Corporate Presentation - Galane Gold: Home – a massive pipe shaped body with a thickness of 35m...

25

Corporate Presentation TSX - V :GG AN UNHE DGE D, LOW RISK GOLD PRODUCE R

Transcript of Corporate Presentation - Galane Gold: Home – a massive pipe shaped body with a thickness of 35m...

Corporate Presentation

T S X - V : G G A N U N H E D G E D , L O W R I S K G O L D P R O D U C E R

Corporate Overview

2

1 See Note 1 on slide 7 2 This is a forward looking statement and is based on a number of assumptions, including Galane’s ability to generate sufficient cash to fund the exploration program.

3 See slide 8 for further details

Low cost production growth from the recently acquired Galaxy Mine1, 2.

Phased, low-cost gold production expansion to over 60,000 oz Au/year at AISC below US$400/oz

M&I resources of 602,696 oz Au at 3.01 g/t Au. Inferred resource of 886,199 oz Au at 3.40 g/t Au

Operating improvements at the Mupane Mine2

Improved grades, higher recoveries and consistent ore supply forecast to increase annual gold production to over 30,000 oz and decrease AISC to US$980/oz Au

Substantial exploration upside3

Excellent potential to expand gold resources at the Galaxy Mine to over 4.0 million oz

Mupane owns ~90% of the highly prospective, 1,200 km2 Tati Greenstone Belt area

Excellent re-rating potential and leverage to rising gold prices Trading at a fraction of the P/NAV multiples of other gold producers in Africa

Opportunity to quickly expand production at a low capital cost at higher gold prices

Experienced management team Extensive mine operating experience and exploration expertise in Botswana and South Africa

1

2

3

4

5

Galane Capital Structure

3

Share Price (September 1, 2016) C$0.11

Basic Shares Outstanding 142,628,884

Stock Options1 12,155,000

NLE Contingency Shares2 7,375,000

Deferred Share Units 3,749,044

Warrants3 4,076,598

Fully Diluted Shares Outstanding 170,084,526

Basic Market Capitalization4 C$15.7 million

Cash US$2.4 million

Debt (see appendix) US$14.9 million

Capital Structure Ownership Breakdown

Galane Share Price Performance against the ETF Market Vector Junior Gold Miners

1. Outstanding options have a weighted average exercise price of C$0..22/share and a weighted average time to expiration of 2 years from year-end December 31, 2015

2. Galane is obligated to issue up to 8,750,000 additional common shares to shareholders relating to the NLE Properties. dependent upon reaching certain milestones . All of the shares will be issuable if the company reports over

1,000,000 M&I NI 43-101 compliant ounces on the former NLE properties in Botswana. On April 7th, 2014 the company issued 1,375,000 NLE Contingency Shares

3. Outstanding warrants have an exercise price of C$0.102/share and expire on November 30, 2019

4. As of September 1, 2016 closing price.

Galaxy and Mupane

4

Galaxy Gold Property3

Location • Barberton in Northeastern South Africa

Ownership • 74% - Acquired in November and December

2015 with a mandatory offer for remaining

shares commenced

Operating

History

• Production commenced in 1884 and through

to date approximately 1.3 million oz Au

mined2

Resources • 602,696 oz Au Measured and Indicated and

886,199 oz Au Inferred (as of August 2015)

Type • Conventional gold mine with mill and carbon-

in-leach processing

Mine Life • Technical report indicates 9 years but new

prefeasibility study to be commenced to

hopefully extend beyond that.

Production

Forecast

• Average of over 15,000 oz Au per annum

• US$688 / oz all-in cost1 in Technical Report

(based on an exchange rate of ZAR

11.70/US$ 1)

BIOX Plant

Main Offices

1 Non-GAAP measure. See “Non-GAAP Measures” below. 2 See Note 1 on slide 7 3 See the Technical Report titled "A Technical Report on the Galaxy Gold Mine, Mpumalanga Province, South Africa" issued on January 4, 2016 with an effective date of September 1, 2015, a copy of which is

available under Galane’s profile on SEDAR at www.sedar.com (the “Galaxy Technical Report”).

