Vaccine Risk Communication: Lessons from Risk Perception ...

description

Corporate Risk Management and the Perception of Terrorism Risk:

The Case of Germany

Christian Thomann*J.-Matthias Graf von der Schulenburg

Bruno GasRazvan Pascalau*

*U of Alabama

Quebec, August, 6th, 2007

2Thomann / Graf von der Schulenburg / Gas / Pascalau ● August 6th 2007

Research Question

How do corporations learn about dynamic risks?

Terrorism Risk is highly dynamic, potentially catastrophic and not well known

It thus provides for an opportunity to: Test if Prospective Reference Theory (Viscusi, 1989)

can be applied in a corporate context Learn how the inflow of new information changes a

corporation‘s risk management Understand how corporations weigh new information

How do corporations learn about dynamic risks?

Terrorism Risk is highly dynamic, potentially catastrophic and not well known

It thus provides for an opportunity to: Test if Prospective Reference Theory (Viscusi, 1989)

can be applied in a corporate context Learn how the inflow of new information changes a

corporation‘s risk management Understand how corporations weigh new information

3Thomann / Graf von der Schulenburg / Gas / Pascalau ● August 6th 2007

Overview

Introduction: Terrorism, Insurance and ExtremusIntroduction: Terrorism, Insurance and Extremus

Hypotheses and Empirical InvestigationHypotheses and Empirical Investigation

ConclusionConclusion

Corporate Risk Attitudes andIndividual Risk PerceptionCorporate Risk Attitudes andIndividual Risk Perception

DatasetDataset

4Thomann / Graf von der Schulenburg / Gas / Pascalau ● August 6th 2007

Overview

Introduction: Terrorism, Insurance and ExtremusIntroduction: Terrorism, Insurance and Extremus

Hypotheses and Empirical InvestigationHypotheses and Empirical Investigation

ConclusionConclusion

Corporate Risk Attitudes andIndividual Risk PerceptionCorporate Risk Attitudes andIndividual Risk Perception

DatasetDataset

5Thomann / Graf von der Schulenburg / Gas / Pascalau ● August 6th 2007

TerrorismA definition

An Act of Terrorism means an act of any person acting on behalf of or in connection with any organisation with activities directed towards the overthrowing or influencing of any government de jure or de facto by force or violence. Reinsurance (Acts of Terrorism) Act 1993

An Act of Terrorism means an act of any person acting on behalf of or in connection with any organisation with activities directed towards the overthrowing or influencing of any government de jure or de facto by force or violence. Reinsurance (Acts of Terrorism) Act 1993

6Thomann / Graf von der Schulenburg / Gas / Pascalau ● August 6th 2007

Terrorism has changed

Old Terrorism (Wilkinson 1986, Hoffman 1992) Motivation: Separation, Nationalism, Marxist Ideology,

Economic Inequality, Goals are well defined Organizational Structure: Command and Control. Terrorists are

trained and are committed full-time to their cause New Terrorism (Enders and Sandler 2000, Hoffman

1997) Motivation: Less comprehensible, embrace amorphous religious

aims Organizational Structure: International networks that can be

diffuse and spontaneous. Terrorists may live normal lives Terrorism in its present form poses a new and

significant challenge to Risk Managers

Old Terrorism (Wilkinson 1986, Hoffman 1992) Motivation: Separation, Nationalism, Marxist Ideology,

Economic Inequality, Goals are well defined Organizational Structure: Command and Control. Terrorists are

trained and are committed full-time to their cause New Terrorism (Enders and Sandler 2000, Hoffman

1997) Motivation: Less comprehensible, embrace amorphous religious

aims Organizational Structure: International networks that can be

diffuse and spontaneous. Terrorists may live normal lives Terrorism in its present form poses a new and

significant challenge to Risk Managers

7Thomann / Graf von der Schulenburg / Gas / Pascalau ● August 6th 2007

Dynamics of TerrorismHomeland Security Advisory System

Date Threat LevelMarch 12, 2002 Introduction: YellowSeptember 10, 2002 OrangeSeptember 24, 2002 YellowFebruary 7, 2003 OrangeFebruary 27, 2003 YellowMarch 17, 2003 OrangeApril 16, 2003 YellowMay 20, 2003 OrangeMay 30, 2003 YellowDecember 21, 2003 OrangeJanuary 9, 2004 YellowAugust 1, 2004 Orange financial services sectors in NYC, NJ and DCNovember 10, 2004 Yellow financial services sectors in NYC, NJ and DCJuly 7, 2005 Raised from Yellow to Orange for mass transitAugust 12, 2005 Lowered from Orange to Yellow for mass transitAugust 10, 2006 Red for flights from the UK to the United StatesAugust 13, 2006 Orange for flights from the UK to the United States

8Thomann / Graf von der Schulenburg / Gas / Pascalau ● August 6th 2007

Dynamics of TerrorismHomeland Security Advisory System

Date Threat LevelMarch 12, 2002 Introduction: YellowSeptember 10, 2002 OrangeSeptember 24, 2002 YellowFebruary 7, 2003 OrangeFebruary 27, 2003 YellowMarch 17, 2003 OrangeApril 16, 2003 YellowMay 20, 2003 OrangeMay 30, 2003 YellowDecember 21, 2003 OrangeJanuary 9, 2004 YellowAugust 1, 2004 Orange financial services sectors in NYC, NJ and DCNovember 10, 2004 Yellow financial services sectors in NYC, NJ and DCJuly 7, 2005 Raised from Yellow to Orange for mass transitAugust 12, 2005 Lowered from Orange to Yellow for mass transitAugust 10, 2006 Red for flights from the UK to the United StatesAugust 13, 2006 Orange for flights from the UK to the United States

