Core Banking System Survey 2008€¦ · · 2017-08-22Temenos T24 TEMENOS CoreBanking (TCB)...

71

www.capgemini.com C S S Core Banking Systems Survey UNDER NON DISCLOSURE THROU

Transcript of Core Banking System Survey 2008€¦ · · 2017-08-22Temenos T24 TEMENOS CoreBanking (TCB)...

www.capgemini.com

Capgemini Nederland B.V.Papendorpseweg 100P.O. Box 2575 – 3500 GN UtrechtTel. +31 (0)30 689 00 00Fax +31 (0)30 689 99 99

Core Banking Systems Survey

Survey results 2008

Financial Services the way we see it

Co

re Banking

System

s Survey

Under non disclosUre throU

Under non disclosUre throU

� Financial�Services the�way�we�see�it

Core Banking Systems Survey

Gert Jan van Dorsten

André Spruit

Arthur Barendsen

Survey results 2008

About the report

Capgemini has conducted a comprehensive study of current trends in core banking and the functionality of the major core banking systems available in the main financial markets in the world.This survey was written and compiled during the period from September to December 2007. The report is based on desk research and on a request for information sent out to the leading core banking system vendors.The authors selected the vendors and their products after consulting with Capgemini’s international Core Banking/Banking Packages network. The survey focused specifically on core banking solutions for top-tier banks having a strong position in the important financial markets in the world and offering the solution in more than one country.The Core Banking Systems Survey 2008 is the latest in a series of banking systems surveys. The ‘Asset Management Systems Survey’ and the ‘Treasury Systems Survey’ were published in 2007. The previous ‘Retail Banking Systems Survey’ was published in 2006.

About the authors

The authors of the Core Banking Systems Survey are Gert Jan van Dorsten, André Spruit and Arthur Barendsen. They are leading consultants within the core banking community of the Capgemini banking practice in the Netherlands. Gert Jan van Dorsten is a principal consultant specialized in banking packages in general, with a focus on the domain of core banking back-office solutions and selecting and implementing package-based solutions for financial institutions. Gert Jan is also expert group manager in the Netherlands for core banking and manager of the global FS Industry Packages Center of Excellence.André Spruit is a managing consultant specialized in selecting and implementing package-based solutions for financial institutions. André focuses on core banking packages and before joining Capgemini at the end of 2006 worked for one of the leading vendors in this domain and in the financial services industry itself.Arthur Barendsen is a consultant with experience in embedding packages in a global banking organization.

Gert Jan van Dorsten Principal Consultant Capgemini Nederland B.V.

André Spruit Managing Consultant Capgemini Nederland B.V.

Arthur Barendsen Consultant Capgemini Nederland B.V.

�

� Financial�Services the�way�we�see�it

Preface

I am very proud to present the results of the 2008 Capgemini’s Core Banking Systems Survey. The 2008 survey pro-vides an in-depth and timely insight into the state of the package solution providers industry serving the core banking business in top-tier banks throughout the world.

The main objective of this survey is to help you understand the various core banking systems that are available in the world. It gives you insights into business trends, banks and vendors, package selection criteria, implementa-tion methods and information concern-ing and provided by the solution vend-ors. It should assist you in efficiently and fundamentally narrowing down the search for the right solution pro-vider and make it easy to connect with the vendors on a well-informed basis.

Capgemini can provide financial insti-tutions with considerable benefits in the area of system selection and imple-mentation, including:■ a broad spectrum of services and in-

depth experience of every phase of the system selection process;

■ an exceptional track record based on the successful implementation of many different types of package solutions;

■ different application maintenance contracts on vendor solutions;

■ leading-edge capabilities closely attuned to current and future indus-try changes;

■ strategic and comprehensive services tailored to the individual-ized need of each client;

■ global services and resources (pro-vided in the Rightshore® offers which combine on-, near and off-shore sourcing models), combined with strong regional teams with excellent local delivery capabilities.

Should you require any further infor-mation or assistance in this area, please contact the appropriate Capgemini rep-resentative, whose details you can find in the appendix, or contact our local offices.

We welcome feedback and sugges-tions for improvements to this survey.

I would like to thank all the partici-pating vendors and all colleagues involved for their efforts and contri-butions, especially Martijn Rom Colthoff, Maurice Vuijk, Pascal Breet and Henk Dekker for their inputs for the chapter on trends.

Yours sincerely,

Gert Jan van DorstenPrincipal ConsultantBanking Practice, The NetherlandsManager Global FS Industry PackagesCenter of ExcellenceCapgemini Nederland B.V.

Utrecht, February 2008

1 Background to the survey 7

2 Trends in core banking 92.1 Core banking replacement 92.2 The core banking market 102.3 The core banking clients 112.3.1 Retail/consumer banking 112.3.2 Wholesale/corporate banking 122.3.3 Others 122.4 The core banking domains 122.4.1 Payments & cash management 132.4.2 Savings 132.4.3 Loans and mortgages 142.4.4 Securities 15

3 Global banking overview 2006 - 2007 163.1 Banks worldwide 163.1.1 North America 163.1.2 Europe 163.1.3 Asia 163.1.4 Australia 163.1.5 South America 163.1.6 Africa 173.2 A changing landscape 173.3 Showcase: ABN AMRO acquisition 17

4 Vendor solutions 184.1 Introduction 184.2 History of core banking systems 184.3 Recent market developments 194.4 Recent developments in package solutions 214.5 Competitive landscape 224.6 Future of the market 224.7 Specialized ‘best of breed’ solutions 23

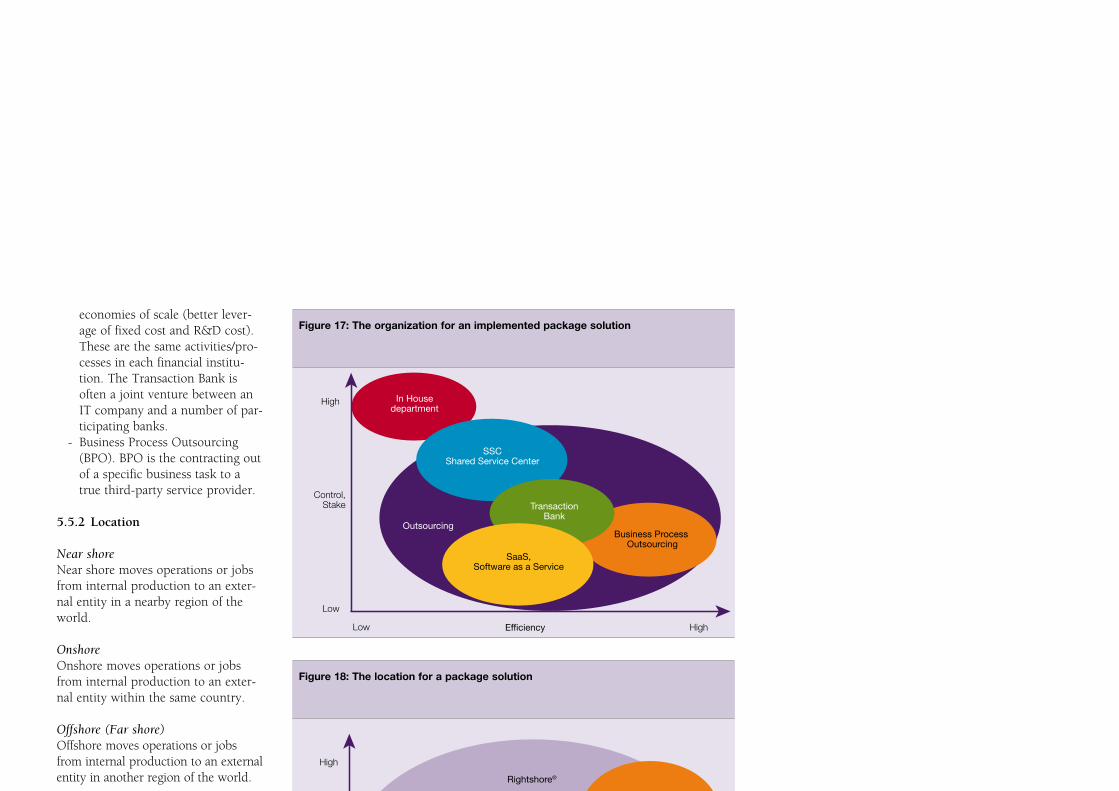

5 Package-based solutions 245.1 Integrated Architecture Framework 245.2 Stage 1: Make or buy 255.3 Stage 2: Selection 265.3.1 Methodology 265.3.2 Integrated or ‘best of breed’ 285.3.3 Selection criteria 295.4 Stage 3: Implementation 305.4.1 Methodology 305.5 Stage 4: Operation 335.5.1 Organization 335.5.2 Location 34

