Corporate Inversions

39

Corporate Inversions Deborah Paul Wachtell, Lipton, Rosen and Katz Steve Edge Slaughter and May Professor Stephen Shay Harvard Law School Robert Stack Deputy Assistant Secretary for International Tax Affairs, Office of Tax Policy, U.S. Department of the Treasury International Tax Institute November 21, 2014

Transcript of Corporate Inversions

Corporate Inversions

Deborah Paul Wachtell, Lipton, Rosen and Katz

Steve Edge

Slaughter and May

Professor Stephen Shay Harvard Law School

Robert Stack

Deputy Assistant Secretary for International Tax Affairs, Office of Tax Policy, U.S. Department of the Treasury

International Tax Institute November 21, 2014

• The UK

• Corporate Tax Reform

• Notice 2014-52

• Earnings Stripping

2 2408541 v3

The U.K. as a Destination for Inversions

The U.K.’s competitive tax policy • History – 40%→52% →30% corporate tax rate + foreign tax credit + non EU compliant controlled foreign

corporation (“CFC”) rules.

• Some previous holding company encouragement (substantial shareholding exemption, foreign income dividends).

• 2007 attempt to tax offshore passive income – some corporate defections.

• EU freedoms litigation – CFC rules and domestic dividend exemption/foreign dividend taxation challenged.

• Bringing it all together – the new package as a response to both CFC challenges and UK inversions (WPP etc).

• A balanced territorial package – encouraging domestic investment and pushing down debt with low corporate tax rate and responding to inversions/multinational corporation vulnerability through CFC reform, foreign dividend exemption.

• Trying to level the playing field and create proper competition – not a race to the bottom.

• Not targeting U.S. inbounds – an unlooked for benefit. Rules targeted at preserving UK multinational corporation base.

• The UK does have CFC rules!

4

The U.K. as a destination • Basic package – no outbound withholding tax on dividends, low corporate tax rate, no

interest allocation, foreign dividend exemption, territorial CFC regime, good treaty network and participation exemption for gains (substantial shareholding exemption rules).

• Tax residence criteria.

• Post-inversion advantages – U.K./U.S. treaty and treatment of US funding (pre-BEPS).

• Other jurisdictions compared.

5

Corporate Tax Reform • Would corporate tax reform eliminate the need for anti-inversion rules?

• Why are there fewer inversions in the EU?

• What has been the effect in the UK on the corporate tax base of the UK tax reforms?

• Does the UK experience have pertinence to the US?

• How does Republican control of the Senate bear upon the likelihood and nature of tax reform?

6

Corporate Tax Reform

• Tax reform proposals to date are unlikely to materially reduce pressure from inversions. – Increased tax on foreign earnings under minimum tax proposals will increase

not decrease pressure.

• Reform proposals do not increase protections of U.S. tax base against erosion by foreign groups. – Corporate residence rules are not materially addressed – Earnings stripping not materially addressed.

7

Pre-Acquisition Distributions

• For purposes of Section 7874, non-ordinary course distributions made by the acquired Domestic Entity in the 36 month period ending on the acquisition date will be “disregarded”.

• “Non-ordinary course distributions” means the excess of (i) all distributions made by the Domestic Entity during a taxable year with respect to its stock or partnership interests over (ii) 110% of the average of such distributions during the 36 month period immediately preceding such taxable year.

• “Distribution” includes Section 301, 302 and 355 distributions. Also includes boot in the acquisition if sourced at the Domestic Entity.

• Treasury Regulation Section 1.367(a)-3(c) will be modified to incorporate the same principles.

8

36-Month Lookback

• Where did the 36-month look-back test come from?

• Does the 36-month look-back test replace the “principal purpose” test? – Is it acceptable to skinny down with a bad principal purpose provided the 36-

month look-back test is satisfied?

9

Pre-Acquisition Distributions Not Involving Buybacks of Shares • How do we “disregard” the distribution?

