly to the CAISO energy markets.

(9) Total capacity available includes planning reserves to meet MID load. It is important to note that not all contracts are available year-round. Source: MID

DRAFT

November 19, 2018 MRW & Associates, LLC 4

MID must comply with California’s Renewable Portfolio Standard (RPS) for load-serving entities. As of the beginning of September 2018, MID is required to serve 50% of its load using qualifying renewable resources by 2030.

2. Transmission and Distribution

The following table summarizes the extent of Electric’s transmission and distribution facilities.

Table 5: Electric's Transmission and Distribution Facilities

Distribution Voltage (kV) Underground Overhead Total 4 kV 0.26 0.04 0.30 6.9 kV 436.96 - 436.96 12 kV 228.78 984.54 1,213.32 17 kV 65.81 29.94 95.75 21 kV 27.44 1.83 29.27 Total Distribution 759.25 1,016.35 1,775.60 Transmission Voltage (kV) Underground Overhead Total 69 kV - 203.90 203.90 115 kV - 37.60 37.60 230 kV - 142.50 142.50 Total Transmission - 384.00 384.00

Source: MID

Electric’s transmission system consists of approximately 384 miles of facilities that are 69 kilovolts (kVs) or above. Electric’s distribution system has both overhead and underground facilities totaling 1,775.60 miles.

At the present time, MID’s electric operations are a part of the overall operations of MID (i.e., the operations are not a separate business unit).7

B. Cost of Service and Rate Design Process Overview

The COS and rate design process includes five steps as follows:

1. Determination of the Revenue Requirement – This first step examines the utility’s financial needs and determines the amount of revenue that must be generated from rates or non-rate revenue sources. The revenue requirement is determined on a “cash basis.” A “cash basis” analysis examines the cash obligations of the utility such as operations and maintenance (O&M) expenses, the Electric Utility’s allocated portion of MID’s administrative and general (A&G) expenses, debt service, and cash funded capital projects, and transfers to or from MID’s reserves.8

7 For simplicity, this report will refer to MID’s electric operations as “Electric” even though it is not a separate business unit. 8 At the present time, MID has a single set of reserves that are used for both Electric and Irrigation.

DRAFT

November 19, 2018 MRW & Associates, LLC 5

Discretionary Revenue is assigned at the discretion of the MID Board. Any Discretionary Revenue assigned to a customer class would have the effect of reducing that class’s revenue requirement and, as a result, that class’s Cost of Service.9

In preparing our analysis of the electric revenues from present rates and the development of the revenue requirement, the Project Team relied upon MID’s historical audited data, the 2018 Budget, records of operation, customer billing data, and other detailed information and data compiled and provided by the MID’s management and staff.

2. Functionalization and Sub-functionalization of Costs – The revenue requirement is then assigned to the particular function or sub-function of the utility. Electric utilities like Electric typically have power supply, transmission, distribution, and customer services functions. Power Supply sub-functions may include utility-owned generation or short- and long-term purchased power from contracts or the wholesale power market. In MID’s case, Electric incurs costs related to hydroelectric generation that is controlled by Irrigation, resulting in an inter-departmental transfer from Electric to Irrigation. Transmission and Distribution sub-functions may include distribution infrastructure by voltage, metering, billing, collection, etc. In MID’s case, Electric uses right-of-way associated with Irrigation’s canals for siting some of its transmission and distribution facilities, resulting in an inter-departmental transfer from Electric to Irrigation. Customer sub-functions include billing and collections, customer service, meter reading, etc.

3. Classification of Costs – Once costs are functionalized, costs are then classified based on the underlying nature of the costs. Of particular importance is the determination of fixed versus variable costs. Fixed costs remain a financial obligation of the utility regardless of the amount of energy produced whereas variable costs fluctuate based on system energy requirements. Also, fixed and variable costs are associated with utility requirements to meet customer demand, energy, and customer service needs.

4. Allocation of Costs – Once costs are classified, costs are then allocated to the various customer classes. Allocation factors align with cost classification. So, demand-related costs are allocated on measures of class demand such as class contribution to the system coincident peak (CP). Energy allocation factors are based on energy consumed by customers. Customer allocation factors are based on various allocators, such as the number of customers.

These first four steps in the COS process are depicted in the figure below.

9 See Appendix 2 for more details about Discretionary Revenues.

DRAFT

November 19, 2018 MRW & Associates, LLC 6

Figure 2: Typical Cost of Service Process

5. Rate Design – The fifth, and final, step is rate design, which translates COS results into rates for each customer class. The rate design establishes tariffs for each group of customers in order to fully recover all revenue requirement allocated to each customer group. Tariffs may include per-customer charges, demand charges, energy charges, or other charges. For this report, the Project Team did not propose revisions to MID’s rate design.

II. REVENUE REQUIREMENTS

Developing the Test Year Revenue Requirement is the first step in the COS and rate design process, as shown in Figure 2. The Test Year Revenue Requirement for Electric was based on the 2018 Budget with adjustments for unusual or one-time expenses or revenues.

There are two primary revenue requirement methodologies employed in the utility industry; the cash basis and the utility basis. The primary differences between the cash basis and the utility basis involve the treatment of depreciation, return on invested capital, and debt service. The cash basis, which is the most common method used by municipalities and irrigation districts, includes debt service, but excludes depreciation and return on invested capital in the revenue requirement determination. The cash basis focuses on meeting the cash demands of the utility. The utility basis, which is most commonly used by private or for-profit utilities, includes depreciation and return on invested capital, but excludes debt service from the revenue requirement determination.

In this COS analysis, the Project Team utilized the cash basis, as it follows the traditional cash-oriented budgeting practices frequently used by government entities. In addition, the cash basis generally is easier to explain to customers since the cash basis attempts to match revenue and expenditures.

DRAFT

November 19, 2018 MRW & Associates, LLC 7

A. Projected Energy Requirements

The electric consumption by Electric’s customers is a key driver in projections of expenses and revenues. The forecast of sales and electric load associated with customer demands was developed by MID. The following table presents assumed electric sales for the Test Year by customer class.10

Table 6: Estimated Energy Requirements for MID

Res. GS-1 GS-2 GS-TOU

GS-3 IC-25 P-3 P-4 SL-1 SL-2 Total

(MWh) Sales 868,272 140,003 5,501 31,965 281,783 287,442 85,619 20,805 9,548 2,419 2,514,597 Losses 34,636 5,523 98 571 5,215 5,128 3,608 93 1,150 94 87,199 Total 902,908 145,526 5,599 32,536 286,998 292,570 89,227 20,898 10,698 2,513 2,601,796 (MW) Peak 359 39 111 4.5 97 36 16 2.00 0 0 664 Losses 18 2 6 0.1 3 1 1 0.01 0 0 31 Total 377 41 117 4.6 100 37 17 2.01 0 0 695

Source: MID. Note: Totals may not add due to rounding.

Total sales for the Test Year are 2,514,597 MWh. Energy supplied (which includes losses) is 2,601,796 MWh in the Test Year. Peak demand at the customer level is 664 MW in the Test Year.

