Copyright © NASSCOM 2008 HOW IS THE INDIAN IT-BPO INDUSTRY FACING THE CURRENT GLOBAL UNCERTAINTIES...

28

Copyright © NASSCOM 2008 HOW IS THE INDIAN IT-BPO INDUSTRY FACING THE CURRENT GLOBAL UNCERTAINTIES ? Ameet Nivsarkar, Vice President, NASSCOM October, 2008

-

Upload

marylou-dawson -

Category

Documents

-

view

216 -

download

1

Transcript of Copyright © NASSCOM 2008 HOW IS THE INDIAN IT-BPO INDUSTRY FACING THE CURRENT GLOBAL UNCERTAINTIES...

Copyright © NASSCOM 2008

HOW IS THE INDIAN IT-BPO INDUSTRY FACING THE CURRENT GLOBAL UNCERTAINTIES ?

Ameet Nivsarkar, Vice President, NASSCOMOctober, 2008

Copyright © NASSCOM 2008

About NASSCOM

2

NASSCOM is the apex body for the IT-BPO sector in India and plays a leading role in the areas of trade development, policy

advocacy and research

Over 1200 members including 250 global companies

Membership accounts for over 90% of exports and a majority of the 2 million professionals employed in the sector

Trade Development

Assisting members explore new markets and business opportunities

Facilitating effective trade development at national and international forums

Nurturing the growth of the small and medium enterprises

Policy Advocacy

Active proponent of global free trade, proactively engaging with policy makers, government and other influencers to

provide guidance and informational support

Committed to encouraging its members to adopt world class management practices, build and uphold highest standards

in quality, security and innovation

Research and Thought-leadership

Acknowledged as the primary source of information about Indian IT-BPO

Prominent role in voicing developmental challenges and devising their solutions – not just for the sector but the country at

large

NASSCOM’s Charter: To build India as the 21st century’s technology powerhouse and establish India as the global sourcing hub for IT-BPO services and software

Copyright © NASSCOM 2008

Current Global Uncertainties

Signs of US Slowdown post sub-prime and wall street

crisis; impact on other economies

Economic instability

Oil crisis, food prices, inflation, unstable currencies,

volatility in stock markets etc.

Concerns over US election; forthcoming Indian

elections

Constraints within India on talent, infrastructure etc.

3

Copyright © NASSCOM 2008

Positive growth in FY08 under clouds of uncertainty

4

FY04 FY05 FY06 FY07 FY08

21.6

28.5

37.4

48.1

64.03.6%4.1%

4.7%5.2% 5.5%

32%

31%

29%

28%*

US$ billion, percentage

Indian IT-BPO SectorRevenue Aggregate and Share of GDP

Exports

Domestic

Percentage of GDP

• Sustained export growth – revalidates strong fundamentals

• Revenue aggregate as a percentage of GDP continues to rise

Source: NASSCOM

* Domestic Revenue Adjusted for Currency

Copyright © NASSCOM 2008

0.5

4.9

8.4

18.0

0.5

6.4

10.9

23.1

Hardware

Product Dev and Engg Services

BPO

IT Services

FY2008

FY2007

All segments grew well in FY 08

5

100% = US$ 64 billion

DomesticMarket

Exports 62-66%

34-38%

*Includes product development and engineering ** Negligible

12%

18%

70%

40%

27.5%

32%

28%

Sourcing model

BPO

IT*

Global CaptivesGlobal Providers

Indian Providers

**

29%

30%

28%

Source: NASSCOM Source: NASSCOM

YOY growth

Copyright © NASSCOM 2008

Growth continued in Q1

6

June 07 Sep 07 Dec 07 Mar 08 Jun 08400

600

800

1000

1200

1400

1600

Revenues

TCSInfosysWiproSatyam

Reve

nues

Diversification driving revenue momentum• Europe, Middle east, APAC• Manufacturing, retail, healthcare• BPO, testing

USD Mn.

