Corporate JKRMIBL

21

JK Risk Managers & Insurance Brokers Ltd. Woman Power

-

Upload

sunil-kumar -

Category

Documents

-

view

59 -

download

1

description

JK Risk Managers and Insurance Brokers Limited

Transcript of Corporate JKRMIBL

JK Risk Managers & Insurance Brokers Ltd.

Woman Power

JK Risk Managers & Insurance Brokers Ltd.

The Team

Defining your expectations, our services

Index

Company Overview

JK Organization

✓

1

2

3

4

5

6

7

Introduction

Our Team

Focus

Contact Us

Corporate Clients

JK Risk Managers & Insurance Brokers Ltd.

.

Company Overview

►JK Risk Managers & Insurance Brokers Ltd is an IRDA

licensed direct insurance broking company specializing

in corporate insurance broking services.

►It is an independent business unit under the umbrella of

the century old JK Group

►JKRMIBL is headquartered in Delhi with major operations

in NCR, Mumbai, Kolkata, & Ahmadabad

JK Risk Managers & Insurance Brokers Ltd.

Promoted by the Century old

JK Organization

JK Risk Managers & Insurance Brokers Ltd.

National Insurance Company Ltd

nationalized in 1972.

Ruby Life Insurance Company

nationalized in 1956.

Mr. Hari Shankar Singhania, Chairman of

JK Organization was an underwriting

member of a syndicate at the Lloyd's of

London for over a decade.

JK Risk Managers is the latest foray of

the Organization into the Insurance

industry post liberalization in India circa

2000

JK Risk Managers & Insurance Brokers Ltd.

Introduction - Legacy

.

JK Risk Managers & Insurance Brokers Ltd.

Mr. Anuraag Kaul- Chief Executive

Mr. Anil Midha – AVP Knowledge

Mr. Orindam Sen - Chief Assistant to

CEO

Mr. Satwinder.S.Farma- Head-Finance

Ms.Shivani Parashar- Head Response

Mr. Sufian Alvi,- Special Projects

Mr Vikas Sinha-Head Rural Distribution

Ms. Shilpa Saxena- Marketing NCR

Mr. B.Vaidyanathan- DGM NCR

Mr. Soumya Bhadra- Head Marketing

Western India.

Mr. Sudipt Bhattacharya- Head Kolkata

Ms. Sonia Duggal-Business Head Retail

& SME

JK Risk Managers & Insurance Brokers Ltd.

Our Team

We make sure your claims R settled

JK Risk Managers & Insurance Brokers Ltd.

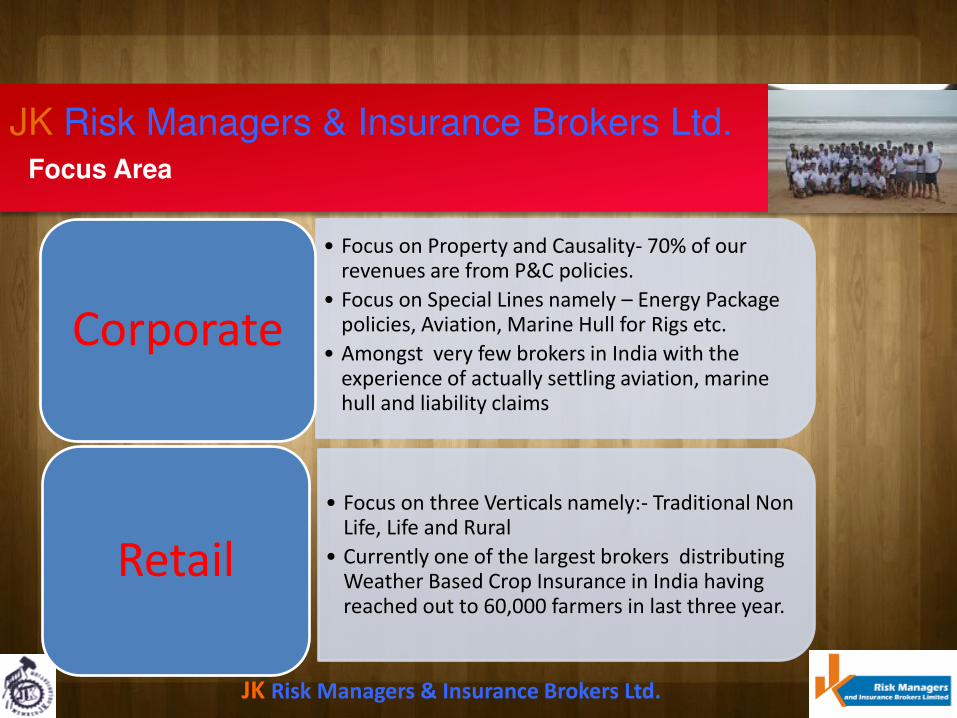

JK Risk Managers & Insurance Brokers Ltd. Focus Area

• Focus on three Verticals namely:- Traditional Non Life, Life and Rural

• Currently one of the largest brokers distributing Weather Based Crop Insurance in India having reached out to 60,000 farmers in last three year.