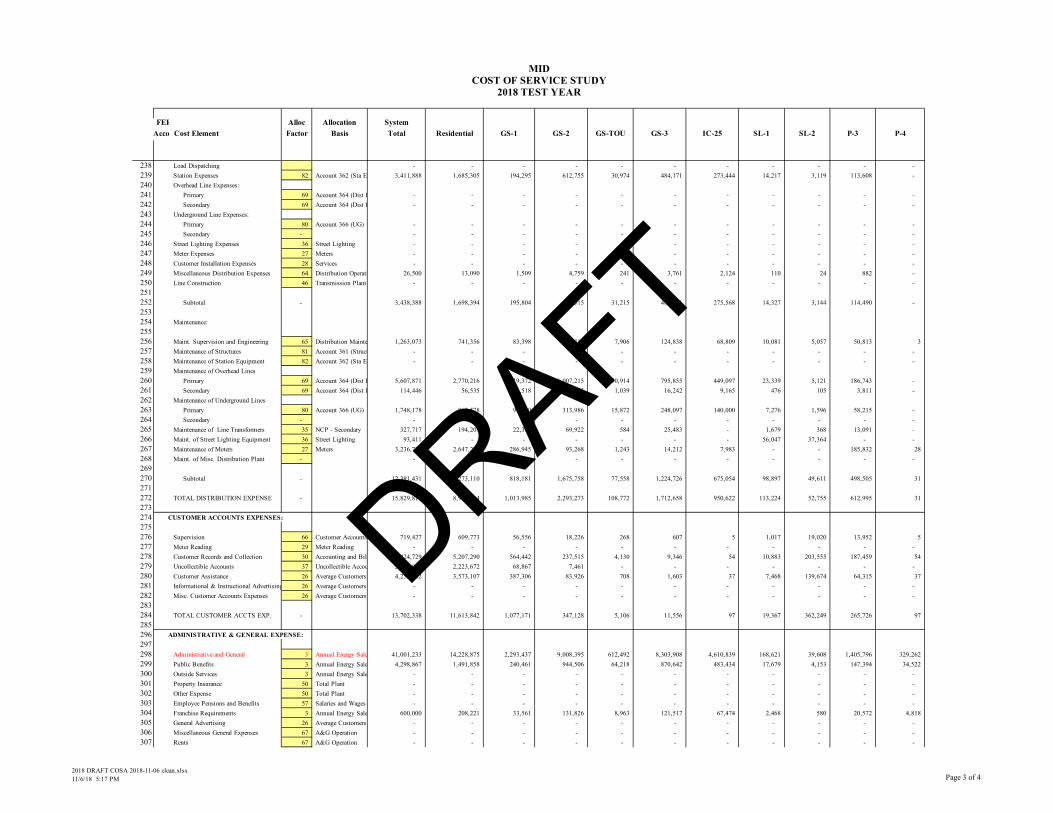

B. Operations and Maintenance Expenses

The first step in developing the revenue requirement forecast for the Test Year was the development of Test Year O&M expenses. O&M expenses for the Test Year are based on MID’s 2018 budget with adjustments as necessary.

O&M expenses consist of costs from five broad categories:

• Power Production • Transmission • Distribution • Customer Accounts • Administrative and General (A&G)

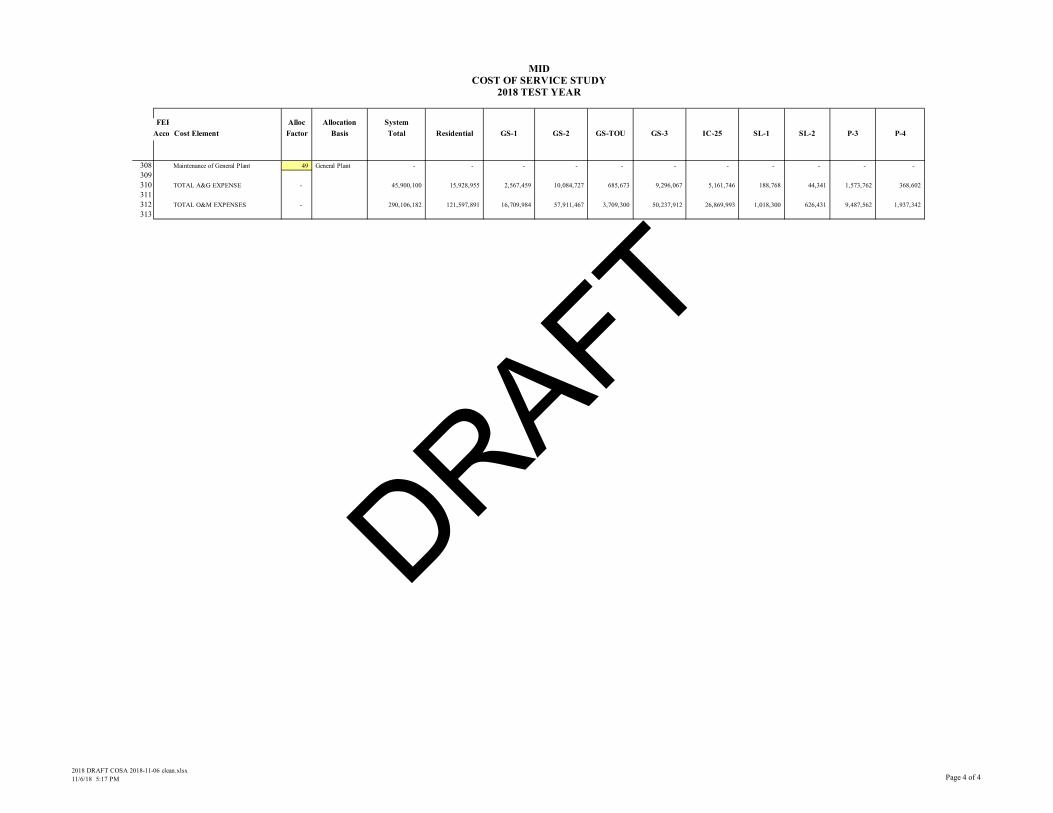

The following table summarizes the O&M costs for the Test Year.

10 Details regarding sales by customer class and rate schedule are found in Appendix 1.

DRAFT

November 19, 2018 MRW & Associates, LLC 8

Table 7: Total O&M for Electric Department for Test Year ($)

Power Production

Transmission Distribution Customer Accounts

A & G Total

205,892,704 8,781,221 15,829,819 13,702,338 45,900,100 290,106,182 Source: Appendix 1, Schedule 3

The following sections provide details for each of these five categories of costs.

1. Power Production

MID’s power production O&M expenses reflect the costs to operate and maintain MID’s generating fleet, purchase fuel for its gas-fired generation, purchase power pursuant to short- and long-term power purchase agreements (PPAs), operate and dispatch MID’s portfolio of power supply assets to meet MID’s customer loads, and to compensate Irrigation for the net value of the energy and capacity that Electric receives from MID’s hydroelectric generating facilities. Table 8 below presents the Power Production O&M expenses for the Test Year.

MID’s largest O&M expenses for Power Production are purchased power and fuel. Each of these categories are discussed in more detail below. Most of the O&M expenses in Table 8 are self-explanatory. However, the category “Hydro Water Charge” deserves additional discussion. The Don Pedro dam has a hydroelectric generating facility. Don Pedro generates electricity that is used by Electric to serve its customers. As a result, Electric is able to avoid either purchasing or generating the quantity of electricity and capacity provided by Don Pedro. Thus, Electric avoids the costs of purchasing both energy and capacity that it receives from Irrigation. At the same time, the responsibility for building, operating, and maintaining Don Pedro has historically been split between the Electric and Irrigation business lines. Electric is responsible for the relicensing of the hydroelectric facility at Don Pedro with the Federal Energy Regulatory Commission (FERC).

