Corporation Auditor Training March 2015 Office of Field Operations Kentucky Department of Revenue...

109

Corporation Auditor Training March 2015 Office of Field Operations Kentucky Department of Revenue Finance and Administration Cabinet

-

Upload

kimberly-janice-baldwin -

Category

Documents

-

view

213 -

download

0

Transcript of Corporation Auditor Training March 2015 Office of Field Operations Kentucky Department of Revenue...

Corporation Auditor Training

March 2015

Office of Field OperationsKentucky Department of Revenue

Finance and Administration Cabinet

Welcome

Marcia Ann Oakman,

Policy/Research Analyst

Don Richardson,

Tax Policy/Research Consultant

Overview

• Pre Audit

• Filing Status

• Federal/Kentucky Income Reconciliation

• Apportionment Factor

• Net Operating Loss (NOL)

• Credits

• LLET

• Narrative

Pre Audit Process

Assignment Tracking System (ATS)

• Review comments section for information from the Selection Officer

• Search to see if the taxpayer has had prior audits

• Search the old Audit Tracking System for prior audits and desk audit (old system available for view access only)

• Documents related to prior audits reviewed by the field can be found at: ..\..\..\..\Field Finalized Audit Documents\Audit

New ATS

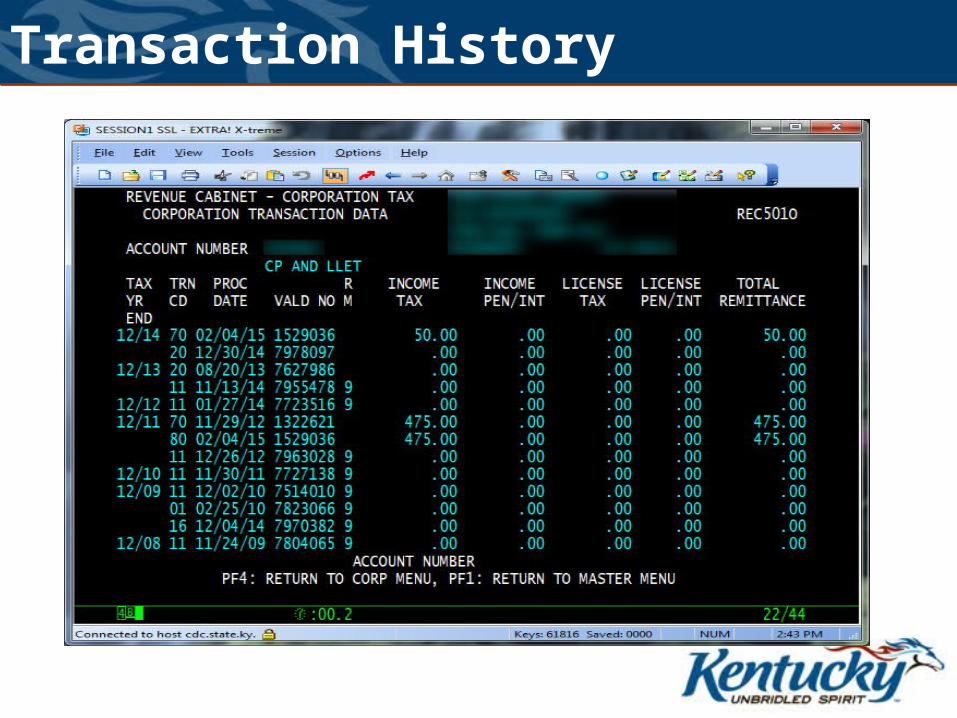

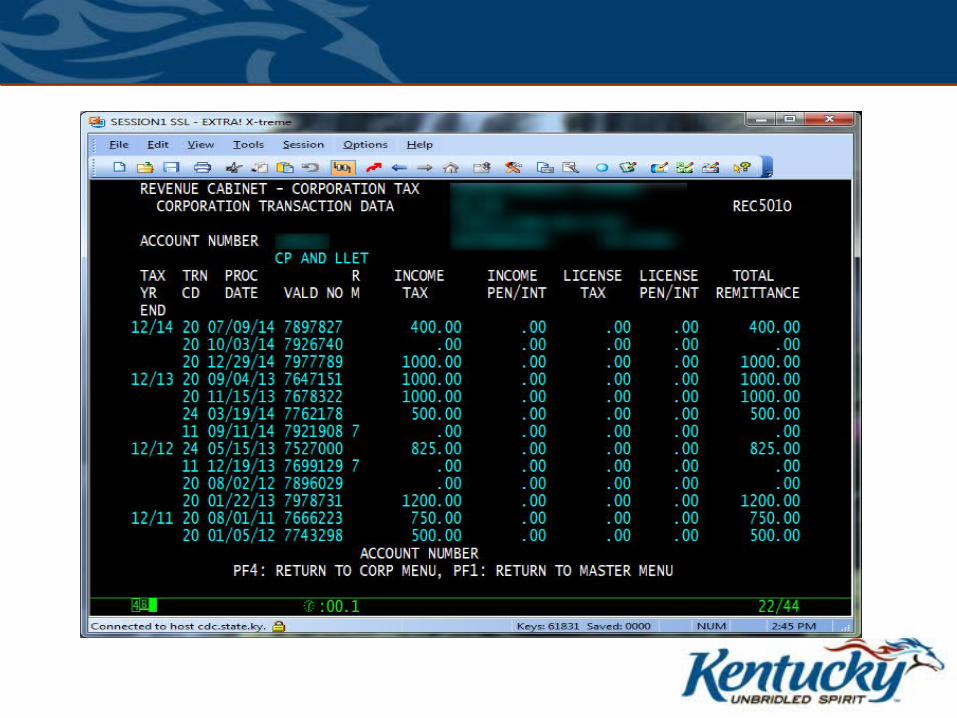

Corporate Database

Transaction History

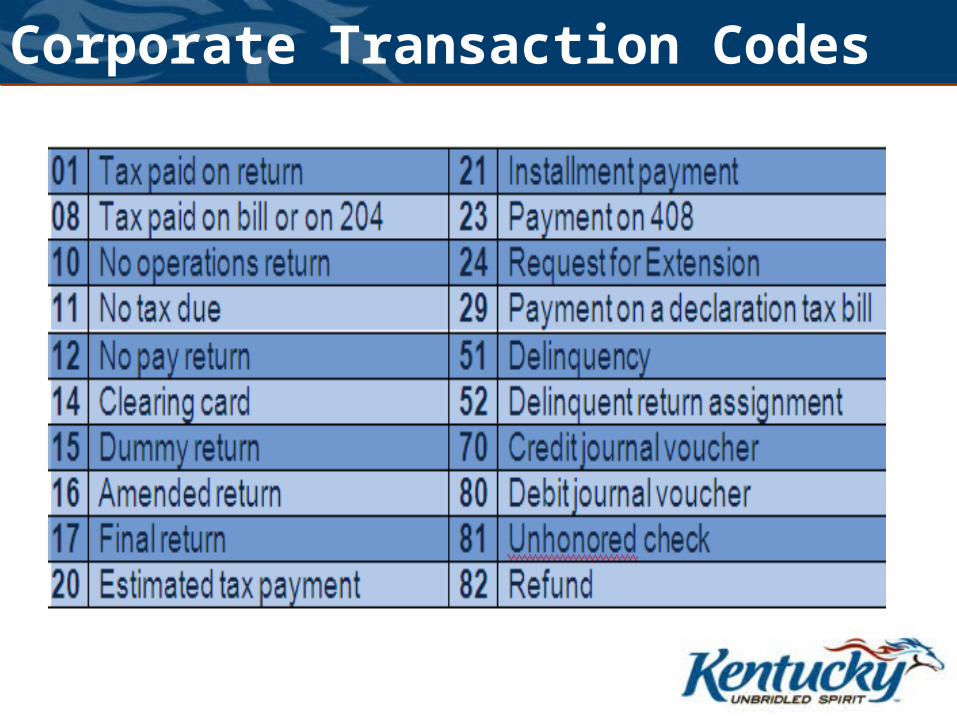

Corporate Transaction Codes

Consolidated Database

Consolidated Database

CARS

To access this screen click PF1 and then select menu item ‘A Billing Menu’.