Retail

• Focus on Property and Causality- 70% of our revenues are from P&C policies.

• Focus on Special Lines namely – Energy Package policies, Aviation, Marine Hull for Rigs etc.

• Amongst very few brokers in India with the experience of actually settling aviation, marine hull and liability claims

Corporate

JK Risk Managers & Insurance Brokers Ltd.

• Corporate team works under the Guidance of Mr.Anuraag Kaul & Anil Midha.

Please read (Snapshot Of Insurance Sector – authored by Mr Kaul)

Please Read (Directors And Officers Liability Insurance - authored by Mr Midha)

• Anil Midha, is a visionary and has been instrumental in introduction of certain

insurance covers in India in his more than three and a half decades of work

experience.

• Mr. Anuraag Kaul with an experience of two and a half decades, manages a

very strong corporate team with dedicated servicing team and he manages a

number of relationships both nationally and internationally.

Corporate

JK Risk Managers & Insurance Brokers Ltd.

JK Risk Managers & Insurance Brokers Ltd.

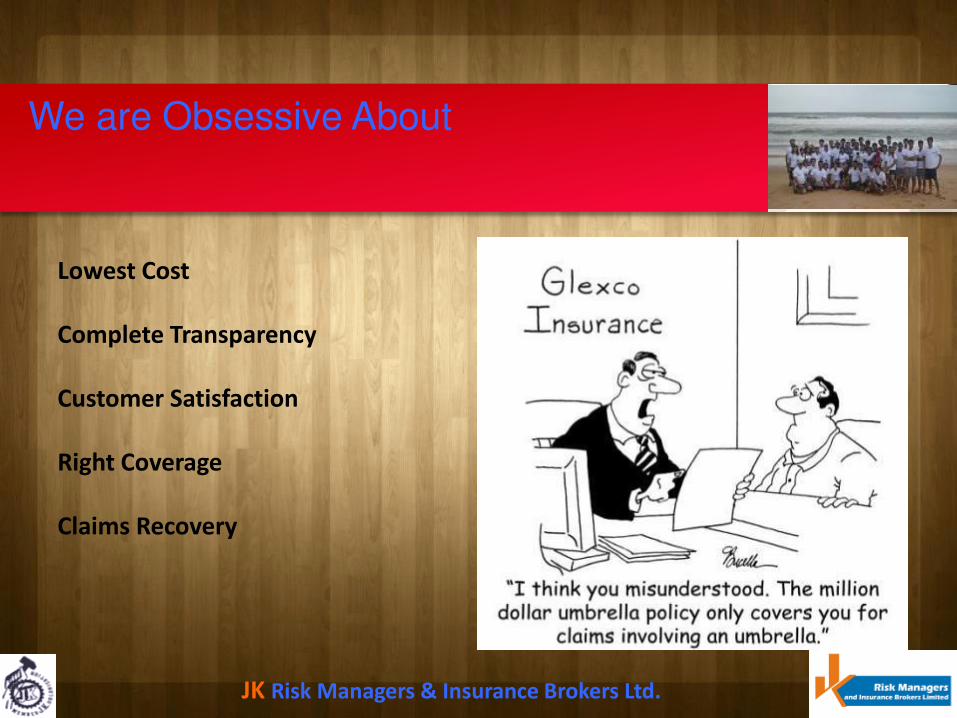

We are Obsessive About

Lowest Cost

Complete Transparency

Customer Satisfaction

Right Coverage

Claims Recovery

JK Risk Managers & Insurance Brokers Ltd.

• Devising annual insurance program – Study current polices and conduct risk audit – Discuss the cost–benefit with the management – Finalise annual insurance program

• Quote procurement and finalization

– Prepare a ‘broking slip’ which encompasses details of coverage required and is given to the whole market including the existing underwriter to involve fair play and equal participation

– Compare the quotes on an ‘apple to apple’ basis – Re-negotiate rates – Call all or top 3/4 players for a re-negotiation with the client – Sit with the client and re-negotiate rates – Client gets to decide on the terms, rates and the insurance company – Finalize a company collect cheque and place the policy

• Regular administration and claims management

Process Led Approach to solving client issues

JK Risk Managers & Insurance Brokers Ltd.

JK Risk Managers & Insurance Brokers Ltd.

