Cooper HERNIS Global Update Agent Seminar Bankok 2012 Cooper... · Turnover/Employees Based in...

33

Cooper HERNIS Global Update Agent Seminar – Bankok 2012 Bjørn Fossestøl, Marketing Director 13 th March, 2012

Transcript of Cooper HERNIS Global Update Agent Seminar Bankok 2012 Cooper... · Turnover/Employees Based in...

Cooper HERNIS Global Update

Agent Seminar – Bankok 2012

Bjørn Fossestøl, Marketing Director

13th March, 2012

2

Agenda

Cooper Industries

Cooper HERNIS overview

Cooper HERNIS 2011

Cooper HERNIS budget 2012

Global Market Outlook

Cooper Industries

Turnover/Employees

Based in Houston, Cooper Industries

is a leading manufacturer of electrical

products and tools with a turnover

of $ 6,5 billion and 28,000 employees.

Crouse-Hinds Bussmann Lighting

Power Systems B-Line Wiring Devices

Safety

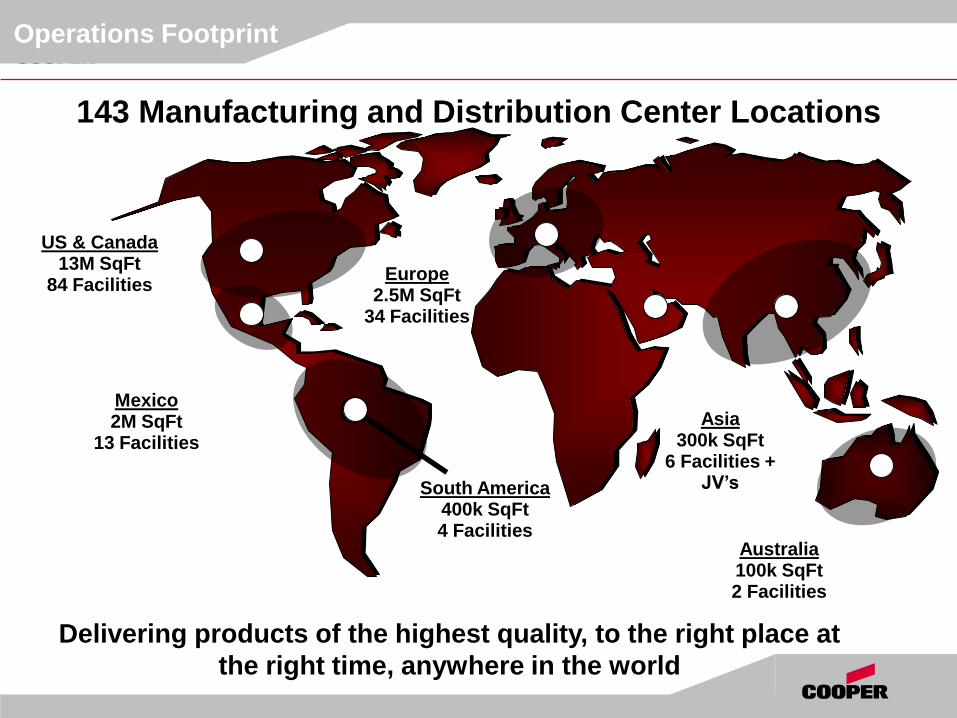

Delivering products of the highest quality, to the right place at

the right time, anywhere in the world

South America 400k SqFt 4 Facilities

US & Canada 13M SqFt

84 Facilities

Mexico 2M SqFt

13 Facilities

Australia 100k SqFt 2 Facilities

Europe 2.5M SqFt

34 Facilities

Asia 300k SqFt

6 Facilities + JV’s

143 Manufacturing and Distribution Center Locations

Operations Footprint

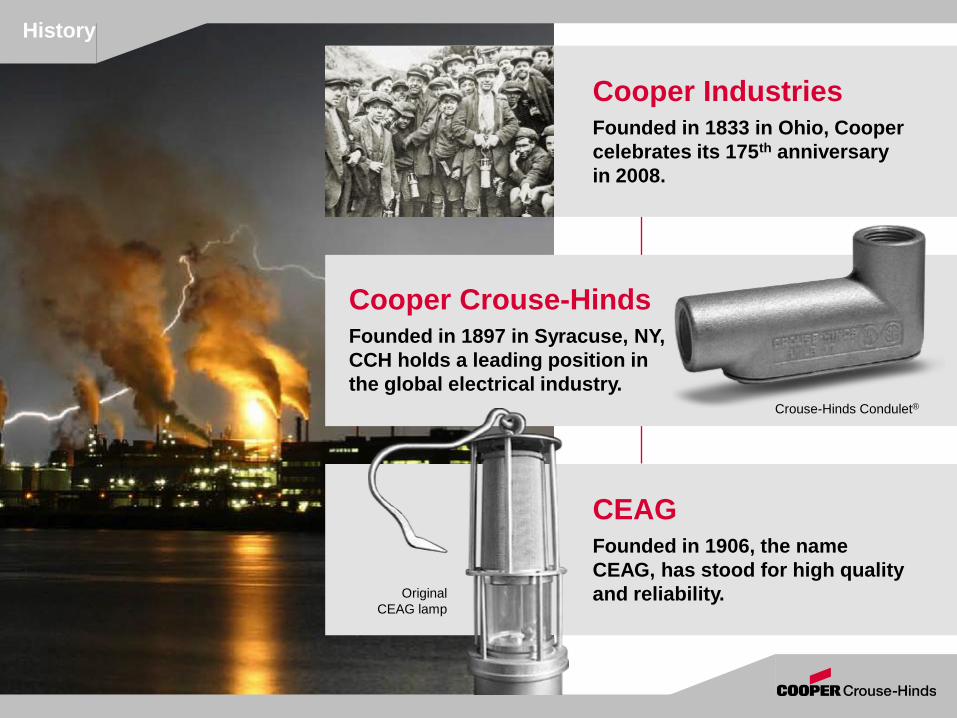

History

Cooper Industries Founded in 1833 in Ohio, Cooper

celebrates its 175th anniversary

in 2008.

Cooper Crouse-Hinds Founded in 1897 in Syracuse, NY,

CCH holds a leading position in

the global electrical industry.

CEAG Founded in 1906, the name

CEAG, has stood for high quality

and reliability.

Crouse-Hinds Condulet®

Original

CEAG lamp

Oil + Gas

Marine

Chemical/Pharmaceutical

Crouse - Hinds

Target Industries

World’s leading provider of products and service for electrical systems in

hazardous environments

Industrial

CSA Canadian

Certification

ATEX Certification for

the European Union

UL Certification for

United States

NEC North

American

Certification

CEPEL Brazilian

Certification

IEC and IECEx International Certification

Gost Russian

Certification

GB Certification

for China

Overview

One Standard All Continents –

World’s leading manufacturer of explosion-

protected products to NEC and IEC standards!

