Copyright 1998, Catherine A. Duran

170

THE IMPACT OF ORGANIZATIONAL DOWNSIZING ON CORPORATE AND STRATEGIC BUSINESS UNIT ECONOMIC PERFORMANCE: AN EMPIRICAL INVESTIGATION OF THE ROLE OF WORK FORCE REDUCTION by CATHERINE A. DURAN, B.S., M.S., M.B.A. A DISSERTATION IN BUSINESS ADMINISTRATION Submitted to the Graduate Faculty of Texas Tech University in Partial Fulfillment of the Requirements for the Degree of DOCTOR OF PHILOSOPHY Approved Chairperson of the Committee Accepted Dedtn of the Graduate School May, 1998

Transcript of Copyright 1998, Catherine A. Duran

THE IMPACT OF ORGANIZATIONAL DOWNSIZING ON CORPORATE

AND STRATEGIC BUSINESS UNIT ECONOMIC PERFORMANCE:

AN EMPIRICAL INVESTIGATION OF THE ROLE

OF WORK FORCE REDUCTION

by

CATHERINE A. DURAN, B.S., M.S., M.B.A.

A DISSERTATION

IN

BUSINESS ADMINISTRATION

Submitted to the Graduate Faculty of Texas Tech University in

Partial Fulfillment of the Requirements for

the Degree of

DOCTOR OF PHILOSOPHY

Approved

Chairperson of the Committee

Accepted

Dedtn of the Graduate School

May, 1998

Copyright 1998, Catherine A. Duran

ACKNOWLEDGMENTS

I would like to thank all the members of ray committee.

Dr. Robert L. Phillips, Dr. Roy D. Howell, Dr. Grant T.

Savage, and Dr. Carlton J. Whitehead for their advice and

never-ending support during the course of my doctoral

program. I am especially grateful to my major professor. Dr.

Phillips, whose knowledge and expertise guided me throughout

my work. I have learned so much from him, not only for this

study, but also for my professional development. I would

also like to especially thank Dr. Howell for giving me his

valuable time on the statistical analysis for this study.

I would like to express deep appreciation to vinitia

Mathews, whose understanding and encouragement were paramount

to this endeavor; and to John Ryan, without whose technical

expertise, programming knowledge and good humor, I could not

have completed this study.

Thanks to my parents for their lasting belief in me, and

for providing so much help in so many ways, without whom this

accomplishment would not be possible. I want to especially

thank my husband, Steve, for his continued support,

encouragement and patience throughout this work, again

without whom I could not have been successful. Finally, I

would like to thank my son, Robert, for keeping me happy and

providing the best reason of all for this achievement.

11

TABLE OF CONTENTS

ACKNOWLEDGMENTS ii

ABSTRACT V

LIST OF TABLES vii

CHAPTER

I. INTRODUCTION 1

Significance of the Study 7

Organization of the Dissertation 8

II. LITERATURE REVIEW 9

Organizational Size 12

Decline in Organizations 16

Organizational Size and Decline 28

Corporate Restructuring 29

Divestment 33

Downsizing Practices 35

Gaps in the Reviewed Literature 42

III. RATIONALE 45

The Point at the End of the Cornucopia 45

Research Strategy 48

IV. METHODOLOGY 49

Data 49

Performance Measures 51

Downsizing Measures 53

Control Measures 54

111

Method of Analysis 57

Empirical Model 58

V. DATA ANALYSIS 60

Descriptive Statistics 60

Time Series Cross-sectional Regression Analysis 63

Base Year Performance as Independent Variables 71

Pooled Cross-sectional Regression Results 7 3

VI. DISCUSSION AND CONCLUSIONS 128

Conclusions 130

Implications 140

Limitations and Strengths 144

Directions for Future Research 146

REFERENCES 148

IV

ABSTRACT

The relationship between downsizing and performance has

not been studied thoroughly, despite the prevalence of

downsizing in the U.S. and overseas. The downsizing issue

continues to be a topic of interest for the nation and the

business world. The streamlining of organizations has become

a perceived necessity in gaining a competitive edge in the

marketplace; however, it has not been clear whether

downsizing does indeed improve profitability. This study

addresses the downsizing-performance link, using

comprehensive multi-year, multi-industry data, and provides a

beginning to understanding the growing (both in occurrence

and importance) phenomenon of downsizing.

The study employs multivariate analysis for the inclusion

of many specific variables that have an impact on economic

performance of an organization. The impact of downsizing (as

workforce reduction) on both corporate and strategic business

unit (SBU) performance is studied, controlling for market

conditions. The study employs both an accounting measure and

a hybrid market/accounting measure of performance to

investigate, not only the impact of downsizing on

organizational profitability, but also on the perceptions of

the market.

The study shows that when controlling for other factors

that affect organizational performance, downsizing has some

negative and some positive effects on SBU and corporate

performance, and that these effects persist for a limited

period of time. Downsizing appears to have some of the

positive effects presented in the anecdotal literature;

however, there appear to be important negative ramifications

of downsizing as well.