9Thomann / Graf von der Schulenburg / Gas / Pascalau ● August 6th 2007

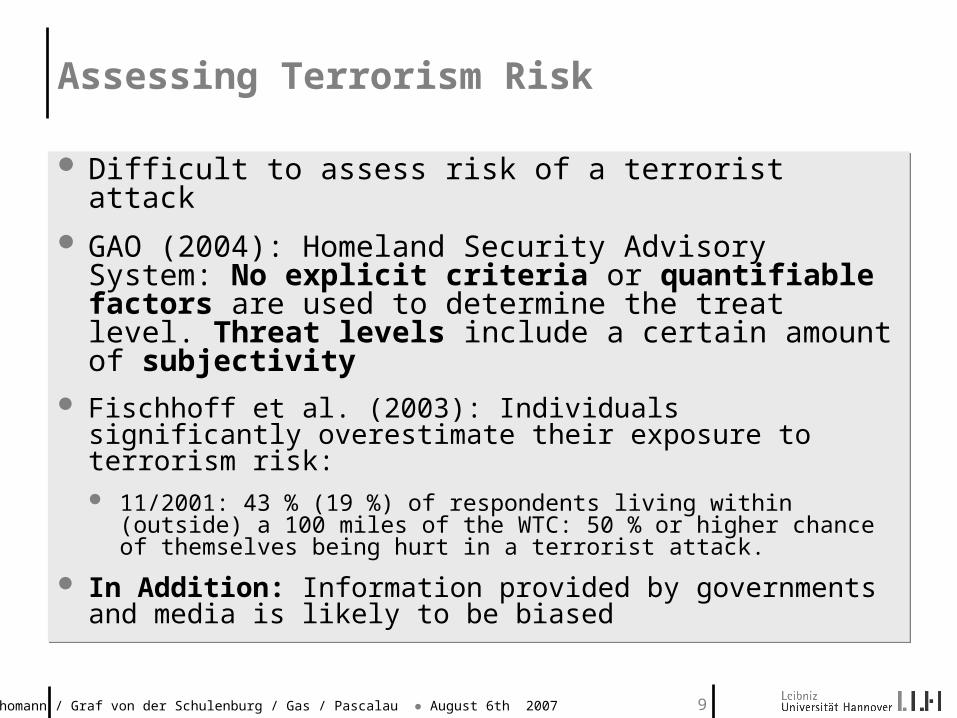

Assessing Terrorism Risk

Difficult to assess risk of a terrorist attack

GAO (2004): Homeland Security Advisory System: No explicit criteria or quantifiable factors are used to determine the treat level. Threat levels include a certain amount of subjectivity

Fischhoff et al. (2003): Individuals significantly overestimate their exposure to terrorism risk: 11/2001: 43 % (19 %) of respondents living within (outside) a 100

miles of the WTC: 50 % or higher chance of themselves being hurt in a terrorist attack.

In Addition: Information provided by governments and media is likely to be biased

Difficult to assess risk of a terrorist attack

GAO (2004): Homeland Security Advisory System: No explicit criteria or quantifiable factors are used to determine the treat level. Threat levels include a certain amount of subjectivity

Fischhoff et al. (2003): Individuals significantly overestimate their exposure to terrorism risk: 11/2001: 43 % (19 %) of respondents living within (outside) a 100

miles of the WTC: 50 % or higher chance of themselves being hurt in a terrorist attack.

In Addition: Information provided by governments and media is likely to be biased

10Thomann / Graf von der Schulenburg / Gas / Pascalau ● August 6th 2007

Terrorism and Insurance

Before 9/11 Terrorism is commonly included in Standard Insurance Policies

9/11 Highest Insured Loss Due to Terrorism Results in Exclusion of Terrorism from Standard Insurance

Contracts

Governments Intervene on Terrorism insurance markets United States (TRIA) Germany (Extremus) France (GAREAT)

Interventions in Germany and US must be prolonged in 2007

Before 9/11 Terrorism is commonly included in Standard Insurance Policies

9/11 Highest Insured Loss Due to Terrorism Results in Exclusion of Terrorism from Standard Insurance

Contracts

Governments Intervene on Terrorism insurance markets United States (TRIA) Germany (Extremus) France (GAREAT)

Interventions in Germany and US must be prolonged in 2007

11Thomann / Graf von der Schulenburg / Gas / Pascalau ● August 6th 2007

Terrorism Insurance in Germany After September, 11th

Government Intervention: Primary Insurer (EXTREMUS)Government Intervention: Primary Insurer (EXTREMUS)

Cover Risks > 25 million € Buildings, Content, Business Interruption and Clean up

Costs

Exclusions NBC, War, ...

Limit for Compensation: 1.5 bn €

Cover Risks > 25 million € Buildings, Content, Business Interruption and Clean up

Costs

Exclusions NBC, War, ...

