Corporate Presentation July 2013. Light Holdings 2.

39

Corporate Presentation July 2013

-

Upload

candace-cox -

Category

Documents

-

view

215 -

download

1

Transcript of Corporate Presentation July 2013. Light Holdings 2.

Corporate Presentation

July 2013

Light Holdings

Light S.A. (Holding)

100% 51% 20%100% 100% 100%100% 100%51% 25.5%100%

Light Serviços de Eletricidade

S.A.

LightgerS.A.

ItaocaraEnergia

Ltda.

Amazônia Energia S.A.

Light EscoPrestação de Serviços S.A.

LightcomComercializadora

de Energia S.A.

Light Soluções em Eletricidade

Ltda.

Instituto Light

AxxiomSoluções

Tecnológicas S.A.

CR ZongshenE-Power

Fabricadora de Veículos S.A.

GuanhãesEnergia

S.A.

21.99%

Renova Energia

S.A.

Central Eólica Fontainha

Ltda.

100%

Central Eólica São Judas

Tadeu Ltda.

100% 9.77%

Norte Energia

S.A.

33%EBL Cia de Eficiência Energética

S.A.

Light Energia S.A.

Distribution Generation Commercialization and Services Institutional Systems ElectricVehicles

51%

2

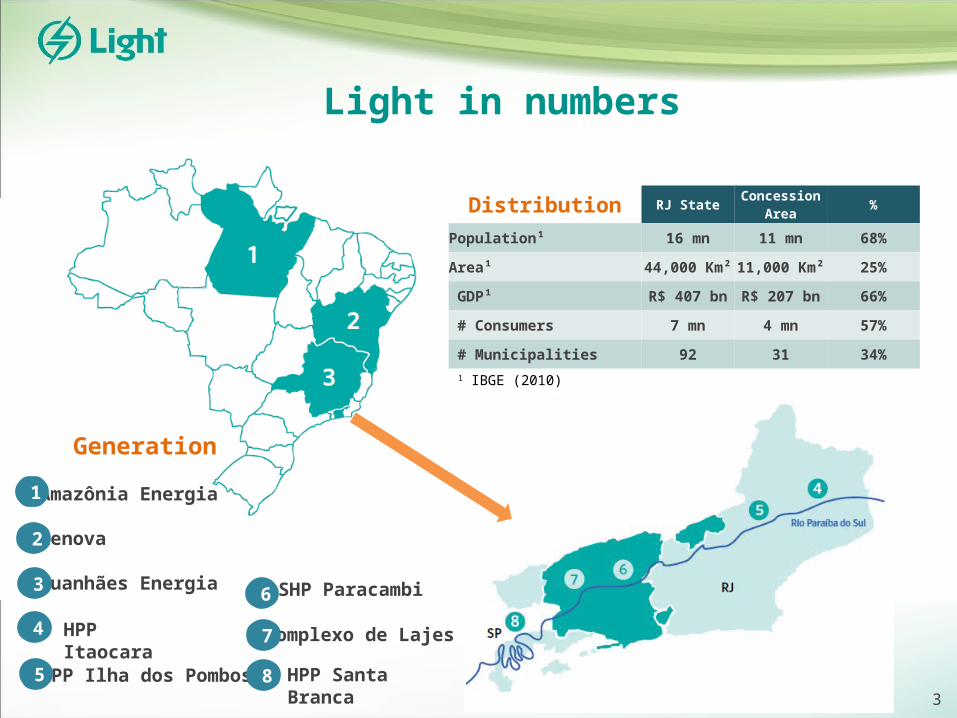

Light in numbers

Amazônia Energia

Renova

Guanhães Energia

Generation

HPP Itaocara Complexo de Lajes

Distribution RJ StateConcession

Area%

Population¹ 16 mn 11 mn 68%

Area¹ 44,000 Km² 11,000 Km² 25%

GDP¹ R$ 407 bn R$ 207 bn 66%

# Consumers 7 mn 4 mn 57%

# Municipalities 92 31 34%

6

HPP Ilha dos Pombos

SHP Paracambi

HPP Santa Branca

1

2

3

1 IBGE (2010)

4

5

7

83

Tractebel AES Tiete Duke CPFL EDP Light

Cemig CPFL Neoenergia Copel Light EDP Eletropaulo Cemig Copel CPFL Paulista

Light Celesc

RankingsAmong the largest players in Brazil

INTEGRATED²Net Revenues 2012 – R$ Billion

GENERATION PRIVATE-OWNED COMPANIES²Installed Hydro-generation Capacity (MW) – 2012

37,626

24,71422,737

21,467 20,05415,018

18.5

15.0

11.8

8.56.9

6.6

5,560

2,658 2,241 2,2192,012

877

DISTRIBUTION¹Energy Consumption in Concession Area (GWh) - 2012

1 – Source: Captive market 2 – Source: Companies reports* Considers the 9 MW of Renova’s SHPs