5

Why Galaxy

6

• Near term production asset with

existing mine and processing facilities

• Cost is a fraction of replacement cost

• Ability to increase production in easy

manageable steps with minimal capital

requirements

• Ability to increase resource

substantially

• Greenbelt underground project which

is a good fit with our existing property

Mupane both in location and skill set

• Surrounded by prospective targets

Galaxy History

• Jack Greaves was a prospector from the UK and discovered

gold at Galaxy in 1888.

• The mine was originally named Agnes Gold after his wife

Jessie Agnes.

• Galaxy in various forms has now existed for over 120 years

and has produced over 1.3 million ounces of gold

7

(1) The historical estimates set out in the table above (the “Historical Estimate”) were disclosed in a report provided by Ga laxy to Galane entitled “Anhaeusser, C R (1986). Archean Mineralization in the Barberton Mountainland. Mineral Deposits of

Southern Africa. Volume 1. (GSSA) and Cluff Mining : AGNES GOLD MINE – BIOLOGICAL LEACHING OF REFRACTORY ORE RESOURCES - PRE-FEASIBILITY STUDY”. The Historical Estimate was prepared in accordance with the South African

Code for the Reporting of Exploration Results, Mineral Resources and Mineral Reserves and does not comply with the CIM Defini tion Standards on Mineral Resources and Mineral Reserves as required by National Instrument 43-101 – Standards of

Disclosure for Mineral Projects (“NI 43-101”). A qualified person has not done sufficient work to classify the Historical Estimate as a current mineral resource in accordance with NI 43- 101 and the issuer is not treating the Historical Estimate as a current

mineral resource.

Galaxy Location

8

Pan African Mines

Barberton is Pan African’s flagship

gold project, producing 115,000 oz per

year at an average cash cost of

approximately US$778/oz. It has a

total of 2.8 million ounces of measured

indicated and inferred mineral

resources.1

Vantage Goldfields

Vantage annual production is

around 30,000 oz per year at an

average cash cost of approximately

US$861/oz. It has a total of 1.9

million ounces of measured

indicated and inferred mineral

resources.2

The Barberton

Greenstone belt

is part of the

Kaapvaal craton

which also

covers our

mining

operation in

Botswana.

1 Pan African Mineral Resource and Mineral Reserves Report, 2014 (as at June 30, 2014). 2 www.vantagegoldfields.com 3 There is no guarantee that Galane will generate similar results at the Galaxy Gold Mine.

9

Mining Licence Detail

1 See the Galaxy Technical Report, a copy of which is available under Galane’s profile on SEDAR at www.sedar.com .

10

Mineral Resource1

11

Processing Plant

• Current plant can process 500 tonnes

per day

• Conventional crush, mill, flotation

followed by CIL plant.

• Operational tailings dam

• BIOX plant was in production but will

need to be restarted or alternative

oxidation process acquired to improve

recovery.

• Prefeasibility study to commence to

support Plant Capacity expansion in

two stages in Year 4 to 1,100tpd and

then Year 8 to 1,500tpd.

• Galaxy – a massive pipe shaped body with a thickness of 35m and a strike of around 100m. Mining

may be carried out using mechanised long hole stoping.

• Woodbine and Giles – both narrow steeply dipping with a thickness of up to 2.4m and a strike of

900m. Mining may be carried out using a fully mechanised cut and fill method.

• Princeton – a steeply dipping body with a thickness of 2m and a strike of 300m. Mining in the

Technical Report envisages a fully mechanised long hole stoping method.

