Cornerstone Family Servicess1.q4cdn.com/663423422/files/doc_presentations/2011/2011_NAPT… ·...

20

NAPTP Presentation May 2011

Transcript of Cornerstone Family Servicess1.q4cdn.com/663423422/files/doc_presentations/2011/2011_NAPT… ·...

NAPTP Presentation

May 2011

Private and Confidential2

Today’s Participants

Lawrence Miller

Chief Executive Officer, President and Chairman

Timothy Yost

Vice President – Financial Reporting and Investor Relations

Private and Confidential33

StoneMor Partners L.P.

StoneMor’s mission is to help families memorialize each life with dignity

StoneMor is the second largest owner and operator of cemeteries in the US

– The Company currently operates 260 cemeteries and 58 funeral homes, diversely

located across 27 states and Puerto Rico

– As of 12/31/2010, over 12,000 acres of land, equivalent to an aggregate weighted

average sales life of 260 years

StoneMor has demonstrated a consistent track record of growth and financial

performance

– 137 cemeteries and 54 funeral homes acquired since inception

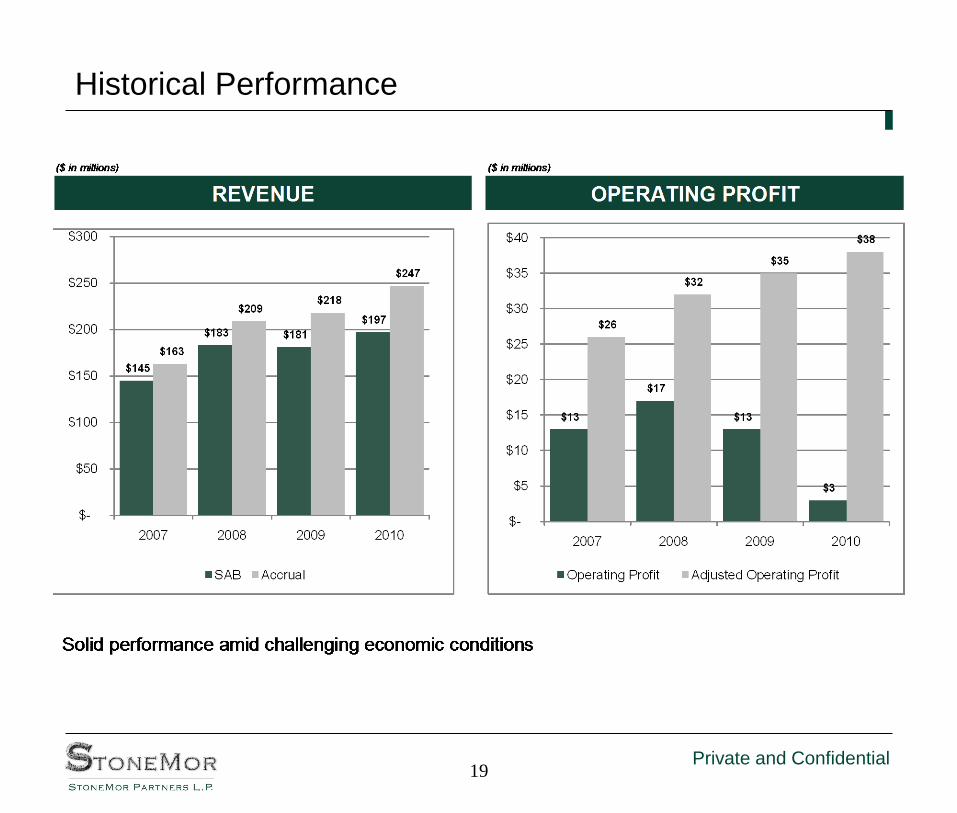

– Revenue has increased from $145 million in 2007 to $197 million in 2010

• 12% ’07-’10 CAGR

– Adjusted operating profits have increased from $26 million in 2007 to $38 million in