*4

Shareholders Structure

11 Board members: 8 from the controlling

group, 2 independents e 1 employees

nominated

A qualifying quorum of 7 members to

approve relevant proposals such as: M&A

and dividend policy

5

CEMIG RME LEPSA BNDESPAR MARKET

PARATI

CEMIGFIP REDENTOR

REDENTORENERGIA

26.06% 13.03% 13.03% 13.46% 34.41%

75% 25%

13.03%100%

96.81% 100%

6.41%19.23%

BTGPACTUAL

SANTANDER

VOTORANTIM

BANCO DO BRASIL

28.57%

5.50%

28.57%

5.50%

28.57%5.50%

14.29%

2.74%

MINORITY

3.19% 0.42%

Free Float 47,9%

25.64%*

FOREIGN NATIONAL

55.93% 44.07%

Stake in blue: indirect interest in LightLight S.A.

(Holding)

Controller Group 52,1%

*12.61% (RME) + 13.03%(LEPSA)

Corporate Governance

General AssemblyGeneral Assembly

Fiscal CouncilFiscal Council

Board of DirectorsBoard of Directors

AuditorsCommitteeAuditors

Committee

Governance and Sustainability

Committee

Governance and Sustainability

Committee

Human Resources Committee

Human Resources Committee

Finances CommitteeFinances

CommitteeManagement Committee

Management Committee

Chief Executive Officer

Chief Executive Officer

Chief HR OfficerChief HR Officer

Chief Business Officer

Chief Business Officer

Corporate Management

Officer

Corporate Management

OfficerChief Legal OfficerChief Legal Officer

Chief Financial and Investor

Relations Officer

Chief Financial and Investor

Relations Officer

Chief Distribution Officer

Chief Distribution Officer

Chief Energy Officer

Chief Energy Officer

João B. Zolini Carneiro

Ricardo Cesar C. Rocha

Evandro L. Vasconcelos

Andreia Ribeiro Junqueira

Fernando Antônio F.Reis

Paulo Carvalho Filho

Evandro L. Vasconcelos*

Paulo Roberto R. Pinto

Chief Communications

Officer

Chief Communications

Officer

Luiz Otavio Ziza Valadares

LGSXYADR-OTC

Interim*

6

Residencial35%

Comercial28%

Livre19%

Outros Cativos13%Industrial5%

1T10 1T11 1T12 1T13

+3.7%

6,1806,291

26.9ºC

27.0ºC

1Q121Q11

6,0876,407

1Q10

27.8ºC28.3º

C

+1.8%

1Q13

1Note: To preserve comparability in the market approved by Aneel in the tariff adjustment process, the billed energy of the free customers Valesul, CSN and CSA were excluded in view of these customers’ planned migration to the Basic Network.

TOTAL MARKET (GWh) ¹

Energy Consumption Distribution – Quarter

With the consumption no longer billed by the change in criteria, the total energy consumption increase in the concession area would be 5.3% over 1Q12.

7

1T10 1T11 1T12 1T13

Industrial5%

Free19%

Others13%

Commercial28%

Residential35%

Total Market

FREECAPTIVE

ELECTRICITY CONSUMPTION (GWh)

TOTAL MARKET – QUARTER

8

RESIDENTIAL INDUSTRIALCOMMERCIAL OTHERS TOTAL

1Q12 1Q13 1Q12 1Q13 1Q12 1Q13 1Q12 1Q13 1Q12 1Q131T12 1T13 1T12 1T13 1T12 1T13 1T12 1T13

+3.7%

1T12 1T13

5,3795,572

6,180

801835

6,407

+3.7%

882 913

932

49 53

966

+7.8%

1.7481.877

1,939

191214

2,091

401 359

962

561 568

927

+3.2%

2,348 2,423

-3.7%

1,748 1,877

Prospects for State of RioInvestments of R$ 211.5 billion in the State of Rio de Janeiro¹

OilR$ 107.7 bn

50.9%

TourismR$ 1.8 bn

0.9%

OthersR$ 1.9 bn

0.9%

Olimpic FacilitiesR$ 8.6 bn

4.1%

InfrastructureR$ 51.0 bn

24.1%

Transformation IndustryR$ 40.5 bn19.1%

Period 2012-2014

¹Source: Firjan (Industry Federation of Rio de Janeiro)