Cooper Crouse-Hinds

Switchgear

NEC-Products Explosion protected

Product Portfolio

Lighting

Lighting Switchgear Connectivity

IEC Product Portfolio

IEC-Products Explosion protected

Lighting Visual Signaling Brass Electrical Products

Product Portfolio

Marine-Products PAULUHN Explosion protected

Portable Power Solutions Explosion protected IEC/NEC

Product Portfolio

Signaling Explosion protected

Safety

CCTV Solutions World leader in Explosion protected

Safety

Cooper HERNIS

Overview

15

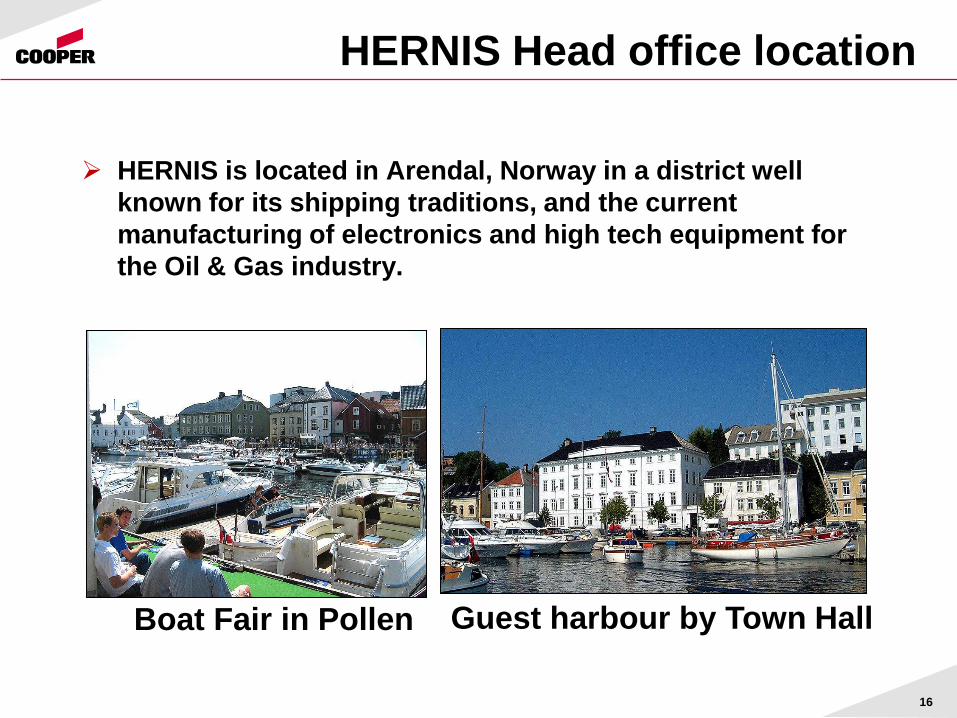

HERNIS Head office location

HERNIS is located in Arendal, Norway in a district well

known for its shipping traditions, and the current

manufacturing of electronics and high tech equipment for

the Oil & Gas industry.