Contents

�

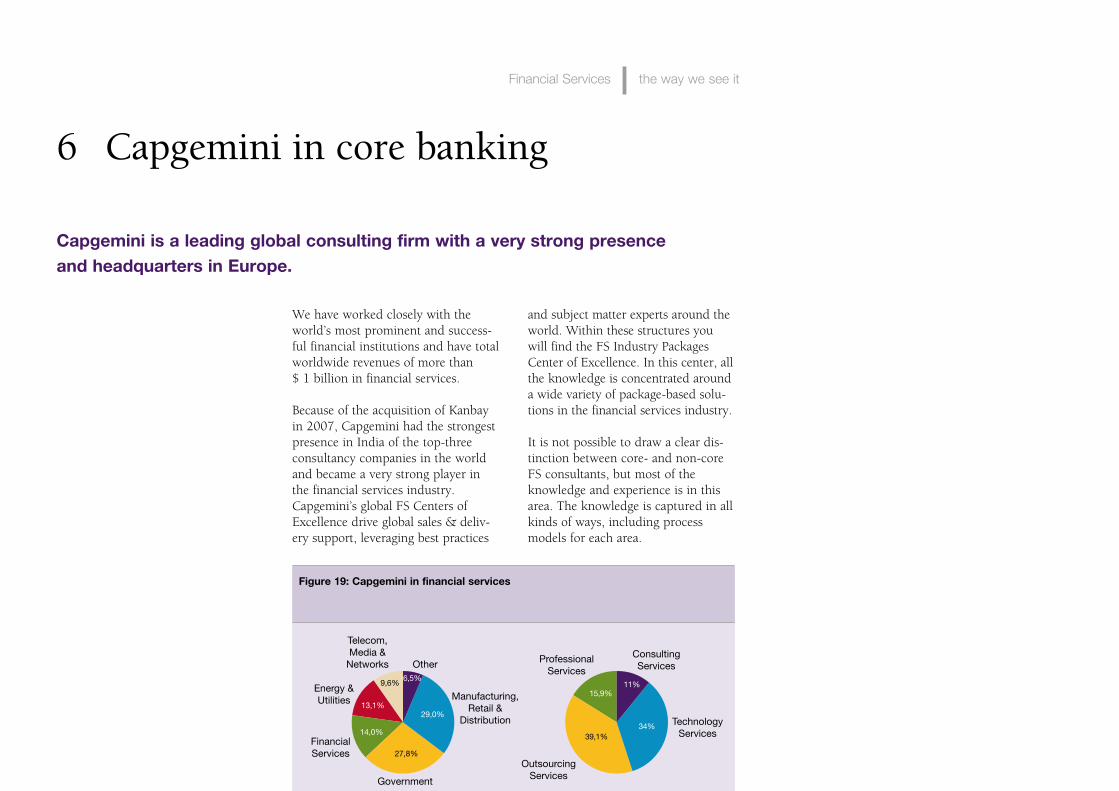

6 Capgemini in core banking 35

Appendix 1: Detailed systems overview 39

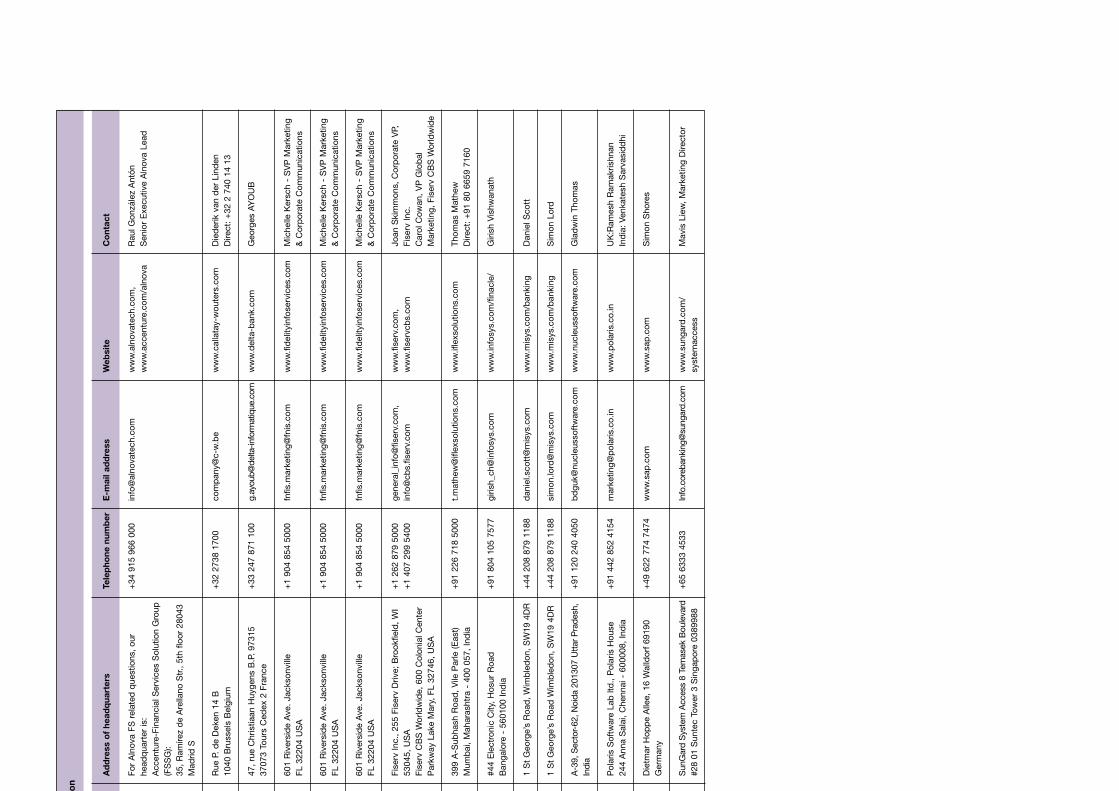

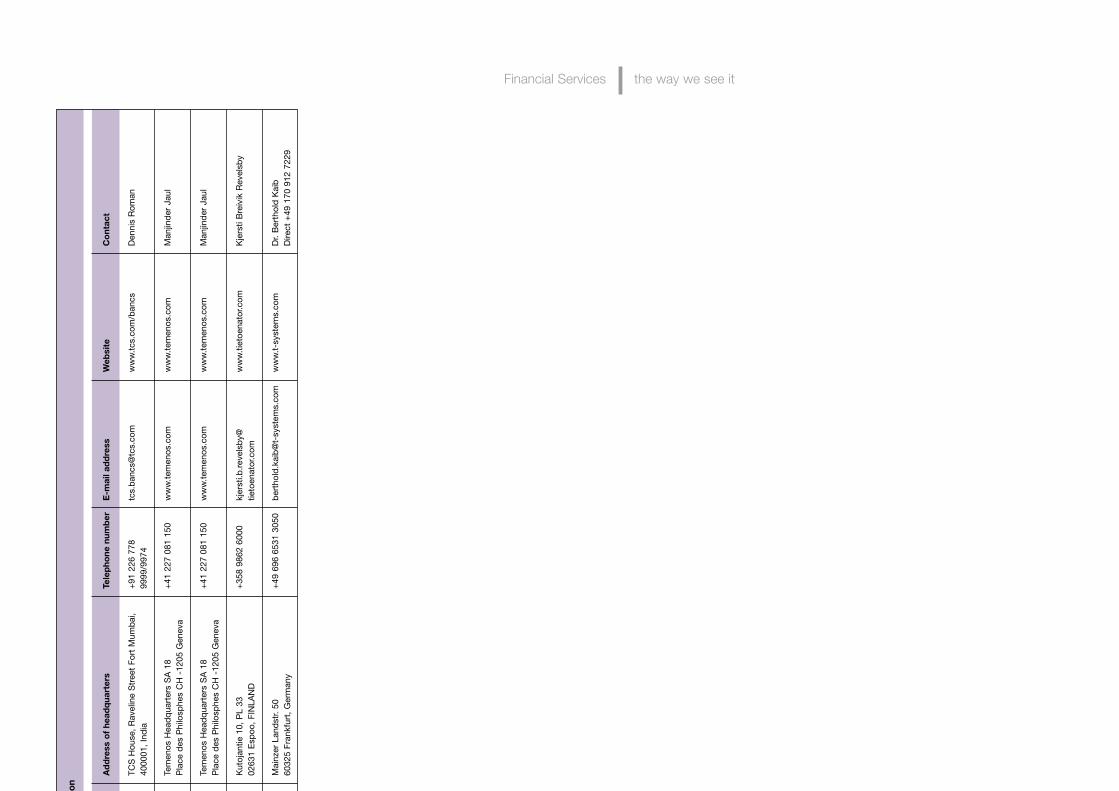

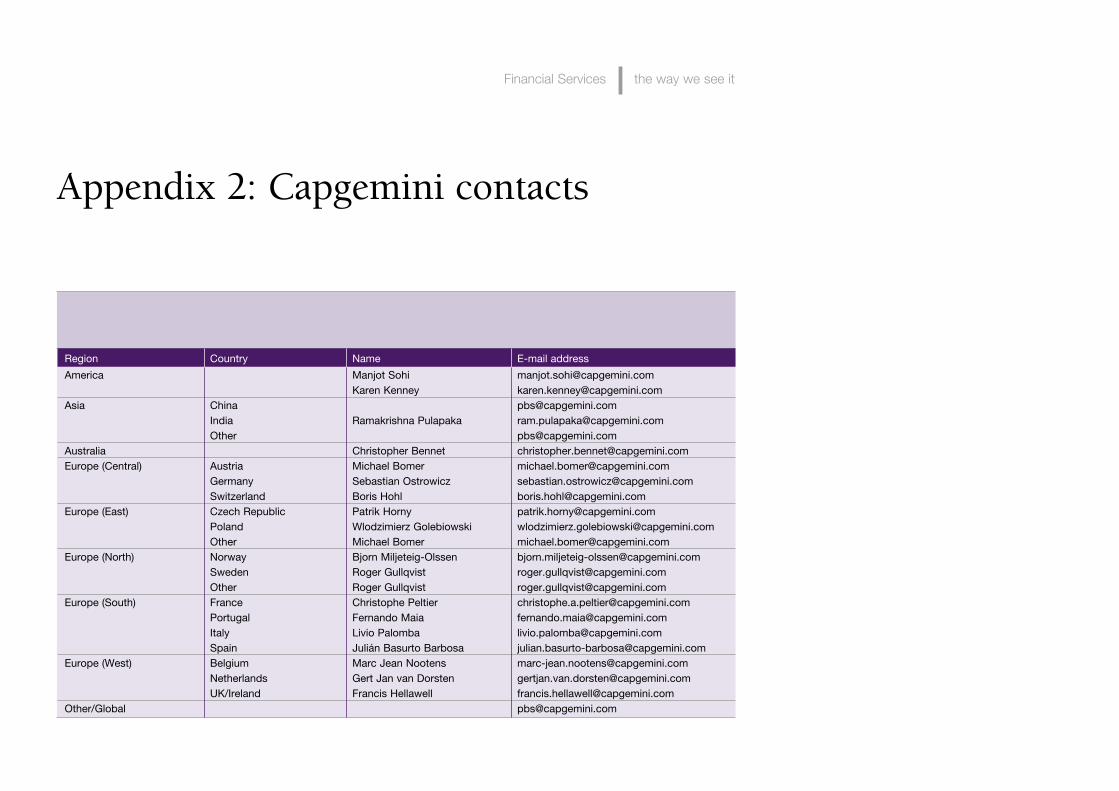

Appendix 2: Capgemini contacts 67

Reference List: The Banker - ‘Retail Banking Performance’ BCG - ‘Renewing core banking IT systems’, 2006BCG - ‘Striving for organic growth in Retail Banking’Capgemini/EFMA/ING - ‘World Retail Banking Report 2007’Capgemini/EFMA/ING - ‘World Retail Banking Report 2008’ Capgemini/EFMA/ABN AMRO - ‘World Payments Report 2008’Capgemini - ‘SOA and Retail Banking Industrialization: An amazing fit’Datamonitor - ‘European Core Systems Strategies, 2007’Forrester - ‘Banking Platform Renewal’, 2005Forrester - ‘Banking Platform Wins 2005’: VendorsForrester - ‘Banking Platform Wins 2006’: Vendors Forrester - ‘The wave of core banking suites 2007’Gartner - Dataquest Insight - ‘Banking Industry Primer, 2006’ Gartner - ‘Magic Quadrant 2006 Retail Core Banking’ Gartner - ‘Hype Cycle for Emerging Back Office Technologies and Applications

(Banking and Investments) 2007’ IBS - ‘Sales League Table 2006’IBS - ‘Sales League Table 2007’IBS - ‘Core Banking Systems - 30 case studies’ SAP/EFMA - ‘Retail Banking Study 2006’

�

� Financial�Services the�way�we�see�it

We feel it provides the reader with valuable insights into the trends and solutions in the domain of core banking.

This survey is the third edition and follows on from the 2003 and 2006 Retail Banking Systems Surveys. It is the latest report in a series of Capgemini publications in the area of package-based solutions in the bank-ing domain. The other areas covered are asset management, private bank-ing, payments, treasury management and risk management.

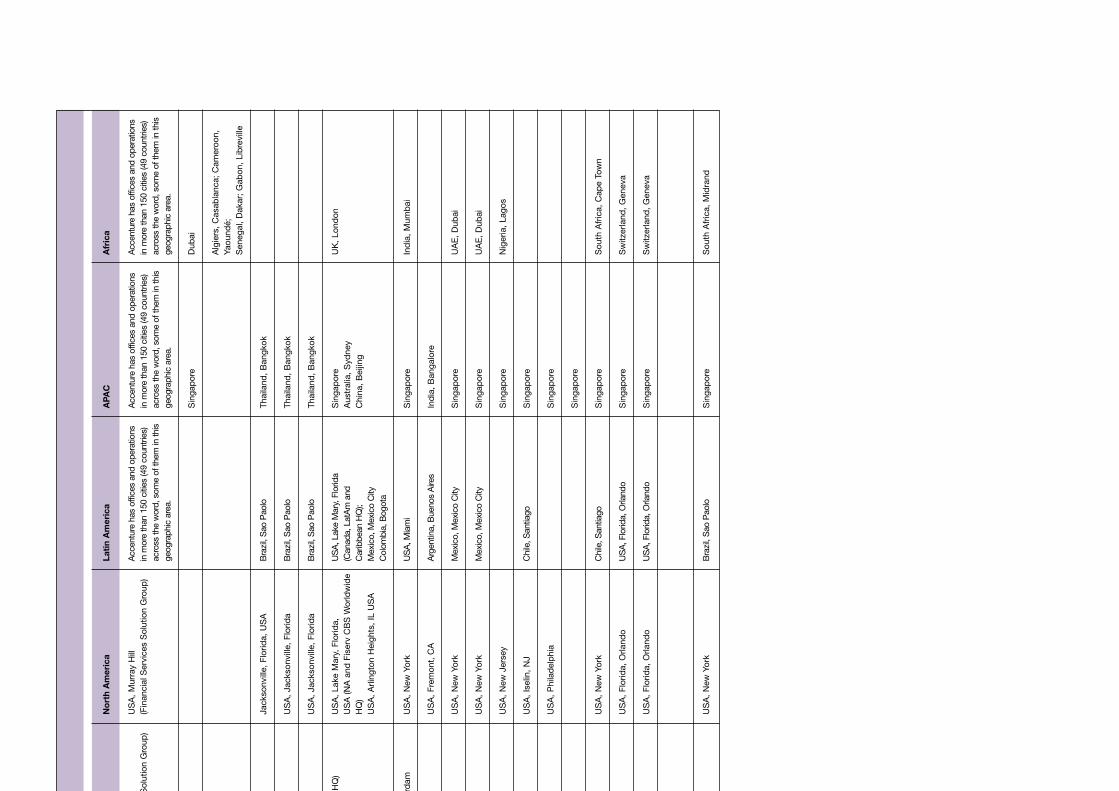

The list of vendors requested for par-ticipation was compiled after con-sulting the banking packages and core banking network of Capgemini and various publications. It includes all the important vendors for the main markets in the world which operate globally or at least regionally in one continent (see figure 1). Capgemini

professionals from all over the world have provided valuable input for the survey. Essential information was gathered from current and previous assignments conducted by Capgemini for core banking clients with package selections or implementations.

Based on requested information, the survey presents a practical overview of the solutions currently available and the capabilities of each system. The main objective is to help users to understand the various products that exist in the market and to narrow down the search and make it easy to connect with the vendors on a well-informed basis. This is very important in the initial phase(s) of the package selection process. It should always be kept in mind that package selection is a challenging, complex process and that it also marks the start of a rela-tionship with one or more external suppliers.

1 Background to the survey

The 2008 Core Banking Systems Survey is based on desk research and a survey sent out to a group of sixteen vendors of core banking solutions.