Copyright © NASSCOM 2008

61%

18%

12%

6%

2%

Geographical spread diversified

7

US

UK

Continental Europe1

APAC2

ROW

100% = US$ 31.4 billion*

30%

US

UKContinental

Europe

APAC

43%

>55%

36%

Percentage

FY2007

CAGR FY2004-07FY2007FY2004

Indian IT-BPO Exports grew at a CAGR of 35% over FY2004-07

• Excludes hardware exports1 Top 3 countries include Germany (~2.5%), Netherlands (~2%), Switzerland (~1%) 2 Top 3 countries include Australia (~1.5%), Japan (~1.5%), and Singapore (~1.3%)

Europe, APAC and Middle East markets growing rapidly

Source: NASSCOM

Copyright © NASSCOM 2008

• Banking, Financial Services, Insurance and Hi-tech / Telecom account for nearly 60% of Indian IT-BPO exports

• Manufacturing and retail are other large sectors

• Airlines, media, healthcare and utilities are some emerging high-growth sectors

New verticals reduce dependency

8

FY2007

* Excludes hardware exports

Vertical market exposure for industry exports is well balanced across several mature and emerging sectors

BFSI40%

Hi-tech / Telecom19%

Manufacturing15%

Retail8%

Media, Publishing and Entertainment

3%

Construction and Utilities4%

Healthcare3%

Airlines and Transportation

3%Other

5%

Source: NASSCOM

Copyright © NASSCOM 2008

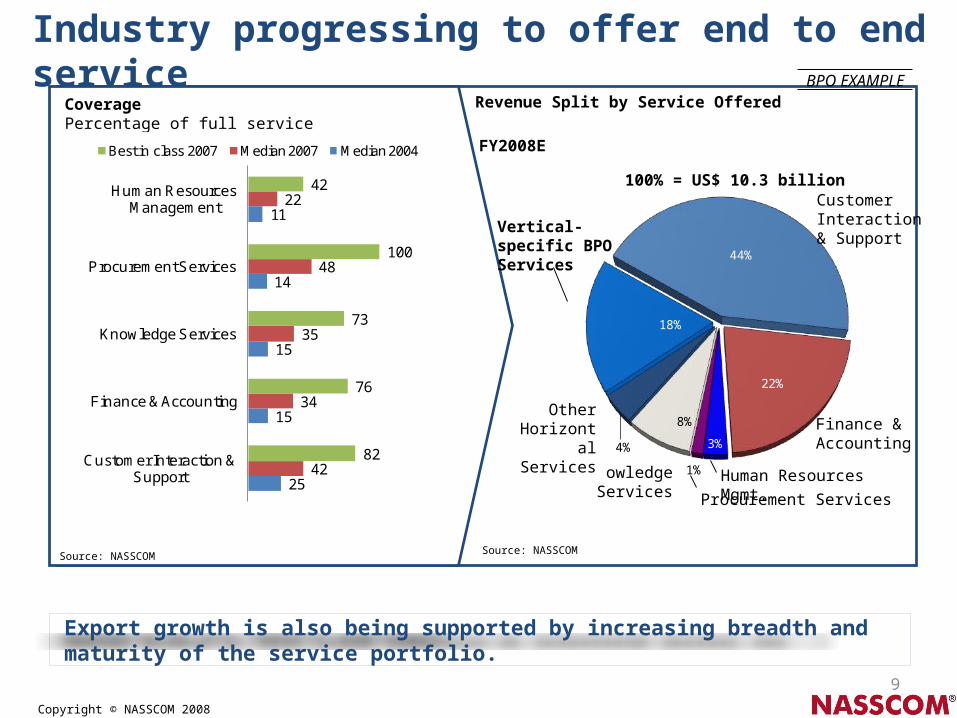

Industry progressing to offer end to end service

9

CoveragePercentage of full service

Revenue Split by Service Offered

FY2008E

Export growth is also being supported by increasing breadth and maturity of the service portfolio.

44%

22%

3%

1%

8%

4%

18%

Customer Interaction & Support

Finance & Accounting

Human Resources Mgmt.