• Suppose Domestic Entity made a $100 non-ordinary course cash distribution two

years before the acquisition. – How do we translate that into a number of Foreign Acquiror shares in the

numerator of the Ownership Fraction?

– Do we increase the numerator in the Ownership Fraction by a number of Foreign Acquiror shares worth (a) $100, (b) $100 plus interest, (c) $100 plus a growth factor?

10

Share Buybacks

• How do we “disregard” the distribution?

• Suppose Domestic Entity redeemed 100 shares for $100 two years prior to the inversion, at a time when the shares were worth $1 each. Suppose Domestic Entity shares are worth $2 per share at the time of inversion. – Do we deem an additional 100, or an additional 50, Domestic Entity shares to

be outstanding?

11

Privately Owned Entities

• If “disregarding” a distribution depends on knowing the value per share of

either Domestic Entity or Foreign Acquiror, how would the rules apply if Domestic Entity or Foreign Acquiror, respectively, is privately owned such that the value of its shares is not readily known?

12

Part Cash/Part Stock Acquisitions

• If the Domestic Entity shareholders get a mixture of Foreign Acquiror stock and cash in the

acquisition, how much Foreign Acquiror stock do we assume is allocated to the additional Domestic Entity stock deemed outstanding?

– Suppose that Domestic Entity made a non-ordinary course distribution of $100 in cash shortly before the acquisition. In the acquisition, Foreign Acquiror pays half cash and half Foreign Acquiror stock to the Domestic Entity shareholders. Each Foreign Acquiror share is worth $1. How many Foreign Acquiror shares are deemed to be in the numerator of the Ownership Fraction on account of the $100 distribution?

• Boot sourced at Domestic Entity is potentially a non-ordinary course distribution but boot

sourced at Foreign Acquiror is not.

13

Stub Period Distributions

• If an inversion happens mid-year, how do we determine if a distribution during the short period at the beginning of the 36-month lookback period is non-ordinary course?

• Suppose that an inversion occurs on July 1, Year 7. The 36-month lookback period begins on July 1, Year 4. Suppose that $20 was distributed in Year 4, half in the first half of the year and half in the second half of the year. – How do we determine if the $10 distribution made during the period July 1

through December 31, Year 4 is non-ordinary course? – The rule for determining whether distributions are ordinary course tests

whether aggregate distributions for Year 4 are non-ordinary course (by measuring them relative to distributions occurring in Years 1, 2 and 3). Suppose we determine that the $20 aggregate distributions in Year 4 are non-ordinary course. How do we know whether the $10 distribution during the July 1 to December 31 portion of Year 4 is non-ordinary course?

14

Year by Year Test for Non-Ordinary Course Distributions • Suppose an acquisition occurs at the end of Year 6 and that the only

relevant distributions are a Year 3 distribution of $100 and a Year 5 distribution of $50.

• $13 of the Year 5 distribution is non-ordinary course (because 110% of the average distribution over Years 2, 3 and 4 = $100/3 × 110% = $37) and therefore disregarded, even though aggregate distributions in Years 4, 5 and 6 were half of the aggregate distributions in Years 2, 3 and 4 or Years 1, 2 and 3.

• Should an aggregate 3-year period be used, rather than a year by year test, for extraordinary distributions?

15

Multiple Classes of Stock: Preferred Stock

• Suppose Domestic Entity makes no distributions during any relevant period except that two years before the acquisition, Domestic Entity redeems a tranche of preferred stock at maturity pursuant to the terms of the preferred stock. Is that a non-ordinary course distribution? If so, how does that translate into a number of Foreign Acquiror shares in the numerator of the Ownership Fraction?

• Suppose that two years before the acquisition, Domestic Entity redeems a portion of the preferred shares that it has outstanding and that the redemption is considered a non-ordinary course distribution. Suppose that in the acquisition, the remaining shares of that class of preferred stock receive cash. Do we deem any additional Foreign Acquiror shares to be in the numerator in light of the fact that the remaining preferred shares were cashed out?

