Cornerstone Institutional Investors,...

210

74 W. Broad St. Suite 340 Bethlehem, PA 18018 www.cornerstone-companies.com Cornerstone Institutional Investors, Inc. October 17, 2014 Christopher Lakatosh, CFP ® , AIF ® Principal & Senior Consultant Email: [email protected] Phone: 800-923-0900 74 W. Broad Street Suite 340 Bethlehem, PA 18018 Contact: Request for Information: Northern York County Regional Police Pension Fund Pension Fund Investment Consulting Services

Transcript of Cornerstone Institutional Investors,...

www.cornerstone-companies.com

74 W. Broad St. Suite 340 Bethlehem, PA 18018

www.cornerstone-companies.com

Cornerstone Institutional Investors, Inc.

October 17, 2014

Christopher Lakatosh, CFP®, AIF®

Principal & Senior Consultant

Email: [email protected]

Phone: 800-923-0900

74 W. Broad Street

Suite 340

Bethlehem, PA 18018

Contact:

Request for Information:

Northern York County Regional Police Pension Fund

Pension Fund Investment Consulting Services

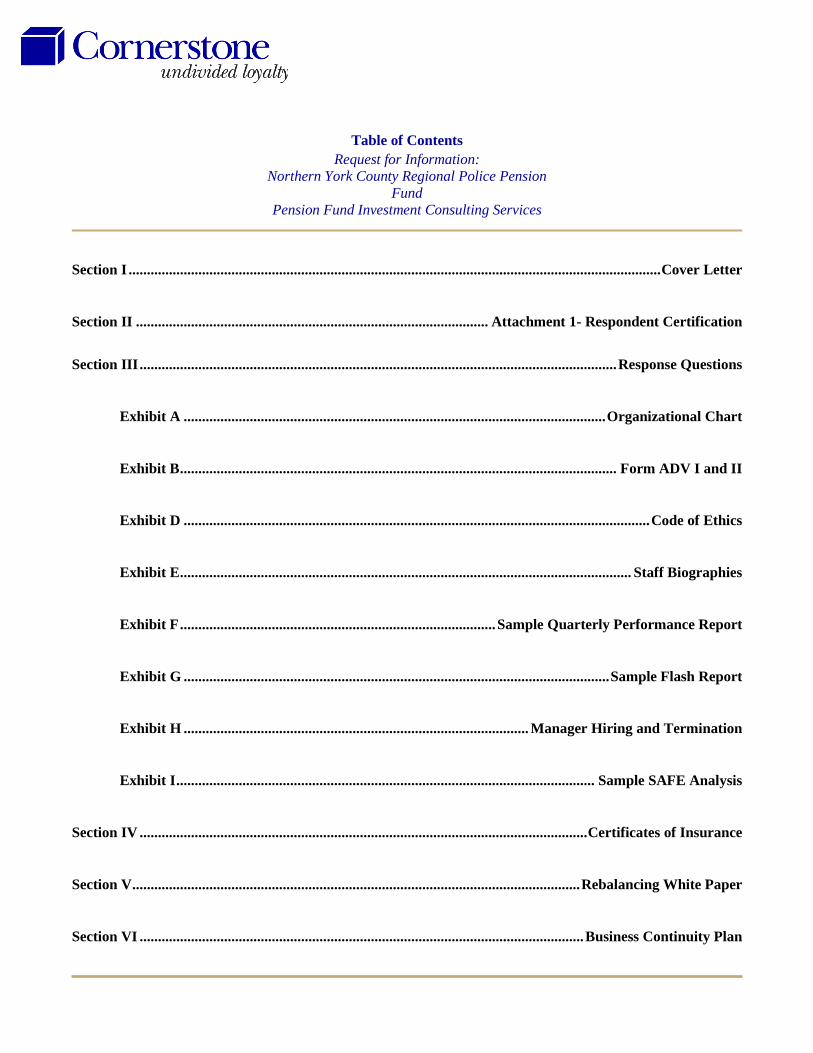

Table of Contents Request for Information:

Northern York County Regional Police Pension Fund

Pension Fund Investment Consulting Services

Section I ................................................................................................................................................. Cover Letter

Section II ................................................................................................ Attachment 1- Respondent Certification

Section III .................................................................................................................................. Response Questions

Exhibit A ................................................................................................................... Organizational Chart

Exhibit B ....................................................................................................................... Form ADV I and II

Exhibit D ............................................................................................................................... Code of Ethics

Exhibit E ........................................................................................................................... Staff Biographies

Exhibit F ...................................................................................... Sample Quarterly Performance Report

Exhibit G .................................................................................................................... Sample Flash Report

Exhibit H .............................................................................................. Manager Hiring and Termination

Exhibit I .................................................................................................................. Sample SAFE Analysis

Section IV .......................................................................................................................... Certificates of Insurance

Section V .......................................................................................................................... Rebalancing White Paper

Section VI ......................................................................................................................... Business Continuity Plan

Section I

Cover Letter

w 74 W. Broad St., Suite 340, Bethlehem, PA 18018 w Phone: 610-694-0900 w Fax: 610-867-8614

www.cornerstone-companies.com 74 W. Broad St., Suite 340, Bethlehem, PA 18018 • (800) 923-0900, (610) 694-0900 • Fax: (610) 867-8614

Securities offered through M Holdings Securities, Inc., a Registered Broker/Dealer, Member FINRA/SIPC. Investment Advisory Services offered through Cornerstone Advisors Asset Management and/or Cornerstone Institutional Investors, Inc., which are independently owned and operated.

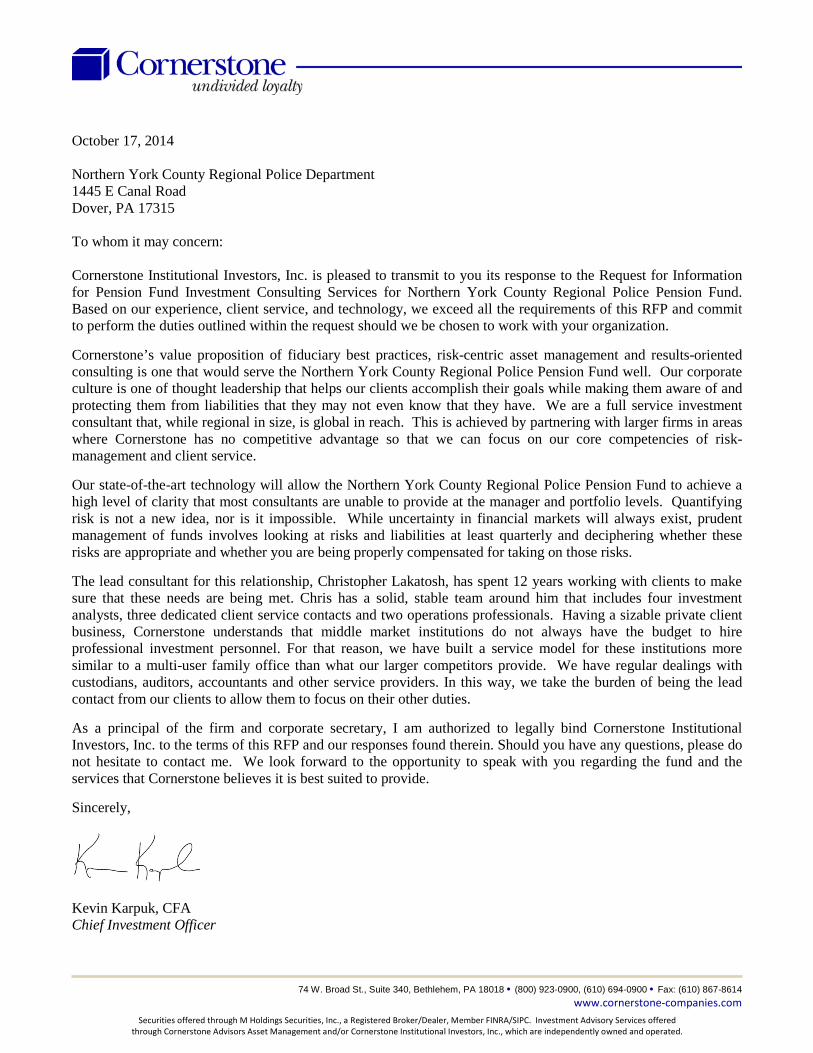

October 17, 2014 Northern York County Regional Police Department 1445 E Canal Road Dover, PA 17315 To whom it may concern: Cornerstone Institutional Investors, Inc. is pleased to transmit to you its response to the Request for Information for Pension Fund Investment Consulting Services for Northern York County Regional Police Pension Fund. Based on our experience, client service, and technology, we exceed all the requirements of this RFP and commit to perform the duties outlined within the request should we be chosen to work with your organization.

Cornerstone’s value proposition of fiduciary best practices, risk-centric asset management and results-oriented consulting is one that would serve the Northern York County Regional Police Pension Fund well. Our corporate culture is one of thought leadership that helps our clients accomplish their goals while making them aware of and protecting them from liabilities that they may not even know that they have. We are a full service investment consultant that, while regional in size, is global in reach. This is achieved by partnering with larger firms in areas where Cornerstone has no competitive advantage so that we can focus on our core competencies of risk-management and client service. Our state-of-the-art technology will allow the Northern York County Regional Police Pension Fund to achieve a high level of clarity that most consultants are unable to provide at the manager and portfolio levels. Quantifying risk is not a new idea, nor is it impossible. While uncertainty in financial markets will always exist, prudent management of funds involves looking at risks and liabilities at least quarterly and deciphering whether these risks are appropriate and whether you are being properly compensated for taking on those risks. The lead consultant for this relationship, Christopher Lakatosh, has spent 12 years working with clients to make sure that these needs are being met. Chris has a solid, stable team around him that includes four investment analysts, three dedicated client service contacts and two operations professionals. Having a sizable private client business, Cornerstone understands that middle market institutions do not always have the budget to hire professional investment personnel. For that reason, we have built a service model for these institutions more similar to a multi-user family office than what our larger competitors provide. We have regular dealings with custodians, auditors, accountants and other service providers. In this way, we take the burden of being the lead contact from our clients to allow them to focus on their other duties. As a principal of the firm and corporate secretary, I am authorized to legally bind Cornerstone Institutional Investors, Inc. to the terms of this RFP and our responses found therein. Should you have any questions, please do not hesitate to contact me. We look forward to the opportunity to speak with you regarding the fund and the services that Cornerstone believes it is best suited to provide. Sincerely,

Kevin Karpuk, CFA Chief Investment Officer

Section II

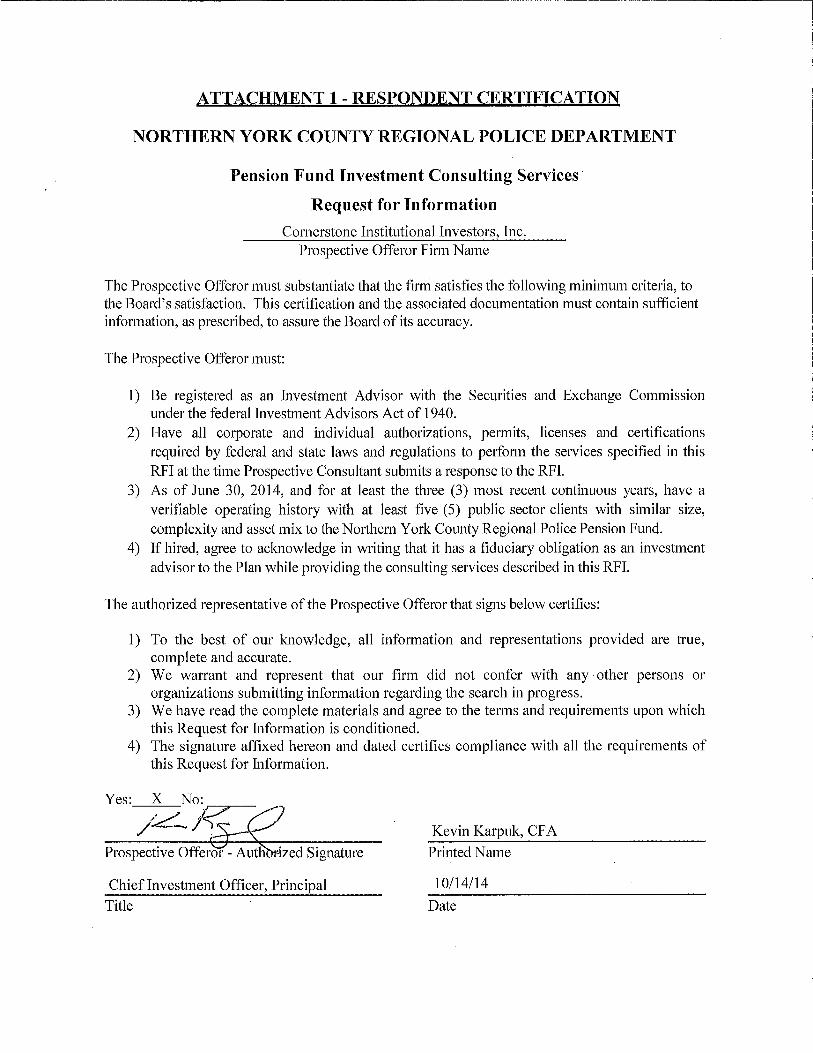

Attachment 1 - Respondent Certification

w 74 W. Broad St., Suite 340, Bethlehem, PA 18018 w Phone: 610-694-0900 w Fax: 610-867-8614

Section III

Response Questions

w 74 W. Broad St., Suite 340, Bethlehem, PA 18018 w Phone: 610-694-0900 w Fax: 610-867-8614

1

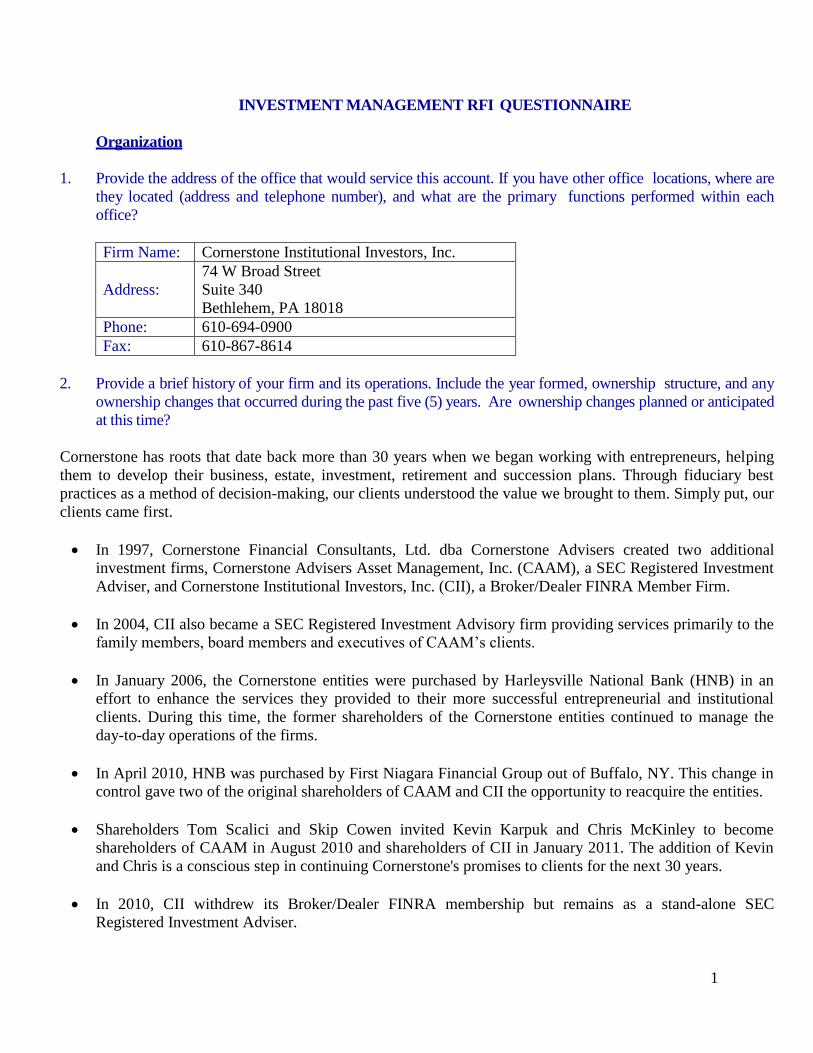

INVESTMENT MANAGEMENT RFI QUESTIONNAIRE

Organization

1. Provide the address of the office that would service this account. If you have other office locations, where are

they located (address and telephone number), and what are the primary functions performed within each

office?

Firm Name: Cornerstone Institutional Investors, Inc.

Address:

74 W Broad Street

Suite 340

Bethlehem, PA 18018

Phone: 610-694-0900

Fax: 610-867-8614

2. Provide a brief history of your firm and its operations. Include the year formed, ownership structure, and any

ownership changes that occurred during the past five (5) years. Are ownership changes planned or anticipated

at this time?

Cornerstone has roots that date back more than 30 years when we began working with entrepreneurs, helping

them to develop their business, estate, investment, retirement and succession plans. Through fiduciary best

practices as a method of decision-making, our clients understood the value we brought to them. Simply put, our

clients came first.

In 1997, Cornerstone Financial Consultants, Ltd. dba Cornerstone Advisers created two additional

investment firms, Cornerstone Advisers Asset Management, Inc. (CAAM), a SEC Registered Investment

Adviser, and Cornerstone Institutional Investors, Inc. (CII), a Broker/Dealer FINRA Member Firm.

In 2004, CII also became a SEC Registered Investment Advisory firm providing services primarily to the

family members, board members and executives of CAAM’s clients.

In January 2006, the Cornerstone entities were purchased by Harleysville National Bank (HNB) in an

effort to enhance the services they provided to their more successful entrepreneurial and institutional

clients. During this time, the former shareholders of the Cornerstone entities continued to manage the

day-to-day operations of the firms.

In April 2010, HNB was purchased by First Niagara Financial Group out of Buffalo, NY. This change in

control gave two of the original shareholders of CAAM and CII the opportunity to reacquire the entities.

Shareholders Tom Scalici and Skip Cowen invited Kevin Karpuk and Chris McKinley to become

shareholders of CAAM in August 2010 and shareholders of CII in January 2011. The addition of Kevin

and Chris is a conscious step in continuing Cornerstone's promises to clients for the next 30 years.

In 2010, CII withdrew its Broker/Dealer FINRA membership but remains as a stand-alone SEC

Registered Investment Adviser.

2

Today, CAAM and CII specialize in consulting to successful institutions and wealthy families who have

fiduciary responsibility for the assets under their care.

Understanding CAAM and CII

CAAM provides services exclusively for clients with assets in excess of $25 million. CII works with clients who

have liquid assets from $1 million to $25 million. Together, the two companies serve sophisticated financial

market participants through investment consulting, retirement plan consulting, executive risk management,

planned giving, wealth management, financial planning, charitable planning and insurance/risk planning.

