Corporate Presentation 3Q 2014 - Bci Personas€¦ · CorporateCorporate Presentation Presentation...

25

Corporate Presentation 2013 Corporate Presentation 2014 Clic para editar título Corporate Presentation 2014 Banco Crédito e Inversiones Corporate Presentation 3Q 2014 December 2014

Transcript of Corporate Presentation 3Q 2014 - Bci Personas€¦ · CorporateCorporate Presentation Presentation...

Corporate Presentation 2013 Corporate Presentation 2014

Clic para editar título

Corporate Presentation 2014

Banco Crédito e Inversiones

Corporate Presentation 3Q 2014

December 2014

Corporate Presentation 2013 Corporate Presentation 2014

Content: 1. Main macroeconomic indicators

2. Chilean Financial System

3. Bci Financial Results

2

Corporate Presentation 2013 Corporate Presentation 2014

Chilean main

macroeconomic indicators

Corporate Presentation 2013 Corporate Presentation 2014

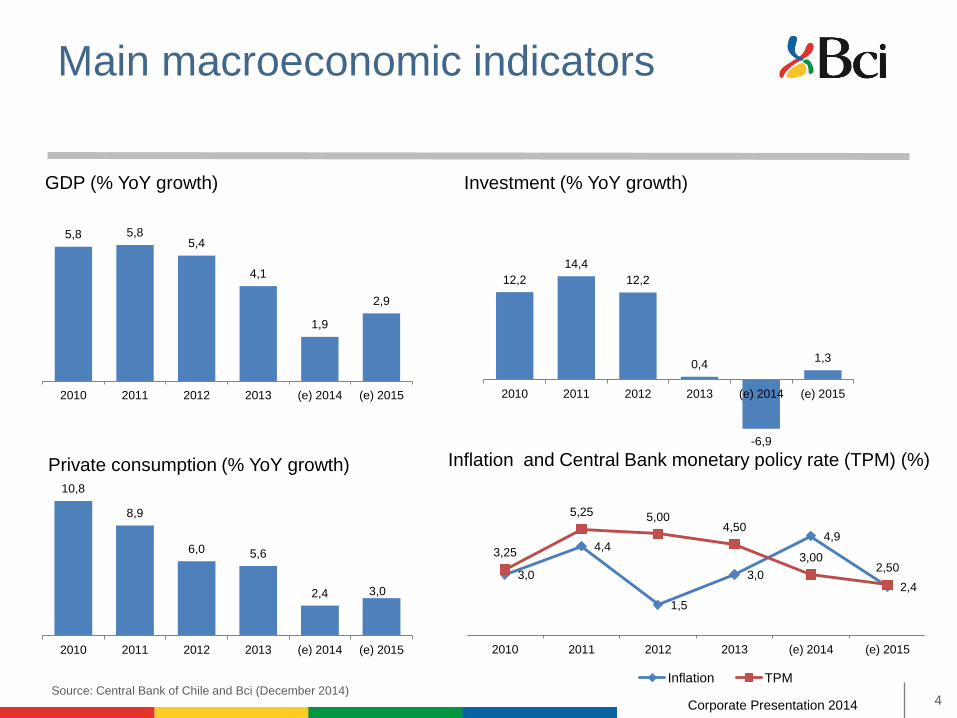

5,8 5,8 5,4

4,1

1,9

2,9

2010 2011 2012 2013 (e) 2014 (e) 2015

Main macroeconomic indicators

10,8

8,9

6,0 5,6

2,4 3,0

2010 2011 2012 2013 (e) 2014 (e) 2015

Private consumption (% YoY growth)

GDP (% YoY growth)

12,2

14,4

12,2

0,4

-6,9

1,3

2010 2011 2012 2013 (e) 2014 (e) 2015

Investment (% YoY growth)

Source: Central Bank of Chile and Bci (December 2014) 4

3,0

4,4

1,5

3,0

4,9

2,4

3,25

5,25 5,00 4,50

3,00 2,50

2010 2011 2012 2013 (e) 2014 (e) 2015

Inflation TPM

Inflation and Central Bank monetary policy rate (TPM) (%)

Chilean Financial System

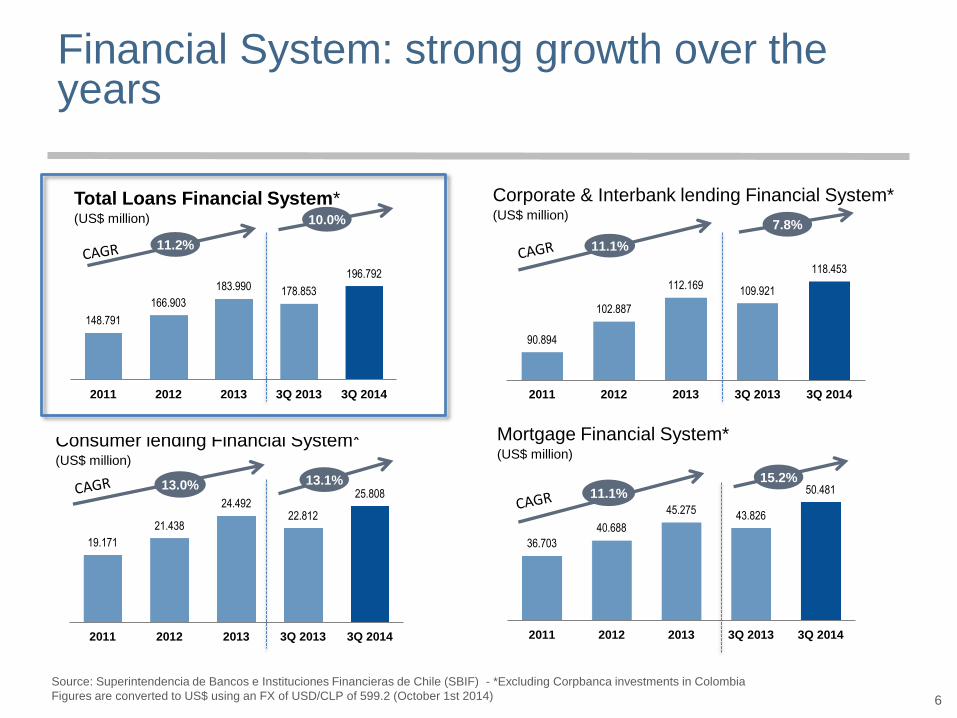

19.171

21.438

24.492 22.812

25.808

2011 2012 2013 3Q 2013 3Q 2014

Consumer lending Financial System* (US$ million)

90.894

102.887

112.169 109.921

118.453

2011 2012 2013 3Q 2013 3Q 2014

148.791

166.903

183.990 178.853

196.792

2011 2012 2013 3Q 2013 3Q 2014

36.703

40.688

45.275 43.826

50.481

2011 2012 2013 3Q 2013 3Q 2014

Financial System: strong growth over the years

11.2%

Total Loans Financial System* (US$ million)