Fastrieve

• Contains corporate returns and pass-through entity returns that may contain Kentucky K-1(s) needed in your audit.

• If the taxpayer provides forms that are not in Fastrieve, a note should be made for the form to be added.

• Results of the desk audit are uploaded to Fastrieve.• Additional Fastrieve information can be found at:

..\..\..\..\Common Folder\Training\Corporate 12_12\Fastrieve

Fastrieve Error Codes

Drop Down Resolution BoxesError Codes Error

ExplanationForm the

Error is onAmount of

Error

• Memorandum – Net Operating Loss and Statute of Limitations 10/01/2012

• Memorandum – Statute of Limitations – Amended Returns

• Memorandum – Interpretation of KRS 141.206(10)

Statute of Limitations – KRS 141.210

The statute date is the later of:• 4 years from the date the original return was filed • 4 years from extended due date OR• Date the return was filed.• 6 years if a corporation:

– understates net income or – omits an amount properly excludable in net income or– both is in excess of 25% of the amount of taxable net

income stated in the return, the additional tax may be assessed at any time within 6 years after the return was filed.

Waiver

• Waiver – agreement between the taxpayer and DOR.

• Note: if waiver is a date before SOL then DOR must go by the waiver date.

CATS (Corporate Audit Template System)

• New template for all corporate field audits starting Jan 2015

• Covers Tax Periods 2005 thru 2014• Different Templates for different types of

Taxpayers (e.g. 722 election, Separate, Mandatory Nexus)

• Launched thru ATS

Public Information

• Department of Library & Archives

• Annual Reports

• SEC Filings

• Corporate Directories

• Business Periodicals and Trade Journals

• Internet – Company’s Website

Information Request

• Specific information needed will vary

• Generally requested items:– General ledgers– Corporate minutes– Work papers used to compile the state

adjustments and apportionment factor– Chart of accounts– Forms 940 or 941– Federal Revenue Agent’s Reports

Initial Taxpayer Discussion

• Familiarization with Tax Department– Establish work environment– Designate contact – Discuss turnaround times– Location and accessibility of records– Qualifications of return preparers– Number and duties of tax department personnel– Status protests – Federal audit activity

Initial Taxpayer Discussion

• Nature of Business, Products, Kentucky Operations– Expand on statements from 10-Ks or annual

reports– Ask questions to clarify assumptions from pre

audit research

Initial Taxpayer Discussion

• Accounting Procedures and Controls– Accounting system– Automated in regard to apportionment factor– Are accounts and procedures standardized

throughout organization– One or more auditing firms– Review instructions for preparing the returns and

correspondence with accounting department

Filing Status

FILING IN KENTUCKY

Tax Periods 1993 to 2004– Separate– 722 Election

Tax Periods 2005 to 2011– Separate– 722 Election – election had to be made by January 1, 2005– Mandatory Nexus

Tax Periods 2012 and Forward– Separate– Mandatory Nexus

Consolidated Database

Mandatory NexusA multi-tiered group of affiliated corporations that are doing business in Kentucky can file a nexus consolidated return provided:

1. All the includible corporations, including the common parent corporation of the multiple-tiered structure have nexus (doing business) in Kentucky;

2. All the includible corporations except for the common parent corporation are directly owned by 80% or more by one or more of the other includible corporations in the group;

3. The common parent directly owns 80% or more of at least one other of the includible corporations in the group.

If the chain or chains of corporations are broken by a member not having nexus in this state or a member not being directly owned by 80% or more by another member, then it is possible for there to be more than one nexus consolidated group within a group of related corporations.

KRS 141.200

"Includible corporation" means any corporation that is doing business in this state except:

1. Corporations exempt from corporation income tax under KRS 141.040(1)(a) to (i);

2. Foreign corporations; ("Foreign corporation" means a corporation that is organized under the laws of a country other than the United States and is related to a member of an affiliated group through stock ownership)

3. Corporations with respect to which an election under Section 936 of the Internal Revenue Code is in effect for the taxable year;

4. Real estate investment trusts as defined in Section 856 of the Internal Revenue Code;

5. Regulated investment companies as defined in Section 851 of the Internal Revenue Code;

6. A domestic international sales company as defined in Section 992(a)(1) of the Internal Revenue Code;

7. Any corporation that realizes a net operating loss whose Kentucky property, payroll, and sales factors pursuant to KRS 141.120(8) are de minimis;

8. Any corporation for which the sum of the property, payroll and sales factors described in KRS 141.120(8) is zero; and

9. For taxable years beginning prior to January 1, 2006, and taxable years beginning on or after January 1, 2007, an S corporation as defined in Section 1361(a) of the Internal Revenue Code;

Nexus Standard per KRS 141.010(25)

KRS 141.010 (25) Doing business in this state” includes but is not limited to:

a) Being organized under the laws of this state;

b) Having a commercial domicile in this state;

c) Owning or leasing property in this state;

d) Having one or more individuals performing services in this state;

e) Maintaining an interest in a pass-through entity doing business in this state;

f) Deriving income from or attributable to sources within this state, including deriving income directly or indirectly from a trust doing business in this state, or deriving income directly or indirectly from a single member limited liability company that is doing business in this state and is disregarded as an entity separate from its single member for federal income tax purposes; or

g) Directing activities at Kentucky customers for the purpose of selling them goods or services.

Schedule A-N

Public Law 86-272• Public Law 86-272 prevents a state from imposing an income tax on income

derived within the state from interstate commerce if the only business activity within the state is the solicitation of orders for tangible personal property, provided that the orders are approved and filled outside the state.

• For Kentucky, Public Law 86-272 is considered when determining whether a corporation’s activity is “protected” or “unprotected” from state income tax. If a corporation performs some of the protected activities listed in Kentucky and also conducts activities in this state that are not protected under the provisions of public law 86-272, then the Commonwealth has the right to tax that corporation’s income.

• Public Law 86-272 does not prevent the taxpayer from filing and paying LLET tax with a minimum of $175. (KRS 141.0401)

To look up protected and unprotected activities go to:

http://www.krew.ky.gov, click on training and then Consolidated Tax Returns Manual (starts on pg 8).

Regulation 103 KAR 16:240“Doing business” is further explained in 103 KAR 16:240. This regulation defines terminology and also sets forth protected and unprotected activities under Public Law 86-272.

1. “Doing Business: does not include an activity that is protected or exempt from state income taxation under provisions of the United States Constitution or Public Law 86-272. Public Law 86-272 prohibits a state from imposing its income tax on a foreign corporation whose only activity in the state is the solicitation of sales of tangible personal property if the sales orders are approved outside the state and are filled by shipment or delivery from a point outside of Kentucky.

2. “Deriving income” includes performing services in Kentucky, whether directly by the corporation or indirectly by directing activity performed by a third party.

3. “Doing business” includes being the single member of a single member LLC that is disregarded for federal income tax purposes.

4. “Doing business” includes entering into franchising or licensing agreements and receiving income from franchising or licensing agreements that have acquired a Kentucky business situs.

5. “Doing business” also includes being the parent of a qualified real estate investment trust subsidiary or qualified subchapter S subsidiary that is doing business in Kentucky.