Events Schedule

Confederations Cup

World Youth Day

World Cup

Olympics

Paralympics

Jun, 15 to 30/2013

Jul, 23 to 28/2013

Jun, 12 to Jul, 13/2014

Aug, 5 to 21/2016

Sep, 7 to 18/2016

9

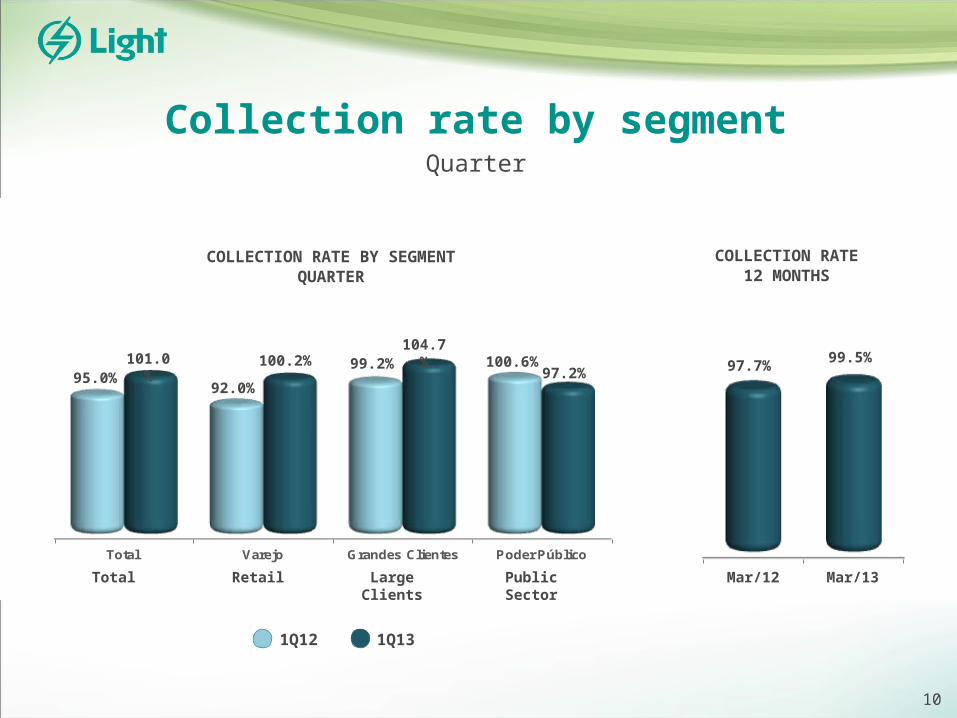

Collection rate by segmentQuarter

10

mar-12 mar-13

Total Varejo Grandes Clientes Poder Público

1T12 1T13

97.2%

COLLECTION RATE12 MONTHS

COLLECTION RATE BY SEGMENTQUARTER

95.0%101.0

%100.2%

92.0%

99.2%104.7

% 100.6%

1Q12

1Q13

97.7% 99.5%

Mar/12 Mar/13Total Retail Large Clients

Public Sector

Losses12 months

32.9%

Technical losses GWh

% Non-technical losses/ LV Market

% Non-technical losses / LV Market - Regulatory

Non-technical losses GWh

Reflects exclusion of long term delinquent customers from the billing system, according to Resolution 414 by Aneel.

