Plastic Packaging Bags & Films by 21st Century Packaging, New Delhi

15, March, 2016

Cosmo Films

“Going from strenght to strenght”

Initiating Coverage Cosmo Films Ltd.

2 | P a g e

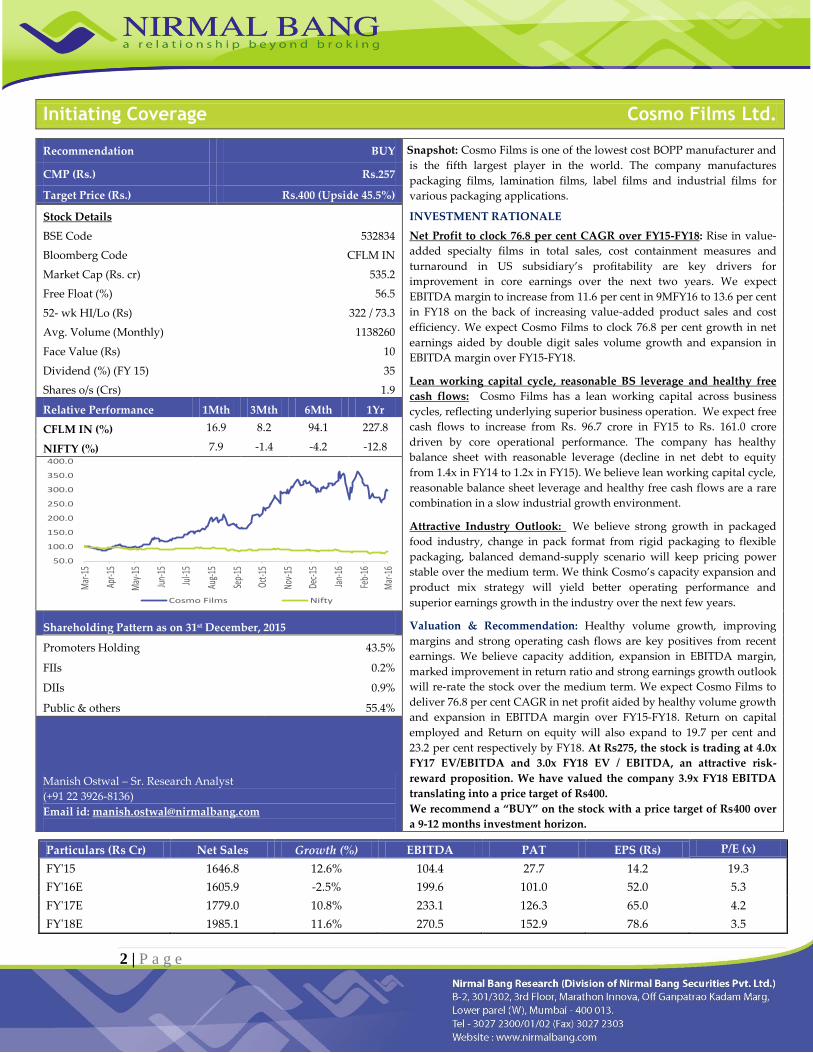

Recommendation BUY

Snapshot: Cosmo Films is one of the lowest cost BOPP manufacturer and

is the fifth largest player in the world. The company manufactures

packaging films, lamination films, label films and industrial films for

various packaging applications.

INVESTMENT RATIONALE

Net Profit to clock 76.8 per cent CAGR over FY15-FY18: Rise in value-

added specialty films in total sales, cost containment measures and

turnaround in US subsidiary’s profitability are key drivers for

improvement in core earnings over the next two years. We expect

EBITDA margin to increase from 11.6 per cent in 9MFY16 to 13.6 per cent

in FY18 on the back of increasing value-added product sales and cost

efficiency. We expect Cosmo Films to clock 76.8 per cent growth in net

earnings aided by double digit sales volume growth and expansion in

EBITDA margin over FY15-FY18.

Lean working capital cycle, reasonable BS leverage and healthy free

cash flows: Cosmo Films has a lean working capital across business

cycles, reflecting underlying superior business operation. We expect free

cash flows to increase from Rs. 96.7 crore in FY15 to Rs. 161.0 crore

driven by core operational performance. The company has healthy

balance sheet with reasonable leverage (decline in net debt to equity

from 1.4x in FY14 to 1.2x in FY15). We believe lean working capital cycle,

reasonable balance sheet leverage and healthy free cash flows are a rare

combination in a slow industrial growth environment.

Attractive Industry Outlook: We believe strong growth in packaged

food industry, change in pack format from rigid packaging to flexible

packaging, balanced demand-supply scenario will keep pricing power

stable over the medium term. We think Cosmo’s capacity expansion and

product mix strategy will yield better operating performance and

superior earnings growth in the industry over the next few years.