Procurement Services

Knowledge Services

Other Horizontal

Services

Vertical-specific BPO Services

100% = US$ 10.3 billion

BPO EXAMPLE

25

15

15

14

11

42

34

35

48

22

82

76

73

100

42

Customer Interaction & Support

Finance & Accounting

Knowledge Services

Procurement Services

Human Resources Management

Best in class 2007 Median 2007 Median 2004

Source: NASSCOMSource: NASSCOM

FY09 outlook: Software and services revenue to grow by 21-24%; exports to reach $50bn

• FY09 software and services growth forecast 21-24% (USD)

• Recent reversal in INR appreciation trends provides an extra cushion, if sustained it will contribute to higher INR growth

• Increased focus on cost and productivity in the recessionary environment is likely to fuel demand for offshore services

• Domestic story remains strong, though sustained inflation may be a medium-term risk

10

$39.6

Source: NASSCOM

$62-64

$52.0

Figures may vary slightly due to rounding off

USD Billion

INR/USD 44.9 40.2 43

Growth of 21-24%(Currency Adjusted)

Copyright © NASSCOM 2008

Key drivers of growth in FY 09

11

The Indian IT-BPO industry is actively building on its leadership position to deliver beyond cost benefits to global buyers

0

20

40

60

80

100

2004 2007

Key benefits driving companies to offshore

Pe

rce

nta

ge

of

resp

on

ses

Cost Savings

Process redesign

Speed to market

Access to Skills

Source: Duke Offshoring Research Network (ORN)

Global delivery model

Innovation

Process maturity

• Expansion of delivery network to include nearshore and onshore centres

• Provision of 24x7 services

• End-to-end process delivery capabilities

• Active service-level improvement

• Process reengineering expertise

• Service innovation e.g., customization for new markets

• Active IP creation – increased filing of patents

Key value-add initiatives

Copyright © NASSCOM 2008

1.1

1.6

5.5

8.0

1.6

2.2

7.9

11.5

BPO

Software

IT Services

Hardware

FY2008EFY2007

Domestic Market continues to show traction

12

DomesticMarket

Exports 62-66%

34-38%

Domestic market is gaining momentum, driven by overall economic growth, increased adoption of technology and outsourcing

100% = US$ 64 billion

• Rapid economic growth

• Increased consumption of goods and services

• Growth in tech-related spends by enterprises

• Internet connectivity

Source: NASSCOM

44%

38%

43%

44% 29%

23%

29%

30%

USD INR

Growth in*

* Difference between growth in USD and INR due to impact of forex changes (INR appreciation)

Copyright © NASSCOM 2008

Tightening the belt

Wake up call 10 months ago when USD touched Rs. 39

Focus on productivity, efficiency, resource utilization

Wage moderation, reduced lateral hiring, reduced attrition

More efficient asset utilization – real estate, IT etc

Expansion into tier 2/3 cities

Domestic market and new markets

These improvements will have lasting impact over

years!