VI

LIST OF TABLES

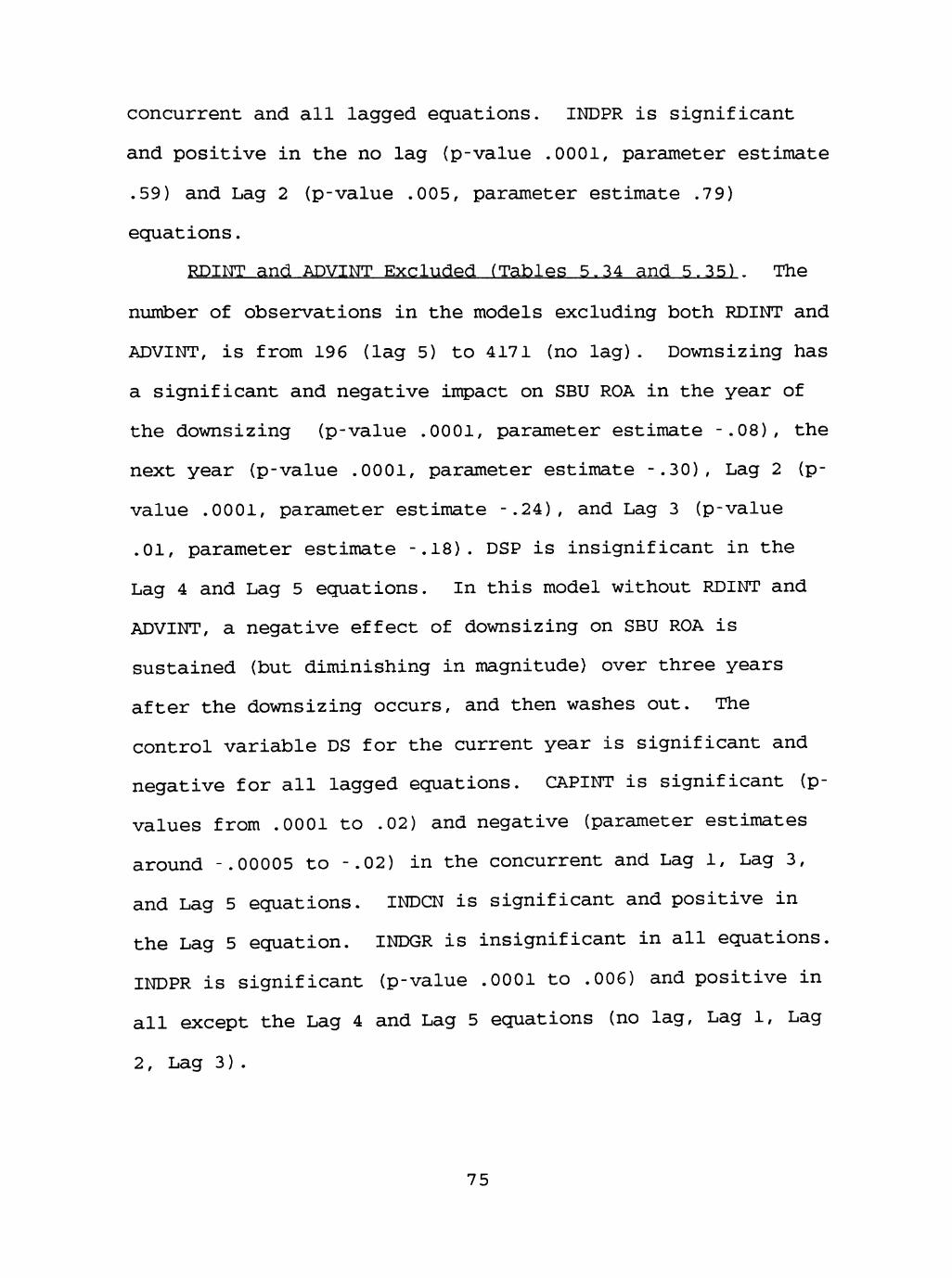

5.1 Descriptive Statistics (SBU datasets) 80

5.2 Descriptive Statistics (CORP datasets) 81

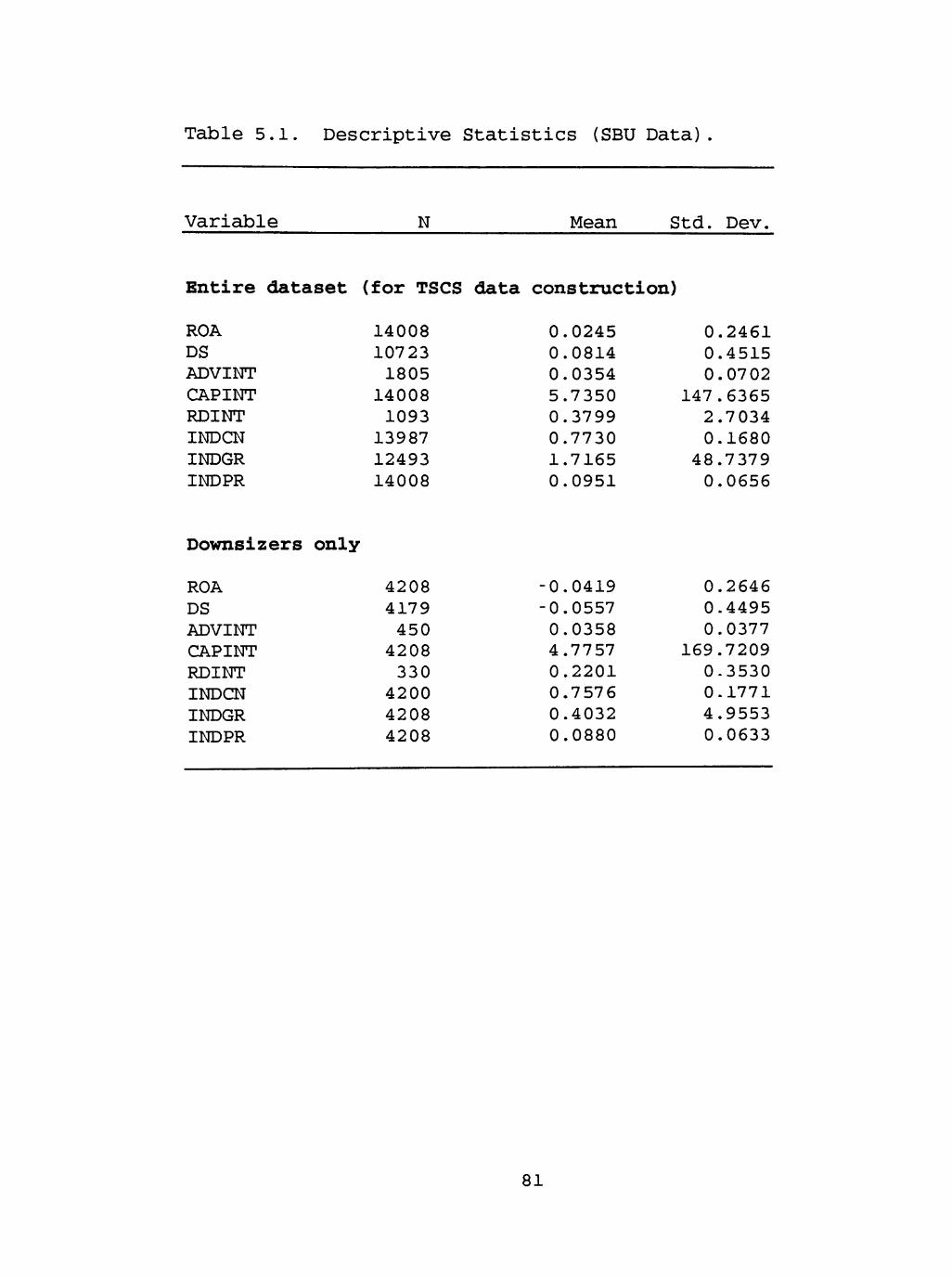

5.3 Correlation Matrices (SBU datasets) 82

5.4 Correlation Matrices (CORP datasets) 83

5.5 Number of SBU's/CORPS by Year 84

5-6 Years of Data Available for TSCS Regressions 85

5.7 Time Series Regression Results (SBU)--All Variables Included 86

5.8 Lagged Time Series Regression Results (SBU)--All Variables Included 87

5.9 Time Series Regression Results (SBU)--ADVINT Excluded 88

5.10 Lagged Time Series Regression Results (SBU)--ADVINT Excluded 89

5.11 Time Series Regression Results (SBU)--RDINT Excluded 90

5.12 Lagged Time Series Regression Results (SBU)--RDINT Excluded 91

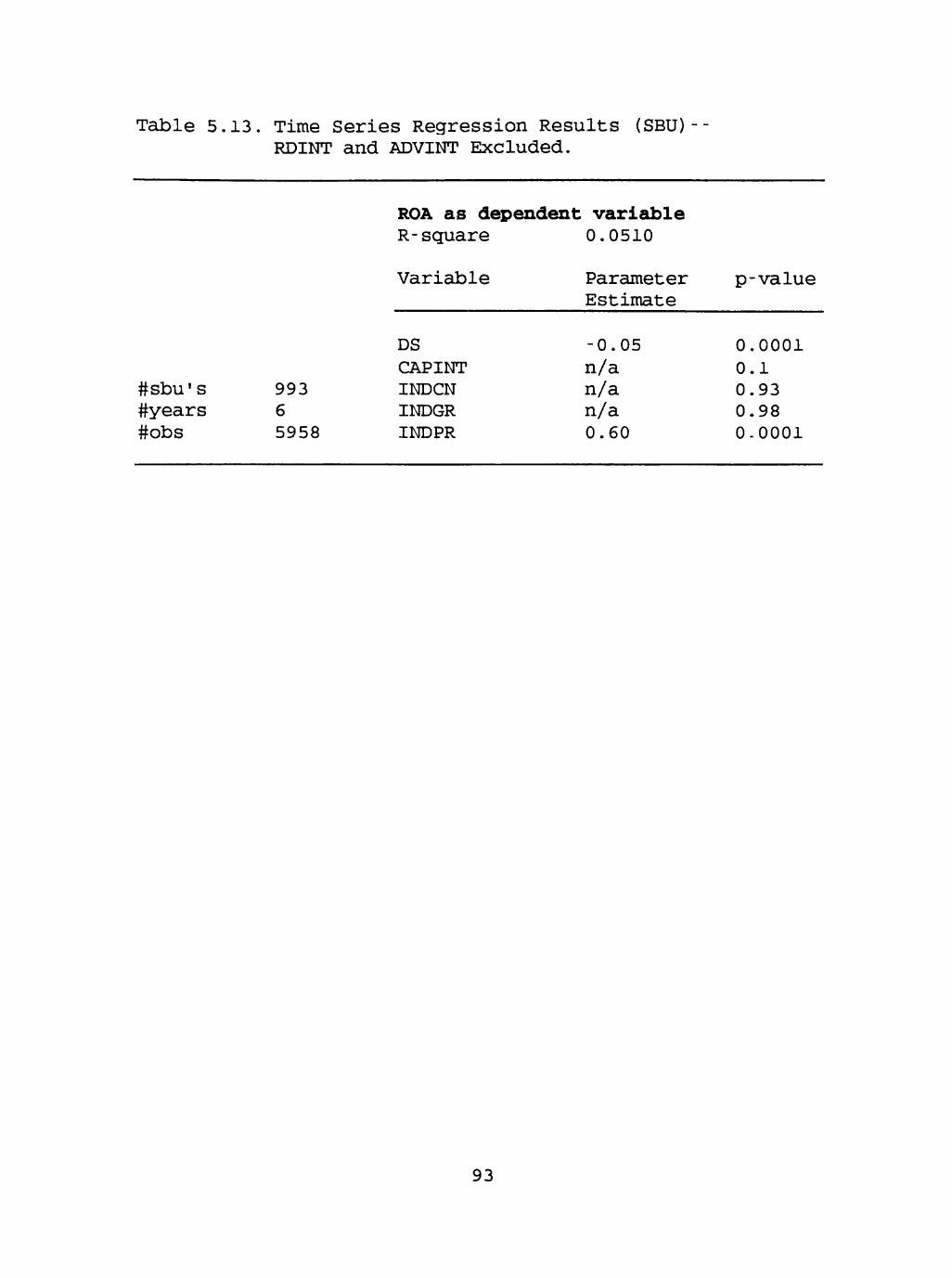

5.13 Time Series Regression Results (SBU)--RDINT and ADVINT Excluded 92

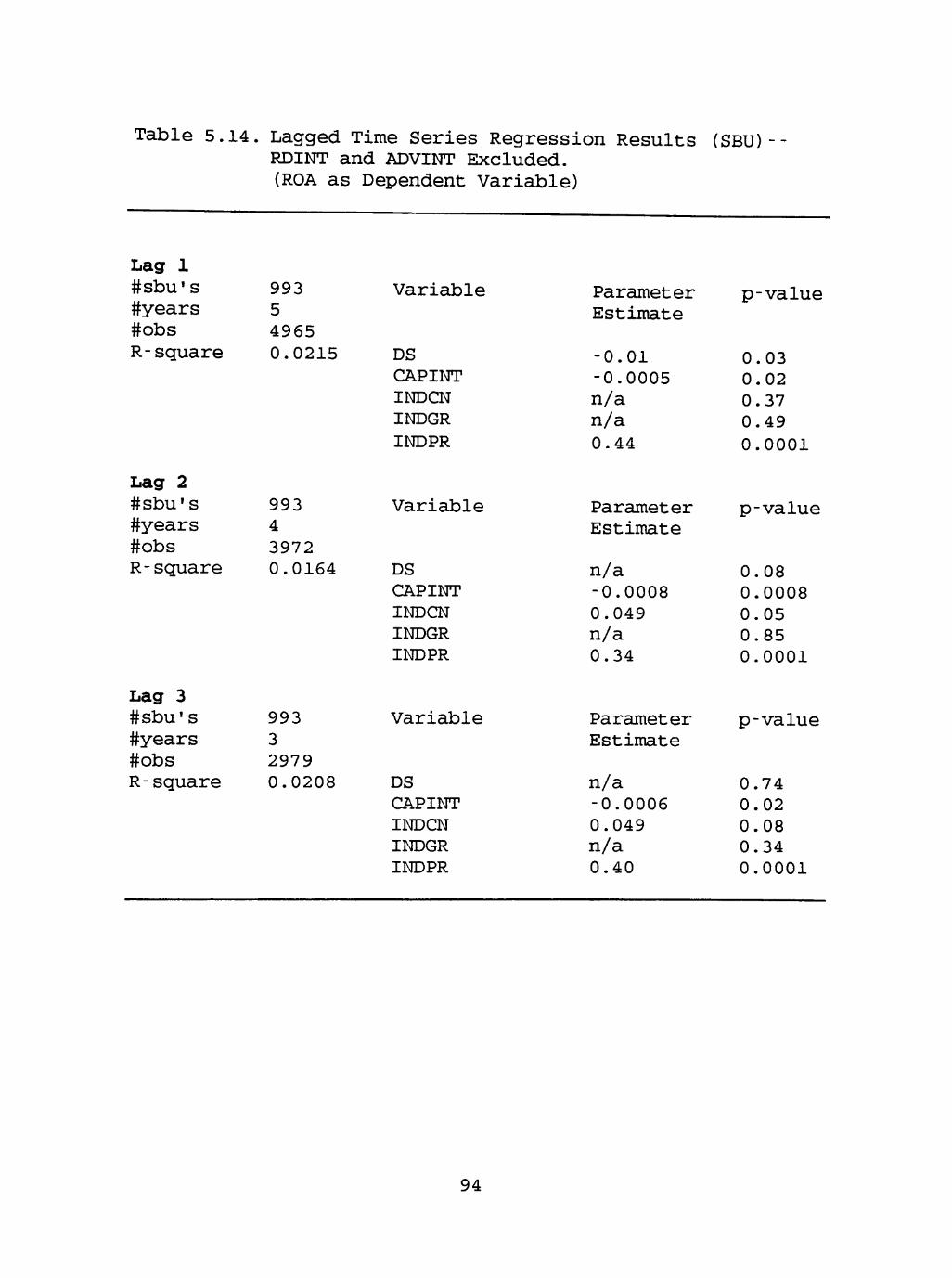

5.14 Lagged Time Series Regression Results (SBU)--RDINT and ADVINT Excluded 93

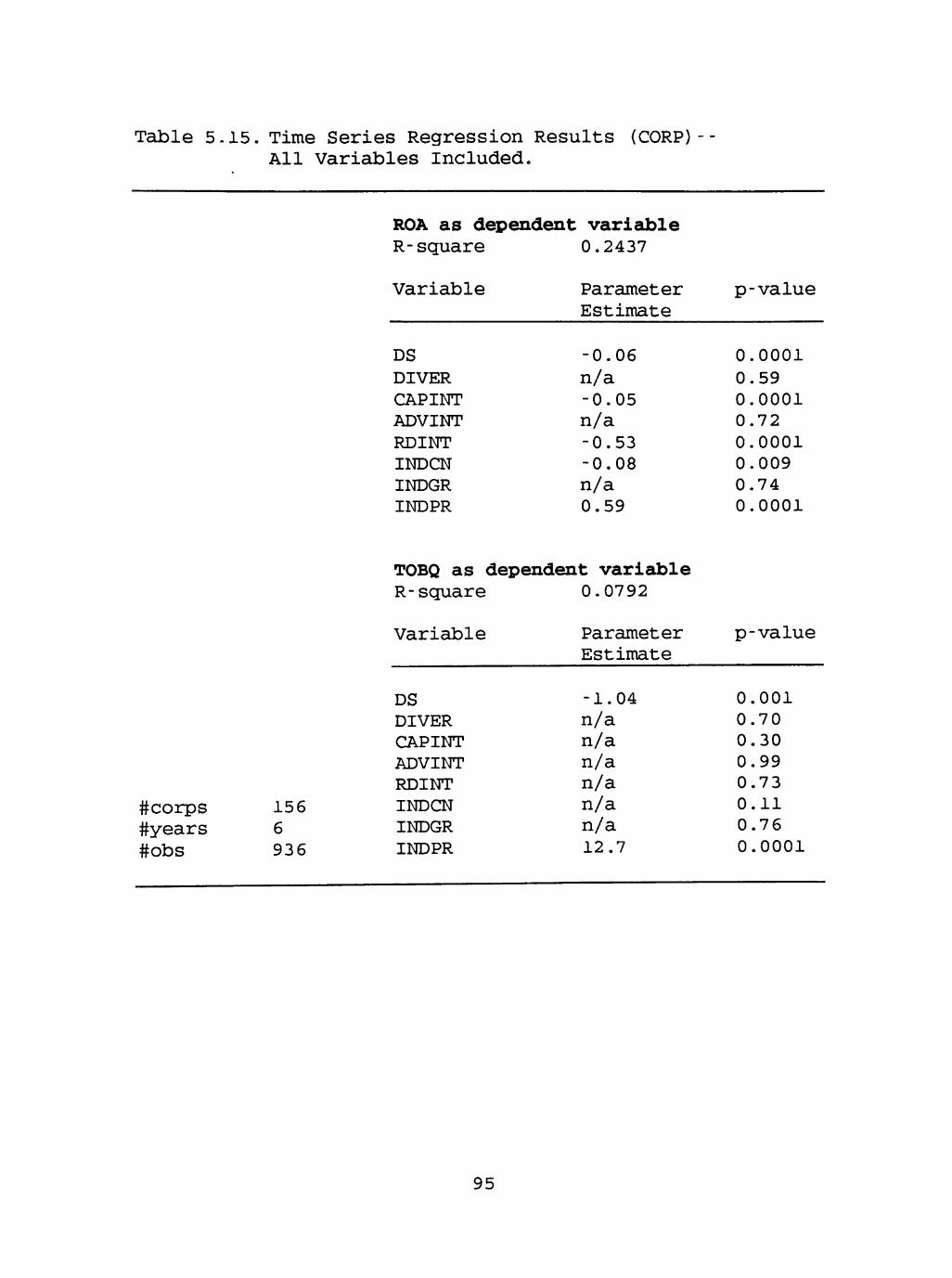

5.15 Time Series Regression Results (CORP)--All Variables Included 94

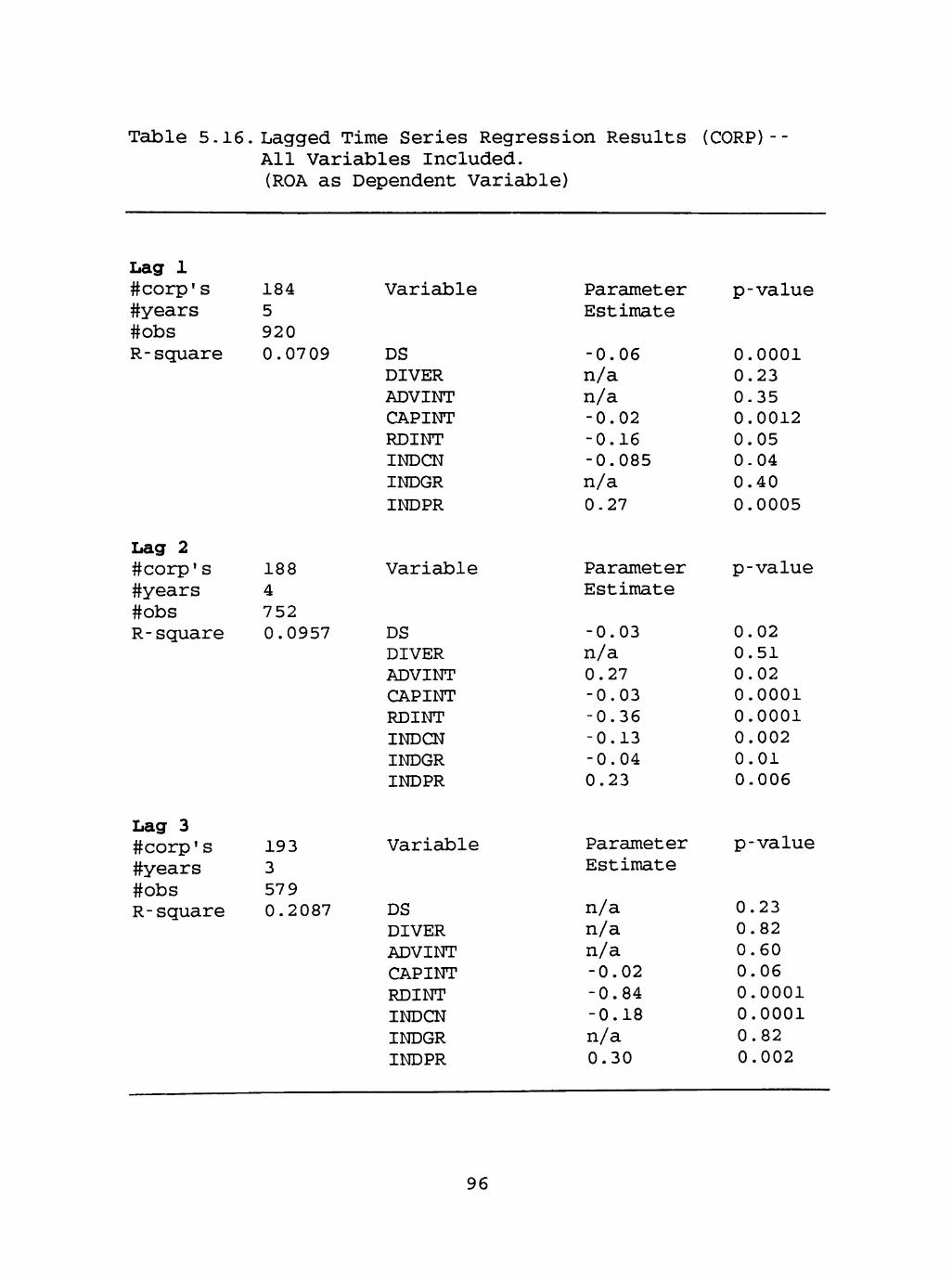

5.16 Lagged Time Series Regression Results (CORP)--All Variables Included (ROA as Dependent Variable)...95

5.17 Time Series Regression Results (CORP)--ADVINT Excluded 96

5.18 Lagged Time Series Regression Results (CORP)--ADVINT Excluded. (ROA as Dependent Variable) 97