16

Multiple Classes of Stock: Preferred Stock

• Suppose that three years before the acquisition, Domestic Entity issues preferred stock that provides for dividends at a 7% rate. Pursuant to the terms of the preferred stock, Domestic Entity pays the annual 7% cash distributions annually. Apart from those distributions, Domestic Entity makes no distributions during any relevant period. Are the annual payments of preferred coupon non-ordinary course distributions? If so, how do we translate those into Foreign Acquiror shares in the numerator of the Ownership Fraction?

17

Multiple Classes of Stock: Voting Power

• Suppose that Domestic Entity has outstanding low vote common (Class A) and high vote common (Class B), while Foreign Acquiror has outstanding only common shares (all with the same voting power). In a non-ordinary course distribution within the 36-month lookback period, Domestic Entity redeems all the Class B (high vote) shares. In the acquisition, all the Domestic Entity shares (i.e., the Class A) receive Foreign Acquiror common. When we deem additional shares of Foreign Acquiror to be in the numerator of the Ownership Fraction, presumably they will be of the class that Foreign Acquiror actually has outstanding, not a class that has higher voting power?

• Any difference if Foreign Acquiror has outstanding high vote shares that were not used in the acquisition?

• Any difference if only a portion of the Class B was redeemed and the remaining Class B received high vote Foreign Acquiror shares (or alternatively regular vote Foreign Acquiror shares)?

18

Predecessors • The Notice disregards distributions by a “predecessor” of Domestic Entity. Is the

concept of predecessor based on F reorg, non-divisive D, Section 381, divisive D, reverse acquisition or something else?

• Suppose that Domestic One and Domestic Entity are historic corporations. Domestic One merges directly into Domestic Entity in an A Reorg or a C Reorg (but not an F or a D Reorg). Then, within 36 months, Foreign Acquiror acquires Domestic Entity. Is Domestic One a “predecessor” of Domestic Entity? – If instead Domestic Entity acquired Domestic One in an (a)(2)(D), (a)(2)(E) or B

reorg, is Domestic One a “predecessor” of Domestic Entity? • Suppose Domestic Parent spins off Domestic Controlled. Is Domestic Parent a

predecessor of Domestic Controlled or vice versa?

19

Spin-Offs: Acquisition of Controlled • If Domestic Parent extracts value from Domestic Controlled before spinning it off,

could the extraction be a non-ordinary course distribution by Domestic Controlled? – Domestic Parent forms Domestic Controlled which, in exchange for property,

either (a) distributes cash to Domestic Parent, (b) assumes debt of Domestic Parent, or (c) issues debt to Domestic Parent. Domestic Parent then spins off Domestic Controlled. Are any of (a), (b) or (c) non-ordinary course distributions by Domestic Controlled?

– Domestic Parent owns historic Domestic Controlled, which distributes cash to Domestic Parent before being spun off. Is that distribution a non-ordinary course distribution?

– Domestic Parent owns historic U.S. subsidiary, which makes a distribution to Domestic Parent. Then Domestic Parent contributes U.S. subsidiary to Domestic Controlled before spinning off Domestic Controlled. Since Domestic Controlled did not make any distribution to Domestic Parent, is it correct to say that no non-ordinary course distribution has occurred or is U.S. subsidiary considered a “predecessor” of Domestic Controlled such that its distributions count?

20

Spin-Offs: Acquisition of Distributing • Suppose that Domestic Parent makes a non-ordinary course distribution of

Domestic Controlled two years before the acquisition of Domestic Parent. At the time of the spin-off, the value of Domestic Controlled is $1000. At the time of the acquisition of Domestic Parent, the value of Domestic Controlled is $2000. What value do we use when we translate the spin-off into a number of shares of Foreign Acquiror?

21

Spin-Offs: Acquisition of Distributing or Controlled • Does the notion of disregarding the distribution apply for purposes of the

“substantial business activities test”? If so, in the case of a spin-off, does that mean we test substantial business activities based on the activities and assets of both Distributing and Controlled even though they are independent companies when the acquisition of Distributing or Controlled occurs?