Limit for Compensation: 1.5 bn €

100 % reinsurance by insurance industry & German Government100 % reinsurance by insurance industry & German Government

12Thomann / Graf von der Schulenburg / Gas / Pascalau ● August 6th 2007

Overview

Introduction: Terrorism, Insurance and ExtremusIntroduction: Terrorism, Insurance and Extremus

Hypotheses and Empirical InvestigationHypotheses and Empirical Investigation

ConclusionConclusion

Corporate Risk Attitudes andIndividual Risk PerceptionCorporate Risk Attitudes andIndividual Risk Perception

DatasetDataset

13Thomann / Graf von der Schulenburg / Gas / Pascalau ● August 6th 2007

Data SetOverview

Data on all government-reinsured terrorism insurance purchases between 11/2002 and 3/2007 in Germany (n>5000)

Name, Industry and Location of Policyholders Amount of Coverage Purchased Price of Insurance Coverage Start and End of Insurance Coverage

Data on all government-reinsured terrorism insurance purchases between 11/2002 and 3/2007 in Germany (n>5000)

Name, Industry and Location of Policyholders Amount of Coverage Purchased Price of Insurance Coverage Start and End of Insurance Coverage

14Thomann / Graf von der Schulenburg / Gas / Pascalau ● August 6th 2007

Data Set, Descriptive StatisticsPolicyholder

2002/3 2004 2005 2006 20072002-2007

MPL (m €)

Mean 554 377 378 365 415 419

p50 48.30 54.20 55.80 58.60 61.10 55.00

UL (m €)

Mean 71.20 73.00 75.60 80.70 85.80 77.20

p50 43.30 46.40 47.60 50.00 50.30 47.80

Degree of Coverage

Mean 0.85 0.86 0.85 0.87 0.87 0.86

p50 1.00 1.00 1.00 1.00 1.00 1.00

Net Premium (€)

Mean 89,014 73,207 58,934 57,151 56,220 67,095

p50 9,558 11,246 11,389 11,654 12,858 11,201

15Thomann / Graf von der Schulenburg / Gas / Pascalau ● August 6th 2007

Data Set, Descriptive StatisticsBy Industry and Year

2002/3 2004 2005 2006 2007Banks Asset Managers 99 111 106 105 92Construction 19 19 31 23 13Utilities 19 16 16 14 13Airports 26 22 20 22 17Real Estate 490 452 460 530 492Real Estate Inv Funds 96 100 107 120 107Churches, Foundations 21 20 19 21 17Hospitals 9 5 7 7 7Logistics 11 15 14 15 12Media, IT 34 33 31 31 24Local Authorities 32 18 18 18 15Heavy Industry 28 31 36 35 23Transportation 10 11 12 11 12Stores, Art, Fairs, Other, Tourism 92 100 112 122 101Insurance 194 118 127 121 105Total 1180 1072 1117 1195 1050

16Thomann / Graf von der Schulenburg / Gas / Pascalau ● August 6th 2007

Data Set, Descriptive StatisticsBy Industry and Year

2002/3 2004 2005 2006 2007Banks Asset Managers 99 111 106 105 92Construction 19 19 31 23 13Utilities 19 16 16 14 13Airports 26 22 20 22 17Real Estate 490 452 460 530 492Real Estate Inv Funds 96 100 107 120 107Churches, Foundations 21 20 19 21 17Hospitals 9 5 7 7 7Logistics 11 15 14 15 12Media, IT 34 33 31 31 24Local Authorities 32 18 18 18 15Heavy Industry 28 31 36 35 23Transportation 10 11 12 11 12Stores, Art, Fairs, Other, Tourism 92 100 112 122 101

Insurance 194 118 127 121 105Total 1180 1072 1117 1195 1050

17Thomann / Graf von der Schulenburg / Gas / Pascalau ● August 6th 2007

Data Set, Descriptive StatisticsBy Month

Policies Sold ΔPRInc

Month Mean SD Min Max Mean SD Min Max

1 924 186 599 1054 -329 2432 -3083 3513

2 40 63 9 153 126 274 -6 616

3 30 40 2 101 306 841 -284 1792

4 30 37 5 84 273 500 4 1022

5 13 6 5 17 32 17 17 52

6 16 12 9 33 26 10 19 41

7 21 8 11 30 12 89 -107 107

8 13 9 7 26 18 27 -22 42

9 12 4 7 16 23 15 4 39

10 14 8 6 23 43 43 14 107

11 9 6 3 19 22 10 14 37

12 24 22 10 62 386 778 21 1778

Total 106 273 2 1054 82 790 -3083 3513

18Thomann / Graf von der Schulenburg / Gas / Pascalau ● August 6th 2007

Data Set, Descriptive StatisticsBy Month

Policies Sold ΔPRInc

Month Mean SD Min Max Mean SD Min Max

1 924 186 599 1054 -329 2432 -3083 3513

2 40 63 9 153 126 274 -6 616

3 30 40 2 101 306 841 -284 1792

4 30 37 5 84 273 500 4 1022

5 13 6 5 17 32 17 17 52

6 16 12 9 33 26 10 19 41

7 21 8 11 30 12 89 -107 107

8 13 9 7 26 18 27 -22 42

9 12 4 7 16 23 15 4 39

10 14 8 6 23 43 43 14 107

11 9 6 3 19 22 10 14 37

12 24 22 10 62 386 778 21 1778

Total 106 273 2 1054 82 790 -3083 3513

19Thomann / Graf von der Schulenburg / Gas / Pascalau ● August 6th 2007

Overview

Introduction: Terrorism, Insurance and ExtremusIntroduction: Terrorism, Insurance and Extremus

Hypotheses and Empirical InvestigationHypotheses and Empirical Investigation

ConclusionConclusion

Corporate Risk Attitudes andIndividual Risk PerceptionCorporate Risk Attitudes andIndividual Risk Perception