Figure 1: Origination of systems

15%Europe-South

Europe-West

Europe-Central

Europe-North

Asia

America

Australia

5%

10%

15%

10%

20%

25%

Background to the survey �

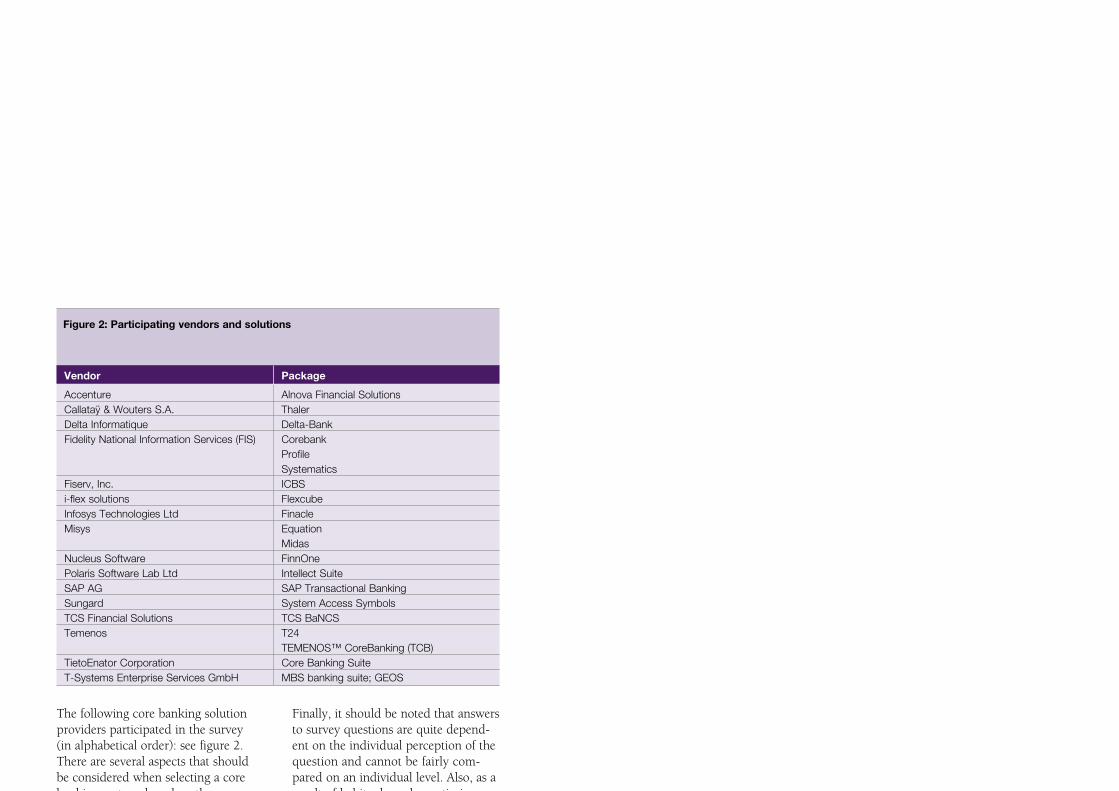

The following core banking solution providers participated in the survey (in alphabetical order): see figure 2.There are several aspects that should be considered when selecting a core banking system, based on the compa-ny’s business vision. These range from functionality, architecture and non-functional requirements to vendor sta-bility and implementation capabilities.

The answers to the vendor survey are published in unamended form as an appendix to this booklet.

Capgemini is an independent advisor and has no exclusive contracts with any of the participating vendors. Furthermore, Capgemini has not attributed opinions to any of the data or vendors.

�

Figure 2: Participating vendors and solutions

Vendor Package

Accenture� Alnova�Financial�SolutionsCallataÿ�&�Wouters�S.A.� ThalerDelta�Informatique� Delta-BankFidelity�National�Information�Services�(FIS)� Corebank� Profile� SystematicsFiserv,�Inc.� ICBSi-flex�solutions� FlexcubeInfosys�Technologies�Ltd� FinacleMisys� Equation� MidasNucleus�Software� FinnOnePolaris�Software�Lab�Ltd� Intellect�SuiteSAP�AG� SAP�Transactional�BankingSungard� System�Access�SymbolsTCS�Financial�Solutions� TCS�BaNCSTemenos� T24� TEMENOS™�CoreBanking�(TCB)TietoEnator�Corporation� Core�Banking�SuiteT-Systems�Enterprise�Services�GmbH� MBS�banking�suite;�GEOS

Finally, it should be noted that answers to survey questions are quite depend-ent on the individual perception of the question and cannot be fairly com-pared on an individual level. Also, as a result of habitual vendor optimism, system functionality on paper is not always the same as system functionality in a real setting.

� Financial�Services the�way�we�see�it

2.1 Core banking replacementDefinition: we define core banking systems as those applications respon-sible for processing and posting trans-actions in the domains of payments, current and saving accounts, loans and securities (such as performing current and deposit accounting, main-taining loan accounts, holding securi-ties positions, clearing payments). Today’s solutions are capable of com-pleting these tasks in an integrated, browser-based environment across multiple delivery channels. They con-stitute a mission-critical element in the financial services industry. Without core banking applications, most banks would instantly come to a grinding halt.

Situation: replacing a core banking sys-tem is often compared with replacing the engine of a Boeing 747 in mid-air. Experts consider core banking replace-ment to be the most complex, risky and expensive IT project that any bank can undertake. A core banking system forms the backbone of a bank’s IT infrastructure and contains records of all customer transactions and the pro-cessing of those transactions. A minor error in this area can cause a bank’s entire system to crash, tarnishing its reputation in the process.

Complex: technology is a key driver of change, and application vendors have long been preaching the virtues of flexible development, speed to mar-ket, real-time processing and a single view of the customer across all lines of business. But, although many early adopter banks in Europe’s middle tier have already embraced this new tech-nology, it is surprising how many of the largest institutions are still battling with the self-imposed handicap of

old-fashioned, outmoded and inade-quate core systems.

Risks: but more than anything else, two factors stand in the way: the risk and cost involved in carrying out a core banking replacement. The costs as well as the risks are high, but the benefits are far greater. Financial insti-tutions that have already announced plans to undertake such projects, will quickly reap the benefits and set an example for others in the industry. They will benefit from greater efficien-cy, easier access to information, and the ability to add new applications without the fear of system crashes. As financial institutions quickly realize that their current, antiquated core sys-tems are no longer adequately meet-ing their needs, many are beginning to consider replacement. Memories of failed attempts continue to haunt many in the industry, however, mak-ing progress slow (one of the largest banks in the world spent around $ 1 billion in the 1990s and still did not succeed!). Getting approval for projects of this scale is also very diffi-cult because banks are currently try-ing to cut costs.

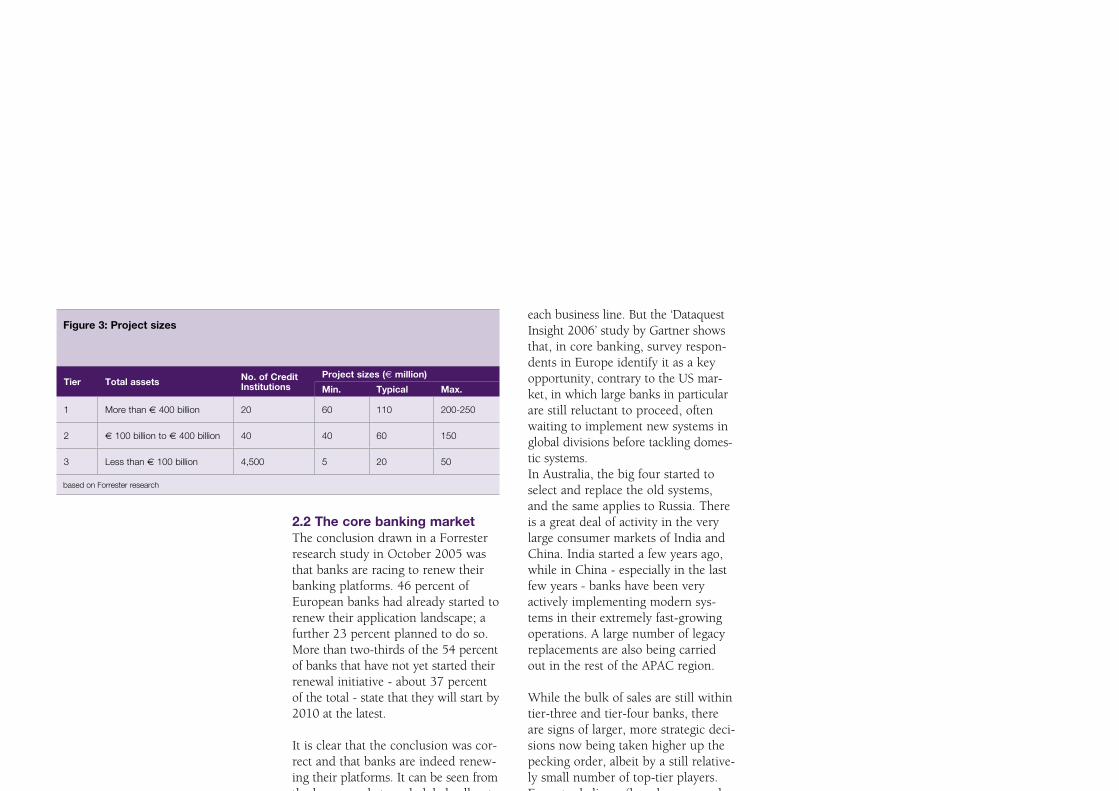

Costs: the project budgets required for software and service are huge: up to € 250 million in extreme cases. Software and services costs for European banks’ renewal initiatives, spread over at least ten years, will be in the € 100 billion range. The European Central Bank estimates that there are about 6,700 credit institu-tions in Europe. These can be broken down into to tier-one, -two and -three banks. That does not take account of all kinds of national par-ticularities, see figure 3.

2 Trends in core banking

Trends in core banking �

Almost all of the top retail banks in the world are still using old legacy systems (originating in the 1960s/1970s) for core banking (in the home markets).

IT globalization appears to be the most important transformation trend for the next five years, with more than 90 percent of the banks we interviewed willing to have a common architecture and modular application suite and a ‘readytogo’ approach to IT implementation.

each business line. But the ‘Dataquest Insight 2006’ study by Gartner shows that, in core banking, survey respon-dents in Europe identify it as a key opportunity, contrary to the US mar-ket, in which large banks in particular are still reluctant to proceed, often waiting to implement new systems in global divisions before tackling domes-tic systems.In Australia, the big four started to select and replace the old systems, and the same applies to Russia. There is a great deal of activity in the very large consumer markets of India and China. India started a few years ago, while in China - especially in the last few years - banks have been very actively implementing modern sys-tems in their extremely fast-growing operations. A large number of legacy replacements are also being carried out in the rest of the APAC region.

While the bulk of sales are still within tier-three and tier-four banks, there are signs of larger, more strategic deci-sions now being taken higher up the pecking order, albeit by a still relative-ly small number of top-tier players. Forrester believes (based on research into vendor deals in 2005 and 2006) that the number of global banking platform deals grew by at least 15 per-cent from 2005 to 2006.The major drivers in the sector for core banking replacements are:■ the severity of regulatory require-

ments and penalties;■ the appeal of a component

approach (SOA - Service Oriented Architecture - and BPM - Business Process Management);

■ a strong focus on architecture for the industrialization of banking, infrastructure and multi-channel enablement;

2.2 The core banking marketThe conclusion drawn in a Forrester research study in October 2005 was that banks are racing to renew their banking platforms. 46 percent of European banks had already started to renew their application landscape; a further 23 percent planned to do so. More than two-thirds of the 54 percent of banks that have not yet started their renewal initiative - about 37 percent of the total - state that they will start by 2010 at the latest.

It is clear that the conclusion was cor-rect and that banks are indeed renew-ing their platforms. It can be seen from the home markets and global roll outs that the top-tier banks are now starting to replace. The smaller banks began earlier. Capgemini’s ‘World Retail Banking Report 2007’ endorses this viewpoint: ‘IT globalization appears to be the most important transformation trend for the next five years, with more than 90 percent of the banks we inter-viewed willing to have a common architecture and modular application suite and a ‘ready-to-go’ approach to IT implementation.’

Most of the top-tier banks in Europe are now busy replacing their legacy systems with a single global system in

10

Figure 3: Project sizes

based�on�Forrester�research

Tier Total assets No. of Credit Institutions

Project sizes (€ million)

Min. Typical Max.

1 More�than�€�400�billion 20 �0 110 200-2�0

2 €�100�billion�to�€�400�billion 40 40 �0 1�0

� Less�than�€�100�billion 4,�00 � 20 �0

� Financial�Services the�way�we�see�it

Trends in core banking 11

■ availability of global resources to tackle back-office systems;

■ industrialization and the shift to transaction banking for core bank-ing back-office systems;

■ new cross-border mergers and acquisitions wave in the European financial services industry.

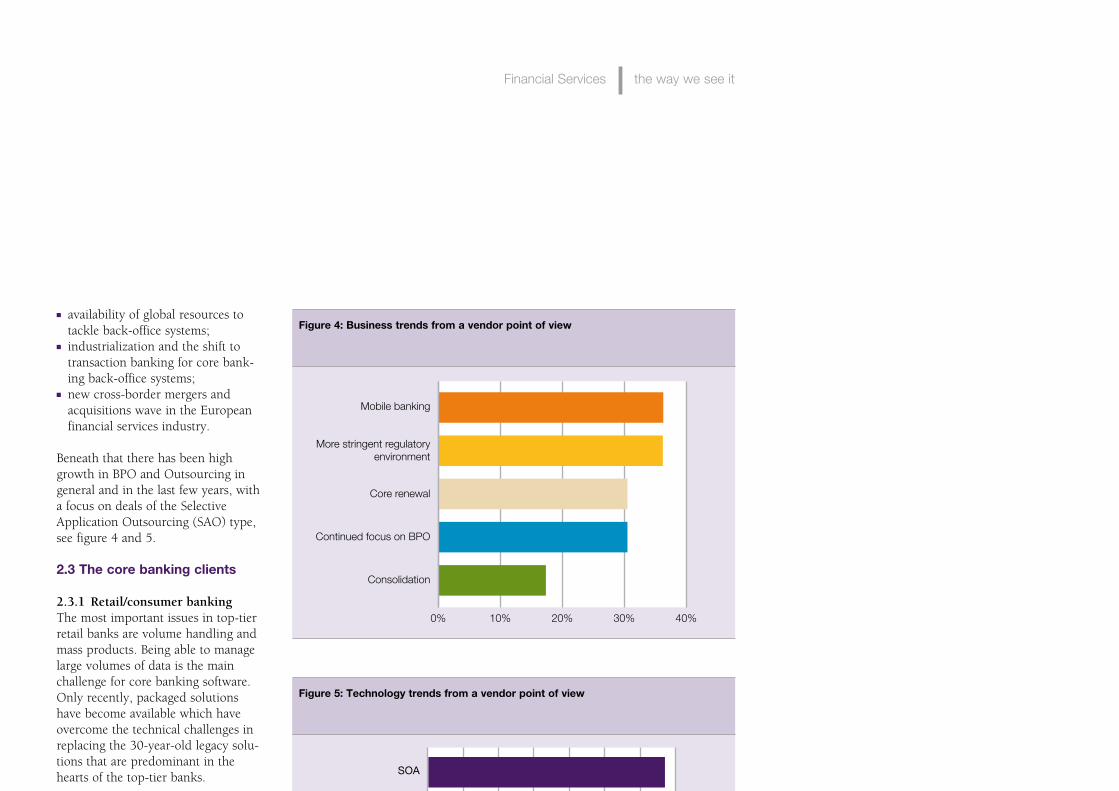

Beneath that there has been high growth in BPO and Outsourcing in general and in the last few years, with a focus on deals of the Selective Application Outsourcing (SAO) type, see figure 4 and 5.