22

Partnership Distributions • Should tax distributions by partnerships count as non-ordinary course

distributions?

23

Subsequent Transfers by Foreign Parent

• Suppose Foreign Target owns Domestic Entity, and Foreign Target merges into Foreign Acquiror. Given that Domestic Entity was already owned by a foreign entity, should that transaction ever be subject to Section 7874?

• Why does the Notice draw a distinction between scenarios where Foreign Acquiror issues shares to third parties (e.g., in a public offering) versus scenarios where Foreign Acquiror only issues shares to former owners of Foreign Target?

24

Subsequent Transfers by Domestic Parent

• Suppose that Domestic Parent contributes Domestic Entity to Foreign Acquiror and then sells Foreign Acquiror for cash to third parties. Why is that treated differently from a scenario where the third parties form Foreign Acquiror and then Foreign Acquiror buys Domestic Entity from Domestic Parent for cash? In the latter case, the five percent de minimis rule applies so that Section 7874 does not apply to the acquisition.

25

Cash Boxes

• If more than 50% of the gross value of the Foreign Acquiror group’s property constitutes “nonqualified property”, a corresponding portion of Foreign Acquiror stock will be excluded from the denominator of the Ownership Fraction.

• Suppose Foreign Acquiror owns cash that is intended to be applied to capital expenditures or for a major acquisition. Should that cash be considered to be nonqualified property?

• Why is property held in a banking business excluded from the concept of nonqualified property if it is described in Section 954 or 1297 while property held in an insurance company is excluded only if it is described in Section 954?

26

Hopscotch Loans

• If, within 10 years after an inversion, an expatriated foreign subsidiary acquires debt or equity of a foreign related person (e.g., the new foreign parent), such debt or equity will be treated as “U.S. property” solely for purposes of § 956.

• What is Treasury’s authority for this rule? Where is the “U.S. property”?

27

Decontrolling CFCs

• A transaction in which stock in a CFC underneath Domestic Entity is issued or otherwise transferred to Foreign Acquiror (or its foreign non-CFC subsidiary) will be recharacterized under Section 7701(l) as if it occurred between Foreign Acquiror (or the foreign non-CFC subsidiary) and Domestic Entity.

• Intended to prevent taxpayers from gaining access to pre-acquisition earnings and profits without a Section 956 inclusion by decontrolling CFCs. Also intended to limit transactions where CFC remains a CFC and, eventually, either distributes cash in a non pro rata redemption to Foreign Acquiror or pays a pro rata extraordinary distribution in part to Foreign Acquiror.

• General recharacterization rule will not apply if (a) the expatriated foreign subsidiary remains a CFC and (b) the value of the stock in the expatriated foreign subsidiary owned by the U.S. shareholder of the expatriated foreign subsidiary does not decrease by more than a de minimis amount as a result of the dilution transaction.

• General recharacterization rule will not apply if CFC stock was transferred by a shareholder and full amount of gain is recognized.

28

Section 304 — Related Party Stock Sales

• If CFC acquires Domestic Entity shares from Foreign Acquiror for property, Section 304(b)(5)(B) will

generally apply such that the Section 304 deemed distribution is treated as coming out of e&p of Domestic Entity, not the CFC.

– CFC’s E&P is not reduced as a result of the transaction but cash is transferred from CFC to Foreign Acquiror. Is it correct that the only US tax on the transaction would be the tax on the deemed dividend from Domestic Entity to Foreign Acquiror (which may be small if Foreign Acquiror is in a favorable treaty jurisdiction)?

29

Tax Treaties

• “The Treasury Department is also reviewing its tax treaty policy regarding inverted groups and the extent to which taxpayers inappropriately obtain tax treaty benefits that reduce U.S. withholding taxes on U.S. source income.” – What does this mean?

30

Earnings Stripping Effective Date

• “Future guidance will apply prospectively; however, the Treasury Department and the IRS expect that, to the extent any tax avoidance guidance applies ONLY [emphasis added] to inverted groups, such guidance will apply to groups that completed inversion transactions on or after September 22, 2014.” – What does this mean?