Sep/11 Dec/11 Jun/12Mar/12 Sep/12Sep/10 Dec/10 Jun/11Mar/11 Mar/13Dec/12

42.2%40.7

%

41.2%40.4

%

43.1%

45.4%

44.9%

42.1%

41.8%

41.6%

41.3%

5,316

2,328 2,349

5,229

7,5827,627 7,665

2,335

5,247 5,615

2,432

8,047

5,457

2,381

7,838

5,330

2,5772,214

6,007

2,618

6,0295,312

2,231

5,278

2,215

5,326

2,293

8,6478,5847,544 7,5437,493 7,619

37% Risky Area

63% Non-Risky Area

11

PARAÍBAVALLEY

LITORÂNEA

WEST EAST

As March / 2013

BAIXADA

Non Technical LossesConcession Area Losses Map

Grupo Light Valley Litorânea East West Baixada

# Clients 4,029,805 418,489 814,157 857,437 934,709 1,005,013

Low Voltage Market (GWh) 13,411 1,129 4,934 2,558 2,507 2,283

Non Technical Losses (GWh) 6,029 43 267 1,787 1,924 2,008

Non Technical Losses/LV Mkt (%) 44.95% 3.78% 5.40% 69.87% 76.74% 87.98% 12

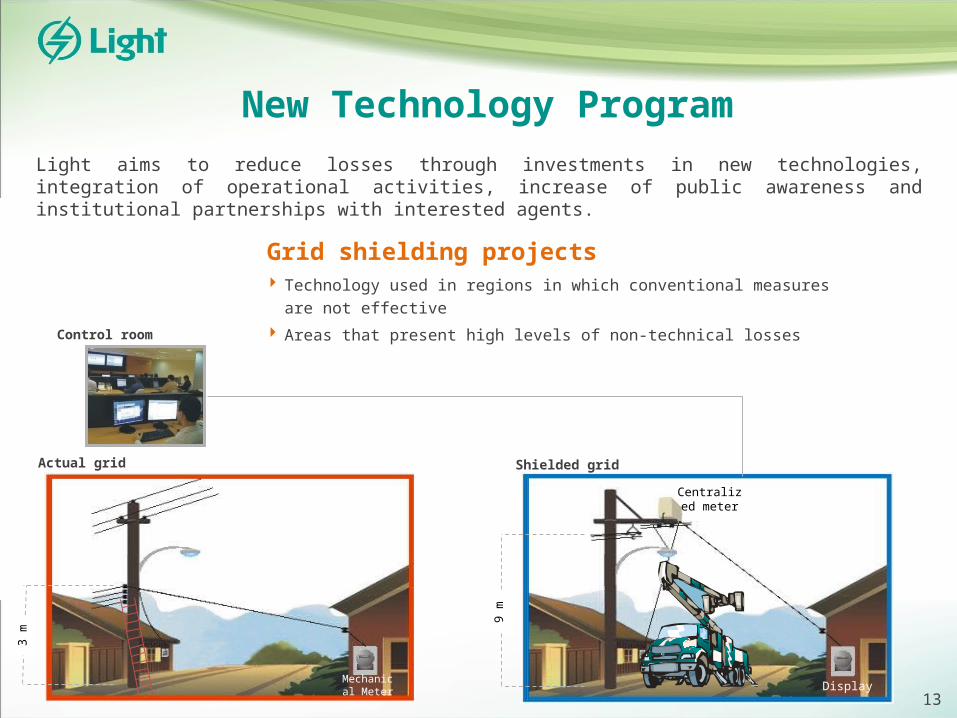

New Technology Program

Technology used in regions in which conventional measures are not effective

Areas that present high levels of non-technical losses

Light aims to reduce losses through investments in new technologies, integration of operational activities, increase of public awareness and institutional partnerships with interested agents.

Grid shielding projects

Actual grid Shielded grid

Control room

3 m

9 m

Mechanical Meter Display

Centralized meter

13

New Technology Program

Monitoring, reading, cutting and reconnection of customers telemetry– MCC (Measuring Center Centralized)

Prioritization in areas of high losses and aggressiveness to the network

Technology hindering inappropriate interference in networks

Meters Installed (Thousands)

OUT OF FAVELASFAVELAS

14

2009 2010 2011 2012 2013

294

79

373

30

69

May/132011 2012

227

341

197272

20102009

7

122

1152

80

78

Pacified Favelas (UPPs)

33 UPPs established

130,000 households

40 UPPs until 2014

Present in 15 UPPs, 9 already concluded

60,000 consumers

200,000 people achieved

30 UPPs until 2014

State Government Light

Safety, citizenship, and social inclusionPARTNERSHIP

15

Focused in areas with 10,000 to 20,000 clients with high level of losses and

delinquency;

Fully-dedicated teams of technicians and commercial agents;

Small areas to cover, enabling higher productivity;

Constant and accurate results monitoring by Light;

Result-linked remuneration for services provided;

Fixed remuneration above market and aggressive

variable remuneration;

Police Force support, when necessary.

Zero Losses AreaProject: “Light Legal” (APZ – Zero Losses Area)

16

Losses Control InitiativesResults until March/13

Favelas

Zero Losses Area (APZ)

Before Current Before CurrentSanta Marta 2009 95.00% 8.22% 0.20% 99.13%

Cidade de Deus 1 2010 52.10% 14.45% 23.10% 78.30%Chapéu Mangueira 16.20% 101.46%

Babilônia 5.40% 99.51%Cabritos 1.40% 96.25%

Tabajaras 9.50% 96.99%Formiga 2011 73.30% 9.37% 31.40% 84.62%

Batan 2012 61.80% 10.66% 1.20% 93.88%Borel 2013 60.50% 31.06% 9.40% 79.10%

2011 62.30% 12.47%

Areas Conclusion Year

Losses Collection

2010 62.70% 14.75%

NeighborhoodClient

NumbersNon-Technical Losses / Low Voltage Market *

Collection Rate

Curicica 13,034 12.1% 99.7%Realengo 10,141 16.9% 99.5%Cosmos 34,933 22.8% 107.7%Sepetiba 18,793 33.5% 96.5%Caxias 1 e 2 13,907 19.5% 93.3%Belford Roxo 1 e 2 19,582 32.4% 94.2%Vigário Geral 16,122 16.1% 98.3%Caxias 3 17,239 25.2% 98.7%Nova Iguaçu 1 31,899 31.9% 98.6%Nova Iguaçu 2 20,213 25.0% 95.2%Nilópolis 9,861 28.8% 89.8%Ricardo de Albuquerque 24,433 19.5% 96.4%Mesquita 8,419 38.4% 96.7%Cabritos/Tabajaras/Chapéu Mangueira/Babilônia

5,208 11.9% 97.7%

Total 243,784 24.3% 98.4%* Reflects the results accumulated until mar/13 since the begining of the implementation of each APZ.