Guest harbour by Town Hall Boat Fair in Pollen

16

17

The very beginning

1982, local newspaper

article

18

The reliable CCTV manufacturer

Offices and Agent Network

19

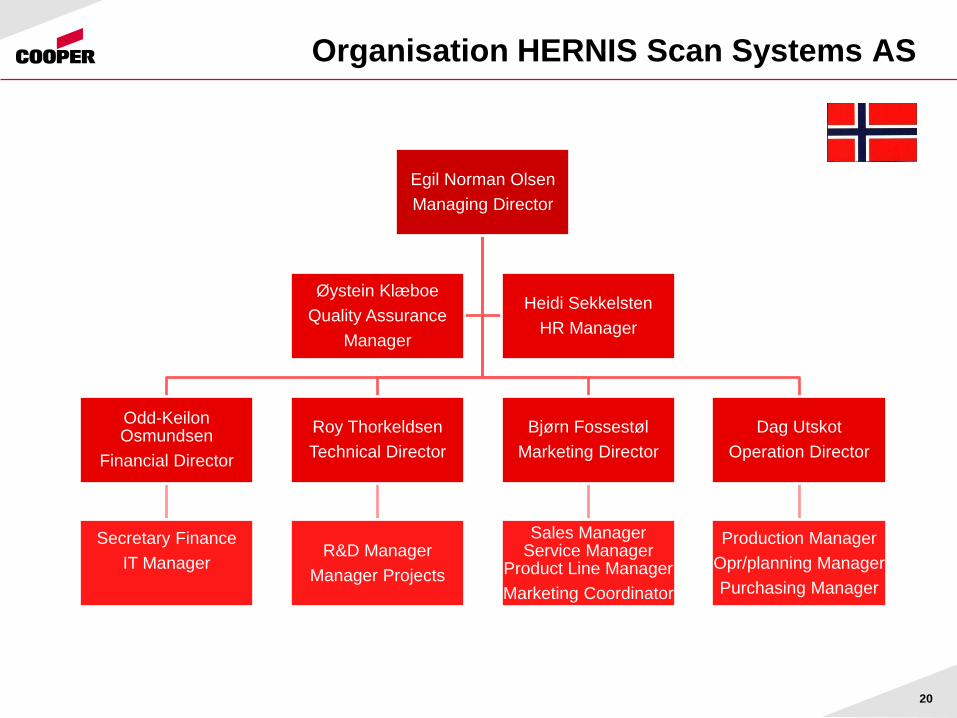

Organisation HERNIS Scan Systems AS

Egil Norman Olsen

Managing Director

Odd-Keilon Osmundsen

Financial Director

Secretary Finance

IT Manager

Roy Thorkeldsen

Technical Director

R&D Manager

Manager Projects

Bjørn Fossestøl

Marketing Director

Sales Manager Service Manager

Product Line Manager

Marketing Coordinator

Dag Utskot

Operation Director

Production Manager

Opr/planning Manager

Purchasing Manager

Øystein Klæboe

Quality Assurance

Manager

Heidi Sekkelsten

HR Manager

20