Filing Status

• Page 1 Check Box

• Page 2 or 3 Schedule Q

• CR/KCR Worksheets

• Federal Form 851

• Organizational Charts

• Public Law 86-272– Nexus Questionnaire (LLET Tax)

http://www.revenue.ky.gov/business/register.htm

720

720 Schedule Q

Federal Form 851

Purpose of form

1. Identify the common parent corporation and each member of the affiliated group.

2. Determine that each subsidiary corporation qualifies as a member of the affiliated group.

Federal Form 851 – Part I

Federal Form 851 – Part II

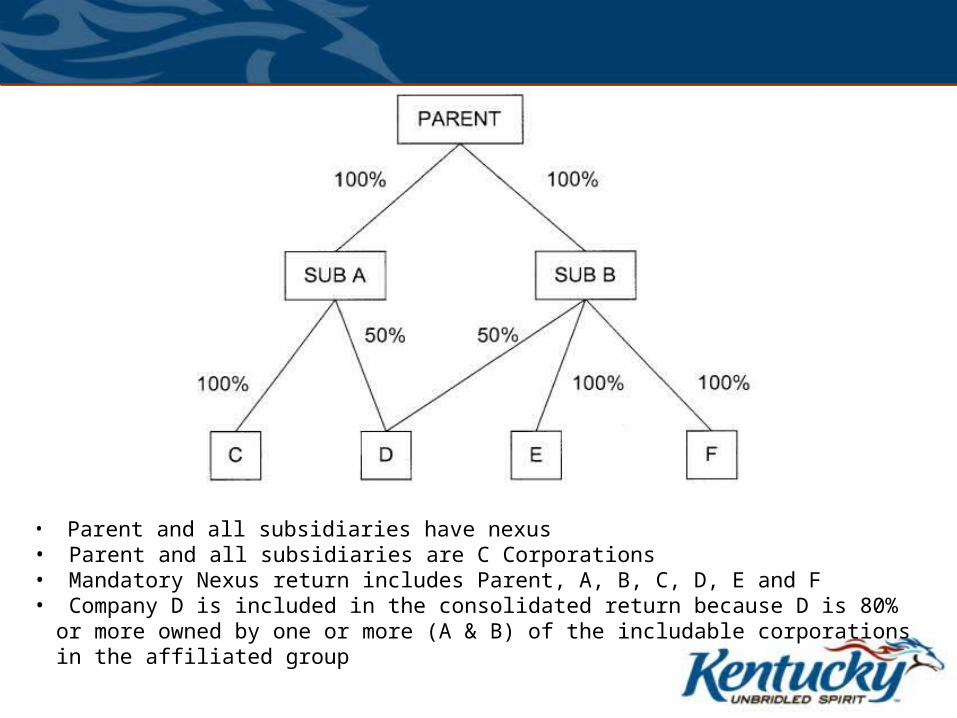

• Parent and all subsidiaries have nexus• Parent and all subsidiaries are C Corporations• Mandatory Nexus return includes Parent, A, B, C, D, E and F• Company D is included in the consolidated return because D is 80% or more owned by one

or more (A & B) of the includable corporations in the affiliated group

• All companies are C Corporations that have Nexus in Kentucky• Company A cannot be included in the consolidated return because the parent does not

own 80% or more of Company A• The parent, B, D & E will form one mandatory nexus consolidated group• Companies A & C form another mandatory nexus consolidated group, with Company A

being the common parent company

• Valid for tax years 2007 and forward• Assume that the C Corporation and all LLCs have Kentucky Nexus• C Corp and LLC1 will be included in mandatory nexus return• LLC2 and LLC3 will file separate returns

• Parent and all subsidiaries are C Corporations• Parent B, C and E can file a mandatory nexus consolidated return• Company D has to file a separate entity return• Company A does not have to file a Kentucky return

Key Points - Mandatory Nexus • Only includes companies with Kentucky nexus

• NOL is applied pre-apportionment

• Companies included in the group have to be owned by an 80 percent plus share by their parent

• Prior year NOL carried into the mandatory nexus group should always be verified (make sure pre-apportioned amounts used)

• Theoretically the last line of the KCR for each company should match the amounts entered on the Schedule NOL columns A and B

• The TOTAL column of the KCR should match the 720 exactly

• Common error: company may omit entering all of the amounts onto the KCR which in turn causes the numbers carried over to the Schedule NOL to be incorrect.

• The sum of all the losses and income on the SCH NOL (sum of line 3) should equal the net income before apportionment on the 720 (2012 Form 720, Part III Line 18)

• Every Mandatory Nexus return should include a Schedule KCR and Schedule CR, and Schedule NOL.

Net Income Adjustments

Net Income

• Start with Federal taxable income• Add back:

– Items taxed by Kentucky and not by Federal– State taxes not deductible for Kentucky– RAR’s resulting in additional federal taxable income– Related expenses– IRC Section 172 deduction (NOL)

• Deduct:– Items taxed by Federal but not Kentucky– RAR’s resulting in additional expenses or nontaxable income– Wages taken as direct tax credit under Jobs –Work Opportunity Tax

Credit on federal return

• Make necessary adjustments if consolidation of subsidiaries and parent involved

Line 1 – Federal Taxable Income

• Should equal the amount on the Federal Form 1120 Line 28

or

• The amount on Line 28 of the Schedule CR

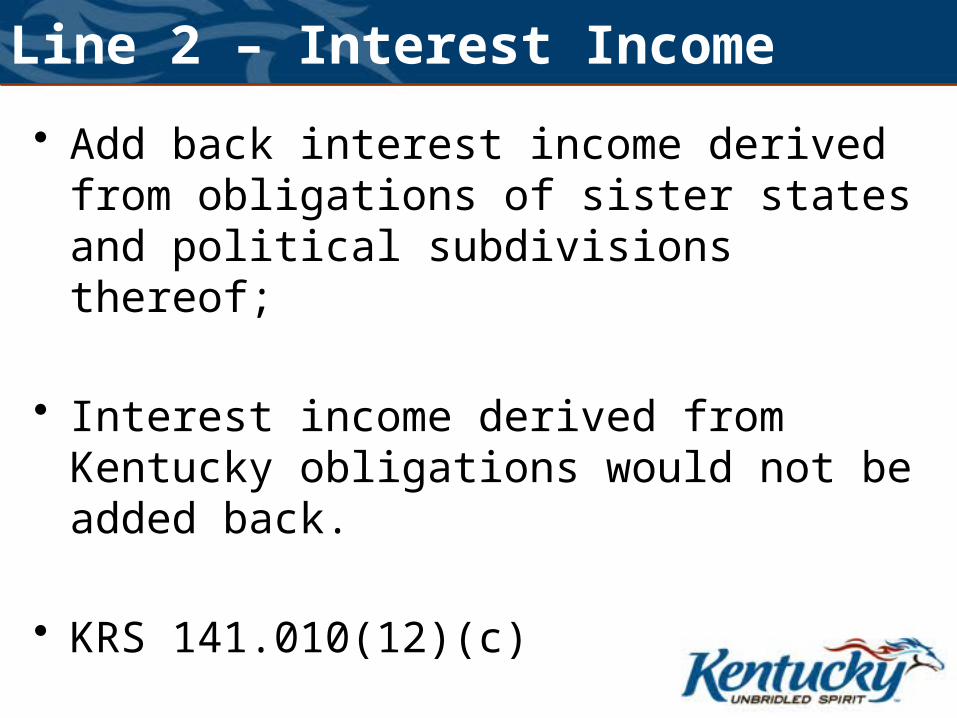

Line 2 – Interest Income

• Add back interest income derived from obligations of sister states and political subdivisions thereof;

• Interest income derived from Kentucky obligations would not be added back.

• KRS 141.010(12)(c)

Line 3 – State Taxes

• Kentucky statute does not allow deductions for state taxes computed in whole or in part, by reference to gross or net income.