vu

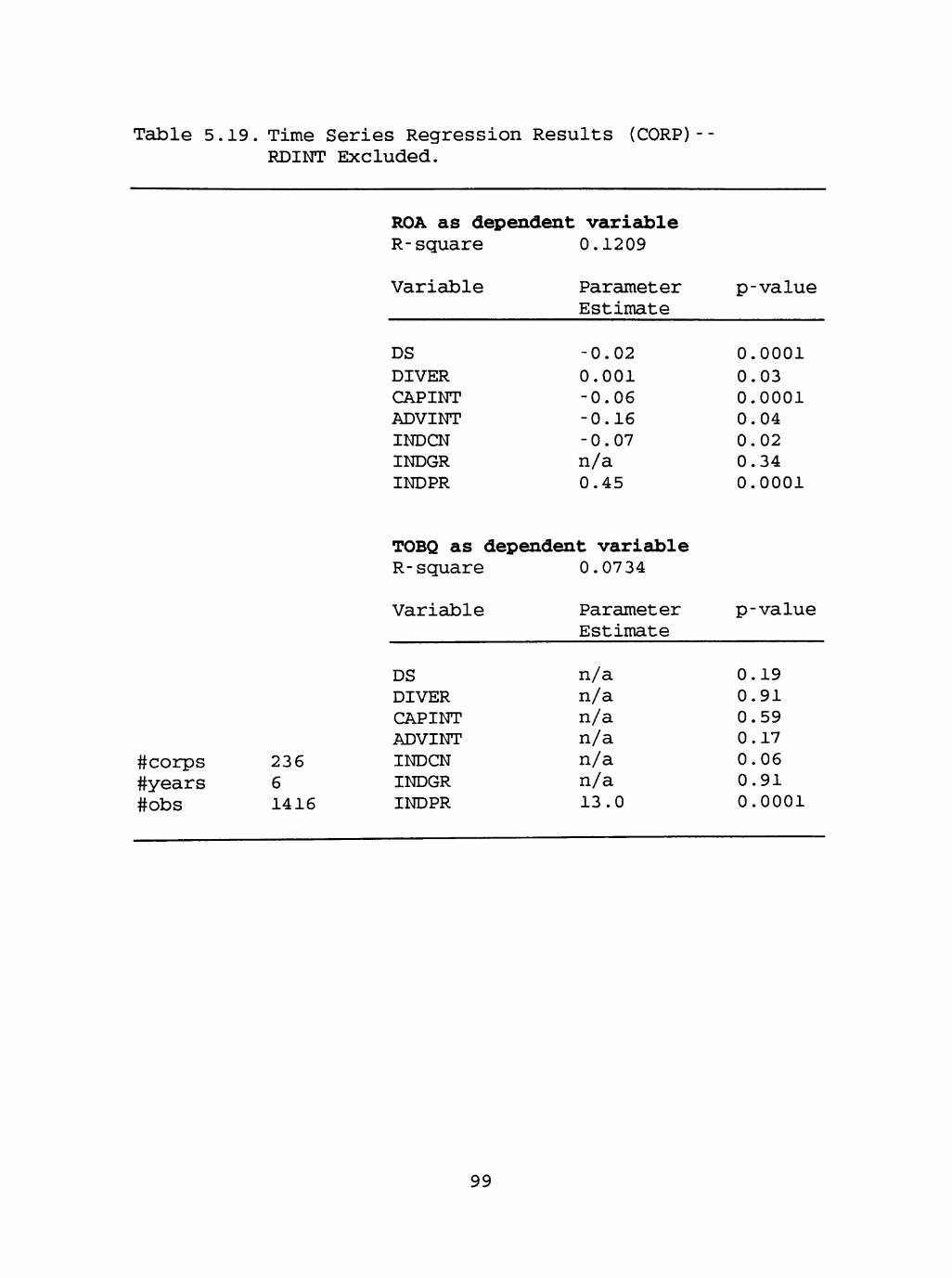

5.19 Time Series Regression Results (CORP)--RDINT Excluded 98

5.20 Lagged Time Series Regression Results (CORP)--RDINT Excluded (ROA as Dependent Variable) 99

5.21 Time Series Regression Results (CORP)--RDINT and ADVINT Excluded 100

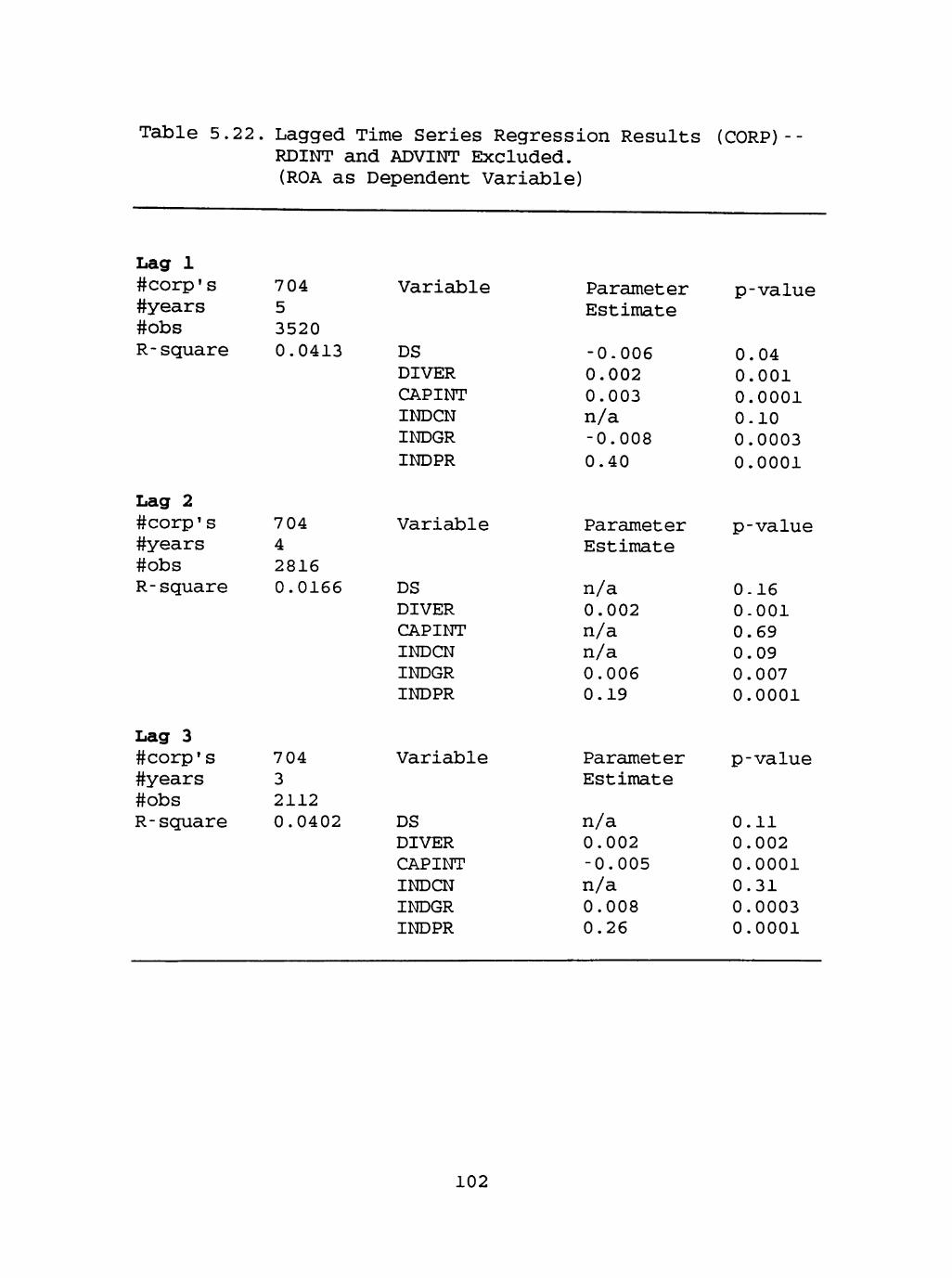

5.22 Lagged Time Series Regression Results (CORP)--RDINT and ADVINT Excluded (ROA as Dependent Variable) 101

5.23 Lagged Time Series Regression Results (CORP)--All Variables Included (TOBQ as Dependent Variable).102

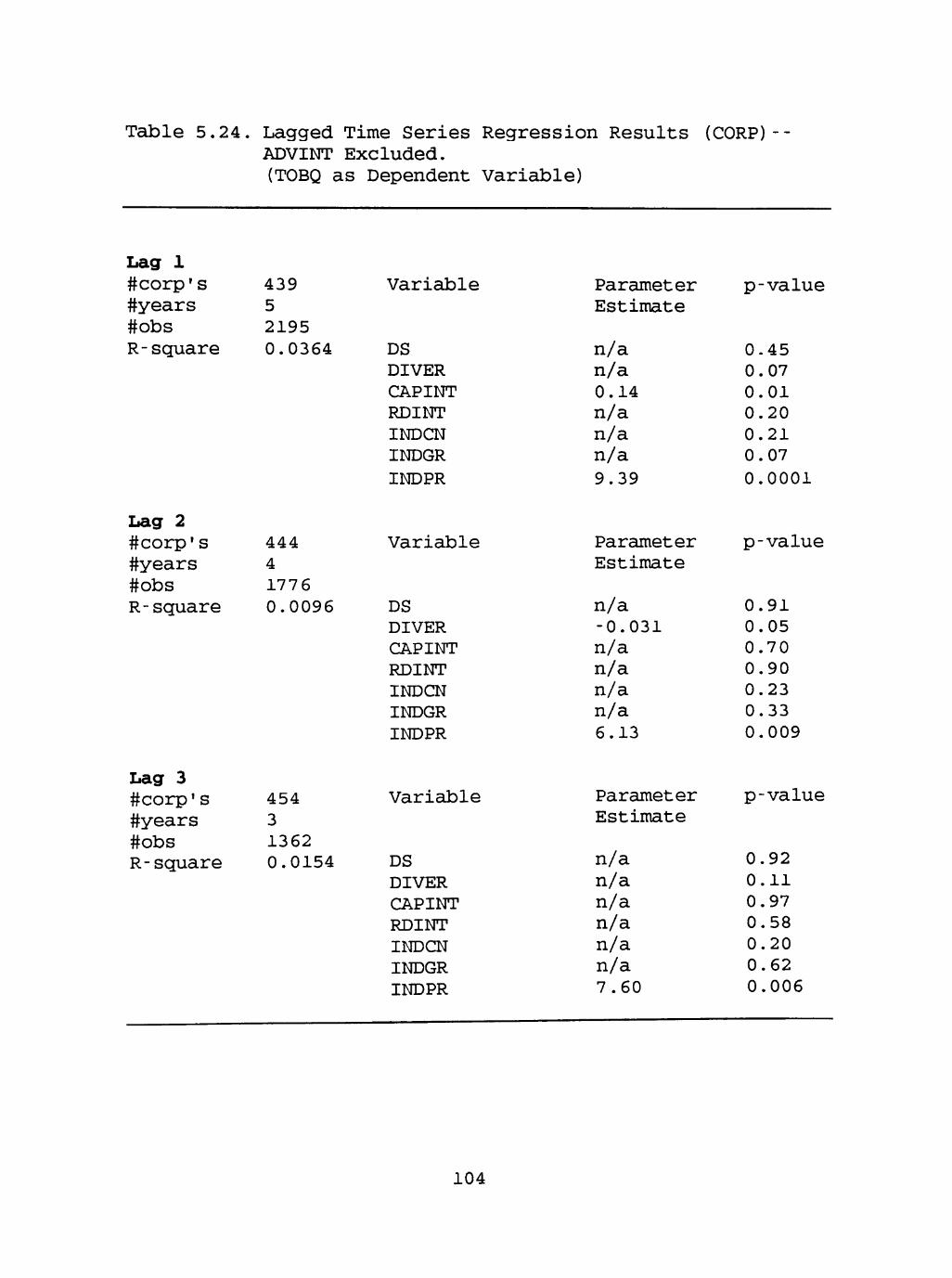

5.24 Lagged Time Series Regression Results (CORP)--ADVINT Excluded. (TOBQ as Dependent Variable) 103

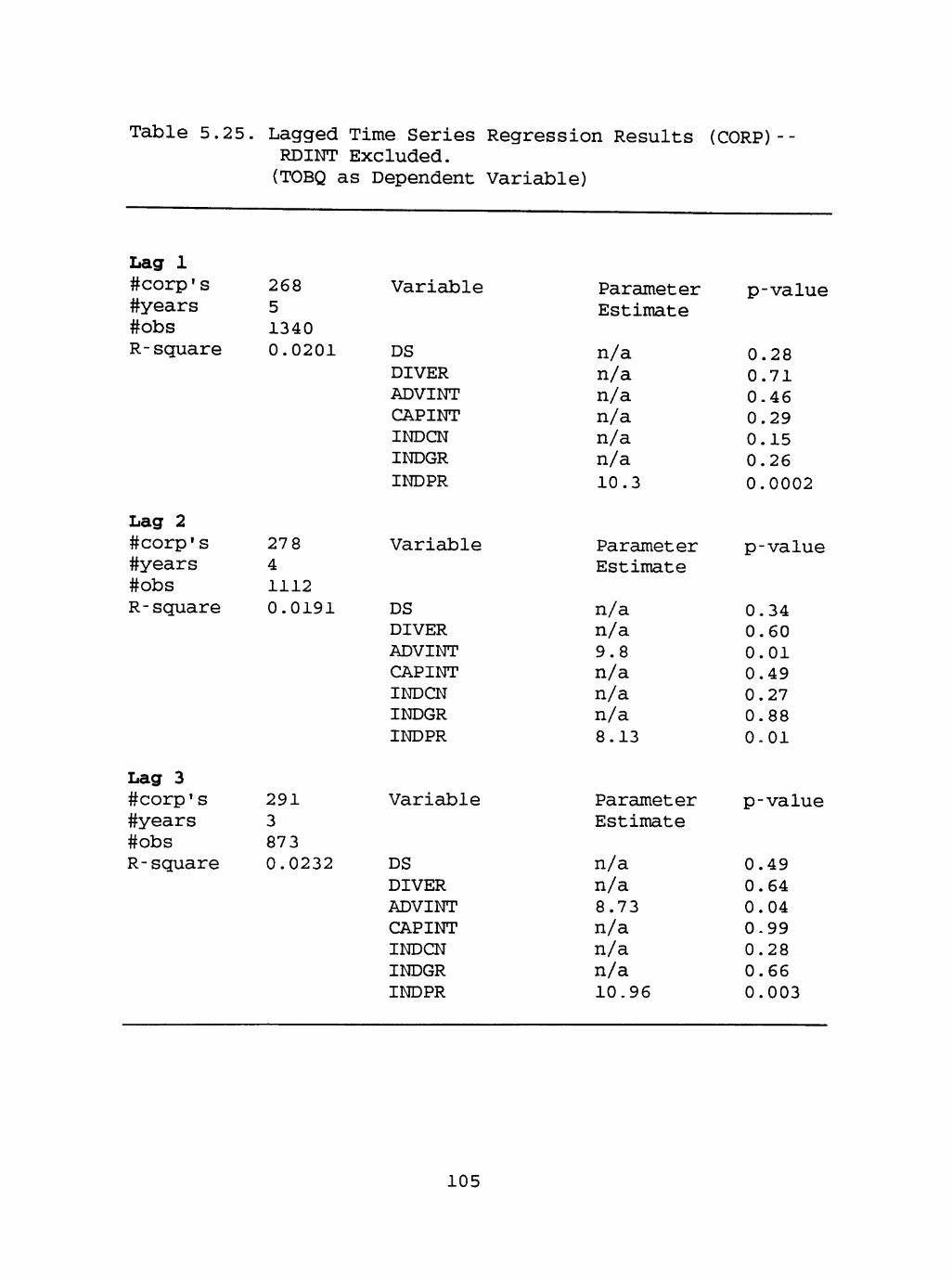

5.25 Lagged Time Series Regression Results (CORP)--RDINT Excluded (TOBQ as Dependent Variable) 104

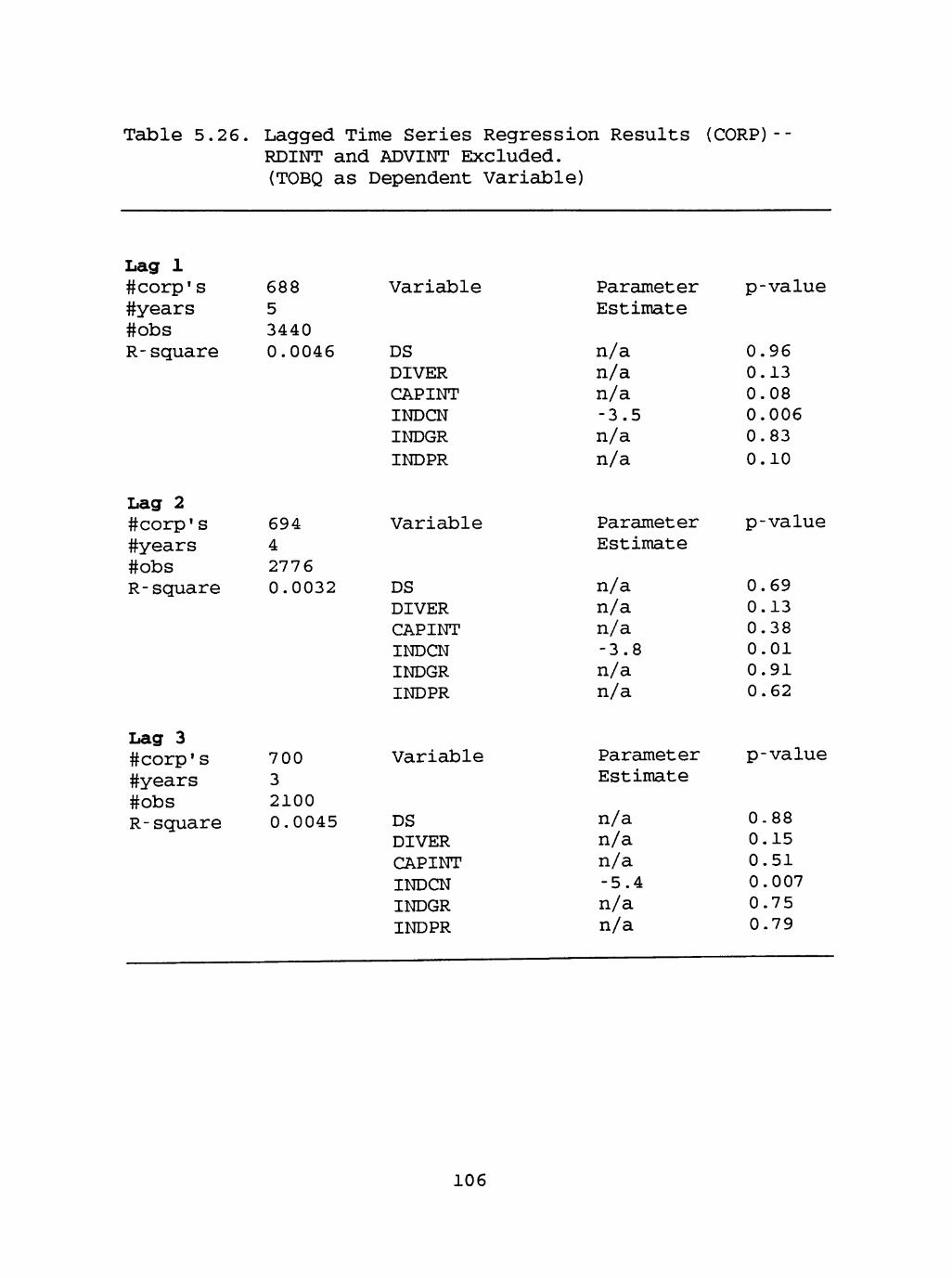

5.26 Lagged Time Series Regression Results (CORP)--RDINT and ADVINT Excluded (TOBQ as Dependent Variable) 105

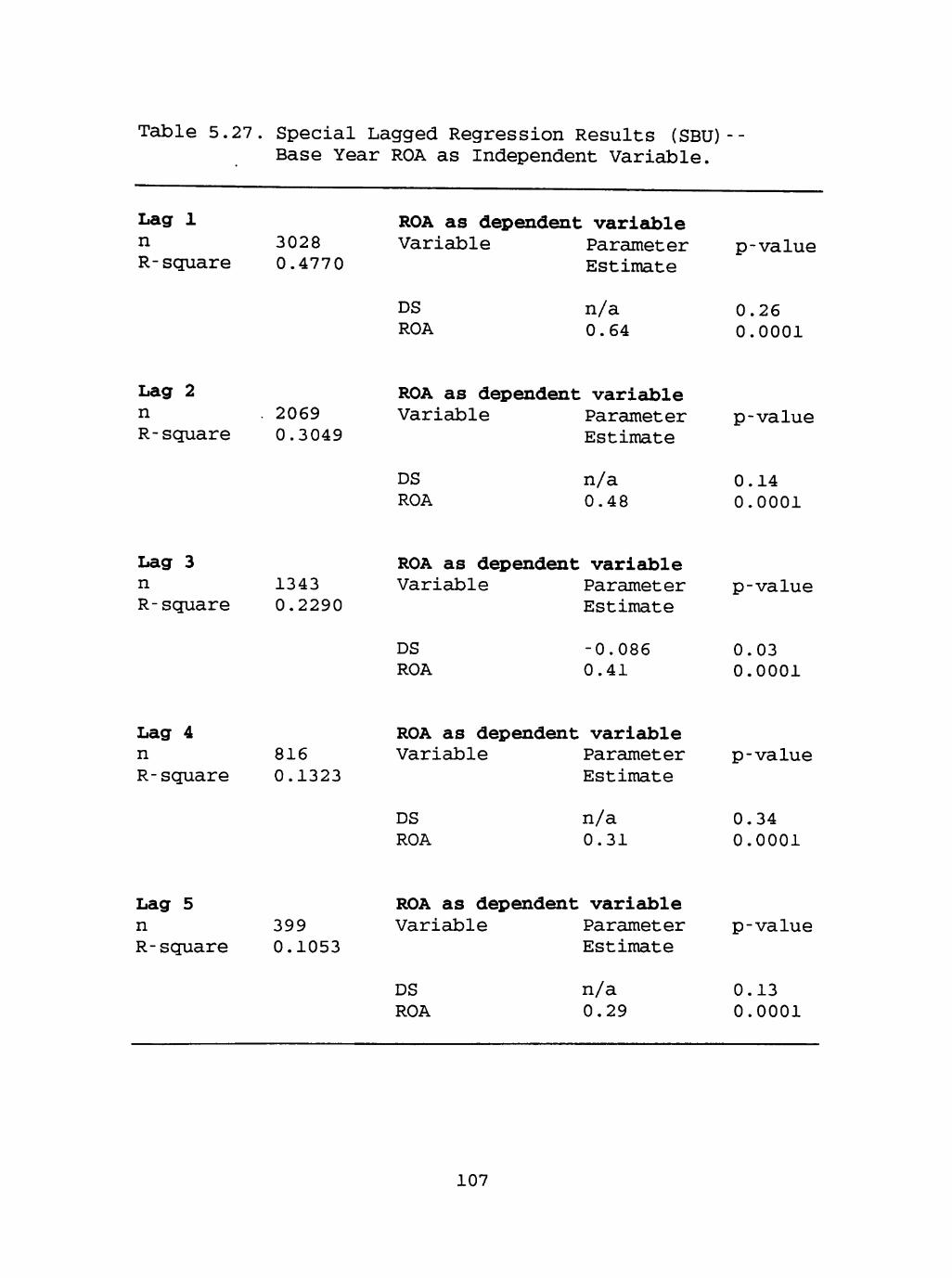

5.27 Special Lagged Regression Results (SBU)--Base Year ROA as Independent Variable 106

5.28 Special Lagged Regression Results (CORP)--Base Year ROA as Independent Variable 107

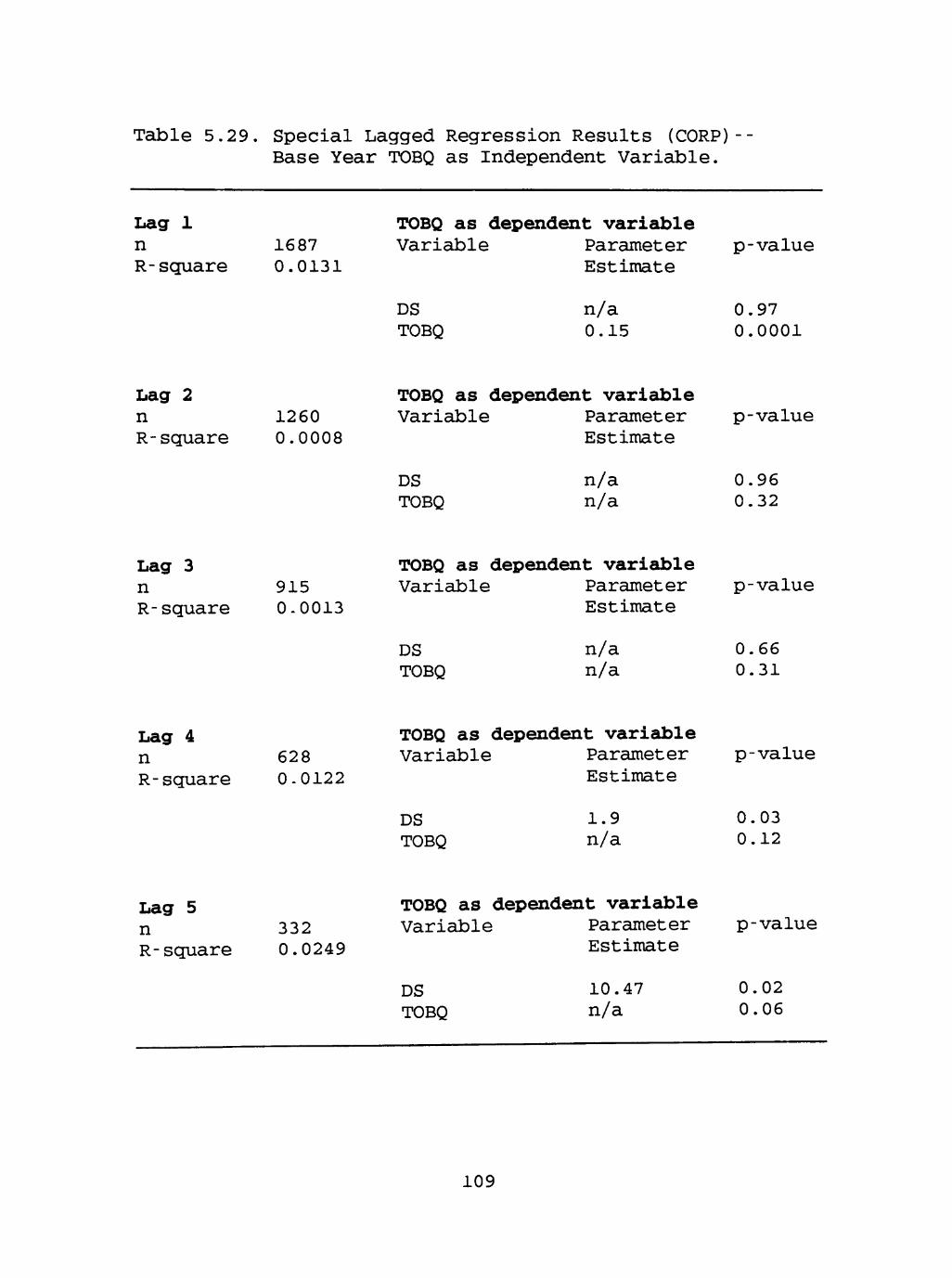

5.29 Special Lagged Regression Results (CORP)--Base Year TOBQ as Independent Variable 108

5.30 Concurrent and Lagged (0-2) Regression Results (SBU)--All Variables Included (ROA as Dependent Variable) 109