17

Average losses reduction: 23.0 p.p.Average Collection increase: 14,5 p.p.

Average losses reduction : 49.5 p.p.Average Collection increase : 80.4 p.p.

Losses Reduction - Business CaseAn example

300 kWh

100 kWh

REAL CONSUMPTION

BILLED CONSUMPTION

NEW METER INSTALLATIO

N

200 kWhLOST ENERGY

ENERGY SAVED

100 kWh

BILLED CONSUMPTION INCREASE

100 kWh

OTHER EFFECTS (BY-PRODUCTS):

CAPEX GOES TO THE RAB

BAD DEBT PROVISION REDUCTION

OPERATIONAL COSTS

REDUCTION

18

GENERATION BUSINESS

Installed Capacity868 MW

HPP Santa Branca

56 MW

HPP Ilha dos Pombos 187 MW

HPP Fontes Nova

132 MWHPP Underground

Nilo Peçanha - 380 MWHPP Pereira Passos

100 MW

SP

RJ

HPP Santa Branca

Paraiba do Sul River

HPP Ilha dos Pombos100%

100%

100%100%100%

Lajes Complex

51%

SHP Paracambi

13 MW

20

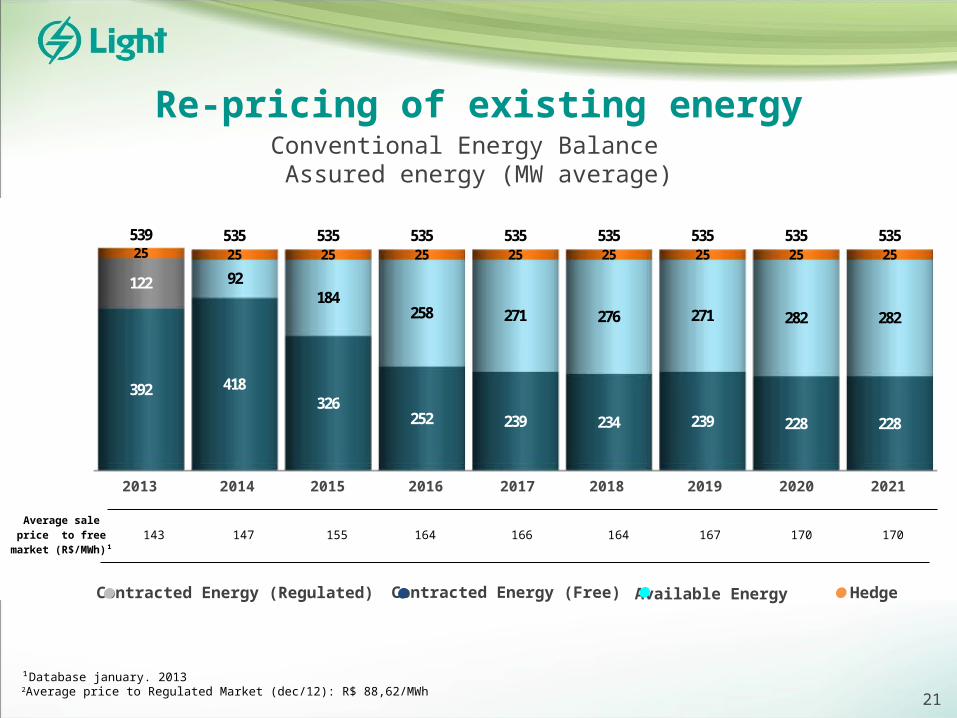

Re-pricing of existing energy

Contracted Energy (Regulated) Contracted Energy (Free) HedgeAvailable Energy

Average sale price to free market

(R$/MWh)¹143 147 155 164 166 164 167 170 170

Conventional Energy Balance Assured energy (MW average)

¹Database january. 20132Average price to Regulated Market (dec/12): R$ 88,62/MWh

21

2013 2014 2015 2016 2017 2018 2019 2020 2021

392 418326

252 239 234 239 228 228

122 92184

258 271 276 271 282 282

25 25 25 25 25 25 25 25 25539 535 535 535 535 535 535 535 535

Balanço de Energia Convencional do Grupo LightEnergia Assegurada (MW médios)

Vendas no ACL 2004-EE-2006-08 Recursos disponíveis para comercialização Hedge Total

2013 2014 2015 2016 2017 2018 2019 2020 2021

Generation Projects

ProjectInstalled Capacity

(MW)Assured Energy(MWaverage)

Operational Start

Stake

Renova335 (in operation)