12

Mining Methods1

1 See the Galaxy Technical Report, a copy of which is available under Galane’s profile on SEDAR at www.sedar.com .

Mining

13

Current Infrastructure

• Adit access to all mineral bodies

• Rail bound and trackless equipment

• Functional shaft to 700 m

• Mining sub-contractor with available

mining fleet

• 21 houses and hostel for employees

Work to commence on a new

prefeasibility study for the following

planned infrastructure amendments

• Year 4 plan to owner operate

underground mining

• Additional adit access

Exploration Plan1,2 - 4,000,000 ozs Au

14

1 In house drilling plan dependent upon generating sufficient free cash flows from operations to fund with no guarantees additional ounces will be discovered. 2 Previous exploration has been used to outline an exploration target of 30.1 million tonnes grading 3.0 to 5.0 g/t (2.9 to 4.8 million oz Au). The potential quantity and grades are conceptual in nature and are based on previous drill results that defined the approximate length, thickness, depth and grade of the portion of the historic resource estimate. There has been insufficient exploration to define a current resource and the Company cautions that there is a risk further exploration will not result in the delineation of a current mineral resource.

Mupane Gold Property

Location • 30 km SE of Francistown (population

~100,000) in Northeastern Botswana

Ownership • 100% - Acquired from IAMGOLD in August of

2011

Operating

History

• Production commenced in 2005 and through

September 30, 2014 there has been a total of

640,606 oz. Au mined

Resources • 422,207 oz Au Measured and Indicated and

213,454 oz Au Inferred (as of Dec 31,

2015)(2)

Type • Conventional gold mine with mill and carbon-

in-leach processing

Mine Life • Currently 5+ years; with opportunity to

significantly extend

Production

Forecast

• Average of 32,000 oz Au per annum

• Approximately $1,050 / oz all-in cost on

5 year plan (incl. operating, capex,

exploration, royalties) (1)

Mupane Gold Mine

Processing Plant

(1) Non-GAAP measure. See “Non-GAAP Measures” below.

15

(2) Measured and Indicated includes 6,227,000 tonnes at 1.53 g/t and 9,639,000 tonnes at 0.35 g/t for the tailings dam . Inferred is 4,330,000 tonnes at 1.53 g/t

Mupane Land Package

16

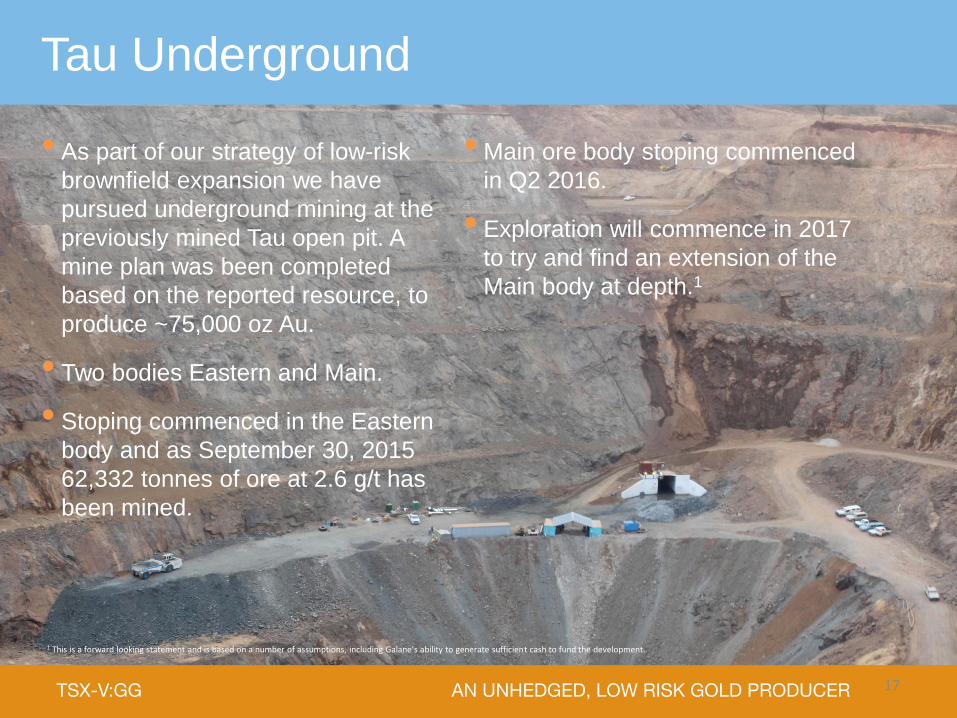

Tau Underground

17

• As part of our strategy of low-risk

brownfield expansion we have

pursued underground mining at the

previously mined Tau open pit. A

mine plan was been completed

based on the reported resource, to

produce ~75,000 oz Au.