5.31 Concurrent and Lagged (3-5) Regression Results (SBU)--All Variables Included (ROA as Dependent Variable) 110

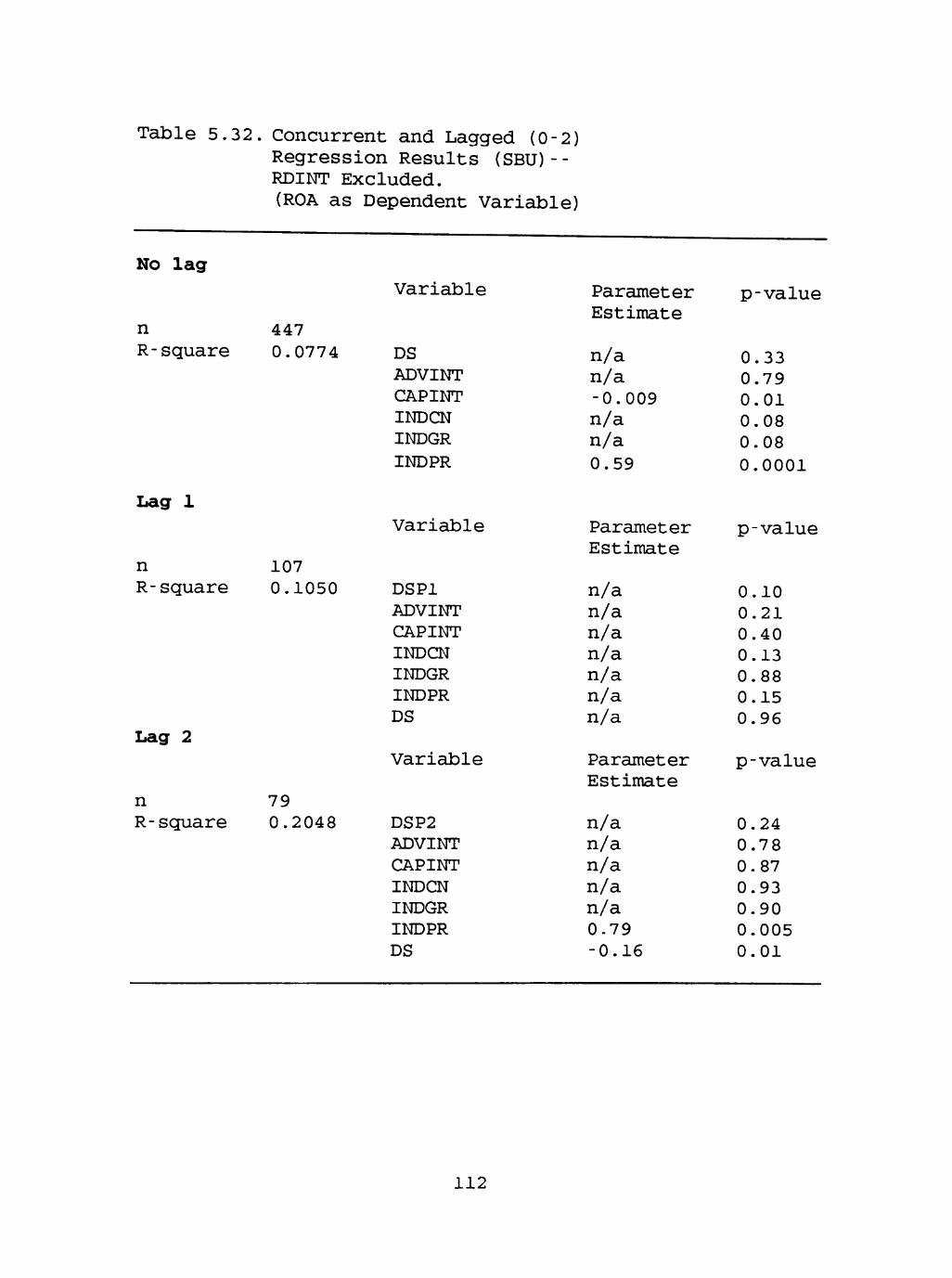

5.32 Concurrent and Lagged (0-2) Regression Results (SBU)--RDINT Excluded (ROA as Dependent Variable) Ill

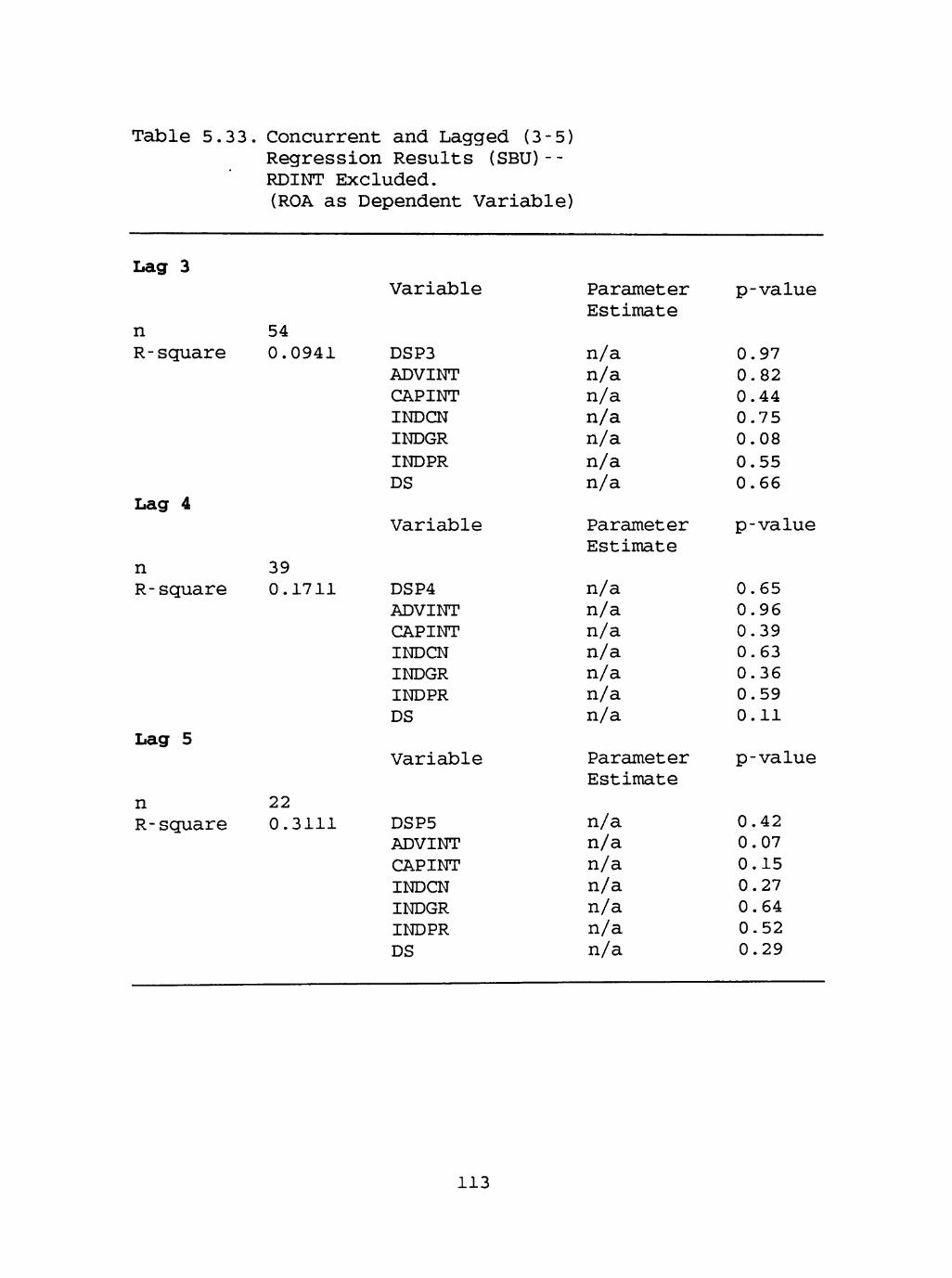

5.33 Concurrent and Lagged (3-5) Regression Results (SBU)--RDINT Excluded (ROA as Dependent Variable) 112

Vlll

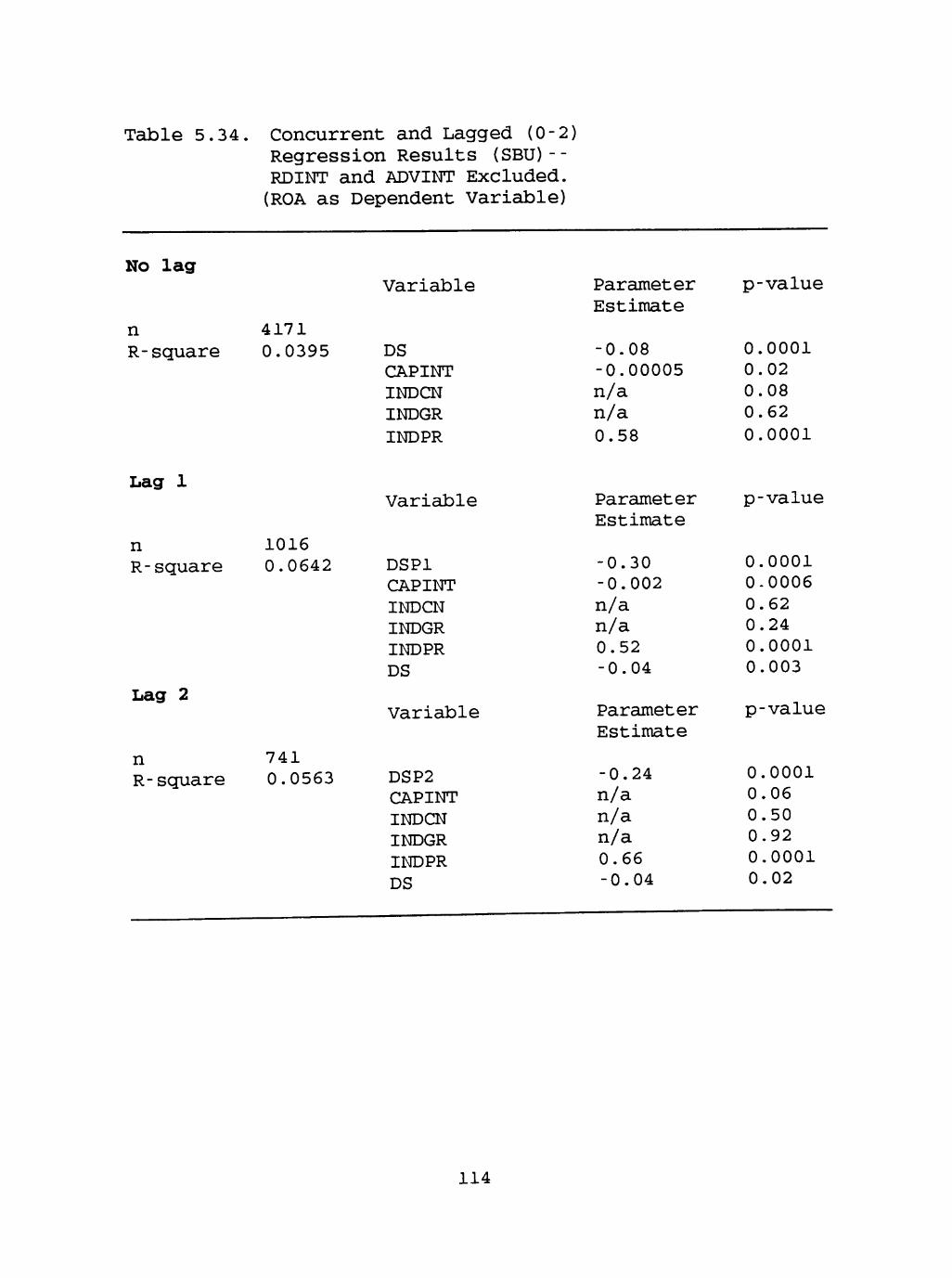

5.34 Concurrent and Lagged (0-2) Regression Results (SBU)--RDINT and ADVINT Excluded (ROA as Dependent Variable) 113

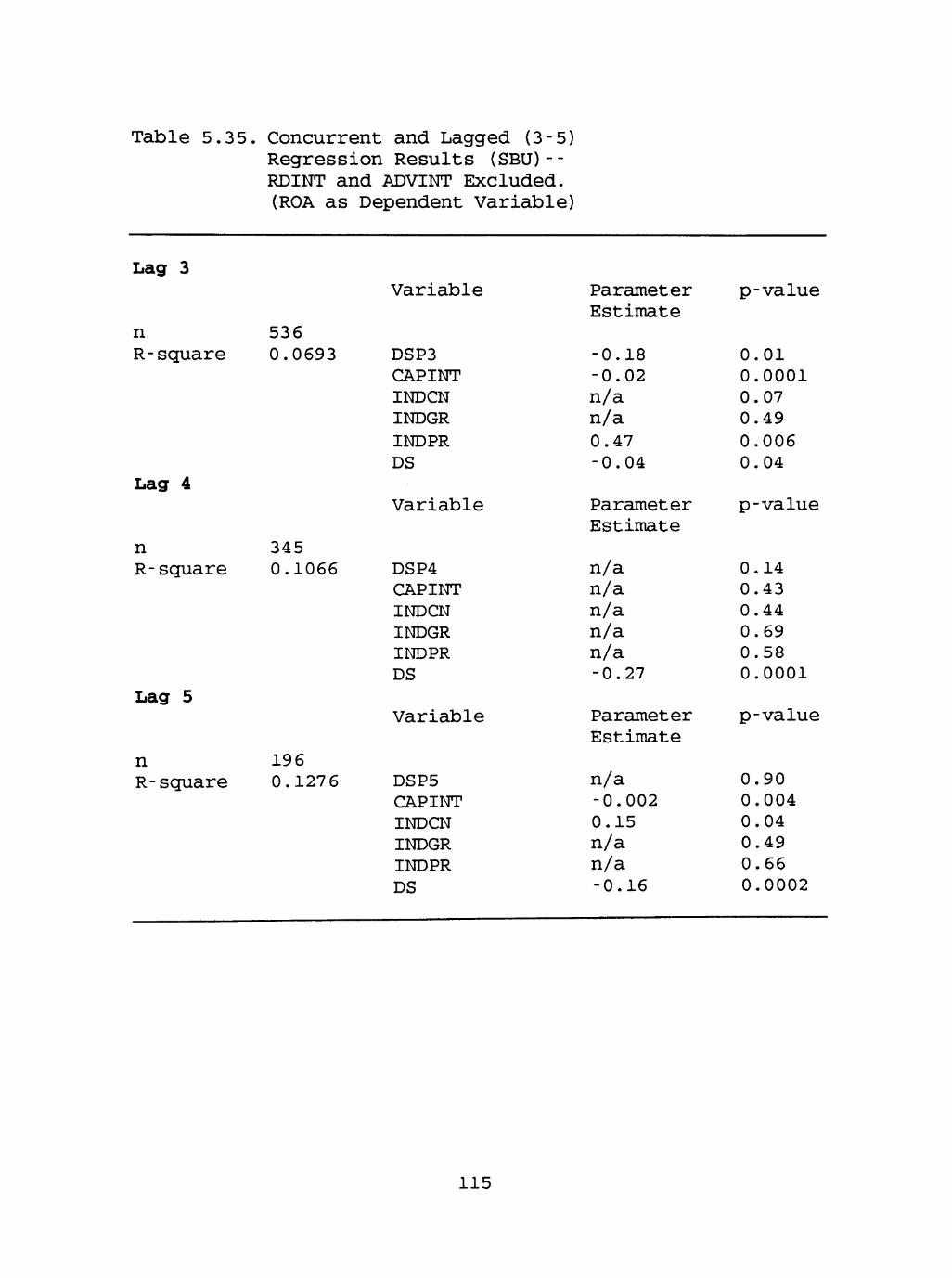

5.35 Concurrent and Lagged (3-5) Regression Results (SBU)--RDINT and ADVINT Excluded (ROA as Dependent Variable) 114

5.36 Concurrent and Lagged (0-2) Regression Results (CORP)--All Variables Included (ROA as Dependent Variable) 115

5.37 Concurrent and Lagged (3-5) Regression Results (CORP)--All Variables Included (ROA as Dependent Variable) 116

5.38 Concurrent and Lagged (0-2) Regression Results (CORP)--RDINT Excluded (ROA as Dependent Variable) 117

5.39 Concurrent and Lagged (3-5) Regression Results (CORP)--RDINT Excluded (ROA as Dependent Variable) 118

5.40 Concurrent and Lagged (0-2) Regression Results (CORP)--RDINT and ADVINT Excluded (ROA as Dependent Variable) 119