The net cost that Electric avoids associated with Don Pedro is the difference between (1) the value of energy and capacity related to the hydroelectric generation provided to Electric from Don Pedro and (2) the costs that Electric bears related to the ownership of the hydroelectric generation at Don Pedro.11

11 For additional details regarding the development of Electric’s net cost associated with Don Pedro, see Appendix 2.

DRAFT

November 19, 2018 MRW & Associates, LLC 9

Table 8: O&M Expenses for Power Production ($)

FERC Account

Description O&M Costs ($)

Hydraulic Power Generation

535 Oper. Supervision and Engineering 69,000 537 Hydraulic Expenses 11,500 538 Electric Expenses 69,000 539 Misc. Hydro Power Generation Exp. 253,971 Subtotal – Operations 403,471 542 Maint. Supervision and Engineering 23,884 543 Maint. Of Res., Dams, and Waterways 368,000 544 Maintenance of Electric Plant 441,631 545 Maint. Of Misc. Hydro Power Plant 34,993 Subtotal – Maintenance 868,508 Total Hydro Power Expense 1,271,978 Other Power Generation

546 Oper. Supervision and Engineering 8,629,732 547 Fuel 22,827,247 548 Generation Expenses 4,073,574 Subtotal – Operations 35,530,553 551 Maint. Supervision and Engineering 180,646 553 Maintenance of Generating Units 2,376,735 554 Maint. Of Misc. Other Power Gener. P.t 2,107,671 Subtotal – Maintenance 4,665,052 Total Other Power Production Expenses 40,195,604 555 Purchased Power 150,436,193 556 System Control and Load Dispatching 7,657,363 557 Hydro Water Charge 6,331,565 Total Other Power Supply Expense 164,425,121 Total Production Expense 205,892,704

Source: Appendix 1, Schedule 3 a) Purchased Power Expenses

Purchased Power expenses are the largest portion of the Power Production O&M expenses, which are the largest of MID’s O&M expenses for Electric. These costs are associated with take or pay contracts, purchased power agreements, and spot market purchases to balance MID’s needs to meet load. Overall, MID’s purchased power expenses for the Test Year are about $150.4 million.

Table 9 below summarizes forecast expenses for Electric’s purchased power for the Test Year.

DRAFT

November 19, 2018 MRW & Associates, LLC 10

Table 9: MID's Purchased Power Costs

Counterparty/Type Cost (MM$) Renewables Wind 55.2 Solar 10.3 Biomass 1.4 Small Hydro 0.2 Subtotal Renewables 67.1 Purchased Power Long Term 5.9 Short Term 43.3 Subtotal Purchased Power 49.2 Lodi Energy Center (Fuel + O&M) 2.9 M-S-R 17.9 TANC 11.6 Misc. Regulatory and Grid Charges 1.9 Total 150.4

Source: MID Note: Components may not sum to total due to rounding b) Fuel Expenses

Fuel expenses are the second-largest portion of MID’s Power Production O&M expenses, which are the largest of MID’s O&M expenses for Electric. These costs are associated with fuel acquired by MID to operate its own power plants and fuel that is delivered to power plants with which MID has tolling agreements. All of MID’s fuel expenses for power production are related to purchases of natural gas. MID’s fuel expenses for the Test Year are $22.8 million.

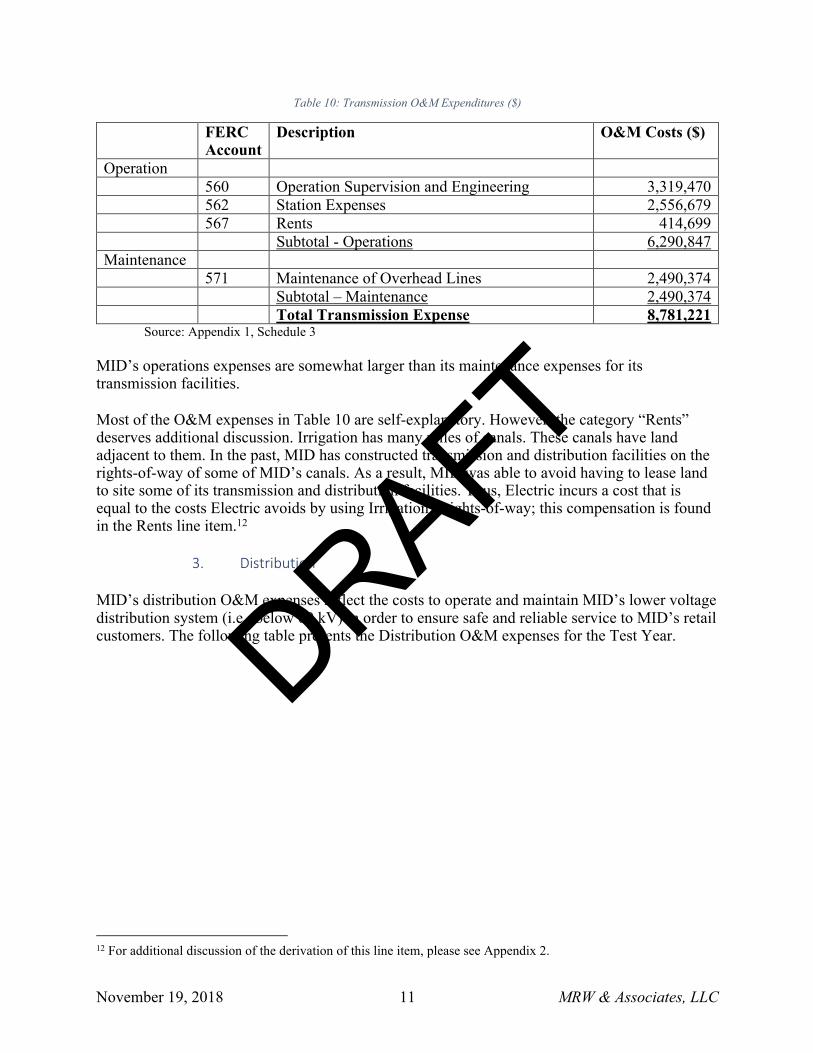

2. Transmission

MID’s transmission O&M expenses reflect the costs to operate and maintain MID’s high voltage transmission system (i.e., 69 kV to 230 kV) in order to ensure safe and reliable service to MID’s retail customers. The following table presents the Transmission O&M expenses for the Test Year.

DRAFT

November 19, 2018 MRW & Associates, LLC 11

Table 10: Transmission O&M Expenditures ($)

FERC Account

Description O&M Costs ($)

Operation 560 Operation Supervision and Engineering 3,319,470

562 Station Expenses 2,556,679 567 Rents 414,699

Subtotal - Operations 6,290,847 Maintenance

571 Maintenance of Overhead Lines 2,490,374 Subtotal – Maintenance 2,490,374

Total Transmission Expense 8,781,221 Source: Appendix 1, Schedule 3 MID’s operations expenses are somewhat larger than its maintenance expenses for its transmission facilities.

Most of the O&M expenses in Table 10 are self-explanatory. However, the category “Rents” deserves additional discussion. Irrigation has many miles of canals. These canals have land adjacent to them. In the past, MID has constructed transmission and distribution facilities on the rights-of-way of some of MID’s canals. As a result, MID was able to avoid having to lease land to site some of its transmission and distribution facilities. Thus, Electric incurs a cost that is equal to the costs Electric avoids by using Irrigation’s rights-of-way; this compensation is found in the Rents line item.12

3. Distribution

MID’s distribution O&M expenses reflect the costs to operate and maintain MID’s lower voltage distribution system (i.e., below 69 kV) in order to ensure safe and reliable service to MID’s retail customers. The following table presents the Distribution O&M expenses for the Test Year.

12 For additional discussion of the derivation of this line item, please see Appendix 2.

DRAFT

November 19, 2018 MRW & Associates, LLC 12

Table 11: Distribution O&M Expenses ($)

FERC Account

Description O&M Costs ($)

Operation 582 Station Expenses 3,411,888

588 Miscellaneous Distribution Expenses 26,500 Subtotal – Operations 3,438,388 Maintenance 590 Maint. Supervision and Engineering 1,263,073

593 Maintenance of Overhead Lines 5,722,318 594 Maintenance of Underground Lines 1,748,178 595 Maintenance of Line Transformers 327,717 596 Maint. Of Street Lighting Equipment 93,411 597 Maintenance of Meters 3,236,735

Subtotal – Maintenance 12,391,431 Total Distribution Expense 15,829,819

Source: Appendix 1, Schedule 3 MID’s maintenance expenses are larger than its operations expenses for its distribution facilities

4. Customer Accounts

MID’s Customer Accounts O&M expenses reflect the costs to provide retail services to MID’s customers. These include revenue-cycle services (e.g., meter reading, billing) as well as customer assistance. The following table presents the Customer Accounts O&M expenses for the Test Year.

