Copyright © 2011 Nelson Education Limited Finance for Non-Financial Managers, 6 th edition...

26

Copyright © 2011 Nelson Education Limited Finance for Non-Financial Managers, 6 th edition PowerPoint Slides to accompany Prepared by Pierre Bergeron, University of Ottawa

-

date post

21-Dec-2015 -

Category

Documents

-

view

223 -

download

0

Transcript of Copyright © 2011 Nelson Education Limited Finance for Non-Financial Managers, 6 th edition...

Copyright © 2011 Nelson Education Limited

Finance for Non-Financial Managers, 6th edition

PowerPoint Slidesto accompany

Prepared by Pierre Bergeron, University of Ottawa

Copyright © 2011 Nelson Education Limited

Finance for Non-Financial Managers, 6th edition

CHAPTER 12

BUSINESS VALUATION

Copyright © 2011 Nelson Education Limited

Business Valuation

Chapter Objectives

1. Differentiate between market value and book value.

2. Discuss the various valuation models.

3. Comment on the meaning of scanning the environment.

4. Explain how to go about documenting planning assumptions.

5. Show how to restate the statement of income and the statement of financial position.

6. Present the various ways of price-tagging an on-going business.

7. Calculate the market value of publicly-traded companies.

8. Calculate investment return on capital projects from an investor’s (venture capitalist) perspective.

Chapter Reference

Chapter 12: Business Valuation

Copyright © 2011 Nelson Education Limited

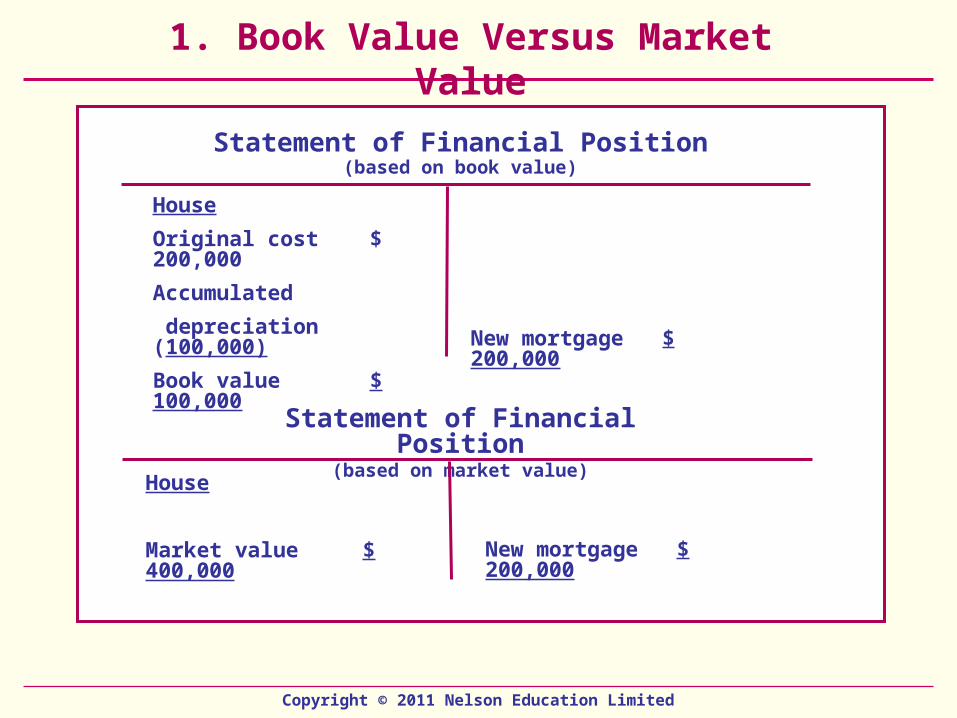

1. Book Value Versus Market Value

Statement of Financial Position(based on book value)

Statement of Financial Position(based on market value)

House

Original cost $ 200,000

Accumulated

depreciation (100,000)