Valuation & Recommendation: Healthy volume growth, improving

margins and strong operating cash flows are key positives from recent

earnings. We believe capacity addition, expansion in EBITDA margin,

marked improvement in return ratio and strong earnings growth outlook

will re-rate the stock over the medium term. We expect Cosmo Films to

deliver 76.8 per cent CAGR in net profit aided by healthy volume growth

and expansion in EBITDA margin over FY15-FY18. Return on capital

employed and Return on equity will also expand to 19.7 per cent and

23.2 per cent respectively by FY18. At Rs275, the stock is trading at 4.0x

FY17 EV/EBITDA and 3.0x FY18 EV / EBITDA, an attractive risk-

reward proposition. We have valued the company 3.9x FY18 EBITDA

translating into a price target of Rs400.

We recommend a “BUY” on the stock with a price target of Rs400 over

a 9-12 months investment horizon.

CMP (Rs.) Rs.257

Target Price (Rs.) Rs.400 (Upside 45.5%)

Stock Details

BSE Code

Bloomberg Code

Market Cap (Rs. cr)

Free Float (%)

52- wk HI/Lo (Rs)

Avg. Volume (Monthly)

Face Value (Rs)

Dividend (%) (FY 15)

Shares o/s (Crs)

532834

CFLM IN

535.2

56.5

322 / 73.3

1138260

10

35

1.9

Relative Performance 1Mth 3Mth 6Mth 1Yr

CFLM IN (%) 16.9 8.2 94.1 227.8

NIFTY (%) 7.9 -1.4 -4.2 -12.8

Shareholding Pattern as on 31st December, 2015

Promoters Holding 43.5%

FIIs 0.2%

DIIs 0.9%

Public & others 55.4%

Manish Ostwal – Sr. Research Analyst

(+91 22 3926-8136)

Email id: [email protected]

50.0

100.0

150.0

200.0

250.0

300.0

350.0

400.0

Mar

-15

Apr-1

5

May

-15

Jun-

15

Jul-1

5

Aug-

15

Sep-

15

Oct-1

5

Nov-

15

Dec-

15

Jan-

16

Feb-

16

Mar

-16

Cosmo Films Nifty

Particulars (Rs Cr) Net Sales Growth (%) EBITDA PAT EPS (Rs) P/E (x)

FY'15 1646.8 12.6% 104.4 27.7 14.2 19.3

FY'16E 1605.9 -2.5% 199.6 101.0 52.0 5.3

FY'17E 1779.0 10.8% 233.1 126.3 65.0 4.2

FY'18E 1985.1 11.6% 270.5 152.9 78.6 3.5

Initiating Coverage Cosmo Films Ltd.

3 | P a g e

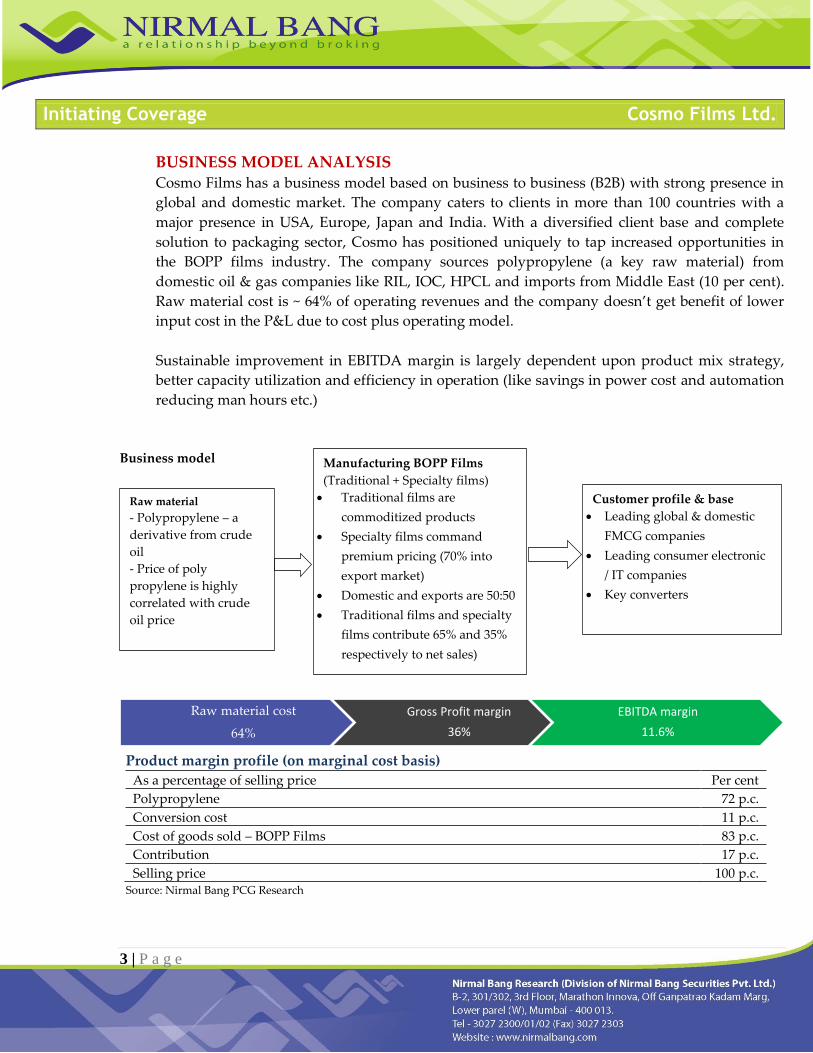

BUSINESS MODEL ANALYSIS Cosmo Films has a business model based on business to business (B2B) with strong presence in

global and domestic market. The company caters to clients in more than 100 countries with a

major presence in USA, Europe, Japan and India. With a diversified client base and complete

solution to packaging sector, Cosmo has positioned uniquely to tap increased opportunities in

the BOPP films industry. The company sources polypropylene (a key raw material) from

domestic oil & gas companies like RIL, IOC, HPCL and imports from Middle East (10 per cent).