Table 12: Customer Accounts O&M Expenditures ($)

FERC Account

Description O&M Costs ($)

Operation 901 Supervision 719,427 903 Customer Records and Collection 6,424,729 904 Uncollectable Accounts 2,300,000 908 Customer Assistance 4,258,182 Total Customer Accts. Expense 13,702,338

Source: Appendix 1, Schedule 3 MID’s Customer Records and Collections are nearly half of MID’s total Customer Accounts O&M expenses.

5. Administrative & General

MID’s A&G expenses reflect the costs to operate the MID enterprise in its entirety. These consist of two sets of costs: (1) certain costs that are directly assigned to Electric and (2) an

DRAFT

November 19, 2018 MRW & Associates, LLC 13

allocated portion of the A&G costs that are not directly assigned to either Electric or Irrigation.13 The following table presents the O&M expenses related to A&G for the Test Year.

Table 13: Administrative & General Expenditures ($)

FERC Account

Description O&M Costs ($)

920 Administrative and General 41,001,233 921 Public Benefits 4,298,867 927 Franchise Requirements 600,000 Total A&G Expense 45,900,100

Source: Appendix 1, Schedule 3 Note: In Appendix 2, A&G Expenses in Table 5 only include FERC Account 920. FERC Account 921 and

927 are included in the “O&M” line item in Table 5 in Appendix 2. In addition to A&G expenses, Electric receives revenue that reimburses A&G expenses that MID bills to others (i.e., the City of Modesto). This revenue is included as a part of the non-rate revenue received by the Electric Department. This is discussed further below.

C. Debt Service

Debt service represents existing and projected debt service for Electric. The existing debt service within the Test Year Revenue Requirement includes the amortization schedules for MID debt as provided by MID. MID’s debt service costs include a 10% adder to ensure debt service coverage is consistent with bond covenants. Finally, MID plans to accelerate payment of outstanding debt. MID has taken this step for the past several years. The accelerated repayment costs included in the COSA are $24.5 million for 2018.

D. Non-Rate Revenue Electric receives non-rate revenue from various sources. The sources of non-rate revenue include customer service fees and certain interest income.14 In addition, as previously discussed, Electric receives revenue that reimburses A&G expenses that MID bills to others. The following table summarizes the major categories of non-rate revenue. The revenue reimbursing the A&G expenses that MID bills to others is included under the category “Other Operating Income”.

13 For additional information regarding the allocation of A&G expenses that are not directly assigned to the Electric Department, see Appendix 2. 14 See Appendix 2 for further discussion of allocation of interest income to Electric.

DRAFT

November 19, 2018 MRW & Associates, LLC 14

Table 14: MID's Non-Rate Revenue for Electric ($)

Category Amount Other Operating Revenues Customer Service Fee Revenue 1,400,000 Total Other Operating Revenues 1,400,000 Other Income Other Operating Income 7,920,489 Interest Income 2,422,534 Total Other Income 10,343,023 Total Non-Rate Revenue 11,743,023

Source: Appendix 1, Schedule 2

E. Total Revenue Requirements Based on the various categories of expenses and non-rate revenue discussed above, the following summarizes the revenue requirements for MID’s Electric Department for the Test Year.

Table 15: MID’s Revenue Requirements for Electric

Line Category Amount 1 O&M 290,106,182 2 Capital Expenses15 6,465,234 3 Debt Service & Debt Service Coverage16 94,613,189 4 Subtotal 391,184,604 5 Less Non-Rate Revenue -11,743,023 7 Less Discretionary Revenue17 -9,030,000 8 Revenue Requirement 370,411,582

Source: Appendix 1, Schedule 1 Note that this table does not include any transfers either to or from MID reserves.

III. RATE REVENUE

MID last established its retail electric rates in 2016.18 Based on those rates and MID’s billing determinants, estimates of total rate revenue as well as rate revenue by customer class were developed. The following table summarizes the forecasted rate revenue for the Test Year.

15 This line item is the capital expenditures that MID expenses and pays out of current revenues. Source: MID. 16 This line item equals the sum of Debt Service (principal plus interest), an allocation for defeasance of debt ($24.5 million), plus an allocation for meeting debt service coverage requirements. See Appendix 1 for more details about this line item. 17 Discretionary Revenues is derived from wholesale revenues and certain interest on reserves. The MID Board has discretion to allocate these revenues on the basis of Board policy. 18 The rate adjustment in 2016 only changed rates for residential customers and the rate change was revenue neutral to that class.

DRAFT

November 19, 2018 MRW & Associates, LLC 15

Table 16: Rate Revenue by Customer Class ($)

Line Customer Class Schedule Rate Revenue ($) 1 Residential Residential 155,733,609 2 Small Commercial GS-1 22,958,570 3 Medium/Large Commercial GS-2 76,301,128 4 GS-TOU 4,867,789 5 Industrial GS-3 56,993,098 6 IC-25 23,387,304 7 Agricultural P-3 12,445,627 8 P-4 2,131,909 9 Street Lighting SL-1 1,281,709 10 SL-2 701,636 11 Total 356,802,380

Source: Appendix 1, Schedule 1 Residential is MID’s single largest customer class, with revenues of almost $156 million. GS-2 is MID’s largest commercial customer class, with revenues of about $76.3 million.

IV. COST OF SERVICE RESULTS

Developing the Test Year Revenue Requirement is the first step in the Cost of Service Study, as shown in Figure 2. After determining the system revenue requirement, a COS for each customer class is developed to determine the specific costs to serve each class. Rate revenues for each Customer class revenues are compared to class revenue requirements to evaluate the current rate’s abilities to fully recover costs. MRW reviewed MID’s approach for determination of the cost to serve each customer class based on the revenue requirement developed in Section 3.

Once completed, the COS results indicate the degree to which existing rates recover the costs to serve customers.

A. Functionalization of Revenue Requirement

The second step in the COS and rate design process, as shown in Figure 2, is to functionalize the revenue requirement. Electric’s costs were unbundled into four functions: production, transmission, distribution, and customer service. The assignment of costs by function falls into two general categories: 1) direct assignments and 2) derived allocations. Direct assignments are costs that are readily associated with a specific utility function and are directly assigned to that function. For example, the purchase power contracts are an expense solely related to power supply, so it is directly assigned to that function.

Derived allocators are allocation factors that are based on the sum, average, or weighted effect of different underlying factors. Derived allocators can be complex and should reflect the logical answer to the following question – what underlying activities drive the cost of this item? Each of the four utility functions is described below.

DRAFT

November 19, 2018 MRW & Associates, LLC 16

1. Production Function

The power supply function consists of costs associated with power generation, the cost of purchased power, and procuring and administering power supply contracts.

2. Transmission Function

The transmission function consists of costs associated with operating and maintaining the transmission portion of the high-voltage electric grid and making capital investments, as necessary. The transmission facilities transmit electricity from the generation stations to the distribution system.

3. Distribution Function

The distribution function consists of costs associated with operating and maintaining the distribution portion of the electric grid and making capital investments, as necessary. The distribution facilities deliver power to the retail customers after it has been transmitted from the generation stations via the transmission grid. This includes low voltage distribution lines, distribution poles, underground lines, customer service connections, meters, and lighting-related assets.

4. Customer Service Function

The customer service function consists of costs associated with operating and maintaining the customer related facilities to meet customer support needs. This includes, but is not limited to, customer service, billing and collection, and meter reading.