Cornerstone Advisors Asset Management, Inc. (CAAM) and Cornerstone Institutional Investors, Inc. (CII) have

earned top rankings for assets under management in the Lehigh Valley. CAAM has been listed as #1 by Lehigh

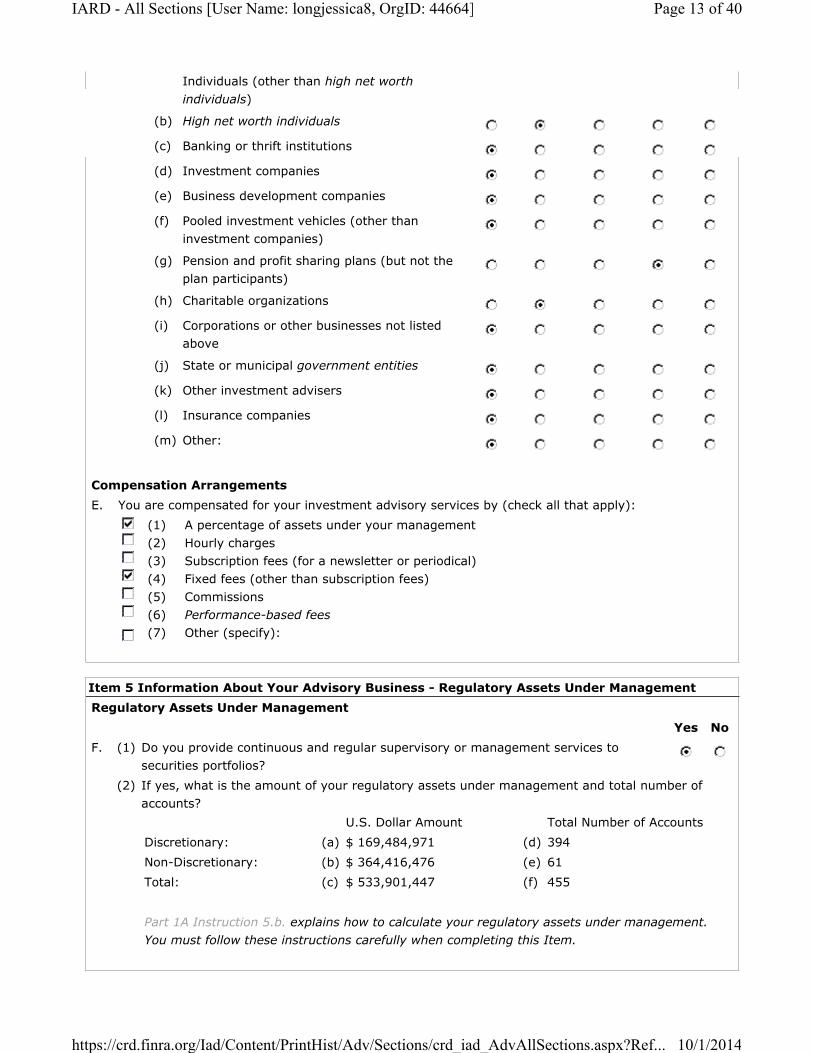

Valley Business with $3.95 billion in fiscal year 2013, while CII earns the #4 spot with $533.9 million.

Outside of the Lehigh Valley, Cornerstone Advisors Asset Management, Inc. was ranked by Financial Advisor

Magazine as the 32nd largest Registered Investment Advisory firm in the country as of December 31, 2013.

Additionally, they are currently recognized as the 95th largest consultant in worldwide institutional advisory

assets by Pensions & Investments magazine.

CII is also a member firm of the M Financial Group (M). M is the largest insurance buying consortium in the

country. M allows our clients access to proprietary products designed to help them protect their assets and

manage the shortfall risk around retirement income funding, disability, long-term care and estate preservation, all

of which have an impact on their liquid asset strategy.

3. Provide copies of the following organizational charts as Exhibit A:

- Organizational structure, including parent/subsidiary relationships, if any;

- Your consulting unit listing major functional areas with the names and titles of key staff in each

area along with the total number of staff in each area and their experience. If there are staffing

overlaps, please indicate and explain as a footnote.

Please see Section III, Exhibit A for Cornerstone’s organizational chart.

4. List your firm’s lines of business and the approximate contributions of each business to your organization’s

total revenue. If you are an affiliate or subsidiary of an organization, what percentage of the parent firm’s total

revenue does your subsidiary or affiliate generate?

Cornerstone provides investment advisory services to several different market segments including defined

benefit, endowment/foundation, defined contribution, and planned giving markets. Regardless of the market

segment, Cornerstone applies our unbiased, independent third-party approach to investment advice. Please see

below for each advisory business segment’s revenue contribution.

Business Segment Revenue Contribution

Planned Giving Services 5%

Retirement Planning - DC 15%

Retirement Planning - DB 20%

Investment Consulting 60%

3

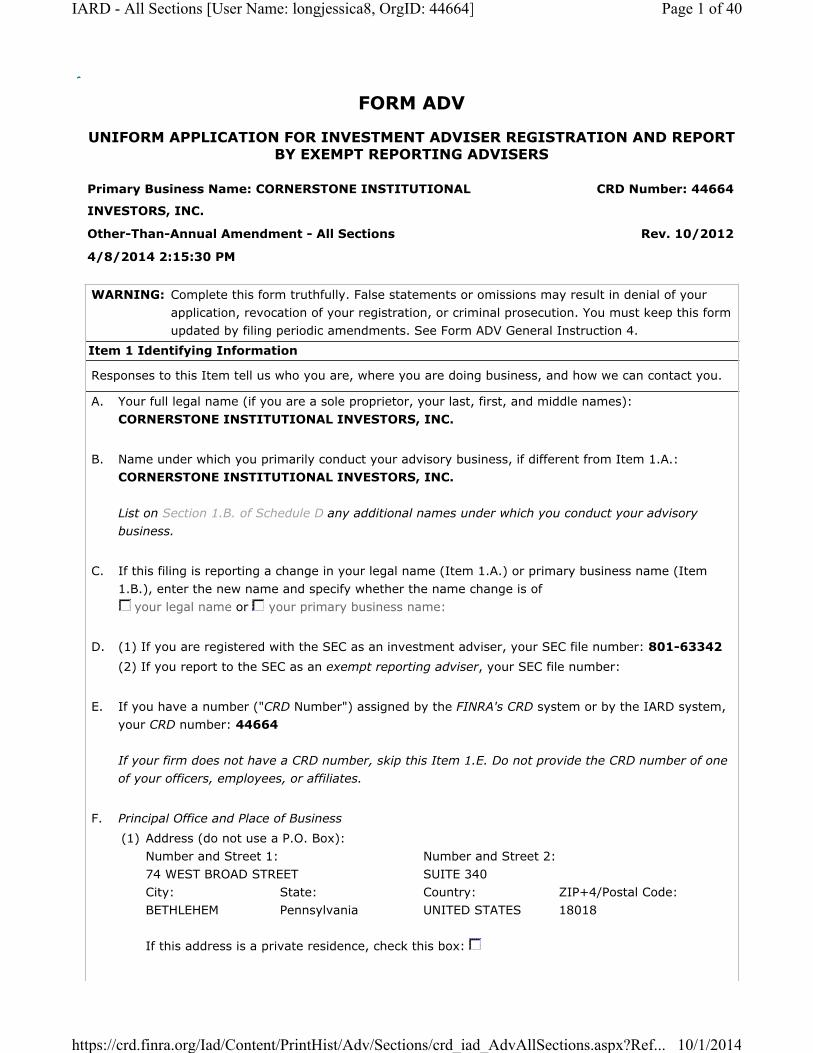

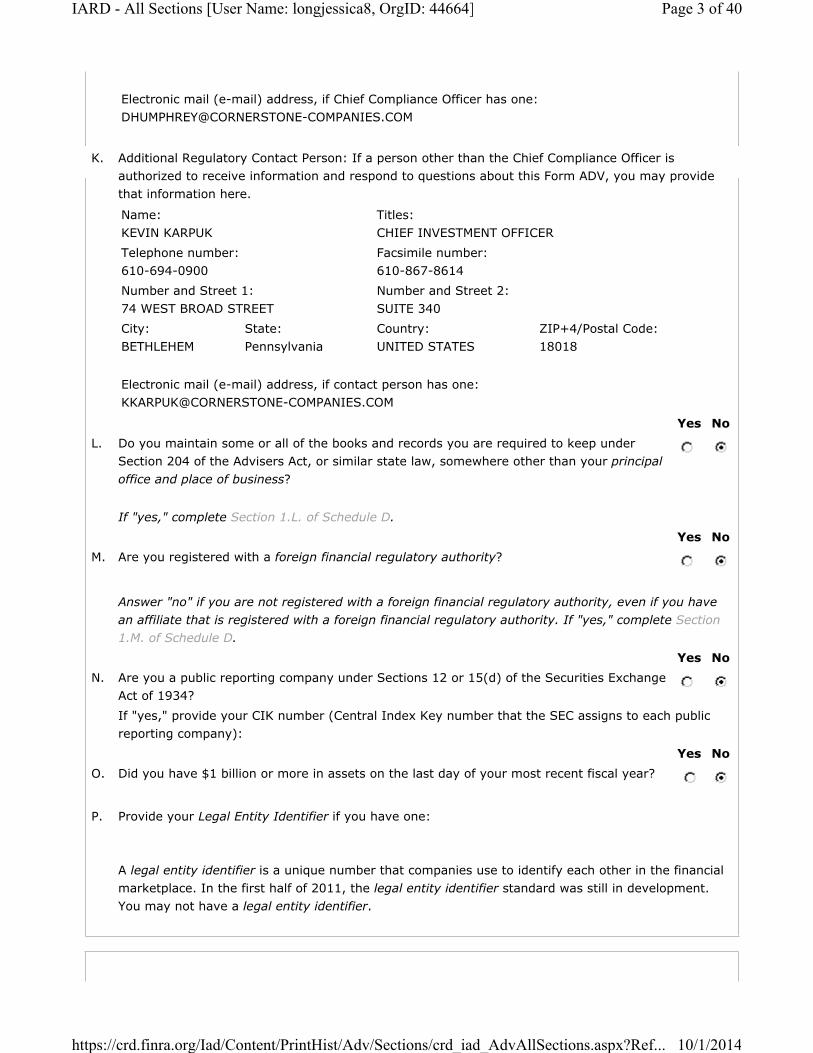

5. When was the firm first registered as an investment advisor under the federal Investment Advisors Act of

1940? Please provide Form ADV I and II as Exhibit B.

Cornerstone Institutional Investors, Inc. is an SEC Registered Investment Advisor since 2004. Please see

Section III, Exhibit B for Cornerstone’s ADV Part I & II.

6. Do you consider yourself a fiduciary under applicable law with respect to recommendations you will provide?

If hired, will you acknowledge in writing that you have a fiduciary obligation as an investment advisor to the

Plan while providing the consulting services we are seeking?

Yes. Since our founding, Cornerstone has been a trendsetter in fiduciary matters among consultants, including

being a co-fiduciary with our clients and accepting discretion for clients’ assets. Though the market is changing

and other consultants are starting to reluctantly embrace the Cornerstone Model of consulting, many clients still

view consultants as third parties who only provide performance monitoring and manager searches rather than

leadership and decision making. We have built a business that fully acknowledges our standing as a guide for

our clients because we believe that it is both the legally and morally correct course of business. By offering

advice for a fee, we become a de facto co-fiduciary with our clients and willingly acknowledge that in writing.

By contractually becoming a co-fiduciary with our clients, we serve as the “Prudent Expert” described in

fiduciary law and provide a “Safe Harbor” for investment committee members with fiduciary liability.

7. Provide details on the financial condition of your firm as Exhibit C. The most recent annual report filed with

the SEC is acceptable, but any recent material changes should be included.

Cornerstone is a privately held firm and does not publish our financials. We would be happy to share with you

the details in a face-to-face setting. Please see Section III, Exhibit B for Cornerstone’s ADV Part I & II

8. Briefly summarize your philosophy relating to the consultant's relationship with Boards/Committees, Staff,

Investment Managers and Brokers.

Cornerstone’s success is driven by the satisfaction and success of our clients. With that in mind, we seek

relationships that are free of conflicts of interest that will best serve our clients. A Cornerstone client is a client

from the Chair of the Board through the receptionist at our client’s front desk. We strive to provide the highest

level of service throughout our clients’ entire organizations, whether that entails regular meetings, ad-hoc

educational sessions, ongoing audit support, or any other part of our wide menu of services.

Cornerstone’s relationships with investment managers, custodians, and brokers are ongoing. As an open

architecture firm, we have no operational or financial ties to any specific vendor. Our analyst team is responsible

for relationships with current and prospective vendors and interacts daily with various industry contacts. We

seek best-of-breed providers who provide attractive services at a competitive cost.

9. Disclose any relationship you have or have had with any Board Member or NYCRPD employee. If there are

none, so state.

Cornerstone does not have nor had any relationships with any Board Member or NYCRPD employee.

4

10. Do you or a related company have relationships with money managers that you recommend, consider for

recommendation, or otherwise mention to clients? If so, describe those relationships.

Cornerstone does not have any relationships or affiliation with any money manager.

11. Do you or a related company receive any payments from money managers that you recommend, consider for

recommendation or otherwise mention to clients? If so, what is the extent of these payments in relation to

your other income (revenue)? What percentage of your clients utilizes money managers, investment funds,

brokerage services or other service providers from whom you receive fees?

We receive no soft dollars and have no financial relationships with any money manager or any kind of third-party

vendors allowing us to be completely independent and unbiased in our services to our clients.

12. Do you have any written policies or procedures to address conflicts of interest, including (but not limited to)

the payment of fees or other consideration from other clients, relationships or entities that may compromise

your fiduciary duty to your clients? If so, please include a copy as Exhibit D.

To combat any sort of conflict of interest, Cornerstone has adopted a Code of Ethics for all employees describing

its high standard of business conduct, and fiduciary duty to our clients. The Code of Ethics includes provisions

relating to the confidentiality of client information, a prohibition on insider trading, entertainment items, and

personal securities trading procedures, among other things. As a summary of the entire Code of Ethics, we

believe that The Statement of General Principles found within the Code of Ethics best encapsulates our internal

rules regarding our relationship with you. It reads as follows:

“In recognition of the trust and confidence placed in the Firm by its clients and to stress its belief that its

operations are directed to the benefit of its clients, the Firm has developed and adopted the following general

principles to guide its associated persons, officers, and directors:

1. The interests of the clients are paramount and all associated persons of the Firm must conduct

themselves in such a manner that the interests of the clients take precedence over all others.

2. All personal securities transactions by associated persons of the Firm must be placed in such

a way as to avoid any conflict between the interest of the Firm’s clients and the interest of any

associated person of the Firm.

3. All associated persons of the Firm must avoid actions or activities that allow personal benefit

or profit from their position with regard to the Firm’s clients.

4. All associated persons will remain compliant with federal securities laws.

5. Any potential violations of this Code of Ethics must be promptly reported to the Chief

Compliance Officer.

Please see Section III for Exhibit D, a copy of Cornerstone’s Code of Ethics.

5

13. In addition to the investment consulting fees paid to your firm by clients who retain your firm as their

investment consultant, what other sources of revenue does your firm and/or your firm’s affiliates receive that

relate (directly or indirectly) to the provision of investment consulting services?

As a conflict free advisor, we receive no payment except the hard dollar fees paid by our clients. We

provide no consulting or marketing services to any third party vendor other than our clients. As a co-

fiduciary, Cornerstone does not enter into any formal or informal business relationships with any service

provider. As such we are not compensated through any soft dollar arrangements. Transparency is at the

forefront of everything we do.

14. Is your firm or affiliate a broker/dealer? If yes, does this broker/dealer execute trades for portfolios for which

your firm provides consulting services? Do you have any arrangement with broker/dealers under which you

or an affiliated/related company will benefit if money managers place trades for their clients with such

broker/dealers?

CII is affiliated with M Holdings Securities, Inc., a FINRA member broker/dealer. This affiliation

affords our private clients access to certain financial products that they otherwise would not have access

to. CII’s institutional investment clients do not have any dealings with our broker-dealer. We receive no

soft dollars and have no financial relationships of any kind with third-party vendors allowing us to be

completely independent and unbiased in our services to our clients.

15. Has your firm or any officer or principal of your organization been involved in litigation or any SEC or other

regulatory action relating to investment management, brokerage or consulting activities in the last ten (10)

years? If so, provide a brief explanation and indicate the current status of the proceedings.

No complaints, claims or investigations as described above have occurred over the last ten years, none are

pending and none are foreseen.

16. Do you subcontract or outsource any parts of your investment consulting business? If yes, please describe in

detail which parts are performed externally and the reason for doing so. Please provide the names of the

providers, their office location, how long they have been in business and the qualifications of the specific

people who would be working on our account.

Cornerstone does not engage in any subcontractor relationships.