6

11.1%

13.0% 11.1%

Corporate & Interbank lending Financial System* (US$ million)

Mortgage Financial System* (US$ million)

Source: Superintendencia de Bancos e Instituciones Financieras de Chile (SBIF) - *Excluding Corpbanca investments in Colombia

Figures are converted to US$ using an FX of USD/CLP of 599.2 (October 1st 2014)

13.1%

7.8% 10.0%

15.2%

Healthy and well capitalized Financial System

Source: Superintendencia de Bancos e Instituciones Financieras de Chile (SBIF)

Tier I according to Basel I

Regulatory capital= Basic capital (paid-in capital + reserves) + subordinated bonds + voluntary allowances for loan losses

2,37%

2,20% 2,12%

2,17% 2,13%

2011 2012 2013 3Q13 3Q14

10,1% 9,9% 9,6% 9,4% 9,6%

13,9% 13,3% 13,3% 12,9% 13,3%

2011 2012 2013 Aug 2013 Aug 2014

Tier I

Regulatory capital/Risk weighted assets

NPL Ratio Financial System

7

Banco Crédito e Inversiones

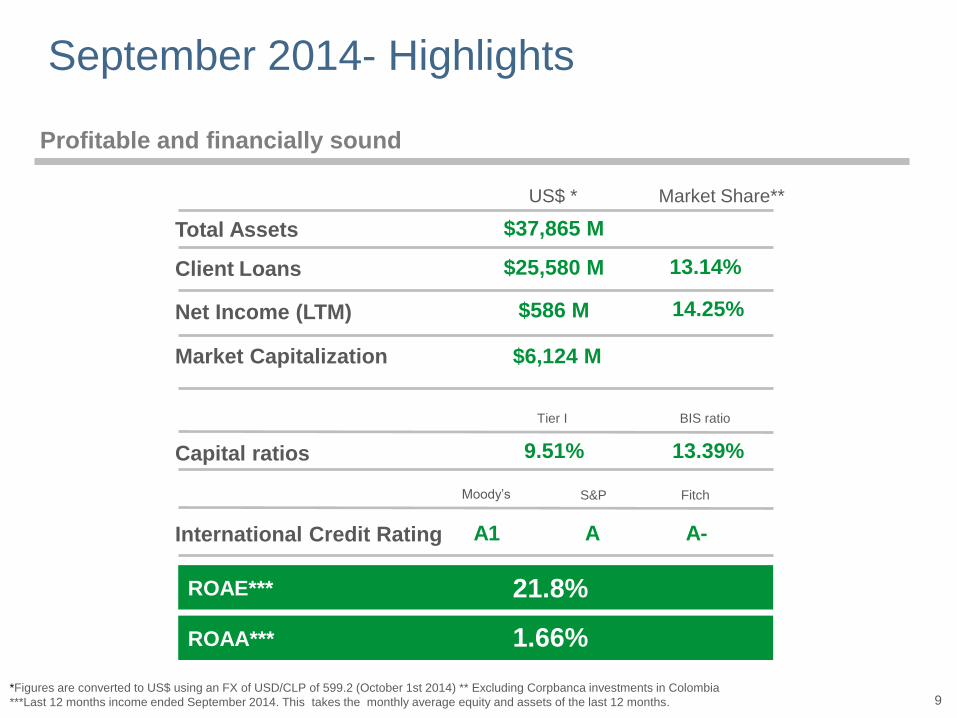

September 2014- Highlights

*Figures are converted to US$ using an FX of USD/CLP of 599.2 (October 1st 2014) ** Excluding Corpbanca investments in Colombia

***Last 12 months income ended September 2014. This takes the monthly average equity and assets of the last 12 months.

US$ * Market Share**

$586 M Net Income (LTM) 14.25%

Client Loans $25,580 M 13.14%

Total Assets $37,865 M

Market Capitalization $6,124 M

9.51%

Tier I BIS ratio

Capital ratios 13.39%

International Credit Rating

Moody’s S&P Fitch

ROAE*** 21.8%

A1 A A-

Profitable and financially sound

9

ROAA*** 1.66%

Selected awards and accolades

1st place 2014

Customer Experience (second year)

IZO

10

7th place 2014

Best Companies to work for in Chile

Great Place to Work

1st place in Chile 2014

• Banking group (Third year) • Private Banking (Third year) •Sustainable Banks • Asset Management (Second year)

2nd place 2014

Corporate Transparency

Local dynamos 2014

Among the 50 most successful local companies

in Emerging Markets

The Boston Consulting Group (BCG)

1st place 2014- Financial System

Customer loyalty index (NPS)

Alco – Diario Estrategia

1st place 2014

Corporate Social Responsibility

Prohumana Foundation

1st place 2014

Most responsible companies and with Best corporate governance MERCO

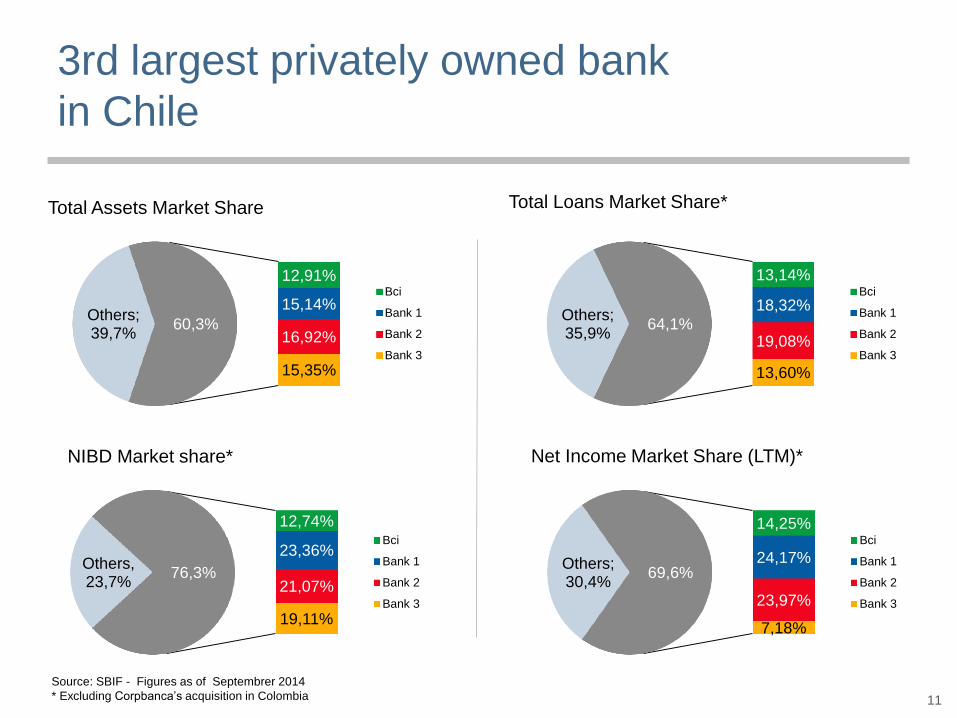

Others; 39,7%

12,91%

15,14%

16,92%

15,35%

60,3%

Bci

Bank 1

Bank 2

Bank 3

3rd largest privately owned bank

in Chile

Source: SBIF - Figures as of Septembrer 2014

* Excluding Corpbanca’s acquisition in Colombia

Total Assets Market Share

NIBD Market share*

Others, 23,7%

12,74%

23,36%

21,07%

19,11%

76,3%

Bci

Bank 1

Bank 2

Bank 3

11

Others; 35,9%

13,14%

18,32%

19,08%

13,60%

64,1%

Bci

Bank 1

Bank 2

Bank 3

Total Loans Market Share*

Net Income Market Share (LTM)*

Others; 30,4%

14,25%

24,17%

23,97%

7,18%

69,6%

Bci

Bank 1

Bank 2

Bank 3

Corporate Presentation 2013 Corporate Presentation 2014 Corporate Presentation 2014