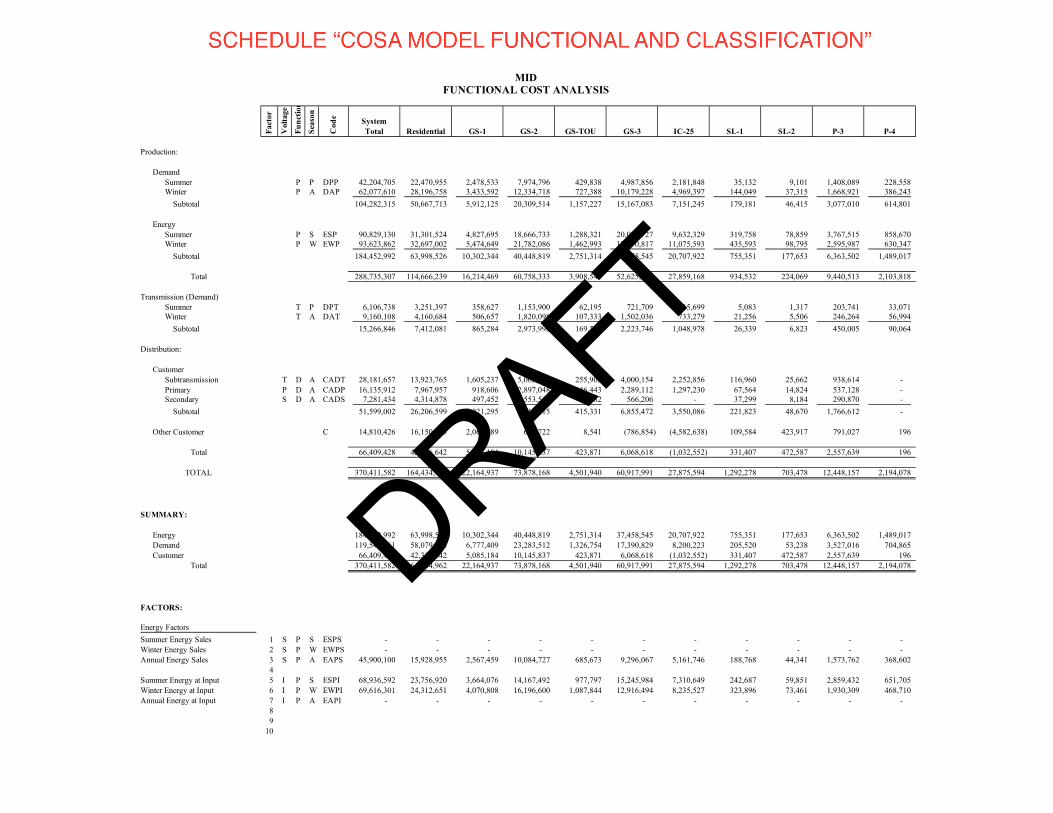

The revenue requirement determined for the Test Year was unbundled into the four functional areas of the system: production, transmission, distribution, and customer. The results of the functional unbundling are summarized in the following table. These are also illustrated further in Appendix 2.

Table 17: Functionalized Test Year Revenue Requirements ($)

Line Function Amount ($) 1 Production 288,735,307 2 Transmission 15,266,846 3 Distribution 51,599,002 4 Customer Service 14,810,426 5 Total 370,411,582

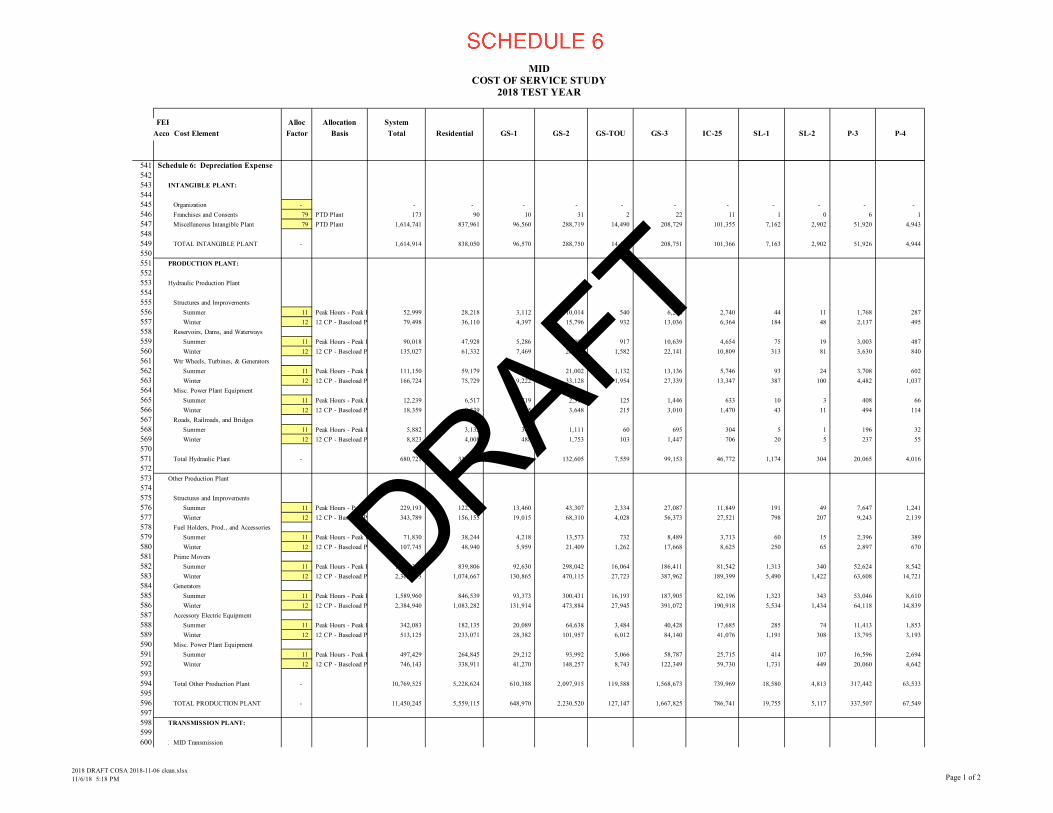

Source: Appendix 1, Schedule “COSA Model Functional and Classification”

The production function represents approximately 78% of the Test Year Revenue Requirement. The distribution function is the second largest cost center representing approximately 14% of the

DRAFT

November 19, 2018 MRW & Associates, LLC 17

Test Year Revenue Requirement. The transmission function and the customer service function each represent 4% of the Test Year Revenue Requirement.19