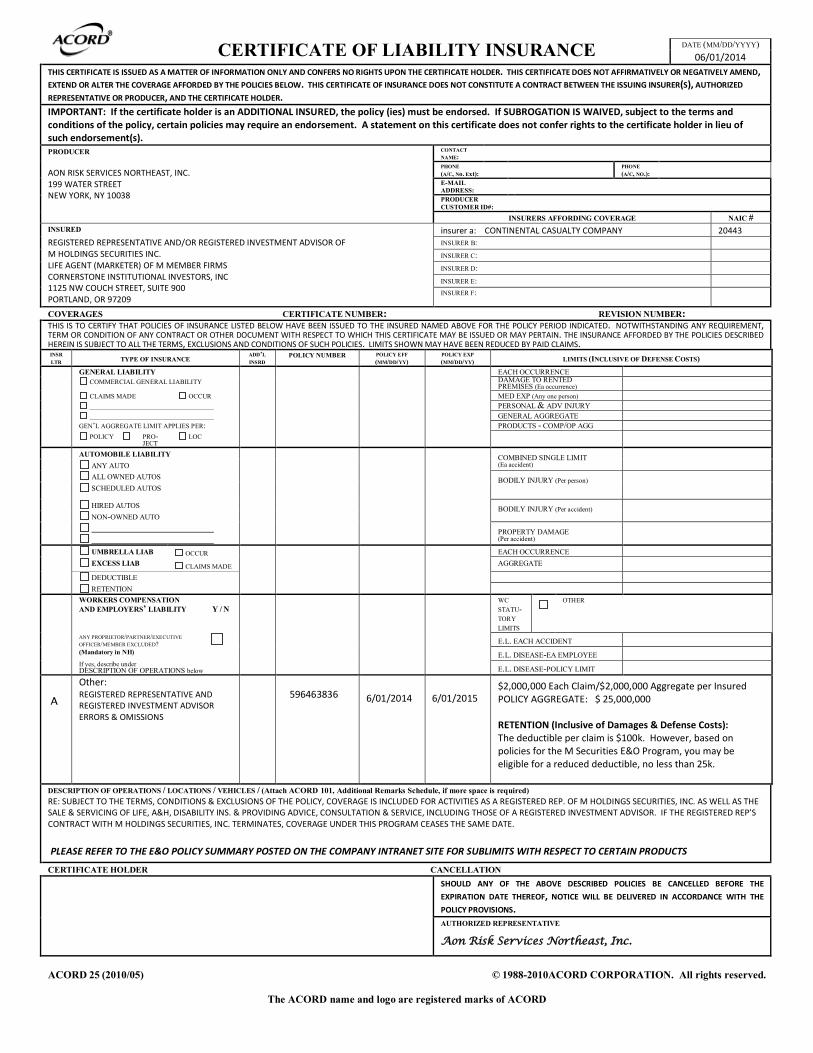

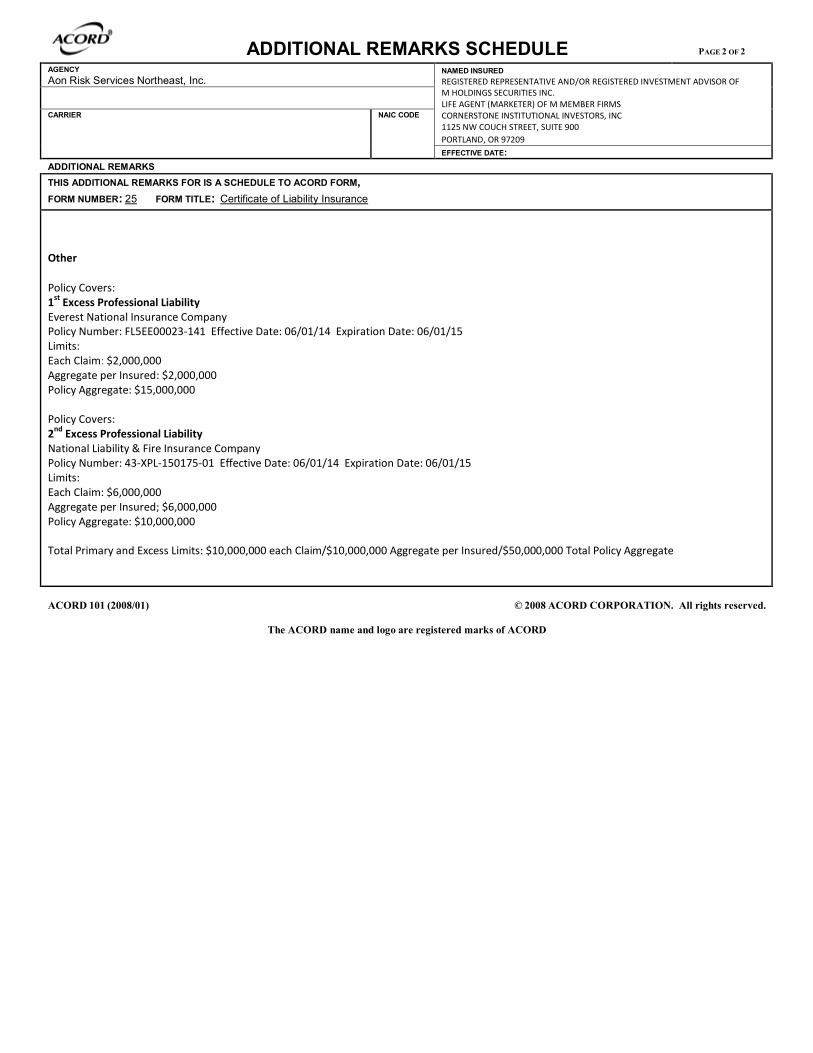

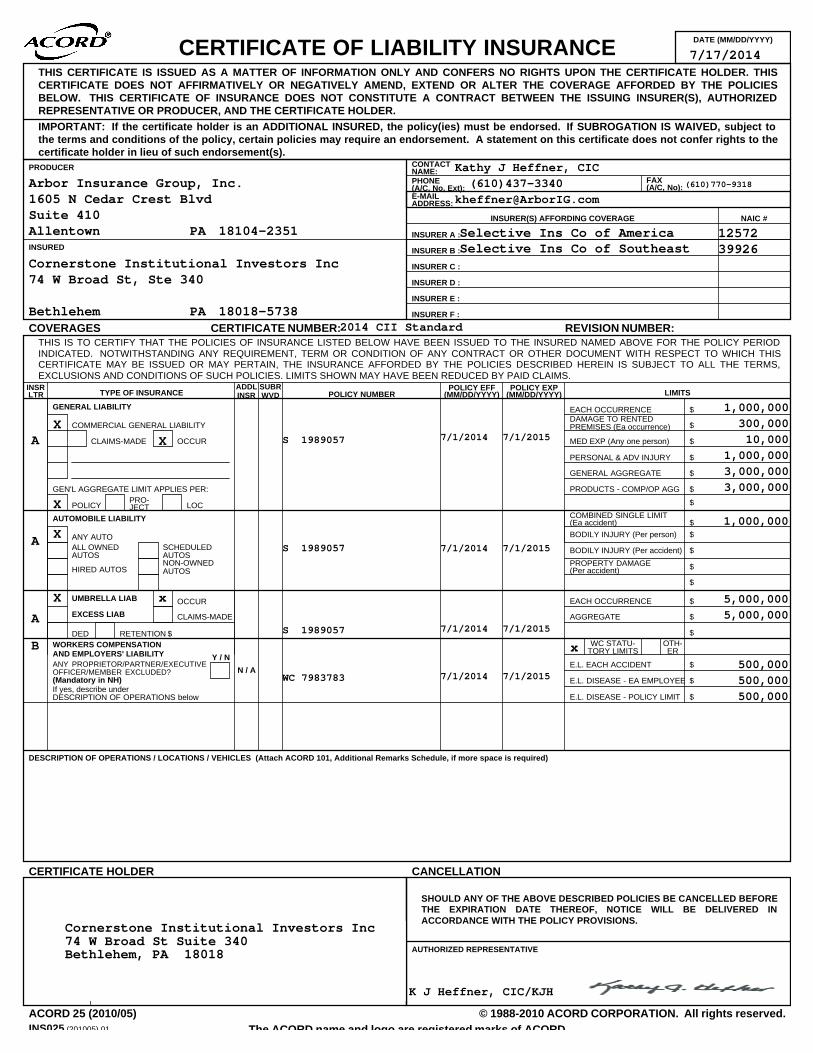

17. Describe the levels of coverage for errors and omissions insurance and any other fiduciary and professional

liability insurance the firm carries. List the insurance carriers providing the coverage.

Cornerstone maintains significant Errors & Omissions insurance issued through various entities. We have four

policies with $10 mm aggregate claims and a fifth with a $5 mm claim maximum. Currently, we are not required

to notify our clients of a pending insurance cancellation but we feel it is our duty to go above and beyond and

notify our clients to any changes with our insurance policies. Certificates of insurance can be found in Section

IV.

18. What are your firm's consulting specialties and strengths? What are your firm’s limitations?

6

All of Cornerstone’s clients benefit from our risk focused investment management process. The world of public

pension plans has been turned on its head over the last several years due to poor market performance, aging

workforces and a long term lack of funding while markets were performing well. The one benefit that public

pension plans have had compared to ERISA plans is that the discount rate associated with liabilities is not tied to

market rates, a major source of private sector underfunding. Cornerstone has been able to work with clients to

provide a framework for success that begins with a robust fiduciary process and then follows with unbiased

consulting that rigorously and continuously monitors the results of the plan.

Should you choose to engage in further conversations with us, we expect you to understand that a healthy

pension fund is a continuously funded, well monitored pool of assets. Investment returns are not a panacea.

Only in coordination with proper funding and prudent liability management does an underfunded fund become a

healthy fund. We strive to set realistic expectations that can be met through prudent management of the

investments and liabilities of the Fund.

We truly believe that we are a firm without limitations. We are agnostic as to who we work with from an

investment management prospective. We can work with any custodian, any mutual fund, any separate account in

the universe and as such can have a completely independent view of our clients position and how best to position

a solution. We customize our reporting and have developed industry leading reporting and performance due

diligence. All of these factors allow us to sit squarely on the same side of the table as our clients.

19. Who are your top five (5) competitors? What differentiates your firm from your competition? Why should the

Plan hire your firm rather than your competitor(s)?

Having a specialized focus in the management of pension plan assets, we have competitors in different markets (large

pensions or small) and different industries. Whether we are working in the large municipal market place or smaller

ERISA governed private pension plans we are regularly competing against national firms and consistently winning

business. A few names that we see are PFM, Morgan Stanley, Wells Fargo, Pierce Park and Beirne Wealth

Consulting.

Our competitors focus blindly on return. What makes Cornerstone unique is our understanding of, the ability to

identify, articulate, monitor and manage the levels of risk within our client portfolios. Risk is neither good nor

bad it is just risk but it does have a direct correlation on the levels of return of the portfolio. Our competitors are

not able to provide to their clients an answer to the question of are they being compensated for the risks that they

are taking. Understanding that the market moves geometrically, meaning if you lose 50% you have to make

100% to get back to even, we pay considerable attention to the risks and most importantly the downside risk

potential of our clients’ accounts. Holding market value in down markets is far more important than squeezing

every last drip of up market capture. Large losses in down markets will wreak havoc on the funded status of the

plan. The other area that sets us apart in the management pension plan assets is our focus on the liability side of

the balance sheet as well. The funded status will have a direct impact on the budget considerations of the

municipality, which can then translate into tighter budgets, higher taxes etc. Identifying risk, being able to

manage and smooth the volatility of the pension, mitigating large losses, identifying the liability side of the

pension balance sheet are all differentiators to our competitors.

20. What investment consulting services do you provide to clients that are not among the specific services

requested in this RFI?

7

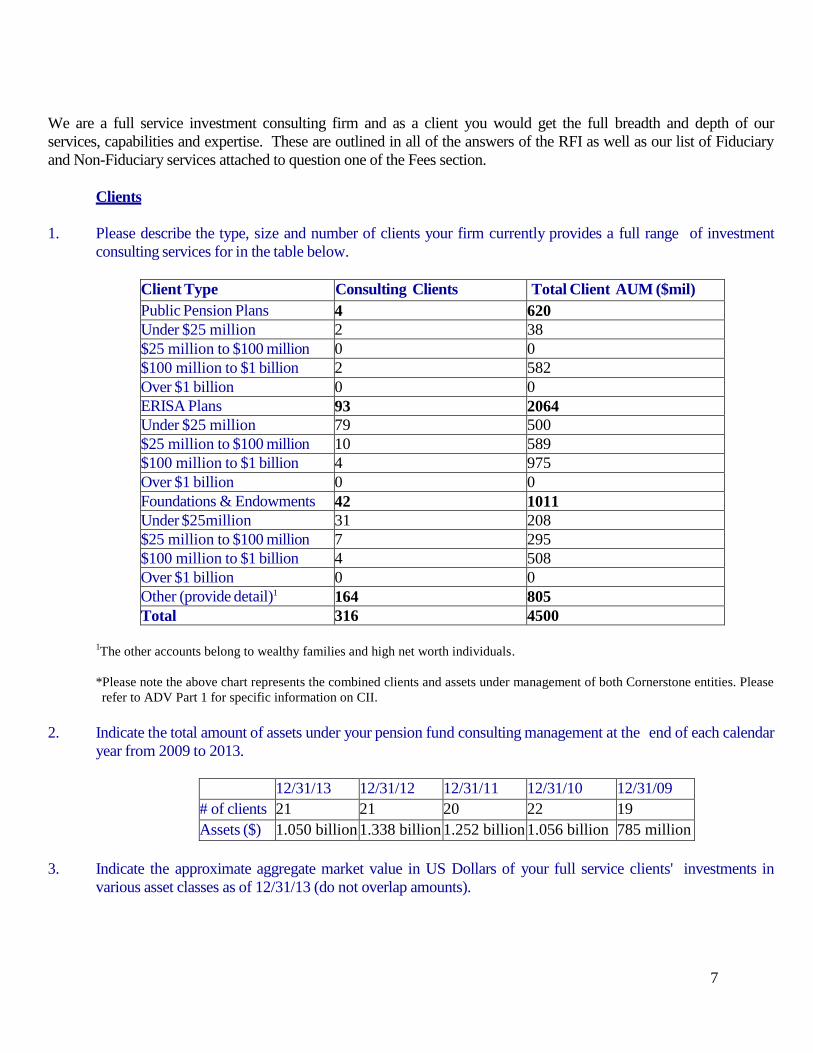

We are a full service investment consulting firm and as a client you would get the full breadth and depth of our

services, capabilities and expertise. These are outlined in all of the answers of the RFI as well as our list of Fiduciary

and Non-Fiduciary services attached to question one of the Fees section.

Clients

1. Please describe the type, size and number of clients your firm currently provides a full range of investment

consulting services for in the table below.

Client Type # of Consulting Clients Total Client AUM ($mil)

Public Pension Plans 4

620

Under $25 million 2 38

$25 million to $100 million 0 0

$100 million to $1 billion 2 582

Over $1 billion 0 0

ERISA Plans 93 2064

Under $25 million 79 500

$25 million to $100 million 10 589

$100 million to $1 billion 4 975

Over $1 billion 0 0

Foundations & Endowments 42 1011

Under $25million 31 208

$25 million to $100 million 7 295

$100 million to $1 billion 4 508

Over $1 billion 0 0

Other (provide detail)1 164 805

Total 316 4500

1The other accounts belong to wealthy families and high net worth individuals.

*Please note the above chart represents the combined clients and assets under management of both Cornerstone entities. Please

refer to ADV Part 1 for specific information on CII.

2. Indicate the total amount of assets under your pension fund consulting management at the end of each calendar

year from 2009 to 2013.

12/31/13 12/31/12 12/31/11 12/31/10 12/31/09

# of clients 21 21 20 22 19

Assets ($) 1.050 billion 1.338 billion 1.252 billion 1.056 billion 785 million

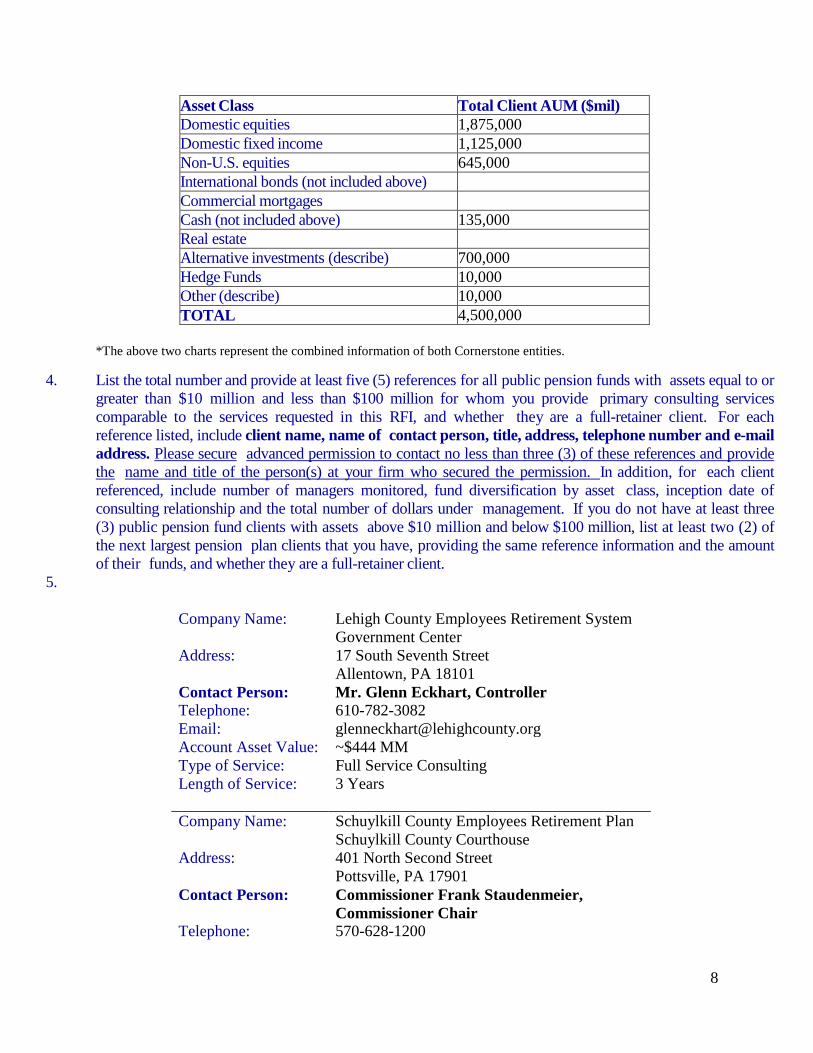

3. Indicate the approximate aggregate market value in US Dollars of your full service clients' investments in

various asset classes as of 12/31/13 (do not overlap amounts).

8

Asset Class Total Client AUM ($mil)

Domestic equities 1,875,000

Domestic fixed income 1,125,000

Non-U.S. equities 645,000

International bonds (not included above)

Commercial mortgages

Cash (not included above) 135,000

Real estate

Alternative investments (describe) 700,000

Hedge Funds 10,000

Other (describe) 10,000

TOTAL 4,500,000

*The above two charts represent the combined information of both Cornerstone entities.

4. List the total number and provide at least five (5) references for all public pension funds with assets equal to or

greater than $10 million and less than $100 million for whom you provide primary consulting services

comparable to the services requested in this RFI, and whether they are a full-retainer client. For each

reference listed, include client name, name of contact person, title, address, telephone number and e-mail

address. Please secure advanced permission to contact no less than three (3) of these references and provide

the name and title of the person(s) at your firm who secured the permission. In addition, for each client

referenced, include number of managers monitored, fund diversification by asset class, inception date of

consulting relationship and the total number of dollars under management. If you do not have at least three

(3) public pension fund clients with assets above $10 million and below $100 million, list at least two (2) of

the next largest pension plan clients that you have, providing the same reference information and the amount

of their funds, and whether they are a full-retainer client.

5.

Company Name: Lehigh County Employees Retirement System

Address:

Government Center

17 South Seventh Street

Allentown, PA 18101

Contact Person: Mr. Glenn Eckhart, Controller

Telephone: 610-782-3082

Email: [email protected]

Account Asset Value: ~$444 MM

Type of Service: Full Service Consulting

Length of Service: 3 Years

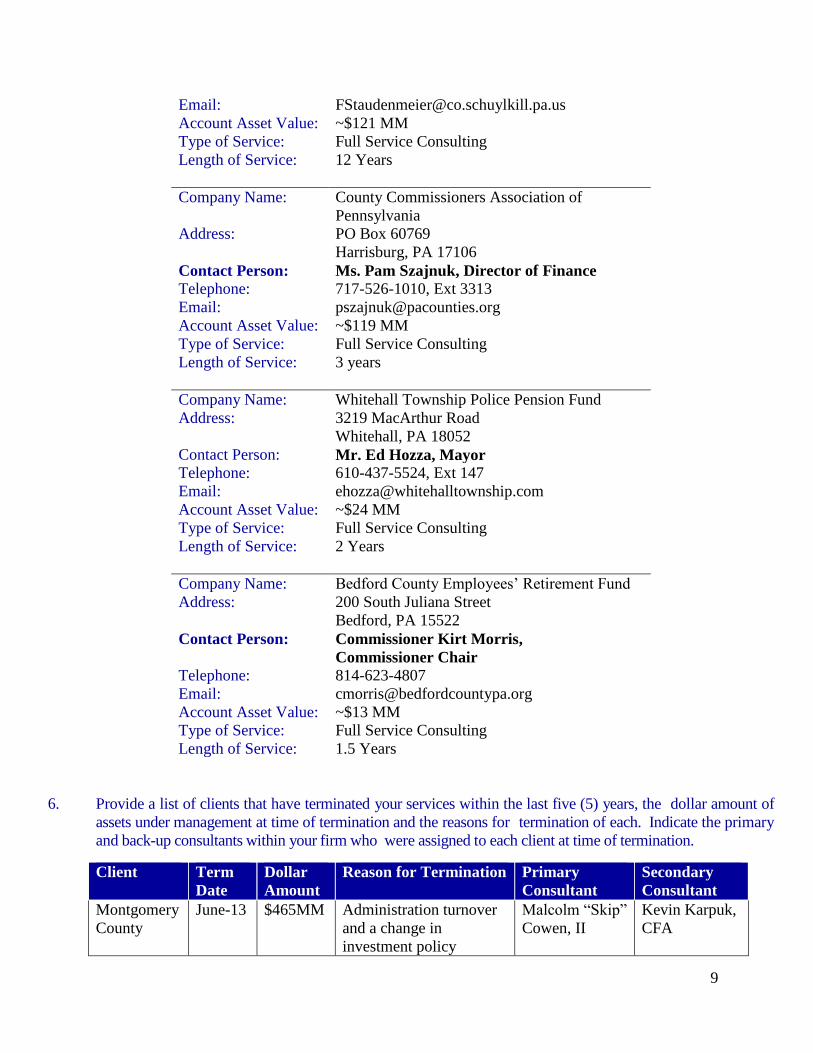

Company Name: Schuylkill County Employees Retirement Plan

Address:

Schuylkill County Courthouse

401 North Second Street

Pottsville, PA 17901

Contact Person: Commissioner Frank Staudenmeier,

Commissioner Chair

Telephone: 570-628-1200

9

Email: [email protected]

Account Asset Value: ~$121 MM

Type of Service: Full Service Consulting

Length of Service: 12 Years

Company Name:

County Commissioners Association of

Pennsylvania

Address: PO Box 60769

Harrisburg, PA 17106

Contact Person: Ms. Pam Szajnuk, Director of Finance Telephone: 717-526-1010, Ext 3313

Email: [email protected]

Account Asset Value: ~$119 MM

Type of Service: Full Service Consulting

Length of Service: 3 years

Company Name: Whitehall Township Police Pension Fund

Address: 3219 MacArthur Road

Whitehall, PA 18052

Contact Person: Mr. Ed Hozza, Mayor

Telephone: 610-437-5524, Ext 147

Email: [email protected]

Account Asset Value: ~$24 MM

Type of Service: Full Service Consulting

Length of Service: 2 Years

Company Name: Bedford County Employees’ Retirement Fund

Address: 200 South Juliana Street

Bedford, PA 15522

Contact Person: Commissioner Kirt Morris,

Commissioner Chair

Telephone: 814-623-4807

Email: [email protected]

Account Asset Value: ~$13 MM

Type of Service: Full Service Consulting

Length of Service: 1.5 Years

6. Provide a list of clients that have terminated your services within the last five (5) years, the dollar amount of

assets under management at time of termination and the reasons for termination of each. Indicate the primary

and back-up consultants within your firm who were assigned to each client at time of termination.

Client Term

Date

Dollar

Amount

Reason for Termination Primary

Consultant

Secondary

Consultant

Montgomery

County

June-13 $465MM Administration turnover

and a change in

investment policy

Malcolm “Skip”

Cowen, II

Kevin Karpuk,

CFA

10

7. Describe your plans for managing the future growth of your firm in terms of staff, maximum assets, number of

clients, etc.

