Cost of Capital - Blog Universitas Padjadjaran | Mari menulis dan...

42

The Cost of Capital

Transcript of Cost of Capital - Blog Universitas Padjadjaran | Mari menulis dan...

The Cost of Capital

Management need to understand the cost of capital to select long-term investments after assessing term investments after assessing their acceptability and relative rangkings.

Gitman & Zutter (2012:358)

The cost of capital represents the firm’s cost of financing and is the minimum rate of return that a project must earn to increase firm value. firm value.

A firm’s cost of capital is estimated at a given point in time and reflects the expected average future cost of funds over the long run.

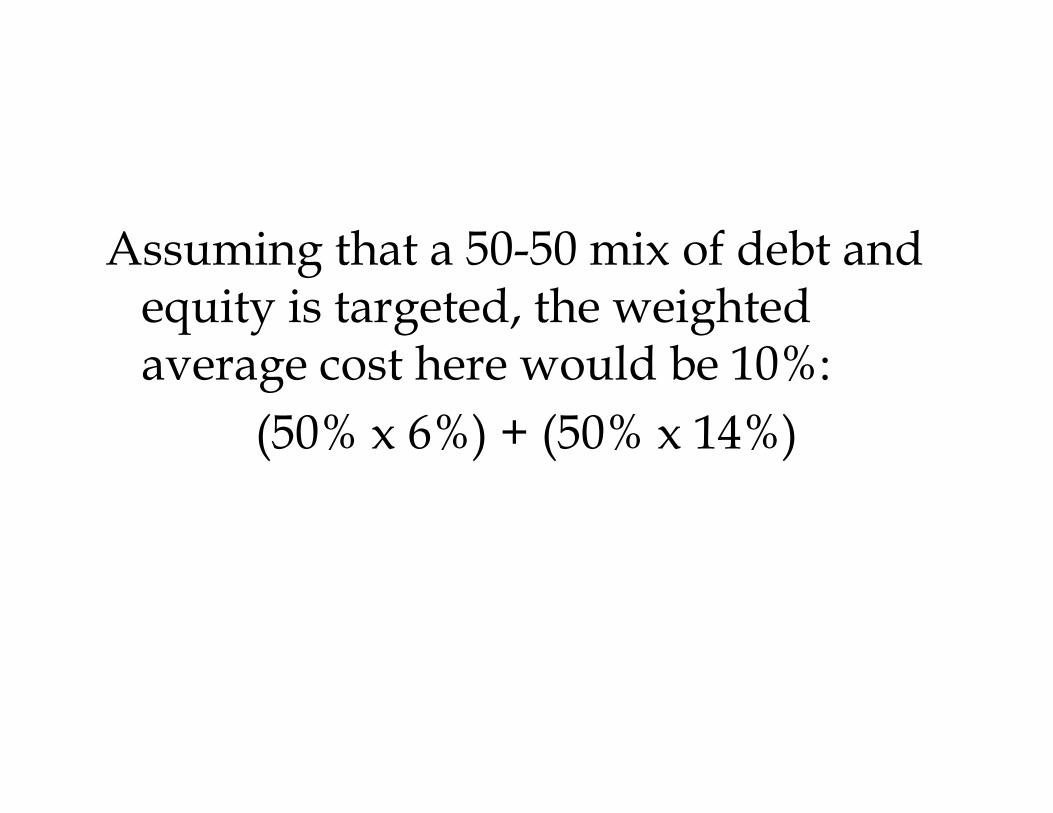

A firm is currently faced with an investment opportunity.

- Best project available today:

Cost $100,000

Life 20 yearsLife 20 years

IRR = 7%

Cost of least-cost financing source available,

Debt = 6%

� The firm undertakes the opportunity

Best project available 1 week later:

Cost $100,000

Life 20 years

IRR = 7%IRR = 7%

Cost of least-cost financing source available: Equity =14%

� The firm rejects the opportunity

Assuming that a 50-50 mix of debt and equity is targeted, the weighted average cost here would be 10%:

(50% x 6%) + (50% x 14%)(50% x 6%) + (50% x 14%)

Mengapa perhitungan “weighted average

cost of capital” diperlukan?

• Suatu pendekatan sederhana untuk evaluasi investasi

• Evaluasi secara keseluruhan mengenai pengambilan keputusan suatu investasi agar pengambilan keputusan suatu investasi agar dapat meningkatkan nilai perusahaan, dalam hal ini memilih projek yang memberikan returnyang lebih besar daripada weighted average cost of financing (or WACC).