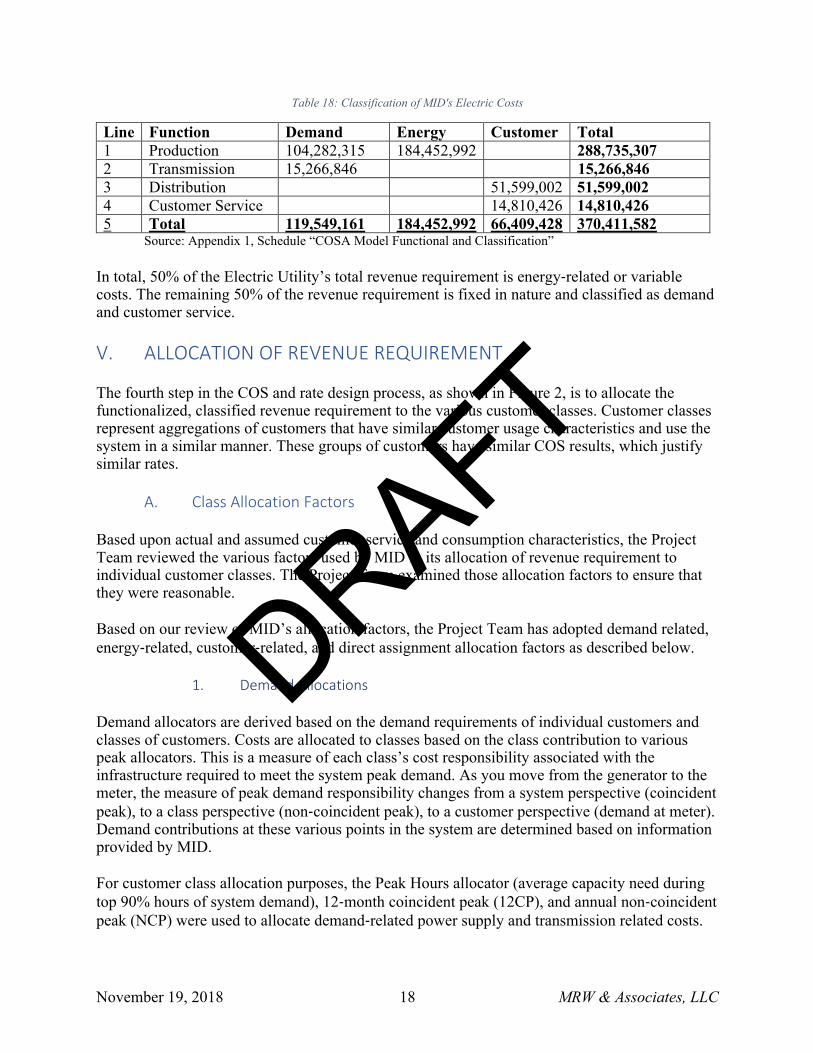

B. Classification of Revenue Requirement

The third step in the COS and rate design process, as shown in Figure 2, is to classify the functionalized revenue requirement. System costs can be classified into four generally-accepted rate-making cost classifications: (1) demand or fixed costs; (2) energy or variable costs; (3) customer-related costs; and (4) directly assignable costs. In order to provide a reasonable basis for the assignment of total revenue requirements (costs) to each customer class, costs for each function have been analyzed and classified into four categories as described below.

1. Demand Costs – Capacity (fixed- or demand-related) costs are those costs incurred to maintain a utility system to allow it to meet the total combined demands of its customers. Capacity costs include demand-related purchased power costs, the fixed portion of O&M expenses, debt service, capital expenditures, and other costs that are generally fixed and do not vary materially with the quantity of energy used or that cannot be designated specifically as a customer or variable cost.

2. Energy Costs – Energy, or variable costs, are costs that vary directly with energy usage, including such items as fuel, energy-related purchased power, and a portion of O&M expenses.

3. Customer Costs – Customer costs are those costs directly related to the number and type of customers, such as customer accounting, customer service, billing, and meter related expenses.

4. Direct Assignment Costs – Direct assignment costs are those costs that are readily identifiable and applicable to a particular customer or customer class (e.g., Lighting).20 The Project Team included Discretionary Revenues in the Direct Assignment category.

Once the costs within each function are assigned to each service category, the demand, energy, customer, and direct assignment component of each service is calculated.

19 For this study, the Project Team assigned Discretionary Revenue to the Customer Service function. 20 MID’s direct assignment costs are included in Customer Costs for the purposes of classification under service category.

DRAFT

November 19, 2018 MRW & Associates, LLC 18

Table 18: Classification of MID's Electric Costs

Line Function Demand Energy Customer Total 1 Production 104,282,315 184,452,992 288,735,307 2 Transmission 15,266,846 15,266,846 3 Distribution 51,599,002 51,599,002 4 Customer Service 14,810,426 14,810,426 5 Total 119,549,161 184,452,992 66,409,428 370,411,582

Source: Appendix 1, Schedule “COSA Model Functional and Classification”

In total, 50% of the Electric Utility’s total revenue requirement is energy-related or variable costs. The remaining 50% of the revenue requirement is fixed in nature and classified as demand and customer service.

V. ALLOCATION OF REVENUE REQUIREMENT

The fourth step in the COS and rate design process, as shown in Figure 2, is to allocate the functionalized, classified revenue requirement to the various customer classes. Customer classes represent aggregations of customers that have similar customer usage characteristics and use the system in a similar manner. These groups of customers have similar COS results, which justify similar rates.

A. Class Allocation Factors

Based upon actual and assumed customer service and consumption characteristics, the Project Team reviewed the various factors used by MID in its allocation of revenue requirement to individual customer classes. The Project Team examined those allocation factors to ensure that they were reasonable.

Based on our review of MID’s allocation factors, the Project Team has adopted demand related, energy-related, customer-related, and direct assignment allocation factors as described below.

1. Demand Allocations

Demand allocators are derived based on the demand requirements of individual customers and classes of customers. Costs are allocated to classes based on the class contribution to various peak allocators. This is a measure of each class’s cost responsibility associated with the infrastructure required to meet the system peak demand. As you move from the generator to the meter, the measure of peak demand responsibility changes from a system perspective (coincident peak), to a class perspective (non-coincident peak), to a customer perspective (demand at meter). Demand contributions at these various points in the system are determined based on information provided by MID.

For customer class allocation purposes, the Peak Hours allocator (average capacity need during top 90% hours of system demand), 12-month coincident peak (12CP), and annual non-coincident peak (NCP) were used to allocate demand-related power supply and transmission related costs.

DRAFT

November 19, 2018 MRW & Associates, LLC 19

The 12CP allocator was used to allocate winter and year-round baseload-related power supply costs. The Peak Hours allocator was used to allocate the peaking related power supply costs during summer months. Transmission costs for Electric were also allocated using the Peak Hours method for summer, which recognizes that the transmission system is constructed to deliver power at the times of the maximum system peak.

Similarly, distribution infrastructure is designed to meet the maximum demands of the localized system or customers, so the NCP allocation factor was used for distribution costs at different voltage levels. An NCP allocator is typically used to allocate distribution costs, as these facilities are sized to meet localized peak demands rather than the system peak demand. The NCP method was used to allocate the distribution system demand-related costs associated with substations, poles, conductors, and distribution transformers.

To account for variability in demands and loads between years, the load data for the last 5 years was used to determine the demand allocators.

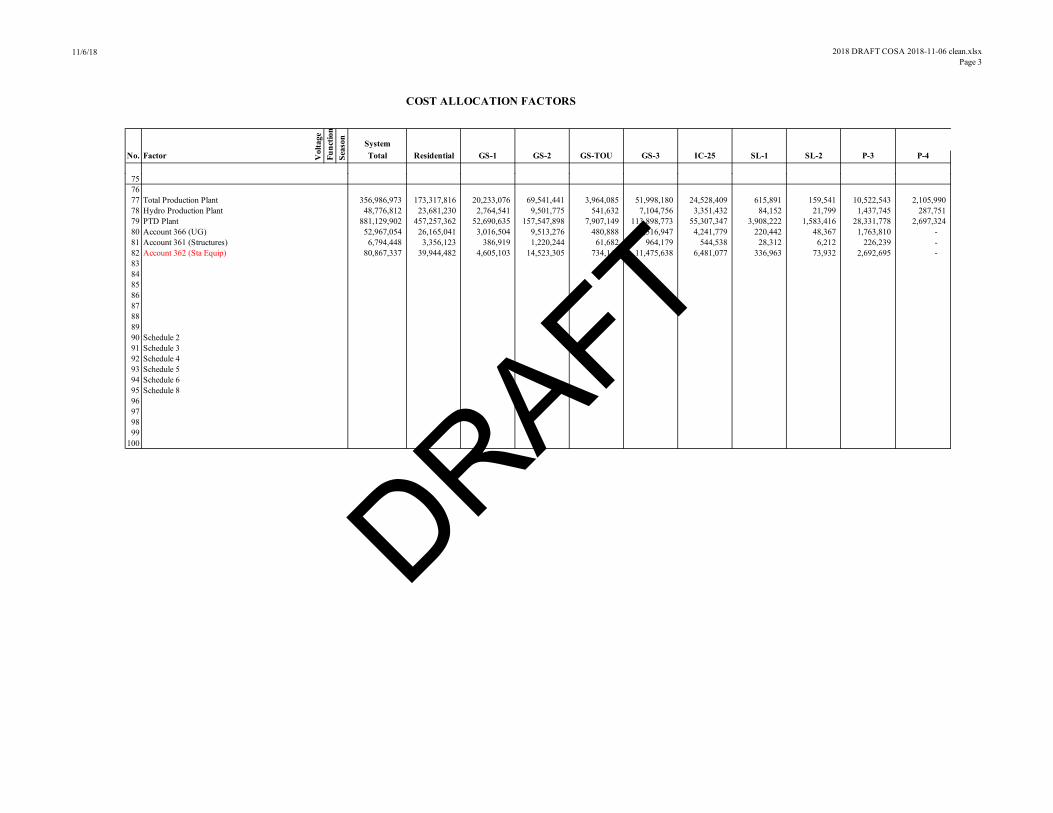

The following table presents the various demand allocators utilized in the Study. These represent the percentage of demand costs that are allocated to each rate schedule based on their load characteristics. The data behind these factors are illustrated further in Appendix 1.