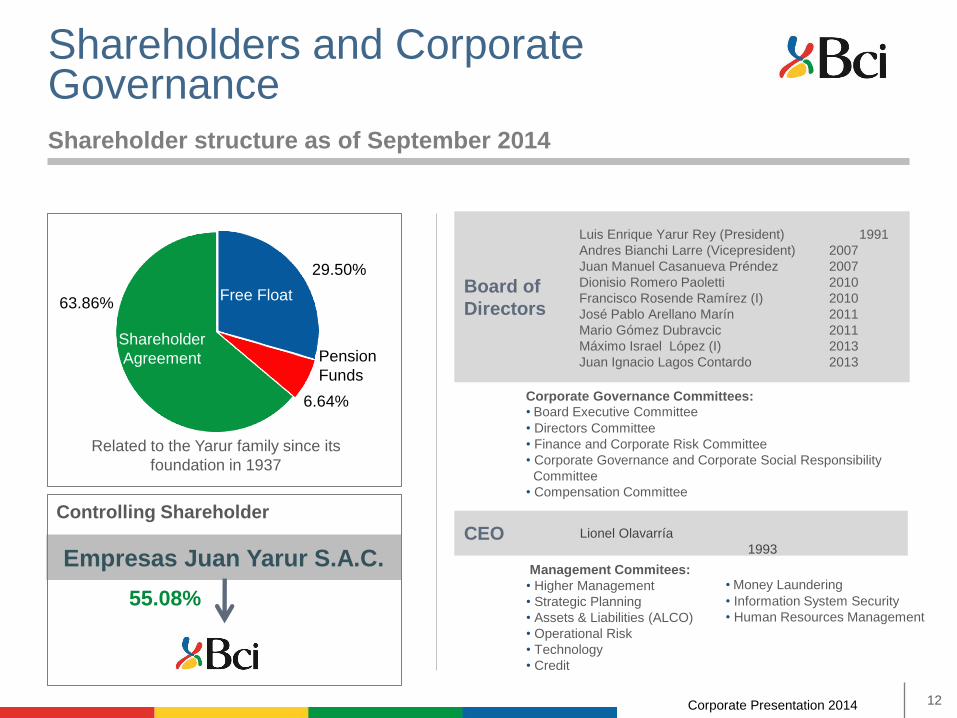

Shareholders and Corporate Governance

Empresas Juan Yarur S.A.C.

Shareholder structure as of September 2014

29.50%

6.64%

63.86%

Shareholder

Agreement Pension

Funds

Related to the Yarur family since its

foundation in 1937

55.08%

Controlling Shareholder

Management Commitees:

• Higher Management

• Strategic Planning

• Assets & Liabilities (ALCO)

• Operational Risk

• Technology

• Credit

Board of

Directors

CEO

Luis Enrique Yarur Rey (President) 1991

Andres Bianchi Larre (Vicepresident) 2007

Juan Manuel Casanueva Préndez 2007

Dionisio Romero Paoletti 2010

Francisco Rosende Ramírez (I) 2010

José Pablo Arellano Marín 2011

Mario Gómez Dubravcic 2011

Máximo Israel López (I) 2013

Juan Ignacio Lagos Contardo 2013

Lionel Olavarría

1993

Corporate Governance Committees:

• Board Executive Committee

• Directors Committee

• Finance and Corporate Risk Committee

• Corporate Governance and Corporate Social Responsibility

Committee

• Compensation Committee

12

• Money Laundering

• Information System Security

• Human Resources Management

Free Float

Corporate Presentation 2013 Corporate Presentation 2014 Corporate Presentation 2014

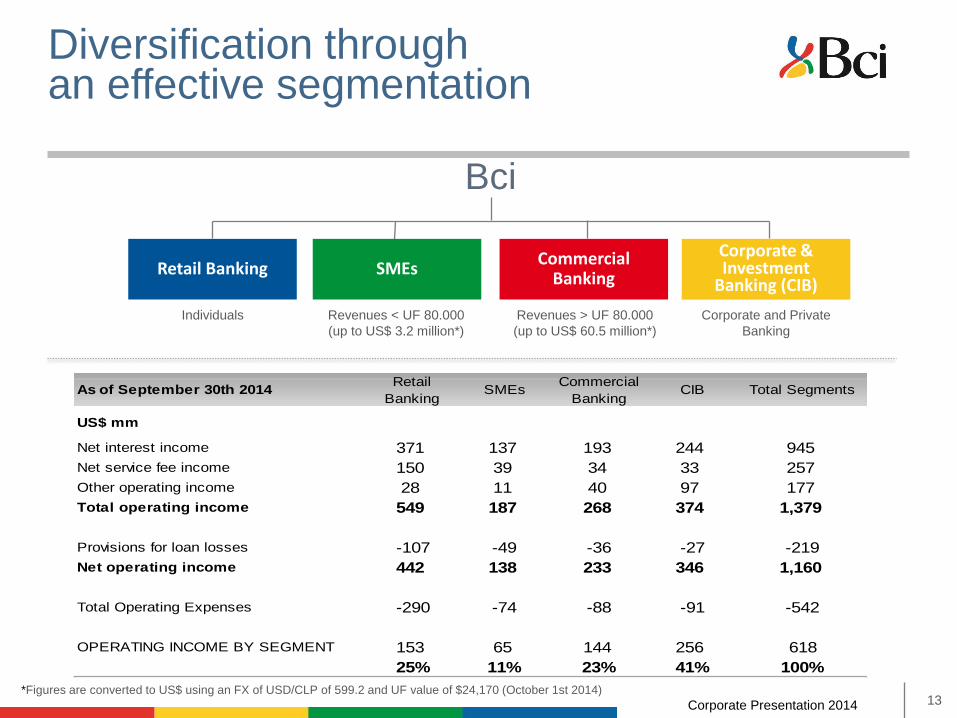

Diversification through an effective segmentation

SMEs Commercial

Banking

Corporate & Investment

Banking (CIB) Retail Banking

Revenues > UF 80.000

(up to US$ 60.5 million*)