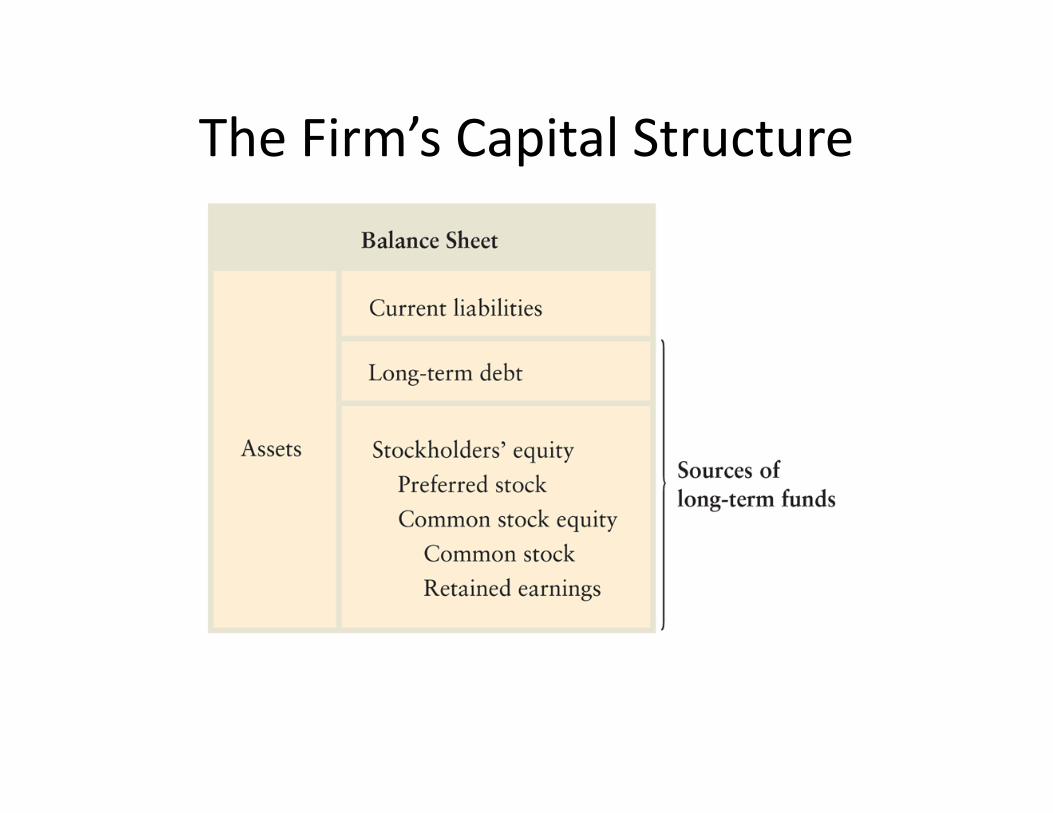

Long-term sources of funds � the

permanent financing:

1. long-term debt

2. Preferred stock

3. Common stock equity: Common stock

and Retained earnings.

The Firm’s Capital Structure

WEIGHTED AVERAGE COST OF CAPITAL (WACC)OF CAPITAL (WACC)

Overall cost of capital: biaya modal rata-rata dari modal/dana jangkapanjang yang digunakanperusahaan untukperusahaan untukmendanai/membiayai perusahaan.

Brealey, Myers & Marcus (2004:322)

The company cost of capital is a weighted

average of the returns demanded by

debt and equity investors.

The weighted average is the expected rate The weighted average is the expected rate

of return investors would demand on a

portfolio of all the firm’s outstanding

securities.

Mengapa penting:

1. Biaya modal akan menentukanpenawaran dana kepadaperusahaan

2. Biaya modal akan mempengaruhi2. Biaya modal akan mempengaruhistruktur modal dan kebijakandividen

WACC ditentukan oleh:

1. Biaya sumber dana secaraindividual

2. Bobot sumber dana dalam strukturmodal

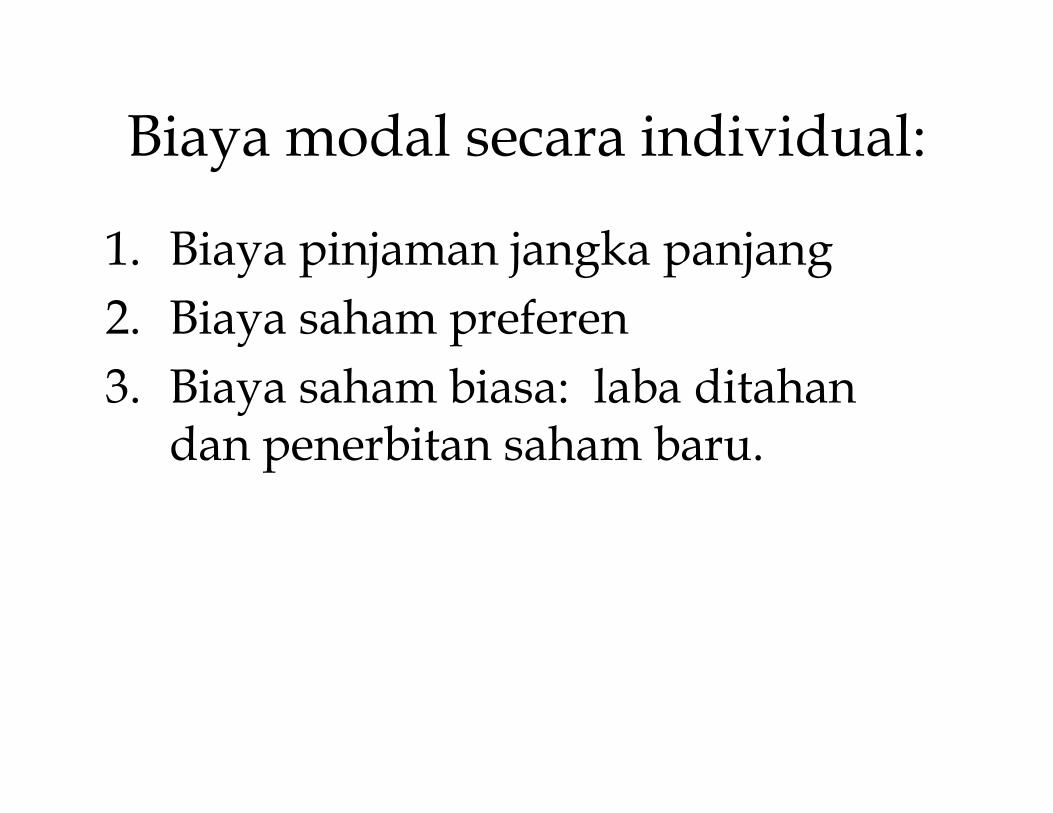

Biaya modal secara individual:

1. Biaya pinjaman jangka panjang

2. Biaya saham preferen

3. Biaya saham biasa: laba ditahan3. Biaya saham biasa: laba ditahandan penerbitan saham baru.

The Cost of Long-Term Debt

Dapat dihitung melalui salah satu cara:

–Persamaan biaya /cost quotations

–Menghitung biaya /Calculating the cost

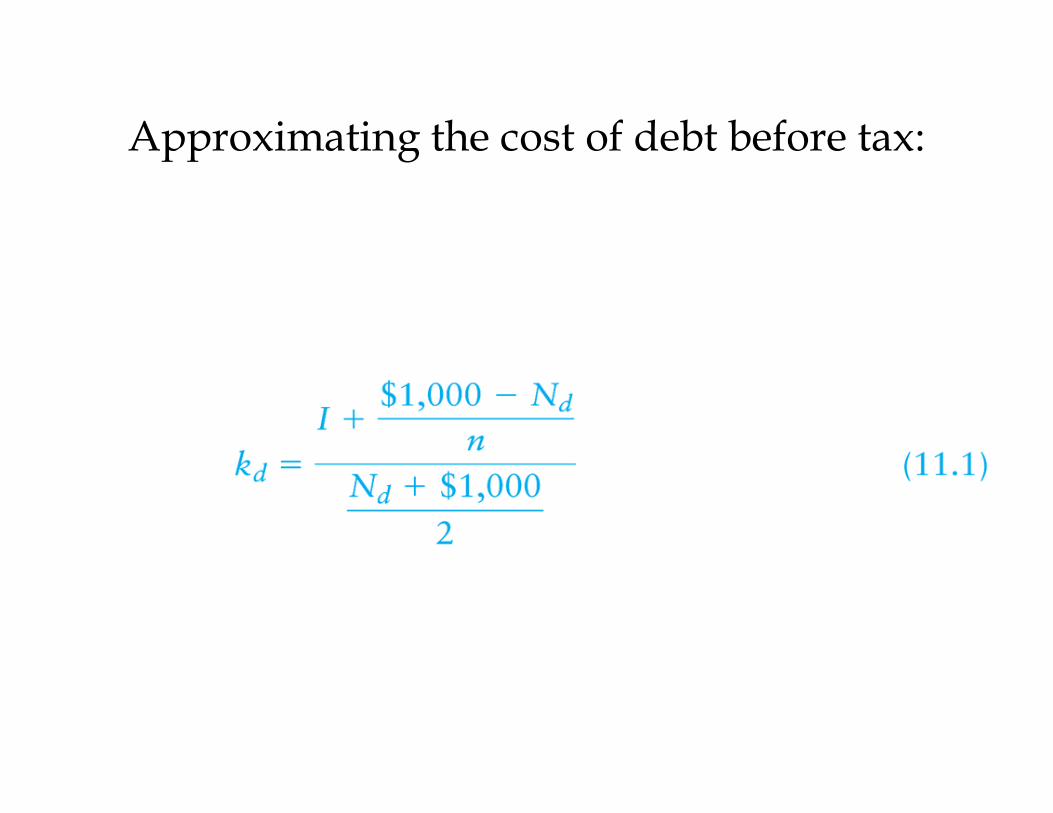

–Memperkirakan biaya/ –Memperkirakan biaya/ Using/Approximating the cost

Cost of Debt

Duchess Corporation, a major hardware manufacturer, is contemplating selling bonds with a par value of $ 1,000 of 20-year, 9% coupon. The firm sell the bonds year, 9% coupon. The firm sell the bonds at $ 980. Flotation costs are 2% or $ 20. The net proceeds to the firm for each bond is therefore $ 960 ($ 980 - $ 20).

Persamaan biaya:

Net proceeds dari penjualan obligasi sama dengan nilai per

lembar nya, dan biaya sebelum pajak akan sama dengan

tingkat bunga kupon

Menghitung biaya

Dilakukan dengan menghitung internal rate of return

(IRR),dengan cara: (a) trial and error, (b) kalkulator

finansial, atau (c) spreadsheet.

Calculating the cost of debt before tax:

Approximating the cost of debt before tax:

Find the after-tax cost of debt for Duchess assuming it has a 40% tax rate:

rd = 9.4% (1- 40%) = 5.6%

This suggests that the after-tax cost of This suggests that the after-tax cost of raising debt capital for Duchess is 5.6%.

The Cost of Preferred Stock

Duchess Corporation is contemplating

issuance of a 10% preferred stock that is

expected to sell for its $87 per share par

value. The cost of issuing and selling the value. The cost of issuing and selling the

stock expected to be $5 per share.

rp = DP/Np = $8.70/$82 = 10.6%

The Cost of Common Stock

• The cost of common stock equity is the rate at which investors discount the expected dividends of the firm to determine its share value.determine its share value.