We have achieved sustainable growth since our inception. Consultant relationships are limited to 25 primary

relationships per consultant and we have increased our minimum relationship size twice in the past ten years to

focus on larger, institutional clients. After hiring two new consultants in 2013, we feel we have ample capacity

for the next three years. As growth continues, we expect to add to our team accordingly.

8. Briefly describe how a new client would transition to your firm. Do you backload transaction and/or

investment performance data? What problems have you encountered in transitioning a new client to your firm

from their previous consultant? Please provide at least one (1) reference (name, fund name, address, phone, e-

mail) of a recent client of yours whom we may contact regarding the transition process.

For every client onboarding, a transition team is appointed to take responsibility from start to finish. Transitions

vary in complexity. Custodian changes, portfolio adjustments and changes, and performance data transfers are

just some of the many issues that can arise. Ideally, if a client is satisfied with their current custodian,

Cornerstone would be able to seamlessly take over consulting responsibilities. Performance and asset flow data

would be moved from the current consultant/custodian onto our systems. This is generally the most time

consuming process. Depending on format, granularity, and the completeness of the data, Cornerstone would

work to integrate the data to the best of our ability so that there is no gap in reporting. Transitions, while tedious,

are excellent opportunities to scrub data and ensure its accuracy. Beginning a relationship with a stable baseline

is critical.

Company Name:

County Commissioners Association of

Pennsylvania

Address: PO Box 60769

Harrisburg, PA 17106

Contact Person: Pam Szajnuk, Director of Finance Telephone: 717-526-1010, Ext 3313

Email: [email protected]

Account Asset Value: ~$120 MM

Type of Service: Full Service Consulting

Personnel

1. Identify the different classifications of employees within your firm and the totals for each classification. What

policies are in effect to control the workload as it relates to the number of clients serviced by each

consultant/relationship manager? Is there a limit on the number of accounts that a consultant/relationship

manager may handle? What is the average number of accounts per consultant?

Please see Section III, Exhibit A for Cornerstone’s organizational chart that breaks down the different

classification for each of our employees.

Currently, Cornerstone’s ratio of institutional relationships to consultant is 19:1. To handle the workload on an

everyday basis, teamwork is our most effective strategy. In the following question’s response, we provide

11

detailed information on all members of the Cornerstone team that will be assigned to this relationship. As an

added layer, Cornerstone does limit the number of institutional client relationships per consultant to 25.

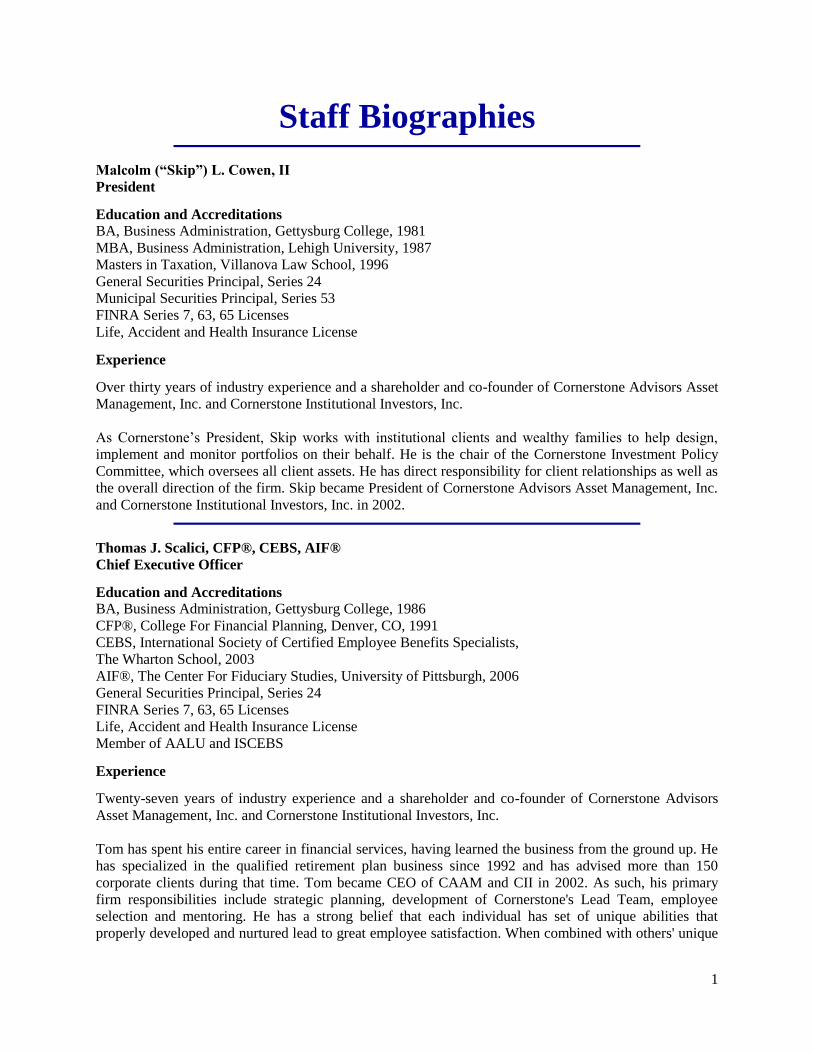

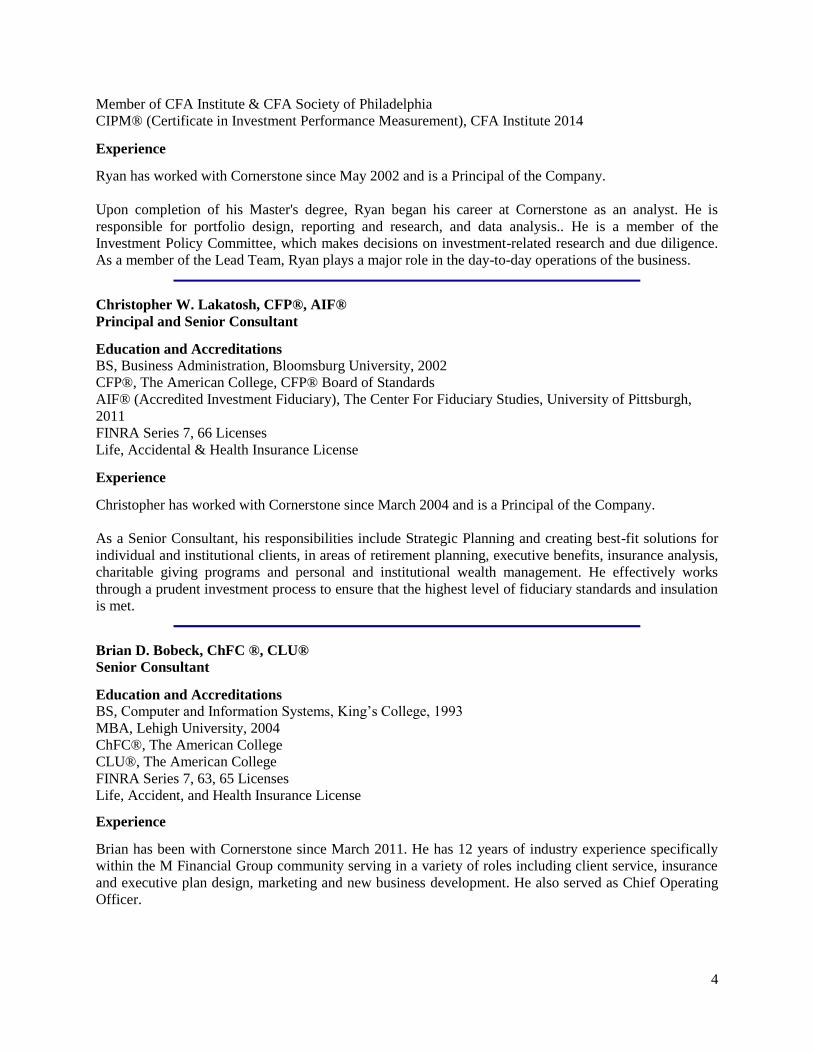

2. Identify and provide biographies of your firm’s senior leadership and the primary and backup consultants who

would be assigned to this engagement as Exhibit E. Who are the clients these consultants currently serve?

Which of these consultants would attend the Northern York County Regional Police Pension Committee

meetings? To which office are they assigned? What measures will your firm employ to ensure that either the

primary or the backup consultant be readily available to answer questions from the Plan’s Staff?

Cornerstone has always utilized a team approach to each of our client relationships. Christopher Lakatosh and

Kevin Karpuk will be the lead and secondary contacts for this relationship. Chris has been providing investment

advisory and fiduciary services to qualified retirement plan sponsors for over ten years. During that time, he has

compiled a well-educated, experienced team of two educational consultants, two operations professionals, three

client service directors and three investment analysts, all of whom are CFA charterholders. Our entire staff is

available to service the needs of our clients directly on an as needed basis. Our service model is built on the

premise that clients should be able to define their experience with Cornerstone, whether that is the older model of

having a relationship manager who is the sole point of contact or a more decentralized system of contacting the

particular employee they need for that particular service.

Please see Section III, Exhibit E for Cornerstone’s staff biographies.

3. Describe the firm’s compensation and incentive program for hiring and retaining key consultant personnel.

How does the firm tie client performance and satisfaction to a consultant’s compensation?

Cornerstone consultants are paid a base salary with benefits plus an annual share of the revenue they generate

and retain for the firm. Client retention is paramount in our culture and we continue to reward consultants as

long as their relationships are healthy. Successful consultants who merit additional compensation are considered

for a principal position which includes profit sharing. This is the next step before ultimately being considered for

a shareholder position in the firm.

4. Has your firm adopted the CFA Code of Ethics and Standards of Professional Conduct? If so, how is

compliance monitored?

Yes. Cornerstone has adopted the CFA Code of Ethics and Standards of Professional Conduct. All policies and

procedures are monitored by Cornerstone’s Chief Compliance Officer.

5. Explain turnover in key professional personnel (senior management and consultants) over the last five (5)

years. Please list staff positions hired, resigned and terminated, including a description of each position and

the reason for turnover.

In the last two years, Cornerstone has seen one consultant leave the firm to join our former business partner. He

chose to pursue insurance sales rather than investment consulting. Since his departure, we have added two

seasoned professionals to backfill and expand our consulting reach.

12

Investment Management

1. Describe your public pension fund experience and approach in developing and monitoring, and updating

investment policies and objectives for a diversified pension fund. Comment on your process for analyzing a

client's legal and regulatory restrictions, liquidity needs, time horizon, social responsibility, funding status,

portfolio structure, and for recommending modifications, including frequency of review.

Cornerstone has provided consulting services to defined benefit plans for over 20 years. Our public pension

experience started in 2000 when the Schuylkill County Retirement Plan retained our services. Our experience

and focus on risk management has led us to be hired by several of the country’s leading independent actuaries to

manage their own defined benefit plans. Managing defined benefit assets is something that is inherent in our

business model because it is very much a two-sided equation. The liabilities of plans grow much more steadily

than the assets, in most cases, and it is our job to understand that and provide insights into COLA’s, duration

management, minimum municipal obligations and other non-traditional consulting inputs. If we focus solely on

your assets, we are doing you a disservice.

We are experienced with the various state rules governing the plan under your care. We also have extensive

experience with Act 44 of 2009 as it pertains to the funding and smoothing methodology applicable to your plan.

To us, Act 44 was a necessary evil. It was passed as funding relief for municipalities, allowing them to realize

losses over longer period of times than was acceptable prior to its passage. Pension funds are long-term vehicles,

which should be able to take some short-term volatility in exchange for increased long-term upside; however,

many plans needed this relief not because of the catastrophic financial markets of 2008, but instead because they

underfunded their plans in the past and had improper asset allocations that didn’t allow them to understand and

appreciate the risk that they had undertaken. The reason that Act 44 was a “necessary evil” is that the legislature

did not undertake hard decisions regarding ongoing funding that would change the behavior of pension plan

sponsors in the public sphere. During good financial markets, plans are thought of as self-funding vehicles

which is patently false. The legislature had the opportunity while modifying Act 205 with Act 44 to require

municipalities to at least contribute the annual cost of plan going forward. This was an opportunity wasted.

The one part of Act 44 that we unequivocally agree with is the “pay-to-play” disclosures. Public funds have long

been used to benefit large political donors. Cornerstone does not make political contributions, nor do we receive

any compensation based on political activities, so the leveling of the playing field was appreciated by

independent firms such as ours. The history of officials using retirement funds as a way to reward political allies

has been long and detrimental to the participants in the plan. With Act 44, we hope that this has changed.

2. Describe your firm's experience in customizing asset allocation studies for individual clients, including

integration of liabilities and funding. How often does your firm recommend reviewing asset allocation?

In order to develop an appropriate asset allocation, it is critical to start with the investment policy statement. We

spend the greatest portion of time working with our clients on their investment policy development,

implementation and monitoring. We look at the current policy statement, current funding ratios and undertake

service provider due diligence at the start of every relationship and create a needs analysis that identifies the most

urgent points that need to be addressed. We then review (quarterly, with a detailed annual report) all of these

aspects of the plan.

The investment policy statement for any client is probably the most important document that a fiduciary has. A

13

well written policy clearly outlines the responsibilities of all parties involved and is signed by each party as

acknowledgement of what is expected of them. We begin this process with reviewing the current investment

policy to ensure that it contains everything necessary from a legal perspective, but then we expand our scope to

ensure the inclusion of the Prudent Investment Practices. If the policy is clearly written and is strictly followed,

it is highly unlikely that fiduciaries will act in a way that will expose them to legal jeopardy.

The first step of developing a statement of investment policy and objectives is to listen to our clients and their

service providers. Since each client is different in their attitude towards investment risk, we cannot develop

proper policy without first talking with them. If a client is willing and able to fund liabilities through cash flow,

our investment solution will be much less volatile than a client who cannot afford to fully fund future obligations

and therefore relies on investment experience to maintain or improve its funding status.

In the next step of the process, we turn the typical return-focused allocation modeling process on its head.

Instead, we work with the client and its actuary to figure out what a “maximum acceptable loss” is and then build

a portfolio to have that risk profile. No one knows what the capital markets will return in a given year, or even

over a given decade as the last one has shown, but what we can do with a high degree of confidence is model

what our clients’ expected downside is. This is important because if we understand the liability stream several

years into the future, we can better fit an asset allocation. With any investment, avoiding large losses while

participating in a large percentage of the upside is important, but in a defined benefit plan, it is crucial.

Once we decide on an acceptable level of downside risk, we then use our software to develop an asset allocation

and portfolio structure. This software uses Monte Carlo simulation of our current capital market assumptions to

provide us with modeled returns. There are two fundamental differences between the way we use this software

and many in the industry do. First, we do not use historical capital market returns to model the future. What has

happened in the markets since 1926 is far less relevant to a client than is a thoughtful look at current market

conditions and their likely effect on future market performance. The second differentiating factor is that we do

not use optimization. By allowing a software program to run a simple “min-max” calculation on risk and return

without regards to common sense causes either unrealistic portfolios or so much human interference that the

output becomes useless.

After determining the appropriate asset allocation and portfolio structure, we turn our attention to the individual

money managers. Here we apply a quantitative and qualitative screening process that is guided by the

investment policy statement. In order for any money manager to be considered, they must meet a set of

minimum criteria. After this initial screen, our team of analysts begins the exhaustive due diligence process to

condense the manger universe.

3. Describe your firm’s capital markets model. Is the model proprietary, or does your firm rely on an outside

vendor’s model? If your firm relies on an outside vendor, indicate the name of the vendor, name of the model,

etc.

Cornerstone relies on Callan’s capital market assumptions which are created using a fundamental building block

approach paired with a common sense overlay. We also consider other major forecasts (JPMorgan, BNY

Mellon, GMO, etc) to look for outliers and to understand differences between the models and their outputs.

4. How does your firm develop inputs to the model? Does your firm develop standard inputs to the model for all

clients? Can these inputs be customized based upon individual client views, needs or requirements?

14

The software we use for modeling is fully customizable. We have a base case model with base inputs that can be

refined to meet the unique needs of our clients.

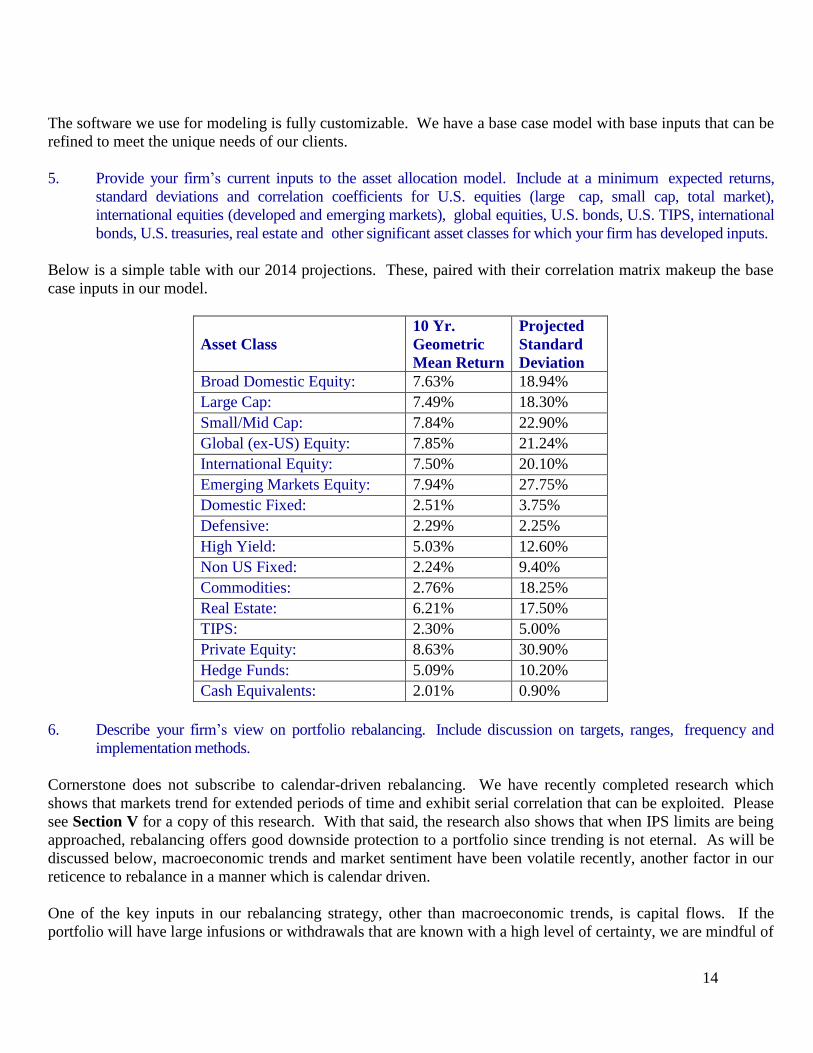

5. Provide your firm’s current inputs to the asset allocation model. Include at a minimum expected returns,

standard deviations and correlation coefficients for U.S. equities (large cap, small cap, total market),

international equities (developed and emerging markets), global equities, U.S. bonds, U.S. TIPS, international

bonds, U.S. treasuries, real estate and other significant asset classes for which your firm has developed inputs.

Below is a simple table with our 2014 projections. These, paired with their correlation matrix makeup the base

case inputs in our model.

Asset Class

10 Yr.

Geometric

Mean Return

Projected

Standard

Deviation

Broad Domestic Equity: 7.63% 18.94%

Large Cap: 7.49% 18.30%

Small/Mid Cap: 7.84% 22.90%

Global (ex-US) Equity: 7.85% 21.24%

International Equity: 7.50% 20.10%

Emerging Markets Equity: 7.94% 27.75%

Domestic Fixed: 2.51% 3.75%

Defensive: 2.29% 2.25%

High Yield: 5.03% 12.60%

Non US Fixed: 2.24% 9.40%

Commodities: 2.76% 18.25%

Real Estate: 6.21% 17.50%

TIPS: 2.30% 5.00%

Private Equity: 8.63% 30.90%

Hedge Funds: 5.09% 10.20%

Cash Equivalents: 2.01% 0.90%

6. Describe your firm’s view on portfolio rebalancing. Include discussion on targets, ranges, frequency and

implementation methods.