13

Copyright © NASSCOM 2008

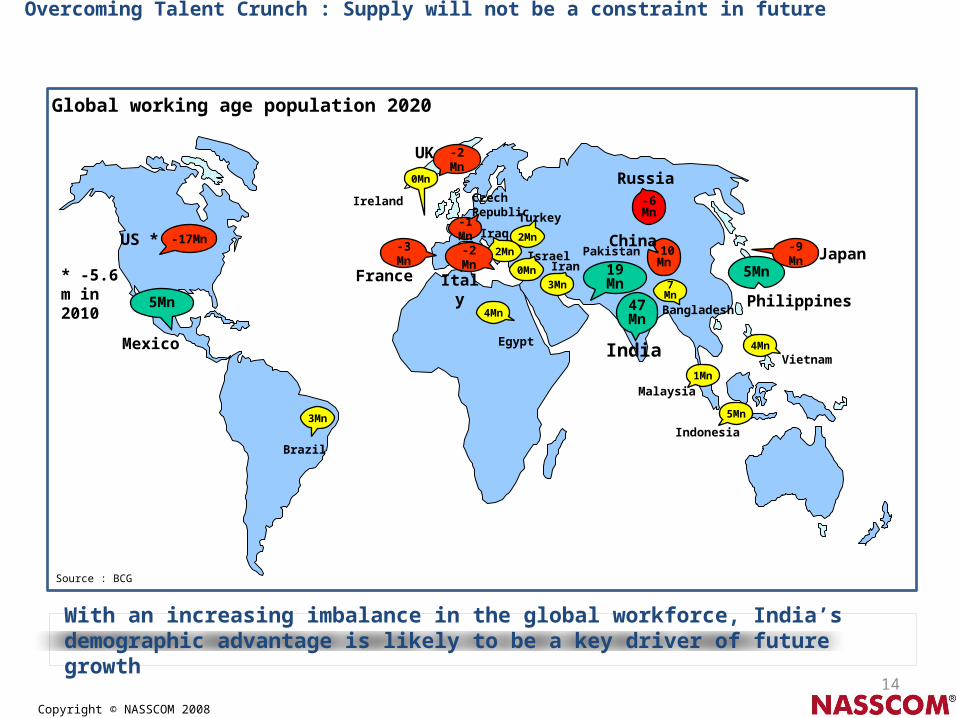

Overcoming Talent Crunch : Supply will not be a constraint in future

14

Source : BCG

47Mn

19Mn 7

Mn

3Mn

5Mn3Mn

India

Bangladesh

PakistanIran

Brazil

Mexico

Philippines

5Mn

4MnVietnam

2Mn

Turkey

-10Mn

China

-6Mn

Russia

5Mn

Indonesia

1Mn

Malaysia

0Mn

Ireland

Israel0Mn

Iraq

2Mn

-1Mn

CzechRepublic

4Mn

Egypt

-17MnUS *

-2 MnUK

-2 Mn

Italy

-3 Mn

France

-9 Mn Japan* -5.6 m in 2010

Global working age population 2020

With an increasing imbalance in the global workforce, India’s demographic advantage is likely to be a key driver of future growth

Copyright © NASSCOM 2008

Cost Competitiveness is sustainable

15

Despite cost increases, India continues to leverage its cost structure to deliver a compelling cost advantage. Additionally, India’s long-term cost advantage is likely to remain robust.

Loaded Costs per IT FTE p.a.2007, US$ ‘000s

Source: Everest, NASSCOM

2007 2008 2009 2010 2011 2012 2013 2014 2015

India @ 28K

US @ 100K

~67

%

~60

%

~53

%

~72

%

Cost Saving

Projected cost comparison, 2007-2015 US$

CAGR increases

@ 3%

Wage @ 15% Other @ 5%

Wage @ 10% Other @ 5%

Wage @ 5% Other @ 5%

Source: NASSCOM estimates

Copyright © NASSCOM 2008

Comprehensive Plan for making India’s large talent base “employable”

16

Recognizing this imperative, the industry is proactively working on several initiatives to strengthen India’s long-term cost advantage

Short Term

Medium Term

Long Term

• Enhance overall yield• Improve employability• Expand to tier 2

locations• Lower skill dependence

Objectives Initiatives

• Industry to enhance investments in training • Entry-level assessment for BPO and IT,

finishing schools : Through NAC, NAC-Tech• New locations identified; govt’s engaged

• Lower training investment

• Enhance specialist and project management expertise

• Add education capacity• Promote education

reform

• Faculty Development Program: to increase the suitability of teachers

• Facilitating industry access to specialist programs offered by independent agencies

• Expansion of higher-education infrastructure: government to set-up 20 new IIITs

• Program to increase PhDs in technology• NASSCOM VC fund focused on technology

innovation

Copyright © NASSCOM 2008

Information Security & Risk Management

Standards

Physical security

Personnel security

• Compliance with global standards e.g., ISO 27001, CoBIT

• Contractual safeguards, robust BCP/DR planning

Network security

Laws

• Secure design, documentation & implementation of network e.g., firewall, antivirus encryption

• Isolation of sensitive areas• Access control systems e.g., CCTV

surveillance, security guards

• Background checks• Non-disclosure agreements

• Compliance with international laws• Strengthening of Indian legal system

• Maximum ISO 27001 certifications obtained globally

• Data Security Council of India formed

• Documented security policies covering use of information, mobile computing, user access

• Robust and uniform best practices

• National Skills registry (NSR) to facilitate personnel background checks

• Cyber security training and awareness

• Amendments to strengthen the IT Act 2000 and Indian Penal Code being enacted

Objectives Initiatives/Impact

The NASSCOM 4 E model for trusted sourcing – Engagement, Education, Enactment and Enforcement is being proliferated.