31

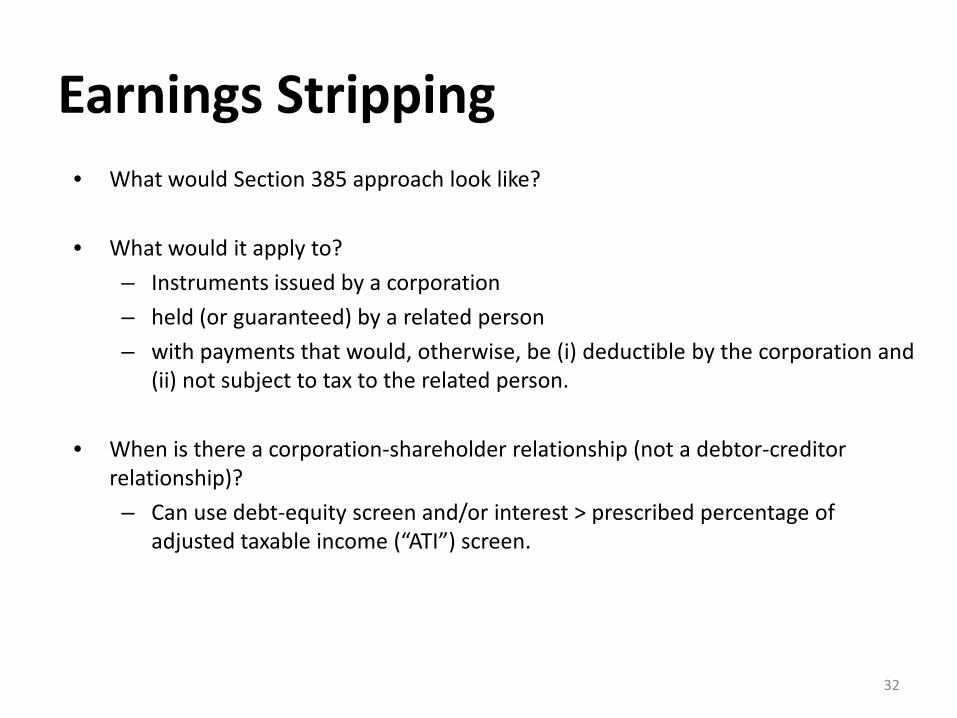

Earnings Stripping • What would Section 385 approach look like?

• What would it apply to?

– Instruments issued by a corporation – held (or guaranteed) by a related person – with payments that would, otherwise, be (i) deductible by the corporation and

(ii) not subject to tax to the related person.

• When is there a corporation-shareholder relationship (not a debtor-creditor relationship)? – Can use debt-equity screen and/or interest > prescribed percentage of

adjusted taxable income (“ATI”) screen.

32

Earnings Stripping • Authority: Section 385

“(a) Authority to prescribe regulations. — The Secretary is authorized to prescribe such regulations as may be necessary or appropriate to determine whether an interest in a corporation is to be treated for purposes of this title as stock or indebtedness (or as in part stock and in part indebtedness). (b) Factors. — The regulations prescribed under this section shall set forth factors which are to be taken into account in determining with respect to a particular factual situation whether a debtor-creditor relationship exists or a corporation-shareholder relationship exists. The factors so set forth in the regulations may include among other factors…”