2.3 The core banking clients

2.3.1 Retail/consumerbankingThe most important issues in top-tier retail banks are volume handling and mass products. Being able to manage large volumes of data is the main challenge for core banking software. Only recently, packaged solutions have become available which have overcome the technical challenges in replacing the 30-year-old legacy solu-tions that are predominant in the hearts of the top-tier banks.

Retail banking represents the most significant source of income for the global financial services industry. The key differentiator between market leaders and poor performers will be profitable growth rather than cost cut-ting to improve profits in the long run. Capgemini’s ‘World Retail Banking Report 2008’ shows that the mature markets (North America, European Union - plus Norway and Switzerland -, Japan and Australia) represent 75 percent of the world retail banking market, which is valued at € 1.3 trillion (in 2006). Following the natural economic trend, the retail

Figure 4: Business trends from a vendor point of view

0%

Mobile banking

More stringent regulatoryenvironment

Core renewal

Continued focus on BPO

Consolidation

10% 20% 30% 40%

Figure 5: Technology trends from a vendor point of view

0%

Mobile technology

SOA

Web 2.0

BPM

Channels integration

SaaS

10% 20% 30% 40% 50% 60% 70%

system is increasingly being chosen for both wholesale and retail opera-tions. Another important trend is a global roll out of a centralized system with central data. The corporate banks (and their clients) want an integrated global view of the custom-er with the possibility for treasury departments to have transparent online and daily insight to all accounts globally.

2.3.3 OthersThere are some other interesting devel-opments regarding core banking solu-tions:■ start-up of banking activities in new

(emerging) markets. Sometimes this is carried out by existing banks from other countries, sometimes by other companies. The internet is usually used as a delivery channel and busi-ness can be conducted using a bank-in-a-box solution (less risk);

■ finance departments/subsidiaries of car companies often choose core

12

banking solutions for their finance activities;

■ retailers are also offering retail bank-ing for their consumers in order to improve customer retention;

■ major corporates are developing in-house banking capabilities, often not only for their own company, but also for the outside world.

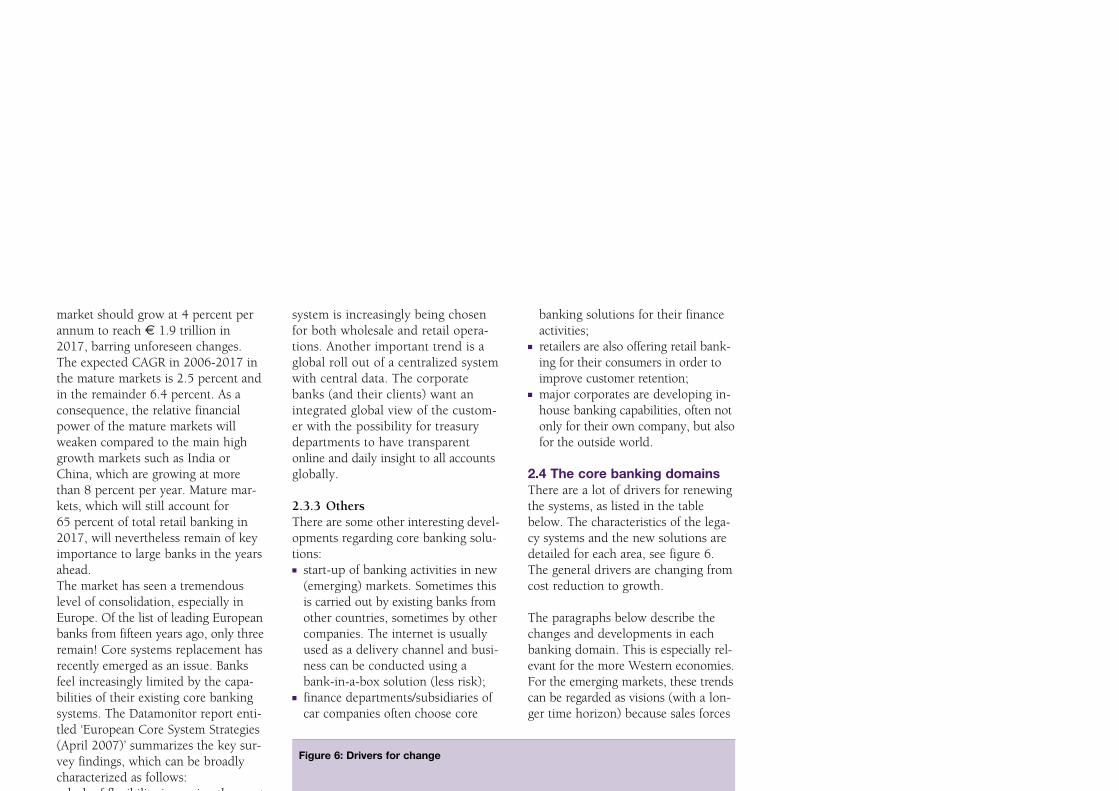

2.4 The core banking domainsThere are a lot of drivers for renewing the systems, as listed in the table below. The characteristics of the lega-cy systems and the new solutions are detailed for each area, see figure 6. The general drivers are changing from cost reduction to growth.

The paragraphs below describe the changes and developments in each banking domain. This is especially rel-evant for the more Western economies. For the emerging markets, these trends can be regarded as visions (with a lon-ger time horizon) because sales forces

Figure 6: Drivers for change

Area Legacy New solutions

Back-office Product-oriented Customer-oriented

Front-office Fragmented/Siloed�channels Integrated�channels

Services Sales/Efficiency-oriented Customer�satisfaction-oriented

Sales Reactive Proactive

View�(Risk) Local/Differentiated Global/Integrated

Operations Per�office Enterprise-wide

Processing Batch,�many�manual�actions Online/Real-time,�STP

Architecture Product/Process-driven Service/Event-driven

Budget Decentralized�budget�discretion Centralized�budget�discretion

Alignment IT-driven Business-driven

Europe Many�different�countries One�European�Union

#�Banks Many�different�(small)�banks Mergers�and�Acquisitions

market should grow at 4 percent per annum to reach € 1.9 trillion in 2017, barring unforeseen changes. The expected CAGR in 2006-2017 in the mature markets is 2.5 percent and in the remainder 6.4 percent. As a consequence, the relative financial power of the mature markets will weaken compared to the main high growth markets such as India or China, which are growing at more than 8 percent per year. Mature mar-kets, which will still account for 65 percent of total retail banking in 2017, will nevertheless remain of key importance to large banks in the years ahead.The market has seen a tremendous level of consolidation, especially in Europe. Of the list of leading European banks from fifteen years ago, only three remain! Core systems replacement has recently emerged as an issue. Banks feel increasingly limited by the capa-bilities of their existing core banking systems. The Datamonitor report enti-tled ‘European Core System Strategies (April 2007)’ summarizes the key sur-vey findings, which can be broadly characterized as follows: ■ lack of flexibility is causing the most

pain in banks’ current core process-ing applications;

■ technology influencers are still domi-nated by cost considerations as the total cost of ownership becomes increasingly important;

■ complexity of implementation is a key challenge for retail banks.

2.3.2 Wholesale/corporatebankingThe core banking market for whole-sale/corporate banking is not as large and as fast-changing as the core banking market for retail banking. However, some trends are interest-ing. One is that a single core banking

� Financial�Services the�way�we�see�it

The most important drivers are com-pliance with all kinds of requirements, often with specific business terms:■ many compliance initiatives, for

example KYC, FATF7, SEPA and the PSD;

■ infrastructure consolidation and collaboration, for example EBA, TARGET2, EMV and SDD;

■ SWIFT is developing the ISO 20022 standard, and standard corporate data is likely to emerge with the drive for STP;

■ emerging standards for the CredEuro and SDD are not easily reconciled with domestic standards (for example use of SWIFT MT103, paper or electronic signature and consumer protection standards), and consistency in implementation has yet to be achieved;

■ Pan-European structures have emerged for cards (Visa & M/C) as well as for high-value payments (TARGET2) and retail payments (EBA STEP2);

■ as consolidation towards emerging standards for transport, messaging and security gains momentum.

2.4.2 SavingsAs in many other markets, the some-what old and long-established savings market is undergoing major change. Whereas previously banks could offer a simple and straightforward savings product differentiated only on the basis of interest rate, now a dynamic and increasingly competitive market, combined with a more demanding customer, is forcing banks to reinvent their savings product strategies.

Primarily, the financial legislation land-scape continues to change as many governments worldwide are revising laws to open up markets and meet the

Trends in core banking 1�

use very basic products to fulfill the demanding targets in such growing markets. Basic improvements to busi-ness processes with adequate platforms are still crucial in banking operations in these countries. Business issues and legal and regulatory requirements are forcing banks to maintain a large num-ber of manual control steps which are no longer required in Central and Western European countries.

2.4.1 Payments&cashmanagementCompliance, in particular SEPA - but also mergers and acquisitions - and cost reduction are the main drivers for renewal of back-office systems. Leading banks, which previously saw payments as a back-office issue, are now tending to bring payments much more to the forefront. The processing of payments, domestic and cross-border, with clear-ing houses and correspondents but also with strategic sourcing, is at the top of the board’s strategy agenda. The reason is very well stated in the ‘World Payments Report 2007’ of Capgemini: ‘SEPA will accelerate Payments Industry Transformation. To be among the major players in SEPA, a bank will need to process at least five billion payments transactions a year. Successful banks will convert their delivery models into open architec-tures, which will enhance their prod-uct offerings and support their needed flexibility.’

Banks are looking to develop a unified and integrated payments infrastructure, which would essentially blur distinc-tions between various payment types: check, cash, debit, credit and e- and m-payments. Payments need to be seen as transparent both to the organization and the consumer.

current standards for integrity, trans-parency, and duty of care. While on the one hand this is causing banks to revise their current products and hence increase cost and competition, it is also creating opportunities for them to create new (combined) sav-ings products. Also, because barriers to entry are being lowered, specialized niche players focused on a specific area such as savings are rapidly gain-ing market share. In some cases these niche players are subsidiaries of foreign banks, but an increasing number of banks are creating or acquiring them.

Additionally, and in part thanks to Al Gore, worldwide media attention has created a trend towards banking with ‘ethical’ banks that differentiate in terms of corporate social responsi-bility. Durable savings products have therefore shown strong, steady growth, and banks are rushing to bring sav-ings products to market to capitalize on this trend.

Apart from the popular topic of dura-ble savings, combinations with security investments, bonus interest, pension savings, and mutual fund savings are still common. And while the reduction in the number of branches is slowly continuing, preference for internet sav-ings accounts is steadily increasing and people are moving their cash around more easily to different accounts.

All-in-all, leading banks are being forced to increase their range of savings products and place greater emphasis on product development. Targeting multiple, segmented parts of the mar-ket with a high number of savings products seems necessary in order to contend with the competition. In an increasingly risk-averse market, the

14

need for savings products is forcing banks to cope with higher volumes over a wider product range and requires a greater focus on product, process and system development and adaptation.

2.4.3 LoansandmortgagesUntil recently, mortgage offers have included a wide range of implicit features, with no provision for the customer to decline them. The devel-opment of a price-driven market is leading mortgage providers to make these features more explicit and optio-nal for the customer. In return for fewer features (and less flexibility), the customer gets a lower rate.

A second trend in the mortgage market is the concentration in the intermedi-ary distribution channel, with resulting complications for the banking systems.

The third major trend in consumer finance is a shift in the pricing strate-gy towards risk-based pricing. The personal risk profile of a customer will be the main factor for the price of a product.Finally, new legislation and regulation are having an impact on the products offered in the mortgage and consumer finance domain.

All these trends require changes to the supporting banking systems, such as:■ more transparent and understand-

able products due to national and international legislation and regula-tion;

■ break-up of the mortgage product into elements that can be included or excluded;

■ straight-through processing to meet the demands of the concentrated

buying power of intermediary orga-nizations;

■ reintroduction of the personal loan. Flexible credit lines have proved to be too risky for some customers and they want more controlled finance: the personal loan;

■ introduction of risk-based pricing. Each customer is offered a price in line with his personal risk profile;

■ new products such as tax-friendly bank savings, which enable banks to compete with insurance compa-nies in tax-friendly products.

2.4.4 SecuritiesThere are a number of drivers of change in the European securities market.

Regulatory changes, for example, will come from multiple initiatives (market, local government and EU) towards an efficient cross-border securities clearing and settlement environment through the harmonization of:■ market rules and practices;■ regulatory, legal and tax differences.