Individuals Revenues < UF 80.000

(up to US$ 3.2 million*)

Corporate and Private

Banking

Bci

13 *Figures are converted to US$ using an FX of USD/CLP of 599.2 and UF value of $24,170 (October 1st 2014)

As of September 30th 2014Retail

BankingSMEs

Commercial

BankingCIB Total Segments

US$ mm

Net interest income 371 137 193 244 945

Net service fee income 150 39 34 33 257

Other operating income 28 11 40 97 177

Total operating income 549 187 268 374 1,379

Provisions for loan losses -107 -49 -36 -27 -219

Net operating income 442 138 233 346 1,160

Total Operating Expenses -290 -74 -88 -91 -542

OPERATING INCOME BY SEGMENT 153 65 144 256 618

25% 11% 23% 41% 100%

Corporate Presentation 2013 Corporate Presentation 2014 Corporate Presentation 2014

Miami Branch + (**

National and international presence

Representation office in Mexico City

Representation office in Lima, Peru

Representation office in Sao Paulo, Brazil

Representation office in Bogotá, Colombia

Business Desk in Madrid, Spain

SOUTH Regions VII to XII and XIV

Antartic included

76 CCP

NORTH Regions I to IV and XV

55 CCP

CENTER Regions V, VI and RM

233 CCP

Presence in 6 countries 364

14

Nacional Commercial Contact Points (CCP):

* Pending US regulatory approval

Corporate Presentation 2013 Corporate Presentation 2014 Corporate Presentation 2014

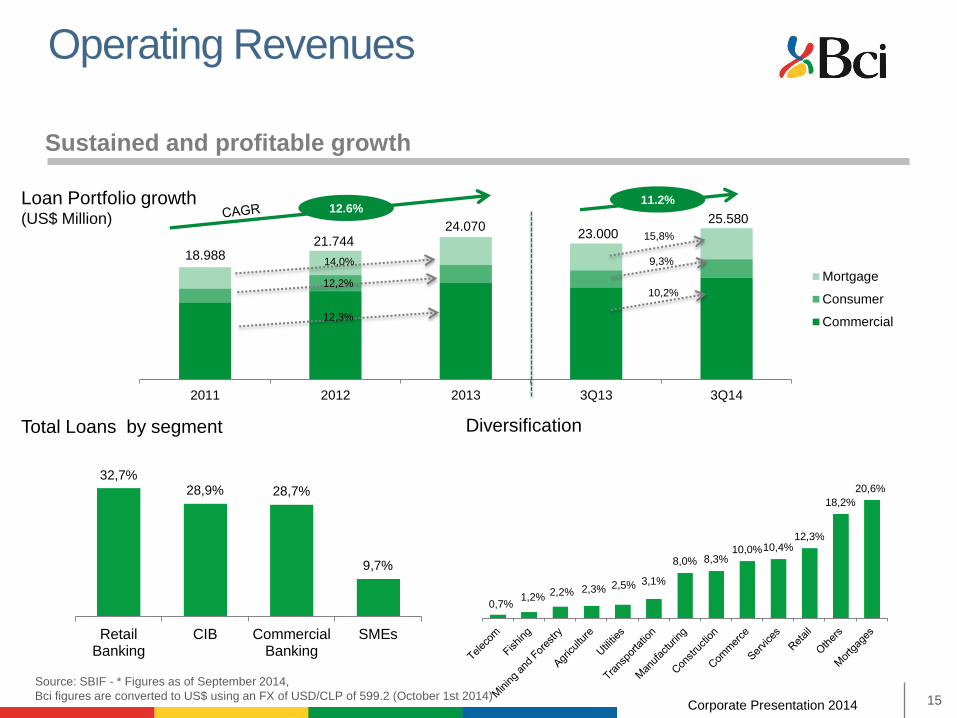

32,7% 28,9% 28,7%

9,7%

RetailBanking

CIB CommercialBanking

SMEs

2011 2012 2013 3Q13 3Q14

Mortgage

Consumer

Commercial

Operating Revenues

15

Loan Portfolio growth (US$ Million)

Source: SBIF - * Figures as of September 2014,

Bci figures are converted to US$ using an FX of USD/CLP of 599.2 (October 1st 2014)

Diversification

8,0% 8,3% 10,0% 10,4%

12,3%

18,2%

20,6%

12.6% 11.2%

18.988 21.744

24.070 23.000

25.580

14,0%

12,2%

12,3%

15,8%

9,3%

10,2%

Total Loans by segment

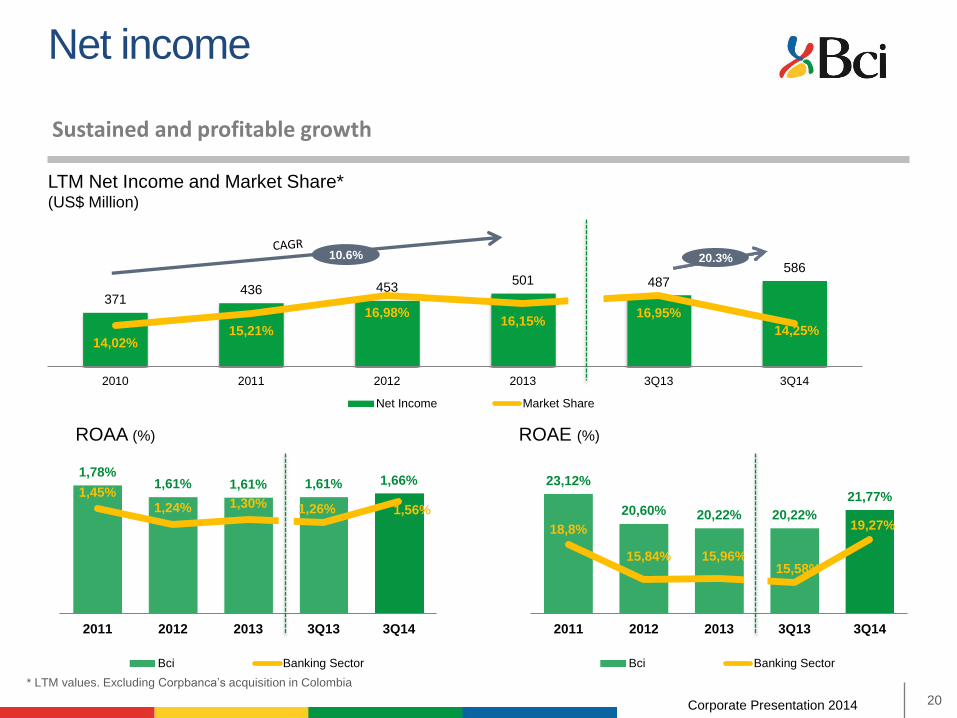

Sustained and profitable growth

0,7% 1,2% 2,2% 2,3% 2,5% 3,1%

Corporate Presentation 2013 Corporate Presentation 2014 Corporate Presentation 2014