Table 19: Demand Allocation Factors

Customer Class

Schedule Peak Hours

12CP NCP Sub-transmission

NCP Primary

NCP Secondary

Residential Residential 51.9% 45.4% 49.4% 49.4% 59.3% Small Commercial

GS-1 5.6% 5.5% 5.7% 5.7% 6.8%

Med/Large Commercial

GS-2 17.9% 19.9% 18.0% 18.0% 21.3%

GS-TOU 1.0% 1.2% 0.9% 0.9% 0.2% Industrial GS-3 14.1% 16.4% 14.2% 14.2% 7.8% IC-25 5.8% 8.0% 8.0% 8.0% 0.0% Agricultural P-3 3.2% 2.7% 3.3% 3.3% 4.0% P-4 0.5% 0.6% 0.0% 0.0% 0.0% Street Lights SL-1 0.1% 0.2% 0.4% 0.4% 0.5% SL-2 0.0% 0.1% 0.1% 0.1% 0.1%

Source: Derived from Appendix 1, Schedule “COSA Model Allocation Factors”

2. Energy Allocations

Energy allocation factors are the basis for allocating costs or expenses classified as variable or energy related and are assumed to vary directly with kWh sales. Energy-related costs classified as variable were energy costs from fuel, purchased power, and costs related to system control and load dispatching. The energy necessary to supply each customer class21 is used to allocate these types of costs to individual customer classes. The following table lists the energy allocation

21 This accounts for energy losses that occur on the transmission and distribution system when delivering energy to customers.

DRAFT

November 19, 2018 MRW & Associates, LLC 20

factor utilized in the Study. The energy at input is the actual energy that has to be generated to account for the losses that will result over the transmission and distribution system. The load data behind these factors are illustrated further in Appendix 1.

Table 20: Energy Allocation Factors

Customer Class

Schedule Summer Energy at Input

Winter Energy at Input

Annual Energy at Input

Residential Residential 34.5% 34.9% 34.7% Small Commercial

GS-1 5.3% 5.8% 5.6%

Med/Large Commercial

GS-2 20.6% 23.3% 22%

GS-TOU 1.4% 1.6% 1.5% Industrial GS-3 22.1% 18.6% 20.3% IC-25 10.6% 11.8% 11.2% Agricultural P-3 4.1% 2.8% 3.4% P-4 0.9% 0.7% 0.8% Street Lights SL-1 0.4% 0.5% 0.4% SL-2 0.1% 0.1% 0.1%

Source: Derived from Appendix 1, Schedule “COSA Model Allocation Factors”

3. Customer Allocations

Customer costs are defined as those costs related to the number of customers and the type of service required. Included in the customer-related costs are the costs associated with meter reading, customer service, sales, billing, collection, and other customer-related activities. The customer allocation factors were largely based on the number of customers in each class.

In allocating certain customer-related costs to the various customer classifications, weighted customer allocation factors were utilized. Weighting reflects that servicing certain types of customers requires more effort and expenses than other types of customers. Weighting factors were adopted from information provided by MID staff. Weighting factors reflect the relationships between the customer classes and the types of equipment or services needed to serve the class and the relative costs of those items. For example, large customers may have more than one meter per customer while residential customers usually have one meter per customer. Thus, the weighting factor for meters is 1 for residential customers, while it is a higher number for commercial customers. The number of customer accounts in each class are shown in the table below. Further details can be found in Appendix 1.

DRAFT

November 19, 2018 MRW & Associates, LLC 21

Table 21: Number of Customers by Schedule

Customer Class Schedule Customers Residential Residential 95,835 Small Commercial GS-1 10,388 Med/Large Commercial GS-2 2,251 GS-TOU 19 Industrial GS-3 43 IC-25 1 Agricultural P-3 1,725 P-4 1 Street Lights SL-1 200 SL-2 3,746

Source: Appendix 1, Schedule “COSA Model Allocation Factors”

4. Direct Assignment Allocations

Certain costs are not allocated to customer classes using the revenue allocators. Instead, those costs are directly assigned to the customer class that is responsible for them. An example of a directly-assigned cost would be O&M costs related to maintenance of streetlight equipment. MID’s direct assignment allocations are included in the Customer Cost classification.

As discussed elsewhere, the Project Team assigned Discretionary Revenues (e.g., wholesale revenues, certain interest income) to specific customer classes.

B. Cost of Service Results

The unbundled COS results by customer class is shown in the following table.

Table 22: Unbundled Revenue Requirements by Class ($)

Function-alized by Class

Res GS-1 GS-2 GS-TOU

GS-3 IC-25 P-3 P-4 SL-1 SL-2 Total

Production 114,666,239 16,214,469 60,758,333 3,908,541 52,625,628 27,859,168 9,440,513 2,103,818 934,532 224,069 288,735,307

Transmission 7,412,081 865,284 2,973,998 169,527 2,223,746 1,048,978 450,005 90,064 26,339 6,823 15,266,846

Distribution 26,206,599 3,021,295 9,513,115 415,331 6,855,472 3,550,086 1,766,612 221,823 48,670 51,599,002

Customer 16,150,043 2,063,889 632,722 8,541 (786,854) (4,582,638) 791,027 196 109,584 423,917 14,810,426

Total COS 164,434,962 22,164,937 73,878,168 4,501,940 60,917,991 27,875,594 12,069,345 2,411,569 1,185,176 701,850 370,411,582

Classified by Class

Energy 63,998,526 10,302,344 40,448,819 2,751,314 37,458,545 20,707,922 6,363,502 1,489,017 755,351 177,653 184,452,992 Demand 58,079,794 6,777,409 23,283,512 1,326,754 17,390,829 8,200,223 3,527,016 704,865 205,520 53,238 119,549,161 Customer 42,356,642 5,085,184 10,145,837 423,871 6,068,618 (1,032,552) 2,557,639 196 331,407 472,587 66,409,428 Total COS 164,434,962 22,164,937 73,878,168 4,501,940 60,917,991 27,875,594 12,448,157 2,194,078 1,292,278 703,478 370,411,582

Source: Appendix 1, Schedule “COSA Model Functional and Classification”

As can be seen from the above table, the residential rate class is MID’s biggest rate class, followed by GS-2, which is a medium/large commercial class, and GS-3 which is an industrial class. MID’s production function is by far the costliest function, while costs are slightly more evenly distributed when classified between demand, energy and customer costs, as the distribution costs are included in the Customer costs classification.

DRAFT

November 19, 2018 MRW & Associates, LLC 22

C. Cost of Service Results Compared to Current Revenue

Estimated operating costs were developed by the Project Team to compare the revenue generated under current rates to the current operating costs of Electric. The following table summarizes the variance between the Test Year Revenue Requirement and the annual revenue generated from current rates, by customer class. The result of comparing the projected revenues to the customer class revenue requirements indicate the degree to which existing rates recover revenues from each customer class on a COS basis.