5.41 Concurrent and Lagged (3-5) Regression Results (CORP)--RDINT and ADVINT Excluded (ROA as Dependent Variable) 120

5.42 Concurrent and Lagged (0-2) Regression Results (CORP)--All Variables Included (TOBQ as Dependent Variable) 121

5.43 Concurrent and Lagged (3-5) Regression Results (CORP)--All Variables Included (TOBQ as Dependent Variable) 122

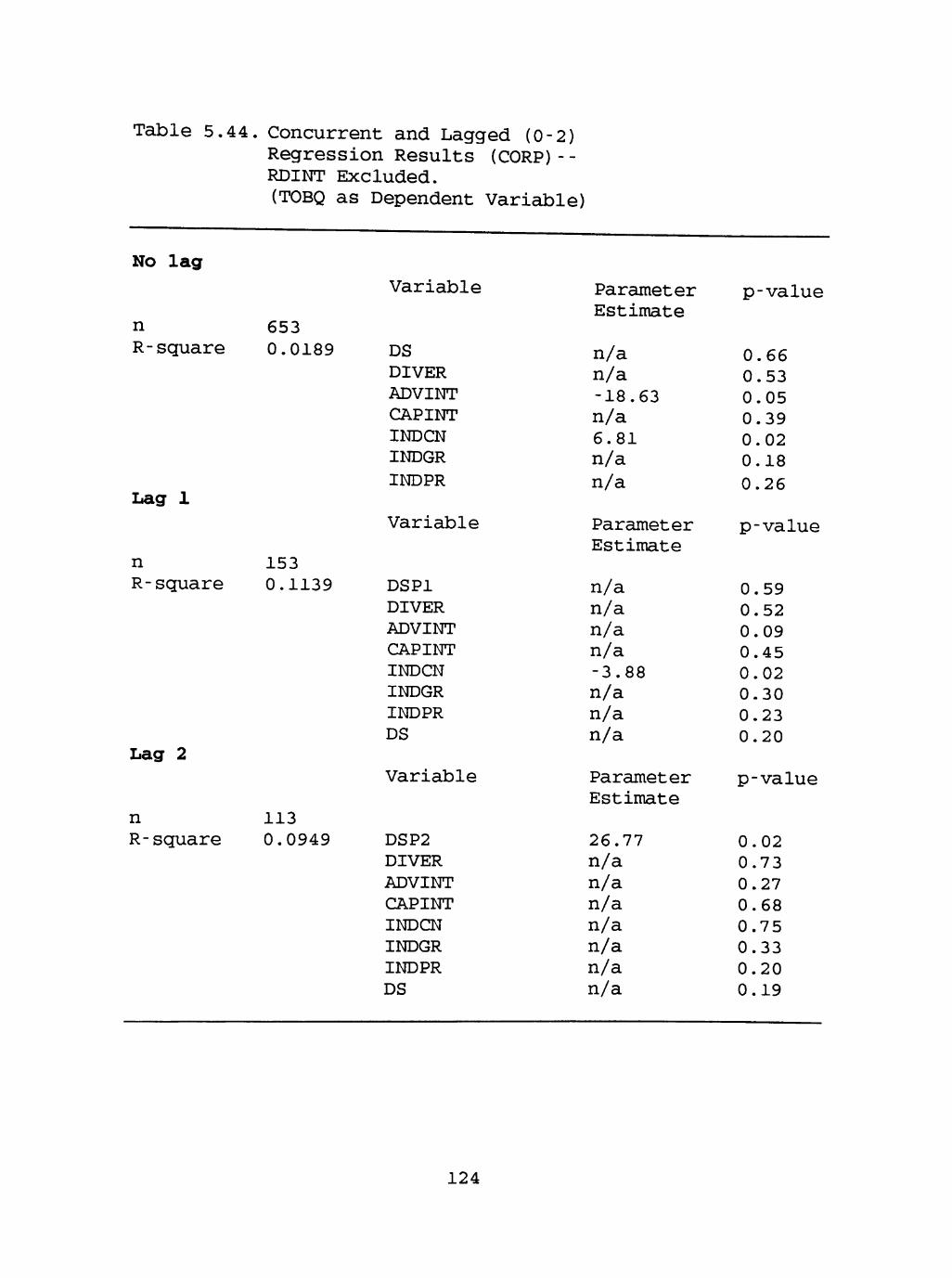

5.44 Concurrent and Lagged (0-2) Regression Results (CORP)--RDINT Excluded (TOBQ as Dependent Variable) 123

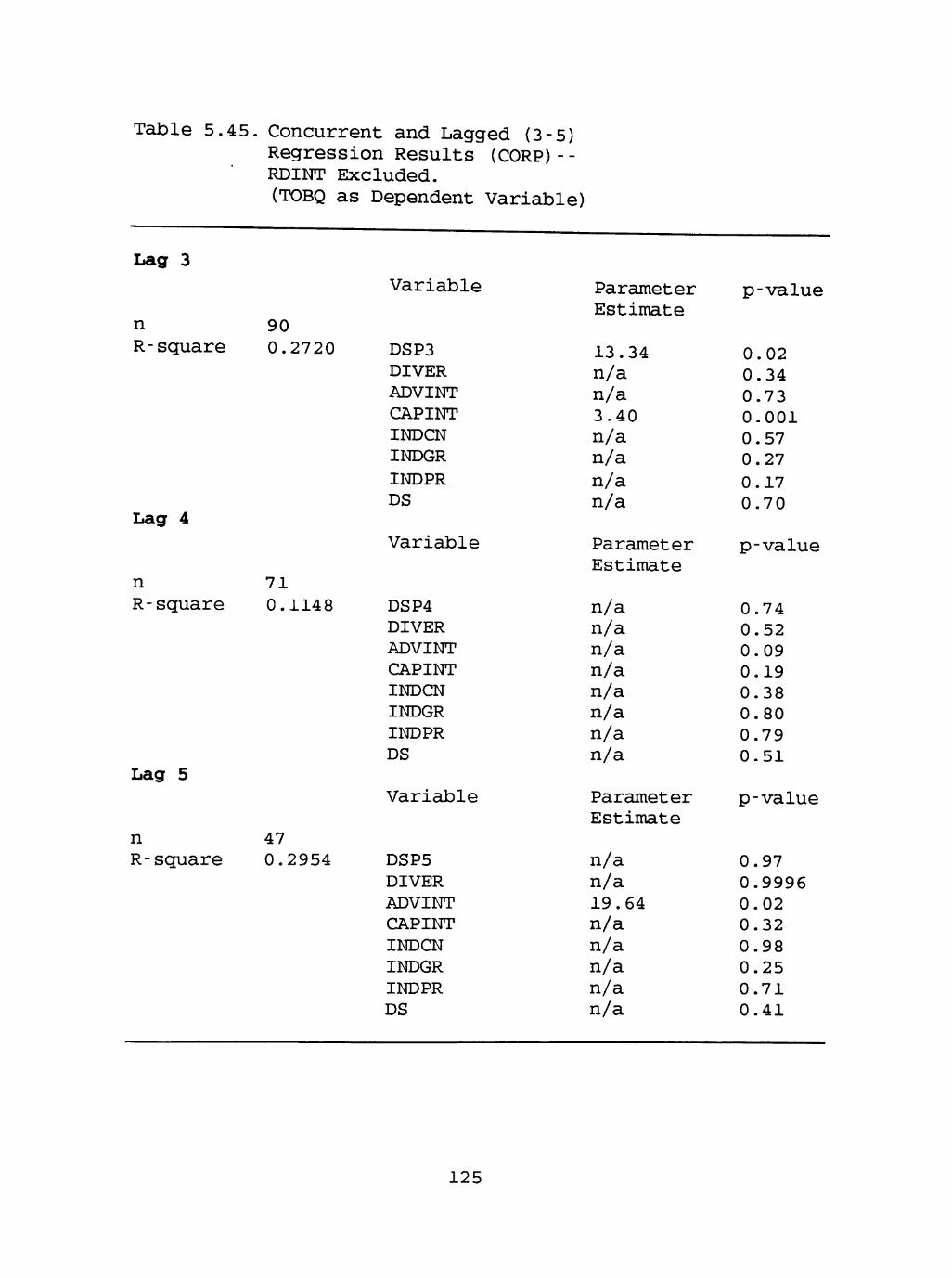

5.45 Concurrent and Lagged (3-5) Regression Results (CORP)--RDINT Excluded (TOBQ as Dependent Variable) 124

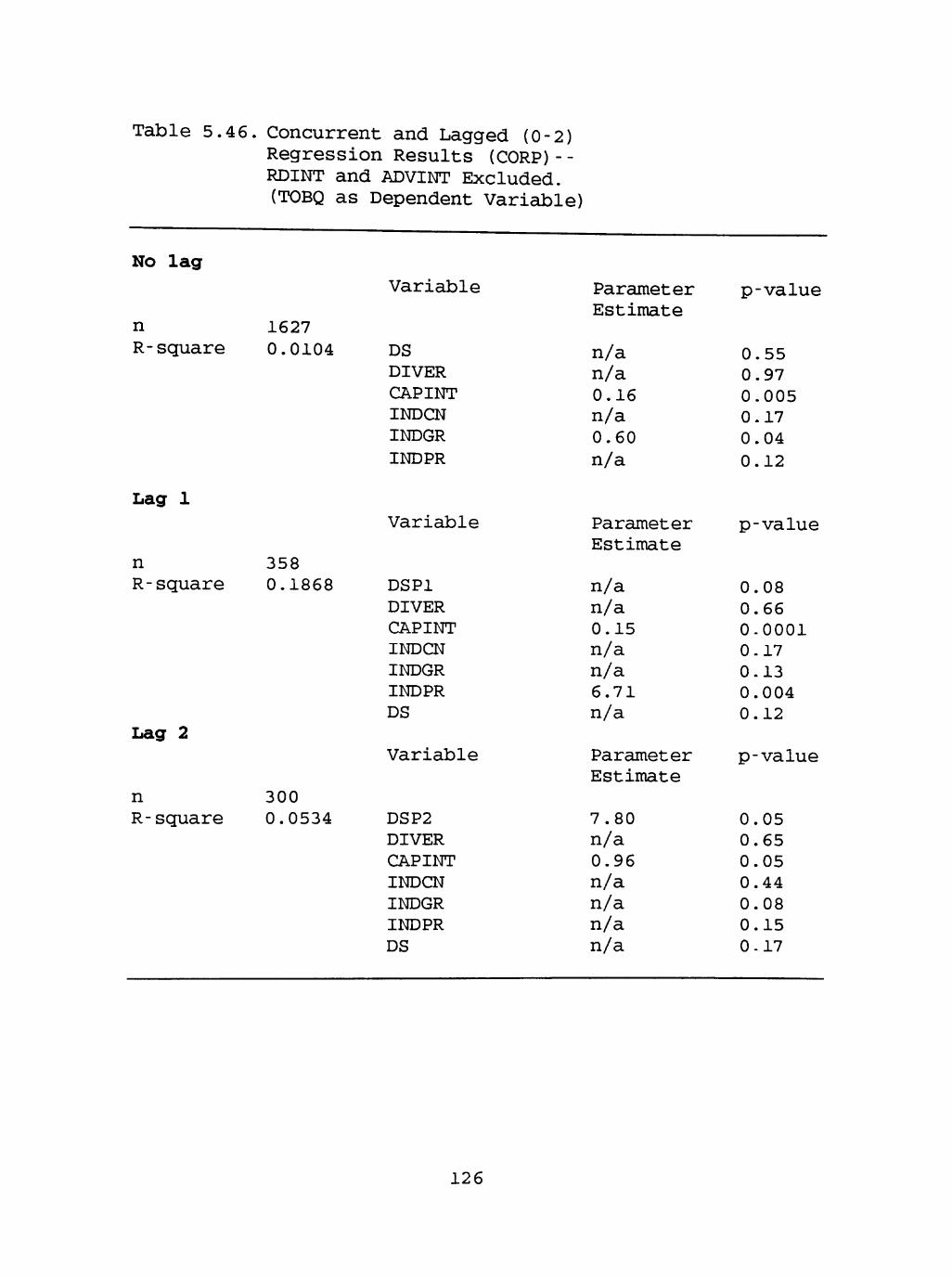

5.46 Concurrent and Lagged (0-2) Regression Results (CORP)--RDINT and ADVINT Excluded (TOBQ as Dependent Variable) 125

IX

5.47 Concurrent and Lagged (3-5) Regression Results (CORP)--RDINT and ADVINT Excluded (TOBQ as Dependent Variable) 126

CHAPTER I

INTRODUCTION

This Study explores the relationship between downsizing

and performance. In this study, downsizing is characterized

as a facet of organizational strategy for improving

performance (Cameron, Freeman, & Mishra, 1993). Although the

subtleties of defining organizational downsizing will be

discussed later, in this research downsizing is defined as an

intentional set of activities designed to improve

organizational performance, and which involves reductions in

personnel (Cameron, Freeman, & Mishra, 1993).