Line 4 - Depreciation

• If the corporation has not taken the 30 percent special depreciation allowance, the 50 percent special depreciation allowance or the increased Section 179 deduction for federal income tax purposes on any assets for which a depreciation deduction is being claimed for the taxable year, then no adjustment will be needed for Kentucky income tax purposes. If federal Form 4562 is required to be filed for income tax purposes, a copy must be submitted with Form 720 to verify that no adjustments are required.

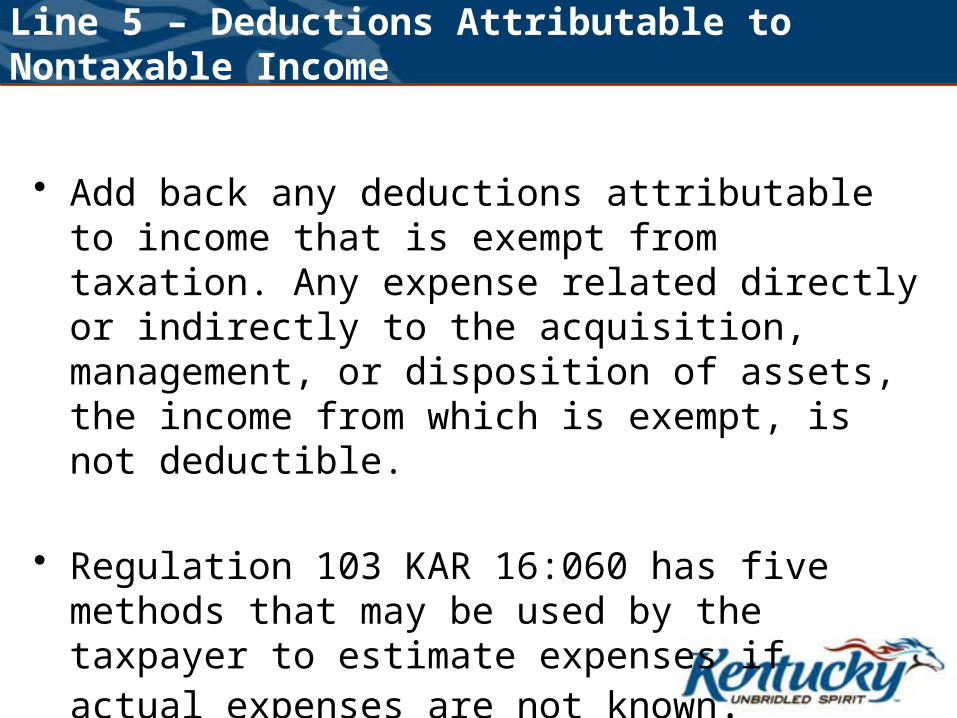

Line 5 – Deductions Attributable to Nontaxable Income

• Add back any deductions attributable to income that is exempt from taxation. Any expense related directly or indirectly to the acquisition, management, or disposition of assets, the income from which is exempt, is not deductible.

• Regulation 103 KAR 16:060 has five methods that may be used by the taxpayer to estimate expenses if actual expenses are not known.

Line 5 – Deduction Attributable to Nontaxable Income

Line 5 – Deductions Attributable to Nontaxable Income - example

Line 5 - Deductions Attributable to Nontaxable Income - solution

Line 6 – Related Party Expenses

• Enter intangible expenses, intangible interest expense, management fees and other related party expenses directly or indirectly paid, accrued or incurred to, or in connection directly or indirectly with one or more direct or indirect transactions with one or more related members of an affiliated group or with a foreign corporation.

• KRS 141.205 and Regulation 103 KAR 16:230

Line 7 – Dividend Paid Deduction

• Add back any dividend paid deduction of a captive real estate investment trust. (REIT)

• KRS 141.010(13)(h)

Line 8 – Domestic Production Activities Deduction

• Enter the amount of domestic production activities deduction from Form 1120 Line 25

• Federal Form 8903 is the source document for this deduction.

• Regulation 103 KAR 16:310

Line 9 – Other

• Before 2009 – Taxpayer should have attached a schedule showing details of other additions.

• After 2009 - Enter the amount from Schedule O-720, Part 1, Line 12.

• Usually includes Federal charitable contributions, Federal 4797 losses, Kentucky 4797 gains, safe harbor lease adjustments, Kentucky capital gains from Kentucky Schedule D, etc.

Line 10 - RAR

• Adjustments from Revenue Agent’s Report following a Federal Audit.

• Usually these adjustments are found on amended returns.

Line 12 – Interest Income

• Interest income from U.S. government bonds or from securities issued by a federal agency or other income exempt from state taxation by the Kentucky Constitution, the U.S. Constitution or the U.S. Code. Securities which are merely guaranteed by the U.S. government are not tax exempt.

• KRS 141.010(12)(a)

Line 13 – Dividend Income

• Dividend income from Form 1120, line 4

or

• Schedule CR Form 720, line 4

Line 14 – Federal Work Opportunity

• Should equal the amount found on the Federal Form 5884.

• For Kentucky purposes, the corporation may deduct the total amount of salary or wages incurred for the taxable year.

• This adjustment does not apply for other federal tax credits.

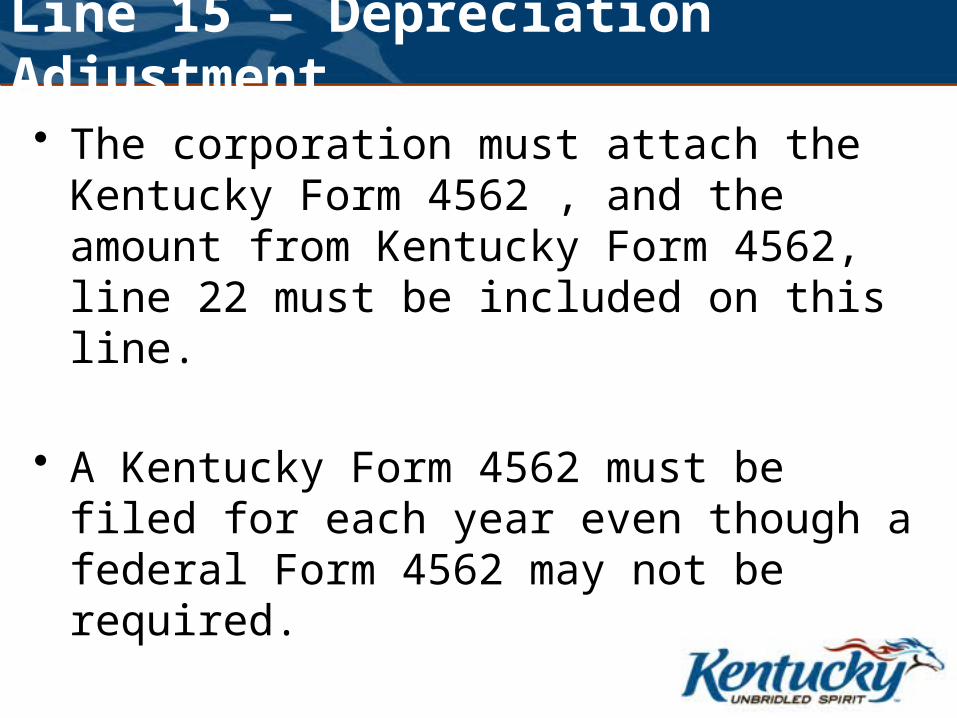

Line 15 – Depreciation Adjustment

• The corporation must attach the Kentucky Form 4562 , and the amount from Kentucky Form 4562, line 22 must be included on this line.

• A Kentucky Form 4562 must be filed for each year even though a federal Form 4562 may not be required.

Line 16 – Other Deductions

• Before 2009 – Taxpayer should have attached a schedule showing details of other subtractions.