DatasetDataset

20Thomann / Graf von der Schulenburg / Gas / Pascalau ● August 6th 2007

Corporate Risk Management

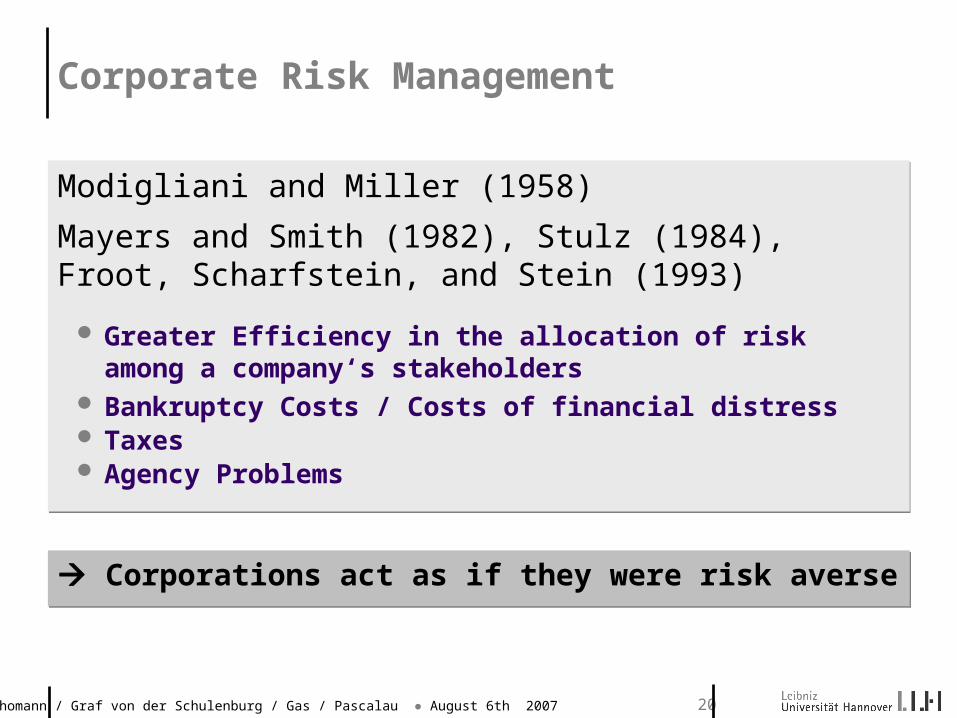

Modigliani and Miller (1958)

Mayers and Smith (1982), Stulz (1984), Froot, Scharfstein, and Stein (1993)

Greater Efficiency in the allocation of risk among a company‘s stakeholders

Bankruptcy Costs / Costs of financial distress Taxes Agency Problems

Modigliani and Miller (1958)

Mayers and Smith (1982), Stulz (1984), Froot, Scharfstein, and Stein (1993)

Greater Efficiency in the allocation of risk among a company‘s stakeholders

Bankruptcy Costs / Costs of financial distress Taxes Agency Problems

Corporations act as if they were risk averse Corporations act as if they were risk averse

21Thomann / Graf von der Schulenburg / Gas / Pascalau ● August 6th 2007

Corporate Risk ManagementEmpirical Studies and Extension

CRM: Empirical Studies (Insurance): Mayers and Smith (1990), Hoyt and Khang (2000), Kleffner

and Doherty (1996), Cole and McCollough (2006) CRM and Bankruptcy: Marin (2007) CRM: Extension to Ambiguous Risks:

Kunreuther et al. (1995): Ambiguity aversion describes prices set by insurance underwriters.

CRM of dynamic risks: has not been analyzed empirically

CRM: Empirical Studies (Insurance): Mayers and Smith (1990), Hoyt and Khang (2000), Kleffner

and Doherty (1996), Cole and McCollough (2006) CRM and Bankruptcy: Marin (2007) CRM: Extension to Ambiguous Risks:

Kunreuther et al. (1995): Ambiguity aversion describes prices set by insurance underwriters.

CRM of dynamic risks: has not been analyzed empirically

Further Similarities between individuals’ and corporations’ behaviorFurther Similarities between individuals’ and corporations’ behavior

22Thomann / Graf von der Schulenburg / Gas / Pascalau ● August 6th 2007

Prospective Reference Theory Assessing Dynamic Risks

Viscusi (1989): Prospective Reference Theory Generalization of the EU model Decision makers assess Probability with a Bayesian process Empirically tested Viscusi and Evans (2006), Viscusi and

O’Connor (1984) Posterior Probability (p*) is the weighted average of:

Prior Probability q (weight: γ) Probability p of the outcome observed (weight: ξ= number of trials)

Viscusi (1989): Prospective Reference Theory Generalization of the EU model Decision makers assess Probability with a Bayesian process Empirically tested Viscusi and Evans (2006), Viscusi and

O’Connor (1984) Posterior Probability (p*) is the weighted average of:

Prior Probability q (weight: γ) Probability p of the outcome observed (weight: ξ= number of trials)

*q p

p

23Thomann / Graf von der Schulenburg / Gas / Pascalau ● August 6th 2007

Overview

Introduction: Terrorism, Insurance and ExtremusIntroduction: Terrorism, Insurance and Extremus

Empirical InvestigationEmpirical Investigation

ConclusionConclusion

Corporate Risk Attitudes andIndividual Risk PerceptionCorporate Risk Attitudes andIndividual Risk Perception