Cornerstone does not subscribe to calendar-driven rebalancing. We have recently completed research which

shows that markets trend for extended periods of time and exhibit serial correlation that can be exploited. Please

see Section V for a copy of this research. With that said, the research also shows that when IPS limits are being

approached, rebalancing offers good downside protection to a portfolio since trending is not eternal. As will be

discussed below, macroeconomic trends and market sentiment have been volatile recently, another factor in our

reticence to rebalance in a manner which is calendar driven.

One of the key inputs in our rebalancing strategy, other than macroeconomic trends, is capital flows. If the

portfolio will have large infusions or withdrawals that are known with a high level of certainty, we are mindful of

15

this during our decision making process. In most cases, if our macroeconomic outlook is negative, we try to raise

as much cash as will be necessary for the foreseeable future. If we know that a large deposit is expected, then we

will discuss with the committee how we would like to allocate it.

7. How do you define risk? Briefly describe the risks to which a public pension fund is exposed.

Our definition of risk is volatility that causes an organization stress. Risk measurement and management is not a

new or nebulous idea. There are many ways to measure volatility including standard deviation, downside risk,

etc.; however, every organization has a different level of risk tolerance. Risk should be a known commodity and

every fiduciary should be able to explain their risk tolerance in measurable terms.

Many pundits believe that the greatest risk to public pension plans is tied to the funding ratio whereas we believe

that the real risk is the volatility of annual contributions. Until the law changes, municipalities will be in the

pension plan business. With that in mind, we consider these plans to be “forever” money. The funding ratio will

move with the capital markets over time, but if managed correctly, it will revert to a mean of being well-funded.

It is the annual required contribution volatility that is truly the greatest risk since if plans are exposed to too much

risk in the capital markets, the contribution will markedly increase at the exact worst time, when the economy is

slowing and the tax base is weakest. One of our core philosophies in managing any pool of money and

especially in public pensions is that minimizing the volatility of these contributions is the greatest success we can

achieve. Anyone who believes that they will invest their way back to full funding rather than contributing their

way back is setting themselves up for a long road with overexposure to volatility.

8. How does your firm monitor risk? List the measurements that are used when evaluating risk.

Cornerstone monitors risk through various measures. The first is our annual capital market assumptions in which

we model a client’s current allocation and look at what the expected downside in a bad market could be. If that

95th

percentile event would irreparably harm a client, then we need to slide down the risk scale. The ongoing risk

monitoring, at both the manager and total fund level is found in our quarterly reviews in which we track statistics

such as standard deviation, beta, downside risk and down market capture to name a few. What we are able to do

with these numbers is not only compare them to the agreed upon benchmark but also a national peer group of

similar sized public plans. If a retirement board is risk seeking (or risk averse), we can build a portfolio that will

reflect these tendencies but ensure that the level of risk is not imprudent compared to the rest of the universe.

9. Describe your firm’s view on risk budgeting. Have you created a risk budget model that is utilized by your

clients?

Cornerstone does not subscribe to the idea of risk budgeting in the classical sense for several reasons. The first is

that to target a particular standard deviation target is to miss the point that over complete business cycles, the

standard deviation of the markets varies greatly, so to target a standard deviation of 8 – 12%, for example, is not

always relevant. Another downside to risk budgeting that we see in the market is that alternative investments

have a lower weighting in the risk budgeting than we are comfortable with. An example of this is that a hedge

fund of funds may have the same risk profile as a bond fund when measured historically, but an astute investor

should understand that the risks inherent in illiquid investments is significantly higher than fixed income.

We do informally budget tracking error in our portfolios. In less efficient areas of the market such as small cap

and emerging markets, we are willing to add more active management than in large cap domestic stocks. If we

16

are going to add tracking error to a portfolio, we wish to do so in errors where there is the chance of positive

alpha, and we minimize tracking error and other risk factors where history shows a lower chance of success.

10. Describe any other risk management capabilities that are offered to clients.

There are many aspects of risk management that come with having a consultant with over 30 years of industry

experience that spans non-public clients as well as public funds. One aspect that we would enjoy sharing with

you would be regarding our proposal to a local municipality that liquidated an asset to fund their massively

underfunded pension plan. While there were headwinds to our concept politically, we believe that the concept

itself highlights the type of forward thinking, risk-centric management that Cornerstone is known for.

11. Discuss the steps your firm would take to analyze the current Plan portfolio.

Cornerstone comes into every new relationship with an open mind. We do not have a prepackaged investment

solution that we require clients to adhere to. Our initial steps to analyze the current Plan portfolio would be to

schedule due diligence meetings with each of the managers to help discern who has been fulfilling their charter

and who may need to be changed. This is an open process in which we meet with each manager and follow our

typical due diligence process. We have found many of our best managers through inheriting them from existing

positions. We would then provide the Board with a written report of what we have found in our research.

In terms of asset allocation or portfolio structure, while our team of analysts is performing manager due

diligence, we would meet with your Board and actuary to discern what the best course of action would be. The

actuary’s input on any expected demographic changes or past smoothing of underperformance is helpful in

planning for the future.

12. Discuss how you optimize the number and types of managers and how you assess the effect of including new

managers. Discuss any statistical analysis that is performed.

We are unaware of any statistical analysis that will yield the optimal number of managers for a given portfolio.

For a portfolio of this size, we would expect around 5 actively managed separate accounts, several index mutual

funds/ETF’s and several other mutual funds to get access to the marginal asset classes such as high yield bonds,

emerging markets, etc. Our strategy is to hire the number of specialist managers needed to fill out the manager

matrix as designed in the policy statement.

13. Describe your firm’s philosophy with respect to manager evaluations (formal review, ad hoc, etc.). Briefly

describe any ongoing due diligence process. What critical issues are examined in the due diligence process?

At what point would your firm recommend terminating an investment manager?

A good manager evaluation program is one that is clearly defined, documented and followed. Within our

Investment Policy Statement, we outline the metrics (as described above) to which we hold our managers. Many

policies we see in the market are tied purely to performance comparisons, a major flaw within the consulting

community. Our policy lays out performance but as an input for risk-adjusted returns. We will not consider a

manager a failure for underperforming a benchmark or peer group if there is a commensurate lower risk profile.

By knowing the managers well and constantly monitoring them, we can understand and even to a certain process

being used to manage money. Every money manager is going to have periods of strong performance and periods

of weak. It is much more important to us to understand that the people and process for the manager remain

17

consistent with what created historical success. If the process changes significantly or key team members

change, we consider that a reason to immediately terminate a relationship since there is an entire universe of

qualified managers from which to choose. A counterpoint to many things we see in the industry is that we favor

hiring firms that have strong organizations and track records but are in the bottom half of their peer groups in

recent time periods. We do not want to hire the hot dot which is a weakness of many wrap programs.

14. Describe your firm’s view of the role of passive management (by asset class) in a client’s portfolio. Indicate

the active/passive allocation in your typical public pension fund client’s portfolio.

We believe passive strategies are powerful tools for investors in sectors of the market in which active

management is limited in its ability to create alpha. Core domestic equity is the most obvious example of

somewhere we would want to employ an index fund. Within the largest 500 companies in the United States,

there exists such a high level of analysis that managers historically have had a difficult time beating their index

without introducing style risk. As co-fiduciaries, we are more comfortable minimizing fees and tracking error in

this portion of the portfolio, allowing us to take on risk in areas that attract alpha creation opportunities, such as

emerging markets, small cap and specialist fixed income mandates.

Utilizing index funds across several asset classes (large cap, core fixed income and developed international) also

allows for the efficient redeployment of assets during portfolio restructuring or tactical shifts in asset allocation.

We do, however, believe that certain asset classes – such as emerging markets, high yield bonds and small cap

stocks – are inefficient enough for active management to yield sufficient alpha over a market cycle.

15. Describe your firm’s view on securities lending. Do you typically recommend lending with the client’s

custodian or with a third-party lender? Describe your viewpoint on each method of implementation.

With large pools of assets, securities lending helps boost returns at the margin under good and normal market

conditions. While we are not against it, Cornerstone does not actively encourage securities lending. As long as

the overseeing body understands the risks associated with it, we are comfortable monitoring it. The reason we

aren’t strong proponents of it is that in a stressed market, securities lending can easily backfire, exactly when you

don’t need another problem. From a risk/return standpoint we usually don’t feel the marginal return is worth the

associated risk.

16. Briefly describe the capabilities associated with the evaluation and monitoring of securities lending programs.

Briefly describe the capabilities associated with the evaluation and monitoring of short-term investment funds

(STIF) or other cash management programs.

Cornerstone will work with your custodian to establish a monitoring system for their securities lending activity.

Cash management and STIF’s are subject to the same rigorous due diligence and monitoring processes we have

established for any other investment manager in your portfolio.

17. Do you believe a plan should have a permanent allocation to cash? Why or why not?

Cornerstone believes a cash allocation is warranted in a portfolio. In most cases, a 1-5% target is typical,

depending on liquidity needs and the payment structure of the Fund. While cash balances pay very little at

present, they provide virtually zero volatility. Also, a rising rate environment should help cash returns in the

future.

18

18. Describe your firm’s view on performance-based fees. What percentage of your firm’s clients utilizes these

types of fees?

Cornerstone accepts performance-based fees as long as the terms of the fees are reasonable and do not

disadvantage the client in declining markets. In areas such as private equity and hedge funds, performance based

fees are typical. Less than 1% of our asset base is with managers who have performance-based fees.

19. Discuss your firm’s philosophy on transition management. Do you recommend clients maintain a pool of

approved transition managers? How have you assisted with a search for qualified transition managers?

Cornerstone personally handles transitions. We have had conversations with transition managers but have not

run across a situation with enough complexity to justify the cost of a dedicated transition manager.

Performance Measurement/Portfolio Analytics & Reporting

1. Describe your firm’s experience and capability for calculating performance. Describe differences, if any, in the

way the firm would calculate performance among different asset classes. How would the firm ensure accuracy

in the performance calculations? How soon after receipt of settlement-date accounting data from the custodian

would accurate performance reports be available to present to the plan’s administrative committee?

The database we use for performance reporting is actually two different systems that we have merged into one.

The first is our manager composite, benchmark and peer group database, which we purchase from Callan

Associates. To verify this information, we also have subscriptions to PSN, Morningstar and various other data

sources. For client-specific performance reporting, our database creates return streams using daily transactions

and valuation for a more precise return calculation than is required by GIPS® standards. Once these returns have

been verified by our performance reporting team, they are automatically loaded into our database as final

numbers and are used in our reporting. Very little data entry or human contact is involved in the production of

performance figures, other than strenuous cross-checking and data validation by our reporting and technology

teams.

To ensure accurate performance reports, trade-date accounting is preferred. However, we do understand this

information may not always be available depending on the custodial relationship and in those instances

settlement-date data must be used. Cornerstone feels confident that accurate performance reports can be

available within two weeks after the receipt of client statement data.

2. Describe how benchmarks are chosen or developed and how performance is compared to similar portfolios.

Can the firm provide custom benchmarks? Style benchmarks? Normal portfolios? Please indicate whether

your firm has ever developed benchmarks, and if so, please provide a description of the benchmarks

developed.

Cornerstone outlines two different benchmarks in our investment policy statements. The first is our “blended

benchmark”. This measure weights the benchmark at the current portfolio weighting. This is most appropriate

to judge whether the managers are providing a benefit to the Fund through active management. Our second

benchmark, the “broad market benchmark”, uses the policy target weightings for the different asset classes.

While some manager performance seeps through to this calculation, for the most part, this will show whether the

deviations from the IPS benchmark have helped or hurt the Plan. Since Cornerstone believes that modest

19

deviations from the policy statement can be beneficial in the long run, we believe that this measure is a good

indicator of whether a consultant is performing well over the long run.

The final measure that we use to measure our performance is to look at the Plan level performance versus others

investing money in a similar fashion with similar goals. We can put a return stream versus a peer group and

compare the total portfolio much like we can an individual manager.

Finally, for investment managers, Cornerstone has the ability to compare managers against any benchmark in

existence and we have found that a handful of well-known indexes (e.g. Standard and Poors, Russell, MSCI,

Barclays Capital) are well suited for evaluating managers.

3. Describe the content and format of your firm’s standard quarterly performance reports for the total fund, major

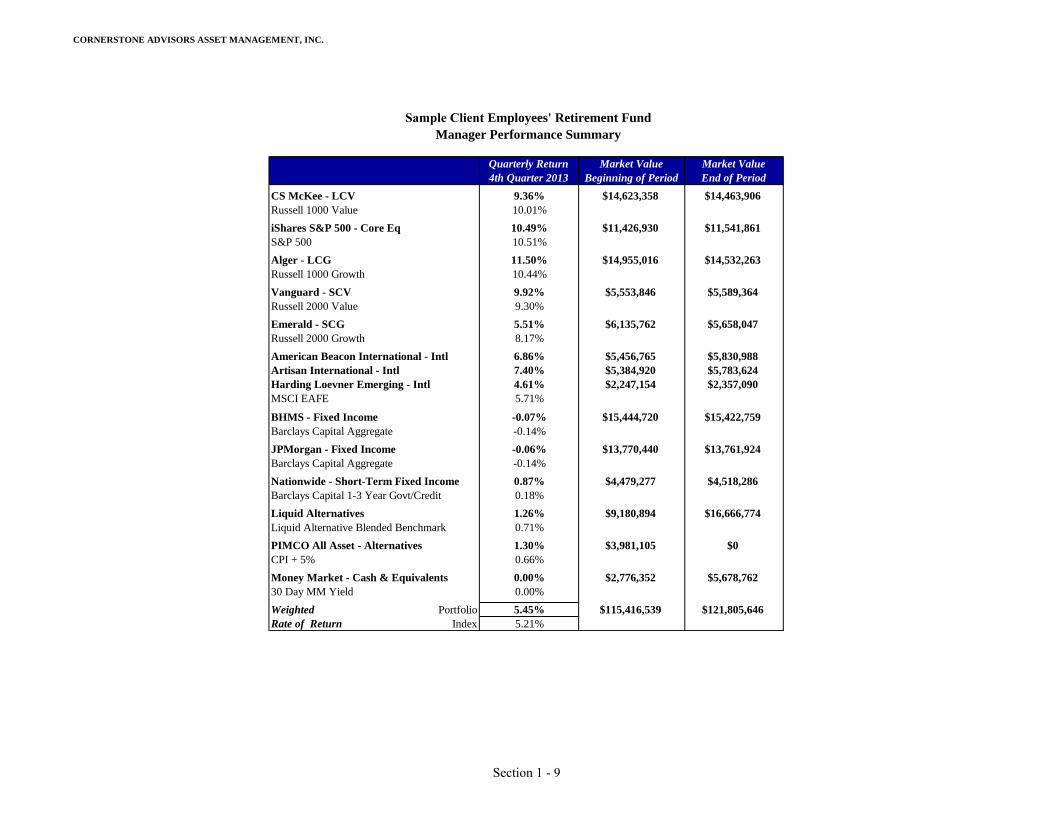

asset classes and individual investment managers. Provide a sample report for one (1) of your firm’s clients

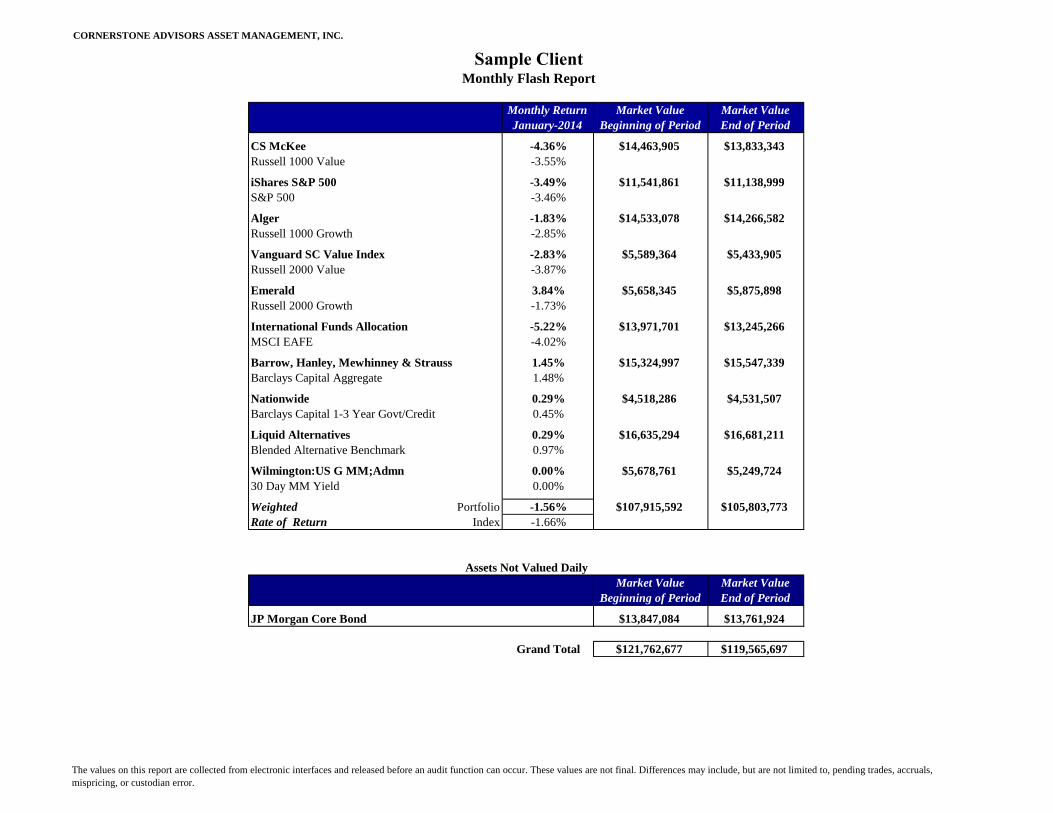

that is structured similarly to the Plan as Exhibit F. Provide samples of other kinds of non-standard reports

available to clients as Exhibit G.

Cornerstone’s typical reporting package includes an audited review book quarterly. Our audited quarterly review

book typically contains three sections. The first section is an overview of the current economic environment.

The second section contains an audited cash flow analysis of the portfolio along with an asset allocation

breakdown and money manager performance. The final section includes our quarterly due diligence on all

money managers within the portfolio.