Raw material cost is ~ 64% of operating revenues and the company doesn’t get benefit of lower

input cost in the P&L due to cost plus operating model.

Sustainable improvement in EBITDA margin is largely dependent upon product mix strategy,

better capacity utilization and efficiency in operation (like savings in power cost and automation

reducing man hours etc.)

Business model

Product margin profile (on marginal cost basis)

As a percentage of selling price Per cent

Polypropylene 72 p.c.

Conversion cost 11 p.c.

Cost of goods sold – BOPP Films 83 p.c.

Contribution 17 p.c.

Selling price 100 p.c. Source: Nirmal Bang PCG Research

Raw material cost

64%

Gross Profit margin

36%

EBITDA margin

11.6%

Manufacturing BOPP Films

(Traditional + Specialty films)

Traditional films are

commoditized products

Specialty films command

premium pricing (70% into

export market)

Domestic and exports are 50:50

Traditional films and specialty

films contribute 65% and 35%

respectively to net sales)

Customer profile & base

Leading global & domestic

FMCG companies

Leading consumer electronic

/ IT companies

Key converters

Raw material

- Polypropylene – a

derivative from crude

oil

- Price of poly

propylene is highly

correlated with crude

oil price

Initiating Coverage Cosmo Films Ltd.

4 | P a g e

INVESTMENT RATIONALE

Net Profit to clock 76.8 per cent CAGR over FY15-FY18

Cosmo Films has returned to high profitability and healthy volume zone with better demand –

supply equation in the BOPP films industry. The company posted very strong core operating

performance with 22 per cent growth in gross profit and 105 per cent growth in EBITDA during

9MFY16. Increasing contribution from high-margin specialty films in total sales, savings in

power cost (around Rs15 crore) and turnaround in US subsidiary’s profitability are key drivers

for improvement in profitability. We expect specialty films contribution in total sales to increase

from current 35 per cent to ~ 45 per cent by March, 2018. In terms of volume growth, we expect

sales volume to grow ~10 per cent CAGR over FY16-FY18.

We believe upgradation of existing facilities, capacity expansion (60,000 MT, taking total

capacity 1,96,000 MT), sales mix tilt with specialty films, US subsidiary’s improving profitability

and operational efficiency measures will drive EBITDA margin expansion and net profit growth

over FY16-FY18. We expect EBITDA margin to increase from 11.6 per cent in 9MFY16 to 13.6 per

cent in FY18 on the back of increasing value-added product sales and cost efficiency.

We expect Cosmo Films to clock 76.8 per cent growth in net earnings aided by double digit

volume growth and expansion in EBITDA margin over FY15-FY18.

Strong Profitability (FY15-FY18) Rs. crore Volume to grow 10% over FY15-FY18

Source: Company, Nirmal Bang PCG Research

104.4

199.6

233.1

270.5

27.7

101.0

126.3

152.9

0.0

50.0

100.0

150.0

200.0

250.0

300.0

FY15 FY16E FY17E FY18E

EBITDA PAT

11.1%

9.0%

11.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

FY16E FY17E FY18E

Initiating Coverage Cosmo Films Ltd.