Book value $ 100,000 New mortgage $ 200,000

House

Market value $ 400,000 New mortgage $ 200,000

Copyright © 2011 Nelson Education Limited

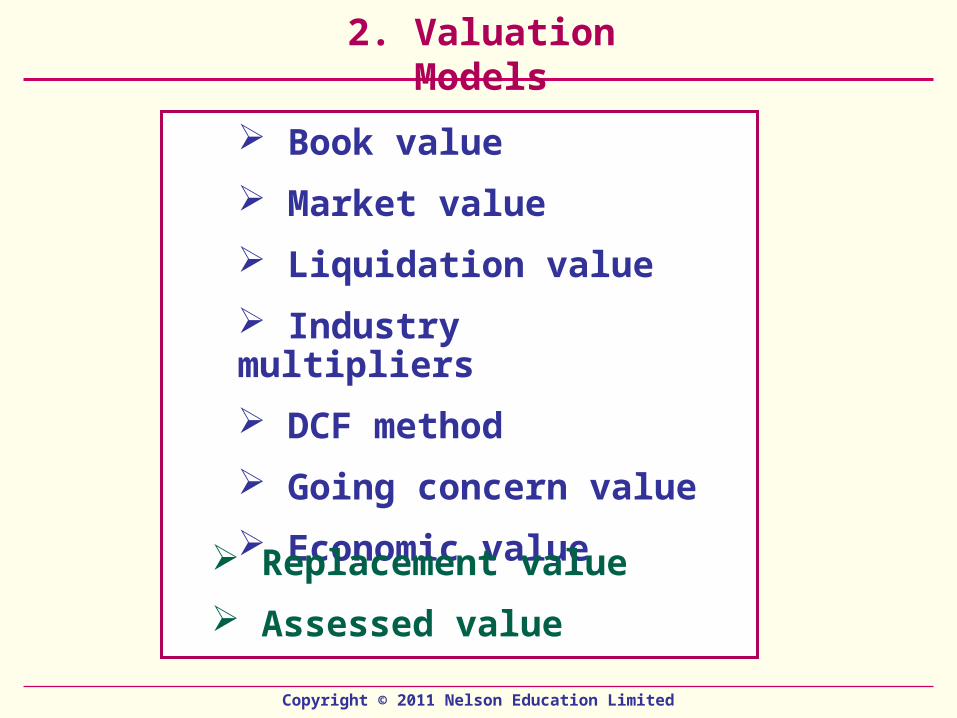

2. Valuation Models

Book value

Market value

Liquidation value

Industry multipliers

DCF method

Going concern value

Economic value Replacement value

Assessed value

Copyright © 2011 Nelson Education Limited

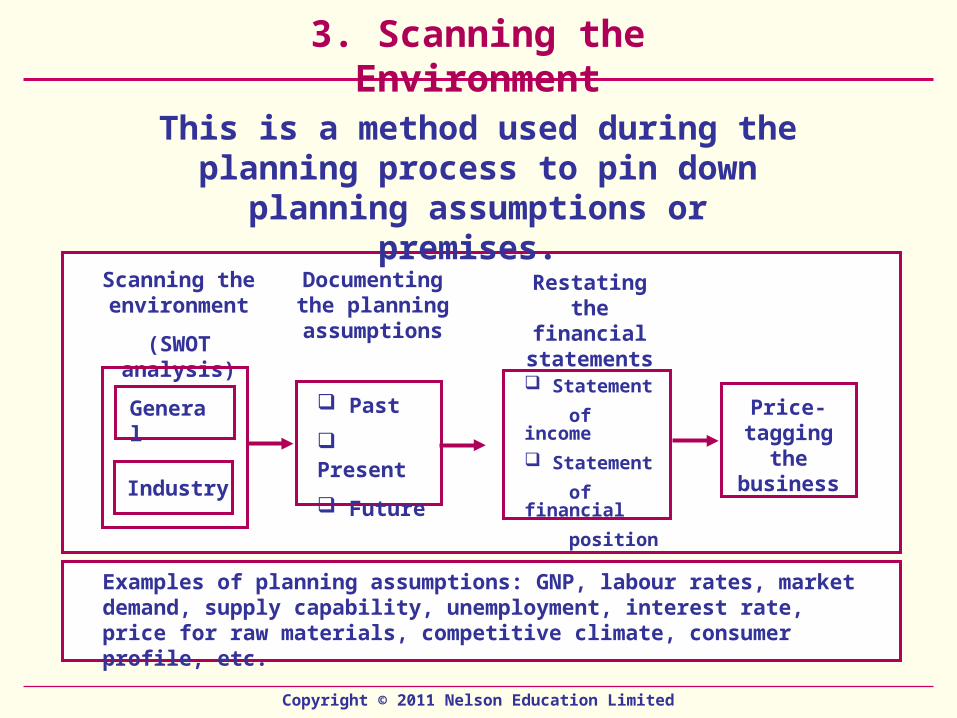

3. Scanning the Environment

This is a method used during the planning process to pin down planning

assumptions or premises.

General Past

Present

Future

Statement

of income

Statement

of financial

position

Scanning the environment

(SWOT analysis)

Documenting the planning assumptions

Restating the financial

statements

Industry

Examples of planning assumptions: GNP, labour rates, market demand, supply capability, unemployment, interest rate, price for raw materials, competitive climate, consumer profile, etc.

Price-tagging the business

Copyright © 2011 Nelson Education Limited

4. Documenting Planning AssumptionsPlanning assumptions are used to prepare a company’s projected financial statements. The following are typical planning assumptions related to the statement of income.