• After 2009 - Enter the amount from Schedule O-720, Part 1, Line 17.

• Usually includes Kentucky charitable contributions, Federal 4797 gains , Kentucky 4797 losses, safe harbor lease adjustments, Federal capital gains from Form 1120, line 8, etc.

Line 17 - RAR

• Adjustments from Revenue Agent’s Report following a Federal Audit.

• Usually these adjustments are found on amended returns.

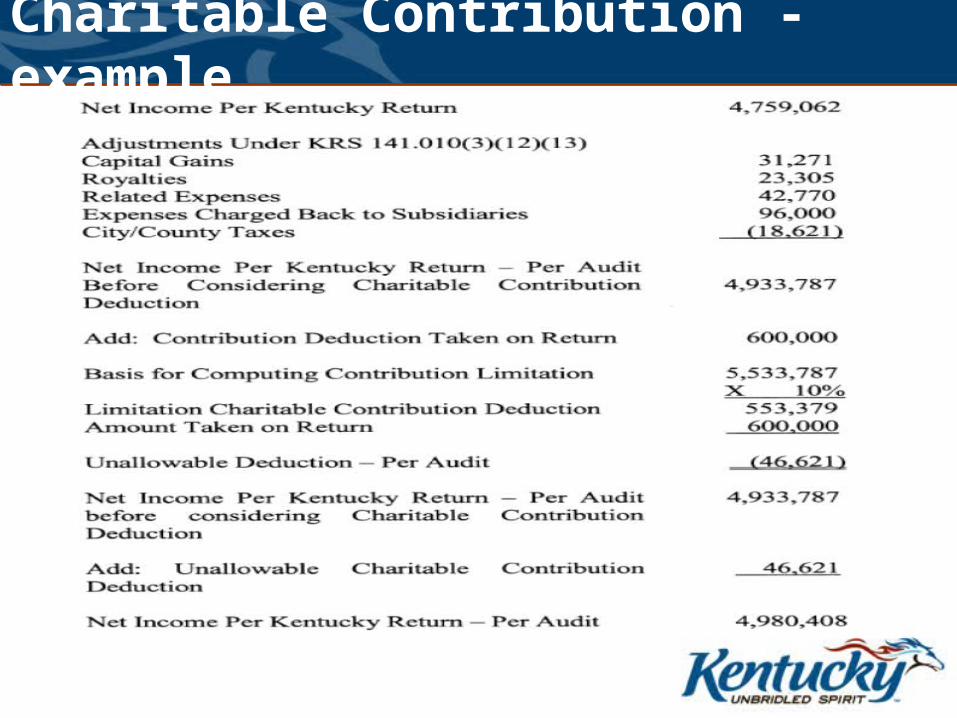

Charitable Contributions

• Limited to 10% of Kentucky net income

• Carryover to 5 succeeding tax years– Also subject to 10% limitation

• Current year contribution takes precedent over carryover

Charitable Contribution - example

Apportionment Factor

Schedule A

Schedule A-C

Payroll Factor 103 KAR 16:090

Compensation is paid or payable in this state if:

1) The individual’s service is performed entirely within the state,

2) The individual service is performed within and without the state, but the service performed without the state is incidental to the individual’s service within the state,

3) Some of the service is performed in the state and the base of operations or, if there is no base of operations, the place from which the service is directed or controlled in this state, or the base of operations or the place from which the service is directed or controlled is not in any state in which some part of the service is performed, but the individual’s residence is in this state.

Compensation shall not include payments to an independent contractor or any other person not property classified as an employee.

Only amounts paid directly to employees shall be included in the payroll factor.**

Payroll Factor

• Review 103 KAR 16:090

• Payroll information to compute payroll factor– Kentucky Unemployment returns (UI-3’s)– Federal Unemployment returns (Form 940)

and/or federal withholding/social security forms (Form 941)

– Actual payroll records– Compare payroll records with payroll that has

been assigned to Kentucky and total

Payroll Factor

• Payroll information to compute payroll factor– Discuss methodology in assigning payroll– Investigate possibility of:

• Foreign wages • Allocated payroll• Employees working for other entities

– Exclude payroll of employees generating nonbusiness/nontaxable income/loss

– Payroll factor can be verified against federal and state unemployment returns (large variations should be questioned)

Property Factor• KRS141.120(8)(b) and 103 KAR 16:290

• Information to verify property factor– Annual report and 10-K– Original cost of tangible property at beginning

and end of year (balance sheet)– Include fully depreciated tangible property– Types of property

• Inventories• Buildings• Machinery & Equipment• Other Tangible Property

Property Factor

• Inventories in transit are assigned to state of designation

• Exclude construction in progress and idle property

• Exclude tangible property producing nonbusiness/nontaxable income/loss

• Add leased property times eight (8)

• Discuss methodology in assigning moveable property

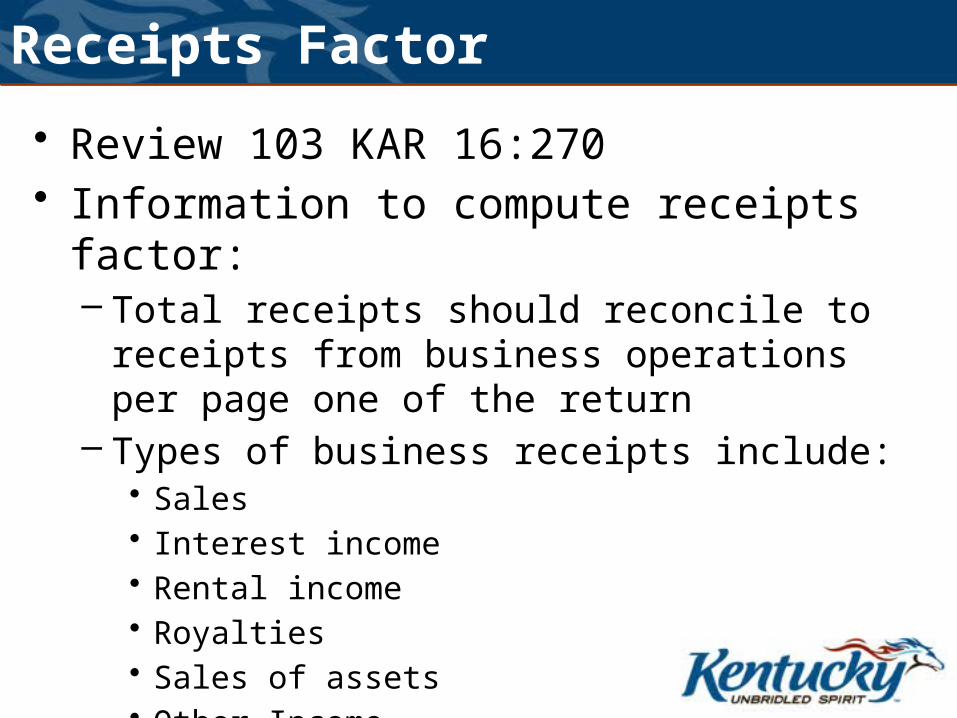

Receipts Factor

• Review 103 KAR 16:270• Information to compute receipts factor:

– Total receipts should reconcile to receipts from business operations per page one of the return

– Types of business receipts include:• Sales• Interest income• Rental income• Royalties• Sales of assets• Other Income