DatasetDataset

24Thomann / Graf von der Schulenburg / Gas / Pascalau ● August 6th 2007

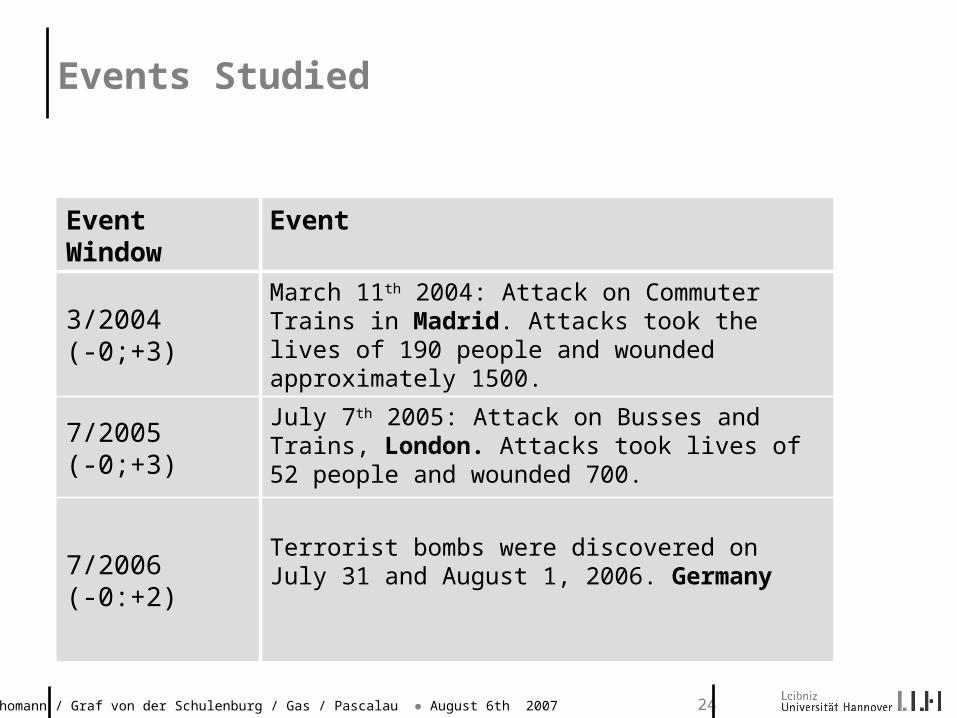

Events Studied

Event Window Event

3/2004(-0;+3)

March 11th 2004: Attack on Commuter Trains in Madrid. Attacks took the lives of 190 people and wounded approximately 1500.

7/2005 (-0;+3)

July 7th 2005: Attack on Busses and Trains, London. Attacks took lives of 52 people and wounded 700.

7/2006 (-0:+2)

Terrorist bombs were discovered on July 31 and August 1, 2006. Germany

25Thomann / Graf von der Schulenburg / Gas / Pascalau ● August 6th 2007

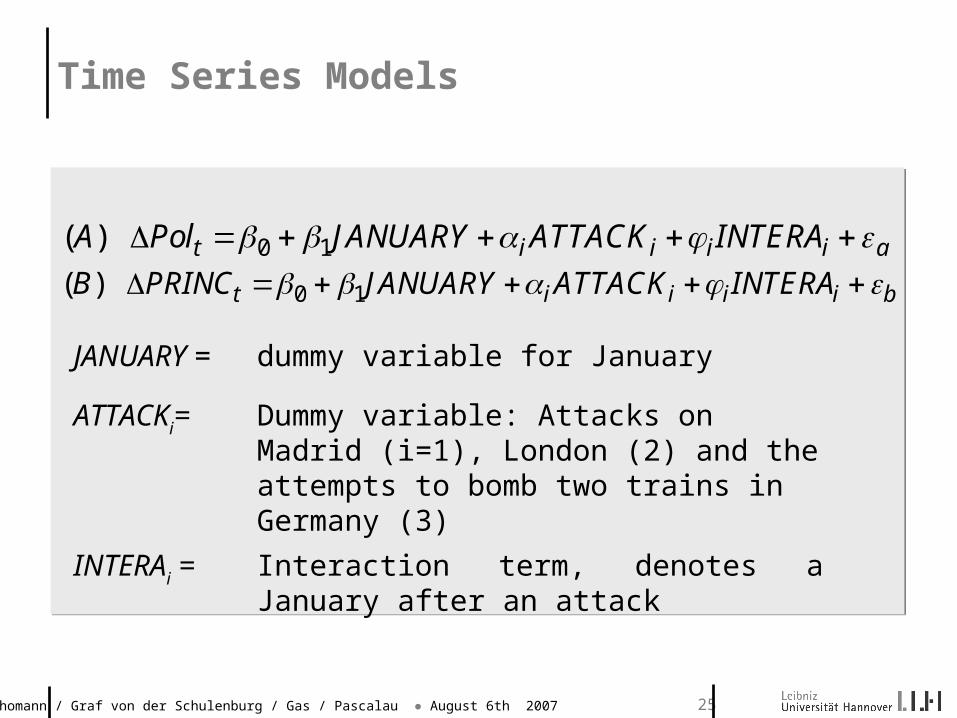

Time Series Models

JANUARY = dummy variable for January

ATTACKi= Dummy variable: Attacks on Madrid (i=1), London (2) and the attempts to bomb two trains in Germany (3)

INTERAi = Interaction term, denotes a January after an attack

0 1( ) t i i i i aA Pol JANUARY ATTACK INTERA

0 1( ) t i i i i bB PRINC JANUARY ATTACK INTERA

26Thomann / Graf von der Schulenburg / Gas / Pascalau ● August 6th 2007

OLS Estimates

Δ Polt Δ PRINC

JANUARY -139.39 *** -3092249 ***

(5.55) (55732.04)

ATTACK14.60 * 9831.609

(2.64) (26587.53)

ATTACK24.10 35944.01

(2.91) (29271.9)

ATTACK31.60 46391.62

(3.31) (33267.96)

INTERA162 *** 1656964 ***

(7.71) (77446.18)

INTERA282 *** 2986772 ***

(7.71) (77446.18)

INTERA31 2529190 ***

(7.71) (77446.18)

_cons 9.39 *** 9093.249

(1.03) (10349.18)

R² 0.97 0.99

Absolute value of t statistics in parentheses, * significant at 10 %; ** significant at 5%; *** significant at 1%

27Thomann / Graf von der Schulenburg / Gas / Pascalau ● August 6th 2007

OLS Estimates

Δ Number of Policies Δ Premium Income

JANUARY -139.39 *** -3092249 ***

(5.55) (55732.04)