2010

• 15% ’07-’10 CAGR

Private and Confidential4

Business Strategy

Enhance

existing

cemetery

operations

Optimize real

estate portfolio

Actively manage

trust fund assets

Execute

disciplined

acquisition

strategy

Private and Confidential5

Value Enhancing Strategy in the Cemetery Business

We are experts at operating and growing a cemetery-focused deathcare business

– Best practices in pre-need marketing

– Extensive and highly driven commission-based sales force

– Volume purchasing lowers costs for cemetery and funeral home merchandise

– Centralized administrative functions lower operating expenses

Our strategy leverages our existing asset base to drive revenues, adjusted operating

profit and cash flow available for distributions to common unitholders

ACCRUAL REVENUESADJUSTED OPERATING

PROFITDISTRIBUTION PER UNIT

($ in millions)

$163

$209 $218

$247

$-

$50

$100

$150

$200

$250

$300

2007 2008 2009 2010

$26

$32 $35

$38

$-

$5

$10

$15

$20

$25

$30

$35

$40

2007 2008 2009 2010

$2.16

$2.22

$2.25

$2.34

$2.05

$2.10

$2.15

$2.20

$2.25

$2.30

$2.35

$2.40

2008 2009 2010 Current

Private and Confidential6

LTM Growth Events

SCI Acquisition Nelms Acquisition

Catholic Archdiocese of Detroit

Completed end of Q1 2010

9 cemeteries in Michigan that conducted

2,400 burials in 2009

Aggregate cash purchase price of $14 million

Received merchandise trusts of $46 million

and perpetual trusts of $15 million, while

assuming $23 million in merchandise

liabilities

First Year Projected Accrual EBITDA - $6.4

Million

Completed end of Q2 2010

8 cemeteries

5 funeral homes

Located in Indiana, Michigan and Ohio

Purchased out of receiverships

2,500 burials and 900 funeral services in the

previous 12 months

Aggregate purchase price of $19.8 million in

cash and units

First Year Projected Accrual EBITDA - $6.7

Million

Completed in July 2010

StoneMor will manage and operate the 3 large cemeteries owned by the Archdiocese

Properties conduct approximately 2,200 interments annually

No “purchase price”; StoneMor steps into Archdiocese P&L

First Year Projected Accrual EBITDA - $1.1 Million

Private and Confidential

2010 Operational Performance Highlights

Increaesed Distributable Free cash Flow by 19%

Increase production-based revenue by 14%

Increased the value of pre-need contracts written by

13%

Increased investment income from trusts by 26%

Increased Adjusted Operating Profit by 6%

7

Private and Confidential

Financing Highlights

Completed offering of 1,500,000 Common Units at $24.00 per unit in

September 2010

– Proceeds used to pay down Acquisition and Revolving Credit Lines

Completed offering of 3,025,000 Common Units at $29.25 per unit in

February 2011

– Proceeds used to redeem Series B&C notes due 2012 and pay off

acquisition and revolving lines of credit due in 2012.

– Eliminated 2012 refinance risk

Renegotiated syndicated bank credit lines

– Reduce interest rate by 50 basis points

– Extended maturity to 2017

– Increased lines from $100 million to $120 million

Only outstanding debt remaining is $150 million senior notes due 2017

8

Private and Confidential9

Diversified Revenue Streams

STONEMOR BUSINESS MIX BY REVENUE – TWELVE MONTHS ENDED DECEMBER 31, 2010

StoneMor’s +800 person sales team creates an unparalleled advantage

in pre-need sales performance

~54% of StoneMor’s

revenue is generated

through highly

predictable at-need

business

Pre-need Sales, 45.9%

At-need Sales, 29.4%

Investment Income, 10.5%

Interest Income, 2.7%

Funeral Home Revenues, 10.8%

Other Cemetery Revenues, 0.7%

Private and Confidential1010

Geographic Diversification

SALES BY STATE – YEAR ENDED DECEMBER 31, 2010

Pennsylvania

17.0%

California

10.3%

New Jersey

8.0%

Virginia

8.1%

Maryland

7.3%

West Virginia

7.3%

Ohio

8.2%

North Carolina

6.3%

Alabama

4.6%

Oregon

4.2%

Other States

18.7%

Private and Confidential11

Cemetery Revenues – How Are Pre-Need Sales Generated?