33

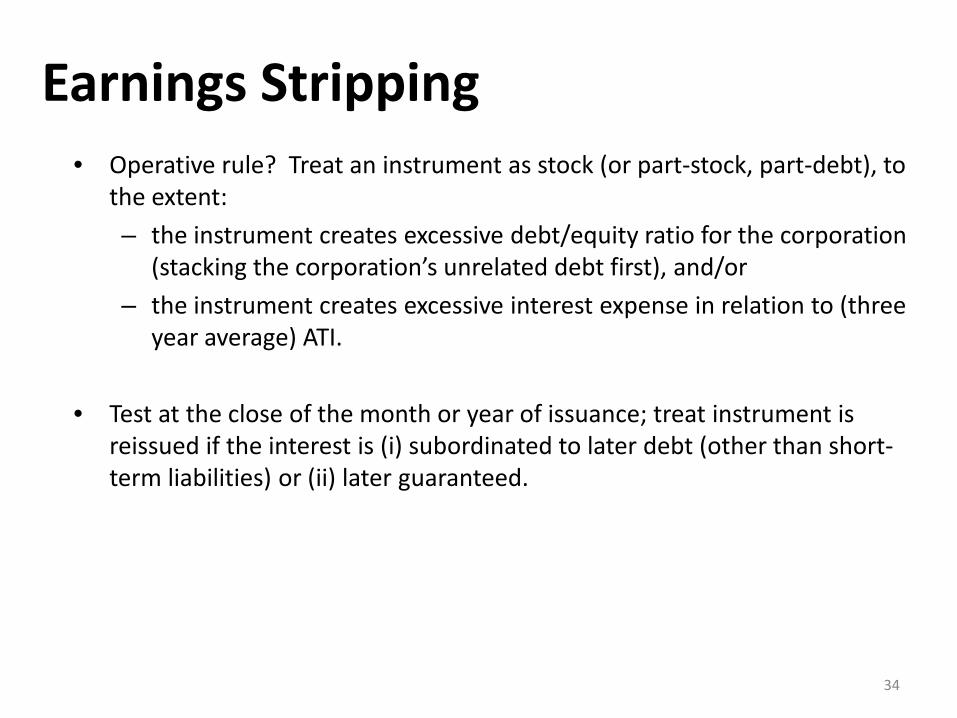

Earnings Stripping • Operative rule? Treat an instrument as stock (or part-stock, part-debt), to

the extent: – the instrument creates excessive debt/equity ratio for the corporation

(stacking the corporation’s unrelated debt first), and/or – the instrument creates excessive interest expense in relation to (three

year average) ATI.

• Test at the close of the month or year of issuance; treat instrument is reissued if the interest is (i) subordinated to later debt (other than short-term liabilities) or (ii) later guaranteed.