Since the 1980's through the present time, around ten

million jobs have been eliminated in the U.S. (Budros, 1997).

Organizational downsizing has been called a "key feature" of

the system of "new capitalism," an economy characterized by

international competition, deregulation of industries, and

technological change (Budros, 1997). It is not clear whether

downsizing does indeed improve profitability, since despite

the prevalence of downsizing, it has not been studied much

(Cameron, 1994). Budros (1997) points out that expectations

are that downsizing will improve performance, and that

companies that downsized are generally seen as positive role

models and acquire social benefits, whether or not operating

efficiencies are achieved. However, there are critics of

downsizing who point out various adverse effects, as well as

more emphasis on growth in recent years (Budros, 1997).

Nevertheless, numerous companies have undergone varying

degrees of downsizing. Over eighty-five percent of the

Fortune 1000 corporations have undergone downsizing (Cameron,

Freeman, & Mishra, 1991). For example, companies that have

downsized extensively include Eastman Kodak (five times in

seven years eliminating over 12,000 jobs). Zenith Electronics

(50 percent of its workforce), UNISYS (50 percent), ITT (over

40 percent), K-Mart (over 20 percent), Peat Marwick (over 20

percent), AT&T (over 10 percent), Sears, Roebuck, & Co. (over

10 percent),and Westinghouse (6 percent) (Cameron, Freeman, &

Mishra, 1991; Lesly & Light, 1992). The downsizing trend is

continuing; among companies with current and future plans of

downsizing are IBM, Xerox, the Postal Service, TRW, Inc., and

General Motors (Cascio, 1993). The 1990's are still filled

with reports of more downsizing (e.g., Uchitelle &

Kleinfield, 1996).

The downsizing issue continues to be a topic of interest

for the nation and the business world. For example, one of

the largest and best known computer businesses in the world,

IBM, has been forced to reevaluate its strategies for

competing in the global market. In an interview with Fortune

(Kirkpatrick, 1993), IBM's new CEO Lou Gerstner says his

first priority is to "get the company right-sized," which

implies more downsizing. Gerstner also says that the

decision on the magnitude and placement of further downsizing

will be at the business unit level. It is not only premiere

U.S. corporations that are facing this phenomenon; Daimler-

Benz of Germany has also announced plans for a workforce

reduction.

The streamlining of organizations has become a

perceived necessity in gaining a competitive edge in the

marketplace; however, it is not clear whether downsizing does

indeed improve profitability. Lesly and Light (1992) point

out that although some downsized companies (e.g., Unisys

Corp., which also narrowed its market) have benefited, many

restructured and so-called "lean" corporations do not appear

to have garnered the long-term expected earnings benefits

from their work-force reductions (e.g., Eastman Kodak, Zenith

Electronics, Sears Roebuck). Interestingly, only one of the

top ten in Fortune's 1993 Ranking of Most Admired

Corporations has fewer employees than it did 5 years ago

(Henkoff, 1993).

Despite the prevalence of downsizing in the U.S. and

overseas, studies of downsizing are relatively sparse in the

strategy and organizational theory literature. The

consequences of downsizing on micro-level issues (e.g.,

usually in human resources and organizational behavior areas)

have, however, been researched, but only to a degree. For

example, studies have been done on survivors of work-force

reductions, and on relating layoffs with motivation (e.g..

Brockner, Davy, & Carter, 1988), self-esteem (e.g., Brockner,

Grover, O'Malley, Reed, & Glynn, 1993, Brockner, 1995;

Daniels, 1995), and organizational commitment (e.g., Wong &

Davis, 1993; Wong & McNally, 1994) . Other work has been done

on how to manage the effects of workforce reductions on those

who remain with the organization, including steps to be taken

before, during, and after the layoffs (Brockner, 1992).

Maintaining the morale of survivors is discussed as an

essential element in successfully implementing mergers and

acquisitions and the attendant layoffs (Gutknecht & Keys,

1993). The phenomenon of survivor guilt has also been

explored (e.g., Brockner, Grover, Reed, DeWitt, & O'Malley,

1987) . Specific issues such as Total Quality Management have

been considered in the literature in relationship to

downsizing (Niven, 1993).

Research on motives behind downsizing actions is just

now beginning to emerge. Kozlowski, Chao, Smith, and Hedlund

(1993) point out that there are many causes and intended

goals associated with downsizing. Harrison (p. 40, 1994)

suggests that downsizing could be explained by diverse

reasons such as "vertical disintegration" of large firms

seeking to escape "bad business climates," an overall shift

from large manufacturing firms to smaller service firms, and

conglomerates trying to return to their core competencies.

Many publications focus on the management of effective

downsizing, attempting to identify processes to implement

downsizing successfully (e.g., Tomasko, 1987; Cameron,

Freeman, & Mishra, 1991; Hendricks, 1992; De Meuse, Bergmann,

Sc Vanderheiden, 1997). Most of the literature on

implementation does not, however, address post-downsizing

organizational performance. In the view of some strategists,

performance issues should be included for research questions

to be of any consequence (Meyer, 1991). There are very few

systematic studies published on the precursors, effects, and

strategies associated with organizational downsizing

(Cameron, Freeman, & Mishra, 1991) . The most extensive and

systematic study of organizational downsizing is that of

Cameron, Freeman, and Mishra (1993), an in-depth field study

including perceptual performance criteria.

Another issue concerning the study of downsizing is that

of divestiture versus work-force reduction. Most of the

strategy literature on restructuring examines divestiture and

diversification refocusing as opposed to work force

reduction. Other studies consider size, but often in terms

of sales or assets instead of number of employees. The

operationalization of size varies greatly by study.

Organizational-size research has been reported in the

organizational theory literature concerning decreasing

financial resources and/or work-force reduction (e.g., see

McKinley, 1992; Sutton & D'Aunno, 1989, 1992). However, in

the organizational theory literature, the dependent variable

in most models is structural (e.g, administrative intensity)

in nature, rather than performance based.

Ginsberg (1988) characterizes empirical research in the

strategy field as addressing two basic questions: (1) "what

factors influence the occurrence of various types of

changes"; and (2) "what are the performance outcomes of these

various types of change." Ginsberg (1988) points out that

the strategy researcher, at some point, must examine

performance outcomes, as improving performance is a basic

tenet of strategic management (Venkatraman & Ramanujam,

1986). This study contributes to the field by focusing on

performance outcomes after downsizing occurs in corporations.

Most of the references to downsizing include anecdotal

evidence (with no clear support for either a negative or

positive effect on profitability) as to the impact of

downsizing. Given the limited amount of theoretical and

empirical work on the very topical and timely issue of

downsizing, especially linked with performance issues, the

primary research question for this study is: What is the

impact of downsizing on corporate and strategic business unit

economic performance, controlling for market conditions?

The use of comprehensive multi-year, multi-industry data

for the examination of performance issues should provide a

beginning to understanding the growing (in both occurrence

and importance) phenomenon of downsizing.

Significance of the Study

This study is significant for the strategic management

field, as well as for the field of organizational theory. It

is concerned with the effect of a strategic change (workforce

reduction) on the performance of organizations, which is of

importance to the strategy field. It also addresses issues

of size, which are clearly of interest in the field of

organizational theory.

The study employs multivariate analysis for the

inclusion of many specific variables that could have an

impact on economic performance of an organization. It uses a

large multi-industry database, which has a variety of

organizations of different sizes. The study provides

information on the relationship between downsizing and

profitability and on the impact of downsizing on the

organization. In summary, the study addresses an issue that

is currently short on theoretical concepts but is of great

importance, not only to the business world, but also to the

national economy.

Limitations

There are some limitations in this study arising from

the use of secondary data bases. For example, the researcher

cannot influence what types or forms of data are collected.

Some variables may not be available in the data base, and

there is little contextual information. Another limitation

to the study is that there is no hypothesis testing; however,

a tentative empirical model is tested.

Organization of the Dissertation

This dissertation has six chapters. Chapter I is the

Introduction. Chapter II contains a review of the relevant

literature in several related subfields of strategy and

organizational theory. Chapter III discusses the rationale

for the study. Chapter IV shows the methodology used, the

regression equations, and the operationalization of the

variables. Chapter V presents the results of the data

analysis. Chapter VI discusses the conclusions based on the

results, and offers implications and strengths and

limitations of the study. Chapter VI closes with directions

for future research.

8

CHAPTER II

LITERATURE REVIEW

The literature reviewed for this study, in the areas of

organizational size, decline, turnaround and retrenchment,

corporate restructuring, and divestiture does not reflect a

consensus on how to conceptualize downsizing. There have

been few empirical research studies on downsizing, and very

little theoretical development. However, there are several

publications geared to practitioners on the implementation of

downsizing.

In addition, there is a small body of literature that

concerns itself with micro-level issues of downsizing, such

as the effect on layoff survivors and how managers should

treat survivors to increase work motivation (e.g., see

Brockner, Grover, O'Malley, Reed, & Glynn, 1993; Brockner,

1995; Daniels, 1995). Other researchers are looking at

layoffs, plant closings, and worker displacement on a

national level (see Hansen, 1988). Hansen (1988) is

concerned with legislation for a displaced worker adjustment

program as part of a comprehensive national employment and

training policy.

The strategic management literature has only just begun

to address the issue of downsizing per se; it appears that

downsizing itself may not have been viewed as a strategic

change. The literature on decline (e.g., see Cameron,

Sutton, & Whetten, 1988; D'Aveni, 1989, Weitzel & Jonsson,

1989) suggests that downsizing is not synonymous with

decline; rather downsizing may be a strategic response to

organizational decline (Greenhalgh, Lawrence, & Sutton, 1988)

or turbulence in the environment.

The corporate restructuring literature generally does

not acknowledge downsizing specifically as an aspect of

restructuring; it instead focuses on asset restructuring

(acquisitions and divestitures), capital restructuring

(infusion of debt), and management restructuring (changes in

organizational structure) (Singh, 1993). In this literature,

downsizing possibly may often be seen as an effect of

restructuring (Bowman & Singh, 1990; Hoskisson, Hitt, & Hill,

1991).

In spite of the scarcity of research on the impact of

downsizing on organizational economic performance, workforce

reduction is viewed as part of the process necessary for

long-term organizational improvements (Cascio, 1993). Many

popular business books and journals give advice to "cut out

the fat" and "get lean and mean" (Cascio, 1993). Tom Peters

(1992) argues for "rethinking scale," and that "big is

dead."

However, some doubt is emerging as to whether the

anticipated economic results of downsizing actually

materialize (Cascio, 1993; Lesly & Light, 1992). Studies by

consulting firms are showing that in many companies that have

10

downsized, expenses have not been reduced adequately, profits

have not increased as expected, and stock prices have not

necessarily gone up over the long term (AMA, 1993; Cascio,

1993; Lesly & Light, 1992). For example, the American

Management Association's (AMA) 1993 Survey on Downsizing

showed that fewer than half of the surveyed organizations

that had downsized since 1988 reported increased profits.

The question of whether downsizing has a positive or

negative relationship with corporate performance has not been

resolved. The American Management Association's (AMA) 1993

Survey on Downsizing showed that on the average, over the

last five years, 45% of the companies surveyed had downsized,

with a five-year average of a 10% reduction of the workforce.

Fewer than half of the surveyed organizations that had

downsized since 1988 reported increased profits. The AMA

(1993) points out that profit levels are affected by many

other variables in addition to workforce reductions. In

contrast, most surveys by consulting and investment firms

usually investigate only a bivariate relationship between

downsizing and profits, leaving out a host of other important

variables that may affect performance.

Neither the practitioner nor the academic literatures

offer theoretical frameworks in which downsizing may be

studied. Indeed, Cameron, Freeman, and Mishra (1993)

recommend that at this early stage of organizational

downsizing study, researchers should be building theories.

11

particularly including the association of downsizing with

successful organizational performance. The impact of

downsizing should be examined in light of strategic moves

(both corporate and SBU), as well as changes in the

environment (e.g., industry structure).

Organizational Size

This section reviews the relevant literature on

organizational size, primarily in the field of organizational

theory. Organizational size is one of the three core

contingency variables (along with technology and the

environment) studied extensively in the organizational theory

field (Bluedorn, 1993). Several basic propositions arose

from the dominant theoretical position of size; the

propositions were concerned with the relationship between

size and organizational structural variables, such as

structural differentiation, administrative proportion,

centralization, and formalization (Bluedorn, 1993). Some

studies have dealt with the relationship between size and

other variables, such as employee pay (Mellow, 1982; villemez

& Bridges, 1988), executive compensation (Gomez-Mejia, Tosi,

Sc Hankin, 1987; Rajagopalan & Prescott, 1990), and

absenteeism (Markham & McKee, 1991).

Other issues concerning size include diversification,

divisionalization, and innovation. There is a debate in the

organizational literature on whether size or diversification

12

strategy is more closely associated with divisionalization

(see Grinyer & Yasai-Ardekani, 1981; Child, 1982; Donaldson,

1982; Grinyer, 1982). Damanpour (1992) found a positive

relationship between size (measured in different ways) and

innovation in a meta-analytic study using 36 correlations.

It was found that the size-innovation relationship was

stronger when size was measured in terms of assets, rather

than number of employees. Damanpour (1992) also suggests

that there is a curvilinear relationship between size and

innovation.

However, there are relatively few studies that consider

performance and size. Christenson and Sachs (1980) found

that government size was positively correlated with perceived

quality of public services. Size was measured as: (1)

number of government employees in a county; (2) the ratio of

government employees to the total population of a county; and

(3) the number of public employees relative to the number of

administrative units. They also found that number of

administrative units was uncorrelated with quality.

A meta-analysis by Gooding and Wagner (1985) showed a

positive correlation between size and performance (absolute

measures), but not between size and efficiency (relative

output/input measures). Results varied with the measure of

size. Performance was measured in various ways including

profits, sales, and number of clients. Size was measured as

number of employees, the log of the number of employees.

13

capacity, assets, and transactions. There was a positive

correlation with performance only when size was

operationalized as the log of the number of employees. No

correlation was seen when size was operationalized as the raw

number of employees, nor as assets. There was a negative

correlation when size was operationalized as capacity or

transactions. Gooding and Wagner (1985) also found that at

the subunit level (as opposed to the organizational level),

there was a negative correlation between size and performance

(depending on the operationalization of performance). It is

evident from the results of the meta-analysis that the

empirical evidence on the relationship between size and

performance is mixed.

Interestingly, an empirical study by Smith, Guthrie, and

Chen (1989) showed that size moderated the relationship

between strategy and firm performance, with strategy measured

using the Miles and Snow (197 8) typology. However,

performance was measured using self-report data. Size was

measured as number of employees.

A meta-analysis was done by Capon, Farley, and Hoenig

(1990) on the determinants of financial performance, relating

environmental, strategic, and organizational factors to

performance. The studies in the meta-analysis analyzed

performance at three levels: industry (7 3 studies),

corporate (205 studies, 163 in multiple industries), and

business (42 studies). Size itself (measured in a variety

14

of ways, usually in terms of sales or assets, but never as

downsizing) appeared to be unrelated to financial performance

(Capon, Farley, & Hoenig, 199 0).