797.2 (contracted)

173.1 (in operation)

395 (contracted)

2008/2012

2013-201721.99%

Belo Monte 11,223 4,571 2015 2.49%

Itaocara 151 83 2015 51%

Guanhães 44 25.03 2014 51%

Lajes 17 16 2015 51%

22

Capacidade Light

Energia

(+) PCH Paracambi

(+) Renova Capacidade Atual

(+) Lajes (+) Itaocara (+) Renova (+) Belo Monte

(+) Guanhães

Capacidade após

expansão

Expansão da Geração (MW)

Generation Projects

Installed Capacity (MW)

Installed Capacity

Capacity After Expansion

Investments in Renova, Belo Monte and Guanhães in line with our strategy of growing in the generation business

¹ Considering 51% stake

² Considering 21.99% stake

³ Considering 2.49% stake

+ 59.8%

(+) Belo Monte³

(+) SHPParacambi¹

(+) SHPLajes¹

(+) HPPItaocara¹ (+) Guanhães¹ (+) Renova²

1,505

1374* 9 77

175

280

855

(+) Renova²Current

Capacity

* 9 MW SHP + 65 MW Wind Farm (since jul/12)

942

22

23

RESULTS

Net Revenue

Industrial 5.5%

NET REVENUE (R$MN)

Generation 7.1% Distribution

84.0%**

NET REVENUE BY SEGMENT (1Q13)*

Commercialization 8.6%

* Eliminations not considered

** Construction revenue not considered

NET REVENUE FROM DISTRIBUTION (1Q13)

Commercial 29.7%

Others (Captive) 11.7%

Network Use (TUSD)(Free +

Concessionaires)

8.0% Residential 45.1%

Construction RevenueRevenue w/out construction revenue

1T12 1T13

+7.5

1,898.7

2,040.0

1Q131Q12

157,3

1,761.3

1,883.1

137,4

+6,9%

25

Operating Costs and Expenses

Manageable (distribution): R$ 317.1(17.8%)

Generation and Commercialization: R$

203.5(11.4%)

Non manageable (distribution): R$ 1,261.2(70.8%)

* Eliminations not considered

** Construction revenue not considered

DISTRIBUTION MANAGEABLE COSTS (R$MN)COSTS (R$MN)*1Q13

1T12 1T13

333.1 317.1

-4.8%

1Q131Q12

R$ MN 1Q12 1Q13 Var.

PMSO 167.6 184.0 9.7%

Provisions 86.5 45.2 -47.7%

PCLD 61.6 29.0 210.2%

Contingencies 24.9 16.2 554.9%

Depreciation 75.7 80.6 6.5%

Other operational/revenues expenses

3.2 7.3 127.3%

Total 333.1 317.1 -4.8%

Não gerenciáveis;

70,8%

Gerenciáveis; 17,8%

Geração e Comercialização

; 11,4%

26

EBITDA

27

CONSOLIDATED EBITDA (R$MN) EBITDA BY SEGMENT*1Q13

Generation 33.4% (EBITDA Margin: 82.1%)

Commercialization 2.8%

(EBITDA Margin: 5.6%)

Distribution 63.8%(EBITDA Margin: 13.5%)

*Eliminations not considered

1T12 1T13

355.1433.4

-18.1%

1Q12 1Q13

Distribuição ;

63,8%; 63,84%

Geração; 33,4%;

33,40%

Comercialização;

2,8%; 2,77%

EBITDA

28

EBITDA Ajustado -

2T11

Ativos e Passivos

Regulatórios

EBITDA -2T11

Receita Líquida

Custos Não Gerenciáveis

Custos Gerenciáveis

(PMSO)

Provisões EBITDA -2T12

Ativos e Passivos

Regulatórios

EBITDA Ajustado -

2T12EBITDA1Q12

EBITDA1Q13

Net Revenu

e

Non-Manageabl

e Costs

Manageable Costs (PMSO)

Provisions

Regulatory Assets and Liabilities

Regulatory Assets and Liabilities

Adjusted EBITDA

1Q12

Adjusted EBITDA

1Q13

EBITDA – 1Q12 / 1Q13(R$ MN)

Other operational/

revenues

(2)

433

122

(175) (19) (7) (1)

101 456

+ 5.8%

- 18.1%

42355

431

Equity Pick-up

Net Income

EBITDA Ajustado -

2T11

Ativos e Passivos

Regulatórios

EBITDA -2T11

Receita Líquida

Custos Não Gerenciáveis

Custos Gerenciáveis

(PMSO)

Provisões EBITDA -2T12

Ativos e Passivos

Regulatórios

EBITDA Ajustado -

2T121Q12 1Q13EBITD

AFinancial

ResultTaxes Others

ADJUESTED NET INCOME 1Q12 / 1Q13 (R$ MN)