ATTACK14.60 * 9831.609

(2.64) (26587.53)

ATTACK24.10 35944.01

(2.91) (29271.9)

ATTACK31.60 46391.62

(3.31) (33267.96)

INTERA162 *** 1656964 ***

(7.71) (77446.18)

INTERA282 *** 2986772 ***

(7.71) (77446.18)

INTERA31 2529190 ***

(7.71) (77446.18)

_cons 9.39 *** 9093.249

(1.03) (10349.18)

R² 0.97 0.99

Absolute value of t statistics in parentheses, * significant at 10 %; ** significant at 5%; *** significant at 1%

28Thomann / Graf von der Schulenburg / Gas / Pascalau ● August 6th 2007

Results

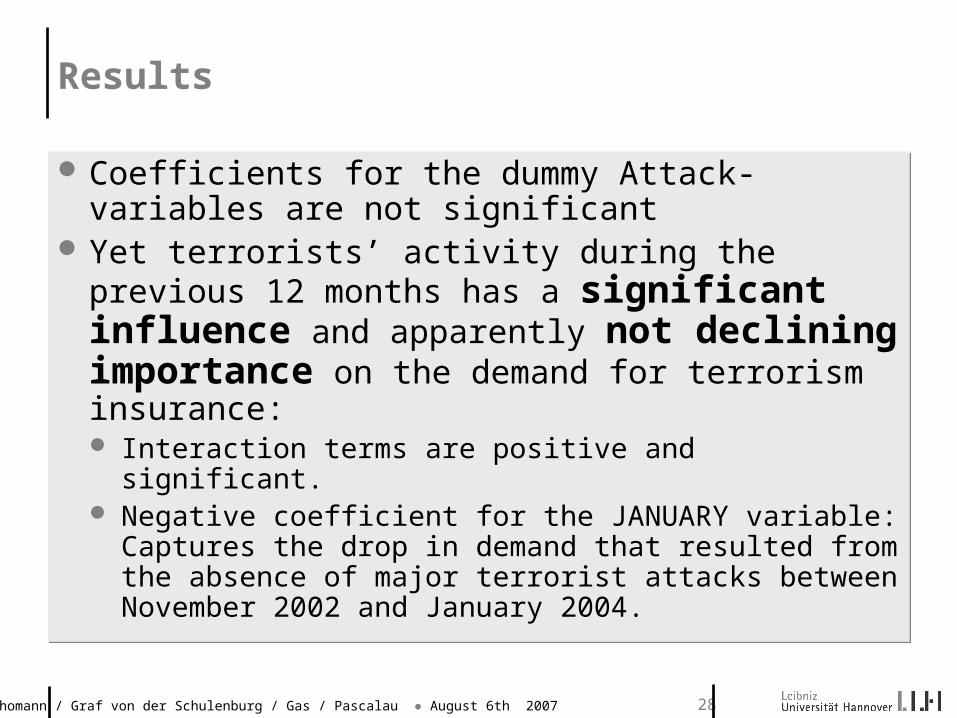

Coefficients for the dummy Attack-variables are not significant

Yet terrorists’ activity during the previous 12 months has a significant influence and apparently not declining importance on the demand for terrorism insurance: Interaction terms are positive and significant. Negative coefficient for the JANUARY variable:

Captures the drop in demand that resulted from the absence of major terrorist attacks between November 2002 and January 2004.

Coefficients for the dummy Attack-variables are not significant

Yet terrorists’ activity during the previous 12 months has a significant influence and apparently not declining importance on the demand for terrorism insurance: Interaction terms are positive and significant. Negative coefficient for the JANUARY variable:

Captures the drop in demand that resulted from the absence of major terrorist attacks between November 2002 and January 2004.

29Thomann / Graf von der Schulenburg / Gas / Pascalau ● August 6th 2007

Further Evidence

The data on the renewal of policies also supports the importance of recent terrorist activity for the demand for terrorism insurance in Germany

The data on the renewal of policies also supports the importance of recent terrorist activity for the demand for terrorism insurance in Germany

2002/3 2004 2005 20062002-2006

% of Contracts renewed in t+1 62 78 86 80 76*

% of contracts renewed until 2007 39 58 71 80

30Thomann / Graf von der Schulenburg / Gas / Pascalau ● August 6th 2007

Overview

Introduction: Terrorism, Insurance and ExtremusIntroduction: Terrorism, Insurance and Extremus

Hypotheses and Empirical InvestigationHypotheses and Empirical Investigation

ConclusionConclusion

Corporate Risk Attitudes andIndividual Risk PerceptionCorporate Risk Attitudes andIndividual Risk Perception