Type of

Policy

Basic

Service

Additional

service 1

Additional

service 2

Additiona

l service 3

Additional

service 4

Additional

service 5

Additional

service 6

Property Placement PRR/Annual

Insurance Plan

Underwriting

Submission

Risk

Management

Study

Expediting

Claim

Negotiation's

Policy

Administration

(In case of

Deceleration

Policy)

Asset

Valuation

Marine Placement

Policy

Administration

Expediting

Claim

Negotiation's

Medical Placement

Policy

Administration

Expediting

Claim

Negotiation's

Help Desk

Motor Placement

Policy

Administration

Expediting

Claim

Negotiation's

Help Desk

Liability Placement

Proper Wording

Evaluation

Other Placement

Expediting Claim

Negotiation's

JK Risk Managers & Insurance Brokers Ltd.

Our Service Offerings

JK Risk Managers & Insurance Brokers Ltd.

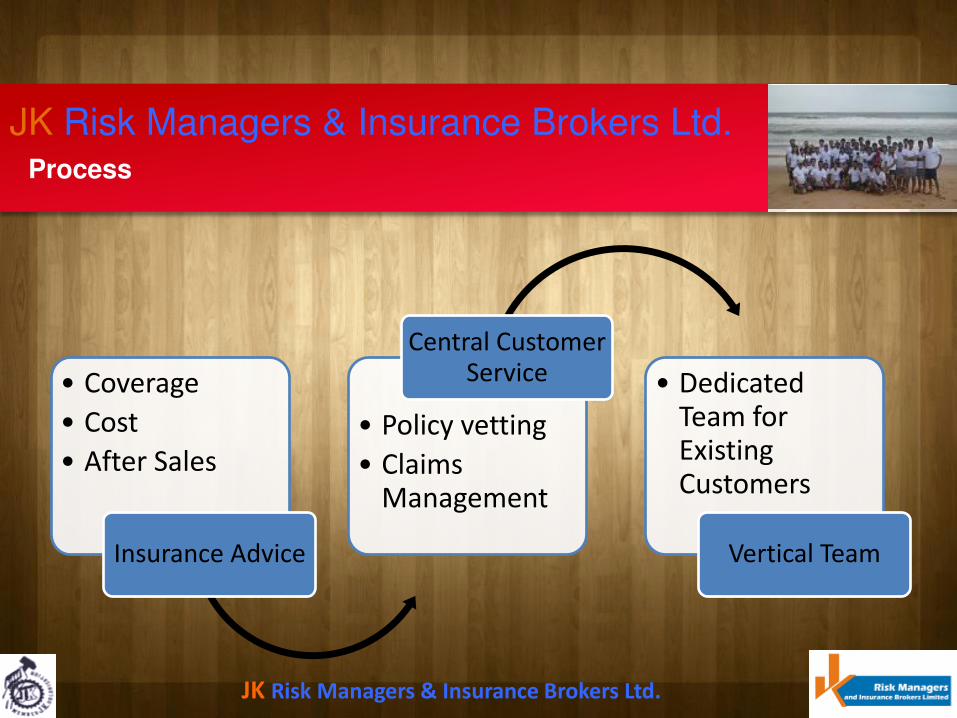

Process

JK Risk Managers & Insurance Brokers Ltd.

• Coverage

• Cost

• After Sales

Insurance Advice

• Policy vetting

• Claims Management

Central Customer Service • Dedicated

Team for Existing Customers

Vertical Team

JK Risk Managers & Insurance Brokers Ltd.

Some of our Corporate Clients

JK Risk Managers & Insurance Brokers Ltd.

JK Risk Managers & Insurance Brokers Ltd.

Contact Us:-

Delhi :- 011 - 30179785

Noida :- 0120 - 3890783

Ahmadabad :- 079 - 40306200

Mumbai :- 022 - 22040794/96

Kolkata: - 033 - 40017421

Bengaluru : - 080 - 42035017

Email ID : [email protected]

Website : www.jkbima.com & www.saralbima.co

JK Risk Managers & Insurance Brokers Ltd.

JK Risk Managers & Insurance Brokers Ltd.

SNAPSHOT OF THE INSURANCE SECTOR

jkrmibl

BACK

Directors And Officers Liability Insurance: Perspectives For Tomorrow’s Global India- Anil Midha, December 2011

As India becomes integrated with the global economy, the business and social environment also is expected to mirror the developed world in many ways. One such change that is expected (and to some extent is already happening), is that society grows more litigious. People more aware of their legal rights would seek legal remedies to enforce these rights. The proliferation of law schools in the country and judicial activism is helping to accelerate this process.

This is also leading to a perceptible attitudinal change in corporate management circles in India. The media frequently highlights cases where non executive directors and senior managers get into trouble for some action or inaction, and face an inquiry or lawsuit. This only adds to the fear. There is, therefore, an eagerness to discuss the regulatory and legal risks faced by corporations and the individuals who run them, and to seek appropriate solutions to manage these risks.

In this context, directors and officers liability insurance has become a popular topic of conversation among top management in India. Although the number of Indian companies with such a policy in their insurance portfolio is very small, this number is rapidly increasing. At the same time, there are many concerns, doubts and apprehensions about the concept and coverage of this policy.