Receipts Factor

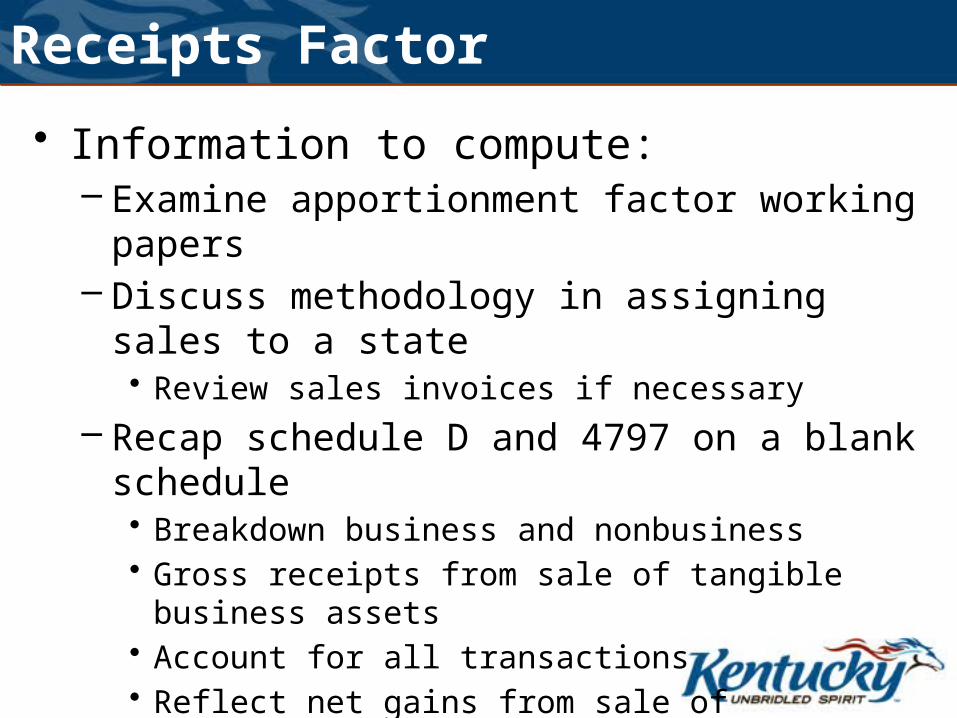

• Information to compute:– Examine apportionment factor working papers– Discuss methodology in assigning sales to a

state• Review sales invoices if necessary

– Recap schedule D and 4797 on a blank schedule• Breakdown business and nonbusiness• Gross receipts from sale of tangible business assets• Account for all transactions• Reflect net gains from sale of intangible business

assets (not losses)

Receipts Factor

• Factor is double weighted

• Negative receipts should not be reflected in factor

• Exclude intercompany transactions

Receipts Factor – 103 KAR 16:___

103 KAR 16:100 Apportionment and allocation; telephone and telegraph companies

103 KAR 16:110 Apportionment and allocation; pipeline companies

103 KAR 16:120 Apportionment and allocation; trucklines, buslines, airlines

103 KAR 16:130 Apportionment and allocation; railroad companies

103 KAR 16:145 Apportionment and allocation; barge line companies

103 KAR 16:150 Apportionment and allocation; financial organizations & loan companies

103 KAR 16:270 Apportionment; sales factor

Net Operating Loss

Net Operating Loss (NOL)

Kentucky

Tax Year Beginning Carryback Carryforward

On/before 8/5/97 3 15

After 8/5/97, but before 1/1/2000 2 20

After 8/5/97, but before 1/1/2000 (Farm Loss)

2 20

On/after 1/2/2000, but before 1/1/2005 2 20

On/after 1/2/2000, but before 1/1/2005 – Farm Loss

5 20

1/1/2005 – forward 0 20

NOL• Net Operating Loss (NOL) – Section 172 (c) of the Internal Revenue Code

defines a net operating loss as the excess of the deductions allowed by Chapter 1 of the Internal Revenue Code over the gross income. The excess shall be computed with the modifications specified in subsection (d) of Section 172 of the Internal Revenue Code.

• Federal and Kentucky Differences – KRS 141.011 provides (i) The net operating loss may differ because of the provisions of KRS Chapter 141 (primarily KRS 141.010; (ii) The net operating loss carry-back deduction shall not be allowed for losses incurred for taxable years beginning on or after January 1, 2005; (iii) For taxable years when the tax due under KRS 141.040 is based on the alternative minimum calculation provided in KRS 141.040, the net operating loss carry-forward deduction that is utilized for the taxable year shall be the amount of taxable income before the net operating deduction, that exceeds the taxable net income equivalent; (iv) For taxable years beginning on or after January 1, 2005, and before December 31, 2006, the net operating loss carry-forward deduction of a corporation shall be reduced by the amount of distributive share income, and deduction distributed to an individual or general partnership as defined in KRS 141.206; and (v) The portion of net operating loss that is not used to offset the income of an affiliate according to the limits in KRS 141.200(11) shall be available for carry-forward, subject to the limitations contained in this section.

NOL• Kentucky Elective Consolidated Tax Return – The NOL of an affiliated group of

corporations filing a consolidated return under Sections 1501 and 1504(b) of the Internal Revenue Code would have only the following federal and Kentucky differences: (i) The net operating loss may differ because of the provisions of KRS Chapter 141 (primarily KRS 141.010); and (ii) The net operating loss carry-back deduction shall not be allowed for losses incurred for taxable years beginning on or after January 1, 2005.

• Kentucky Nexus Consolidated Tax Return – The NOL of an affiliated group of corporations filing a nexus consolidated return as provided by KRS 141.200(11) would have the following federal and Kentucky differences: (i) The net operating loss may differ because of the provisions of KRS Chapter 141 (primarily KRS 141.010); (ii) The net operating loss carry-back deduction shall not be allowed for losses incurred for taxable years beginning on or after January 1, 2005; (iii) For taxable years when the tax due under KRS 141.040 is based on the alternative minimum calculation provided in KRS 141.040, the net operating loss carry-forward deduction that is utilized for the taxable year shall be the amount of taxable income before the net operating deduction, that exceeds the taxable net income equivalent; (iv) For taxable years beginning on or after January 1, 2005, and before December 31, 2006, the net operating loss carry-forward deduction of a corporation shall be reduced by the amount of distributive share income, loss, and deduction distributed to an individual or general partnership as defined in KRS 141.206; and (v) The portion of net operating loss that is not used to offset the income of an affiliate according to the limits in KRS 141.200(11) shall be available for carry-forward, subject to the limitations contained in this section.

NOL

• Separate Return loss Year (SRLY) – A SRLY is generally defined as a tax year of a subsidiary in which the subsidiary was not a member of the consolidated group. The loss carryovers of a member arising (or treated as arising) in SRLYs are limited based on the contribution to consolidated taxable income of that member. This rule applies to the NOL of an affiliated group of corporations filing an elective consolidated return under Sections 1501 and 1504(b) of the Internal Revenue Code. However, the SRLY rules do not apply to NOL of an affiliated group of corporations filing a nexus consolidated return as provided by KRS 141.200(11).

• IRC Section 382 Limitation – In general, following an ownership change of more than 50% by one or more five-percent shareholders within a three-year period, the corporation’s NOLs incurred prior to the change of ownership can be utilized each year in an amount equal to the IRC Section 382 limitation. The IRC Section 382 limitation is equal to the fair market value of the loss corporation’s stock immediately before the ownership change multiplies by the federal long-term taxexempt rate. This rule applies to the NOL of an affiliated group of corporations filing an elective consolidated return under Section 1501 and 1504(b) of the Internal Revenue Code. However, the IRC Section 382 limitation does not apply to the NOL of an affiliated group of corporations filing a nexus consolidated return as provided by KRS 141.200(11).