Revenue: size of market, profile of key competitors, consumer preferences, selling price, existing products/services

Cost of sales: key suppliers, location of suppliers, cost of raw materials, labour rates, freight costs, distribution network, competencies or skills required in manufacturing

Distribution costs: profile of typical sales representative, compensation package, competencies or skills needed, advertising costs, promotional programs, training and development, management fees, insurance premiums

Administrative expenses: number of people and composition of people working in overhead units, compensation package, leasing costs, composition of non-current assets, management fees

Other charges: interests, downsizing costs, fluctuation of Canadian dollar

Copyright © 2011 Nelson Education Limited

Documenting Planning Assumptions (continued)

The following are typical planning assumptions related to the statement of financial position.

Non-current assets: assets to be purchased, composition of non-current assets, amount to be invested in new assets, modernization, expansion, assets to be sold, depreciation and CCA rates for different non-current assets

Current assets: cash required in the bank to meet on-going activities, composition of the prepaid expenses, aging of the trade receivables, estimated bad debts, inventories in raw materials, work-in-process and finished goods, holding costs, ordering costs

Equity: number of shares outstanding, dividend policy

Long-term borrowings: amount outstanding, cost of debt, nature of agreements

Current liabilities: payment policies, terms required by suppliers, amount outstanding and interest rates, nature of accruals

Copyright © 2011 Nelson Education Limited

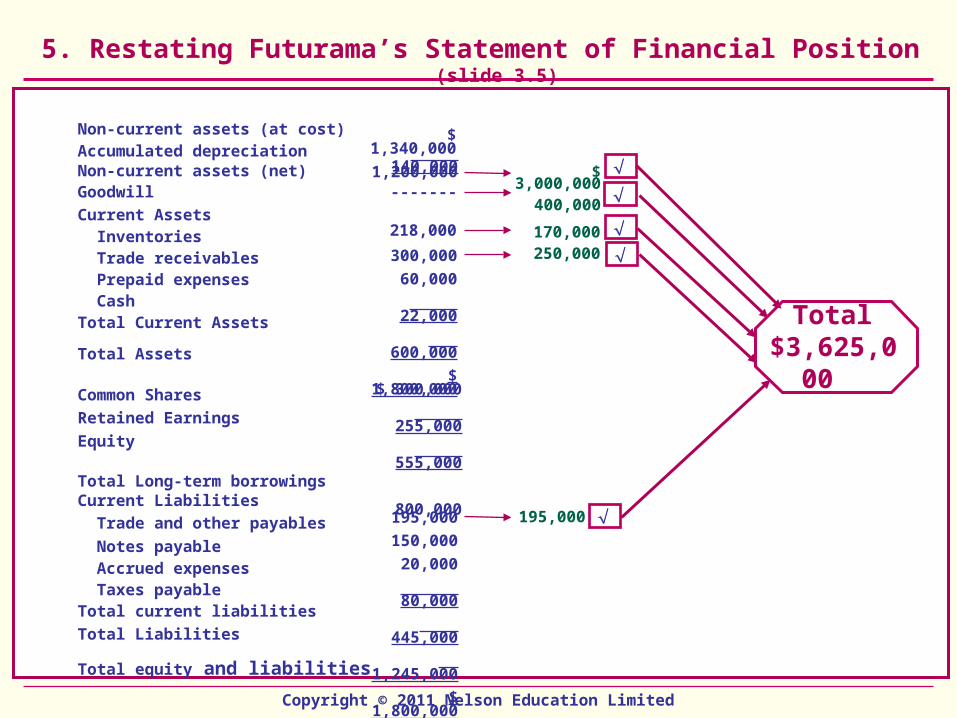

5. Restating Futurama’s Statement of Financial Position (slide 3.5)

Non-current assets (at cost)Accumulated depreciationNon-current assets (net)Goodwill

Current Assets Inventories Trade receivables Prepaid expenses CashTotal Current Assets

Total Assets

Common Shares

Retained Earnings

Equity

Total Long-term borrowingsCurrent Liabilities

Trade and other payables

Notes payable Accrued expenses Taxes payableTotal current liabilities

Total Liabilities

Total equity and liabilities

$ 3,000,000400,000

170,000250,000

195,000

$ 1,340,000 140,000 1,200,000

-------

218,000

300,000

60,000

22,000

600,000

$ 1,800,000

$ 300,000

255,000

555,000

800,000

195,000

150,000

20,000

80,000

445,000

1,245,000

$ 1,800,000

Total $3,625,000

Copyright © 2011 Nelson Education Limited

Restating Futurama’s Income Statement (slide 3.6)

Revenue $ 2,500,000

Cost of sales (1,900,000)

Gross profit 600,000

Salaries (300,000)

Rent (50,000)

Depreciation (40,000)

Other expenses (15,000)

Total expenses 405,000

Profit before taxes 195,000

Income tax expense (97,500)