A study examining the relationship between size and

change (measured as expansion into new markets) found an

inverted U-shaped relationship between size and change for

some markets (Haveman, 1993). Haveman (1993) suggests that

size should not be conceptualized as solely an organizational

characteristic, as internal and external constraints vary

among settings, which could affect the relationships under

study.

An empirical study on diversification and corporate

restructuring by Chang (1996) showed that larger firms can

improve performance more than smaller firms, with various

entry and exit strategies. However, firm size was measured

as the log of total assets, rather than in terms of numbers

of employees.

The concept of downsizing certainly has some connection

with the literature on organizational size. However, most

studies on size do not consider changes in size within

organizations, which is inherent in any study of downsizing.

The operationalization of size is also open to question in

the literature; size is not often measured in terms of number

of employees. The literature does not thoroughly address the

relationship between size and performance, as there is little

agreement seen in empirical studies. Additionally, the

15

operationalization of performance is usually perceptual,

rather than objective, in nature.

Decline in Organizations

This section briefly considers the literature on

organizational decline. Within the stream of research on

phases of the organizational life cycle, particularly on

birth, death, and decline (Bluedorn, 1993), the decline phase

has emerged as a very important topic for business

researchers. The high number of overall business failures

and the extensive loss of jobs in the manufacturing

industries (Cameron, Sutton, & whetten, 1988) underscores the

significance of studying decline. However, organizational

decline has been defined in many ways, often ambiguously

(Cameron, Sutton, & Whetten, 1988). Also, downsizing and

retrenchment have frequently been confused with decline.

Cameron, Sutton, and whetten (1988) have suggested a

working definition of organizational decline that

distinguishes responses to decline from decline itself. In

their definition, deterioration of the organization's

adaptation to the microniche leads to reduction of resources

within the organization.

There are organizational, group, and individual

responses to organizational decline. Cameron, Sutton, and

Whetten (1988) clearly consider downsizing, along with

turnaround, divestment, and executive succession, as possible

16

organizational responses to decline. It is interesting to

note that downsizing could occur in response to either K-type

(shifting market demand results in a declining population) or

r-type (where the population is stable or growing) decline.

(See Wilson [1980] for detailed writings on K-type and r-type

deterioration.)

Zammuto and Cameron (1985), in a model based on

population ecology, propose four types of decline: erosion

(continuous change in niche size), contraction (discontinuous

change in niche size), dissolution (continuous change in

niche shape), and collapse (discontinuous change in niche

shape). They suggest that organizations in niches of

decreasing size would be likely candidates for cutback

activities (i.e., a type of structural adjustment). Zammuto

and Cameron (1985) also propose five domain-altering

strategic responses: domain defense (buffering from the

environment), domain offense (expanding markets or product

line), domain creation (diversifying or innovating), domain

consolidation (reducing size of domain and peripheral

actions), and domain substitution (replacing domain when

carrying capacity of original niche goes to zero).

Downsizing activities could be part of a domain consolidating

strategy, with change by deletion as the primary structural

adjustment, in response to a contraction type of decline.

Kozlowski, Chao, Smith, and Hedlund (1993) have combined

the Zammuto and Cameron (1985) dimensions with a model of

17

downsizing decision process formulated by Freeman and Cameron

(1993) . Freeman and Cameron (1993) use the Tushman and

Romanelli (1985) notions of convergence (long time spans of

incremental change) and reorientation (shorter periods of

discontinuous change). Kozlowski, Chao, Smith, and Hedlund

(1993) suggest that environmental variation can affect the

downsizing decision process, and have proposed that

convergent forms of downsizing are more likely to be

associated with changes in niche size, whereas reorientation

forms of downsizing are more likely to be associated with

changes in niche shape. DeWitt (1993) presents a normative

model of downsizing implementation, which includes four

downsizing strategy alternatives to be used when an

organization is facing organizational and/or environmental

decline. The strategies vary in terms of domain and

structural changes. However, the above models are primarily

concerned with processes, rather than performance outcomes,

of downsizing.

Cameron, Sutton, and Whetten (1988) further emphasize

the distinction between decline and downsizing or

retrenchment. Workforce reduction is a strategic response to

conditions caused by decline, but is not decline itself

(Greenhalgh, Lawrence, & Sutton, 1988). Furthermore,

downsizing can be either functional or dysfunctional

(Cameron, Sutton, & Whetten, 1988). If the wrong strategy is

chosen, or a strategy is poorly implemented, further erosion

18

in organizational adaptation and resource flow may occur. On

the other hand, downsizing could signal to customers and

stockholders that the organization is responding correctly to

decline. Cameron, Sutton, and Whetten (1988) point out that

a majority of Fortune 500 companies have downsized to some

degree, regardless of their objective growth or decline

pattern.

There is little integrative work on the consequences of

decline, with most of the literature relying on case studies

in single industries (Cameron, Sutton, & Whetten, 1988). Nor

has there been much work on the consequences of

organizational responses to decline, such as downsizing.

Ford (1980a) proposed a conceptual framework for looking at

the structural changes in declining organizations, where the

occurrence of structural hysteresis is explained. Ford

(19 80a) suggests the relationship between size and structure

is different depending on whether the organization is growing

or declining, but downsizing itself was not considered, and

performance outcomes were not included.

Some of the work that has been done on decline is

concerned with the relationship between decline and

organization variables such as technical and structural

complexity, administrative intensity (McKinley, 1987), and

centralization (Cameron, Whetten, & Kim 1987). McKinley

(1987) found that the positive relationship between

19

internal complexity and administrative intensity was

moderated by organizational growth and decline.

Ludwig (1993) investigated structural and organizational

adaptations of a population of a religious order under

conditions of decline (decreasing membership). In Ludwig's

(1993) study, retrenchment was characterized as either

cutback (percentage by which total organizational operations

were reduced) or reallocation (percentage of allocations to

individual units). Personnel changes were examined in terms

of admissions, departures, and transfers; while downsizing

itself was not addressed.

Others have investigated organizational decline in

relation to the environment. For example, Cameron, Kim, and

Whetten (1987) investigated the related constructs of

turbulence, stagnation and environmental decline. They base

their ideas on three streams of research: (1) organization-

environment literature, especially resource dependence; (2)

crisis-management literature; and (3) uncertainty literature.

They point out that the environment may or may not have

changed when a company goes into decline (as a reduction of

the resources within the organization itself). They also

view decline neutrally; i.e., the management of the decline

will determine positive or negative consequences (Cameron,

Kim, and Whetten, 1987).

An interesting study by Meyer (1982) showed that

organizations respond and adapt in many different ways to

20

environmental jolts (in this case, a doctors' strike

affecting numerous hospitals). Although hospital admission

and occupancy levels were drastically lowered, some hospital

administrators used employee layoffs as short-term solutions,

while others did not.

Harrigan (1980) suggests that firms in declining

industries follow different strategies based on environmental

traits. Divestiture is shown as part of one strategy (early

exit), but downsizing is not mentioned.

Hambrick and D'Aveni (1988) looked at dynamics of

corporate failure where poor performance was a significant

feature of a downward spiral. Weitzel and Jonsson (1991)

provide a model of decline that may serve as a frame of

reference for managers to try to ameliorate or reverse the

downward spiral.

Some researchers chose to study part of the process of

decline by investigating retrenchment as a response to

financial decline and also as an initial phase of a

turnaround strategy (see Robbins & Pearce, 1992). Robbins

and Pearce (1992) roughly classify several activities,

including restructuring, downsizing, and downscoping, as

retrenchment. They use the term retrenchment to primarily

signify cost and asset reductions, and they briefly mention

"head count cuts" as one of the possible strategies in the

retrenchment stage of the turnaround response model.

However, in the empirical test of their model, they did not

21

operationalize retrenchment as workforce reduction; instead

they used reduction of total costs between two times, and net

reduction in assets between two times (Robbins & Pearce,

1992). Turnaround performance was considered as the net

change in ROI between two times.

Barker and Mone (1994) take issue with the contention

that retrenchment is a cause of turnaround (as Robbins and

Pearce [1992] maintain) and suggest that retrenchment is

instead a consequence of organizational decline. Barker and

Mone (1994) believe that how an organization executes its

downsizing or retrenching activities is more important to

turnaround (i.e., performance recovery), than the actual

initiation of retrenchment programs. Again, retrenchment in

the Barker and Mone (1994) empirical study, was

operationalized as reduction in assets or costs, rather than

reduction in personnel.

There is a growing debate in the strategic management

literature on the organizational significance of retrenchment

and downsizing. Pearce and Robbins (1994) assert that the

Barker and Mone (1994) research actually supports the

original Robbins and Pearce (1992) turnaround process theory

with retrenchment as its cornerstone. The question of

retrenchment value has not been resolved.

A later study by Barker and Duhaime (1997) avers that

although some empirical studies demonstrate performance

turnarounds for declining firms resulting from cutback

22

activities (i.e., retrenchment) which increase efficiency,

strategic reorientation is vital to the recovery process of

declining firms. They present a model where the extent of

strategic change varies with the need for and capacity of

declining firms to reorient their strategies. In their

model, firms must have weak strategic postures for strategic

change to be critical for turnaround; i.e., levels of

strategic health, as well as the amount of strategic change,

must be identified and measured for a definitive turnaround

study. They also point out that the causes (or types) of

decline should be controlled for (e.g., firm-based decline

vs. industry-based decline). For example, extensive

strategic change is seen in turnarounds from firm-based

decline, whereas, little strategic change is seen in

industry-based decline. The latter is described in the study

as operational turnaround based on asset and cost reduction

as discussed by Hofer (1980). Also, the capacity for

strategic change is important, and can be controlled for by

firm size and diversification profile.

There appears to be a need for more empirical research

and theory building. Special care should be taken in the

operationalization of variables, particularly when dealing

with downsizing specifically, as has scarcely been done.

The strategic and managerial consequences of

organizational decline were studied by D'Aveni (1989). The

consequences reflected threat-rigidity responses. Like

23

others mentioned in this section, D'Aveni (1989) makes a

clear distinction between decline and downsizing. D'Aveni

(19 89) defines organizational decline as decreasing internal

resource munificence over time. His definition of downsizing

involves changes of organizational size and scope, including

selling off fixed assets, or subsidiaries (e.g.,

divestiture), and reducing product-market domains. However,

he does not explicitly include work-force reduction in his

definition of downsizing, nor in his operationalization in

the study.

D'Aveni (1989) also maintains that while many declining

organizations downsize, "downsizing and decline do not always

occur simultaneously or at the same rate" (p. 57 8). He also

concludes that the effectiveness of downsizing depends on

environmental conditions. Downsizing may give the

organization time to wait for environmental improvement, but

does not necessarily guarantee turnaround (D'Aveni, 1989).

D'Aveni (1989) also concludes that downsizing may become a

habit, "providing an illusion of temporary well-being" (p.

600). He found that, contrary to the idea that downsizing

could be a factor in creating slack for diversification

efforts and strategic change, post-decline managerial

imbalances inhibited the use of funds garnered from

downsizing efforts for successful turnaround strategies.

Murray and Jick (1985) studied six underfunded hospitals

over a period of five years, and documented responses of the

24

hospitals. They propose a framework for organizational

decline management, providing managers with a problem-solving

approach to resource scarcity threats, while recommending to

researchers that a holistic view must be taken (and a multi-

method approach) when studying organizational decline.

Other researchers have looked at decline and

retrenchment issues in terms of turnaround and rejuvenation.

Some have offered prescriptions. For example, Hofer (1980)

offers a framework for designing turnaround strategies at the

SBU level, in response to major declines in performance (in

terms of decreasing profitability, sales, or market share).

Hofer (19 80) distinguishes between operational and strategic

turnaround. Cutting costs or assets is termed operational in

nature, but downsizing itself is not considered.

Stopford and Baden-Fuller (1990) differentiate between

corporate turnaround (finance and efficiency oriented) and

corporate rejuvenation (concerned with both efficiency and

creation of sustainable growth). Detailed industry and case

analyses yielded insights on how corporate rejuvenation was

accomplished. Holistic changes in structure, strategy,

systems, technology, and individuals were required for

sustainable corporate rejuvenation (Stopford & Baden-Fuller,

1990).

Greenhalgh (1982) believes organizational retrenchment

occurs in a situation where an organization fails to adapt or

the carrying capacity of an environmental niche is reduced.

25

The organization then responds by cutting back its scale of

operations, and the size of the workforce is usually reduced

proportionally. Greenhalgh (1982) recommends an action

research program to facilitate comprehensive work force

planning and maintain organizational effectiveness.

Greenhalgh's (1982) action research program is designed

primarily to alleviate common problems arising from workforce

reduction, such as impaired job security. Organizational

effectiveness measures were self-report data on employee

productivity and propensity to leave the organization.

Much of the decline research looks at organizations

under conditions of decline and the concomitant unique

situational aspects and management challenges. Cameron,

Whetten, and Kim (1987) empirically explored a set of

dysfunctional characteristics (including many at the

individual and group levels) of organizations in decline.

Organizational dysfunctions associated with decline include

increases in conflict, secrecy, scapegoating, self-protective

behaviors, rigidity, turnover, decreases in morale,

innovativeness, participation, and long-term planning.

Weitzel and Jonsson (1989) point out an interesting

aspect of decline, in that cutback in terms of size (Whetten,

1980) does not necessarily negatively affect the survival an

organization. Whetten (1980) explains cutbacks in size as

rising from a reduction in the market in which the

organization operates, or from a decrease in the

26

organization's ability to compete with others in its market.

Weitzel and Jonsson (1989) suggest that cutback may not be a

form of decline; instead it may be "temporary adjustment that

is an appropriate response to the environment and enhances,

rather than diminishes, long-term viability" (p.93). This

would be in line with considering downsizing as a strategic

change, its organizational impact to be empirically

determined.

An interesting study by Wiseman and Bromiley (1996)

explores the relationship between decline, risk and

performance. They contrast two theoretical perspectives: a

decline theoretical approach which states that declining

organizations decrease risky activities, and the decreased

risk-taking leads to further poor performance, versus a risk

theoretical approach which states that declining firms take

more risks, and the increased risky behavior (again) leads to

more low performance. The ensuing empirical investigation

shows that when financial resources are decreased (i.e.,

organizational decline), risk-taking is increased, which in

turn leads to lower performance. Although performance is

central to the study, downsizing itself is not considered (as

financial resources are considered in terms of different

kinds of slack, none involving numbers of employees).

The literature on decline clearly shows that downsizing

and decline are not synonymous. Organizational downsizing is

often seen as a type of adaptation to organizational decline.

27

and is considered to be a subject of controversy (McKinley,

1993).

Organizational Size and Decline

This section extends the discussion on organizational

size and decline by briefly reviewing the relevant literature

on the relationship between decreasing size and

organizational decline. Much of the work in this area is

concerned with how to implement downsizing or workforce

reduction strategies. For example, Greenhalgh, Lawrence, and

Sutton (1988) introduce five strategies for workforce

reduction, along with sample tactics for implementing the

strategies. Further, they offer a set of propositions on

which strategies will be chosen, depending on labor

oversupply characteristics, and on contextual factors such as

skill levels, age and seniority, company structure

(multidivisional vs. unitary), and ownership.

Another study looked at the relationship between

decreasing organizational size and unemployment rates,

focusing on absenteeism (Markham & McKee, 1991). Ford

(1980b) found in a study of school districts that the

relationship between size and administrative components

differed depending on whether the study was conducted cross-

sectionally or longitudinally, and that the number of

personnel actually increased during periods of decline.

28

A debate in the organizational theory literature between

researchers (see Sutton & D'Aunno, 1989; McKinley, 1992;

Sutton Sc D'Aunno, 1992) concerns building a model of

workforce reduction. Sutton and D'Aunno (1989) focus on the

effects of decreased workforce size on organizational

structure, including degree of mechanistic structure, and

need for coordination and control.

McKinley (1992) criticizes the Sutton and D'Aunno (1989)

model, by questioning some of their assumptions. McKinley

(1992) believes that there are asymmetries between growth and

decline, both in magnitude and direction of structural

change. However, throughout the debate in the literature,

organizational performance is not addressed.

Corporate Restructuring

This section of the literature review discusses some of

the literature on corporate restructuring and its

relationship to the issue of downsizing. Some researchers

maintain that downsizing and downscoping are a result of

corporate restructuring (Hoskisson, Hitt, & Hill, 1991; Hitt

Sc Keats, 1992). Hoskisson, Hitt and Hill (1991) say that

downsizing and downscoping: (1) reduce vertical controls;

and (2) facilitate the development of strong core values in

the organization.

Hitt and Keats (1992) take an interesting approach and

show a reciprocal interdependence between restructuring and

29

strategic leadership. They define restructuring activities

as mergers and acquisitions, downscoping (reduction in the

number of businesses or products), and downsizing (reducing

operational slack, subtracting administrative layers).

Workforce reduction is seen as a component of both

downscoping and downsizing.