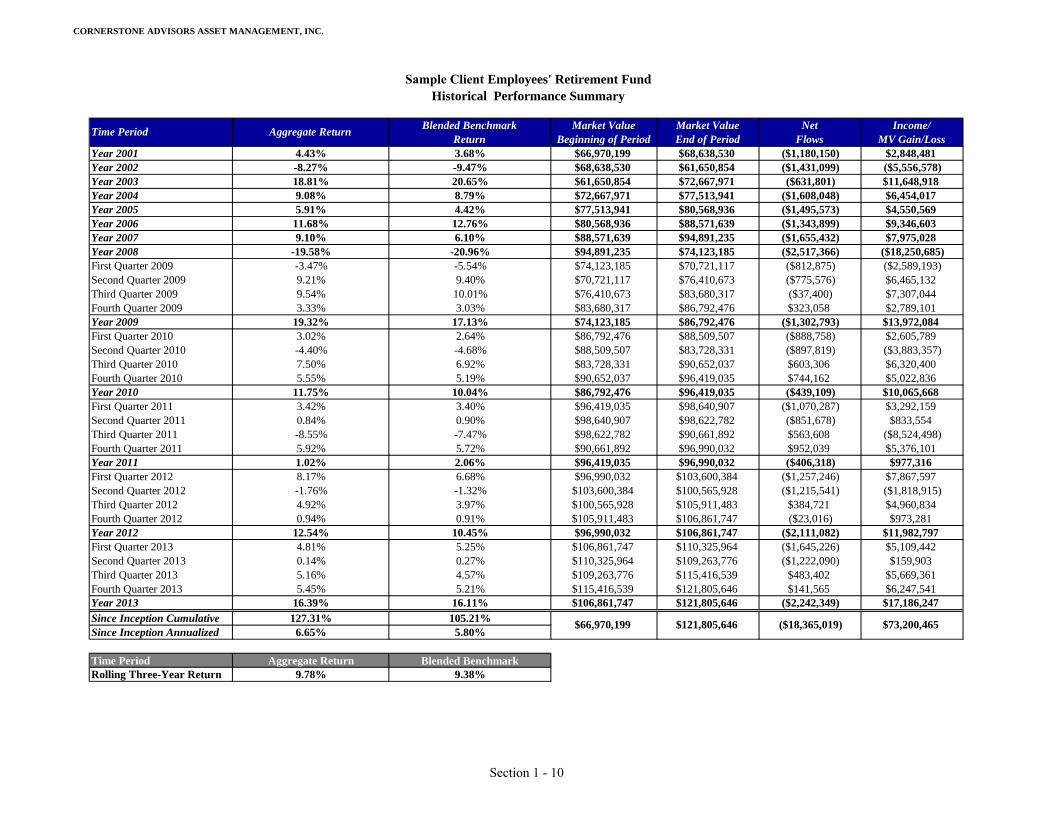

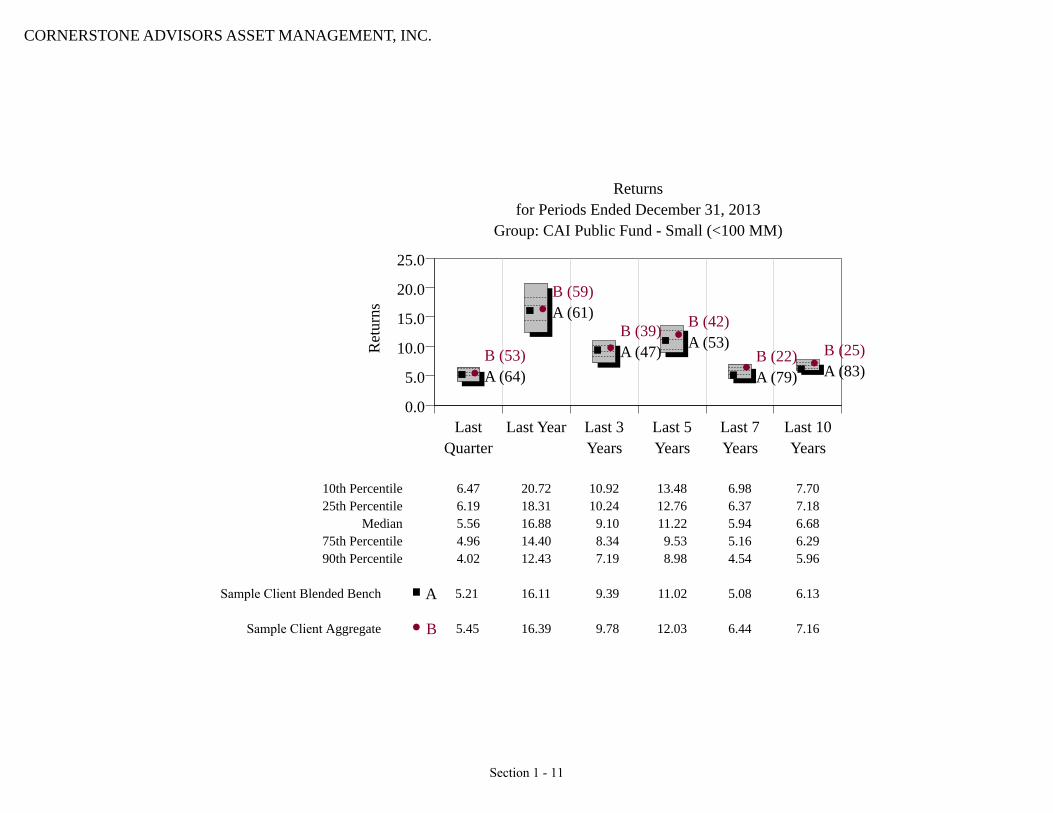

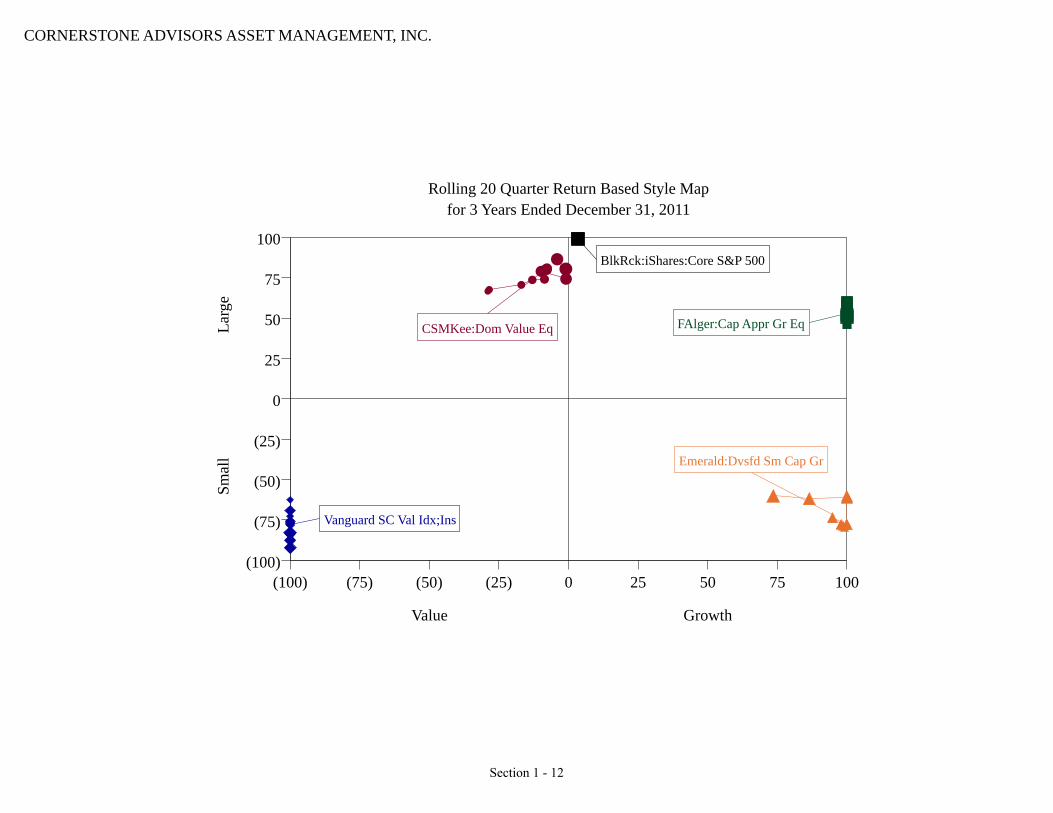

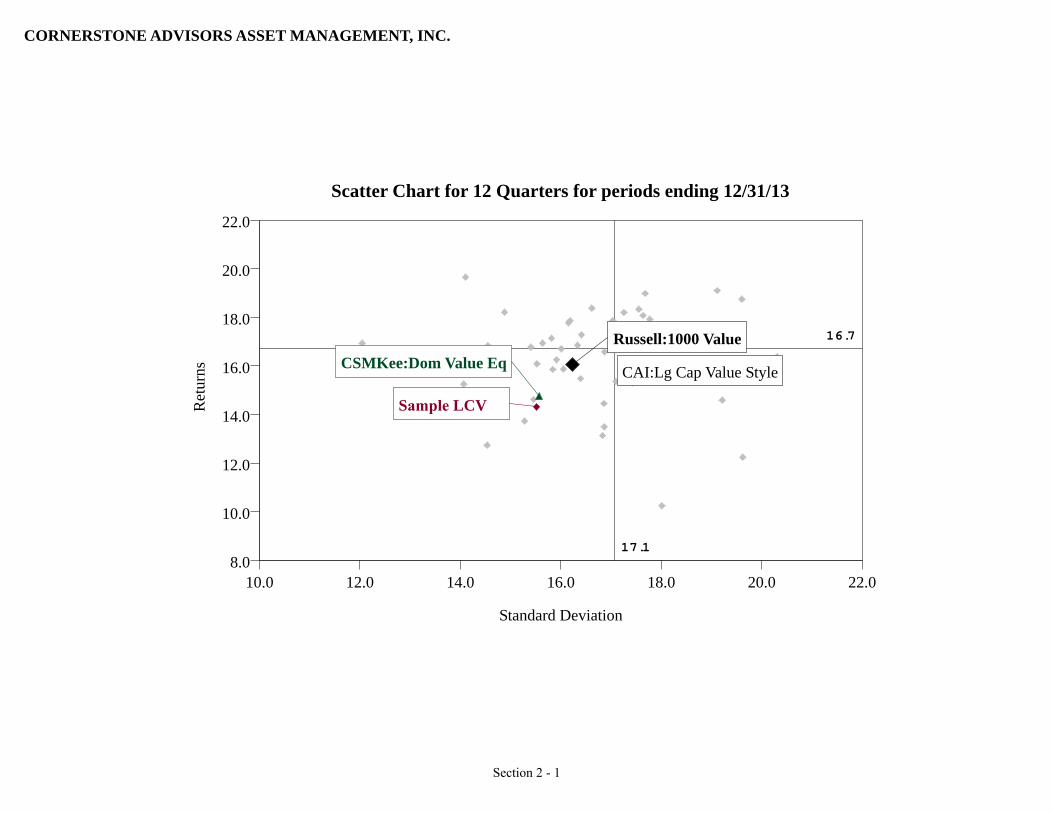

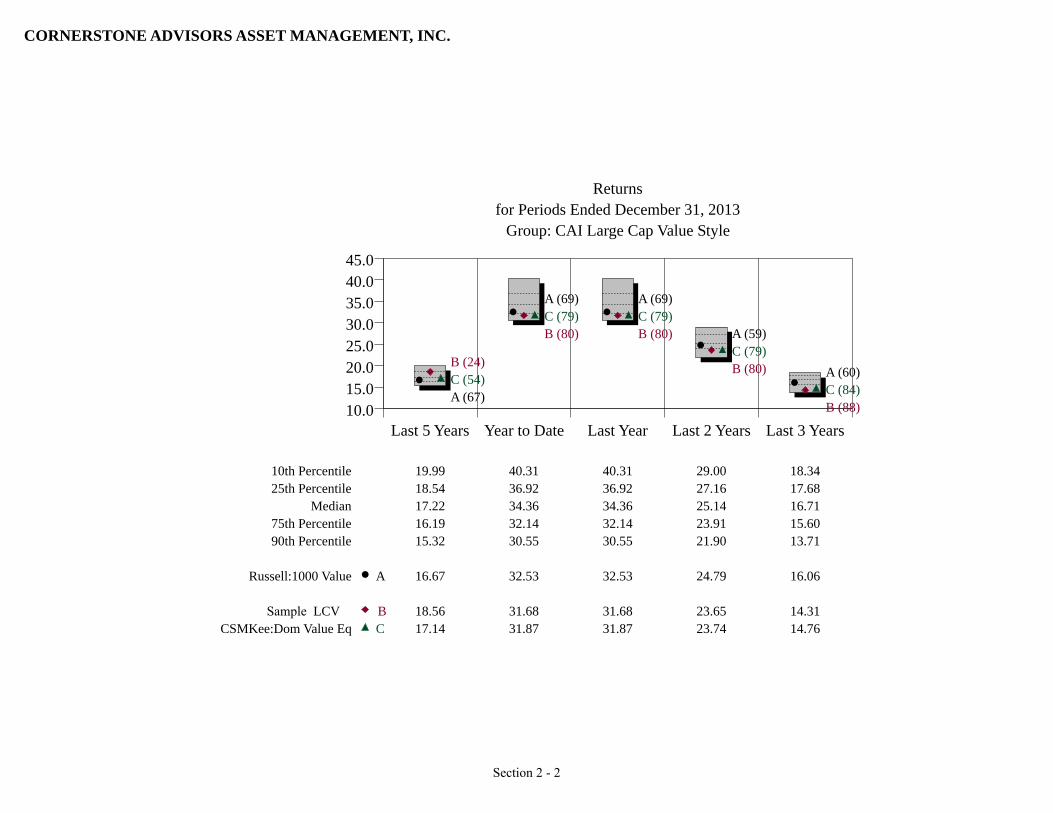

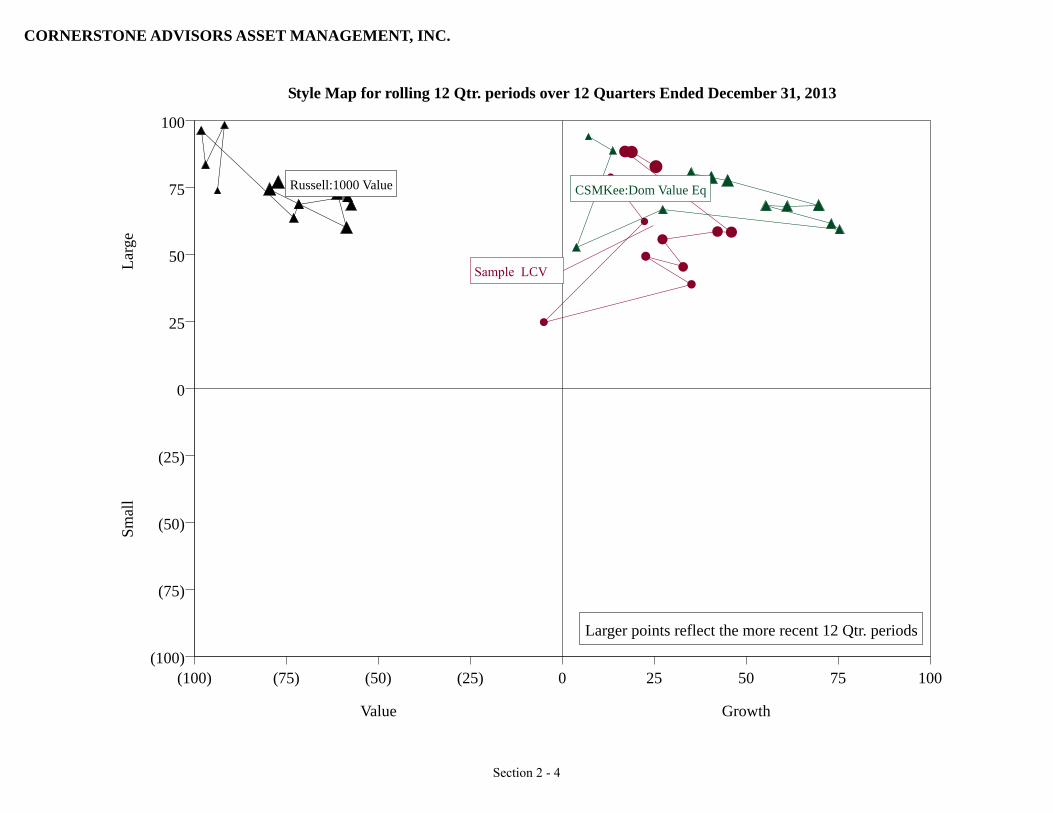

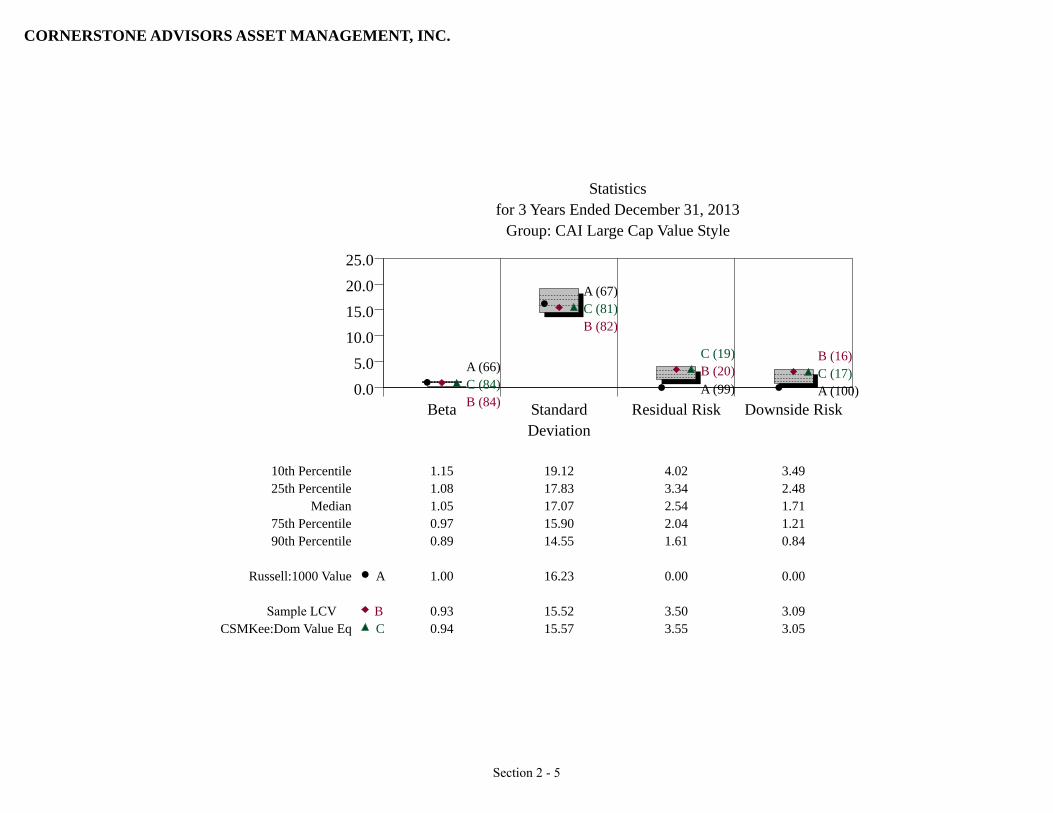

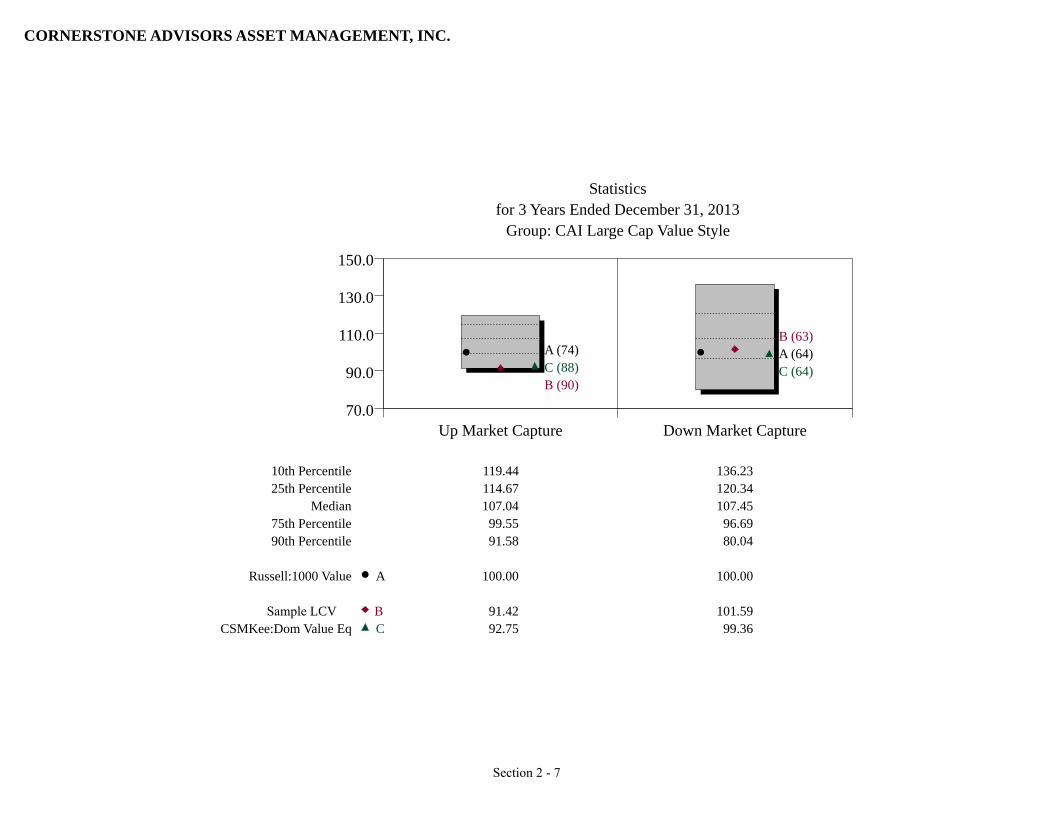

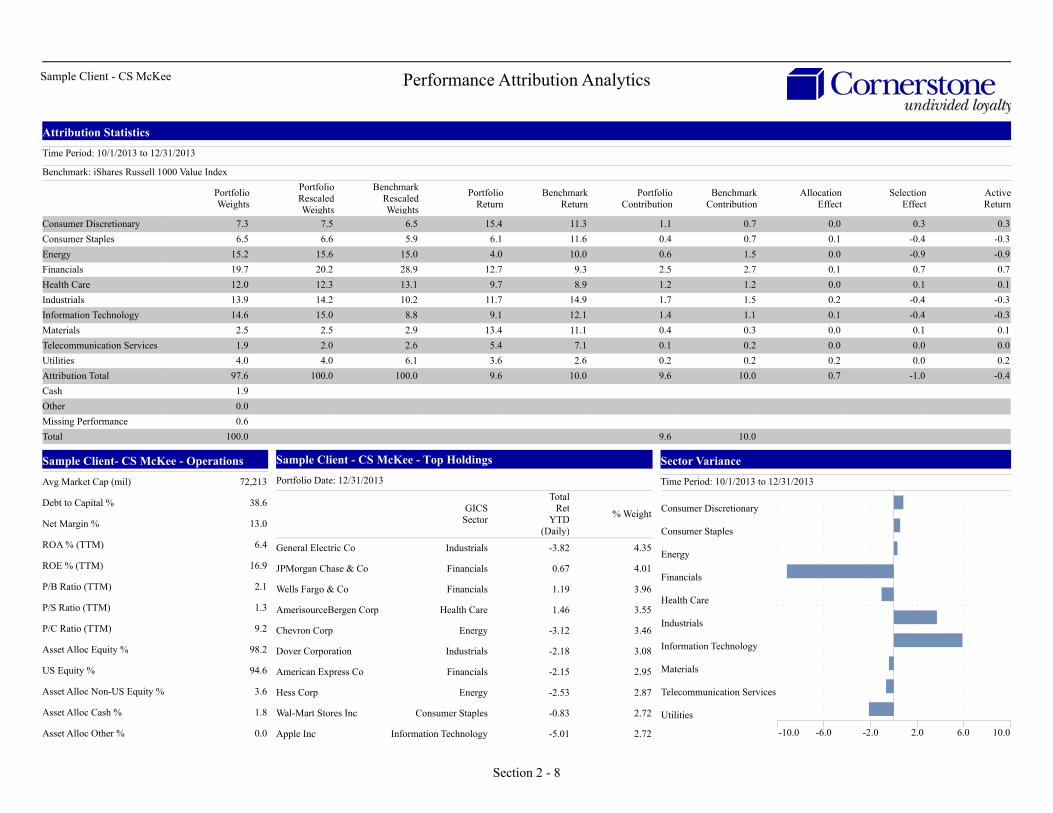

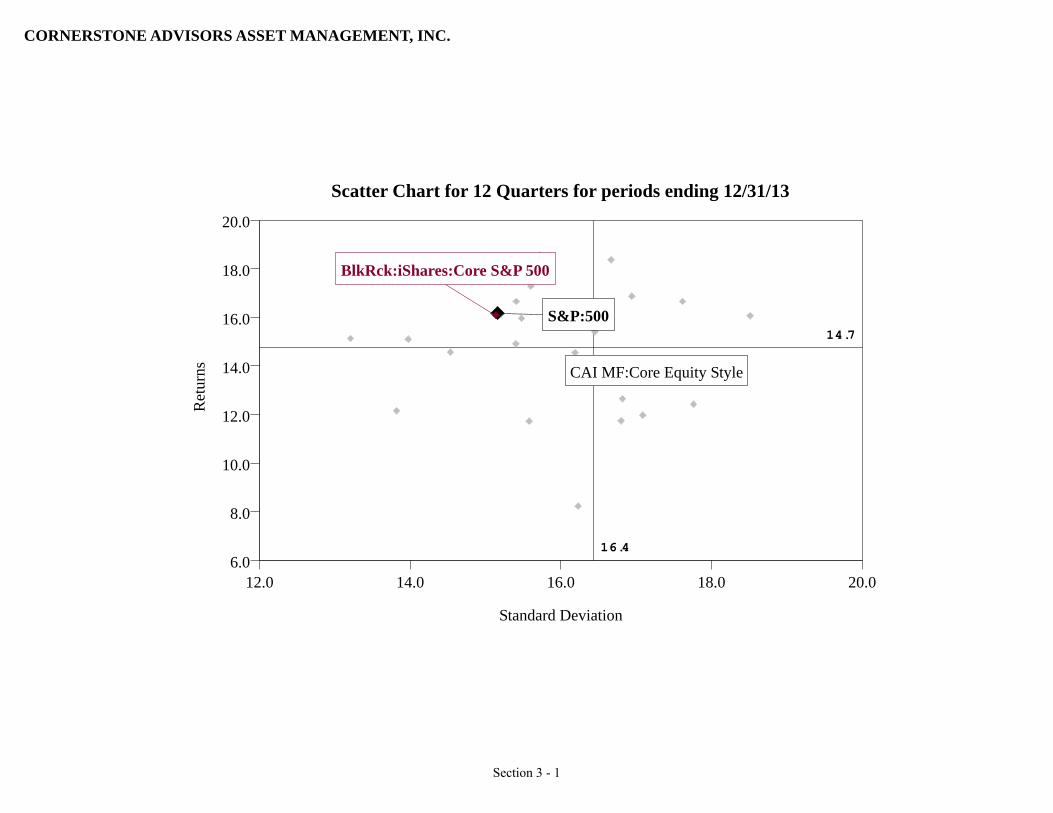

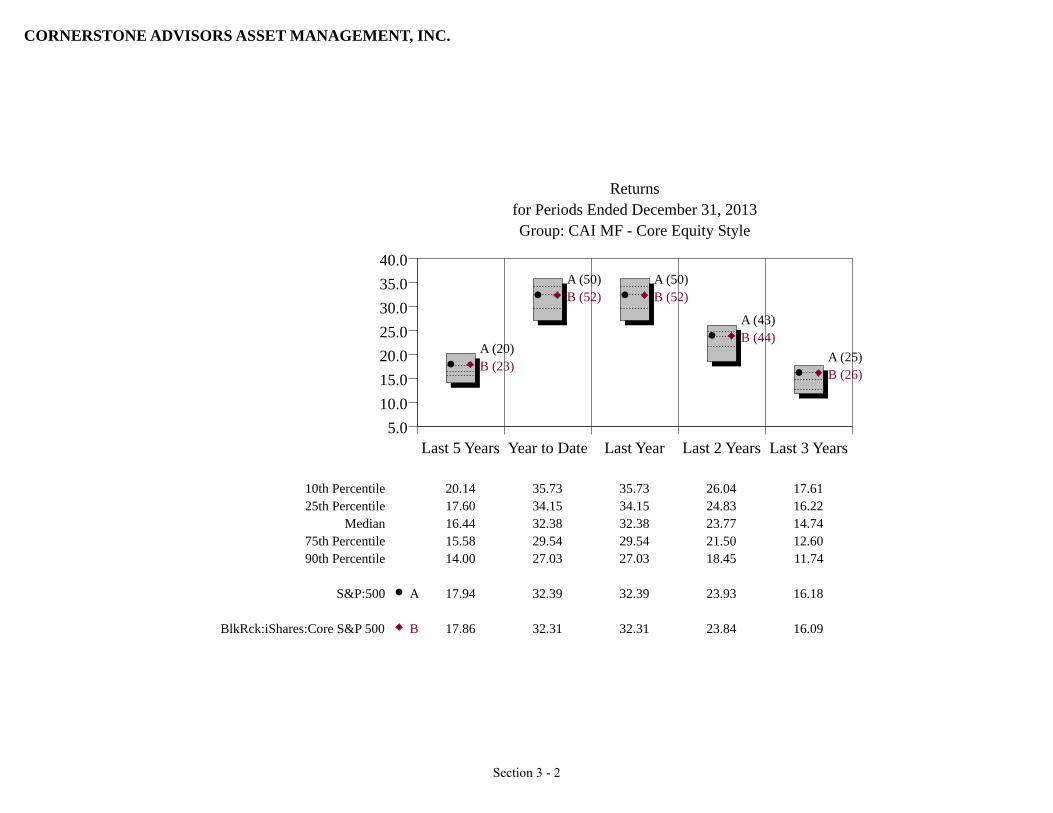

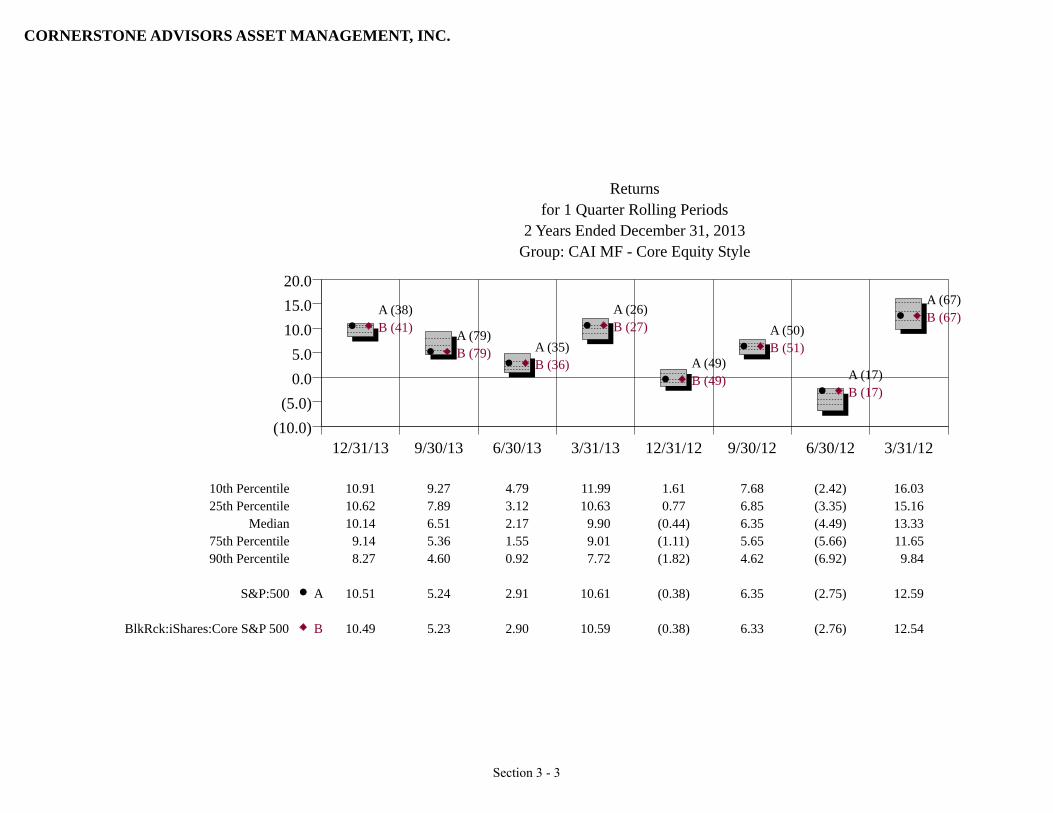

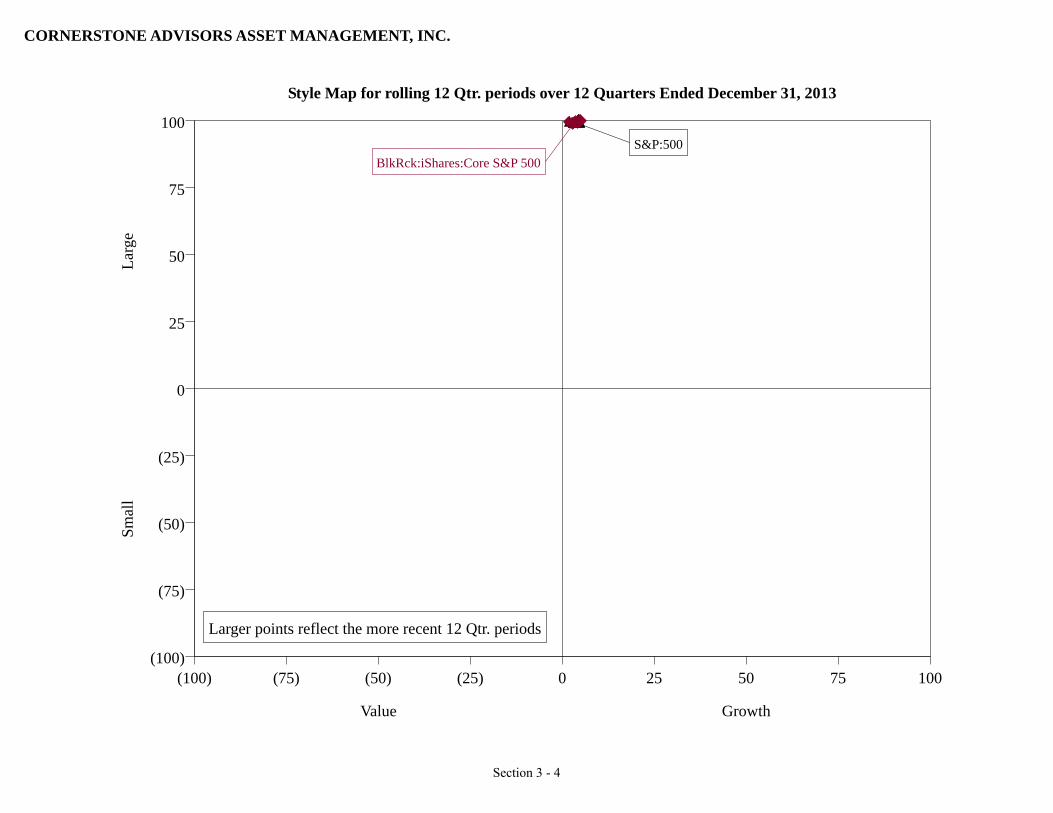

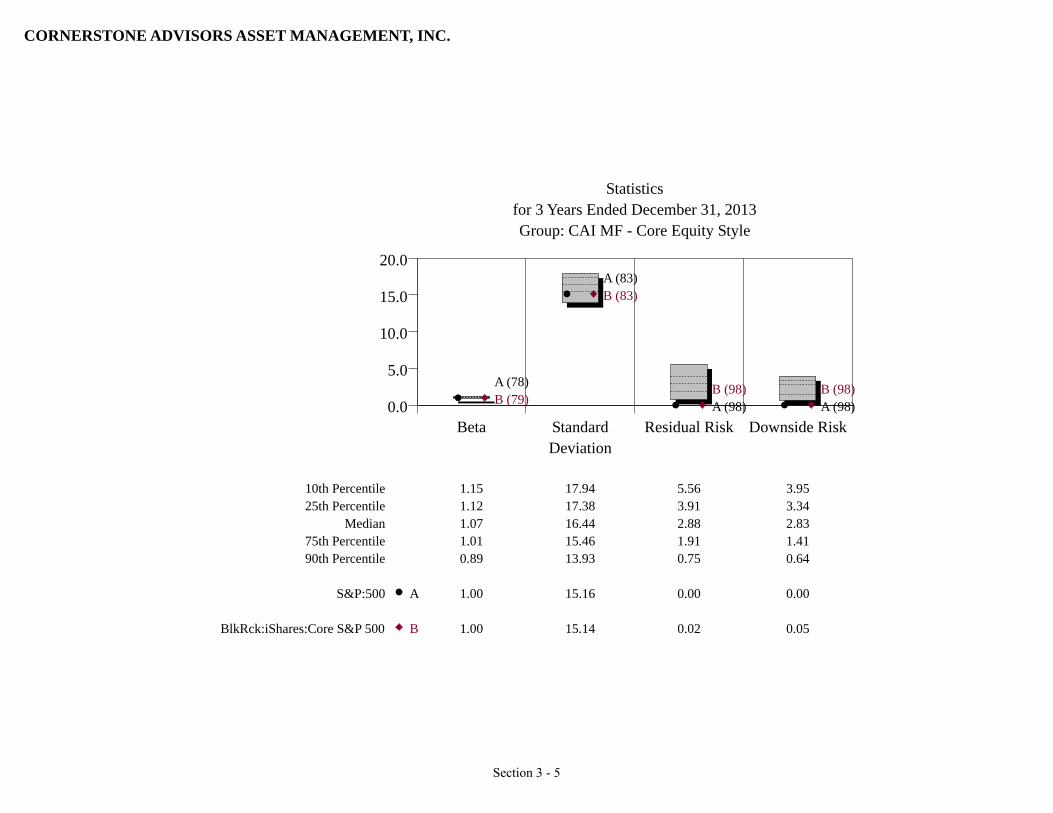

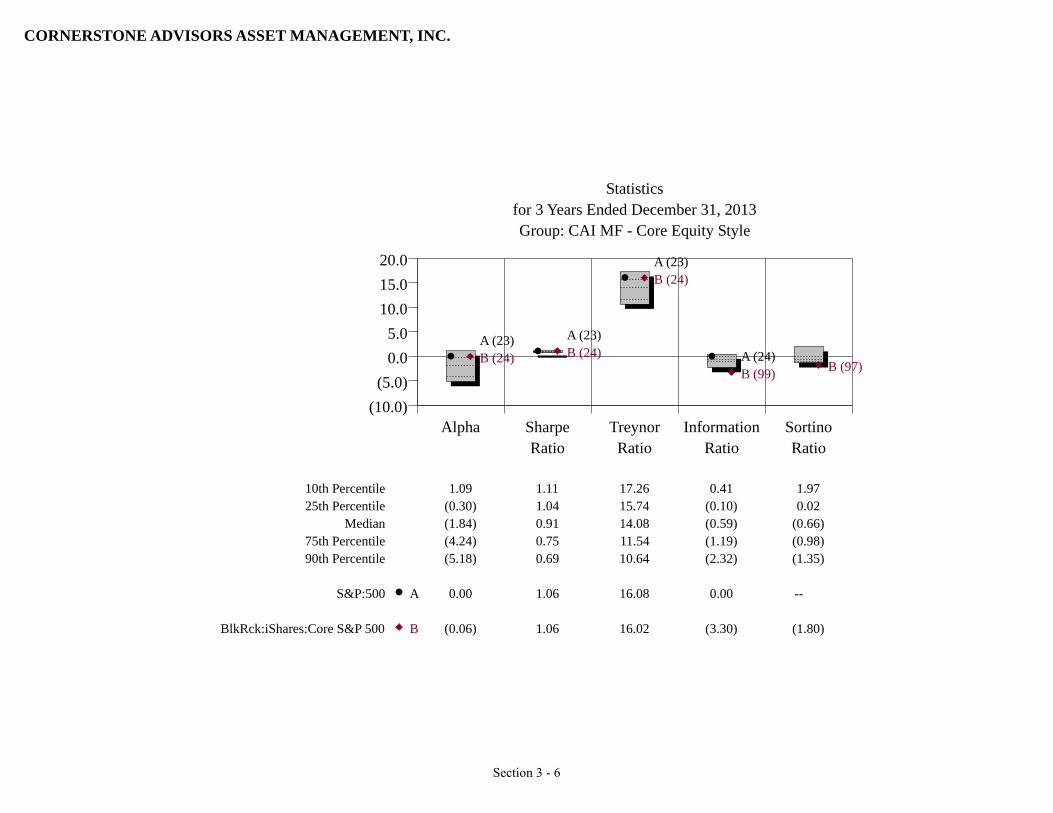

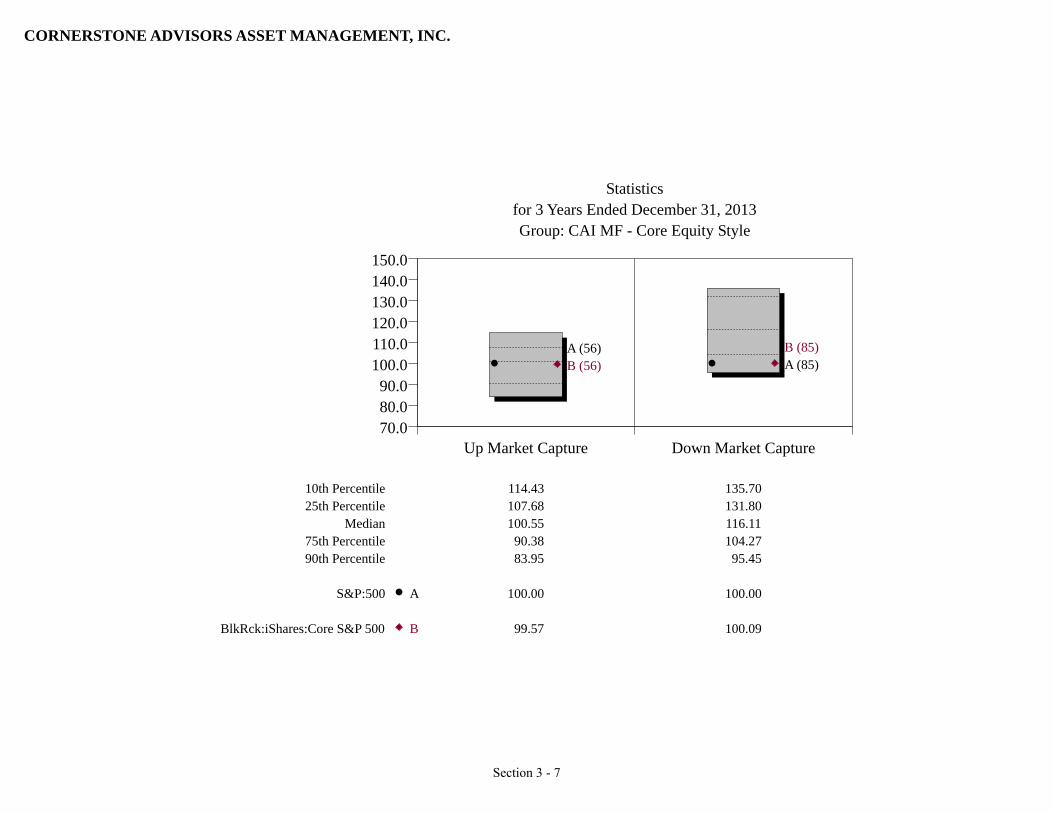

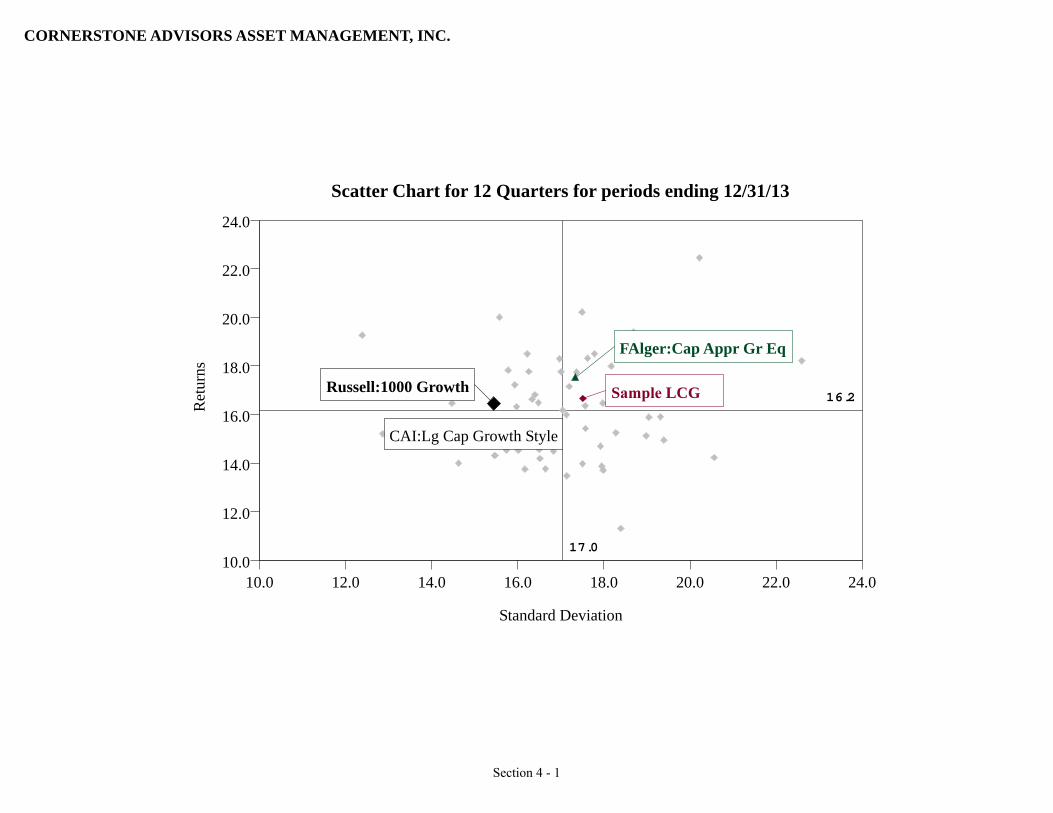

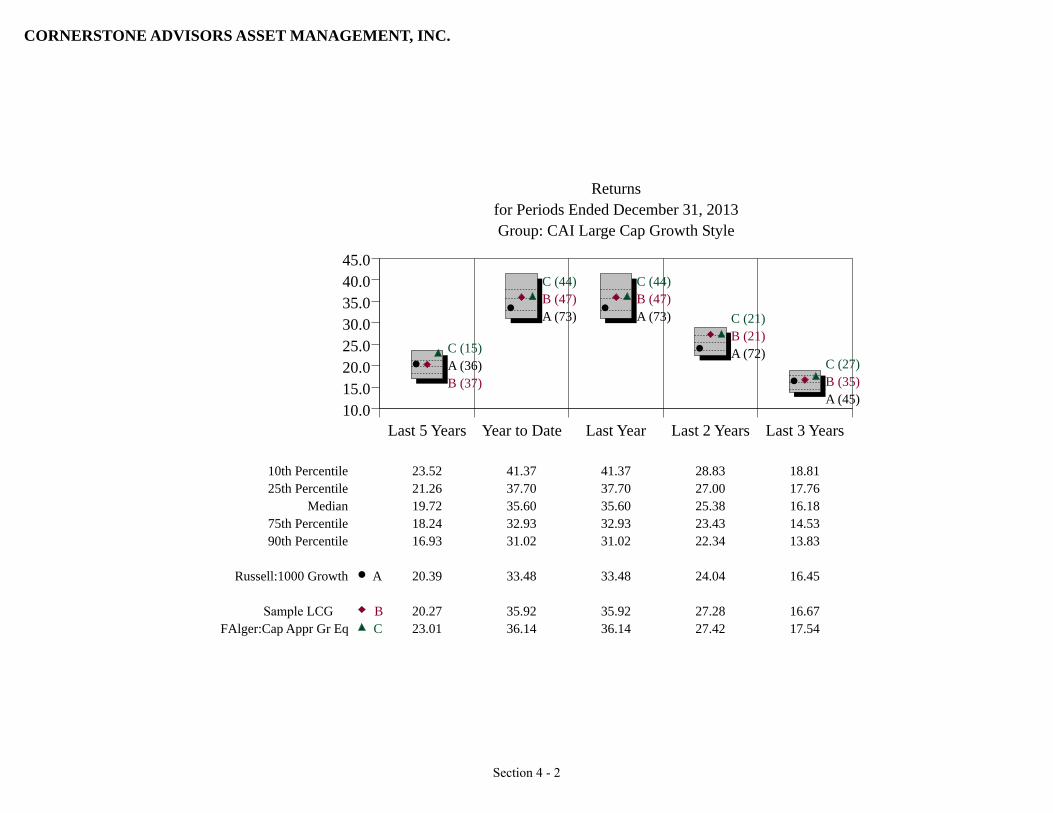

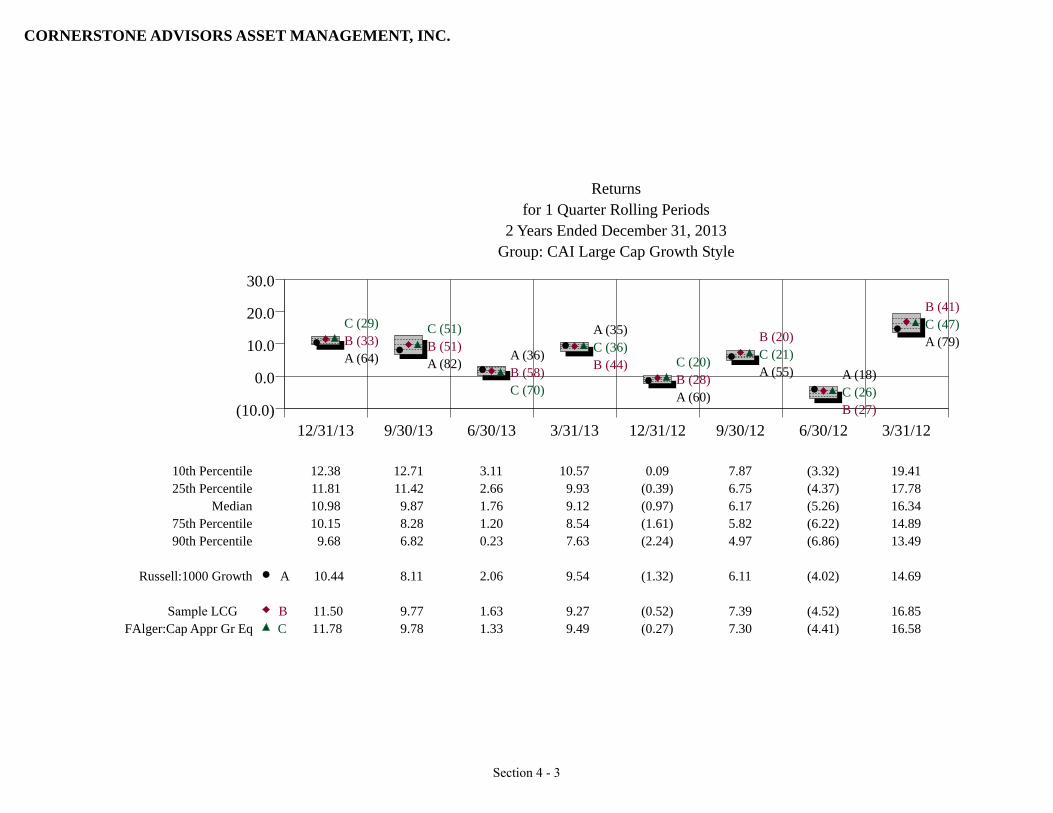

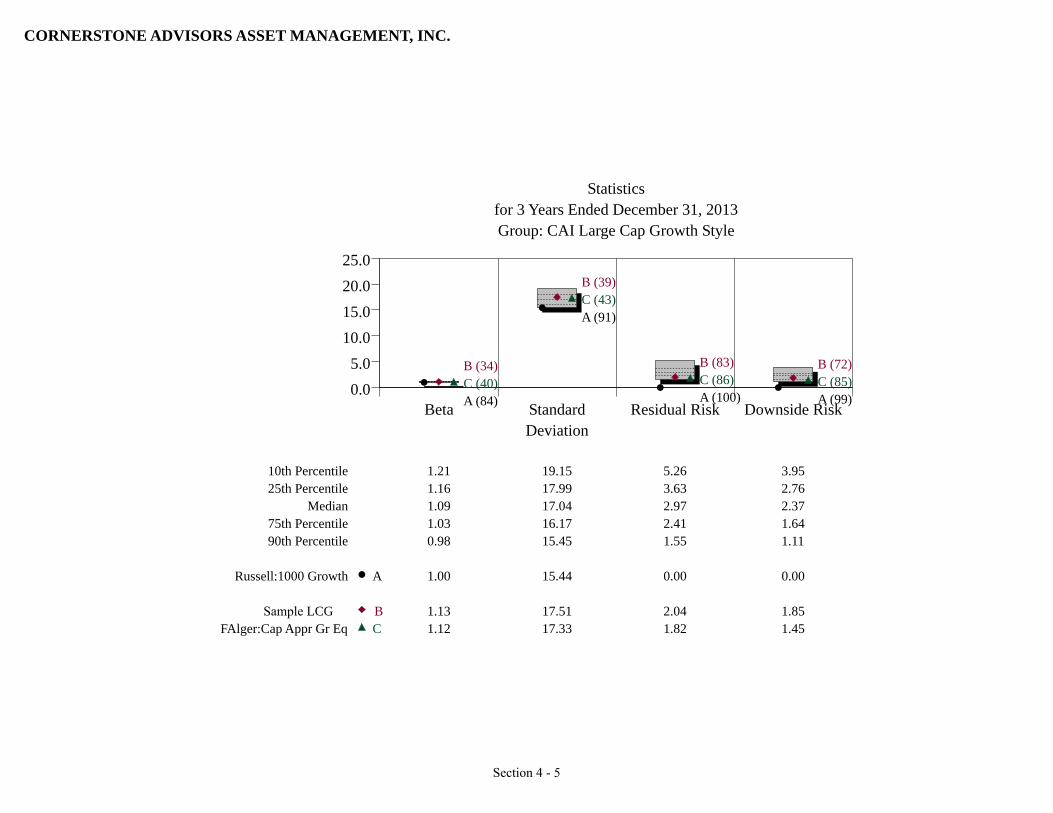

Please see Section III, Exhibit F for a sample detailed quarterly review book.

4. Can these reports be customized to accommodate the Plan’s information needs? Are there charges for these

additional information requests? Within what time frames can these requested changes be implemented?

Cornerstone’s reporting is completely customizable. Our goal while designing our standard reports was to track

the goals and restrictions outlined in the investment policy statement, while maintaining flexibility to add,

subtract or modify the format in many different ways. Normally, Cornerstone does not assess a fee for

customization; however, depending on the extent of customization, a discussion with the Board regarding fees

may be necessary.

Cornerstone is confident we can meet any customization requests with a three month time frame.

5. Describe the process and data needed to input historical Plan performance data into the responding firm’s

system.

The ideal set of data we utilize to populate our performance database is daily transactional and market value data

at the manager level. This allows us to calculate GIPS compliant returns for not only each individual manager

but also for the aggregate portfolio. Knowing this information is not always available, we have the ability to

work with the Fund’s current custodian in order to gather the necessary information. After the data gathering

process has been completed, Cornerstone can normalize the data for import into our performance reporting

database.

20

6. Describe your firm’s source, if any, to determine comparable plan sponsor returns. Indicate the size (#’s and

$’s), composition (#’s and $’s) and data compilation method.

As a member of Callan’s Independent Advisor Group we receive robust peer groups from Callan Associates

across all asset classes, sub asset classes, and at the overall portfolio level. The applicable peer group

Cornerstone would use for a pension plan of your size is the Public Funds Small Funds Group which consists of

75-100 public pension plans with assets of less than $100,000,000.

7. Describe your firm’s view on the most relevant methods of evaluating performance. Include the firm’s

approach to the measurement risk-adjusted performance.

Cornerstone evaluates performance streams for their absolute returns, relative returns, risk levels, and risk-

adjusted statistics compared to an appropriate benchmark and against an appropriate peer group. We have found

that using rolling periods of three and five years removes much of the noise in a manager return stream and

allows us to get a more accurate view of how a manager performs in various market conditions. Risk is neither

good nor bad as long as sufficient returns are generated over full market cycles.

8. Describe your firm’s performance attribution capabilities. Include a breakdown of domestic and international