5 | P a g e

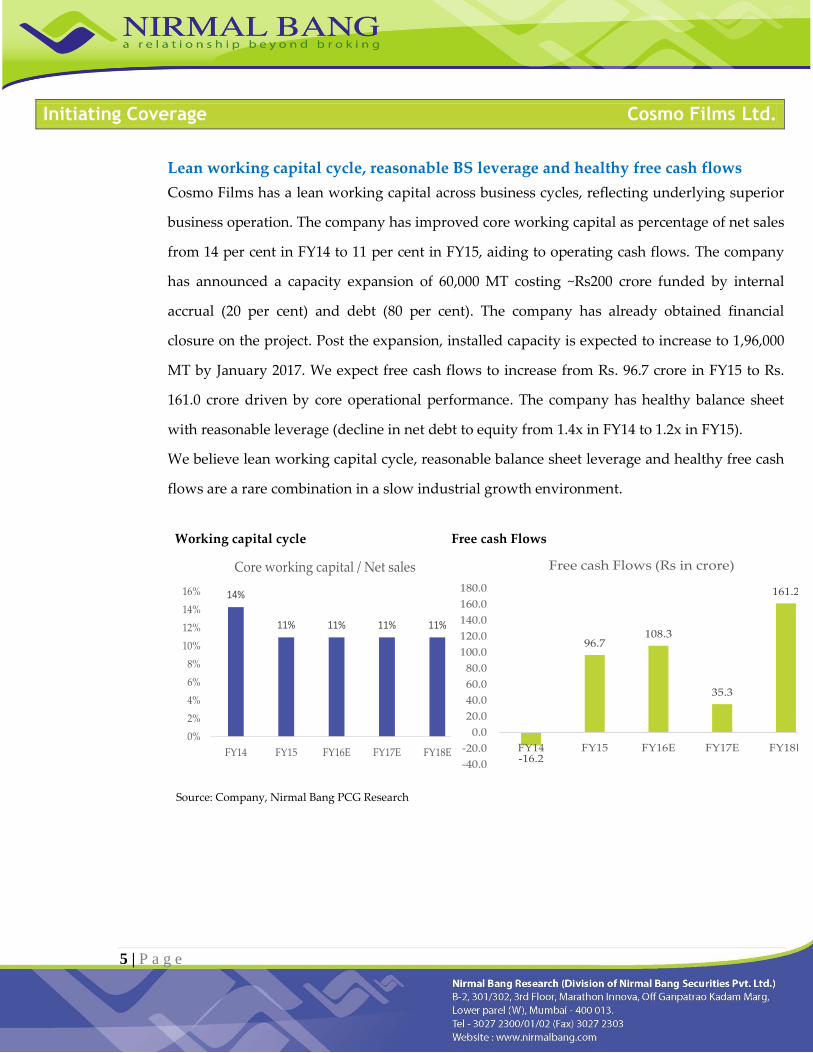

Lean working capital cycle, reasonable BS leverage and healthy free cash flows

Cosmo Films has a lean working capital across business cycles, reflecting underlying superior

business operation. The company has improved core working capital as percentage of net sales

from 14 per cent in FY14 to 11 per cent in FY15, aiding to operating cash flows. The company

has announced a capacity expansion of 60,000 MT costing ~Rs200 crore funded by internal

accrual (20 per cent) and debt (80 per cent). The company has already obtained financial

closure on the project. Post the expansion, installed capacity is expected to increase to 1,96,000

MT by January 2017. We expect free cash flows to increase from Rs. 96.7 crore in FY15 to Rs.

161.0 crore driven by core operational performance. The company has healthy balance sheet

with reasonable leverage (decline in net debt to equity from 1.4x in FY14 to 1.2x in FY15).

We believe lean working capital cycle, reasonable balance sheet leverage and healthy free cash

flows are a rare combination in a slow industrial growth environment.

Working capital cycle Free cash Flows

Source: Company, Nirmal Bang PCG Research

14%

11% 11% 11% 11%

0%

2%

4%

6%

8%

10%

12%

14%

16%

FY14 FY15 FY16E FY17E FY18E

Core working capital / Net sales

-16.2

96.7108.3

35.3

161.2

-40.0

-20.0

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

180.0

FY14 FY15 FY16E FY17E FY18E

Free cash Flows (Rs in crore)

Initiating Coverage Cosmo Films Ltd.

6 | P a g e

Attractive Industry Outlook

Global BOPP demand is estimated to be ~ 72 lakh MT growing 5-6% annually with

balanced demand-supply situation. Domestic BOPP Films industry has grown 12 per

cent CAGR aided by strong growth in flexible packaging industry over the last five

years.

During FY12-13, the industry saw sharp decline in profitability due to intense pricing

pressure and significant over-capacity leading to lower utilization. Cosmo Films and

other players in the industry also witnessed steep decline in gross profit margin and

EBITDA margin during the same period.

Now, pricing, profitability and demand-supply trends have reversed in FY15-FY16. At

present India’s BOPP production is estimated at approx. 5 lakh MT per annum.

Domestic BOPP consumption is approx. 3.5 lakh MT per annum and export from India

is about 1.1 lakh MT per annum. The Indian BOPP Industry has been growing at

almost double of India’s GDP growth rate. Current demand-supply scenario coupled

with capacity utilization shows reasonable stable trend on pricing power front. In

order to benefit from attractive industry outlook, Jindal Poly and Cosmo Films are

expanding BOPP capacity over the next two years by 30000 MT and 60000 MT

respectively.

We believe strong growth in packaged food industry, change in pack format from rigid

packaging to flexible packaging, balanced demand-supply scenario will keep pricing

power stable over the medium term. We think Cosmo’s capacity expansion and

product mix strategy will yield better operating performance and superior earnings

growth in the industry.

Initiating Coverage Cosmo Films Ltd.

7 | P a g e

Operational efficiency, turnaround in US subsidiary and tax benefits from SEZ

Cosmo Films is also working towards operational efficiency by cost-containment

measures. The company will save power cost around Rs. 15 crore and Rs. 25 crore in

FY16 and FY17 respectively due to change in power procurement from State grid to

long-term power purchase agreement (PPA) from private players and lower power

consumption. Upgradation of manufacturing facilities will increase automation in

plant operation and reduce power consumption per unit of production. We believe

that power cost-saving / automation measures along with efficient raw material

procurement make Cosmo Films the lowest cost BOPP film manufacture in the world.