Profit for the year 97,500

Add back depreciation 40,000

Total cash flow $ 137,000

$ 4,000,000

$ 369,000

$ 150,000

$ 519,000

Copyright © 2011 Nelson Education Limited

6. Book Value Method Futurama Ltd. (slide 3.5)

Book Value

Assets

Non-current assets $ 1,200,000

Inventories 218,000

Trade receivables 300,000

Prepaid expenses 60,000

Cash 22,000

Total assets $ 1,800,000

Equity

Liabilities

Trade and other payables 195,000

Misc. loans 1,050,000

Total Liabilities 1,245,000

Total equity and _________

liabilities $ 1,800,000

Difference between assets and liabilities

Book value

$ 555,000

Copyright © 2011 Nelson Education Limited

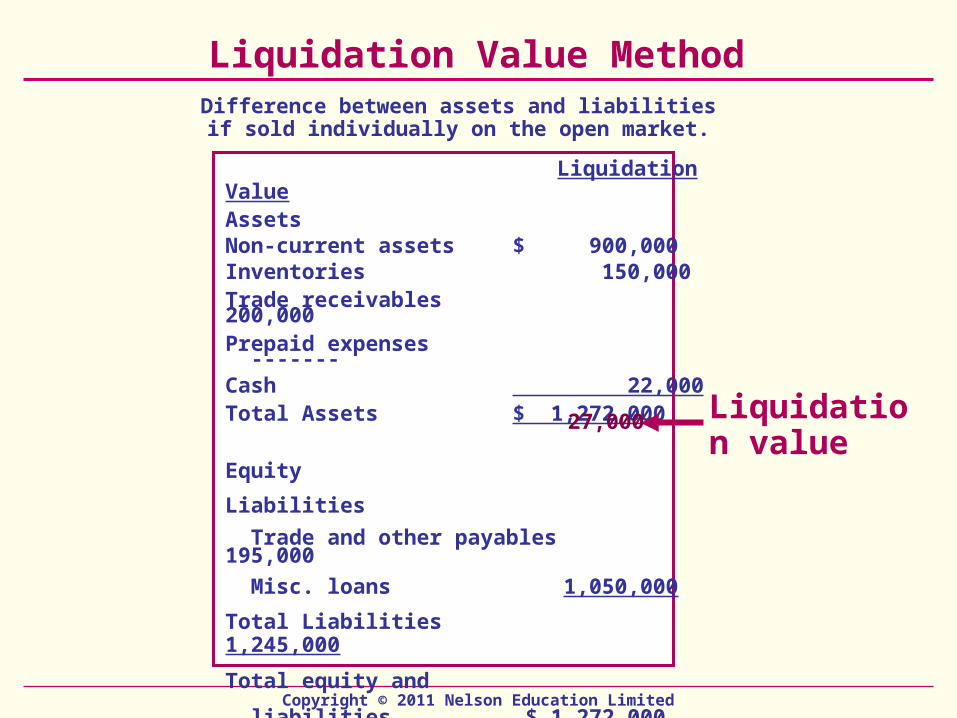

Liquidation Value Method

Liquidation ValueAssetsNon-current assets $ 900,000Inventories 150,000Trade receivables 200,000Prepaid expenses -------Cash 22,000Total Assets $ 1,272,000

Equity

Liabilities

Trade and other payables 195,000

Misc. loans 1,050,000

Total Liabilities 1,245,000

Total equity and

liabilities $ 1,272,000

Difference between assets and liabilities if sold individually on the open market.