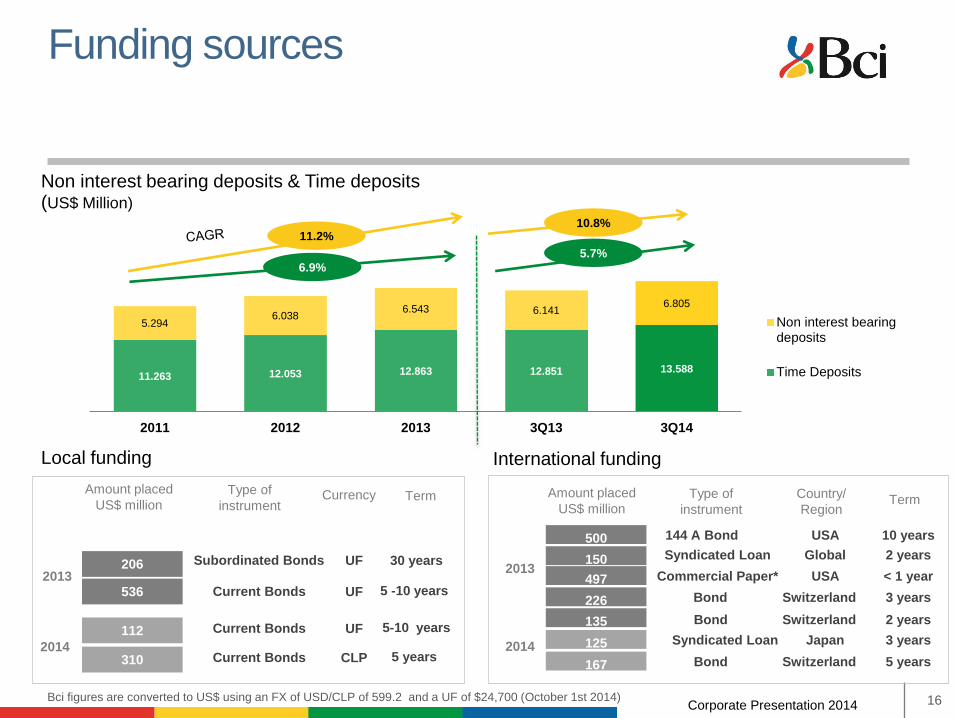

Funding sources

16

Non interest bearing deposits & Time deposits (US$ Million)

11.263 12.053 12.863 12.851 13.588

5.294 6.038

6.543 6.141 6.805

2011 2012 2013 3Q13 3Q14

Non interest bearingdeposits

Time Deposits

11.2%

6.9%

Bci figures are converted to US$ using an FX of USD/CLP of 599.2 and a UF of $24,700 (October 1st 2014)

5.7%

10.8%

Amount placed

US$ million Country/

Region Term

2013

2014

500

226

135

150

497

125

167

Type of

instrument

144 A Bond

Bond

Bond

Syndicated Loan

Commercial Paper*

Syndicated Loan

Bond

USA

Switzerland

Switzerland

Global

USA

Japan

Switzerland

10 years

3 years

2 years

2 years

< 1 year

3 years

5 years

Local funding

Amount placed

US$ million Term

2013

112

206

Type of

instrument

Current Bonds

Subordinated Bonds

5-10 years

30 years

Currency

UF

UF

International funding

2014

536 Current Bonds 5 -10 years UF

310 Current Bonds 5 years CLP

Corporate Presentation 2013 Corporate Presentation 2014 Corporate Presentation 2014

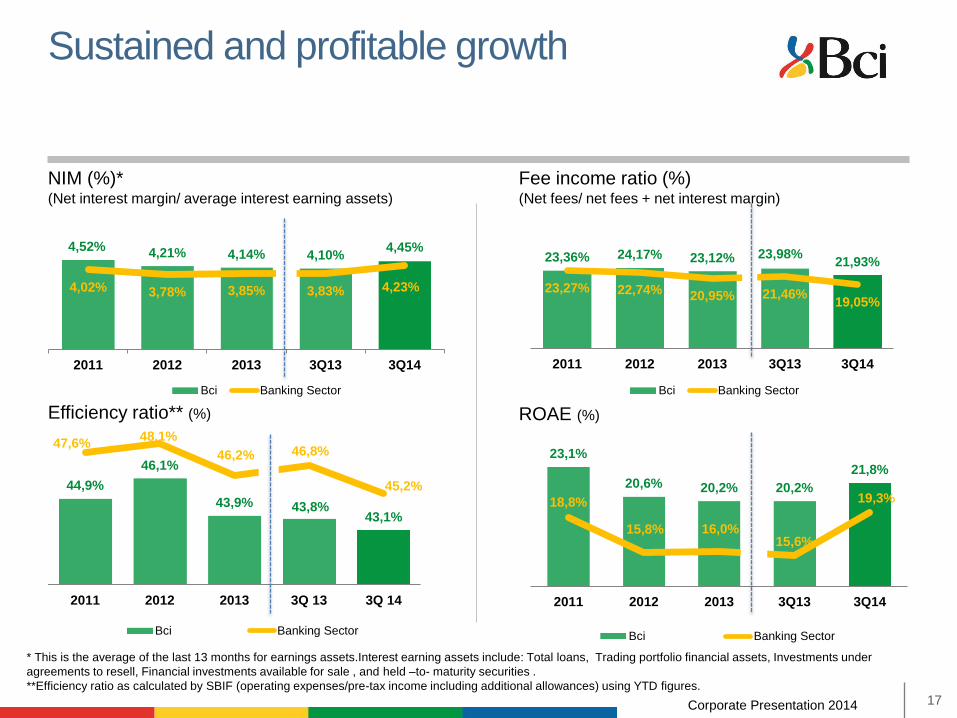

23,36% 24,17% 23,12% 23,98% 21,93%

23,27% 22,74% 20,95% 21,46% 19,05%

0,0 0%

5,0 0%

10, 00%

15, 00%

20, 00%

25, 00%

30, 00%

2011 2012 2013 3Q13 3Q14

Bci Banking Sector

4,52% 4,21% 4,14% 4,10%

4,45%

4,02% 3,78% 3,85% 3,83% 4,23%

2011 2012 2013 3Q13 3Q14

Bci Banking Sector

44,9%

46,1%

43,9% 43,8% 43,1%

47,6% 48,1%

46,2% 46,8%

45,2%

2011 2012 2013 3Q 13 3Q 14

Bci Banking Sector

23,1%

20,6% 20,2% 20,2%

21,8%

18,8%

15,8% 16,0% 15,6%

19,3%

2011 2012 2013 3Q13 3Q14

Bci Banking Sector

Sustained and profitable growth

ROAE (%)

NIM (%)* (Net interest margin/ average interest earning assets)

Fee income ratio (%) (Net fees/ net fees + net interest margin)

Efficiency ratio** (%)

* This is the average of the last 13 months for earnings assets.Interest earning assets include: Total loans, Trading portfolio financial assets, Investments under

agreements to resell, Financial investments available for sale , and held –to- maturity securities .