31Thomann / Graf von der Schulenburg / Gas / Pascalau ● August 6th 2007

Conclusion

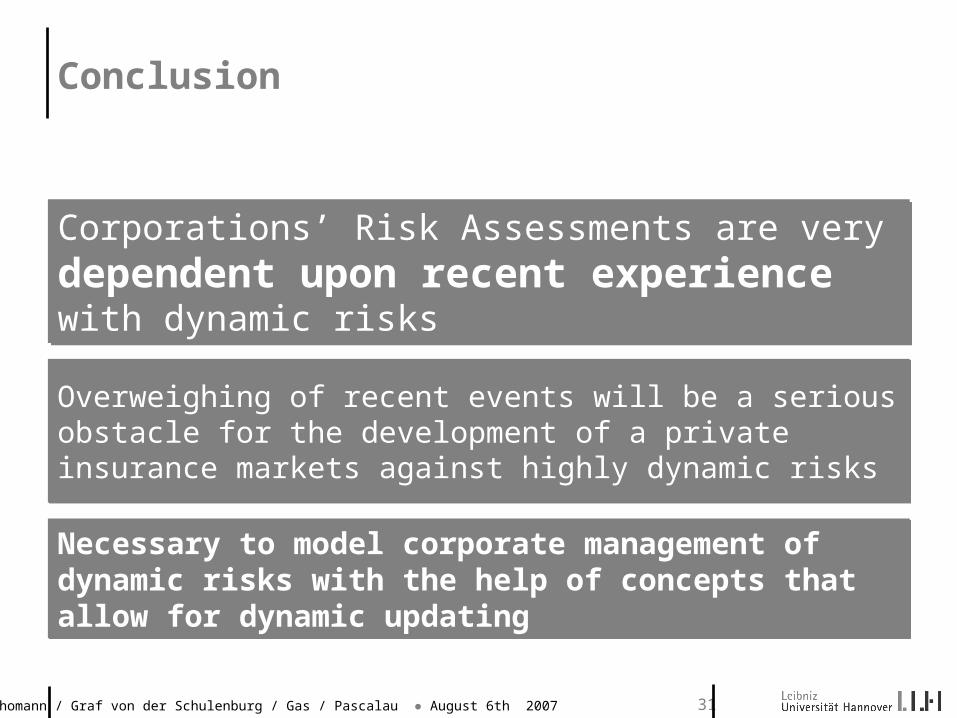

Corporations’ Risk Assessments are very dependent upon recent experience with dynamic risks

Corporations’ Risk Assessments are very dependent upon recent experience with dynamic risks

Necessary to model corporate management of dynamic risks with the help of concepts that allow for dynamic updating

Necessary to model corporate management of dynamic risks with the help of concepts that allow for dynamic updating

Overweighing of recent events will be a serious obstacle for the development of a private insurance markets against highly dynamic risks

Overweighing of recent events will be a serious obstacle for the development of a private insurance markets against highly dynamic risks

32Thomann / Graf von der Schulenburg / Gas / Pascalau ● August 6th 2007

Terrorism Insurance Expectations and Experience in Germany

When Extremus was founded in 2002 its shareholders expected to generate premium income of € 250 millions.When Extremus was founded in 2002 its shareholders expected to generate premium income of € 250 millions.

2002/3 2004 2005 2006 2007 2002-2007

Contracts sold 1180 1071 1116 1195 1050 5612

Premium Income (€ m)

105 78.4 65.8 68.3 59 377

Sum of Max. Poss. Losses (€ bn)

653 407 422 436 436 2350

Sum of Upper Limits (€ bn)

84 78.7 84.5 96.5 90.1 434

33Thomann / Graf von der Schulenburg / Gas / Pascalau ● August 6th 2007

Thank you

34Thomann / Graf von der Schulenburg / Gas / Pascalau ● August 6th 2007

Results

Recent Terrorist Activity has a strong and not declining importance for a company’s insurance decision. The demand for terrorism insurance decreases in the absence of terrorist attacksRecent terrorist attacks stabilize the demand for terrorism insurance

Recent Terrorist Activity has a strong and not declining importance for a company’s insurance decision. The demand for terrorism insurance decreases in the absence of terrorist attacksRecent terrorist attacks stabilize the demand for terrorism insurance

When making Risk Management Decisions Corporations place a great and not declining weight on their recent experience with terrorism risk.

Necessary to model corporate management of dynamic risks with the help of concepts that allow for dynamic updating

When making Risk Management Decisions Corporations place a great and not declining weight on their recent experience with terrorism risk.

Necessary to model corporate management of dynamic risks with the help of concepts that allow for dynamic updating

35Thomann / Graf von der Schulenburg / Gas / Pascalau ● August 6th 2007

Corporate Risk ManagementEmpirical Studies and Extensions

Mayers and Smith (1990)Demand for reinsurance by US insurersMayers and Smith (1990)Demand for reinsurance by US insurers

Hoyt and Khang (2000)Corporate demand for primary insurance (US)Hoyt and Khang (2000)Corporate demand for primary insurance (US)

Kleffner and Doherty (1996) Supply of earthquake insurance in CaliforniaKleffner and Doherty (1996) Supply of earthquake insurance in California

McCollough/McCollough/

McCollough/McCollough/

36Thomann / Graf von der Schulenburg / Gas / Pascalau ● August 6th 2007

Terrorism InsuranceExperience in Germany and the U.S.

0%

10%

20%

30%

40%

50%

60%

70%

80%

> 25 m.€ > 5 bn. € <100 Mio. $ 5 - 10 bn $

Pick-up RateUSA 2004

Market PenetrationExtremus Germany2004

0%

10%

20%

30%

40%

50%

60%

70%

80%

> 25 m.€ > 5 bn. € <100 Mio. $ 5 - 10 bn $

Pick-up RateUSA 2004

Market PenetrationExtremus Germany2004

37Thomann / Graf von der Schulenburg / Gas / Pascalau ● August 6th 2007

Definition

„Terrorakte sind jegliche Handlungen von Personen oder Personengruppen zur Erreichung politischer, religiöser, ethnischer oder ideologischer Ziele, die geeignet sind, Angst [...] in [...] Teilen der Bevölkerung zu verbreiten und dadurch auf eine Regierung oder staatliche Einrichtungen Einfluss zu nehmen.“

Extremus Allgemeine Bedingungen für die Terrorversicherung

Definition

„Terrorakte sind jegliche Handlungen von Personen oder Personengruppen zur Erreichung politischer, religiöser, ethnischer oder ideologischer Ziele, die geeignet sind, Angst [...] in [...] Teilen der Bevölkerung zu verbreiten und dadurch auf eine Regierung oder staatliche Einrichtungen Einfluss zu nehmen.“

Extremus Allgemeine Bedingungen für die Terrorversicherung

Terrorismus

38Thomann / Graf von der Schulenburg / Gas / Pascalau ● August 6th 2007

Absence of Terrorism InsuranceEconomic Effects

Hubbard et al. 2005

Absent Major Attack: “…GDP may be $ 53 billion (0.4 %) lower, household net worth may be $ 512 billion (0.9 %) lower, and roughly 326,000 (0.2 %) fewer jobs may be created.”