17

Copyright © NASSCOM 2008

43 tier 2/3 Delivery locations identified

18

Bangalore 36%

Mumbai, Pune

15%

Chennai 15%

New Delhi, Noida, Gurgaon

17%

Hyderabad 14%

The industry is well spread across multiple locations. Tier 2/3 cities emerging

Others 3%

Source: NASSCOM

Leader Cities

New Emerging Cities

• 7 centers account for over 95% of exports• 43 tier 2/3 cities emerging; will reduce

pressure on these centers• On an average, costs in tier 2/3 cities is

28% less than leader cities• By 2018, it is forecasted that 40% of IT-

BPO exports will originate from non-leader locations

Employment Distribution Amongst Location Categories (‘000s)

1,996

8,0742

Non-Leader

Leader1

CAGR

40%

60%

34%

10%

>18X

>2.5X

Note: 1. Leader locations are Bangalore, Chennai, Hyderabad, Kolkata, Mumbai, NCR (Delhi, Noida, Gurgaon, Faridabad), Pune 2. Assuming a conservative growth in employment at 15% CAGR over next decade

Copyright © NASSCOM 2008

Key Messages

Nuclear deal has improved US and Global confidence about

India and has helped remove some uncertainty

However, WTO stance has not helped global perception

Security instances also cause for concern

Diversification is working well for Indian IT-BPO companies India’s value proposition is sustainable Operational efficiencies will have a lasting effect

The next 2-3 Quarters may be challenging, but the long term growth path is intact

19

Copyright © NASSCOM 2008

Trade development activities

Copyright © NASSCOM 2008

Intensity Map

Outreach Community Catalyst •US

• H-1 B • Anti outsourcing • Totalization • Image management • Messaging • Think tanks • Analysts • PR • Security

•UK• Immigration • Trade • Security

•EU • Blue card • Think tanks • Security

•Various agencies worldwide

•Increased relations with Embassies & trade missions

•Indian embassies overseas

•Associations

•Inward delegations •Outward delegations

•Overseas councils / chapters / forums

•Country desk •Website

•Customer and analyst meets

•Global competition

•New market development

•WTO •FTAs

•Government support • MEA • MOIA • Commerce

Copyright © NASSCOM 2008

Country Focus

Market Focus Partner Focus Competition Watch•US •UK •EU

• France • Germany • Netherlands • Spain • Italy

•Scandinavia• Finland • Norway • Sweden

•Ireland •Switzerland •APAC

• Australia • Japan • Korea

•South Africa

•APAC• Malaysia • Philippines • Vietnam

•Eastern Europe• Hungary • Romania • Poland • Czech Republic

•Latin America• Brazil • Mexico

•Egypt

•China

Copyright © NASSCOM 2008

Key observations - US• H-1 B issue

– Strong emotions– Resolution unlikely in the medium term– White paper completed and widely circulated

• Permanent visas– Good support across the board– 3 key bills on table– Will reduce H-1 B pressure

• Totalisation– Progress being seen

• WTO and Trade – India’s role

• Image– Very strong perception across board that Indian companies are misusing the system

• Providing cheap labour • Not taking enough efforts to recruit locally

– Lack of understanding on the role Indian companies play, “job shop” image exists.– Perception that Indian companies are gaming the system, law being followed but not in