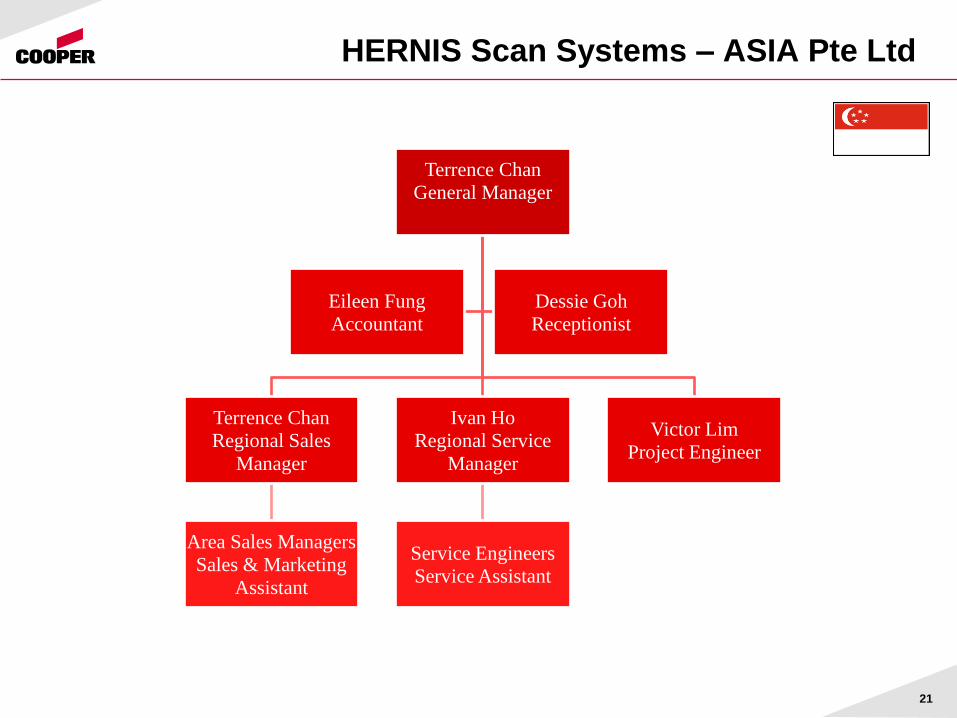

HERNIS Scan Systems – ASIA Pte Ltd

Terrence Chan

General Manager

Terrence Chan

Regional Sales

Manager

Area Sales Managers

Sales & Marketing

Assistant

Ivan Ho

Regional Service

Manager

Service Engineers

Service Assistant

Victor Lim

Project Engineer

Eileen Fung

Accountant

Dessie Goh

Receptionist

21

Organisation HERNIS Scan Systems –US Inc.

Micheal Weston

General Manager

Charlene Bellows

Office Coordinator

Kevin Clark

Sales / Technical

Support

22

Cooper HERNIS

“Numbers”

23

24

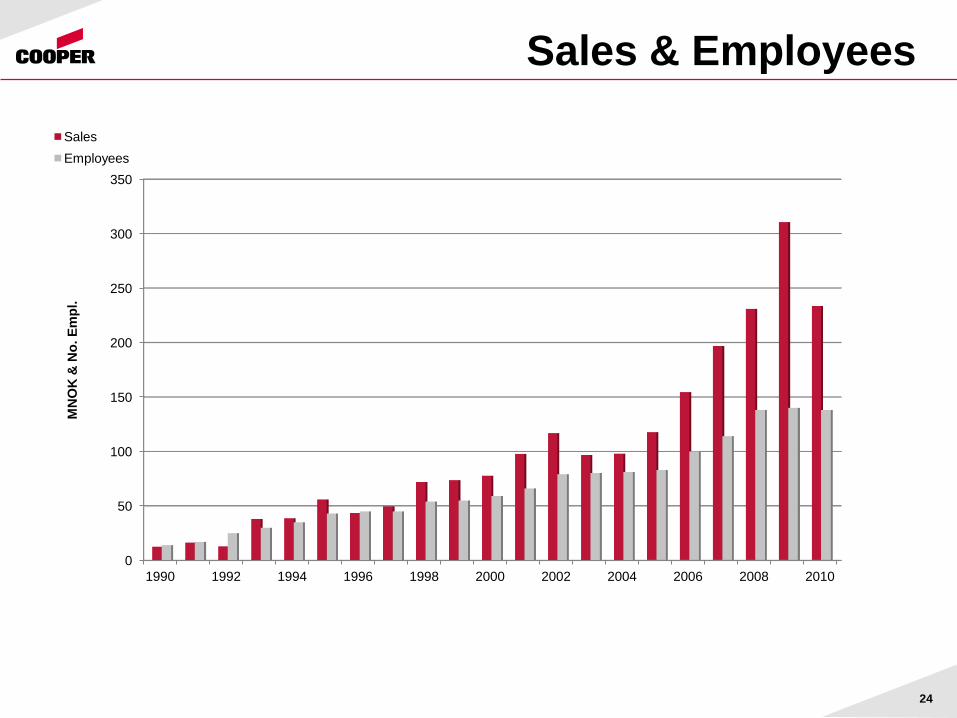

Sales & Employees

0

50

100

150

200

250

300

350

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

MN

OK

& N

o. E

mp

l.