At a fundamental level, it is sometimes asked why an individual needs to cover his personal financial liability for something he has or has not done in the course of his official work. The company is vicariously liable for his action, so why does the individual need protection? Unless, of course, the individual has committed a criminal offence, in which case, the policy will not provide protection anyway. This traditional thinking has long been replaced by the development of the Principle of Attribution. It has been held by various court judgments that the fact that the corporation acts through its servants or agents does not mean that the conduct or state of knowledge of those individuals should be attributed to it in every circumstance. Where, for instance, the individual has acted beyond his powers or has used his powers for a purpose different from its intended use, he would have to face personal liability, and his act cannot be attributed to the corporation.

Directors And Officers Liability Insurance: Perspectives For Tomorrow’s Global India- Anil Midha, December 2011

Of course, for all bona fide acts of the officers of the companies, the company may indemnify these individuals. However, Section 201 of the Companies Act allows this indemnification only if in any proceeding for civil or criminal offence against the officer, the judgment is given in his favour, or he is acquitted or discharged. The difficulty with this limited relaxation is that the officer invariably would have to incur huge legal and other related expenses before he is finally acquitted and indemnified by his company. And obviously, there is no indemnification if he is not acquitted. So the directors and officers policy is the only financial recourse available to the officer to meet the defence expenses on an ongoing basis, and to eventually meet the liability if it does arise. The D&O policy, incidentally, will also pay for all these expenses even where the company is able to reimburse the individual officer or the director, though such payments are made by the insurance company under a separate section of the policy and with some compulsory deduction from the claimed amount. The policy excludes coverage for dishonest acts or other such offences of a criminal nature. It also excludes payment for fines and penalties. This is because providing financial protection to such acts would be opposed to public policy. Some policy wordings go further and even deny protection to those individuals who have condoned such acts. However, the big relief to innocent directors and officers is that mere allegation of, or investigation of, or even proceedings for, a criminal offence are not enough to deny this protection under the policy. The protection is denied only if the director or the officer admits to the criminal wrongdoing, or if such wrongdoing is established by the final adjudication of a judicial or arbitral tribunal, in which case the insurance company has the right to recover all the expenses paid on his behalf from the guilty officer or director. Worldwide, the majority of claims filed under D&O policies have arisen out of action initiated by shareholders and employees. Quite often, such proceedings are both against the director/officer and the company itself. Therefore, it is not surprising that most policy wordings protect the company itself (called entity coverage) in addition to the individual directors/officers for offences relating to securities and employee practices. This additional cover, particularly relating to employee practices liability, is generally given for an additional premium.

Thus D&O insurance has expanded beyond its original and basic coverage of personal financial liability to include the coverage of the company itself for certain offences. A large number of Indian companies are still family owned or controlled and the promoter shareholding in India is higher than in many other countries. Recent measures announced by the Securities and Exchange Board of India (SEBI) are likely to expand public shareholding. It is therefore quite likely that activism on the part of minority shareholders would follow the pattern of the western world and we may see more suits filed by shareholders against companies and their directors and officers. India is also undergoing a change on the employee front. Although we do not see the kind of militant unionism that was prevalent in the 70s and 80s, there is a much greater awareness among employees about what is going on in their organization. Also, in view of the greater availability of job opportunities, employees have less fear in asserting their rights.

Directors And Officers Liability Insurance: Perspectives For Tomorrow’s Global India- Anil Midha, December 2011

Therefore, we are likely to see more shareholders and employees filing complaints and initiating action against both companies and individual directors and officers. We have already seen regulators initiating inquiries and investigations in many cases on the basis of such complaints, and such action will increase as the public mounts more pressure on corporations relating to governance.

Directors and officers liability insurance, as in the western world, is thus tipped to be a must-have policy for every company in India. Already there is a proposal by SEBI to make it compulsory for every company listed on the stock exchange.

Coming to the operational aspects of the policy, there are two main concerns. One is that most D&O policies do not impose a duty to defend by the insurer. This is equivalent to a medical insurance or vehicle insurance not being ‘cashless’ in nature. However, most D&O policies do allow an advance against legal expenses. Also, the insured generally has the right to select counsel, subject to the insurer’s consent. Secondly, it becomes a difficult task for most companies to choose the limit of liability for which to buy this insurance. In the US and some other countries, the limits fixed are proving to be inadequate in most cases. This is primarily because a large number of persons in the organization get involved in any act of misfeasance, each requiring a separate defence. In India, the average limit for listed companies is around $1m and this is likely to increase substantially as companies grow in size and become more globalised.

Anil Midha is an AVP and Head of Knowledge at J K Risk Managers & Insurance Brokers Limited. He can be contacted on +91 98 1035 9791 or by email: [email protected].

jkrmibl

BACK