NOL

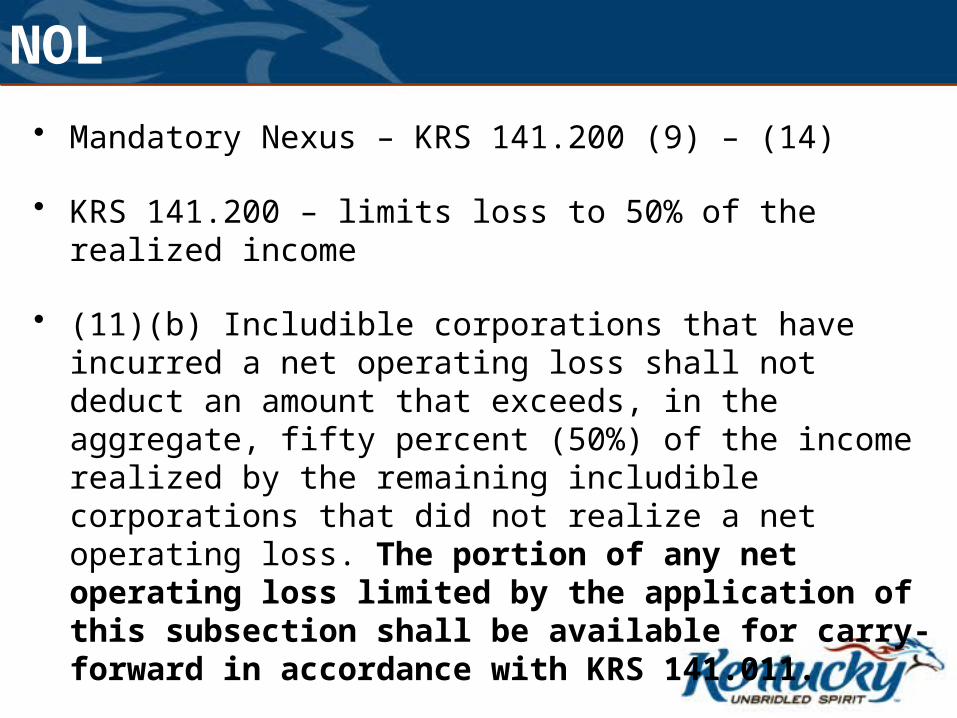

• Mandatory Nexus – KRS 141.200 (9) – (14)

• KRS 141.200 – limits loss to 50% of the realized income

• (11)(b) Includible corporations that have incurred a net operating loss shall not deduct an amount that exceeds, in the aggregate, fifty percent (50%) of the income realized by the remaining includible corporations that did not realize a net operating loss. The portion of any net operating loss limited by the application of this subsection shall be available for carry-forward in accordance with KRS 141.011.

• NOL Schedule – before apportionment

NOL EXAMPLE #1Corporation Newby filed its initial Kentucky separate entity return in 2005. After three years of operation, 80% of the corporation’s stock was purchased by Corporation ACB who also had nexus with the state of Kentucky and Newby was included in the return required to be filed by ABC pursuant to KRS 141.200.

(Income and loss figures reported below are after application of the apportionment factor)

YEAR Income Loss Apportionment Factor

2005 15,000 13%

2006 (12,000) 8%

2007 (20,000) 10%

1. How much of the 2007 loss can be carried back to offset the income earned in year 2005?

2. What type of return is required of Corporation ACB for tax year 2008?

3. What is the amount of loss that will be carried forward to the 2008 return from Corporation Newby?

4. What is the amount of NOL carry-forward available to Newby if the filing method for 2008 was elective consolidated?

NOL EXAMPLE #2The following table represents the income and losses reported by an elective consolidated

group after apportionment:

Year Corporation Income Loss Apportionment Factor

2008 Parent 100,000 25%

Number 1 (80,000)

Number 2 65,000

Number 3 (90,000)

Number 4 (30,000)

Total 165,000 (200,000) = (35,000)

1. What is the amount of NOL carry-forward that is available to Corporations 3 & 4 when they become members of a mandatory nexus filing in 2009?

2. Corporation 1 is required to file a separate entity return for tax year 2009. What is the available NOL carry-forward for this corporation?

NOL EVALUATION PROBLEM

2 HOUR Exercise

Credits

Tax Credits

• If no adjustments are made– Enter ‘per return’ amount in ‘per audit’ column

• Audit Review will verify credits with the Tax Credit Section

Common Mistakes

• Overstating debt service/approved costs on tracking schedules,

• Calculating tax credit on 100% of income instead of calculating credit on income from the project only,

• Not taking into account the wage assessments claimed when determining credit limitations,

• Continue to claim credits once project is paid off.

Some common mistakes made by companies with economic development projects are:

Who to Contact

Email or call the following people to get tax credits verified:

• Valerie Brock - (502) 564-7266 – KREDA, KJDA, KIDA, KIRA, KEOZ, KJRA, KRA, KESA,

and KBI

• Marion Parker - (502) 564-7253 – Recycling/Composting

• Regina Ritchey - (502) 564-7256 – all other tax credits

LLET

LLET• KRS 141.0401

– Applicable for tax years beginning on or after January 1, 2007 based on Kentucky gross receipts or Kentucky gross profits

– Minimum of $175– A nonrefundable credit based on the tax calculated less

$175 – Exempt organizations include (see KRS 141.0401(6) for

other exempt organizations):• Financial institutions• Savings and loan associations• Insurance company

– Not protected by Public Law 86-272

KRS 141.0401

“Kentucky gross receipts” means an amount equal to the computation of the numerator of the sales factor under the provisions of KRS 141.120(8)(c), KRS 141.120(9), any administrative regulations related to the computation of the sales factor, and KRS 141.121 and includes the proportionate share of Kentucky gross receipts of all wholly or partially owned limited liability pass-through entities, including all layers of a multi-layered pass-through structure.

“Gross receipts from all sources” means an amount equal to the computation of the denominator of the sales factor under the provisions KRS 141.120(8)(c), KRS 141.120(9), any administrative regulations related to the computation of the sales factor, and KRS 141.121 and includes the proportionate share of gross receipts from all sources of all wholly or partially owned limited liability pass-through entities, including all layers of a multi-layered pass-through structure.

KRS 141.0401 (cont.)

“Kentucky gross profits” means Kentucky gross receipts reduced by returns and allowances attributable to Kentucky gross receipts, less cost of goods sold attributable to Kentucky gross receipts. If the amount of returns and allowances attributable to Kentucky gross receipts and the cost of goods sold attributable to Kentucky gross receipts are zero, then “Kentucky gross profits” means Kentucky gross receipts.

“Gross profits from all sources” means gross receipts from all sources reduced by returns and allowances attributable to gross receipts from all sources, less cost of goods sold attributable to gross receipts from all sources. If the amount of returns and allowances attributable to gross receipts from all sources and the cost of goods sold attributable to gross receipts from all sources are zero, then gross profits from all sources means gross receipts from all sources.