**Efficiency ratio as calculated by SBIF (operating expenses/pre-tax income including additional allowances) using YTD figures.

17

Corporate Presentation 2013 Corporate Presentation 2014 Corporate Presentation 2014

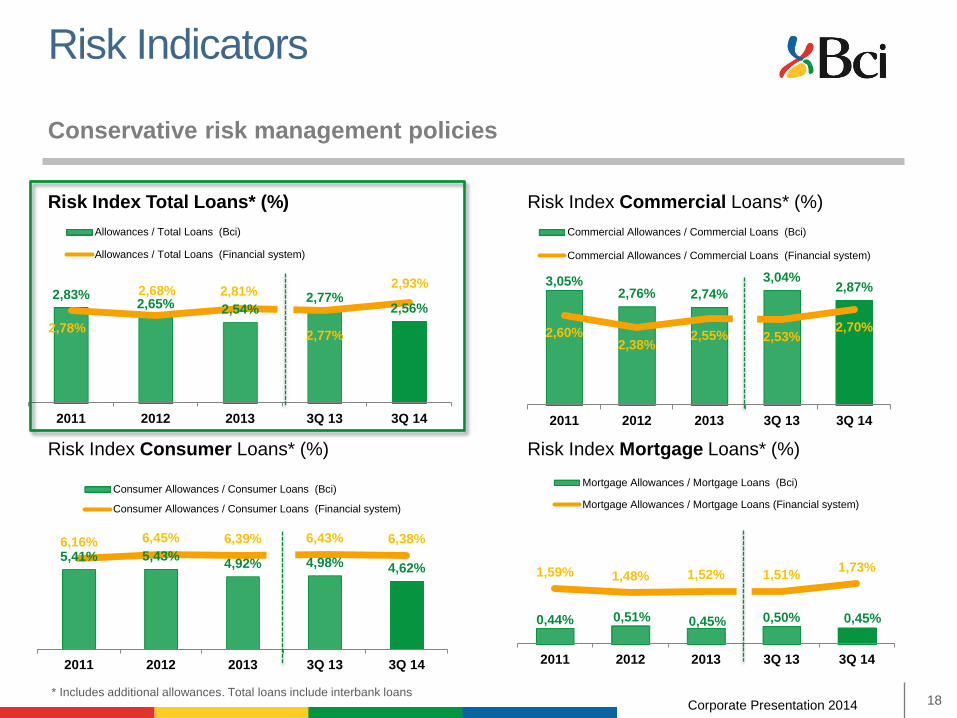

3,05% 2,76% 2,74%

3,04% 2,87%

2,60% 2,38%

2,55% 2,53% 2,70%

2011 2012 2013 3Q 13 3Q 14

Commercial Allowances / Commercial Loans (Bci)

Commercial Allowances / Commercial Loans (Financial system)

0,44% 0,51% 0,45% 0,50% 0,45%

1,59% 1,48% 1,52% 1,51% 1,73%

2011 2012 2013 3Q 13 3Q 14

Mortgage Allowances / Mortgage Loans (Bci)

Mortgage Allowances / Mortgage Loans (Financial system)

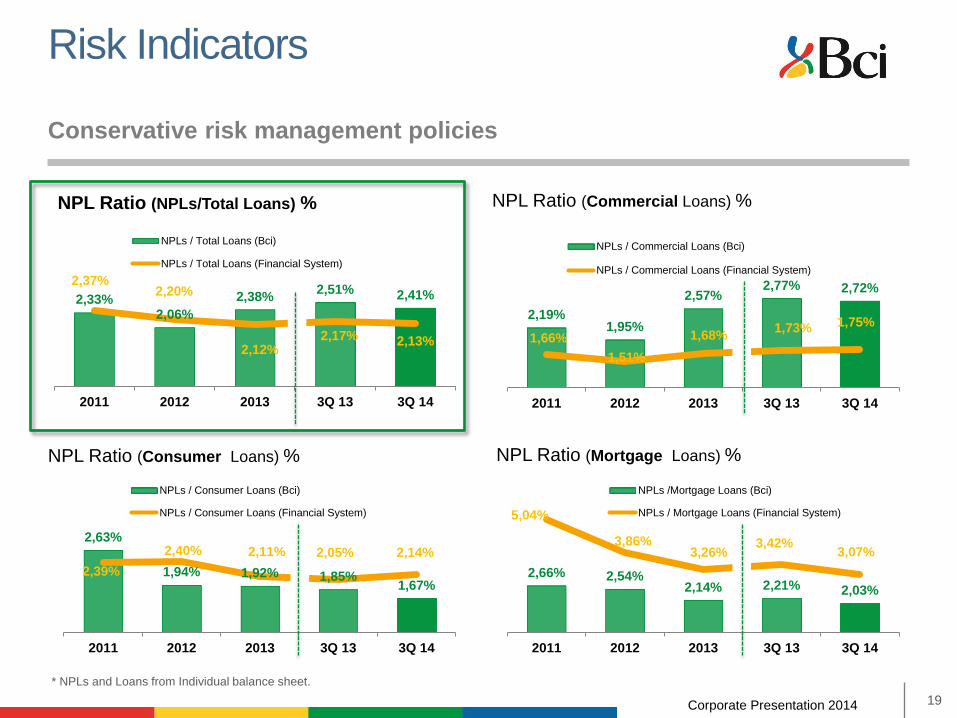

Risk Indicators Conservative risk management policies

18

Risk Index Mortgage Loans* (%)

Risk Index Commercial Loans* (%) Risk Index Total Loans* (%)

2,83% 2,65% 2,54%

2,77% 2,56%

2,78%

2,68% 2,81%

2,77%

2,93%

2011 2012 2013 3Q 13 3Q 14

Allowances / Total Loans (Bci)

Allowances / Total Loans (Financial system)

5,41% 5,43% 4,92% 4,98% 4,62%

6,16% 6,45% 6,39% 6,43% 6,38%

2011 2012 2013 3Q 13 3Q 14

Consumer Allowances / Consumer Loans (Bci)

Consumer Allowances / Consumer Loans (Financial system)

Risk Index Consumer Loans* (%)

* Includes additional allowances. Total loans include interbank loans

Corporate Presentation 2013 Corporate Presentation 2014 Corporate Presentation 2014

2,66% 2,54% 2,14% 2,21% 2,03%

5,04%

3,86% 3,26%

3,42% 3,07%

2011 2012 2013 3Q 13 3Q 14

NPLs /Mortgage Loans (Bci)

NPLs / Mortgage Loans (Financial System)

Risk Indicators Conservative risk management policies

NPL Ratio (NPLs/Total Loans) %

19

2,33% 2,06%

2,38% 2,51% 2,41%

2,37% 2,20%

2,12% 2,17% 2,13%

2011 2012 2013 3Q 13 3Q 14

NPLs / Total Loans (Bci)

NPLs / Total Loans (Financial System)

* NPLs and Loans from Individual balance sheet.