Regulatory Assets and Liabilities

Regulatory Assets and Liabilities

Adjusted Net Income

1Q12

Adjusted Net Income

1Q13

LL Ajustado 4T11

Ativos e passivos

Regulatórios

1T12 EBITDA Resultado Financeiro

Impostos Outros 1T13 Ativos e passivos

Regulatórios

LL Ajustado 4T12

Lucro Líquido e Lucro Líquido Ajustado 1T12/1T13 - R$ Milhões

139

(1)

140

(78)(9)

30

(4)

79

67 145

- 43.8%

+ 4.8%

29

Dividends

2007 2008 2009 2010 2011 2012

100% 100%

76.3% 81.0%

100.0%

86.5%

50%

Minimum Dividend PolicyPayout

1S08 2S08 1S09 2S09 1S10 2S10 1S11 2S11 1S12 2S12 1S13

203

351408

187

432363 351

118182 170

92

8787

4.2%

8.2%9.9%

1.7%

8.1% 8.1%6.1%

3.4% 3.3%5.4%

2.4%

Dividend Yeld*Dividends

*Based on the closing price the day before the announcement.

Interest on Equity

257

182205

351363

432

187

408351

203

92

*Based on Net Income of the year. before IFRS adjustments

*

30

Indebtedness

*ConsideringHedge

US$/Euro 0.4%

CDI/Selic 73.3%

TJLP 24.3%

Others

2.0%

31

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 After

2022

Average Term: 4.7 years

AMORTIZATION SCHEDULE* (R$ MN)

Nominal Cost Real Cost

NET DEBTWithout Pension Fund

* Principal only

COST OF DEBT

2012201120102007 2008 2009 set/10

Custo Real Custo Nominal

Mar/13

Net Debt / EBITDA for covenants

2009 2010 2011 2012

Custo Nominal Custo Real

2009 2010 2011 2012

Custo Nominal Custo Real

2009 2010 2011 2012

Custo Nominal Custo Real

3T09 3T10 9M09 9M10Mar/13Dec/12

Custo Nominal Custo Real

2.24%

8.21%

4.87%

11.08%

4.25%

11.03%

7.73%

1.07%

357

792 759982

616394

17642 42 42

194

2009 2010

Custo Real

Custo Real

3,991.9 1

4,031.4

2.83 2.73

1 Reclassified to reflect the deconsolidation results of jointly controlled companies.

Investments

CAPEX (R$ MN)CAPEX BREAKDOWN

(R$ MN)1Q13

Generation Projects

26.9 Quality Improveme

nt13.4

Generation Maintenanc

e3.1 Others

17.2

Develop. of Distribution System

51.6

Losses Combat

44.7

Investments in Electric Assets (Distribution)

Commerc./Energy

Eficiency26.1

2008 2009 2010 2011 2012 2008 2009 2010 2011 9M11 9M1220102009

563.8

928.6

700.6

2011 2012

796.8

694.1

102.7

446.9

116.9

518.8

181.8774.8

153.8

2008 2009 2010 2011 9M11 9M121Q131Q12

131.2 127.0

11.7 35.8142.9 162.7

+13.9%

32

Why invest in Light?

Major upcoming events Integration of favelas Pro-business environment New plants investments Expansion of the existing ones Market growth

Economic Transformation in the Concession

Area

Progress in the Technology Program

New network and meters in the pacified favelas

Smart metering development“Zero Losses Area” Program

Energy Losses Reduction

Investment in Renova, Belo Monte and Guanhães (total of 477 MW)

SHP Lajes under construction.HPP Itaocara

Growth in the Generation Business

New PPAs starting in 2013 and 2014

Revenues increase with no aditional costs.

Very active trading subsidiary

Repricing of Existing Energy

Listed in “Novo Mercado” of Bovespa;

Board Committees very active Included in the Sustainability

Index (ISE) of Bovespa for the sixth year.

Best-in-Class Corporate

Governance

Sound Dividend Policy: minimum 50% of net income;

Average payout since 2007: 91%

Dividend track Record

33

Regulatory Framework

The Provisional Measure 579 was enacted on September 11, 2012 and thereafter converted into Law

12,783 providing for electric power concessions, reduction of sector charges and reasonable tariffs which

although these have not directly affected Light, as its concessions will expire only in 2026, resulted in the

following developments:

on January 24, 2013, Resolution issued by Aneel approved an average reduction of 19.63% in Light

SESA’s tariffs. For residential consumers (low voltage), the reduction was 18.10%. The measure will

have no impact on the company’s result or cash flow since it reflects an equal reduction in costs.

on the same date, the distribution of power plants energy quotas was ratified, which had their

concession renewed:

(i) but lower to the distribution companies’ contracting needs, thus, causing an involuntary

exposure, and only for Light it accounted for average 156 MW; and

(ii) made distribution companies to start sharing the hydrological risks, which before was only

supported by generation companies

As of October 2012, an adverse hydrological situation was characterized in Brazil’s electricity sector, the

basis of which is mainly hydric, enforcing the System National Operator to dispatch all the thermal power

plants available in the system, thus significantly rising the costs of distribution companies by increasing

fuel expenditures in availability agreements, increasing System Service Charges due to energy security and

acquisitions on the spot market in order to answer that involuntary exposure.