34

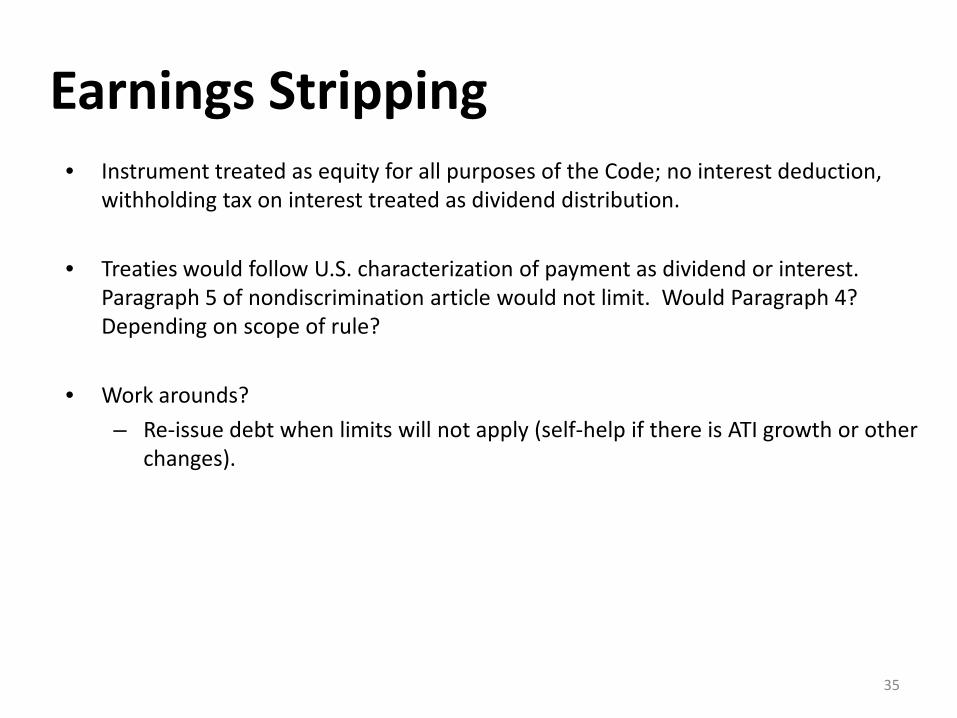

Earnings Stripping • Instrument treated as equity for all purposes of the Code; no interest deduction,

withholding tax on interest treated as dividend distribution.

• Treaties would follow U.S. characterization of payment as dividend or interest. Paragraph 5 of nondiscrimination article would not limit. Would Paragraph 4? Depending on scope of rule?

• Work arounds? – Re-issue debt when limits will not apply (self-help if there is ATI growth or other

changes).

35

Deborah L. Paul Wachtell, Lipton, Rosen & Katz

212-403-1300 (tel.) [email protected]

Deborah L. Paul is a partner in the Tax Department at Wachtell, Lipton, Rosen & Katz where she focuses on the tax aspects of corporate transactions, including mergers and acquisitions, joint ventures, spinoffs and financial instruments. Ms. Paul has been the principal tax lawyer on numerous domestic and cross-border transactions, including strategic acquisitions and private equity buyouts. Ms. Paul is a frequent speaker at Practising Law Institute, American Bar Association, New York State Bar Association and New York City Bar Association conferences on tax aspects of mergers and acquisitions and related topics. She is rated a leading tax lawyer by Chambers USA, Super Lawyers, the Legal 500 and Who’s Who Legal. She was elected partner in 2000.

Ms. Paul is an active member of the Executive Committee of the Tax Section of the New York State Bar Association. Prior to joining Wachtell Lipton in 1997, Ms. Paul was an assistant professor at the Benjamin N. Cardozo School of Law (1995-1997) and an acting assistant professor at New York University School of Law (1994-1995).

Ms. Paul received an A.B. from Harvard University in 1986, a J.D. from Harvard Law School in 1989 and an LL.M. in taxation from New York University School of Law in 1994.

STEVE EDGE

SLAUGHTER AND MAY

Steve Edge qualified with Slaughter and May in 1975 and acts for clients across the full range of the firm’s practice.

Steve read law at Exeter University and then completed his legal training period at Slaughter and May. In 2012, he was awarded an honorary doctorate in law by the University.

At Slaughter and May, Steve advises on the tax aspects of private and public mergers, acquisitions, disposals and joint ventures and on business and transaction structuring (including transfer pricing in all its aspects) more generally. He also advises many banks, insurance companies, hedge funds and others in the financial services sector in a wide range of areas.

It follows that much of Steve’s work has multinational cross-border aspects to it and that he needs to work closely with other leading international tax advisors around the world.

Steve plays a trusted advisor role for many of his multinational clients.

In recent years, Steve has been heavily involved in many in-depth tax investigations of specific domestic or international issues including transfer pricing in particular. He thus has considerable experience of negotiating and dealing with HMRC at all levels.

Steve has recently been on formal panels appointed by Government to introduce a REIT regime into the UK, to steer through the recent UK CFC changes and to formulate official Government guidance on the newly introduced GAAR.

Steve was also involved at the inception of the current Government’s approach to constructing a competitive tax policy in the UK.

Because of his involvement in that process in particular and also because of his international reputation, Steve was called upon in 2011 to give evidence to the Ways & Means Committee of Congress in the US about the UK experience in introducing a territorial tax system. He was also called by the House of Lords in 2013 to give evidence to its Economic Affairs Committee when it looked at the business tax regime in the UK generally.

In recent months, Steve has been heavily involved in consultations with the OECD on BEPS, particularly in relation to the anti-hybrid proposals.

He retains an active interest in matters of international tax policy.