2,19% 1,95%

2,57% 2,77% 2,72%

1,66%

1,51%

1,68% 1,73% 1,75%

2011 2012 2013 3Q 13 3Q 14

NPLs / Commercial Loans (Bci)

NPLs / Commercial Loans (Financial System)

2,63%

1,94% 1,92% 1,85% 1,67%

2,39%

2,40% 2,11% 2,05% 2,14%

2011 2012 2013 3Q 13 3Q 14

NPLs / Consumer Loans (Bci)

NPLs / Consumer Loans (Financial System)

NPL Ratio (Commercial Loans) %

NPL Ratio (Consumer Loans) % NPL Ratio (Mortgage Loans) %

Corporate Presentation 2013 Corporate Presentation 2014 Corporate Presentation 2014

1,78% 1,61% 1,61% 1,61% 1,66%

1,45% 1,24% 1,30% 1,26% 1,56%

2011 2012 2013 3Q13 3Q14

Bci Banking Sector

371 436 453

501 487 586

14,02% 15,21%

16,98% 16,15%

16,95%

14,25%

10,0%

12,0%

14,0%

16,0%

18,0%

20,0%

0

100

200

300

400

500

600

700

2010 2011 2012 2013 3Q13 3Q14

Net Income Market Share

10.6%

23,12%

20,60% 20,22% 20,22%

21,77%

18,8%

15,84% 15,96% 15,58%

19,27%

2011 2012 2013 3Q13 3Q14

Bci Banking Sector

Net income

ROAE (%)

* LTM values. Excluding Corpbanca’s acquisition in Colombia

20

ROAA (%)

LTM Net Income and Market Share* (US$ Million)

20.3%

Sustained and profitable growth

Corporate Presentation 2013 Corporate Presentation 2014 Corporate Presentation 2014

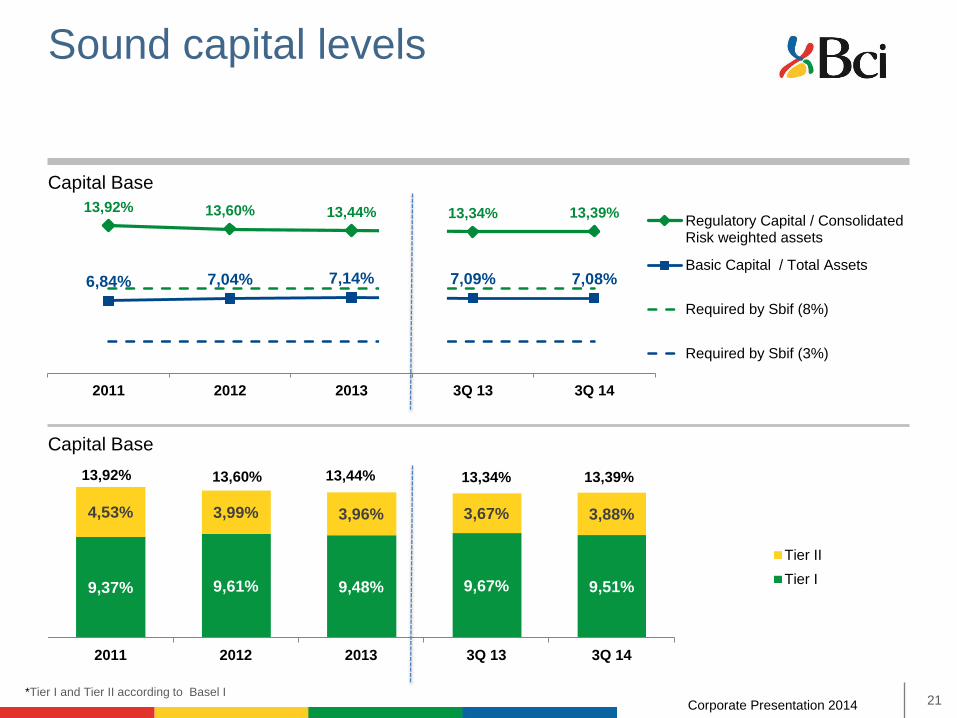

Sound capital levels

21

13,92% 13,60% 13,44% 13,34% 13,39%

6,84% 7,04% 7,14% 7,09% 7,08%

2011 2012 2013 3Q 13 3Q 14

Regulatory Capital / ConsolidatedRisk weighted assets

Basic Capital / Total Assets

Required by Sbif (8%)

Required by Sbif (3%)

Capital Base

9,37% 9,61% 9,48% 9,67% 9,51%

4,53% 3,99% 3,96% 3,67% 3,88%

13,92% 13,60% 13,44% 13,34% 13,39%

2011 2012 2013 3Q 13 3Q 14

Tier II

Tier I

Capital Base

*Tier I and Tier II according to Basel I

Corporate Presentation 2013 Corporate Presentation 2014 Corporate Presentation 2014

Summary

22

Strong loan growth: As of September 2014 it reaches 11.2%, higher than the financial industry’s 10% growth.

High levels of NIM: Reaching a level of 4.45% as of September.

Better efficiency levels than the financial system:43.9% compared to 46.6% for the industry.

Attractive Net Income growth: 20.3% for the last twelve months-.400 bps higher than in 2013.

High return: ROAE of 21.8%.

One of the best credit ratings in the region: A (according to Standard & Poor’s)

Enhancing risk processes through a transformational project that will lead us to have market leading

practices.

Our capital level continues to improve-.Tier1 Ratio of 9.37% in 2011 versus 9.51% as of September 2014.

Through profitable and healthy growth, Bci continues to generate value for its shareholders.

Corporate Presentation 2013 Corporate Presentation 2014

Clic para editar título

Corporate Presentation 2014

“This presentation contains forward-looking statements in various places throughout therein, related to, without limitation, our future business development. Forward-looking information is often, but not always, identified by the use of words such as “anticipate”, “believe”, “expect”, “plan”, “intend”, “forecast”, “project”, “may”, “will”, “should”, “could”, “estimate”, “predict” or similar words suggesting future outcomes or language suggesting an outlook. While

these forward looking statements represent our judgment and future expectations concerning the development of our business, a number of risks, uncertainties and other important factors could cause actual developments and results to differ materially from our plans, objectives, expectations, anticipations, estimates and intentions expressed

in such forward-looking statements. The risk factors and other key factors that we have indicated in our past and future filings and reports, including those with local or foreign authorities, could adversely affect our business and financial performance. The information contained herein is subject to, and must be read in conjunction with, all other publicly available information, including relevant document published by Banco de Crédito e Inversiones (“BCI”) or any of its related

companies.

The forward-looking statements represent our views as of the date of this presentation and should not be relied upon as representing our views as of any date subsequent to the date of this presentation. We undertake no obligation to update any of these statements.

Recipients of this presentation are not to construe the contents therein as legal, tax or investment advice and such recipients should consult their own advisors in this regard. Likewise, this presentation does not constitute or form any part of any offer, invitation or inducement to sell or issue, or any solicitation of any offer to purchase or subscribe for, any shares or other securities issued or related to BCI.