Leads are generated and appointments made

– 40% of leads result in a presentation

20-25% of all presentations result in a sale

Pre-need sale is usually financed on terms averaging 36 months

– 22% of all sales are cash at the time of the sale

Customers make monthly payments, including interest, on

financed sales

– Down payments average 12%

– Finance charges range from 7% to 12%

Private and Confidential12

Highly Fragmented Industry…

Cemeteries,

9,600

Funeral

Homes,

22,000

$11 billion

$6 billion

___________________________

Source: National Directory of Morticians; Public Filings.

___________________________

Source: ABN Amro Research; Public Filings.(1) Includes StoneMor, SCI, Stewart, Carriage and Loewen.

$17 Billion Market

LARGE DEATH CARE INDUSTRY HIGHLY FRAGMENTED INDUSTRY REVENUE

Independent

Operators

80%

Owned by

Consolidators

20%

(1)

Private and Confidential13

Investment Highlights

9.4% yield superior to most MLPs

Proven acquisition track record

High barriers to entry

Expertise in Cemetery Operations generates significant value

Favorable demographic trends

Secure, stable asset profile

– Diversely located properties

– Merchandise Trust Assets exceed liabilities by approximately $188 million

Experienced management

– Averages over 28 years of industry experience

Conservative financial profile

– No significant near-term debt maturities

– Consistent growth in cash flows

– Tax free structure and minimal capital expenditures

Private and Confidential14

Attractive Yield

8.9% yield attractive relative to alternative MLPs

9.4%

6.0%

7.1%

6.7%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

Ston Median Pipeline Median Propane Median Coal

Stonemor Yield vs Median MLPs

Note: As of May 18, 2011. Pipeline MLPs include BWP, DEP, EPB, ETP, EPD, HEP, KMP, MMP, NS, PAA, SEP, WPZ.. Propane MLPs include APU, FGP, NRGY, SPH.

Coal MLPs include ARLP, NRP, PVR.

Private and Confidential15

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

1930

1931

1932

1933

1934

1935

1936

1937

1938

1939

1940

1941

1942

1943

1944

1945

1946

1947

1948

1949

1950

1951

1952

1953

1954

1955

1956

1957

1958

1959

1960

Favorable Demographics

Aging of the Baby Boom Generation will accelerate the death rate and expand

our target pre-need market

___________________________

Source: Department of Health and Human Services.

ANNUAL BIRTHS IN THE UNITED STATES 1930-1960

Private and Confidential

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

16

Favorable Demographics

Sharply increasing population in our target pre-need market

Pro

jecte

d U

.S. P

op

ula

tion

(in

th

ou

sa

nd

s)

___________________________

Source: U.S. Department of Commerce Census Bureau.

PROJECTED U.S. POPULATION IN 55-65 YEAR OLD CATEGORY

Target Market

More Resilient to

Economic

Downturns

Target 55 to 65 age range

Near retirement – low unemployment risk

Mortgage paid-off (or almost) – minimal debt obligations

Adult children – no tuition costs

Private and Confidential

2,000,000

2,200,000

2,400,000

2,600,000

2,800,000

3,000,000

3,200,000

3,400,000

17

Favorable Demographics

Steady increase in projected mortality rate in the U.S. over the next 20 years

PROJECTED ANNUAL DEATHS IN THE UNITED STATES

___________________________

Source: U.S. Department of Commerce Census Bureau.

Private and Confidential18

Significant Underlying Assets

Cemetery Land

– Approximately 12,000 Acres

– Weighed Average Estimated Sales life of over 260 years

– Book Value of approximately $283.5 million as of December 31, 2010.

Accounts Receivable

– Gross balance of approximately $135.8 million, including approximately $14.5 million in Unearned Interest as of December 31, 2010.

Perpetual Care Trust

– Approximately $249.7 MM as of December 31, 2010

– 10 to 15% of the lot selling price is deposited into a perpetual care fund

– Gains and losses stay in fund – no impact on earnings

– Income from Perpetual Care Trust used to offset cemetery maintenance costs

Merchandise Trust

– Approximately $318.3 MM as of December 31, 2010

– Various percentages of merchandise selling price deposited into trust as cash is received and redeemed once merchandise is delivered

– Gains and losses and income to Company

– Includes approximately $205 MM in assets in excess of the amount required to fund all merchandise liabilities

Private and Confidential19

Historical Performance

Private and Confidential20

Year-to-Date 2011 Performance