999999/10322 TX 523376530 4 SME 171114:1646

STEPHEN E. SHAY Professor of Practice

Hauser 324 Harvard Law School

1575 Massachusetts Avenue Cambridge, MA 02138

Telephone: (617) 384-5311 E-mail: [email protected]

Stephen E. Shay is a Professor of Practice at Harvard Law School. Before joining the Harvard Law School faculty in 2011, Professor Shay was Deputy Assistant Secretary for International Tax Affairs in the United States Department of the Treasury. Prior to re-joining the Treasury Department in 2009, he was a tax partner for 22 years with Ropes & Gray, LLP. Professor Shay served in the Office of International Tax Counsel at the Department of the Treasury, including as International Tax Counsel, from 1982 to 1987. Professor Shay has published scholarly and practice articles relating to international taxation, and testified for law reform before Congressional tax-writing committees. He has consulted for the International Monetary Fund and the World Bank on international tax policy issues for project teams in Africa and the Caribbean and he is engaged in ongoing pro bono projects in Africa for the International Senior Lawyers Project. While in private practice, Professor Shay provided advice to business clients on a full range of international tax issues as well as advising governments on transfer pricing and information exchange issues. Professor Shay was recognized as a leading practitioner in Chambers Global: The World's Leading Lawyers, Chambers USA: America's Leading Lawyers, The Best Lawyers in America, Euromoney's Guide to The World's Leading Tax Advisers and Euromoney's, Guide to The Best of the Best. Professor Shay is a Vice President of the American Tax Policy Institute and a member of the Executive Committee of the New York State Bar Association Tax Section. Professor Shay has been active in the American Bar Association Tax Section as a Council Director and Chair of the Committee on Foreign Activities of U.S. Taxpayers, in the American Law Institute as an Associate Reporter and in the International Bar Association. Professor Shay’s outside activities may be found in a disclosure form appended to his Harvard Law School website biography. Professor Shay is a 1972 graduate of Wesleyan University, and he earned his J.D. and his M.B.A. from Columbia University in 1976.

ROBERT B. STACK DEPUTY ASSISTANT SECRETARY (INTERNATIONAL TAX AFFAIRS)

U.S. DEPARTMENT OF THE TREASURY

Bob Stack is the Deputy Assistant Secretary for International Tax Affairs in the Office of Tax Policy at the US Department of the Treasury. In this capacity, he is responsible, on behalf of the Assistant Secretary, for the conduct of legal and economic aspects of tax policy relative to the representation of the United States in bilateral and multilateral relations with other countries, as well as advising the legal and economic staffs within the Office of Tax Policy, other offices of the Treasury Department and other government agencies as to policy analysis and interpretation for domestic legislation and administrative guidance in all matters involving cross border taxation. Mr. Stack serves as the U.S. delegate to the Committee on Fiscal Affairs (CFA) in the Organization for Economic Cooperation and Development (the OECD). In addition, Mr. Stack oversees the Office of Tax Policy’s participation in the various working bodies of the CFA and sits on the CFA Bureau (the CFA’s governing body). Mr. Stack also serves as the U.S. delegate to the Global Forum on Transparency. Prior to joining Treasury, Mr. Stack served as head of the international tax practice group at the law firm of Ivins, Phillips & Barker. In the private sector, he has over 26 years of experience in international tax matters, representing both corporations and individuals. His work for corporations has included structuring both inbound and outbound ventures, the establishment of efficient cross border structures, the formation of joint ventures and private equity funds and all aspects of international mergers and acquisitions. He is a member of the American Bar Association Tax Section, New York State Bar Association Tax Section, and International Fiscal Association. Mr. Stack has participated in numerous panels on international tax issues at the meetings of the American Bar Association Tax Section as well as the Federal Bar Association. He graduated from Georgetown University Law Center in 1984, where he was editor-in-chief of the Georgetown Law Journal. After graduating, he clerked for Judge Thomas A. Flannery of the United States District Court for the District of Columbia and Justice Potter Stewart (Ret.) of the United States Supreme Court.