Sales

Employees

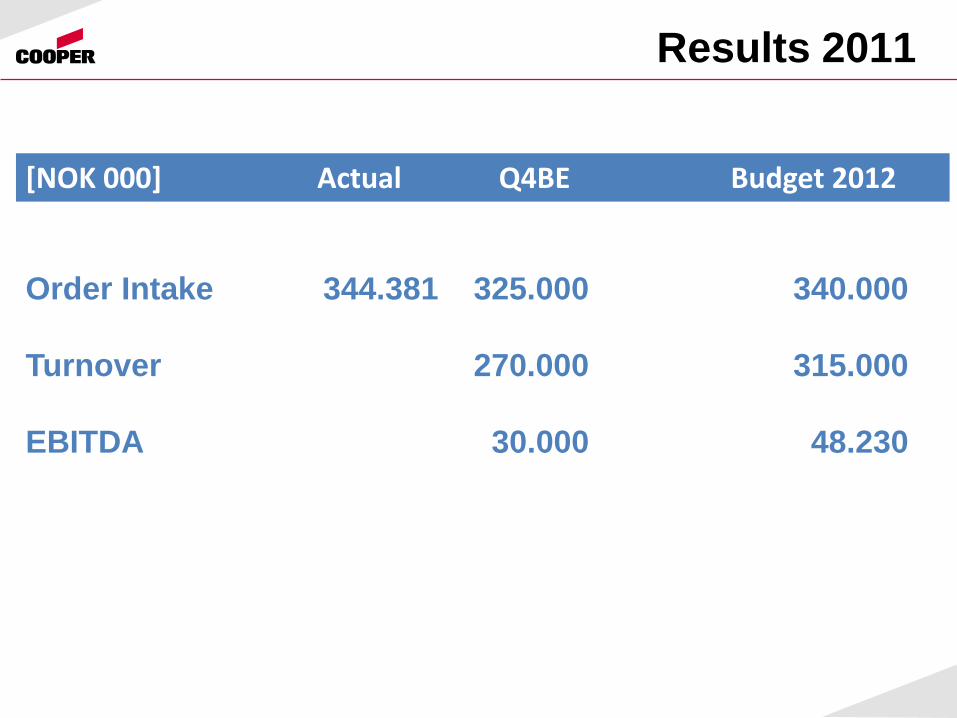

Results 2011

Order Intake 344.381 325.000 340.000

Turnover 270.000 315.000

EBITDA 30.000 48.230

[NOK 000] Actual Q4BE Budget 2012

Market Outlook

26

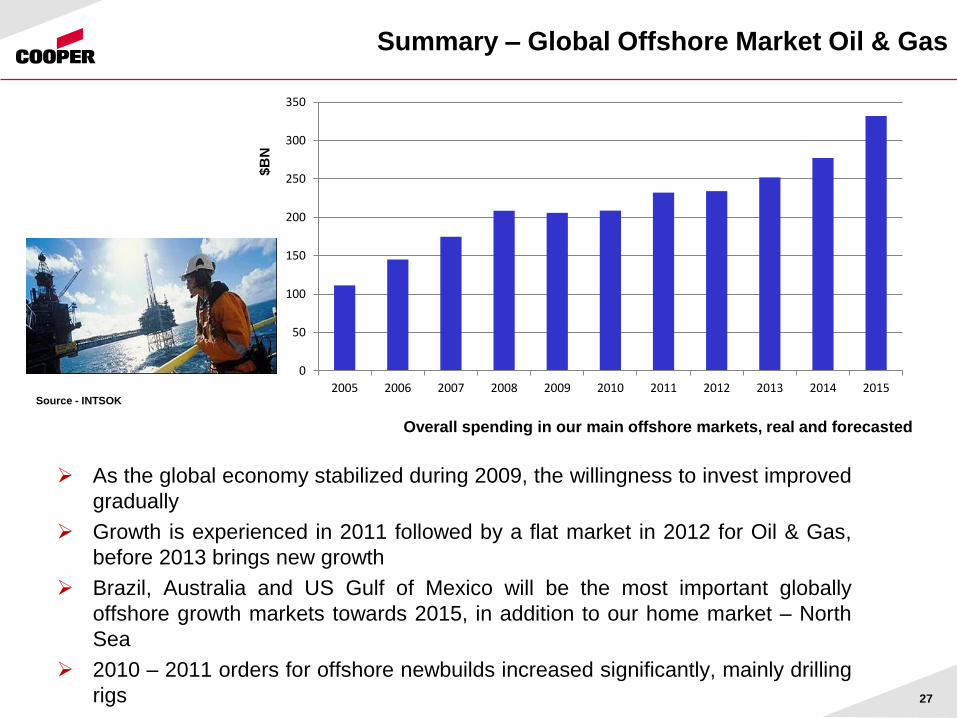

As the global economy stabilized during 2009, the willingness to invest improved

gradually

Growth is experienced in 2011 followed by a flat market in 2012 for Oil & Gas,

before 2013 brings new growth

Brazil, Australia and US Gulf of Mexico will be the most important globally

offshore growth markets towards 2015, in addition to our home market – North

Sea

2010 – 2011 orders for offshore newbuilds increased significantly, mainly drilling