34

On March 8, 2013, the federal government issued the Decree 7,945 preventing the coverage of part of the non-

manageable costs not covered by the 2013 tariff, through the resources transferred from the Energetic Development

Accout (CDE) for the following costs:

System Service Charge (ESS) – The monthly transfer will be determined by the amounts settled in the

CCEE.

Involuntary Exposure associated with the quotas – The monthly CDE transfer will cover the difference

between the difference settlement price (PLD) and the tariff of the repositioning amount recognized in Light’s

last tariff adjustment.

Hydrological Risk - The net monthly amount settled in the CCEE will be transferred directly via the CDE.

It is worth mentioning that the amounts approved for Light reflect the methodology approved by Aneel on May 6th, 2013.

Regulatory Framework

1T13 sem decreto

CDE 1T13 1T12CDEtransfer

1Q13without Decree

1Q13 1Q12

362.2

144.9

267.1

371.0

225.7

291.970.4

144.9

267.1

371.0

225.7

27.2122.8235.4

362.1

70.7

1,370.9

1,079.9

818.2

ENERGY PURCHASE (R$ MN)

Availability Contracts

Other Auctions

Norte Fluminense

ItaipuSpot

1T13 sem decreto

CDE 1T13 1T12CDEtransfer

1Q13Without Decree

1Q13 1Q12

ESS Transport Other Charges

215.3

52.8

46.1

79.0

52.8

46.1

23.5

130.9

49.5

136.3

314.2

177.9203.9

CHARGES AND TRANSPORT (R$ MN)

+ 31.9%

-12.8%

35

R$ 2.7 billion (nominal terms) invested during the current cycle (2008-2013)

Capitalization improvement driven by simulations

Physical-accounting assets concilliation

Constant interactions with Aneel staff, including site visits

Intensive training of teams for correct accounting records

Accounting system blocked against input errors

Aiming the flexibility of the regulatory target, based on Aneel’s excepcionality criteria:

large gap between actual and regulatory level of losses;

social and economic conditions hindered the achievement of the target; and

there are no comparable peer companies with lower level of losses.

Non-Technical LossesRemuneration Asset Base

36

2013 Tariff Review Critical Issues

2013 Tariff Review Schedule

Date Event

July 16 Aneel forwards first proposal (without remuneration and depreciation) to the concessionary and to the consumers representatives

August 01 Internet presentation of the Tariff Review Proposal prepared by Aneel

From Aug/5 to Aug/16 Regulatory Asset Base fiscalization

September 05 Public Hearing

October 03 Aneel forwards new proposal consolidated to the concessionary and to the consumers representatives

October 24 Aneel Board Meeting

November 07 Periodic Tariff Review Date

37

Important Notice

This presentation may include declarations that represent forward-looking statements according to Brazilian regulations and international movable values. These declarations are based on certain assumptions and analyses made by the Company in accordance with its experience, the economic environment, market conditions and future events expected, many of which are out of the Company’s control. Important factors that can lead to significant differences between the real results and the future declarations of expectations on events or business-oriented results include the Company’s strategy, the Brazilian and international economic conditions, technology, financial strategy, developments of the public service industry, hydrological conditions, conditions of the financial market, uncertainty regarding the results of its future operations, plain, goals, expectations and intentions, among others. Because of these factors, the Company’s actual results may significantly differ from those indicated or implicit in the declarations of expectations on events or future results.

The information and opinions herein do not have to be understood as recommendation to potential investors, and no investment decision must be based on the veracity, the updated or completeness of this information or opinions. None of the Company’s assessors or parts related to them or its representatives will have any responsibility for any losses that can elapse from the use or the contents of this presentation.

This material includes declarations on future events submitted to risks and uncertainties, which are based on current expectations and projections on future events and trends that can affect the Company’s businesses. These declarations include projections of economic growth and demand and supply of energy, in addition to information on competitive position, regulatory environment, potential growth opportunities and other subjects. Various factors can adversely affect the estimates and assumptions on which these declarations are based on.

38

Contacts

João Batista Zolini CarneiroCFO and IRO

Luiz Felipe Negreiros de SáSuperintendent of Finance and Investor Relations

+55 21 2211 2814 [email protected]

Gustavo WerneckIR Manager

+ 55 21 2211 [email protected]

www.light.com.br/ri

39