Table 23: Cost of Service Compared to Rates ($)

Line Customer Class

Schedule Cost of Service

[a]

Test Year Rate

Revenues [b]

Difference ($)

[c] = [a]-[b]

Difference (%)

[d]=[c]/[b]

1 Residential Residential 164,434,962 155,733,609 8,701,353 5.6% 2 Small

Commercial GS-1 22,164,937 22,958,570 (793,634) -3.5%

3 M/L Commercial

GS-2 73,878,168 76,301,128 (2,422,960) -3.2%

4 GS-TOU 4,501,940 4,867,789 (365,850) -7.5% 5 Industrial GS-3 60,917,991 56,993,098 3,924,893 6.9% 6 IC-25 27,875,594 23,387,304 4,488,289 19.2% 7 Agricultural P-3 12,448,157 12,445,627 2,530 0.02% 8 P-4 2,194,078 2,131,909 62,169 2.9% 9 Street Lights SL-1 1,292,278 1,281,709 10,569 0.8% 10 SL-2 703,478 701,636 1,842 0.3% 11 Total 370,411,582 356,802,380 13,609,202 3.8%

Source: Appendix 1, Schedule 1

As shown in Table 23, overall COS analysis forecasts that current costs are $370,411,582 and the current rate revenue is $356,802,380.

Table 23 shows that all customer classes except for tariffs serving Small and Medium/Large Commercial customers are paying less than their costs of service (i.e., Test Year rate revenues are less than Cost of Service). For example, Residential’s Cost of Service is $164,434,962 but its Rate Revenues under current rates are only $155,733,609, meaning that Residential’s Cost of Service is 5.6% greater than its rate revenue. The levels of under- or over-collection for each customer class on a percentage basis are, on an absolute value basis, less than was found in late 2010, meaning that the current MID rates are “closer” to cost of service than what was found in 2010. The following table presents the level of under- or over-collection in late 2010 and under MID’s current rates.

DRAFT

November 19, 2018 MRW & Associates, LLC 23

Table 24: Comparison of Under- or Over-Collection of Costs Under Current Rates Compared to Rates and Costs in 2010 (%)

Line Customer Class Schedule Under/(Over) Collection of Costs in 2010 (%)

Under/(Over) Collection of Costs Under Current Rates (%)

1 Residential Residential 5.6% 5.6% 2 Small Commercial GS-1 -3.9% -3.5% 3 M/L Commercial GS-2 -9.7% -3.2% 4 GS-TOU -8.4% -7.5% 5 Industrial GS-3 6.9% 6.9% 6 IC-25 19.3% 19.2% 7 Agricultural P-3 3.0% 0.02% 8 P-4 4.8% 2.9% 9 Street Lights SL-1 3.5% 0.8% 10 SL-2 105.0% 0.3%

Source: MID and Appendix 1, Schedule 1

D. Grandfathering Under Proposition 26 As shown in Table 24 above, MID historically has over-recovered costs from rates paid by commercial customers taking service under Schedules GS-1, GS-2, and GS-TOU, and its policy to do so is pre-Proposition 26 legislation that is grandfathered by the measure. Commercial customers will continue to pay above their cost of service, as permitted by pre-Proposition 26 legislative choices which survive it. Moreover, because the proposed percentage of revenue allocation for those customers will decrease the extent to which commercial customers pay more than the cost of service (i.e., bringing them closer to service cost), they do not violate Proposition 26.

Based on this, the Project Team believes that the rates currently in effect at MID are reasonable.

VI. CONCLUSIONS

The Project Team concludes:

• The rates currently in force at MID are reasonable given the cost of service for MID. • The rate revenue collected by Electric is less than MID’s cost of service for Electric. • Any under- or over-collection of cost of service by Electric pursuant to the rates currently

in effect are similar or less than the level of under- or over-collection of cost of service by Electric as was found in early 2011 (based on a Cost of Service Analysis prior to the enactment of Proposition 26), meaning that the MID rates that are currently in force are reasonable based on the grandfathering of the levels of under- or over-collection found in early 2011.

DRAFT

November 19, 2018 MRW & Associates, LLC

APPENDIX 1

SUPPORTING TABLES

DRAFT

2018 DRAFT COSA 2018-11-06 clean.xlsx11/6/18 5:14 PM Page 1 of 1

MIDCOST OF SERVICE STUDY

2018 TEST YEAR Allocation Factor

FERC Alloc Allocation SystemAccountCost Element Factor Basis Total Residential GS-1 GS-2 GS-TOU GS-3 IC-25 SL-1 SL-2 P-3 P-4

Schedule 1: Summary of Results

A. REVENUE REQUIREMENT CALCULATION (CASH BASIS)

Operating Expenses:1 Operation & Maintenance Expenses 91 Schedule 3 290,106,182 121,597,891 16,709,984 57,911,467 3,709,300 50,237,912 26,869,993 1,018,300 626,431 9,487,562 1,937,342

2 Public Purpose/DSM Programs 3 Annual Energy Sales - - - - - - - - - - -

34 Total Operating Expenses - 290,106,182 121,597,891 16,709,984 57,911,467 3,709,300 50,237,912 26,869,993 1,018,300 626,431 9,487,562 1,937,342

56 Operating Margin:7 Capital Improvements 52 Rate Base 6,465,234 3,405,258 391,673 1,138,010 56,478 820,136 399,420 19,522 5,490 210,953 18,293

8 Principal Portion of Debt Service 52 Rate Base 57,895,000 30,493,472 3,507,357 10,190,676 505,755 7,344,168 3,576,733 174,815 49,161 1,889,049 163,814

9 Debt Service 52 Rate Base 29,480,626 15,527,535 1,785,976 5,189,179 257,535 3,739,713 1,821,303 89,017 25,033 961,920 83,416

10 Debt Service Coverage 52 Rate Base 7,237,563 3,812,046 438,461 1,273,956 63,225 918,108 447,134 21,854 6,146 236,154 20,479

11 Total Operating Margin - 101,078,422 53,238,312 6,123,466 17,791,821 882,993 12,822,125 6,244,589 305,208 85,829 3,298,076 286,002

1213 Total Required Revenues - 391,184,604 174,836,203 22,833,450 75,703,288 4,592,293 63,060,037 33,114,582 1,323,509 712,261 12,785,638 2,223,344

1415 Less: Other Operating Revenues 90 Schedule 2 (1,400,000) (1,353,539) (41,919) (4,542) - - - - - - -

16 Less: Other Income 90 Schedule 2 (19,373,023) (9,047,701) (626,594) (1,820,579) (90,354) (2,142,046) (5,238,988) (31,231) (8,783) (337,481) (29,266)

1920 Required Revenues From Sales - 370,411,582 164,434,962 22,164,937 73,878,168 4,501,940 60,917,991 27,875,594 1,292,278 703,478 12,448,157 2,194,078

2122 Revenues at Existing Rates 90 Schedule 2 356,802,380 155,733,609 22,958,570 76,301,128 4,867,789 56,993,098 23,387,304 1,281,709 701,636 12,445,627 2,131,909

2324 Increase (Decrease) Required - $ - 13,609,202 8,701,353 (793,634) (2,422,960) (365,850) 3,924,893 4,488,289 10,569 1,842 2,530 62,169

25 - % 3.8% 5.6% -3.5% -3.2% -7.5% 6.9% 19.2% 0.8% 0.3% 0.0% 2.9%

2627 B. BILLING UNITS2829 Energy (MWh): energy sales

30 Annual 2,590,737 899,077 144,915 569,212 38,701 524,697 291,344 10,655 2,503 88,828 20,805

3334 Demand (kW): billing demands