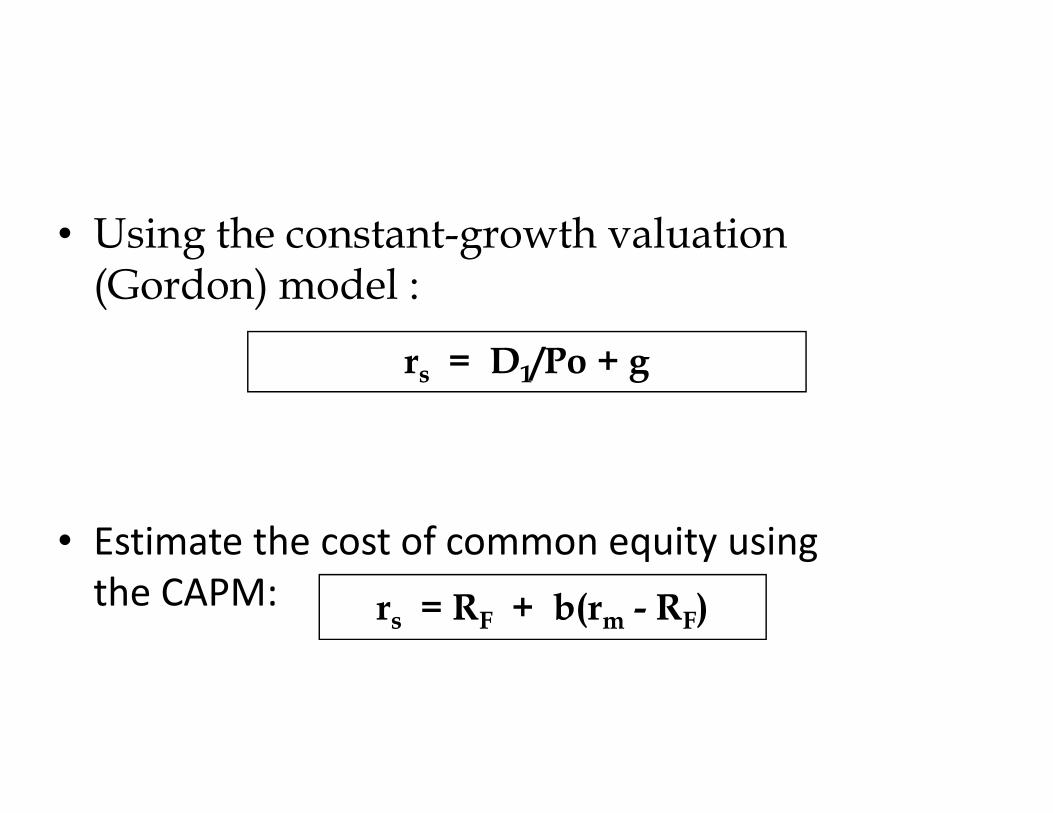

• Estimasi cost of common equity: the constant-growth valuation model, dancapital asset pricing model (CAPM).

• Using the constant-growth valuation (Gordon) model :

rs = D1/Po + g

• Estimate the cost of common equity using

the CAPM: rs = RF + b(rm - RF)

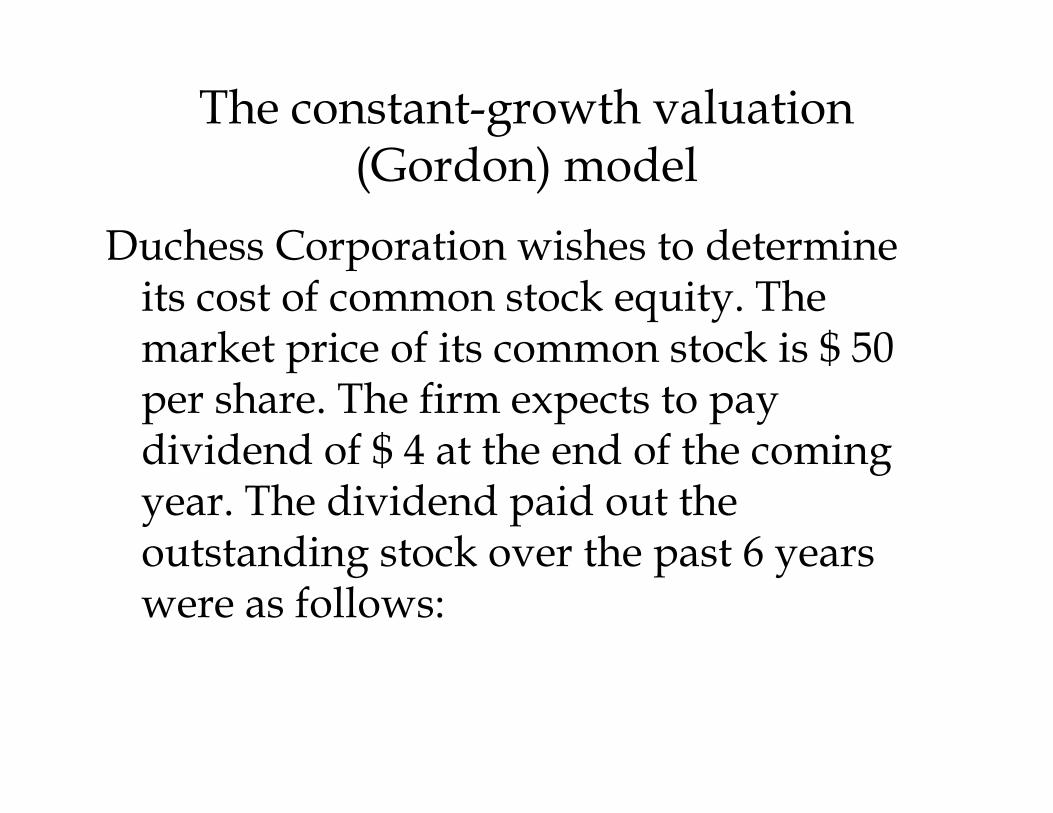

The constant-growth valuation (Gordon) model

Duchess Corporation wishes to determine its cost of common stock equity. The market price of its common stock is $ 50 per share. The firm expects to pay per share. The firm expects to pay dividend of $ 4 at the end of the coming year. The dividend paid out the outstanding stock over the past 6 years were as follows:

Year Dividend

2012 $ 3.80

2011 $ 3.62

2010 $ 3.472010 $ 3.47

2009 $ 3.33

2008 $ 3.12

2007 $ 2.97

g = 5%

P0 = $ 50

D1 = $ 4

Cost of common stock equity = 13%

• CAPM memperhitungkan risikoperusahaan yaitu beta, sedangkan The constant-growth valuation (Gordon) model tidak memperhitungkan risiko.

• The constant-growth valuation (Gordon) model menggunakan hargapasar (P0) sebagai tingkat risk-return yang diharapkan.

• Cost of Retained Earnings (ke)

– Constant-Growth Model

For example, assume a firm has just paid a dividend of

$2.50 per share, expects dividends to grow at 10% $2.50 per share, expects dividends to grow at 10%

indefinitely, and is currently selling for $50.00 per share.

D1 = $ 2.50 (1+ 10%) = $ 2.75

kS = ($2.75/$50.00) + 10% = 15.5%.

– Security Market Line Approach

rs = rF + b(rM - rF).

For example, if the 3-month T-bill rate is

currently 5.0%, the market risk premium is 9%,

and the firm’s beta is 1.20, the firm’s cost of

retained earnings will be:

rs = 5.0% + 1.2 (9.0%) = 15.8%.

• The previous example indicates that our estimate of the cost of retained earnings is somewhere between 15.5% and 15.8%. At this point, we could either choose one or the other estimate or average the two.estimate or average the two.

• Using some managerial judgment and preferring to err on the high side, we will use 15.8% as our final estimate of the cost of retained earnings.

• Cost of New Issues of Common Stock (rn)

rn = = D1/Nn + g

Continuing with the previous example, how much would Continuing with the previous example, how much would

it cost the firm to raise new equity if flotation costs

amount to $4.00 per share?

rn = [$2.75/($50.00 - $4.00)] + 10% = 15.97% or 16%.

Capital Structure Weights

• For example, assume the market value of the firm’s debt is $40 million, the market value of the firm’s preferred stock is $10 million, and the preferred stock is $10 million, and the market value of the firm’s equity is $50 million.

• Dividing each component by the total of $100 million gives us market value weights of 40% debt, 10% preferred, and 50% common.and 50% common.

WACC = ka = wiki + wpkp + wskn

The weights in the above equation are intended

to represent a specific financing mix (where wito represent a specific financing mix (where wi

= % of debt, wp = % of preferred, and ws= % of

common).

Using the costs previously calculated along with the market value weights, we may calculate the weighted average cost of capital as follows:

WACC =

0.40(5.6%) + 0.10(10.6%) + 0.50(15.8%)

= 11,2%

• This assumes the firm has sufficient retained earnings to fund any anticipated investment fund any anticipated investment projects.

WACC

• Cost of debt = 5,6%

• Cost of preferred stock = 10,6%

• Cost of retained earnings = 15,8%

• Cost of new common stock = 16%• Cost of new common stock = 16%

• Source of capital:

- Long term debt 40%

- Preferred stock 10%

- Common stock equity 50%

Capital Structure Weights:

• One method uses book values from the firm’s balance sheet. For example, to estimate the weight for debt, simply divide the book value of the firm’s long-term debt by the book value of its total term debt by the book value of its total assets.

• A second method uses the market values of the firm’s debt and equity. To find the market value proportion of debt, simply multiply the price of the firm’s bonds by multiply the price of the firm’s bonds by the number outstanding. This is equal to the total market value of the firm’s debt.

Brealey, Myers & Marcus (2004:324)

The cost of capital must be based on what

investors are actually willing to pay for

the company’s outstanding securities –

that is, based on the securities’ market that is, based on the securities’ market

values.

![[PPT]Akuakultur Indonesia dan Prospeknya - Blog Universitas ...blogs.unpad.ac.id/roffigrandiosa/files/2011/12/... · Web viewPotensiAkuakulturdalamProduksiBahan Baku IndustriFarmasi,](https://static.fdocuments.net/doc/165x107/5b2721317f8b9aca6f8b47e1/pptakuakultur-indonesia-dan-prospeknya-blog-universitas-blogsunpadacidroffigrandiosafiles201112.jpg)