spirit and original intent – Rapid improvement required

Copyright © NASSCOM 2008

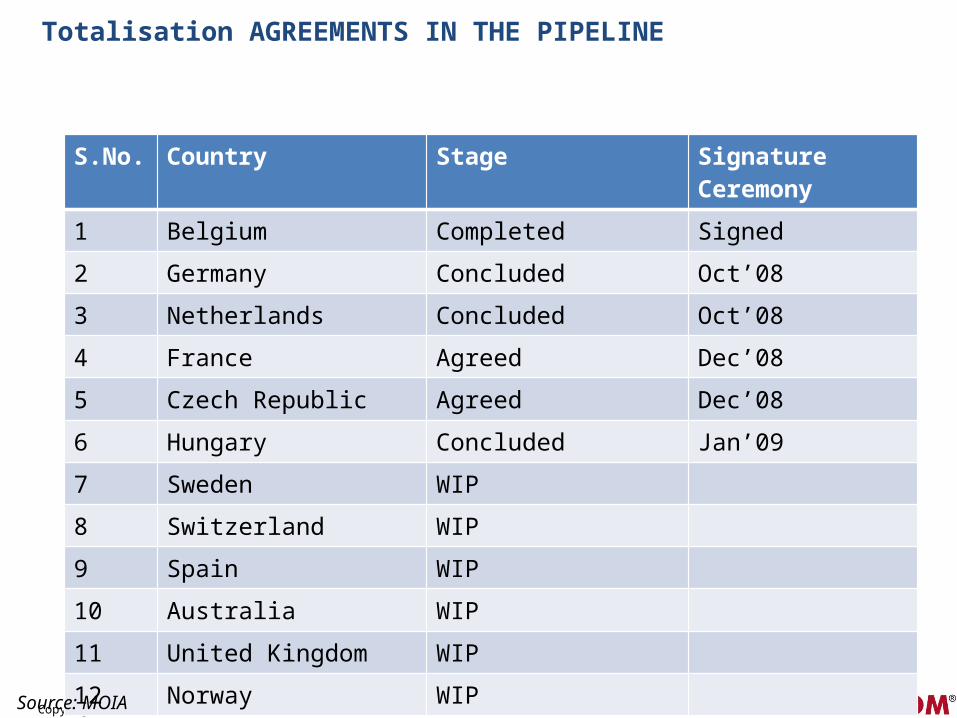

Totalisation AGREEMENTS IN THE PIPELINE

S.No. Country Stage Signature Ceremony

1 Belgium Completed Signed

2 Germany Concluded Oct’08

3 Netherlands Concluded Oct’08

4 France Agreed Dec’08

5 Czech Republic Agreed Dec’08

6 Hungary Concluded Jan’09

7 Sweden WIP

8 Switzerland WIP

9 Spain WIP

10 Australia WIP

11 United Kingdom WIP

12 Norway WIP

Source: MOIA

Copyright © NASSCOM 2008

Key observations - UK

• India is seen as a partner, second largest investor in the UK

• In excess of 50% of ICTs and Work Permits are Indian companies

• NASSCOM, considered an ally by the Govt• New PBS system goes live from Nov 24, 2008• Onus and thus responsibility lies on the

employer

Introduction of PBS• Comprehensive paper circulated• New system goes live on 24th Nov’08 • Onus of registration and issue of work permit is on employers

Employer files application for license with home office,UKBA

Submits all necessary documents to home office

Home office inspects & processes application (5-6

weeks) and assigns rank as A or B

Employer Obtains Licence to Sponsor

Employer does necessary background checks for employee

Qualifies/Allots him rating per PBS. (min 60 points needed for

qualification)

Logs on to online sponsorship management system &

generates certificate numberSends reference number (valid for 3 months) to the employee

Employer obtaining license to sponsor migrants in UK

Employer obtaining license to sponsor migrants in UK

Qualifying employee on PBS & generating sponsorship certificate

Qualifying employee on PBS & generating sponsorship certificate

Work permit issued to the employee with permission to enter

Work permit issued to the employee with permission to enter

1

2

3

Copyright © NASSCOM 2008

New Markets

• Focusing on markets other than the US and UK for industry growth– Combination of Research, outreach and policy level interaction with key markets

• Countries identified– Japan– Nordic - Scandinavian countries (Denmark, Sweden, Finland, Norway) – Benelux (Belgium, Netherlands, Luxemburg)– German speaking countries in the EU – France– Middle East (Oman, Saudi Arabia, UAE, Bahrain, Kuwait)

• The first activity initiated is on Japan – Visit completed, meeting concerned stakeholders– Action items identified– Research report along with PWC being released titled – “How to crack the Japanese

maze”, covering –

• Current state of Japanese marketplace • Opportunities that Japan offers for Indian IT industry• Obstacles which make it a difficult market for industry• Key winning strategies • Competitive overview

Copyright © NASSCOM 2008

Thank You !

28