In Case of an Attack “… tens of thousands more jobs could be lost due to the lack of insurance coverage and thousands of additional bankruptcies could occur compared to the 9/11 event, which was covered by the insurance industry.”

Hubbard et al. 2005

Absent Major Attack: “…GDP may be $ 53 billion (0.4 %) lower, household net worth may be $ 512 billion (0.9 %) lower, and roughly 326,000 (0.2 %) fewer jobs may be created.”

In Case of an Attack “… tens of thousands more jobs could be lost due to the lack of insurance coverage and thousands of additional bankruptcies could occur compared to the 9/11 event, which was covered by the insurance industry.”

39Thomann / Graf von der Schulenburg / Gas / Pascalau ● August 6th 2007

Individual Risk Perception

Individual’s perception of risk not systematically governed by probability of event:

Biases Overestimation of Dread Risk, Unknown Risk

(Slovic, 1987)

Probabilities Assessed with Availability Heuristic

(Tversky and Kahneman, 1973)

Individual’s perception of risk not systematically governed by probability of event:

Biases Overestimation of Dread Risk, Unknown Risk

(Slovic, 1987)

Probabilities Assessed with Availability Heuristic

(Tversky and Kahneman, 1973)

40Thomann / Graf von der Schulenburg / Gas / Pascalau ● August 6th 2007

41Thomann / Graf von der Schulenburg / Gas / Pascalau ● August 6th 2007

Country Name of Insurance Scheme

Israel * Victims of Enemy Action

Northern Ireland*

Criminal Damage Compensation Scheme)

Spain * Consorcio de Compensación de Seguros (CCS)

France Gestion de l’assurance et la Réassurance des Risques Attentats et Actes de Terrorisme (GAREAT)

South Africa * South Africa Special Risks Insurance Association. (SASRIA))

Great Britain * Pool Reinsurance Company

USA Terrorism Risk Insurance Act

Germany Extremus

*=founded before 2001

42Thomann / Graf von der Schulenburg / Gas / Pascalau ● August 6th 2007

Data Set, Descriptive StatisticsNumber of Policies Sold by Month

Month Mean Std. Dev. Min Max

1 923.6 186.24 599 1054

2 40.4 63.04 9 153

3 30 40.22 2 101

4 30.25 36.54 5 84

5 13 5.66 5 17

6 15.75 11.53 9 33

7 21 7.87 11 30

8 13.25 8.96 7 26

9 12 3.92 7 16

10 13.5 7.59 6 23

11 9 6.32 3 19

12 24.2 21.71 10 62

Total (n=5611) 105.9 272.61 2 1054

43Thomann / Graf von der Schulenburg / Gas / Pascalau ● August 6th 2007

Data Set, Descriptive StatisticsNumber of Policies Sold by Month

Month Mean Std. Dev. Min Max

1 923.6 186.24 599 10542 40.4 63.04 9 153

3 30 40.22 2 101

4 30.25 36.54 5 84

5 13 5.66 5 17

6 15.75 11.53 9 33

7 21 7.87 11 30

8 13.25 8.96 7 26

9 12 3.92 7 16

10 13.5 7.59 6 23

11 9 6.32 3 19

12 24.2 21.71 10 62

Total (n=5611) 105.9 272.61 2 1054

44Thomann / Graf von der Schulenburg / Gas / Pascalau ● August 6th 2007

Terrorism

Terrorism is the premeditated use, or threat of use, of extra-normal violence or brutality to gain a political objective through intimidation or fear against a targeted audience (United States Department of State, 2000)

Terrorism is the premeditated use, or threat of use, of extra-normal violence or brutality to gain a political objective through intimidation or fear against a targeted audience (United States Department of State, 2000)

45Thomann / Graf von der Schulenburg / Gas / Pascalau ● August 6th 2007

International Terrorist Attacks1990-2003

0

100

200

300

400

500

600

1990

1992

1994

1996

1998

2000

2002

Source: US Department of State

46Thomann / Graf von der Schulenburg / Gas / Pascalau ● August 6th 2007

Extremus Market Penetration in Germany

2003 2004 2005 2006

% of corporations that are customers of Extremus

< 1 bn € 2.9 2.6 2.7 2.8

> 5 bn € 21.7 15.0 18.3 16.7

% of total sums insured by Extremus

< 1 bn € 4.6 4.5 4.7 5.2

> 5 bn € - 40.6 39.0 38.0

47Thomann / Graf von der Schulenburg / Gas / Pascalau ● August 6th 2007

„Omar, I think the boat is not going straight“

Private Public Partnership

48Thomann / Graf von der Schulenburg / Gas / Pascalau ● August 6th 2007

Terrorism and Insurance

After September 11th, 2001 Terrorism has been excluded from many standard insurance contracts

Terrorism poses significant problems for insurers:

Dynamic Uncertainty Asymmetric Distribution of Information between

Government and Private Sector Potential of Catastrophic Losses

After September 11th, 2001 Terrorism has been excluded from many standard insurance contracts

Terrorism poses significant problems for insurers:

Dynamic Uncertainty Asymmetric Distribution of Information between

Government and Private Sector Potential of Catastrophic Losses