The impact of the globalization of the securities industry can also be seen in the:■ creation of electronic trading plat-

forms (for example Turquoise and CHI-X);

■ increasing number of trading houses trading globally 24x7 requiring round-the-clock settlement;

■ consolidation of CSD and ICSDs;■ creation of BPO centers for securi-

ties operations activities;■ increase in multiple listings of secu-

rities;■ consolidation of stock exchanges

(Euronext-NYSE, et cetera);■ banks outsourcing their securities

operations activities; ■ growing interest in Eastern

European securities markets.

Other drivers for change in the market can be found in the following initia-tives:■ Target II Securities from the

European Central Bank. With this initiative the ECB creates a platform for the cross-border and domestic settlement of securities against cen-tral bank money (€). The platform will service the Central Securities Depositories (CSDs) and will be run by the Eurosystem.

■ Euroclear group’s single platform. With this initiative Euroclear Group is consolidating the services pro-vided by the group onto a single platform and harmonizing the vari-ous practices for settlement, custo-dy, payments, reference data and tax.

Trends in core banking 1�

� Financial�Services the�way�we�see�it

This chapter gives an overview of the biggest market players and the chang-ing landscape, illustrated by a show-case on mergers and acquisitions.

3.1 Banks worldwideThe six sections below are based on the rankings presented in the 2007 edition of ‘The Banker’ magazine’s renowned top 1.000 World Banks (based on strength of tier-one capital).

3.1.1 NorthAmericaTop-ranking banks in North America:1. Bank of America (USA)2. Citigroup (USA)5. JPMorgan Chase & Co (USA)16. Wachovia Corporation (USA)18. Wells Fargo & Co (USA)

Although cracks are appearing in North American banking, US banks remained very profitable in 2006 and 2007. However, Canadian banks showed a higher return on their bank-ing capital than US banks.

3.1.2 EuropeTop-ranking banks in Europe:3. HSBC (United Kingdom)4. Crédit Agricole (France)8. The Royal Bank of Scotland

(United Kingdom)11. BNP Paribas (France)12. Barclays Bank (United Kingdom)13. HBOS (United Kingdom)17. UniCredit (Italy)19. Rabobank Group (Netherlands)20. ING Bank (Netherlands)

Compared to the banks in the United States, the growth in Europe has been higher. Emerging Central and Eastern European banks differ from the large established banks in Western Europe, although both sub-regions show the

same positive trend with regards to profitability.

3.1.3 AsiaTop-ranking banks in Asia:6. Mitsubishi UFJ Financial Group

(Japan)7. ICBC (China)9. Bank of China (China)14. China Construction Bank

Corporation (China)15. Mizuho Financial Group (Japan)

The majority of banks in Asia are also showing healthy growth in profita-bility. With two banks in the global top 10, China is leading in the region. In parallel with the positive results in China, other (new) successful banks are rapidly emerging in Asia. The best of the rest is the Kookmin Bank in Korea (62).

3.1.4 AustraliaTop-ranking banks in Australia:38. National Australia Bank59. ANZ Banking Group60. Commonwealth Bank Group71. Westpac Banking Corporation

While China and Japan are home to the largest tier-one capital banks in the APAC region, Australian banks remain rock-solid regional players.

3.1.5 SouthAmericaTop-ranking banks in South America:54. Banco Itaú Holding Financeira

(Brazil)64. Banco Bradesco (Brazil)73. Banco do Brasil (Brazil)

Banks in the South American region showed very positive profitability fig-ures in 2006 and 2007.

3 Global banking overview 2006 - 2007

1�

In line with the current positive global economic environment, banks have generally done well over the past year.

3.1.6 AfricaThe top-ranking bank in Africa is:116. Standard Bank Group (South Africa)

Whilst African banks have consider-ably less tier-one capital than the major global players, developments in Africa match up to the global trend in growth over the past year.

3.2 A changing landscapeAlthough very positive overall, the banking landscape seems to be chang-ing rapidly. The mergers and acquisi-tion (M&A) and consolidation trend, both on a domestic and cross-border level, is generally expected to continue in the near future. The M&A trend has materialized in a number of interesting deals completed in the last year, for example:■ the acquisition of ABN AMRO Bank

by the consortium consisting of The Royal Bank of Scotland, Fortis Bank and Banco Santander;

■ the acquisition of LaSalle Bank by Bank of America from ABN AMRO;

■ the acquisition of BNL by BNP Paribas;

■ the acquisition of Capitalia by UniCredit in Italy;

■ the merger of Banca Intesa and Sanpaolo IMI.

Interestingly, another trend is the investment of huge amounts of cash by non-traditional, non-Western investors in the financial services industry of the Western world. The fourth quarter of 2007 saw a number of investments by Chinese and Middle Eastern entities in European and North American finan-cial institutions, examples being: ■ the Abu Dhabi Investment Authority

invested $ 7.5 billion in Citigroup, offering the largest US bank the

necessary capital in order to offset big losses from mortgages and other investments;

■ Chinese insurer Ping An acquired 4.3 percent of the share capital of Fortis and appointed a member to the Supervisory Board.

3.3 Showcase: ABN AMRO acquisition

The changing landscape referred to earlier applies very much to the Netherlands. From 1991 to 2007, ABN AMRO was one of the largest banks in Europe and had operations in about 63 countries around the world. Originating in the Netherlands, its history dated back to 1824. A con-sortium of three European banks, The Royal Bank of Scotland Group, Fortis and Banco Santander, announced on October 8, 2007, that an offer for 86 percent of outstanding ABN AMRO stock had been accepted, paving the way for the largest ever bank takeover in history.

The dismantling of ABN AMRO has commenced after many months of uncertainty about its future. Events started when in February 2007 TCI hedge fund asked the ABN AMRO Supervisory Board to actively investi-gate a merger, acquisition or break-up of ABN AMRO, since, in its opinion, the market capitalization of ABN AMRO did not reflect the value of the underlying assets. In April 2007, ABN AMRO and Barclays announced the proposed acquisition of ABN AMRO by Barclays. The deal was valued at € 67 billion and included the sale of the LaSalle Bank to Bank of America for € 21 bil-lion. A few days after the joint announ-cement by Barclays and ABN AMRO, the consortium issued their indicative

Global banking overview 2006 - 2007 1�

offer, which at that time was worth approximately € 72 billion. A precondition of the offer was that ABN AMRO would abandon its sale of LaSalle Bank to Bank of America. However, during the shareholders’ meeting on the following day a majori-ty of the shareholders voted in favor of the sale of LaSalle.In July 2007, Barclays raised its offer for ABN AMRO to € 67.5 billion. It did so after securing investments from the governments of China and Singapore. The offer remained below the offer made by the consortium in the previous week. At the end of July 2007, the ABN AMRO board withdrew its support for the Barclays offer, which was lower than the offer by the group led by RBS. The board stated that it could no longer recommend the offer from a financial point of view. At the beginning of October, Barclays withdrew its bid for ABN AMRO and, with 86 percent of the shareholders accepting the consortium bid and Fortis completing its financing, the consortium was able to formalize its offer and take control of ABN AMRO.

� Financial�Services the�way�we�see�it

4.1 IntroductionThis chapter provides an overview of the market for core banking systems. We begin by providing a brief history of the market. How was this market shaped?

We continue with the developments since the previous version of this sur-vey, dating from 2006. What hap-pened in 2006 and 2007? What acqui-sitions and alliances took place? Which partnerships broke up? Who won the major deals and are there any new challengers emerging?

Finally, we take a look into the future. What are the trends in vendor solu-tions, functionally and technically? Where do we feel the market will go?

4.2 History of core banking systems

The first core banking solutions appeared in the 1970s in the United States. Most of them ran on main-frame computers and were designed by the banks themselves or by third parties in conjunction with the large US banks. Limitations to exporting these systems outside the US were that these were mainly single-currency- based as they were designed for the US market only. In the 1980s, these solutions moved to all continents, mostly as a result of following the major US banks such as Citibank.

During the 1970s, 1980s and most of the 1990s, packaged banking solutions flourished in international operations. For domestic retail operations, howev-er, most large banks preferred to stay with the systems they had developed in-house. Some brave top-tier institu-tions did try replacing the in-house systems with package solutions cus-

tomized by top-tier banks, but these efforts consistently failed.

In the 1980s, we saw package solu-tions coming from other parts of the world, primarily Europe, Asia and Australia. Vendors with a different but comparable background also entered the arena, for example the private bank-ing solutions developed in countries such as Switzerland and Luxembourg. Because - due to the nature of their business - these were more customer-focused than the transaction-oriented, transaction-crunching engines avail-able before, they had a natural fit with the customer centricity that was com-ing increasingly into focus. Limitations of these systems mainly had to do with the ability to handle large volumes.

The 1990s saw new players emerging in India, benefiting from the opening up of the Indian economy, the avail-ability of English language skills, and the huge pool of highly skilled engi-neers. i-flex solutions (and its legal predecessor CITIL) can be considered as the first successful software product company from India that managed to sell outside the Indian subcontinent. It was followed by the likes of Infosys and Tata Consultancy Services (TCS) - companies that originally focused more on providing off-shoring, consulting and outsourcing services but moved into the software product business - and later by other product companies such as Polaris Labs and Nucleus.

At the end of the 1990s, new players made their entry. ERP giants such as SAP and IBM started entering the mar-ket (following a strategy of organic growth and development and with a presence at the heart of the accounting domain in many banks), followed a

1�

4 Vendor solutions

When did core banking become a market for vendor solutions, and what generations of solutions have there been?

few years later by Oracle (through the acquisition of i-flex solutions and Siebel and aligning these to their tech-nology and application strategies).

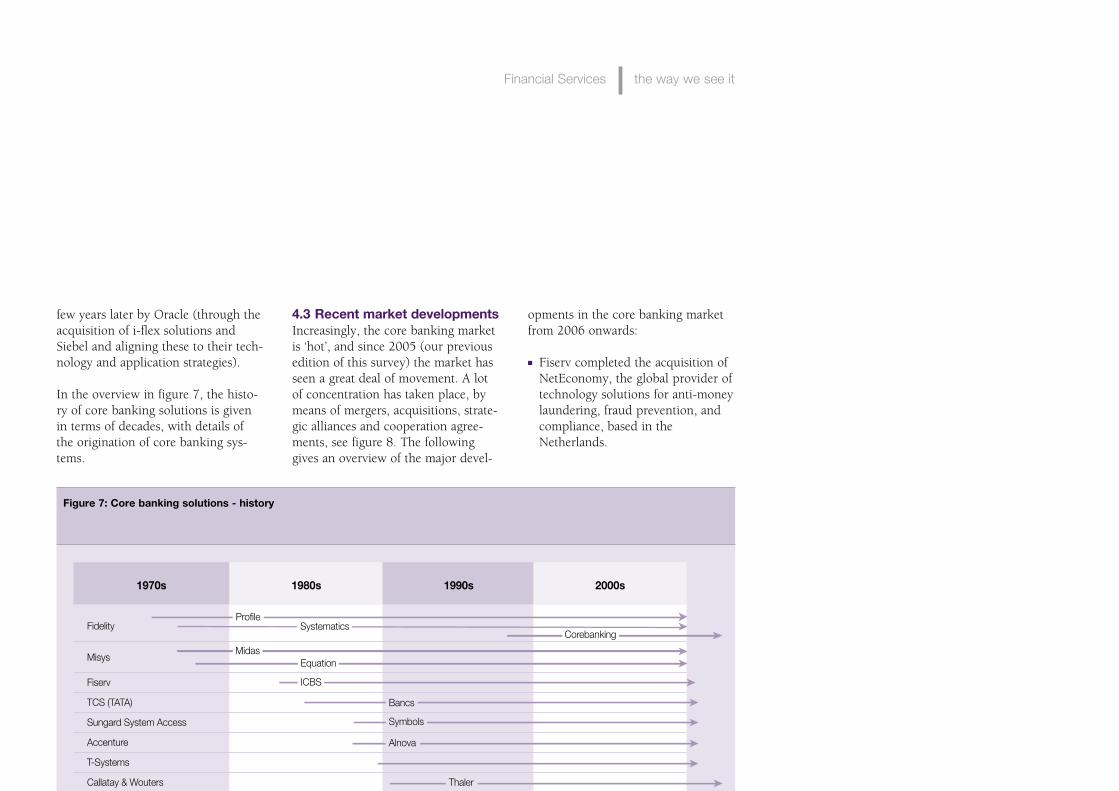

In the overview in figure 7, the histo-ry of core banking solutions is given in terms of decades, with details of the origination of core banking sys-tems.

4.3 Recent market developments Increasingly, the core banking market is ‘hot’, and since 2005 (our previous edition of this survey) the market has seen a great deal of movement. A lot of concentration has taken place, by means of mergers, acquisitions, strate-gic alliances and cooperation agree-ments, see figure 8. The following gives an overview of the major devel-

Figure 7: Core banking solutions history

Fidelity

Misys

Fiserv

TCS (TATA)

Sungard System Access

Accenture

T-Systems

Callatay & Wouters

Tietoenator

Temenos

Delta Informatique

SAP

I-Flex

Infosys

Nucleus

Polaris

1980s 1990s 2000s1970s

Source in the United States

First backoffice systems

Build in house, third party

Evolved to first packages

Take-overs/shake-out

Entrance new players

Replacing first systems

Failed to replace core

Move to all continents

Booming business

Follow banks oversea

Failed to replace core

Important sources India

Replacing core banking

Customer focus

Outsourcing

Equation

ICBS

Profile

Midas

SystematicsCorebanking

Bancs

Symbols

Alnova

Thaler

Core Banking Suite

T24

SAP Corebanking

Flexcube

Finacle

TCB

Delta Bank

Finnone

Intellect suite

Vendor solutions 1�

opments in the core banking market from 2006 onwards:

■ Fiserv completed the acquisition of NetEconomy, the global provider of technology solutions for anti-money laundering, fraud prevention, and compliance, based in the Netherlands.