performance attribution capabilities. Does your firm’s quarterly reporting package contain attribution analysis

at the total fund, asset class and investment manager level?

Cornerstone is capable of providing performance attribution on individual equity managers (both domestic and

international) as well as at the overall fund level. All of the above can be provided in our quarterly performance

package.

9. Please list and describe the specific analytical tools and/or software programs used by the firm with regard to:

- General Market & Economic Research

i. Bank Credit Analyst

ii. Bloomberg

iii. Research Foundation of CFA Institute

iv. Financial Analysts Journal

- Asset/Liability Modeling and Asset Allocation

v. Callan Associates AssetMax

- Risk Management

vi. Callan Associates AssetMax

vii. Callan Associates Performance Evaluation Program

- Public Market Investment Manager Oversight, Selection & Monitoring

viii. Callan Associates

ix. Informa

x. Morningstar

- Private Markets/Real Estate Opportunities

xi. Callan Associates

- Performance Measurement/Attribution

xii. Callan Associates

xiii. Morningstar

- Other (please specify)

21

xiv. Iconics Reportworx – database management tool that produces our fully

customizable reporting suite

10. Are your performance reports and attribution analysis tools available on-line?

Yes. Cornerstone virtual vault is a secure online location for storage and easy access to client documents

including performance reports.

Selection and Retention of Investment Managers

1. Describe your experience and capabilities in conducting searches for investment managers and other

investment services.

Cornerstone uses both a quantitative and qualitative process to select managers to work on behalf of our clients.

Through twenty years of experience in manager search and selection, we have found that past performance is not

truly an indicator of future results. Instead, we look for internal stability, a good business plan and sound

investment processes when choosing a money manager.

Our process begins with a proprietary screening model that identifies investment style and analyzes a manager’s

historical returns as they compare to risk. Then, performance attribution analysis identifies managers that add

value through security selection, sector allocation and other performance-enhancing techniques. This part of the

process reduces the number of potential managers from approximately seven-thousand to three-hundred.

Next, we quantify both market and residual risk through fundamental analysis of the positions held by a manager

and risk factor assessment. This typically reduces possibilities from three-hundred to fifty.

The final step involves a visit and organizational due diligence that reviews investment processes, systems and

technology, organizational capabilities, legal and compliance reviews and personnel. This is all analyzed in the

context of an executable business plan and reduces our list of candidates to about eight or twelve firms with

which we would like to do business in each sub-style.

Our open architecture philosophy coupled with our objective evaluation process eliminates any manager bias.

2. During calendar years 2011, 2012 and 2013, what type and how many manager searches did you conduct for

clients with between $10 million and $50 million in assets for each year? How many different managers were

recommended by you for each year in each asset category?

Cornerstone conducted six major manager searches during this time period.

a. A large cap domestic value search was conducted due to a manager change. Two different managers were

hired as a result of that search.