rigs

Overall spending in our main offshore markets, real and forecasted

0

50

100

150

200

250

300

350

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Summary – Global Offshore Market Oil & Gas

$B

N

Source - INTSOK

27

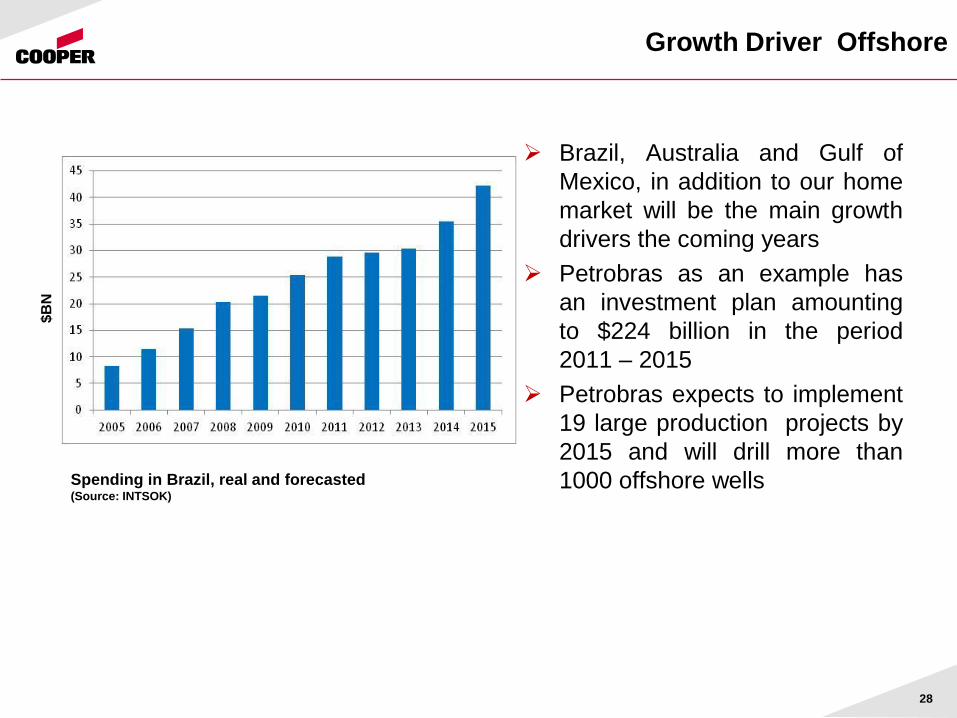

Growth Driver Offshore

Brazil, Australia and Gulf of

Mexico, in addition to our home

market will be the main growth

drivers the coming years

Petrobras as an example has

an investment plan amounting

to $224 billion in the period

2011 – 2015

Petrobras expects to implement

19 large production projects by

2015 and will drill more than

1000 offshore wells

Spending in Brazil, real and forecasted (Source: INTSOK)