• Two bodies Eastern and Main.

• Stoping commenced in the Eastern

body and as September 30, 2015

62,332 tonnes of ore at 2.6 g/t has

been mined.

• Main ore body stoping commenced

in Q2 2016.

• Exploration will commence in 2017

to try and find an extension of the

Main body at depth.1

1 This is a forward looking statement and is based on a number of assumptions, including Galane’s ability to generate sufficient cash to fund the development..

Low Grade Stockpiles

18

• 471,000 tonnes of low grade stockpile

at an average grade of 0.85 g/t.

• There is a further 1.1 million tonnes of

sub grade at an estimated grade of

0.70 g/t.

• Screening plant installed in 2014 can

upgrade by approximately 10% the

sulphide stockpiles.

Exploration Potential

19

20

Ravi Sood

Chairman

• Chairman of Feronia Inc., one of Africa’s oldest operating companies and

largest employers

• Former CEO of Navina Asset Management, a Toronto based investment firm

that was acquired by a major financial institution

• Canadian

Nicholas Brodie

CEO & Director

• 22 years experience in accounting, with 8 years in Africa, including the last 7

years focused on the mining industry in Africa

• Former CFO of Katanga Mining, Financial Advisor to Metallon Gold,

CFO of Copperbelt Energy Corporation, Head of Finance at Cinergy

and Financial Controller of Total SA in the UK

• British

Wayne

Hatton Jones

Chief Operating

Officer & Director

• Mining Professional with 26 years experience in Africa, Asia and Europe

• Former GM (Goldridge), COO (Galaxy Gold), GM Metallurgy (Avocet),

Process Manager (Randgold) and Metallurgical Manager (Harmony)

• B.Sc. (Witwatersrand), MDP (University of South Africa)

• South African

Management Team

21 21

Charles Byron

Chief Geologist

• 30+ years as geologist focused on Archean gold exploration

• Previously with Phelps Dodge, Falconbridge and Gallery Gold, where he led the team that

discovered the Mupane Gold Deposit and saw it into production in 2004

• B.Sc. (Hons) Geology, Soils, Geography (University of Natal)

• Motswana (Botswana)

Kevin Crossling

Business

Development

• Mining Professional with 13 years experience in progressively snr roles

• Former Operations Mgr (Allied Gold), Geology Manager (St Barbara), Principle Geologist

(Geocross), Mineral Resource Manager (Pilanesberg)

• B.Sc. (Hons) Geology

• South African

Cedric Sam

Mining

Manager

• Mining Engineer with 17 years of experience

• Inspector of Mines & Explosives with Dept of Mines, Manager Mine Planning with Tati Nickel

Mining Company and Mining Manager with African Copper Mining

• BSc in Mining Engineering from the Queens University in Kingston, Ontario, Canada

• Motswana

Management Team

Investment Highlights

22

Immediate Leverage to Spot Gold

Unhedged gold producer

Free operating cash flow

from current Mupane LOM

plan

Ability to size production to

prevailing gold price and

remain nimble1

Exploration Upside

Control virtually 100% of

the Tati Greenstone belt

Substantial portfolio of drill-

ready targets at Galaxy

Potential to increase

reported resource to over 4

million oz.1

Skilled & Trusted Management Team

Strong operators with the

know-how to optimize and

expand production

The Company successfully

put Tau Underground into

production in less than 6

months.

Compelling Valuation Prospect

Current Valuation

Gold Price

Exploration New Valuation

Galaxy Production

1 This is a forward looking statement and is based on a number of assumptions, including generating sufficient funds to undertake exploration program, prevailing gold price and economic production and different

production levels.