� Financial�Services the�way�we�see�it

■ Fiserv also acquired Checkfree, a provider of financial electronic com-merce services and products includ-ing electronic bill payment and internet banking.

■ Oracle completed the acquisition of Siebel Systems (customer relation-ship management solution provider) and Hyperion (performance man-agement solution provider). It also raised its stake in i-flex to over 80 percent.

■ Oracle announced the formation of its Financial Services Global Business Unit, which would provide an integrated suite of standards-based, industry-specific applications for banks, insurance companies and capital market firms. The unit is led by Rajesh Hukku, founder, former CEO and now Chairman of the Board of i-flex solutions.

■ i-flex solutions acquired Mantas, a US provider of anti-money launder-ing and compliance technology.

■ SAP and Accenture ended their stra-tegic cooperation in the banking domain.

■ SAP acquired Business Objects. The companies believe that customers will gain significant business bene-fits through the combination of new, innovative offerings of enter-prise-wide business intelligence solutions along with embedded ana-lytics in transactional applications.

■ SAP and Callataÿ & Wouters announced collaboration between the companies to offer an end-to-end core banking solution for mid-size banks to build a business pro-cess platform, based on SAP soft-ware and technology.

■ interestingly, Misys also announced a strategic alliance with SAP to deliver an integrated banking sys-tem based on its BankFusion tech-nology, which will run on the Sap NetWeaver platform.

■ Tata Consultancy Services (TCS) consolidated its financial products business into a new Strategic Business Unit, TCS Financial Solutions.

■ TCS also announced the completion of the acquisition of its Switzerland-based partner TKS-Teknosoft (TKS), expanding its portfolio of banking products and consolidating its European operations.

■ Temenos and Metavante have entered into an agreement whereby Metavante will distribute the Temenos CoreBanking platform in the US. Temenos will retain royal-ties on license and maintenance fees, outsourcing fees and profes-sional services revenues. Metavante, one of the three largest US bank technology and payment-processing firms, will have exclusive US access to a co-developed global software

20

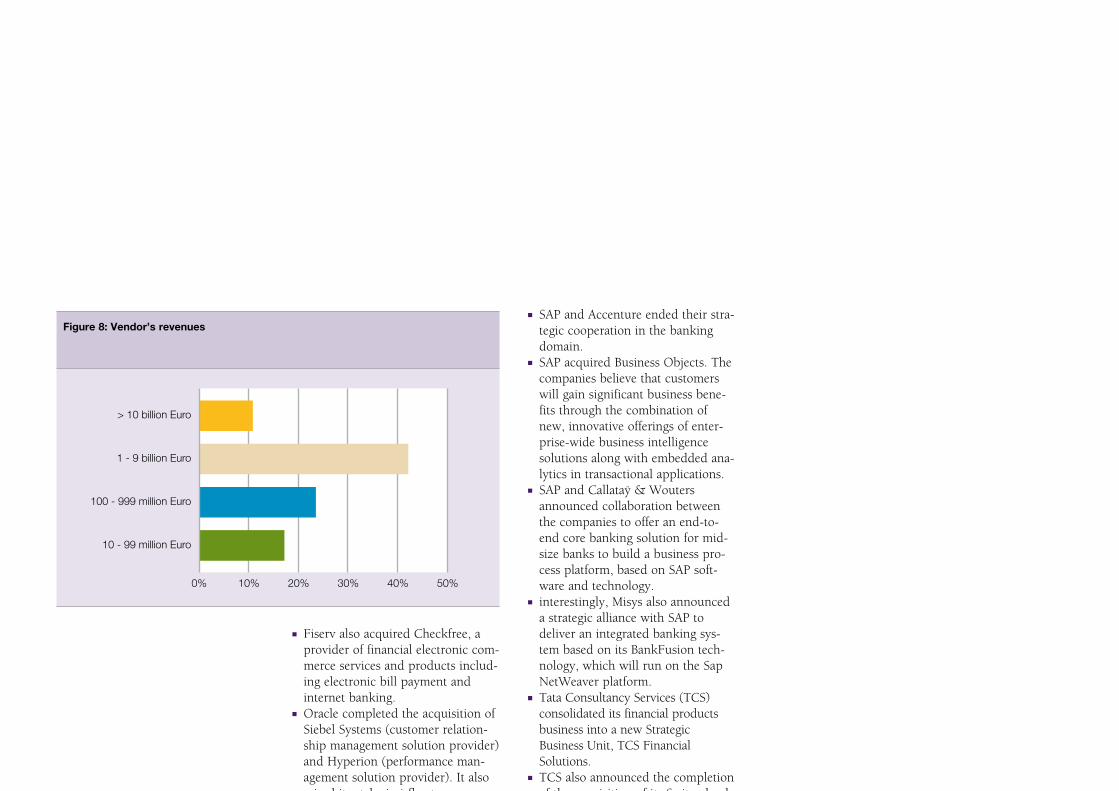

Figure 8: Vendor’s revenues

0%

> 10 billion Euro

1 - 9 billion Euro

100 - 999 million Euro

10 - 99 million Euro

10% 20% 30% 40% 50%

platform for the US market that is based on TCB.

■ T-Systems acquired MBS of Alldata and GEOS of SDS, but has not hith-erto sold it outside the German-speaking market.

4.4 Recent developments in package solutions

The core banking systems area is becoming more and more mature, with packaged solutions increasingly attaining a functional richness that was previously available only from in-house legacy solutions. They are also attaining a technical and organi-zational level that meets the business expectations in terms of agility, time to market and operational support.

“Although the argument that core banking functionality is fast becoming a commodity is valid, the means to support banking functionality in the back-office is changing. Business expectations for rapid time to market for products, and the corresponding operational support, are quickly out-stripping the capacity of development organizations to facilitate change. Most of this is due to trapped, line-of-business logic buried in appli-cation-specific legacy environments,” says Gartner’s Don Free. “The matura-tion of middleware messaging archi-tectures, the evolutionary path to serv-ices and event-driven constructs and new development techniques, such as service-oriented development, are simplifying maintenance and support of products while reducing volatility commonly associated with the intro-duction of new products and services. Some core banking vendors are already progressing quickly to achieve componentization of their back-office offerings.”

FunctionalityOn the functional side, we have not seen any fundamental change in the functionality required from core bank-ing systems. This means that many core banking system vendors have been able to bridge the functionality gap between them and the leading platforms. Some vendors have been able to improve the volume-processing capabilities of their functionally broad-er or more advanced systems. As a result, advanced functionality that was previously limited to private bank-ing clientele, for example, is now avail-able in core banking systems that are able to handle the volumes commonly arising in the mass retail banking mar-ket.

TechnologyOn the technical side, we have seen a move away from dependencies on hardware platforms and operating sys-tems. The vendor offerings conse-quently have access to a larger mar-ketplace. Conversely, it has given banks access to a much larger set of vendors and solutions. Banks can operate core banking systems on their platform of preference. Some banks prefer to stay on their well-embedded and reliable mainframe infrastructure. Others move to highly scalable com-modity platforms, freeing them from a lock-in to an increasingly small set of expensive mainframe specialists.

Messaging,serviceorientationandarchitectureWith regard to business expectations, the expectations for rapid time to market for products and the corre-sponding operational support are quickly outstripping the capacity of development organizations to facilitate change. This is leading to major devel-

Vendor solutions 21

“Although�the�argument�that�core�banking�functionality�is�fast�becoming�a�commodity�is�valid,�the�means�to�support�banking�functionality�in�the�back-office�is�changing.�Business�expectations�for�rapid�time�to�market�for�products,�and�the�correspond-ing�operational�support,�are�quickly�outstripping�the�capacity�of�development�organizations�to�facilitate�change.�Most�of�this�is�due�to�trapped,�line-of-business�logic�buried�in�application-specific�legacy�environments.”Don Free

Research�Director�Banking�

Gartner

� Financial�Services the�way�we�see�it

opments in the core banking area, namely messaging, service orientation and architecture. Messaging middle-ware has become a de facto standard. Service orientation and loose event-based coupling have become part of mainstream thinking. We have seen the arrival of the first business process frameworks for banking. Business process modeling and orchestration is on the rise. All this will give banks a great deal of freedom. A bank can buy the services that are available on the market from vendors, service-enable existing legacy systems or create its own services in areas where it feels this gives the bank an advantage in the market. And it can outsource when it feels that a service is not its core competence! We have seen vend-ors coming up with strategies in this area in the last two years and we have also seen the first resulting products.

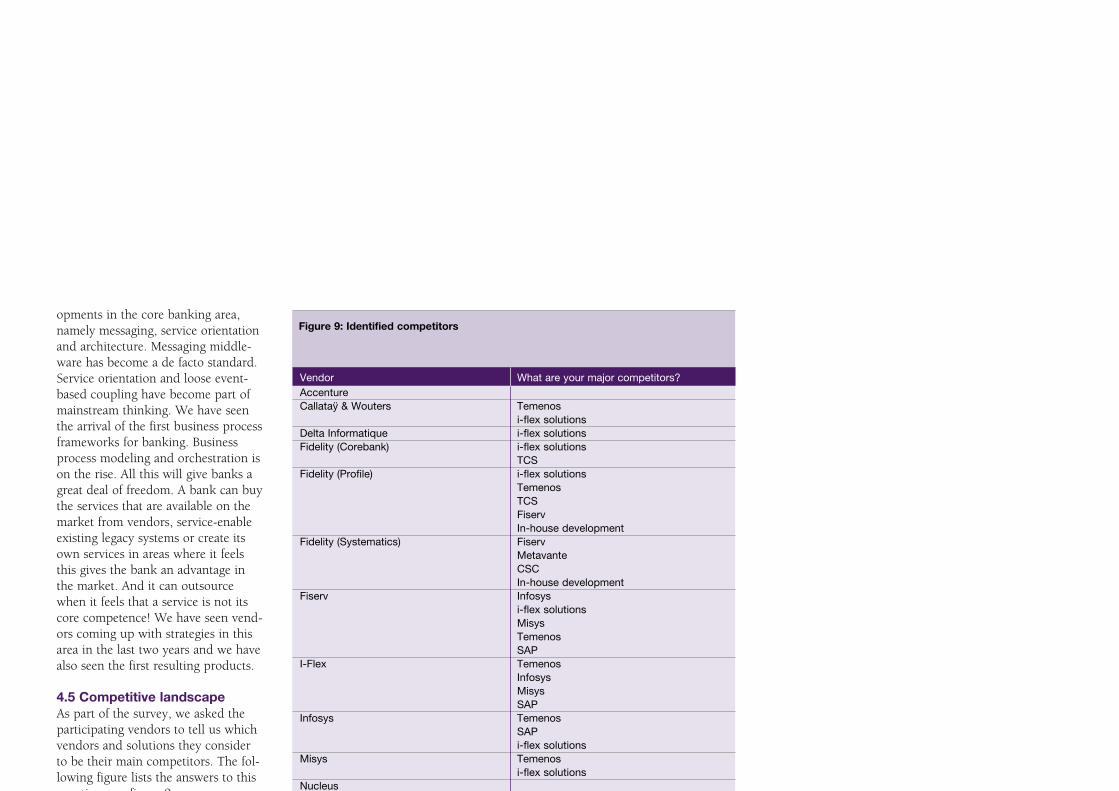

4.5 Competitive landscapeAs part of the survey, we asked the participating vendors to tell us which vendors and solutions they consider to be their main competitors. The fol-lowing figure lists the answers to this question, see figure 9.

4.6 Future of the marketIn the past, there were a large num-ber of specialized solutions in the market. Some were strong in account handling, others strong in wholesale or retail lending and finally there were separate financial accounting solutions. All these packages had their own, proprietary architectural footprints.

Nowadays there seems to be a move towards alignment with the architec-ture stacks and frameworks of the ERP giants SAP and Oracle in this market.

Figure 9: Identified competitors

Vendor What are your major competitors?Accenture Callataÿ & Wouters Temenos i-flex solutionsDelta Informatique i-flex solutionsFidelity (Corebank) i-flex solutions TCSFidelity (Profile) i-flex solutions Temenos TCS Fiserv In-house developmentFidelity (Systematics) Fiserv Metavante CSC In-house developmentFiserv Infosys i-flex solutions Misys Temenos SAPI-Flex Temenos Infosys Misys SAPInfosys Temenos SAP i-flex solutionsMisys Temenos i-flex solutionsNucleus Polaris Temenos i-flex solutionsSAP AG i-flex solutions Temenos In-house developmentSunGard i-flex solutions Temenos Path Solutions (Islamic Banking) Misys TCS InfosysTCS i-flex solutions TemenosTemenos Fidelity Infosys i-flex solutionsTietoEnator T-Systems Kordoba Fiducia

22

Alongside the core banking offerings of the ERP giants (or subsidiaries), most independent vendors are aligning themselves to one of these platforms.

This should deliver the additional bene-fits promised in some of the initiatives of these ERP giants: embedded busi-ness intelligence, integrated customer relationship management, integrated financial accounting and reporting and integrated risk management, regulatory compliance and fraud detection.

So far we have seen Misys and Callataÿ & Wouters deciding on a strategic cooperation with SAP. i-flex solutions obviously aligns itself to the Oracle stack.

Fiserv has integrated business intelli-gence, customer relationship manage-ment, and integrated risk manage-ment, regulatory compliance, and fraud detection, which can be com-bined with financial accounting and reporting capabilities from within the Fiserv group of companies.