Cost of Goods Sold

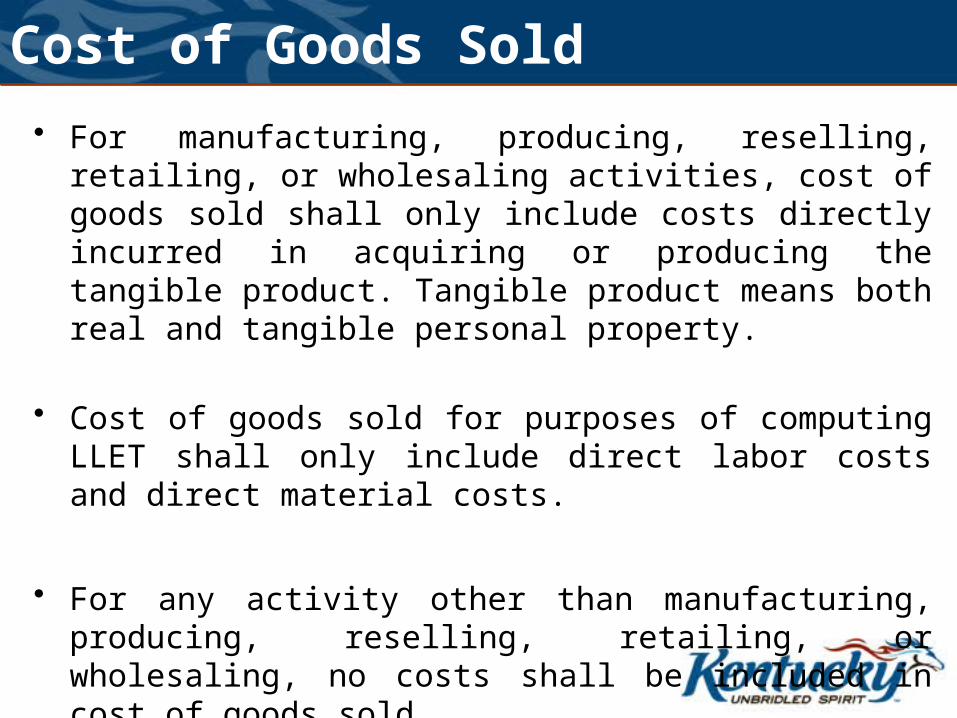

• For manufacturing, producing, reselling, retailing, or wholesaling activities, cost of goods sold shall only include costs directly incurred in acquiring or producing the tangible product. Tangible product means both real and tangible personal property.

• Cost of goods sold for purposes of computing LLET shall only include direct labor costs and direct material costs.

• For any activity other than manufacturing, producing, reselling, retailing, or wholesaling, no costs shall be included in cost of goods sold.

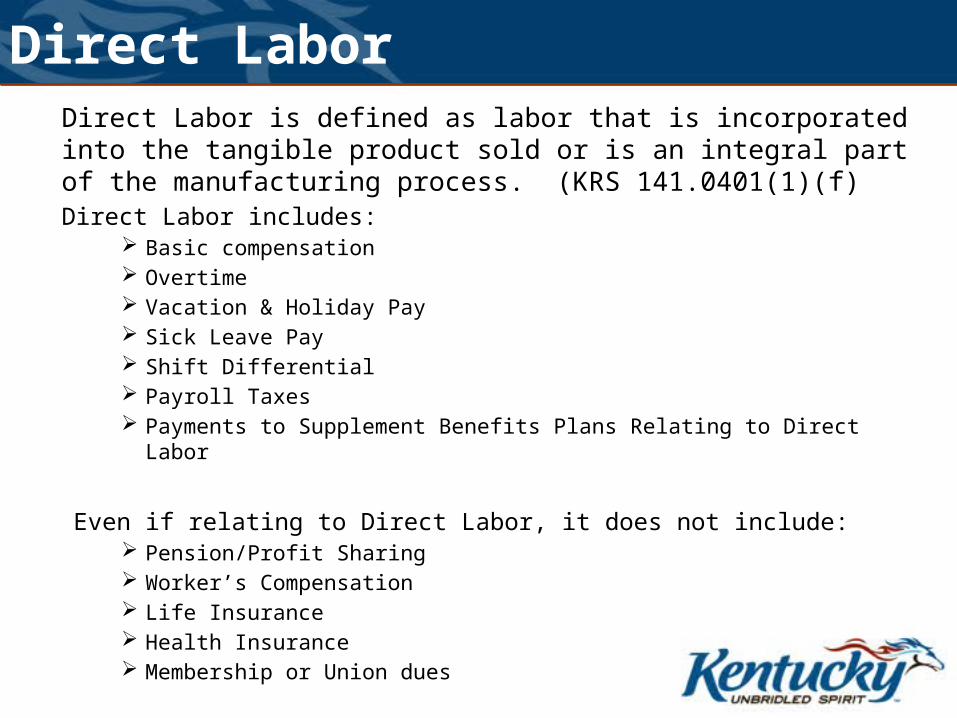

Direct LaborDirect Labor is defined as labor that is incorporated into the tangible product sold or is an integral part of the manufacturing process. (KRS 141.0401(1)(f)Direct Labor includes:

Basic compensation Overtime Vacation & Holiday Pay Sick Leave Pay Shift Differential Payroll Taxes Payments to Supplement Benefits Plans Relating to Direct Labor

Even if relating to Direct Labor, it does not include: Pension/Profit Sharing Worker’s Compensation Life Insurance Health Insurance Membership or Union dues

Direct Materials• Direct material means material that is incorporated into the tangible product sold

or manufactured. The test is whether it is direct or indirect, not whether the cost is necessary.

• For example, in IRC Section 263A, there are direct costs that are necessary for production and indirect costs that are necessary for production.

• Costs allowable under Section 263A of the Internal Revenue Code may be included only to the extent the costs are incurred in acquiring or producing the tangible product generating the Kentucky gross receipts.

• The following are examples of categories of costs that are not allowed in COGS for purposes of computing LLET and are typically listed as indirect costs pursuant to IRC Section 263A:– Utilities– Repairs and Maintenance– Depreciation– Insurance– Quality Control– Rent

KRS 141.0401 also allows bulk delivery costs to be included in Cost of Goods Sold.

"Bulk delivery costs" means the cost of delivering the product to the consumer if:

1. The tangible product is delivered in bulk and requires specialized equipment that generally precludes commercial shipping; and

2. The tangible product is taxable under KRS 138.220.

This applies to entities that deliver consumers gasoline and special fuels that are subject to the tax under KRS 138.220.

Schedule COGS• In completing the Schedule COGS, separate accounting must be utilized in order

to calculate and report the amount of Kentucky COGS.

• If separate accounting is not possible for the taxpayer, a supporting statement explaining why separate accounting cannot be used to complete Schedule COGS must be attached.

• In such instances, as an alternative to separate accounting, the taxpayer must then take the following four steps in filling out Schedule COGS:

1. Complete the column titled Federal Form 1125-A Cost of Goods Sold, in its entirety.

2. Complete Column B, Total Costs of Goods Sold, in its entirety. Please note that the beginning and ending inventory may be different from the amounts reported on Federal Form 1125-A because of costs excluded from the COGS calculation. For a discussion of what costs must be excluded, please see the September 2013 Kentucky Tax Alert and the instructions to Schedule COGS.

3. Multiply the Total Cost of Goods Sold in Column B by the taxpayer’s Kentucky sales factor.

4. Enter the result of step 3 on Column A, Cost of Goods Sold, Line 8.

(If the Taxpayer does not comply with these steps, then the Department will assume separate accounting was possible and compliance the return on that basis.)

Federal Cost of Goods Sold

Schedule LLET

Schedule LLET-C

LLET Credits

• Nonrefundable LLET Credits

LLET– Nonrefundable LLET credit from KY Schedule(s) K-1– Nonrefundable Tax Credits from Schedule TCS

Income Tax– Nonrefundable LLET Credit (LLET less $175)– Nonrefundable LLET Credit from Corporation LLET Credit

Worksheet(s) KY Schedule(s) K-1

• Refundable LLET Credit– Certified Rehabilitation Tax Credit– Film Industry Tax Credit

Narrative

Narrative

Agent’s Narrative Report

• Explain how taxpayer was filing during the audit period. – If mergers, reverse acquisitions, etc. should be

mentioned.

• If taxpayer filed incorrectly should explain how taxpayer should have filed for audit period.

Narrative

• Use the most current narrative template at: S:\Field Division\Common Folder\Field Auditor\Audit Templates\Narrative Templates\Blank Corporate Audit Narrative Rev 01-15

• Items to be included:– Description of business– Detail scope of examination– Explanation of all adjustments– Address issues from the transmittal

• Do not:– Reference file names– State whether the taxpayer agrees with the audit– Quote memo or policies– Mention penalties

Conclusion

Questions?