Liquidation value

27,000

Copyright © 2011 Nelson Education Limited

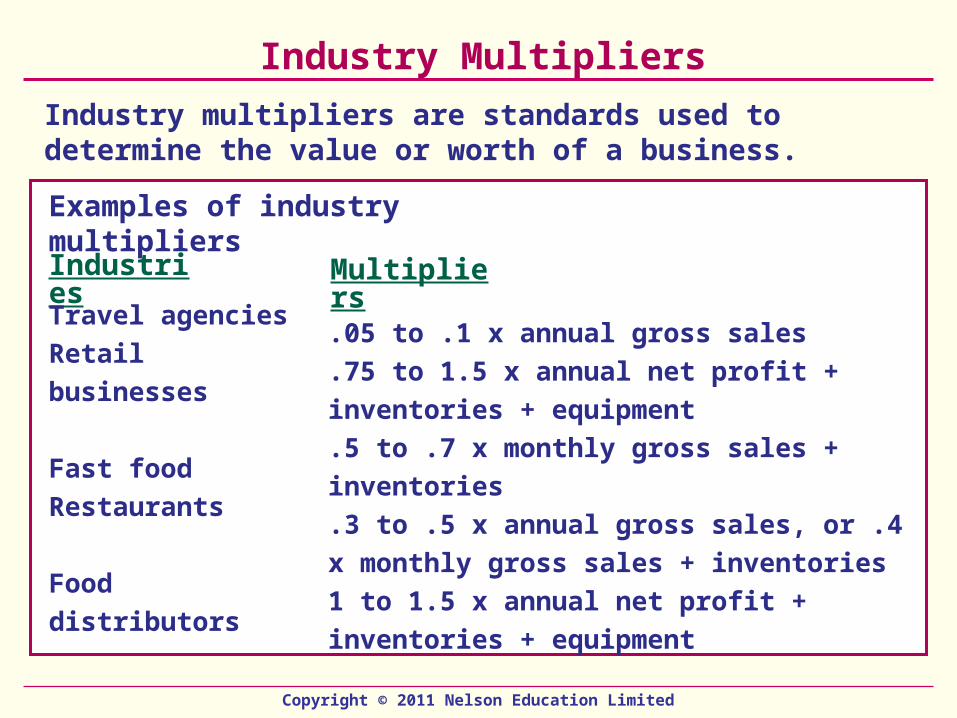

Industry Multipliers

Industry multipliers are standards used to determine the value or worth of a business.

Examples of industry multipliers

MultipliersIndustries

Travel agencies

Retail businesses

Fast food

Restaurants

Food distributors

.05 to .1 x annual gross sales

.75 to 1.5 x annual net profit + inventories +

equipment

.5 to .7 x monthly gross sales + inventories

.3 to .5 x annual gross sales, or .4 x monthly

gross sales + inventories

1 to 1.5 x annual net profit + inventories +

equipment

Copyright © 2011 Nelson Education Limited

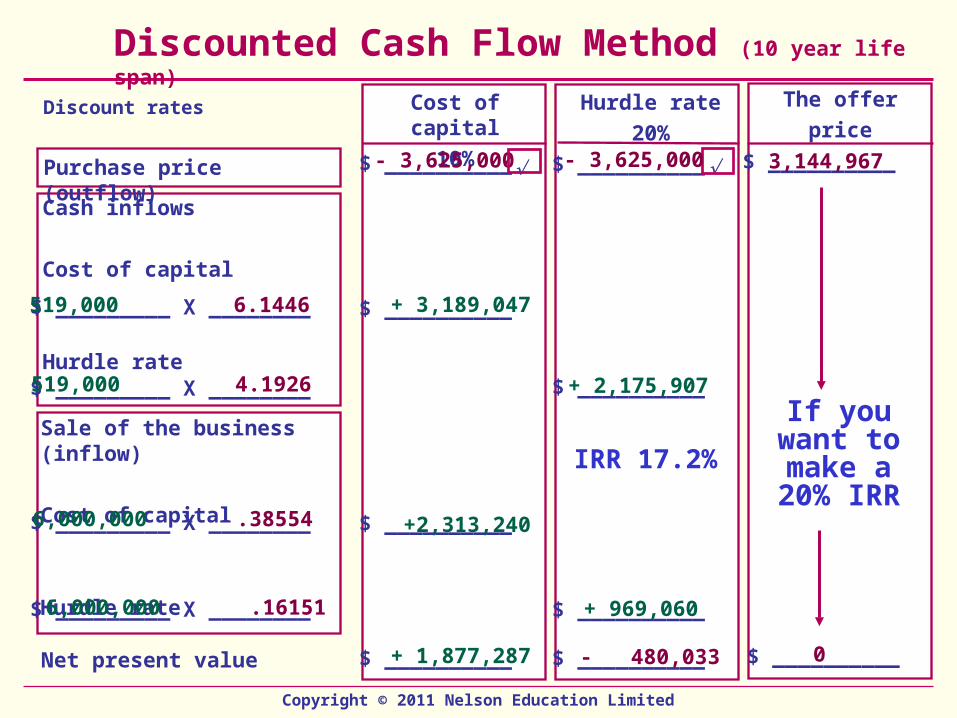

Discounted Cash Flow Method (10 year life span)

Discount rates Cost of capital

10%

Purchase price (outflow)

Cash inflows

Cost of capital

Hurdle rate

Net present value

Sale of the business (inflow)

Cost of capital

Hurdle rate

Hurdle rate

20%

The offer

price

$ __________

$ __________

$ __________

$ __________

$ __________

$ __________

$ __________

$ _________ X ________

$ _________ X ________

$ _________ X ________

$ _________ X ________

$ __________

- 3,625,000

519,000 6.1446 + 3,189,047

519,000 4.1926 + 2,175,907

6,000,000 .38554 +2,313,240

+ 969,0606,000,000 .16151

+ 1,877,287 - 480,033

IRR 17.2%

$ __________

- 3,625,000 $ __________3,144,967

0

If you want to make a

20% IRR

Copyright © 2011 Nelson Education Limited

Going Concern Value (using the capitalization rate)

Capitalization Value

Cash flow from operations $ 519,000

(from transparency 12.8)

Divided by capitalization rate* ÷ 20%

Going concern value (present value) $2,595,000

*Capitalization rate represents the required rate of return for the company which is based on a number of subjective factors and conditions at the time of the valuation.