Vendor solutions 2�

Figure 10: Best of breed solutions

Domain Vendor Solution

Payments ACI�WorldwideDovetail�SystemsFundtechCBAClear2PayTietoEnator

ACI�Payments�FrameworkDovetail�SystemsGlobal�PayPlusIBASOPFGlobal�Payments�Solution

Lending FidelityMisysSS&CBAIAFSNucleus

ACBSLoan�IQLMS�Loan�SuiteComponent�BankerAFS�Lending�SolutionFinnOne

Securities T-SystemsADP�DSTSS&CSungard

GeosGloss�&�TarotHiPortfolioDifferent�solutionsDifferent�solutions

The Indian pure players have so far chosen to remain agnostic in this respect and have come up with SOA and BPM stacks of their own.

4.7 Specialized ‘best of breed’ solutions

Besides the core banking solutions, there are also some very good special-ized solutions in specific domains. Figure 10 lists some of these in the domains of Payments, Lending and Securities.

� Financial�Services the�way�we�see�it

The four main stages are:■ Make or buy■ Selection■ Implementation■ Operation

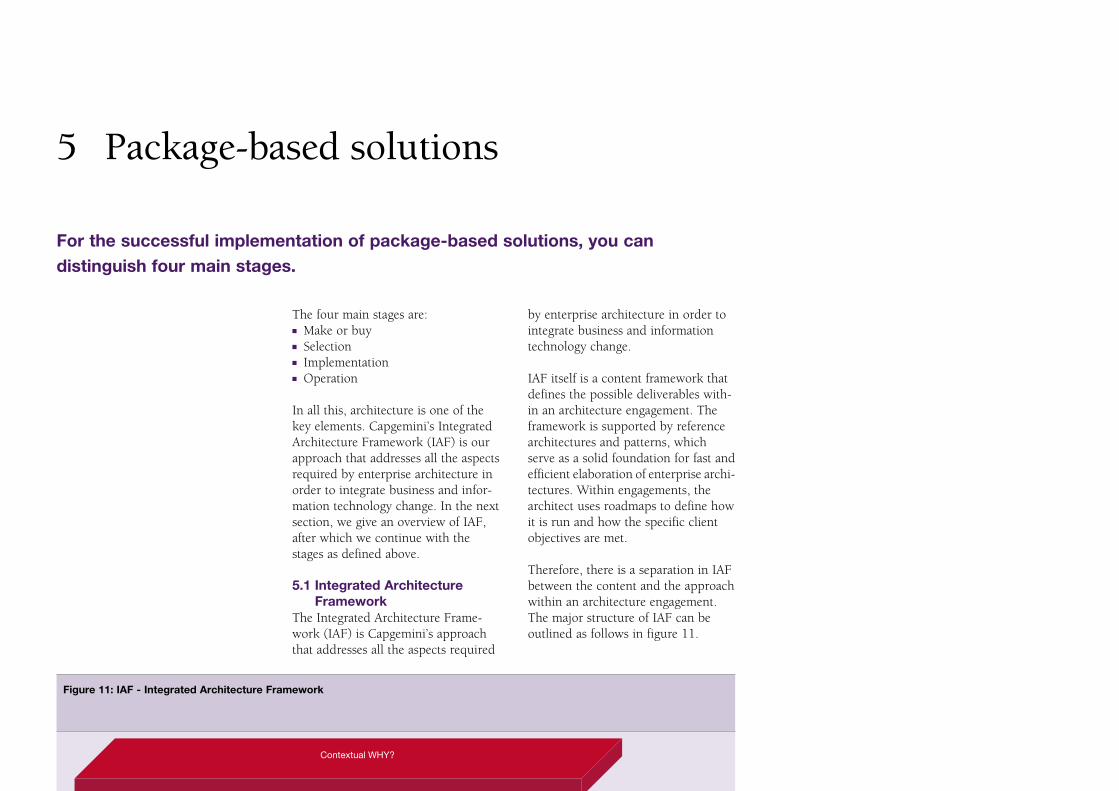

In all this, architecture is one of the key elements. Capgemini’s Integrated Architecture Framework (IAF) is our approach that addresses all the aspects required by enterprise architecture in order to integrate business and infor-mation technology change. In the next section, we give an overview of IAF, after which we continue with the stages as defined above.

5.1 Integrated Architecture Framework

The Integrated Architecture Frame-work (IAF) is Capgemini’s approach that addresses all the aspects required

by enterprise architecture in order to integrate business and information technology change.

IAF itself is a content framework that defines the possible deliverables with-in an architecture engagement. The framework is supported by reference architectures and patterns, which serve as a solid foundation for fast and efficient elaboration of enterprise archi-tectures. Within engagements, the architect uses roadmaps to define how it is run and how the specific client objectives are met.

Therefore, there is a separation in IAF between the content and the approach within an architecture engagement. The major structure of IAF can be outlined as follows in figure 11.

5 Package-based solutions

Figure 11: IAF Integrated Architecture Framework

Artifacts & views Artifacts & views Artifacts & viewsPhysical

WITH WHAT?Artifacts & views

Business TechnologyinfrastructureInformation Information systems

Security

Contextual WHY?

Governance

Artifacts & views

Artifacts & views

Artifacts & views

Artifacts & views

Artifacts & views

Artifacts & views

Artifacts & viewsConceptual

WHAT?

LogicalHOW?Artifacts & views

24

For the successful implementation of packagebased solutions, you can distinguish four main stages.

IAF addresses four architecture aspect areas: Business (B), Information (I), Information Systems (IS), and Techno-logy Infrastructure (TI). An aspect area looks at one system from a specific standpoint. The topics addressed in each of the aspect areas may differ, but there are strong interdependencies between each of the aspect areas. Ideally, all aspect areas must be incor-porated in the architecture design to ensure its usability as a single system; omitting any of the aspect areas intro-duces additional risk.

Developments in business and tech-nology often require special attention to the architecture design. Within IAF this is translated into two specialized views: governance and security. Both specialized views emphasize the quali-ty aspect of the architecture and are selected parts of the aspect areas.

IAF recognizes four levels of abstrac-tion: contextual, conceptual, logical, and physical. The first, contextual, is for answering the ‘why’ question and to provide context information and key principles that support the value proposition for the architecture to be developed.

The benefits of using IAF include:■ The architecture is defined by and

justified in terms of business needs. There is a direct link between the business and its supporting IT. IAF is a key prerequisite for business-IT alignment.

■ The architecture is maintainable, thus maximizing the original invest-ment by the business. It can be used as a basis for capacity planning and control.

■ IAF ensures completeness of the design.

■ IAF reduces the risk of ‘losing requirements’ between the phases.

■ IAF provides an approach for Enter-prise Application Integration (EAI).

■ IAF has proven consistency with the latest software delivery methods such as the Rational Unified Process (RUP).

5.2 Stage 1: Make or buy

A major consideration for banks with a demand for system replacement is whether to build it in-house or buy an off-the-shelf package. Most large banks have until recently preferred the in-house route, on the basis that core banking systems are responsible for the most critical tasks of bank opera-tions and require complete and ulti-mate control by the bank. Therefore, they did not want to rely on vendor solutions for managing accounts and processing transactions.

A bank has several options for its core banking systems, with the most appro-priate option being based on its drivers and the relative effect on its KPIs:

■ Donothingbutcontinuethenor-malmaintenanceonthecurrentsystem(s). For the old legacy systems this means that maintenance costs and risks will increase significantly as time passes, so another decision will normally have to be made in the next few years.

■ Developanewsystemin-house. Although cost and risk may well rule this out, this is still the biggest com-

Make or buy Selection Implementation Operation

Package-based solutions 2�

Making a clear and strategic choice in this phase is essential before entering the package selection phase.

� Financial�Services the�way�we�see�it

petitor, mostly because of the influ-ence of the IT department, and from the end-user perspective the number of changes will be limited. If this alternative is chosen, risks can be mitigated by opting for approaches based on service-oriented architec-ture or model-driven architecture.

■ Procureapackagedsolution. The challenge of this option is to find a packaged solution that is suit-ably scalable and that will integrate into the bank’s technical environ-ment. Plug-and-play packaged solu-tions provide flexibility in product development and deployment and enable lower cost development through buying commoditized devel-opment services from third-party suppliers. Changes in the current processes are unavoidable in order to benefit from the strengths of a pack-aged solution. Choosing a packaged solution makes it possible to take advantage of functionalities devel-oped for other banks. This makes it possible to benefit from these func-tionalities within short timeframes.

■ Outsourcetheservice. The challenges of this option are to integrate with and manage such a service. Outsourcing can offer ways to defray capital costs and reduce risk. Outsourcing can be based on the company’s own solution or a (new) package. The size of the bank is likely to influence which option is preferable. Alignment between own and outsourced processes is essen-tial and they are managed via serv-ice level agreements.

Making a clear and strategic choice in this phase is essential before entering the package selection phase.

5.3 Stage 2: Selection

5.3.1 MethodologyCapgemini’s well-proven system selec-tion methodology has been applied for leading customers in the financial services industry around the world and has minimized the risks involved in system selection. Selecting the right system can make an enormous differ-ence in terms of market offerings and process efficiency.

In this section, we give a brief over-view of Capgemini’s system selection methodology, see figure 12.

Make or buy Selection Implementation Operation

Figure 12: Delivery selection method

Start up

Milestone

Time

Phase 1

Phase 2

Phase 3

Phase 4

Phase 5

Phase 6

Define short list

Evaluate

Validate(optional)

Approved project plan

Approved long list

Approved short list

Preliminary choice

Validated package

Implementation

Confirm and finalise preferred

solutionGo/no go

Focus & direct

2�

It has been developed and continu-ously refined over a number of years as a refinement and adaptation of gen-eral system selection methodologies for the specific needs of the bank and other financial service institutions.The package selection method is used to select a software package that best matches the business needs of the cli-ent. The method supports and objec-tifies decision making with respect to software selection and consists of seven streams and five phases.

The starting point of the method is a business requirement to automate a business functionality by using a stan-dard software package. Standard soft-ware is defined as a software package that is supplied by a software vendor and has 80 percent of the required functionality out of the box. A stan-dard software package may be highly parameterized. Therefore, a large set-up may be necessary to achieve the 80 percent of productive functionality. The method can be used to select one or a combination of software packages.

The selection method is used to devise objective criteria so that the decision process is rationalized. Besides sup-porting the decision making process, the package selection method pre-pares the organization for the imple-mentation of the software package.A properly executed package selection can save a lot of time during imple-mentation of the package!

Start-upThe purpose of the start-up effort is to ensure that sufficient resources are available to the project, so that a clear plan with deadlines is in place, the members of the project team are aware of their responsibilities, and

that there is sound management buy-in to the project.

Focus and directThe focus and direct phase scopes the package selection project, answering the questions as to why the business will start the project, what goals the business will attain, what approach will be used by the project to attain the goals and what the limits of operation of the project are. While the start-up phase has a strong focus on preparing the - organizational - conditions for conducting the project appropriately, the package selection project starts in earnest with the focus and direct phase. The focus is business-oriented, or one might say content-oriented.

Define shortlistIn this phase the project team tries to deliver a shortlist of three to five packages which most closely match the current and future requirements specified by the organization. After a long list of packages has been drawn up, with the aid of the Capgemini packages database, a Request for Information (RFI) is sent to these vendors. Based on the answers to the RFI, a shortlist is drawn up which will serve as the basis for the remainder of the selection process.

EvaluateThis phase provides the package eval-uation process. During this package selection phase, the project team will conduct a thorough review and analy-sis of several potential short-listed software tools which meet the client’s business requirements and enable the desired business processes. This phase ends with one preferred potential soft-ware tool which meets the client’s business requirements.

Package-based solutions 2�

� Financial�Services the�way�we�see�it

port in the future. It is essential to select a system that not only supports the current situation, but also allows the organization to respond to future market demands and change its value proposition and customer experience accordingly.An important aspect is the choice of an integrated system or a ‘best of breed’ infrastructure. Smaller institutions will often have a preference for integrated systems. A well-chosen system pro-vides all the necessary functionality, causes not too much trouble with interfacing and innovation, and is supported by the vendor. Large and sophisticated banks, however, will opt for a ‘best of breed’ infrastructure. No single system totally covers their requirements, so they have to choose specific software components for spe-cific functionalities.

A solid architectural basis is key in these cases. These infrastructures intro-duce the need for a middleware com-ponent. This is vital, since it reduces the interfacing issues to a minimum and guarantees flexibility in a complex environment, see figure 13.

2�

ValidateIn the validate phase, the package solution will be tested in full practice. The provider will have to install the system in a client’s test environment. The reason for doing this is to elimi-nate the final uncertainties. In the previous phase, a short valida-tion of the package is included as part of the package selection. This short validation may be a proof of concept in which specific functionality is test-ed. This test is included to ensure that the package can be parameterized or extended to support the required functionality. This short test is not used to test all functions of the pack-age. The validate phase is included for the checking of all functions. To start this phase, the client signs a letter of intent. In this letter of intent he declares that he will purchase the package subject to a positive valida-tion in this phase.

This validation phase is optional. In most situations, all the information gathered in combination with a short proof of concept in the evaluation phase will be sufficient to reach a decision.

Confirm and finalize the preferred solutionThe objective of this phase is to get the final sign-off of the package selec-tion project. With this sign-off the cli-ent agrees to the solution as advised by the project team.

5.3.2 Integratedor‘bestofbreed’The selection of a core banking sys-tem is a strategic decision with long-term implications. The future business vision needs to be established in order to determine what business setting the new banking system will have to sup-

The selection of a core banking system is a strategic decision with longterm implications.