Moreover, refinancing of existing loans at lower rates will reduce interest cost in

coming years. The company has net debt of Rs. 390 crs, of which Rs. 220 crore are

foreign currency loans with natural hedge in the form of exports revenues and

financial hedge.

The company’s US subsidiary is also witnessing operational improvement on the back

of new products launches, increased sales force, plugged wastage and acting as a

warehouse for products manufactured in India. We believe positive earnings from US

subsidiary will aid consolidated net profit growth over FY16-FY18. Notably, there was

negative contribution of the US subsidiary amounting to Rs25.3 crore at normalized

consolidated PAT level during 2014-15.

Cosmo Films’s Shendra plant (dedicated to export business) will claim tax exemption

from FY15-16 onwards, dropping overall effective tax rate to 22-23 per cent. The

company is entitled to claim 100 per cent profit exemption for first five years and 50

per cent profit exemption for another five years on export business from its notified

SEZ.

Initiating Coverage Cosmo Films Ltd.

8 | P a g e

We believe cost-containment measures, turnaround in US subsidiary operation and

lower tax rate will also support net profit growth over the next two years.

Sustained entry barrier in specialty films and no threat from China

Cosmo Films enjoys significant entry barriers in specialty films segment. The company

has built unique small size production lines for specialty films to offer customized and

innovative product for premium consumer products. Notably, specialized films are

selling 2.5x premium to traditional BOPP films, a key profitability driver over the long

term.

The company is one of the lowest cost manufacturer of BOPP films in the world. The

difference between manufacturing BOPP films in India and China is very minimal.

Moreover, import duty of 7.5 per cent along with freight cost attached to imported

films makes import an unattractive option for domestic BOPP end-user industries.

Hence, BOPP films imported from China will not adversely impact pricing power and

supply scenario in domestic market.

Competitors

Major competitors are Jindal Poly (210000 MT), Max Films (54000 MT), Nahar Poly

(30000 MT), Taghleef UAE (410000 MT) and Terofan (132000 MT). We believe full-

fledged BOPP films product portfolio, lowest cost of production and diversified client

base are key strengths to sustain profitability and improve market share.

Initiating Coverage Cosmo Films Ltd.

9 | P a g e

RISKS & CONCERNS

Sharp volatility in raw material price Sharp fluctuation in polypropylene price may result in volatility in EBITDA margin and the

company might see inventory losses. Notably, raw material cost stands at ~ 64 per cent of net

sales.

Delay in expansion plan

Cosmo Films is expanding its capacity by 60000 MT. New capacity will start

commercial production from April 2017. Any delay in new capacity may affect net

sales and earnings growth in FY18.

Initiating Coverage Cosmo Films Ltd.