Furthermore, any liability for losses arising from the use of material contained in this presentation, which is confidential and submitted to prior selected recipients only, is accepted by BCI or its executives, directors or

related companies. This presentation may not be reproduced (in whole or in part) to any other person, without our prior written consent”.

Thank you

“

Corporate Presentation 2013 Corporate Presentation 2014

%∆

YoY

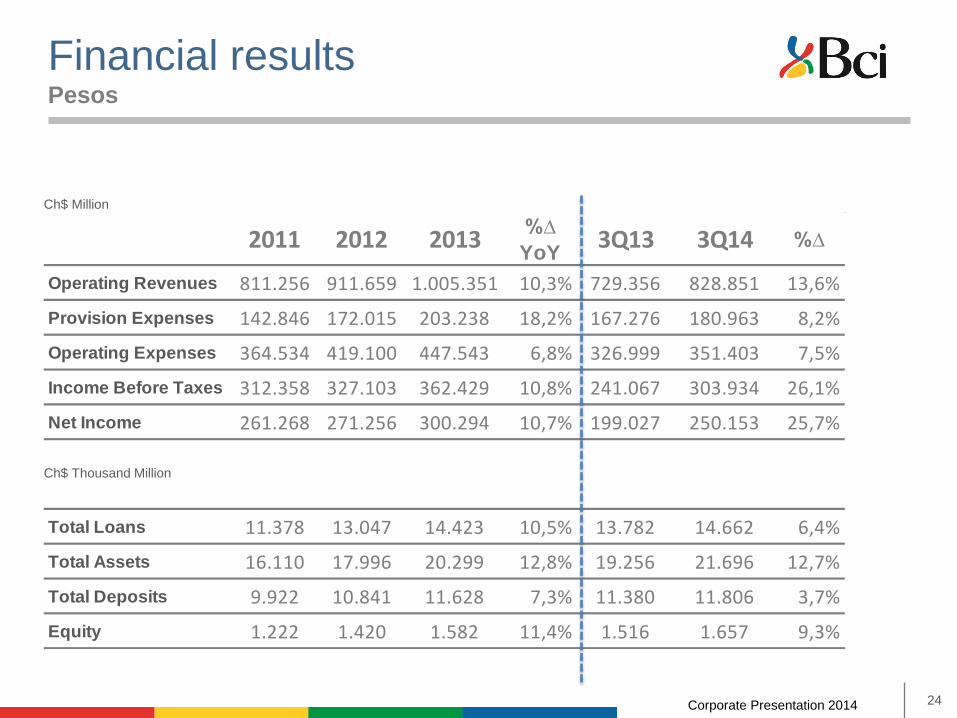

Operating Revenues 811.256 911.659 1.005.351 10,3% 729.356 828.851 13,6%

Provision Expenses 142.846 172.015 203.238 18,2% 167.276 180.963 8,2%

Operating Expenses 364.534 419.100 447.543 6,8% 326.999 351.403 7,5%

Income Before Taxes 312.358 327.103 362.429 10,8% 241.067 303.934 26,1%

Net Income 261.268 271.256 300.294 10,7% 199.027 250.153 25,7%

Total Loans 11.378 13.047 14.423 10,5% 13.782 14.662 6,4%

Total Assets 16.110 17.996 20.299 12,8% 19.256 21.696 12,7%

Total Deposits 9.922 10.841 11.628 7,3% 11.380 11.806 3,7%

Equity 1.222 1.420 1.582 11,4% 1.516 1.657 9,3%

%∆2011 2012 2013 3Q13 3Q14

Financial results

Ch$ Thousand Million

24

Ch$ Million

Pesos

Corporate Presentation 2013 Corporate Presentation 2014

%∆

YoY

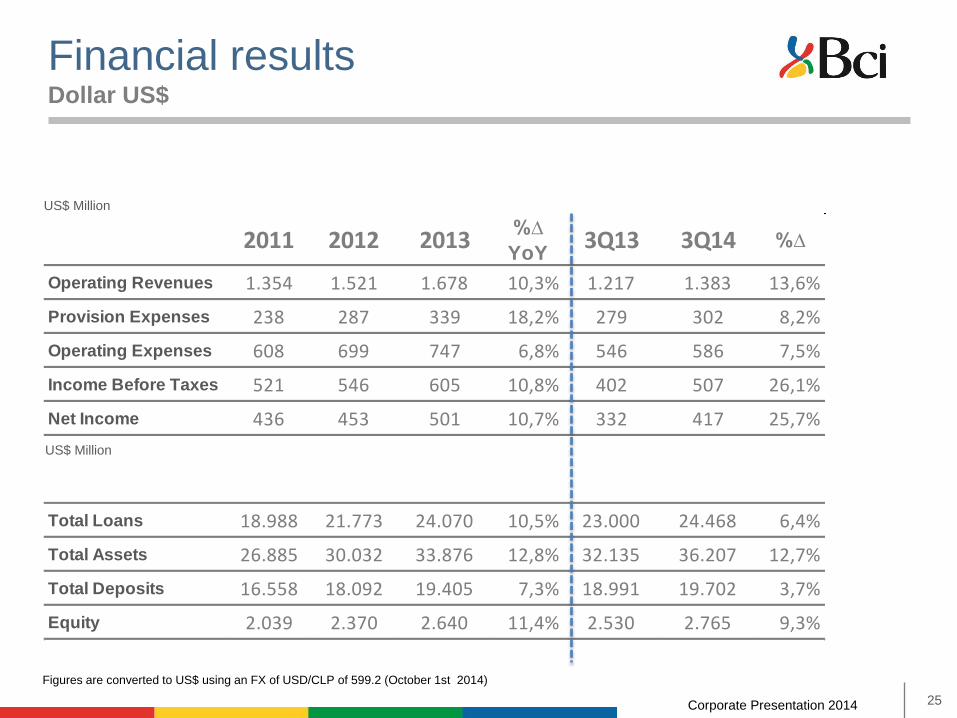

Operating Revenues 1.354 1.521 1.678 10,3% 1.217 1.383 13,6%

Provision Expenses 238 287 339 18,2% 279 302 8,2%

Operating Expenses 608 699 747 6,8% 546 586 7,5%

Income Before Taxes 521 546 605 10,8% 402 507 26,1%

Net Income 436 453 501 10,7% 332 417 25,7%

Total Loans 18.988 21.773 24.070 10,5% 23.000 24.468 6,4%

Total Assets 26.885 30.032 33.876 12,8% 32.135 36.207 12,7%

Total Deposits 16.558 18.092 19.405 7,3% 18.991 19.702 3,7%

Equity 2.039 2.370 2.640 11,4% 2.530 2.765 9,3%

2011 2012 2013 3Q13 3Q14 %∆

Financial results

US$ Million

25

US$ Million

Dollar US$

Figures are converted to US$ using an FX of USD/CLP of 599.2 (October 1st 2014)