Cautionary Statements

Certain statements contained in this presentation constitute “forward-looking statements.” All statements other than statements of historical fact contained in this presentation, including,

without limitation, those regarding Galane Gold’s results of operations, strategy, plans, objectives, goals and targets, and any statements preceded by, followed by or that include the

words “believe”, “expect”, “aim”, “intend”, “plan”, “continue”, “will”, “may”, “would”, “anticipate”, “estimate”, “forecast”, “predict”, “project”, “seek”, “should” or similar expressions or the

negative thereof, are forward-looking statements. These statements are not historical facts but instead represent only Galane Gold’s expectations, estimates and projections regarding

future events. These statements are not guarantees of future performance and involve assumptions, risks and uncertainties that are difficult to predict. Therefore, actual results may

differ materially from what is expressed, implied or forecasted in such forward-looking statements.

Additional factors that could cause actual results, performance or achievements to differ materially include, but are not limited to: Galane Gold’s dependence on two mineral projects;

gold price volatility; risks associated with the conduct of Galane Gold’s mining activities in Botswana and South Africa; regulatory, consent or permitting delays; risks relating to Galane

Gold’s exploration, development and mining activities being situated in two countries; risks relating to reliance on Galane Gold’s management team and outside contractors; risks

regarding mineral resources and reserves; Galane Gold’s inability to obtain insurance to cover all risks, on a commercially reasonable basis or at all; currency fluctuations; risks

regarding the failure to generate sufficient cash flow from operations; risks relating to project financing and equity issuances; risks arising from Galane Gold’s fair value estimates with

respect to the carrying amount of mineral interests; mining tax regimes; risks arising from holding derivative instruments; Galane Gold’s need to replace reserves depleted by

production; risks and unknowns inherent in all mining projects, including the inaccuracy of reserves and resources, metallurgical recoveries and capital and operating costs of such

projects; contests over title to properties, particularly title to undeveloped properties; laws and regulations governing the environment, health and safety; operating or technical

difficulties in connection with mining or development activities; lack of infrastructure; employee relations, labour unrest or unavailability; health risks in Africa; Galane Gold’s interactions

with surrounding communities and artisanal miners; Galane Gold’s ability to successfully integrate acquired assets; the speculative nature of exploration and development, including the

risks of diminishing quantities or grades of reserves; development of Galane Gold’s exploration properties into commercially viable mines; stock market volatility; conflicts of interest

among certain directors and officers; lack of liquidity for shareholders of Galane Gold; risks related to the market perception of junior gold companies; and litigation risk. Details of

certain of the risk factors relating to Galane Gold are discussed under the heading “Risks and Uncertainties” in Galane Gold’s annual management’s discussion and analysis for the

year ended December 31, 2014, a copy of which is available on Galane Gold’s SEDAR profile at www.sedar.com. Management provides forward-looking statements because it

believes they provide useful information to readers when considering their investment objectives and cautions readers that the information may not be appropriate for other purposes.

Consequently, all of the forward-looking statements made in this presentation are qualified by these cautionary statements and other cautionary statements or factors contained herein,

and there can be no assurance that the actual results or developments will be realized or, even if substantially realized, that they will have the expected consequences to, or effects on,

Galane Gold. These forward-looking statements are made as of the date of this presentation and Galane Gold assumes no obligation to update or revise them to reflect subsequent

information, events or circumstances or otherwise, except as required by law.

The forward-looking statements in this presentation are based on numerous assumptions regarding Galane Gold’s present and future business strategies and the environment in which

Galane Gold will operate in the future, including assumptions regarding gold prices, business and operating strategies, and Galane Gold’s ability to operate on a profitable basis.