Company will be sold as a viable business generating a cash flow of say $519,000/year forever.

Going concern value

Copyright © 2011 Nelson Education Limited

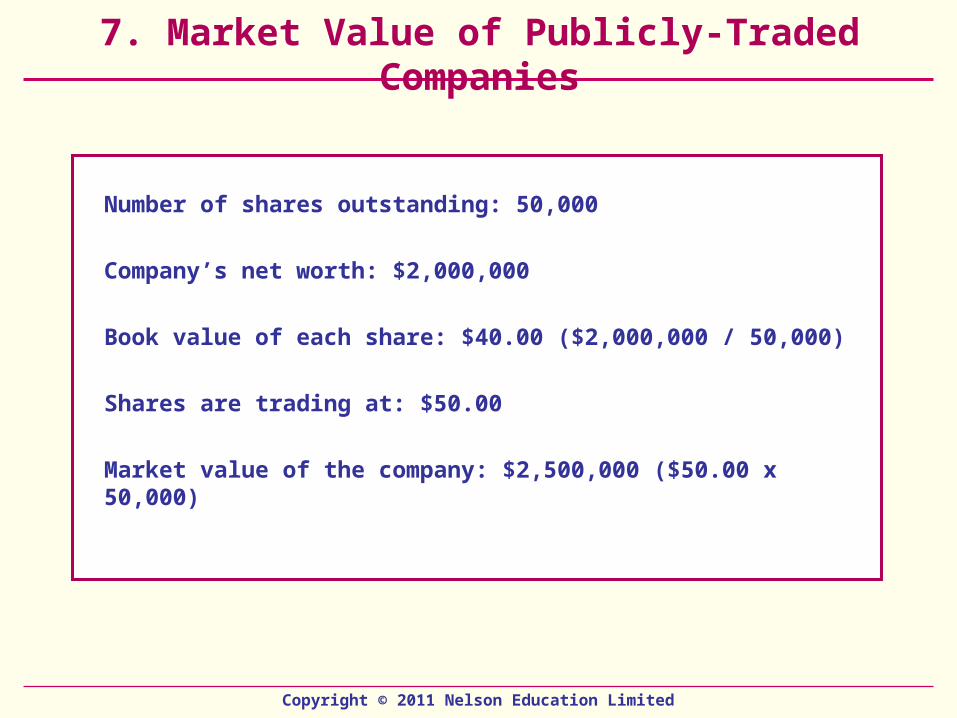

7. Market Value of Publicly-Traded Companies

Number of shares outstanding: 50,000

Company’s net worth: $2,000,000

Book value of each share: $40.00 ($2,000,000 / 50,000)

Shares are trading at: $50.00

Market value of the company: $2,500,000 ($50.00 x 50,000)

Copyright © 2011 Nelson Education Limited

8. Projects From an Investor’s Perspective

Step 1: Cash flow forecast

Step 2: Residual value of the forecast period

Step 3: Estimated market value

Step 4: Investor’s return (40% investment in the business)a) Before taxb) After tax

Copyright © 2011 Nelson Education Limited

Projects from an investor’s (venture capitalist) perspective

Investors are looking for a Winning Combination!

Products/Services (%)(the horse)

Management Team

(The jockey)

Copyright © 2011 Nelson Education Limited

The Rich-Gumpert Evaluation System

1/1

2/1 2/2

1/2

3/1 3/2 3/3

2/3

1/3

4/1 4/2 4/3 4/4

3/4

2/4

1/4

Level 1A single would-be

founder/Entrepreneur.

Management Status

MOST

DESIRABLE

MOST DESIRABLE

PRODUCT/SERVICE

STATUS

Level 2Two founders, additional slots

but personnel not identified.

Level 3Partly staffed team, absent members

but will join when firm is funded.

Level 4Fully staffed by

experienced management

team.

Level 4Product/servicefully developed.

Many satisfied users.Market established.

Level 2Product/service

pilot operative. Notyet developed for

production.Market assumed.

Level 3Product/servicefully developed.

Few or no users as yet.Market assumed.

Level 1Product/service

idea and notyet operable.

Market assumed.

Source: Business Plans that Wins $$$, Stanley R. Rich and David E. Gumpert, Harpor & Row, 1986, p. 169.