b. A small cap domestic value search was conducted due to concerns about high turnover. A single manager

was used as a replacement.

c. A domestic fixed income search was conducted. Two managers were selected as replacements.

d. Three searches were conducted in the liquid alternatives space. Four managers with four separate mandates

were selected.

22

3. Describe your database that is used for manager searches.

- How many managers do you maintain on your manager search database?

Our database includes nearly the entire universe of investment managers totally well over 10,000. More

importantly, we have the ability to add any manager to our proprietary database. If we come across a new

manager with a certain asset class, we can immediately add them to our database and compare them against all of

the other managers within that particular asset class.

- Is your system purchased or proprietary?

Cornerstone does maintain a proprietary database of investment managers; however, the backbone of our

database is updated daily through our relationship with Callan Associates, Inc.

- How do you gather, verify, analyze and update manager information? How frequently? How many

years of performance data are on the system?

Cornerstone’s database is constantly being updated on a daily basis with both client specific and third-party

money manager data. We gather this data from several different sources which we believe is essential when

verifying its accuracy. Having relationships with multiple sources (Callan, Bloomberg, Morningstar, PSN, etc.),

gives Cornerstone the ability to cross check the information contained in our proprietary database. If any

discrepancy were to arise, we utilize all the difference data sources to triangulate its origination at which point

we can notify the appropriate parties.

- What criteria do you use in evaluating managers for inclusion in your database?

To eliminate any type of manager bias, Cornerstone allows any manager that possesses a GIPS compliant return

stream inclusion within our database.

4. What fees or other consideration do you receive from managers who wish to be maintained on your database?

Cornerstone does not charge any direct or indirect fees for inclusion in our database.

5. How do you categorize managers? List manager styles and characteristics that distinguish each style in

your classification system, and include concise definitions. How does the firm monitor consistency of style?

Each investment manager is categorized and placed into a specific investment style based on the manager’s

investment strategy and philosophy. Based on those two factors, we are able to place each investment manager

in a peer group that consists of other managers who implement a similar investment style. On a quarterly basis,

we evaluate the manager’s style by looking at each of the individual holdings as well as the holding’s individual

weights within the portfolio. This creates a way for us to plot the manager’s overall portfolio style so that we

may compare it to the broad market.

23

6. Describe the firm’s methodology and sources of data for analyzing and evaluating a potential manager’s

performance. Discuss benchmarks and comparisons with other managers. How is risk factored into this

analysis? How do you verify investment manager information such as performance history and their

compliance with CFA Institute performance reporting standards?

As mentioned above, Cornerstone subscribes to industry wide databases in order to gather CFA Institute

compliant data streams. If a firm is unable to provide CFA Institute compliant and verified returns they are

dropped from all searches. A manager’s mandate will determine the benchmark used during the search.