Hitt and Keats (1992) note three human resource

approaches in downsizing and downscoping activities:

decreasing numbers of upper-echelon, highly paid members of

the organization; eliminating middle management layers; and

across-the-board layoffs. Hitt and Keats (1992) point out

that effective restructuring does not necessarily mean

indeterminate workforce reduction; critical organizational

functions must be evaluated in light of long-term goals and

individual skills. They develop the argument that effective

strategic leadership during restructuring must balance short-

term needs with long-term growth and survival.

Other researchers characterize corporate restructuring

as change along the dimensions of assets, capital structure,

or management (Bowman & Singh, 1990, 1993) . Bowman and Singh

(1993) point out that restructuring decisions are a part of

long-term strategic planning. They also discuss the

multidimensionality of restructuring, and the need to

consider the consequences of restructuring on performance.

One type of restructuring, corporate refocusing, was

investigated by Markides (1992). He looked at the

30

relationship between reduction of diversification and

profitability, finding a curvilinear relationship- However,

his study did not include downsizing as a variable.

Markides* (1992) findings are in line with the evidence from

Hoskisson and Hitt (1990), work which shows a curvilinear

relationship between diversification and performance.

Markides (1995) later goes on to further investigate the

links between diversification, restructuring, and

performance. A decrease in diversification (by divestiture,

thereby refocusing on the firm's core business) by

overdiversifled firms was shown to lead to increased

profitability. The study defined restructuring as

refocusing, rather than share repurchasing, consolidation, or

leveraged recapitalization, nor was downsizing considered.

Lewis (1990) includes acquisition or divestiture,

replacement or reassignment of senior managers, reduction in

employee counts, and debt recapitalization as restructuring

activities, and contends that the degree of restructuring is

very important. Most articles and book chapters on corporate

restructuring appear to focus on issues such as valuation,

board of director involvement and corporate governance,

leveraged buyouts, employee stock ownership, executive

succession and compensation, and tax implications (e.g., see

Rock Sc Rock, 1990; Bowman & Singh, 1993) . Downsizing is

considered rarely, with possible limited significance, and

31

sometimes as a part of the aforementioned restructuring

issues.

An exception to the restricted use of downsizing as an

important research concept is the work of Bethel and

Liebeskind (1993). They show that blockholder ownership is a

significant determinant of corporate restructuring, as

operationalized as downsizing (percentage change in firm

sales and firm employees over a period of time). Bethel and

Liebeskind (1993) consider downsizing as a measure of

portfolio restructuring. They frame their study and results

within agency theory. Performance issues, however, were not

addressed.

Singh (1993) uses a trade definition of corporate

restructuring as he found no accepted definition in the

academic literature. The term restructuring is used for

"significant and rapid changes in the firm's assets, capital

structure, or organizational structure" (p. 147). Singh

(1993) reiterates the multifaceted and complex nature of

restructuring. He discusses many aspects of corporate

restructuring, including acquisitions, divestitures,

management buyouts, top management teams and boards, and

mergers; however, downsizing is not included.

Hatfield, Liebeskind, and Opler (1996) explore the

relationship between corporate restructuring and

specialization at the industry level. The study found that

while plant closings and industry entry were important.

32

corporate control transactions such as sell-offs had no

effect on aggregate industry specialization. Although plant

closing were dealt with, downsizing specifically was not.

A study by Chang (1996) examined firm entry and exit

decisions as searching for improved performance, in terms of

diversification and corporate restructuring. Poor

performance was shown to lead to exit, but not entry.

Divestiture (exit) was associated with improved performance,

but when industry profitability was taken into account, the

performance improvements disappeared. Although many

variables were included in the analysis, including firm size

(measured as log of total assets), and line of business size

(measured in terms of sales), downsizing was not considered.

Divestment

This section discusses the relevant literature on

divestment and any links with downsizing. Much of the

literature on divestitures is in the finance field, and very

specifically related to corporate investment and financing

decisions. Pre- and post-divestment organizational

performance was compared by divesting and non-divesting firms

by Montgomery and Thomas (1988) . Weak performers were shown

to be more likely to divest. However, downsizing was not

addressed.

Other work on divestment has focused on the performance

of the divested business -- spin-offs of the corporate parent

33

(see Woo, Willard, & Daellenbach, 1992). The results showed

that for both related and unrelated subsidiaries, post spin

off performance declined. Again, downsizing was not

included.

Duhaime and Grant (1984) point out that several branches

of the management literature are related to divestment, such

as life cycle theory, end-game strategies, stages of

corporate development, and corporate portfolio theory. Their

work focuses on the effects of various factors hypothesized

to be important influences on the divestment decisions of

large, diversified firms.

Factors influencing corporate divestment decisions

include business unit financial and competitive strength,

business unit interdependency, and corporate financial

strength relative to industry averages (Duhaime & Grant,

1984). General economic conditions and managerial attachment

did not influence corporate divestment decisions. Although

Duhaime and Grant (1984) define corporate divestment as a

decision to dispose a significant portion of assets,

downsizing did not play a role in their study.

Duhaime and Baird (1987) focused on business unit size

effects on divestment decisions. Divestment situations were

characterized as defensive (eliminating a unit with poor

performance) and aggressive (opportunity grabbing, or funding

for potential stars in the portfolio, gathering cash for

bankrolling a new product). Divestment reason was found to

34

be curvilinear; small and large units were divested for

defensive reasons, while medium units were divested for

aggressive reasons (Duhaime & Baird, 1987).

Questions were brought up as to the minimum efficient

size for business units in a corporation's portfolio.

Differences in size of business units was specifically

addressed in the Duhaime and Baird (1987) study, but

downsizing was not.

Wright and Ferris (1997) studied the effect of

divestment on corporate value (in terms of stock returns).

The study was based on agency theory and explored the effect

of public and private political forces on corporate strategy,

The effect of divestment of South African business units on

stock price was found to be negative, indicating that

managers do not always act in the best interests of firm

owners. Downsizing per se was not a part of the study.

Downsizing Practices

Much has been written on how to implement downsizing,

retrenchment, and work-force reduction; however, there are

few theoretical frameworks, nor are there many attempts to

associate various downsizing practices with actual

performance (especially objective measures). This section

offers a brief glimpse of some of the literature on "the

management of downsizing."

35

Hardy (1987) compared two organizations, one that

successfully retrenched, and another that was unsuccessful.

Hardy's (1987) observations were based on attempted plant

and hospital closings, rather than on the more general

concept of downsizing. Through interviews and documentation

analysis. Hardy (1987) suggests how to avoid the costs of

retrenchment by managing several issues, including awareness,

involvement, fair play, disclosure, understanding, and blame.

Another study on the management of workforce reduction

focuses on plant closings (Price & D'Aunno, 1983). Price and

D'Aunno (1983) take the perspective that exchange

relationships are the key to managing the transitions

associated with organizational decline. The links between

the company, transition managers, displaced workers, and the

community are examined through case studies. Prescriptions

are offered for the role of transition manager, including

such concepts as bounded rationality, top management's key

role, the necessity for a long-term view, and the management

of transactions rather than people.

A downsizing program is outlined by Appelbaum, Simpson,

and Shapiro (1987). In their paper, downsizing is defined as

a systematic reduction of a workforce. They develop ten

steps for the human resource department of an organization to

follow for successful downsizing, as well as ten very general

steps for top management, particularly the strategic human

resources executives, to take while planning the downsizing

36

action. Appelbaum, Simpson, and Shapiro (1987) view

downsizing as one possible tool for maintaining or improving

performance, and suggest that monitoring and evaluation are

important for success.

Organizational downsizing may be necessary for many

hospitals in the future (Mullaney, 1989). Mullaney (1989)

offers a case study of a hospital system facing decreasing

demand. Mullaney (19 89) recommends the establishment of a

steering committee, a productivity measurement system, and a

specific reduction-in-force plan.

Robertson (1987) presents two approaches to downsizing,

that have been successful in large organizations. The

product/service approach to downsizing determines which

products and/or services can be streamlined or eliminated,

and then staffing is reduced. The more commonly used

management systems approach is often budget driven, where

middle managers are given new resource allocations to define

the number of workers they can fund (Robertson, 1987) .

Robertson (1987) concludes with suggesting that a vision and

a process for integrating the vision are crucial for

successful downsizing efforts. Performance issues are not

discussed.

An attitudinal study on downsizing in manufacturing

firms was done by McCune, Beatty, and Montagno (1988) , which

sought to identify prescriptions for human resource practice,

Seniority was perceived to be the most used determinant for

37

layoffs, although worker performance was considered in many

non-union firms. Downsizing "programs" typically were

planned and implemented in less than two months.

Prescriptions for human resource managers included using

human resources as a competitive weapon, as well as

integrating human resource strategy with organization

strategy; developing a flexible workforce, adopting employee

stabilization techniques; and ensuring that downsizings are

strategically planned.

McCune, Beatty, and Montagno (1988) also call for future

research, particularly empirical investigation to examine the

validity of the many prescriptive models that abound. They

also suggest that research should be done on the consequences

of downsizing, especially in the areas of survivor reactions,

as well as career transitions.

Cameron, Freeman, and Mishra (1991) present six general

strategies for successful downsizing, gleaned from a field

study of U.S. automobile manufacturers. The "best practice"

strategies appear contradictory in some respects. For

example, successful downsizing was implemented from the top-

down, but was also initiated from the bottom-up; successful

downsizing was short-term and across-the-board, but also

long-term when systemically implemented. Other successful

downsizing practices included outplacement services and

family counseling.

38

The most interesting aspect of the Cameron, Freeman, and

Mishra (1991) study was the apparent contradictory strategies

of effective downsizers. Therein lies much fodder for future

research, especially along broad lines.

A study by De Meuse, Bergmann, and Vanderheiden (1997)

explicates several myths about corporate downsizing. The

first myth is that downsizing is widespread in the U.S., but

in fact, there has been more growth in jobs that loss of

jobs. However, restructuring has become a common corporate

way of life. The second myth is that downsizing improves

profitability, but in reality the savings are overestimated,

and the costs of downsizing are underestimated. The third

myth is that downsizing increases corporate responsiveness,

including communication within the company and with

customers, while there is actually much fear, anger and

resentment which impedes communication and involvement. The

fourth myth is that downsizing focuses on terminated

employees, yet actually those employees left in the company

often have lasting impact on the corporation after downsizing

(e.g., in terms of low morale, increased health costs,

decreased productivity, and increased numbers of lawsuits).

The fifth myth is that downsizing is a last resort, whereas

in reality, it is often implemented without considering

creative alternatives such as pay cuts, unpaid vacations,

shortened work weeks, job sharing, retraining for temporary

other jobs, etc. The sixth myth is that downsizing only

39

happens once, but if downsizing is used for cost cutting, it

will be likely used again. The seventh and final myth

discussed by De Meuse, Bergmann, and Vanderheiden (1997) is

that downsizing is an end in itself, while instead it should

be part of a complete organizational plan that focuses on the

firm after the downsizing occurs. The authors maintain that

downsizing can be implemented successfully if there is

effective strategic planning and communication programs in

place, as well as a supportive corporate culture, where

temporary measures are taken to solve financial problems,

using employee involvement to produce some of the solutions.

Bruton, Keels, and Shook (1996) showed that downsizing

could be beneficial to firms, if the downsizing were a part

of strategic reorientations, by refocusing the firm on its

core businesses. Successful downsizers often reduced asset

size through divestiture. Bruton, Keels, and Shook (1996)

recommend a contingency approach of downsizing integrated

with strategic direction.

An interesting study by Lee (1997) showed differences in

the effect of layoffs on stock price, depending on nation

(U.S. or Japan) . Additionally, the U.S. results showed that

although layoff announcements had a negative effect on stock

price overall (within a five-day period), the type of layoff

mitigated the lowered stock price.

For example, single layoff announcements are worse that

multiple announcements; permanent layoffs are worse than

40

temporary layoffs; the extent of the layoff is important; the

first announcement in the industry is the worst; and

reactive layoffs (those that are the only response to poor

financial performance) are worse than proactive layoffs

(those that are part of a deliberate restructuring strategy).

DeWitt (1998) considers downsizing approaches as

strategic choices for staying in or leaving an industry (or

somewhere in between) . The study characterizes downsizing as

retrenchment, downscaling, or downscoping. Retrenchment

approaches keep the same scope and output of a firm, while

redundant facilities or jobs are eliminated, or managerial

responsibilities are realigned. Downscaling keeps the same

scope but lowers output, by making permanent cuts in human

and physical resources. Downscoping reduces both scope and

output, by product line pruning or market withdrawal, for the

most part.

Firm influences such as capacity and production

investment; industry influences, such as cost advantages

and product differentiation; and strategy influences, such as

domain breadth were shown to be important in choosing

downsizing type, depending on whether the firm was broad of

focused in terms of scope. Dewitt (1998) points out that the

characterization of downsizing is important for understanding

strategic decisions and their impact, and that the downsizing

approach itself is different from the complete strategy of a

declining firm.

41

Gaps in the Reviewed Literature

There are gaps in the organizational science literature

in the exploration and explication of downsizing and its

relationships with other concepts. In the literature on

"size," one of the most important gaps is that changes in

size within organizations are not addressed. One of the

effects, therefore, is that there are no definitions of

downsizing, nor theoretical frameworks on downsizing offered.

Moreover, the operationalization of size is inconsistent,

often contributing to differences in results. Another

drawback in the size literature, at least in relation to

downsizing, is that number of employees is not always

considered. The performance and size relationship is

inadequately studied, and when performance is addressed,

perceptual measures are usually used instead of objective

measures.

In the literature on "decline," there is great

conceptual confusion between downsizing and decline. There

is also blurring of the distinction between decline and

responses to decline. There are few theoretical linkages

between downsizing and decline. Rather, there are many

discussions on how to "handle" decline and the focus is often

on implementation issues. In addition, in the decline

literature, performance relationships are rarely addressed.

In the small amount of literature on "size and decline"

42

together, there is no definitional clarity of concepts;

workforce reduction is often used, even as decline itself.

Implementations issues are addressed, with little emphasis on

theoretical constructs. There is disagreement in the

literature on the possible asymmetry between growth and

decline. Performance issues are, again, not addressed.

The "corporate restructuring" literature has gaps in it

relating to downsizing, as well. Downsizing itself is rarely

considered; downsizing is not usually included in

restructuring definitions. In the one study reviewed. Bethel

and Liebeskind (1993), there was no study of the relationship

between downsizing and performance. Overall, the

consequences of restructuring on performance have been

neglected.

In the literature on "divestment," downsizing is not

addressed. Divestment could be part of an overall downsizing

strategy, but it is not seen that way in the literature on

divestment. Downsizing and divestment appear to be separate

and distinct concepts.

There is a body of literature on "downsizing practices."

Most is at the individual and group level, rather than the

organizational level. Theoretical frameworks are lacking in

the downsizing practices literature. At the same time, there

is little empirical support offered. Another problem in the

downsizing practices literature is that there are no explicit

conceptualizations of downsizing; often, downsizing is

43

discussed in very general terms. The relationship between

downsizing practices and performance has scarcely been

considered. Overall, there is scant scholarly and systematic

research in the area of downsizing practices, and downsizing

in general.

44

CHAPTER III

RATIONALE

The Point at the End of the Cornucopia

The previous literature review may be thought of as a

vast cornucopia of ideas and information related to the

concept of downsizing. There are many yet unresolved

questions about downsizing, including how to study this

phenomenon, and whether (or under what conditions) downsizing

has a positive or negative effect on organizational

profitability. There has been very little systematic and

scholarly research on downsizing. In the words of Cameron,

Freeman, and Mishra (1993),

...it is because of the underdeveloped downsizing theory that investigators should first adopt a theory-building approach as opposed to a theory-testing approach. That is, because no current theories exist regarding organizational downsizing or its association with successful performance, an important first step in research is to identify patterns, relationships, and dynamics rather than to set forth a theory for testing, (p. 28, italics added)

Cameron, Freeman, and Mishra (1993) have set forth

several research questions for current downsizing research,

one of which is the basis for this study, namely: "what is

the impact of downsizing on the organization?" Cameron,

Freeman, and Mishra (1993) state

... almost no empirical studies have empirically investigated the effectiveness of (these) prescriptions. The question of whether

45

organizational downsizing inhibits or enhances organizational performance has largely remained unaddressed, as has the more precise question of which particular downsizing processes are helpful and which are hurtful, (p. 30)

The study attempts to answer the question of whether

organizational downsizing inhibits or enhances organizational

performance.

In the study, organizational downsizing is defined and

characterized as an intentional set of activities designed to

improve organizational performance, and involving reductions

in personnel (Cameron, Freeman, & Mishra, 1993). Downsizing

is considered conceptually distinct from organizational

decline (Cameron, Freeman, & Mishra, 1991, 1993; DeWitt,

1993; Kozlowski, Chao, Smith, & Hedlund, 1993; McKinley,

1993) . According to Cameron, Freeman, and Mishra (1993),

downsizing is strategic in nature, and its purpose is to

improve organizational performance. In the study, the

performance effects of downsizing are studied using a multi-

year, multi-organizational data base. The study includes an

empirical investigation of the performance implications of

downsizing, based on a tentative model. The study does not

test hypotheses, as there is not enough testable theory on