Ready for an IPO

Copyright © 2011 Nelson Education Limited

Steps When Approaching Venture Capitalists

Demonstrate investment

potential

Demonstrate management

team capabilities

Identify potential

needs

Write investment proposal

Meet potential investors

Negotiate the deal

Close the deal

Identify potential investors

Step 1 Step 6 Step 7Step 5Step 4

Step 3

Step 2

Step 8

Copyright © 2011 Nelson Education Limited

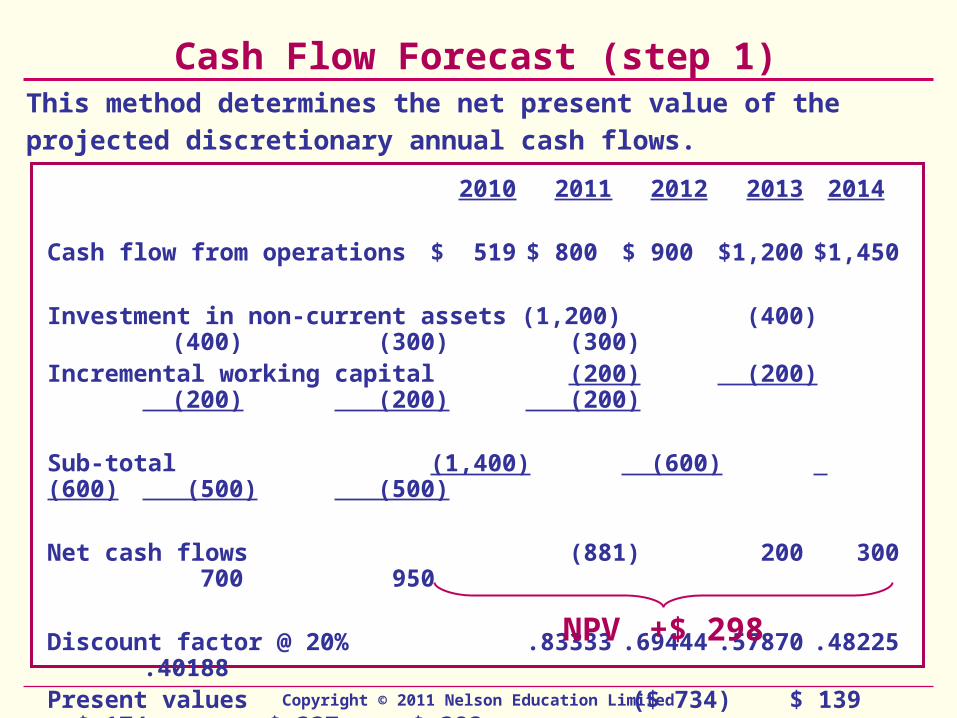

2010 2011 2012 2013 2014

Cash flow from operations $ 519 $ 800 $ 900 $1,200 $1,450

Investment in non-current assets (1,200) (400) (400) (300) (300)Incremental working capital (200) (200) (200) (200) (200)

Sub-total (1,400) (600) (600) (500) (500)

Net cash flows (881) 200 300 700 950

Discount factor @ 20% .83333 .69444 .57870 .48225 .40188Present values ($ 734) $ 139 $ 174 $ 337 $ 382

Cash Flow Forecast (step 1)This method determines the net present value of the projected

discretionary annual cash flows.

NPV +$ 298

Copyright © 2011 Nelson Education Limited

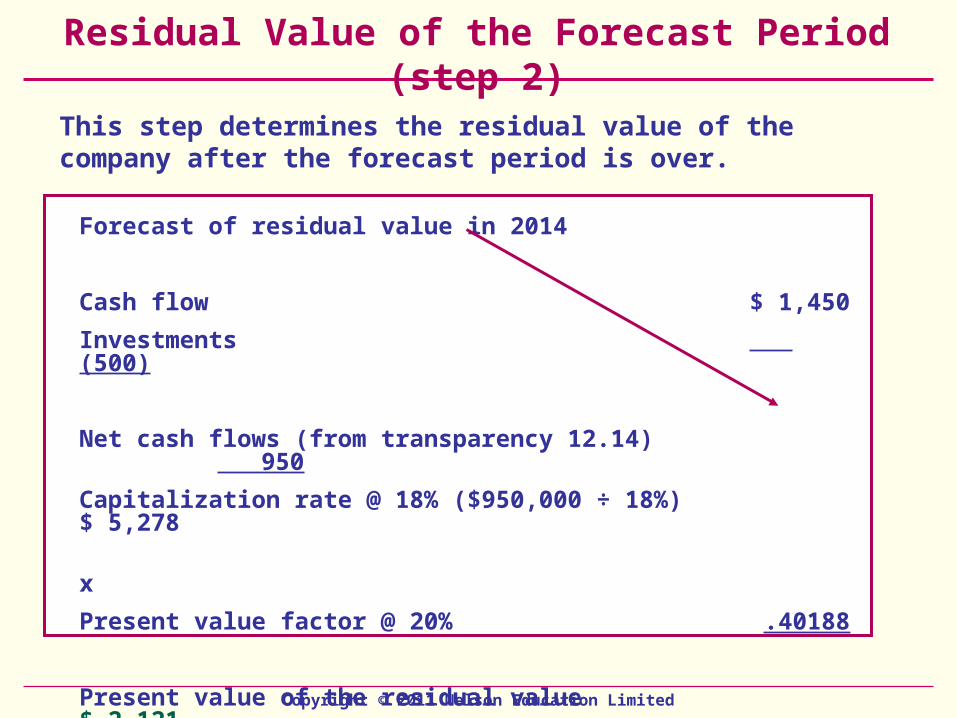

Residual Value of the Forecast Period (step 2)