10 | P a g e

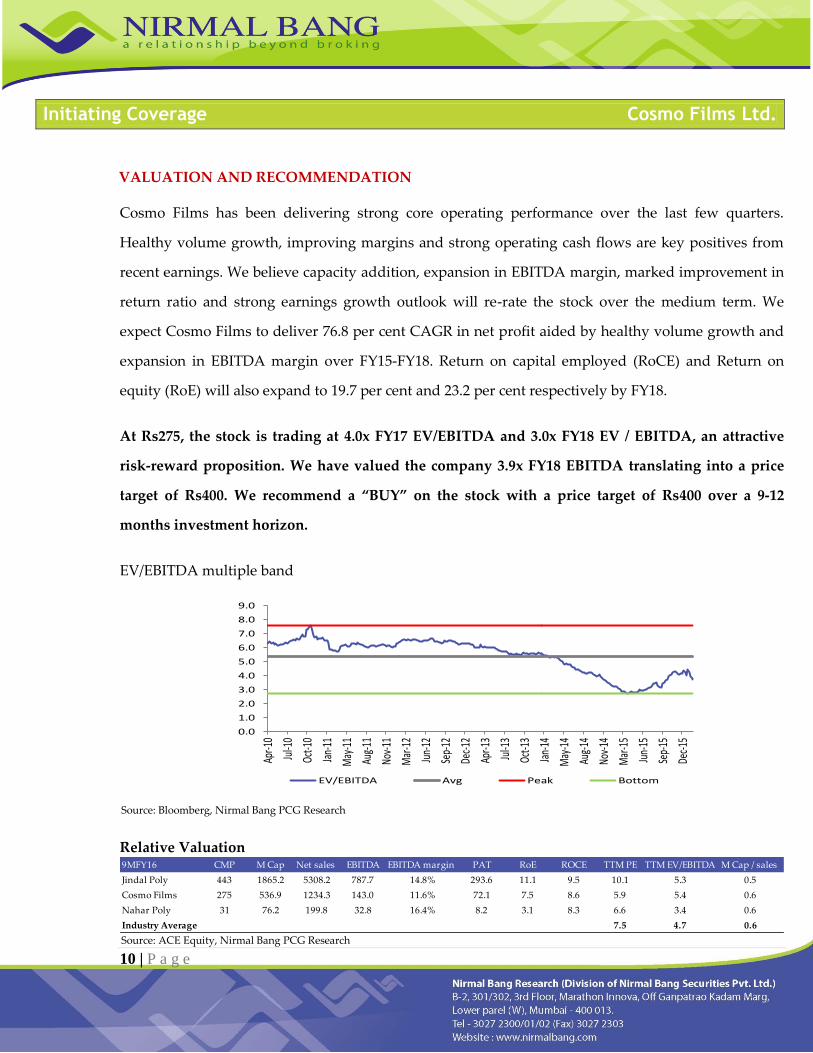

VALUATION AND RECOMMENDATION

Cosmo Films has been delivering strong core operating performance over the last few quarters.

Healthy volume growth, improving margins and strong operating cash flows are key positives from

recent earnings. We believe capacity addition, expansion in EBITDA margin, marked improvement in

return ratio and strong earnings growth outlook will re-rate the stock over the medium term. We

expect Cosmo Films to deliver 76.8 per cent CAGR in net profit aided by healthy volume growth and

expansion in EBITDA margin over FY15-FY18. Return on capital employed (RoCE) and Return on

equity (RoE) will also expand to 19.7 per cent and 23.2 per cent respectively by FY18.

At Rs275, the stock is trading at 4.0x FY17 EV/EBITDA and 3.0x FY18 EV / EBITDA, an attractive

risk-reward proposition. We have valued the company 3.9x FY18 EBITDA translating into a price

target of Rs400. We recommend a “BUY” on the stock with a price target of Rs400 over a 9-12

months investment horizon.

EV/EBITDA multiple band

Source: Bloomberg, Nirmal Bang PCG Research

Relative Valuation

Source: ACE Equity, Nirmal Bang PCG Research

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

Apr-1

0

Jul-1

0

Oct-1

0

Jan-

11

May

-11

Aug-

11

Nov-

11

Mar

-12

Jun-

12

Sep-

12

Dec-

12

Apr-1

3

Jul-1

3

Oct-1

3

Jan-

14

May

-14

Aug-

14

Nov-

14

Mar

-15

Jun-

15

Sep-

15

Dec-

15

EV/EBITDA Avg Peak Bottom

9MFY16 CMP M Cap Net sales EBITDA EBITDA margin PAT RoE ROCE TTM PE TTM EV/EBITDA M Cap / sales

Jindal Poly 443 1865.2 5308.2 787.7 14.8% 293.6 11.1 9.5 10.1 5.3 0.5

Cosmo Films 275 536.9 1234.3 143.0 11.6% 72.1 7.5 8.6 5.9 5.4 0.6

Nahar Poly 31 76.2 199.8 32.8 16.4% 8.2 3.1 8.3 6.6 3.4 0.6

Industry Average 7.5 4.7 0.6

Initiating Coverage Cosmo Films Ltd.

11 | P a g e

COMPANY BACKGROUND

Cosmo Flims is a leading manufacturer of BOPP films and specialty films with ~ 20 per cent market

share. The company offers cost-effective innovative packaging solutions to leading FMCG and

global brands. Over the years, the company expanded product portfolio to improve profitability and

growth. Its products include newer products like thermal, coating and metalizing films besides the

traditional BOPP films. The company has three manufacturing facilities in India and one each in

Korea and USA. It caters to clients in more than 100 countries with major presence in USA, Europe,

Japan and India. The company derives 50 per cent sales from export market and balance 50 per cent

from domestic market. Out of export sales, 70 per cent is value-added high margin specialty films.

The company reported sharp improvement in profitability with 105 per cent Y-o-Y growth in

EBITDA in 9MFY16. Healthy volume growth, improving EBITDA margin and strong net earnings

growth are key trends from 9MFY16 result.

Product Portfolio

S No

Brief detail

1 Packaging Films Print and pouching films, Barrier films and Overwrap films

2

Lamination

Films Dry lamination and Wet lamination

3 Label Films

Pressure sensitive label films, direct thermal printable films, in-mould films and

Wrap around label films

4 Industrial Films Synthetic paper and Tape and textile films

Manufacturing facilities Location BOPP Thermal Coating Metalizing

Waluj, Aurangabad, India 5 Lines 2 Lines 2 Lines 1 Line

Karjan, Vododara, India 2 Lines 2 Lines 2 Lines 1 Line

Shendra, Aurangabad, India 1 Lines 3 Lines 1 Line 1 Line

Korea, Choongnam 1 Line

USA, Hagerstown 1 Line

Total Installed capacity 136000 40000 TPA 10000 TPA 15000 TPA

Source: Company

Initiating Coverage Cosmo Films Ltd.