$B

N

28

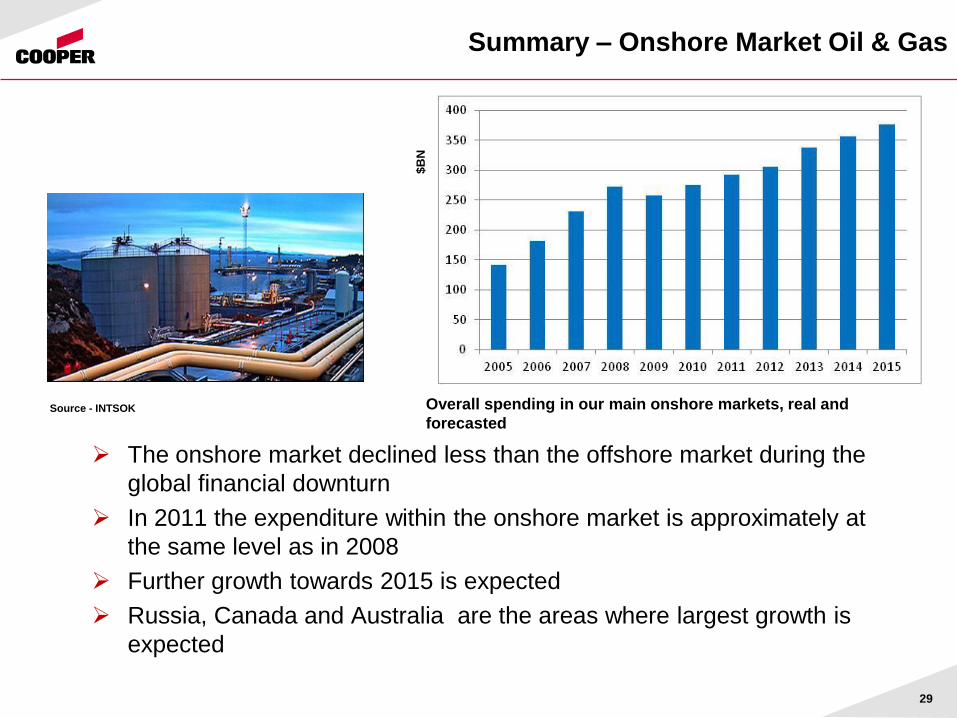

Summary – Onshore Market Oil & Gas

The onshore market declined less than the offshore market during the

global financial downturn

In 2011 the expenditure within the onshore market is approximately at

the same level as in 2008

Further growth towards 2015 is expected

Russia, Canada and Australia are the areas where largest growth is

expected

Overall spending in our main onshore markets, real and

forecasted

$B

N

Source - INTSOK

29

Growth Driver Onshore

The Middle East onshore

market going forward is

forecasted to be relatively flat

The growth opportunity in this

area is to increase our market

share

The Canada onshore market is

forecasted to grow by 50 % in

the next four years, mostly

stemming from oil sand

development

Spending Middle East – Onshore, real and forecasted

$B

N

Spending Canada – Onshore, real and forecasted

$B

N

Source - INTSOK

Source - INTSOK 30

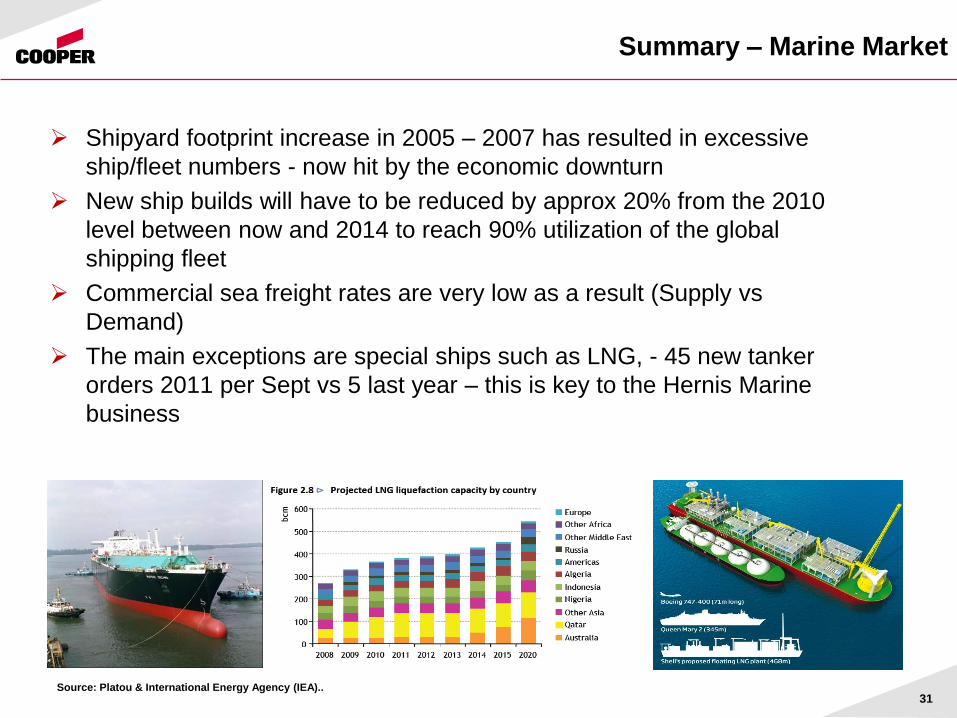

Summary – Marine Market

Shipyard footprint increase in 2005 – 2007 has resulted in excessive

ship/fleet numbers - now hit by the economic downturn

New ship builds will have to be reduced by approx 20% from the 2010