Forecast of residual value in 2014

Cash flow $ 1,450

Investments (500)

Net cash flows (from transparency 12.14) 950

Capitalization rate @ 18% ($950,000 ÷ 18%) $ 5,278

x

Present value factor @ 20% .40188

Present value of the residual value $ 2,121

This step determines the residual value of the company after the forecast period is over.

Copyright © 2011 Nelson Education Limited

Estimated Market Value (step 3)

Forecast of discretionary cash flow $ 298 (from transp. 12.19)

Add: residual value 2,121 (from transp. 12.20)

Estimated fair market $ 2,419

value of the shares

This step determines the residual value of the company after the forecast period is over.

Estimated fair market

value

Copyright © 2011 Nelson Education Limited

2009 2010 2011 2012 2013 2014

A. Investment return before taxes --- --- --- ---

Initial investment ($ 600) --- --- --- ---

Cash distribution to investors (transparency 12.19) $ 950 Multiplier 8.0 Total value at exit 7,600

Investor’s required share (40%) --- --- --- 3,040 Initial investment ($ 600) Total discounted cash inflow $ 600 $ 3,040

Investor’s Return - Before Tax (step 4)This method takes into account the discounted value of the future cash flows to calculate the investor’s return.

Before-tax return to investor 38.34%

Copyright © 2011 Nelson Education Limited

B. After-tax return Proceeds received on exit $3,040 Initial investment (600) Capital gain on investment 2,440

Taxable portion (75%) 1,830 Investor’s tax payable (50%) 915

Gross proceeds received on exit 3,040 Investor’s tax payable 915

Net after-tax proceeds to investor $ 2,125

Investor’s Return - After Tax

Copyright © 2011 Nelson Education Limited

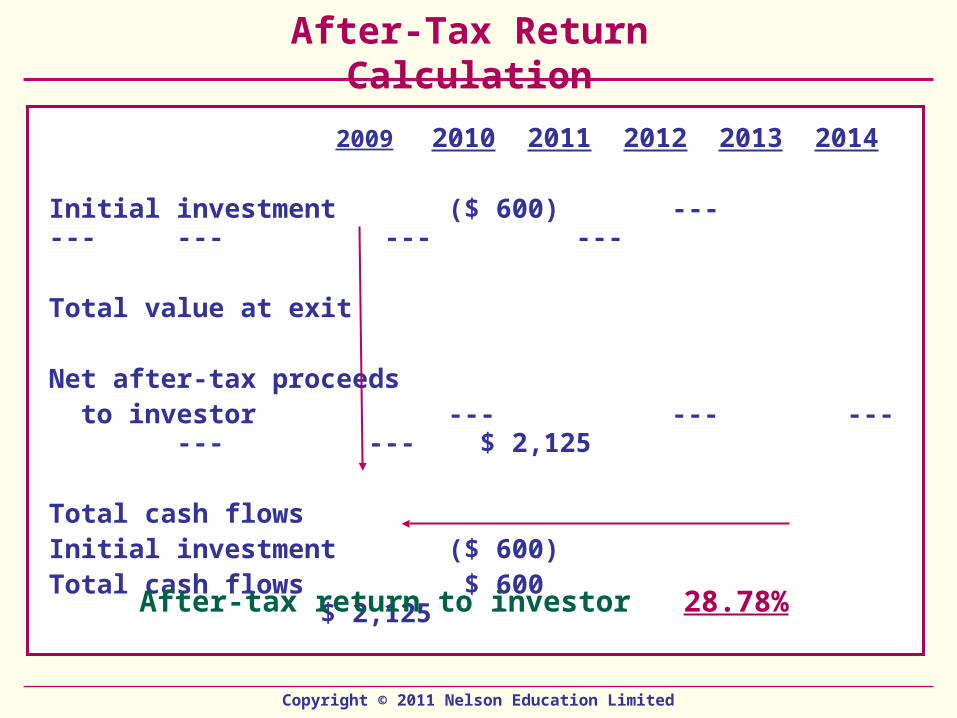

2009 2010 2011 2012 2013 2014

Initial investment ($ 600) --- --- --- --- ---

Total value at exit

Net after-tax proceeds to investor --- --- --- --- --- $ 2,125

Total cash flowsInitial investment ($ 600)Total cash flows $ 600 $ 2,125

After-Tax Return Calculation

After-tax return to investor 28.78%