Figure 13: ‘Best of breed’ or integrated solution

Best of breed(multiple systems)

Integrated solution(one system)

Pros Advanced�functionality No�interfaces�in�the�transaction�flow

Switching�parts�of�the�systems�architecture�gives�lower�costs

Makes�reporting�easier�across�the�transaction�flow

Less�dependence�on�one�vendor Easier�maintenance�of�databases

Cons Implementation�and�maintenance�is��complicated Does�not�cover�all�functionality�requirements

Multiple�databases�often�cause��inconsistent�data

Specialized�systems�outside�transaction�flow�might�be�inevitable

Overall�higher�costs�for�licenses Replacing�the�complete�system�architecture�results�in�higher�costs

Vendors�have�to�cooperate�during�implementation

5.3.3 SelectioncriteriaSystem selection does not mean choos-ing a system with the most extensive functionality. It is a dynamic process in which different selection criteria must be matched with existing and future business processes and system architectures. There should be a match between the business processes, the system and the organization.

The system selection process must be driven primarily from a business per-spective, rather than being treated as a choice between change and improve-ment of the current state. Any emo-tional bias towards an existing solu-tion will introduce hidden variables that influence the decision.

VendorSelecting a core banking solution should not be a tactical, point-driven, decision making effort. It is entirely strategic and vital to the long-term health of the bank. The viability of a vendor is therefore a crucial element in the search for a replacement sys-tem. Analyze a vendor’s viability, not just in terms of financial stability, but also by scrutinizing technical compe-tence, development capability, quality of support, marketing and sales reach, alliances and partnerships, and man-agement performance.

Support and ServicesPart of selecting the right vendor is having a good understanding of the support and services a vendor pro-vides during the implementation proj-ect and once the solution is in produc-tion. What is the release and upgrade strategy? How are new requirements incorporated in the solution? What types of consultants are available dur-ing the implementation project?

Implementation and migrationOne of the most compelling areas of a bank’s analysis lies in the implementa-tion practice of the vendor. Failure to perform due diligence regarding ven-dor project management capabilities has the potential to drive implementa-tion costs exponentially and dispirit bank staff.

It is vital to talk with a vendor’s cus-tomers to gain ‘real world’ experienc-es. Vendors will have their targeted list of references for use in the sales cycle. It is important to talk with banks that have similar profiles - how they use the system and matching scale - to gain a more balanced per-spective. However, be aware that the banks on these lists often receive pref-erential treatment from the vendor.

Functional aspectsFunctionality is the most important cri-terion in the system selection process. When evaluating a system’s functional-ity in relation to the needs of the bank’s business, it is imperative to con-sider not only the current needs and functionality, but also future needs, as well as the vendor’s policy towards upgrades, changes, and additions. Functional aspects vary between finan-cial institutions with different strategies and different commercial activities.

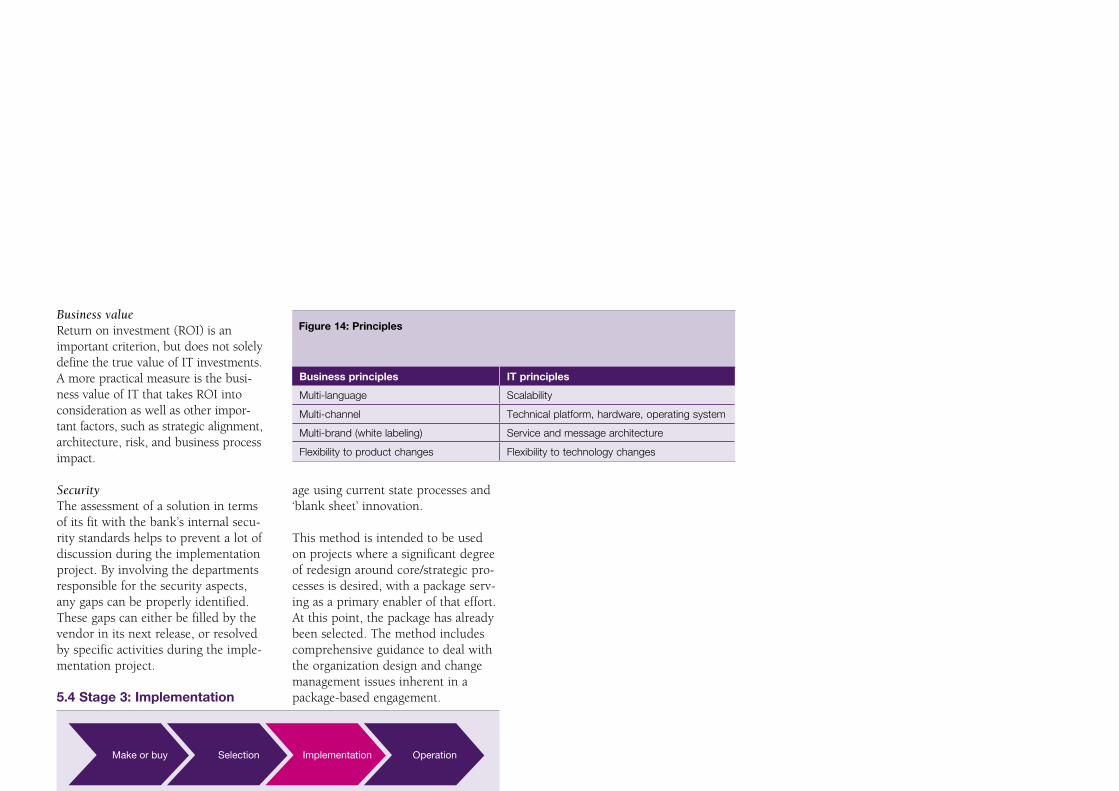

Technical aspectsThe organization’s existing technical infrastructure and capabilities limit the choices. Adding new components to an existing technical architecture can substantially influence operational and maintenance costs. Technical pre-conditions for the selection process, based on IT and business principles, can be defined in the terms as shown in figure 14.

Package-based solutions 2�

� Financial�Services the�way�we�see�it

Business valueReturn on investment (ROI) is an important criterion, but does not solely define the true value of IT investments. A more practical measure is the busi-ness value of IT that takes ROI into consideration as well as other impor-tant factors, such as strategic alignment, architecture, risk, and business process impact.

SecurityThe assessment of a solution in terms of its fit with the bank’s internal secu-rity standards helps to prevent a lot of discussion during the implementation project. By involving the departments responsible for the security aspects, any gaps can be properly identified. These gaps can either be filled by the vendor in its next release, or resolved by specific activities during the imple-mentation project.

5.4 Stage 3: Implementation

5.4.1 MethodologyTo implement the package on a solid basis, the best option is to use a struc-tured approach based on best practices. Capgemini offers an implementation method and a multi-site implementa-tion framework, which can also be combined.

RAPIDThe Redesign through Application Package Iterative Development (RAPID) method resides between the extremes of just implementing a pack-

age using current state processes and ‘blank sheet’ innovation.

This method is intended to be used on projects where a significant degree of redesign around core/strategic pro-cesses is desired, with a package serv-ing as a primary enabler of that effort. At this point, the package has already been selected. The method includes comprehensive guidance to deal with the organization design and change management issues inherent in a package-based engagement.

RAPID strives to accelerate the speed to value by focusing the redesign effort on those processes that will yield the greatest value to the organi-zation while adopting the package processes in non-core/strategic areas. The business case serves as the benchmark by which ‘value’ is mea-sured. Key project decisions should be evaluated based on their quantita-tive benefit versus qualitative opin-ions on what is critical to the organi-zation.

Figure 14: Principles

Business principles IT principles

Multi-language Scalability

Multi-channel Technical�platform,�hardware,�operating�system

Multi-brand�(white�labeling) Service�and�message�architecture

Flexibility�to�product�changes Flexibility�to�technology�changes

�0

To implement the package on a solid basis, the best option is to use a structured approach based on best practices.

Make or buy Selection Implementation Operation

RAPID draws on leading practices, innovative deliverables, and lessons learned from our most successful ERP projects to improve quality and accel-erate results. There are several Capgemini differentiators that have been included in RAPID to ensure the solution provides speed, value, and quality. Some of the major areas are noted below:■ Accelerated Workshops: the method

recommends the use of Accelerated Workshops to improve the speed and quality of the project. These ses-sions provide a major differentiator as compared to all our competitors, and can accelerate the time to the first go live. This unique approach dramatically accelerates the project, compressing months of work into days of intensely focused effort.

■ Development Centers: we strongly urge all projects to utilize our off-shore Delivery and Development Centers to accelerate our time to deliv-ery. Using offshore centers also pro-vides a reduced cost for the project.

■ Project Management Method: our project management method is a complete end-to-end project man-agement method. Within RAPID, all activities that have been identified as project management activities are

Package-based solutions �1

linked directly with the project management method, see figure 15.

To conclude, through RAPID, Capgemini offers the following key benefits in implementing packaged solutions:■ RAPID is a comprehensive and well-

tested route map covering all aspects of a large package implementation, where the package is seen as an ‘enabler’ of business change.

■ The main characteristic of RAPID is its business-oriented approach towards large-scale IT projects, ensuring that business goals are used as a yardstick of success throughout the engagement.

■ RAPID integrates people, processes, and technology aspects within its main phases of solution definition, solution development, and imple-mentation.

■ RAPID ensures process innovation and improvement and reduces delivery time and risk.

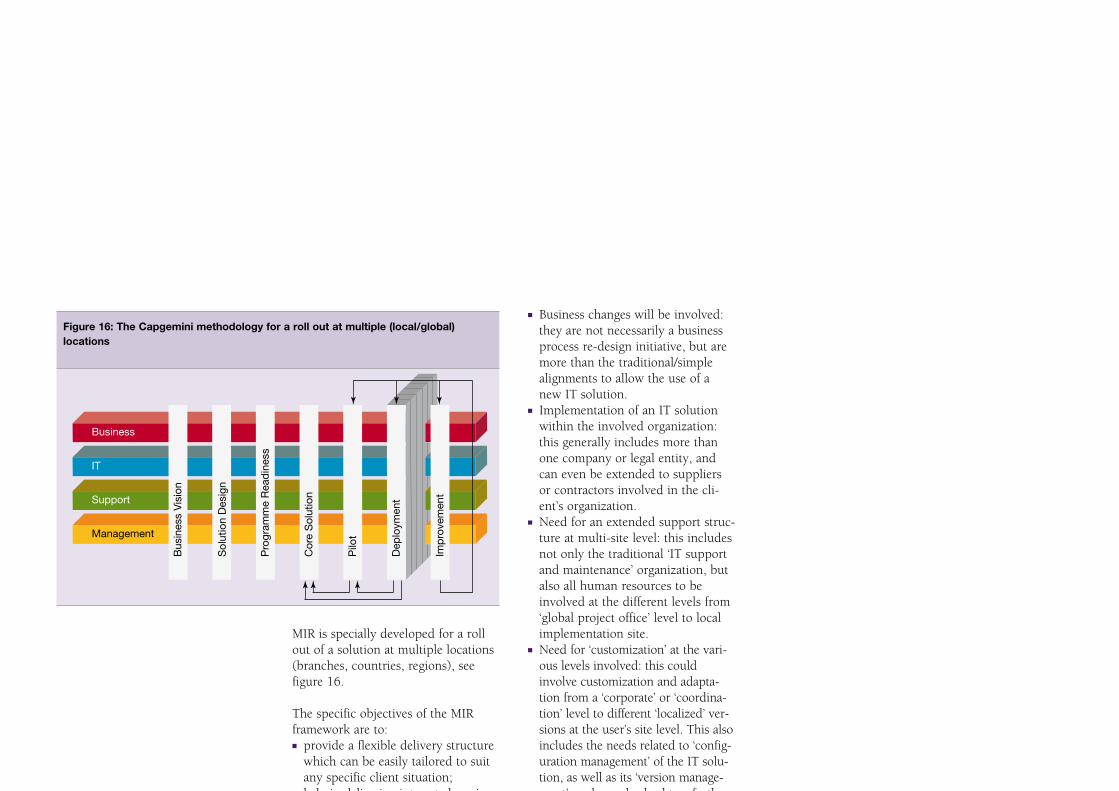

MIRThe objective of a Multi-site Implementation and Roll out (MIR) initiative is to enable an organization to adopt a consistent approach to its business processes, by delivering real business benefits through the con-trolled implementation of a common enterprise system to multiple locations within a business sphere of influence.

The Multi-site Implementation and Roll out framework is used when a package or a specific solution needs to be implemented at a number of sites (international or otherwise) within an organization. MIR is Capgemini’s serv-ice offering to manage such large-scale programs, regardless of the type of system implemented.

Figure 15: The Capgemini methodology for a package implementation

Project management

Build-to-run transition

Projectinitiation

Solutiondefinition

Solutiondevelopment

Implemen-tation

Post-Implemen-tation support

RAPID

� Financial�Services the�way�we�see�it

MIR is specially developed for a roll out of a solution at multiple locations (branches, countries, regions), see figure 16.

The specific objectives of the MIR framework are to:■ provide a flexible delivery structure

which can be easily tailored to suit any specific client situation;

■ help in delivering integrated services; ■ lower risk of failure; ■ provide a platform for operating

units to share and leverage best practices to support the framework.

An important part of this method is a pilot in one location and, after improvement, a roll out to the other locations. Implementation features to define a MIR initiative include:■ Multi-site implementation: not nec-

essarily international, but ten or more sites at different levels from upper ‘global’ or ‘coordination’ level to ‘local’ or ‘user’s site’ level.