12 | P a g e

Growth and Profitability

Rs in crore Standalone Consolidated

FY14 FY15 9MFY15 FY14 FY15 9MFY16

Net sales 1256.7 1478.7 1130.1 1468.4 1646.8 1091.1

EBITDA 103.6 122.4 78.0 108.7 104.4 146.0

PAT 8.1 40.4 22.1 -5.5 27.7 79.4

Normalized PAT 28.6 49.6 31.5 23.2 24.3 84.1

Source: Company

Management Team

S. No. Name Profile

1 Mr. Ashok Jaipuria,

Chairman & Managing Director

Founder Chairman & Managing Director has more

than 40 years of experience of the Corporate World.

He is a Member of the Executive Committee of the

FICCI, president of the Golf Foundation, a member of

the Board of Governors of IIT- Patna and among the

Board of Directors of DPS, Gurgaon.

2 Mr. Pankaj Poddar,

Chief Executive Officer

Mr Pankaj Poddar’s career spans over a period of 20

years in finance, advisory, assurance and various

leadership as well as management roles. Before joining

Cosmo, Pankaj has worked with automotive & FMCG

industries. His last stint was with Avon Beauty

products as “Director Finance”. Pankaj has also

worked as the India CFO for Delphi Automotive

Systems, Regional Head Assurance Services for Reckitt

Benckiser and Manager Advisory & Assurance

Services in Ernst & Young.

3 Mr. Neeraj Jain,

Chief Financial Officer

Mr. Neeraj has over 16 years of experience in finance,

business planning and strategy, taxation and risk

management. Neeraj is with the Cosmo Films from

March 2013 and has worked with Havells, Aditya Birla

Group and Bajaj Allianz before joining Cosmo Films.

4 Mr. Satish Subramanian,

Vice President - Global Sales &

Marketing

Mr. Satish has over 20 years of sales experience in B2B

& B2C and has expertise in Global Account

Management, Business Development, Multi-Channel

Sales, Solution Selling, Strategy Development, Retail

Supply Chain, Product Management and P&L

Management.

Source: Company presentation

Initiating Coverage Cosmo Films Ltd.

13 | P a g e

Financials

Rs in crore FY14 FY15 FY16E FY17E FY18E

Income Statement

Net sales 1468.4 1646.8 1605.9 1779.0 1985.1

EBIDTA 108.7 104.4 199.6 233.1 270.5

Other income 6.8 5.0 5.5 8.0 18.0

Depreciation 45.3 34.5 35.6 41.0 50.0

EBIT 70.1 74.8 169.5 200.1 238.5

Interest expense 43.2 39.9 32.5 35.0 38.7

Profit before tax -1.8 38.2 132.9 165.1 199.8

Tax expense 3.7 10.6 31.9 38.8 47.0

PAT -5.5 27.7 101.0 126.3 152.9

Normalised PAT 23.2 24.3 105.1 126.3 152.9

Balance sheet

Equity share capital 19.4 19.4 19.4 19.4 19.4

Reserve & Surplus 340.5 361.2 452.9 568.7 709.9

Networth 360.0 380.6 472.3 588.1 729.3

Debt 586.9 489.8 439.8 559.8 544.8

Other non-current liabilities 51.6 57.2 57.2 57.2 57.2

Current liabilities 152.3 148.3 145.3 158.1 173.2

Total 1150.8 1075.9 1114.6 1363.1 1504.4

Fixed assets 638.6 609.5 633.9 732.9 722.9

Other non-current assets 36.1 57.0 57.0 57.0 57.0

Inventories 202.4 179.5 175.4 194.4 216.7

Trade receivables 138.3 122.0 118.4 131.2 146.3

Cash and bank balances 54.1 18.3 40.2 158.1 271.9

Short term loans and advances 49.4 56.5 56.5 56.5 56.5

Other current assets 31.9 33.1 33.1 33.1 33.1

Total 1150.8 1075.9 1114.6 1363.1 1504.4

Cash Flow Statement

Operating cash flow 59.3 134.1 168.3 175.3 201.2

CAPEX -75.5 -37.4 -60.0 -140.0 -40.0

Free cash flow -16.2 96.7 108.3 35.3 161.2

Cash flow from investing -71.8 -42.6 -54.5 -132.0 -22.0

Cash flow from financing 19.4 -121.3 -91.9 74.5 -65.3

Change in cash 7.0 -29.8 21.9 117.9 113.8

Opening balance 47.2 48.2 18.3 40.2 158.1

Closing balance 54.1 18.3 40.2 158.1 271.9

Initiating Coverage Cosmo Films Ltd.