level between now and 2014 to reach 90% utilization of the global

shipping fleet

Commercial sea freight rates are very low as a result (Supply vs

Demand)

The main exceptions are special ships such as LNG, - 45 new tanker

orders 2011 per Sept vs 5 last year – this is key to the Hernis Marine

business

Source: Platou & International Energy Agency (IEA).. 31

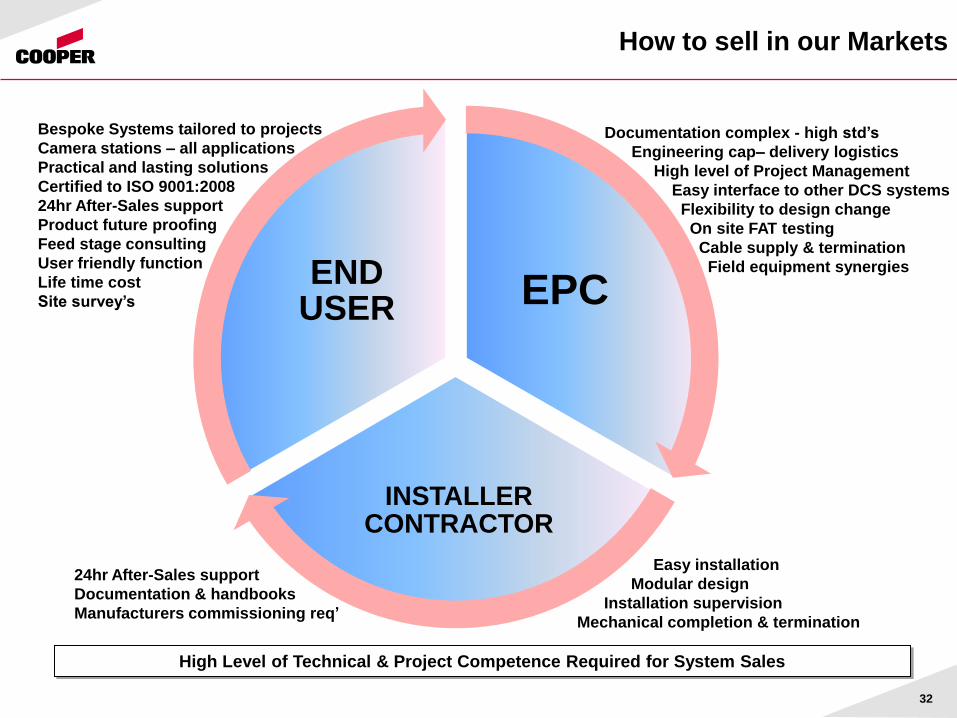

How to sell in our Markets

High Level of Technical & Project Competence Required for System Sales

EPC

INSTALLER CONTRACTOR

END USER

Bespoke Systems tailored to projects

Camera stations – all applications

Practical and lasting solutions

Certified to ISO 9001:2008

24hr After-Sales support

Product future proofing

Feed stage consulting

User friendly function

Life time cost

Site survey’s

Documentation complex - high std’s

Engineering cap– delivery logistics

High level of Project Management

Easy interface to other DCS systems

Flexibility to design change

On site FAT testing

Cable supply & termination

Field equipment synergies

Easy installation

Modular design

Installation supervision

Mechanical completion & termination

24hr After-Sales support

Documentation & handbooks

Manufacturers commissioning req’

32

Thank You for Your Attention!

33