23

Cautionary Statements

For more information regarding the mineral resource figures and technical information set out in this presentation, please refer to: (i) the news release dated March 18, 2013 entitled

“Galane Gold Ltd. Announces a Mineral Resource Update For its Botswana Properties”; (ii) the news release dated February 5, 2013 entitled “Galane Gold Ltd. Releases Drilling

Results from the Jim’s Luck Project That Shows Significant Gold Mineralization from Surface Open at Depth and Along Strike”; (iii) the news release dated October 31, 2013 entitled

“Galane Gold Ltd. Announces Mineral Resources at the Tekwane Prospect”; (iv) the news release dated August 5, 2014 entitled “Galane Gold Ltd. Commissions New Screening Plant

to Process Seven Hundred Thousand Tonnes of Low Grade Ore”; (v) the news release dated November 20, 2015 entitled “Galane Gold Ltd. Completes Acquisition of Galaxy Gold

Mining Limited; (vi) the news release dated January 26, 2016 entitled “Galane Gold Ltd. Files Technical Report for Galaxy Gold Mine”; (vii) the technical report in respect of the Mupane

Property entitled “Independent Technical Report on the Mupane Gold Mine” dated May 10, 2011; and (viii) the technical report in respect of the Galaxy Gold Mine entitled "A Technical

Report on the Galaxy Gold Mine, Mpumalanga Province, South Africa" issued on January 4, 2016 with an effective date of September 1, 2015, each of which is available under Galane

Gold’s profile on SEDAR at www.sedar.com.

Economic assessments in this presentation are preliminary in nature and include inferred mineral resources that are considered to be too speculative geologically to have the economic

considerations applied to them that would enable them to be categorized as mineral reserves. There is no certainty that the economic assessments will be realized. Mineral resources

are not mineral reserves and do not have demonstrated economic viability. There is no guarantee that any of the mineral resources disclosed in this presentation will be converted to

mineral reserves. There is also no guarantee that any of the inferred mineral resources will be upgraded to measured or indicated mineral resources. Information of a technical and

scientific nature that forms the basis of the disclosure in this presentation has been approved by Charles Byron Pr. Sci. Nat., MAusIMM., MGSSA and Chief Geologist for Galane Gold,

and a “qualified person” as defined by NI 43- 101.

Non-GAAP Measures

The presentation often refers to earnings from mining operations per ounce, total operating cash cost excluding royalties per ounce, direct cash cost per ounce, all in cash cost per

ounce and cash flows from operations before working capital adjustments, all non-GAAP performance measures, in order to provide investors with information about measures used by

management to monitor performance. This information is used to assess how well the producing gold mines are performing compared to plan and prior periods, and also to assess the

overall effectiveness and efficiency of gold mining operations. Cash cost figures are calculated in accordance with a standard developed by the Gold Institute, which was a worldwide

association of suppliers of gold and gold products and included leading North American gold producers. The Gold Institute ceased operations in 2002, but the standard is still an

accepted standard of reporting cash costs of gold production in North America. Adoption of the standard is voluntary, and the cost measures presented herein may not be comparable

to other similarly titled measures of other companies. Cash cost includes mine site operating costs such as mining, processing, administration, and attributable realized derivative gain

or loss, but are exclusive of amortization, reclamation, and exploration and development costs. Cash cost excluding royalties is cash cost less royalties. Operating cash cost is the total

cash cost less those costs capitalized as attributable to the removal of excess waste in developing new resources. Operating cash cost excluding royalties is operating cash cost less

royalties. These costs are then divided by the Company’s ounces of gold produced to arrive at the cash cost measures on a per ounce basis. These measures, along with sales, are

considered to be key indicators of a company’s ability to generate operating earnings and cash flow from its mining operations. These measures of cash costs do not have any

standardized meaning prescribed by IFRS and differ from measures determined in accordance with IFRS. They are intended to provide additional information and should not be

considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS. These measures are not necessarily indicative of net earnings or cash flow

from operations as determined under IFRS.

24

25

Contact Info

Ravi Sood Chairman

Mobile: +1 647 987 7663

Nick Brodie Chief Executive Officer

Mobile +44 7905089878

Investor Relations [email protected]

Mobile: +44 7905089878

TSX-V:GG ANUNHEDGED,LOWRISKGOLDPRODUCER