14 | P a g e

Source: Nirmal Bang PCG Research

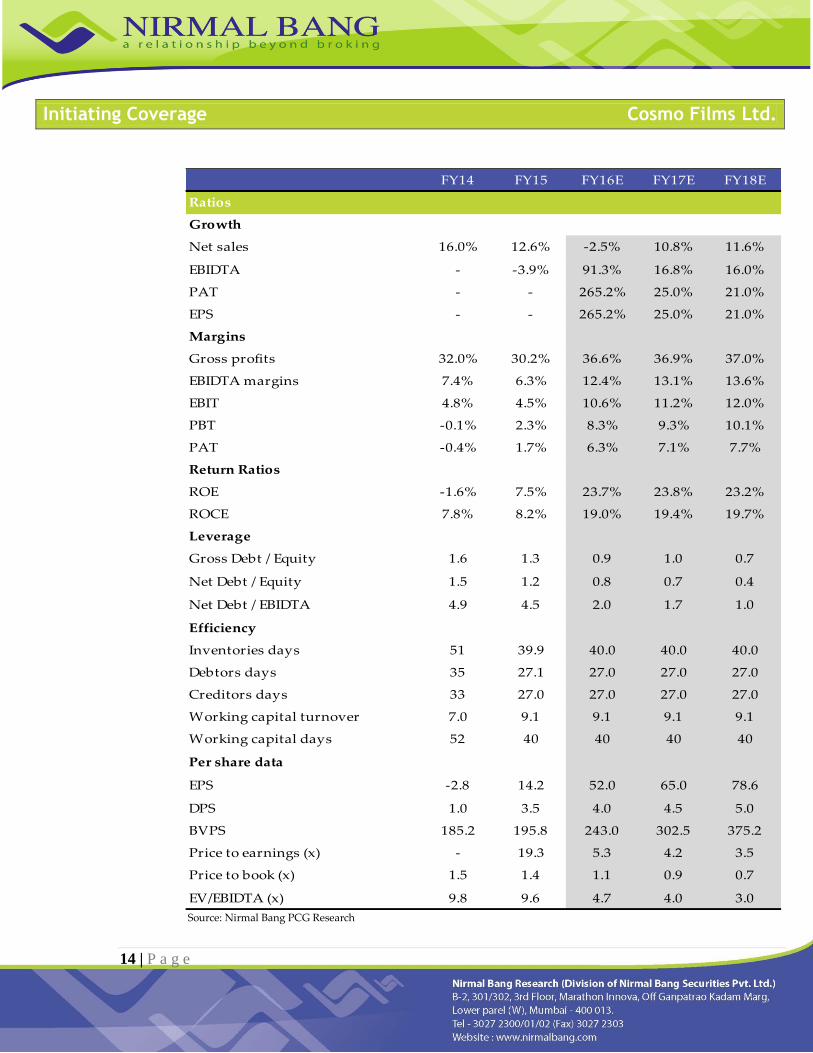

FY14 FY15 FY16E FY17E FY18E

Ratios

Growth

Net sales 16.0% 12.6% -2.5% 10.8% 11.6%

EBIDTA - -3.9% 91.3% 16.8% 16.0%

PAT - - 265.2% 25.0% 21.0%

EPS - - 265.2% 25.0% 21.0%

Margins

Gross profits 32.0% 30.2% 36.6% 36.9% 37.0%

EBIDTA margins 7.4% 6.3% 12.4% 13.1% 13.6%

EBIT 4.8% 4.5% 10.6% 11.2% 12.0%

PBT -0.1% 2.3% 8.3% 9.3% 10.1%

PAT -0.4% 1.7% 6.3% 7.1% 7.7%

Return Ratios

ROE -1.6% 7.5% 23.7% 23.8% 23.2%

ROCE 7.8% 8.2% 19.0% 19.4% 19.7%

Leverage

Gross Debt / Equity 1.6 1.3 0.9 1.0 0.7

Net Debt / Equity 1.5 1.2 0.8 0.7 0.4

Net Debt / EBIDTA 4.9 4.5 2.0 1.7 1.0

Efficiency

Inventories days 51 39.9 40.0 40.0 40.0

Debtors days 35 27.1 27.0 27.0 27.0

Creditors days 33 27.0 27.0 27.0 27.0

Working capital turnover 7.0 9.1 9.1 9.1 9.1

Working capital days 52 40 40 40 40

Per share data

EPS -2.8 14.2 52.0 65.0 78.6

DPS 1.0 3.5 4.0 4.5 5.0

BVPS 185.2 195.8 243.0 302.5 375.2

Price to earnings (x) - 19.3 5.3 4.2 3.5

Price to book (x) 1.5 1.4 1.1 0.9 0.7

EV/EBIDTA (x) 9.8 9.6 4.7 4.0 3.0

Initiating Coverage Cosmo Films Ltd.

15 | P a g e

Disclaimer

Nirmal Bang Securities Private Limited (hereinafter referred to as “NBSPL”)is a registered Member of National Stock

Exchange of India Limited, Bombay Stock Exchange Limited and MCX stock Exchange Limited. We have been granted

certificate of Registration as a Research Analyst with SEBI, Registration no. is INH000001766 for the period 23.09.2015 to

22.09.2020.

NBSPL or its associates including its relatives/analyst do not hold any financial interest/beneficial ownership of more than 1%

in the company covered by Analyst.

NBSPL or its associates/analyst has not received any compensation from the company covered by Analyst during the past

twelve months.

NBSPL /analyst has not served as an officer, director or employee of company covered by Analyst and has not been engaged

in market making activity of the company covered by Analyst.

The views expressed are based solely on information available publicly and believed to be true. Investors are advised to

independently evaluate the market conditions/risks involved before making any investment decision.